Attached files

| file | filename |

|---|---|

| EX-21.1 - Employers Holdings, Inc. | c60367_ex21-1.htm |

| EX-32.1 - Employers Holdings, Inc. | c60367_ex32-1.htm |

| EX-32.2 - Employers Holdings, Inc. | c60367_ex32-2.htm |

| EX-31.2 - Employers Holdings, Inc. | c60367_ex31-2.htm |

| EX-31.1 - Employers Holdings, Inc. | c60367_ex31-1.htm |

| EX-23.1 - Employers Holdings, Inc. | c60367_ex23-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

|

|

S |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

|

|

|

£ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-33245

EMPLOYERS HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

|

|

|

NEVADA |

04-3850065 |

10375 Professional Circle, Reno, Nevada 89521

(Address of principal executive offices and zip code)

(888) 682-6671

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

Title of each class |

Name of each exchange on which registered |

|

Common Stock, $0.01 par value per share |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes £ No S

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes £ No S

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes S No £

*Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes £ No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer S Accelerated filer £ Non-accelerated filer £ Smaller reporting company £

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2009 was $620,534,946.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes £ No S

|

|

|

Class |

February 19, 2010 |

|

Common Stock, $0.01 par value per share |

42,588,446 shares outstanding |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement relating to the 2010 Annual Meeting of Stockholders are incorporated by reference in Items 10, 11, 12, 13 and 14 of Part III of this report.

TABLE OF CONTENTS

Page No.

3 Business

5 Risk Factors

37 Unresolved Staff Comments

53 Properties

54 Legal Proceedings

54 Submission of Matters to a Vote of Security Holders

54 Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

55 Selected Financial Data

59 Management’s Discussion and Analysis of Financial Condition and Results of Operations

63 Quantitative and Qualitative Disclosures About Market Risk

99 Financial Statements and Supplementary Data

103 Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

146 Controls and Procedures

146 Other Information

146 Directors, Executive Officers and Corporate Governance

147 Executive Compensation

147 Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

147 Certain Relationships and Related Transactions, and Director Independence

147 Principal Accountant Fees and Services

147 Exhibits and Financial Statement Schedules

148 2

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and 21E of the Securities Exchange Act of 1934. You should not place undue reliance on these statements. These forward-looking statements include those related to our expected financial position,

business, financing plans, litigation, future premiums, revenues, earnings, pricing, investments, business relationships, expected losses, loss reserves, acquisitions, competition and rate increases with respect to our business and the insurance industry in general. These forward-looking statements reflect our views with

respect to future events and financial performance. The words “believe,” “expect,” “plan,” “intend,” “project,” “estimate,” “may,” “should,” “will,” “continue,” “potential,” “forecast” and “anticipate” and similar expressions identify forward-looking statements. Although we believe that these expectations reflected

in such forward-looking statements are reasonable, we can give no assurance that the expectations will prove to be correct. Actual results may differ from those expected due to risks and uncertainties, including those discussed in “Risk Factors” in Item 1A of this report and the following:

•

impact of the unprecedented volatility and uncertainty in the financial markets; • adequacy and accuracy of our pricing methodologies; • our dependence on a concentrated geographic market and on the workers’ compensation market; • developments in the frequency or severity of claims and loss activity that our underwriting, reserving or investment practices do not anticipate based on historical experience or industry data; • downgrade of our rating or changes in rating agency policies or practices; • negative developments in the workers’ compensation insurance market; • increased competition on the basis of coverage availability, claims management, safety services, payment terms, premium rates, policy terms, types of insurance offered, overall financial strength, financial ratings and reputation; • changes in the availability, cost or quality of reinsurance and failure of our reinsurers to pay claims timely or at all; • changes in regulations or laws applicable to us, our policyholders or the agencies that sell our insurance; • changes in legal theories of liability under our insurance policies; • effects of acts of war, terrorism or natural or man-made catastrophes; • non-receipt of expected payments; • performance of the financial markets and their effects on investment income and the fair values of investments; • failure of our information technology or communications systems; • adverse state and federal judicial decisions; • litigation and government proceedings; • loss of the services of any of our executive officers or other key personnel; • cyclical nature of the insurance industry; • changes in demand for our products; • our status as an insurance holding company with no direct operations; • the effects of acquisitions that we may undertake; and • changes in general economic conditions, including interest rates, inflation and other factors. 3

The foregoing factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from historical or anticipated results, depending on a number of factors. These risks and uncertainties include, but are not limited to, those listed under the heading “Risk Factors” in

Item 1A of this report. All subsequent written and oral forward-looking statements attributable to us or individuals acting on our behalf are expressly qualified in their entirety by these cautionary statements. We caution you not to place undue reliance on these forward-looking statements, which speak only as of

the date of this report. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. Before making an investment decision, you should carefully consider all of the factors identified in this

report that could cause actual results to differ. NOTE REGARDING RELIANCE ON STATEMENTS IN OUR CONTRACTS The agreements included or incorporated by reference as exhibits to this Annual Report on Form 10-K contain representations and warranties by each of the parties to the applicable agreement. These representations and warranties were made solely for the benefit of the other parties to the applicable

agreement and:

•

were not intended to be treated as categorical statements of fact, but rather as a way of allocating the risk to one of the parties if those statements prove to be inaccurate; • may have been qualified in such agreement by disclosures that were made to the other party in connection with the negotiation of the applicable agreement; • may apply contract standards of “materiality” that are different from “materiality” under the applicable securities laws; and • were made only as of the date of the applicable agreement or such other date or dates as may be specified in the agreement. The Company acknowledges that, notwithstanding the inclusion of the foregoing cautionary statements, it is responsible for considering whether additional specific disclosures of material information regarding material contractual provisions are required to make the statements in this report not misleading. 4

Overview Employers Holdings, Inc. (EHI) is a Nevada holding company and is the successor to EIG Mutual Holding Company (EIG), which was incorporated in Nevada in 2005. EHI’s principal executive offices are located at 10375 Professional Circle, in Reno, Nevada. Our insurance subsidiaries are domiciled in

California, Florida and Nevada. Unless otherwise indicated, all references to “we,” “us,” “our,” the “Company” or similar terms refer to EHI together with its subsidiaries. We are a specialty provider of workers’ compensation insurance focused on select small businesses engaged in low to medium hazard industries. We employ a disciplined, conservative underwriting approach designed to individually select specific types of businesses, predominantly those in the four lowest of the

seven workers’ compensation insurance industry-defined hazard groups, that we believe will have fewer and less costly claims relative to other businesses in the same hazard groups. Workers’ compensation is a statutory system under which an employer generally is required to provide coverage for its employees’

medical, disability, vocational rehabilitation and death benefit costs for work-related injuries or illnesses. We distribute our products almost exclusively through independent agents and brokers and through our strategic partnerships and alliances. We operate as a single reportable segment and conduct operations in

