Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - MARRIOTT VACATIONS WORLDWIDE Corp | d492913d8k.htm |

Marriott

Vacations Worldwide Corporation

February 25, 2013

Exhibit 99.1 |

Forward-Looking Statements

This presentation contains “forward-looking statements”

within the meaning of federal securities

laws,

including

statements

about

earnings

trends,

estimates,

and

assumptions,

and

similar

statements

concerning

anticipated

future

events

and

expectations

that

are

not

historical

facts.

We caution you that these statements are not guarantees of future performance and are

subject to

numerous

risks

and

uncertainties,

including

volatility

in

the

economy

and

the

credit

markets,

supply

and

demand

changes

for

vacation

ownership

and

residential

products,

competitive

conditions, the availability of capital to finance growth, and other matters referred to

under the heading “Risk Factors”

contained in our most recent annual report on Form 10-K filed with the

U.S Securities and Exchange Commission (the “SEC”) and in subsequent SEC filings,

any of which

could

cause

actual

results

to

differ

materially

from

those

expressed

in

or

implied

in

this

presentation.

These

statements

are

made

as

of

February

25,

2013

and

we

undertake

no

obligation to publicly update or revise any forward-looking statement, whether as a

result of new information, future events, or otherwise.

Throughout this presentation we report certain financial measures, each identified with a

double asterisk (“**”), that are not prescribed or authorized by United

States generally accepted accounting principles (“GAAP”). We discuss our

reasons for reporting these non-GAAP measures and reconcile each to the most

directly comparable GAAP measure at the end of this

presentation.

1 |

Introduction

2

Stephen P. Weisz

President and

Chief Executive Officer

John E. Geller, Jr.

Executive Vice President and

Chief Financial Officer

Jeff Hansen

Vice President, Investor Relations |

3

Who we are:

–

Marriott Vacations Worldwide Corporation (“VAC”) is an

industry leader in the upscale and luxury vacation

ownership segments

–

More than 420,000 owners

–

Over 60 global vacation and resort destinations

What we do:

–

Sell vacation ownership products

–

Rent vacation ownership inventory

–

Finance consumer purchases of vacation ownership

products

–

Manage resorts and provide services for owners and

members

–

Revenues are derived from diverse sources and nearly

half is recurring and stable

Who

We

Are

and

What

We

Do

Mission Statement:

Deliver Unforgettable Experiences

That Make Vacation Dreams Come True! |

Strategic Initiatives

4

Improve Development Margin:

•

Marketing and Sales

•

Cost of Vacation Ownership Products

Rationalize Organizational Structure and Costs

Growth:

•

New Timeshare Properties / Sales Distributions

•

New Timeshare Business Opportunities

Sell Excess Land and Luxury Inventory |

Segment

Strategies Asia Pacific

$68

Europe

$63

NORTH AMERICA

Improve development margins

Leverage

fixed

marketing

and

sales

costs

through

increased

sales

efficiency

Lower cost of vacation ownership products sold

Improve rental margins

Continue

to

enhance

Marriott

Vacation

Club

Destinations™

offerings.

Add new resort inventory with new sales distributions and vacation experiences

ASIA PACIFIC

Add new resort locations with on-site sales distribution

Improve development margins

Continue to enhance Asia points product offerings

5 |

Segment

Strategies Asia Pacific

$68

Europe

$63

EUROPE

Sell remaining developed inventory over next 2 years

Enhanced value proposition through access to the North America points program

LUXURY

Sell excess Luxury inventory through the North America points program over the next 2

