Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON DC, 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

INNOPHOS HOLDINGS, INC.

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

| Delaware | 001-33124 | 20-1380758 | ||

| (state or other jurisdiction of incorporation) |

(Commission File number) | (IRS Employer Identification No.) |

259 Prospect Plains Road

Cranbury, New Jersey 08512

(Address of Principal Executive Officer, including Zip Code)

(609) 495-2495

(Registrants’ Telephone Number, Including Area Code)

Not Applicable

(Former name or former address, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $.001 per share | Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ¨ Accelerated Filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

The aggregate market value of the voting common equity held by non-affiliates of the registrant was approximately $549.7 million as of June 30, 2010, the last business day of the Registrant’s most recently completed second quarter (based on the Nasdaq Global Select Market closing price on that date).

As of February 23, 2011, the registrant had 21,492,694 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

| Document |

Incorporated By Reference In Part No. | |

| Portions of Innophos Holdings, Inc. Proxy Statement to be filed for its Annual Meeting of Stockholders to be held May 20, 2011 |

III (Items 10, 11, 12, 13 and 14) |

Table of Contents

Page 3 of 90

Table of Contents

FORWARD-LOOKING STATEMENTS

Certain information set forth in this report contains “forward-looking statements” within the meaning of the federal securities laws. Forward-looking statements include statements concerning our plans, objectives, goals, strategies, future events, future revenues or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions and other information that is not historical information. In some cases, forward-looking statements can be identified by terminology such as “believes,” “expects,” “may,” “will,” “should,” or “anticipates,” or the negative of such terms or other comparable terminology, or by discussions of strategy. We may also make additional forward-looking statements from time to time.

All forward-looking statements, including without limitation, management’s examination of historical operating trends, are based upon our current expectations and various assumptions. Our expectations, beliefs and projections are expressed in good faith and we believe there is a reasonable basis for them, but there can be no assurance that management’s expectations, beliefs and projections will result or be achieved. All forward-looking statements apply only as of the date made. Unless required by law, we undertake no obligation to update or revise forward-looking statements to reflect events or circumstances after the date made or to reflect the occurrence of unanticipated events.

There are a number of risks and uncertainties that could cause our actual results to differ materially from the forward-looking statements contained in or contemplated by this report. The following are among the factors that could cause actual results to differ materially from the forward-looking statements. There may be other factors, including those discussed elsewhere in this report, which may cause our actual results to differ materially from the forward-looking statements. Any forward-looking statements should be considered in light of the risk factors specified in this Form 10-K.

Unless the context otherwise indicates, all references in this report to the “Company,” “Innophos,” “we,” “us” or “our” or similar words are to Innophos Holdings, Inc. and its consolidated subsidiaries. Innophos Holdings, Inc. is a Delaware corporation and was incorporated July 15, 2004.

Page 4 of 90

Table of Contents

| ITEM 1. | BUSINESS |

Our Company

Innophos commenced operations as an independent company in August 2004 after purchasing our North American specialty phosphates business from affiliates of Rhodia, S.A., or Rhodia. In November 2006, we completed an initial public offering and listed our Common Stock for trading on the Nasdaq Global Select Market under the symbol “IPHS”.

Innophos is a leading North American producer of specialty phosphates. Many specialty phosphates are application-specific compounds engineered to meet customer performance requirements. Specialty phosphates are often critical to the taste, texture and performance of foods, beverages, pharmaceuticals, oral care products and other applications. For example, specialty phosphates act as flavor enhancers in beverages, electrolytes in sports drinks, texture additives in cheeses, leavening agents in baked goods, calcium and phosphorus sources for nutritional supplements, pharmaceutical excipients and cleaning agents in toothpaste.

Key Product Lines

We have three principal Specialty Phosphates product lines: (i) Specialty Ingredients (formerly Specialty Salts and Specialty Acids), (ii) Food and Technical Grade purified phosphoric acid, or PPA, and (iii) Technical Sodium Tripolyphosphate (STPP) & Detergent Grade PPA. Our products serve diverse end-use markets which historically have exhibited stable demand growth.

Specialty Ingredients

Specialty Ingredients (including specialty phosphate salts and specialty phosphoric acids) are the most highly engineered products in our portfolio. There are a wide range of application-specific products for specialty phosphate salts, such as flavor enhancers in beverages, electrolytes in sports drinks, texture modifiers in cheeses, leavening agents in baked goods, calcium and phosphorus sources for nutritional supplements, pharmaceutical excipients and abrasives in toothpaste. Specialty phosphoric acids are used in industrial applications such as asphalt modification and petrochemical catalysis.

The table below presents a list of the main Specialty Ingredients sold by us in 2010:

| Product |

Description/End-Use Application | |

| Sodium Aluminum Phosphate, Acidic and Basic (“SALP”) | Premier leavening agent for baking mixes, cakes, self-rising flours, baking powders, batter & breadings (acidic). Improves melting properties of cheese (basic). | |

| Sodium Acid PyroPhosphate (“SAPP”) | Leavening agent for baking powders, doughnuts, and biscuits; inhibits browning in potatoes; provides moisture and color retention in poultry and meat. | |

| Sodium HexaMetaPhosphate (“SHMP”) | Water treatment applications; anti-microbial and sequestrant in beverages; cheese emulsifier; improves tenderness in meat, seafood and poultry applications. | |

| Monocalcium Phosphate (“MCP”) | Leavening agent in double-acting baking powder; acidulant; buffering agent. | |

| Calcium Acid Pyrophosphate (“CAPP”) | Calcium based, slow acting, multifunctional leavening acid used in a wide variety of baked goods | |

| Dicalcium Phosphate (“DCP”) | Toothpaste abrasive; leavening agent; calcium fortification. | |

| Tricalcium Phosphate (“TCP”) | Calcium and phosphorus fortifier in food and beverage applications (e.g., orange juice, cereals, and cheese); flow aid; additive in expandable polystyrene. | |

| Pharma Calcium Phosphates (“A-Tab®”, “Di-Tab®”, “Tri-Tab®”) | Excipients in vitamins, minerals, nutritional supplements and pharmaceuticals. | |

| Ammonium Phosphates (“MAP”, “DAP”) | High-end fertilizer products for horticultural use; flame retardant; cigarette additives; culture nutrient. | |

Page 5 of 90

Table of Contents

| Product |

Description/End-Use Application | |

| Potassium Phosphates (“TKPP”, “DKP”, “MKP”, “KTPP”) | Water treatment; sports drinks; buffering agent; improves tenderness in meat, seafood and poultry applications; horticulture applications. | |

| Specialty Acids (e.g., Polyacid) | Additive improving performance properties of asphalt. | |

| Sodium Blends (e.g., Sodium Tripolyphosphate (STPP (food grade))) | Ingredient improving yield, tenderness, shelf life, moisture and color retention in meat, seafood and poultry applications. | |

| Other (Sodium Bicarbonate, Tetrasodium Pyrophosphate (“TSPP”), Mono, Di, & Trisodium Phosphates (“MSP”, “DSP”, “TSP”)) | Baking powders; gelling agent in puddings; cheese emulsifiers. | |

Each salt or acid derivative typically has a number of different applications and end uses. For example, DCP can be used both as a leavening agent in bakery products and as an abrasive in oral care products. However, several food grade salts are unique to the end user in their particular finished product application. Manufacturers often work directly with customers to tailor products to their required specifications.

Our major competitor in the downstream Specialty Ingredients is Israel Chemicals Limited, or ICL.

Food and Technical Grade PPA

Food and Technical Grade PPA are high purity forms of PPA, distinct from the agricultural-grade merchant green phosphoric acid, or MGA, used in fertilizer production. PPA is used to manufacture specialty phosphate salts and acids and is also used directly in beverage applications as a flavor enhancer and in water treatment applications. We also sell Technical Grade PPA in the merchant market to third-party phosphate derivative producers.

