Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CenterState Bank Corp | d715378d8k.htm |

| FOR IMMEDIATE RELEASE | Exhibit 99.1 | |||

| April 22, 2014 |

CenterState Banks, Inc. Announces

First Quarter 2014 Operating Results

(All dollar amounts are in thousands, except per share information)

(All earnings per share amounts are reported on a diluted basis unless otherwise noted)

DAVENPORT, FL. – April 22, 2014 - CenterState Banks, Inc. (NASDAQ: CSFL) reported earnings per share of $0.03 ($0.13 excluding merger expenses and branch closure related expenses) on net income of $1,053 for the first quarter of 2014, compared to $0.06 per share on net income of $1,800 reported during the prior quarter.

A comparison of current quarter earnings and prior quarter is presented in the table below:

| 1Q14 | 4Q13 | |||||||

| Earnings per share (GAAP) |

$ | 0.03 | $ | 0.06 | ||||

| Net operating income per share (Non-GAAP) |

$ | 0.13 | $ | 0.07 | ||||

Net operating income is a non-gaap financial measurement used by management to evaluate and monitor financial results of operations excluding certain non-recurring items that include merger and acquisition related expenses and non-recurring charges related to the Company’s efficiency and profitability initiatives announced last quarter, which included impairment charges on the real estate of several of the branches closed during April 2014. A reconciliation table of this non-gaap measurement is presented on page 16, Explanation of Certain Unaudited Non-GAAP Financial Measures.

The primary reason for the increase in net operating income between sequential quarters is the January 17, 2014 acquisition of Gulfstream Bancshares, Inc. and its subsidiary Gulfstream Business Bank (collectively “Gulfstream”). The Company’s NIM remained stable at 4.65% for each of the two comparable quarters, while net interest income increased by $4,112 due to higher average balances of interest earning assets, resulting from the acquisition of Gulfstream. Operating expenses (included in “All other non-interest expense” in the Quarterly Condensed Consolidated Statements of Operations on page 4) increased between the comparable periods due to the four branches and additional operating expenses also acquired from Gulfstream. Gulfstream’s core data processing system was converted into CenterState’s core system on February 14, 2014, and as such, CenterState expects to recognize additional efficiencies in the second quarter compared to the first quarter. The core system termination fees, conversion fees as well as other Gulfstream merger related expenses were approximately $2,072 during the current quarter and are included in “Merger and acquisition related expenses” in the Quarterly Condensed Consolidated Statements on page 4.

In January 2014, the Company announced its efficiency and enhanced profitability initiatives which included consolidating and closing 7 branches and one stand-alone drive-thru facility. These have been closed during April. The Company estimated that the branch closures and other initiatives would produce gross cost savings of approximately $685 during 2Q14 compared to 1Q14. The cumulative quarterly gross cost savings are expected to approximate $1,500 ($6 million on an annualized run-rate basis) compared to the third quarter of 2013, the baseline measurement quarter, by the second quarter of 2015. In January 2014, management also reported that the one-time charges related to these initiatives and the Gulfstream merger related expenses combined would approximate $5.1 million in 1Q14. Actual one time charges recognized during 1Q14 was approximately $5.5 million, however approximately $275 of this amount was initial merger expenses related to the January 29, 2014 announced acquisition of First Southern Bancorp, Inc. (“First Southern) which was not contemplated in the $5.1 million estimate. These charges included approximately $2.5 million of impairment charges on branch office real estate transferred to held-for-sale.

1

As the Gulfstream merger is now fully integrated, management’s focus is now on the completion and integration of First Southern and its subsidiary, First Southern Bank (collectively “First Southern”). The various regulatory applications are in process and the initial registration statement was filed on April 1, 2014. Management expects to close the transaction later this summer.

Loan growth

Non purchased credit impaired (“PCI”) loans increased $322,076 during the quarter, but this included $329,515 acquired on January 17th in the Gulfstream acquisition. Excluding the Gulfstream acquisition, the Company’s non-PCI loans decreased $7,439, or approximately 2.4% on an annualized basis. A summary of the current quarter’s change in non-PCI loans outstanding is presented in the table below.

| Balance at 12/31/13 |

$ | 1,242,758 | ||

| Acquisition of non-PCI loans from Gulfstream 1/17/14 |

329,515 | |||

| Net change in non-PCI loans during the quarter |

(7,439 | ) | ||

|

|

|

|||

| Balance at 3/31/14 |

$ | 1,564,834 | ||

|

|

|

Total PCI loans increased by $19,379 during the quarter, which included $30,068 of PCI loans acquired on January 17th in the Gulfstream acquisition. Excluding the Gulfstream acquisition, the Company’s PCI loans decreased $10,689, or approximately 18.5% on an annualized basis. Of the $250,800 PCI loans outstanding at March 31, 2014 $219,733 are covered by FDIC loss sharing agreements. A summary of the current quarter’s change in PCI loans outstanding is presented in the table below.

| Balance at 12/31/13 |

$ | 231,421 | ||

| Acquisition of PCI loans from Gulfstream 1/17/14 |

30,068 | |||

| Net change in PCI loans during the quarter |

(10,689 | ) | ||

|

|

|

|||

| Balance at 3/31/14 |

$ | 250,800 | ||

|

|

|

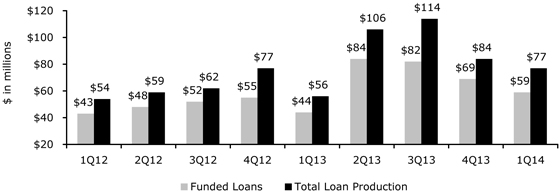

Total new loans originated during the quarter approximated $76.5 million, of which $58.6 million were funded. The weighted average interest rate on funded loans was approximately 4.54%. About 27% of loan production was single family residential, 33% commercial real estate (“CRE”), 24% commercial and industrial (“C&I”) and 16% were all other. Approximately 65% of the current quarter production was fixed rate and 35% variable rate. The graph below summarizes total loan production and funded loan production over the past nine quarters.

2

Although the production was lower in 1Q14 compared to 4Q13, the pipeline is $140 million at March 31, 2014 compared to $114 million at December 31, 2013.

FDIC covered PCI loans and the related indemnification asset

Total PCI loans at March 31, 2014 is equal to $250,800 of which $219,733 are covered by FDIC loss sharing agreements. FDIC covered PCI loans have been performing better than previously estimated. To the extent future estimated cash flows have improved (i.e. future estimated losses have decreased), the additional amount of future estimated cash flows are accreted into interest income over the remaining life of the related loan pool(s), thereby increasing the pool’s yield. The yields on the aggregate covered portion of the PCI loan portfolio have been trending upward as a result of a decrease in the estimate of future losses. During the past nine quarters, the yields on the covered PCI loan portfolio were as follows:

| (unaudited) |

1Q14 | 4Q13 | 3Q13 | 2Q13 | 1Q13 | 4Q12 | 3Q12 | 2Q12 | 1Q12 | |||||||||||||||||||||||||||

| FDIC covered PCI loans |

13.74 | % | 12.91 | % | 14.15 | % | 12.03 | % | 11.06 | % | 7.71 | % | 7.03 | % | 7.51 | % | 6.69 | % | ||||||||||||||||||

The FDIC Indemnification Asset (“IA”) represents the amount that is expected to be collected from the FDIC for reimbursement of 80% of the estimated losses in the covered PCI loan pools. When the Company decreases its estimate of future losses, the expected reimbursement from the FDIC, or IA, is decreased by 80% of this amount. The decrease in estimated reimbursements is expensed (negative accretion) over the lesser of the remaining expected life of the related loan pool(s) or the remaining term of the related loss share agreement(s), and is included in the Company’s non-interest income as a negative amount.

