Attached files

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

[x]

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

fiscal year ended December 31, 2009

OR

|

[ ]

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

transition period from ______ to ______

Commission

file

number: 1-1445

HAVERTY

FURNITURE COMPANIES, INC.

|

Maryland

|

58-0281900

|

|

(State

of Incorporation)

|

(IRS

Employer Identification Number)

|

|

780

Johnson Ferry Road, Suite 800

Atlanta,

Georgia

|

30342

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

|

(404)

443-2900

|

|

|

(Registrant’s

telephone number, including area

code)

|

|

Securities

registered pursuant to Section 12(b) of the Act:

|

Title

of each Class

|

Name

of each exchange of which registered

|

|

Common

Stock ($1.00 Par Value)

|

New

York Stock Exchange, Inc.

|

|

Class

A Common Stock ($1.00 Par Value)

|

New

York Stock Exchange, Inc.

|

Securities registered pursuant to

Section 12(g) of the Act: None.

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes ¨ No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Exchange Act.Yes ¨ No x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No ¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such

files). Yes ¨ No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, or a non-accelerated filer, or a smaller reporting company.

See definition of “large accelerated filer,” “accelerated filer” and

“smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large

accelerated filer o

|

Accelerated

filer x

|

|

Non-accelerated

filer o

(Do

not check if a smaller reporting company)

|

Smaller

reporting company o

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12B-2 of the Exchange Act). Yes ¨ No x

As of

June 30, 2009, the aggregate market value of the registrant’s common stock held

by non-affiliates of the registrant was $174,515,615 (based on the closing sale

prices of the registrant’s two classes of common stock as reported by the New

York Stock Exchange).

There

were 17,534,348 shares of common stock and 3,892,532 shares of Class A common

stock, each with a par value of $1.00 per share outstanding at February 28,

2010.

DOCUMENTS

INCORPORATED BY REFERENCE

Portions

of the registrant’s Proxy Statement for the Annual Meeting of Stockholders to be

held May 10, 2010 are incorporated by reference in Part III.

HAVERTY

FURNITURE COMPANIES, INC.

Annual

Report on Form 10-K for the year ended December 31, 2009

Table

of Contents

|

Page

|

|||

|

PART

I

|

|||

|

Item

1.

|

Business

|

1

|

|

|

Item

1A.

|

Risk

Factors

|

5

|

|

|

Item

1B.

|

Unresolved

Staff Comments

|

9

|

|

|

Item

2.

|

Properties

|

9

|

|

|

Item

3.

|

Legal

Proceedings

|

10

|

|

|

Item

4.

|

Reserved

|

10

|

|

|

PART

II

|

|||

|

Item

5.

|

Market

for the Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

11

|

|

|

Item

6.

|

Selected

Financial Data

|

14

|

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

15

|

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures about Market Risk

|

26

|

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

27

|

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

27

|

|

|

Item

9A.

|

Controls

and Procedures

|

27

|

|

|

Item

9B.

|

Other

Information

|

30

|

|

|

PART

III

|

|||

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

30

|

|

|

Item

11.

|

Executive

Compensation

|

31

|

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

31

|

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

32

|

|

|

Item

14.

|

Principal

Accounting Fees and Services

|

32

|

|

|

PART

IV

|

|||

|

Item

15.

|

Exhibits,

Financial Statement Schedules

|

32

|

ITEM

1. BUSINESS

Unless

otherwise indicated by the context, we use the terms “Havertys," "we," "our," or

"us" when referring to the consolidated operations of Haverty Furniture

Companies, Inc.

This

document contains “forward-looking statements” – that is, statements related to

future, not past, events. In this context, forward-looking statements often

address our expected future business and financial performance and financial

condition.

Forward-looking

statements include, but are not limited to:

|

·

|

projections

of revenues, costs, earnings per share, capital expenditures, dividends or

other financial measures;

|

|

·

|

descriptions

of anticipated plans or objectives of our management for operations or

products;

|

|

·

|

forecasts

of performance; and

|

|

·

|

assumptions

regarding any of the foregoing.

|

Because

these statements involve anticipated events or conditions, forward-looking

statements often include words such as “anticipate,” “believe,” “estimate,”

“expect,” “intend,” “plan,” “project,” “target,” “can,” “could,” “may,”

“should,” “will,” “would,” or similar expressions. Do not unduly rely on

forward-looking statements. They represent our expectations about the future and

are not guarantees. Forward-looking statements are only as of the date they are

made and they might not be updated to reflect changes as they occur after the

forward-looking statements are made.

For

example, forward-looking statements include expectations regarding:

|

·

|

sales

or comparable store sales;

|

|

·

|

gross

profit;

|

|

·

|

SG&A

expenses; and

|

|

·

|

capital

expenditures.

|

Overview

Havertys

is a specialty retailer of residential furniture and accessories. Our founder,

J.J Haverty began the business in 1885 in Atlanta, Georgia with one store and

made deliveries using horse-drawn wagons. The Company grew to 18 stores and

accessed additional capital for growth through its initial public offering in

October 1929.

Havertys

has grown to over 100 stores in 17 states in the Southern and Midwest regions.

All of our stores are operated using the Havertys name and we do not franchise

our stores. We provide our customers a wide selection of products and styles

primarily in the middle to upper-middle price ranges. A majority of the

furniture merchandise we carry bears the Havertys brand. We also offer

nationally well-known bedding product lines of Sealy®, Serta® and

Tempur-Pedic®. We tailor our merchandise presentation to the needs

and tastes of the local markets we serve with a product mix that is roughly 12%

regionalized. This varietal mix allows us to offer more “coastal” or “western”

or “urban” looks to the appropriate markets.

We have

avoided utilizing lower quality, promotional price-driven merchandise favored by

many national chains, which we believe would devalue the Havertys brand with the

consumer. As an added convenience to our customers, we offer

financing through an internal revolving charge credit plan or by a third-party

finance company.

1

Revenues

The

following table sets forth the approximate percentage contributions by product

and service to our gross revenues for the past three years:

|

Year ended

December 31,

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Merchandise:

|

||||||||||||

|

Living

Room Furniture

|

48.4 | % | 48.2 | % | 48.1 | % | ||||||

|

Bedroom

Furniture

|

20.4 | 21.4 | 21.3 | |||||||||

|

Dining

Room Furniture

|

11.4 | 11.7 | 11.6 | |||||||||

|

Bedding

|

10.1 | 9.4 | 10.1 | |||||||||

|

Accessories

and Other (1)

|

9.5 | 9.0 | 8.6 | |||||||||

|

Credit

Service Charges

|

0.2 | 0.3 | 0.3 | |||||||||

| 100.0 | % | 100.0 | % | 100.0 | % | |||||||

(1) Includes

delivery charges and product protection.

Stores

We strive

to have our stores reflect the distinctive style and comfort consumers expect to

find when purchasing their home furnishings. The store’s curb appeal

is important to the type of middle to upper-middle income consumer that we

target and our use of classical facades and attractive landscaping complements

the quality and style of our merchandise. Interior details such as

floor surfaces, lighting and music have been carefully chosen as backgrounds for

a pleasant and inviting shopping experience. We persistently review

our showrooms’ floor layouts to ensure that we are merchandising in the best

manner.

As of

December 31, 2009, we operated 121 stores serving 80 cities in 17 states. We

have executed a program of remodeling and expanding showrooms and replacing

older smaller stores in growth markets with new larger stores, closing certain

locations and moving into new markets. Accordingly, the number of retail

locations has increased by 18 since the end of 1999, but total square footage

has increased approximately 25%.

