Attached files

| file | filename |

|---|---|

| 8-K - 8-K - VWR Corp | d888412d8k.htm |

Barclays 2015

Global Healthcare Conference

March 11, 2015

VWR Corporation

Exhibit 99.1 |

Forward-Looking Statement

Non-GAAP Measures and Other Definitions

Safe Harbor

2

To evaluate our performance, we monitor a number of key indicators at the consolidated level

and, in certain cases, at the segment level. As appropriate, we supplement our results

of operations determined in accordance with GAAP with certain non-GAAP financial measurements that we believe are useful to

investors, creditors and others in assessing our performance. These measurements should not be

considered in isolation or as a substitute for reported GAAP results because they may

include or exclude certain items as compared to similar GAAP-based measurements, and such measurements may not be

comparable to similarly-titled measurements reported by other companies. Rather, these

measurements should be considered as an additional way of viewing aspects of our

operations that provide a more complete understanding of our business. We strongly encourage readers to review our consolidated

financial statements included elsewhere herein and in publicly filed reports in their entirety

and not rely solely on any one, single financial measurement. See “Non-GAAP

Measures” in our publicly filed reports. This presentation contains statements about future events and expectations that constitute

forward-looking statements. Forward-looking statements are based on our

beliefs, assumptions and expectations of our future financial and operating performance and growth plans, taking into account the information

currently available to us. These statements are not statements of historical fact.

Forward-looking statements involve risks and uncertainties that may cause our

actual results to differ materially from the expectations of future results we express or imply in any forward-looking statements and you should not place

undue reliance on such statements. Factors that could contribute to these differences

include, but are not limited to, the factors described in "Risk Factors" in

VWR’s Annual Report on Form 10-K. Words such as “anticipates”,

“believes”, “continues”, “estimates”, “expects”, “goal”, “objectives”, “intends”, “may”,

“opportunity”, “plans”, “potential”, “near-term”,

“long-term”, “projections”, “assumptions”, “projects”, “guidance”, “forecasts”, “outlook”, “target”, “trends”,

“should”, “could”, “would”, “will” and similar

expressions are intended to identify such forward-looking statements. We qualify any forward-looking

statements entirely by these cautionary factors. We assume no obligation to update or

revise any forward-looking statements for any reason, or to update the reasons

actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the

future. Comparisons of results for current and any prior periods are not intended to

express any future trends or indications of future performance, unless expressed as

such, and should only be viewed as historical data. |

VWR:

Outperforming the Industry Positioned in

large, growing

global market

Independent

solutions

provider

Revenue

growth vs.

industry

Annual Adjusted

EPS growth

next

3-5 years

$49B

#1

EMEA-APAC

#2 The

Americas

Targeting

~2X

faster

Targeting

Double-

digit

3 |

AGENDA

VWR:

Outperforming the Industry

Global player with solid performance record

Positioned in attractive markets

Unique value proposition

Resilient business model

1

2

3

4

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit

Powerful growth drivers

5

4 |

VWR AT A

GLANCE Leading Global Provider of Laboratory

Products and Services

Americas

EMEA-APAC

44%

56%

2014 Segment

Revenue Breakdown

2014 Revenues

Market cap

IPO

Acquisitions since 2007

Employees worldwide

$4.4B

$3.3B

Oct. 2014

37

8,500+

5 |

VWR:

A Profile

of Leadership

6

Global Scale

Market Leader

•

~9% share of

$49B global market

•

#1 in Europe

•

#2 in The Americas

Broad

Product Range

•

Over 1M SKUs

•

~4,500 laboratory

suppliers

•

17,000 orders per day

•

Over 160 facilities

•

34 countries

•

~120,000 customers

9% |

Consistent Record

of Growth and Margin Expansion 7

Revenues

Adjusted EBITDA

Adjusted EBITDA

Margin

$3.3B

$4.4B

2006

2014

4%

CAGR

8%

CAGR

$235M

$449M

2006

2014

7.2%

10.3%

2006

2014

+310

bps |

EMEA-APAC

Segment: A Key Growth Driver 8

Leading market position

Integrated IT platform and

distribution network

Record of seamless

tuck-in acquisitions

Long-standing customer

relationships

Strengths

Performance Highlights

2006 to 2014

Revenue growth

Adj. EBITDA growth

Adj. EBITDA margin

in 2014

Adj. EBITDA margin

expansion since 2006

7%

CAGR

14%

CAGR

11.8%

460 bps |

Americas

Segment: Replicating Success of EMEA-APAC, Driving Improved Results

9

Clear Evidence Performance

is Improving

Upgraded IT infrastructure

Shifted go-to-market

strategy

New state of the art

distribution facility

Upgraded e-commerce

Strengthened

management team

Initiatives/

Investments

Q/Q Organic Revenue Growth

-2.8%

-2.8%

-2.7%

+0.6%

+3.4%

+7.2%

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14 |

AGENDA

VWR: Outperforming the Industry

10

Global player with solid performance record

Positioned in attractive markets

Unique value proposition

Resilient business model

1

2

3

4

Powerful growth drivers

5

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit |

Positioned in

Large, Growing Market 11

$49B VWR

Addressable Market*

Steadily

Growing

$39B

Lab services

Bioprocess

chemicals and

consumables

~2% annually

$4B

$6B

Lab products

*Source: Frost & Sullivan’s 2014 Annual Report: Forecast and Analysis of the

Global Market for Laboratory Products (published October 2014), Market Size

of Global and U.S. Laboratory Services Market and Laboratory Chemicals Market Clarification

(commissioned July 2014) and US and Global Validation of the Bioprocess Chemicals and

Consumables Market (commissioned August 2014) Increased R&D

Growing regulations

Globalization of customers |

Competitive

Landscape: VWR is Uniquely Positioned in Highly Fragmented Lab Products Market

12

Fragmented market with

many smaller niche companies

Regional

Global

Footprint

Narrow

Broad

Product

Range |

Successful

Acquisition Record – 37 Since 2007

13

Focus of Acquisitions

to Date

Product growth

(Self-Manufacturing

Capacity)