At March 31, 2014, the total IA on the Company’s balance sheet was $64,719. Of this amount, the Company expects to receive reimbursements from the FDIC of approximately $30,805 related to future estimated losses, and expects to expense approximately $33,914 for previously estimated losses that are no longer expected. The $33,914 is now expected to be paid by the borrower (or realized upon the sale of OREO) instead of a reimbursement from the FDIC. At March 31, 2014, the $33,914 previously estimated reimbursements from the FDIC will be written off as expense (negative accretion) in the Company’s non-interest income as summarized below.

| Year |

Year |

|||||||||

| 2014 (9 months) |

37.4 | % | 2018 | 5.3 | % | |||||

| 2015 |

25.2 | % | 2019 | 4.6 | % | |||||

| 2016 |

16.6 | % | 2020 thru 2022 | 4.0 | % | |||||

|

|

|

|||||||||

| 2017 |

6.9 | % | Total | 100.0 | % | |||||

|

|

|

|||||||||

3

Quarterly condensed consolidated income statements (unaudited) are shown below for the periods indicated. See notes 1 and 2 below for a discussion related to FDIC revenue and amortization (negative accretion) included in non-interest income.

Quarterly Condensed Consolidated Statements of Operations (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Interest income |

$ | 29,782 | $ | 25,479 | $ | 26,034 | $ | 24,487 | $ | 24,378 | ||||||||||

| Interest expense |

1,589 | 1,398 | 1,424 | 1,507 | 1,556 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

28,193 | 24,081 | 24,610 | 22,980 | 22,822 | |||||||||||||||

| Recovery (provision) for loan losses |

41 | (183 | ) | 1,273 | (1,374 | ) | 360 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after loan loss provision |

28,234 | 23,898 | 25,883 | 21,606 | 23,182 | |||||||||||||||

| Income from correspondent banking and bond sales division |

3,136 | 3,070 | 2,909 | 4,904 | 6,140 | |||||||||||||||

| Gain on sale of securities available for sale |

— | 22 | — | 1,008 | 30 | |||||||||||||||

| FDIC- IA amortization (negative accretion) (1) |

(5,185 | ) | (4,500 | ) | (3,836 | ) | (3,272 | ) | (2,199 | ) | ||||||||||

| FDIC- revenue (2) |

1,268 | 185 | 3,333 | 1,396 | 628 | |||||||||||||||

| All other non-interest income |

6,541 | 6,420 | 6,201 | 5,827 | 5,680 | |||||||||||||||

| Credit related expenses |

(523 | ) | (510 | ) | (821 | ) | (1,014 | ) | (1,105 | ) | ||||||||||

| FDIC credit related expenses |

(1,301 | ) | (1,310 | ) | (4,934 | ) | (2,120 | ) | (916 | ) | ||||||||||

| Correspondent banking division expenses |

(4,378 | ) | (4,683 | ) | (4,377 | ) | (5,363 | ) | (6,075 | ) | ||||||||||

| Merger and acquisition related expenses |

(2,347 | ) | (539 | ) | (183 | ) | — | — | ||||||||||||

| Branch closure and efficiency initiatives |

(3,158 | ) | — | — | — | — | ||||||||||||||

| All other non-interest expense |

(20,696 | ) | (19,407 | ) | (19,535 | ) | (18,876 | ) | (18,994 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income tax |

1,591 | 2,646 | 4,640 | 4,096 | 6,371 | |||||||||||||||

| Income tax provision |

(538 | ) | (846 | ) | (1,531 | ) | (1,338 | ) | (1,795 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NET INCOME |

$ | 1,053 | $ | 1,800 | $ | 3,109 | $ | 2,758 | $ | 4,576 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings per share (basic) (GAAP) |

$ | 0.03 | $ | 0.06 | $ | 0.10 | $ | 0.09 | $ | 0.15 | ||||||||||

| Earnings per share (diluted) (GAAP) |

$ | 0.03 | $ | 0.06 | $ | 0.10 | $ | 0.09 | $ | 0.15 | ||||||||||

| Net operating income per share (Non-GAAP) (3) |

$ | 0.13 | $ | 0.07 | $ | 0.11 | $ | 0.07 | $ | 0.15 | ||||||||||

| Average common shares outstanding (basic) |

34,465,022 | 30,112,475 | 30,109,728 | 30,098,853 | 30,089,726 | |||||||||||||||

| Average common shares outstanding (diluted) |

34,862,703 | 30,244,648 | 30,243,873 | 30,161,241 | 30,159,188 | |||||||||||||||

| Common shares outstanding at period end |

35,535,530 | 30,112,475 | 30,112,475 | 30,104,270 | 30,095,520 | |||||||||||||||

| note 1: | On the date of an FDIC acquisition (with loss share), the Company estimates expected future losses and the timing of those losses by loan pool. The related reimbursements from the FDIC for approximately 80% of those losses are recorded as a receivable from the FDIC, referred to as indemnification asset or “IA.” The Company updates its estimate of future losses and the timing of the losses each quarter. To the extent management estimates that future losses are less than prior expected future losses, management adjusts its estimates of future expected cash flows and this increase is accreted to interest income over the remaining life of those specific loan pools, increasing the yield on loans. Because management no longer expects these incremental future losses on the loan pool(s), then the expected future reimbursements from the FDIC for approximately 80% of these losses are also reduced. Instead of immediately charging down the IA for expected future FDIC reimbursements, the IA is written down over the shorter of the loss share period or the life of the related loan pool(s) by negative accretion (amortization) in this line item. |

| note 2: | Two FDIC related revenue items are included in this line item. The first item is FDIC reimbursement income from the sale of OREO. When OREO (those covered by loss share agreements) is sold for a loss, approximately 80% of the loss is recognized as income and included in this line item. Second, when a loan pool (with loss share) is impaired, the impairment expense is included in provision for loan losses, and approximately 80% of that loss is recognized as income from FDIC reimbursement, and included in this line item as well. |

| note 3: | This non-gaap metric represents gaap net income excluding nonrecurring income and expense items net of the effective tax rate for the period presented. Items excluded are gains on sales of securities held for sale, acquisition and merger related expenses and one time charges related to the Company’s efficiency and profitability initiatives announced last quarter, which include impairment charges on the real estate of several of the branches closed during April 2014, divided by the average diluted common shares outstanding. A reconciliation table is presented on page 16, Explanation of Certain Unaudited Non-GAAP Financial Measures. |

4

The condensed quarterly results of the Company’s correspondent banking and bond sales segment are presented below.

Quarterly Condensed Segment Information - Correspondent banking and bond sales division (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Net interest income |

$ | 707 | $ | 748 | $ | 725 | $ | 607 | $ | 774 | ||||||||||

| Total non-interest income (note 1) |

3,931 | 4,025 | 3,771 | 5,609 | 7,005 | |||||||||||||||

| Total non-interest expense (note 2) |

(4,378 | ) | (4,683 | ) | (4,377 | ) | (5,363 | ) | (6,075 | ) | ||||||||||

| Income tax provision |

(100 | ) | (35 | ) | (46 | ) | (329 | ) | (657 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 160 | $ | 55 | $ | 73 | $ | 524 | $ | 1,047 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Contribution to diluted earnings per share |

$ | — | $ | — | $ | — | $ | 0.02 | $ | 0.03 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allocation of indirect expense net of inter-company earnings credit, net of income tax benefit (note 3) |

$ | (150 | ) | $ | (353 | ) | $ | (303 | ) | $ | (283 | ) | $ | (286 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Contribution to diluted earnings per share after deduction of allocated indirect expenses |

$ | — | $ | (0.01 | ) | $ | (0.01 | ) | $ | 0.01 | $ | 0.03 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| note 1: | The primary component in this line item is gross commissions earned on bond sales (“income from correspondent banking and bond sales division”) which was $3,136, $3,070, $2,909, $4,904 and $6,140 for 1Q14, 4Q13, 3Q13, 2Q13 and 1Q13 respectively. The remaining non interest income items in this category include fees from safe-keeping activities, bond accounting services, asset/liability consulting related activities, international wires, clearing and corporate checking account services, and other correspondent banking related revenue and fees. |

| note 2: | A significant portion of these expenses are variable in nature and are a derivative of the income from correspondent banking and bond sales division. The amounts do not include any indirect support allocation costs. |

| note 3: | A portion of the cost of the Company’s indirect departments such as human resources, accounting, deposit operations, item processing, information technology, compliance and others have been allocated to the correspondent banking and bond sales division based on management’s estimates. In addition, commencing in 1Q14, an inter-company earnings credit is allocated to the segment for services provided to the commercial bank segment, also based on management’s estimates and judgment. |

Net Interest Margin (“NIM”)

The Company’s NIM remained stable quarter to quarter at 4.65%. The yields on non PCI loans, 4.64% during 4Q13, would have decreased slightly in 1Q14 because the average interest rate on new loans funded during 1Q14 was approximately 4.54%, but the yields on the non PCI loans acquired from Gulfstream during the current quarter were higher than the 4.64% average from last quarter, which is the primary reason why the yield in this loan category increased from 4.64% to 4.75% between sequential quarters.

