Attached files

| file | filename |

|---|---|

| 8-K - 8-K - XPO Logistics, Inc. | d791699d8k.htm |

| EX-99.2 - EX-99.2 - XPO Logistics, Inc. | d791699dex992.htm |

Investor Presentation

September 2014

Exhibit 99.1 |

2

Forward-Looking Statements Disclaimer

This document includes forward-looking statements within the meaning of Section

27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended, including the company’s full year 2014 and full year 2017

financial targets. All statements other than statements of historical fact are, or

may be deemed to be, forward-looking statements. In some cases,

forward-looking statements can be identified by the use of forward-looking terms such as "anticipate," "estimate,"

"believe," "continue," "could," "intend,"

"may," "plan," "potential," "predict," "should," "will," "expect," "objective," "projection,"

"forecast,"

"goal,"

"guidance,"

"outlook,"

"effort,"

"target"

or

the

negative

of

these

terms

or

other

comparable

terms.

However,

the

absence

of

these

words

does

not

mean

that

the

statements

are

not

forward-looking.

These

forward-looking

statements

are

based

on certain assumptions and analyses made by us in light of our experience and our

perception of historical trends, current conditions and expected future

developments, as well as other factors we believe are appropriate in the circumstances.

These forward-looking statements are subject to known and unknown risks,

uncertainties and assumptions that may cause actual results, levels of

activity, performance or achievements to be materially different from any future results, levels of activity,

performance or achievements expressed or implied by such forward-looking

statements. Factors that might cause or contribute to a material difference

include those discussed in XPO’s filings with the SEC and the following: economic conditions generally;

competition;

XPO’s

ability

to

find

suitable

acquisition

candidates

and

execute

its

acquisition

strategy;

the

expected

impact

of

acquisitions, including the expected impact on XPO's results of operations; the

ability to realize anticipated synergies and cost savings with respect to

acquired companies; XPO’s ability to raise debt and equity capital; XPO’s ability to attract and retain key

employees

to

execute

its

growth

strategy,

including

acquired

companies’

management

teams;

litigation,

including

litigation

related

to alleged misclassification of independent contractors; the ability to develop and

implement a suitable information technology system; the ability to maintain

positive relationships with XPO’s networks of third-party transportation providers; the ability to retain

XPO’s

and

acquired

companies’

largest

customers;

XPO’s

ability

to

successfully

integrate

acquired

businesses;

rail

and

other

network changes; weather and other service disruptions; and governmental

regulation. All forward-looking statements set forth in this document

are qualified by these cautionary statements and there can be no assurance that the actual results or

developments anticipated will be realized or, even if substantially realized, that

they will have the expected consequences to, or effects on, XPO or its

businesses or operations. Forward-looking statements set forth in this document speak only as of the date

hereof, and XPO undertakes no obligation to update forward-looking statements

to reflect subsequent events or circumstances, changes in expectations or

the occurrence of unanticipated events except to the extent required by law. |

3

One of the Largest 3PLs in North America

We facilitate over 31,000 deliveries per day

#4 freight brokerage firm and Top 50 logistics company

#3 provider of intermodal services

#1 provider of cross-border Mexico intermodal

#1 manager of expedited shipments

#1 provider of last-mile logistics for heavy goods

Leading provider of technology-enabled contract logistics

Growing presence in freight forwarding, LTL and managed

Sources for rankings: Transport Topics, Journal of Commerce and company data

transportation |

4

Clearly Defined Strategy for Value Creation

Acquire companies that bring value and are highly scalable

Significantly scale up and optimize existing operations

Open cold-starts where sales recruitment can drive revenue

We are ahead of plan in transforming XPO Logistics into

a leading multi-modal supply chain provider |

5

$700 Million Strategic Investment in XPO

Three global institutions have invested a total of $700 million of

equity to further XPO’s growth strategy

–

PSP Investments, one of Canada's largest pension investment

managers

–

GIC of Singapore, the fourth largest sovereign fund in the world

–

Ontario Teachers’

