Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - INDEPENDENCE REALTY TRUST, INC. | d786259d8k.htm |

Independence

Realty Trust, Inc. September 2014

Exhibit 99.1 |

Forward Looking

Statements, Non-GAAP Financial Measures and Disclaimers 2

This document and the related presentation may contain forward-looking statements within

the meaning of the Private Securities Litigation Reform Act of 1995. These

forward-looking statements include, but are not limited to, statements about

Independence

Realty

Trust,

Inc.’s

(“IRT”)

plans,

objectives,

expectations

and

intentions

with

respect

to

future

operations,

projected acquisitions of properties under contract or in IRT’s pipeline and other

statements that are not historical facts. Forward-looking statements are sometimes

identified by the words “may”, “will”, “should”, “potential”, “predict”, “continue”,

“project”, “guide”, or other similar words or expressions. These

forward-looking statements are based upon the current beliefs and expectations of

IRT's management and are inherently subject to significant business, economic and competitive

uncertainties and contingencies, many of which are difficult to predict and generally not

within IRT’s control. In addition, these forward-looking statements are

subject to assumptions with respect to future business strategies and decisions that are

subject to change. IRT does not guarantee that the assumptions underlying such forward looking

statements are free from errors. Actual results may differ materially from the

anticipated results discussed in these forward-looking statements. The following

factors, among others, could cause actual results to differ materially from the anticipated results or other

expectations expressed in the forward-looking statements: the risk factors and other

disclosure contained in filings by IRT with the Securities and Exchange Commission

(“SEC”), including, without limitation, IRT’s most recent annual and quarterly reports

filed

with

SEC.

IRT’s

SEC

filings

are

available

on

IRT’s

website

at

www.irtreit.com.

You are cautioned not to place undue reliance on these forward-looking statements,

which speak only as of the date of this presentation. All subsequent written and oral

forward-looking statements attributable to IRT or any person acting on its behalf

are expressly qualified in their entirety by the cautionary statements contained or referred

to in this document and the related presentation.

Except

to

the

extent

required

by

applicable

law

or

regulation,

IRT

undertakes

no

obligation

to

update

these

forward-looking statements to reflect events or circumstances after the date of this

presentation or to reflect the occurrence of unanticipated events.

This document and the related presentation may contain non-U.S. generally accepted

accounting principles (“GAAP”) financial measures. A reconciliation of

these non-GAAP financial measures to the most directly comparable GAAP financial measure is

included in this document and/or IRT’s most recent annual and quarterly reports.

This presentation is for informational purposes only and does not constitute an offer

to sell or a solicitation of an offer to buy any securities of IRT.

|

•

IRT is an apartment REIT focused on building a portfolio of well-located apartment properties

in supply constrained secondary and tertiary markets which generate

attractive current returns with

the potential for rent increases and improved operating efficiency.

–

Listed

on

the

NYSE

MKT

in

August

2013

–

“IRT”

–

Targets markets with strong demographic and employment trends with minimal new supply

