Attached files

| file | filename |

|---|---|

| 8-K - U.S. CONCRETE, INC. 8-K - U.S. CONCRETE, INC. | usconcrete8k.htm |

BB&T Commercial & Industrial Conference

April 7, 2011

Forward-Looking Statement

Certain statements provided in this presentation, including those that express a belief, expectation or intention and those that are not of historical fact, are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements involve a number of risks and uncertainties and are intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These risks and uncertainties may cause actual results to differ materially from expected results and are described in detail in filings made by U.S. Concrete, Inc. (the “Company”) with the Securities and Exchange Commission, including the Company’s Annual Report on Form 10-K for the year ended December 31, 2010.

Certain statements provided in this presentation, including those that express a belief, expectation or intention and those that are not of historical fact, are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements involve a number of risks and uncertainties and are intended to qualify for the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. These risks and uncertainties may cause actual results to differ materially from expected results and are described in detail in filings made by U.S. Concrete, Inc. (the “Company”) with the Securities and Exchange Commission, including the Company’s Annual Report on Form 10-K for the year ended December 31, 2010.

The forward-looking statements speak only as of the date of this presentation. Investors are cautioned not to rely unduly on them. Many of these forward-looking statements are based on expectations and assumptions about future events that may prove to be inaccurate. The Company’s management considers these expectations and assumptions to be reasonable, but they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond the Company’s control. The Company undertakes no obligation to update these statements unless required by applicable securities laws.

Also, this presentation will contain various financial measures not in conformity with generally accepted accounting principles (“GAAP”). A reconciliation to the most comparable GAAP financial measure can be found at the end of this presentation.

Company Overview

Top 10 Producer of Ready Mixed Concrete in the U.S.Ready mixed concrete

3.8 million cubic yards in 2010

102 fixed concrete and 11 portable plants

Leading market position in 4 regions

Precast products

Seven production facilities

Serving 3 states

Aggregate business

11 owned and leased aggregate facilities

2 of 11 aggregate facilities leased to third parties

Revenue by Business Segment 2009 Revenue 2010 Revenue $57 $428 $56 $400 Ready Mix Precast

Note: Ready-Mix revenue net of intersegment sales

Broad Geographic Footprint HEADQUARTERs FIXED READY-MIXED PRECAST AGGREGATES

113 ready mixed concrete plants producing 3.8 million cubic yards of concrete Approximately 72 million tons of owned and leased reserves

7 pre-cast concrete plants generating $56 million in annual revenue 800+ ready-mixed concrete trucks 1,232 other vehicles

$29 million book value of owned real estate

Consolidated Revenue Ready-Mixed Only Note: 2005 – 2007 includes Michigan revenue Revenue Series 2 Series 3 2005 $525.6 2.4 2 2006 $728.5 4.4 2 2007 $803.8 1.8 3 2008 $685.4 2.8 5 2009 $485.4 2010 $455.7 Commercial Residential Public Works 2005 45.9% 50.4% 3.7% 2006 50.5% 42.2% 7.3% 2007 49.1% 35.0% 16.0% 2008 54.7% 26.0% 19.3% 2009 54.7% 18.9% 26.4% 2010 53.0% 19.5% 27.5%

Industry Overview

Industry Overview

Large, Fragmented Market Concrete Products Market Size

Over $43.0 billion in annual revenue

More than 2,300 independent ready-mixed concrete producers

More than 3,500 precast concrete manufacturers

Increasing vertical integration among cement, aggregates and concrete producers

& 60.0 $ 40.0 $ 20.0 $0.0 Pre-Cast $18.5

($ in billions)

Ready Mixed $24.7

Source: National Ready-Mixed Concrete Association and National Precast Concrete Association

Route to Market ready mixed concrete and concrete products are the principle route to market for both cement and aggregates Cementitious Aggregates Inland Agg. Marine Agg. Bitumen Mortor Ready Mix Concrete Products Asphalt + Construction Services Customer Home Builders General Contractors/ Self Builders Merchants/DIY Civil Engineering Local Authorities / Highway Agency % Indicates amount of volume moved through each report