Pension Plan, the largest single-profession

plan in Canada

Strong endorsement of XPO’s plan for value creation

Capital primarily will be used to capitalize on acquisition pipeline

Transaction completed September 17, 2014 |

6

Targets raised in light of the $700 million investment

Updated 2017 Full Year Targets

$9 billion of revenue

$575 million of EBITDA |

7

Completed 13 strategic acquisitions and established

23 cold-starts in less than three years

Created leading-edge recruiting and training programs

Introduced scalable IT platform

Added national operations centers for shared services, carrier

procurement and last-mile operations

Stratified customers, assigned a single point of contact to each

Created a culture of passionate on-time performance

Disciplined focus on operational excellence

Precise Execution of Growth Plan |

8

Strong Commitment to Shipper Satisfaction

Integrated network with cross-company visibility

203 locations in the U.S., Canada, Mexico, Asia and Europe

Approximately 10,400 employees

More than 3,600 owner-operator trucks under contract for

Relationships with an additional 27,000 vetted carriers

Access to 60,000 miles of network rail routes

drayage, expedited and last mile subsidiaries |

9

Significant Growth Embedded in XPO’s Model

Strategic

accounts:

market

to

large

shippers

Cold-starts:

expand

footprint

in

markets

with

best

access

to sales talent

Scale

and

productivity:

recruit

sales

reps

and

provide

state-

of-the-art training and IT

Supply

chain

offering:

build

leadership

positions

in

the

fastest-growing areas of logistics

Performance:

become

the

logistics

partner

of

choice

by

providing the most compelling multi-modal supply chain offering

M&A

program:

focus

on

the

top

100

pipeline

prospects |

10

Secular Trends Driving Industry Growth

Growth in e-commerce retailing

Outsourcing of logistics services and capacity

Conversion from over-the-road to intermodal rail

Near-shoring of manufacturing in Mexico

Just-in-time lean production

Driver shortage

Automation of the transportation logistics process |

11

Leading Positions in High-Growth Sectors

Sources: Armstrong & Associates, Norbridge, Inc., EVE Partners LLC, FTR

Associates, SJ Consulting Group, Inc., Bureau of Economic Analysis, US

Department of Commerce Sector

Market

Size

($ billions)

Projected

Growth

(x GDP)

Growth Drivers

Truck brokerage

$50

2-3 times

Outsourcing and technology

Intermodal

$15

3-5 times

Long-haul rail efficiencies and

near-sourcing of

manufacturing in Mexico

Heavy goods,

last-mile

$13

5-6 times

Outsourcing and e-commerce |

Major

Coverage: U.S., Mexico and Canada Source: Company data

Serving over

Manufacturing

Retail, E-commerce

Commercial

Life Sciences

Food and Beverage

Governmental

12

14,000 customers |

13

Acquisition of New Breed Logistics

Compelling reasons for the transaction

Transformational for XPO’s scale and value proposition

–

Combined company of over 200 locations

–

Most differentiated supply chain offering for end-to-end solutions

Capitalizes on trend toward outsourcing reverse logistics,

transportation management, lean manufacturing and aftermarket

support, and other contract logistics services

Expected to create significant cross-selling opportunities with XPO

strategic accounts, New Breed customers and their vendors

Source: Company data |

14

XPO Gains a Preeminent Platform for Growth

Leads the most desirable sector of contract logistics

Technology-enabled solutions for blue chip customers

–

Very stable relationships with low cyclicality

–

Top 10 customers have utilized New Breed for an average of

10 years

Focuses on high-growth industries

–

Technology, telecom, e-commerce, aerospace and defense,

medical equipment and select areas of manufacturing

Operations are led by Louis DeJoy, New Breed’s visionary CEO

Sources: Company data |

15

New Breed’s Attractive Financial Model

16% revenue CAGR for the past 10 years

38% return on invested capital (FY 2013)

(1)

Approximately 99% contractual revenue renewal rate over the

past three years

Low capex requirements (4.2% of revenue in FY 2013) and

largely devoted to IT development

(1)

Return on invested capital equals ongoing operations EBIT divided by the sum of

net working capital and net PP&E Source: Company data

|

16

Industry-defining Technology

Integration of proprietary IT will create strong differentiation

–

XPO NLM is the largest web-based manager of expedited

shipments in North America

–

New Breed’s transportation management system uses

sophisticated tools for dynamic freight optimization, routing

guide management and carrier selection

–

New Breed acquisition has doubled XPO’s IT workforce to

more than 600

Sources: Company data

Combination of two robust managed transportation solutions

|

17

Details of the New Breed Transaction

$615 million cash purchase price

Adds approximately $597 million of revenue (trailing 12 months

ended June 30, 2014)

