Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - HEALTH NET INC | d8k.htm |

| EX-99.2 - PRESS RELEASE - HEALTH NET INC | dex992.htm |

Health Net, Inc.

Health Net, Inc.

2011 Investor Day

2011 Investor Day

February 17, 2011

Exhibit 99.1 |

Cautionary Statement

2

All statements in this presentation, other than statements of

historical information provided herein, including but not limited

to the guidance for future periods included herein and the assumptions

and underlying such projections, may be deemed to be

forward-looking statements and as such are subject to a number of risks and uncertainties. These statements are based on

management’s analysis, judgment, belief and expectation only as of

the date hereof, and are subject to uncertainty and changes in

circumstances. Without limiting the foregoing, the guidance as to expected future period results and statements

including the words “believes,” “anticipates,”

“plans,” “expects,” “may,” “should,” “could,” “estimate,” “intend” and other

similar expressions are intended to identify forward-looking

statements. Actual results could differ materially due to, among

other things, health care reform, including the ultimate impact of the

Affordable Care Act, which could materially adversely affect the

company’s financial condition, results of operations and cash flows through, among other things, reduced

revenues, new taxes, expanded liability, and increased costs (including

medical, administrative, technology or other costs), or require

changes to the ways in which the company does business; rising health care costs; continued slow economic

growth or a further decline in the economy; negative prior period

claims reserve developments; trends in medical care ratios;

membership declines; unexpected utilization patterns or unexpectedly severe or widespread illnesses; rate cuts

affecting the company’s Medicare or Medicaid businesses; costs,

fees and expenses related to the post-closing administrative

services provided under the administrative services agreements entered into in connection with the sale of the

company’s Northeast business; potential termination of the

administrative services agreements by the service recipients

should the company breach such agreements or fail to perform all or a

material part of the services required thereunder; any

liabilities of the Northeast business that were incurred prior to the

closing of its sale as well as those liabilities incurred

through the winding-up and running-out period of the Northeast

business; litigation costs; regulatory issues with agencies such

as the California Department of Managed Health Care, the Centers for Medicare and Medicaid Services and state

departments of insurance, including the continued suspension of the

marketing of and enrollment into the company’s Medicare

products for a significant period of time, which could have a material adverse impact on the company’s Medicare

business; operational issues; investment portfolio impairment charges;

volatility in the financial markets; and general business and

market conditions. Additional factors that could cause actual results to differ materially from those reflected in

the forward-looking statements include, but are not limited to, the

risks discussed in the “Risk Factors” section included

within the company's most recent Annual Report on Form 10-K

and subsequent Quarterly Reports on Form 10-Q filed with

the Securities and Exchange Commission (“SEC”), and the risks

discussed in the company’s other filings with the SEC.

Readers are cautioned not to place undue reliance on these

forward-looking statements. The company undertakes no

obligation to publicly revise its guidance, the assessment of the

underlying assumptions or any of its forward-looking

statements to reflect events or circumstances that arise after the date

of this presentation. |

3

Non-GAAP Measures

These presentations include quarterly and full year

income statement measurements that are not calculated

and presented in accordance with Generally Accepted

Accounting Principles. Audience participants should refer

to the financial table included in the Appendix to the

presentations, which also is available on the company’s

website at www.healthnet.com, and reconciles certain

non-GAAP financial information to GAAP financial

information. |

4

Agenda

8.30 a.m. –

9.00 a.m.

Welcoming Remarks

Angie McCabe, Vice President, Investor Relations

Introduction and Strategic Overview

Jay Gellert, President and Chief Executive Officer

9.00 a.m. –

10.00 a.m.

Commercial Growth and Margin Expansion

Steven Sell, President, Western Region Health Plan

Underwriting and Actuarial Review

Richard Hall, FSA, MAAA, Chief Actuarial Officer

10.00 a.m. –

10.15 a.m.

BREAK

10.15 a.m. –

11.15 a.m.

Medicare and State Programs

Scott Kelly, Chief Government Programs Officer

Federal Services

Steven Tough, President, Government Programs

11.15 a.m. –

12.15 p.m.

Operations Review

Juanell

Hefner, Chief Customer Services Officer

Jay Gellert, President and Chief Executive Officer

Financial Review

Joseph Capezza, Chief Financial Officer

12.15 p.m. –

12.30 p.m.

Closing Remarks

Jay Gellert, President and Chief Executive Officer

Note: Presentation times subject to change. |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Strategic

Overview Strategic Overview

Jay Gellert

President and

Chief Executive Officer |

7

Emerging Environment

Emerging Environment

•

Economy is driving change

•

Federal and state budget pressures

will affect health care

•

Future implementation of Affordable Care Act

remains to be defined

•

Diverse book of businesses where value

differentiation is key |

8

Our Strategy To Date

Our Strategy To Date

•

Build value-based products

•

Diverse book of businesses

–

Risk and fee

–

Medicaid, Medicare, TRICARE and commercial

•

Deemphasize volatile segments

–

e.g., individual

•

Invest in G&A efficiencies

•

Dispose of weak assets

•

Strengthen balance sheet |

9

2011 Key Milestones

2011 Key Milestones

•

Stronger risk membership

•

TRICARE to ASO

•

Maintain low G&A ratio

•

Expand commercial margins

•

Continue to add new products

•

Use cash for benefit of shareholders |

10

Future Opportunities

Future Opportunities

•

Broadening commercial business

•

Rebound in Medicare

•

Medicaid expansion

•

Department of Defense options

•

G&A leverage

•

Balance sheet flexibility |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Commercial

