Attached files

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form

10-K

(Mark

One)

[X] ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the fiscal year ended December 31,

2009

OR

[ ] TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For

the transition period ________ to ________

|

Commission

File Number 1-12368

|

|

Tandy Leather Factory,

Inc.

|

|

(exact

name of registrant as specified in its

charter)

|

|

Delaware

|

75-2543540

|

|

|

(State

or other jurisdiction of incorporation)

|

(IRS

Employer Identification Number)

|

|

|

1900

Southeast Loop 820, Fort Worth, TX 76140

|

817/872-3200

|

|

|

(Address

of principal executive offices)

|

(Registrant’s

telephone number, including area code)

|

|

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of Each Class

|

Name

of Each Exchange on Which Registered

|

|

|

Common

Stock, par value $0.0024

|

NYSE

Amex

|

Securities registered pursuant to

Section 12(g) of the Act: NONE

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act Yes [ ] No

[X]

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes

[ ] No [X]

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes [X] No [ ]

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of

this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files). Yes

[ ] No [ ] (The registrant is not

yet required to submit Interactive Data)

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant's knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. [ ]

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer. See definition of

“accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange

Act. (Check one): Large accelerated filer

[ ] Accelerated filer

[ ] Non-accelerated filer [X] Smaller reporting

company [ ]

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Act). Yes [ ] No [X]

The

aggregate market value of the common stock held by non-affiliates of the

registrant was approximately $17,145,950 at June 30, 2009 (the last business day

of its most recently completed second fiscal quarter). At March 10,

2010, there were 10,141,522 shares of the registrant's common stock

outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the registrant’s definitive Proxy Statement for the Annual Meeting of

Stockholders to be held on May 18, 2010, are incorporated by reference in Part

III of this report.

TABLE

OF CONTENTS

|

Item

|

Page

|

|

|

Part

1

|

||

|

1

|

Business

|

1

|

|

1A

|

Risk

Factors

|

5

|

|

2

|

Properties

|

6

|

|

3

|

Legal

Proceedings

|

7

|

|

4

|

Submission

of Matters to a Vote of Security Holders

|

7

|

|

Part

II

|

||

|

5

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

7

|

|

6

|

Selected

Financial Data

|

8

|

|

7

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

9

|

|

7A

|

Quantitative

and Qualitative Disclosures about Market Risk

|

13

|

|

8

|

Financial

Statement and Supplementary Data

|

14

|

|

9

|

Change

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

30

|

|

9A

|

Controls

and Procedures

|

30

|

|

9B

|

Other

Information

|

30

|

|

Part

III

|

||

|

10

|

Directors,

Executive Officers and Corporate Governance

|

30

|

|

11

|

Executive

Compensation

|

30

|

|

12

|

Security

Ownership of Certain Owners and Management and Related Stockholder

Matters

|

30

|

|

13

|

Certain

Relationships and Related Transactions and Director

Independence

|

30

|

|

14

|

Principal

Accountant Fees and Services

|

30

|

|

Part

IV

|

||

|

15

|

Exhibits,

Financial Statement Schedules

|

31

|

PART

I

ITEM

1. BUSINESS

General

We are a

retailer and wholesale distributor of a broad line of leather and related

products, including leather, leatherworking tools, buckles and adornments for

belts, leather dyes and finishes, saddle and tack hardware, and do-it-yourself

kits. We also manufacture leather lacing and some of our do-it-yourself

kits. During 2009, our consolidated sales totaled $54.5 million of

which approximately 13% were export sales. We maintain our principal

offices at 1900 Southeast Loop 820, Fort Worth, Texas 76140. Our

common stock trades on the NYSE Amex under the symbol "TLF."

Our

company was founded in 1980 as Midas Leathercraft Tool Company, a Texas

corporation. Midas' original business activity focused on the

distribution of leathercraft tools. In addition, the founders of

Midas entered into a consulting agreement with Brown Group, Inc., a major

footwear retailer, as a result of their proposal to develop a multi-location

chain of wholesale stores known as "The Leather Factory." In 1985,

Midas purchased the assets of The Leather Factory from Brown Shoe Group, which

then consisted of six wholesale stores.

In 1993,

we changed our name to "The Leather Factory, Inc.", and reincorporated in the

state of Delaware in 1994. In 2005, we changed our name to Tandy

Leather Factory, Inc.

Our

Development in Recent Years

We have

expanded our wholesale chain by opening new stores and by making numerous

acquisitions of small businesses in strategic geographic locations including the

acquisition of our Canadian distributor, The Leather Factory of Canada, Ltd., in

1996. By 2000, we had grown to 27 Leather Factory stores located in

the United States and two Leather Factory stores in Canada. In

November 2000, we acquired the operating assets of two subsidiaries of

Tandycrafts, Inc. to form Tandy Leather Company. In 2002, we began

opening retail stores under the "Tandy Leather" name. During that

year, Tandy Leather purchased four independent leathercraft retail stores and

opened another 10 stores. We also opened our thirtieth Leather

Factory store - our third in Canada. In 2003, we opened 12 Tandy

Leather retail stores. In 2004, we purchased three independent

leathercraft retail stores and opened an additional nine stores in the

U.S. We also opened another store in Canada which is operating as a

Tandy Leather retail store. In November 2004, we acquired all of the

issued and outstanding shares of capital stock of Heritan Ltd. and its parent,

our primary Canadian competitor, headquartered in Barrie,

Ontario. The acquisition resulted in an additional three retail

stores in Canada, bringing the total locations in Canada to seven - three

Leather Factory stores and four Tandy Leather stores. In 2005, we

opened eight Tandy Leather retail stores. In 2006, we opened 11 Tandy

Leather retail stores and converted one wholesale store to a retail

store. In 2007, we purchased one independent leathercraft store

and opened an additional nine retail stores - eight in the U.S. and one in

Canada. We also purchased Mid-Continent Leather Sales, Inc., a

competitor located in Oklahoma, which became our thirtieth wholesale

store. In 2008, we opened one retail store in the U.S. and one

combination wholesale and retail store in Northampton, United

Kingdom. In 2009, we opened two retail stores in the

U.S.

At

December 31, 2009, we operated 30 wholesale stores – 29 operating under the

Leather Factory name (26 in the U.S. and three in Canada) and one operating

under the Mid-Continent Leather Sales name. We also operated 75

retail stores operating under the Tandy Leather name (69 in the U.S. and six in

Canada) as well as one combination wholesale and retail store operating under

the Tandy Leather Factory name in the United Kingdom.

Our

growth, measured both by our net sales and net income, occurs as a result of the

increase in the number of stores we have and the increase from year to year of

the sales in our existing stores. The following tables provide

summary store count information for our Leather Factory wholesale stores and

Tandy Leather retail stores in each of our fiscal years from 1999 to

2009.