Total PCI loan yields increased from 13.00% to 13.27% between sequential quarters primarily due to an increase in the yield on FDIC covered PCI loans, which comprises approximately 88% of this portfolio. Yield on FDIC covered PCI loans increased from approximately 12.91% to 13.74% between sequential quarters. The FDIC covered PCI loans are performing better than previously estimated, and as such the future estimated cash flows are higher, which is accreted into interest income over the remaining lives of the loan pools resulting in increasing yields.

5

The table below summarizes yields and costs by various interest earning asset and interest bearing liability account types for the current quarter, the previous calendar quarter and the same quarter last year.

Yield and cost table (unaudited)

| 1Q14 | 4Q13 | 1Q13 | ||||||||||||||||||||||||||||||||||

| average | interest | avg | average | interest | avg | average | interest | avg | ||||||||||||||||||||||||||||

| balance | inc/exp | rate | balance | inc/exp | rate | balance | inc/exp | rate | ||||||||||||||||||||||||||||

| Loans (TEY)* |

$ | 1,513,060 | $ | 17,727 | 4.75 | % | $ | 1,229,868 | $ | 14,388 | 4.64 | % | $ | 1,133,046 | $ | 13,718 | 4.91 | % | ||||||||||||||||||

| PCI loans (note 1) |

251,587 | 8,231 | 13.27 | % | 240,804 | 7,890 | 13.00 | % | 287,181 | 7,827 | 11.05 | % | ||||||||||||||||||||||||

| Taxable securities |

492,766 | 3,478 | 2.86 | % | 414,107 | 2,843 | 2.72 | % | 417,185 | 2,389 | 2.32 | % | ||||||||||||||||||||||||

| Tax -exempt securities (TEY) |

39,280 | 511 | 5.28 | % | 39,551 | 516 | 5.18 | % | 43,043 | 533 | 5.02 | % | ||||||||||||||||||||||||

| Fed funds sold and other |

197,915 | 239 | 0.49 | % | 161,270 | 210 | 0.52 | % | 137,776 | 198 | 0.58 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Tot. interest earning assets(TEY) |

$ | 2,494,608 | $ | 30,186 | 4.91 | % | $ | 2,085,600 | $ | 25,847 | 4.92 | % | $ | 2,018,231 | $ | 24,665 | 4.96 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Interest bearing deposits |

$ | 1,653,806 | $ | 1,337 | 0.33 | % | $ | 1,405,244 | $ | 1,225 | 0.35 | % | $ | 1,462,511 | $ | 1,383 | 0.38 | % | ||||||||||||||||||

| Fed funds purchased |

41,999 | 6 | 0.06 | % | 34,782 | 5 | 0.06 | % | 44,662 | 5 | 0.05 | % | ||||||||||||||||||||||||

| Other borrowings |

29,768 | 23 | 0.31 | % | 19,729 | 18 | 0.36 | % | 20,381 | 18 | 0.36 | % | ||||||||||||||||||||||||

| Corporate debentures |

22,573 | 223 | 4.01 | % | 16,994 | 150 | 3.50 | % | 16,975 | 150 | 3.58 | % | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total interest bearing liabilities |

$ | 1,748,146 | $ | 1,589 | 0.37 | % | $ | 1,476,749 | $ | 1,398 | 0.38 | % | $ | 1,544,529 | $ | 1,556 | 0.41 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Net Interest Spread (TEY) |

4.54 | % | 4.54 | % | 4.55 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Net Interest Margin (TEY) |

4.65 | % | 4.65 | % | 4.64 | % | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

| * | TEY = tax equivalent yield |

| note 1: | Purchased Credit Impaired (“PCI”) loans are loans accounted for pursuant to ASC Topic 310-30. Total PCI loans at March 31, 2014 are equal to $250,800, of which $219,733 is covered by FDIC loss share agreements. |

The table below summarizes the Company’s yields on interest earning assets and costs of interest bearing liabilities over the prior five quarters.

Five quarter trend of yields and costs (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Yield on loans (TEY)* |

4.75 | % | 4.64 | % | 4.70 | % | 4.84 | % | 4.91 | % | ||||||||||

| Yield on PCI loans |

13.27 | % | 13.00 | % | 14.17 | % | 12.03 | % | 11.05 | % | ||||||||||

| Yield on securities (TEY) |

3.04 | % | 2.94 | % | 2.62 | % | 2.44 | % | 2.57 | % | ||||||||||

| Yield on fed funds sold and other |

0.49 | % | 0.52 | % | 0.74 | % | 0.51 | % | 0.58 | % | ||||||||||

| Yield on total interest earning assets |

4.84 | % | 4.85 | % | 5.18 | % | 4.82 | % | 4.90 | % | ||||||||||

| Yield on total interest earning assets (TEY) |

4.91 | % | 4.92 | % | 5.25 | % | 4.89 | % | 4.96 | % | ||||||||||

| Cost of interest bearing deposits |

0.33 | % | 0.35 | % | 0.35 | % | 0.37 | % | 0.38 | % | ||||||||||

| Cost of fed funds purchased |

0.06 | % | 0.06 | % | 0.05 | % | 0.07 | % | 0.05 | % | ||||||||||

| Cost of other borrowings |

0.31 | % | 0.36 | % | 0.36 | % | 0.35 | % | 0.36 | % | ||||||||||

| Cost of corporate debentures |

4.01 | % | 3.50 | % | 3.55 | % | 3.54 | % | 3.58 | % | ||||||||||

| Cost of interest bearing liabilities |

0.37 | % | 0.38 | % | 0.38 | % | 0.40 | % | 0.41 | % | ||||||||||

| Net interest margin (TEY) |

4.65 | % | 4.65 | % | 4.96 | % | 4.59 | % | 4.64 | % | ||||||||||

| Cost of total deposits |

0.22 | % | 0.24 | % | 0.25 | % | 0.27 | % | 0.28 | % | ||||||||||

| * | TEY = tax equivalent yield |

6

The table below summarizes selected financial ratios over the prior five quarters.