Multiple of approximately 8.0 times trailing 12 months

adjusted EBITDA

Financed with the proceeds from XPO’s August 2014 private

placement of $500 million of senior notes and available cash

on hand

Transaction completed September 2, 2014 |

18

$500 Million Senior Notes Issued August 2014

Proceeds used to finance the acquisition of New Breed

7.875% senior notes maturing September 1, 2019

High yield market could present attractive avenue for additional

growth capital

Additive to $415 million accounts receivable facility

Long-term leverage targets: fully-drawn ABL plus 2x EBITDA

–

Callable at XPO’s option, September 2016 |

19

Acquired ACL in July 2014

Compelling reasons for the transaction

Non-asset, multi-regional, last mile logistics provider

Moves high volumes of e-commerce purchases for

mega-companies

Adds approximately 160 employees, 14 locations and 650

contracted trucks to XPO

Complementary delivery schedules allow XPO Last Mile to

leverage combined capacity

Pipeline still active for last mile acquisitions |

20

Details of the ACL Transaction

$36.5 million cash purchase price

Adds approximately $63 million of revenue (trailing 12 months

ended June 30, 2014)

Multiple of approximately 5.9 times trailing 12 months

adjusted EBITDA

Transaction completed July 2014 |

21

Acquired Pacer in March 2014

Gained instant scale in North American intermodal

–

Third largest provider of intermodal services

–

#1 provider of cross-border Mexico intermodal, with

30 years’

experience

–

Access to 60,000 miles of network rail routes

–

Decades-deep relationships with the railroads

Added $980 million of revenue (FY 2013), 31 locations and

approximately 800 employees

Sources: SJ Consulting Group, Inc., Bureau of Economic Analysis, US Department of Commerce and company data |