30 states, with approximately 50% of our business in California. In January 2009, we began implementation of a strategic restructuring plan to achieve the corporate and operational objectives of the acquisition and integration of AmCOMP Incorporated (AmCOMP), and in response to then current economic conditions. The restructuring plan included net staff reductions of

approximately 150 employees, or 14% of our total workforce, and consolidation of corporate functions into our Reno, Nevada headquarters. The restructuring, which consisted of office consolidations, rebranding and staff reductions, was largely completed in the first half of 2009. The remainder of our integration

plan, including consolidation of our claims and underwriting systems, was completed in January 2010. In June 2009, Standard & Poor’s added the Company to the S&P SmallCap 600 Index, which we believe is one of the leading small-capitalization market indices in the United States. Our insurance subsidiaries have each been assigned an A.M. Best Company (A.M. Best) rating of “A-” (Excellent), the fourth highest of sixteen possible ratings, with a “stable” financial outlook. This A.M. Best rating is a financial strength rating designed to reflect our ability to meet our obligations to

policyholders. This rating does not reflect our ability to meet non-insurance obligations and is not a recommendation to purchase or discontinue any policy or contract issued by us or to buy, hold or sell our securities. We had net premiums written of $368.3 million and $308.3 million, total revenues of $495.9 million and $396.8 million and net income of $83.0 million and $101.8 million for the years ended December 31, 2009 and 2008, respectively. Our combined ratio on a statutory basis was 99.0% for the year ended

December 31, 2009 (elsewhere in this report, unless otherwise stated, the term “combined ratio” refers to a calculation based on U.S. generally accepted accounting principles (GAAP)). For the purpose of calculating our combined ratio on a statutory basis, the results of operations of AmCOMP are included for the

12 months ended December 31, 2008. Our combined ratio on a statutory basis for the five years ended December 31, 2008 was 84.9%. This ratio was lower than the industry composite combined ratio calculated by A.M. Best for individual companies for which more than 50% of their business is in workers’

compensation. The industry combined ratio on a statutory basis for these companies was 105.9% during the same five-year period. Companies with lower combined ratios than their peers generally experience greater profitability. We had total assets of $3.7 billion at December 31, 2009. 5

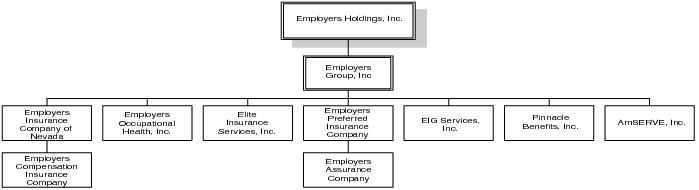

Our corporate structure is as follows: The states of domicile of our four insurance subsidiaries are as follows:

State of Domicile

Employers Insurance Company of Nevada (EICN)

Nevada

Employers Compensation Insurance Company (ECIC)

California

Employers Preferred Insurance Company (EPIC)

Florida

Employers Assurance Company (EAC)

Florida History On January 1, 2000, our Nevada insurance subsidiary, EICN, assumed all the assets, liabilities and operations of the Nevada State Industrial Insurance System (the Fund), including in-force policies and historical liabilities associated with the Fund for losses prior to January 1, 2000, pursuant to legislation

enacted in the 1999 Nevada legislature. In connection with that assumption, our Nevada insurance subsidiary assumed the Fund’s rights and obligations under a retroactive 100% quota share reinsurance agreement (referred to as the LPT Agreement), which the Fund had entered into with third party reinsurers. The

LPT Agreement substantially reduced the exposure to losses for pre-July 1995 Nevada insured risks. The Fund, which was an agency of the State of Nevada, had over 80 years of workers’ compensation experience in Nevada. Subsequently, through July 2002, we operated exclusively in Nevada. We formed a wholly-owned stock corporation incorporated in California, ECIC, and on July 1, 2002 we acquired the renewal rights to a book of workers’ compensation insurance business, and certain other tangible and intangible assets from Fremont Compensation Insurance Group and its affiliates, or

collectively, Fremont. The book of business we acquired from Fremont was primarily comprised of accounts in California and, to a lesser extent, in Colorado, Idaho, Montana and Utah. As a result of this transaction, we were able to establish our important relationships and distribution agreements with ADP, Inc.

(ADP) and Anthem Blue Cross, an operating subsidiary of Wellpoint, Inc. (Wellpoint). In 2003, EICN and ECIC, as well as our wholly-owned subsidiaries Employers Occupational Health, Inc. (EOH), and Elite Insurance Services, Inc. (Elite), began to operate under the Employers Insurance Group trade name. On April 1, 2005, we reorganized into a mutual insurance holding company, EIG

Mutual Holding Company, wholly-owned by the policyholders of EICN. Effective February 5, 2007, we completed an initial public offering (IPO), which occurred in conjunction with our conversion from a mutual insurance holding company owned by our policyholder members to a Nevada stock corporation owned by our public stockholders, and changed our name to “Employers

Holdings, Inc.” and all of the membership interests in EIG were extinguished. In exchange, eligible members of EIG received shares of our common stock or cash. On October 31, 2008, we acquired 100% of the outstanding common stock of AmCOMP (the Acquisition). The Acquisition included two insurance subsidiaries and three other subsidiaries: EIG Services, Inc. (formerly Pinnacle Administrative Company), Pinnacle Benefits, Inc. and AmSERV, Inc. The newly

acquired insurance subsidiaries, EPIC and EAC, are mono-line workers’ compensation 6

insurance companies focused on small businesses engaged in low to medium hazard industries, primarily in Southeastern and Midwestern states. Our Strategies We plan to continue pursuing profitable growth and favorable return on equity through the following strategies: Maintain Focused Operations We focus on providing workers’ compensation insurance to select small businesses engaged in low to medium industry-defined hazard groups. We believe this focus provides us with a unique competitive advantage because we are able to gain in-depth customer and market knowledge and expertise. We execute

our business strategy through regional managers and their local teams who have a deep understanding of the business climate and our targeted policyholders in the states in which we operate. Our focus on small businesses also enables us to provide specialized attention to our customers’ unique needs, which we

believe leads to higher satisfaction and policy retention. Maintain Focus on Underwriting Profitability We intend to maintain focus on disciplined underwriting and continue to pursue profitable growth opportunities across market cycles. We carefully monitor market trends to assess new business opportunities that we expect will meet our pricing and risk standards. We employ a disciplined, conservative and highly automated underwriting approach designed to individually select specific types of businesses that we believe will have fewer and less costly claims relative to other businesses in the same industry-defined hazard group. Within each industry-defined hazard group,

our underwriters use their local market expertise and disciplined underwriting to assess employers and risks on an individual basis and to select those types of employers and risks that allow us to generate attractive returns. We believe that as a result of our disciplined underwriting standards, we are able to price our

policies competitively and profitably. Continue to Grow in Our Existing Markets We plan to continue to seek profitable growth in our existing markets by addressing the workers’ compensation insurance needs of small businesses, which we believe represent a large and profitable market segment. We intend to expand our presence in our existing markets, including significant new markets

serviced by our acquired insurance subsidiaries, EPIC and EAC, by seeking to expand our relationships with agents and by entering into additional strategic partnerships and alliances. We believe that the A.M. Best “A-” (Excellent) financial strength rating issued to EPIC and EAC, which were not previously

rated, will also create additional growth opportunities. In the states in which we operate, the workers’ compensation market for small businesses is not highly concentrated, with a significant portion of premiums being written by numerous insurance companies with small individual market shares. We believe that our focus on workers’ compensation insurance, our

disciplined underwriting and risk selection, and our loss control and claims management expertise for small businesses position us to profitably increase market share in our existing markets. Capitalize on Strategic Partnerships and Alliances to Reach Target Markets We intend to continue to leverage our partnerships and alliances, taking into account the adequacy of premium rates, market dynamics, the labor market, political and economic conditions and the regulatory environment. Our strategic partnerships with ADP and Wellpoint have allowed us to access new

customers and to write attractive business in an efficient manner. We are actively pursuing additional strategic partnership and alliance opportunities. 7