Our major PPA competitor is Potash Corporation of Saskatchewan Inc., or PCS, a global fertilizer company for which specialty phosphates represents only a small part of its business. We consume the majority of our PPA production in our downstream operations and sell the remainder on the North American merchant market and to other downstream phosphate derivative producers, where we compete with PCS. To the best of our knowledge, PCS does not have any downstream technical or food grade phosphate derivative production capacity, other than a small potassium phosphate salt unit.

Technical Grade Sodium Tripolyphosphate (STPP) & Detergent Grade PPA

STPP is a specialty phosphate derived from reacting phosphoric acid with a sodium alkali. STPP is a key ingredient in cleaning products, including automatic dishwashing detergents, industrial and institutional cleaners and (outside the U.S.) consumer laundry detergents. In addition to its use in cleaning products, STPP is also used in water treatment, clay processing, and copper ore processing. Over 90% of the end use market for STPP is derived from consumer product applications. Detergent Grade PPA is a lower grade form of PPA used primarily in the production of STPP.

Our major North American STPP competitor is Mexichem, S.A.B. de C.V., or Mexichem, in Mexico. Currently, Mexichem produces STPP at two manufacturing locations in Mexico. We also compete with imports from North Africa, Europe and China.

Over the past several decades, there have been efforts to reduce the use of STPP in consumer and institutional cleaners. In the 1980’s STPP use in consumer laundry applications was discontinued in the U.S. and Canada. Over the last several years momentum has gained in eliminating STPP use in consumer automatic dishwashing applications in the U.S. and Canada. Most detergent manufacturers discontinued the use of STPP in automatic dishwashing detergent applications during 2010. The Industrial & Institutional market has also reformulated some of its products to reduce STPP content in an effort to market a lower cost and reduced phosphate content product line. In 2008, a global retailer began an initiative to materially reduce the use of STPP in consumer laundry detergent in Latin America by 2011. Our Mexican operations have historically dedicated a significant portion of their capacity to the production of STPP directly and have sold detergent grade PPA to other producers of STPP. In anticipation of reduced detergent demand for STPP, Innophos Mexico is investing in upgrading the food grade PPA and salts capability of our major Coatzacoalcos facility, and consequently substantially reducing the portion of capacity dedicated to detergent grade products.

Page 6 of 90

Table of Contents

GTSP & Other

Granular Triple Super Phosphate, or GTSP, is a fertilizer product line produced at our Coatzacoalcos facility. GTSP is used throughout Latin America for increasing crop yields in a wide range of agricultural sectors. GTSP is made as a co-product of our purified wet acid manufacturing process.

Our Industry

The North American marketplaces for each of our product lines have seen consolidation to two primary producers and several secondary suppliers. We consider the two key producers in each product category to be: (i) our Company and ICL, which acquired Astaris LLC, or Astaris, in 2005, in Specialty Ingredients; (ii) our Company and PCS, in Food and Technical Grade PPA; and (iii) our Company and Mexichem in Technical STPP. The production of specialty phosphates begins with phosphate rock, which can be processed in two alternative ways to produce PPA: (i) the thermal acid method, in which elemental phosphorus is combusted in a furnace and subsequently hydrated to produce purified phosphoric acid; or (ii) the purified wet acid method (PWA), in which mined phosphate rock is reacted with sulfuric acid to produce merchant green acid, (agricultural grade phosphoric acid), which is then purified through solvent-based extraction into purified phosphoric acid. The conversion of merchant green acid into PPA is a technically complex and a capital-intensive process.

The thermal acid method of production is based on the electrolytic production of elemental phosphorus and is therefore electricity intensive, while phosphoric acid made by the purified wet acid process requires the use of significant amounts of sulfuric acid. The relative overall costs of the two methods depend on the availability and cost of their component processes, electricity and coke for the former and sulfur for the latter. PPA is reacted with appropriate mineral salts or inorganic compounds to produce various specialty phosphate salts or STPP as required. We currently use PPA manufactured via the wet acid process for all of our Specialty Ingredients manufacturing needs.

Consolidation of producers has been most significant in the Specialty Ingredients market.

In addition to consolidation of producers, uneconomic production capacity has been eliminated in North America across all three major specialty phosphate product categories. For instance, in 2001, Rhodia closed its specialty salts and specialty acids plants in Buckingham, Quebec and Morrisville, Pennsylvania. In 2002, Vicksburg Chemical Company closed a specialty salts plant in Vicksburg, Mississippi. In 2003 and 2004, Astaris closed three manufacturing facilities, eliminating roughly 320,000 metric tons of capacity: a purified wet phosphoric acid plant in Conda, Idaho; a specialty salts plant in Trenton, Michigan; and an STPP plant in Green River, Wyoming. In January 2009, Mexichem closed its Coatzacoalcos facility eliminating approximately 50% of their estimated STPP capacity.

In June 2006, PCS started up a fourth PWA based PPA production train at its Aurora, NC facility, a capacity addition less than the estimated combined level of 2006 North American PPA imports and domestic PPA produced via the thermal process. The PCS capacity increase was also comparable in capacity to the Astaris Idaho plant closed in 2003 following a failed start-up.

Penetration from Imports

Over the past several years, we estimate that imports, including domestically located production facilities owned by foreign based organizations, have accounted for approximately 15-20% of the North American specialty phosphate market. This market share has been fairly stable for the last three years.

The following are the primary importers of PPA products and derivatives into North America: (i) Prayon SA, or Prayon, and Rotem Amfert Negev Ltd. (a subsidiary of ICL) for PPA, with Prayon primarily supplying acid to its specialty salts manufacturing facility in Augusta, Georgia; and (ii) various Chinese, European, and Israeli specialty phosphate manufacturers such as Chemische Fabrik Budenheim, Thermphos, Hubei Xingfa, Jiangyin Chengxing, Guangxi Mingli and BK Giulini Chemie GmbH & Co. (a subsidiary of ICL) for specialty salts and STPP.

Page 7 of 90

Table of Contents

Our Customers

Our customer base is principally composed of consumer goods manufacturers, distributors and specialty chemical manufacturers. Our customers manufacture products such as soft drinks, sports drinks and juices, various food products, toothpaste and other dental products, petroleum and petrochemical products, and various cleaners and detergents. Our customers include major consumer goods manufacturers with global market recognition in the food, beverage, pharmaceutical and cleaning product markets. We have maintained long-term relationships with the majority of our key customers, with the average customer relationship having lasted over 15 years, and some relationships spanning nearly a century. Our specialty chemical products are often critical ingredients in the formulation of our customers’ products, and typically represent only a small percentage of their total product costs. As a result, we believe that the risks associated with our customers switching suppliers often outweigh the potential gains.

For the years ended December 31, 2010, 2009 and 2008, we generated net sales of $714.2 million, $666.8 million and $934.8 million, respectively. The Company delivered record revenues in 2008 as we responded to rapidly rising market raw material costs by effectively raising our own selling prices. By early 2009, raw material costs had fallen rapidly together with recessionary economic conditions that also negatively affected demand in 2009 compared to 2008. We responded with reductions in our own selling prices during 2009. Prices stabilized in the first quarter 2010 and subsequently improved on a sequential basis as we raised prices in anticipation of increasing raw material costs. Volumes also improved significantly across all products and markets. Through this period our continued focus on demonstrating the value of our products and service to high value end markets has enabled us to significantly enhance our mix with approximately 50% of our sales to food, pharma, beverage and oral care customers in comparison to 33% in 2006.