to 3 years

Reduce Luxury unsold maintenance fees

Enhance offerings to existing Luxury fractional owners

6 |

Diversified Revenue Sources

2012 Revenues**

7

** 2012 revenues excludes cost reimbursements of $362 million. See non-GAAP financial

measures. $1,286 Million**

Rental

17%

Financing

12%

Resort

Management and

Other Services

20%

Sale of

Vacation

Ownership

Products

49%

Other

2% |

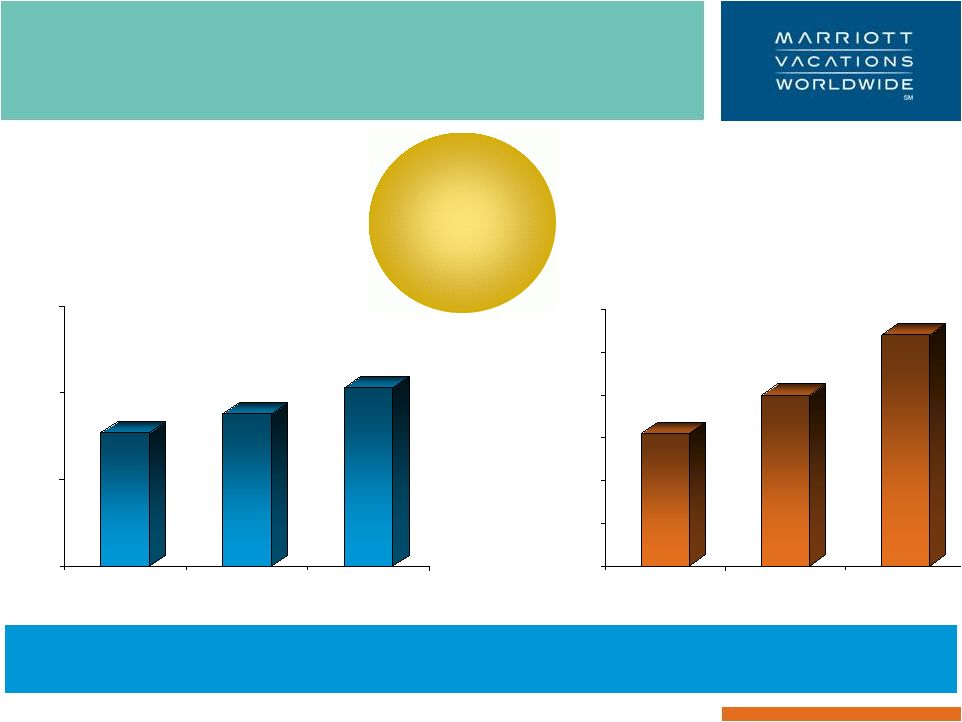

Gross

Contract Sales Performance 8

($ in millions)

Total gross contract sales for 2013 are

projected to be flat to 5% higher than 2012

North America gross contract sales are

projected to increase 5% to 10% from 2012

North America 2013 Contract Sales projected to increase by $29 million to

$58 million from 2012, driven by volume per guest increases.

$676

$514

$578

$688

$688 -

$722

$607 -

$636

$300

$450

$600

$750

2011

2012

2013 |

9

Adjusted development margin

1, **

1

Development margin represents sale of vacation ownership products revenues, net of expenses

(sale of vacation ownership products revenues less the cost of vacation ownership

products expenses and marketing and sales expenses) divided by sale of vacation ownership products revenues.

**

See Non-GAAP Financial Measures for adjustments to Development margin.

1% pt margin

improvement =

~$7M in

Adj. EBITDA

Improving Development Margins

54.7%

51.3%

49%

52.6%

47.7%

37.9%

32.6%

33.5%

to

34.5%

39.1%

32.7%

7.4%

16.1%

16.5%

to

17.5%

8.3%

19.6%

0%

20%

40%

60%

80%

100%

2011

2012

2013

North America

2011

North America

2012

Adjusted marketing and sales expenses**

Adjusted cost of vacation ownership products expenses**

Adjusted Development margin ** |

Resort Management and Other

Services revenues net of expenses

10

$227

$238

$253

$150

$200

$250

$300

2010

2011

2012

($ in millions)

Increasing

management

fees and club

dues; improving

margins

$31

$40

$54

$0

$10

$20

$30

$40

$50

$60

2010

2011

2012

($ in millions)

Management fees increase from $60 million in 2010 to $67 million

in 2012.

Club dues increase from $7

million in 2010 to $22 million in 2012.

Resort Management and Other

Services revenues

Resort Management and Other

Services revenues net of expenses |

11

Rental revenues net of expenses

($12)

($8)

($4)

$0

$4

$8

$12

$16

$20

2010

2011

2012

$(7)

$17

$12

$(8)

All segments

North America segment

($ in millions)

Maintenance fees from unsold inventory totaled $68 million in

2010, $65 million in 2011 and $60 million in 2012.

$0

$15

Improving

rental margins

$100

$150

$200

$250

2010

2011

2012

($ in millions)

$187

$152

$195

$212

$225

$180

Rental revenues

Rental revenues net of expenses |

Financing revenues net of financing

expenses and consumer financing

interest expense

12

Financing revenue

$169

$188

$99

$91

($ in millions)

$151

$84

Profits should

stabilize as of

2012

Consumer financing interest expense decreases from $63 million on a

pro forma basis in 2010 down to $41 million in 2012.