Capitalize on the Flexibility of Our Corporate Structure As a publicly traded company, we have access to capital and equity markets. We believe this gives us financial and strategic flexibility to consider acquisitions, joint ventures and other strategic transactions, as well as new product offerings that make strategic sense for our business while achieving our goal of

profitable growth. Maintain Capital Strength We believe that our financial strength is an important factor for independent agents, brokers and customers selecting our products. We intend to manage our capital prudently relative to our overall risk exposure, establishing adequate loss reserves to protect against future adverse developments while seeking to

grow profits and long-term stockholder value. We will continue to fund the growth of our business and invest in infrastructure and may return capital to stockholders in order to achieve an optimal level of overall leverage to support our underwriting activities and to maintain our financial strength and ratings over

the long-term. As a result of the volatility in the financial markets and the tightening of the credit markets, we have taken steps to improve our liquidity, including increasing levels of cash and cash equivalents. We believe that opportunities to further expand our insurance operations and to invest at attractive returns will be

available to us in the future. We believe that increasing liquidity and preserving available cash now will allow us greater flexibility in reacting to changes in the investment markets in the future. Leverage Infrastructure, Technology and Systems We believe we have an efficient, cost-effective and scalable infrastructure that complements our geographic reach and business model. We have developed a highly automated underwriting system, which allows for the electronic submission and review of insurance applications that employs our underwriting

standards and guidelines. We believe our policy administration system reduces transaction costs and provides for more efficient and timely processing of applications for small policies that meet our standards. We believe this saves our independent agents and brokers considerable time in processing customer

applications and maintains our competitiveness in our target markets. In January 2009, we implemented a new claims system that is designed to improve efficiency and enhance our ability to support claims processing. We will continue to invest in technology and systems across our business to maximize efficiency

and create increased capacity that will allow us to lower our expense ratios while growing premiums. In January 2010, EPIC and EAC were successfully converted to both our policy administration and claims administration systems. Industry The principal concept underlying workers’ compensation is that an employee injured in the course of his or her employment has only the legal remedies available under workers’ compensation laws and does not have any other recourse against his or her employer. Generally, workers are covered for injuries

that occur within the course and scope of their employment. An employer’s obligation to pay workers’ compensation benefits does not depend on any negligence or wrongdoing on the part of the employer and exists even for injuries that result from the negligence or wrongdoings of another person, including the

employee. The level of benefits varies by state, the nature and severity of the injury or disease and the wages of the injured worker. Workers’ compensation insurance policies generally provide that the insurance company will pay all benefits that the insured employer may become obligated to pay under applicable workers’ compensation laws. Each state has a statutory, regulatory and adjudicatory system that sets the amount of wage

replacement to be paid, determines the level of medical care required to be provided, establishes the degree of permanent impairment and specifies the options in selecting healthcare providers. These state laws generally require two types of benefits for injured employees: (a) medical benefits, which include

expenses related to diagnosis and treatment of an injury and/or disease, as well as any required rehabilitation and (b) indemnity payments, which consist of temporary wage replacement, permanent disability payments and death benefits to surviving family members. To fulfill 8

these mandated financial obligations, virtually all businesses are required to purchase workers’ compensation insurance or, if permitted by state law or approved by the U.S. Department of Labor, to self-insure, thereby retaining all risk. The businesses may purchase workers’ compensation coverage from a private

insurance company such as our insurance subsidiaries, a state-sanctioned assigned risk pool, a state agency, or a self-insurance fund (an entity that allows businesses to obtain workers’ compensation coverage on a pooled basis, typically subjecting each employer to joint and several liability for the entire fund). Workers’ compensation was the fourth largest property and casualty insurance line in the U.S. in 2008, on a net written premium basis, according to A.M. Best. A.M. Best reported direct premiums written in 2008 (the most recent data available) for the workers’ compensation industry (excluding governmental

writers) were approximately $39.0 billion, or 7.9% of the estimated $492.9 billion in direct premiums written for the property and casualty insurance industry as a whole. According to A.M. Best, we were the fourteenth largest writer of non-governmental workers’ compensation insurance in the United States in

2008. Excluding governmental writers, premium volume in the workers’ compensation industry was down 10.7% in 2008 compared to 2007, while the entire property and casualty industry experienced an 8.7% increase in direct premiums written for the same time period, according to A.M. Best. The workers’ compensation insurance industry classifies risks into seven industry-defined hazard groups, as defined by the National Council on Compensation Insurance (NCCI), based on severity of claims with businesses in the first or lowest group having the lowest claims costs. Businesses in the four lowest

industry-defined hazard groups include restaurants, stores, educational institutions, physician offices, dentist offices, clothing manufacturers, machine shops, automobile and automobile service or repair centers and drivers. Competition and Market Conditions In 2009, the workers’ compensation sector continued to see average medical and indemnity claims costs rise as claim frequency declined. We believe the current environment is characterized by decreased operating margins caused primarily by a combination of decreasing premiums due to continued downward

rate pressure and declining payrolls and increased price competition. In 2009 and going forward into 2010, we continue to have concerns related to increased volatility and uncertainty in the financial markets and the current economic conditions, including the high rate of unemployment. We believe that overall

market conditions, while challenging, still allow for profitable operations. Our competitors include, but are not limited to, other specialty workers’ compensation carriers, state agencies, multi-line insurance companies, professional employer organizations, third-party administrators, self-insurance funds and state insurance pools. Many of our existing and potential competitors are

significantly larger and possess considerably greater financial and other resources than we do. Consequently, they can offer a broader range of products, provide their services nationwide, and/or capitalize on lower expenses to offer more competitive pricing. Our three primary competitors in California are the

California State Compensation Insurance Fund, Berkshire Hathaway Insurance Group, and Republic Indemnity Company of America. Competition in the workers’ compensation insurance industry is based on many factors, including:

•

pricing (either through premium rates or participating dividends); • level of service; • insurance ratings; • capitalization levels; • quality of care management services; • loss cost management; • effective loss prevention; and • the ability to reduce claims expense. 9

Our A.M. Best rating of “A-” (Excellent), allows us to compete effectively for our target customers, select small businesses engaged in low to medium hazard industries. In addition, we believe our competitive advantages include our strong reputation in the markets in which we operate, excellent claims service,

experienced and professional independent agents and brokers, and our strategic partnerships and alliances. We also strive to maintain the quality of our care management services, and to provide consultation services to clients to educate them on loss prevention and loss reduction strategies. We also compete on

price, based on our actuarial analysis of current and anticipated loss cost trends, as appropriate. California Market California is the largest workers’ compensation insurance market in the United States. In 2008, California accounted for an estimated $7.6 billion in direct premiums written according to the 2009 Best’s State/Line Report for property casualty lines of business, or approximately 16.5% of the U.S. workers’

compensation market. Our direct premiums written in California were $222.4 million in 2008. This made us the ninth largest non-governmental writer of workers’ compensation in the state, as reported by A.M. Best. California is a very competitive market. Although we continue to see an increase in new business submittals, the economic conditions in the state, including the high rate of unemployment, have contributed to a lower average policy size. In 2003 and 2004, California enacted three key pieces of workers’ compensation legislation that reformed medical determinations of injuries or illness, established medical fee schedules, allowed for the use of medical provider panels, modified benefit levels, changed the proof needed to file claims, and reformed

