Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SOUTHERN Co GAS | form_8-k.htm |

| EX-99.1 - EXHIBIT 99.1 - SOUTHERN Co GAS | exhibit_99-1.htm |

Second Quarter 2013 Earnings Presentation July 31, 2013

* $ in millions * Cautionary Statements & Supplemental Information Forward-Looking Statements Certain expectations and projections regarding our future performance referenced in this presentation, in other reports or statements we file with the SEC or otherwise release to the public, and on our website, are forward-looking statements. Senior officers and other employees may also make verbal statements to analysts, investors, regulators, the media and others that are forward-looking. Forward-looking statements involve matters that are not historical facts, such as statements regarding our future operations, prospects, strategies, financial condition, economic performance (including growth and earnings), industry conditions and demand for our products and services. Because these statements involve anticipated events or conditions, forward-looking statements often include words such as "anticipate," "assume," "believe," "can," "could," "estimate," "expect," "forecast," "future," "goal," "indicate," "intend," "may," "outlook," "plan," "potential," "predict," "project," "seek," "should," "target," "would," or similar expressions. Forward-looking statements contained in this presentation include, without limitation, statements regarding the Nicor Gas depreciation study and related legislation, the approval of our infrastructure programs, the rewatering schedule of our storage cavern at Golden Triangle, the expected financial impact from our acquisition of certain customer relationships in our retail operations segment, our capital expenditures, our priorities for 2013 and our 2013 earnings outlook and related expectations and assumptions. Our expectations are not guarantees and are based on currently available competitive, financial and economic data along with our operating plans. While we believe our expectations are reasonable in view of the currently available information, our expectations are subject to future events, risks and uncertainties, and there are several factors - many beyond our control - that could cause results to differ significantly from our expectations. Such events, risks and uncertainties include, but are not limited to, changes in price, supply and demand for natural gas and related products; the impact of changes in state and federal legislation and regulation, including changes related to climate change; actions taken by government agencies on rates and other matters, including regulatory approval of new partnerships and infrastructure programs; concentration of credit risk; utility and energy industry consolidation; the impact on cost and timeliness of construction projects by government and other approvals; development project delays; adequacy of supply of diversified vendors; unexpected change in project costs, including the cost of funds to finance these projects; the impact of acquisitions and divestitures, including the Nicor merger; limits on natural gas pipeline capacity; direct or indirect effects on our business, financial condition or liquidity resulting from a change in our credit ratings or the credit ratings of our counterparties or competitors; interest rate fluctuations; financial market conditions, including disruptions in the capital markets and lending environment and the current economic uncertainty; general economic conditions; uncertainties about environmental issues and the related impact of such issues; the impact of changes in weather, including climate change, on the temperature-sensitive portions of our business; the impact of natural disasters such as hurricanes on the supply and price of natural gas; the outcome of litigation; acts of war or terrorism; and other factors which are provided in detail in our filings with the Securities and Exchange Commission. Forward-looking statements are only as of the date they are made, and we do not undertake to update these statements to reflect subsequent changes. Supplemental Information Company management evaluates segment financial performance based on operating margin and earnings before interest and taxes (EBIT), which includes the effects of corporate expense allocations. EBIT is a non-GAAP (accounting principles generally accepted in the United States of America) financial measure that includes operating income, other income and expenses. Items that are not included in EBIT are financing costs, including debt and interest expense and income taxes. The company evaluates each of these items on a consolidated level and believes EBIT is a useful measurement of our performance because it provides information that can be used to evaluate the effectiveness of our businesses from an operational perspective, exclusive of the costs to finance those activities and exclusive of income taxes, neither of which is directly relevant to the efficiency of those operations. Operating margin is a non-GAAP measure calculated as operating revenues minus cost of goods sold and revenue taxes, excluding operation and maintenance expense, depreciation and amortization, and taxes other than income taxes. These items are included in the company's calculation of operating income. The company believes operating margin is a better indicator than operating revenues of the contribution resulting from customer growth, since cost of goods sold and revenue taxes are generally passed directly through to customers. In addition, in this presentation, the company presents a non-GAAP measure of its earnings per share (EPS), which is adjusted to exclude expenses incurred with respect to the Nicor Inc. (Nicor) merger and its wholesale services segment. As the company does not routinely engage in transactions of the magnitude of the Nicor merger, and consequently does not regularly incur transaction related expenses with correlative size, the company believes presenting EPS excluding Nicor merger expenses provides investors with an additional measure of the company’s core operating performance. In addition, the company believes that presenting EPS excluding the wholesale services segment provides investors with additional measure of core operating performance by excluding the volatility effects resulting from mark-to-market accounting in the wholesale services segment. EBIT, operating margin and adjusted EPS should not be considered as alternatives to, or more meaningful indicators of, the company's operating performance than operating income or EPS as determined in accordance with GAAP. In addition, the company's EBIT, operating margin and adjusted EPS may not be comparable to similarly titled measures of another company. Reconciliations of non-GAAP financial measures referenced in this presentation are available on the company’s Web site at www.aglresources.com.