–

19 properties in 11 states representing 5,342 units at June 30, 2014

–

Focused on delivering strong risk-adjusted returns

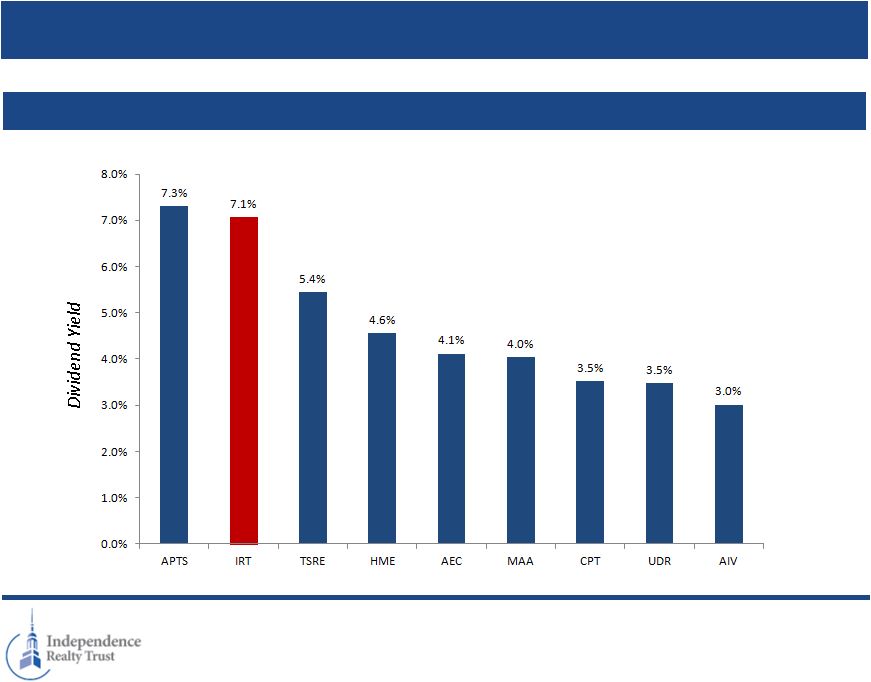

–

Monthly common dividend of $0.06 or $0.72 annually representing a 7.1% yield with a $10.08

stock price at September 4, 2014

–

IRT

is

externally

managed

by

a

subsidiary

of

RAIT

Financial

Trust

(NYSE:

RAS)

–

a

multi-strategy

commercial real estate company with a vertically integrated platform and significant

experience owning and lending against apartment properties

–

Seasoned external manager with significant resources for IRT’s benefit

Who are we?

3 |

Attractive

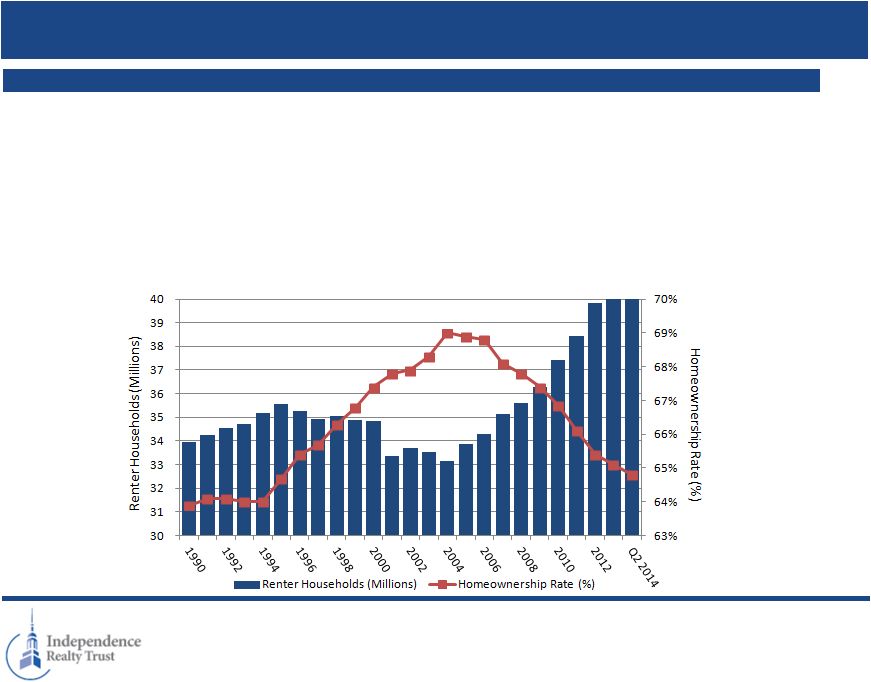

Apartment Industry Dynamics Support Strong Demand 4

IRT expects conditions will remain favorable for apartment fundamentals for the foreseeable

future in secondary markets. •

Positive

Demographic

Factors.

The

Echo

boom

generation

(born

early

80’s

–

’00’s),

which

is

significantly

larger

than

Gen

X

(born

early

60’s –

80’s), is entering the rental market. Harvard research suggests that renters could

make up half of all new households by 2020. This equates to up to 7 million new

renter households this decade. •

Supply Shortage.

