Attached files

| file | filename |

|---|---|

| 8-K - Vystar Corp | v165544_8k.htm |

Vystar

Investor Presentation NOVEMBER 2009

Why Vytex NRL? Latex Allergy

Concerns 3%* general

population 17% healthcare

workers 10% condom users Global

Environmental Awareness Vytex: all natural,

renewable

resource Increased use

petroleum-based

synthetics Human

carcinogenicity/ toxicity Proven Raw

Material 40,000+ products

made with

natural rubber

latex $2.6B global market Superior

performance

over synthetics *Source: American Latex Allergy Association

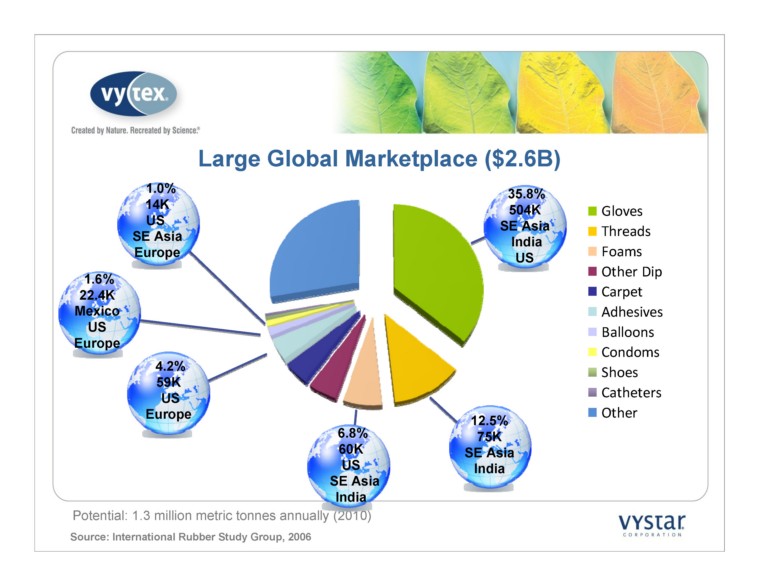

1.6% 22.4K Mexico US Europe 4.2% 59K US Europe 6.8% 60K US SE Asia India 12.5% 75K SE Asia India 35.8% 504K SE Asia India US Potential: 1.3 million metric tonnes annually (2010) Source: International Rubber Study Group, 2006 Large Global Marketplace ($2.6B) Gloves Threads Foams Other Dip Carpet Adhesives Balloons Condoms Shoes Catheters Other

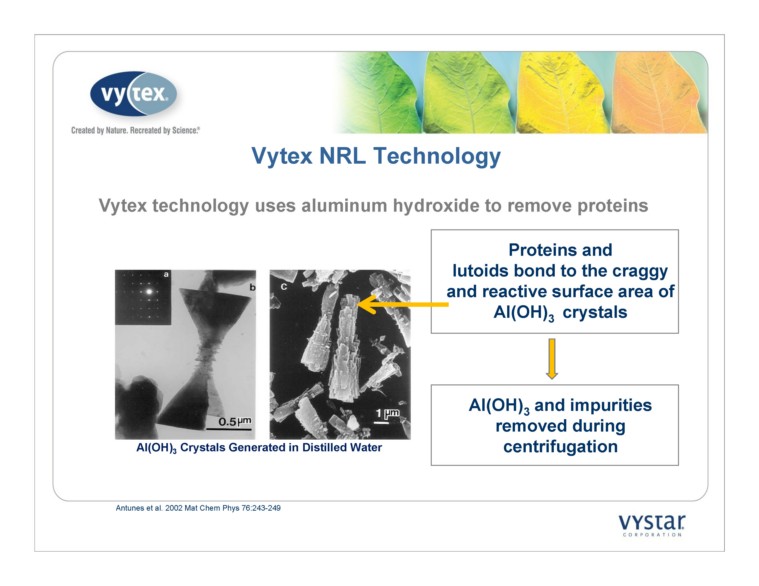

Antunes et al. 2002 Mat Chem Phys 76:243-249 3 Crystals Generated in Distilled Water NRL Technology Vytex technology uses aluminum hydroxide to remove proteins Proteins and 3 crystals and impurities