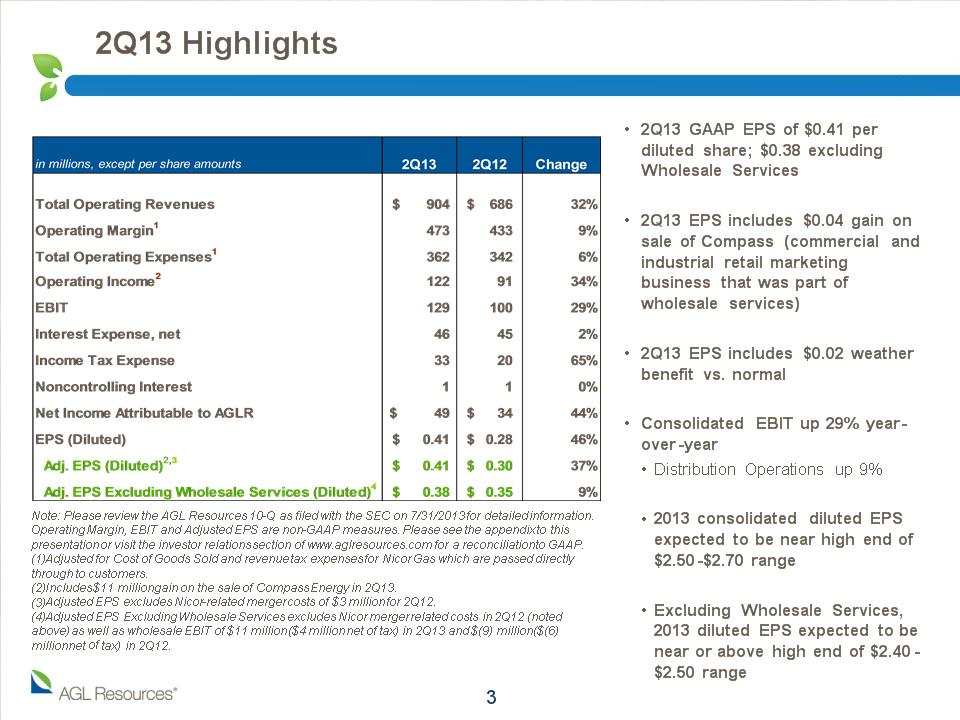

2Q13 GAAP EPS of $0.41 per diluted share; $0.38 excluding Wholesale Services 2Q13 EPS includes $0.04 gain on sale of Compass (commercial and industrial retail marketing business that was part of wholesale services) 2Q13 EPS includes $0.02 weather benefit vs. normal Consolidated EBIT up 29% year-over-year Distribution Operations up 9% 2013 consolidated diluted EPS expected to be near high end of $2.50-$2.70 range Excluding Wholesale Services, 2013 diluted EPS expected to be near or above high end of $2.40-$2.50 range 2Q13 Highlights * millions Note: Please review the AGL Resources 10-Q as filed with the SEC on 7/31/2013 for detailed information. Operating Margin, EBIT and Adjusted EPS are non-GAAP measures. Please see the appendix to this presentation or visit the investor relations section of www.aglresources.com for a reconciliation to GAAP. Adjusted for Cost of Goods Sold and revenue tax expenses for Nicor Gas which are passed directly through to customers. Includes $11 million gain on the sale of Compass Energy in 2Q13. Adjusted EPS excludes Nicor-related merger costs of $3 million for 2Q12. Adjusted EPS Excluding Wholesale Services excludes Nicor merger related costs in 2Q12 (noted above) as well as wholesale EBIT of $11 million ($4 million net of tax) in 2Q13 and $(9) million ($(6) million net of tax) in 2Q12.

6-mos 2013 GAAP EPS of $1.72 per diluted share; $1.61 excluding Wholesale Services 6-mos 2013 EPS includes: Contribution from colder-than-normal weather of $0.05 ($0.18 vs. 6-mos 2012) across distribution and retail businesses $0.04 gain on sale of Compass Energy Consolidated EBIT up 18% year-over-year Distribution contributed 75% of consolidated operating EBIT through June with Retail contributing 19% Meaningful legislative and regulatory developments in Illinois and Georgia 6-Months 2013 Highlights * millions Note: Please review the AGL Resources 10-Q as filed with the SEC on 7/31/2013 for detailed information. Operating Margin, EBIT and Adjusted EPS are non-GAAP measures. Please see the appendix to this presentation or visit the investor relations section of www.aglresources.com for a reconciliation to GAAP. Adjusted for Cost of Goods Sold and revenue tax expenses for Nicor Gas which are passed directly through to customers. Includes $11 million gain on the sale of Compass Energy in 2Q13. Adjusted EPS excludes Nicor-related merger costs of $13 million for 1H12. Adjusted EPS Excluding Wholesale Services excludes Nicor merger related costs in 1H12 (noted above) as well as wholesale EBIT of $26 million ($13 million net of tax) in 1H13 and $10 million ($6 million net of tax) in 1H12.