$40

$80

$120

$160

$200

2010

2011

2012

Financing

revenue,

net

of

financing

expenses

and

consumer

financing

interest

expense**

-

see

Non-GAAP

Financial

Measures. |

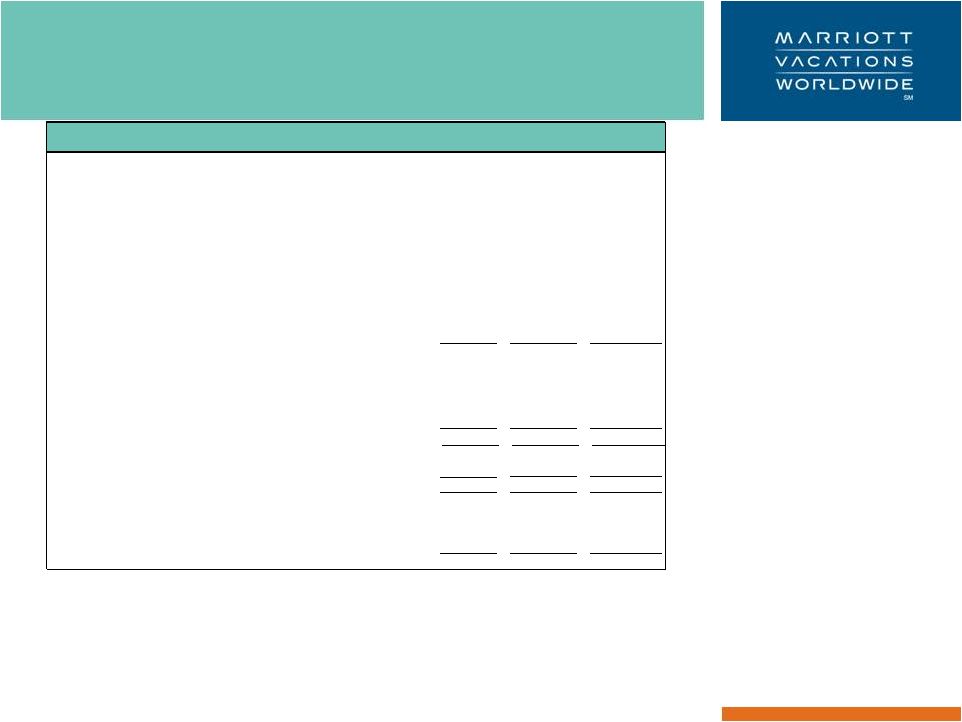

13

2013 Guidance

$ 688

16.1%

$ 50

$ 138

2012

$ 688

16.5%

$ 66

$ 150

2013 Outlook (ranges)

$ 722

17.5%

$ 74

$ 165

Gross Contract Sales

Adjusted Development

Margin**

Adjusted Net Income**

Adjusted EBITDA, as

adjusted

**

($ in millions)

** See Non-GAAP Financial Measures.

$ 676

7.4%

$ 20

$ 96

2011 |

Normalized Adjusted Free Cash Flow **

-

2013

14

** See Non-GAAP Financial Measures.

($ in millions)

2013 Outlook

2013

Low

High

Mid-Point

Adjustments

Normalized **

Adjusted net income

**

66

$

74

$

70

$

70

$

Adjustments to reconcile Adjusted net income to net cash

provided by operating

activities:

Adjustments for non-cash items ¹

84

86

85

85

Deferred income taxes

(10)

(14)

(12)

12

$

2

-

Net change in assets and liabilities:

Notes receivable originations

(275)

(285)

(280)

(280)

Notes receivable collections

275

280

278

278

Inventory

-

10

5

5

Liability for Marriott Rewards customer loyalty program

(40)

(45)

(43)

43

3

-

Organizational and separation related and litigation charges

(33)

(30)

(32)

32

4

-

Other working capital changes

(30)

(23)

(27)

10

5

(17)

Net cash provided by operating

activities

37

53

45

96

141

Capital expenditures for property and equipment:

Organizational and separation related capital expenditures

(7)

(10)

(9)

9

4

-

Other

(25)

(18)

(22)

(22)

Increase in restricted cash

(4)

(2)

(3)

(3)

Free cash flow

**

1

23

12

105

117

Borrowings from securitization

transactions

307

298

303

303

Repayment of debt related to

securitizations

(318)

(311)

(315)

(315)

Subtotal

(11)

(13)

(12)

-

(12)

Adjusted free cash flow

**

(10)

$

10

$

-

$

105

$

105

$

1

Includes depreciation, amortization of debt issuance costs, provision for loan losses,

gain/loss on disposals, and share-based compensation. 2

Represents higher cash taxes resulting from the tax benefits remaining with Marriott

International as part of the Spin-off. 3

Represents payment for Marriott Rewards Points issued prior to the Spin-off.

Liability to be fully paid in 2016. 4

Represents costs associated with MVW's organizational and separation related efforts (efforts

projected to be completed in 2014) as well as litigation cash settlements to be paid in

2013. 5

Represents elimination of one-time cash outflows. |

Inventory Calculation -

Example

15

Example assumes revenue from the sale of vacation ownership products grows annually

at 5%.

With

those

growth

levels,

MVW

would

target

inventory

of

$514M

on

hand

at

the

end

of

2016 which represents 2 years of inventory on hand (considered stabilized level).

As such, with inventory of $604M on hand at the beginning of 2013, MVW’s inventory

would need to be reduced by $90M by the end of 2016.

($ in millions)

2013

2014

2015

2016

Sale of vacation ownership products revenue

663

$

696

$

731

$

768

$

Cost of vacation ownership products

220

$

233

$

245

$

257

$

Product cost percentage

33%

33%

33%

33%

Inventory on-hand:

-

Assume stablized inventory on-hand of 2 years

Inventory Requirement:

514

$

2013 -

2016

Balance at beginning of 2013

1

604

$

Spending less than product cost

(90)

Balance desired at end of 2016

514

$

1

Includes finished goods of $484M and work-in-progress of $120M at the beginning of

2013 (excludes land and infrastructure) |

Strategic Initiatives

16

Improve Development Margin:

Rationalize Organizational Structure and Costs

Growth:

•

New Timeshare Properties / Sales Distributions

•

New Timeshare Business Opportunities

Sell Excess Land and Luxury Inventory

•

Marketing and Sales

•

Cost of Vacation Ownership Products |

17

Appendix |

Normalized Adjusted Free Cash Flow **

-

2012

** See Non-GAAP Financial Measures.

18

($ in millions)

2012

2012

Actual

Adjustments

Normalized **

Adjusted net income

**

50

$

50

$

Adjustments to reconcile Adjusted net income to net cash

provided by operating

activities:

Adjustments for non-cash items ¹

77

77

Deferred income taxes

(50)

50

$

4

-

Net change in assets and liabilities:

Notes receivable originations

(262)

(262)

Notes receivable collections

311

311

Inventory

68

(68)

5

-

Liability for Marriott Rewards customer loyalty program

(64)

64

6

-

Organizational and separation related and litigation charges

(57)

57

7

-

Other working capital changes

90

(105)

8

(15)

Net cash provided by operating

activities

163

(2)

