Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Avanos Medical, Inc. | d807372d8k.htm |

| EX-99.1 - EX-99.1 - Avanos Medical, Inc. | d807372dex991.htm |

| EX-4.2 - EX-4.2 - Avanos Medical, Inc. | d807372dex42.htm |

| EX-4.1 - EX-4.1 - Avanos Medical, Inc. | d807372dex41.htm |

Exhibit 99.2

October 17, 2014

Dear Fellow Kimberly-Clark Stockholder:

I am pleased to inform you that on October 6, 2014 the executive committee of our Board of Directors approved the spin-off of Halyard Health, Inc., a wholly-owned subsidiary that owns Kimberly-Clark’s health care business.

The spin-off of Halyard will allow us to further sharpen our focus on our consumer and professional brands, while allowing Halyard to optimize its performance and flexibility in a rapidly changing industry.

The spin-off of Halyard is scheduled to occur on October 31, 2014. If you hold Kimberly-Clark common stock at the close of business on the record date for the spin-off, which is October 23, 2014, you will receive a distribution of one share of Halyard common stock for every eight shares of Kimberly-Clark common stock that you hold on that date.

You don’t need to take any action to receive shares of Halyard common stock to which you are entitled as a Kimberly-Clark stockholder. In addition, you don’t need to pay any consideration or surrender or exchange your Kimberly-Clark common stock.

Following the spin-off, Kimberly-Clark common stock will continue to trade on the New York Stock Exchange under the symbol “KMB,” and Halyard’s common stock will trade on the New York Stock Exchange under the symbol “HYH.”

I encourage you to read the attached information statement carefully, which provides a description of the spin-off and includes important information about Halyard, including its historical combined financial data.

We look forward to your continued support as a stockholder in both Kimberly-Clark and Halyard.

Sincerely,

Thomas J. Falk

Chairman of the Board and Chief Executive Officer

October 17, 2014

Dear Future Halyard Health, Inc. Stockholder:

It is my pleasure to welcome you as a stockholder of our new company, Halyard Health, Inc.

Halyard will be a global healthcare company that seeks to advance health and healthcare by preventing infection, eliminating pain and speeding recovery. We will focus on delivering clinically-superior solutions with remarkable service to improve the well-being of the people we touch every day.

Our employee teams are excited about the opportunity and are committed to realizing the potential that exists for us operating as a more focused company, independent of Kimberly-Clark.

I encourage you to learn more about Halyard by reading the attached information statement. Halyard has been authorized to list its common stock on the New York Stock Exchange under the symbol “HYH.”

Thank you for your support of our new company. We look forward to having you as a fellow stockholder.

Sincerely,

Robert E. Abernathy

Chairman of the Board and Chief Executive Officer

INFORMATION STATEMENT

Halyard Health, Inc.

Common Stock

(par value $0.01 per share)

We are providing this information statement to you as a stockholder of Kimberly-Clark Corporation in connection with Kimberly-Clark’s distribution to its stockholders of all of the outstanding shares of common stock of Halyard Health, Inc. (“Halyard”), a wholly-owned subsidiary of Kimberly-Clark. Halyard was formed to hold directly or indirectly the assets and liabilities associated with Kimberly-Clark’s health care business. All of the issued and outstanding shares of Halyard will be distributed to stockholders in a manner that is intended to generally be tax-free for U.S. federal income tax purposes (other than with respect to cash received in lieu of fractional shares).

We expect that the distribution will be made on October 31, 2014, which we refer to as the “distribution date,” to the holders of record of Kimberly-Clark common stock on October 23, 2014, which we refer to as the “record date.” If you are a holder of record of Kimberly-Clark common stock at the close of business on the record date, you will receive one share of Halyard common stock for every eight shares of Kimberly-Clark common stock you hold on that date. Kimberly-Clark will distribute the shares of Halyard in book-entry form, which means that Halyard will not issue physical stock certificates. In lieu of fractional shares, stockholders of Kimberly-Clark will receive cash, which generally will be taxable.

You are not required to vote on or take any other action in connection with the spin-off. We are not asking you for a proxy, and you are requested not to send us a proxy. You will not be required to pay any consideration for the shares of Halyard common stock you receive in the spin-off, surrender or exchange your shares of Kimberly-Clark common stock or take any action in connection with the spin-off.

Kimberly-Clark currently owns all of the outstanding shares of Halyard common stock. Accordingly, no trading market for Halyard common stock currently exists. We expect, however, that a limited trading market for Halyard common stock, commonly known as a “when-issued” trading market, will develop on or shortly before the record date for the distribution, and we expect “regular-way” trading of Halyard common stock will begin on the first trading day after the distribution date. We have been authorized to list Halyard common stock on the New York Stock Exchange under the symbol “HYH.”

In reviewing this information statement, you should carefully consider the matters described in the section entitled “Risk Factors” beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this information statement is truthful or complete. Any representation to the contrary is a criminal offense.

This information statement is not an offer to sell, or a solicitation of an offer to buy, any securities.

The date of this information statement is October 17, 2014.

This information statement was first mailed to Kimberly-Clark stockholders on or about October 24, 2014.

TABLE OF CONTENTS

| Page | ||||

| Summary |

1 | |||

| Questions and Answers about the Separation and Distribution |

6 | |||

| Risk Factors |

12 | |||

| Cautionary Statement Concerning Forward-Looking Statements |

26 | |||

| The Separation and Distribution |

27 | |||

| Material U.S. Federal Income Tax Consequences |

34 | |||

| Our Relationship with Kimberly-Clark after the Distribution |

36 | |||

| Dividend Policy |

41 | |||

| Description of Material Indebtedness |

41 | |||

| Capitalization |

45 | |||

| Unaudited Pro Forma Condensed Combined Financial Statements |

47 | |||

| Selected Historical Combined Financial Data |

54 | |||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

56 | |||

| Business |

71 | |||

| Management |

87 | |||

| Executive Compensation |

95 | |||

| Ownership of Halyard Stock by Certain Beneficial Owners and Management |

127 | |||

| Description of Halyard Capital Stock |

129 | |||

| Certain Relationships and Related Party Transactions |

134 | |||

| 2015 Annual Meeting of Stockholders |

136 | |||

| Where You Can Find More Information |

136 | |||

| Index to Financial Statements |

F-1 | |||

Presentation of Information

Except as otherwise indicated or unless the context otherwise requires, the information included in this information statement about Halyard assumes the completion of all of the transactions referred to in this information statement in connection with the transfer of Kimberly-Clark’s health care business to Halyard and the distribution of Halyard common stock to Kimberly-Clark common stockholders. Our historical financial results as part of Kimberly-Clark contained herein may not reflect our financial results in the future as a separate publicly-traded company or what our financial results would have been had we been operated as a stand-alone company during the periods presented.

Trademarks, Trade Names and Service Marks

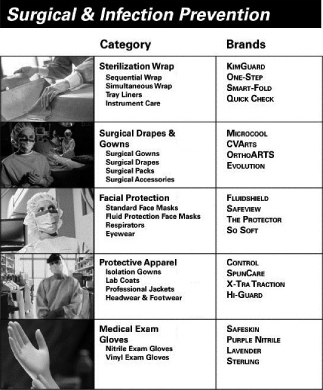

Halyard owns or has the rights to use the trademarks, trade names and service marks that it uses in connection with the operation of its business. Some of the more important marks that Halyard owns or has the rights to use in the United States or in other jurisdictions that appear in this information statement include: KIMGUARD ONE-STEP sterilization wrap, MICROCOOL surgical gowns, FLUIDSHIELD face masks and ON-Q PAINBUSTER pain pumps. Halyard’s rights to some of these trademarks may be limited to select markets. Each trademark, trade name or service mark of any other company appearing in this information statement is, to Halyard’s knowledge, owned by such other company.