5% 5% 75% 15% 2% 22% 36% 15% 25%

Ready-Mixed Concrete End Use Markets

Commercial and industrial sectors generate higher margins Streets and highways often self-performed by construction companies Total U.S. Market Street, Highway & Other Public Works 73% Commercial & Industrial 14% Residential Source: 2010 McGraw-Hill Construction Data

Economic Conditions and Forecast

Construction Outlook The outlook for the US construction industry and consequent demand for concrete will be shaped by public policy action in the short-term.

The US construction industry is expected to produce year-over-year growth for the first time since 2006; total US construction starts are forecasted to increase 3% in 2010 to a dollar value of $432.0 billion after declining

Total U.S. Construction Starts Growth (YOY % Growth) approximately 25% in 2009. Although 2010 construction starts were projected to grow from their 2009 level, on a dollar value basis, they remain 37% below their 2006 peak of $690.0 billion. Total U.S. Construction Starts ($ in billions)

Portland Cement Masonry Cement Source: McGraw-Hill 2010 Construction Outlook

2005 13% 2006 3% 2007 -7% 2008 -13% 2009 -25% 2010 3%

Portland Cement Masonry Cement 2005 $670 2006 $690 2007 $641 2008 $555 2009 $419 2010 $432

Residential Demand Number of Starts Note: PCA Fall 2010

Single Family Multi-Family

2005 1,719 354 2006 1,474 338 2007 1,038 306 2008 617 282 2009440113 2010476126 2011492155

2012 690 190 2013 945 240 2014 1,175 325

2015 1,236 355 2005 $2,073.0 2006 $1,812.0 -12.6%

2007 $1,344.0 -25.8% 2008 $899.0 -33.1% 2009 $553.0 -38.5%

2010 $602.0 8.9% 2011 $647.0 7.5% 2012 $880.0 36.0% 2013$1,185.034.7% 2014$1,500.026.6% 2015$1,591.06.1%

Commercial DemandMetric Tons of Cement Note: PCA Fall 2010

2009 6,092

2010 4,503

2011 4,266

2012 4,372

2013 5,766

2014 8,863

2015 12,620

2009 $6,092.0

2010 $4,503.0 -26.1%

2011 $4,266.0 -5.3%

2012 $4,372.0 2.5%

2013 $5,766.0 31.9%

2014 $8,863.0 53.7%

2015 $12,620.0 42.4%

Public Construction DemandMetric Tons of Cement Note: PCA Fall 2010

2009 35,770

2010 36,495

2011 36,590

2012 35,375

2013 39,230

2014 45,302

2015 50,277

2009 $35,770.0

2010 $36,495.0 2.0%

2011 $36,590.0 0.3%

2012 $35,375.0 -3.3%

2013 $39,230.0 10.9%

2014 $45,302.0 15.5%

2015 $50,277.0 11.0%

Company Strategy and Focus

Strategic Plan Key Elements Market and Customer Segmentation Reposition existing customer and product mix Promote value-added products Change the point-of-sale Pursue sustainable construction market Maximize Operational Excellence Be a low cost operator Provide outstanding customer service Eliminate waste and inefficiencies Exploit systems and technology advantage Evaluate Assets, Business Units and Opportunities

Long-term market demand conditions Customer mix versus market demand

Vertically integrated competition ROI and capital requirements

Continue to aggressively manage through current economic cycle

Closely monitor liquidity

Limit capital spending to internally generated cash flow

Evaluate assets, business units and opportunities

Ensure assets are delivering appropriate returns

Develop plan to improve underperforming operations

Stick to our knitting

Maximize value of our existing operations

Focus on value-added products, customer service and operating efficiency

Pursue Strategic Development Opportunities

Look to businesses that enhance existing position, such as aggregates

Utilize creative structures to limit capital investment required

Financial Summary

Performance Summary Analysis

Volume and Price Trend

Revenue, EBITDA and Margin Trend

Volume ASP Series 3

2008 5,674 $96.19 2

2009 3,948 $96.38 2

2010 3,805 $92.54 3

Category 4 4.5 2.8 5

Revenue Adjusted EBITDA % Margin

2008 $685.4 $41.1 6.0%

2009 $485.4 $16.7 3.4%

2010 $455.7 $12.5 2.7%

Category 4 $4.5 $2.8 500.0%

2010 Highlights

Restructuring of balance sheet completed with long-term debt reduced by $243.0 million

