Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-12019

QUAKER CHEMICAL CORPORATION

(Exact name of Registrant as specified in its charter)

| A Pennsylvania Corporation | No. 23-0993790 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| One Quaker Park, 901 E. Hector Street, Conshohocken, Pennsylvania |

19428-2380 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (610) 832-4000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each Exchange on which registered | |

| Common Stock, $1.00 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files) Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant. (The aggregate market value is computed by reference to the last reported sale on the New York Stock Exchange on June 30, 2010): $304,994,986

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock as of the latest practicable date: 11,506, 450 shares of Common Stock, $1.00 Par Value, as of February 28, 2011.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement relating to the Annual Meeting of Shareholders to be held on May 11, 2011 are incorporated by reference into Part III.

Table of Contents

PART I

As used in this Report, the terms “Quaker,” the “Company,” “we” and “our” refer to Quaker Chemical Corporation, its subsidiaries, and associated companies, unless the context otherwise requires.

| Item 1. | Business. |

General Description

Quaker develops, produces, and markets a broad range of formulated chemical specialty products for various heavy industrial and manufacturing applications and, in addition, offers and markets chemical management services (“CMS”). Quaker’s principal products and services include: (i) rolling lubricants (used by manufacturers of steel in the hot and cold rolling of steel and by manufacturers of aluminum in the hot rolling of aluminum); (ii) corrosion preventives (used by steel and metalworking customers to protect metal during manufacture, storage, and shipment); (iii) metal finishing compounds (used to prepare metal surfaces for special treatments such as galvanizing and tin plating and to prepare metal for further processing); (iv) machining and grinding compounds (used by metalworking customers in cutting, shaping, and grinding metal parts which require special treatment to enable them to tolerate the manufacturing process, achieve closer tolerance, and improve tool life); (v) forming compounds (used to facilitate the drawing and extrusion of metal products); (vi) hydraulic fluids (used by steel, metalworking, and other customers to operate hydraulically activated equipment); (vii) technology for the removal of hydrogen sulfide in various industrial applications; (viii) chemical milling maskants for the aerospace industry and temporary and permanent coatings for metal and concrete products; (ix) construction products, such as flexible sealants and protective coatings, for various applications; (x) specialty greases; and (xi) programs to provide chemical management services. Individual product lines representing more than 10% of consolidated revenues for any of the past three years are as follows:

| 2010 | 2009 | 2008 | ||||||||||

| Rolling lubricants |

21.2 | % | 20.8 | % | 19.7 | % | ||||||

| Machining and grinding compounds |

20.3 | % | 18.1 | % | 17.7 | % | ||||||

| Hydraulic fluids |

13.7 | % | 12.9 | % | 11.1 | % | ||||||

| Corrosion preventives |

11.5 | % | 9.9 | % | 10.2 | % | ||||||

| Chemical management services |

3.5 | % | 8.4 | % | 11.1 | % | ||||||

A substantial portion of Quaker’s sales worldwide are made directly through its own employees and its CMS programs with the balance being handled through value-added resellers and agents. Quaker employees visit the plants of customers regularly and, through training and experience, identify production needs which can be resolved or alleviated either by adapting Quaker’s existing products or by applying new formulations developed in Quaker’s laboratories. Quaker makes little use of advertising but relies heavily upon its reputation in the markets which it serves. Generally, separate manufacturing facilities of a single customer are served by different personnel. As part of the Company’s chemical management services, certain third-party product sales to customers are managed by the Company. Where the Company acts as principal, revenues are recognized on a gross reporting basis at the selling price negotiated with the customers. Where the Company acts as an agent, such revenue is recorded using net reporting as service revenues at the amount of the administrative fee earned by the Company for ordering the goods. Third-party products transferred under arrangements resulting in net reporting totaled $56.5 million, $27.5 million and $32.2 million for 2010, 2009 and 2008, respectively. The Company recognizes revenue in accordance with the terms of the underlying agreements, when title and risk of loss have been transferred, collectability is reasonably assured, and pricing is fixed or determinable. This generally occurs for product sales when products are shipped to customers or, for consignment arrangements, upon usage by the customer and when services are performed. License fees and royalties are recognized in accordance with agreed-upon terms, when performance obligations are satisfied, the amount is fixed or determinable, and collectability is reasonably assured, and are included in other income.

1

Table of Contents

In 2010, the Company completed the acquisition of D.A. Stuart’s U.S. aluminum hot rolling oil business from Houghton International for approximately $6.8 million. With this acquisition, Quaker became a leading player in the U.S. aluminum hot rolling market. The Company also completed the acquisition of Summit Lubricants Inc., a leading specialty grease manufacturer and distributor of specialty greases, for approximately $29.1 million. This acquisition is complementary to the Company’s existing business lines and the purchase price approximates expected 2011 sales.

Competition

The chemical specialty industry comprises a number of companies of similar size as well as companies larger and smaller than Quaker. Quaker cannot readily determine its precise position in every industry it serves. Based on information available to Quaker, however, it is estimated that Quaker holds a leading and significant global position (among a group in excess of 25 other suppliers) in the market for process fluids to produce sheet steel. It is also believed that Quaker holds significant global positions in the markets for process fluids in portions of the automotive and industrial markets. The offerings of many of our competitors differ from Quaker, with some who offer a broad portfolio of fluids including general lubricants to those who have a more specialized product range and all of whom provide different levels of technical services to individual customers. Competition in the industry is based primarily on the ability to provide products that meet the needs of the customer and render technical services and laboratory assistance to customers and, to a lesser extent, on price.

Major Customers and Markets

In 2010, Quaker’s five largest customers (each composed of multiple subsidiaries or divisions with semi-autonomous purchasing authority) accounted for approximately 20% of its consolidated net sales with the largest customer (Arcelor-Mittal Group) accounting for approximately 9% of consolidated net sales. A significant portion of Quaker’s revenues are realized from the sale of process fluids and services to manufacturers of steel, automobiles, appliances, and durable goods, and, therefore, Quaker is subject to the same business cycles as those experienced by these manufacturers and their customers. Furthermore, steel customers typically have limited manufacturing locations as compared to metalworking customers and generally use higher volumes of products at a single location. Accordingly, the loss or closure of a steel mill or other major customer site can have a material adverse effect on Quaker’s business.

Raw Materials

Quaker uses over 1,000 raw materials, including mineral oils and derivatives, animal fats and derivatives, vegetable oils and derivatives, ethylene derivatives, solvents, surface active agents, chlorinated paraffinic compounds, and a wide variety of other organic and inorganic compounds. In 2010, three raw material groups (mineral oils and derivatives, animal fats and derivatives, and vegetable oils and derivatives) each accounted for as much as 10% of the total cost of Quaker’s raw material purchases. The price of mineral oil can be affected by the price of crude oil and refining capacity. In addition, animal fat and vegetable oil prices are impacted by increased biodiesel consumption. Accordingly, significant fluctuations in the price of crude oil can have a material effect upon the Company’s business. Many of the raw materials used by Quaker are “commodity” chemicals, and, therefore, Quaker’s earnings can be affected by market changes in raw material prices. Reference is made to the disclosure contained in Item 7A of this Report.

Patents and Trademarks

Quaker has a limited number of patents and patent applications, including patents issued, applied for, or acquired in the United States and in various foreign countries, some of which may prove to be material to its business. Principal reliance is placed upon Quaker’s proprietary formulae and the application of its skills and experience to meet customer needs. Quaker’s products are identified by trademarks that are registered throughout its marketing area.