161

Capital expenditures for property and equipment:

Organizational and separation related capital expenditures

(2)

2

7

-

Other

(15)

(15)

Increase in restricted cash

12

12

Free cash flow

**

158

-

158

Borrowings from securitization

transactions

238

238

Repayment of debt related to

securitizations

(411)

(411)

Subtotal

(173)

-

(173)

Adjusted free cash flow

**

(15)

-

(15)

Borrowings available from the securitization of sellable vacation

109

109

ownership notes receivable through the Warehouse Credit Facility

² Litigation settlement

³ 38

(38)

-

Adjusted free cash flow, as adjusted ** (excluding Litigation settlement)

132

$

(38)

$

94

$

1

Includes depreciation, amortization of debt issuance costs, provision for loan losses, excess

tax benefit on share-based compensation, share-based compensation, gain/loss on

disposals, equity method loss, and impairment reversals on equity investment. 2

Represents cash available to Marriott Vacations Worldwide to the extent the company securitized

sellable vacation ownership notes receivable through the Warehouse Credit Facility at year end.

3

Represents cash outflow not reflected in previous guidance.

4

Represents higher cash taxes resulting from the tax benefits remaining with Marriott

International as part of the Spin-off. 5

Represents adjustment to align real estate inventory spending with real estate inventory costs

(i.e., product costs). 6

Represents payment for Marriott Rewards Points issued prior to the Spin-off.

Liability to be fully paid in 2016. 7

Represents costs associated with MVW's organizational and separation related efforts (efforts

projected to be completed in 2014) as well as a litigation cash settlement paid in 2012.

8

Represents elimination of one-time cash inflows mainly associated with the Spin-off

(e.g., health and welfare plans, 401k plan, timing of other payments, etc.). |

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION

19

In this presentation we report certain financial measures that are not prescribed or

authorized by United States generally accepted accounting principles

(“GAAP”). We discuss management’s reasons for reporting these non-GAAP financial measures below, and reconcile

the most directly comparable GAAP financial measure to each non-GAAP financial measure

that we refer to (identified by a double asterisk ("**")

in

this

presentation).

Although

management

evaluates

and

presents

these

non-GAAP

financial

measures

for

the

reasons

described

below, please be aware that these non-GAAP financial measures have limitations and

should not be considered in isolation or as a substitute for revenues, net income,

earnings per share or any other comparable operating measure prescribed by GAAP. In addition, these

non-GAAP financial measures may be calculated and / or presented differently than

measures with the same or similar names that are reported

by

other

companies,

and

as

a

result,

the

non-GAAP

financial

measures

we

report

may

not

be

comparable

to

those

reported

by

others.

Adjusted

Net

Income

and

Adjusted

Pro

Forma

Net

Income.

Management

evaluates

non-GAAP

financial

measures

that

(1)

exclude

charges

incurred

in

the

16

weeks

and

52

weeks

ended

December

28,

2012

and

December

30,

2011,

including

non-cash

impairment

charges and other charges, (2) exclude the gain on the disposition of a Luxury segment golf

course and related assets in the 16 weeks and 52 weeks ended December 28, 2012, and

(3) include pro forma adjustments for the 16 weeks and 52 weeks ended December 30, 2011 to

reflect results as if the company were a stand alone public company in such period, because

those non-GAAP financial measures allow for period-over-period

comparisons of our on-going core operations before the impact of material charges and the gain on the disposition of

Luxury segment assets. These adjustments are itemized below and

on the following pages. These non-GAAP financial measures also

facilitate management’s comparison of results from our on-going operations before

material charges and the gain on the disposition of Luxury

segment

assets

with

results

from

other

vacation

ownership

companies.

Other

Charges

-

16

weeks

and

52

weeks

ended

December

28,

2012.

In

our

16

weeks

ended

December

28,

2012

Statements

of

Operations, we recorded $52 million of pre-tax charges comprised of $39 million for a

legal settlement related to a project in our Luxury segment

under

the

"Litigation

settlement"

caption,

$7

million

of

organizational

and

separation

related

costs

under

the

"Organizational

and

separation related" caption, $4 million related to closing off-site sales locations

in our Asia Pacific segment under the "Marketing and sales" caption,

$1

million

of

severance

in

our

Europe

segment

under

the

"Marketing

and

sales"

caption,

and

$1

million

of

costs

associated

with

removing the Ritz-Carlton brand from one of our properties in the Luxury segment under

the "Resort management and other services" caption. In our 52 weeks

ended December 28, 2012 Statements of Operations, we recorded $64 million of pre-tax charges comprised of

$41 million for a legal settlement related to a project in our Luxury segment under the

"Litigation settlement" caption, $16 million of organizational and separation

related costs under the "Organizational and separation related" caption, $4 million related to closing off-site

sales

locations

in

our

Asia

Pacific

segment

under

the

"Marketing

and

sales"

caption,

$1

million

of

severance

in

our

Luxury

segment

under

the

"Marketing

and

sales"

caption,

$1

million

of

severance

in

our

Europe

segment

under

the

"Marketing

and

sales"

caption,

and

$1

million

of

costs associated with removing the Ritz-Carlton brand from one of our properties in the

Luxury segment under the "Resort management and other services"

caption. Non-GAAP Financial Measures |

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION

20

Non-GAAP Financial Measures

Adjusted Net Income and Adjusted Pro Forma Net Income (continued)