Raw Materials and Energy

We purchase a range of raw materials and energy sources on the open market, including phosphate rock, sulfur and sulfuric acid, agricultural grade phosphoric acid (also known as MGA), PPA, natural gas and electricity. To help secure supply, we purchase several of our key raw materials under long-term contracts generally providing for fixed or minimum quantities of materials, or purchase of our full requirements, and predetermined pricing formulae based on various market indices and other factors. We do not engage in any significant futures or other derivative contracts to hedge against fluctuations of raw material. We are not integrated vertically back to our sources of supply by ownership interests, joint ventures or affiliated companies, as a result of which raw materials acquisition at economical price levels is a major risk of our business. See Item 1A “Raw Materials Availability and Pricing” of this Report Form 10-K.

Phosphate Rock and Merchant Green Acid (MGA). MGA is the main raw material for the creation of our downstream salts and acids. We purchase MGA for processing at our Geismar, LA facility through a long-term agreement with PCS. At our Coatzacoalcos facility in Mexico, we typically purchase phosphate rock in order to produce MGA internally; however, we can also process externally purchased MGA, available from various suppliers globally. The Company has agreements with three preferred phosphate rock suppliers for 2011 to supply the Coatzacoalcos facility. In addition to these primary sources, the Company has options for other spot suppliers and will continue to qualify and develop additional sources for potential future supply.

Sulfur and Sulfuric Acid. Sulfur is the key raw material used in the production of Sulfuric Acid. Sulfuric acid is a key raw material used in the production of merchant green acid. We produce the vast majority of the sulfuric acid required to operate our Coatzacoalcos facility. The majority of the sulfuric acid required for the production of MGA by PCS Geismar is supplied by Rhodia. Our U.S. needs for sulfuric acid and our Mexican needs for sulfur are handled through long term contracts with Rhodia and Pemex-Gas y Petroquimica Basica, or PEMEX, respectively.

Purified Phosphoric Acid. The key raw material input for all of our downstream specialty phosphate salt and specialty phosphoric acid operations is PPA. We purchase certain quantities of our PPA supply from third parties to optimize our consumption and net sales, including from PCS with whom we have a long-term supply contract. In 2010 Innophos produced approximately 75% and purchased approximately 25% of its total PPA supply.

Natural Gas and Electricity. Natural gas and electricity are used to operate our facilities and generate heat and steam for the various manufacturing processes. We typically purchase natural gas and electricity on the North American open market at so-called “spot rates.” From time to time, we will enter into longer term natural gas and electricity supply contracts in an effort to eliminate some of the volatility in our energy costs. We also seek to increase the energy efficiencies of our facilities and reduce costs through investments such as the co-generation project for our Coatzacoalcos plant commissioned into service in March 2008.

Page 8 of 90

Table of Contents

Research and Development

Our product engineering and development activities are aimed at developing and enhancing products, processes, applications and technologies to strengthen our position in our markets and with our customers. We focus on:

| • | developing new or improved application-specific specialty phosphate products based on our existing product line and identified or anticipated customer needs; |

| • | creating specialty phosphate products to be used in new applications or to serve new markets; |

| • | providing customers with premier technical services as they integrate our specialty phosphate products into their products and manufacturing processes; |

| • | ensuring that our products are manufactured in accordance with our stringent regulatory, health and safety policies and objectives; |

| • | developing more efficient and lower cost manufacturing processes; and |

| • | expanding existing, and developing new, relationships with customers to meet their product engineering needs. |

Our research expenditures were $2.4 million, $1.9 million and $2.3 million for the years ended December 31, 2010, 2009 and 2008, respectively.

Environmental and Regulatory Compliance

Certain of our operations involve manufacturing ingredients for use in food, nutritional supplement and pharmaceutical excipient products, and therefore must comply with stringent U.S. Food and Drug Administration, or FDA, or the U.S. Department of Agriculture, or USDA, good manufacturing practices as well as the quality requirements of our customers. In addition, our operations that involve the use, handling, processing, storage, transportation and disposal of hazardous materials, are subject to extensive and frequently changing environmental regulation by federal, state, and local authorities, as well as regulatory authorities with jurisdiction over our foreign operations. Our operations also expose us to the risk of claims for environmental remediation and restoration or for exposure to hazardous materials. Our production facilities require operating permits that are subject to renewal or modification. Violations of health and safety and environmental laws, regulations, or permits may result in restrictions being imposed on operating activities, substantial fines, penalties, damages, the rescission of an operating permit, third-party claims for property damage or personal injury, or other costs, any of which could have a material adverse effect on our business, financial condition, results of operations, or cash flows. Due to changes in health and safety and environmental laws and regulations, the time frames when those laws and regulations might be applied, and developments in environmental control technology, we cannot predict with certainty the amount of capital expenditures to be incurred for environmental purposes.

Some environmental laws and regulations impose liability and responsibility on present and former owners, operators or users of facilities, and sites for contamination at such facilities and sites without regard to causation or knowledge of contamination. Many of our sites have an extended history of industrial use. Soil and groundwater contamination have been detected at some of our sites, and additional contamination might occur or be discovered at these sites or other sites in the future (including sites to which we may have sent hazardous waste). We continue to investigate, monitor or cleanup contamination at most of these sites. The potential liability for all these sites will depend on several factors, including the extent of contamination, the method of remediation, future developments and increasingly stringent regulation , the outcome of discussions with regulatory agencies, the liability of third parties, potential natural resource damage, and insurance coverage. Accruals for environmental matters are recorded in the accounting period in which our responsibility is established and the cost can be reasonably estimated. Due to the uncertainties associated with environmental investigations and cleanups and the ongoing nature of the investigations and cleanups at our sites, we are unable to predict precisely the nature, cost and timing of our future remedial obligations with respect to our sites and, as a result, our actual environmental costs and liabilities could significantly exceed our accruals.

Further information, including the current status of significant environmental matters and the financial impact incurred for the remediation of such environmental matters, is included in Note 16, Commitments and Contingencies, of the Notes to Financial Statements in “Item 8. Financial Statements and Supplementary Data,” and in “Item 1A. Risk Factors”.

Intellectual Property

We rely on a combination of patent, copyright and trademark laws to protect certain key intellectual aspects of our business. In addition, our pool of proprietary information, consisting of manufacturing know-how, trade secrets and unregistered copyrights relating to the design and operation of our facilities and systems, is considered particularly important and valuable. Accordingly, we protect proprietary information through all legal means practicable. However, monitoring the

Page 9 of 90

Table of Contents

unauthorized use of our intellectual property is difficult, and the steps we have taken may not prevent all unauthorized use by others. While we consider our copyrights and trademarks to be important to our business, ultimately our established reputation and the products and service we provide to the end-customer are more important.

Insurance

In the normal course of business, we are subject to numerous operating risks, including risks associated with environmental, health and safety while manufacturing, developing and supplying products, potential damage to a customer, and the potential for an environmental accident.

We currently have in force insurance policies covering property, general liability, excess liability, workers’ compensation/employer’s liability, product liability, product recall, fiduciary and other coverages. We seek to maintain coverages consistent with market practices and required by those with whom we do business. We believe that we are appropriately insured for the insurable risks associated with our business.