STORE

COUNT

YEARS

ENDED DECEMBER 31, 1999 through 2009

|

Leather Factory wholesale

stores

|

Tandy Leather retail

stores

|

|||||

|

Year

Ended

|

Opened

|

Conversions(1)

|

Total

|

Opened (2)

|

Closed

|

Total

|

|

Balance

Fwd

|

22

|

N/A

|

||||

|

1999

|

4

|

0

|

26

|

N/A

|

||

|

2000

|

2

|

0

|

28

|

1*

|

0

|

1

|

|

2001

|

2

|

0

|

30

|

0

|

0

|

1

|

|

2002

|

1

|

(1)

|

30

|

14

|

1*

|

14

|

|

2003

|

0

|

0

|

30

|

12

|

0

|

26

|

|

2004

|

0

|

0

|

30

|

16

|

0

|

42

|

|

2005

|

0

|

0

|

30

|

8

|

0

|

50

|

|

2006

|

0

|

(1)

|

29

|

12

|

0

|

62

|

|

2007

|

1^

|

0

|

30

|

10

|

0

|

72

|

|

2008

|

0

|

0

|

30

|

1

|

0

|

73

|

|

2009

|

0

|

0

|

30

|

2

|

0

|

75

|

(1)

Leather Factory wholesale store converted to a Tandy Leather retail

store.

(2) Includes

conversions of Leather Factory wholesale stores to Tandy Leather retail

stores.

(*) The

Tandy Leather operation began as a central mail-order fulfillment center in 2000

which was closed in 2002.

(^) Wholesale

store operating as Mid-Continent Leather Sales

No single

customer’s purchases represent more than 5% of our total sales in

2009. Sales to our five largest customers combined to represent 6.3%,

6.2% and 8.3% of consolidated sales in 2009, 2008 and 2007,

respectively. While management does not believe the loss of one of

these customers would have a significant negative impact on our operations, it

does believe the loss of several of these customers simultaneously or a

substantial reduction in sales generated by them could temporarily affect our

operating results.

1

Our

Operating Divisions

We

service our customers primarily through the operation of three

divisions. We identify those divisions based on management

responsibility, customer focus, and store location. The Wholesale

Leathercraft division consists of 30 wholesale stores of which 27 are located in

the United States and three are located in Canada. As of March 1,

2010, the Retail Leathercraft division consists of 76 Tandy Leather retail

stores of which 69 are located in the United States and seven are located in

Canada. Both of these divisions sell leather and leathercraft-related

products. The International Leathercraft division consists of all

stores, wholesale or retail, located outside of North

America. Currently, we have one such store located in the United

Kingdom.

Wholesale

Leathercraft

The

Wholesale Leathercraft operation distributes its broad product line of leather

and leathercraft-related products in the United States and internationally

through Leather Factory stores. This segment had net sales of

$25.1 million, $26.4 million and $29.6 million for 2009, 2008 and 2007,

respectively. The wholesale stores operate under the name, “The

Leather Factory”, with the exception of the one store we acquired in February

2007 which operates under the name “Mid-Continent Leather Sales.”

General We operate

wholesale stores in 20 states and three Canadian provinces. The

stores range in size from 2,350 square feet to 15,000 square feet, with the

average size of a store being approximately 6,000 square

feet. The type of premises utilized for our wholesale

stores is generally light industrial office/warehouse space in proximity to a

major freeway or with other similar access. This type of location

typically offers lower rents compared to other more retail-oriented

locations.

Business

Strategy

The Leather Factory business concept focuses on the wholesale

distribution of leather and related accessories to retailers, manufacturers and

end users. Our strategy is that a customer can purchase the leather,

related accessories and supplies necessary to complete his project from a single

source. The size and layout of the stores are planned to allow large

quantities of product to be displayed in an easily accessible and visually

appealing manner. Leather is displayed by the pallet where the

customer can see and touch it, assessing first-hand the numerous sizes, styles

and grades offered. The location of the stores is selected based on

the location of customers, so that delivery time to customers is

minimized. A two-day maximum delivery time for phone, internet and

mail orders is our goal.

Our

wholesale stores serve customers through various means including walk-in

traffic, phone, internet and mail order. We also employ a distinctive

marketing tactic in that we maintain an internally-developed target customer

mailing list for use in our aggressive direct mail advertising

campaigns. We staff our stores with experienced managers whose

compensation is tied to the operating profit of the store they

manage. Sales are generated by the selling efforts of the store

personnel, our direct mail advertising, our website

(www.tandyleatherfactory.com), our participation at trade shows and, on a

limited basis, the use of sales representative organizations. The

sales representative organizations consist of companies located in specific

geographic areas that represent numerous companies in a similar

industry. These organizations call on customers and show multiple

products from more than one vendor at a time.

Customers Our

customer base consists of individuals, wholesale distributors, tack and saddle

shops, institutions (prisons and prisoners, schools, hospitals), western stores,

craft stores and craft store chains, other large volume purchasers,

manufacturers and retailers dispersed geographically throughout the

world. Wholesale sales constitute the majority of our business,

although retail customers may purchase products from our wholesale

stores. The Wholesale Leathercraft division’s sales generally do not

reflect significant seasonal patterns.

Our

Authorized Sales Center (“ASC”) program was developed to create a presence in

geographical areas where we do not have a store. An unrelated person

operating an existing business who desires to become an ASC must submit an

application and upon approval, place a minimum initial order. There

are also minimum annual purchase amounts to which the ASC must adhere in order

to maintain ASC status. In exchange, the benefits to the ASC are free

advertising in various sale flyers produced and distributed by us, preferred

pricing on many products, advance notice of new products, and priority shipping

and handling on all orders. Our wholesale stores service 132

ASC's: 81 located in the U.S., 43 located in Canada, and 8 located

outside North America.

Merchandise Our

products are generally organized into 13 categories. We carry a wide

assortment of products including leather, lace, hand tools, kits and craft

supplies. We operate a light manufacturing facility in Fort Worth

whose processes generally involve cutting leather into various shapes and

patterns using metal dies. The factory produces approximately 20% of

our products and also assembles and repackages products as

needed. Products manufactured in our factory are distributed through

our stores under the TejasTM

brand name. We also distribute product under the Tandy LeatherTM

and Dr. Jackson'sTM

brands. We develop new products through the ideas and referrals of

customers and store personnel as well as the analysis of fads and trends of

interest in the market.

We offer

an unconditional satisfaction guarantee to our customers. Simply

stated, we will accept product returns for any reason. We believe

this liberal policy promotes customer loyalty. We offer credit terms

to our non-retail customers, upon receipt of a credit application and approval

by our credit manager. Generally, our open accounts are net 30

days.