many additional areas of the workers’ compensation benefits and delivery system. Workers’ compensation insurers in California responded to these reforms, which have reduced claim costs, by reducing their rates through 2008. In October 2008, the Workers’ Compensation Insurance Rating Bureau (WCIRB) recommended a 16.0% increase in the claims cost benchmark, representing advisory pure premium rates. The California Commissioner of Insurance (California Commissioner) responded with the approval of a 5.0% average

increase in the claims cost benchmark on new and renewal policies beginning January 1, 2009. Based upon our actuarial analysis of current and anticipated loss cost trends, we filed for an average 10.0% rate increase in California for new and renewal policies incepting on or after February 1, 2009. In April 2009, the WCIRB submitted a revised recommendation to increase the claims cost benchmark 23.7% effective July 1, 2009. This recommendation was based upon two principal components: the WCIRB’s evaluation of December 31, 2008 loss experience produced an indicated increase in the claims cost

benchmark of 16.9%, indicating increased medical costs and an increase of 5.8% directly attributable to additional costs arising from Workers’ Compensation Appeals Board decisions. On July 8, 2009, the California Commissioner rejected the recommendation of the WCIRB and left the claims cost benchmark

unchanged. We increased our rates in California by an average of 10.5% for all new and renewal policies incepting on or after August 15, 2009. In August 2009, the WCIRB recommended a 22.8% increase in the claims cost benchmark effective January 1, 2010. This recommendation was based upon the WCIRB’s evaluation of March 31, 2009 loss experience, which produced an indicated increase in the claims cost benchmark of 16.0%, again reflecting

increased medical costs. The recommendation also indicated an increase of 5.8% directly attributable to additional costs arising from several Workers’ Compensation Appeals Board decisions. On November 9, 2009, the California Commissioner again rejected the WCIRB recommendation and left the claims cost

benchmark unchanged. On March 15, 2010, we will increase our rates in California 3.0% on new and renewal policies. 10

Other Significant Markets Florida Market. Florida is an “administered pricing” state. In administered pricing states, insurance rates are set by the state insurance regulators and are adjusted periodically. Rate competition generally is not permitted and consequently, policy dividend programs, which reflect an insured’s risk profile, are an

important competitive factor. Effective in October 2003, workers’ compensation reform legislation was enacted in Florida in an effort to reverse a trend of increasing costs in the state. These reforms have reduced claim costs and resulted in subsequent rate decreases, including an 18.6% average rate decrease for new and renewal policies

incepting on or after January 1, 2009. The NCCI cited a significant drop in claims frequency and a reduction in the cost of claims as reasons for this most recent rate reduction. On February 10, 2009, the Florida Insurance Commissioner (Florida Commissioner) approved a 6.4% increase in workers’ compensation rates for new and renewal business incepting on or after April 1, 2009. This rate increase was in response to an October 2008 Florida Supreme Court decision that materially

impacted the statutory caps on attorney fees that were part of the 2003 reforms. In June 2009, the Florida Commissioner approved a 6.0% decrease in workers’ compensation rates effective July 1, 2009, for new and renewal policies and the unexpired portions of in-force policies with inception dates from April 1,

2009 through June 30, 2009. This rate decrease was due to the impact of Florida House Bill 903, which restored the statutory caps on attorney fees. In August 2009, NCCI recommended a 6.8% overall average rate decrease in Florida for new and renewal policies incepting on or after January 1, 2010. According to the NCCI, this decrease was the result of significant reductions in claims frequency, although the NCCI noted that the pace of improvement has

moderated. The Florida Commissioner approved this rate decrease, making a 63.2% cumulative rate decrease since the reforms of 2003. Wisconsin Market. Wisconsin is also an “administered pricing” state. In July 2008, the Wisconsin Commissioner of Insurance (Wisconsin Commissioner) approved a 2.9% overall rate increase on new and renewal policies incepting on or after October 1, 2008. On May 14, 2009, the Wisconsin Compensation

Rating Bureau recommended an overall rate increase of 0.4% for new and renewal policies incepting on or after October 1, 2009. On July 29, 2009, the Wisconsin Commissioner approved the recommended increase. Nevada Market. As a result of increased competition, as well as decreasing claim costs, we have reduced our premium rates by 21.4% from 2003 through 2009. Beginning in 2007 and continuing through 2009, we saw competition from the self-insured market and a significant decline in payrolls. We filed for an average 7.8% rate decrease for new and renewal policies incepting on or after March 1, 2009. Additionally, on March 1, 2010, we will decrease rates in Nevada 7.6% on new and renewal policies. Illinois Market. In 2008, the Illinois Commissioner of Insurance (Illinois Commissioner) approved 3.5% and 2.5% average rate increases on new and renewal policies incepting on or after January 1, 2009 and April 1, 2009, respectively. EAC, our primary insurance subsidiary doing business in Illinois, increased

average rates 2.8% and 2.5% on new and renewal policies incepting on or after January 1, 2009 and April 1, 2009, respectively. In September 2009, the NCCI recommended no change to the overall premium level and an overall loss cost level decrease of 0.1% for industrial classes to become effective on January 1, 2010, for new and renewal policies. On November 10, 2009, the Illinois Commissioner approved the recommended rates.

EAC decreased rates 0.1% for new and renewal policies in Illinois incepting on or after January 1, 2010. Customers Our target customers are select small businesses engaged in low to medium hazard industries. Our historical loss experience has been more favorable for lower industry-defined hazard groups than for higher hazard groups. Further, we believe it is generally more costly to service and manage the risks associated

with higher hazard groups. By targeting businesses in low to medium hazard groups, we 11

believe that we improve our ability to generate profitable underwriting results. As of December 31, 2009, 83.2% of our in-force premiums were generated by insureds in the four lowest industry-defined hazard groups (A-D). Within each hazard group, our underwriters use their local market expertise and disciplined

underwriting to select specific types of businesses and risks that allow us to generate attractive returns. We underwrite these businesses based on individual risk characteristics, as opposed to following an occupational class-based underwriting approach. For example, while we insure many physician offices, our

underwriting guidelines generally exclude offices that we believe have a higher risk profile, such as psychiatrist offices and drug treatment centers. The following table sets forth our in-force premiums by type of insured for our top ten types of insureds and as a percentage of our total in-force premiums as of December 31, 2009: Employer Classifications

Hazard

In-force

Percentage of

(in thousands, except percentages) Restaurants

A

$

38,171

9.9

% Physician and physician office clerical

C

29,994

7.8 Automobile service or repair center and drivers

D

25,260

6.6 Store: Wholesale not otherwise classified

B

16,599

4.3 College: Professional employees and clerical

B

9,957

2.6 Store: Retail not otherwise classified

B

8,758

2.3 Machine shops not otherwise classified

D

6,768

1.8 Clerical office employees not otherwise classified

C

6,552

1.7 Hotel: All other employees and salespersons, drivers

B

6,535

1.6 Stores: Groceries and provisions—retail

C

6,254

1.6 Total

$

154,848

40.2

% The following table sets forth our in-force premiums by hazard group and as a percentage of our total in-force premiums as of December 31: Hazard