Employees

As of December 31, 2010, we had 1,087 employees, of whom 684 were unionized hourly wage employees. We currently employ both union and non-union employees at most of our facilities. We believe we have a good working relationship with our employees, which has resulted in high productivity and low turnover in key production positions. We have experienced no work stoppages or strikes at any of our unionized facilities since acquiring them in 2004. We are a party to a collective bargaining agreement with the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Service Workers International Union, Local No. 7-765 through January 16, 2014 at the Chicago Heights facility; International Union of Operating Engineers, Local No. 912 through April 15, 2013 at the Nashville facility; the Health Care, Professional, Technical, Office, Warehouse and Mail Order Employees Union, affiliated with the International Brotherhood of Teamsters, Local 743 through June 17, 2011 at the Chicago (Waterway) facility; the United Steelworkers of America, Local No. 6304 through April 30, 2011 at the Port Maitland, Ontario facility; and the Sindicato de Trabajadores de la Industria Química, Petroquímica, Carboquímica, Gases, Similares y Conexos de la República Mexicana, at the Mexico facilities. The agreement at the Coatzacoalcos, Mexico facility is for an indefinite period, but wages are reviewed every year and the rest of the agreement is subject to negotiation every two years. The current two-year period will expire in June 2012.

Executive Officers

The following table and biographical material present information about the persons serving as our executive officers, and key employees:

| Name |

Age | Position | ||||

| Randolph Gress |

55 | Chairman of the Board, Chief Executive Officer, President and Director | ||||

| Neil Salmon |

42 | Vice President and Chief Financial Officer | ||||

| William Farran |

61 | Vice President, General Counsel and Corporate Secretary | ||||

| Charles Brodheim |

47 | Corporate Controller | ||||

| Louis Calvarin |

47 | Vice President, Operations | ||||

| Mark Feuerbach |

51 | Vice President, Investor Relations, Treasury, Financial Planning & Analysis | ||||

| Joseph Golowski |

49 | Vice President, Specialty Phosphates | ||||

| Wilma Harris |

64 | Vice President, Human Resources | ||||

| Russell Kemp |

52 | Vice President, Research & Development and Chief Risk Officer | ||||

| Michael Lovrich |

57 | Vice President, Supply Chain | ||||

| Abraham Shabot |

49 | Vice President, Director General, Innophos Latin America | ||||

| Mark Thurston |

51 | Vice President, Corporate Strategy and Worldwide Business Development | ||||

Biographical Material

Randolph Gress is Chairman of the Board, Chief Executive Officer, President and Director of Innophos. Previously, Mr. Gress joined Rhodia in 1997 and became Vice President and General Manager of the sulfuric acid business. He was named global President of Specialty Phosphates (based in the U.K.) in 2001. Prior to joining Rhodia, Mr. Gress spent fourteen years at FMC Corporation where he worked in various managerial capacities in the Chemical Products, Phosphorus Chemicals and Corporate Development groups. From 1977 to 1980, Mr. Gress worked at Ford Motor Company in various capacities within the Plastics, Paint and Vinyl Division. Mr. Gress earned a B.S.E. in Chemical Engineering from Princeton University and an M.B.A. from Harvard Business School.

Page 10 of 90

Table of Contents

Neil Salmon is Vice President and Chief Financial Officer of Innophos. Mr. Salmon joined Innophos in October 2009. Prior to joining Innophos, Mr. Salmon was the Chief Financial Officer of the Adhesives Business Group of Imperial Chemical Industries PLC. The Adhesives Business Group was the largest specialty chemical division representing around 25% of ICI in 2007 with a major presence in North America, Europe, Asia Pacific and Latin America. From 2004 to 2006, Mr. Salmon was the Chief Financial Officer, Asia Pacific for National Starch and Chemical Company, an ICI subsidiary, and from 2001 to 2003, he was the Commercial Finance Director of ICI’s U.S. Specialty Polymers and Adhesives Group in Bridgewater, New Jersey. From 1991 to 2001, Mr. Salmon held various management positions within the ICI Group. Mr. Salmon holds an M.A. in Politics, Philosophy and Economics from Oxford University (1991).

William Farran is Vice President, General Counsel and Corporate Secretary of Innophos. Mr. Farran joined Rhodia in 1987 as Environmental Counsel and held various positions in the Rhodia Legal Department, including Senior Operations Counsel and Assistant General Counsel, providing and managing a wide range of legal services to various Rhodia North American enterprises. In addition to his legal responsibilities, Mr. Farran also led the North American Total Quality Management function and served as Director, Public Affairs and Communications. Prior to joining Rhodia, Mr. Farran was Senior Counsel for UGI Corporation, Valley Forge, PA, and an associate with Morgan, Lewis & Bockius, Philadelphia, PA. Mr. Farran earned his B.S. in Economics from the Wharton School, University of Pennsylvania and his J.D. from Case Western Reserve University. He is a member of the bars of the Supreme Court of Pennsylvania and the Supreme Court of the United States.

Charles Brodheim is Corporate Controller of Innophos. Mr. Brodheim joined Rhodia in 1988 and held various tax, accounting and business analyst positions within Rhodia. Mr. Brodheim was the North American Finance Director for Specialty Phosphates from 2000-2002. After 2002, Mr. Brodheim was a Finance Director for various Rhodia North American Enterprises, including its Eco-Services enterprise. Mr. Brodheim earned a B.B.A. degree in Finance/Accounting from Temple University and is a certified public accountant.

Louis Calvarin is Vice President, Operations of Innophos. Dr. Calvarin joined Rhodia in France in 1986. He has been Director of Manufacturing and Engineering for Specialty Phosphates since January 2004. Prior to that, Dr. Calvarin held the positions of Director of Manufacturing for Specialty Phosphates (U.S.), Mineral Chemicals Industrial Operations Manager for Home, Personal Care and Industrial Ingredients, and Projects Director for Paint, Paper and Construction Materials. Dr. Calvarin earned a Ph.D. degree in Chemical Engineering from the Ecole Nationale Superieure des Mines in France and graduated from Ecole Polytechnique in France.

Mark Feuerbach is Vice President, Investor Relations, Treasury, Financial Planning & Analysis and had previously served as Chief Financial Officer of Innophos from August 2004 through April 2005 and again from June through September 2009. Mr. Feuerbach joined Rhodia in 1989 and was Global Finance Director of Specialty Phosphates from 2000 to 2004, including a two-year assignment in the U.K. immediately following the purchase of the phosphates business of Albright & Wilson. Prior to this assignment, Mr. Feuerbach was the Finance Director of Rhodia’s North American phosphates business from 1997 to 2000 and he previously held various finance positions in a number of Rhodia’s businesses. Prior to joining Rhodia, Mr. Feuerbach held various accounting and finance positions in both manufacturing and service companies. Mr. Feuerbach earned a B.A. in Business Administration/Accounting from Rutgers College and an M.B.A. in Finance/Information Systems from Rutgers Graduate School of Management.

Joseph Golowski is Vice President of the Specialty Phosphates Business of Innophos, appointed to that position in April 2010. Joining Rhodia in 1989 in Market Development, Mr. Golowski has since then held progressive roles in Business Development, Sales, Marketing and Management. From 1997 through 2000, Mr. Golowski served as a Global Market Director for Rhodia Rare Earths based in Paris, France. Returning to the U.S., he became the North American Asset Manager for Phosphoric Acid and subsequently the Director of Sales for the Specialty Phosphate Business. This path brought him to be appointed Vice President of Sales in 2006 and to his current role as Vice President for the Specialty Phosphate Business. Mr. Golowski earned a B.S. in Ceramic Engineering from Rutgers University, College of Engineering.

Wilma Harris is Vice President, Human Resources of Innophos. Ms. Harris joined Rhodia in 1986 as Human Resource Manager for the Agricultural Products business located in Research Triangle Park, NC. Since that time she has held various positions in corporate, shared services and business human resources and information technology. From January 2003 until August 2005, she was the Human Resources Director for the Specialty Phosphates and Performance Phosphates and Derivatives businesses. Prior to joining Rhodia, Ms. Harris worked for Union Carbide Corporation in several labor relations and research and development positions. She holds a B.S. degree from West Virginia State University, a M.P.A. degree from Marshall University and Masters Degrees in Theological Studies and Divinity from New Brunswick Theological Seminary.