The

downturn in the retail sector has generated a number of available “empty boxes”

and we are considering select locations within our geographic

footprint. We are also evaluating our existing stores for relocation

or closure. Two stores that reached the end of their lease were

closed in early 2010. We expect to reduce our retail square footage

by 1% to 2% in 2010.

Internet

Our

website has proven to be useful in reaching the growing number of consumers that

use the internet to pre-shop before going to a store. The site also

provides our sales associates a tool to further engage the customer while she is

in the store and extend her shopping experience when she returns

home. We limit on-line sales of our furniture to within our delivery

network, and accessories to the continental United States. We believe

that a direct-to-customer business complements our retail store operations by

building brand awareness and is an effective advertising vehicle.

The first

stage of our improved website went live in early October 2007 and featured

enhanced shopping, consumer product reviews, credit application and delivery

availability. Our site now provides consumers with room planners,

allows them to develop “wish lists,” place orders on-line and set delivery of

their purchases. Post-purchase features include “follow the

truck” for deliveries and customer service opportunities. Our

website received approximately 6 million unique visitors during 2009, a 17%

increase over 2008.

2

Suppliers

We have

developed strong relationships with our suppliers and believe that we receive

excellent pricing and service from our key vendors due to the volume and

reliability of our purchase commitments. We buy our merchandise from

numerous foreign and domestic manufacturers and importers, the largest of which

accounted for approximately 9% of our purchasing during

2009. Wood products, or “case goods,” are generally imported

from Asia, with less than 7% of our selected case goods at December 31, 2009

produced domestically. Upholstered items are not as heavily imported,

with the exception of our leather products. Approximately 93% of our

leather merchandise was imported from Mexico or Asia during 2009.

Competition

The

retail sale of home furnishings is a highly fragmented and competitive business.

The degree and source of competition vary by geographic area. We compete with

numerous individual retail furniture stores as well as chains and certain

department stores. Department stores benefit competitively from more established

name recognition in specific markets, a larger customer base due to their

non-furnishings product lines and proprietary credit cards. Furniture

manufacturers have also opened their own dedicated retail stores in an effort to

control and protect the distribution prospects of their branded

merchandise.

We

believe Havertys is uniquely positioned in the marketplace, with a targeted mix

of merchandise that appeals to customers who are somewhat more affluent than

those of competitive price-oriented furniture store chains. We believe that our

customer segment responds more cautiously to typical discount promotions and

focuses on the product quality and customer service offered by a retailer. We

believe our ability to make prompt delivery of orders through maintenance of

inventory and to tailor merchandise to customers’ desires on a local market

basis are significant competitive advantages. We also consider our experienced

sales personnel and customer service as important factors in our competitive

success.

Employees

As of

December 31, 2009, we had approximately 3,000 employees: 2,310 in individual

retail store operations, 150 in our corporate and credit operations, 40 in our

customer-service call centers, and 500 in our warehouse and delivery

points. Our full-time headcount decreased by approximately 16%

in 2009 compared to 2008. These reductions were necessary to align

staffing levels with the sales declines. None of our employees are a

party to any union contract.

Trademarks

and Domain Names

We have

registered our various logos, trademarks and service marks. We

believe that our trademark position is adequately protected in all markets in

which we do business. In addition, we have registered and

maintain numerous internet domain names including

“havertys.com.” Collectively, the trademarks, service marks and

domain names that we hold are of material importance to us. We

believe that our trade names are recognized by consumers and are associated with

a high level of quality, value and service.

Governmental

Regulation

Our

operations are required to meet federal, state and local regulatory standards in

the areas of safety, health and environmental pollution controls. Historically,

compliance with these standards has not had a material adverse effect on our

operations. We believe that our facilities are in compliance, in all material

respects,

with applicable federal, state and local laws and regulations concerned with

safety, health and environmental protection.

3

The

products we sell are subject to federal regulatory standards including, but not

limited to, those outlined in the Consumer Product Safety Improvement

Act. We have processes in place to ensure compliance with these

standards and that these processes are adjusted as necessary for changes in the

regulations. We believe that the products we sell are in substantial

compliance with the regulatory standards governing such products.

The

extension of credit to consumers is a highly regulated area of our business.

Numerous federal and state laws impose disclosure and other requirements on the

origination, servicing and enforcement of credit accounts. These laws include,

but are not limited to, the Federal Truth and Lending Act, Equal Credit

Opportunity Act, Credit CARD Act, and Federal Trade Commission Act. State laws

impose limitations on the maximum amount of finance charges that we can charge

and also impose other restrictions on consumer creditors, such as us, including

restrictions on collection and enforcement. We routinely review our contracts

and procedures to ensure compliance with applicable consumer credit laws.

Failure on our part to comply with applicable laws could expose us to

substantial penalties and claims for damages and, in certain circumstances, may

require us to refund finance charges already paid and to forego finance charges

not yet paid under non-complying contracts. We believe that we are in

substantial compliance with all applicable federal and state consumer credit and

collections laws.

For

More Information About Us

Filings

with the SEC

As a

public company, we regularly file reports and proxy statements with the

Securities and Exchange Commission. These reports are required by the Securities

Exchange Act of 1934 and include:

|

·

|

annual

reports and Form 10-K (such as this

report);

|

|

·

|

quarterly

reports on Form 10-Q;

|

|

·

|

current

reports on Form 8-K; and

|

|

·

|

proxy

statements on Schedule 14A.

|

The SEC

maintains an internet site that contains our reports, proxy and information

statements, and our other SEC filings; the address of that site is

http://www.sec.gov.

Also, we

make our SEC filings available on our own internet site as soon as reasonably

practicable after we have filed with the SEC. Our internet address is

http://www.havertys.com. The information on our website is not

incorporated by reference into this annual report on Form 10-K.

Corporate

Governance

We have a

Code of Business Conduct for our employees and members of our Board of

Directors. A copy of the code and additional information about our corporate

governance guidelines are posted on our website. Click on the “About

Us” and then “Corporate Governance” buttons to find, among other

things:

|

·

|

Corporate

Governance Guidelines;

|

|

·

|

Charter

of the Audit Committee;

|

|

·

|

Charter

of the Compensation Committee; and

|

|

·

|

Charter

of the Governance and Nominating

Committee.

|

4

Any of

these items are available in print free of charge to any stockholder who

requests them. Requests should be sent to Corporate Secretary, Haverty Furniture

Companies, Inc., 780 Johnson Ferry Road, Suite 800, Atlanta,

Georgia 30342.

ITEM

1A. RISK FACTORS

The

following discussion of risk factors contains “forward-looking statements,” as

discussed in Item 1. “Business”. These risk factors may be important to

understanding any statement in this Annual Report on Form 10-K or elsewhere. The

following information should be read in conjunction with Part II, Item 7.

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations” (MD&A), and the consolidated financial statements and related

notes in Part II, Item 8. “Financial Statements and Supplementary Data” of this

Form 10-K Report.

We

routinely encounter and address risks, some of which will cause our future

results to be different – sometimes materially different – than we presently

anticipate. Below, we describe certain important operational and strategic

risks. Our reactions to material future developments as well as our competitors’

reactions to those developments will affect our future results.

Changes in economic conditions could

adversely affect demand for our products.