2009

Percentage

2008

Percentage

2007

Percentage

(in thousands, except percentages) A

$

45,683

11.9

%

$

46,838

10.1

%

$

33,905

10.4

% B

82,086

21.3

94,080

20.2

77,871

23.8 C

137,973

35.8

157,481

33.8

118,215

36.1 D

54,582

14.2

63,206

13.6

42,345

12.9 E

43,036

11.2

61,936

13.3

31,890

9.8 F

20,131

5.2

39,410

8.5

21,440

6.6 G

1,534

0.4

2,657

0.5

1,346

0.4 Total

$

385,025

100.0

%

$

465,608

100.0

%

$

327,012

100.0

% In 2009, our insureds had average annual premiums of approximately $8,700. We are not dependent on any single employer and the loss of any single employer would not have a material adverse effect on our business. We currently write business in 30 states and are licensed to write business in six additional states and the District of Colombia. 12

Group

Level

Premiums

Total

Group

of 2009

Total

of 2008

Total

of 2007

Total

The following table sets forth our in-force premiums by state and as a percentage of total in-force premiums as of December 31: State

2009

Percentage

2008

Percentage

2007

Percentage

(in thousands, except percentages) California

$

180,474

46.9

%

$

203,694

43.8

%

$

230,424

70.5

% Florida

27,964

7.3

46,248

9.9

510

0.2 Wisconsin

24,125

6.3

29,040

6.2

—

— Nevada

24,050

6.2

38,971

8.4

59,598

18.2 Illinois

19,389

5.0

17,885

3.8

2,045

0.6 Texas

15,761

4.1

21,418

4.6

1,458

0.5 Georgia

12,744

3.3

12,826

2.8

—

— Indiana

10,873

2.8

13,950

3.0

—

— Tennessee

10,765

2.8

14,502

3.1

—

— Kentucky

9,685

2.5

10,431

2.2

—

— Virginia

7,805

2.0

7,760

1.7

—

— South Carolina

5,530

1.4

7,698

1.7

—

— Idaho

5,428

1.4

6,053

1.3

6,347

1.9 Colorado

5,073

1.3

8,073

1.7

11,839

3.6 Montana

4,947

1.3

3,882

0.8

4,600

1.4 North Carolina

4,418

1.1

5,346

1.1

—

— Other

15,994

4.3

17,831

3.9

10,191

3.1 Total

$

385,025

100.0

%

$

465,608

100.0

%

$

327,012

100.0

% The following table sets forth the number of in-force policies by state and as a percentage of total in-force policies as of December 31: State

2009

Percentage

2008

Percentage

2007

Percentage California

27,812

63.0

%

27,942

61.3

%

24,997

74.2

% Nevada

4,119

9.3

5,221

11.4

6,145

18.2 Florida

2,630

6.0

3,115

6.8

79

0.2 Texas

1,592

3.6

1,747

3.8

151

0.5 Wisconsin

922

2.1

892

2.0

—

— Illinois

801

1.8

689

1.5

96

0.3 Colorado

713

1.6

823

1.8

980

2.9 Indiana

687

1.6

804

1.8

—

— Tennessee

593

1.3

639

1.4

—

— Georgia

539

1.2

435

1.0

—

— Virginia

454

1.0

363

0.8

—

— Idaho

449

1.0

422

0.9

362

1.1 South Carolina

433

1.0

407

0.9

—

— Other

2,410

5.5

2,100

4.6

889

2.6 Total

44,154

100.0

%

45,599

100.0

%

33,699

100.0

% At December 31, 2009, we experienced a year-over-year decrease of 3.2% in the total number of in-force policies, with the decrease occurring primarily in Nevada and Florida. Nevada policy count decreased 1,102, or 21.1%, while Florida policy count decreased 485, or 15.6% as a result of the continuing effects

of adverse economic conditions. However, we experienced policy count growth in other states in which we operate, particularly in the Midwest and Southeast, which partially offset the declines in Nevada and Florida. Premium revenues in 2009 reflect additional premiums from the Acquisition, cumulative rate increases of 21.6% in California, the net 2009 rate decrease in Florida of 18.6%, rate reductions in several other states, as well as the impacts of competitive pressures and lower payrolls due to the 13

of 2009

Total

of 2008

Total

of 2007

Total

of 2009

Total

of 2008

Total

of 2007

Total

economic contraction. We believe our policy count in the majority of our states will continue to grow, particularly in the Midwest and Southeast where we believe our A- (Excellent) A.M. Best rating is resulting in an increase in new business submissions. We emphasize disciplined pricing objectives and

underwriting guidelines and we believe we are well positioned to continue to grow profitably. However, we cannot be certain how these trends will ultimately impact our consolidated financial position and results of operations. Marketing and Distribution We market and sell our workers’ compensation insurance products through independent local, regional and national agents and brokers, and through our strategic partnerships and alliances, including our principal partners ADP and Wellpoint. Policies underwritten directly or through our independent agents

and brokers generated $312.7 million and $386.7 million, or 81.2% and 83.1%, of our in-force premiums as of December 31, 2009 and 2008, respectively. Independent Insurance Agents and Brokers We establish and maintain strong, long-term relationships with independent agents and brokers who actively market our products and services. We emphasize personal interaction, offering responsive service and competitive commissions and maintaining a focus on workers’ compensation insurance. Our sales

representatives and field underwriters work closely with independent agents and brokers to market and underwrite our business, regularly visiting their offices and participating in presentations to customers. This results in enhanced understanding of the businesses and risks we underwrite and the needs of

prospective customers. We believe that the decision by independent agents and brokers to place business with an insurer depends in part upon superior services offered by the insurer to the agents and brokers and policyholders, as well as the insurer’s expertise and dedication to a particular line of business. Accordingly, we

continually seek to enhance the ease of doing business with us and to provide superior service. For example, our automated underwriting system enables agents and brokers to directly input data into the system and in some instances the system prices the risk and binds the coverage without human intervention. We

do not delegate underwriting authority to agents or brokers that sell our insurance. We pay commissions on premiums written that we believe are competitive with other workers’ compensation insurers. Additionally, we believe that we deliver prompt, efficient and professional support services. As of December 31, 2009, we marketed and sold our insurance products through approximately 3,800 independent insurance agents and brokers in approximately 1,600 appointed agencies. Those agents and brokers produced $309.5 million, $381.9 million and $235.6 million, or 80.4%, 82.0%, and 72.1% of our

in-force premiums as of December 31, 2009, 2008 and 2007, respectively. No single agency or brokerage accounted for more than 0.7%, 1.2% and 2.0% of our in-force premiums as of December 31, 2009, 2008 and 2007, respectively. Strategic Partnerships and Alliances To expand our distribution, we have developed important strategic relationships with companies that have established sales forces and common markets. Since 2002, we have jointly marketed our workers’ compensation insurance products with ADP’s payroll services primarily to small businesses in ten states

and with Wellpoint’s group health insurance plans in California. Additionally, we have entered into additional strategic partnerships with E-chx, Inc. (E-chx) and Granite Professional Insurance Brokerage, Inc. (Granite), Intego Insurance Services, LLC (Intego) and Small Business Payroll Services Group of Wells