During

2009 and 2008, Wholesale Leathercraft division sales by product category were as

follows:

|

Product Category

|

2009 Sales Mix

|

2008 Sales Mix

|

|

|

Belts

strips and straps

|

2%

|

2%

|

|

|

Books,

patterns, videos

|

2%

|

1%

|

|

|

Buckles

|

4%

|

4%

|

|

|

Conchos^

|

4%

|

5%

|

|

|

Craft

supplies

|

6%

|

6%

|

|

|

Custom

tools and hardware

|

0%

|

0%

|

|

|

Dyes,

finishes, glues

|

6%

|

6%

|

|

|

Hand

tools

|

13%

|

12%

|

|

|

Hardware

|

7%

|

7%

|

|

|

Kits

|

8%

|

8%

|

|

|

Lace

|

9%

|

9%

|

|

|

Leather

|

35%

|

36%

|

|

|

Stamping

tools

|

4%

|

4%

|

|

|

100%

|

100%

|

^A concho

is a metal adornment attached to clothing, belts, saddles, etc., usually made

into a pattern of some southwestern or geometric object.

In

addition to meeting ordinary operational requirements, our working capital

demands are a product of the need to maintain a level of inventory sufficient to

fill customer orders as they are received with minimal backorders and the time

required to collect our accounts receivable. Because availability of

merchandise and prompt delivery time are important competitive factors for us,

we maintain higher levels of inventory than our smaller

competitors. For additional information regarding our cash, inventory

and accounts receivable at the end of 2009 and 2008, see "Item 7. Management's

Discussion and Analysis of Financial Condition and Results of

Operations."

Suppliers We purchase merchandise and raw materials from approximately 200 vendors dispersed throughout the United States and in approximately 15 foreign countries. In 2009, our 10 largest vendors accounted for approximately 75% of our inventory purchases.

Because

leather is sold internationally, market conditions abroad are likely to affect

the price of leather in the United States. Outbreaks of mad cow and

hoof-and-mouth disease (or foot-and-mouth disease) in any part of the world can

influence the price of the leather we purchase. Because an occurrence

of such an event is beyond our control, we cannot predict when and to what

extent we could be affected in the future. Aside from increasing

purchases when we anticipate price increases (or possibly delaying purchases if

we foresee price declines), we do not attempt to hedge our inventory

costs.

Overall,

we believe that our relationships with suppliers are strong and do not

anticipate any material changes in these supplier relationships. Due

to the number of alternative sources of supply, the loss of any of these

principal suppliers would not have a material impact on our

operations.

Operations

Hours of operations vary by location, but generally range from 8:00 am to 6:00

pm Monday through Friday, and from 9:00 am to 4:00 pm on

Saturdays. The stores maintain uniform prices, except where lower

prices are necessary to meet local competition.

Competition Most of our

competition comes in the form of small, independently-owned retailers who in

most cases are also our customers. We estimate that there are a few

hundred of these small independent stores in the United States and

Canada. We compete on price, availability of merchandise, and

delivery time. While there is competition in connection with a number

of our products, to our knowledge there is no direct competition affecting our

entire product line. Our large size relative to most competitors

gives us the advantage of being able to purchase large volumes and stock a full

range of products.

2

Distribution The wholesale

stores receive the majority of their inventory from our central warehouse

located in Fort Worth, Texas, although occasionally, merchandise is shipped

directly from the vendor. Inventory is shipped to the stores from our

central warehouse once a week to meet customer demand without sacrificing

inventory turns. Customer orders are filled as received, and we do

not have backlogs.

We

attempt to maintain the optimum number of items in our product line to minimize

out-of-stock situations against carrying costs involved with such an inventory

level. We generally maintain higher inventories of imported items to

ensure a continuous supply. The number of products offered changes

every year due to the introduction of new items and the discontinuance of

others. We carry approximately 2,800 items in the current lines of

leather and leather-related merchandise. All items are offered in all

stores.

Expansion Our

wholesale store expansion across the United States has been fairly consistent

since we purchased the original six stores in 1985. We opened our

thirtieth store in August 2002. We converted one wholesale (Leather

Factory) store to a retail (Tandy Leather) store in 2006, reducing the number of

wholesale stores to 29. We acquired Mid-Continent Leather Sales in

2007, a wholesale store located in Oklahoma, increasing the number of wholesale

stores to 30. While we do not believe there is a significant and

immediate opportunity for expansion of the Leather Factory store system in terms

of opening additional locations, we do believe expansion could be achieved by

acquiring companies in related areas/markets which offer collaborative

advantages based on the local markets and/or the product lines of the

businesses.

Retail

Leathercraft

Our

Retail Leathercraft division consists of a growing chain of retail stores

operating under the name, “Tandy Leather.” Tandy Leather Company,

established in 1919 as Hinkley-Tandy Leather Company, is the oldest and

best-known supplier of leather and related supplies used in the leathercraft

industry. We offer a product line of quality tools, leather,

accessories, kits and teaching materials. This segment had net

sales of $28.1 million, $25.2 million and $24.7 million for 2009, 2008 and 2007,

respectively.

General As

of March 1, 2010, the Tandy Leather retail chain has 76 stores located in 36

states and six Canadian provinces with plans to reach 100 to 120 stores as

opportunities arise over the next several years. The stores range in

size from 1,200 square feet to 3,800 square feet, with the average size of a

store being approximately 2,000 square feet. The type of

premises utilized for a retail store is generally an older strip shopping center

located at well-known crossroads, making the store easy to find.

Business

Strategy Tandy

Leather has long been known for its reputation in the leathercraft industry and

its commitment to promoting and developing the craft through education and

customer development. Our commitment to this strategy is evidenced by

our re-establishment of the retail store chain throughout the United States

following our acquisition of the assets of Tandy Leather in 2000. We

continue to broaden our customer base by working with various youth

organizations and institutions where people are introduced to leathercraft, as

well as hosting classes in our stores.

The

retail stores serve walk-in, mail and phone order customers as well as orders

generated from our website, www.tandyleatherfactory.com. Our retail

stores are staffed by knowledgeable sales people whose compensation is based, in

part, upon the profitability of their store. Sales by Tandy Leather

are driven by the efforts of the store staff, trade shows, and our direct mail

and e-mail marketing program.

Customers Individual retail

customers are our largest customer group, representing approximately 65% of

Tandy Leather's 2009 sales. Youth groups, summer camps, schools and a

limited number of wholesale customers complete our customer

base. Like the wholesale stores, the retail stores fill orders as

they are received, and there is no order backlog. The retail stores

maintain reasonable amounts of inventory to fill these orders. Tandy

Leather’s retail store operations historically generate slightly more sales in

the fourth quarter of each year (30-32% of annual sales), while the other three

quarters remain fairly even at 23-25% of annual sales each quarter.