22

Major Intermodal Market Opportunity

$15 billion sector in North America

Sources: SJ Consulting Group, Inc., FTR Associates and

company data –

Growing at three to five times GDP

One of the fastest-growing areas of transportation logistics

Enables shippers to lower transportation costs for freight

traveling 600 miles or more

–

Rail is more fuel-efficient than truckload for long haul

–

Intermodal can lower shipper’s cost by up to 20%

|

23

High-Growth Cross-Border Mexico Sector

Near-shoring

in

Mexico

–

fast

becoming

the

manufacturing

country of choice

–

Competitively priced labor force versus China

–

Faster speed-to-market than overseas locales

–

Can be more cost effective than cross-border truckload

–

Growth driven by billions of dollars invested by major

manufacturers, Mexican government and the rails

Large opportunity to covert to intermodal: an estimated

2.8 million trucks move cross-border each year

Sources: AlixPartners and company data |

24

Integration of Intermodal Is Driving Results

XPO now manages approximately 10% of all domestic

intermodal loads in North America

Stronger value proposition as a large, single-source supply

chain partner with deep capacity

Energetically cross-selling intermodal to XPO customer base,

and selling full service range to intermodal customers

Q2: intermodal revenue up 11.7% and volume up 7.5% YOY

On track to realize $15 million of targeted cost synergies from

integration

Source: Company data |

25

Rebranded as XPO Last Mile

Largest provider of last-mile logistics for heavy goods home

delivery in North America

Facilitates approximately 7 million last-mile deliveries per year

Leading, proprietary software for workflow and customer

experience management

Strong customer-centric culture built by experienced leaders

who now run the business for XPO

Acquired 3PD in August 2013

Source: Company data |

26

XPO Last Mile serves one of the fastest-growing sectors of

non-asset, third party logistics

–

Heavy goods home delivery

growing at five to six times GDP

–

Strong tailwinds from e-commerce and outsourcing

$13 billion market for heavy goods home deliveries

–

Only 30% currently going through 3PLs

Highly fragmented with many small, regional providers

Last Mile’s Exciting Market Potential

Sources: Norbridge, Inc. and EVE Partners LLC |

27

Capitalizing on major advantages of scale and growing

–

Cost efficiencies, productivity, access to trucks, rigorous

quality control systems, expertise

Acquired Optima Service Solutions in November 2013

–

Highly scalable supplier, leading arranger of last mile

installations of large appliances and electronics

Acquisition of ACL brought deep relationships in retail

e-commerce channels

XPO Has a Strong Platform for Last Mile

Source: Company data |

28

Rebranded as XPO NLM

#1 web-based expediter, made XPO the #1 manager of

expedited shipments in North America

Manages an annual run rate of more than three quarters of a

billion dollars of gross transportation spend

–

Online auction system proprietary to XPO

–

Carriers bid on loads that are awarded electronically

Benefits from trend toward just-in-time inventories, and

supply chain disruptions

Acquired NLM in December 2013 |

29

Focused Sales and Marketing Effort

Differentiate XPO by providing a passionate commitment to

customer satisfaction across a range of services

Single point of contact for each customer

–

Strategic accounts team marketing to largest 2,000 shippers

–

National accounts team focused on next largest

5,000 companies

–

Branch network expands our reach to hundreds of

thousands of small and medium-sized shippers

Capture more of the $32 billion less-than-truckload opportunity

Sources: SJ Consulting Group, Inc., company data |

30

One common IT platform for freight brokerage in all cold-starts

and acquired companies

Proprietary freight optimizer tools for pricing and load-covering

put in place in 2012

Highly scalable load execution and tendering via automated

load-to-carrier matching

Total IT budget of more than $70 million for 2014

(1)

Increasing Productivity through Technology

(1) Includes full year IT budget for Pacer and excludes New Breed IT

budget |

31

23 cold-starts

–

11 in freight brokerage, including Kansas City opened

in March; 11 in freight forwarding; one in expedited

Freight brokerage cold-starts on an annual revenue run rate

of more than $220 million

Up from $90 million 12 months ago

Low capital investment can deliver outsized returns

Hire strong industry veterans as branch presidents

Position in prime recruitment areas and scale up

Growth through Cold-starts |

32

Founded and led four highly successful companies,

including world-class public corporations

United Rentals:

Built world’s largest equipment rental company

United Waste:

Created 5th largest solid waste business in North America

Hamilton Resources:

Grew global oil trading company to ~$1 billion

Amerex Oil Associates:

Built one of world’s largest oil brokerage firms

United Rentals stock outperformed S&P 500 by 2.2x from 1997 to 2007

United Waste stock outperformed S&P 500 by 5.6x from 1992 to 1997

CEO Bradley S. Jacobs |

33

Highly Skilled Management Team

Partial list

The full management team can be found on www.xpologistics.com

Troy Cooper

Chief Operating Officer

Paul Smith

President, Intermodal division

Karl Meyer

Chief Executive Officer, XPO Last Mile

Chris Healy

President, Expedited Transportation

John Hardig

Chief Financial Officer

Tom Connolly

Senior Vice President, Acquisitions

Dave Rowe

Chief Technology Officer

Mario Harik

Chief Information Officer

Julie Luna

Chief Commercial Officer

Scott Malat

Chief Strategy Officer

Gordon Devens

General Counsel

United Rentals, United Waste

Pacer International

Boyd Brothers, Caliber Logistics, Roberts Express

Stifel Nicolaus, Alex. Brown

EVE Partners

Echo Global Logistics

Oakleaf Waste Management

AutoNation, Skadden Arps

Goldman Sachs, UBS, JPMorgan Chase

Pacer International, Union Pacific

3PD, Inc., Home Depot |

34

Deep Bench of Industry Experience Partial list

Lou Amo

Vice President, Operational Initiatives

Jake Schnell

Sr. Operational Process and Integration Manager

Jenna Sargent

Regional Sales and Operation Manager

Evan Laskaris

Director of Operations, Chicago

Bud Workmon

President, XPO Last Mile

Jim Commiskey

Strategic Accounts Manager

Greg Ritter

Senior Vice President, Strategic Accounts

Doug George

Branch President, Dallas

Will O’Shea

Chief Sales and Marketing Officer, XPO Last Mile

Andrew Armstrong

Sales and Operations Manager

Drew Wilkerson

Branch President, Charlotte

3PD, Inc., Cardinal Logistics

Electrolux, Union Pacific, Odyssey Logistics

C.H. Robinson

OHL, Schneider Logistics

AFN, CEVA Logistics, Menlo

Pacer International, UPS, Menlo

Knight Brokerage, C.H. Robinson

AFN, Ryder Integrated Logistics

Livingston International, Echo Global Logistics

C.H. Robinson

3PD, Inc., Ryder Integrated Logistics, Cardinal Logistics

|

35

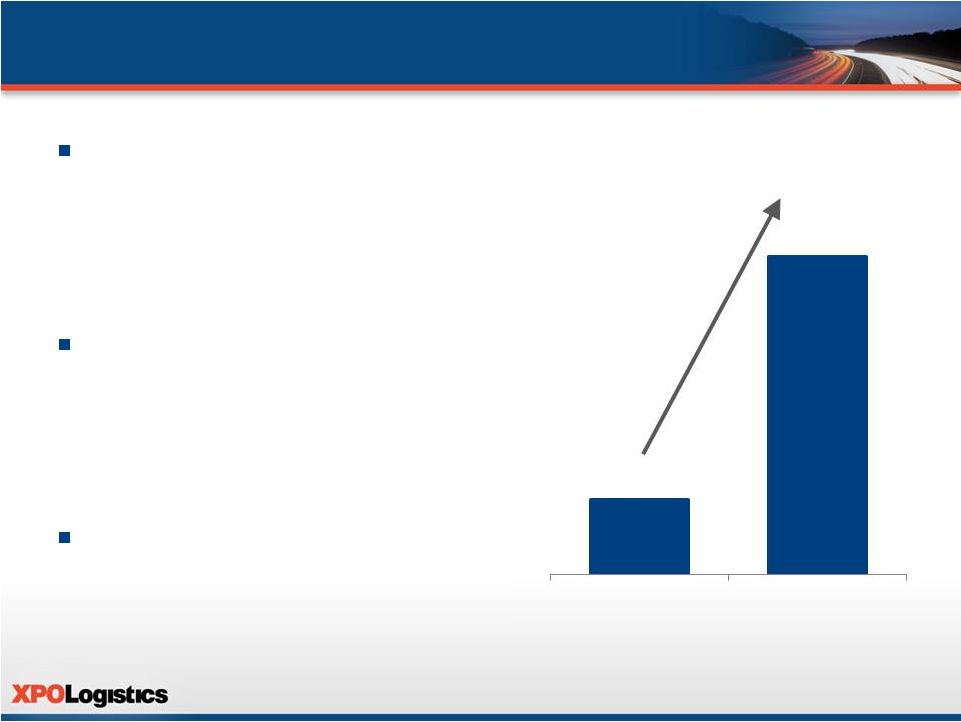

Revenue trajectory

–

2011 revenue of $177 million

–

Approximately $2.3 billion annual

revenue run rate as of 6/30/14

(1)

Q2 company-wide, 2014 vs. 2013

–

Organic growth up 49%

–

Gross revenue up 324%

–

Net revenue up 530%

Organic growth in freight

brokerage up 67%

Revenue and Margin Growth

Gross Revenue ($ millions)