Operations, we recorded $10 million of pre-tax charges comprised of $4 million of

spin-off related charges under the "General and administrative" caption,

$3 million of severance costs ($1 million under the "Marketing and sales" caption and $2 million under the

"General and administrative" caption), and $3 million of legal related charges under

the "Marketing and sales" caption. In our 52 weeks ended December 30,

2011 Statements of Operations, we recorded $18 million of pre-tax charges comprised of $5 million of severance

costs ($3 million under the "Marketing and sales" caption and $2 million under the

"General and administrative" caption), $4 million of spin-off related

charges under the "General and administrative" caption, $3 million of costs related to ADA compliance and Hurricane

Irene damage at a resort in the Bahamas under the "Cost of vacation ownership

products" caption, $3 million for a legal settlement related to a project in our

Luxury segment under the "Litigation settlement" caption, and $3 million of legal related charges under the

"Marketing and sales" caption.

2012 Statements of Operations, we did not record any non-cash impairment charges.

In our 52 weeks ended December 28, 2012 Statements of Operations, we reversed

$2 million related to our previously recorded impairment of an equity investment in a Luxury

segment vacation ownership joint venture project, because the actual costs incurred to

suspend the marketing and sales operations were lower than previously estimated,

under the "Impairment reversals on equity investment" caption. 2011 Statements of Operations, we did not record any non-cash impairment charges.

In preparation for the spin-off from Marriott International, management assessed

the intended use of excess undeveloped land and built inventory and the current market conditions

for those assets. During 2011, management approved a plan to accelerate cash flow through

the monetization of certain excess undeveloped land in the United States, Mexico, and

the Bahamas and to accelerate sales of excess built Luxury fractional and residential

inventory. As a result, in accordance with the guidance for accounting for the impairment or disposal of long-lived assets,

because the nominal cash flows from the planned land sales and the estimated fair values of

the land and excess built Luxury inventory were less than their respective carrying

values, we recorded a pre-tax non-cash impairment charge of $324 million in our 36 weeks

ended September 9, 2011 Statements of Operations under the “Impairment”

caption. Additionally, in our 36 weeks ended September 9, 2011 Statements of

Operations, under the "Impairment reversals on equity investment" caption, we reversed nearly $4 million of a more

than $16 million funding liability we originally recorded in 2009 related to a Luxury

segment vacation ownership joint venture project, based on facts and circumstances

surrounding the project, including favorable resolution of certain construction related claims and

contingent obligations to refund certain deposits relating to sales that have subsequently

closed. Other

Charges

-

16

weeks

and

52

weeks

ended

December

30,

2011.

In

our

16

weeks

ended

December

30,

2011

Statements

of

Non-cash

Impairment

Charges

-

16

weeks

and

52

weeks

ended

December

28,

2012.

In

our

16

weeks

ended

December

28,

Non-cash

Impairment

Charges

-

16

weeks

and

52

weeks

ended

December

30,

2011.

In

our

16

weeks

ended

December

30, |

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION

21

Non-GAAP Financial Measures

Adjusted Net Income and Adjusted Pro Forma Net Income (continued)

associated with the sale of the golf course, clubhouse and spa formally known as The

Ritz-Carlton Golf Club and Spa, Jupiter in our Luxury segment under the

"Gains and other income" caption. Statements of Operations, we included $18 million of pre-tax pro forma adjustments

comprised of $15 million of royalty fees, $2 million of interest expense and $1

million of dividends on mandatorily redeemable preferred stock of a consolidated subsidiary. In our 52 weeks

ended December 30, 2011 Statements of Operations, we included $71 million of pre-tax pro

forma adjustments comprised of $58 million of royalty fees, $9 million of interest

expense and $4 million of dividends on mandatorily redeemable preferred stock of a consolidated

subsidiary.

Adjusted Development Margin (Adjusted Sale of Vacation Ownership Products Net of Expenses)

as an indicator of operating performance. Our Adjusted Development Margin

adjusts Sale of vacation ownership products revenues for the impact of revenue

reportability, includes corresponding adjustments to both the Cost of vacation ownership

products expense and the Marketing and sales expense associated with the change in

revenues from the Sale of vacation ownership products, and includes adjustments for other

charges itemized in our Adjusted Net Income and Adjusted Pro Forma Net Income non-GAAP

financial measures explanation above. We evaluate Adjusted Development Margin

because it allows for period-over-period comparisons of our ongoing core operations before

the impact of revenue reportability and other charges on our Development margin.

or authorized by GAAP, reflects earnings excluding the impact of interest expense, provision

for income taxes, depreciation and amortization. We consider EBITDA to be an

indicator of operating performance, and we use it to measure our ability to service debt, fund

capital expenditures and expand our business. We also use EBITDA, as do analysts, lenders,

investors and others, because it excludes certain items that can vary widely across

different industries or among companies within the same industry. For example, interest

expense can be dependent on a company’s capital structure, debt levels and credit

ratings. Accordingly, the impact of interest expense on earnings can vary

significantly among companies. The tax positions of companies can also vary because of their differing abilities to

take advantage of tax benefits and because of the tax policies of the jurisdictions in which

they operate. As a result, effective tax rates and provision for income taxes can

vary considerably among companies. EBITDA also excludes depreciation and amortization because

companies utilize productive assets of different ages and use different methods of both

acquiring and depreciating productive assets. These differences can result in

considerable variability in the relative costs of productive assets and the depreciation and amortization

expense among companies.