Growth Commercial Growth

and Margin Expansion

and Margin Expansion

Steven Sell

President, Western Region Health Plan |

Commercial: Positioned for Growth

Commercial: Positioned for Growth

•

Economy is driving HMO demand

•

Health Net has a strong and sustainable

HMO market position

•

Tailored products and networks drive growth

•

Margin expansion opportunities

13 |

Economy Driving Demand

•

Market research shows customers looking for:

–

Affordable solutions

–

Convenient access

–

Clear and simple choices

•

Consumer-directed health plans (CDHP)

show some stress

–

Among highest premium increases

•

HMO value proposition: “back to the future”

–

Affordable premiums

–

Primary care leadership

–

Comprehensive benefits / low copays

14 |

Health Care Reform

Health Care Reform

Favors Managed Care

Favors Managed Care

•

PPO benefit advantages being reduced

–

Elimination of annual and lifetime limits in 2011

–

Zero copay

preventive care in 2011

–

Deductible caps coming in 2014

•

Traditional ASO vs. risk

–

Risk still best value in California –

even for large,

national employers

•

Providers will play more prominent role

–

Incentives in law to create managed care

infrastructure (e.g., accountable care organizations)

–

Seeking to balance Medicare and Medicaid revenue

pressures with commercial growth

15 |

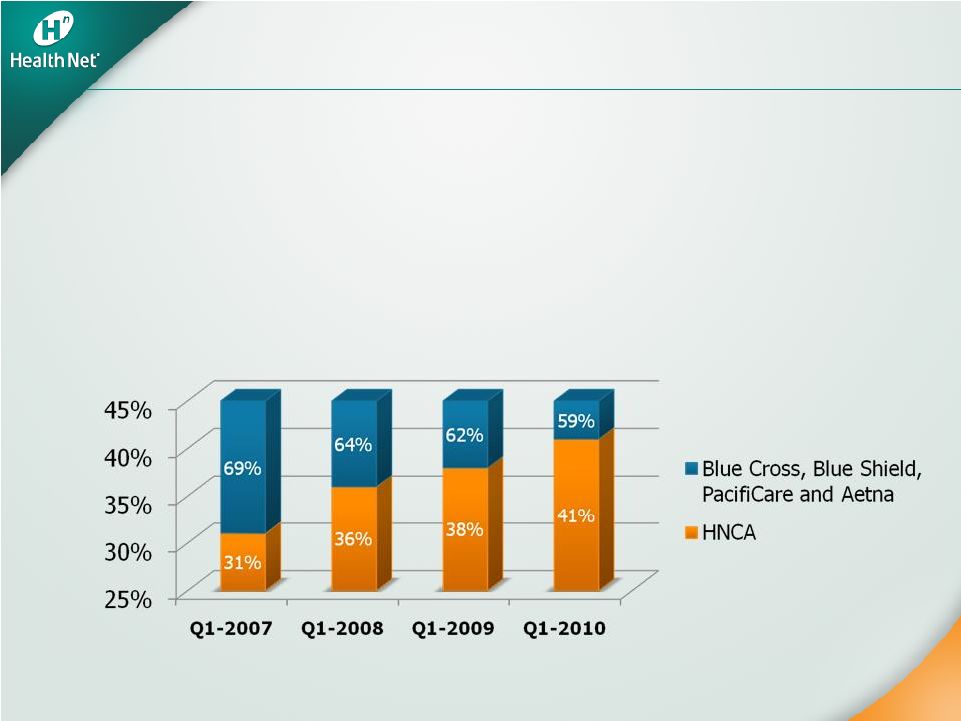

16

Health Net:

Health Net:

Strong HMO Market Share

Strong HMO Market Share

•

Dominant network HMO player in California market

•

Steady market share growth over the last four years

•

Small group market share increase: 31 percent

to 41 percent in the past four years

Source: Data from Department of Managed Health Care and excludes Kaiser and all PPO

data. Percent share reflects percent share of top statewide competitors.

Small Group Network Model HMO Market Share |

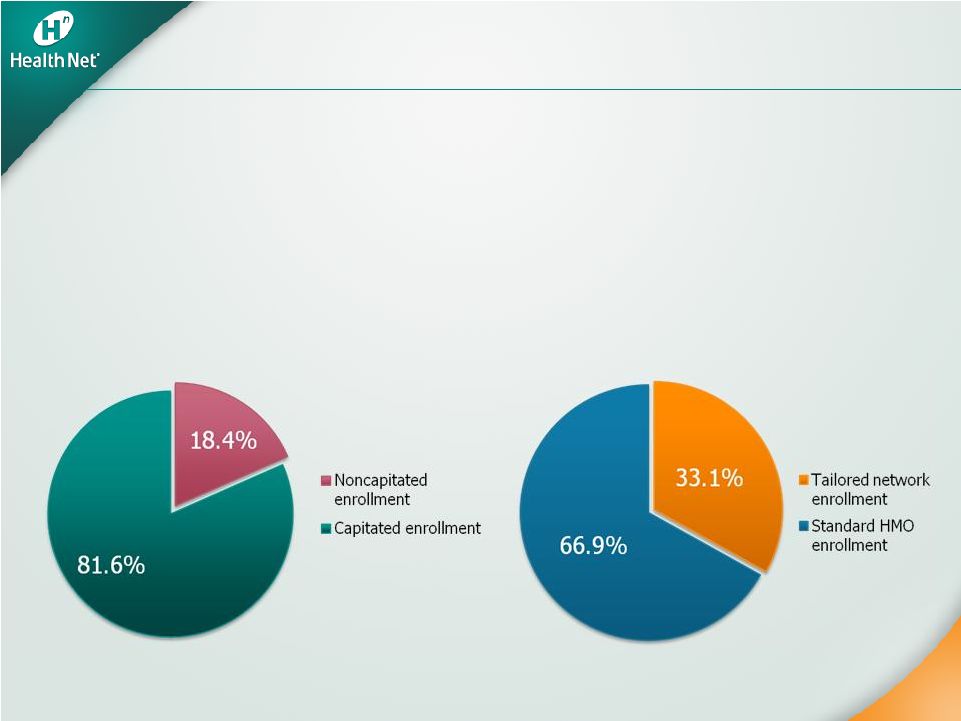

The Power of

Capitation The Power of Capitation

•

Focuses providers on cost management and commercial growth

•

Stabilizes trends and makes them more predictable

•

Reduces administrative costs as claims processing is delegated

Source: Based on Health Net internal data as of December 31, 2010.