Ready-mixed and precast backlog increased significantly from 2009 year-end

Relatively stable raw material spread 44.2%

Average sales price appears to be stabilizing

4th quarter 2010 revenues up 3.3% over prior year on an 8.6% increase in ready-mixed volume

Condensed Consolidated Balance Sheet

"December 31,

2010" "December 31,

2009"

(in thousands)

ASSETS

Cash $5,290 $4,229

Other current assets 118,141 124,360

Property, plant and equipment, net 140,274 239,917

Goodwill and other assets 11,823 20,654

Total assets $275,528 $389,160

LIABILITY

Current liabilities $85,200 $94,108

Long-term debt, net of current maturities 52,017 288,669

Other long-term liabilities 12,178 16,574

Equity and noncontrolling interest 126,133 (10,191)

Total liabilities and equity $275,528 $389,160

Liquidity Summary

"December 31,

2010" "September 30,

2010"

Remaining Revolver Capacity $30.6 $34.0

Cash 5.3 4.6

Note: Total liquidity expected to decline during 1Q2011.

Trend in Average Selling Prices

% Change Versus Prior Year Comparable Period

Oct-09 2.0%

Nov-09 -1.7%

Dec-09 -2.4%

Jan-10 -7.5%

Feb-10 -1.1%

Mar-10 -5.5%

Apr-10 -5.5%

May-10 -2.7%

Jun-10 -5.1%

Jul-10 -5.6%

Aug-10 -5.6%

Sep-10 -2.9%

Oct-10 -2.7%

Nov-10 1.4%

Dec-10 -1.0%

Jan-11 0.8%

Feb-11 -3.3%

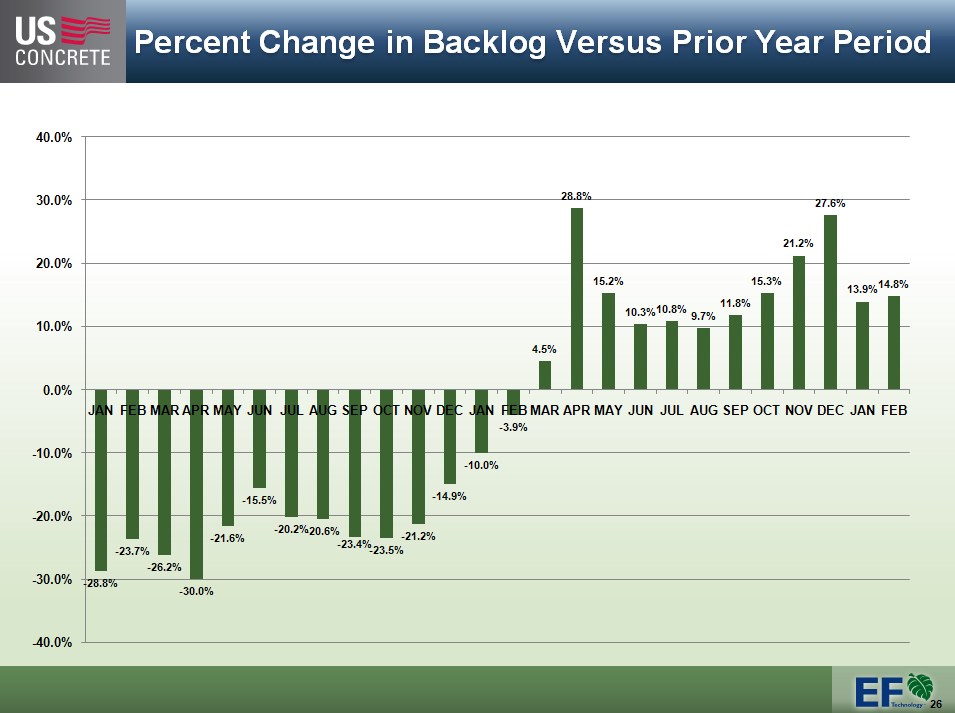

Percent Change in Backlog Versus Prior Year Period

JAN -28.8% 2.4 2

FEB -23.7% 4.4 2

MAR -26.2% 1.8 3

APR -30.0% 2.8 5

MAY -21.6%

JUN -15.5%

JUL -20.2%

AUG -20.6%

SEP -23.4%

OCT -23.5%

NOV -21.2%

DEC -14.9%

JAN -10.0%

FEB -3.9%

MAR 4.5%

APR 28.8%

MAY 15.2%

JUN 10.3%

JUL 10.8%

AUG 9.7%

SEP 11.8%

OCT 15.3%

NOV 21.2%

DEC 27.6%

JAN 13.9%

FEB 14.8%

Key Investment Highlights

Poised to benefit from rebound in construction activity

Experienced management team lead by industry veterans throughout the organization

Solid financial condition with recapitalized balance sheet

High quality assets with significant market share located in attractive markets

Strategic customer of vertically integrated cement producers due to volume

Disclosure of Non-GAAP Financial Measures

U.S. CONCRETE, INC.

ADDITIONAL STATISTICS

(In thousands, unless otherwise noted; unaudited)