Gain

on

the

disposition

of

a

Luxury

segment

golf

course

and

related

assets

-

16

weeks

and

52

weeks

ended

December

28,

2012.

In our 16 weeks and 52 weeks ended December 28, 2012 Statements of Operations, we recorded a

net $8 million gain Pro

Forma

Adjustments

-

16

weeks

and

52

weeks

ended

December

30,

2011.

In

our

16

weeks

ended

December

30,

2011

Adjusted

Development

Margin

(Adjusted

Sale

of

Vacation

Ownership

Products

Net

of

Expenses).

Management

also

evaluates

Earnings

Before

Interest,

Taxes,

Depreciation

and

Amortization

("EBITDA").

EBITDA,

a

financial

measure

which

is

not

prescribed |

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION

22

Adjusted

EBITDA.

We

also

evaluate

Adjusted

EBITDA,

another

non-GAAP

financial

measure,

as

an

indicator

of

performance.

Our

Adjusted

EBITDA excludes the impact of non-cash impairment charges or reversals and restructuring

charges and includes the impact of interest expense associated with the debt from the

Warehouse Credit Facility and from the securitization of our vacation ownership notes receivable in the term

ABS market, which together we refer to as consumer financing interest expense. We deduct

consumer financing interest expense in determining Adjusted EBITDA since the debt is

secured by vacation ownership notes receivable that have been sold to bankruptcy remote special purpose

entities and is generally non-recourse to us. We evaluate Adjusted EBITDA, which adjusts

for these items, to allow for period-over-period comparisons of our ongoing

core operations before material charges. Adjusted EBITDA is also useful in measuring our ability to service our non-

securitized debt. Together, EBITDA and Adjusted EBITDA facilitate our comparison of results

from our ongoing operations with results from other vacation ownership companies.

Adjusted

EBITDA

as

adjusted

and

Adjusted

Pro

Forma

EBITDA

as

adjusted.

Management

also

evaluates

Adjusted

EBITDA

as

adjusted

and Adjusted Pro Forma EBITDA as adjusted, which reflect adjustments for other charges

incurred in the 16 weeks and 52 weeks ended December 28, 2012 and December 30, 2011,

as well as the gain on the disposition of a Luxury segment golf course and related assets in the 16

weeks and 52 weeks ended December 28, 2012, and include pro forma adjustments for the 16

weeks and 52 weeks ended December 30, 2011, as itemized in our Adjusted Net Income

and Adjusted Pro Forma Net Income non-GAAP financial measures explanation. We evaluate Adjusted

EBITDA as adjusted and Adjusted Pro Forma EBITDA as adjusted as indicators of operating

performance because they allow for period-over- period comparisons of our

ongoing core operations before the impact of material charges and the gain on the disposition of Luxury segment

assets, and reflect results as if we were a stand alone public company in each period.

Non-GAAP Financial Measures |

MARRIOTT VACATIONS WORLDWIDE CONFIDENTIAL AND PROPRIETARY INFORMATION

23

Non-GAAP Financial Measures

Free Cash Flow.

Adjusted Free Cash Flow.

Normalized Adjusted Free Cash Flow.

Management also evaluates Free Cash Flow as a liquidity measure that provides useful information to

management and investors about the amount of cash provided by operating activities after

capital expenditures for property and equipment and changes in restricted cash.

Management considers Free Cash Flow to be a liquidity measure that provides useful

information to management and investors about the amount of cash generated by the business

that can be used for strategic opportunities, including making acquisitions and

strengthening the balance sheet. Analysis of Free Cash Flow also facilitates

management's comparison of the Company's results to its competitors' results.

Management also evaluates Adjusted Free Cash Flow as a

liquidity measure that provides useful information to management and investors about

the amount of cash provided by operating activities after capital expenditures for

property and equipment, changes in restricted cash, and the borrowing and repayment activity

related to our securitizations. Management considers Adjusted Free Cash Flow to

be a liquidity measure that provides useful information to management and investors

about the amount of cash generated by the business that can be used for strategic opportunities, including making

acquisitions and strengthening the balance sheet. Analysis of Adjusted Free Cash Flow

also facilitates management's comparison of the Company's results to its competitors'

results.

Management also evaluates Normalized Adjusted Free Cash Flow as a liquidity measure

that provides useful information to management and investors about the amount of cash

provided by operating activities after capital expenditures for property and

equipment, changes in restricted cash, the borrowing and repayment activity related to our

securitizations, and adjustments to remove the impact of cash flow items not expected to

occur on a regular basis. Adjustments in 2012 and 2013 eliminate the impact of

excess cash taxes, payments of Marriott Rewards Points issued prior to the Spin-off,

payments for organizational and separation related efforts, litigation cash settlements and

other working capital changes. Adjustments in 2012 also eliminate the benefit of

lower real estate inventory spending. Management considers Normalized Adjusted Free

Cash Flow to be a liquidity measure that provides useful information to management and investors about the amount of cash

generated by the business that can be used for strategic opportunities, including making

acquisitions and strengthening the balance sheet. Analysis of Normalized

Adjusted Free Cash Flow also facilitates management's comparison of the Company's results to its

competitors' results. |

Financing

Revenue,

Net

of

Financing

Expenses

and

Consumer

Financing

Interest

Expense.

