Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - STRATUS PROPERTIES INC | ex23-1.htm |

| EX-31.1 - EXHIBIT 31.1 - STRATUS PROPERTIES INC | ex31-1.htm |

| EX-24.2 - EXHIBIT 24.2 - STRATUS PROPERTIES INC | ex24-2.htm |

| EX-32.2 - EXHIBIT 32.2 - STRATUS PROPERTIES INC | ex32-2.htm |

| EX-23.2 - EXHIBIT 23.2 - STRATUS PROPERTIES INC | ex23-2.htm |

| EX-24.1 - EXHIBIT 24.1 - STRATUS PROPERTIES INC | ex24-1.htm |

| EX-21.1 - EXHIBIT 21.1 - STRATUS PROPERTIES INC | ex21-1.htm |

| EX-32.1 - EXHIBIT 32.1 - STRATUS PROPERTIES INC | ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - STRATUS PROPERTIES INC | ex31-2.htm |

| EX-10.50 - EXHIBIT 10.50 - STRATUS PROPERTIES INC | ex10-50.htm |

| EX-10.40 - EXHIBIT 10.40 - STRATUS PROPERTIES INC | ex10-40.htm |

| EX-10.39 - EXHIBIT 10.39 - STRATUS PROPERTIES INC | ex10-39.htm |

|

UNITED STATES

|

||

|

SECURITIES AND EXCHANGE COMMISSION

|

||

|

Washington, D.C. 20549

|

||

|

FORM 10-K

|

||

|

(Mark One)

|

||

|

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the fiscal year ended December 31, 2010

|

||

|

OR

|

||

|

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the transition period from

|

to

|

|

|

Commission File Number: 0-19989

|

||

|

|

||

|

Stratus Properties Inc.

|

||

|

(Exact name of registrant as specified in its charter)

|

||

|

Delaware

|

72-1211572

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

212 Lavaca St., Suite 300

|

|

|

Austin, Texas

|

78701

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

(512) 478-5788

|

|

|

(Registrant's telephone number, including area code)

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock, par value $0.01 per share

|

NASDAQ

|

|

|

Preferred Stock Purchase Rights

|

NASDAQ

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act 0 Yes R No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. 0 Yes R No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. R Yes 0 No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ÿ0 Yes 0 No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. R

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. 0 Large accelerated filer 0 Accelerated filer 0 Non-accelerated filer R Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). 0 Yes R No

The aggregate market value of common stock held by non-affiliates of the registrant was approximately $58.8 million on March 15, 2011, and approximately $43.8 million on June 30, 2010.

Common stock issued and outstanding was 7,494,086 shares on March 15, 2011, and 7,470,117 shares on June 30, 2010.

|

STRATUS PROPERTIES INC.

|

|

|

TABLE OF CONTENTS

|

|

|

Page

|

|

|

1

|

|

|

1

|

|

|

1

|

|

|

3

|

|

|

6

|

|

|

6

|

|

|

6

|

|

|

6

|

|

|

6

|

|

|

12

|

|

|

12

|

|

|

12

|

|

|

13

|

|

|

13

|

|

|

14

|

|

|

29

|

|

|

54

|

|

|

54

|

|

|

54

|

|

|

54

|

|

|

54

|

|

|

54

|

|

|

54

|

|

|

55

|

|

|

55

|

|

|

56

|

|

|

56

|

|

|

S-1

|

|

|

F-1

|

|

|

E-1

|

|

PART I

Items 1. and 2. Business and Properties

Except as otherwise described herein or the context otherwise requires, all references to “Stratus,” “we,” “us,” and “our” in this Form 10-K refer to Stratus Properties Inc. and all entities owned or controlled by Stratus Properties Inc. All of our periodic report filings with the Securities and Exchange Commission (SEC) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, are available, free of charge, through our web site, www.stratusproperties.com, including our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports. These reports and amendments are available through our web site as soon as reasonably practicable after we electronically file or furnish such material to the SEC. All references to “Notes” in this report refer to the Notes to Consolidated Financial Statements located in Item 8. of this Form 10-K.

Overview

We are engaged in the acquisition, development, management, operation and sale of commercial, hotel, entertainment, multi-family and single-family residential real estate properties located primarily in the Austin, Texas area. Prior to the development of the W Austin Hotel & Residences project (see discussion below), we primarily generated revenues from sales of developed properties and through rental income from our commercial properties. Developed property sales can include an individual tract of land that has been developed and permitted for residential use or a developed lot with a home already built on it. We may, on occasion, sell properties under development or undeveloped properties, if opportunities arise that we believe will maximize overall asset values.

In December 2010, the hotel at our W Austin Hotel & Residences project opened, and in 2011, we began closing on sales of condominium units at the project. The W Austin Hotel & Residences project is located on a two-acre city block in downtown Austin and contains a 251-room luxury hotel, 159 residential condominium units, office, retail and entertainment space. The hotel is managed by Starwood Hotels & Resorts Worldwide, Inc. pursuant to our existing contract. The office space totals approximately 41,000 square feet and the retail space totals approximately 18,000 square feet. The entertainment space includes a live music venue and production studio, with a maximum capacity of 3,000 people (see “Company Strategies and Development Activities”).

Our principal real estate holdings are in southwest Austin, Texas. The number of developed lots, developed or under development acreage and undeveloped acreage as of December 31, 2010, that comprise our principal real estate properties are presented in the table below. A developed lot is an individual tract of land that has been developed and permitted for residential use. As of December 31, 2010, we own only one developed lot with a home that has already been built on it (the Calera Court Courtyard home). Developed acreage or acreage under development includes real estate for which infrastructure work over the entire property has been completed, is currently being completed or is able to be completed and necessary permits have been obtained. The undeveloped acreage shown in the table below is presented according to anticipated uses for single-family lots and commercial development based upon our understanding of the properties’ existing entitlements. However, there is no assurance that the undeveloped acreage will be developed because of the nature and cost of the approval and development process and market demand for a particular use. Undeveloped acreage includes real estate that can be sold “as is” (i.e., no infrastructure or development work has begun on such property).

|

Acreage

|

|||||||||||||||||

|

Under Development

|

Undeveloped

|

||||||||||||||||

|

Developed

|

Single

|

Multi-

|

Single

|

Total

|

|||||||||||||

|

Lots

|

Family

|

family

|

Commercial

|

Total

|

Family

|

Commercial

|

Total

|

Acreage

|

|||||||||

|

Austin

|

|||||||||||||||||

|

Barton Creek

|

120

|

-

|

249

|

368

|

617

|

781

|

28

|

809

|

1,426

|

||||||||

|

Lantana

|

-

|

-

|

-

|

-

|

-

|

-

|

223

|

223

|

223

|

||||||||

|

Circle C

|

21

|

-

|

-

|

23

|

23

|

132

|

363

|

495

|

518

|

||||||||

|

W Austin Hotel

|

|||||||||||||||||

|

& Residences

|

-

|

-

|

-

|

2

|

a

|

2

|

-

|

-

|

-

|

2

|

|||||||

|

San Antonio

|

|||||||||||||||||

|

Camino Real

|

-

|

-

|

-

|

-

|

-

|

-

|

2

|

2

|

2

|

||||||||

|

Total

|

141

|

-

|

249

|

393

|

642

|

913

|

616

|

1,529

|

2,171

|

||||||||

|

a.

|

Represents a city block in downtown Austin developed for a mixture of hotel, residential, office, retail and entertainment uses.

|

Our other Austin holdings at December 31, 2010, consisted of two 75,000-square-foot office buildings at 7500 Rialto Boulevard (7500 Rialto) located in our Lantana development, a 22,000-square-foot retail complex and a 3,300-square-foot bank building representing phase one of Barton Creek Village, and two retail buildings totaling 21,000 square feet and a 4,000-square-foot bank building on an existing ground lease at the 5700 Slaughter retail complex in the Circle C Ranch (Circle C) community.