Tuck-ins

Geographic

expansion

32%

22%

46%

•

Disciplined approach

–

hurdle rate of 15%

•

Invested $550M on

acquisitions since 2007

•

Adds >1% to revenue

growth per annum |

AGENDA

VWR: Outperforming the Industry

14

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit

1

Global player with solid performance record

2

Positioned in attractive markets

3

Unique value proposition

4

Resilient business model

5

Powerful growth drivers |

15

Leading Independent Global Provider of Laboratory Products,

Services and Solutions to the Lab Market

~4,500

lab suppliers

Branded and private label products and services

~120,000

customers

Highly diversified -

No single customer >4% of sales |

Our Unique Value

Proposition 16

Superior Product

Choice

Operational

Excellence

Differentiated

Services

•

Unbiased

•

Broadest range

•

Logistical expertise

•

Supply chain partner

•

Customized solutions

•

People and technology |

Customized and

Differentiated Strategy 17

Examples |

Key Offerings

that Further Differentiate VWR 18

Offering

Customer Advantages

Impact on VWR

Private

Label Products

~15%

of revenues

•

Greater choice at lower

price points

•

Complement branded

suppliers

•

8-10% Revenue growth

•

Attractive margin profile

Chemical

Manufacturing

~5%

of revenues

•

Customized product

solutions

–

biochemicals

–

buffers

–

reagents

•

Strong revenue and

margin profile

•

Mostly direct –

avoid

channel conflict

•

$6B bioprocess chemical

and consumable market

growing DD |

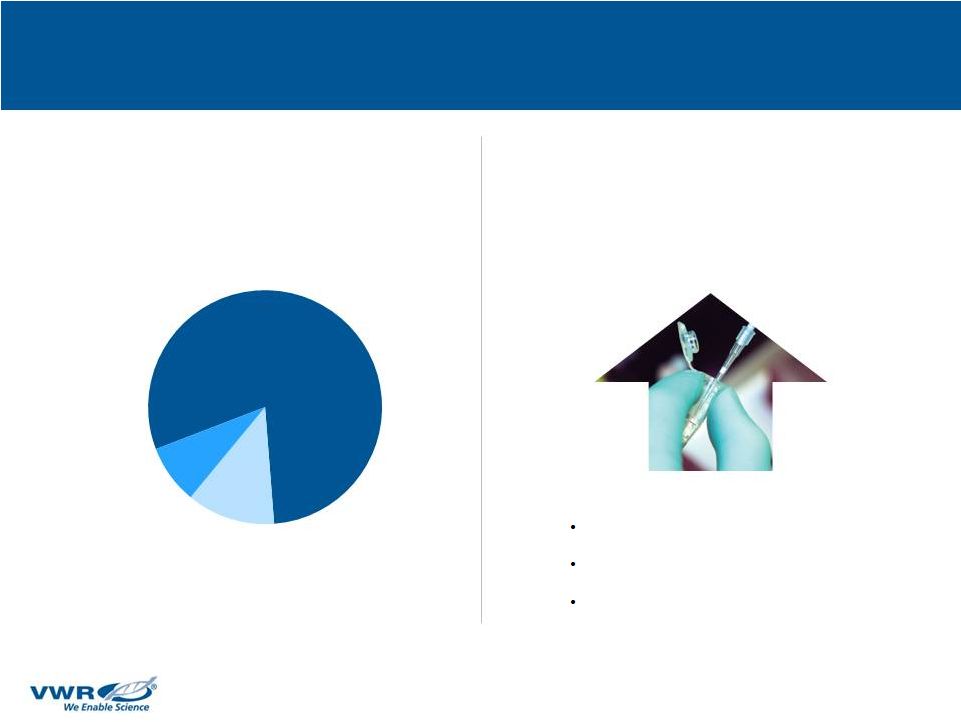

VWR

Lab Services

Key Offerings that Further Differentiate VWR

19

Offering

Customer Advantages

Impact on VWR

3%

of revenues, but affects

customers representing

~25% of revenues

•

Allows labs to outsource

services such as

–

facility and inventory

management

–

lab maintenance processes

•

An "Onsite CRO" concept

•

Lower costs, improved

productivity

•

Deepens relationships

-

~900 onsite associates

-

~240 customer sites

•

Powerful differentiator

•

More value-add for our

customers

CATALYST |

VWR:

Outperforming the Industry 20

Global player with solid performance record

Positioned in attractive markets

Unique value proposition

Resilient business model

1

2

3

4

Powerful growth drivers

5

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit |

Resilient and

Attractive Business Model 21

High recurring, stable

revenues ~80%

Expanding Adjusted

EBITDA margins

Growing cash flow

Double-digit Adjusted

EPS growth

1

2

4

3

–

for deleveraging

and acquisitions |

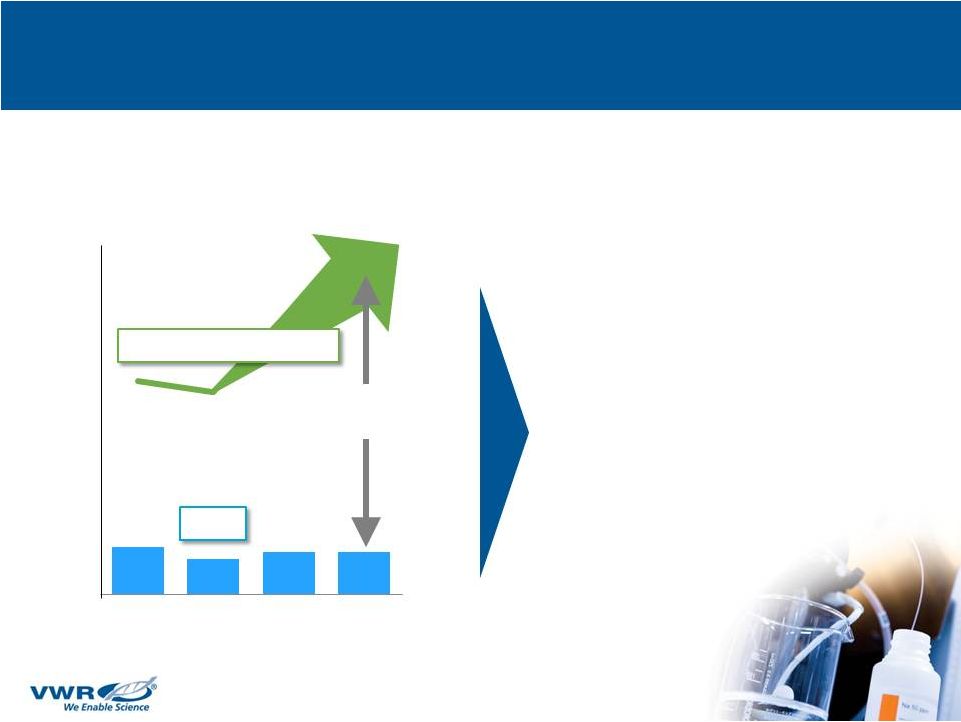

Powerful Cash

Flow Engine 22

Growing Free

Cash Flow…

Fueling Growth

in Earnings

CapEx

•

Deleveraging balance sheet

–

Debt to Adjusted EBITDA

down from 6.4x a year ago

to 4.4x at year end 2014

•

Accelerating growth with

acquisitions

–

$50-$75M annually

Cash flow from operations

Growing

free cash flow

2013

2014

2015

2016 |

A

G

E

N

D

A

VWR:

The Industry Growth Leader

23

Global player with solid performance record

Positioned in attractive markets

Unique value proposition

Resilient business model

1

2

3

4

Powerful growth drivers

5

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit |

Multiple Factors

Driving Sustained Growth 24

Market

Growth

~2%

Double-digit

Adjusted EPS

Growth

VWR Earnings

Growth

Faster

organic growth

Acquisitions

OI Margin

expansion

Deleveraging

•

Private label

•

Custom manuf.

•

VWR

•

Average

$50M-$75M

annually

•

Lower

interest costs

•

Globalize

Best

Practices

CATALYST |

Double-

digit

growth

Naturally

delevering

~2X

faster

Long Term Financial Targets

25

Revenue

Growth vs.

Industry

Operating

Income

Margin

Adjusted EPS

Growth

Growing Free

Cash Flow

~40+ bps

Per year

expansion

next

2-3 years |

Deleveraging

Continues…. Net Debt / Adjusted EBITDA

26

9.3x

8.4x

7.7x

7.1x

6.4x

6.9x

6.4x

4.4x

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14 |

Full Year 2014

– Performance Highlights

EMEA-APAC continues to outperform the market

Americas: Turnaround confirmed and organic earnings growth established

Expanded Adjusted EBITDA Margin 30 bps to 10.3%

Delevered & executed on our acquisition strategy

Adjusted EPS of $1.21 increased 29% YoY

A successful IPO

27 |

4Q14

– Performance Highlights

•

Organic revenue growth of 5.9%

•

Americas organic growth 7.2% and

EMEA-APAC organic growth 4.4%

•

Solid cash flow quarter, operating

cash flow of $104M

•

Adjusted EBITDA $119.5M, up 1% YoY

28

Revenue ($M)

Adjusted EPS

+4%

+16%

$1,059

$1,102

4Q13

4Q14

$0.37

$0.43

4Q13

4Q14 |

FY15

Guidance 29

2014

Actual

SBC

Adj.

2014

Adj.

2015 Guidance Range

Low High

Revenue

$4,375

$4,375

$4,244

$4,310

Adjusted EBITDA

$449

–

$449

$456

$463

Adjusted EPS

$1.21

$(0.01)

$1.20

$1.42

$1.50

Note:

2015 Adj. EPS guidance includes share-based compensation estimated at $5 to $6 million

(pretax). 2015 Adj. EBITDA guidance excludes share-based compensation.

($ millions, except EPS) |

VWR:

The Industry Growth Leader

30

Global player with solid performance record

Positioned in attractive markets

Unique value proposition

Resilient business model

1

2

3

4

Powerful growth drivers

5

Targeting

Adjusted

EPS growth

next 3-5 years:

Double-digit |