This summary highlights selected information from this information statement and may not contain all of the information concerning our company, our separation from Kimberly-Clark, Kimberly-Clark’s distribution of Halyard common stock to Kimberly-Clark’s stockholders or other information that may be important to you. To better understand the distribution and our business and financial position, you should carefully review this entire information statement, particularly the discussion of “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our historical combined financial statements and unaudited pro forma condensed combined financial statements and the notes to those statements appearing elsewhere in this information statement.

References in this information statement to “Halyard,” “we,” “our” and “us” mean Halyard Health, Inc., a Delaware corporation, and its subsidiaries. References in this information statement to our historical assets, liabilities, products, operations or activities of our business are to the historical assets, liabilities, products, operations or activities of the transferred health care business as they were historically owned, incurred or conducted as part of Kimberly-Clark prior to the distribution.

References in this information statement to “Kimberly-Clark” mean Kimberly-Clark Corporation, a Delaware corporation, and its subsidiaries, other than Halyard, unless the context otherwise requires. References in this information statement to the “distribution” mean Kimberly-Clark’s distribution of Halyard common stock to Kimberly-Clark stockholders following the completion of our separation from Kimberly-Clark. Unless otherwise indicated or the context otherwise requires, the information included in this information statement assumes the completion of the separation and distribution.

Halyard

Overview

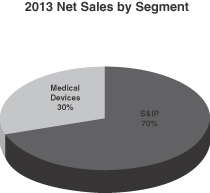

We are a global company which seeks to advance health and healthcare by preventing infection, eliminating pain and speeding recovery. Our products and solutions are designed to address some of today’s most important healthcare needs, namely, preventing infection and reducing the use of narcotics while helping patients move from surgery to recovery. We have two business segments: Surgical and Infection Prevention (S&IP) and Medical Devices.

We have operated our S&IP business for over 30 years, providing products that address the prevention of healthcare-acquired infections (HAIs) and provide protection for both healthcare workers and patients. We have recognized brands and leading market positions in the United States across our entire S&IP product portfolio, which includes sterilization wrap, surgical drapes and gowns, facial protection, protective apparel and medical exam gloves. Our S&IP product portfolio is supported by a global sales force, a customer support team with significant industry experience and robust product training, and customer education programs.

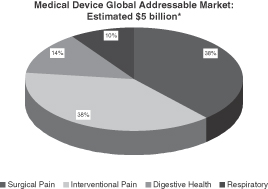

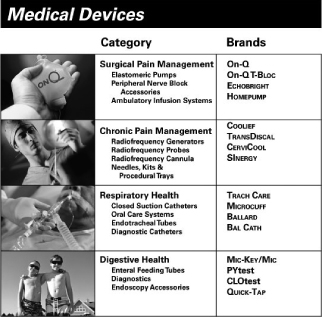

Our Medical Devices business is comprised of a diverse set of medical device solutions focused on improving patient outcomes, patient safety and reducing the cost of care. Our innovative portfolio includes post-operative pain management solutions, minimally invasive interventional (or chronic) pain therapies, closed airway suction systems and enteral feeding tubes. Our recognized brands and highly specialized sales team in each of these medical device product areas strategically position us for growth.

Strengths

Our competitive advantages include:

| • | Our established portfolio of S&IP products with leading market positions and significant brand recognition. |

1

| • | Our growing and innovative Medical Devices business with solutions that reduce the cost and improve the quality of care. |

| • | Our global commercial infrastructure. |

| • | Our strong cash flow. |

| • | Our strong management team with significant healthcare experience. |

See the discussion under “Business – Strengths” below for further information.

Strategies

To achieve our mission, we have three strategies:

| • | Maintain market leadership and improve margins in our S&IP business through operational excellence and innovation. |

| • | Grow our Medical Devices business by accelerating utilization of our unique solutions through clinical education and awareness, and innovation. |

| • | Identify, develop and pursue new growth opportunities. |

See the discussion under “Business – Strategies” below for further information.

Risks Related to Our Business and the Distribution and Our Separation from Kimberly-Clark

An investment in Halyard common stock is subject to a number of risks, including risks relating to the separation and distribution. The following list of risk factors is not exhaustive. Please read the information in the section captioned “Risk Factors” for a more thorough description of these and other risks.

Risks Related to Our Business and Industry

| • | We face strong competition. Our failure to compete effectively could have a material adverse effect on our business. |

| • | We may not be successful in developing, acquiring or marketing competitive products and technologies. |

| • | We are exposed to price fluctuations of key commodities, which may negatively impact our results of operations. |

| • | An inability to obtain key components, raw materials or manufactured products from third parties may have a material adverse effect on our business. |

| • | An interruption in our ability to manufacture products may have a material adverse effect on our business. |

| • | We are subject to extensive government regulation, which may require us to incur significant expenses to ensure compliance. If we fail to comply with those regulations, this noncompliance could have a material adverse effect on our business, results of operations, financial condition and cash flows. |

| • | We are subject to healthcare fraud and abuse laws and regulations that could result in significant liability, require us to change our business practices or restrict our operations in the future. |

| • | We must obtain clearance or approval from the appropriate regulatory authorities prior to introducing a new product or a modification to an existing product. The regulatory clearance process may result in substantial costs, delays and limitations on the types and uses of products we can bring to market, any of which could have a material adverse effect on our business. |

2

| • | We may incur product liability losses, litigation liability, product recalls, safety alerts or regulatory action associated with our products which can be costly and disruptive to our business. |

| • | Current economic conditions have affected and may continue to adversely affect our business, results of operations, financial condition and cash flows. |

| • | Cost-containment efforts of our customers, purchasing groups, third-party payors and governmental organizations could adversely affect our sales and profitability. |

| • | We face significant uncertainty in the healthcare industry due to government healthcare reform in the United States and elsewhere. |

| • | Our customers depend on third-party coverage and reimbursements. The failure of healthcare programs to provide coverage and reimbursement, or reductions in levels of reimbursement, could have a material adverse effect on our business. |

| • | We are subject to political, economic and regulatory risks associated with doing business outside of the United States. |

| • | Currency exchange rate fluctuations could have a material adverse effect on our business and results of operations. |

| • | We cannot guarantee that any of our strategic acquisitions, investments or alliances will be successful. |

| • | We may need additional financing in the future to meet our capital needs or to make acquisitions, and such financing may not be available on favorable terms, if at all, and may be dilutive to existing stockholders. |

| • | We may be unable to protect our intellectual property rights or may infringe the intellectual property rights of others. |

| • | We may be unable to attract and retain key employees necessary to be competitive. |

| • | Breaches of our information technology systems could have a material adverse effect on our business. |