Selected financial ratios (unaudited)

| As of or for the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Return on average assets (annualized) |

0.15 | % | 0.30 | % | 0.53 | % | 0.46 | % | 0.78 | % | ||||||||||

| Return on average equity (annualized) |

1.32 | % | 2.60 | % | 4.56 | % | 4.00 | % | 6.76 | % | ||||||||||

| Loan / deposit ratio |

71.0 | % | 71.7 | % | 74.3 | % | 72.6 | % | 70.3 | % | ||||||||||

| Stockholders’ equity (to total assets) |

11.1 | % | 11.3 | % | 11.7 | % | 11.5 | % | 11.6 | % | ||||||||||

| Common tangible equity (to total tangible assets) |

9.4 | % | 9.4 | % | 9.7 | % | 9.5 | % | 9.6 | % | ||||||||||

| Tier 1 capital (to average assets) |

10.0 | % | 10.4 | % | 10.6 | % | 10.3 | % | 10.1 | % | ||||||||||

| Efficiency ratio, including correspondent banking (note 1) |

74.6 | % | 80.9 | % | 78.1 | % | 77.8 | % | 75.6 | % | ||||||||||

| Efficiency ratio, excluding correspondent banking (note 2) |

70.9 | % | 75.2 | % | 72.8 | % | 73.7 | % | 73.0 | % | ||||||||||

| Common equity per common share |

$ | 9.38 | $ | 9.08 | $ | 9.06 | $ | 9.02 | $ | 9.18 | ||||||||||

| Common tangible equity per common share |

$ | 6.95 | $ | 7.38 | $ | 7.35 | $ | 7.30 | $ | 7.45 | ||||||||||

| note 1: | Numerator equals non-interest expense less non-recurring expenses (e.g. merger costs, bank property impairment, etc.) less intangible amortization (both CDI and Trust intangible) less credit related expenses. Denominator equals net interest income on a taxable equivalent yield basis (“TEY”) before the provision for loan losses plus non-interest income less non-recurring income (e.g. gain on sale of securities available for sale, etc.) less FDIC income related to losses on the sales of covered OREO properties and impairment of loan pool(s) covered by FDIC loss share arrangements. |

| note 2: | Numerator starts with the same numerator as in “note 1”, less correspondent bank non-interest expense, including indirect expense allocations. Denominator starts with the same denominator as in “note 1”, less correspondent bank net interest income and less correspondent bank non-interest income. |

7

Loan portfolio mix and covered loans

Approximately 12% of the Company’s loans, or $219,733, are covered by FDIC loss sharing agreements related to the acquisition of three failed financial institutions during the third quarter of 2010 and two during the first quarter of 2012. Pursuant to the terms of the loss sharing agreements, the FDIC is obligated to reimburse the Company for 80% of losses with respect to the covered loans beginning with the first dollar of loss incurred, subject to the terms of the agreements. The Company will reimburse the FDIC for its share of recoveries with respect to the covered loans. The loss sharing agreements applicable to single family residential mortgage loans provide for FDIC loss sharing and the Company reimbursement to the FDIC for recoveries for ten years. The loss sharing agreements applicable to commercial loans provides for FDIC loss sharing for five years and Company reimbursement to the FDIC for a total of eight years for recoveries. All of the covered loans acquired are accounted for pursuant to ASC Topic 310-30.

In addition to the FDIC covered loans, the Company also has $31,067 of other Purchased Credit Impaired (“PCI”) loans at March 31, 2014 which are also accounted for pursuant to ASC Topic 310-30. Of this amount $1,101 are consumer loans acquired pursuant to FDIC assisted transactions of failed financial institutions that are not covered by FDIC loss sharing agreements and $29,966 acquired in the Company’s January 17, 2014 acquisition of Gulfstream Business Bank. The table below summarizes the Company’s loan mix over the most recent five quarter ends.

Loan mix (unaudited)

| At quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Loans |

||||||||||||||||||||

| Real estate loans |

||||||||||||||||||||

| Residential |

$ | 495,450 | $ | 458,331 | $ | 449,224 | $ | 437,946 | $ | 432,892 | ||||||||||

| Commercial |

736,406 | 528,710 | 529,172 | 504,487 | 478,790 | |||||||||||||||

| Land, development and construction loans |

60,726 | 62,503 | 60,375 | 60,928 | 59,524 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total real estate loans |

1,292,582 | 1,049,544 | 1,038,771 | 1,003,361 | 971,206 | |||||||||||||||

| Commercial loans |

217,482 | 143,263 | 126,451 | 124,465 | 115,217 | |||||||||||||||

| Consumer and other loans |

54,205 | 49,547 | 49,065 | 48,084 | 47,991 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans before unearned fees and costs |

1,564,269 | 1,242,354 | 1,214,287 | 1,175,910 | 1,134,414 | |||||||||||||||

| Unearned fees and costs |

565 | 404 | 135 | (2 | ) | (217 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Non-PCI loans |

1,564,834 | 1,242,758 | 1,214,422 | 1,175,908 | 1,134,197 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| PCI loans |

||||||||||||||||||||

| Real estate loans |

||||||||||||||||||||

| Residential |

117,879 | 120,030 | 124,027 | 128,930 | 135,068 | |||||||||||||||

| Commercial |

112,558 | 100,012 | 109,285 | 118,999 | 130,549 | |||||||||||||||

| Land, development and construction loans |

11,144 | 6,381 | 5,673 | 4,897 | 7,777 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total real estate loans |

241,581 | 226,423 | 238,985 | 252,826 | 273,394 | |||||||||||||||

| Commercial loans |

8,118 | 3,850 | 3,906 | 4,002 | 4,577 | |||||||||||||||

| Consumer and other loans (note 1) |

1,101 | 1,148 | 1,259 | 2,851 | 2,818 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total PCI loans (note 2) |

250,800 | 231,421 | 244,150 | 259,679 | 280,789 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Loans |

$ | 1,815,634 | $ | 1,474,179 | $ | 1,458,572 | $ | 1,435,587 | $ | 1,414,986 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| note 1: | Consumer loans acquired pursuant to five FDIC assisted transactions of failed financial institutions during the third quarter of 2010 and first quarter of 2012. These loans are not covered by an FDIC loss share agreement and are being accounted for pursuant to ASC Topic 310-30. |

| note 2: | Included in the $250,800 PCI loans at March 31, 2014 are $219,733 of loans that are covered by FDIC loss sharing arrangements. Of the remaining PCI loan amount, $29,966 were acquired in the Company’s January 17, 2014 acquisition of Gulfstream Business Bank and $1,101 are consumer loans acquired pursuant to FDIC assisted transactions of failed financial institutions that are not covered by FDIC loss sharing agreements referred to in note 1 above. |

8

Credit quality and allowance for loan losses

During the quarter, excluding PCI loans, the Company recorded a negative loan loss provision expense of $464 and charge-offs net of recoveries of $317, resulting in a decrease in the allowance for loan losses (excluding PCI loans) of $781 as shown in the table below.

With regard to PCI loans, the Company recorded a loan loss provision expense of $423, resulting in an increase in the allowance for loan losses on PCI loans of $423. See the table “Allowance for loan losses” for additional information.

The allowance for loan losses (“ALLL”) was $20,096 at March 31, 2014 compared to $20,454 at December 31, 2013, a decrease of $358. This decrease is the result of the aggregate effect of a $889 decrease in general loan loss allowance, a $108 increase in the specific loan loss allowance related to impaired loans and a $423 increase in the loan loss allowance related to PCI loans accounted for pursuant to ASC Topic 310-30. The changes in the Company’s ALLL components between March 31, 2014 and December 31, 2013 are summarized in the table below.

| Mar 31, 2014 | Dec 31, 2013 | increase (decrease) | ||||||||||||||||||||||||||||||||||

| loan | ALLL | loan | ALLL | loan | ALLL | |||||||||||||||||||||||||||||||

| balance | balance | % | balance | balance | % | balance | balance | |||||||||||||||||||||||||||||

| Non impaired loans |

$ | 1,218,614 | $ | 16,994 | 1.39 | % | $ | 1,218,648 | $ | 17,883 | 1.47 | % | $ | (34 | ) | $ | (889 | ) | -8 bps | |||||||||||||||||

| Gulfstream loans (note 1) |

319,665 | — | — | % | — | — | % | 319,665 | — | |||||||||||||||||||||||||||

| Impaired loans |

26,555 | 1,919 | 7.23 | % | 24,110 | 1,811 | 7.51 | % | 2,445 | 108 | -28 bps | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Non-PCI loans |