Page 11 of 90

Table of Contents

Russell Kemp is Vice President, Research & Development and Chief Risk Officer of Innophos. Mr. Kemp joined Rhodia in 1989, first holding several manufacturing management jobs and – from 1998 through 2007 – fulfilling a business management role. Previously, he worked as a process and production engineer at Monsanto. Mr. Kemp earned a B.S. in Chemical Engineering from the Colorado School of Mines and an MBA from Southern Illinois University – Edwardsville.

Michael Lovrich is Vice President, Supply Chain of Innophos. Mr. Lovrich joined Innophos in August, 2007 from Coach, Inc., where he served as Vice President, Supply Chain from 2004 through 2007 for that specialty leather and women’s accessories manufacturer. Prior to his tenure with Coach, Mr. Lovrich was with Engelhard Corporation where he held various positions in Supply Chain Operations and Information Technology, leading several supply chain transformation initiatives at the business unit and corporate level. Prior to Engelhard, Mr. Lovrich held positions with Fisher Scientific, Thompson Medical and Becton-Dickinson. Mr. Lovrich earned his B.A. in History from William Paterson College and his M.B.A. from New York University Stern School of Business. Mr. Lovrich also holds professional certifications in supply chain management and project management.

Abraham Shabot is Vice President and Director General for Innophos Latin America. Mr. Shabot joined Innophos in July 2009. Prior to joining Innophos, he served as Managing Director of Kaltex Fibers, a leading acrylic fiber producer in the Americas, from 2007 to 2009. Before that, he held various positions in Sales and Business Development for Comex, a large Mexican building supplies manufacturer and distributor. In addition, he was Latin American Director for Polyone Corporation, a large publicly held manufacturer and distributor of plastic resin and rubber compounds. He earned a degree in Chemical Engineering from Iberoamericana University in Mexico City.

Mark Thurston is Vice President, Corporate Strategy and Worldwide Business Development of Innophos. Mr. Thurston joined Rhodia in 1985 working in Fine Organics and has been Vice President of Strategy and Worldwide Business Development since 2009. Previously, he was Vice President of Specialty Chemicals from 2004 to 2008 and Vice President and General Manager of Food Ingredients North America from 2002 to 2004. Prior to that, he worked in various sales and marketing capacities for Rhodia. Mr. Thurston previously worked at RTZ Corp. as an assistant planning and marketing manager and an assistant production manager. Mr. Thurston earned a B.S. in Chemical Engineering from the University of Aston in Birmingham, England.

Available Information

The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers, including the Company, that file electronically with the SEC. The public can obtain any documents that the Company files with the SEC at http://www.sec.gov. The Company files annual reports, quarterly reports, proxy statements and other documents with the Securities and Exchange Commission (SEC) under the Securities Exchange Act of 1934 (Exchange Act). The public may read and copy any materials that the Company files with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

Innophos also makes available free of charge through its website (www.innophos.com) the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports filed or furnished pursuant to the Exchange Act as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the SEC.

Page 12 of 90

Table of Contents

| ITEM 1A. | RISK FACTORS |

Investing in our company involves a significant degree of risk of varying origins, including from our operations and financial matters. If any of the following risks or uncertainties actually occurs, our business, prospects, financial condition and results of operations could be materially and adversely affected.

Risks Related to Our Business Operations

Raw Materials Availability and Pricing

Our principal raw materials consist of phosphate rock, sulfur and sulfuric acid, MGA, PPA and energy (principally natural gas and electricity). Our raw materials are purchased under supply contracts that vary from long term multi-year supply arrangements to annual agreements. Pricing within contracts is typically set according to predetermined formulae dependent on price indices or market prices with pricing for some shorter term contracts set by negotiation with reference to market conditions. The prices we pay under these contracts will generally lag the underlying market prices of the raw material. Approximately 25% of our supply for 2011 is bought under fixed annual pricing arrangements with the remaining quantities adjusted to quarterly pricing with approximately a three month lag to market prices.

Various market conditions can affect the price and supply of our raw materials. The primary demand for both phosphate rock and sulfur, globally, is for fertilizer production. The costs of these materials are heavily influenced by demand conditions in the fertilizer market and freight costs, which traditionally have been volatile. Prices for both materials escalated rapidly during 2007 and 2008, declined during 2009 and began to increase again during 2010. Increased raw material pricing may adversely affect our margins if we are not able to offset costs with sales price increases as we explain under “Price Competition” below.

Following completion of a two year initiative to qualify alternative sources of phosphate rock for our Coatzacoalcos, Mexico site, we have now successfully processed industrial scale quantities of phosphate rock from five suppliers and, for 2011, we expect the majority of our requirements to be met from three of these suppliers. Previously the Coatzacoalcos facility was supplied exclusively by OCP, S.A., a state-owned mining company in Morocco under a 1992 supply agreement that expired in September 2010. Although the Coatzacoalcos facility has made significant advances in its ability to handle alternative grades of rock without adversely affecting the operating efficiency; further investment will be required to realize the full benefits of improved process flexibility. Accordingly, it remains possible that process efficiency issues will arise as the plant processes new sources of rock over longer time periods, necessitating further investment or a change in rock suppliers to better suit plant processing capability. We cannot be sure that those kinds of efficiency issues will not arise, or if they do, that our existing or other suppliers would be able to supply sufficient additional quantities or grades to meet our full requirements, factors that could significantly affect our phosphate rock availability and may weaken our ability to maintain our existing levels of operations. Although the diversification of our supply base has reduced our dependence on any one supplier, tight demand conditions overall in the fertilizer market would mean that our purchases could be constrained were any of our major suppliers to experience a significant disruption in their ability to supply, for example as a result of capacity constraints, political unrest, or adverse weather conditions in the areas where that supplier operates. We also cannot be sure the annual or other periodic contracts we have in-place will be renewed on similar terms to those currently enjoyed.

Natural gas prices have experienced significant volatility in the past several years. Wide fluctuations in natural gas prices may result from relatively minor changes in supply and demand, market uncertainty, and other factors, both domestic and foreign, that are beyond our control. In addition, natural gas is often a substitute for petroleum-based energy supplies and natural gas prices are positively correlated with petroleum prices. Future increases in the price of petroleum (resulting from increased demand, political instability or other factors) may result in significant additional increases in the price of natural gas. We typically purchase natural gas at spot market prices for use at our facilities which exposes us to that price volatility, except in those instances where, from time to time, we enter into longer term, fixed-price natural gas contracts.

Most of our raw materials are supplied to us by either one or a small number of suppliers. Some of those suppliers rely, in turn, on sole or limited sources of supply for raw materials included in their products. Failure of our suppliers to maintain sufficient capability to meet changes in demand or to overcome unanticipated interruptions in their own sources of supply from force majeure conditions, such as disaster or political unrest, may prevent them from continuing to supply raw materials as we require them, or at all. Our inability to obtain sufficient quantities of sole or limited source raw materials or to develop alternative sources on a timely basis if required could result in increased costs, which may be material, in our operations or our inability to properly maintain our existing level of operations.

Page 13 of 90

Table of Contents

Price Competition

We face significant competition in each of our markets. In some markets, our products are subject to price competition due to factors such as competition from low-cost producers, import competition, excess industry capacity and consolidation among our customers and competitors. In addition, in the specialty chemicals industry, price competition is also based upon a number of other considerations, including product differentiation and innovation, product quality, technical service, and supply reliability. New products or technologies developed by competitors may also have an adverse impact on our price position. Future expansions could also have a negative impact on our price position.