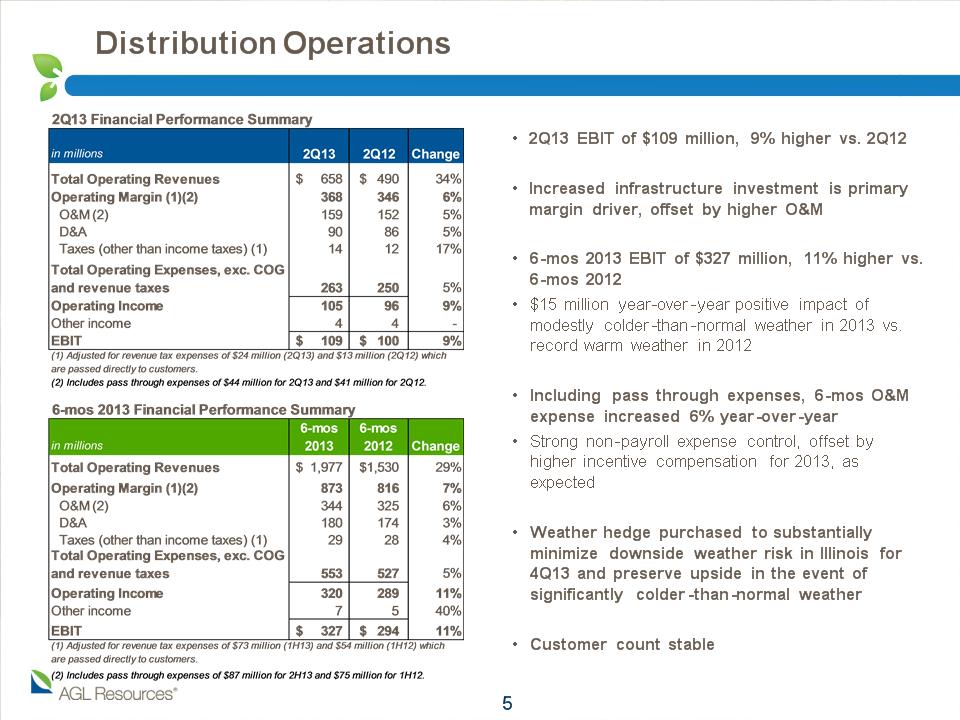

2Q13 EBIT of $109 million, 9% higher vs. 2Q12 Increased infrastructure investment is primary margin driver, offset by higher O&M 6-mos 2013 EBIT of $327 million, 11% higher vs. 6-mos 2012 $15 million year-over-year positive impact of modestly colder-than-normal weather in 2013 vs. record warm weather in 2012 Including pass through expenses, 6-mos O&M expense increased 6% year-over-year Strong non-payroll expense control, offset by higher incentive compensation for 2013, as expected Weather hedge purchased to substantially minimize downside weather risk in Illinois for 4Q13 and preserve upside in the event of significantly colder-than-normal weather Customer count stable Distribution Operations *

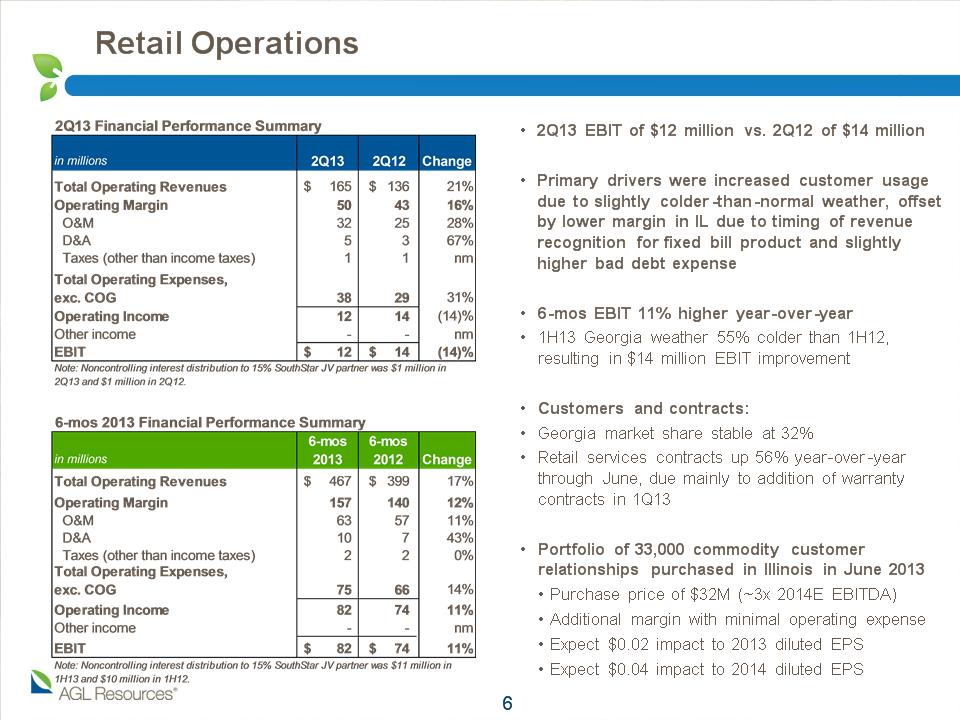

2Q13 EBIT of $12 million vs. 2Q12 of $14 million Primary drivers were increased customer usage due to slightly colder-than-normal weather, offset by lower margin in IL due to timing of revenue recognition for fixed bill product and slightly higher bad debt expense 6-mos EBIT 11% higher year-over-year 1H13 Georgia weather 55% colder than 1H12, resulting in $14 million EBIT improvement Customers and contracts: Georgia market share stable at 32% Retail services contracts up 56% year-over-year through June, due mainly to addition of warranty contracts in 1Q13 Portfolio of 33,000 commodity customer relationships purchased in Illinois in June 2013 Purchase price of $32M (~3x 2014E EBITDA) Additional margin with minimal operating expense Expect $0.02 impact to 2013 diluted EPS Expect $0.04 impact to 2014 diluted EPS Retail Operations *

2Q13 EBIT of $11 million vs. 2Q12 $(9) million $11 million EBIT gain on sale of Compass Energy in 2Q13 $13 million y/y improvement in commercial activity for 2Q13 $5 million hedge gain, net of LOCOM, in 2Q13 vs. $10 million hedge gain (no LOCOM adjustment) in 2Q12 Storage rollout schedule was $14 million as of 6/30/13 vs. $47 million at 6/30/12 Operating margin components Wholesale Services * millions 4Q12 millions 2Q13

2Q13 EBIT of $0 vs. 2Q12 EBIT of $2 million 6-mos EBIT of $2 million vs. $5 million in 2012 Declines driven primarily by recontracting capacity at current market rates (primarily at Jefferson Island), as well as higher depreciation, property taxes, storage expenses and outside services due to new facilities in service vs. 2012 Market fundamentals remain challenging; uncontracted capacity being managed in-house until market conditions improve to support term contracts Midstream Operations * millions Contracted storage capacity as of 6/30/13 Subscribed firm capacity includes 1.5 Bcf at Jefferson Island and 2 Bcf at GTS that are contracted by Sequent. Cavern 1 at GTS (6 Bcf) undergoing rewater throughout most of 2013.