1,564,834 | 18,913 | 1.21 | % | 1,242,758 | 19,694 | 1.58 | % | 322,076 | (781 | ) | -37 bps | ||||||||||||||||||||||||

| PCI loans (note 2) |

250,800 | 1,183 | 231,421 | 760 | 19,379 | 423 | ||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

| Total loans |

$ | 1,815,634 | $ | 20,096 | 1.11 | % | $ | 1,474,179 | $ | 20,454 | 1.39 | % | $ | 341,455 | $ | (358 | ) | -28 bps | ||||||||||||||||||

| note 1: | Loans acquired in the Company’s January 17, 2014 acquisition of Gulfstream Business Bank that are not PCI loans. These are performing loans recorded at estimated fair value at the acquisition date. The fair value adjustment at the acquisition date was approximately $7,680, or approximately 2.3% of the outstanding aggregate loan balances. This amount is accreted into interest income over the remaining lives of the related loans on a level yield basis. Because these loans were recorded at estimated fair value on January 17, 2014, no provision for loan loss was recorded related to these loans at March 31, 2014. |

| note 2: | Included in the $250,800 PCI loans at March 31, 2014 are $219,733 of loans that are covered by FDIC loss sharing arrangements. Of the remaining PCI loan amount, $29,966 were acquired in the Company’s January 17, 2014 acquisition of Gulfstream Business Bank and $1,101 are consumer loans acquired pursuant to FDIC assisted transactions of failed financial institutions that are not covered by FDIC loss sharing agreements. |

The general loan loss allowance (non-impaired loans) decreased by a net amount of $889. This decrease was primarily due to the continued improvement in the local economy and real estate market, and the continued decline in the Company’s two year charge-off history. The Company’s other credit metrics, such as the levels of and trends in the Company’s non-performing loans, past-due loans and impaired loans were also considered when adjusting its qualitative factors, which ultimately increased the current two year historical loss factor ratios.

The specific loan loss allowance (impaired loans) is the aggregate of the results of individual analyses prepared for each one of the impaired loans, excluding PCI loans. The Company recorded partial charge offs in lieu of specific allowance for a number of the impaired loans. The Company’s impaired loans have been written down by $1,454 to $26,555 ($24,636 when the $1,919 specific allowance is considered) from their legal unpaid principal balance outstanding of $28,009. In the aggregate, total impaired loans have been written down to approximately 88% of their legal unpaid principal balance, and non-performing impaired loans have been written down to approximately 78% of

9

their legal unpaid principal balance. The Company’s total non-performing loans (non-accrual loans plus loans past due greater than 90 days and still accruing, $30,689 at March 31, 2014) have been written down to approximately 82% of their legal unpaid principal balance.

Approximately $14,740 of the Company’s impaired loans (56%) are accruing performing loans. This group of impaired loans is not included in the Company’s non-performing loans or non-performing assets categories.

PCI loans, including those covered by FDIC loss sharing agreements, are accounted for pursuant to ASC Topic 310-30. PCI loan pools are evaluated for impairment each quarter. If a pool is impaired, an allowance for loan loss is recorded.

Management believes the Company’s allowance for loan losses is adequate at March 31, 2014. However, management recognizes that many factors can adversely impact various segments of the Company’s market and customers, and therefore there is no assurance as to the amount of losses or probable losses which may develop in the future. The table below summarizes the changes in allowance for loan losses during the previous five quarters.

Allowance for loan losses (unaudited)

| as of or for the quarter ending |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Loans, excluding PCI loans |

||||||||||||||||||||

| Allowance at beginning of period |

$ | 19,694 | $ | 19,265 | $ | 21,800 | $ | 22,631 | $ | 24,033 | ||||||||||

| Charge-offs |

(1,160 | ) | (774 | ) | (1,570 | ) | (2,603 | ) | (1,231 | ) | ||||||||||

| Recoveries |

843 | 457 | 344 | 310 | 163 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net charge-offs |

(317 | ) | (317 | ) | (1,226 | ) | (2,293 | ) | (1,068 | ) | ||||||||||

| (Recovery) provision for loan losses |

(464 | ) | 746 | (1,309 | ) | 1,462 | (334 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowance at end of period for loans other than PCI loans |

$ | 18,913 | $ | 19,694 | $ | 19,265 | $ | 21,800 | $ | 22,631 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| PCI loans |

||||||||||||||||||||

| Allowance at beginning of period |

$ | 760 | $ | 2,056 | $ | 2,020 | $ | 2,623 | $ | 2,649 | ||||||||||

| Charge-offs |

— | (733 | ) | — | (515 | ) | — | |||||||||||||

| Recoveries |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net charge-offs |

— | (733 | ) | — | (515 | ) | — | |||||||||||||

| Provision (recovery) for loan losses |

423 | (563 | ) | 36 | (88 | ) | (26 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Allowance at end of period for PCI loans |

$ | 1,183 | $ | 760 | $ | 2,056 | $ | 2,020 | $ | 2,623 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total allowance at end of period |

$ | 20,096 | $ | 20,454 | $ | 21,321 | $ | 23,820 | $ | 25,254 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

The Company defines non-performing loans (“NPLs”) as non-accrual loans plus loans past due 90 days or more and still accruing interest. NPLs do not include PCI loans whether covered by FDIC loss share agreements or not. PCI loans are accounted for pursuant to ASC Topic 310-30. NPLs as a percentage of total Non-PCI loans were 1.96% at March 31, 2014 compared to 2.18% at December 31, 2013. The current quarter end ratios were impacted by the Gulfstream acquisition and would be different without Gulfstream.

Non-performing assets (“NPAs”) (which the Company defines as NPLs, as defined above, plus (a) OREO (i.e. real estate acquired through foreclosure, in-substance foreclosure, or deed in lieu of foreclosure), excluding OREO covered by FDIC loss share agreement; and (b) other repossessed assets that are not real estate, and are not covered by FDIC loss share agreement), were $40,719 at March 31,

10

2014, compared to $33,636 at December 31, 2013. NPAs as a percentage of total assets was 1.35% at March 31, 2014 compared to 1.39% at December 31, 2013. NPAs as a percentage of loans plus OREO and other repossessed assets, excluding PCI loans and OREO covered by FDIC loss share agreements, was 2.59% at March 31, 2014 compared to 2.69% at December 31, 2013.

The table below summarizes selected credit quality data for the periods indicated. The current quarter end ratios were impacted by the Gulfstream acquisition and would be different without Gulfstream.

Selected credit quality ratios (unaudited)

| As of or for the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Non-accrual loans (note 1) |

$ | 30,689 | $ | 27,077 | $ | 21,104 | $ | 24,219 | $ | 24,456 | ||||||||||

| Past due loans 90 days or more and still accruing interest (note 1) |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-performing loans (“NPLs”) (note 1) |

30,689 | 27,077 | 21,104 | 24,219 | 24,456 | |||||||||||||||

| Other real estate owned (OREO) (note 1) |

9,895 | 6,409 | 4,804 | 5,469 | 6,186 | |||||||||||||||

| Repossessed assets other than real estate (note 1) |

135 | 150 | 141 | 223 | 380 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-performing assets (“NPAs”) (note 1) |

$ | 40,719 | $ | 33,636 | $ | 26,049 | $ | 29,911 | $ | 31,022 | ||||||||||

| Non-performing loans as percentage of total loans excluding PCI loans |

1.96 | % | 2.18 | % | 1.74 | % | 2.06 | % | 2.15 | % | ||||||||||

| Non-performing assets as percentage of total assets |

1.35 | % | 1.39 | % | 1.12 | % | 1.27 | % | 1.30 | % | ||||||||||

| Non-performing assets as percentage of loans and OREO plus other repossessed assets (note 1) |