removed during

centrifugation

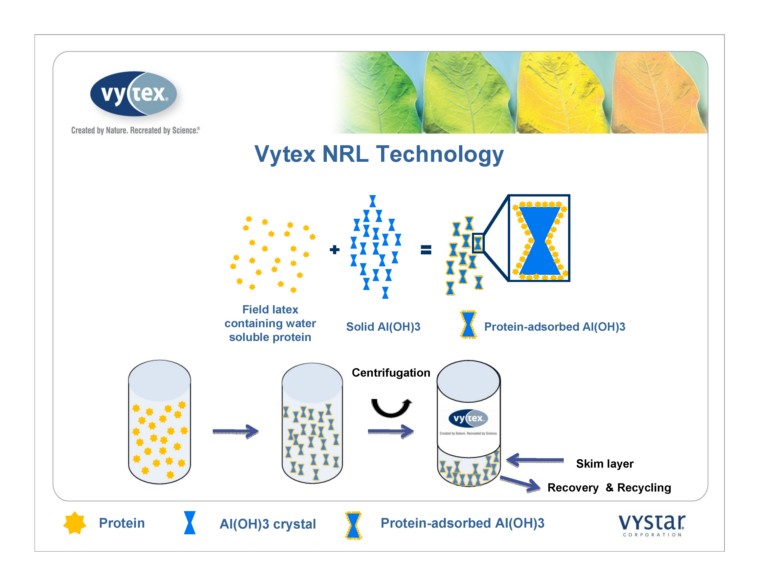

Protein Al(OH)3 crystal Field latex

containing water

soluble protein Solid Al(OH)3 Protein-adsorbed Al(OH)3 Protein-adsorbed Al(OH)3 Recovery & Recycling Skim layer Centrifugation