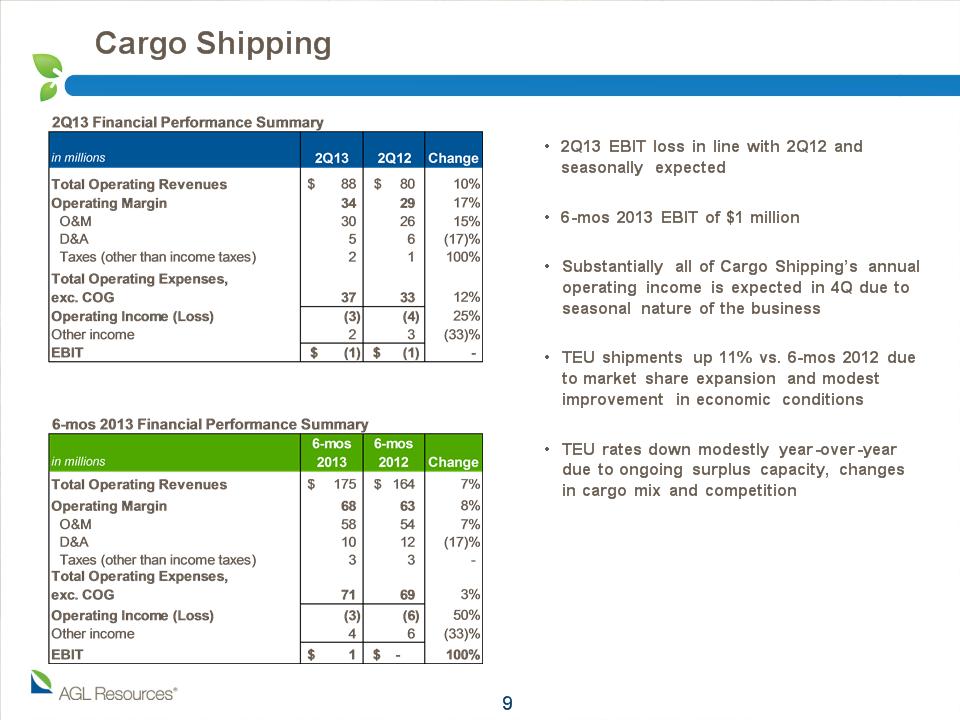

2Q13 EBIT loss in line with 2Q12 and seasonally expected 6-mos 2013 EBIT of $1 million Substantially all of Cargo Shipping’s annual operating income is expected in 4Q due to seasonal nature of the business TEU shipments up 11% vs. 6-mos 2012 due to market share expansion and modest improvement in economic conditions TEU rates down modestly year-over-year due to ongoing surplus capacity, changes in cargo mix and competition Cargo Shipping * millions

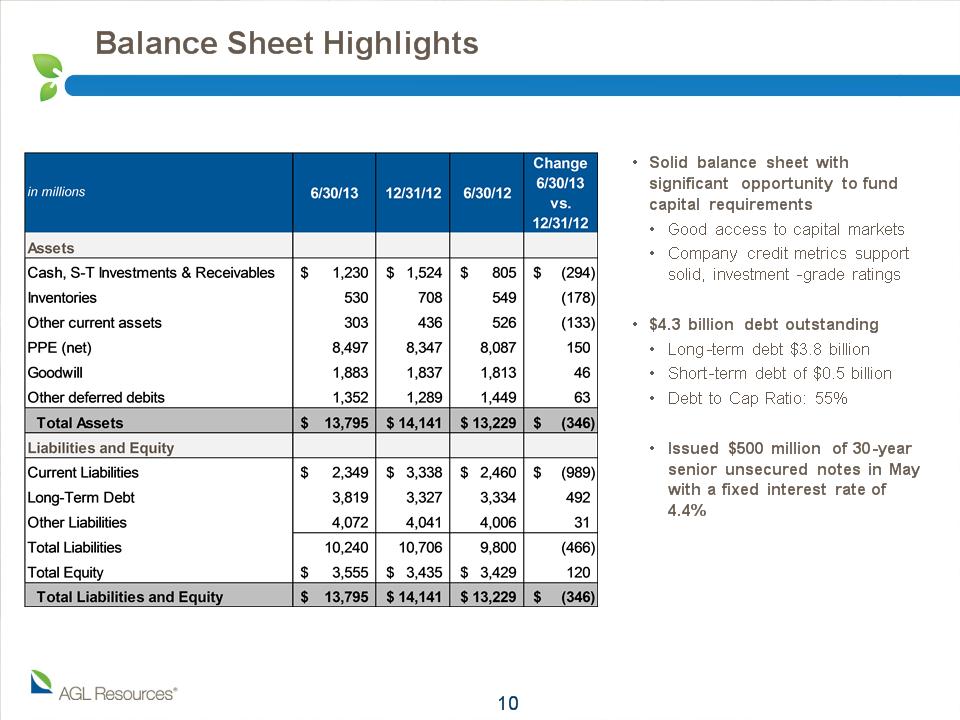

Solid balance sheet with significant opportunity to fund capital requirements Good access to capital markets Company credit metrics support solid, investment-grade ratings $4.3 billion debt outstanding Long-term debt $3.8 billion Short-term debt of $0.5 billion Debt to Cap Ratio: 55% Issued $500 million of 30-year senior unsecured notes in May with a fixed interest rate of 4.4% Balance Sheet Highlights * millions