Risks Related to the Distribution and Our Separation from Kimberly-Clark

| • | We have no operating history as a separate company, and our historical and pro forma financial data are not necessarily representative of the results we would have achieved as a stand-alone publicly-traded company and therefore may not be reliable as an indicator of our performance. |

| • | Following our separation from Kimberly-Clark, we will have a significant amount of debt that could adversely affect our business. |

| • | We have not previously operated as an independent company, and our management team has been assembled for only a short time. |

| • | We could incur significant tax liabilities if the distribution becomes a taxable event. |

| • | We may not be able to engage in certain corporate transactions for up to two years after the distribution. |

| • | As we build our information technology infrastructure and transition our data to our own systems, we could incur substantial additional costs and experience temporary business interruptions. |

| • | We may not realize potential benefits from the separation of our business from Kimberly-Clark’s other businesses. |

| • | The transition services to be provided to us by Kimberly-Clark for a limited time may be difficult for us to perform or replace without operational problems or additional cost. |

| • | Following our separation from Kimberly-Clark, we may experience increased costs resulting from decreased purchasing power, which could decrease our overall profitability and cash flow. |

3

The Separation and Distribution

On November 14, 2013, Kimberly-Clark announced that its Board of Directors authorized management to evaluate a potential tax-free spin-off of our business. In September 2014, after further review and evaluation of the potential spin-off, Kimberly-Clark’s Board of Directors authorized its executive committee to approve the final terms and conditions of the distribution. On October 6, 2014, the executive committee of Kimberly-Clark’s Board of Directors approved the distribution of all of the issued and outstanding shares of Halyard common stock on the basis of one share of Halyard common stock for every eight shares of Kimberly-Clark common stock held as of the close of business on October 23, 2014, the record date for the distribution.

Formation of Halyard

Halyard Health, Inc. was incorporated in Delaware on February 25, 2014 for the purpose of holding Kimberly-Clark’s health care business following the distribution. Prior to the distribution, we and Kimberly-Clark expect to engage in a series of transactions that are designed to transfer ownership of Kimberly-Clark’s health care business to us.

Prior to the distribution, we expect to borrow approximately $640.0 million through the issuance of senior unsecured notes and a secured term loan. We also anticipate entering into a revolving credit facility allowing borrowings of up to $250.0 million. We expect to use the net proceeds from the senior unsecured notes and the secured term loan to fund a portion of the cash distribution to Kimberly-Clark as described below. Funds under the revolving credit facility are expected to be available for our working capital and other requirements after the distribution. For additional information regarding our indebtedness see, “Description of Material Indebtedness.”

Immediately prior to the distribution, we will make a cash distribution to Kimberly-Clark equal to the estimated amount of all of our available cash on the distribution date in excess of the minimum amount (as defined herein). The minimum amount is equal to $40.0 million plus the estimated net amount of certain intercompany assets and liabilities on the distribution date that are to be retained by Kimberly-Clark plus approximately $1.0 million associated with certain retention bonus obligations to be transferred to Halyard; provided, that the minimum amount will be no less than $40.0 million.

We will fund the cash distribution with the net proceeds from our senior unsecured notes and secured term loan and the remainder will be funded with cash on hand and cash transferred to us by Kimberly-Clark in settlement of intercompany transactions associated with the separation. Kimberly-Clark expects to use the proceeds of this cash distribution to make open-market share repurchases.

Prior to the transfer by Kimberly-Clark to us of its health care business, we will have no operations other than those related to our formation and in preparation for the separation and distribution. Following the distribution, we will be a separate public company, and Kimberly-Clark will have no continuing stock ownership in us.

Our Post-Distribution Relationship with Kimberly-Clark

Prior to the distribution, we will enter into a distribution agreement with Kimberly-Clark. In connection with the distribution, we will also enter into various other agreements to effect the separation of our business from Kimberly-Clark’s other businesses and set forth our contractual relationships with Kimberly-Clark after the distribution. These agreements will provide for the allocation, between us and Kimberly-Clark, of Kimberly-Clark’s assets, employees, liabilities and obligations (including its investments, property and employee benefits and tax-related assets and liabilities) attributable to periods prior to, at and after the distribution. The agreements will include a transition services agreement, a tax matters agreement, an employee matters agreement, intellectual property agreements, and manufacturing and supply agreements.

For additional information regarding the distribution agreement and other transaction agreements, see “Risk Factors – Risks Related to the Distribution and Our Separation from Kimberly-Clark” and “Our Relationship with Kimberly-Clark after the Distribution.”

4

Reasons for the Separation and Distribution

Kimberly-Clark’s Board of Directors believes that separating its health care business from the remainder of Kimberly-Clark is in the best interests of Kimberly-Clark and its stockholders for a number of reasons, including:

| • | Strategic Focus. The distribution will allow each business to focus its attention and financial resources to more effectively pursue its own distinct operating priorities and strategies, which have diverged over time. |

| • | Capital Flexibility. The distribution will permit each company to concentrate its financial resources solely on its own operations without having to compete with each other for investment capital and will allow us to utilize our expected excess cash flow to invest in the growth of our business. In addition, we and Kimberly-Clark will have direct access to the debt and equity capital markets to fund our and its respective growth opportunities in a time and manner appropriate for our and Kimberly-Clark’s respective business needs. |

| • | Employee Incentives. We will be able to develop incentive programs to better attract and retain key employees through the use of stock-based and performance-based incentive plans that more directly link compensation with the financial performance of our business. |

| • | Distinct Investment Identity. The distribution will allow investors to separately value Kimberly-Clark and Halyard based on their unique investment identities, including the merits, performance and future prospects of Kimberly-Clark’s and our respective businesses. The distribution will also provide investors with two distinct and targeted investment opportunities. |

| • | Management Realignment. Each company will be able to realign its management structure to better focus on its different product markets and the pursuit of unique business opportunities for long-term growth and profitability. |

Kimberly-Clark’s Board of Directors considered a number of potentially negative factors in evaluating the separation and distribution, including loss of synergies and increased costs, disruptions to the business as a result of the distribution, increased significance of certain costs and liabilities, one-time costs of the separation and distribution, inability to realize anticipated benefits of the distribution, and limitations placed upon Halyard as a result of the tax matters agreement. The Board of Directors, however, concluded that the potential benefits of the separation and distribution outweighed these factors. For more information, see the sections entitled “Risk Factors” and “The Separation and Distribution – Reasons for the Separation and Distribution” included elsewhere in this information statement.

Corporate Information

After the separation, our principal executive offices will be located at 5405 Windward Parkway, Suite 100 South, Alpharetta, GA 30004, and our telephone number will be (678) 425-9273. Our website address is www.halyardhealth.com. Information contained on, or connected to, our website or Kimberly-Clark’s website is not part of this information statement, and you should not rely on that information in making an investment decision.

Reason for Furnishing this Information Statement

This information statement is being furnished solely to provide information to stockholders of Kimberly-Clark who will receive shares of Halyard common stock in the distribution. It is not, and is not to be construed as, an inducement or encouragement to buy or sell any of Halyard’s or Kimberly-Clark’s securities. The information contained in this information statement is believed by Halyard to be accurate as of the date on the cover. Changes may occur after that date, and neither we nor Kimberly-Clark will update the information except in the normal course of our and Kimberly-Clark’s respective disclosure obligations and practices.