A large

portion of our sales represent discretionary spending by our customers. A number

of economic factors, including, but not limited to availability of consumer

credit, interest rates, consumer confidence and debt levels, retail trends,

housing starts, sales of existing homes, and the level of mortgage refinancing,

generally affect demand for our products. Higher unemployment rates, higher fuel

and other energy costs, and higher tax rates adversely affect demand. The

decline in economic activity and conditions in the markets in which we operate

has, and may continue to, adversely affect our financial condition and results

of operations for the foreseeable future.

The

financial crisis could adversely affect our business and financial

performance.

The

ongoing financial crisis has tightened credit markets and lowered liquidity

levels. Lower credit availability may increase borrowing costs. Some of our

suppliers are experiencing serious financial problems due to reduced access to

credit and lower revenues. Financial duress may prompt some of our suppliers to

seek to renegotiate terms with us, reduce production or file for bankruptcy

protection. Our customers may be unable to obtain financing to purchase products

and meet their payment obligations to us. The occurrence of these

events may adversely affect our operations, earnings, cash flows and/or

financial position.

We

face significant competition from national, regional and local retailers of home

furnishings.

The

retail market for home furnishings is highly fragmented and intensely

competitive. We currently compete against a diverse group of retailers,

including national department stores, regional or independent specialty stores,

and dedicated franchises of furniture manufacturers. National mass merchants

such as COSTCO also have limited product offerings. We also compete with

retailers that market products through store catalogs and the Internet. In

addition, there are few barriers to entry into our current and contemplated

markets, and new competitors may enter our current or future markets at any

time.

5

We

may not be able to compete successfully against existing and future competitors.

Some of our competitors have financial resources that are substantially greater

than ours and may be able to purchase inventory at lower costs and better

sustain economic downturns. Our competitors may respond more quickly to new or

emerging technologies and may have greater resources to devote to promotion and

sale of products.

Our

existing competitors or new entrants into our industry may use a number of

different strategies to compete against us, including:

|

·

|

aggressive

advertising, pricing and marketing;

|

|

·

|

extension

of credit to customers on terms more favorable than we

offer;

|

|

·

|

larger

store size, which may result in greater operational efficiencies, wider

product assortments or innovative store

formats;

|

|

·

|

adoption

of improved retail sales methods;

and

|

|

·

|

expansion

by our existing competitors or entry by new competitors into markets where

we currently operate.

|

Competition

from any of these sources could cause us to lose market share, revenues and

customers, increase expenditures or reduce prices, any of which could have a

material adverse effect on our results of operations.

If

new products are not introduced or consumers do not accept new products, our

sales may decline.

Our

ability to maintain and increase revenues depends to a large extent on the

periodic introduction and availability of new products. We believe that the

introduction and consumer acceptance of our proprietary Havertys brand is a

significant part of our ability to maintain or increase revenues. These products

are subject to fashion changes and pricing limitations which could affect the

success of these and other new products.

If

we fail to anticipate changes in consumer preferences, our sales may

decline.

Our

products must appeal to our target consumers whose preferences cannot be

predicted with certainty and are subject to change. Our success depends upon our

ability to anticipate and respond in a timely manner to fashion trends relating

to home furnishings. If we fail to identify and respond to these changes, our

sales of these products may decline. In addition, we often make commitments to

purchase products from our vendors in advance of proposed delivery dates.

Significant deviation from the projected demand for products that we sell may

have a material adverse effect on our results of operations and financial

condition, either from lost sales or lower margins due to the need to reduce

prices to dispose of excess inventory.

We

import a substantial portion of our merchandise from foreign sources. Changes in

exchange rates or tariffs could impact the price we pay for these goods,

resulting in potentially higher retail prices and/or lower gross profit on these

goods.

During

2009, approximately 71% of our furniture purchases, on a dollar basis were for

goods not produced domestically. All of these purchases were denominated in U.S.

dollars. As exchange rates between the U.S. dollar and certain other currencies

become unfavorable, the likelihood of price increases from our vendors

increases. Some of the products we purchase are also subject to tariffs. If

tariffs are imposed on additional products or the tariff rates are increased our

vendors may increase their prices. Such price increases, if they occur, could

have one or more of the following impacts:

|

·

|

we

could be forced to raise retail prices so high that we are unable to sell

the products at current unit

volumes;

|

6

|

·

|

if

we are unable to raise retail prices commensurately with the costs

increases, gross profit as recognized under our LIFO inventory accounting

method could be negatively impacted;

or

|

|

·

|

we

may be forced to find alternative sources of comparable product, which may

be more expensive than the current product, of lower quality, or the

vendor may be unable to meet our requirements for quality, quantities,

delivery schedules or other key

terms.

|

Fluctuations and volatility in the

cost of raw materials and components could adversely affect our

profits.

The

primary materials our vendors use to produce and manufacture our products are

various woods and wood products, resin, steel, leather, cotton, and certain oil

based products. On a global and regional basis, the sources and prices of those

materials and components are susceptible to significant price fluctuations due

to supply/demand trends, transportation costs, government regulations and

tariffs, changes in currency exchange rates, price controls, the economic

climate, and other unforeseen circumstances. Significant increases in these and

other costs in the future could materially affect our vendors’ costs and our

profits as discussed above.

As

a result of our reliance on foreign sourcing our ability to service customers

could be adversely affected and result in lower sales and earnings.

Our

overseas vendors may not supply goods that meet our quality specifications or

are in conformity with the regulations set forth in the Consumer Product Safety

Improvements Act or other federal regulations. If suppliers do not

provide a general conformity certificate then U.S. Customs may turn the goods

away at the port. We may reject product that does not meet our

specifications. Accordingly, we may be forced to find alternative

sourcing arrangements at a higher cost or to discontinue the

product.

Our

revenue could be adversely affected by a disruption in our supply

chain.

Disruptions

to our supply chain could result in late arrivals of product. This could

negatively affect sales due to increased levels of out-of-stock merchandise and

loss of confidence by customers in our ability to deliver goods as

promised.

The

rise of oil and gasoline prices could affect our profitability.

A

significant increase in oil and gasoline prices could adversely affect our

profitability. Our distribution system, which utilizes three distribution

centers and multiple home delivery centers to reach our markets across 17

Southern and Midwestern states, is very transportation dependent. Additionally,

we deliver substantially all of our customers’ purchases to their

homes.

If

transportation costs exceed amounts we are able to effectively pass on to the

consumer, either by higher prices and/or higher delivery charges, then our

profitability will suffer.

Our business depends on our ability

to meet our labor needs.

Our

success depends on hiring and retaining quality managers and sales associates to

maintain consistency in the high level of customer service in our stores. Also,

our sales associates are compensated under a commission structure which

historically fosters a high rate of turnover. We are also dependent

on the employees who staff our distribution centers, many of whom are skilled.

We may be unable to meet our labor needs and control our costs due to external

factors such as unemployment levels, minimum wage legislation and wage

inflation. Although none of our employees are currently covered under collective

bargaining agreements, we cannot guarantee that our employees will not elect to

be represented by labor unions in the future.

7

Because

of our limited number of distribution centers, should one become damaged, our

operating results could suffer.

We

utilize three large distribution centers to flow our merchandise from the vendor

to the consumer. This system is very efficient for reducing inventory

requirements, but makes us operationally vulnerable should one of these

facilities become damaged.

Our

information technology infrastructure is vulnerable to damage that could harm

our business.