Infrastructure investment legislation pertaining to natural gas utilities approved by IL General Assembly (SB 2266) Signed by Illinois governor on July 5, 2013 Any rider-based program rates could not take effect for Nicor Gas until January 2015, the timing of which is consistent with the base rate freeze in place as part of the merger agreement Under the legislation, the cumulative amount of increases billed under the surcharge shall not exceed an annual average 4% of the utility's delivery base rate revenues Depreciation legislation approved by IL General Assembly (HB 3104) Governor has until August 18 to review the bill If approved, Nicor Gas expects to file a depreciation study with the Illinois Commerce Commission (ICC) in August, with a 120-day ICC review period Any change in the depreciation rate would be effective as of the date that the depreciation study was filed Current depreciation rate at Nicor Gas is 4.1%; each 10 bps reduction in the depreciation rate is expected to result in reduced annual depreciation expense of approximately $4 million to $6 million A lower depreciation rate would not impact customer bills, would provide incentive for Nicor Gas to increase capital expenditures and create jobs in the state Illinois – Legislative Update *

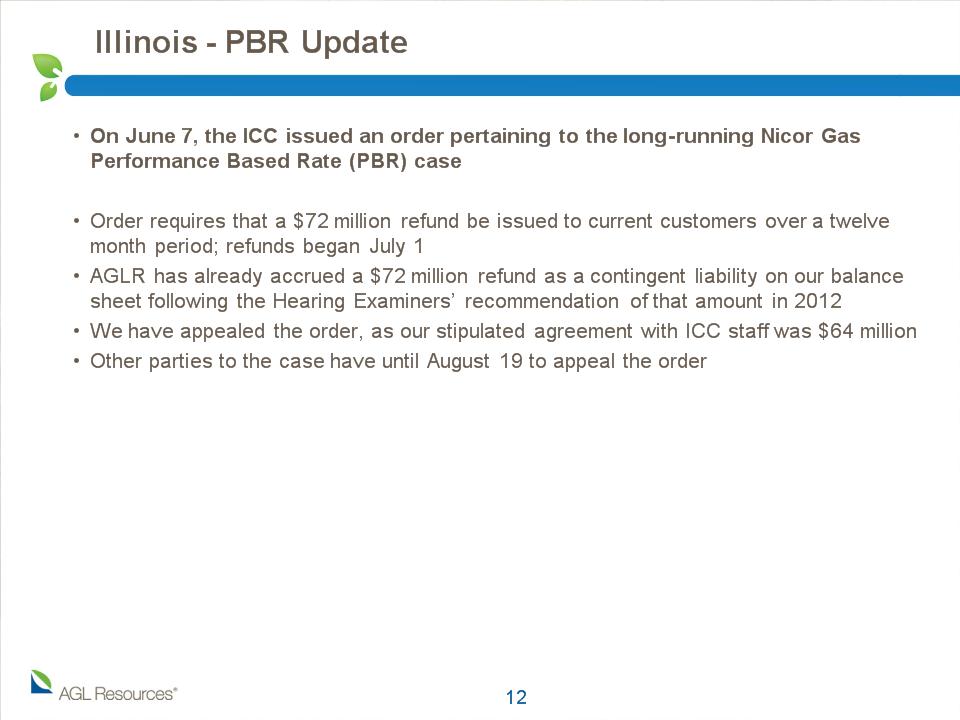

On June 7, the ICC issued an order pertaining to the long-running Nicor Gas Performance Based Rate (PBR) case Order requires that a $72 million refund be issued to current customers over a twelve month period; refunds began July 1 AGLR has already accrued a $72 million refund as a contingent liability on our balance sheet following the Hearing Examiners’ recommendation of that amount in 2012 We have appealed the order, as our stipulated agreement with ICC staff was $64 million Other parties to the case have until August 19 to appeal the order Illinois – PBR Update *

Filed a settlement with the Georgia Commission staff on July 18 on the i-VPR proposal related to vintage plastic pipeline replacement Settlement calls for capex of $275 million to replace approximately 750 miles of pipeline by December 31, 2017 Expect Commission vote in early August Expect to file updated forecast of and three year construction/investment program for infrastructure requirements under i-SRP (Integrated System Reinforcement Program) and i-CGP (Integrated Customer Growth Program) on August 1, 2013 Combined programs would account for approximately $260 million in capital expenditures over 4-year period Current i-SRP, i-CGP and PRP (pipeline replacement program) sunset in 2013 Georgia – STRIDE II Update *

Utility Capital Expenditures Overview * millions Estimate pending approval of plan to be filed with the ICC and based on the legislative cap. Actual capital spending to be determined. (2) Base capex is pro-forma to include Nicor Gas capex prior to merger completion in December 2011.