Merchandise

Our products are generally organized into 13 categories. We carry a

wide assortment of products including leather, hand tools, kits, dyes &

finishes and stamping tools. During 2009 and 2008, Retail

Leathercraft division sales by product category were as follows:

|

Product Category

|

2009 Sales Mix

|

2008 Sales Mix

|

|

|

Belts

strips and straps

|

5%

|

4%

|

|

|

Books,

patterns, videos

|

3%

|

3%

|

|

|

Buckles

|

4%

|

4%

|

|

|

Conchos

|

4%

|

4%

|

|

|

Craft

supplies

|

4%

|

4%

|

|

|

Dyes,

finishes, glues

|

8%

|

8%

|

|

|

Hand

tools

|

16%

|

15%

|

|

|

Hardware

|

6%

|

6%

|

|

|

Kits

|

10%

|

11%

|

|

|

Lace

|

4%

|

4%

|

|

|

Leather

|

31%

|

31%

|

|

|

Stamping

tools

|

5%

|

6%

|

|

|

100%

|

100%

|

As

indicated above, the products sold in our retail stores are also sold in our

wholesale stores. Therefore, the discussion above regarding products,

their sources and the working capital requirements for the Wholesale

Leathercraft division also apply to the Retail Leathercraft

division. Sales at the retail stores are generally made through cash

transactions or through national credit cards. We also sell on open

account to selected wholesale customers including schools and other institutions

and small retailers. Our terms are generally net 30

days. Like the wholesale stores, the retail stores have an

unconditional return policy.

Operations Hours of

operation are 9:00 am to 6:00 pm Monday through Friday, and from 9:00 am to 4:00

pm on Saturdays. In addition, most of the stores stay open late one

night a week for leathercrafting classes taught in the

stores. Selling prices are uniform throughout the retail store

system.

Competition Our competitors

are generally small local craft stores that carry a limited line of leathercraft

products. Several national retail chains that are customers in our

Wholesale Leathercraft division also carry leathercraft products on a very small

scale relative to their overall product line. To our knowledge, our

retail store chain is the only one in existence solely specializing in

leathercraft.

Distribution The retail stores

receive their inventory from our central warehouse located in Fort Worth,

Texas. The stores generally restock their inventory once a week with

a shipment from the warehouse. Retail Leathercraft’s inventory turns

are higher than Wholesale Leathercraft’s because the Wholesale Leathercraft

calculation includes the central warehouse inventory whereas the Retail

Leathercraft calculation includes only the inventory in the Tandy Leather retail

stores.

Expansion We

intend to expand the Tandy Leather retail store chain to between 100 and 120

stores throughout North America as it makes financial sense to do so. 14 stores

were opened in 2002; 12 stores were opened in 2003; 16 were opened in 2004

(including four in Canada); eight were opened in 2005, 12 were opened in 2006,

ten were opened in 2007; one was opened in 2008, and two were opened in

2009. Of the 75 stores opened as of December 2009, 11 were

independent leathercraft stores that we acquired. Separately, these

acquisitions are not material. The other 64 stores have been new

stores opened by us. In 2010, we plan to open one to two retail

stores.

3

International

Leathercraft

Our

International Leathercraft division consists of company-owned stores located

outside of North America. Currently, we have one wholesale and retail

combination store located in Northampton, United Kingdom, which we opened in

February 2008. It operates under the Tandy Leather Factory trade

name. This segment had net sales of $1.3 million and $836,000 in 2009

and 2008, respectively.

Business

Strategy The business concept for our International

Leathercraft division is a blending of our Leather Factory and Tandy Leather

business strategies – the wholesale distribution of leather and related

accessories to retailers, manufacturers and other businesses, as well as the

promotion and continuance of leathercraft through education and development of

the retail customers. The store is located in a 6,600 square foot

building in a light industrial area. We maintain sufficient inventory

so that our customers can purchase the leather, related accessories and supplies

necessary to complete their projects from one supplier. The layout of

the store is such that large quantities of product can be displayed in an easily

accessible and visually appealing manner. The store services walk-in,

mail and phone order customers as well as orders generated from our website,

www.tandyleatherfactory.com. Sales

are driven by the efforts of the store staff, trade shows, and our direct mail

and e-mail marketing programs.

Customers The

growing customer base consists of individuals, wholesale distributors,

equine-related shops, cobblers, dealers, and retailers dispersed geographically

throughout the UK and Europe. Retail sales generally occur via cash

transactions or through national credits cards. We also sell on open

account to selected wholesale customers including dealers, manufacturers, and

retailers. Like our USA stores, our UK store has an unconditional

return policy.

Merchandise The

products sold in our UK store are also sold in our USA

stores. Therefore, the discussion above regarding products, their

sources and the working capital requirements for the Wholesale and Retail

Leathercraft divisions also apply here.

Operations Hours

of operation are 8:00 am to 5:00 pm Monday through Friday, and from 8:00 am to

2:00 pm on Saturdays. Selling prices are consistent with the USA

store pricing, adjusted for currency fluctuation.

Distribution The

UK store receives the majority of its inventory from our central warehouse

located in Fort Worth, Texas, although occasionally, merchandise is shipped

directly from the vendor. Inventory is shipped from our warehouse to

the store several times per month to meet customer demand without sacrificing

inventory turns. Customer orders are filled as received, and we do

not have backlogs.

Expansion We

intend to expand further internationally, although we have no specific time

frame at this time. We will continue to grow our customer base

throughout Europe as well as other parts of the world so that we can support

additional stores.

For more

information about our business and our reportable segments, see Item 7

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations” on page 9.

Additional

Information

Compliance

With Environmental Laws Our compliance

with federal, state and local environmental protection laws has not had, and is

not expected to have, a material effect on our capital expenditures, earnings or

competitive position.

Employees As of December

31, 2009, we employed 447 people, 351 of whom were employed on a full-time

basis. We are not a party to any collective bargaining

agreements. Overall, we believe that relations with employees are

good.

Intellectual

Property We own approximately 20 registered trademarks,

including federal trade name registrations for "The Leather Factory" and "Tandy

Leather Company." We also own approximately 20 registered foreign

trademarks worldwide. We own

approximately 500 registered copyrights in the United States covering more than

600 individual works relating to various products. We also own

several United States patents for specific belt buckles and leather-working

equipment. These rights are valuable assets, and we defend them as

necessary.

International

Operations

Information regarding our revenues from the United States and abroad and

our long-lived assets are found in Note 15 to our Consolidated Financial

Statements, Segment

Information.

Our

Website and Availability of SEC Reports We file reports

with the Securities and Exchange Commission ("SEC"). These reports

include our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current

Reports on Form 8-K and any amendments to these filings. The public

may read any of these filings at the SEC's Public Reference Room at 100 F

Street, NE, Washington, DC 20549. In addition, the public

may obtain information on the operation of the Public Reference Room by calling

the SEC at 1-800-SEC-0330. Further, the SEC maintains an Internet

site that contains reports, proxy and information statements and other

information concerning us. You can connect to this site at

http://www.sec.gov.

Our

corporate website is located at

http://www.tandyleatherfactory.com. We make copies of our Annual

Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form

8-K, proxy statements and any amendments filed with or furnished to the SEC

available to investors on or through our website free of charge as soon as

reasonably practicable after we electronically file them with or furnish them to

the SEC. Our SEC filings can be found on the Investor Relations page

of our website through the "SEC Filings" link. In addition, certain

other corporate governance documents are available on our website through the

"Corporate Governance" link.