The following table summarizes the estimated development potential of our Austin-area acreage as of December 31, 2010:

|

Single

|

Commercial

|

|||||||

|

Family

|

Multi-family

|

Office

|

Retail

|

|||||

|

(lots)

|

(units)

|

(gross square feet)

|

||||||

|

Barton Creek

|

464

|

1,860

|

1,590,000

|

23,000

|

||||

|

Lantana

|

-

|

-

|

1,314,800

|

371,400

|

||||

|

Circle C

|

57

|

-

|

760,000

|

212,440

|

||||

|

Austin 290 Tract

|

-

|

-

|

-

|

20,000

|

||||

|

Total

|

521

|

1,860

|

3,664,800

|

626,840

|

||||

For 2010, the only commercial leasing property that exceeded ten percent or more of our total assets or represented ten percent or more of our aggregate gross revenue was 7500 Rialto. This property provided 69 percent of our 2010 commercial leasing revenues and 38 percent of our 2010 total revenues. We currently have ten tenants at 7500 Rialto who are involved in computer electronics, medical devices, restaurant management and engineering, among other businesses. The two largest tenants, Arthocare Corporation and ST-Ericsson Inc., each generated approximately 11 percent of our 2010 total revenues and occupy approximately 28 percent and 25 percent, respectively, of leased square footage at 7500 Rialto. The first 75,000-square-foot building at 7500 Rialto became available for lease in 2002 and the second 75,000-square-foot building became available for lease in September 2006. A summary of the average occupancy rates and average rentals per square foot for 7500 Rialto and for our total portfolio of commercial leasing properties, excluding the office and retail space at the W Austin Hotel & Residences project which will be completed in 2011, for each of the last five years follows:

|

2010

|

2009

|

2008

|

2007

|

2006

|

|||||

|

Average occupancy:

|

|||||||||

|

7500 Rialto

|

94%

|

87%

|

95%

|

81%

|

82%

|

||||

|

Total portfolio

|

91%

|

79%

|

87%

|

79%

|

82%

|

||||

|

Average rentals per square foot:a

|

|||||||||

|

7500 Rialto

|

$23.84

|

$25.90

|

$24.78

|

$22.33

|

$16.94

|

||||

|

Total portfolio

|

$27.31

|

$28.40

|

$27.36

|

$23.77

|

$18.56

|

||||

|

a. Based on revenue for contractual rentals plus expense reimbursements for leased space.

|

|||||||||

Our scheduled expirations of leased square footage as of December 31, 2010, as a percentage of total leased space follow:

|

2011

|

2012

|

2013

|

2014

|

2015

|

2017

|

Thereafter

|

|||||||

|

7500 Rialto

|

8%

|

-

|

35%

|

9%

|

20%

|

28%

|

-

|

||||||

|

Total portfolio

|

6%

|

1%

|

32%

|

11%

|

18%

|

26%

|

6%

|

For information about our operating segments see “Results of Operations” in Item 7. and Note 10.

Company Strategies and Development Activities

Stratus Properties was formed as a corporation in March 1992 to hold, operate and develop the domestic real estate and oil & gas properties of our former parent company. We sold all of our oil & gas properties during the 1990's and have since focused solely on our real estate operations. Our overall strategy is to enhance the value of our properties by securing and maintaining development entitlements and developing and building real estate projects on these properties for sale or investment. We also continue to review and pursue opportunities for new projects that offer the possibility of acceptable returns and risks.

As a result of the settlement of certain development-related lawsuits and an increasing level of cooperation with the City of Austin (the City) regarding the development of our properties, we substantially increased our development activities and expenditures during the last five years (see discussion below), which has resulted in our debt increasing to $201.5 million at December 31, 2010. We have funded our development activities primarily through property sales proceeds, and borrowings under our long-term debt and our expanded credit facility (see “Credit Facility and Other Financing Arrangements” below and Note 6), which was established as a result of the financing relationship we have built with Comerica Bank (Comerica) over the past several years. The credit facility and other sources of financing have increased our financial flexibility and have allowed us to focus our efforts on developing our properties, acquiring other properties and increasing shareholder value. In addition, we continue to pursue additional development opportunities, and currently believe we can obtain bank financing necessary for developing our properties, although our ability to obtain bank financing in the future may be impacted by U.S. economic conditions. For further discussion of our operations and current real estate market conditions see Item 1A. and “Real Estate Market Conditions” in Item 7.

Our accomplishments over the last several years include the following:

|

·

|

We purchased a city block in downtown Austin, Texas and developed a multi-use property.

|

The W Austin Hotel & Residences

In December 2006, we acquired a two-acre city block in downtown Austin for $15.1 million to develop a multi-use project. The project, known as the W Austin Hotel & Residences project, contains a mixture of hotel, residential, office, retail and entertainment space. In 2008, we entered into a joint venture with Canyon-Johnson Urban Fund II, L.P., (Canyon-Johnson) for the development of the W Austin Hotel & Residences project (see Note 2). Construction of the $300 million project commenced in second-quarter 2008. We have executed an agreement with Starwood Hotels & Resorts Worldwide, Inc. for the management of hotel operations. The hotel opened in December 2010 and includes 251 luxury rooms and suites, a full service spa, gym and rooftop pool. Delivery of the first condominium units began in January 2011. Condominium units will continue to be completed on a floor-by-floor basis with delivery of pre-sold units continuing through mid-2011. As of March 15, 2011, 58 of the 159 condominium units were under contract and 25 condominium units had closed. Proceeds from the sales of the condominium units and net operating income will be used to repay debt incurred in connection with the project. The project also includes a live music venue and production studio with a maximum capacity of approximately 3,000 people. In addition to hosting concerts and private events, the venue will be the new home of Austin City Limits, a television program showcasing popular music legends. The venue opened in February 2011, has hosted 22 events through March 15, 2011, and has booked events through October 2011. The project has approximately 41,000 square feet of leasable office space, which opened in March 2011, and 18,000 square feet of leasable retail space are scheduled to open in June 2011. As of March 15, 2011, we had entered into leases for 17,500 square feet of the office space (including 9,000 for our corporate office) and for 2,700 square feet of the retail space. See Note 2 for additional discussion regarding the W Austin Hotel & Residences project.

|

·

|

We have successfully permitted and developed significant projects in our Barton Creek and Lantana project areas.

|

Barton Creek

Calera. Calera is a residential subdivision with plat approval for 155 lots. During 2004, we began construction of 16 courtyard homes at Calera Court, the 16-acre initial phase of the Calera subdivision. The second phase of Calera, Calera Drive, consisting of 53 single-family lots, many of which adjoin Fazio

Canyons Golf Course, received final plat and construction permit approval in 2005. Construction of the final phase, known as Verano Drive, began in 2007, was completed in July 2008 and includes 71 single-family lots. We sold one Calera Court courtyard home in 2010 and, as of December 31, 2010, one courtyard home at Calera Court, eight lots at Calera Drive and 67 lots at Verano Drive remained unsold.