AGL Resources - 2013 Priorities Invest necessary capital to maintain and enhance system reliability Remain a low-cost leader within the industry Opportunistically expand system and capitalize on potential customer conversions Maintain margins in Georgia and Illinois while continuing to expand into other profitable retail markets Integrate new retail businesses and expand reach Maximize strong storage and transportation rollout value created in 2012 Effectively perform on existing asset management agreements and expand customers Bring cost structure in line with market fundamentals Optimize storage portfolio, including expiring contracts Complete GTS Cavern 1 re-water and place back into service Pursue land-based LNG transportation opportunities Effectively control expenses and focus on capital discipline in each of our business segments Maximize vessel and container utilization and improve margin per TEU Prudently deploy capital investment and diligently manage operating costs Distribution Expenses Wholesale Midstream Shipping Retail *

Appendix *

Debt Maturities * millions redeemed millions

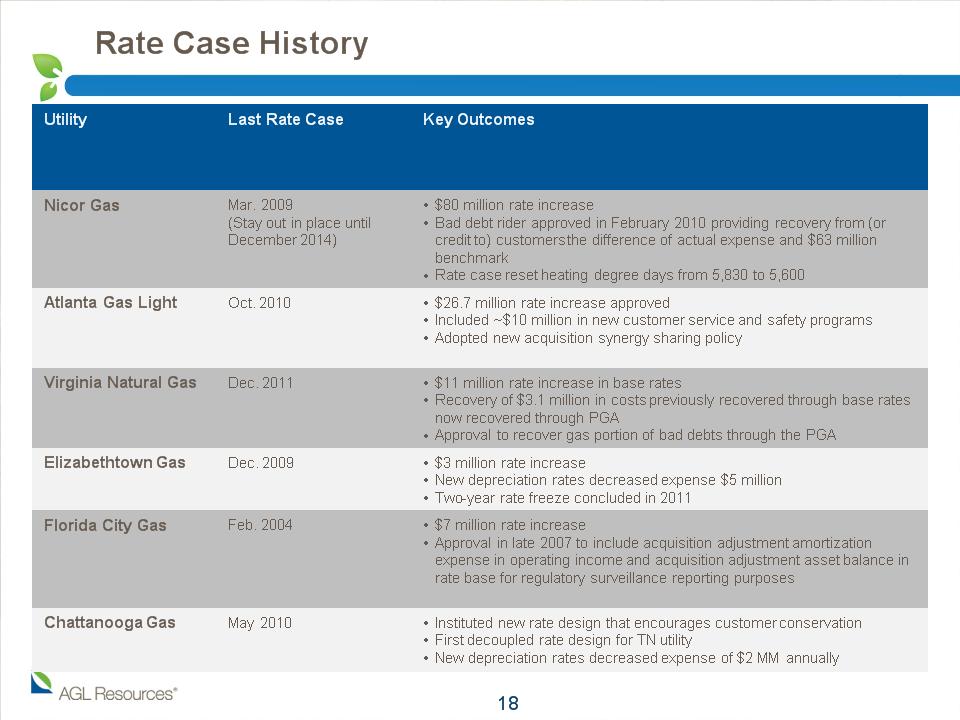

Rate Case History * millions redeemed Utility Last Rate Case Key Outcomes Nicor Gas Mar. 2009 (Stay out in place until December 2014) $80 million rate increase Bad debt rider approved in February 2010 providing recovery from (or credit to) customers the difference of actual expense and $63 million benchmark Rate case reset heating degree days from 5,830 to 5,600 Atlanta Gas Light Oct. 2010 $26.7 million rate increase approved Included ~$10 million in new customer service and safety programs Adopted new acquisition synergy sharing policy Virginia Natural Gas Dec. 2011 $11 million rate increase in base rates Recovery of $3.1 million in costs previously recovered through base rates now recovered through PGA Approval to recover gas portion of bad debts through the PGA Elizabethtown Gas Dec. 2009 $3 million rate increase New depreciation rates decreased expense $5 million Two-year rate freeze concluded in 2011 Florida City Gas Feb. 2004 $7 million rate increase Approval in late 2007 to include acquisition adjustment amortization expense in operating income and acquisition adjustment asset balance in rate base for regulatory surveillance reporting purposes Chattanooga Gas May 2010 Instituted new rate design that encourages customer conservation First decoupled rate design for TN utility New depreciation rates decreased expense of $2 MM annually

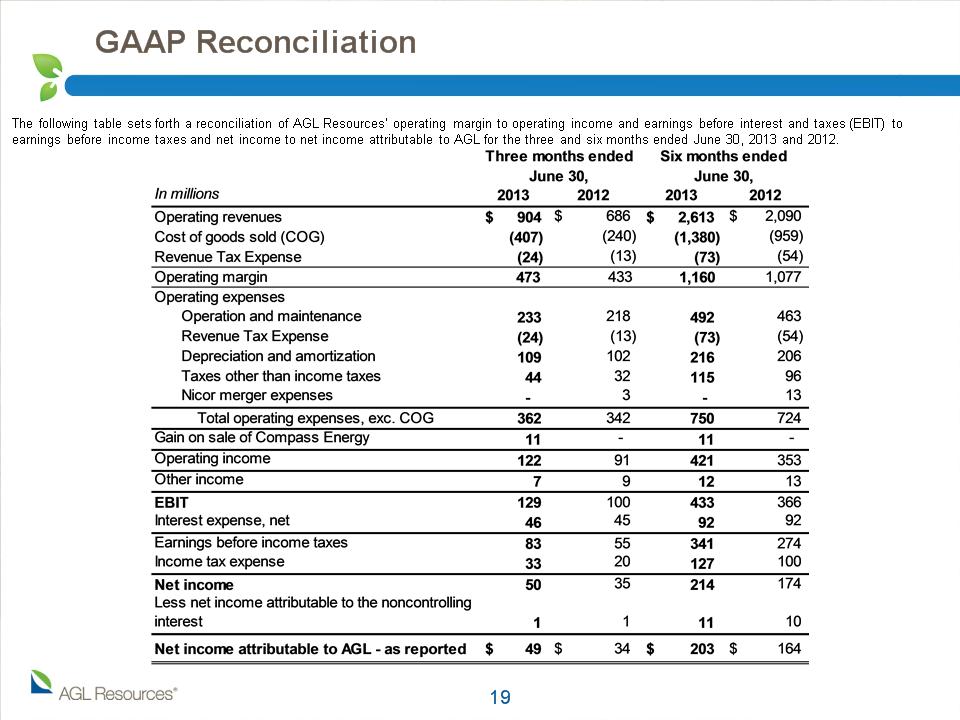

GAAP Reconciliation * The following table sets forth a reconciliation of AGL Resources’ operating margin to operating income and earnings before interest and taxes (EBIT) to earnings before income taxes and net income to net income attributable to AGL for the three and six months ended June 30, 2013 and 2012.