4

Executive

Officers of the Registrant

The

following table sets forth information concerning our executive officers as of

March 20, 2010:

|

Name and Age

|

Position

and Business Experience During Past Five Years

|

Served as Officer Since

|

|

Jon

W. Thompson, 48

|

Chief

Executive Office since July 2009; President since June 2008; Senior Vice

President from June 1993 to June 2008

|

2008

|

|

Shannon

L. Greene, 44

|

Chief

Financial Officer since May 2000

|

2000

|

|

Mark

J. Angus, 49

|

Senior

Vice President since June 2008; Vice President of Merchandising since June

1993

|

2008

|

|

William

M. Warren, 66

|

Secretary

and Corporate Counsel

|

1993

|

Jon W. Thompson has served as

our Chief Executive Officer since July 2009. He has also served as

President and Chief Operating Officer since June 2008. He served as

Senior Vice President from June 1993 to June 2008. Mr. Thompson is

the son of Wray Thompson, Chairman of the Board.

Shannon L. Greene has served

as our Chief Financial Officer and Treasurer since May 2000 and director since

January 2001. Ms. Greene is also our Chief Accounting

Officer. Ms. Greene, a certified public accountant, also serves on

our 401(k) Plan committee. Her professional affiliations include the

American Institute of Certified Public Accountants, the Texas Society of

Certified Public Accountants and its Fort Worth chapter, and the Financial

Executives International. She also sits on the Board of Directors of

the U.S. Chamber of Commerce.

Mark J. Angus has served as

Senior Vice President since June 2008. He served as Vice President of

Merchandising since January 1993.

William M. Warren has served

as Secretary and General Counsel since 1993. Since 1979, Mr. Warren

has been President and Director of Loe, Warren, Rosenfield, Kaitcer, Hibbs,

Windsor & Lawrence, P.C., a law firm located in Fort Worth,

Texas.

All officers are elected annually by

the Board of Directors to serve for the ensuing year.

ITEM

1A. RISK FACTORS

You

should carefully consider the following risk factors together with all of the

other information included in this annual report, including the financial

statements and related notes, when deciding to invest in us. You

should be aware that the occurrence of any of the events described in this Risk

Factors section and elsewhere in this annual report could have a material

adverse effect on our business, financial position, results of operations and

cash flows. Some, but not all, of the important risks which could

cause actual results to differ materially from those suggested by

forward-looking statements made by us include the following:

|

·

|

We

might fail to realize the anticipated benefits of the opening of Tandy

Leather retail stores or we might be unable to obtain sufficient new

locations on acceptable terms to meet our growth

plans. Further, we might fail to hire and train competent

managers to oversee the stores

opened.

|

|

·

|

Continued

weakness in the economy in the United States, as well as abroad, may cause

our sales to decrease or not to increase or adversely affect the prices

charged for our products. Also, hostilities, terrorism or other

events could worsen this condition.

|

|

·

|

Negative

trends in general consumer-spending levels, including the impact of the

availability and level of consumer debt and levels of consumer confidence

could adversely affect our sales.

|

|

·

|

Political

considerations here and abroad could disrupt our sources of supplies from

abroad or affect the prices we pay for

goods.

|

|

·

|

Continued

involvement by the United States in war and other military operations in

the Middle East and other areas abroad could disrupt international trade

and affect our inventory sources.

|

|

·

|

As

a result of the on-going threat of terrorist attacks on the United States,

consumer buying habits could change and decrease our

sales.

|

|

·

|

Livestock

diseases such as mad cow could reduce the availability of hides and

leathers or increase their cost. Also, the prices of hides and

leathers fluctuate in normal times, and these fluctuations can affect

us.

|

|

·

|

If,

for whatever reason, the costs of our raw materials and inventory

increase, we may not be able to pass those costs on to our

customers.

|

|

·

|

Other

factors could cause either fluctuations in buying patterns or possible

negative trends in the craft and western retail markets. In addition, our

customers may change their preferences to products other than ours, or

they may not accept new products as we introduce

them.

|

|

·

|

Any

change in the commercial banking environment may affect us and our ability

to borrow capital as needed.

|

Other

uncertainties, which are difficult to predict and many of which are beyond our

control, may occur as well.

5

ITEM

2. PROPERTIES

We lease

all of our store locations premises, with the majority of our stores having

initial lease terms of approximately five years. The leases are

generally renewable, with increases in lease rental rates in some

cases. We believe that all of our properties are adequately covered

by insurance. The properties leased by us are described in Item 1 in

the description of each of our three operating segments. We also

lease a 284 square-foot showroom in the Denver Merchandise Mart for $5,908 per

year. This lease will expire in October 2011.

We own

our corporate headquarters, which includes our central warehouse and

manufacturing facility, sales, advertising, administrative, and executive

offices. The facility consists of 191,000 square feet located on

approximately 30 acres.

The

following table summarizes the locations of our leased premises as of December

31, 2009:

|

State

|

Wholesale

Leathercraft

|

Retail

Leathercraft

|

International

|

|

Alabama

|

-

|

1

|

-

|

|

Alaska

|

-

|

1

|

-

|

|

Arizona

|

2

|

3

|

-

|

|

Arkansas

|

-

|

1

|

-

|

|

California

|

3

|

7

|

-

|

|

Colorado

|

1

|

3

|

-

|

|

Connecticut

|

-

|

1

|

-

|

|

Florida

|

1

|

3

|

-

|

|

Georgia

|

-

|

1

|

-

|

|

Idaho

|

-

|

1

|

-

|

|

Illinois

|

1

|

1

|

-

|

|

Indiana

|

-

|

2

|

-

|

|

Iowa

|

1

|

-

|

-

|

|

Kansas

|

1

|

-

|

-

|

|

Kentucky

|

-

|

1

|

-

|

|

Louisiana

|

1

|

-

|

-

|

|

Maryland

|

-

|

1

|

-

|

|

Massachusetts

|

-

|

1

|

-

|

|

Michigan

|

1

|

1

|

-

|

|

Minnesota

|

-

|

2

|

-

|

|

Missouri

|

1

|

2

|

-

|

|

Montana

|

1

|

-

|

-

|

|

Nebraska

|

-

|

1

|

-

|

|

Nevada

|

-

|

2

|

-

|

|

New

Mexico

|

1

|

2

|

-

|

|

New

York

|

-

|

1

|

-

|

|

North

Carolina

|

-

|

2

|

-

|

|

North

Dakota

|

-

|

1

|

-

|

|

Ohio

|

1

|

2

|

-

|

|

Oklahoma

|

1

|

2

|

-

|

|

Oregon

|

1

|

-

|

-

|

|

Pennsylvania

|

1

|

2

|

-

|

|

South

Carolina

|

-

|

1

|

-

|

|

South

Dakota

|

-

|

1

|

-

|

|

Tennessee

|

1

|

3

|

-

|

|

Texas

|

5

|

9

|

-

|

|

Utah

|

1

|

2

|

-

|

|

Virginia

|

-

|

1

|

-

|

|

Washington

|

1

|

2

|

-

|

|

Wisconsin

|

-

|

1

|

-

|

|

Wyoming

|

-

|

1

|

|

Canadian

locations:

|

|||

|

Alberta

|

1

|

1

|

-

|

|

British

Columbia

|

-

|

1

|

-

|

|

Manitoba

|

1

|

-

|

-

|

|

Nova

Scotia

|

-

|

1

|

-

|

|

Ontario

|

1

|

2

|

-

|

|

Quebec

|

-

|

1

|

-

|

|

International

locations:

|

|||

|

United

Kingdom

|

-

|

-

|

1

|

6

ITEM

3. LEGAL PROCEEDINGS

We are

involved in litigation in the ordinary course of business but are not currently

a party to any material pending legal proceedings.