Amarra Drive. Amarra Drive Phase I, which is the initial phase of the Amarra Drive subdivision, was completed in 2007 and includes eight lots, with sizes ranging from approximately one to four acres, some of which are course-side lots on the Fazio Canyons Golf Course and others are secluded lots adjacent to the Nature Conservancy of Texas. As of December 31, 2010, seven Amarra Drive Phase I lots remained unsold. In 2008, we commenced development of Amarra Drive Phase II, which consists of 35 lots on 51 acres. Development was substantially completed in October 2008, but no sales have occurred.

Mirador. The Mirador subdivision consists of 34 estate lots, with each lot averaging approximately 3.5 acres in size. As of December 31, 2010, two Mirador estate lots remained unsold.

Wimberly Lane. Wimberly Lane included two phases, with phase one consisting of 75 residential lots and phase two consisting of 47 residential lots. We entered into a contract with a national homebuilder to sell 41 lots within the Wimberly Lane Phase II subdivision. The last homebuilder lot was sold in January 2008, and the final Wimberly Lane lot was sold in December 2010.

Barton Creek Village. The first phase of Barton Creek Village includes a 22,000-square-foot retail complex, which was completed in 2007, and a 3,300-square-foot bank building, which was completed in early 2008 and is located within the retail complex. As of December 31, 2010, the retail complex was 89 percent leased and the bank building is leased through January 2023.

Lantana

Lantana is a partially developed, mixed-use real-estate development project. As of December 31, 2010, we had remaining entitlements for approximately 1.7 million square feet of office and retail use on 223 acres. Regional utility and road infrastructure is in place with capacity to serve Lantana at full build-out permitted under our existing entitlements.

Lantana also includes two 75,000-square-foot office buildings at 7500 Rialto Boulevard. As of December 31, 2010, occupancy was 85 percent for the first 7500 Rialto office building and 100 percent for the second office building.

|

·

|

We have made significant progress in obtaining the permitting necessary to pursue development of additional Austin-area properties.

|

Circle C Community

Effective August 2002, the City granted final approval of a development agreement (the Circle C settlement), which firmly established all essential municipal development regulations applicable to our Circle C properties for 30 years. In 2004, we amended our Circle C settlement to modify the permits and approvals necessary to develop 1.16 million square feet of commercial space, 504 multi-family units and 830 single-family residential lots. The City also provided us $15 million of cash incentives in connection with our future development of our Circle C and other Austin-area properties. These incentives, which are in the form of Credit Bank capacity, can be used for City fees and for reimbursement of certain infrastructure costs. Annually, we may elect to sell up to $1.5 million of the incentives to other developers for their use in paying City fees related to their projects. As of December 31, 2010, we have permanently used $9.5 million of our City-based incentives including cumulative sales of $4.5 million to other developers. We also have $1.9 million in Credit Bank capacity in use as temporary fiscal deposits. At December 31, 2010, available Credit Bank capacity was $3.6 million.

We are developing the Circle C community based on the entitlements secured in our Circle C settlement. Our 800-lot Meridian project within the Circle C community included our contracts with three national homebuilders to complete the construction and sales of the first 494 lots at Meridian over four phases. Phases one and two consisted of 134 lots each, phase three consisted of 108 lots and phase four consisted of 118 lots. We sold the final 13 lots for $0.9 million in the first quarter of 2010.

In 2006, we signed another contract with a national homebuilder for 42 additional lots. Development of those lots commenced in 2007 and was substantially completed in April 2008. In June 2009, this contract was terminated by the homebuilder. As of the date the contract was terminated, there were 30 remaining unclosed lots. In connection with the termination, the homebuilder forfeited a deposit of $0.6 million, which we recorded as other income in 2009. We are currently pursuing contracts with other homebuilders for the remaining lots. One lot was sold in 2009 for $0.1 million, eight lots were sold in 2010 for $1.1 million and 21 lots remained unsold as of December 31, 2010. The final phase of Meridian is expected to consist of 57 one-acre lots.

In addition, several retail sites at the Circle C community received final City approvals and are being developed. In the third quarter of 2008, we completed the construction of two retail buildings totaling 21,000 square feet at 5700 Slaughter. This retail project also includes a 4,000-square-foot building on an existing ground lease. As of December 31, 2010, occupancy was approximately 91 percent for the two retail buildings.

The Circle C community also includes Parkside Village, a 92,440-square-foot planned retail project. The project consists of a 33,650-square-foot full-service movie theater and restaurant, a 13,890-square-foot medical clinic office, three tilt-wall retail buildings at 14,775 square feet, 10,600 square feet and 8,075 square feet, and two pads available for ground leases or build-to-suit retail or restaurant uses. In February 2011, we entered into a joint venture with Moffett Holdings, LLC. (Moffett) to develop Parkside Village, obtained final permits and entitlements and began construction.

|

·

|

We believe that we have the potential right to receive approximately $7.1 million of future reimbursements associated with previously incurred Barton Creek utility development costs.

|

At December 31, 2010, we had approximately $2.0 million of expected future reimbursements of previously incurred costs recorded as a component of real estate on our balance sheet. The remaining potential future reimbursements are not recorded on our balance sheet because they relate to costs incurred prior to the 1995 formation of the Barton Creek Municipal Utility District (MUD). Since these costs pre-date the formation of the MUDs, there is less certainty in their potential reimbursement. Costs incurred after the 1995 formation of the MUDs were capitalized into property costs and subsequently expensed through cost of sales as properties sold. A significant portion of the additional costs, which we will incur in the future as our development activities at Barton Creek continue, is expected to be eligible for reimbursement. We received total MUD reimbursements of $5.1 million during 2010 and $7.0 million during 2009. As discussed in “Results of Operations” within Item 7., we account for MUD reimbursements as reductions to cost of sales, reductions in capital expenditures and interest income.

|

·

|

We formed a joint venture in November 2005 to purchase and develop a multi-use property in Austin, Texas.

|

Crestview Station

In 2005, we formed a joint venture partnership with Trammell Crow Central Texas Development, Inc. (Trammell Crow) to acquire an approximate 74-acre tract at the intersection of Airport Boulevard and Lamar Boulevard in Austin, Texas for $7.7 million. The property, known as Crestview Station, is a single-family, multi-family, retail and office development, which is located on the site of a commuter rail line. The joint venture completed environmental remediation, which the State of Texas certified as complete in 2007, and permitting of the property. The initial phase of utility and roadway infrastructure is complete. Crestview Station sold substantially all of its multi-family and commercial properties in 2007 and one commercial site in the first quarter of 2008. The joint venture retained the single family component of Crestview Station and one commercial site. The joint venture has obtained permits to develop Crestview Station as a 450-unit transit-oriented neighborhood. At December 31, 2010, our investment in the Crestview Station project totaled $3.1 million and the joint venture partnership had $8.2 million of outstanding debt, of which we guarantee $1.4 million (see Note 5 for further discussion).