More than 80 percent of HNCA’s

commercial membership is enrolled

in capitated

medical groups

More than 30 percent of HNCA’s

commercial capitated

membership is

enrolled in tailored network plans

17 |

•

Drives volume to “high value”

providers (low cost/high quality)

•

Employer premiums up to 30 percent lower

•

Offers comprehensive coverage

•

Increased interest in new geographies and segments

Strong and Evolving Tailored Networks

Strong and Evolving Tailored Networks

18

Source: Based on Health Net internal data

HNT Tailored Network Membership |

How

Tailored Network Products Work How Tailored Network Products Work

•

Foundation is traditional HMO capitated

networks

–

Broad physician panel in group or IPA

–

Includes wide range of institutional options

–

Comprehensive benefits with low copays

•

Tailored networks

–

Include cost-effective provider groups

•

Stronger partnerships built on higher volume

and joint marketing

–

Includes select institutional options that optimize

cost and quality

•

Substantial savings accrue to customer by excluding

high cost, geographically remote institutions

–

Comprehensive benefits with low copays

19 |

Growth with Margin Expansion

Growth with Margin Expansion

•

Strategically changing mix

–

Segment: small group and mid-market

–

Product: tailored network products

–

Geographic: Southern California vs.

Northern California

•

Targeted sales and improved retention

•

Disciplined underwriting and pricing

•

Continued focus on health care cost containment

–

Stronger provider partnerships

20 |

Well Positioned for Growth

Well Positioned for Growth

•

Growing market share in California

•

Product solutions meeting market demand

–

Opportunities to apply solutions to

Arizona and Oregon

•

Margin expansion driven by:

–

Improved product and segment mix

–

Consistent underwriting and pricing discipline

•

Provider-payor

relationships evolving

21 |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Underwriting

and Underwriting and

Actuarial Review

Actuarial Review

Richard T. Hall, FSA, MAAA

Chief Actuarial Officer |

A

New Commercial Environment A New Commercial Environment

•

Underwriting and pricing discipline

•

Return to HMO plans / pressure on

less managed plans

•

Regulatory pressure and individual

market issues

•

Providers seeking commercial share to

offset growing cost shift

•

2011 pricing assumptions and outlook

24 |

Underwriting and Pricing Discipline

Underwriting and Pricing Discipline

•

Rigorous planning process

–

Analyze membership

–

Identify best gross margin opportunities

–

Sensitivity analyses

•

Targeted geographies, segments and

products where we have a clear

competitive advantage

•

Enhanced sales and underwriting process to

optimize profitable membership growth

25 |

26

2010 Results Affirm Strategy

2010 Results Affirm Strategy

•

Targeted pricing to improve mix in large group

–

MCR of renewing groups in California was better

than canceled groups by 100 basis points in 2010

–

Implemented processes to achieve an improved

retention rate

•

From 81 percent in 2010 to 91 percent in

January 2011

•

Industry standard is approximately 82 percent

•

Membership and margin opportunities in small group segment

–

MCR of renewing groups was better than canceled groups by

210 basis points in 2010 |

Return to HMO

Return to HMO

•

Demonstrable premium differential for

equivalent benefits

•

ASO vs. risk: California experience

•

Growing out-of-pocket limits not sustainable

for members and providers

•

Health care reform and economy limit ability

to shift costs to employees

27 |

Premium Differentials

Premium Differentials

•

Traditional HMO vs. PPO –

HMO is 30 percent less

–

Example: Los Angeles County

–

HMO –

$30 copay

/ $2,000 out-of-pocket maximum

–

PPO –

$30 copay

in-network / $500 deductible /

$2,000 out-of-pocket maximum

•

Tailored network 10 percent to 25 percent less than

traditional HMO

–

Targeted to specific, cost-effective provider groups

–

Better performing MCR than traditional HMO

–

Less expensive than Kaiser in many cases

28 |

Regulatory Pressure

Regulatory Pressure

and Individual Market Issues

and Individual Market Issues

•

Cautious approach to individual market

•

Emerging regulatory environment

•

External focus on rate increases

•

Preparing for implementation of exchanges

29 |

Changing the Provider-Payor

Changing the Provider-Payor

Paradigm

Paradigm

30

•

Market driving to integrated approach

•

Health Net offers value to providers

–

People and relationships

–

True local presence

–

Business model

–

All segment focus

–

Providers seeking to retain and build

commercial market share

•

Joint efforts in cost and quality management |

2011 Commercial Pricing Assumptions

2011 Commercial Pricing Assumptions

•

2010 physician and institutional utilization

moderated from 2009

•

2011 pricing assumes upward pressure on

physician and institutional utilization

•

2011 unit cost trends expected to be lower

than 2010 trends

•

2011 pharmacy cost increases expected to

be similar to 2010

31 |

Beyond 2011

Beyond 2011

•

Sectoral

–

not cyclical –

changes in market

–

Driven by health care reform and economy

•

Trends remain moderate by historical standards

–

Growing impact of tailored network plans

and focus on affordability

•

Steadily growing influence of capitated

systems

•

Institutional providers seek new partnerships to

achieve cost effectiveness and enhance

competitive position

32 |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Medicare

and Medicare and

State Programs

State Programs

Scott Kelly

Chief Government

Programs Officer |

Solid Medicare Outlook

Solid Medicare Outlook

•

Balance Medicare Advantage revenue,

benefits/premiums and costs to ensure:

–

Stable margins

–

Continued competitive product offerings

•

Continued focus on capitated

networks

•

Enhance strategic provider partnerships in

coordination with commercial business

•

Position Part D book for 2012 growth

•

Strengthening operations and controls to

respond to CMS sanction issues

35 |

Medicare Advantage: 2011

Medicare Advantage: 2011

•

Building from solid 2010

•

January enrollment results better than

initial expectations

•

Total revenues PMPM expected to be up 1.5 percent

–

Member premiums up 3.4 percent PMPM

•

Expect MCR to be flat year-over-year

–

Health care cost stability

–

Benefit changes: hospital and outpatient

copays, deductibles

•

Preparing for 2012 bidding process

36 |

Medicare Part D

Medicare Part D

•

2010 margins maintained by favorable

prescription drug performance and unit costs

•

2011 enrollment expected to decline

14 percent to 16 percent compared with 2010

•

Guiding to breakeven 2011 performance due to

effects of CMS sanctions

37 |

CMS

Sanctions CMS Sanctions

What Happened?

•

CMS identified issues in HNT’s

Part D program

What’s Next?

•

Corrective actions are in process

•

Plan to review corrective actions with CMS in

second quarter of 2011

•

Broader compliance initiatives in place to

ensure appropriate administration of

government business overall

38 |

Medicare Advantage

Medicare Advantage

Provider Networks

Provider Networks

•

Nearly 40 percent of health care costs capitated

–

Over 50 percent in California market

–

More than 135 provider groups in 21 counties

•

Mostly percent of premium contracts

•

Collaboration with organized health systems to

reduce total costs to achieve margin stability

•

Working closely on risk adjuster capture and

accuracy with key groups

39 |

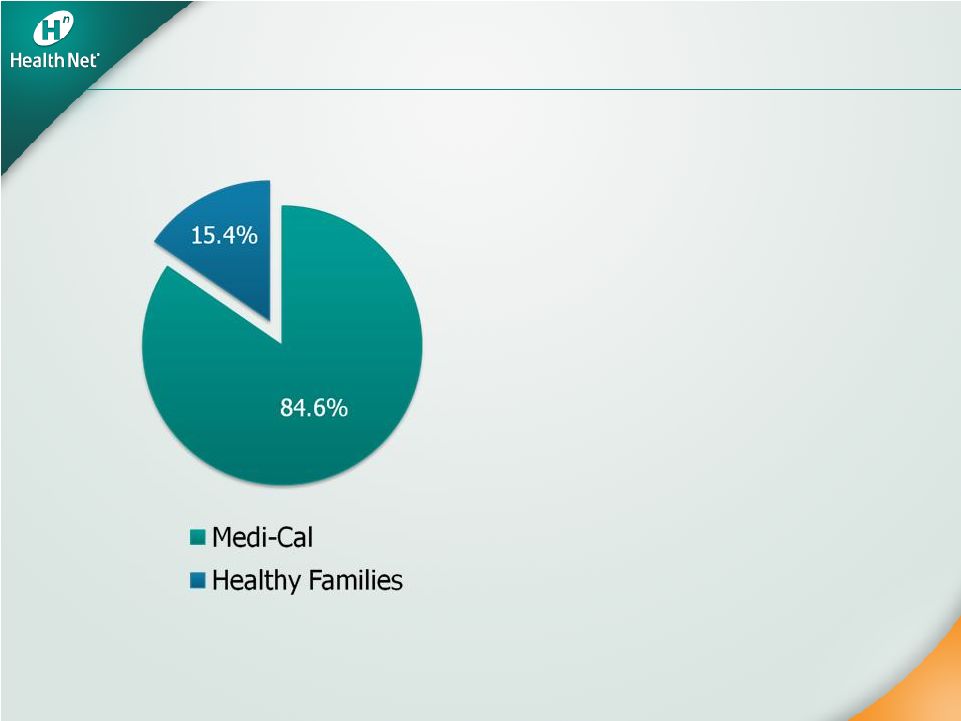

State Health

Programs State Health Programs

•

Potential for growth

–

Health care reform

–

Seniors and Persons

with Disabilities (SPD)