Supply has been constrained since the recession; U.S. needs 300,000 new apartments every year

to meet demand. Supply is still playing catch-up from the impacts of the

recession. In 2010, there were only 100,804 new apartments built. In 2013,

134,520 new apartments were built. The majority of new developments since the downturn

have been focused on primary markets. •

Low homeownership.

Changing demographic factors and lifestyles plus stringent mortgage lending standards and

competition from own-to-rent

investors

have

resulted

in

the

homeownership

rate

at

levels

last

seen

in

the

mid-1990s

Positive Trends

Data Source: U.S. Census Bureau, National Multifamily Housing Council (NMHC), Economy.com,

RAIT Financial Trust |

Key Statistics

- Strong Momentum in the Business

5

•

Since June 30, 2013, IRT has more than doubled its portfolio by number of units and

properties (1) Weighted average monthly effective rent per occupied unit

represents the average monthly rent collected for all occupied units after giving

effect

to

tenant

concessions.

We

do

not

report

average

effective

rent

per

unit

in

the

month

of

acquisition

as

it

is

not

representative

of

a

fullmonth

of operations. Same Store weighted average effective rent per unit was $798, $795, $792,

$784, and $784 for the periods presented above, respectively. Same Store is defined as

properties in the portfolio as of March 31, 2013. As of or For the Three-Month Periods Ended

June 30,

2014 March 31,

2014 December 31,

2013 September 30,

2013 June 30,

2013 Financial Statistics:

Total revenue ....................................

$

11,649

$

8,135

$

5,768

$

4,787

$

4,700

Earnings (loss) per share-diluted ........

$

(0.01)

$

0.19

$

0.03

$

0.03

$

0.01

Funds from Operations (“FFO”) per

share ............................................

$

0.18

$

0.33

$

0.17

$

0.17

$

0.23

Core funds from operations (“CFFO”)

per share ......................................

$

0.19

$

0.17

$

0.20

$

0.17

$

0.23

Dividends declared per common

share ............................................

$

0.18

$

0.18

$

0.16

$

0.16

$

0.16

Total Shares Outstanding ...................

17,751,540

17,742,540

9,652,540

9,643,540

5,643,540

Apartment Property Portfolio:

Reported investments in real estate

at cost ...........................................

$

362,323

$

320,437

$

190,096

$

166,665

$

154,040

Net operating income ........................

$

6,081

$

4,147

$

3,159

$

2,373

$

2,459

Number of properties owned.............

19

17

10

9

8

Multifamily units owned ....................

5,342

4,970

2,790

2,358

2,004

Portfolio weighted average

occupancy .....................................

93.1

93.9

94.6%

94.4%

94.2%

Weighted average monthly effective

rent per unit

...............................

$

764

$

730

$

765

$

784

$

784

(1) |

•

IRT seeks to acquire well-located, stable apartment properties in secondary and tertiary

markets –

IRT owned 19 apartment properties totaling 5,342 units in 11 states at June 30, 2014

–

IRT

corporate

office

–

Philadelphia,

PA

Where we are?

6

(1)

Figures are as of and for the three months ended June 30, 2014.

Geographic Diversity (by units)

(1)

National Footprint

(1)

Apartment Property |

IRT

Portfolio 7

Raindance Apts

Oklahoma City,

Oklahoma

Tresa at Arrowhead

Phoenix, Arizona

Augusta Apts

Oklahoma City,

Oklahoma

Belle Creek

Henderson, Colorado

Invitational Apts

Oklahoma City,

Oklahoma

Centrepoint

Tucson, Arizona

Heritage Park Apts

Oklahoma City,

Oklahoma

Cumberland Glen

Smyrna, Georgia

Windrush

Edmund,

Oklahoma

Crestmont

Marietta, Georgia

The Reserve at Eagle Ridge

Waukegan, Illinois

At June 30, 2014

Runaway Bay

Indianapolis, Indiana

Heritage Trace

Newport News, Virginia

Copper Mill

Austin, Texas

The Crossings

Jackson, Mississippi

Berkshire Square

Indianapolis, Indiana

King’s Landing

Creve Coeur, Missouri

Arbors at the

Reservoir

Ridgeland, MS

Carrington Park

Little Rock, AR |

Stable,

Geographically Diversified Portfolio 8

(1)

All dates are for the year in which a significant renovation program was completed, except for

Runaway Bay, King's Landing, Carrington Park and Arbors at the Reservoir, which is the year construction was completed.