Competition

The real estate development business is highly competitive and fragmented. We compete against numerous public and private developers of varying sizes, ranging from local to national in scope. As a result, we may be competing for investment opportunities, financing, and potential buyers with entities that may possess greater financial, marketing, or other resources than we have. Competition for potential buyers has been intensified by an increase in the number of available residential properties resulting from recent weak conditions in the real estate market. Our prospective customers generally have a variety of choices of new and existing homes and homesites when considering a purchase. We attempt to differentiate our properties primarily on the basis of community design, quality, uniqueness, amenities, location and developer reputation.

The real estate investment industry is highly fragmented among individuals, partnerships and public and private entities, with no dominant single entity or person. Although we may compete against large sophisticated owners and operators, owners and operators of any size can provide effective competition for prospective tenants. As a result of the decline in the real estate market beginning in 2008, vacancies for commercial properties have increased, which further increases competition for prospective tenants. We compete for tenants primarily on the basis of property location, rent charged, and the design and condition of improvements.

Credit Facility and Other Financing Arrangements

Acquiring and maintaining adequate financing is an important element of our business. For information about our credit facility and other financing arrangements, see “Credit Facility and Other Financing Arrangements” in Item 7. and Note 6.

Regulation and Environmental Matters

Our real estate investments are subject to extensive local, city, county and state rules and regulations regarding permitting, zoning, subdivision, utilities and water quality as well as federal rules and regulations regarding air and water quality and protection of endangered species and their habitats. Such regulation has delayed and may continue to delay development of our properties and result in higher developmental and administrative costs.

We have made, and will continue to make, expenditures for the protection of the environment with respect to our real estate development activities. Emphasis on environmental matters will result in additional costs in the future. Based on an analysis of our operations in relation to current and presently anticipated environmental requirements, we currently do not anticipate that these costs will have a material adverse effect on our future operations or financial condition.

Employees

At December 31, 2010, we had a total of 35 full-time employees and one part-time employee located at our Austin, Texas headquarters. We do not have any union employees. We believe we have a good relationship with our employees. Since January 1, 1996, numerous services necessary for our business and operations, including certain executive, administrative, accounting, financial and other services, have been performed by FM Services Company (FM Services) pursuant to a services agreement. FM Services is a wholly owned subsidiary of Freeport-McMoRan Copper & Gold Inc. Either party may terminate the services agreement at any time upon 60 days notice or earlier upon mutual written agreement.

Item 1A. Risk Factors

This report includes forward looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including statements about our plans, strategies, expectations, assumptions and prospects. Forward-looking statements are all statements other than statements of historical facts, such as those statements regarding future reimbursements for infrastructure costs, future events related to financing and regulatory matters, anticipated development plans and sales of land, units and lots, projected timeframes for development, construction and completion of our projects, projected capital expenditures, liquidity and capital resources, anticipated results of our business strategy, and other plans and objectives of management for future operations and activities. The words “anticipates,” “may,” “can,” “plans,” “believes,” “estimates,” “expects,” “projects,” “intends,” “likely,” “will,” “should,” “to be,” and any similar

expressions and/or statements that are not historical facts are intended to identify those assertions as forward-looking statements.

We believe that our forward-looking statements are based on reasonable assumptions. However, we caution readers that these statements are not guarantees of future performance and our actual experience and future financial results may differ materially from those anticipated, projected or assumed in the forward-looking statements. Important factors that may cause our actual results to differ materially from those anticipated by the forward-looking statements include, but are not limited to, changes in economic and business conditions, business opportunities that may be presented to and/or pursued by us, the availability of financing, increases in foreclosures and interest rates, the termination of sales contracts or letters of intent due to, among other factors, the failure of one or more closing conditions or market changes, the failure to attract homebuilding customers for our developments or their failure to satisfy their purchase commitments, the failure to complete agreements with strategic partners and/or appropriately manage relationships with strategic partners, a decrease in the demand for real estate in the Austin, Texas market, competition from other real estate developers, increases in operating costs, including real estate taxes and the cost of construction materials, changes in laws, regulations or the regulatory environment affecting the development of real estate and other factors.

Accuracy of the forward-looking statements depends on assumptions about events that change over time and is thus susceptible to periodic change based on actual experience and new developments. In addition, we may make changes to our business plans that could or will affect our results. We caution investors that we do not intend to update our forward-looking statements more frequently than quarterly, notwithstanding any changes in our assumptions, changes in our business plans, our actual experience, or other changes, and we undertake no obligation to update any forward-looking statements.

Important factors that could cause actual results to differ materially from our expectations include, without limitation, the following:

We need significant amounts of cash to service our debt. If we are unable to generate sufficient cash to service our debt, our financial condition and results of operations could be negatively affected.

As of December 31, 2010, our outstanding debt totaled $201.5 million. Our level of indebtedness could have important consequences. For example, it could:

|

·

|

increase our vulnerability to adverse changes in economic and industry conditions;

|

|

·

|

require us to dedicate a substantial portion of our cash flow from operations and proceeds from asset sales to pay or provide for our indebtedness, thus reducing the availability of cash flows to fund working capital, capital expenditures, acquisitions, investments and other general corporate purposes;

|

|

·

|

limit our flexibility to plan for, or react to, changes in our business and the market in which we operate;

|

|

·

|

place us at a competitive disadvantage to our competitors that have less debt; and

|

|

·

|

limit our ability to borrow money to fund our working capital, capital expenditures, debt service requirements and other financing needs.

|

Although we plan to repay a portion of our debt with proceeds from the sales of condominium units at our W Austin Hotel & Residences project, those sales may not occur as anticipated. In addition, the terms of the agreements governing our indebtedness include restrictive covenants and require that certain financial ratios be maintained. For example, the debt service coverage ratio covenant contained in most of our debt agreements requires us to maintain total stockholders’ equity of no less than $120.0 million. At December 31, 2010, our total stockholders’ equity was $128.6 million. Accordingly, we may need to raise additional capital through equity transactions to maintain compliance with the covenants in our loan agreements. We may also need to incur additional indebtedness in the future in the ordinary course of business to fund our development projects and our operations. If new debt is added to current debt levels, the risks described above could intensify. Further, if future financing is not available to us when required or is not available on acceptable terms, we may be unable to grow our business, take advantage of business opportunities, respond to competitive pressures or refinance maturing debt, any of which could have a material adverse effect on our financial condition and results of operations.

The deterioration of the credit and capital markets may adversely impact our ability to obtain financing on acceptable terms, which may hinder or prevent us from meeting our future operational and capital needs and could have a material adverse effect on our financial condition and results of operations.

Beginning in 2008, the credit markets experienced a disruption of a significant magnitude. This disruption reduced the availability and significantly increased the cost of most sources of funding. In some cases, these sources were eliminated. While the credit market has shown signs of improving since the second half of 2009, liquidity remains constrained and it is impossible to predict when the market will return to normalcy. This uncertainty may lead market participants to continue to act more conservatively. Because of these factors and the continued uncertainties that exist in the economy and for real estate developers in general, we cannot be certain that funding will be available if needed and, to the extent required, on acceptable terms. If funding is not available when needed, or is available only on unfavorable terms, we may be unable to meet our obligations as they come due or be required to post collateral to support our obligations, or we may be unable to implement our development plan, enhance our existing projects, complete projects or otherwise take advantage of business opportunities or respond to competitive pressures, any of which could have a material adverse effect on our financial condition and results of operations.