ITEM

4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY

HOLDERS

There

were no matters submitted to a vote of our security holders during the fourth

quarter of our fiscal year ended December 31, 2009.

PART II

ITEM 5. MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PRUCHASES

OF EQUITY SECURITIES

Our

common stock is traded on the NYSE Amex using the symbol “TLF”. The

high and low trading prices for each calendar quarter during the last two fiscal

years are as follows:

|

2009

|

High

|

Low

|

2008

|

High

|

Low

|

|

|

4th

quarter

|

$4.08

|

$3.00

|

4th

quarter

|

$2.75

|

$1.72

|

|

|

3rd

quarter

|

$3.30

|

$2.35

|

3rd

quarter

|

$3.07

|

$2.49

|

|

|

2nd

quarter

|

$2.85

|

$1.90

|

2nd

quarter

|

$3.37

|

$2.63

|

|

|

1st

quarter

|

$2.42

|

$1.55

|

1st

quarter

|

$3.32

|

$2.30

|

There

were approximately 476 stockholders of record on March 1,

2010.

We have

never declared or paid any cash dividends on the shares of our common

stock. Our Board of Directors has historically followed a

policy of reinvesting our earnings in the expansion of our

business. This policy is subject to change based on future industry

and market conditions, as well as other factors.

We did

not sell any shares of our equity securities during our fiscal year ended

December 31, 2009 that were not registered under the Securities

Act.

The

following table provides information about purchases we have made of our common

stock during the quarter ended December 31, 2009:

|

ISSUER

PURCHASES OF EQUITY SECURITIES

|

||||

|

Period

|

(a)

Total Number of Shares Purchased

|

(b)

Average Price Paid per Share

|

(c)

Total Number of Shares Purchased as Part of Publicly Announced Plans or

Programs

|

(d)

Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be

Purchased Under the Plans or Programs

|

|

October

1 through October 31

|

-

|

-

|

-

|

974,773

|

|

November

1 through November 30

|

-

|

-

|

-

|

974,773

|

|

December

1 through December 31

|

35,700(1)

|

$3.69

|

35,700

|

964,300

|

|

Total

|

35,700

|

$3.69

|

35,700

|

964,300

|

|

(1)

|

Represents

shares purchased through a stock repurchase program permitting us to

repurchase up to one million shares of our common stock at prevailing

market prices not to exceed $3.70 per share. We announced the

program on December 9, 2009, such program replacing our previous stock

repurchase program which permitted us, on the date of its termination, to

repurchase up to 974,773 shares of our common stock at prevailing prices

not to exceed $2.85 per share. Purchases under the program

commenced on December 9, 2009 and will terminate on December 10,

2010.

|

7

Stockholder

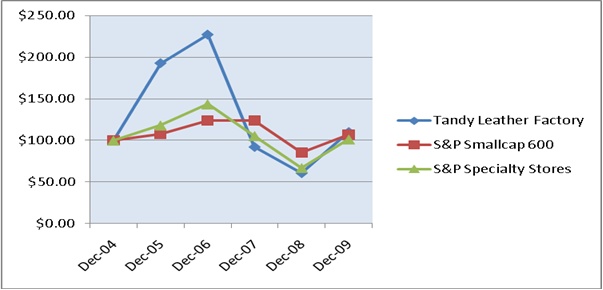

Return Performance Graph

The line

graph below compares the yearly percentage change in our cumulative five-year

total stockholder return on our common stock with the Standard & Poor’s

SmallCap 600 Index and the S&P Specialty Stores Index. The graph

assumes that $100 was invested on December 31, 2004 in our common stock,

the Standard & Poor’s SmallCap 600 Index, and the S&P Specialty Stores

Index, and that all dividends were reinvested. The returns shown on

the graph are not necessarily indicative of future performance.

COMPARISON

OF FIVE-YEAR CUMULATIVE TOTAL RETURNS

Tandy

Leather Factory, Inc.

|

Company

Name / Index

|

Dec

04

|

Dec

05

|

Dec

06

|

Dec

07

|

Dec

08

|

Dec

09

|

|

TANDY

LEATHER FACTORY

|

100

|

192.96

|

227.32

|

92.11

|

60.56

|

110.14

|

|

S&P

SMALLCAP 600 INDEX

|

100

|

107.68

|

123.96

|

123.59

|

85.19

|

106.97

|

|

S&P

SPECIALTY STORES

|

100

|

118.10

|

143.57

|

105.38

|

66.82

|

101.21

|

Data

Source: Research Data Group, Inc., San Francisco, CA

ITEM 6. SELECTED

FINANCIAL DATA

The

selected financial data presented below are derived from and should be read in

conjunction with our Consolidated Financial Statements and related

notes. This information should also be read in conjunction with "Item

7 - Management’s Discussion and Analysis of Financial Condition and Results of

Operations.” Data in prior years has not been restated to reflect

acquisitions, if any, that occurred in subsequent years.

|

Income

Statement Data,

Years

ended December 31,

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||

|

Net

sales

|

$54,482,739

|

$52,491,538

|

$54,219,728

|

$53,458,649

|

$49,069,483

|

||||

|

Cost

of sales

|

21,873,365

|

21,441,179

|

23,039,396

|

22,435,222

|

20,774,584

|

||||

|

Gross

profit

|

32,609,374

|

31,050,359

|

31,180,332

|

31,023,427

|

28,294,899

|

||||

|

Operating

expenses

|

27,514,273

|

27,025,017

|

26,859,301

|

24,129,115

|

22,806,049

|

||||

|

Operating

income

|

5,095,101

|

4,025,342

|

4,321,031

|

6,894,312

|

5,488,850

|

||||

|

Other

(income) expense

|

133,699

|

67,072

|

(316,831)

|

(97,161)

|

(134,502)

|

||||

|

Income

from continuing operations before income taxes

|

4,961,402

|

3,958,270

|

4,635,942

|

6,991,473

|

5,623,352

|

||||

|

Income

tax provision (benefit)