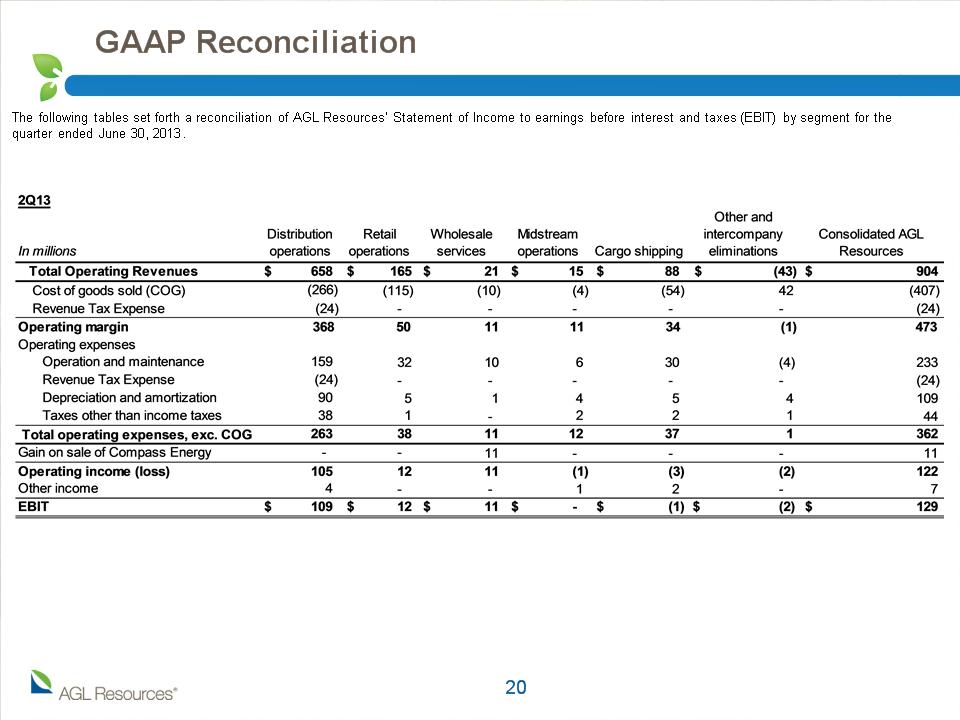

GAAP Reconciliation * The following tables set forth a reconciliation of AGL Resources’ Statement of Income to earnings before interest and taxes (EBIT) by segment for the quarter ended June 30, 2013.

GAAP Reconciliation * The following tables set forth a reconciliation of AGL Resources’ Statement of Income to earnings before interest and taxes (EBIT) by segment for the quarter ended June 30, 2012.

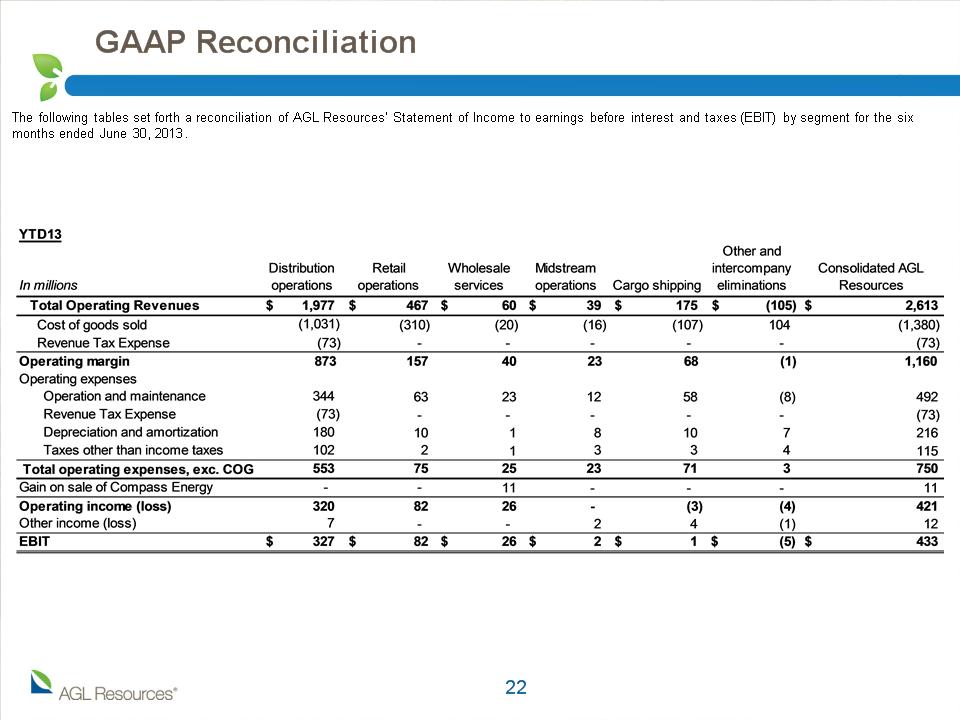

GAAP Reconciliation * The following tables set forth a reconciliation of AGL Resources’ Statement of Income to earnings before interest and taxes (EBIT) by segment for the six months ended June 30, 2013.