The success of our business is significantly related to general economic conditions and, accordingly, our business could be harmed by an extended economic slowdown and downturn in real estate asset values, property sales and leasing activities.

Periods of economic weakness or recession, significantly rising interest rates, declining employment levels, declining demand for real estate, declining real estate values, or the public perception that any of these events may occur, may negatively affect our business. These economic conditions can result in a general decline in acquisition, disposition and leasing activity, as well as a general decline in the value of real estate and in rents, which in turn reduces revenue derived from property sales and leases as well as revenues associated with development activities. In addition, these conditions can lead to a decline in property sales prices as well as a decline in funds invested in existing commercial real estate and related assets and properties planned for development.

During an economic downturn, investment capital is usually constrained and it may take longer for us to dispose of real estate investments, including residential condominium units at our W Austin Hotel & Residences project, or selling prices may be lower than originally anticipated. As a result, the value of our real estate investments may be reduced and we could realize losses or diminished profitability.

Beginning in 2008, credit became severely constrained and prohibitively expensive and real estate market activity contracted sharply in most markets as a result of the global financial crisis and the economic recession. These adverse macroeconomic conditions impacted real estate services companies like ours by significantly hampering transaction activity and lowering real estate valuations.

If the recent economic and market conditions were to continue, our business performance and profitability could again deteriorate. If this were to occur, we could fail to comply with certain financial covenants in our credit agreement which would force us to seek an amendment with our lenders. No assurance can be given that we would be able to obtain any necessary waivers or amendments on satisfactory terms, if at all.

We are vulnerable to concentration risks because our operations are almost exclusive to the Austin, Texas, market.

Our real estate activities are almost entirely located in Austin, Texas. Because of our geographic concentration and limited number of projects, our operations are more vulnerable to local economic downturns and adverse project-specific risks than those of larger, more diversified companies. The performance of the Austin economy greatly affects our sales and consequently the underlying values of our properties. Our geographic concentration may create increased vulnerability during regional economic downturns, which can significantly affect our financial condition and results of operations.

We currently participate in three joint ventures and may participate in other joint ventures in the future. We could be adversely impacted if any of our joint venture partners would fail to fulfill their obligations or if we had disagreements with any of our joint venture partners that were not satisfactorily resolved.

We currently have investments in and commitments to three joint ventures with unrelated parties to develop land and we may participate in other joint ventures in the future. Under existing joint venture agreements, we and our joint venture partners could be required to, among other things, provide guarantees of obligations or contribute additional capital until specified capital contribution requirements are met and we may have little or no control over the amount or timing of these obligations. In some circumstances, decisions of the joint venture are made by unanimous vote of the partners. If there is another economic downturn, our existing joint ventures or the joint venture partners may become unable or unwilling to fulfill their economic or other obligations. If our joint venture partners are unable or unwilling to fulfill their obligations or if we have any unresolved disagreements with our joint venture partners, we may be required to fulfill those obligations alone, expend additional resources to continue development of projects or delay further construction of projects, or we may be required to write down our investments at amounts that could be significant.

We may participate in other joint ventures in the future, which could subject us to certain risks, which may not otherwise be present, including:

|

·

|

the potential that our joint venture partner may not perform;

|

|

·

|

the joint venture partner may have economic, business or legal interests or goals that are inconsistent with or adverse to our interests or goals or the goals of the joint venture;

|

|

·

|

the joint venture partner may take actions contrary to our requests or instructions or contrary to our objectives or policies;

|

|

·

|

the joint venture partner might become bankrupt or fail to fund its share of required capital contributions;

|

|

·

|

we and the joint venture partner may not be able to agree on matters relating to the property; and

|

|

·

|

we may become liable for the actions of our third-party joint venture partners. Any unresolved disputes that may arise between joint venture partners and us may result in litigation or arbitration that would increase our expenses and prevent us from focusing our time and effort on the business of the joint ventures or our other business.

|

Our results of operations, cash flows and financial condition are greatly affected by the performance of the real estate industry.

The U.S. real estate industry is highly cyclical and is affected by changes in global, national and local economic conditions, which significantly deteriorated beginning in 2008, and events, such as general employment and income levels, availability of financing, interest rates, consumer confidence and overbuilding or decrease in demand for residential and commercial real estate. Our real estate activities are subject to numerous factors beyond our control, including local real estate market conditions (both where our properties are located and in areas where our potential customers reside), substantial existing and potential competition, general national, regional and local economic conditions, fluctuations in interest rates and mortgage availability, changes in demographic conditions and changes in government regulations or requirements. The occurrence of any of the foregoing could result in a reduction or cancellation of sales and/or lower gross margins for sales. Lower than expected sales as a result of these occurrences could have a material adverse effect on the level of our profits and the timing and amounts of our cash flows.

Real estate investments often cannot easily be converted into cash and market values may be adversely affected by these economic circumstances, market fundamentals, competition and demographic conditions. Because of the effect these factors have on real estate values, it is difficult to predict the level of future sales or sales prices that will be realized for individual assets.

Mortgage financing issues, including lack of supply of mortgage loans and tightened lending requirements, could reduce demand for our properties.

Our real estate operations are dependent upon the availability and cost of mortgage financing for potential customers, to the extent they finance their purchases, and for buyers of the potential customers’ existing residences. Many mortgage lenders and investors in mortgage loans experienced severe financial difficulties arising from losses incurred on sub-prime and other loans originated before the recent downturn in the real

estate market. These factors led to a decrease in the availability of financing and an increase in the cost of financing. A continuation of the weakness in the mortgage lending industry could adversely affect potential purchasers of our properties, negatively affecting demand for our properties.

Declines in the market value of our land and developments could adversely affect our financial condition and results of operations.

The market value of our land and our developments depend on market conditions. We acquire land for expansion into new markets and for replacement of land inventory and expansion within our current markets. If real estate demand decreases below what we anticipated when we acquired our properties, we may not be able to recover our investment in such property through sales or leasing, and our profitability may be adversely affected. If there is another economic downturn, we may have write-downs to the carrying values of our properties and/or be required to sell properties at a loss.

Unfavorable changes in market and economic conditions could negatively impact occupancy or rental rates, which could negatively affect our financial condition and results of operations.

Another decline in the real estate market and economic conditions could significantly affect rental rates. Occupancy and rental rates in our market, in turn, could significantly affect our profitability and our ability to satisfy our financial obligations. The risks that could affect conditions in our market include the following:

|

·

|

a further deterioration in economic conditions;

|

|

·

|

local conditions, such as oversupply of office space, a decline in the demand for office space or increased competition from other available office buildings;

|

|

·

|

the inability or unwillingness of tenants to pay their current rent or rent increases; and

|

|

·

|

declines in market rental rates.

|

We cannot predict with certainty whether any of these conditions will occur or whether, and to what extent, they will have an adverse effect on our operations.

Our operations are subject to an intensive regulatory approval process and opposition from environmental groups that could cause delays and increase the costs of our development efforts or preclude such developments entirely.