–

New counties

40

Total State Program Revenues |

Medi-Cal Position

Medi-Cal Position

•

753,700 members at year-end 2010, an

increase of 7 percent year-over-year

•

Second largest Medi-Cal plan in California

–

58 percent of membership in

Los Angeles County

–

34 percent in Central Valley

•

Market share stable at over 24 percent

•

Remain the highest ranking Medi-Cal HMO plan

in California by U.S. News and World Report

41 |

2011 Medi-Cal Outlook

2011 Medi-Cal Outlook

•

Expect 6 percent membership growth

•

Maintain stable financial performance

–

Rate environment understood

•

Key strategic position for health care reform

•

SPD program offers potential significant

growth opportunity

42 |

Healthy Families

Healthy Families

•

145,800 members at year-end 2010, a

decrease of 4.7 percent year-over-year

–

Market share remains flat as general

statewide enrollment declines

•

2011 program outlook

–

Expect 6 percent membership decline

–

Margin stable

43 |

State Programs Provider Networks

State Programs Provider Networks

•

80 percent of State Programs enrollment

linked to capitated

provider groups

•

Over 45 percent of health care costs under

capitated

arrangements

–

75 percent of physician costs

–

27 percent of hospital costs

•

Noncapitated

hospital rates on Medicaid

fee schedule

44 |

Stable Government Programs

Stable Government Programs

•

Margin stability in long-standing Medicare

Advantage network-model markets

–

Predictable cost structure

–

Solid membership retention

•

Medi-Cal: prepare for growth of SPDs

and

health care reform expansion

•

2011 focus on strong operational and

regulatory performance and preparations

for 2012 open enrollment

45 |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Federal

Services Federal Services

Steve Tough

President,

Government Programs |

Government Contracts Highlights

Government Contracts Highlights

•

New TRICARE contract begins April 1, 2011

•

ASO, fee-based, five-year contract

•

Improves company balance between risk

and fee-based businesses

•

Opens door to new opportunities as

Department of Defense (DoD) faces

budget pressures

48 |

2011: A Transition Year

2011: A Transition Year

•

Contract financial structure changes from cost

plus risk sharing to cost plus incentive

–

New contract accounted for as ASO

•

2011 includes ¼

year of current contract,

¾

year of new contract, plus current contract

phase-out revenues and expenses

–

Expect 2011 pretax contribution from

Government Contracts to decline by

approximately $25 million from 2010

49 |

Current Contract to New Contract:

Current Contract to New Contract:

Incentive and Risk Changes

Incentive and Risk Changes

•

Fixed-dollar underwriting fee

•

Administrative efficiencies under a fixed

administrative budget

•

Underwriting incentives –

network discount, network

usage and national cost trend

–

National cost trend incentive based on our PMPM

health care cost trend for contractor enrollees vs.

national health care expenditure per capita trend

•

Performance guarantees and incentives

•

Award fee calculated twice yearly (Q2 and Q4) under

new contract vs. quarterly under current contract

50 |

Growth Opportunities

Growth Opportunities

•

Military & Family Life Consultant (MFLC)

program success

–

Apply MFLC model to other federal customers

•

DoD

efforts under way –

budget challenges create

potential opportunities

–

Extend services to National Guard and Reservists

–

Managed solutions for TRICARE for Life

•

Behavioral health outreach requirements continue to

grow as needs escalate

•

Veterans Affairs (VA) seeks expansion of its rural

behavioral health support program

•

Existing services and products have application to other

government programs

51 |

Key

Takeaways Key Takeaways

•

Well positioned to continue leadership role

with DoD

and VA

•

Transition to new contract on track

•

Wide range of behavioral health opportunities

–

Build on MFLC success

•

Continue to expand VA and state

administrative footprint

52 |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Operations

Review Operations Review

Jay Gellert

President and

Chief Executive Officer

Juanell Hefner

Chief Customer Services Officer |

Operations

Strategy Operations Strategy

and Stranded Costs

and Stranded Costs

•

Announced a three-year effort to restructure

operations in 2007

•

Built around these goals:

Optimize outsourcing

Eliminate operations and system inefficiencies

Enhance scalability

Improve competitive platform

•

Reduce “stranded costs”

associated with sale of

Northeast and new TRICARE contract

•

Goal: support sustained long-term margin improvement

55 |

G&A Expense

Reductions G&A Expense Reductions

•

Invested $145 million after tax in G&A expense

reduction activities over the last three years

(i.e., severance, asset impairment, etc.)