2

Table of Contents

Research and Development—Laboratories

Quaker’s research and development laboratories are directed primarily toward applied research and development since the nature of Quaker’s business requires continual modification and improvement of formulations to provide chemical specialties to satisfy customer requirements. Quaker maintains quality control laboratory facilities in each of its manufacturing locations. In addition, Quaker maintains in Conshohocken, Pennsylvania, Santa Fe Springs, California, Uithoorn, The Netherlands and Qingpu, China laboratory facilities that are devoted primarily to applied research and development.

Research and development costs are expensed as incurred. Research and development expenses during 2010, 2009 and 2008 were $15.7 million, $15.0 million and $16.9 million, respectively.

Most of Quaker’s subsidiaries and associated companies also have laboratory facilities. Although not as complete as the Conshohocken, Santa Fe Springs, Uithoorn or Qingpu laboratories, these facilities are generally sufficient for the requirements of the customers being served. If problems are encountered which cannot be resolved by local laboratories, such problems may be referred to the laboratory staff in Conshohocken or Uithoorn.

Regulatory Matters

In order to facilitate compliance with applicable Federal, state, and local statutes and regulations relating to occupational health and safety and protection of the environment, the Company has an ongoing program of site assessment for the purpose of identifying capital expenditures or other actions that may be necessary to comply with such requirements. The program includes periodic inspections of each facility by Quaker and/or independent experts, as well as ongoing inspections and training by on-site personnel. Such inspections address operational matters, record keeping, reporting requirements and capital improvements. In 2010, capital expenditures directed solely or primarily to regulatory compliance amounted to approximately $0.7 million compared to $0.7 million and $1.7 million in 2009 and 2008, respectively. In 2011, the Company expects to incur approximately $1.9 million for capital expenditures directed primarily to regulatory compliance.

Number of Employees

On December 31, 2010, Quaker’s consolidated companies had 1,385 full-time employees of whom 513 were employed by the parent company and its U.S. subsidiaries and 872 were employed by its non-U.S. subsidiaries. Associated companies of Quaker (in which it owns 50% or less) employed 225 people on December 31, 2010.

Product Classification

The Company organizes its segments by type of product sold. The Company’s reportable segments are as follows:

(1) Metalworking process chemicals—industrial process fluids for various heavy industrial and manufacturing applications.

(2) Coatings—temporary and permanent coatings for metal and concrete products and chemical milling maskants.

(3) Other chemical products—other various chemical products.

Incorporated by reference is the segment information contained in Note 17 of Notes to Consolidated Financial Statements included in Item 8 of this Report.

3

Table of Contents

Non-U.S. Activities

Since significant revenues and earnings are generated by non-U.S. operations, Quaker’s financial results are affected by currency fluctuations, particularly between the U.S. Dollar, the E.U. Euro, the Brazilian Real, and the Chinese Renminbi, and the impact of those currency fluctuations on the underlying economies. Incorporated by reference is (i) the foreign exchange risk information contained in Item 7A of this Report, (ii) the geographic information in Note 17 of Notes to Consolidated Financial Statements included in Item 8 of this Report, and (iii) information regarding risks attendant to foreign operations included in Item 1A of this Report.

Quaker on the Internet

Financial results, news and other information about Quaker can be accessed from the Company’s Web site at http://www.quakerchem.com. This site includes important information on products and services, financial reports, news releases, and career opportunities. The Company’s periodic and current reports on Forms 10-K, 10-Q and 8-K, including exhibits and supplemental schedules filed therewith, and amendments to those reports, filed with the Securities and Exchange Commission (“SEC”) are available on the Company’s Web site, free of charge, as soon as reasonably practicable after they are electronically filed with or furnished to the SEC. Information contained on, or that may be accessed through, the Company’s Web site is not incorporated by reference in this Report and, accordingly, you should not consider that information part of this Report.

Factors that May Affect Our Future Results

(Cautionary Statements under the Private Securities Litigation Reform Act of 1995)

Certain information included in this Report and other materials filed or to be filed by Quaker with the SEC (as well as information included in oral statements or other written statements made or to be made by us) contain or may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements can be identified by the fact that they do not relate strictly to historical or current facts. We have based these forward-looking statements on our current expectations about future events. These forward-looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, intentions, financial condition, results of operations, future performance, and business, including:

| • | statements relating to our business strategy; |

| • | our current and future results and plans; and |

| • | statements that include the words “may,” “could,” “should,” “would,” “believe,” “expect,” “anticipate,” “estimate,” “intend,” “plan” or similar expressions. |

Such statements include information relating to current and future business activities, operational matters, capital spending, and financing sources. From time to time, oral or written forward-looking statements are also included in Quaker’s periodic reports on Forms 10-Q and 8-K, press releases, and other materials released to, or statements made to, the public.

Any or all of the forward-looking statements in this Report, in Quaker’s Annual Report to Shareholders for 2010, and in any other public statements we make may turn out to be wrong. This can occur as a result of inaccurate assumptions or as a consequence of known or unknown risks and uncertainties. Many factors discussed in this Report will be important in determining our future performance. Consequently, actual results may differ materially from those that might be anticipated from our forward-looking statements.

We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise. However, any further disclosures made on related subjects in Quaker’s subsequent reports on Forms 10-K, 10-Q and 8-K should be consulted. These forward-looking statements are subject to risks, uncertainties and assumptions about us and our operations that are subject to change based on various important factors, some of which are beyond our control. A major risk is that the demand for the Company’s

4

Table of Contents

products and services is largely derived from the demand for its customers’ products, which subjects the Company to uncertainties related to downturns in a customer’s business and unanticipated customer production shutdowns. Other major risks and uncertainties include, but are not limited to, significant increases in raw material costs, worldwide economic and political conditions, foreign currency fluctuations, and terrorist attacks such as those that occurred on September 11, 2001, each of which is discussed in greater detail in Item 1A of this Report. Furthermore, the Company is subject to the same business cycles as those experienced by steel, automobile, aircraft, appliance, and durable goods manufacturers. These risks, uncertainties, and possible inaccurate assumptions relevant to our business could cause our actual results to differ materially from expected and historical results. Other factors beyond those discussed in this Report could also adversely affect us. Therefore, we caution you not to place undue reliance on our forward-looking statements. This discussion is provided as permitted by the Private Securities Litigation Reform Act of 1995.

| Item 1A. | Risk Factors. |

Changes to the industries and markets that Quaker serves could have a material adverse effect on the Company’s liquidity, financial position and results of operations.

The chemical specialty industry comprises a number of companies of similar size as well as companies larger and smaller than Quaker. It is estimated that Quaker holds a leading and significant global position in the markets for process fluids to produce sheet steel and significant global positions in portions of the automotive and industrial markets. The industry is highly competitive, and a number of companies with significant financial resources and/or customer relationships compete with us to provide similar products and services. Our competitors may be positioned to offer more favorable pricing and service terms, resulting in reduced profitability and loss of market share for us. Historically, competition in the industry has been based primarily on the ability to provide products that meet the needs of the customer and render technical services and laboratory assistance to the customer and, to a lesser extent, on price. Factors critical to the Company’s business include successfully differentiating the Company’s offering from its competition, operating efficiently and profitably as a globally integrated whole, and increasing market share and customer penetration through internally developed business programs and strategic acquisitions.