Financing

revenue,

net

of

financing

expenses and consumer financing interest expense includes interest income earned on vacation

ownership notes receivable as well as fees earned

from

servicing

the

existing

loan

portfolio,

net

of

direct

costs

to

support

the

financing,

servicing

and

securitization

processes,

as

well

as

consumer financing interest expense. We believe it is a meaningful measure as it

highlights the overall profitability of our financing business. Total

Revenues

Excluding

Cost

Reimbursements.

Cost

reimbursements

revenue

includes

direct

and

indirect

costs

that

property

owners'

associations

and

joint

ventures

we

participate

in

reimburse

to

us,

and

relates,

predominantly,

to

payroll

costs

where

we

are

the

employer.

As

we

record

cost

reimbursements

based

upon

costs

incurred

with

no

added

markup,

this

revenue

and

related

expense

has

no

impact

on

net

income attributable to us because cost reimbursements revenue net of reimbursed costs

expense is zero. We consider total revenues excluding cost reimbursements to be

a meaningful metric as it represents that portion of revenue that impacts net income attributable to us.

24

Non-GAAP Financial Measures

($ in millions)

2010

2011

2012

Financing revenue

188

$

169

$

151

$

Less: financing expenses

(26)

(28)

(26)

Less: consumer financing interest expense ¹ (63)

(50)

(41)

Financing revenue, net of financing expenses

and consumer financing interest

expense** 99

$

91

$

84

$

**

Denotes non-GAAP financial measures.

1

Consumer financing interest expense includes pro forma adjustments of

$7 million and $3 million for 2010 and 2011,

respectively. ($ in millions)

2012

Total revenues

1,648

$

Less: cost reimbursements

(362)

Total revenues excluding cost reimbursements**

1,286

$

**

Denotes non-GAAP financial measures.

|

Non-GAAP

Financial

Measures

–

Consolidated

Adjusted

Development

Margin

(Adjusted

Sale

of

Vacation

Ownership Products Net of Expenses)

25

52 Weeks Ended

($ in millions)

December 28, 2012

December 30, 2011

Gross company-owned contract sales

1

688

$

658

$

Revenue recognition adjustments:

Reportability

2

(6)

25

Sales

Reserve

3

(42)

(36)

Other

(13)

(13)

Sale of vacation ownership products

627

$

634

$

1

Gross company-owned contract sales excludes sales generated under a

marketing sales arrangement with a joint venture and cancellation reversals.

2

Adjustment

for

lack

of

required

downpayment,

contract

sales

in

rescission

period,

or

percentage

completion

accounting

on

company-owned

contract

sales.

3

Represents additional reserve for current year financed vacation

ownership product sales, which we also refer to as sales reserve.

4

Adjustment for sales incentives that will not be recognized as Sale of

vacation ownership products revenues. CONSOLIDATED ADJUSTED

DEVELOPMENT MARGIN (ADJUSTED SALE OF VACATION OWNERSHIP PRODUCTS NET OF EXPENSES)**

Revenue

Revenue

($ in millions)

As Reported

Recognition

As Adjusted

As Reported

Recognition

As Adjusted

52 Weeks Ended

Other

Reportability

52 Weeks Ended

52 Weeks Ended

Other

Reportability

52 Weeks Ended

December 28, 2012

Charges

Adjustment

December 28, 2012

**

December 30, 2011

Charges

Adjustment

December 30, 2011

**

Sale of vacation ownership products

627

$

-

$

6

$

633

$

634

$

-

$

(25)

$

609

$

Less:

Cost of vacation ownership products

205

-

2

207

242

(3)

(9)

230

Marketing and sales

330

(6)

-

324

342

(6)

(3)

333

Development margin

92

$

6

$

4

$

102

$

50

$

9

$

(13)

$

46

$

Development margin percentage

1

14.8%

16.1%

8.0%

7.4%

** Denotes non-GAAP financial measures.

Note: We have reclassified certain prior year amounts to conform

to our 2012 presentation.

1

Development margin percentage represents Development margin divided by

Sale of vacation ownership products. Development margin percentage is calculated using whole dollars.

CONSOLIDATED GROSS COMPANY-OWNED CONTRACT SALES TO SALE OF

VACATION OWNERSHIP PRODUCTS |

26

Non-GAAP Financial Measures —

North America

Adjusted Development Margin (Adjusted Sale of Vacation

Ownership Products Net of Expenses)

($ in millions)

52 Weeks Ended

December 28, 2012

December 30, 2011

Gross company-owned contract sales

578

$

514

$

Revenue recognition adjustments:

Reportability ¹

(4)

20

Sales Reserve ²

(32)

(37)

Other ³

(13)

(13)

Sale of vacation ownership products

529

$

484

$

1

Adjustment for lack of required downpayment, contract sales in

rescission period, or percentage completion accounting on company-owned contract sales.

2

Represents additional reserve for current year financed vacation

ownership product sales, which we also refer to as sales reserve.