We report our financial results in accordance with generally accepted accounting principles in the United States (“GAAP”). However, our management believes that certain non-GAAP performance measures and ratios, which our management uses in managing our business, may provide users of this financial information additional meaningful comparisons between current results and results in prior operating periods. See the table below for presentations of our adjusted EBITDA and adjusted EBITDA margin for the years 2008, 2009, and 2010.

We define adjusted EBITDA as our net income (loss) from continuing operations plus the provision (benefit) for income taxes, net interest expense, reorganization costs, non-cash impairments, depreciation, depletion and amortization. We define adjusted EBITDA margin as the amount determined by dividing adjusted EBITDA by total revenue. We have included adjusted EBITDA and adjusted EBITDA margin in the accompanying tables because they are often used by investors for valuation and for comparing our financial performance with the performance of other building material companies. We also use adjusted EBITDA to monitor and compare the financial performance of our operations. Adjusted EBITDA does not give effect to the cash we must use to service our debt or pay our income taxes and thus does not reflect the funds actually available for capital expenditures. In addition, our presentation of adjusted EBITDA may not be comparable to similarly titled measures other companies report.

Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, our reported operating results or cash flow from operations or any other measure of performance prepared in accordance with GAAP.

Disclosure Non-GAAP Financial Measures

U.S. Concrete, Inc. and Subsidiaries

Reconciliation of Net Income (Loss) from continuing operations to Adjusted EBITDA

(amount in thousands) Year Year Year

Ended Ended Ended

31-Dec-10 31-Dec-09 31-Dec-08

Adjusted EBITDA reconciliation:

Net income (loss) from continuing operations $19,763 $(78,354) $(128,454)

Income tax expense (benefit) 628 (315) (17,996)

Interest expense, net 20,754 25,941 26,470

Goodwill and other asset impairments - 47,595 135,613

Depreciation, depletion and amortization 23,744 26,325 25,446

Derivative income (996) - -

Gain on purchase of senior notes - (7,406)

Reorganization Items (59,191) - -

Reorganization items included in SG&A expenses 7,790 - -

Non-cash loss on sale of Sacramento assets - 2,954 -

Adjusted EBITDA $12,492 $16,740 $41,079

Adjusted EBITDA margin 2.7% 3.4% 6.0%

BB&T Commercial & Industrial Conference

April 7, 2011