|

1,700,259

|

1,446,423

|

1,740,420

|

2,362,725

|

1,867,820

|

||||

|

Net

income from continuing operations

|

3,261,143

|

$2,511,847

|

$2,895,522

|

$4,628,748

|

$3,755,532

|

||||

|

Income

from discontinued operations, net of tax

|

56,914

|

92,336

|

192,609

|

148,318

|

(41,818)

|

||||

|

Net

income

|

$3,318,057

|

$2,604,183

|

$3,088,131

|

$4,777,066

|

$3,713,714

|

||||

Net

income per share from continuing operations

|

Basic

|

$0.31

|

$0.23

|

$0.26

|

$0.43

|

$0.35

|

||||

|

Diluted

|

$0.31

|

$0.23

|

$0.26

|

$0.42

|

$0.34

|

Net

income per share including discontinued operations

|

Basic

|

$0.32

|

$0.24

|

$0.28

|

$0.44

|

$0.35

|

|||||

|

Diluted

|

$0.31

|

$0.24

|

$0.28

|

$0.43

|

$0.34

|

|||||

|

Weighted

average common shares outstanding for:

|

||||||||||

|

Basic

EPS

|

10,471,103

|

10,931,306

|

10,951,481

|

10,807,316

|

10,643,004

|

|||||

|

Diluted

EPS

|

10,535,736

|

11,015,657

|

11,157,775

|

11,113,855

|

10,975,178

|

|||||

|

Balance

Sheet Data, as of December 31,

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||

|

Cash

and certificates of deposit

|

$12,908,962

|

$10,821,298

|

$6,810,396

|

$6,739,981

|

$3,215,727

|

||||

|

Total

assets

|

43,327,231

|

40,975,913

|

37,651,506

|

31,916,635

|

25,680,473

|

||||

|

Capital

lease obligation, including current portion

|

-

|

593,949

|

-

|

111,723

|

245,789

|

||||

|

Long-term

debt, including current portion

|

3,712,500

|

3,915,000

|

4,050,000

|

-

|

-

|

||||

|

Total

Stockholders’ Equity

|

$33,359,655

|

$31,264,762

|

$29,815,504

|

$26,323,243

|

$21,257,857

|

8

ITEM

7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

We intend

for the following discussion to provide you with information that will assist

you in understanding our financial statements, the changes in key items in those

financial statements from year to year and the primary factors that accounted

for those changes, as well as how particular accounting principles affect our

financial statements. This discussion also provides information about

the financial results of the various segments of our business so you may better

understand how those segments and their results affect our financial condition

and results of operations as a whole. Finally, we have identified and

discussed trends known to management that we believe are likely to have a

material effect.

This

discussion should be read in conjunction with our financial statements as of

December 31, 2009 and 2008 and the two years then ended and the notes

accompanying those financial statements. You are also urged to

consider the information under the caption "Summary of Critical Accounting

Policies."

Summary

We are

the world's largest specialty retailer and wholesale distributor of leather and

leathercraft-related items. Our operations are centered on operating

retail and wholesale stores. We have built our business by offering

our customers quality products in one location at competitive

prices. The key to our success is our ability to grow our base

business. We grow that business by opening new locations and by

increasing sales in our existing locations. We intend to continue to

expand both domestically, in the short-term, and internationally, in the

long-term.

We

operate in three segments. First, Wholesale Leathercraft, consisting

of our Leather Factory stores and our national account group, is our oldest

segment with sales of $25.1 million in 2009. Historically, in normal

economic conditions, this division generally offers steady but very modest

increases in sales. Sales in 2009 declined 5.0% compared to

2008. The wholesale stores’ sales declined 5.3% compared to 2008 and

national account sales were down 3.4%. Much of the sales decline at

the stores and in national accounts is attributed to an overall weakness in

consumer spending as a result of the weak U.S. economy.

Since

acquiring its assets in 2000, Tandy Leather has been re-established as the

operator of retail leathercraft stores. These retail stores comprise

our second segment, Retail Leathercraft. This segment has experienced

the greatest increases in sales ($28.1 million in 2009, up from $25.2 million in

2008) and in 2009, surpassed our Wholesale Leathercraft segment to become our

largest source of revenues. Our business plan calls for opening an

average of 10-12 stores annually as we work toward a goal of 100+ stores from 75

stores at the end of 2009. We have slowed down our new store openings

in recent years due to the general economic conditions in the U.S. and because

of the lack of personnel qualified for store manager positions. We

plan to open one to two new stores in 2010, one of which was opened in the first

quarter.

Our third

segment is International Leathercraft, which consists of stores located outside

of North America. Currently, we have one retail/wholesale combination

store located in the United Kingdom, which was opened in February

2008. It is our intention to add more stores to this segment once we

have a large enough customer base to support additional stores.

On a

consolidated basis, a key indicator of costs, gross margin as a percent of total

net sales, increased in 2008 and in 2009. Operating

expenses increased 2% between 2008 and 2009 and between 2007 and

2008.

We

reported consolidated net income for 2009 of $3.3

million. Consolidated net income for 2008 and 2007 was $2.6 million

and $3.1 million, respectively. We use our cash flow to fund our

operations, to fund the opening of new Tandy Leather stores, to purchase

necessary property and equipment and to make acquisitions of small competitors

in the retail and wholesale market. In 2007, we incurred $4.0 million

in bank debt to purchase a 191,000 square foot building to house our corporate

headquarters and central support units. We moved into that facility

in the first quarter of 2008. At the end of 2009, our stockholders’

equity had increased to $33.3 million from $31.3 million the previous

year.

Comparing

the December 31, 2009 balance sheet with the prior year’s balance sheet, we

increased our investment in inventory from $16.0 million to $16.9 million, while

total cash (including certificates of deposit and other short-term investments)

increased from $10.8 million from $12.9 million.

Net

Sales

Net sales

for the three years ended December 31, 2009 were as follows:

|

Year

|

Wholesale Leathercraft

|

Retail Leathercraft

|

International Leathercraft

|

Total Company

|

Incr (Decr) from Prior

Year

|

|

2009

|

$25,095,392

|

$28,079,862

|

$1,307,485

|

$54,482,739

|

3.8%

|

|

2008

|

$26,423,858

|

$25,231,145

|

$836,535

|

$52,491,537

|

(3.2)%

|

|

2007

|

$29,555,978

|

$24,663,750

|

N/A

|

$54,219,728

|

1.4%

|

Our net

sales increased by 3.8% in 2009 when compared with 2008 and fell by 3.2% in 2008

when compared with 2007. In 2009 and 2008, our Retail and

International Leathercraft segments reported sales increases while our Wholesale

Leathercraft segment reported sales declines. The reduction in sales

in our wholesale stores is the result of the overall economic slowdown in the

U.S. That economic slowdown has impacted our retail stores as well,

although not as significantly.