Fargo Bank, National Association (Wells Fargo). We are actively pursuing opportunities for other strategic partnerships and alliances. Policies underwritten through our strategic partnerships and alliances generated $72.3 million, $78.9 million and $84.4 million, or 18.8%, 16.9% and 25.8% of our in-force premiums as of December 31, 2009, 2008 and 2007, respectively. The decrease in 2008, as compared to 2007, as a percentage of total in-force

premiums was primarily attributable to increased total premium related to the Acquisition, 14

partially offset by overall premium declines attributable to our strategic partnerships and alliances, which continued in 2009. We do not delegate underwriting authority to our strategic distribution partners. Wellpoint. The Wellpoint Integrated MedicompSM joint marketing program includes two agreements, a small group health insurance plan (for businesses with 1 to 50 employees) and a large group health insurance plan (for businesses with 51 to 250 employees). These two group health insurance plans are

offered with our standard workers’ compensation insurance policy. This exclusive relationship allows us to distribute an integrated group health/workers’ compensation product in California through Wellpoint’s life and health agents. The primary benefit to the employer is a single bill for their group health and

workers’ compensation insurance coverage and a discount on workers’ compensation premiums. We believe that, in general, when businesses purchase this combination of coverage, their employees make fewer workers’ compensation claims because those employees are insured for non-work related illnesses or

injuries and thus are less likely to seek treatment for a non-work related illness or injury through their employers’ workers’ compensation insurance policy. We believe another key benefit to this program is the increased satisfaction from employees who are able to use the same medical network for occupational and

non-occupational illness and injury. As the largest group health carrier in California, Wellpoint has negotiated favorable rates with its medical providers and associated facilities, which we benefit from through reduced claims costs. We pay Wellpoint fees that are a percentage of premiums paid for services provided

under the Integrated MediComp program. The small group and large group agreements automatically renew for one-year periods unless terminated by either party with at least 60 days notice prior to the expiration of the current term. These agreements have automatically renewed through January 1, 2011 and July 1, 2010, respectively. ADP. ADP is a payroll services company which provides services to small and medium-sized businesses, and is the largest payroll service provider in the United States. As part of its services, ADP sells our workers’ compensation insurance product along with its payroll and accounting services through ADP’s

insurance agency and field sales staff primarily to small businesses in ten states (Arizona, California, Colorado, Florida, Idaho, Illinois, Nevada, Oregon, Texas, and Utah). The majority of business written is through ADP’s small business unit, which has accounts of 1 to 50 employees. We pay ADP fees that are a

percentage of premiums paid for services provided through the ADP program. ADP utilizes innovative methods to market workers’ compensation insurance including the Pay-by-Pay® (PBP) program. An advantage of ADP’s PBP program is that the policyholder is not required to pay a deposit at the inception of the policy. Rather, the workers’ compensation premium is deducted each

time ADP processes the policyholders’ payrolls along with their appropriate federal, state, and local taxes. These characteristics of the PBP program enable us to competitively price the workers’ compensation insurance written as a part of that program. Although we do not have an exclusive relationship with ADP, we believe we are a key strategic partner of ADP for our selected markets and classes of business. Our agreement with ADP may be terminated without cause upon 120 days notice. E-chx and Granite. We entered into a joint sales, services and program administration agreement with E-chx and Granite in November 2006, pursuant to which E-chx, a payroll solutions company providing payroll outsourcing solutions for small businesses, markets our workers’ compensation insurance product

with its payroll services. The program is only available in California. Although we do not have an exclusive relationship with E-chx, we are its only strategic partner in California. E-chx may terminate the agreement without cause upon 90 days written notice. E-chx offers products and services in all 50 states. We

pay E-chx fees that are a percentage of premiums paid for services provided through the program. E-chx offers an E-PAYSM program. An advantage of this program is that the policyholder is not required to pay a deposit at the inception of the policy. Rather, the workers’ compensation premium is deducted each time E-chx processes the policyholders’ payrolls along with their appropriate federal, state, and

local taxes. These characteristics of the E-Pay program enable us to competitively price the workers’ compensation insurance written as a part of that program. 15

Additionally, as part of our distribution relationship, Granite markets our products through other payroll providers. Intego. In 2007, we entered into a Partner Program and Agency Agreement with Intego, a full service insurance brokerage that works with approved, independent payroll service companies to identify potential business leads. Pursuant to this non-exclusive agreement, Intego markets our workers’ compensation

insurance product in Texas, Florida and Illinois to business customers of the independent payroll service companies with a billing that is integrated with their payroll products. Intego may terminate this agreement without cause upon 90 days written notice. Wells Fargo. In 2008, we entered into a strategic relationship with the Small Business Payroll Services Group of Wells Fargo. This non-exclusive relationship allows the Small Business Payroll Services Group to offer our workers’ compensation products as part of ExpressPay® and other payroll services in most of

the western states in which we do business. ExpressPay is sold through Wells Fargo banking operations by bankers who are trained to identify and cross-sell the ExpressPay product. Direct Business We write a small amount of business that comes to us directly without using an agent or broker or one of our strategic distribution relationships. This direct business is a legacy of our assumption of the assets and liabilities of the Fund. Although we do not market any direct business, we intend to maintain this

book of business because it is very well known by our underwriters and is profitable. At December 31, 2009, 2008 and 2007, approximately $3.2 million, $4.8 million and $7.0 million, respectively, of our in-force premiums were from direct business. Underwriting and Products Disciplined Underwriting We target select small businesses engaged in low to medium hazard industries. We employ a disciplined underwriting approach designed to individually select specific types of businesses, predominantly those in the four lowest of the seven workers’ compensation insurance industry-defined hazard groups, that

we believe will have fewer and less costly claims relative to other businesses in the same hazard groups. Our underwriting guidelines are designed to minimize underwriting of classes and subclasses of business which have historically demonstrated claims severity that do not meet our target risk profiles. We price our policies based on the specific risks associated with each potential insured rather than solely on the

industry class in which a potential insured is classified. As of December 31, 2009, policyholders in the four lowest industry-defined hazard groups generated approximately 83.2% of our in-force premiums. This is consistent with our strategy of targeting insureds in low to medium hazard businesses. Our statutory

losses and loss adjustment expenses (LAE) ratio, a measure which relates inversely to our underwriting profitability, was 57.5% and 51.4% in 2009 and 2008, respectively, 15.6 and 21.7 percentage points below the 2008 statutory industry composite losses and LAE ratio calculated by A.M. Best for U.S. insurance

companies having more than 50% of their premiums generated by workers’ compensation insurance products. Our statutory losses and LAE ratio was at least ten percentage points below the A.M. Best composite losses and LAE ratio for the industry for each of the five years ended December 31, 2008. Our

disciplined underwriting approach is a critical element of our culture and has allowed us to offer competitive prices, diversify our risks and achieve profitable growth. We provide workers’ compensation insurance coverage to several homogeneous groups of business such as physicians, dentists, restaurants, artisan contractors and retail stores. We review the premium, payroll, and loss history trends of each group annually and develop a schedule rating modification that is

applied to all policyholders that meet the qualification standards for a given group. Qualification standards vary between groups and may include factors such as management experience, loss experience, and nature of operations conducted by the insured and/or other exposures specific to the class of business.