(2)

Units represents the total number of apartment units available for rent at June 30, 2014.

(3)

Physical occupancy for each of our properties is calculated as (i) total units rented as of

June 30, 2014 divided by (ii) total units available as of June 30, 2014, expressed as a percentage.

(4)

Average monthly effective rent per occupied unit represents the average monthly rent for all

occupied units for the three-month period ended June 30, 2014. (5)

Does

not

include

6,256

square

feet

of

retail

space

in

six

units,

of

which

1,010

square

feet

of

space

is

occupied

by

RAIT

Residential

for

use

as

the

leasing

office.

The

remaining

5,246

square

feet

of

space

is

86%

occupied

by

four

tenants with an average monthly base rent of $1,603, or $16 per square foot per year. These

five tenants engaged in the following businesses: grocery, retail and various retail services.

(6)

Acquired

as

part

of

the

Oklahoma

City

Portfolio

for

an

aggregate

purchase

price

of

$65,000.

(7)

Assumed

as

part

of

the

Oklahoma

City

Portfolio

and

currently

has

an

aggregate

outstanding

balance

of

$45,435.

(8)

We

do

not

report

average

effective

rent

per

unit

in

the

month

of

acquisition

as

it

is

not

representative

of

a

full

month

of

operations.

Average

effective

rent

during

the

period

of

acquisition

for

Arbors

at

the

Reservoir

was

$1,064.

Property Name

Location

Acquisition Date

Purchase

Price

Debt

Year Built or

Renovated(1)

Units(2)

Physical

Occupancy(3)

Average Monthly

Effective Rent per

Occupied Unit(4)

Belle Creek

Henderson, Colorado

4/29/2011

14,100

$

10,575

$

2011

162

(5)

97.5%

989

$

Copper Mill

Austin, Texas

4/29/2011

14,715

7,245

2010

320

97.5%

786

Crestmont

Marietta, Georgia

4/29/2011

13,500

6,653

2010

228

99.1%

716

Cumberland

Smyrna, Georgia

4/29/2011

13,800

6,802

2010

222

96.4%

704

Heritage Trace

Newport News, Virginia

4/29/2011

11,000

5,422

2010

200

90.5%

687

Tresa

Phoenix, Arizona

4/29/2011

36,675

27,500

2006

360

95.0%

821

Centrepoint

Tucson, Arizona

12/16/2011

29,500

17,600

2006

320

95.9%

816

Runaway Bay

Indianapolis, Indiana

10/11/2012

15,750

10,128

2002

192

95.3%

909

Berkshire Square

Indianapolis, Indiana

9/19/2013

13,250

8,612

2012

354

92.1%

584

The Crossings

Jackson, Mississippi

11/22/2013

23,000

15,313

2012

432

92.4%

735

Reserve at Eagle Ridge

Waukegan, Illinois

1/31/2014

29,000

18,850

2008

370

94.6%

934

Augusta

Oklahoma City, Oklahoma

2/28/2014

65,000

(6)

45,435

(7)

2011

197

82.2%

724

Heritage Park

Oklahoma City, Oklahoma

2/28/2014

-

(6)

-

(7)

2011

453

90.5%

619

Invitational

Oklahoma City, Oklahoma

2/28/2014

-

(6)

-

(7)

2011

344

93.0%

673

Raindance

Oklahoma City, Oklahoma

2/28/2014

-

(6)

-

(7)

2011

504

90.5%

532

Windrush

Edmond, Oklahoma

2/28/2014

-

(6)

-

(7)