2.59 | % | 2.69 | % | 2.13 | % | 2.53 | % | 2.72 | % | ||||||||||

| Net charge-offs (note 1) |

$ | 317 | $ | 317 | $ | 1,226 | $ | 2,293 | $ | 1,068 | ||||||||||

| Net charge-offs as a percentage of average loans for the period (note 1) |

0.02 | % | 0.03 | % | 0.10 | % | 0.20 | % | 0.09 | % | ||||||||||

| Net charge-offs as a percentage of average loans for the period on an annualized basis (note 1) |

0.08 | % | 0.12 | % | 0.40 | % | 0.80 | % | 0.36 | % | ||||||||||

| Loans past due 30 thru 89 days and accruing interest as a percentage of total loans (note 1) |

0.77 | % | 0.85 | % | 0.75 | % | 0.99 | % | 1.06 | % | ||||||||||

| Allowance for loan losses as percentage of NPLs (note 1) |

62 | % | 73 | % | 91 | % | 90 | % | 93 | % | ||||||||||

| Troubled debt restructure (“TDRs”) (note 2) |

$ | 14,986 | $ | 15,447 | $ | 15,811 | $ | 13,103 | $ | 14,073 | ||||||||||

| Impaired loans that were not TDRs |

11,569 | 8,663 | 24,069 | 25,590 | 26,031 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total impaired loans |

26,555 | 24,110 | 39,880 | 38,693 | 40,104 | |||||||||||||||

| Acquired Gulfstream loans |

319,665 | — | — | — | — | |||||||||||||||

| All other non-impaired loans |

1,218,614 | 1,218,648 | 1,174,542 | 1,137,215 | 1,094,093 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Non-PCI loans |

1,564,834 | 1,242,758 | 1,214,422 | 1,175,908 | 1,134,197 | |||||||||||||||

| Total PCI loans |

250,800 | 231,421 | 244,150 | 259,679 | 280,789 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans |

$ | 1,815,634 | $ | 1,474,179 | $ | 1,458,572 | $ | 1,435,587 | $ | 1,414,986 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| ALLL for Non-PCI loans |

||||||||||||||||||||

| Specific loan loss allowance- impaired loans |

$ | 1,919 | $ | 1,811 | $ | 784 | $ | 600 | $ | 990 | ||||||||||

| General loan loss allowance- Gulfstream loans |

— | n/a | n/a | n/a | n/a | |||||||||||||||

| General loan loss allowance- non impaired |

16,994 | 17,883 | 18,481 | 21,200 | 21,641 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total allowance for loan losses |

$ | 18,913 | $ | 19,694 | $ | 19,265 | $ | 21,800 | $ | 22,631 | ||||||||||

| ALLL as a percentage of period end loans: |

||||||||||||||||||||

| Impaired loans (note 1) |

7.23 | % | 7.51 | % | 1.97 | % | 1.55 | % | 2.47 | % | ||||||||||

| Acquired Gulfstream loans |

— | % | n/a | n/a | n/a | n/a | ||||||||||||||

| All other non impaired loans (note 1) |

1.39 | % | 1.47 | % | 1.57 | % | 1.86 | % | 1.97 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total loans (note 1) |

1.21 | % | 1.58 | % | 1.58 | % | 1.85 | % | 1.99 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Note 1: Excludes PCI loans and OREO covered by FDIC loss share agreements.

11

| Note 2: | The Company has approximately $14,986 of TDRs. Of this amount $12,649 are performing pursuant to their modified terms, and $2,337 are not performing and have been placed on non-accrual status and included in non performing loans (“NPLs”). Current accounting standards require TDRs to be included in our impaired loans, whether they are performing or not performing. Only non performing TDRs are included in our NPLs. |

Deposit activity

On January 17, 2014, the Company assumed $478,999 of deposits in the acquisition of Gulfstream, which included approximately $84,995 of time deposits. During the quarter, the Company’s total deposits increased by $502,473 (time deposits increased by $59,179 and non-time deposits increased by $443,294). The cost of interest bearing deposits in the current quarter decreased by 1bp to 37bps compared to the prior quarter. The overall cost of total deposits (i.e. includes non-interest bearing checking accounts) decreased by 2bps to 0.22% in the current quarter compared to 0.24% in the prior quarter. The table below summarizes the Company’s deposit mix over the periods indicated.

Deposit mix (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Checking accounts |

||||||||||||||||||||

| Non-interest bearing |

$ | 838,764 | $ | 644,915 | $ | 562,027 | $ | 555,721 | $ | 565,404 | ||||||||||

| Interest bearing |

558,845 | 483,842 | 452,583 | 456,660 | 459,528 | |||||||||||||||

| Savings deposits |

234,908 | 232,942 | 240,431 | 241,609 | 239,127 | |||||||||||||||

| Money market accounts |

482,133 | 309,657 | 306,706 | 312,891 | 316,785 | |||||||||||||||

| Time deposits |

444,054 | 384,875 | 400,208 | 409,811 | 432,752 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

$ | 2,558,704 | $ | 2,056,231 | $ | 1,961,955 | $ | 1,976,692 | $ | 2,013,596 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Non time deposits as percentage of total deposits |

83 | % | 81 | % | 80 | % | 79 | % | 79 | % | ||||||||||

| Time deposits as percentage of total deposits |

17 | % | 19 | % | 20 | % | 21 | % | 21 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total deposits |

100 | % | 100 | % | 100 | % | 100 | % | 100 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

12

Presented below are condensed consolidated balance sheets and average balance sheets for the periods indicated.

Condensed Consolidated Balance Sheets (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Cash and due from banks |

$ | 29,862 | $ | 21,581 | $ | 21,216 | $ | 21,160 | $ | 20,823 | ||||||||||

| Fed funds sold and Fed Res Bank deposits |

190,399 | 153,308 | 85,600 | 82,395 | 155,872 | |||||||||||||||

| Trading securities |

— | — | 398 | — | — | |||||||||||||||

| Investments securities, available for sale |

617,143 | 457,086 | 456,555 | 492,087 | 460,534 | |||||||||||||||

| Loans held for sale |

1,017 | 1,010 | 1,317 | 1,760 | 2,131 | |||||||||||||||

| PCI loans |

250,800 | 231,421 | 244,150 | 259,679 | 280,789 | |||||||||||||||

| Loans |

1,564,834 | 1,242,758 | 1,214,422 | 1,175,908 | 1,134,197 | |||||||||||||||

| Allowance for loan losses |

(20,096 | ) | (20,454 | ) | (21,321 | ) | (23,820 | ) | (25,254 | ) | ||||||||||

| FDIC indemnification assets |

64,719 | 73,433 | 81,603 | 88,716 | 97,958 | |||||||||||||||

| Premises and equipment, net |

95,103 | 96,619 | 97,289 | 96,506 | 96,946 | |||||||||||||||

| Goodwill |

76,440 | 44,924 | 44,924 | 44,924 | 44,924 | |||||||||||||||

| Core deposit intangible |

8,800 | 4,958 | 5,196 | 5,441 | 5,691 | |||||||||||||||

| Bank owned life insurance |

54,574 | 49,285 | 48,961 | 48,634 | 48,296 | |||||||||||||||

| OREO covered by FDIC loss share agreements |

13,892 | 19,111 | 21,633 | 28,532 | 29,434 | |||||||||||||||

| OREO not covered by FDIC loss share agreements |

9,895 | 6,409 | 4,804 | 5,469 | 6,186 | |||||||||||||||

| Other assets |

48,315 | 34,118 | 29,274 | 27,962 | 30,712 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TOTAL ASSETS |

$ | 3,005,697 | $ | 2,415,567 | $ | 2,336,021 | $ | 2,355,353 | $ | 2,389,239 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Deposits |