5

QUESTIONS AND ANSWERS ABOUT THE SEPARATION AND DISTRIBUTION

| What is Halyard and why is Kimberly-Clark separating its health care business and distributing Halyard common stock? | Halyard currently is a wholly-owned subsidiary of Kimberly-Clark that was formed to hold Kimberly-Clark’s health care business. Following the distribution, Halyard will no longer be a wholly-owned subsidiary of Kimberly-Clark. The separation of our business from Kimberly-Clark and the distribution of Halyard common stock is intended to provide you with equity investments in two distinct companies—Kimberly-Clark and Halyard—that will each be able to focus on its own distinct operating needs, priorities and strategies. The separation and distribution is expected to result in improved long-term performance of our and Kimberly-Clark’s respective businesses for the reasons discussed in “The Separation and Distribution – Reasons for the Separation and Distribution.” | |

| How will the separation and distribution work? | The separation and distribution will be accomplished through a series of transactions in which Kimberly-Clark will transfer its health care business to us and then distribute all of the outstanding shares of Halyard common stock to the stockholders of Kimberly-Clark on a pro rata basis. | |

| What will our relationship be with Kimberly-Clark after the distribution? | We will be a separate, publicly-traded company and Kimberly-Clark will not own Halyard common stock after the distribution. We will, however, enter into a distribution agreement and various other agreements with Kimberly-Clark to effect the separation and set forth our contractual relationships with Kimberly-Clark after the distribution. These agreements will provide for the allocation, between us and Kimberly-Clark, of Kimberly-Clark’s assets, employees, liabilities and obligations (including its investments, property and employee benefits and tax-related assets and liabilities) attributable to periods prior to, at and after the distribution. These agreements also will govern certain relationships between us and Kimberly-Clark after the distribution.

For additional information, see “Our Relationship with Kimberly-Clark after the Distribution.” | |

| How will we be managed after the distribution? | Robert Abernathy is our Chief Executive Officer. Mr. Abernathy joined Kimberly-Clark in 1982 and has held senior management positions throughout Kimberly-Clark, including having overall responsibility for Kimberly-Clark’s health care business from 1997 to early 2004. He will be supported by an experienced management team that includes Christopher Lowery, Senior Vice President and Chief Operating Officer, and Steven Voskuil, Senior Vice President and Chief Financial Officer. For more information on our management team, see “Management.” | |

| When will the distribution occur? | We expect that Kimberly-Clark will distribute the shares of Halyard common stock on October 31, 2014 to holders of record of Kimberly-Clark common stock on the record date. | |

| What is the record date for the distribution? | October 23, 2014. | |

6

| What do I have to do to participate in the distribution? | You are not required to take any action to receive Halyard common stock in the distribution, but you are encouraged to read this entire information statement carefully. No vote will be taken for the distribution. You are not being asked for a proxy.

You do not need to pay any consideration, exchange or surrender your existing Kimberly-Clark common stock or take any other action to receive your shares of Halyard common stock. If you own Kimberly-Clark common stock as of the close of business on the record date, a book-entry account statement reflecting your ownership of shares of Halyard common stock will be mailed to you, or your brokerage account will be credited for the shares.

You should not and do not need to mail in Kimberly-Clark common stock certificates to receive Halyard common stock. | |

| How many shares of Halyard common stock will I receive? | Kimberly-Clark will distribute one share of Halyard common stock for every eight shares of Kimberly-Clark common stock you own as of the close of business on the record date. For example, if you own 80 shares of Kimberly-Clark common stock on the record date, you will receive 10 shares of Halyard common stock in the distribution. Based on approximately 372,114,350 shares of Kimberly-Clark common stock that we expect to be outstanding on the record date, Kimberly-Clark will distribute a total of approximately 46,514,294 shares of Halyard common stock, representing 100% of the outstanding Halyard common stock. For more information, see “The Separation and Distribution.” | |

| Will I receive physical stock certificates representing shares of Halyard common stock? | No, you will not receive a stock certificate in connection with the distribution.

Instead, if you own Kimberly-Clark common stock as of the close of business on the record date, including shares owned in certificate form or through the Kimberly-Clark dividend reinvestment plan, Kimberly-Clark, with the assistance of Computershare Inc. (“Computershare”), the settlement and distribution agent, will electronically distribute shares of Halyard common stock to you or to your brokerage firm on your behalf by way of direct registration in book-entry form. Computershare will mail you a book-entry account statement that reflects your shares of Halyard common stock, or your bank or brokerage firm will credit your account for the shares. | |

| Will Kimberly-Clark distribute fractional shares? | No. In lieu of fractional shares of Halyard common stock, stockholders of Kimberly-Clark will receive cash. Fractional shares you would otherwise be entitled to receive will be aggregated and sold in the public market by the distribution agent. The aggregate net cash proceeds of these sales will be distributed ratably to those stockholders who would otherwise have received fractional shares of Halyard common stock. If you own less than eight shares of Kimberly-Clark common stock on the record date, you will not receive any shares of Halyard common stock in the distribution, but you will receive cash in lieu of fractional shares. Cash you receive in lieu of fractional shares will generally be taxable. | |

| What are the conditions to the distribution? | The distribution is subject to a number of conditions, including, among others:

• the debt financing contemplated to be obtained by Halyard in connection with the distribution, as described in the distribution agreement, shall have been obtained, | |

7

| • the making of a cash distribution from Halyard to Kimberly-Clark prior to the distribution in an amount equal to all of Halyard’s available cash on the distribution date in excess of the minimum amount,

• the receipt of an opinion of Baker Botts, L.L.P. to the effect that the separation and the distribution will qualify as a “reorganization” under Sections 368(a)(1)(D) and 355 of the Internal Revenue Code of 1986, as amended (Code),

• the receipt of an opinion from Houlihan Lokey, Inc. with respect to the solvency of Halyard in connection with the distribution,

| ||

| • Kimberly-Clark shall have completed the transfer to us of assets and liabilities as well as the permits, licenses and registrations relating to our business as described in this information statement,

• the U.S. Securities and Exchange Commission (SEC) shall have declared effective our registration statement on Form 10, of which this information statement is a part, under the Securities Exchange Act of 1934, as amended (Exchange Act), and no stop order relating to our registration statement shall be in effect,

• we and Kimberly-Clark shall have received all permits, registrations and consents required under the securities or blue sky laws of states or other political subdivisions of the United States or of foreign jurisdictions in connection with the distribution,

• the shares of Halyard common stock to be distributed shall have been accepted for listing on the New York Stock Exchange, subject to official notice of distribution,

• execution and delivery of the transaction agreements relating to the separation as described in “Our Relationship with Kimberly-Clark after the Distribution,”

• no order, injunction or decree issued by any court of competent jurisdiction or other legal restraint or prohibition shall be in effect that prevents consummation of the separation, distribution or any of the related transactions, including the transfers of assets and liabilities contemplated by the distribution agreement, and

• no other event or development shall be in existence or have occurred that, in the judgment of Kimberly-Clark’s Board of Directors, in its sole discretion, makes it inadvisable to effect the distribution and other related transactions. | ||

|

Neither we nor Kimberly-Clark can assure you that any or all of these conditions will be met. In addition, Kimberly-Clark can decline at any time to go forward with the separation and distribution. For a complete discussion of all of the conditions to the distribution, see “The Separation and Distribution – Distribution Conditions and Termination.” | ||

| Can Kimberly-Clark decide to cancel the distribution of Halyard common stock even if all of the conditions have been met? | Yes. The distribution is subject to the satisfaction or waiver of certain conditions. Until the distribution has occurred, Kimberly-Clark’s Board of Directors has the right to cancel the distribution, even if all of the conditions are satisfied. See the section entitled “The Separation and Distribution – Distribution Conditions and Termination.” | |

8

| What if I want to sell my Kimberly-Clark common stock or my Halyard common stock? | You should consult with your financial advisors, such as your stockbroker, bank or tax advisor. | |

| What is “regular-way” and “ex-distribution” trading of Kimberly-Clark stock? | Beginning on or shortly before the record date and continuing up to and through the distribution date, it is expected that there will be two markets in Kimberly-Clark common stock: a “regular-way” market and an “ex-distribution” market. Kimberly-Clark common stock that trades in the “regular-way” market will trade with an entitlement to shares of Halyard common stock distributed pursuant to the distribution. Shares that trade in the “ex-distribution” market will trade without an entitlement to shares of Halyard common stock distributed pursuant to the distribution.