Our

ability to operate our business from day to day, in particular our ability to

manage our point-of-sale, credit operations and distribution system, largely

depends on the efficient operation of our computer hardware and software

systems. We use management information systems to communicate customer

information, provide real-time inventory information, manage our credit

portfolio and to handle all facets of our distribution system from receiving of

goods in the DCs to delivery to our customers’ homes. These systems and our

operations are vulnerable to damage or interruption from:

|

·

|

power

loss, computer systems failures and Internet, telecommunications or data

network failures.

|

|

·

|

operator

negligence or improper operation by, or supervision of,

employees;

|

|

·

|

physical

and electronic loss of data or security breaches, misappropriation and

similar events;

|

|

·

|

computer

viruses;

|

|

·

|

intentional

acts of vandalism and similar events;

and

|

|

·

|

tornadoes,

fires, floods and other natural

disasters.

|

Any

failure due to any of these causes, if it is not supported by our disaster

recovery plan and redundant systems, could cause an interruption in our

operations and result in reduced net sales and profitability.

We

may incur costs resulting from security risks we face in connection with our

electronic processing and transmission of confidential customer

information.

We accept

electronic payment cards for payment in our stores. During 2009, approximately

50% of our sales were attributable to credit card transactions, and credit card

usage could continue to increase.

We may in

the future become subject to claims for purportedly fraudulent transactions

arising out of the actual or alleged theft of credit or debit card information,

and we may also be subject to lawsuits or other proceedings in the future

relating to these types of incidents. Proceedings related to theft of credit or

debit card information may be brought by payment card providers, banks and

credit unions that issue cards, cardholders (either individually or as part of a

class action lawsuit) and federal and state regulators. Any such proceedings

could distract our management from running our business and cause us to incur

significant unplanned losses and expenses. Consumer perception of our brand

could also be negatively affected by these events, which could further adversely

affect our results and prospects.

Significant

differences between actual results and estimates of the amount of future funding

for our pension plans and significant changes in funding assumptions or

significant increases in funding obligations due to regulatory changes could

adversely affect our financial results.

We have a

funded non-contributory defined benefit pension plan that covers most of our

employees. We also have an unfunded non-qualified, non-contributory

supplemental executive retirement plan (SERP). The Employee

Retirement Income Security Act of 1974 (ERISA) and the Internal Revenue Code

govern the funding obligations for our pension plans. Our defined

benefit plan was frozen as of December 31, 2006 for substantially all

participants. For 2007 and beyond, Havertys employees may participate in our

enhanced defined contribution plan.

As of

December 31, 2009, our projected benefit obligations under our retirement plans

exceeded the fair value of plan assets by an aggregate of approximately $14.4

million ($9.6 million of which was

8

attributable

to the defined pension plan and $4.8 million of which was attributable to the

SERP). Estimates for the amount and timing of the future funding obligations of

these plans are based on various assumptions. These assumptions include the

discount rates and expected long-term rate of return on plan assets. These

assumptions are subject to change based on interest rates on high quality bonds,

and stock and bond market returns. Significant differences in results

or significant changes in assumptions may materially affect our retirement plan

obligations and related future contributions and expense.

The terms of our revolving credit

facility impose operating and financial restrictions on us, which may constrain

our ability to respond to changing business and economic conditions. This

constraint could have a significant adverse impact on our

business.

Our

current revolving credit facility contains provisions which restrict our ability

to, among other things, incur additional indebtedness, issue additional shares

of capital stock in certain circumstances, make particular types of investments,

incur certain types of liens, pay cash dividends, redeem capital stock,

consummate mergers of certain sizes, enter into transactions with affiliates or

make substantial asset sales. In addition, our obligations under the revolving

credit facility are secured by interests in substantially all of our personal

property, primarily our inventories, accounts receivable and cash, excluding

store and distribution center equipment and fixtures. In the event of a

significant loss in value of our inventory the amount available to borrow will

be reduced and may place us in default. In the event of insolvency,

liquidation, dissolution or reorganization, the lenders under our revolving

credit facility would be entitled to payment in full from our assets before

distributions, if any, were made to our stockholders.

If we are

unable to generate sufficient cash flows from operations in the future, we may

have to refinance all or a portion of our debt and/or obtain additional

financing. We cannot assure you that refinancing or additional financing on

favorable terms could be obtained.

Use

of Estimates

Our

Consolidated Financial Statements and accompanying Notes include estimates and

assumptions made by Management that affect reported amounts. Actual results

could differ materially from those estimates.

ITEM

1B. UNRESOLVED

STAFF COMMENTS

Not

applicable.

ITEM

2. PROPERTIES

Stores

Our

retail store space at December 31, 2009 totaled approximately 4,278,000 square

feet for 121 stores compared to 4,292,000 square feet for 122 stores at December

31, 2008. The following table sets forth the number of stores we

operated at December 31, 2009 by state for our 121 locations:

|

State

|

Number

of Stores

|

State

|

Number

of Stores

|

|

|

Florida

|

28

|

Kentucky

|

4

|

|

|

Texas

|

21

|

Maryland

|

3

|

|

|

Georgia

|

16

|

Arkansas

|

2

|

|

|

Virginia

|

9

|

Mississippi

|

1

|

|

|

North

Carolina

|

8

|

Ohio

|

2

|

|

|

Alabama

|

7

|

Indiana

|

1

|

|

|

South

Carolina

|

7

|

Kansas

|

1

|

|

|

Tennessee

|

6

|

Missouri

|

1

|

|

|

Louisiana

|

4

|

9

The 41

retail locations which we owned at December 31, 2009, had a net book value of

land and buildings of $95.7 million. Additionally, we have three

leased locations with a net book value of $6.2 million which, due to financial

accounting rules, are included in our financial statements. The

remaining 77 locations are leased by us with various termination dates through

2025 plus renewal options.

Distribution

Facilities

We lease

or own regional distribution facilities in the following locations:

|

Location

|

Owned

or Leased

|

Approximate

Square Footage

|

|

Braselton,

Georgia

|

Leased

|

808,000

|

|

Coppell,

Texas

|

Owned

|

238,000

|

|

Lakeland,

Florida

|

Owned

|

226,000

|

|

Colonial

Heights, Virginia

|

Owned

|

129,000

|

|

Fairfield,

Ohio

|

Leased

|

50,000

|

|

Jackson,

Mississippi

|

Leased

|

26,000

|

We also

use five smaller leased cross-dock facilities, one of which is attached to a

retail location.

Corporate

Facilities

Our

executive and administrative offices are located at 780 Johnson Ferry Road,

Suite 800, Atlanta, Georgia. These leased facilities contain approximately

48,000 square feet of office space on two floors of a mid-rise office building.

Havertys Credit leases 7,000 square feet of office space in Chattanooga,

Tennessee.

For

additional information, see “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” included in this report under Item 7 of

Part II.

ITEM

3. LEGAL PROCEEDINGS

There are

no material pending legal proceedings to which we are a party or of which any of

our properties is the subject.

ITEM

4. RESERVED

10

PART

II

|

ITEM

5.

|

MARKET

FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

Market

Information

The

Company’s common stock and Class A common stock are traded on the New York Stock

Exchange under the trading symbols “HVT” and “HVTA”. Information

regarding the high and low sales prices per share of both classes of common

stock in 2009 and 2008 is included in Note 16, “Market Prices and Dividend

Information,” to the Company’s Consolidated Financial Statements.