$ | 2,558,704 | $ | 2,056,231 | $ | 1,961,955 | $ | 1,976,692 | $ | 2,013,596 | ||||||||||

| Federal funds purchased |

45,183 | 29,909 | 45,356 | 53,274 | 45,130 | |||||||||||||||

| Other borrowings |

49,901 | 37,453 | 39,140 | 38,873 | 37,398 | |||||||||||||||

| Other liabilities |

18,745 | 18,595 | 16,829 | 15,098 | 16,890 | |||||||||||||||

| Common stockholders’ equity |

333,164 | 273,379 | 272,741 | 271,416 | 276,225 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

$ | 3,005,697 | $ | 2,415,567 | $ | 2,336,021 | $ | 2,355,353 | $ | 2,389,239 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Condensed Consolidated Average Balance Sheets (unaudited) | ||||||||||||||||||||

| For quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Federal funds sold and other |

$ | 197,915 | $ | 161,270 | $ | 80,346 | $ | 179,982 | $ | 137,776 | ||||||||||

| Security investments |

532,046 | 453,658 | 471,114 | 437,815 | 460,228 | |||||||||||||||

| PCI loans |

251,587 | 240,804 | 251,626 | 267,312 | 287,181 | |||||||||||||||

| Loans |

1,513,060 | 1,229,868 | 1,192,633 | 1,153,194 | 1,133,046 | |||||||||||||||

| Allowance for loan losses |

(20,970 | ) | (21,438 | ) | (23,819 | ) | (23,962 | ) | (26,782 | ) | ||||||||||

| All other assets |

396,123 | 341,437 | 377,072 | 367,969 | 398,334 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TOTAL ASSETS |

$ | 2,869,761 | $ | 2,405,599 | $ | 2,348,972 | $ | 2,382,310 | $ | 2,389,783 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Deposits- interest bearing |

$ | 1,653,806 | $ | 1,405,244 | $ | 1,402,753 | $ | 1,433,806 | $ | 1,462,511 | ||||||||||

| Deposits- non interest bearing |

767,926 | 635,383 | 581,827 | 574,345 | 545,579 | |||||||||||||||

| Federal funds purchased |

41,999 | 34,782 | 36,823 | 35,619 | 44,662 | |||||||||||||||

| Other borrowings |

52,341 | 36,723 | 39,834 | 40,812 | 37,356 | |||||||||||||||

| Other liabilities |

30,389 | 18,516 | 17,315 | 22,135 | 25,200 | |||||||||||||||

| Stockholders’ equity |

323,300 | 274,951 | 270,420 | 275,593 | 274,475 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

$ | 2,869,761 | $ | 2,405,599 | $ | 2,348,972 | $ | 2,382,310 | $ | 2,389,783 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

13

Non interest income and non interest expense

The table below summarizes the Company’s non-interest income for the periods indicated.

Quarterly Condensed Consolidated Non Interest Income (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Income from correspondent banking and bond sales division |

$ | 3,136 | $ | 3,070 | $ | 2,909 | $ | 4,904 | $ | 6,140 | ||||||||||

| Other correspondent banking related revenue |

795 | 955 | 862 | 705 | 865 | |||||||||||||||

| Wealth management related revenue |

1,217 | 1,172 | 1,179 | 1,130 | 1,070 | |||||||||||||||

| Service charges on deposit accounts |

2,262 | 2,313 | 2,244 | 2,081 | 1,819 | |||||||||||||||

| Debit, prepaid, ATM and merchant card related fees |

1,506 | 1,394 | 1,399 | 1,342 | 1,285 | |||||||||||||||

| BOLI income |

352 | 324 | 327 | 338 | 339 | |||||||||||||||

| Other service charges and fees |

409 | 262 | 190 | 231 | 302 | |||||||||||||||

| Gain on sale of securities available for sale |

— | 22 | — | 1,008 | 30 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Subtotal |

$ | 9,677 | $ | 9,512 | $ | 9,110 | $ | 11,739 | $ | 11,850 | ||||||||||

| FDIC indemnification asset – amortization (see explanation below) |

(5,185 | ) | (4,500 | ) | (3,836 | ) | (3,272 | ) | (2,199 | ) | ||||||||||

| FDIC indemnification income |

1,268 | 185 | 3,333 | 1,396 | 628 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non-interest income |

$ | 5,760 | $ | 5,197 | $ | 8,607 | $ | 9,863 | $ | 10,279 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

The FDIC indemnification asset (“IA”) is producing amortization (versus accretion) due to reductions in the estimated losses in the FDIC covered PCI loan portfolio. To the extent current projected losses in the covered PCI loan portfolio are less than originally projected losses, the related projected reimbursements from the FDIC contemplated in the IA are less, which produces a negative income accretion in non-interest income. This event corresponds to the increase in yields in the FDIC covered PCI loan portfolio, although there is not perfect correlation. Higher expected cash flows (i.e. less expected future losses) on the loan side of the equation is accreted into interest income over the life of the related loan pool. The lower expected reimbursement from the FDIC (i.e. 80% of the lower expected future losses) is amortized over the lesser of the remaining life of the related loan pool(s) or the remaining term of the loss share period.

When a FDIC covered OREO property is sold at a loss, the loss is included in non-interest expense as loss on sale of OREO, and approximately eighty percent of the loss is recorded as FDIC indemnification income and included in non-interest income. In addition, 80% of any related loan pool impairments also are reflected in this non-interest income account.

14

The table below summarizes the Company’s non-interest expense for the periods indicated.

Quarterly Condensed Consolidated Non Interest Expense (unaudited)

| For the quarter ended: |

3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | |||||||||||||||

| Employee salaries and wages |

$ | 11,873 | $ | 11,200 | $ | 11,168 | $ | 12,142 | $ | 12,665 | ||||||||||

| Employee incentive/bonus compensation accrued |

1,238 | 1,375 | 1,325 | 1,171 | 1,094 | |||||||||||||||

| Employee stock based compensation expense |

187 | 173 | 147 | 143 | 146 | |||||||||||||||

| Deferred compensation expense |

107 | 147 | 147 | 134 | 141 | |||||||||||||||

| Health insurance and other employee benefits |

987 | 968 | 842 | 796 | 951 | |||||||||||||||

| Payroll taxes |

1,120 | 613 | 655 | 733 | 1,017 | |||||||||||||||

| 401K employer contributions |

360 | 268 | 276 | 308 | 367 | |||||||||||||||

| Other employee related expenses |

258 | 381 | 272 | 344 | 296 | |||||||||||||||

| Incremental direct cost of loan origination |

(449 | ) | (575 | ) | (487 | ) | (537 | ) | (437 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total salaries, wages and employee benefits |

15,681 | 14,550 | 14,345 | 15,234 | 16,240 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (Gain) loss on sale of OREO |

(30 | ) | (93 | ) | 68 | 177 | 76 | |||||||||||||

| Loss (gain) on sale of FDIC covered OREO |

107 | 801 | 1,784 | 386 | (77 | ) | ||||||||||||||

| Valuation write down of OREO |

70 | 110 | 338 | 295 | 342 | |||||||||||||||

| Valuation write down of FDIC covered OREO |

950 | 51 | 2,846 | 1,385 | 645 | |||||||||||||||

| (Gain) loss on repossessed assets other than real estate |

(2 | ) | 16 | 39 | 104 | 242 | ||||||||||||||

| Loan put back expense |

— | — | — | — | 4 | |||||||||||||||

| Foreclosure and repossession related expenses |

485 | 477 | 376 | 438 | 441 | |||||||||||||||

| Foreclosure and repo expense, FDIC (note 1) |

244 | 458 | 304 | 349 | 348 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total credit related expenses |

1,824 | 1,820 | 5,755 | 3,134 | 2,021 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Occupancy expense |