If you decide to sell your Kimberly-Clark common stock before the distribution date, you should make sure your stockbroker, bank or other nominee understands whether you want to sell your Kimberly-Clark common stock with or without your entitlement to Halyard common stock pursuant to the distribution. | |

| Is the distribution taxable for U.S. federal income tax purposes? | The distribution is conditioned on the receipt by Kimberly-Clark of an opinion from its outside tax counsel, Baker Botts L.L.P., to the effect that the contribution of our business to us by Kimberly-Clark and the distribution of our common stock will qualify as a “reorganization” under Sections 368(a)(1)(D) and 355 of the Code. Assuming the separation and the distribution qualify as a “reorganization” under Sections 368(a)(1)(D) and 355 of the Code, for U.S. federal income tax purposes, gain or loss generally will not be recognized by Kimberly-Clark on the distribution and, except for gain realized on the receipt of cash paid in lieu of fractional shares, no gain or loss will be recognized by you, and no amount will be included in your income for U.S. federal income tax purposes, upon the receipt of shares of Halyard common stock in the distribution. For more information regarding the potential U.S. federal income tax consequences to Kimberly-Clark and to you of the distribution, see “Material U.S. Federal Income Tax Consequences.” | |

| How will the distribution affect my tax basis in Kimberly-Clark common stock? | For U.S. federal income tax purposes, your basis in the Kimberly-Clark common stock will be allocated between the Kimberly-Clark common stock and Halyard common stock received in the distribution in proportion to their relative fair market values on the date of the distribution. Within a reasonable | |

| time after the distribution is completed, Kimberly-Clark will provide to U.S. taxpayers information to enable them to compute their tax bases in both Kimberly-Clark and Halyard common stock and other information they will need to report their receipt of Halyard common stock on their 2014 U.S. federal income tax return as a tax-free transaction. See “Material U.S. Federal Income Tax Consequences” for a more complete description of the effects on your tax basis. | ||

| Are there risks associated with owning Halyard common stock? | Yes. Ownership of Halyard common stock is subject to both general and specific risks relating to our business, the industry in which we operate, our ongoing contractual relationships with Kimberly-Clark and our status as a separate, publicly-traded company. Ownership of Halyard common stock is also subject to risks relating to the distribution. These risks are described in the “Risk Factors” section of this information statement. You are encouraged to read that section carefully. | |

9

| Will I be paid any dividends on Halyard common stock? | We currently do not anticipate paying cash dividends on Halyard common stock. See “Dividend Policy” for additional information on our dividend policy after the distribution. | |

| Where will I be able to trade shares of Halyard common stock? | We have been authorized to list the Halyard common stock on the New York Stock Exchange under the symbol “HYH.” We anticipate that trading in shares of Halyard common stock will begin on a “when-issued” basis on or around the record date and will continue up to and through the distribution date, and that “regular-way” trading will begin on the first trading day after the distribution date. If trading does begin on a “when-issued” basis, you may purchase or sell Halyard common stock after that time, but your transaction will not settle until after the distribution date. We cannot predict the trading prices of Halyard common stock before, on or after the distribution date. | |

| Will the number of Kimberly-Clark shares I own change as a result of the distribution? | No. The number of shares of Kimberly-Clark common stock you own will not change as a result of the distribution. | |

| What will happen to the listing of Kimberly-Clark common stock? | Kimberly-Clark common stock will continue to be traded on the New York Stock Exchange under the symbol “KMB” following the distribution. | |

| Will Halyard incur any debt prior to or at the time of the distribution? | Yes. We anticipate having approximately $640.0 million of indebtedness upon completion of the distribution. Prior to the distribution, we expect to borrow approximately $640.0 million through the issuance of senior unsecured notes and a secured term loan. We also anticipate entering into a revolving credit facility allowing borrowings of up to $250.0 million. See “Description of Material Indebtedness.” | |

| Who will be the distribution agent, transfer agent and registrar for the Halyard common stock? | The distribution agent, transfer agent and registrar for Halyard common stock will be Computershare. For questions relating to the transfer or mechanics of the stock distribution, you should contact:

Computershare Trust Company, N.A. (866) 286-9199 www.computershare.com/investor

If your shares are held by a bank, broker or other nominee please call them directly. | |

| Where can I find more information about Kimberly-Clark and Halyard? | Before the distribution, if you have any questions relating to Kimberly-Clark, you should contact:

Kimberly-Clark Corporation P.O. Box 619100 Dallas, Texas 75261-9100 Attention: Stockholder Services (972) 281-1522 www.kimberly-clark.com | |

10

|

After the distribution, Halyard stockholders who have any questions relating to Halyard should contact us at:

Halyard Health, Inc. 5405 Windward Parkway Suite 100, South Alpharetta, GA 30004 Attention: Stockholder Services (678) 425-9273 www.halyardhealth.com |

11

You should carefully consider each of the following risks and all of the other information contained in this information statement. Some of the risks described below relate principally to our business and the industry in which we operate, while others relate principally to the distribution and our separation from Kimberly-Clark. The remaining risks relate principally to the securities markets generally and ownership of Halyard common stock.

Our business, results of operations, financial condition or cash flows could be materially adversely affected by any of these risks, and, as a result, the trading price of Halyard common stock could decline.

These risks are not the only ones we face. Other risks that we do not presently know about or that we presently believe are not material could also adversely affect us.

Risks Related to Our Business and Industry

We face strong competition. Our failure to compete effectively could have a material adverse effect on our business.

Our industry is highly competitive. We compete with many domestic and foreign companies ranging from small start-up enterprises that might sell only a single or limited number of competitive products or compete only in a specific market segment, to companies that are larger and more established than us, have a broad range of competitive products, participate in numerous markets and have access to significantly greater financial and marketing resources than we do. We also face competition from distributors who are expanding their private label portfolios and aggressively marketing their product lines. For example, our products are distributed by Cardinal Health, Inc. and Medline Industries, Inc., each of which sells its own private label products and solutions that compete with our offerings. Competitive factors include price, alternative clinical practices, innovation, quality and reputation. Our failure to compete effectively could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may not be successful in developing, acquiring or marketing competitive products and technologies.

Our industry is characterized by extensive research and development and rapid technological advances. The future success of our business will depend, in part, on our ability to design, acquire and manufacture new competitive products and enhance existing products. Accordingly, we commit substantial time, funds and other resources to new product development, including research and development, acquisitions, licenses, clinical trials and physician education. We make these substantial expenditures without any assurance that our products will obtain regulatory clearance or reimbursement approval, acquire adequate intellectual property protection or receive market acceptance. Development by our competitors of improved products, technologies or enhancements may make our products, or those we develop, license or acquire in the future, obsolete or less competitive which could negatively impact our net sales. Our failure to successfully develop, acquire or market competitive new products or enhance existing products could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We are exposed to price fluctuations of key commodities, which may negatively impact our results of operations.