Stockholders

The

number of stockholders was approximately 2,850 for our common stock and 250 for

our Class A common stock as of December 31 2009.

Dividends

The

payment of dividends and the amount are determined by the Board of Directors and

depend upon, among other factors, our earnings, operations, financial condition,

capital requirements and general business outlook at the time such dividend is

considered. We had paid a quarterly cash dividend since 1935 but

given the general economic decline, the board suspended the dividend in the

fourth quarter of 2008. The board approved a dividend in the fourth

quarter of 2009. Information regarding the payments of dividends for

2009 and 2008 is included in Note 16, “Market Prices and Dividend Information,”

to our Consolidated Financial Statements

Equity

Compensation Plans

Information concerning

the Company’s equity compensation plans is set forth in Item 11 of Part II of

this Annual Report on Form 10-K.

11

Stock

Performance Graph

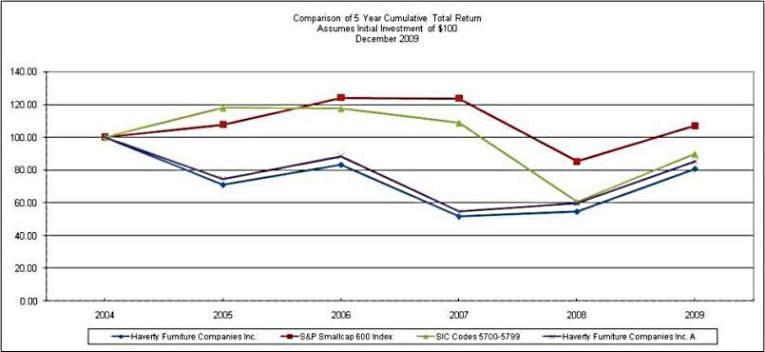

The

following graph compares the performance of Havertys’ common stock and Class A

common stock against the cumulative return of the NYSE/AMEX/Nasdaq Home

Furnishings & Equipment Stores Index (SIC Codes 5700 – 5799) and the S&P

Smallcap 600 Index for the period of five years commencing December 31, 2004 and

ended December 31, 2009. The graph assumes an initial investment of

$100 on January 1, 2004 and reinvestment of dividends.

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

|||||||||||||||||||

|

HVT

|

$ | 100.0 | $ | 70.98 | $ | 83.06 | $ | 51.70 | $ | 54.69 | $ | 80.65 | ||||||||||||

|

HVT-A

|

$ | 100.0 | $ | 74.55 | $ | 88.36 | $ | 54.67 | $ | 59.57 | $ | 85.14 | ||||||||||||

|

S&P

600 Index – Total Return

|

$ | 100.0 | $ | 107.68 | $ | 123.96 | $ | 123.59 | $ | 85.19 | $ | 106.98 | ||||||||||||

|

SIC

Codes 5700-5799

|

$ | 100.0 | $ | 117.92 | $ | 117.70 | $ | 108.88 | $ | 60.61 | $ | 89.75 | ||||||||||||

12

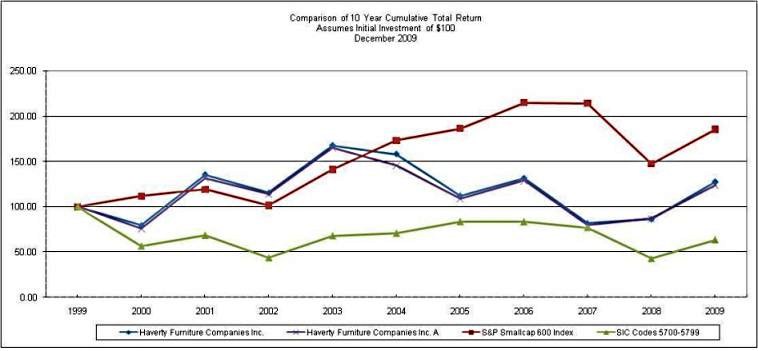

We are

also presenting a ten-year performance graph comparing the yearly percentage

change in the cumulative total stockholder return on Havertys’ common stock and

Class A common stock against the cumulative return of the NYSE/AMEX/Nasdaq Home

Furnishings & Equipment Stores Index (SIC Codes 5700-5799) and the S&P

Smallcap 600 Index for the period of ten years commencing December 31, 1999, and

ended December 31, 2009. The graph assumes an initial investment of

$100 on January 1, 1999 and reinvestment of dividends.

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

2005

|

2006

|

2007

|

2008

|

2009

|

||||||||||||||||||||||||||||||||||

|

HVT

|

$ | 100.00 | $ | 79.66 | $ | 135.55 | $ | 115.50 | $ | 167.55 | $ | 158.15 | $ | 112.26 | $ | 131.37 | $ | 81.77 | $ | 86.50 | $ | 127.55 | ||||||||||||||||||||||

|

HVT-A

|

$ | 100.00 | $ | 75.59 | $ | 131.08 | $ | 113.87 | $ | 164.95 | $ | 145.50 | $ | 108.47 | $ | 128.56 | $ | 79.55 | $ | 86.67 | $ | 123.87 | ||||||||||||||||||||||

|

S&P

600 Index

Total

Return

|

$ | 100.00 | $ | 118.80 | $ | 119.11 | $ | 101.68 | $ | 141.13 | $ | 173.09 | $ | 186.39 | $ | 214.56 | $ | 213.92 | $ | 147.46 | $ | 185.17 | ||||||||||||||||||||||

|

SIC

Codes

5700-5799

|

$ | 100.00 | $ | 56.64 | $ | 68.40 | $ | 43.82 | $ | 67.92 | $ | 70.76 | $ | 83.44 | $ | 83.28 | $ | 77.04 | $ | 42.88 | $ | 63.50 | ||||||||||||||||||||||

13

ITEM

6. SELECTED

FINANCIAL DATA

The

following selected financial data should be read in conjunction with

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations” included in Item 7 below and the Consolidated Financial Statements

and Notes thereto included in Item 8 below.

|

Year

ended December 31,

|

||||||||||||||||||||

|

(Dollars

in thousands, except per share data)

|

2009

|

2008

|

2007

|

2006

|

2005

|

|||||||||||||||

|

Net

sales

|

$ | 588,264 | $ | 691,079 | $ | 784,613 | $ | 859,101 | $ | 827,658 | ||||||||||

|

Gross

profit

|

305,498 | 357,089 | 389,750 | 426,155 | 395,567 | |||||||||||||||

|

Percent

of net sales

|

51.9 | % | 51.7 | % | 49.7 | % | 49.6 | % | 47.8 | % | ||||||||||

|

Selling,

general and administrative expenses

|

310,523 | 364,080 | 391,105 | 404,518 | 377,435 | |||||||||||||||

|

Percent

of net sales

|

52.8 | % | 52.7 | % | 49.8 | % | 47.1 | % | 45.6 | % | ||||||||||

|

(Loss)