The business environment in which the Company operates remains uncertain. The Company is subject to the same business cycles as those experienced by steel, automobile, aircraft, appliance, and durable goods manufacturers. A major risk is that the Company’s demand is largely derived from the demand for its customers’ products, which subjects the Company to uncertainties related to downturns in our customers’ business and unanticipated customer production shutdowns or curtailments. The Company has limited ability to adjust its cost level contemporaneously with changes in sales and gross margins. Thus, a significant downturn in sales or gross margins due to weak end-user markets, loss of a significant customer, and/or rising raw material costs could have a material adverse effect on the Company’s liquidity, financial position, and results of operations.

Our business depends on attracting and retaining qualified management personnel.

The unanticipated departure of any key member of our management team could have an adverse effect on our business. Given the relative size of the Company and the breadth of its global operations, there are a limited number of qualified management personnel to assume the responsibilities of management level employees should there be management turnover. In addition, because of the specialized and technical nature of our business, our future performance is dependent on the continued service of, and our ability to attract and retain, qualified management, commercial and technical personnel. Competition for such personnel is intense, and we may be unable to continue to attract or retain such personnel.

Inability to obtain sufficient price increases or contract concessions to offset increases in the costs of raw material could have a material adverse effect on the Company’s liquidity, financial position and results of operations. Price increases implemented could result in the loss of sales.

Quaker uses over 1,000 raw materials, including mineral oils and derivatives, animal fats and derivatives, vegetable oils and derivatives, ethylene derivatives, solvents, surface active agents, chlorinated paraffinic

5

Table of Contents

compounds, and a wide variety of other organic and inorganic compounds. In 2010, three raw material groups (mineral oils and derivatives, animal fats and derivatives, and vegetable oils and derivatives) each accounted for as much as 10% of the total cost of Quaker’s raw material purchases. The price of mineral oil can be affected by the price of crude oil and refining capacity. In addition, many of the raw materials used by Quaker are “commodity” chemicals. Accordingly, Quaker’s earnings can be affected by market changes in raw material prices.

Over the past three years, Quaker has experienced significant volatility in its raw material costs, particularly crude oil derivatives. For example, the price of crude oil averaged $79 per barrel in 2010 versus $61 in 2009 and $100 in 2008 and is currently trading in the $100 per barrel range with market conditions that currently reflect the political instability in the Middle East. In addition, refining capacity has also been constrained by various factors, which further contributed to volatile raw material costs and negatively impacted margins. Animal fat and vegetable oil prices have been impacted by increased biodiesel consumption. In response, the Company has aggressively pursued price increases to offset the increased raw material costs. Although the Company has been successful in recovering a substantial amount of the raw material cost increases, it has experienced competitive as well as contractual constraints limiting pricing actions. In addition, as a result of the Company’s pricing actions, customers may become more likely to consider competitors’ products, some of which may be available at a lower cost. Significant loss of customers could result in a material adverse effect on the Company’s results of operations.

Availability of raw materials, including sourcing from some single suppliers, could have a material adverse effect on the Company’s liquidity, financial position and results of operations.

The chemical specialty industry can experience some tightness of supply of certain raw materials. In addition, in some cases, we choose to source from a single supplier. Any significant disruption in supply could affect our ability to obtain raw materials, which could have a material adverse effect on our liquidity, financial position and results of operations.

Loss of a significant manufacturing facility may materially and adversely affect the Company’s liquidity, financial position and results of operations.

Quaker has multiple manufacturing facilities throughout the world. In certain countries such as Brazil and China, there is only one such facility. If one of the Company’s facilities was damaged to such extent that production was halted for an extended period, the Company may not be able to timely supply affected customers. This could result in a loss of sales over an extended period or permanently. The Company does take steps to mitigate against this risk including contingency planning and procuring property and casualty insurance (including business interruption insurance). Nevertheless, the loss of sales in any one region over any extended period of time could have a significant material adverse effect on Quaker’s liquidity, financial position and results of operations.

Bankruptcy of a significant customer could have a material adverse effect on our liquidity, financial position and results of operations.

A significant portion of Quaker’s revenues is derived from sales to customers in the U.S. steel and automotive industries, including some of our larger customers, where a number of bankruptcies occurred during recent years and companies have experienced financial difficulties. As part of the bankruptcy process, the Company’s pre-petition receivables may not be realized, customer manufacturing sites may be closed or contracts voided. The bankruptcy of a major customer could have a material adverse effect on the Company’s liquidity, financial position, and results of operations. Steel customers typically have limited manufacturing locations as compared to metalworking customers and generally use higher volumes of products at a single location. The loss or closure of a steel mill or other major site of a significant customer could have a material adverse effect on Quaker’s business.

During 2010, our five largest customers (each composed of multiple subsidiaries or divisions with semi-autonomous purchasing authority) together accounted for approximately 20% of our consolidated net sales with the largest customer (Arcelor-Mittal Group) accounting for approximately 9% of consolidated net sales.

6

Table of Contents

Failure to comply with any material provision of our credit facility or other debt agreements could have a material adverse effect on our liquidity, financial position and results of operations.

The Company maintains a $175.0 million unsecured credit facility (the “Credit Facility”) with a group of lenders, which can be increased to $225.0 million at the Company’s option if lenders agree to increase their commitments and the Company satisfies certain conditions. The Credit Facility, which matures in 2014, provides the availability of revolving credit borrowings. In general, the borrowings under the Credit Facility bear interest at either a base rate or LIBOR rate plus a margin based on the Company’s consolidated leverage ratio.

The Credit Facility contains limitations on capital expenditures, investments, acquisitions and liens, as well as default provisions customary for facilities of its type. While these covenants and restrictions are not currently considered to be overly restrictive, they could become more difficult to comply with as our business or financial conditions change. In addition, deterioration in the Company’s results of operations or financial position could significantly increase borrowing costs.

Quaker is exposed to market rate risk for changes in interest rates, due to the variable interest rate applied to the Company’s borrowings under its Credit Facility. Accordingly, if interest rates rise significantly, the cost of debt to Quaker will increase, perhaps significantly, depending on the extent of Quaker’s borrowings under the Credit Facility. At December 31, 2010, the Company had $55.0 million outstanding under its credit facilities. The Company has entered into interest rate swaps in order to fix a portion of its variable rate debt and mitigate the risks associated with higher interest rates. The combined notional value of the swaps was $15.0 million at December 31, 2010.

Failure to generate taxable income could have a material adverse effect on our financial position and results of operations.

At December 31, 2010, the Company had net U.S. deferred tax assets totaling $14.8 million, excluding deferred tax assets relating to additional minimum pension liabilities. In addition, at that date, the Company had $2.1 million in operating loss carryforwards primarily related to certain of its foreign operations. The Company records valuation allowances when necessary to reduce its deferred tax assets to the amount that is more likely than not to be realized. The Company considers future taxable income and ongoing prudent and feasible tax planning strategies in assessing the need for a valuation allowance. However, in the event the Company were to determine that it would not be able to realize all or part of its net deferred tax assets in the future, an adjustment to the deferred tax asset would be a non-cash charge to income in the period such determination was made, which could have a material adverse effect on the Company’s financial statements. The Company continues to closely monitor this situation as it relates to its net deferred tax assets and the assessment of valuation allowances.

Environmental laws and regulations and pending legal proceedings may materially and adversely affect the Company’s liquidity, financial position and results of operations.