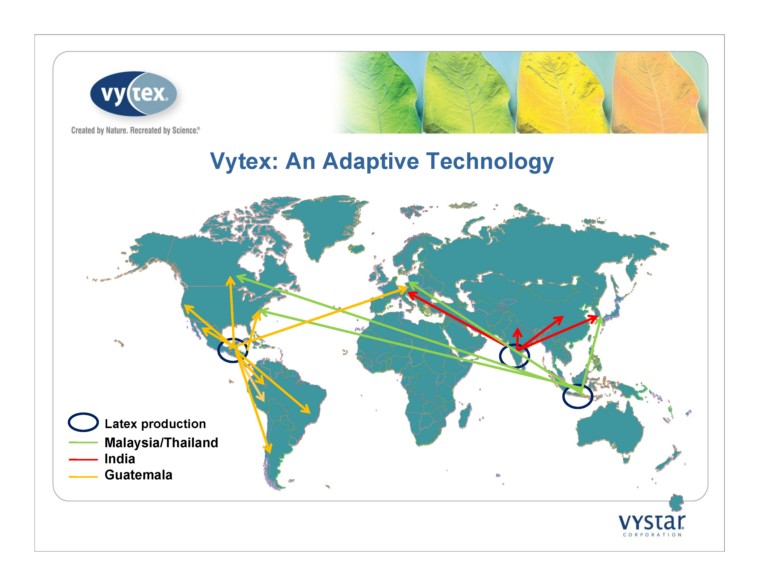

Vytex: An Adaptive Technology Latex production Malaysia/Thailand India Guatemala

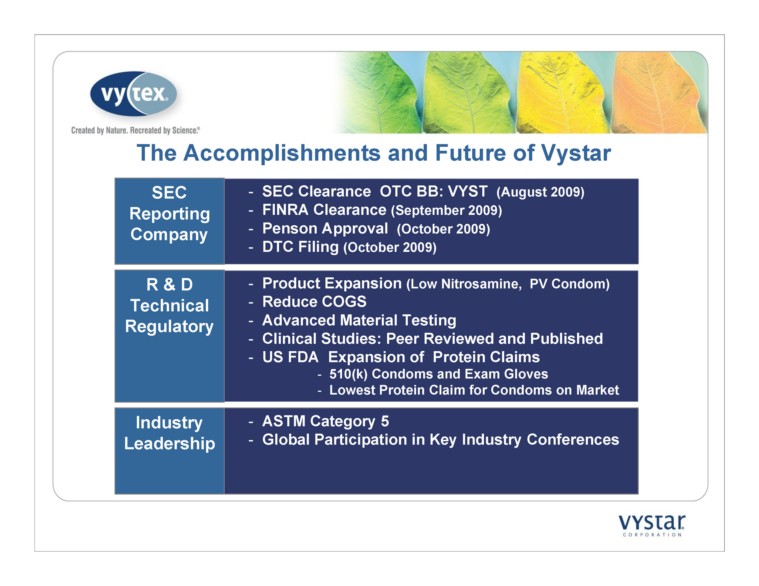

The Accomplishments and Future of Vystar - R & D Technical Regulatory Line Extensions Process Improvements to Reduce COGS Advanced Material Testing to Enhance Value Clinical Studies: Peer Reviewed and Published - - Industry Leadership ASTM Category 5 Global Participation in Key Industry Conferences SEC

Reporting Company (August 2009) (October 2009) (October 2009) (Low Nitrosamine, PV Condom) Reduce COGS Advanced Material Testing Clinical Studies: Peer Reviewed and Published US FDA Expansion of Protein Claims 510(k) Condoms and Exam Gloves Lowest Protein Claim for Condoms on Market

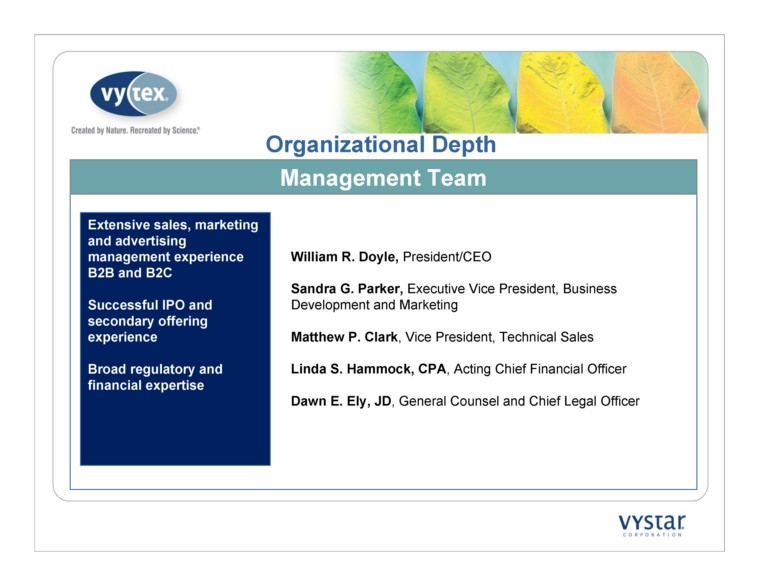

Management Team Extensive sales, marketing

and advertising

management experience

B2B and B2C Successful IPO and

secondary offering

experience Broad regulatory and

financial expertise President/CEO Executive Vice President, Business

Development and Marketing , Vice President, Technical Sales , Acting Chief Financial Officer , General Counsel and Chief Legal Officer Organizational Depth