+324%

(1) Excludes beneficial impact of ACL and New Breed acquisitions

Q2 ‘13

Q2 ‘14

$137

$581 |

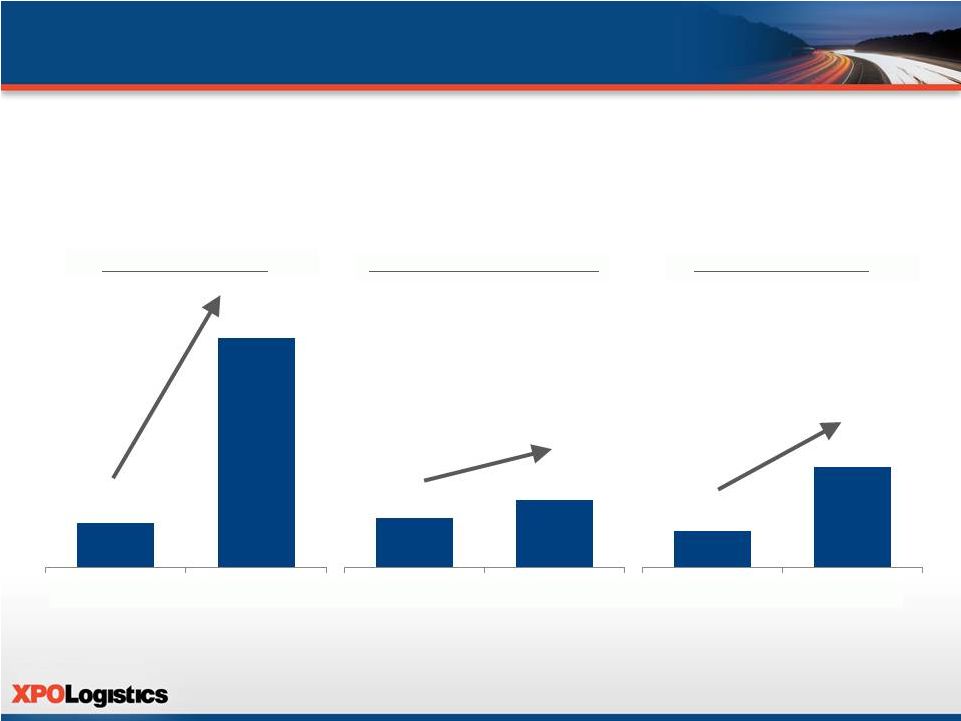

Key

Financial Statistics Expedited Transportation

Freight Brokerage

Freight Forwarding

Q2 Revenue Growth by Business Unit, 2014 vs. 2013

Revenue ($ millions)

+417%

+37%

+180%

36

$26

$36

$19

$54

$493

$95

Q2 ’

13

Q2 ’

14

Q2 ’

13

Q2 ’

14

Q2 ’

13

Q2 ’

14 |

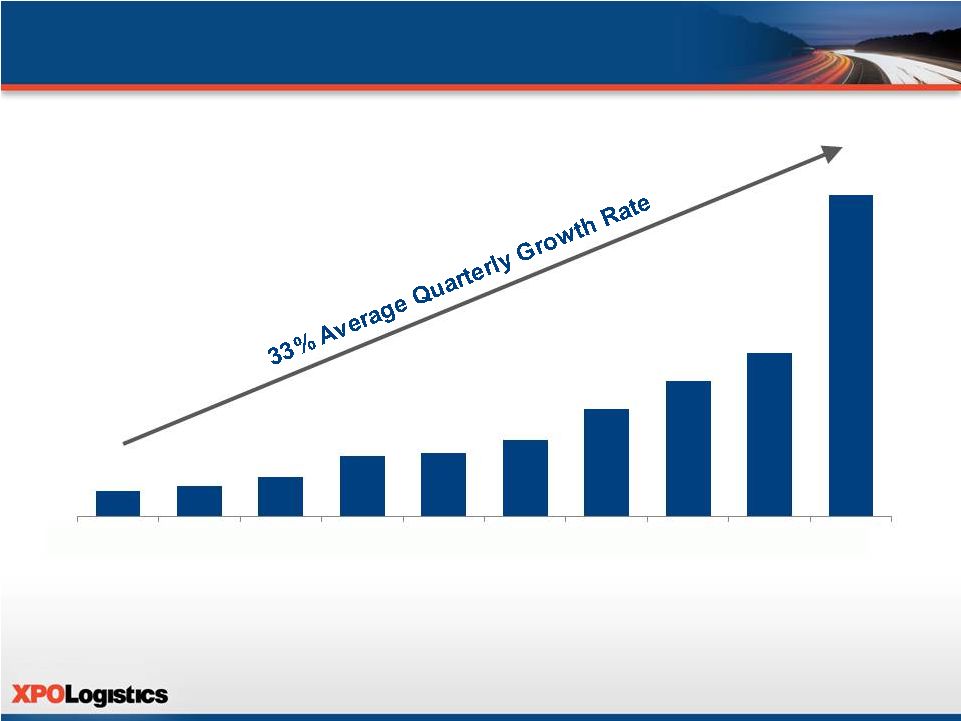

First

30 Months of Growth Strategy 2012

2013

2014

Revenue ($ millions)