The Company is a party to proceedings, cases, and requests for information from, and negotiations with, various claimants and Federal and state agencies relating to various matters, including environmental matters. An adverse result in one or more matters could materially and adversely affect the Company’s liquidity, financial position and results of operations. Incorporated herein by reference is the information concerning pending asbestos-related litigation against an inactive subsidiary and amounts accrued associated with certain environmental non-capital remediation costs in Note 22 of Notes to Consolidated Financial Statements which appears in Item 8 of this Report.

Climate change and greenhouse gas restrictions may materially affect the Company’s liquidity, financial position and results of operations.

The Company is subject to various regulations regarding its emission of greenhouse gases in its manufacturing facilities. In addition, a number of countries have adopted, or are considering the adoption of

7

Table of Contents

regulatory frameworks to reduce greenhouse gas emissions. These include adoption of cap and trade regimes, carbon taxes, increased efficiency standards and incentives or mandates for renewable energy. These requirements could make our products more expensive and reduce demand for our products. Current and pending greenhouse gas regulations may also increase our compliance costs.

We might not be able to timely develop, manufacture and gain market acceptance of new and enhanced products required to maintain or expand our business.

We believe that our continued success depends on our ability to continuously develop and manufacture new products and product enhancements on a timely and cost-effective basis, in response to customers’ demands for higher performance process chemicals, coatings and other chemical products. Our competitors may develop new products or enhancements to their products that offer performance, features and lower prices that may render our products less competitive or obsolete and, as a consequence, we may lose business and/or significant market share. The development and commercialization of new products require significant expenditures over an extended period of time, and some products that we seek to develop may never become profitable. In addition, we may not be able to develop and introduce products incorporating new technologies in a timely manner that will satisfy our customers’ future needs or achieve market acceptance.

The scope of our international operations subjects the Company to risks, including risks from changes in trade regulations, currency fluctuations, and political and economic instability.

Since significant revenues and earnings are generated by non-U.S. operations, Quaker’s financial results are affected by currency fluctuations, particularly between the U.S. Dollar, the E.U. Euro, the Brazilian Real, and the Chinese Renminbi, and the impact of those currency fluctuations on the underlying economies. During the past three years, sales by non-U.S. subsidiaries accounted for approximately 59% to 65% of our annual consolidated net sales. All of these operations use the local currency as their functional currency. The Company generally does not use financial instruments that expose it to significant risk involving foreign currency transactions; however, the size of non-U.S. activities has a significant impact on reported operating results and attendant net assets. Therefore, as exchange rates vary, Quaker’s results can be materially affected. Incorporated by reference is the foreign exchange risk information contained in Item 7A of this Report and the geographic information in Note 17 of Notes to Consolidated Financial Statements included in Item 8 of this Report.

Additional risks associated with the Company’s international operations include, but are not limited to, the following:

| • | changes in economic conditions from country to country, |

| • | changes in a country’s political condition, such as the current political unrest in the Middle East, |

| • | trade protection measures, |

| • | licensing and other legal requirements, |

| • | longer payment cycles in certain foreign markets, |

| • | restrictions on the repatriation of our assets, including cash, |

| • | significant foreign and United States taxes on repatriated cash, |

| • | the difficulties of staffing and managing dispersed international operations, |

| • | less protective foreign intellectual property laws, |

| • | legal systems that may be less developed and predictable than those in the United States, and |

| • | local tax issues. |

8

Table of Contents

The breadth of Quaker’s international operations subjects the Company to various local non-income taxes, including value-added-taxes (“VAT”). With VAT, the Company essentially operates as an agent for various jurisdictions by collecting VAT from customers and remitting those amounts to the taxing authorities on the goods it sells. The laws and regulations regarding VAT can be complex and vary widely among countries as well as among individual states within a given country for the same products, making full compliance difficult. As VAT is often charged as a percentage of the selling price of the goods sold, the amounts involved can be material. Should there be non-compliance by the Company, it may need to remit funds to the tax authorities prior to collecting the appropriate amounts from customers or jurisdictions which may have been incorrectly paid. In addition, the Company may choose for commercial reasons not to seek repayment from certain customers. This could have a material adverse affect on the Company’s liquidity, financial position and results of operations. Refer to Note 22 of Notes to Consolidated Financial Statements, included in Item 8 of this Report, which is incorporated herein by this reference, for further discussion.

Terrorist attacks, other acts of violence or war may affect the markets in which we operate and our profitability.

Terrorist attacks may negatively affect our operations. There can be no assurance that there will not be further terrorist attacks against the U.S. or U.S. businesses. Terrorist attacks, other acts of violence or armed conflicts may directly impact our physical facilities or those of our suppliers or customers. Additional terrorist attacks may disrupt the global insurance and reinsurance industries with the result that we may not be able to obtain insurance at historical terms and levels for all of our facilities. Furthermore, any of these events may make travel and the transportation of our supplies and products more difficult and more expensive and ultimately affect the sales of our products. The consequences of terrorist attacks, other acts of violence or armed conflicts can be unpredictable, and we may not be able to foresee events that could have an adverse effect on our business.

| Item 1B. | Unresolved Staff Comments. |

None.

| Item 2. | Properties. |

Quaker’s corporate headquarters and a laboratory facility are located in Conshohocken, Pennsylvania. Quaker’s other principal facilities are located in Detroit, Michigan; Middletown, Ohio; Santa Fe Springs, California; Batavia, New York; Uithoorn, The Netherlands; Santa Perpetua de Mogoda, Spain; Rio de Janeiro, Brazil; Tradate, Italy; and Qingpu, China. All of the properties except that in Santa Fe Springs, California are used by the metalworking process chemicals segment. The Santa Fe Springs, California property is used by the coatings segment. With the exception of the Conshohocken, Santa Fe Springs and Tradate sites, which are leased, all of these principal facilities are owned by Quaker and as of December 31, 2010 were mortgage free. Quaker also leases sales, laboratory, manufacturing, and warehouse facilities in other locations.

Quaker’s principal facilities (excluding Conshohocken) consist of various manufacturing, administrative, warehouse, and laboratory buildings. Substantially all of the buildings (including Conshohocken) are of fire-resistant construction and are equipped with sprinkler systems. All facilities are primarily of masonry and/or steel construction and are adequate and suitable for Quaker’s present operations. The Company has a program to identify needed capital improvements that are implemented as management considers necessary or desirable. Most locations have various numbers of raw material storage tanks ranging from 18 to 58 at each location with a capacity ranging from 1,000 to 82,000 gallons and processing or manufacturing vessels ranging in capacity from 7 to 16,000 gallons.

Each of Quaker’s 50% or less owned non-U.S. associated companies owns or leases a plant and/or sales facilities in various locations.