3

Adjustment for sales incentives that will not be recognized as Sale of

vacation ownership products revenues. NORTH AMERICA ADJUSTED

DEVELOPMENT MARGIN (ADJUSTED SALE OF VACATION OWNERSHIP PRODUCTS NET OF EXPENSES)

Revenue

Revenue

($ in millions)

As Reported

Recognition

As Adjusted

As Reported

Recognition

As Adjusted

52 Weeks Ended

Reportability

52 Weeks Ended

52 Weeks Ended

Other

Reportability

52 Weeks Ended

December 28, 2012

Adjustment

December 28, 2012

**

December 30, 2011

Charges

Adjustment

December 30, 2011

**

Sale of vacation ownership products

529

$

4

$

533

$

484

$

-

$

(20)

$

464

$

Less:

Cost of vacation ownership products

173

2

175

190

(1)

(8)

181

Marketing and sales

254

-

254

248

(2)

(2)

244

Development margin

102

$

2

$

104

$

46

$

3

$

(10)

$

39

$

Development

margin

percentage

1

19.3%

19.6%

9.5%

8.3%

** Denotes non-GAAP financial measures.

1

Development margin percentage represents Development margin divided by

Sale of vacation ownership products. Development margin percentage is calculated using whole dollars.

NORTH AMERICA GROSS COMPANY-OWNED CONTRACT SALES TO SALE OF

VACATION OWNERSHIP PRODUCTS |

27

Non-GAAP Financial Measures –

2012

Adjusted Net Income and 2011 Adjusted Pro Forma Net

Income

As Adjusted

As Reported

As Adjusted

As Reported

Pro-Forma

($ in millions)

52 Weeks Ended

Other

52 Weeks Ended

52 Weeks Ended

Other

52 Weeks Ended

December 28, 2012

Charges

December 28, 2012

**

December 30, 2011

Charges

Pro-Forma

December 30, 2011

**

Revenues

Sale of vacation ownership

products

627

$

-

$

627

$

634

$

-

$

-

$

634

$

Resort management and other

services

253

-

253

238

-

-

238

Financing

151

-

151

169

-

-

169

Rental

225

-

225

212

-

-

212

Other

30

-

30

29

-

-

29

Cost

reimbursements

362

-

362

331

-

-

331

Total

revenues

1,648

-

1,648

1,613

-

-

1,613

Expenses

Cost of vacation ownership

products

205

-

205

242

(3)

-

239

Marketing and

sales

330

(6)

324

342

(6)

-

336

Resort management and other

services

199

(1)

198

198

-

-

198

Financing

26

-

26

28

-

-

28

Rental

225

-

225

220

-

-

220

Other

14

-

14

13

-

-

13

General and

administrative

86

-

86

81

(6)

-

75

Organizational and separation related

16

(16)

-

-

-

-

-

Litigation settlement

41

(41)

-

3

(3)

-

-

Interest

58

-

58

47

-

13

60

Royalty

fee

61

-

61

4

-

58

62

Impairment

-

-

-

324

(324)

-

-

Cost

reimbursements

362

-

362

331

-

-

331

Total

expenses

1,623

(64)

1,559

1,833

(342)

71

1,562

Gains and other

income

9

(8)

1

2

-

-

2

Equity in earnings

1

-

1

-

-

-

-

Impairment reversals on equity

investment

2

(2)

-

4

(4)

-

-

Income (loss) before income taxes

37

54

91

(214)

338

(71)

53

(Provision) benefit for income

taxes

(21)

(20)

(41)

36

(96)

27

(33)

Net income

(loss)

16

$

34

$

50

$

(178)

$

242

$

(44)

$

20

$

Total Contract Sales

Total Contract Sales

Gross Contract Sales

52 Weeks Ended

52 Weeks Ended

Cancellation

52 Weeks Ended

December 28, 2012

December 30, 2011

Reversal

December 30, 2011

Contract

sales

688

$

680

$

(4)

$

676

$

** Denotes non-GAAP financial measures.

|

28

Non-GAAP

Financial

Measures

–

2012

and

2011

EBITDA, Adjusted EBITDA, and Adjusted Pro

Forma EBITDA as adjusted

As Adjusted

As Reported

As Adjusted

As Reported

Pro-Forma

($'s in millions)

52 Weeks Ended

Other

52 Weeks Ended

52 Weeks Ended

Other

52 Weeks Ended

December 28, 2012

Charges

December 28, 2012

**

December 30, 2011

Charges

Pro-Forma

December 30, 2011

**

Net

income

16

$

34

$

50

$

(178)

$

242

$

(44)

$

20

$

Interest

expense

58

-

58

47

-

13

60

Tax

provision

21

20

41

(36)

96

(27)

33

Depreciation and

amortization

30

-

30

33

-

-

33

EBITDA

**

125

54

179

(134)

338

(58)

146

Impairment charges:

Impairments

-

-

-

324

(324)

-

-

Impairment reversals on equity investment

(2)

2

-

(4)

4

-

-

Consumer financing interest

expense

(41)

-

(41)

(47)

-

(3)

(50)

Adjusted

EBITDA**

82

$

56

$

138

$

139

$

18

$

(61)

$

96

$

** Denotes non-GAAP financial measures.

|

29

Non-GAAP Financial Measures –

2013 Outlook

(EBITDA and Adjusted EBITDA)

($ in millions)

Fiscal Year 2013

(low)

Fiscal Year 2013

(high)

Adjusted net

income

66

$

74

$

Interest

expense

43

45

Tax

provision

51

58

Depreciation and

amortization

23

23

EBITDA, as

adjusted**

183

$

200

$

Consumer financing interest

expense

(33)

(35)

Adjusted EBITDA, as

adjusted**

150

$

165

$

** Denotes non-GAAP financial measures.

2013 EBITDA and ADJUSTED EBITDA OUTLOOK |