income before income taxes

|

(5,408 | ) | (6,532 | ) | 1,944 | 25,624 | 23,554 | |||||||||||||

|

Net

(loss) income1

|

(4,179 | ) | (12,101 | ) | 1,758 | 16,000 | 15,054 | |||||||||||||

|

Basic

net (loss) earnings per share

|

||||||||||||||||||||

|

Common

Stock

|

$ | (0.20 | ) | $ | (0.57 | ) | $ | 0.08 | $ | 0.72 | $ | 0.67 | ||||||||

|

Class

A

|

$ | (0.19 | ) | $ | (0.55 | ) | $ | 0.07 | $ | 0.67 | $ | 0.63 | ||||||||

|

Diluted net

(loss) earnings per share

|

||||||||||||||||||||

|

Common

Stock

|

$ | (0.20 | ) | $ | (0.57 | ) | $ | 0.08 | $ | 0.70 | $ | 0.66 | ||||||||

|

Class

A

|

$ | (0.19 | ) | $ | (0.55 | ) | $ | 0.07 | $ | 0.67 | $ | 0.63 | ||||||||

|

Cash

dividends:

|

$ | 473 | $ | 4,246 | $ | 5,979 | $ | 6,014 | $ | 5,678 | ||||||||||

|

Amount

per share:

|

||||||||||||||||||||

|

Common

Stock

|

$ | 0.0225 | $ | 0.2025 | $ | 0.270 | $ | 0.270 | $ | 0.255 | ||||||||||

|

Class

A

|

$ | 0.0200 | $ | 0.1875 | $ | 0.250 | $ | 0.250 | $ | 0.235 | ||||||||||

|

Accounts

receivable, net

|

$ | 16,143 | $ | 26,383 | $ | 66,751 | $ | 78,970 | $ | 91,110 | ||||||||||

|

Credit

service charges

|

1,210 | 1,974 | 2,450 | 2,823 | 3,506 | |||||||||||||||

|

Provision

for doubtful accounts

|

978 | 1,654 | 1,328 | 656 | 1,011 | |||||||||||||||

|

Inventories

|

$ | 93,301 | $ | 103,743 | $ | 102,452 | $ | 124,764 | $ | 107,631 | ||||||||||

|

Capital

expenditures

|

$ | 3,259 | $ | 9,544 | $ | 13,830 | $ | 23,640 | $ | 35,007 | ||||||||||

|

Depreciation/amortization

expense

|

19,346 | 21,603 | 22,416 | 21,663 | 21,035 | |||||||||||||||

|

Property

and equipment, net

|

176,363 | 197,423 | 209,912 | 221,245 | 217,391 | |||||||||||||||

|

Total

assets

|

$ | 360,933 | $ | 363,393 | $ | 421,937 | $ | 469,754 | $ | 463,052 | ||||||||||

|

Long-term

debt, including current portion

|

$ | 7,183 | $ | 7,494 | $ | 28,684 | $ | 37,849 | $ | 44,161 | ||||||||||

|

Total

debt

|

7,183 | 7,494 | 28,684 | 50,449 | 48,461 | |||||||||||||||

|

Interest

expense (income), net

|

805 | 390 | (1,307 | ) | (363 | ) | 1,362 | |||||||||||||

|

Accounts

receivable, net to debt

|

224.7 | % | 352.1 | % | 232.7 | % | 156.6 | % | 188.0 | % | ||||||||||

|

Debt

to total capital

|

2.9 | % | 3.0 | % | 9.3 | % | 14.7 | % | 14.8 | % | ||||||||||

|

Stockholders’

equity

|

$ | 244,557 | $ | 244,968 | $ | 278,845 | $ | 291,923 | $ | 279,270 | ||||||||||

|

Shares

outstanding (in thousands):

|

||||||||||||||||||||

|

Common

|

17,519 | 17,291 | 17,308 | 18,473 | 18,133 | |||||||||||||||

|

Class

A

|

3,908 | 4,032 | 4,136 | 4,202 | 4,306 | |||||||||||||||

|

Total

shares

|

21,427 | 21,323 | 21,444 | 22,675 | 22,439 | |||||||||||||||

|

Other

Supplemental Data:

|

||||||||||||||||||||

|

Employees

|

3,000 | 3,600 | 4,200 | 4,500 | 4,400 | |||||||||||||||

|

Retail

sq. ft. (in thousands)

|

4,278 | 4,292 | 4,324 | 4,208 | 4,144 | |||||||||||||||

|

Number

of retail locations

|

121 | 122 | 123 | 120 | 118 | |||||||||||||||

|

Annual

net sales per weighted average sq. ft.

|

$ | 139 | $ | 160 | $ | 186 | $ | 206 | $ | 202 | ||||||||||

|

(1)

|

During

the fourth quarter of 2008 we recorded an $8.2 million charge to income

tax expense to record a valuation allowance on certain of our deferred tax

assets. For additional information see page 20 in Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

14

ITEM

7 MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

Overview

We focus

on several key metrics in managing and evaluating our operating performance and

financial condition including the following: comparable store sales,

sales per square foot, gross profit, operating costs as a percentage of sales,

cash flow, total debt to total capital, and earnings (loss) per

share.

Our sales

are generated by customer purchases of home furnishings in our retail stores or

via our website and recorded as revenue when delivered to the

customer. There is typically a two-week lag between a customer

placing an order and their ability to arrange their schedule for

delivery. Comparable-store or “comp-store” sales is a measure which

indicates the performance of our existing stores by comparing the growth in

sales for these stores for a particular period over the corresponding period in

the prior year. Stores are considered non-comparable if open for less

than 12 full calendar months or if the selling square footage has been changed

significantly during the past 12 full calendar months. Large

clearance sales events from warehouses or temporary locations are also excluded

from comparable store sales, as are periods when stores are closed or being

remodeled. As a retailer, comp-store sales is an indicator of relative customer

spending and store performance.

Our cost

of sales consist primarily of the purchase price of the merchandise together

with inbound freight, handling within our distribution centers and

transportation costs to the local markets we serve. Our gross profit

is primarily dependent upon vendor pricing, the mix of products sold and

promotional pricing activity. Many retailers have used the lower

costs from overseas production to support their heavy promotional

pricing. Our approach has been to offer products with greater value

at our established middle to upper-middle price points. Substantially all of our

occupancy and home delivery costs are included in selling, general and

administrative expenses as is a portion of our warehousing

expenses. Accordingly, our gross profit may not be comparable to

those entities that include these expenses in cost of goods sold.

The

longer lead times required for deliveries from overseas factories and the

production of merchandise exclusively for Havertys makes it imperative for us to

have both warehousing capabilities and effective supply chain

control. Our Eastern Distribution Center has sufficient capacity to

store imported goods and flow product from our domestic upholstery

suppliers. Our distribution facilities are currently under utilized

due to the severe recession in retail home furniture sales. We

believe our infrastructure could service $1 billion in sales. During

2008 and 2009 we made significant reductions in our warehouse and distribution

workforce in response to the lower sales levels. Product flow

from overseas manufacturers is currently particularly

challenging. Our merchandising and advertising teams provide input to

the ordering process such that we currently have overall inventory levels within

an appropriate range and have reduced the amount of written sales awaiting

product for delivery. Advancements in the availability of real-time

information allow our supply chain team to more closely follow our import orders

from the manufacturing plant through each stage of transit. Using

this tool we can more accurately set customer delivery dates prior to receipt of

product.

Cash

flows continued to be strong during 2009 as we reduced costs and managed our

inventories and generated a $40.8 million increase in cash. Our total

debt to total capital was 2.9% at December 31, 2009.