9

Table of Contents

| Item 3. | Legal Proceedings. |

The Company is a party to proceedings, cases, and requests for information from, and negotiations with, various claimants and Federal and state agencies relating to various matters, including environmental matters. For information concerning pending asbestos-related litigation against an inactive subsidiary, amounts accrued associated with certain environmental non-capital remediation costs and the Company’s value-added-tax dispute settlements, reference is made to Note 22 of Notes to Consolidated Financial Statements, included in Item 8 of this Report, which is incorporated herein by this reference. The Company is a party to other litigation which management currently believes will not have a material adverse effect on the Company’s results of operations, cash flow, or financial condition.

| Item 4. | [Reserved] |

| Item 4(a). | Executive Officers of the Registrant. |

Set forth below is information regarding the executive officers of the Company, each of whom (with the exception of Mr. Claro) has been employed by the Company for more than five years, including the respective positions and offices with the Company held by each over the respected periods indicated. Each of the executive officers, with the exception of Mr. Hill, is elected annually to a one-year term. Mr. Hill is considered an executive officer in his capacity as principal accounting officer for purposes of this item.

| Name, Age, and Present Position with the Company |

Business Experience During Past Five Years and Period Served as an Officer | |

| Michael F. Barry, 52 Chairman of the Board, Chief Executive Officer and President and Director |

Mr. Barry, who has been employed by the Company since 1998, has served as Chairman of the Board since May 13, 2009, in addition to his position as Chief Executive Officer and President held since October 2008. He served as Senior Vice President and Managing Director—North America from January 2006 to October 2008. He served as Senior Vice President and Global Industry Leader—Metalworking and Coatings from July 2005 through December 2005. He served as Vice President and Global Industry Leader—Industrial Metalworking and Coatings from July 2005 through December 2005 and Vice President and Chief Financial Officer from 1998 to August 2004. | |

| Mark A. Featherstone, 49 Vice President, Chief Financial Officer and Treasurer |

Mr. Featherstone, who has been employed by the Company since 2001, has served as Chief Financial Officer and Treasurer since April 2007 and has served as Vice President since March 2005. He served as Global Controller from May 2001 to April 2007. | |

| D. Jeffry Benoliel, 52 Vice President-Global Strategy, |

Mr. Benoliel, who has been employed by the Company since 1995, has served as Vice President-Global Strategy, General Counsel and Corporate Secretary since October 2008. He served as Vice President, Secretary and General Counsel from 2001 through September 2008. | |

10

Table of Contents

| Name, Age, and Present Position with the Company |

Business Experience During Past Five Years and Period Served as an Officer | |

| Joseph A. Berquist, 39 Vice President and Managing Director—North America |

Mr. Berquist, who has been employed by the Company since 1997, was elected as Vice President and Managing Director—North America on April 1, 2010. He served as Senior Director, North America Commercial from October 2008 through March 2010, as Industry Business Director—Metalworking/Fluid Power from July 2006 through September 2008 and as Industry Business Manager—Metalworking/Fluid Power from January 2006 until July 2006. He served as Regional Sales Manager—Metalworking from November 2004 through December 2005. | |

| Jose Luiz Bregolato, 65 Vice President and Managing Director— |

Mr. Bregolato, who has been employed by the Company since 1994, has served in his current position since 1994. | |

| Carlos Claro, 49 Vice President |

Mr. Claro joined the Company on February 1, 2011 as Vice President. Prior to joining the Company, Mr. Claro was Americas Business Director at Cytec Industries, a specialty chemicals and materials technology company, responsible for the Powder Coating Resins business from April 2008 through January 2011. He served as Latin America Resins Commercial Director and Country Manager—Brazil at Cytec Industries from June 2005 until April 2008. | |

| George H. Hill, 36 Global Controller |

Mr. Hill, who has been employed by the Company since 2002, has served in his current position since April 2007. He served as Assistant Global Controller from May 2004 until April 2007. | |

| Joseph F. Matrange, 69 Vice President—Global Coatings |

Mr. Matrange, who has been employed by the Company since 2001, has served as Vice President—Global Coatings since October 2008. He has also served as President of AC Products, Inc., a California subsidiary, since October 2000, and Epmar Corporation, a California subsidiary, since April 2002. | |

| Jan F. Nieman, 50 Vice President and Managing Director— |

Mr. Nieman, who has been employed by the Company since 1992, has served as Vice President since February 2005, and has served in the position of Managing Director, Asia/Pacific since August 2003. | |

| Wilbert Platzer, 49 Vice President and Managing Director—Europe |

Mr. Platzer, who has been employed by the Company since 1995, has served in his current position since January 2006. He served as Vice President—Global Industrial Metalworking from July 2005 through December 2005 and served as Vice President—Worldwide Operations from January 2001 through June 2005. | |

11

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

The Company’s common stock is listed on the New York Stock Exchange (“NYSE”) under the trading symbol KWR. The following table sets forth, for the calendar quarters during the past two most recent fiscal years, the range of high and low sales prices for the common stock as reported on the NYSE composite tape (amounts rounded to the nearest penny), and the quarterly dividends declared and paid:

| Price Range | Dividends Declared |

Dividends Paid |

||||||||||||||||||||||||||||||

| 2010 | 2009 | |||||||||||||||||||||||||||||||

| High | Low | High | Low | 2010 | 2009 | 2010 | 2009 | |||||||||||||||||||||||||

| First quarter |

$ | 27.71 | $ | 16.14 | $ | 16.53 | $ | 4.65 | $ | 0.23 | $ | — | $ | 0.23 | $ | 0.23 | ||||||||||||||||

| Second quarter |

36.49 | 22.55 | 15.25 | 7.60 | 0.235 | 0.46 | 0.23 | 0.23 | ||||||||||||||||||||||||

| Third quarter |

38.16 | 24.64 | 23.20 | 11.97 | 0.235 | 0.23 | 0.235 | 0.23 | ||||||||||||||||||||||||

| Fourth quarter |

45.80 | 32.30 | 23.82 | 17.18 | 0.235 | 0.23 | 0.235 | 0.23 | ||||||||||||||||||||||||

There are no restrictions that currently materially limit the Company’s ability to pay dividends or that the Company believes are likely to materially limit the future payment of dividends. If a default under the Company’s primary credit facility were to occur and continue, the payment of dividends would be prohibited. Reference is made to the “Liquidity and Capital Resources” disclosure contained in Item 7 of this Report.

As of January 17, 2011, there were 1,020 shareholders of record of the Company’s common stock, its only outstanding class of equity securities.

Every holder of Quaker common stock is entitled to one vote or ten votes for each share held of record on any record date depending on how long each share has been held. As of January 17, 2011, 11,494,448 shares of Quaker common stock were issued and outstanding. Based on the information available to the Company on January 17, 2011, as of that date the holders of 871,597 shares of Quaker common stock would have been entitled to cast ten votes for each share, or approximately 45% of the total votes that would have been entitled to be cast as of that record date and the holders of 10,622,851 shares of Quaker common stock would have been entitled to cast one vote for each share, or approximately 55% of the total votes that would have been entitled to be cast as of that date. The number of shares that are indicated as entitled to one vote includes those shares presumed to be entitled to only one vote. Because the holders of these shares may rebut this presumption, the total number of votes entitled to be cast as of January 17, 2011 could be more than 19,338,821.

Reference is made to the information in Item 12 of this Report under the caption “Equity Compensation Plans,” which is incorporated herein by this reference.

12

Table of Contents

The following table sets forth information concerning shares of the Company’s common stock acquired by the Company during the fourth quarter of the fiscal year covered by this Report, all of which were acquired from employees in payment of the exercise price of employee stock options exercised during the period.