•

Without these investments, Western Region G&A

would have been higher by approximately

$100 million pretax in 2010

•

Achieved additional savings in the Northeast and

Government Contracts division

•

Targeting an additional $100 million in pretax

savings in 2011 and 2012 to compensate for

Northeast stranded costs and TRICARE gap

–

Savings primarily from headcount reductions

56 |

Northeast

Wind-down and Overhead Reductions

Northeast Wind-down and

Overhead Reductions

Operations Strategy

Operations Strategy

•

Infrastructure outsourcing

•

Application outsourcing

•

Business process outsourcing

•

Management restructuring

•

Operational efficiencies

•

Vendor management

•

Wind-down of NE operations

•

Finance outsourcing

•

Additional operations outsourcing

•

Managerial restructuring

•

Arizona systems migration

•

Print and fulfillment

•

Real estate cost improvements

•

Operational efficiencies

Areas of Savings

Areas of Savings

57 |

Improved

Operations Improved Operations

•

Operations are better integrated

–

More consistent procedures

–

Greater flexibility to use staff and

resources efficiently

–

Improved performance management

•

Have realized benefits from business process

outsourcing of noncustomer facing functions

–

Scalability

–

Cost improvements

–

High levels of quality and performance

58 |

Improved

Operational Performance Improved Operational Performance

•

Claims

–

Accuracy

–

Claims turnaround time

•

Call center performance

–

First call resolution

•

Enrollment and eligibility performance

–

Enrollment accuracy

–

Enrollment timeliness

–

Eligibility accuracy

All key operational metrics have improved or

All key operational metrics have improved or

stabilized over the past three years

stabilized over the past three years

59 |

Positioned for

the Future •

Improved speed to market

–

Outsourcing allows for rapid capacity

ramp-up to support growth

–

Can leverage vendor expertise and

resources to create new and expanded

operational capabilities

•

Technology infrastructure now positioned to

support future performance and growth

–

New equipment and software upgrades

–

Network upgrades

–

Investment in strategic applications

60 |

Key

Takeaways Key Takeaways

•

Further G&A reductions will contribute

to margin improvement

•

Operations positioned to support

long-term growth

•

G&A positioned to offset minimum

MCR requirements

•

Eliminating stranded costs associated with

Northeast business and new TRICARE contract

•

Improved operations enhance capacity to deliver

new products and services

61 |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Financial

Review Financial Review

Joseph C. Capezza

Chief Financial Officer |

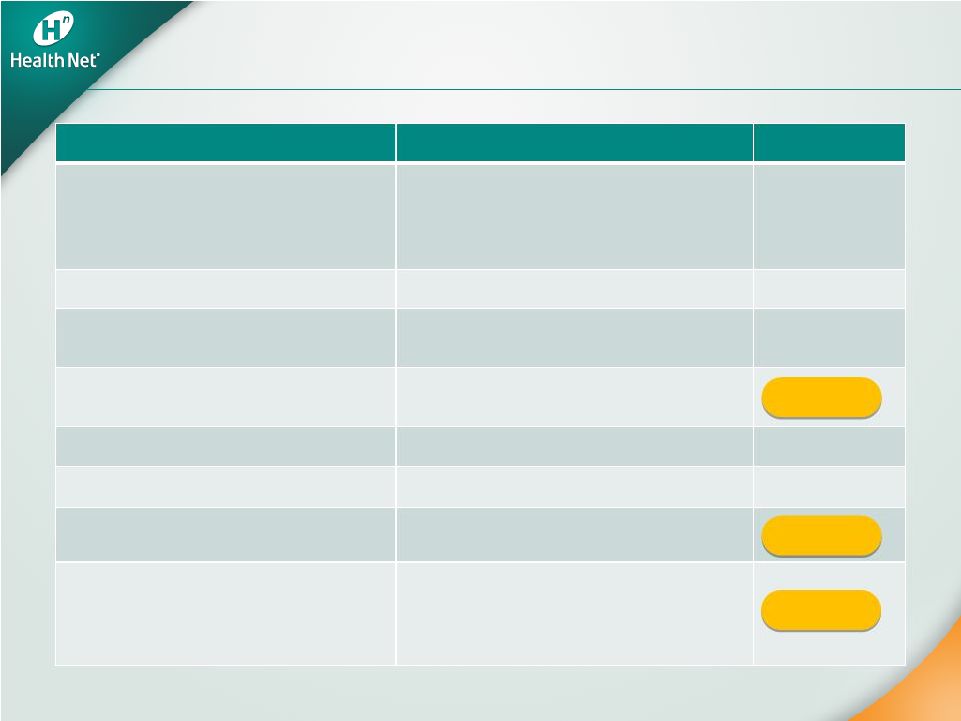

64

Original Guidance

Actual

Year-end membership

•

Commercial: -1% to -2%

•

Medicaid: +5% to +6%

•

Medicare Advantage: -2% to -3%

•

PDP: +1% to +2%

-4.4%

+5.1%

-2.2%

-7.2%

Consolidated revenues

$13 billion to $13.5 billion

$13.6 billion

Commercial premium yields

(a)

~ 8.3% to 8.8%

(Western Region 2009: ~$316 PMPM)

7.9%

Commercial health care cost

trends

(a)

~ 20-40 bps < premium yields

(Western Region 2009: ~$274 PMPM)

Government Contracts ratio

~ 94.5% to 95%

94.7%

G&A Expense ratio

~ 8.8% to 9%

8.9%

Weighted-average fully

diluted shares outstanding

103 million to 104 million

GAAP EPS

Combined Western Region

Operations and Government

Contracts EPS

$1.92 to $2.02

$2.32 to $2.42

$2.06

(a)

Commercial premium yields and commercial health care cost comparisons are on a same-store

basis for the company’s Western Region Operations only for both 2009 and

2010. 80 bps

80 bps

99.2 M

99.2 M

$2.60

$2.60

2010 Results

2010 Results |

65

A Solid 2010 Sets Stage for 2011

A Solid 2010 Sets Stage for 2011

•

Strong year: met or exceeded key commitments

•

Commercial margin expansion

–

2010 gross margin increased 13 percent to

$47 per member per month (PMPM)