Additionally, an insured’s experience modification is applied in the determination of its premium. 16

Our underwriting strategy involves continuing our disciplined underwriting approach in pursuing profitable growth opportunities. We carefully monitor market trends to assess new business opportunities, only pursuing opportunities that we expect to meet our pricing and risk standards. We seek to underwrite

our portfolio of low to medium hazard risks with a view toward maintaining long-term underwriting profitability across market cycles. We execute our underwriting processes through automated systems and seasoned underwriters with specific knowledge of local markets. Within these systems, we have developed underwriting templates for specific, targeted classes of business that produce faster quotations when all underwriting criteria are met

by a specific risk. These underwriting guidelines consider many factors such as type of business, nature of operations, risk exposures and other employer-specific conditions, and are designed to minimize underwriting of certain classes and subclasses of business such as chemical manufacturing, high-rise construction

and long-haul trucking, which have historically demonstrated claims severity that do not meet our target risk profiles. While our underwriting systems are automated, we do not delegate underwriting authority to agents or brokers that sell our insurance or to any other third party. To create efficiency and standardization, we implemented an underwriting and policy administration system. As a result, two of our legacy

underwriting systems have been discontinued and one remaining legacy system will be phased out beginning in early 2010. Our field underwriters continue to work closely with independent agents, brokers and our strategic distribution partners to market and underwrite our business, regularly visiting their offices

and participating in presentations to customers. The average length of experience of our current underwriters exceeds ten years. Our underwriting guidelines are defined centrally by our Corporate Underwriting Department and our Chief Underwriting Officer, who is responsible for supervision of the underwriting conducted at all of the business units, has

the authority to permit a business unit to underwrite particular risks that fall outside the classes of business specified in our underwriting guidelines on a case-by-case basis. Loss Control Our loss control professionals provide consultation to policyholders to assist them in preventing losses and containing costs once claims occur. They also assist our underwriting personnel in evaluating potential and current policyholders and are an important part of our loss control strategy. Premium Audit We conduct premium audits on our policyholders annually upon the expiration of each policy. The purpose of these audits is to comply with applicable state and reporting bureau requirements and to verify that policyholders have accurately reported their payroll and employee job classifications. In addition to

annual audits, we selectively perform interim audits on certain classes of business if unusual claims are filed or concerns are raised regarding projected annual payrolls, which could result in substantial variances at final audit. Principal Products and Pricing Our workers’ compensation insurance product is written primarily on a guaranteed cost basis, meaning the premium for a policyholder is set in advance and varies based only upon changes in the policyholder’s class and payroll. Class and specific risk credits are formulated to fit the needs of targeted classes and

employer groups. Premiums are based on the particular class of business and our estimates of expected losses, LAE and other expenses related to the policies we underwrite. Generally, premiums for workers’ compensation insurance policies are a function of:

•

the amount of the insured employer’s payroll; • the applicable premium rate, which varies with the nature of the employees’ duties and the business of the insured; • the insured’s industry classification; and • factors reflecting the insured employer’s historical loss experience. 17

In addition, our pricing decisions take into account the workers’ compensation insurance regulatory requirements of each state in which we conduct operations, because such requirements address the rates that industry participants in that state may or should charge for policies. We write business in “administered pricing” and “loss cost” states. In administered pricing states, insurance rates are set by the state insurance regulators and are adjusted periodically. Rate competition generally is not permitted in these states and, consequently, policy dividend programs, which reflect an

insured’s risk profile, are an important competitive factor. Florida, Wisconsin and Idaho are administered pricing states, while the other states in which we operate are loss cost states. In loss cost states, we have more flexibility to offer premium rates that reflect the risk we are taking based on each employer’s

profile. We offer dividend plans to eligible policyholders, primarily in Florida and Wisconsin, under which a portion of the premium paid by a policyholder may be returned in the form of a dividend. Eligibility for these programs varies based upon the nature of the policyholder’s operations, value of premium

generated, loss experience and existing controls intended to minimize workers’ compensation claims and costs. Payment of policy dividends specified in the dividend plans cannot be guaranteed. In loss cost states, the state first approves a set of loss costs that provide for expected loss and, in most cases, LAE payments, which are prepared by an insurance rating bureau (for example, the WCIRB in California and the NCCI in Nevada). An insurer then selects a factor, known as a loss cost multiplier, to

apply to loss costs to determine its rates. In these states, regulators permit pricing flexibility primarily through: (a) the selection of the loss cost multiplier; and (b) schedule rating modifications that allow an insurer to adjust premiums upwards or downwards for specific risk characteristics of the policyholder such as:

•

type of work conducted at the premises or work environment; • on-site medical facilities; • level of employee safety; • use of safety equipment; and • policyholder management practices. In all of the loss cost states in which we currently operate, we use both variables (a) and (b) above to calculate a policy premium that we believe will cover the claim payments, losses and LAE, and company overhead and result in a reasonable profit for us. Claims and Medical Case Management The role of our claims department is to actively investigate, evaluate and pay claims efficiently, and to aid injured workers in returning to work in accordance with applicable laws and regulations. We have implemented rigorous claims guidelines, reporting and control procedures in our claims units and have

claims operations throughout the markets we serve. We also provide medical case management services for all claims that we determine will benefit from such involvement. Our claims department also provides claims management services for those claims incurred by the Fund and assumed by our Nevada insurance subsidiary in connection with the LPT Agreement with a date of injury prior to July 1, 1995. We receive a management fee from the third party reinsurers equal to 7%

of the loss payments on these claims. In Nevada, we have created our own medical provider network, and we make every appropriate effort to direct injured workers into this network. In the other states in which we do business, we utilize networks affiliated with Wellpoint and Coventry Health Care, Inc. In addition to our medical networks, we

work closely with local vendors, including attorneys, medical professionals and investigators, to bring local expertise to our reported claims. We pay special attention to reducing costs in each region and have established discounting arrangements with the aforementioned service providers. We use preferred provider

organizations, bill review services and utilization management to closely monitor medical costs and to verify that providers charge no more than the applicable fee schedule, or in some cases what is usual and customary. 18

We actively pursue subrogation and recovery in an effort to mitigate claims costs. Subrogation rights are based upon state and federal laws, as well as the insurance policy issued to the insured. Our subrogation efforts are handled through a dedicated subrogation unit. Losses and Loss Adjustment Expenses Reserves We are directly liable for losses and LAE under the terms of insurance policies our insurance subsidiaries underwrite. Significant periods of time can elapse between the occurrence of an insured loss, the reporting of the loss to us and our payment of that loss. Loss reserves are reflected on our balance sheets

under the line item caption “unpaid losses and loss adjustment expenses.” As of December 31, 2009, our reserves for unpaid losses and LAE, net of reinsurance, were $1.4 billion. The process of estimating reserves involves a considerable degree of judgment by management and, as of any given date, is inherently

uncertain. For a detailed description of our reserves, the judgments, key assumptions and actuarial methodologies that we use to estimate our reserves and the role of our consulting actuary, see “Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting

Policies—Reserves for Losses and Loss Adjustment Expenses.” The following table provides a reconciliation of the beginning and ending loss reserves on a GAAP basis:

December 31,

2009

2008

2007

(in thousands) Unpaid losses and LAE, gross of reinsurance, at beginning of period

$

2,506,478

$

2,269,710

$

2,307,755 Less reinsurance recoverable, excluding bad debt allowance, on unpaid losses and LAE

1,076,350

1,052,641

1,098,103 Net unpaid losses and LAE at beginning of period

1,430,128

1,217,069

1,209,652 Losses and LAE, net of reinsurance, acquired in business combination

—

247,006

— Losses and LAE, net of reinsurance, incurred in: Current year

283,827

226,643

221,347 Prior years

(51,359

)

(71,707

)

(60,011

) Total net losses and LAE incurred during the period

232,468

154,936

161,336 Deduct payments for losses and LAE, net of reinsurance, related to: Current year

74,944

53,397

44,790 Prior years

214,499

135,486

109,129 Total net payments for losses and LAE during the period

289,443

188,883

153,919 Ending unpaid losses and LAE, net of reinsurance

1,373,153

1,430,128

1,217,069 Reinsurance recoverable, excluding bad debt allowance, on unpaid losses and LAE

1,052,505

1,076,350

1,052,641 Unpaid losses and LAE, gross of reinsurance, at the end of period

$

2,425,658

$

2,506,478

$

2,269,710 Our estimates of incurred losses and LAE attributable to insured events of prior years have decreased for past accident years because actual losses and LAE paid and current projections of unpaid losses and LAE were less than we originally anticipated. We refer to such decreases as favorable developments.