Issuer Purchases of Equity Securities

| Period |

(a) Total Number of Shares Purchased (1) |

(b) Average Price Paid per Share (2) |

(c) Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (3) |

(d) Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (3) |

||||||||||||

| October 1 – October 31 |

— | $ | — | — | 252,600 | |||||||||||

| November 1 – November 30 |

30,039 | $ | 38.06 | — | 252,600 | |||||||||||

| December 1 – December 31 |

— | $ | — | — | 252,600 | |||||||||||

| Total |

30,039 | $ | 38.06 | — | 252,600 | |||||||||||

| (1) | All of the 30,039 shares acquired by the Company during the period covered by this report were acquired from employees upon their surrender of previously owned shares in payment of the exercise price of employee stock options. |

| (2) | The price paid per share, in each case, represents either a) the average of the high and low price of the Company’s common stock on the date of exercise; or b) the closing price of the Company’s common stock on date of exercise, as specified by the plan pursuant to which the applicable option was granted. |

| (3) | On February 15, 1995, the Board of Directors of the Company authorized a share repurchase program authorizing the repurchase of up to 500,000 shares of Quaker common stock, and, on January 26, 2005, the Board authorized the repurchase of up to an additional 225,000 shares. Under the 1995 action of the Board, 27,600 shares may yet be purchased. Under the 2005 action of the Board, none of the shares authorized has been purchased and, accordingly, all of those shares may yet be purchased. Neither of the share repurchase authorizations has an expiration date. |

13

Table of Contents

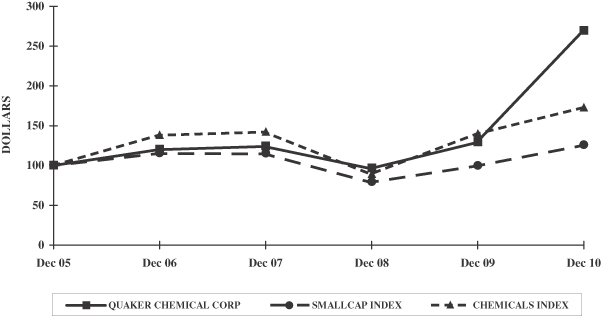

The following graph compares the cumulative total return (assuming reinvestment of dividends) from December 31, 2005 to December 31, 2010 for (i) Quaker’s common stock, (ii) the S&P SmallCap 600 Stock Index (the “SmallCap Index”) and (iii) the S&P Chemicals (Specialty) Index-SmallCap (the “Chemicals Index”). The graph assumes the investment of $100 on December 31, 2005 in each of Quaker’s common stock, the stocks comprising the SmallCap Index, and the stocks comprising the Chemicals Index.

COMPARISON OF CUMULATIVE FIVE–YEAR TOTAL RETURN

| 12/31/2005 | 12/31/2006 | 12/31/2007 | 12/31/2008 | 12/31/2009 | 12/31/2010 | |||||||||||||||||||

| Quaker |

$ | 100.00 | $ | 119.89 | $ | 124.06 | $ | 96.46 | $ | 128.93 | $ | 269.14 | ||||||||||||

| SmallCap Index |

100.00 | 115.12 | 114.78 | 79.11 | 99.34 | 125.47 | ||||||||||||||||||

| Chemicals Index |

100.00 | 138.28 | 142.16 | 89.29 | 139.86 | 172.90 | ||||||||||||||||||

14

Table of Contents

| Item 6. | Selected Financial Data. |

The following table sets forth selected financial information for the Company and its consolidated subsidiaries:

| Year Ended December 31, | ||||||||||||||||||||

| 2010 (1) | 2009 (2) | 2008 (3) | 2007 (4) | 2006 | ||||||||||||||||

| (In thousands, except per share amounts) | ||||||||||||||||||||

| Summary of Operations: |

||||||||||||||||||||

| Net sales |

$ | 544,063 | $ | 451,490 | $ | 581,641 | $ | 545,597 | $ | 460,451 | ||||||||||

| Income before taxes, equity income and noncontrolling interest |

46,213 | 23,692 | 16,629 | 22,735 | 18,440 | |||||||||||||||

| Net income attributable to Quaker Chemical Corporation |

31,807 | 16,220 | 11,132 | 15,471 | 11,667 | |||||||||||||||

| Per share: |

||||||||||||||||||||

| Net income attributable to Quaker Chemical Corporation Common Shareholders—basic |

$ | 2.82 | $ | 1.48 | $ | 1.06 | $ | 1.53 | $ | 1.18 | ||||||||||

| Net income attributable to Quaker Chemical Corporation Common Shareholders—diluted |

$ | 2.77 | $ | 1.47 | 1.05 | 1.52 | 1.18 | |||||||||||||

| Dividends declared |

0.935 | 0.92 | 0.92 | 0.86 | 0.86 | |||||||||||||||

| Dividends paid |

0.93 | 0.92 | 0.905 | 0.86 | 0.86 | |||||||||||||||

| Financial Position: |

||||||||||||||||||||

| Working capital |

$ | 114,291 | $ | 98,994 | $ | 116,962 | $ | 107,150 | $ | 96,062 | ||||||||||

| Total assets |

449,430 | 395,292 | 385,439 | 399,049 | 357,382 | |||||||||||||||

| Long-term debt |

73,855 | 63,685 | 84,236 | 78,487 | 85,237 | |||||||||||||||

| Equity |

187,099 | 156,295 | 129,875 | 134,906 | 114,866 | |||||||||||||||

Following amounts in thousands

| (1) | The results of operations for 2010 include a pre-tax final charge of $1,317 related to the retirement of the Company’s former Chief Executive Officer in 2008; a net pre-tax charge of $4,132 related to a Non-Income tax contingency; a $322 charge related to a currency devaluation at the Company’s 50% owned affiliate in Venezuela; a $564 charge related to an out-of-period adjustment at the Company’s 40% owned affiliate in Mexico; offset by a $2,441 tax benefit from the derecognition of various uncertain tax positions due to the expiration of applicable statutes of limitations and resolution of tax audits for certain tax years. |

| (2) | The results of operations for 2009 include a pre-tax charge for restructuring and related activities of $2,289; a pre-tax charge of $2,443 related to the retirement of the Company’s former Chief Executive Officer in 2008; offset by a gain of $1,193 on the disposition of land in Europe and a $583 tax benefit from the derecognition of various uncertain tax positions due to the expiration of applicable statutes of limitations and resolution of tax audits for certain tax years. |

| (3) | The results for operations for 2008 include a pre-tax charge for restructuring and related activities of $2,916; a pre-tax charge of $3,505 for the incremental charges related to the retirement of the Company’s Chief Executive Officer; offset by a net arbitration award of $956 related to litigation with one of the former owners of the Company’s Italian subsidiary; a tax refund of $460 relating to the Company’s increased investment in China; and a $1,508 tax benefit from the derecognition of various uncertain tax positions due to the expiration of applicable statutes of limitations and resolution of tax audits for certain tax years. |

| (4) | The results of operations for 2007 include a pre-tax environmental charge of $3,300 for the settlement of the AC Products, Inc. litigation and ongoing remediation activities at the site; a pre-tax charge of $701 related to a discontinued strategic initiative; a pre-tax charge of $487 related to certain customer bankruptcies; a tax refund of $665 related to the Company’s increased investment in China; a non-cash out-of-period tax benefit adjustment of $993 primarily related to deferred tax accounting for the Company’s foreign pension plans; and a $391 tax charge related to the revaluation of deferred tax assets as a result of a tax law change. |

15

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Executive Summary

Quaker Chemical Corporation is a leading global provider of process chemicals, chemical specialties, services and technical expertise to a wide range of industries—including steel, aluminum, automotive, mining, aerospace, tube and pipe, coatings and construction materials. Our products, technical solutions and chemical management services (“CMS”) enhance our customers’ processes, improve their product quality and lower their costs.