Before we can develop a property, we must obtain a variety of approvals from local and state governments with respect to such matters as zoning, and other land use issues, subdivision, site planning and environmental issues under applicable regulations. Some of these approvals are discretionary. Because government agencies and special interest groups have in the past expressed concerns about our development plans in or near Austin, our ability to develop these properties and realize future income from our properties could be delayed, reduced, prevented or made more expensive.

Several special interest groups have in the past opposed our plans in the Austin area and have taken various actions to partially or completely restrict development in some areas, including areas where some of our most valuable properties are located. We have actively opposed these actions and do not believe unfavorable rulings would have a significant long-term adverse effect on the overall value of our property holdings. However, because of the regulatory environment that has existed in the Austin area and the opposition of these special interest groups, there can be no assurance that our expectations will prove correct.

Our operations are subject to governmental environmental regulation, which can change at any time and generally would result in an increase to our costs.

Real estate development is subject to state and federal regulations and to possible interruption or termination because of environmental considerations, including, without limitation, air and water quality and protection of endangered species and their habitats. Certain of the Barton Creek properties include nesting territories for the Golden-cheeked Warbler, a federally listed endangered species. In 1995, we received a permit from the U.S. Wildlife Service pursuant to the Endangered Species Act, which to date has allowed the development of the Barton Creek and Lantana properties free of restrictions under the Endangered Species Act related to the

maintenance of habitat for the Golden-cheeked Warbler.

Additionally, in April 1997, the U.S. Department of Interior listed the Barton Springs Salamander as an endangered species after a federal court overturned a March 1997 decision by the Department of Interior not to list the Barton Springs Salamander based on a conservation agreement between the State of Texas and federal agencies. The listing of the Barton Springs Salamander has not affected, nor do we anticipate it will affect, our Barton Creek and Lantana properties for several reasons, including the results of technical studies and our U.S. Fish and Wildlife Service 10(a) permit obtained in 1995. The development permitted by our 2002 Circle C settlement with the City has been reviewed and approved by the U.S. Fish and Wildlife Service and, as a result, we do not anticipate that the 1997 listing of the Barton Springs Salamander will impact our Circle C properties.

We are making, and will continue to make, expenditures with respect to our real estate development for the protection of the environment. Emphasis on environmental matters will result in additional costs in the future. New environmental regulations or changes in existing regulations or their enforcement may be enacted and such new regulations or changes may require significant expenditures by us. The recent trend toward stricter standards in environmental legislation and regulations is likely to continue and could have an additional impact on our operating costs.

The real estate business is very competitive and many of our competitors are larger and financially stronger than we are.

The real estate business is highly competitive. We compete with a large number of companies and individuals that have significantly greater financial, sales, marketing and other resources than we have. Our competitors include local developers who are committed primarily to particular markets and also national developers who acquire properties throughout the U.S. The current downturn in the real estate industry could significantly increase competition among developers. Increased competition could cause us to increase our selling incentives and/or reduce our prices. An oversupply of real estate properties available for sale or lease, as well as the potential significant discounting of prices by some of our competitors, may adversely affect the results of our operations.

Changes in weather conditions or natural disasters could adversely impact and materially affect our business, financial condition and results of operations.

Our performance may be adversely affected by weather conditions that delay development or damage property, resulting in substantial repair or replacement costs to the extent not covered by insurance, a reduction in property values, or a loss of revenue, each of which could have a material adverse impact on our business, financial condition and results of operations. Our competitors may be affected differently by such changes in weather conditions or natural disasters depending on the location of their supplies or operations.

Our common stock is thinly traded; therefore, our stock price may fluctuate more than the stock market as a whole.

As a result of the thin trading market for our stock, its market price may fluctuate significantly more than the stock market as a whole or the stock prices of similar companies. Without a larger float, our common stock will be less liquid than the stock of companies with broader public ownership, and as a result, the trading prices for our common stock may be more volatile. Among other things, trading of a relatively small volume of common stock may have a greater impact on the trading price than would be the case if public float were larger.

Item 3. Legal Proceedings

We are from time to time involved in various legal proceedings of a character normally incident to the ordinary course of our business. We believe that potential liability from any of these pending or threatened proceedings will not have a material adverse effect on our financial condition or results of operations. We maintain liability insurance to cover some, but not all, potential liabilities normally incident to the ordinary course of our business as well as other insurance coverage customary in our business, with such coverage limits as management deems prudent.

Item 4. (Removed and Reserved)

Executive Officers of the Registrant

Certain information, as of March 15, 2011, regarding our executive officers is set forth in the following table and accompanying text.

|

Name

|

Age

|

Position or Office

|

||

|

William H. Armstrong III

|

46

|

Chairman of the Board, President and Chief Executive Officer

|

||

|

Erin D. Pickens

|

49

|

Senior Vice President and Chief Financial Officer

|

Mr. Armstrong has been employed by us since our inception in 1992. Mr. Armstrong has served as Chairman of the Board since August 1998, Chief Executive Officer since May 1998 and President since August 1996.

Ms. Pickens has served as our Senior Vice President since May 2009 and as our Chief Financial Officer since June 2009. Ms. Pickens previously served as Executive Vice President and Chief Financial Officer of Tarragon Corporation from November 1998 until April 2009, and as Vice President and Chief Accounting Officer from September 1996 until November 1998 and Accounting Manager from June 1995 until August 1996 for Tarragon and its predecessors. Tarragon Corporation filed for voluntary reorganization under Chapter 11 of the U.S. Bankruptcy Code on January 12, 2009, and emerged from bankruptcy on July 6, 2010.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock trades on the The Nasdaq Stock Market (NASDAQ) under the symbol STRS. The following table sets forth, for the periods indicated, the range of high and low sales prices of Stratus’ common stock, as reported by NASDAQ.

|

2010

|

2009

|

||||||||

|

High

|

Low

|

High

|

Low

|

||||||

|

First Quarter

|

$11.49

|

$8.00

|

$14.57

|

$4.52

|

|||||

|

Second Quarter

|

12.24

|

8.40

|

11.18

|

5.33

|

|||||

|

Third Quarter

|

10.09

|

8.01

|

8.60

|

4.50

|

|||||

|

Fourth Quarter

|

9.60

|

8.16

|

11.60

|

7.54

|

|||||

As of March 15, 2011, there were 546 holders of record of our common stock. We have not in the past paid, and do not anticipate in the future paying, cash dividends on our common stock. The declaration of dividends is at the discretion of our Board of Directors. Our current ability to pay dividends is restricted by terms of our credit agreement.

The following table sets forth information with respect to shares of our common stock that we repurchased during the three-month period ended December 31, 2010.

|

Period

|

Total Number of Shares Purchased

|

Average Price Paid Per Share

|

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programsa

|

Maximum Number of Shares That May Yet Be Purchased Under the Plans or Programsa

|

|||||

|

October 1 to 31, 2010

|

-

|

$

|

-

|

-

|

161,145

|

||||

|

November 1 to 30, 2010

|

-

|

-

|

-

|

161,145

|

|||||

|

December 1 to 31, 2010

|

-

|

-

|

-

|

161,145

|

|||||

|

Total

|

-

|

-

|

-

|

||||||

|

a.

|

In February 2001, our Board of Directors approved an open market share purchase program for up to 0.7 million shares of our common stock. The program does not have an expiration date. Our modified unsecured term loans prohibit common stock purchases while any of the loans are outstanding.