From time to time, we have experienced pricing pressure, particularly from significant customers and often coincident with periods of overcapacity in the markets in which we compete. In the past, we have taken steps to reduce costs and resist possible price reductions by structuring our contracts and developing strong “value-oriented” non-price related customer service relationships. However, price reductions in the past have adversely affected our sales and margins, and if we are not able to offset price pressure when it arises through improved operating efficiencies, reduced expenditures and other means, we may be subject to those same effects in the future.

Innophos has experienced more intense pricing pressures in markets, and for applications, where competing producers, particularly those located in China and North Africa, have similar product offerings, established supply relationships, and potential cost advantages. Historically, this has occurred most frequently in markets such as South America where Innophos does not have local production capability and for less specialized products such as detergent grade STPP. Chinese phosphate producers generally utilize the “thermal” method, a process more heavily dependent on energy that may be cost advantaged compared to “wet” method producers (such as Innophos) during periods of low energy prices. Both North African and some Chinese producers are integrated back to phosphate rock, which also may provide cost advantages to them depending on the markets in which they choose to compete. If the relative competitiveness of Chinese and North African producers increases significantly, or they are successful in extending their product lines to more specialized product applications, pricing pressure on Innophos could increase significantly.

Environmental, Product Regulations and Sustainability Initiative Concerns

Our operations involve the use, handling, processing, storage, transportation and disposal of hazardous materials and some of our products are ingredients in foods, nutritional supplements or pharmaceutical excipients that are used in finished products consumed or used by humans or animals. As a result, we are subject to extensive and frequently changing environmental and other regulatory requirements and periodic inspection by federal, state, and local authorities, including the U.S. Environmental Protection Agency, or EPA, the FDA, and the USDA, as well as other regulatory authorities and those with jurisdiction over our foreign operations and product markets. Our operations also expose us to the risk of claims for environmental remediation and restoration or for exposure to hazardous materials. Our production facilities require various operating permits that are subject to renewal or modification. Violations of environmental laws, regulations, or permits may result in restrictions being imposed on operating activities, substantial fines, penalties, damages, the rescission of operating permits, third-party claims for property damage or personal injury, or other costs.

Additional laws or regulations focused on phosphate-based products may be implemented in the future. For example, a number of states within the U.S. and the Canadian provinces have moved or are moving to effectively ban the use of phosphate-based products in consumer automatic dishwashing detergents. The trade association that includes major manufacturers of consumer automatic dishwashing detergents has actively supported these efforts in the U.S. and Canada, with non-phosphate legislation becoming effective in July 2010. This trend and related changes in consumer preferences has already reduced our requirements for auto dish markets and we have responded with a shift in our capabilities to serve other food and industrial applications. We cannot predict the impact and the corresponding responses made by our competitors. Furthermore, although already banned in consumer laundry detergents in many U.S. States, phosphates are still permitted for those applications in many Latin American regions and other parts of the world. We cannot be sure that such a ban for use in consumer laundry detergents may not be implemented in some or all of these markets in the future, or that the same effect may not result from manufacturers reformulating to reduce phosphate levels. Additional laws, regulations or distribution policies focused on reduced use of other phosphate-based products could occur in the future. For example, a global retailer, as part of a corporate sustainability initiative, issued a statement indicating its intent to reduce phosphates in laundry and dish detergents by 70% in its Latin American and Canadian stores. Also, some jurisdictions have threatened to further regulate or ban the use of polyphosphoric acid and orthophosphoric acid in asphalt road construction. During 2008, such restrictions were implemented in New York State, but reversed in Nebraska and in 2009 restrictions were reversed in Wyoming and relaxed in Colorado. In 2009, Colorado allowed the use of polyphosphoric acid in asphalt road construction on an exception basis. Such a ban, if instituted in multiple jurisdictions or throughout the U.S. and Canada, could have a significant impact on our business. Changes in composition or permitted-use regulations in domestic or export countries may affect the regulatory status of our finished products and our ability to sell these products into some markets. Such changes may in turn require reformulation or alternative raw material sourcing, potentially incurring additional cost. If these measures are not successful, the available markets for our products may be limited.

Page 14 of 90

Table of Contents

Maintaining compliance with health and safety and environmental laws and regulations has resulted in ongoing costs for us. Currently, we are involved in several compliance and remediation efforts and agency inspections concerning health, safety and environmental matters.

Some existing environmental laws and regulations impose liability and responsibility on present and former owners, operators or users of facilities and sites for contamination at those locations without regard to causation or knowledge of contamination. Many of our sites have an extended history of industrial use. Soil and groundwater contamination have been detected at some of our sites, and additional contamination might occur or be discovered at these sites or other sites (including sites to which we may have sent hazardous waste) in the future. We continue to investigate, monitor or clean-up contamination at most of these sites. Due to the uncertainties associated with environmental investigations and clean-ups and the ongoing nature of the investigations and clean-ups at our sites, we cannot predict precisely the nature, cost, and timing of our future remedial obligations with respect to our sites.

International Operations

We have significant production operations in Mexico and Canada, and we continually evaluate business opportunities that may expand our operations to other areas beyond the Americas. We believe that revenue from sales outside the U.S. will continue to account for a material portion of our total revenue for the foreseeable future. There are inherent risks in international operations, the most notable being currency fluctuations and devaluations, economic and business conditions that differ from U.S. cycles, divergent social and political conditions that may become unsettled or even disruptive, and communication and translation delays and errors due to cultural and language barriers. Among those additional risks potentially affecting our Mexican operations are changes in local economic conditions, currency devaluations, potential disruption from socio-political violence in that country, and difficulty in contract enforcement due to differences in the Mexican legal and regulatory regimes compared to those of the U.S. Risks to our Canadian operations, though generally less than for Mexico, nevertheless include a differing federal and provincial regulatory environment from that in the U.S. and currency fluctuations and devaluations. In the event we establish operations in new regions, our exposures to risks from the noted causes and from other as yet unknown causes may increase.

Our overall success as a multinational business depends, in part, upon our ability to succeed in differing economic, social and political conditions. Among other things, we are faced with potential difficulties in building and starting up local facilities, staffing and managing local workforces, and designing and effecting solutions to manage commercial risks posed by local customers and distributors. We may not continue to succeed in developing and implementing policies and strategies that are effective in each location where we do business. These risks are not limited to only those countries where we actually operate facilities, but may extend to areas and regions that supply and service our facilities or are supplied and serviced by them.

As a U.S. corporation, we are subject to the regulations imposed by the Foreign Corrupt Practices Act, or FCPA, which generally prohibit U.S. companies, their subsidiaries and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or keeping business. We sell many of our products in developing countries through sales agents and distributors whose personnel are not subject to our disciplinary procedures. While we and our subsidiaries are committed to conducting business in a legal and ethical manner wherever we operate, and we communicate and seek to monitor compliance with our policies by all who do business with us, we cannot be sure that all our third party distributors or agents remain in full compliance with the FCPA or comparable local regulation at all times.

Product Liability Exposure

Many of our products are additives used in the food and beverage, consumer product, nutritional supplement and pharmaceutical industries. The sale of these additives and our customers’ products that include them involve the risk of product liability and personal injury claims, which may be brought by our customers or end-users of products. While we adhere to stringent quality standards, in the course of their production, storage and transportation, our products could be subject to adverse effects from foreign matter such as moisture, dust, odors, insects, mold, or other substances (organic or inorganic), or from excessive temperature. Historically, we have not been subject to material product liability claims, and none are currently outstanding. However, because our products are used in manufacturing a wide variety of our customers’ products, including those ingested by people, we cannot be sure we will not be subject to material product liability or recall claims in the future.