The 21% growth in revenue during 2010 compared to 2009 was principally due to double-digit volume increases experienced across the globe as the Company continued to recover from the global economic downturn. These volume increases were partially offset by lower CMS revenue reported on a gross basis as a result of contract renegotiations. While the Company’s gross margin improved from 34.7% in 2009 to 35.4% in 2010, the Company experienced significantly higher raw material costs as 2010 progressed, only a portion of which were recovered through price increases in 2010. Additional price increases are being implemented in early 2011 as part of the Company’s efforts to recover margins. The Company’s selling, general and administrative expenses (“SG&A”) increased 10% during 2010 due to higher selling costs with increased business activity, inflationary costs, increased incentive compensation costs as well as higher professional fees related to acquisitions. However, SG&A as a percentage of sales decreased from 28% in 2009 to 26% in 2010.

In 2010, the Company completed the acquisition of D.A. Stuart’s U.S. aluminum hot rolling oil business from Houghton International for approximately $6.8 million. With this acquisition, Quaker became a leading player in the U.S. aluminum hot rolling market. The Company also completed the acquisition of Summit Lubricants Inc., a leading specialty grease manufacturer and distributor of specialty greases, for approximately $29.1 million. This acquisition is complementary to the Company’s existing business.

The full year 2010 results include some unusual items. The 2010 results include a $4.1 million charge related to a non-income tax contingency discussed below. The Company incurred a final charge related to the former CEO’s supplemental retirement plan of approximately $1.3 million. Equity in net income of associated companies includes charges totaling $0.9 million related to the devaluation of the Venezuelan Bolivar Fuerte and an out-of-period charge related to shortfalls in reserves for pensions and other items. The effective tax rate for 2010 includes approximately $2.4 million of benefit from the derecognition of various uncertain tax positions due to the expiration of applicable statutes of limitations.

The full year 2009 results included some unusual items as well. A $2.3 million restructuring charge was taken in an effort to reduce operating costs as volume declines continued in the U.S. and Europe and extended to other regions. The Company also incurred charges related to the former CEO’s supplemental retirement plan of approximately $2.4 million. Other income for 2009 includes a $1.2 million gain related to the disposition of excess land in Europe. The effective tax rate for 2009 reflected no tax expense being provided on the land sale gain due to the utilization of net operating losses which were previously not benefited and included approximately $0.6 million of benefit from the derecognition of various uncertain tax positions due to the expiration of applicable statutes of limitations and resolution of tax audits for certain tax years.

The net result was earnings per diluted share of $2.77, up 88% compared to $1.47 for 2009, with 2010 net income surpassing that of any year in the Company’s history. In addition, the Company raised its dividend in 2010, made two strategic acquisitions and enhanced its financial flexibility for future growth by amending its primary credit facility. The Company expects to have good growth in 2011 due to its leadership positions in faster growing economies like China, Brazil and India, as well as continued recovery in the more mature markets such as the U.S. and Europe. The Company will also be investing in additional resources to support that growth, especially in the emerging markets. While the current Middle East tensions put greater uncertainty on raw material pricing, the Company’s goal is to continue its profit growth and build upon the record profits achieved in 2010. In addition, the Company expects to continue to make strategic acquisitions and is currently evaluating several opportunities.

16

Table of Contents

Critical Accounting Policies and Estimates

Quaker’s discussion and analysis of its financial condition and results of operations are based upon Quaker’s consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires Quaker to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. On an ongoing basis, Quaker evaluates its estimates, including those related to customer sales incentives, product returns, bad debts, inventories, property, plant, and equipment, investments, goodwill, intangible assets, income taxes, financing operations, restructuring, incentive compensation plans (including equity-based compensation), pensions and other postretirement benefits, and contingencies and litigation. Quaker bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

Quaker believes the following critical accounting policies describe the more significant judgments and estimates used in the preparation of its consolidated financial statements:

1. Accounts receivable and inventory reserves and exposures—Quaker establishes allowances for doubtful accounts for estimated losses resulting from the inability of its customers to make required payments. If the financial condition of Quaker’s customers were to deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be required. As part of its terms of trade, Quaker may custom manufacture products for certain large customers and/or may ship product on a consignment basis. Further, a significant portion of Quaker’s revenues is derived from sales to customers in the U.S. steel and automotive industries, where a number of bankruptcies have occurred during recent years and companies have experienced financial difficulties. When a bankruptcy occurs, Quaker must judge the amount of proceeds, if any, that may ultimately be received through the bankruptcy or liquidation process. These matters may increase the Company’s exposure should a bankruptcy occur, and may require write down or disposal of certain inventory due to its estimated obsolescence or limited marketability. Reserves for customers filing for bankruptcy protection are generally dependent on the Company’s evaluation of likely proceeds from the bankruptcy process. Large and/or financially distressed customers are generally reserved for on a specific review basis while a general reserve is established for other customers based on historical experience. The Company’s consolidated allowance for doubtful accounts was $4.3 million and $4.0 million at December 31, 2010 and 2009, respectively. Further, the Company recorded provisions for doubtful accounts of $0.9 million, $1.4 million and $1.1 million in 2010, 2009 and 2008, respectively. An increase of 10% to the recorded provisions would have decreased the Company’s pre-tax earnings by approximately $0.1 million in 2010, 2009 and 2008, respectively.

2. Environmental and litigation reserves—Accruals for environmental and litigation matters are recorded when it is probable that a liability has been incurred and the amount of the liability can be reasonably estimated. Accrued liabilities are exclusive of claims against third parties and are not discounted. Environmental costs and remediation costs are capitalized if the costs extend the life, increase the capacity or improve the safety or efficiency of the property from the date acquired or constructed, and/or mitigate or prevent contamination in the future. Estimates for accruals for environmental matters are based on a variety of potential technical solutions, governmental regulations and other factors, and are subject to a large range of potential costs for remediation and other actions. A considerable amount of judgment is required in determining the most likely estimate within the range, and the factors determining this judgment may vary over time. Similarly, reserves for litigation and similar matters are based on a range of potential outcomes and require considerable judgment in determining the most probable outcome. If no amount within the range is considered more probable than any other amount, the Company accrues the lowest amount in the range in accordance with generally accepted accounting principles. See Note 22 of Notes to Consolidated Financial Statements which appears in Item 8 of this Report.

3. Realizability of equity investments—Quaker holds equity investments in various foreign companies, whereby it has the ability to influence, but not control, the operations of the entity and its future results. Quaker

17

Table of Contents

records an investment impairment charge when it believes an investment has experienced a decline in value that is other than temporary. Future adverse changes in market conditions, poor operating results of underlying investments, or devaluation of foreign currencies could result in losses or an inability to recover the carrying value of the investments that may not be reflected in an investment’s current carrying value. These factors may result in an impairment charge in the future. The carrying amount of the Company’s equity investments at December 31, 2010 was $9.2 million and was comprised of four investments totaling $5.8 million in Nippon Quaker Chemical, Ltd. (Japan) at 50%, $1.7 million in TecniQuimia Mexicana S.A. de C.V. (Mexico) at 40%, $1.5 million in Kelko Quaker Chemical, S.A. (Venezuela) at 50% and $0.2 million in Kelko Quaker Chemical, S.A. (Panama) at 50%, respectively. See Note 6 of Notes to Consolidated Financial Statements which appears in Item 8 of this Report.