2011

160

85.6%

775

King's Landing

Creve Coeur, Missouri

3/31/2014

32,700

21,200

2005

152

93.5%

1,460

Carrington Park

Little Rock, Arkansas

5/07/2014

21,500

-

1999

202

92.6%

1,066

Arbors at the Reservoir

Ridgeland, Mississippi

6/4/2014

20,250

-

2000

170

93.5%

-

(8)

Total/Weighted Average

353,740

$

201,335

$

5,342

93.1%

764

$

At June 30, 2014

($ in thousands, except per unit data) |

Disciplined

Approach to Acquisitions 9

•

Focus on acquiring assets in

supply constrained submarkets

–

Secondary and tertiary markets

–

Sub-markets with no substantial

new apartment construction

–

Stable resident bases and

occupancy rates

–

Positive net migration trends

–

Markets with strong employment

drivers

•

Source acquisitions through existing

relationships and established

channels

–

Existing RAIT relationships

–

Existing property manager

relationships

–

Brokerage community

–

Off-market transactions

–

TIC Syndicates

•

Target Profile for Acquisitions

–

Mid-rise/garden style (150-500 units)

with good amenities

–

Acquire at less than replacement cost in

the $10 -

$35M price range; with 5 to 15

year operating track record

–

In-place cash flow with room to grow

rents

–

Operating efficiencies through

professional property management

–

Well-located property with good access

and favorable local work force

conditions

Markets

Sourcing

Assets

1

2

3 |

Property

Acquisition & Pipeline Update Since 6/30/2014 10

(1)

IRT

cannot

assure

you

that

it

will

acquire

this

property

or

that

any

actual

acquisition

price

will

not

be

significantly

different

from

what

IRT

currently

estimates.

(2)

IRT has determined that no acquisitions in the pipeline are probable as of the date of this

presentation. IRT cannot assure you that it will acquire any of the properties in the

pipeline or that any actual acquisition price will not be significantly different from what IRT currently estimates.

•

Since June 30, 2014, IRT has acquired 2 properties totaling 626 units for purchase prices

aggregating approximately $52.2 million

-

360 units in Memphis, TN for $27.9 million

-

266 units in Raleigh, NC for $24.3 million

•

Property

under

contract

(1)

-

500 unit property in Memphis, TN for $29.8 million (expected mid-September closing)

•

Additionally, IRT currently has an acquisition pipeline of approximately 2,171 units with

an estimated

aggregate

purchase

price

of

$229.5

million

(2) |

Sponsor: RAIT

Financial Trust (NYSE: RAS) 11

•

RAIT is a multi-strategy commercial real estate company organized as an

internally-managed REIT with $5.3 billion of assets under management as of June 30,

2014 –

RAIT’s IPO –

January 1998

–

Offices in Philadelphia, New York, Chicago, and Charlotte

–

Since its inception, RAIT has originated in excess of $1.8 billion of apartment loans and has

owned more than $1.1 billion of apartment properties

–

Allows RAIT to source attractive, off-market acquisition opportunities

–

Provides significant competitive advantage in targeting geographically diversified

portfolios •

Scalable “in-house”

commercial real estate platform with approximately 700 employees, including

property management personnel

•

Seasoned executive team with extensive real estate equity and debt experience

•

Substantial expertise lending to, owning and managing apartment properties

•

Extensive networks of contacts in the apartment industry

•

RAIT Residential, an apartment property management company that is majority-owned by RAIT,

manages over 12,500 apartments in 17 states |

•

RAIT is the largest stockholder in IRT with 7.3 million shares or 28.2% of IRT’s

outstanding common stock at August 20, 2014

•

RAIT provides management and public company services to IRT

•

RAIT controls entities that advise and manage IRT and its properties

–

Externally managed by Independence Realty Advisors, a wholly-owned subsidiary of

RAIT –

Properties managed by RAIT Residential, a full-service apartment property manager that is

majority-owned by RAIT with approximately 300 employees

•

Management agreement structured to incentivize performance

–

No

acquisition,

disposition,

or

financing

fees

and

no

management

fees

on

shareholder

equity

–

No

management

fee

on

8

properties

acquired

prior

to

August

2013;

approximately

$154

million

of

real

estate

–

Low management fee (75 bps of gross real estate assets) on properties acquired after August

2013 –

Incentive fee (20% over a Core FFO yield of 7% (annualized))

Strong Alignment of Interests Between Sponsor and Stockholders

12 |

Scott F.