15

Operating

Results

The

following table sets forth for the periods indicated selected statement of

operations data, expressed as a percentage of net sales:

|

Percentage

of Net Sales

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Net

Sales

|

100.0 | % | 100.0 | % | 100.0 | % | ||||||

|

Cost

of sales

|

48.1 | 48.3 | 50.3 | |||||||||

|

Gross

profit

|

51.9 | 51.7 | 49.7 | |||||||||

|

Credit

service charges

|

0.2 | 0.3 | 0.3 | |||||||||

|

Selling,

general and administrative expenses

|

52.8 | 52.7 | 49.9 | |||||||||

|

Provision

for doubtful accounts

|

0.2 | 0.2 | 0.2 | |||||||||

|

(Loss)

income before income taxes

|

(0.9 | ) | (0.9 | ) | 0.3 | |||||||

|

Net

(loss) income

|

(0.7 | ) | (1.8 | ) | 0.2 | |||||||

Net

Sales

Total

sales declined $102.8 million or 14.9% in 2009 and $93.5 million or 11.9% in

2008, respectively. Comparable store sales declined 14.2% or $94.6

million in 2009 and 14.3% or $109.5 million in 2008. The remaining

$8.2 million and $16.0 million of the changes in 2009 and 2008, respectively,

were from closed, new and otherwise non-comparable stores.

The

following outlines our sales and comp-store sales increases and decreases for

the periods indicated. (Amounts and percentages may not always add to totals due

to rounding.)

|

December

31,

|

|||||||||||||||||||||

|

2009

|

2008

|

2007

|

|||||||||||||||||||

|

Net

Sales

|

Comp-Store

Sales

|

Net

Sales

|

Comp-Store

Sales

|

Net

Sales

|

Comp-Store

Sales

|

||||||||||||||||

|

Period

Ended

|

Dollars

in

millions

|

%

Increase

(decrease)

over

prior

period

|

%

Increase

(decrease)

over

prior

period

|

Dollars

in

millions

|

%

Increase

(decrease)

over

prior

period

|

%

Increase

(decrease)

over

prior

period

|

Dollars

in

millions

|

%

Increase

(decrease)

over

prior

period

|

%

Increase

(decrease)

over

prior

period

|

||||||||||||

| Q1 |

$

|

144.2

|

(22.1

|

)%

|

(22.9

|

)%

|

$

|

185.2

|

(3.1)

|

%

|

(6.3)

|

%

|

$

|

191.1

|

(8.6)

|

%

|

(10.4)

|

%

|

|||

| Q2 |

129.7

|

(23.0

|

)

|

(22.6

|

)

|

168.4

|

(10.0)

|

(12.7)

|

187.1

|

(11.3)

|

(12.7)

|

||||||||||

| Q3 |

151.9

|

(13.5

|

)

|

(11.9

|

)

|

175.6

|

(12.5)

|

(14.9)

|

200.6

|

(10.0)

|

(11.6)

|

||||||||||

| Q4 |

162.4

|

0.4

|

2.0

|

161.9

|

(21.3)

|

(22.6)

|

205.8

|

(4.7)

|

(7.7)

|

||||||||||||

|

Year

|

$

|

588.3

|

(14.9

|

)%

|

(14.2

|

)%

|

$

|

691.1

|

(11.9)

|

% |

(14.3)

|

%

|

$

|

784.6

|

(8.7)

|

%

|

(10.6)

|

%

|

|||

Sales in 2007 declined as consumers reined in their spending and postponed non-essential purchases. There was an increased concentration of sales volume around traditional sales events as consumers believed the best pricing and credit offers were available during these periods. There was significant pressure in our industry as home sales slowed, home prices declined and credit standards tightened.

Sales in

2008 mirrored retail sales in the home furnishings industry which were worse

than the general economic downturn, with the declines accelerating in the fourth

quarter. During the first half of the year we promoted a longer-term

no interest financing offer through a third-party and special pricing on select

merchandise to help stimulate sales. We remained competitive but not

overly aggressive with our general merchandise pricing as we did not believe

such stimulus would be sufficiently accretive to earnings.

16

Sales in

2009 continued to fall as housing sales, one driver of furniture purchases,

remained at historically low levels. Home values have declined and

lending has tightened such that consumers have less access to funding for large

discretionary purchases. We continued to promote longer term no

interest financing but for somewhat shorter periods than last

year. We highlighted more of our price point sensitive items within

our merchandise line-up and showcased their value to appeal to the more cost

conscious consumer.

2010

Outlook

There are

no current indications that the very difficult macro environment is improving in

the near term. We expect to gain share as weak competitors exit the

markets we serve. Our total sales for 2010 and comparable store sales

are expected to be positive given the severity of the declines in 2009, but we

believe total sales will still be below our 2008 levels.

Gross

Profit

Year-to-Year

Comparisons

Gross

profit as a percentage of net sales was relatively flat in 2009 compared to

2008. Strengthened inventory management reduced the impact of

close-out and damaged merchandise by approximately $2.5 million in 2009 compared

to 2008. There was modest deflation and inventory levels declined in

2009. The impact of the change to our LIFO reserve was approximately

a $1.1 million benefit in 2009 compared to a $1.0 million expense in

2008. These changes, along with improvements generated by new

products helped offset much of the impact from promotional pricing discounts on

our gross profit.

Gross

profit improved approximately 200 basis points in 2008 compared to

2007. Reductions in markdowns and our cessation of in-house free

financing for terms greater than one year were the primary contributors to the

improvement. We maintained our pricing discipline and strengthened

our product sourcing which also aided our results.

2010

Outlook

We do not

expect to implement heavy price promotions to stimulate sales. Our

strategy is to generally use promotional pricing selectively during traditional

holiday and other sales events or to highlight specific products or categories.

We expect that gross margins for 2010 will return to our 2008

levels. We anticipate increasing freight costs and labor rates for

our suppliers will generate pressure on product costs which may be difficult to

initially recover in our retail pricing.

Selling,

General and Administrative Expenses

SG&A

expenses are comprised of five categories: selling; occupancy;

delivery and certain warehousing costs; advertising and

administrative. Selling expenses primarily are comprised of

compensation of sales associates and sales support staff, and fees paid to

credit card and third-party finance companies. Occupancy costs

include rents, depreciation charges, insurance and property taxes, repairs and

maintenance expense and utility costs. Delivery costs include

personnel, fuel costs, and depreciation and rental charges for rolling

stock. Warehouse costs include demurrage, supplies, depreciation and

rental charges for equipment. Advertising expenses are primarily

media production and space, direct mail costs, market research expenses,

employee compensation and agency fees. Administrative expenses are

comprised of compensation costs for store management, information systems,

executive finance, merchandising, supply chain, real estate and human resource

departments.

Year-to-Year

Comparisons

Our

SG&A costs decreased $53.6 million for 2009 compared to 2008, a decrease of

14.7%, which mirrors the reduction in sales volume of 14.9% in

2009. Total SG&A costs, as a percentage of net sales were 52.8%

for 2009 as compared to 52.7% in 2008 and 49.9% in 2007.

17

Selling

expenses generally vary with sales volume. The cost of our

third-party financing offers will vary based on usage and the types of credit

programs we offer and those selected by our customers. These costs

were relatively flat as a percentage of net sales in 2009 compared to

2008. During 2008, we offered more promotional credit programs in the

first half of the year and the usage of third-party financing by our customers

increased over 2007. This resulted in increased costs related to

these programs of approximately 24 basis points of sales in 2008.

Occupancy

costs in 2009 decreased $4.8 million from 2008. Reductions in

utilities, depreciation and facility closing costs were partially offset by

increases in store rents. Occupancy expenses increased $0.9 million

in 2008 over 2007 due primarily to higher rents for two new and two relocated

stores.