4. Tax exposures, valuation allowances and uncertain tax positions—Quaker records expenses and liabilities for taxes based on estimates of amounts that will be ultimately determined to be deductible in tax returns filed in various jurisdictions. The filed tax returns are subject to audit, often several years subsequent to the date of the financial statements. Disputes or disagreements may arise during audits over the timing or validity of certain items or deductions, which may not be resolved for extended periods of time. Quaker applies the provisions of FASB’s guidance regarding uncertain tax positions. The guidance applies to all income tax positions taken on previously filed tax returns or expected to be taken on a future tax return. The guidance prescribes a benefit recognition model with a two-step approach, a more-likely-than-not recognition criterion, and a measurement attribute that measures the position as the largest amount of tax benefit that is greater than 50% likely of being realized upon effective settlement. The guidance further requires that the amount of interest expense and income to be recognized related to uncertain tax positions be computed by applying the applicable statutory rate of interest to the difference between the tax position recognized in accordance with the guidance, including timing differences, and the amount previously taken or expected to be taken in a tax return. Quaker also records valuation allowances when necessary to reduce its deferred tax assets to the amount that is more likely than not to be realized. While Quaker has considered future taxable income and ongoing prudent and feasible tax planning strategies in assessing the need for the valuation allowance, in the event Quaker were to determine that it would be able to realize its deferred tax assets in the future in excess of its net recorded amount, an adjustment to the deferred tax asset would increase income in the period such determination was made. Likewise, should Quaker determine that it would not be able to realize all or part of its net deferred tax assets in the future, an adjustment to the deferred tax asset would be charged to income in the period such determination was made which could have a material adverse impact on the Company’s financial statements. U.S. income taxes have not been provided on the undistributed earnings of non-U.S. subsidiaries since it is the Company’s intention to continue to reinvest these earnings in those subsidiaries for working capital needs and growth initiatives. U.S. and foreign income taxes that would be payable if such earnings were distributed may be lower than the amount computed at the U.S. statutory rate due to the availability of foreign tax credits.

5. Restructuring liabilities—Restructuring charges may consist of charges for employee severance, rationalization of manufacturing facilities and other items. The Company applies FASB’s guidance regarding exit or disposal cost obligations. The guidance requires that a liability for a cost associated with an exit or disposal activity be recognized when the liability is incurred.

6. Goodwill and other intangible assets—The Company records goodwill and intangible assets at fair value as of the acquisition date and amortizes intangible assets which do not have indefinite lives on a straight-line basis over the lives of the intangible assets based on third-party valuations of the assets. Goodwill and intangible assets, which have indefinite lives, are not amortized and are required to be assessed at least annually for impairment. The Company compares the assets’ fair value to their carrying value primarily based on future discounted cash flows in order to determine if an impairment charge is warranted. The estimates of future cash flows involve considerable management judgment and are based upon assumptions about expected future operating performance. Assumptions used in these forecasts are consistent with internal planning. The actual cash flows could differ from management’s estimates due to changes in business conditions, operating performance, and economic conditions. The Company completed its annual impairment assessment as of the end

18

Table of Contents

of the third quarter 2010, and no impairment charge was warranted. The Company’s consolidated goodwill and indefinite-lived intangible assets at December 31, 2010 and 2009 were $53.9 million and $47.1 million, respectively. The Company’s assumption of weighted average cost of capital and estimated future net operating profit after tax (NOPAT) are particularly important in determining whether an impairment charge has been incurred. The Company currently uses a weighted average cost of capital of 12% and, at September 30, 2010, this assumption would have had to increase by more than 6.75 percentage points before any of the Company’s reporting units would fail step one of the impairment analysis. Further, at September 30, 2010, the Company’s estimate of future NOPAT would have had to decrease by more than 36% before any of the Company’s reporting units would be considered potentially impaired. As a result, the estimated fair value of each of the Company’s reporting units substantially exceeds their carrying value.

7. Postretirement benefits—The Company provides certain pension and other postretirement benefits to employees and retirees. Independent actuaries, in accordance with accounting principles generally accepted in the United States, perform the required valuations to determine benefit expense and, if necessary, non-cash charges to equity for additional minimum pension liabilities. Critical assumptions used in the actuarial valuation include the weighted average discount rate, rates of increase in compensation levels, and expected long-term rates of return on assets. If different assumptions were used, additional pension expense or charges to equity might be required. The Company’s U.S. pension plan year-end is November 30, and the measurement date is December 31. The following table highlights the potential impact on the Company’s pre-tax earnings due to changes in assumptions with respect to the Company’s pension plans, based on assets and liabilities at December 31, 2010:

| 1/2 Percentage

Point Increase |

1/2 Percentage

Point Decrease |

|||||||||||||||||||||||

| Foreign | Domestic | Total | Foreign | Domestic | Total | |||||||||||||||||||

| (Dollars in millions) | ||||||||||||||||||||||||

| Discount rate |

$ | (0.2 | ) | $ | (0.1 | ) | $ | (0.3 | ) | $ | 0.3 | $ | 0.1 | $ | 0.4 | |||||||||

| Expected rate of return on plan assets |

$ | (0.2 | ) | $ | (0.2 | ) | $ | (0.4 | ) | $ | 0.2 | $ | 0.2 | $ | 0.4 | |||||||||

Recently Issued Accounting Standards

The FASB updated its guidance regarding a vendor’s multiple-deliverable arrangements in October 2009. The updated guidance establishes a selling price hierarchy to be followed in determining the selling price for each deliverable in multiple-deliverable arrangements, eliminates the residual method of allocation and requires that arrangement consideration be allocated at the inception of the arrangement using the relative selling price method and requires enhanced disclosure regarding multiple-deliverable arrangements. The guidance is effective prospectively for revenue arrangements entered into or materially modified in fiscal years beginning after June 15, 2010. The Company is currently assessing the impact of this guidance on its financial statements.

Liquidity and Capital Resources

Quaker’s cash and cash equivalents increased to $25.8 million at December 31, 2010 from $25.1 million at December 31, 2009. The $0.7 million increase resulted primarily from $37.5 million of cash provided by operating activities, $41.0 million of cash used in investing activities, $4.3 million of cash provided by financing activities and a $0.1 million decrease from the effect of exchange rates on cash.

Net cash flows provided by operating activities were $37.5 million in 2010, compared to $41.6 million provided by operating activities in 2009. The Company’s improvement in net income was more than offset by increased investment in working capital. During 2009, the Company experienced significantly lower business activity as it was still recovering from the global economic downturn, which in turn greatly reduced the Company’s investment in working capital. As business volumes began to recover later in 2009 and continued to increase in 2010, the Company’s need for working capital investment correspondingly increased. The Company’s first quarter 2009 disposition of land in Europe, reduced pension contributions compared to 2009, and the 2009 completion of restructuring activities also impacted the operating cash flow comparisons.

19

Table of Contents

Net cash flows used in investing activities were $41.0 million in 2010, compared to $6.6 million of cash used in investing activities in 2009. Payments related to acquisitions were the primary driver in the change in cash flows used in investing activities. During the third quarter of 2010, the Company completed the acquisition of D.A. Stuart’s U.S. aluminum hot rolling business from Houghton International for $6.8 million and, in the fourth quarter of 2010, the Company completed the acquisition of Summit Lubricants, Inc. for $29.1 million. Cash paid for acquisitions in 2009 included the final $1.0 million payment related to the 2005 acquisition of the remaining 40% interest in the Company’s Brazilian joint venture and the final payment related to the 2006 acquisition of the remaining minority interest in its China joint venture for approximately $1.0 million. In addition, the 2009 proceeds from the disposition of land in Europe were offset by lower capital expenditures in 2010 as the Company completed its Middletown, Ohio expansion project. Reductions in the use of restricted cash related to the expansion project also affected the investing cash flow comparisons.