Schaeffer Management Team

13

Chairman

and

CEO

–

Independence

Realty

Trust,

Inc.

and

Chairman

and

CEO

–

RAIT

Financial

Trust

CEO and Manager –

Independent Realty Advisors, LLC

Over 28 year career in real estate

James J. Sebra

CFO

and

Treasurer

–

Independence

Realty

Trust,

Inc.

and

CFO

and

Treasurer

–

RAIT

Financial

Trust

Treasurer –

Independent Realty Advisors, LLC

17 years of real estate experience

Farrell M. Ender

President

–

Independence

Realty

Trust,

Inc.

and

Senior

Vice

President

–

RAIT

Financial

Trust

President –

Independent Realty Advisors, LLC

Over 10 years experience in the acquisition/disposition, property management, construction

management of apartment properties

Raphael Licht

Manager

–

Independent

Realty

Advisors,

LLC

and

General

Counsel–

RAIT

Financial

Trust

17 years of real estate experience |

Attractive

Dividend 14

(1)

Dividend yields based on share price as of 9/2/2014 and most recently declared quarterly

dividend annualized, except for IRT, which is based on most recently declared monthly

dividend annualized.

Dividend Yield

(1)

(%) |

Core FFO per

Share IRT Financial Highlights

15

Revenue

NOI

Dividends per Share

($ in millions, except per share data)

Note: Refer to slide 18 for reconciliation of Core FFO to GAAP net income (loss).

(1)

Represents a monthly dividend of $0.06 or $0.18 per quarter for Q1, Q2 & Q3.

|

Highlights

16

Strong Momentum in the Business

1

Disciplined Acquisition Strategy with Robust Pipeline

2

Strong Sponsorship and Alignment of Interest with IRT Stockholders

3

Attractive Dividend

4

5

Stable Portfolio in Supply-Constrained Markets |

Appendix

XXX

X |

Income

Statement 18

At June 30, 2014 ($ in millions, except per unit data)

For the Three-Month

Periods Ended June 30

For the Six-Month

Periods Ended June 30

2014 2013 2014 2013 REVENUE:

Rental income

.............................................................................. $

10,613

$

4,218

$

17,966

$

8,396

Tenant reimbursement income.....................................................

436

220

802

443

Other income

............................................................................... 600

262

1,016

549

EXPENSES:

Property operating expenses ........................................................

5,585

2,241

9,573

4,406

General and administrative expenses ...........................................

378

94

546

271

Asset Management Fees

...............................................................

501

79

647

161

Acquisition expenses

.................................................................... 152

—

514

—

Depreciation and amortization .....................................................

3,232

1,063

5,355

2,099

Total expenses ....................................................................

9,848

3,477

16,635

6,937

Operating income

........................................................................

1,801

1,223

3,149

2,451

Interest expense

...........................................................................

(1,930)

(899

(3,229)

(1,787)

Interest income

............................................................................ 1

0

5

0

Gain (loss) on assets

..................................................................... —

—

2,882

—

Net income (loss):

........................................................................

(128)

324

2,807

664

Income allocated to preferred shares ...........................................

0

(4

0

(8)

Income (loss) allocated to noncontrolling interest

.........................

0

(272

0

(604)

Net income (loss) allocable to common shares ............................

$

(128)

$

48

$

2,807

$

52

Earnings (loss) per share:

Basic

................................................................................... $

(0.01)

$

0.01

$

0.17

$

0.03

Diluted

................................................................................ $

(0.01)

$

0.01

$

0.17

$

0.03

Weighted-average shares:

Basic

................................................................................... 17,707,287

3,556,349

16,459,623

1,959,998

Diluted

................................................................................ 17,707,287

3,556,349

16,484,357

1,959,998

|

Balance

Sheet 19

At June 30, 2014 ($ in millions, except per unit data)

As of

June 30,

2014 As of

December 31,

2013

ASSETS:

Investments in real estate:

Investments in real estate at cost

................................................................................................