Costs

and Expenses

In

general, our gross profit as a percentage of sales (our gross margin) fluctuates

based on the mix of customers we serve, the mix of products we sell and our

ability to source products globally. Our negotiations with suppliers

for lower pricing are an on-going process, and we have varying degrees of

success in those endeavors. Sales to retail customers tend to produce

higher gross margins than sales to wholesale customers due to the difference in

pricing levels. Therefore, as retail sales increase in the overall

sales mix, higher gross margins tend to follow. Finally, there is

significant fluctuation in gross margins between the various merchandise

categories we offer. As a result, our gross margins can vary

depending on the mix of products sold during any given time period.

For 2009,

our cost of sales decreased as a percentage of total net sales when compared to

2009, resulting in an increase in consolidated gross profit margin from 59.2% to

59.9%. Our 2008 cost of sales as a percentage of our total net sales

decreased as a percentage of total net sales when compared to 2007, resulting in

an increase in consolidated gross profit margin from 57.5% to

59.2%. Increases in gross margin are primarily due to increased

retail sales from year to year.

Our gross

margins for the three years ended December 31, 2009 were as

follows:

|

Year

|

Wholesale Leathercraft

|

Retail Leathercraft

|

International Leathercraft

|

Total Company

|

|

2009

|

58.5%

|

60.9%

|

63.6%

|

59.9%

|

|

2008

|

56.5%

|

61.6%

|

68.4%

|

59.2%

|

|

2007

|

55.7%

|

59.7%

|

-

|

57.5%

|

9

Our

operating expenses decreased 1.0% as a percentage of total net sales to 50.5% in

2009 when compared with 51.5% in 2008. This decrease indicates that

our operating expenses grew more slowly than our sales during this

period. 2009 operating expenses were $490,000 higher than those of

2008. Significant expense fluctuations in 2009 compared to 2008 are

as follows:

|

Expense

|

2009 amount

|

Incr (Decr) over 2008

|

|

Employee

compensation & benefits

|

$14.5

million

|

$500,000

|

|

Rent

& utilities

|

3.3

million

|

(90,000)

|

|

Depreciation

and amortization

|

1.1

million

|

100,000

|

|

Loss

on impairment and disposal of equipment

|

365,000

|

365,000

|

|

Professional

fees and licenses

|

700,000

|

(62,000)

|

|

Freight

out – shipping product to customers

|

1.3

million

|

(160,000)

|

|

Property

taxes

|

340,000

|

80,000

|

|

Outside

services

|

102,000

|

(157,000)

|

Our

operating expenses increased 2.0% as a percentage of total net sales to 51.5% in

2008 when compared with 49.5% in 2007. This increase indicates that

our operating expenses grew faster than our sales during this

period. Significant expense fluctuations in 2008 compared to 2007 are

as follows:

|

Expense

|

2008 amount

|

Incr (Decr) over 2007

|

|

Employee

compensation & benefits

|

$14.0

million

|

$(160,000)

|

|

Rent

& utilities

|

4.1

million

|

323,000

|

|

Depreciation

and amortization

|

985,000

|

350,000

|

|

Advertising

|

3.0

million

|

(400,000)

|

|

Freight

out – shipping product to customers

|

1.5

million

|

(140,000)

|

|

Property

taxes

|

260,000

|

135,000

|

|

Outside

services

|

260,000

|

(240,000)

|

Other

Income/Expense (net)

Other

Income/Expense consists primarily of currency exchange fluctuations, interest

income and interest expense. In 2009, we had other expense (net) of

$134,000 compared to other income (net) of $67,000 in 2008. We

received $32,000 in gas royalties. We earned $128,000 in interest

income on our cash and paid $297,000 in interest expense on our bank

debt. We had a currency exchange loss of $98,000 in 2009 compared to

$114,000 in 2008.

In 2008,

we had other expense (net) of $67,000 compared to other income (net) of $315,000

in 2007. We received $230,000 for surface damage and additional

access related to the oil and gas lease associated with a portion of the land

surrounding our corporate facility. We earned $141,000 in interest

income on our cash and paid $332,000 in interest expense on our bank

debt. We had a currency exchange loss of $114,000 in 2008 compared to

income of $9,000 in 2007.

Net

Income

During

2009, we earned net income of $3.3 million, a 27% increase over our net income

of $2.6 million earned during 2008. The increase in net income was

the result of the increase in sales and gross profit, partially offset by the

reduction in other income.

During

2008, we earned net income of $2.6 million, a 16% decline over our net income of

$3.1 million earned during 2007. The decline in net income was the

result of the decrease in gross profit and the decrease in other income,

partially offset by the reduction in income tax expense.

Wholesale

Leathercraft

The

increases (or decreases) in net sales, operating income, operating income

increases (or decreases) and operating income as a percentage of sales from our

Wholesale Leathercraft stores for the three years ended December 31, 2009 were

as follows:

|

Year

|

Net

Sales Incr

(Decr)

from Prior Yr

|

Operating

Income

|

Operating

Income Incr

(Decr)

from Prior Year

|

Operating

Income as a Percentage

of Sales

|

|

2009

|

(5.3)%

|

$2,382,998

|

29.3%

|

9.5%

|

|

2008

|

(10.6)%

|

$1,842,526

|

(34.8)%

|

6.9%

|

|

2007

|

(3.7)%

|

$2,826,710

|

(41.3)%

|

9.6%

|

Wholesale

Leathercraft, consisting of our 30 wholesale stores and our national account

group, accounted for 45.6% of our consolidated net sales in 2009, which compares

to 49.6% in 2008 and 53.4% in 2007. The decrease in this division's

contribution to our total net sales is the result of the growth in Retail

Leathercraft, and we expect this trend to continue.

Sales in

the wholesale stores decreased 5.3% in 2009 compared to sales in 2008 while the

sales decline in our national account group was 3.4% from 2008 to

2009. By customer group, we increased sales to our retail customers,

but had sales declines in all other groups. The most significant

decreases were in our wholesale and manufacturer groups. The

customers comprising these groups are small businesses and have been

significantly affected by the weakness in our economy. Our sales mix

by customer group in the Wholesale Leathercraft division was as

follows:

|

Customer Group

|

2009

|

2008

|

2007

|

|

Retail

|

29%

|

26%

|

23%

|

|

Institution

|

7%

|

8%

|

8%

|

|

Wholesale

|

42%

|

41%

|

42%

|

|

National

Accounts

|

15%

|

17%

|

15%

|

|

Manufacturers

|

7%

|

8%

|

12%

|

|

100%

|

100%

|

100%

|

The 2009

increase in operating income as a percentage of divisional sales resulted from a

decrease in operating expenses of $500,000. Significant operating

expense decreases occurred in legal and professional fees ($57,000), moving

expenses ($114,000), advertising and marketing ($200,000), outside services

($158,000), rent and utilities ($95,000) and freight out

($143,000). These decreases were offset somewhat by a loss incurred

on the impairment of certain computer equipment totaling $365,000.

The 2008

decrease in operating income as a percentage of divisional sales resulted from a

decrease of 9.2% in gross margin (as a percentage of sales) compared with 2007,

offset partially by a decrease of 3.4% in operating expenses as a percent of

sales. Significant operating expense decreases occurred in employee