Production Facility Operating Hazards

Our production facilities are subject to hazards associated with the manufacturing, handling, storage, and transportation of chemical materials and products, including failure of pipeline integrity, explosions, fires, inclement weather and natural

Page 15 of 90

Table of Contents

disasters, terrorist attacks, mechanical failures, unscheduled downtime, transportation interruptions, remedial complications, chemical spills, discharges or releases of toxic or hazardous substances, storage tank leaks and other environmental risks. We have implemented and installed various management systems and engineering controls and procedures at all our production facilities to minimize these risks. We also insure our facilities to protect against a range of risks. However, these potential hazards do exist and could cause personal injury and loss of life, severe damage to or destruction of property and equipment, and environmental and natural resource damage, and may result in a suspension of operations (or extended shutdowns) and the imposition of civil or criminal penalties, whose nature, timing, severity and non-insured exposures are unknown.

Intellectual Property Rights

We rely on a combination of contractual provisions, confidentiality procedures and agreements, and patent, trademark, copyright, unfair competition, trade secrecy, and other intellectual property laws to protect our intellectual property and other proprietary rights. Nonetheless, we cannot be sure that any pending patent application or trademark application will result in an issued patent or registered trademark, or that any issued or registered patents or trademarks will not be challenged, invalidated, circumvented or rendered unenforceable. The use of our intellectual property by others could reduce any competitive advantage we have developed or otherwise harm our business. Moreover, we cannot be sure that our property rights can be asserted in all cases or that we can defend ourselves successfully or cost-effectively against the assertion of rights by others.

Contingency Planning

We operate a number of manufacturing facilities in the US, Canada and Mexico, and we coordinate company activities, including our sales, customer service, information technology systems and administrative services and the like, through headquarters operated in those countries. In 2009, we began an enterprise resource planning, or ERP, system and business process redesign project to upgrade our information technology systems including updated contingency plans with an estimated full scale start-up in mid 2011. We cannot be sure that our plans, intentions or expectations of the business process redesign and information technology systems upgrade will be achieved on the schedules we anticipate or fully in accord with our expectations, as a result of which we may experience business disruptions from implementing our planned upgrade.

Our sites and those of others who provide services to them are subject to varying risks of disaster and follow on consequences, both manmade and natural, that could degrade or render inoperable one or more of our facilities for an extended period of time. Such disaster related risks and effects are not predictable with certainty and, although they can be mitigated, they cannot be avoided. We seek to mitigate our exposures to physical disaster events in a number of ways. For example, where feasible, we design and engineer the configuration of our plants to reduce the consequences of disasters. We also maintain insurance for our facilities against casualties, including extended business interruption, and we continually evaluate our risks and develop contingency plans for dealing with them and policies for avoiding them in the future. For example, after suffering extensive flood damage to our products (substantially all of which was covered by insurance) at a third party Nashville, TN warehouse in May 2010, we have relocated our area warehousing to other facilities on safer ground. Although we have reviewed and analyzed a broad range of risks applicable to our business, the ones that actually affect us may not be those we have concluded most likely to occur. Furthermore, although our reviews have led to more systematic contingency planning, our plans are in varying stages of development and execution, such that they may not be adequate at the time of occurrence for the magnitude of any particular disaster event that befalls us.

Certain Financial Risks

Contingencies Affecting Dividends

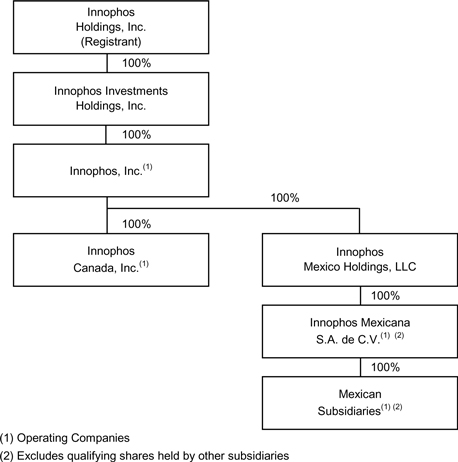

Following our 2006 public offering, our Board of Directors initiated a policy of paying regular quarterly cash dividends on our Common Stock, subject to the availability of funds, legal and contractual restrictions and prudent needs of our business. We have maintained that policy and paid dividends continuously since that time. However, we are a holding company that does not conduct any business operations of our own. As a result, we are normally dependent upon cash dividends, distributions and other transfers from our subsidiaries, most directly Innophos, Inc., our primary operating subsidiary, and Innophos Investments Holdings, Inc., its parent, to make dividend payments on our Common Stock. The amounts available to us to pay cash dividends are restricted by covenants in our debt agreements and by provisions of Delaware law. As allowed by existing debt instruments, we may incur additional indebtedness that may restrict to an even greater degree, or prohibit, the payment of dividends on stock. We cannot be sure the level of our operations or agreements governing our current or future indebtedness will permit us to adhere to our current dividend policy, or pay any dividends at all, or that continued payment of dividends will remain prudent for our business in the future judgment of our Board of Directors.

Page 16 of 90

Table of Contents

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

Our headquarters are located in Cranbury, New Jersey, with manufacturing facilities strategically located throughout the United States, Canada, and Mexico. We operate seven facilities which manufacture our four main product lines: Specialty Ingredients, Food and Technical Grade PPA, STPP & Detergent Grade PPA, and GTSP & Other Products. Our largest manufacturing facility is located in Coatzacoalcos, Mexico. We operate four medium-size plants in Chicago Heights, Illinois, Nashville, Tennessee, Port Maitland, Canada (Ontario), and Geismar, Louisiana, which collectively produce our major products. We produce additional specialty salts in two plants located in Chicago, Illinois (Waterway), and Mission Hills, Mexico. All the facilities listed above are owned with the exception of Mission Hills, Mexico, where the land is leased long-term. We also lease facilities at Cranbury, New Jersey, Mexico City, Mexico, and Mississauga, Canada (Ontario) which house our executive, commercial, administrative, product engineering and research and development employees, with the Cranbury, New Jersey facility serving as our world headquarters. We also own a distribution facility in Chicago which we use to service our customer base. We do not own and are not responsible for any closed U.S. or Canadian elemental phosphorus or phosphate production sites, as these were not part of the assets or liabilities acquired when we commenced our independent business in 2004.

| ITEM 3. | LEGAL PROCEEDINGS |

The information set forth in Note 16 of Notes to Consolidated Financial Statements, “Commitments and Contingencies,” in “Item 8. Financial Statements and Supplementary Data”.

| ITEM 4. | (REMOVED AND RESERVED) |

None.

Page 17 of 90

Table of Contents

| ITEM 5. | MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Certain Market Data

Our Common Stock has been listed and traded since November 2006 on the Nasdaq Global Select Market under the symbol “IPHS.”

Stock price comparisons:

| 2010 | 2009 | |||||||||||||||||||||||

| Quarter |

High | Low | Dividends Paid Per Share |

High | Low | Dividends Paid Per Share |

||||||||||||||||||

| First |

$ | 28.04 | $ | 17.79 | $ | 0.17 | $ | 19.81 | $ | 7.80 | $ | 0.17 | ||||||||||||

| Second |

31.00 | 25.20 | 0.17 | 19.44 | 11.23 | 0.17 | ||||||||||||||||||

| Third |

33.10 | 24.22 | 0.17 | 21.10 | 16.10 | 0.17 | ||||||||||||||||||

| Fourth |

37.67 | 32.72 | 0.17 | 25.78 | 18.60 | 0.17 | ||||||||||||||||||

The Company paid the $0.17 per share dividend declared in the fourth quarter of 2010 in the first quarter of 2011.

The number of holders of record of our Common Stock at February 15, 2011 was 9,061.