We rely on product inputs, such as nitrile and polypropylene, as well as other commodities, in the manufacture of our products. Prices of oil and gas affect our distribution and transportation costs. Prices of these commodities are volatile and have fluctuated significantly in recent years, which has contributed to, and in the future may continue to contribute to, fluctuations in our results of operations. Our ability to hedge commodity price volatility is limited. Furthermore, due to competitive dynamics, the cost containment efforts of our customers and third-party payors, and contractual limitations, particularly with respect to products we sell under group purchasing agreements, which generally set pricing for a three-year term, we may be unable to pass along commodity-driven

12

cost increases through higher prices. If we cannot fully offset cost increases through other cost reductions, or recover these costs through price increases or surcharges, we could experience lower margins and profitability which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

An inability to obtain key components, raw materials or manufactured products from third parties may have a material adverse effect on our business.

We depend on the availability of various components, raw materials and manufactured products supplied by others for our operations. If the capabilities of our suppliers and third-party manufacturers are limited or stopped, due to quality, regulatory or other reasons or if we are unable to outsource the manufacturing capabilities currently conducted in our manufacturing facility in Thailand where we have initiated a plan to exit, it could negatively impact our ability to manufacture or deliver our products and could expose us to regulatory actions. Further, for quality assurance or cost effectiveness, we purchase from sole suppliers certain components and raw materials such as polymers used in our S&IP products, latex bladders for our pain pumps, and synthetic rubber nitrile for our medical exam gloves. Although there are other sources in the market place for these items, we may not be able to quickly establish additional or replacement sources for certain components or materials due to regulations and requirements of the U.S. Food and Drug Administration (FDA) and other regulatory authorities regarding the manufacture of our products. The loss of any sole supplier or any sustained supply interruption that affects our ability to manufacture or deliver our products in a timely or cost effective manner could have a material adverse effect on our business, results of operations, financial condition and cash flows.

An interruption in our ability to manufacture products may have a material adverse effect on our business.

Many of our key products are manufactured at single locations, with limited alternate facilities, including in certain cases by third-party manufacturers. If one or more of these facilities experience damage, or if these manufacturing capabilities are otherwise limited or stopped due to quality, regulatory or other reasons, including natural disasters or prolonged power or equipment failures, it may not be possible to timely manufacture the relevant products at previous levels or at all. For example, floods have negatively impacted our medical exam gloves manufacturing facility in Thailand in recent years, which has resulted in temporary shut downs of the facility and an associated decrease in production of our medical exam gloves. A reduction or interruption in any of these manufacturing processes could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We are subject to extensive government regulation, which may require us to incur significant expenses to ensure compliance. If we fail to comply with those regulations, this noncompliance could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Many of our products are subject to extensive regulation in the United States by the FDA and other regulatory authorities and by comparable government agencies in other countries concerning the development, design, approval, manufacture, labeling, importing and exporting and sale and marketing of many of our products. Furthermore, our facilities are subject to periodic inspection by the FDA and other federal, state and foreign government authorities, which require manufacturers of medical devices to adhere to certain regulations, including the FDA’s Quality System Regulation, which requires periodic audits, design controls, quality control testing and documentation procedures, as well as complaint evaluations and investigation. Regulations regarding the development, manufacture and sale of medical products are evolving and subject to future change. We cannot predict what impact those regulatory changes may have on our business. Failure to comply with applicable regulations could lead to manufacturing shutdowns, product shortages, delays in product manufacturing, product seizures, recalls, operating restrictions, withdrawal or suspension of required licenses, and prohibitions against exporting of products to, or importing products from, countries outside the United States and may require significant resources to resolve. Any one or more of these events could have a material adverse effect on our business, results of operations, financial condition and cash flows.

13

We are subject to healthcare fraud and abuse laws and regulations that could result in significant liability, require us to change our business practices or restrict our operations in the future.

We are subject to various U.S. federal, state and local laws targeting fraud and abuse in the healthcare industry, including anti-kickback and false claims laws. Violations of these laws are punishable by criminal or civil sanctions, including substantial fines, imprisonment and exclusion from participation in healthcare programs such as Medicare and Medicaid. These laws and regulations are wide ranging and subject to changing interpretation and application, which could restrict our sales or marketing practices. Furthermore, since many of our customers rely on reimbursement from Medicare, Medicaid and other governmental programs to cover a substantial portion of their expenditures, our exclusion from such programs as a result of a violation of these laws could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We must obtain clearance or approval from the appropriate regulatory authorities prior to introducing a new product or a modification to an existing product. The regulatory clearance process may result in substantial costs, delays and limitations on the types and uses of products we can bring to market, any of which could have a material adverse effect on our business.

In the United States, before we can market a new medical device, or a new use of, or claim for, or significant modification to, an existing product, we generally must first receive clearance or approval from the FDA and certain other regulatory authorities. Most major markets for medical devices outside the United States also require clearance, approval or compliance with certain standards before a product can be commercially marketed. The process of obtaining regulatory clearances and approvals to market a medical device can be costly and time consuming, involve rigorous pre-clinical and clinical testing, require changes in products or result in limitations on the indicated uses of products. There can be no assurance that these clearances and approvals will be granted on a timely basis, or at all. In addition, once a device has been cleared or approved, a new clearance or approval may be required before the device may be modified, its labeling changed or marketed for a different use. Medical devices are cleared or approved for one or more specific intended uses and promoting a device for an off-label use could result in government enforcement action. Furthermore, a product approval or clearance can be withdrawn or limited due to unforeseen problems with the device or issues relating to its application. The regulatory clearance and approval process may result in, among other things, delayed, if at all, realization of product net sales, substantial additional costs and limitations on the types of products we may bring to market or their indicated uses, any one of which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may incur product liability losses, litigation liability, product recalls, safety alerts or regulatory action associated with our products which can be costly and disruptive to our business.

The risk of product liability claims is inherent in the design, manufacture and marketing of the medical products of the type we produce and sell. A number of factors could result in an unsafe condition or injury to, or death of, a patient with respect to the products that we manufacture or sell, including physician technique and experience in performing the relevant surgical procedure, component failures, manufacturing flaws, design defects or inadequate disclosure of product-related risks or information.

We are one of several manufacturers of continuous infusion medical devices, such as our ON-Q PAINBUSTER pain pumps, that are involved in several different pending or threatened litigation matters brought by multiple plaintiffs alleging that use of the continuous infusion device to deliver anesthetics directly into a synovial joint after surgery resulted in postarthroscopic glenohumeral chondrolysis, or a disintegration of the cartilage covering the bones in the joint (typically, in the shoulder). Plaintiffs generally seek monetary damages and attorneys’ fees. While Kimberly-Clark is retaining the liabilities related to these matters, the distribution agreement between us and Kimberly-Clark will provide that we will indemnify Kimberly-Clark for any Post-Spin I-Flow Liabilities (as defined herein). There can be no assurance that additional related or unrelated claims or other product liability claims, including potential class actions, will not be made following the distribution date that allege that our products have resulted in or could result in an unsafe condition or injury. Any of these proceedings, regardless of the merits, may result in substantial costs, the diversion of management’s attention from other business concerns,

14

additional restrictions on our sales or the use of our products, or settlement payments and adjustments not covered by or in excess of insurance. Insurance for these types of claims varies in cost and can be difficult to obtain on terms acceptable to us or at all.