37

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

$45

$55

$71

$109

$114

$137

$194

$257

$282

$581 |

38

As of December 31, 2014

Annual revenue run rate of at least $3 billion

Annual EBITDA run rate of at least $150 million

2014 Financial Targets |

39

Incentivized XPO Management

Equity ownership aligns management team with shareholders

Management and directors own approx. 22% of the company

(1)

Common Stock Equivalent Capitalization as of 9/17/14

Common Shares

76.6 million

(2)

Preferred Shares

10.5 million

Warrants (Strike Price $7 per share)

10.6 million (8.7 million dilutive)

(3)

Convertible Senior Notes

7.3 million shares

(4)

Stock Options and RSUs

2.3 million shares dilutive

(5)

Fully Diluted Shares Outstanding

105.4 million shares

(1)

Based on SEC beneficial ownership calculation as of September 17, 2014; includes (i) 10.7 million

shares issued pursuant to the September 2014 private placement (the “Private

Placement”) and (ii) 12.1 million shares on a pro forma basis that are issuable upon conversion of preferred stock

that was issued pursuant to the Private Placement (2)

Includes the common shares described in clauses (i) and (ii) of note (1) above, assuming, on a pro

forma basis, the conversion of preferred shares into common stock, which is subject to

shareholder approval (3)

Dilutive effect of warrants calculated using treasury method (using XPO closing price of

$39.72 on September 17, 2014); total warrant proceeds of $74.0 million (4)

Assumes conversion in full of $120.7 million in aggregate principal amount of outstanding 4.50%

convertible senior notes due 2017

(5)

Dilutive effect of outstanding RSUs and stock options calculated using treasury method (using XPO

closing price of $39.72 on September 17, 2014) |

40

Significant growth embedded in XPO’s business model

Leading positions in fastest-growing areas of transportation

Compelling value proposition as a multi-modal, single-source

provider

Passionate culture of on-time performance and productivity

Top management talent with skills that uniquely fit XPO’s

growth strategy

Clear Path for Significant Value Creation |

41

Additional Information about the Investment

XPO will file a proxy statement and other documents relating to the securities

issued pursuant to the Investment Agreement, dated

as

of

September

11,

2014,

by

and

among

XPO

and

the

Purchasers

named

therein

(the

“Investment”)

with

the

Securities

and Exchange Commission (the “SEC”). INVESTORS AND SECURITY HOLDERS ARE

URGED TO READ THE PROXY STATEMENT AND OTHER DOCUMENTS FILED WITH THE SEC

WHEN THEY BECOME AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO

THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION

ABOUT

THE

INVESTMENT.

Investors

and

security

holders

may

obtain

these

documents

free

of

charge

at

the

SEC’s

website

at

www.sec.gov.

You

may

also

obtain

these

documents

free

of

charge

at

www.xpo.com.

You

may

also

read

and

copy any reports, statements and other information filed by XPO with the SEC at the

SEC public reference room at 100 F Street N.E., Room 1580, Washington, D.C.

20549. Participants in Solicitation

XPO and

its

executive

officers

and

directors

may

be

deemed

to

be

participants

in

the

solicitation

of

proxies

from

XPO

shareholders with respect to the Investment. Information about XPO’s executive

officers and directors is available in XPO’s proxy statement

on

Schedule

14A

for

its

2014

annual

meeting

of

shareholders,

filed

with

the

SEC

on

April

25,

2014.

Investors

and

shareholders may obtain more detailed information regarding the direct and indirect

interests of XPO and its executive officers and directors in the Investment

by reading the proxy statement regarding the Investment when it becomes available. Copies of

these documents may be obtained, free of charge, as described above. This document

shall not constitute an offer to sell or the solicitation

of

an

offer

to

sell

or

the

solicitation

of

an

offer

to

buy

any

securities,

nor

shall

there

be

any

sale

of

securities

in any

jurisdiction in which such offer, solicitation or sale would be unlawful prior to

registration or qualification under the securities laws of any such

jurisdiction. |