Dividends

Consistent with the determination of our Board of Directors made in December 2006, we continued to declare and pay quarterly dividends of $0.17 per share of Common Stock in 2010. Subject to action by the Board of Directors on a quarterly basis, management’s present policy is to recommend dividends be continued, reflecting its judgment at the present time that stockholders are better served if we distribute to them, as quarterly dividends payable at the discretion of the Board, a portion of the cash generated by our business in excess of our expected cash needs rather than retaining or using the cash for other purposes. Our expected cash needs include operating expenses and working capital requirements, interest and principal payments on our indebtedness, capital expenditures, costs associated with being a public company, taxes and other costs. If our financial needs change, management’s recommendations concerning dividends may also change.

We are not required to pay dividends, and our stockholders will not be guaranteed, or have contractual or other rights, to receive dividends. Our Board of Directors may decide, in its discretion at any time, to decrease or increase the amount of dividends, otherwise modify or repeal the dividend policy or discontinue entirely the payment of dividends.

In addition to prudent business considerations, our ability to pay dividends is restricted by the laws of Delaware, our state of incorporation, and may be restricted by agreements governing debt.

Since we are a holding company, substantially all assets shown on our consolidated balance sheet are held by our subsidiaries. Accordingly, our earnings and cash flow and our ability to pay dividends are largely dependent upon the earnings and cash flows of our subsidiaries and the distribution or other payment of such earnings to us in the form of dividends. Our ability to pay dividends on our Common Stock is limited by restrictions in our indebtedness affecting the ability to pay dividends. See Note 9 of Notes to Consolidated Financial Statements in “Item 8. Financial Statements and Supplementary Data”.

Page 18 of 90

Table of Contents

Equity Compensation Plans

The following information is provided for our most recently completed fiscal year for certain plans providing compensation in the form of equity securities.

Equity Compensation Plan Information

| Plan category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted average exercise price of outstanding options, warrants and rights |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) |

|||||||||

| (a) | (b) ** | (c) | ||||||||||

| Equity compensation plans approved by security holders |

1,470,980 | $ | 15.75 | 1,972,046 | * | |||||||

| Equity compensation plans not approved by security holders |

— | $ | — | — | ||||||||

| Total |

1,470,980 | $ | 15.75 | 1,972,046 | ||||||||

| * | Includes in the total 129,367 shares of Common Stock available for future grant and issuance under our 2006 Long Term Equity Incentive Plan. The remaining shares shown in column (c) are attributable to our 2009 Long Term Incentive Plan. |

| ** | In column (b), the weighted average exercise price is only applicable to stock options and restricted stock. |

Issuer Purchases of Equity Securities

The Company has not repurchased Common Stock since its initial public offering in November 2006.

Page 19 of 90

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA |

The following table presents selected historical consolidated statements of operations, balance sheet and other data for the periods presented and should only be read in conjunction with our audited consolidated financial statements and the related notes thereto, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are included elsewhere in this Form 10-K.

| (Dollars in thousands, except per share amounts, share amounts or

where otherwise noted) |

||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||

| Net sales |

$ | 714,231 | $ | 666,759 | $ | 934,758 | $ | 578,982 | $ | 541,797 | ||||||||||

| Cost of goods sold |

556,826 | 470,780 | 570,176 | 474,785 | 449,516 | |||||||||||||||

| Gross profit |

157,405 | 195,979 | 364,582 | 104,197 | 92,281 | |||||||||||||||

| Operating expenses: |

||||||||||||||||||||

| Selling, general and administrative |

59,564 | 67,151 | 63,417 | 54,441 | 59,598 | |||||||||||||||

| Research and development |

2,405 | 1,938 | 2,310 | 2,047 | 1,734 | |||||||||||||||

| Total operating expenses |

61,969 | 69,089 | 65,727 | 56,488 | 61,332 | |||||||||||||||

| Operating income |

95,436 | 126,890 | 298,855 | 47,709 | 30,949 | |||||||||||||||

| Interest expense, net |

28,289 | 23,313 | 34,193 | 41,559 | 58,242 | |||||||||||||||

| Foreign exchange (gains) losses, net |

659 | (769 | ) | 2,663 | 40 | (162 | ) | |||||||||||||

| Other income, net |

— | — | (386 | ) | (299 | ) | (228 | ) | ||||||||||||

| Income (loss) before income taxes |

66,488 | 104,346 | 262,385 | 6,409 | (26,903 | ) | ||||||||||||||

| Provision for income taxes |

21,333 | 41,202 | 55,202 | 11,896 | 5,914 | |||||||||||||||

| Net income (loss) |

$ | 45,155 | $ | 63,144 | $ | 207,183 | $ | (5,487 | ) | $ | (32,817 | ) | ||||||||

| Allocation of net income (loss) to common shareholders (a): |

||||||||||||||||||||

| Class A |

* | * | * | * | $ | (26,546 | ) | |||||||||||||

| Class L |

* | * | * | * | $ | 1,605 | ||||||||||||||

| Common |

$ | 45,141 | $ | 63,141 | $ | 207,150 | $ | (5,487 | ) | $ | (7,876 | ) | ||||||||

| Per share data: |

||||||||||||||||||||

| Income (loss) per share: |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Class A |

* | * | * | * | $ | (2.77 | ) | |||||||||||||

| Class L |

* | * | * | * | $ | 0.60 | ||||||||||||||

| Common |

$ | 2.11 | $ | 2.97 | $ | 9.89 | $ | (0.27 | ) | $ | (0.39 | ) | ||||||||

| Diluted |

||||||||||||||||||||

| Class A |

* | * | * | * | $ | (2.77 | ) | |||||||||||||

| Class L |

* | * | * | * | $ | 0.60 | ||||||||||||||

| Common |

$ | 2.02 | $ | 2.87 | $ | 9.54 | $ | (0.27 | ) | $ | (0.39 | ) | ||||||||

| Weighted average shares outstanding: |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Class A |

* | * | * | * | 9,595,061 | |||||||||||||||

| Class L |

* | * | * | * | 2,677,648 | |||||||||||||||

| Common |

21,421,226 | 21,258,536 | 20,956,566 | 20,676,859 | 20,270,463 | |||||||||||||||

| Diluted |

||||||||||||||||||||

| Class A |

* | * | * | * | 9,595,061 | |||||||||||||||

| Class L |

* | * | * | * | 2,677,648 | |||||||||||||||

| Common |

22,359,447 | 21,968,904 | 21,718,537 | 20,676,859 | 20,270,463 | |||||||||||||||

| * | Not applicable |

| (a) | As a result of the Company’s Class A common stock and Class L common stock being converted into a single class of common stock, the 2006 earnings per share is calculated by allocating the net income on a pro-rata basis to the weighted average number of shares of each class outstanding during the reporting period. |

Page 20 of 90

Table of Contents

| (Dollars in thousands) | ||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| Other data: |

||||||||||||||||||||

| Cash flows provided from (used in): |

||||||||||||||||||||

| Operating activities |

$ | 75,958 | $ | 174,100 | $ | 142,794 | $ | 43,441 | $ | 40,937 | ||||||||||

| Investing activities |

(31,192 | ) | (19,609 | ) | (18,536 | ) | (30,476 | ) | (15,577 | ) | ||||||||||

| Financing activities |

(113,511 | ) | (147,368 | ) | (14,591 | ) | (29,064 | ) | (55,003 | ) | ||||||||||

| Capital expenditures |

31,192 | 19,609 | 18,536 | 28,356 | 15,577 | |||||||||||||||

| Ratio of earnings to fixed charges (1) |

3.2x | 4.6x | 8.0x | 1.1x | * | |||||||||||||||

| * | Due to the loss for 2006 the coverage ratio was less than 1:1. Innophos would have had to generate additional earnings of $26,903 for 2006 to achieve a ratio of 1:1. |

| (Dollars in thousands) | ||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

| Balance sheet data: |

||||||||||||||||||||

| Cash and cash equivalents |