•

Commercial enrollment stabilized in the second half

of 2010

•

Strong cash: operating cash flow of $271 million, or

1.3 times net income

•

Repurchased 9 percent of 2009 shares outstanding

•

Further margin improvement opportunities |

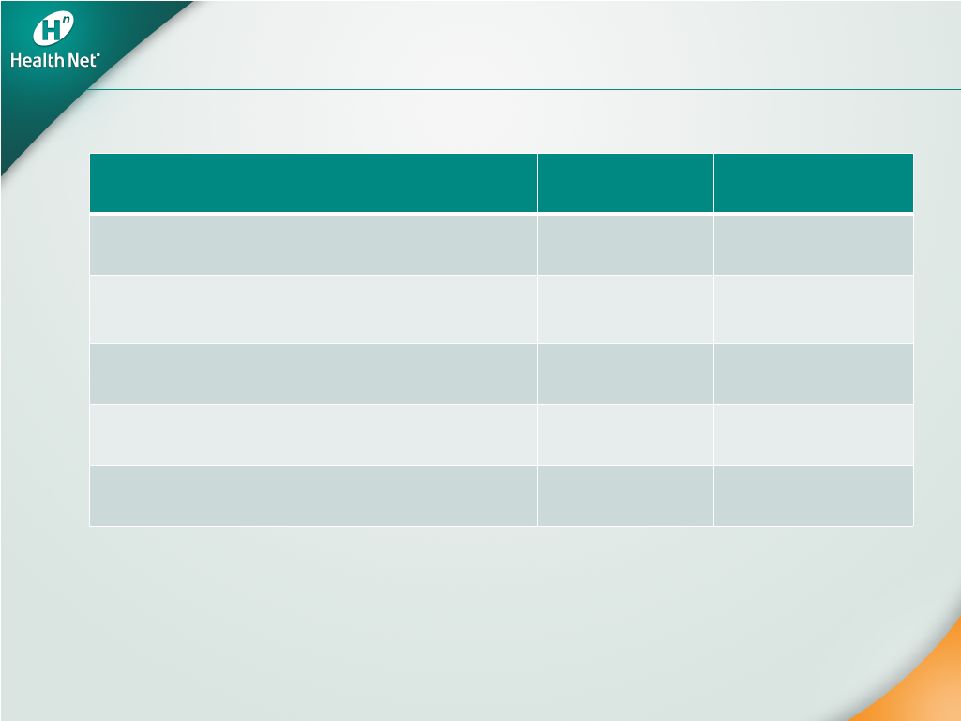

Stronger Balance

Sheet Stronger Balance Sheet

66

2010

2009

Current ratio

1.70

1.68

Adjusted days claims payable

*

57.2

54.2

Debt-to-total capital ratio

19%

26%

Tangible net equity per share

$11

$10

Risk-based capital

>400%

>400%

*See Appendix for a reconciliation of this metric to the comparable GAAP financial

measure |

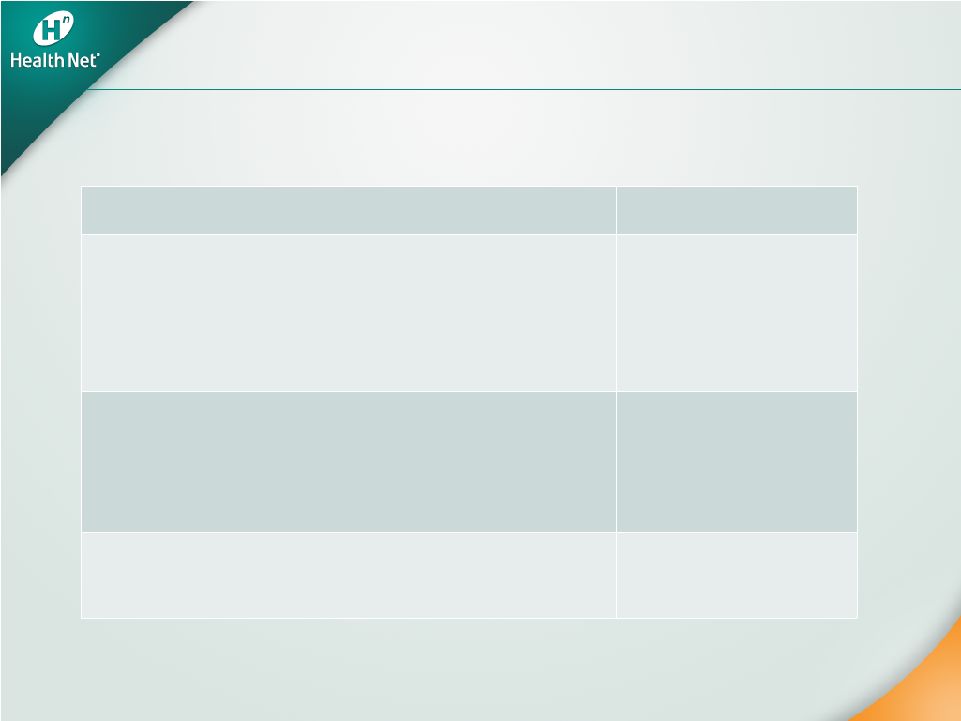

Northeast

Transaction Net Cash Northeast Transaction Net Cash

67

2009

$377 million

2010

$63 million

2011

$80 million to $100 million

Total

$520 million to $540 million

Original

Guidance

$490 million to $610 million |

68

2011 Earnings Guidance

2011 Earnings Guidance

Year-end membership

(a)

•

Medicaid: +6% to +7%

•

Medicare Advantage

(d)

: -15% to -17%

•

Total Western Region Operations

medical membership: +2% to +3%

•

PDP

(d)

: -14% to -16%

Consolidated revenues

(b)(d)

$12.0 to $12.5 billion

Commercial premium yields

(a)

~ 7.8% to 8.3%

Commercial health care cost trends

(a)

G&A expense ratio

(a)

~ 8.7% to 8.9%

Weighted-average fully

diluted shares outstanding

(c)

96 million to 97 million

GAAP EPS

(c)(d)

Combined Western Region Operations and

Government Contracts segments EPS

(c)(d)

At least $2.05

Commercial: +1% to +2%

Commercial: +1% to +2%

~

~

40

40

to

to

60

60

bps

bps

<

<

Premium

Premium

Yields

Yields

(a)

For the company’s Western Region Operations segment

(b)

For the combined Western Region Operations and Government Contracts segments

(c)

The company’s guidance does not include the impact of share repurchases other than to

counter dilution. (d)