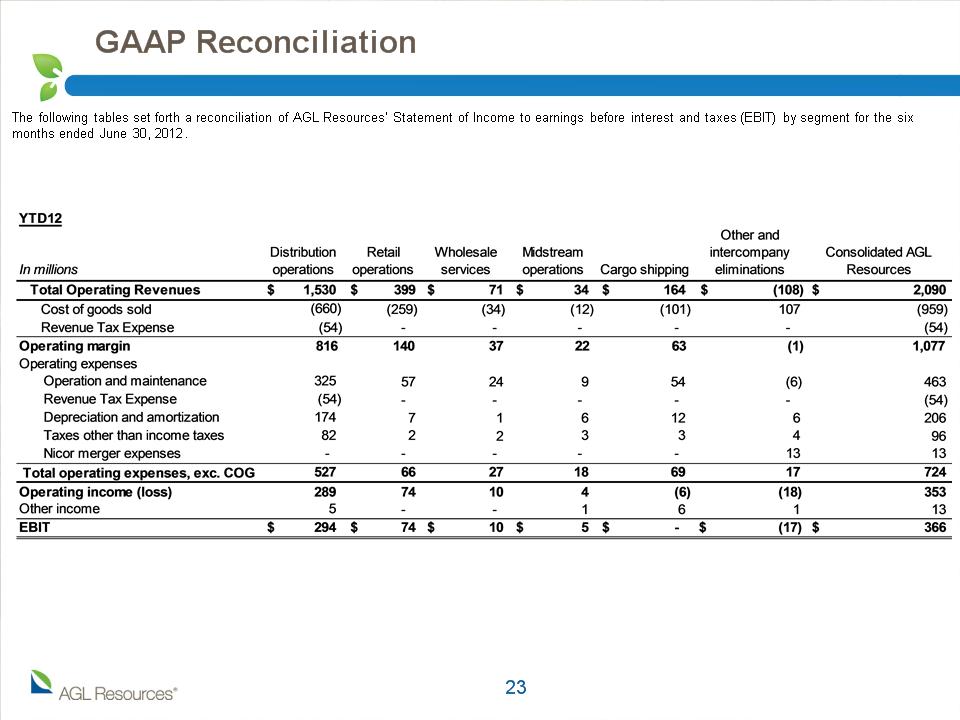

GAAP Reconciliation * The following tables set forth a reconciliation of AGL Resources’ Statement of Income to earnings before interest and taxes (EBIT) by segment for the six months ended June 30, 2012.

GAAP Reconciliation * The following tables set forth a reconciliation of AGL Resources’ Basic and Diluted earnings per share – as reported (GAAP) to Basic and Diluted earnings per share – as adjusted (Non-GAAP; excluding Nicor merger costs in 2012 and excluding wholesale services in 2013 and 2012), for the three and six months ended June 30, 2013 and 2012.

GAAP Reconciliation * Reconciliations of operating margin, EBIT and adjusted EPS are available in our quarterly reports (Form 10-Q) and annual reports (Form 10-K) filed with the Securities and Exchange Commission and on the Investor Relations section of our website at www.aglresources.com. Our management evaluates segment financial performance based on operating margin and EBIT, which includes the effects of corporate expense allocations. EBIT is a non-GAAP (accounting principles generally accepted in the United States of America) financial measure. Items that are not included in EBIT are income taxes and financing costs, including debt and interest, each of which the company evaluates on a consolidated basis. The company believes EBIT is a useful measurement of its performance because it provides information that can be used to evaluate the effectiveness of its businesses from an operational perspective, exclusive of the costs to finance those activities and exclusive of income taxes, neither of which is directly relevant to the efficiency of those operations. We also use EBIT internally to measure performance against budget and in reports for management and the Board of Directors. Projections of forward-looking EBIT are used in our internal budgeting process, and those projections are used in providing forward-looking business segment EBIT projections to investors. We are unable to reconcile our forward-looking EBIT business segment guidance to GAAP net income, because we do not predict the future impact of unusual items and mark-to-market gains or losses on energy contracts. The impact of these items could be material to our operating results reported in accordance with GAAP. Operating margin is a non-GAAP measure calculated as revenues minus cost of goods sold and revenue taxes, excluding operation and maintenance expense, depreciation and amortization, certain taxes other than income taxes and the gain or loss on the sale of assets, if any. These items are included in our calculation of operating income. We believe operating margin is a better indicator than operating revenues of the contribution resulting from customer growth, since cost of goods sold and revenue taxes are generally passed directly through to customers. We present our EPS excluding expenses incurred with respect to the merger with Nicor and excluding our wholesale services segment. As we do not routinely engage in transactions of the magnitude of the Nicor merger, and consequently do not regularly incur transaction related expenses of correlative size, we believe presenting our EPS excluding Nicor merger expenses provides investors with an additional measure of our core operating performance. In addition, we believe that excluding our wholesale services segment from our EPS provides investors with additional measure of core operating performance by excluding the volatility effects resulting from mark-to-market accounting in the wholesale services segment. EBIT, operating margin and adjusted EPS should not be considered as alternatives to, or more meaningful indicators of, our operating performance than operating income or EPS as determined in accordance with GAAP. In addition, our EBIT, operating margin and adjusted EPS may not be comparable to similarly titled measures of another company. We believe these financial measures are useful to investors because they provide an alternative method for assessing the company’s operating results in a manner that is focused on the performance of the company’s ongoing operations. The presentation of these financial measures is not meant to be a substitute for financial measures prepared in accordance with GAAP.