1,960 | 1,944 | 1,924 | 1,942 | 1,892 | |||||||||||||||

| Depreciation of premises and equipment |

1,478 | 1,560 | 1,364 | 1,455 | 1,497 | |||||||||||||||

| Supplies, stationary and printing |

227 | 280 | 268 | 285 | 288 | |||||||||||||||

| Marketing expenses |

620 | 681 | 722 | 586 | 528 | |||||||||||||||

| Data processing expenses |

1,039 | 962 | 1,026 | 912 | 884 | |||||||||||||||

| Legal, auditing and other professional fees |

775 | 951 | 1,176 | 844 | 783 | |||||||||||||||

| Bank regulatory related expenses |

631 | 565 | 588 | 635 | 581 | |||||||||||||||

| Postage and delivery |

268 | 266 | 266 | 267 | 285 | |||||||||||||||

| ATM and debit card related expenses |

474 | 414 | 435 | 428 | 511 | |||||||||||||||

| Amortization of CDI |

331 | 237 | 246 | 250 | 253 | |||||||||||||||

| Internet and telephone banking |

378 | 334 | 286 | 239 | 224 | |||||||||||||||

| Put back option amortization expense |

— | — | — | — | 37 | |||||||||||||||

| Correspondent account and Federal Reserve charges |

135 | 116 | 114 | 120 | 109 | |||||||||||||||

| Conferences, seminars, education and training |

100 | 155 | 138 | 138 | 153 | |||||||||||||||

| Director fees |

115 | 102 | 99 | 102 | 102 | |||||||||||||||

| Travel expenses |

65 | 102 | 119 | 104 | 74 | |||||||||||||||

| Other expenses |

797 | 871 | 796 | 698 | 628 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Subtotal |

26,898 | 25,910 | 29,667 | 27,373 | 27,090 | |||||||||||||||

| Merger and acquisition related expenses |

2,347 | 539 | 183 | — | — | |||||||||||||||

| Branch closure and efficiency initiatives |

3,158 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total non- interest expense |

$ | 32,403 | $ | 26,449 | $ | 29,850 | $ | 27,373 | $ | 27,090 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| note 1: | These are foreclosure and repossession related expenses related to FDIC covered assets, and are shown net of FDIC reimbursable amounts pursuant to FDIC loss share agreements. |

15

Explanation of Certain Unaudited Non-GAAP Financial Measures

This press release contains financial information determined by methods other than Generally Accepted Accounting Principles (“GAAP”). The financial highlights provide reconciliations between GAAP interest income, net interest income and tax equivalent basis interest income and net interest income, as well as total stockholders’ equity and tangible common equity. It also reconciles net income and net operating income. Management uses these non-GAAP financial measures in its analysis of the Company’s performance and believes these presentations provide useful supplemental information, and a clearer understanding of the Company’s performance. The Company believes the non-GAAP measures enhance investors’ understanding of the Company’s business and performance. These measures are also useful in understanding performance trends and facilitate comparisons with the performance of other financial institutions. The limitations associated with operating measures are the risk that persons might disagree as to the appropriateness of items comprising these measures and that different companies might calculate these measures differently. The Company provides reconciliations between GAAP and these non-GAAP measures. These disclosures should not be considered an alternative to GAAP.

Reconciliation of GAAP to non-GAAP Measures. All amounts are in thousands except per share data (unaudited):

| 1Q14 | 4Q13 | 1Q13 | ||||||||||

| Interest income, as reported (GAAP) |

$ | 29,782 | $ | 25,479 | $ | 24,378 | ||||||

| tax equivalent adjustments |

404 | 368 | 287 | |||||||||

|

|

|

|

|

|

|

|||||||

| Interest income (tax equivalent) |

$ | 30,186 | $ | 25,847 | $ | 24,665 | ||||||

|

|

|

|

|

|

|

|||||||

| Net interest income, as reported (GAAP) |

$ | 28,193 | $ | 24,081 | $ | 22,822 | ||||||

| tax equivalent adjustments |

404 | 368 | 287 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net interest income (tax equivalent) |

$ | 28,597 | $ | 24,449 | $ | 23,109 | ||||||

|

|

|

|

|

|

|

|||||||

| 3/31/14 | 12/31/13 | 9/30/13 | 6/30/13 | 3/31/13 | ||||||||||||||||

| Total stockholders’ equity (GAAP) |

$ | 333,164 | $ | 273,379 | $ | 272,741 | $ | 271,416 | $ | 276,225 | ||||||||||

| Goodwill |

(76,440 | ) | (44,924 | ) | (44,924 | ) | (44,924 | ) | (44,924 | ) | ||||||||||

| Core deposit intangible |

(8,800 | ) | (4,958 | ) | (5,196 | ) | (5,441 | ) | (5,691 | ) | ||||||||||

| Trust intangible |

(1,113 | ) | (1,158 | ) | (1,209 | ) | (1,259 | ) | (1,309 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Tangible common equity |

$ | 246,811 | $ | 222,339 | $ | 221,412 | $ | 219,792 | $ | 224,301 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| 1Q14 | 4Q13 | 3Q13 | 2Q13 | 1Q13 | ||||||||||||||||

| Net income (GAAP) |

$ | 1,053 | $ | 1,800 | $ | 3,109 | $ | 2,758 | $ | 4,576 | ||||||||||

| exclude gain on sale of AFS securities |

— | (22 | ) | — | (1,008 | ) | (30 | ) | ||||||||||||

| add back merger and acquisition related expenses |

2,347 | 539 | 183 | — | — | |||||||||||||||

| add back branch closure and efficiency initiatives |

3,158 | — | — | — | — | |||||||||||||||

| tax effected using the effective tax rate for the period presented |

(1,862 | ) | (165 | ) | (60 | ) | 329 | 8 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net operating income |

$ | 4,696 | $ | 2,152 | $ | 3,232 | $ | 2,079 | $ | 4,554 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Average diluted shares outstanding during the period presented |

34,863 | 30,245 | 30,244 | 30,161 | 30,159 | |||||||||||||||

| Net operating income per share |

$ | 0.13 | $ | 0.07 | $ | 0.11 | $ | 0.07 | $ | 0.15 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

16

About CenterState Banks, Inc.

The Company, headquartered in Davenport, Florida, between Orlando and Tampa, is a bank holding company that was formed in June 2000 as part of a merger of three independent commercial banks. Currently, the Company operates through one subsidiary bank with 51 full service branch banking locations in 19 counties throughout central Florida. Through its subsidiary bank the Company provides a range of consumer and commercial banking services to individuals, businesses and industries.

In addition to providing traditional deposit and lending products and services to its commercial and retail customers in central Florida, the Company also operates a correspondent banking and bond sales division. The division is integrated with and part of the Company’s subsidiary bank located in Winter Haven, Florida, although the majority of the bond salesmen, traders and operations personnel are physically housed in leased facilities located in Birmingham, Alabama, Atlanta, Georgia and Winston-Salem, North Carolina. The customer base includes small to medium size financial institutions primarily located in southeastern United States.

For additional information contact Ernest S. Pinner, CEO, John C. Corbett, EVP, or James J. Antal, CFO, at 863-419-7750.

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995:

Some of the statements in this report constitute forward-looking statements, within the meaning of the Securities Act of 1933 and the Securities Exchange Act of 1934. These statements related to future events, other future financial and operating performance, costs, revenues, economic conditions in our markets, loan performance, credit risks, collateral values and credit conditions, or business strategies, including expansion and acquisition activities and may be identified by terminology such as “may,” “will,” “should,” “expects,” “scheduled,” “plans,” “intends,” “anticipates,” “believes,” “estimates,” “potential,” or “continue” or the negative of such terms or other comparable terminology. Actual events or results may differ materially. In evaluating these statements, you should specifically consider the factors described throughout this report. We cannot assure you that future results, levels of activity, performance or goals will be achieved, and actual results may differ from those set forth in the forward looking statements.

Forward-looking statements, with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance or achievements of the Company or the Bank to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. You should not expect us to update any forward-looking statements. All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation, those risks and uncertainties described in our annual report on Form 10-K for the year ended December 31, 2013, and otherwise in our SEC reports and filings.

17