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

OVERVIEW

In management’s discussion and analysis “we,” “us,” and “our” refer to Stratus Properties Inc. and its consolidated subsidiaries and joint ventures. You should read the following discussion in conjunction with our consolidated financial statements and the related discussion of “Business and Properties” and “Risk Factors” included elsewhere in this Form 10-K. The results of operations reported and summarized below are not necessarily indicative of our future operating results. All references to “Notes” refer to Notes to Consolidated Financial Statements located in Item 8. “Financial Statements and Supplementary Data.”

We are engaged in the acquisition, development, management, operation and sale of commercial, hotel, entertainment, multi-family and single-family residential real estate properties located primarily in the Austin, Texas area. Prior to the development of the W Austin Hotel & Residences project (see discussion below), we primarily generated revenues from sales of developed properties and through rental income from our commercial properties. Developed property sales can include an individual tract of land that has been developed and permitted for residential use or a developed lot with a home already built on it. We may, on occasion, sell properties under development or undeveloped properties, if opportunities arise that we believe will maximize overall asset values.

In December 2010, the hotel at our W Austin Hotel & Residences project opened, and in 2011, we began closing on sales of condominium units at the project. The W Austin Hotel & Residences project is located on a two-acre city block in downtown Austin and contains a 251-room luxury hotel, 159 residential condominium units, office, retail and entertainment space. The hotel is managed by Starwood Hotels & Resorts Worldwide, Inc. pursuant to our existing contract. The office space totals approximately 41,000 square feet and the retail space totals approximately 18,000 square feet. The entertainment space includes a live music venue and production studio, with a maximum capacity of 3,000 people (see “Development and Other Activities – W Austin Hotel & Residences”).

Our principal real estate holdings are in southwest Austin, Texas. The number of developed lots, developed or under development acreage and undeveloped acreage as of December 31, 2010, that comprise our principal real estate development projects are presented in the following table.

|

Acreage

|

|||||||||||||||||

|

Under Development

|

Undeveloped

|

||||||||||||||||

|

Developed

|

Single

|

Multi-

|

Single

|

Total

|

|||||||||||||

|

Lots

|

Family

|

family

|

Commercial

|

Total

|

Family

|

Commercial

|

Total

|

Acreage

|

|||||||||

|

Austin

|

|||||||||||||||||

|

Barton Creek

|

120

|

-

|

249

|

368

|

617

|

781

|

28

|

809

|

1,426

|

||||||||

|

Lantana

|

-

|

-

|

-

|

-

|

-

|

-

|

223

|

223

|

223

|

||||||||

|

Circle C

|

21

|

-

|

-

|

23

|

23

|

132

|

363

|

495

|

518

|

||||||||

|

W Austin Hotel

|

|||||||||||||||||

|

& Residences

|

-

|

-

|

-

|

2

|

a

|

2

|

-

|

-

|

-

|

2

|

|||||||

|

San Antonio

|

|||||||||||||||||

|

Camino Real

|

-

|

-

|

-

|

-

|

-

|

-

|

2

|

2

|

2

|

||||||||

|

Total

|

141

|

-

|

249

|

393

|

642

|

913

|

616

|

1,529

|

2,171

|

||||||||

|

a.

|

Represents a city block in downtown Austin developed for a mixture of hotel, residential, office, retail and entertainment uses.

|

Our other Austin holdings at December 31, 2010, consisted of two 75,000-square-foot office buildings at 7500 Rialto Boulevard (7500 Rialto) located in our Lantana development, a 22,000-square-foot retail complex and a 3,300-square-foot bank building representing phase one of Barton Creek Village, and two retail buildings totaling 21,000 square feet and a 4,000-square-foot bank building on an existing ground lease at the 5700 Slaughter retail complex in the Circle C community.

The continued weakness in the Austin area real estate market, among other factors, has had a significant negative impact on our consolidated financial results. In addition, we recorded valuation allowances totaling $10.5 million in 2010 against our net deferred tax assets upon concluding that it was more likely than not that

these assets will not be realized. In 2010, we reported $9.1 million of revenues and a net loss attributable to Stratus common stock of $15.3 million, compared to $10.8 million of revenues and a net loss attributable to Stratus common stock of $5.9 million in 2009.

Real Estate Market Conditions

Factors that significantly affect United States (U.S.) real estate market conditions include interest rate levels and the availability of financing, the supply of product (i.e. developed and/or undeveloped land, depending on buyers’ needs) and current and anticipated future economic conditions. These market conditions historically move in periodic cycles, and can be volatile in specific regions. Because of the concentration of our assets primarily in the Austin, Texas area, market conditions in this region significantly affect our business.

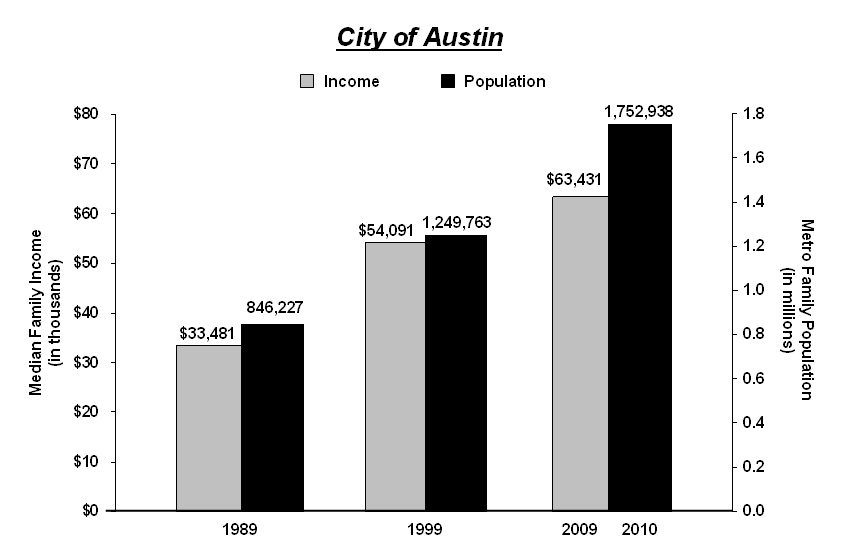

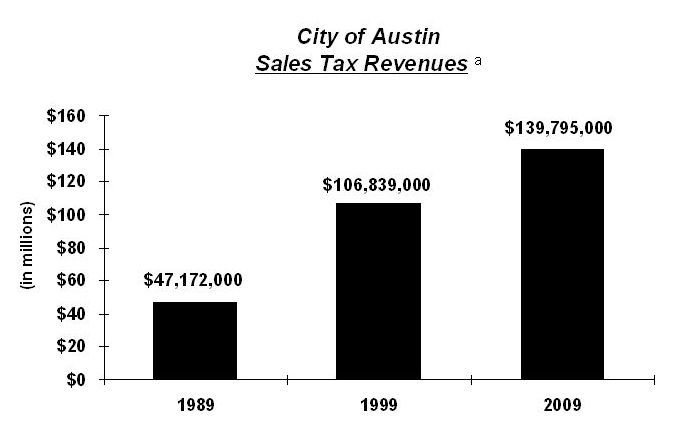

In addition to the traditional influence of state and federal government employment levels on the local economy, in recent years the Austin area has experienced significant growth in the technology sector. The Austin-area population increased approximately 40 percent between 1999 and 2010, largely because of an influx of technology companies and related businesses. Median family income levels in Austin also increased during the period from 1999 through 2009, rising by 17 percent. The expanding economy resulted in rising demands for residential housing, commercial office space and retail services. Between 1999 and 2009, sales tax receipts in Austin rose by approximately 31 percent, an indication of the dramatic increase in business activity during the period. The increases in population, income levels and sales tax revenues have been less dramatic over the last few years.