Warehouse

expenses in 2009 were $7.3 million lower than in 2008 as sales continued to

decline and personnel costs were reduced. Warehouse expenses

decreased $4.8 million in 2008 compared to 2007 as wages and labor costs were

reduced to more closely reflect business conditions.

Delivery

costs decreased in 2009 by approximately $8.8 million from 2008 levels

reflecting the further reductions made in our delivery teams as our business

weakened. Delivery costs decreased in 2008 relative to 2007 by

approximately $2.3 million primarily due to reductions in compensation related

to lower sales volumes offset by the increase in fuel prices.

Total

advertising and marketing costs as a percentage of sales were 6.6% for 2009,

7.0% for 2008 and 7.4% for 2007. Our spending decreased $9.5 million

in 2009 from 2008. We adjusted our advertising mix in 2009 with less

focus on newspaper and more on direct mail and our television advertising is

being shown more frequently during shorter cycles of time for greater impact.

Our spending decreased $9.7 million in 2008 over 2007 without significant

changes in our media mix. We continue to focus on television branding

messages, targeted mail and electronic advertising. These approaches

are a continuation of the “HAVE” brand building campaign begun in late

2006.

Administrative

costs decreased $9.0 million or 11.1% for 2009 over 2008 due primarily to

reductions in staffing levels and related compensation costs partially offset by

increased pension costs. Administrative costs for 2008 declined $3.9 million or

4.6% from 2007 amounts due to reductions in compensation and general insurance

costs.

2010

Outlook

We expect

that SG&A expenses will be lower for 2010 compared to 2009 as a percentage

of net sales as we leverage our fixed costs. Although we are always

looking for ways to contain spending and improve efficiencies, we believe our

fixed cost reductions are significantly complete.

We

believe that we have good controls over our spending and that 2010 sales levels

of approximately $150 to $152 million per quarter at a 51.5% gross margin are

needed to cover our expected fixed and variable operating costs.

18

Credit

Service Charge Revenue and Allowance for Doubtful Accounts

The

following highlights the changes in credit service charge revenue, credit

promotions, related accounts receivable and allowance for doubtful accounts

(dollars in thousands):

|

Year

Ended December 31,

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Credit

Service Charges

|

$ | 1,210 | $ | 1,974 | $ | 2,450 | ||||||

|

Amount

Financed as a % of Sales:

|

||||||||||||

|

Havertys

|

6.2 | % | 8.1 | % | 15.4 | % | ||||||

|

Third

Party

|

37.0 | 36.3 | 31.2 | |||||||||

| 43.2 | % | 44.4 | % | 46.6 | % | |||||||

|

%

Financed by Havertys:

|

||||||||||||

|

No

Interest for 12 Months

|

64.6 | % | 62.2 | % | 18.8 | % | ||||||

|

No

Interest for > 12 Months

|

— | 5.0 | 59.6 | |||||||||

|

No

Interest for < 12 Months

|

4.9 | 10.3 | 8.1 | |||||||||

|

Other

|

30.5 | 22.5 | 13.5 | |||||||||

| 100.0 | % | 100.0 | % | 100.0 | % | |||||||

|

Accounts

receivable

|

$ | 17,143 | $ | 28,083 | $ | 68,901 | ||||||

|

Allowance

for doubtful accounts

|

$ | 1,000 | $ | 1,700 | $ | 2,150 | ||||||

|

Allowance

as a % of accounts receivable

|

5.8 | % | 6.1 | % | 3.1 | % | ||||||

Our

credit service charge revenue has continued to decline as our receivables

portfolio is reduced and customers choose credit promotions with no interest

features.

The

in-house financing program most frequently chosen by our customers carries no

interest for 12 months, or longer periods if offered, and requires equal monthly

payments. These programs generate very minor credit revenue, but

incur lower bad debts relative to our deferred payment in-house credit

programs. In addition, we offer our customers different credit

promotions through a third-party credit provider. Sales financed by

this provider are not Havertys’ receivables, and accordingly, we do not have any

credit risk or service responsibility for these accounts, and there is no credit

or collection recourse to Havertys. The most popular programs offered

through the third-party provider for 2009 were no interest offers requiring 18

to 24 monthly payments and a no payment program for 12 months. The

deferred payment offer has an interest accrual that is waived if the entire

balance is paid in full by the end of the deferral period.

The

allowance as a percent of total accounts receivable decreased in 2009 as we

experienced improvement in the delinquency and problem category

percentages. The dollar amount of the allowance is lower compared to

2008 due to the reduction in total accounts receivable.

19

Interest

Expense, Net

Interest

expense (income), net is primarily comprised of interest expense on the

Company’s debt and the amortization of the discount on the Company’s receivables

which have no interest terms for greater than 12 months. The

following table summarizes the components of interest expense (income), net (in

thousands):

|

Year

Ended December 31,

|

||||||||||||

|

2009

|

2008

|

2007

|

||||||||||

|

Interest

on debt

|

$ | 973 | $ | 1,997 | $ | 3,456 | ||||||

|

Amortization

of discount on accounts receivable

|

(56 | ) | (1,351 | ) | (4,340 | ) | ||||||

|

Other,

including capitalized interest and interest

income

|

(112 | ) | (256 | ) | (423 | ) | ||||||

| $ | 805 | $ | 390 | $ | (1,307 | ) | ||||||

Interest

expense on debt decreased in 2009 and 2008 as average debt decreased and the

effective interest rate was relatively unchanged.

We have

made available to customers in-house interest free credit programs, which mostly

ranged from 12 to 18 months. In connection with these programs, which

are greater than 12 months, we are required to discount the payments to be

received over the expected life (considering prepayments) of the interest free

credit program. On the basis of the credit worthiness of the

customers and our low delinquency rates under these programs, we discounted the

receivables utilizing the prime rate of interest at the date of

sale. The discount is recorded as a contra receivable and charged to

cost of goods sold and is amortized as a credit to interest expense over the

life of the receivable.

The

amount of amortization is decreasing as we ceased these promotions at the

beginning of 2008.

Provision

for Income Taxes

Our

effective tax rate was 22.7%, (85.3)% and 9.6% for 2009, 2008 and

2007, respectively. Refer to Note 7 of the Notes to the Consolidated Financial

Statements for a reconciliation of our income tax expense to the Federal income

tax rate.

Our 2009

rate included the impact of the changes in Federal tax laws enacted in the

fourth quarter of 2009 related to the treatment of net operating loss carrybacks

and the amending of prior years’ tax returns. These changes resulted

in a reduction of current tax expense of approximately $671,000 for additional

refunds and a related increase in deferred tax expense of $495,000 for the

decrease in alternative minimum tax credit carryforwards. The 2009

rate also includes the unfavorable impact of $700,000 for the increase in our

deferred tax valuation allowance.

Our 2008

rate included the unfavorable impact of $8.2 million related to our deferred tax

asset valuation allowance. During the fourth quarter of 2008 we

increased the valuation allowance $14.7 million. We charged $8.2

million to tax expense and the portion of the increase related to our pension

plan of $6.5 million was charged to accumulated other comprehensive

loss. Although this valuation allowance reduces the amount of the net

deferred tax assets on the balance sheet, we will be able to utilize these

assets to reduce tax expense in future profitable periods. The tax

rate was also positively impacted by $276,000 related to changes in the reserve

for uncertain tax positions.