The reductions in reserves were $51.4 million, $71.7 million and $60.0 million for the years ended December 31, 2009, 2008 and 2007, respectively. Estimates of net incurred losses and LAE are established by management utilizing actuarial indications based upon our historical and industry experience regarding

claim emergence and claim payment patterns, and regarding claim cost trends, adjusted for future anticipated changes in claims-related and economic trends, as well as regulatory and legislative changes, to establish our best estimate of the losses and LAE reserves. The decrease in the prior year reserves was

primarily the result of actual paid losses being less than expected, and revised assumptions used in the projection of future losses and LAE payments based on more current 19

information about the impact of certain changes, such as legislative changes, which was not available at the time the reserves were originally established. While we have had favorable developments over the past three years, the magnitude of these developments illustrates the inherent uncertainty in our liability for

losses and LAE, and we believe that favorable or unfavorable developments of similar magnitude, or greater, could occur in the future. For a detailed description of the major sources of recent favorable developments, see “Item 7—Management’s Discussion and Analysis of Financial Condition and Results of

Operations—Critical Accounting Policies—Reserves for Losses and Loss Adjustment Expenses” and Note 11 in the Notes to our Consolidated Financial Statements. Our reserves for unpaid losses and loss adjustment expenses (gross and net), as well as our case and “incurred but not reported” or IBNR reserves were as follows:

December 31,

2009

2008

2007

(in thousands) Case reserves

$

915,378

$

886,789

$

740,133 IBNR

1,198,019

1,293,313

1,235,124 LAE

312,261

326,376

294,453 Gross unpaid losses and LAE

2,425,658

2,506,478

2,269,710 Reinsurance recoverables on unpaid losses and LAE, gross

1,052,505

1,076,350

1,052,641 Net unpaid losses and LAE

$

1,373,153

$

1,430,128

$

1,217,069 Loss Development The following tables show changes in the historical loss reserves, on a gross basis and net of reinsurance, as of each of the ten years ended December 31, 2009, for EICN and ECIC and as of each of the years ended December 31, 2009 and 2008, for EPIC and EAC. These tables are presented on a GAAP basis.

The paid and reserve data in the following tables is presented on a calendar year basis. The top line of each table shows the net reserves and the gross reserves for unpaid losses and LAE recorded at each year-end. Such amount represents an estimate of unpaid losses and LAE occurring in that year as well as future payments on claims occurring in prior years. The upper portion of these tables

(net and gross cumulative amounts paid, respectively) present the cumulative amounts paid during subsequent years on those losses for which reserves were carried as of each specific year. The lower portions (net reserves re-estimated) show the re-estimated amounts of the previously recorded reserves based on

experience as of the end of each succeeding year. The re-estimated amounts change as more information becomes known about the actual losses for which the initial reserve was carried. An adjustment to the carrying value of unpaid losses for a prior year will also be reflected in the adjustments for each subsequent

year. For example, an adjustment made in the 2000 year will be reflected in the re-estimated ultimate net loss for each of the years thereafter. The gross cumulative redundancy, or deficiency, line represents the cumulative change in estimates since the initial reserve was established. It is equal to the difference

between the initial reserve and the latest re-estimated reserve amount. A redundancy means that the original estimate was higher than the current estimate. A deficiency means that the current estimate is higher than the original estimate. 20

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

(in thousands) Net reserves for losses and LAE Originally estimated

$

936,000

$

887,000

$

908,326

$

962,457

$

1,089,814

$

1,208,481

$

1,209,652

$

1,217,069

$

1,430,128

$

1,373,153 Net cumulative amounts paid One year later

108,748

81,022

80,946

91,130

96,661

106,859

109,129

127,912

214,499 Two years later

161,721

120,616

130,386

150,391

161,252

175,531

186,014

219,496 Three years later

191,453

149,701

165,678

193,766

207,868

229,911

249,059 Four years later

215,015

173,204

194,400

226,127

247,217

279,405 Five years later

235,613

194,980

218,453

255,851

285,388 Six years later

255,772

215,507

242,143

288,039 Seven years later

275,750

235,653

269,341 Eight years later

294,760

260,036 Nine years later

318,262 Net reserves re-estimated One year later

896,748

875,522

847,917

924,878

1,011,759

1,101,352

1,149,641

1,151,246

1,378,767 Two years later

885,221

781,142

805,058

886,711

975,765

1,049,628

1,085,358

1,100,706 Three years later

800,959

742,272

779,373

884,426

954,660

1,004,589

1,035,028 Four years later

766,204

719,912

788,262

877,151

927,382

970,671 Five years later

743,997

730,112

788,481

858,617

900,588 Six years later

754,447

730,456

776,329

839,430 Seven years later

754,462

720,155

763,988 Eight years later

745,665

712,717 Nine years later

744,085 Net cumulative redundancy:

191,915

174,283

144,338

123,027

189,226

237,810

174,624

116,363

51,359

0 Gross reserves—December 31

2,326,000

2,226,000

2,212,368

2,193,439

2,284,542

2,349,981

2,307,755

2,269,710

2,506,478

2,425,658 Reinsurance recoverable, gross

1,390,000

1,339,000

1,304,042

1,230,982

1,194,728

1,141,500

1,098,103

1,052,641

1,076,350

1,052,505 Net reserves—December 31

936,000

887,000

908,326

962,457

1,089,814

1,208,481

1,209,652

1,217,069

1,430,128

1,373,153 Gross re-estimated reserves

2,071,274

1,990,116

2,000,610

2,030,945

2,050,937

2,084,854

2,110,615

2,148,399

2,470,746

2,425,658 Re-estimated reinsurance recoverables

1,327,189

1,277,399

1,236,622

1,191,515

1,150,349

1,114,183

1,075,587

1,047,693

1,091,979

1,052,505 Net re-estimated reserves

744,085

712,717

763,988

839,430

900,588

970,671

1,035,028

1,100,706

1,378,767

1,373,153 Gross reserves for losses and LAE Originally estimated

2,326,000

2,226,000

2,212,368

2,193,439

2,284,542

2,349,981

2,307,755

2,269,710

2,506,478

2,425,658 Gross cumulative amounts paid as of: One year later

160,978

128,066

128,462

137,968

142,632

152,006

152,879

170,626

258,412 Two years later

260,995

215,176

224,740

243,203

252,379

264,430

272,478

304,146 Three years later

338,243

291,099

306,006

331,731

342,748

361,524

377,459 Four years later

408,643

360,535

379,881

407,845

424,811

452,955 Five years later

475,174

427,307

447,687

480,283

504,918 Six years later

540,329

490,296

514,091

554,408 Seven years later

602,371

553,103