The following chart compares Austin’s five-county metro area population and median family income for 1989, 1999 and the most current information available for 2009 and 2010, based on U.S. Census Bureau data and City of Austin (the City) data.

Based on the City’s fiscal year of October 1st through September 30th, the chart below compares Austin’s sales tax revenues for 1989, 1999 and 2009 (the latest period for which data is available).

a. Source: Comprehensive Annual Financial Report for the City of Austin, Texas.

Real estate development in southwest Austin historically has been constrained as a result of various restrictions imposed by the City. Several special interest groups have also traditionally opposed development in that area, where most of our property is located. From 2001 through 2004, a downturn in the technology sector negatively affected the Austin real estate market, especially the high-end residential and commercial leasing markets; however, beginning in 2005 through mid-2007, market conditions improved. Beginning in the third quarter of 2007, market conditions began to weaken again. The December 31, 2010 and 2009 vacancy percentages for various types of developed properties in Austin are noted below.

|

December 31,

|

||||

|

2010

|

2009

|

|||

|

Building Type

|

Vacancy Factor

|

|||

|

Industrial Buildings

|

21% a

|

22% a

|

||

|

Office Buildings (Class A)

|

23% a

|

25% a

|

||

|

Multi-Family Buildings

|

7% b

|

10% b

|

||

|

Retail Buildings

|

7% b

|

9% b

|

||

|

a.

|

CB Richard Ellis: Austin MarketView

|

|

b.

|

Texas A&M University Real Estate Center: Texas Market News

|

Our financial condition and results of operations are highly dependent upon market conditions for real estate activity in Austin, Texas. Our future operating cash flows and, ultimately, our ability to develop our properties and expand our business will be largely dependent on the level of our real estate sales. In turn, these sales will be significantly affected by future real estate market conditions in Austin, Texas, including development costs, interest rate levels, the availability of credit to finance real estate transactions, demand for residential and commercial real estate, and regulatory factors including our land use and development entitlements.

During 2008 and 2009, economic conditions resulted in a general decline in leasing activity across the U.S., and caused vacancy rates to increase in most markets, including Austin, Texas. Investment sales activity in the U.S. declined sharply during 2008 because of, among other factors, limited availability and increased cost of financing, especially the absence of securitized debt, which was the source of the heightened investment

activity, and the resulting gap between buyer and seller expectations of value. Sales activity has yet to return to pre-2008 levels.

Periods of economic weakness or recession, significantly rising interest rates, declining employment levels, declining demand for real estate, declining real estate values, or the public perception that any of these events may occur, may negatively affect our business. These economic conditions can result in a general decline in acquisition, disposition and leasing activity, as well as a general decline in the value of real estate and in rents, which in turn reduces revenue derived from property sales and leases as well as revenues associated with development activities. In addition, these conditions can lead to a decline in property sales prices as well as a decline in funds invested in existing commercial real estate and related assets and properties planned for development.

Beginning in 2008, the credit markets experienced a disruption of a significant magnitude. This disruption reduced the availability and significantly increased the cost of most sources of funding. In some cases, these sources were eliminated. While the credit market has shown signs of improving since the second half of 2009, liquidity remains constrained and it is impossible to predict when the market will return to normalcy.

We continue to focus on our near-term goal of developing our properties and projects in an uncertain economic climate and our long-term goal of maximizing the value of our development projects. We believe that Austin, Texas, continues to be a desirable market and many of our developments are in locations that are unique and where approvals and entitlements, which we have already obtained, are increasingly difficult to secure. Real estate development in southwest Austin historically has been constrained as a result of various restrictions imposed by the City and several special interest groups have also traditionally opposed development in the area where most of our property is located. We believe that many of our developments have inherent value given their unique nature and location and that this value should be sustainable in the future.

Our long-term success will depend on our ability to maximize the value of our real estate by developing and selling our properties in a timely manner at a reasonable cost. In addition, we continue to pursue additional development opportunities, and currently believe that we can obtain financing necessary for developing our properties, although our ability to obtain financing in the future, as well as the cost of such financing, may be impacted by U.S. economic conditions. See “Risk Factors” located in Item 1A.

CRITICAL ACCOUNTING POLICIES

Management’s discussion and analysis of our financial condition and results of operations are based on our consolidated financial statements, which have been prepared in conformity with accounting principles generally accepted in the United States of America. The preparation of these statements requires that we make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses. We base these estimates on historical experience and on assumptions that we consider reasonable under the circumstances; however, reported results could differ from those based on the current estimates under different assumptions and/or conditions. The areas requiring the use of management’s estimates are discussed in Note 1 to our consolidated financial statements under the heading “Use of Estimates.” We believe that our most critical accounting policies relate to our real estate and commercial leasing assets, revenue recognition, deferred tax assets and our allocation of overhead costs.

Management has reviewed the following discussion of its development and selection of critical accounting estimates with the Audit Committee of our Board of Directors.

· Real Estate and Commercial Leasing Assets. Real estate held for sale is stated at the lower of cost or fair value less costs to sell. The cost of real estate sold includes acquisition, development, construction and carrying costs and other related costs through the development stage. Real estate under development and land held for future development are stated at cost. Commercial leasing assets, which are held for investment, are also stated at cost. When events or circumstances indicate that an asset’s carrying amount may not be recoverable, an impairment test is performed. For real estate held for sale, if estimated fair value less costs to sell is less than the related carrying amount, then a reduction of the asset’s carrying value to fair value less costs to sell is required. For real estate under development, land held for future development and real estate held for investment, if the projected undiscounted cash flow from the asset is less than the related carrying amount, then a reduction of the carrying amount of the asset to fair value is required. Measurement of the impairment loss is based on the fair value of the asset. Generally, we determine fair value using valuation techniques such as discounted expected future cash flows.

In developing estimated future cash flows for impairment testing for our real estate assets, we have incorporated our own market assumptions including those regarding real estate prices, sales pace, sales and marketing costs, infrastructure costs and financing costs regarding real estate assets. Our assumptions are based, in part, on general economic conditions, the current state of the real estate industry, expectations about the short- and long-term outlook for the real estate market, and competition from other developers in the area in which we develop our properties. These assumptions can significantly affect our estimates of future cash flows. For those properties held for sale and deemed to be impaired, we determine fair value based on appraised values, adjusted for estimated development costs and costs to sell, as we believe this is the value for which the property could be sold. We recorded no impairment losses during 2010 or 2009 (see Note 1).

The estimate of our future revenues is also important because it is the basis of our development plans and also a factor in our ability to obtain the financing necessary to complete our development plans. If our estimates of future cash flows from our properties differ from expectations, then our financial position and liquidity may be impacted, which could result in our default under certain debt instruments or result in our suspending some or all of our development activities.