$

362,323

$

190,096

Accumulated depreciation

...........................................................................................................

(18,804)

(15,775)

Investments in real estate, net

.....................................................................................................

343,519

174,321

Cash and cash equivalents

....................................................................................................................

8,054

3,334

Restricted cash

.....................................................................................................................................

2,698

1,122

Accounts receivable and other

assets....................................................................................................

2,682

1,731

Intangible assets, net of accumulated amortization of $2,513 and $569, respectively

............................

1,126

517

Deferred costs, net of accumulated amortization of $293 and $151, respectively

.................................. 1,568

846

Total Assets

..........................................................................................................................................

$

359,647

$

181,871

LIABILITIES AND EQUITY:

Indebtedness

........................................................................................................................................

$

215,628

$

103,303

Accounts payable and accrued expenses

...............................................................................................

5,725

2,374

Accrued interest payable

......................................................................................................................

30

63

Dividends payable

................................................................................................................................

1,076

515

Other liabilities

.....................................................................................................................................

946

708

Total

Liabilities......................................................................................................................................

223,405

106,963

Equity:

Stockholders’ equity:

...................................................................................................................

Preferred stock, $0.01 par value; 50,000,000 shares authorized, 0 and 0 shares issued and

outstanding, respectively

...............................................................................................

—

—

Common stock, $0.01 par value; 300,000,000 shares authorized, 17,751,540 and

9,652,540 shares issued and outstanding, including 40,000 unvested restricted

common share awards, as of June 30, 2014

.................................................................... 177

96

Additional paid-in capital

....................................................................................................

140,973

78,112

Retained earnings (accumulated deficit)

............................................................................. (6,867)

(3,300)

Total shareholders’ equity

..................................................................................................

134,283

74,908

Noncontrolling interests

..............................................................................................................

1,959

—

Total Equity

..........................................................................................................................................

136,242

74,908

Total Liabilities and Equity

....................................................................................................................

$

359,647

$

181,871

|

Mortgage

Indebtedness 20

At June 30, 2014 ($ in millions, except per unit data)

Outstanding Principal

Carrying Amount

Effective Interest Rate

Maturity Date

Belle Creek Apartments……..

$

10,575

$

10,575

2.4%(1)

April 28, 2021

Berkshire Square Apartments ..

8,612

8,612

4.4%(2)

January 1, 2021

Centrepoint Apartments ..........

17,600

17,600

3.7%(3)

January 1, 2019

Copper Mill Apartments ...........

7,245

7,245

5.7%

May 1, 2021

Crestmont Apartments .............

6,653

6,653

5.7%

May 1, 2021

Cumberland Glen Apartments

..

6,802

6,802

5.7%

May 1, 2021

Heritage Trace Apartments ......

5,422

5,422

5.7%

May 1, 2021

Runaway Bay Apartments ........

10,128

10,128

3.6%

November 1, 2022

Tresa at Arrowhead ..................

27,500

27,500

2.4%(1)

April 28, 2021

Reserve at Eagle Ridge .............

18,850

18,850

4.7%

March 1, 2024

OKC Portfolio ............................

45,435

47,578

2.8%(4)

April 1, 2016

Kings’ Landing

...........................

21,200

21,200

4.0%(5)

June 1, 2021

Crossings

...................................

15,313

15,313

3.9%(5)

June 1, 2024

Total mortgage debt/

Weighted-Average...............

$

201,335

$

203,478

3.7%

Secured Credit Facility ..............

12,150

12,150

2.9%(6)

October 25, 2016

Total indebtedness /Weighted-

Average ...............................

$

213,485

$

215,628

3.6%

|

Non-GAAP

Financial Measures: FFO and CFFO (1)

21 |