In addition to product liability claims and litigation, an unsafe condition or injury to, or death of, a patient associated with our products could lead to a recall of, or issuance of a safety alert relating to, our products, or suspension or delay of regulatory product approvals or clearances, product seizures or detentions, governmental investigations, civil or criminal sanctions or injunctions to halt manufacturing and distribution of our products. Any one of these could result in significant costs and negative publicity resulting in reduced market acceptance and demand for our products and harm our reputation. In addition, a recall or injunction affecting our products could temporarily shut down production lines or place products on a shipping hold.

All of the foregoing types of legal proceedings and regulatory actions are inherently unpredictable and, regardless of the outcome, could disrupt our business, result in substantial costs or the diversion of management attention and could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Current economic conditions have affected and may continue to adversely affect our business, results of operations, financial condition and cash flows.

Disruptions in the financial markets and other macro-economic challenges currently affecting the economy and the economic outlook of the United States, Europe and other parts of the world may continue to have an adverse impact on our results of operations, financial condition and cash flows. Recessionary conditions and depressed levels of consumer and commercial spending have caused and may continue to cause our customers to reduce, modify, delay or cancel plans to purchase our products, and we have observed certain hospitals delaying as well as prioritizing purchasing decisions, which has had and may continue to have a material adverse effect on our business, results of operations, financial condition and cash flows.

In addition, as a result of these recessionary conditions, our customers inside and outside the United States, including foreign governmental entities or other entities that rely on government healthcare systems or government funding, may be unable to pay their obligations on a timely basis or to make payment in full. If our customers’ cash flow or operating and financial performance deteriorate or fail to improve, or if our customers are unable to make scheduled payments or obtain credit, they may not be able to pay, or may delay payment of, accounts receivable owed to us. These conditions also may have an adverse effect on certain of our suppliers who may reduce output or change terms of sales, which could cause a disruption in our ability to produce our products. Any inability of current and/or potential customers to pay us for our products or any demands by our suppliers for different payment terms may have a material adverse effect on our business, results of operations, financial condition and cash flows.

Cost-containment efforts of our customers, purchasing groups, third-party payors and governmental organizations could adversely affect our sales and profitability.

Many of our customers are members of group purchasing organizations, or GPOs, or integrated delivery networks, or IDNs. GPOs and IDNs negotiate pricing arrangements with healthcare product manufacturers and distributors and offer the negotiated prices to affiliated hospitals and other members. Although we are the sole contracted supplier to certain GPOs for certain product categories, members of the GPO are generally free to purchase from other suppliers, and such contract positions can offer no assurance that sales volumes of those products will be maintained. In addition, initiatives sponsored by government agencies and other third-party payors to limit healthcare costs, including price regulation and competitive bidding for the sale of our products, are ongoing in markets where we sell our products. Pricing pressure has also increased in our markets due to consolidation among healthcare providers, trends toward managed care, governments becoming payors of healthcare expenses and regulation relating to reimbursements. The increasing leverage of organized buying groups and consolidated customers and pricing pressure from third-party payors may reduce market prices for our products, thereby reducing our profitability.

15

We face significant uncertainty in the healthcare industry due to government healthcare reform in the United States and elsewhere.

In March 2010, comprehensive healthcare reform legislation was signed into law in the United States through the passage of the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act. Among other initiatives, the legislation implemented a 2.3% excise tax on the sales of certain medical devices in the United States, effective January 2013. In 2013, the excise tax had an impact on us of approximately $6.5 million. In addition, the new legislation implements payment system reforms and significantly alters Medicare and Medicaid reimbursements for medical services and medical devices, which could result in downward pricing pressure and decreased demand for our products.

As additional provisions of healthcare reform are implemented, we anticipate that the U.S. Congress, regulatory agencies and certain state legislatures, as well as international legislators and regulators, will continue to review and assess alternative healthcare delivery systems and payment methods with an objective of ultimately reducing healthcare costs and expanding access. We cannot predict with certainty what healthcare initiatives, if any, will be implemented by states or foreign governments or what ultimate effect federal healthcare reform or any future legislation or regulation may have on our customers’ purchasing decisions regarding our products. However, the implementation of new legislation and regulation may lower reimbursements for our products, reduce medical procedure volumes and adversely affect our business, results of operations, financial condition and cash flows.

Our customers depend on third-party coverage and reimbursements. The failure of healthcare programs to provide coverage and reimbursement, or reductions in levels of reimbursement, could have a material adverse effect on our business.

The ability of our customers to obtain coverage and reimbursements is important to our business. Demand for many of our existing and new medical products is, and will continue to be, affected by the extent to which government healthcare programs and private health insurers reimburse our customers for patients’ medical expenses in the countries where we do business. Any reduction in the amount of reimbursements received by our customers could harm our business by reducing their selection of our products and the prices they are willing to pay.

In addition, as a result of their purchasing power, third-party payors are implementing cost-cutting measures such as seeking discounts, price reductions or other incentives from medical products suppliers and imposing limitations on coverage and reimbursements for medical technologies and procedures. These trends could compel us to reduce prices for our existing products and potential new products and could cause a decrease in the size of the market or a potential increase in competition that could have a material adverse effect on our business, results of operations, financial condition and cash flows.

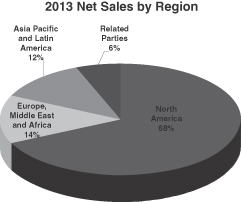

We are subject to political, economic and regulatory risks associated with doing business outside of the United States.

We operate manufacturing facilities outside the United States in Honduras, Mexico and Thailand and source many of our raw materials and components from foreign suppliers. We distribute and sell our products in over 100 countries. In 2013, approximately 28% of our net sales (excluding related party sales) were generated outside of North America, and we expect this percentage will grow over time. Our operations outside of the United States are subject to risks that are inherent in conducting business internationally, including compliance with both United States and foreign laws and regulations that apply to our international operations. These laws and regulations include robust data privacy requirements, labor relations laws that may impede employer flexibility, tax laws, anti-competition regulations, import, customs and trade restrictions, export requirements, economic sanction laws, environmental, health and safety laws, anti-bribery laws such as the U.S. Foreign Corrupt Practices Act and similar anti-bribery laws in other jurisdictions. Given the high level of complexity of these

16

laws, there is a risk that some provisions may be violated inadvertently or through fraudulent or negligent behavior of individual employees, our failure to comply with certain formal documentation requirements or otherwise. In addition, these laws are subject to changes, which may require additional resources or make it more difficult for us to comply with these laws. Violations of the laws and regulations governing our international operations could result in fines or criminal sanctions against us, our officers or our employees, and prohibitions on the conduct of our business. Any such violations could include prohibitions on our ability to manufacture or distribute our products in one or more countries and could have a material adverse effect on our reputation, our brand, our international expansion efforts, our ability to attract and retain employees, our business and our results of operations and financial condition. Our success depends, in part, on our ability to anticipate and prevent or mitigate these risks and manage difficulties as they arise.