Includes

the

impact

of

the

CMS

sanctions

previously

announced

on

November

19,

2010

At least $2.75

At least $2.75 |

69

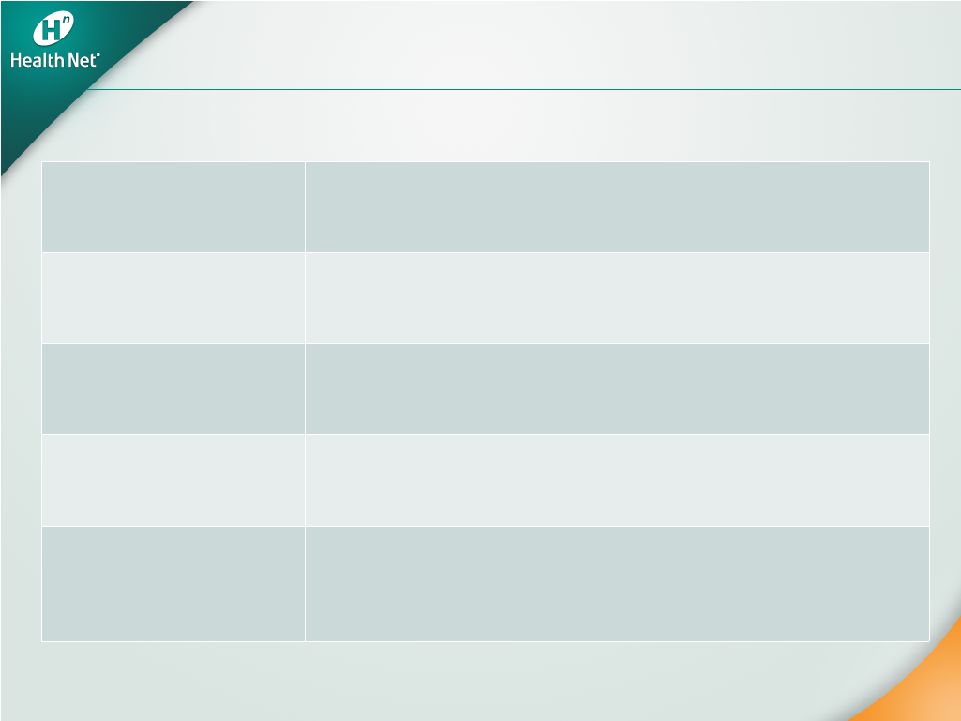

2011 Cash at Parent

2011 Cash at Parent

Beginning cash (12/31/10)

$204

Sources of cash

Net cash flow from subsidiaries

NE proceeds

$225 -

$235

$80 -

$100

Uses of cash

Share repurchases through 1/31/11

Other corporate uses

$34

~$85

Ending cash*

(12/31/11)

~$390 -

$420

*Excludes the impact of any future share repurchases

$ in millions |

70

HNT: On Track

HNT: On Track

•

Continued commercial gross margin expansion

•

Commercial membership growth

•

Seamless transition to new TRICARE contract

•

Continued strong cash flow performance

–

Opportunities for further capital deployment |

Appendix

Appendix |

Disclosures

Regarding Disclosures Regarding

Non-GAAP Financial Information

Non-GAAP Financial Information

72

Q4 2010

Q3 2010

Q4 2009

FY 2010

FY 2009

(1)Reserve for Claims and Other Settlements

$942.0

$904.4

$951.7

$942.0

$951.7

Less: Reserve for Claims and Other Settlements for Divested Businesses

-

-

-

-

-

Less: Capitation Payable, Provider and Other Claim Settlements and Medicare Part D

(108.7)

(130.0)

(162.8)

(108.7)

(162.8)

(2)Reserve

for

Claims

and

Other

Settlements -

Adjusted

$833.3

$774.4

$788.9

$833.3

$788.9

(3)Health Plan Services Cost

$2,100.0

$2,134.7

$2,557.1

$8,609.1

$10,732.0

Less: Health Plan Services Cost for Divested Businesses

-

-

(460.7)

-

(2,123.0)

Less: Capitation Payable, Provider and Other Claim Settlements and Medicare Part D

(762.6)

(804.4)

(818.4)

(3,291.1)

(3,296.0)

(4)Health Plan Services Cost -

Adjusted

$1,337.4

$1,330.3

$1,278.0

$5,318.0

$5,313.0

(5)Number of Days in Period

92

92

92

365

365

=

(1)

/

(3)

*

(5)

Days

Claims

Payable

-

(using

end

of

period

reserve

amount)

41.3

39.0

34.2

39.9

32.4

=

(2)

/

(4)

*

(5)

Days

Claims

Payable

-

Adjusted

(using

end

of

period

reserve

amount)

57.3

53.6

56.8

57.2

54.2

Management believes that adjusted days claims payable (adjusted for divested businesses,

capitation, provider and other claim settlements and

Medicare

Part

D),

a

non-GAAP

financial

measure,

provides

useful

information

to

investors

because

the

adjusted

days

claims

payable

calculation excludes amounts related to divested businesses and health care costs for which no

or minimal reserves are maintained. Therefore,

management

believes

that

adjusted

days

claims

payable

may

present

a

more

accurate

reflection

of

days

claims

payable

calculated

from claims-based reserves than does GAAP days claims payable, which includes such costs.

This non-GAAP financial information should be considered in addition to, not as a

substitute for, financial information prepared in accordance with GAAP. The following table provides a

reconciliation of the differences between adjusted days claims payable and days claims payable,

the most directly comparable GAAP financial measure. You are encouraged to evaluate

these adjustments and the reasons we consider them appropriate for supplemental analysis. In

evaluating the adjusted amounts, you should be aware that we have incurred expenses that are

the same as or similar to some of the adjustments in the current presentation and we may

incur them again in the future. Our

presentation

of

the

adjusted

amounts

should

not

be

construed

as

an

inference

that

our

future

results

will

be

unaffected

by

unusual

or

non-recurring items.

$ in millions |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |

Closing

Remarks Closing Remarks

Jay Gellert

President and

Chief Executive Officer |

75

HNT: Building Shareholder Value

HNT: Building Shareholder Value

•

Strategic response to changing environment

•

Diverse book of stable businesses

•

Opportunities for growth and further

gross margin and G&A improvements

•

Financial flexibility |

Health Net,

Inc. Health Net, Inc.

2011 Investor Day

2011 Investor Day |