In addition to the foregoing, engaging in international business inherently involves a number of other difficulties and risks, including:

| • | different local medical practices, product preferences and product requirements, |

| • | price and currency controls and exchange rate fluctuations, |

| • | cost and availability of international shipping channels, |

| • | longer payment cycles in certain countries other than the United States, |

| • | minimal or diminished protection of intellectual property in certain countries, |

| • | uncertainties regarding judicial systems, including difficulties in enforcing agreements through certain non-U.S. legal systems, |

| • | political instability and actual or anticipated military or political conflicts, expropriation of assets, economic instability and the impact on interest rates, inflation and the credit worthiness of our customers, |

| • | potentially negative consequences from changes in or interpretations of tax laws, including changes regarding taxation of income earned outside the United States, and |

| • | difficulties and costs of staffing and managing non-U.S. operations. |

These risks and difficulties, individually or in the aggregate, could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Currency exchange rate fluctuations could have a material adverse effect on our business and results of operations.

Due to our international operations, we transact business in many foreign currencies and are subject to the effects of changes in foreign currency exchange rates, including the Thai baht, Mexican peso, Japanese yen and the Euro. Our financial statements are reported in U.S. dollars with international transactions being translated into U.S. dollars. If the U.S. dollar strengthens in relation to the currencies of other countries where we sell our products, our U.S. dollar reported net sales and income will decrease. Additionally, we incur significant costs in foreign currencies and a fluctuation in those currencies’ value can negatively impact manufacturing and selling costs. While we have in the past engaged, and may in the future engage, in various hedging transactions to minimize the effects of foreign currency exchange rate fluctuations, there can be no assurance that these hedging transactions will be effective. Changes in the relative values of currencies occur regularly and could have an adverse effect on our business, results of operations, financial condition and cash flows.

We cannot guarantee that any of our strategic acquisitions, investments or alliances will be successful.

We intend to supplement our growth through strategic acquisitions of, investments in and alliances with new medical technologies. The success of any acquisition, investment or alliance may be affected by a number of factors, including our ability to properly assess and value the potential business opportunity or to successfully

17

integrate any business we may acquire into our existing business. These types of transactions may require more resources and investments than originally anticipated, may divert management’s attention from our existing business, may result in exposure to unexpected liabilities of the acquired business, and may not result in the expected benefits, savings or synergies. There can be no assurance that any past or future acquisition, investment or alliance will be cost-effective, profitable or successful.

We may need additional financing in the future to meet our capital needs or to make acquisitions and such financing may not be available on favorable terms, if at all, and may be dilutive to existing stockholders.

We intend to increase our investment in research and development activities and expand our sales and marketing activities. We also intend to make acquisitions. In the past, our working capital and capital expenditure requirements have been met from cash flow generated by our businesses and from Kimberly-Clark. Following the distribution, however, we may need to seek additional debt or equity financing. We may be unable to obtain any desired additional financing on terms favorable to us, if at all. If we lose a previously assigned credit rating or adequate funds are not available on acceptable terms, we may be unable to fund our expansion, successfully develop or enhance products or respond to competitive pressures, any of which could negatively affect our business. If we raise additional funds through the issuance of equity securities, Halyard stockholders will experience dilution of their ownership interest. If we raise additional funds by issuing debt, we may be subject to limitations on our operations due to restrictive covenants. Furthermore, we do not expect that any debt financing we might obtain would reflect interest rates or other terms as favorable as those historically enjoyed by Kimberly-Clark because any credit rating assigned to our debt is likely to be less favorable than similar ratings assigned to the debt of Kimberly-Clark.

We may be unable to protect our intellectual property rights or may infringe the intellectual property rights of others.

We rely on patents, trademarks, trade secrets and other intellectual property assets in the operation of our business. Our efforts to protect our intellectual property and proprietary rights may not be sufficient. We cannot be sure that pending patent applications will result in the issuance of patents or that patents issued or licensed to us will remain valid or prevent competitors from introducing similar competing technologies. Our ability to enforce and protect our intellectual property rights may be limited in certain countries outside of the United States in which we operate, which could make it easier for our competitors to develop or distribute similar competing technologies in those jurisdictions. In addition, our competitive position may be adversely affected by expirations of our significant patents, which would allow competitors to freely use our technology to compete with us.

We operate in an industry characterized by extensive patent litigation and competitors may claim that our products infringe their intellectual property rights. Resolution of patent litigation or other intellectual property claims is inherently unpredictable, typically time consuming and costly and can result in significant damage awards and injunctions that could prevent the manufacture and sale of the affected products or require us to make significant royalty payments in order to continue selling the affected products. Any one of these could have a material adverse effect on our business, results of operations, financial condition and cash flows. At any given time we are involved as either a plaintiff or a defendant in a number of patent infringement actions, the outcomes of which may not be known for prolonged periods of time. We can expect to face additional claims of patent infringement in the future.

We may be unable to attract and retain key employees necessary to be competitive.

Our ability to compete effectively depends upon our ability to attract and retain executives and other key employees, including people in technical, marketing, sales and research and development positions. Competition for experienced employees, particularly for persons with specialized skills, can be intense. Our ability to recruit such talent will depend on a number of factors, including compensation and benefits, work location and work environment. If we cannot effectively recruit and retain qualified executives and employees, our business could be materially adversely affected.

18

Breaches of our information technology systems could have a material adverse effect on our business.

We rely on information technology systems to process, transmit, and store electronic information in our day-to-day operations. Our information technology systems may be subjected to computer viruses or other malicious codes, unauthorized access attempts and cyber- or phishing-attacks. We also store certain information with third parties that could be subject to these types of attacks. These attacks could result in our intellectual property and other confidential information being lost or stolen, disruption of our operations, loss of reputation, and other negative consequences, such as increased costs for security measures or remediation costs and diversion of management attention. While we will continue to implement additional protective measures to reduce the risk of and detect future cyber incidents, cyber-attacks are becoming more sophisticated and frequent, and the techniques used in such attacks change rapidly. There can be no assurances that our protective measures will prevent future attacks that could have a material adverse effect on our business.

Risks Related to the Distribution and Our Separation from Kimberly-Clark

We have no operating history as a separate company, and our historical and pro forma financial data are not necessarily representative of the results we would have achieved as a stand-alone publicly-traded company and therefore may not be reliable as an indicator of our performance.

The historical combined financial data we have included in this information statement present the results of operations and financial position of Kimberly-Clark’s health care business to be transferred to us as that business has historically been operated by Kimberly-Clark. Our historical combined financial data and unaudited pro forma condensed combined financial data included in this information statement are derived from the historical consolidated financial statements and accounting records of Kimberly-Clark. Accordingly, these data may not be indicative of our future performance, nor necessarily reflect what our financial position and results of operations or cash flows would have been, had we operated as a separate, stand-alone publicly-traded entity during the periods presented. This is because, among other things:

| • | Kimberly-Clark performed various corporate functions for us, such as employee payroll and benefits administration, information technology services, financial and tax services, transportation and logistics, procurement services, order management and processing, regulatory compliance and other support services. Following the distribution, Kimberly-Clark will provide some of these functions for a limited period of time as described in “Our Relationship with Kimberly-Clark after the Distribution.” Our historical combined financial data and unaudited pro forma condensed combined financial data reflect adjustments and allocations with respect to corporate and administrative costs relating to these functions which are less than the expenses we expect would have been incurred had we operated as a stand-alone company. |