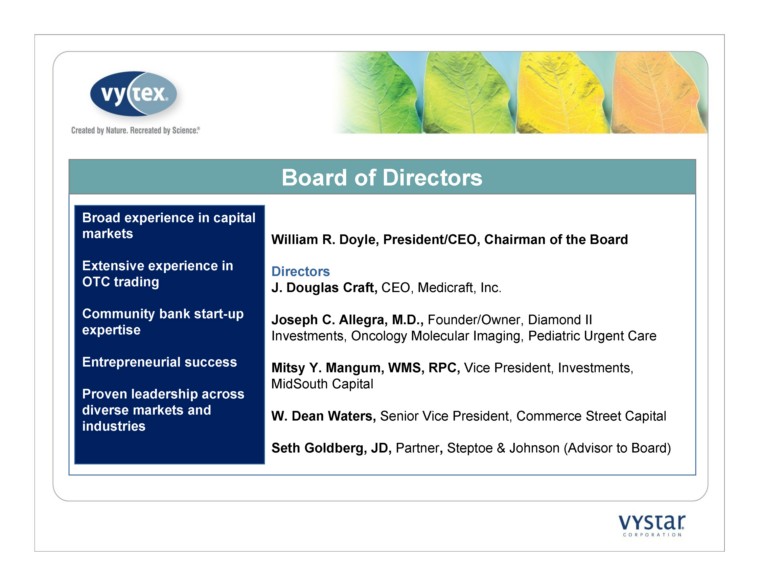

Board of Directors Broad experience in capital

markets Extensive experience in

OTC trading Community bank start-up

expertise Entrepreneurial success Proven leadership across

diverse markets and

industries William R. Doyle, President/CEO, Chairman of the Board Directors CEO, Medicraft, Inc. Founder/Owner, Diamond II Investments, Oncology Molecular Imaging, Pediatric Urgent Care Vice President, Investments,

MidSouth Capital Senior Vice President, Commerce Street Capital Steptoe & Johnson (Advisor to Board)

Technical Catharine C. Calkins-Burke, Ph.D Ranjit K. Matthan, Ph.D, KA Prevulcanised P Ltd. Quan-Tec Air, Inc.; formerly Mayo Foundation Jasmine Elastomerics Selvaraj V M Muthuraja, Stratoshift Technologies, Sdn Bhd Clinical formerly Shands at University of Florida , UCLA Medical Center formerly Ohio State University Medical Center Parker Lee, formerly CEO, Ansell Medical Products, Ansell Ltd. Advisors Extensive raw materials research and development Known expertise on natural rubber latex Active management P&L responsibilities and purchasing influence Noted clinical authors and speakers

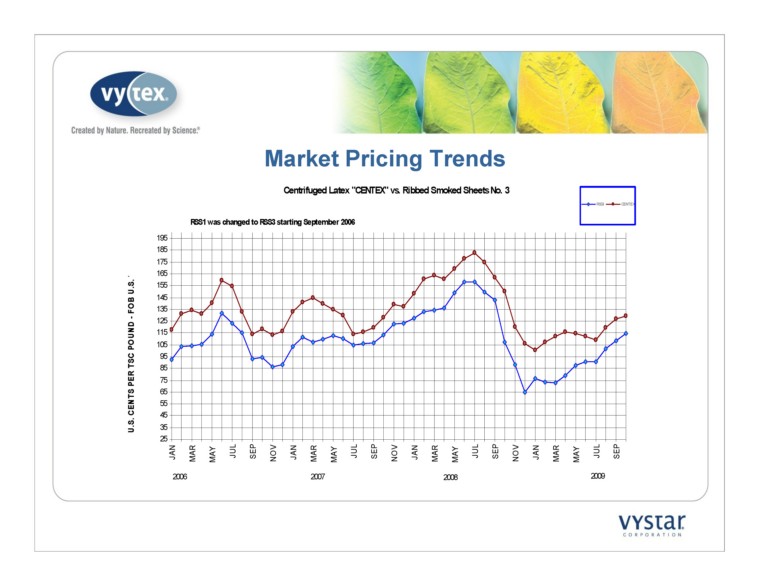

Market Pricing Trends

Financial Projections THE FOLLOWING PROJECTIONS ARE FORWARD-LOOKING STATEMENTS. WE MAY NOT ACTUALLY ACHIEVE THE PROJECTIONS DISCLOSED AND YOU SHOULD NOT PLACE UNDUE RELIANCE UPON SUCH FORWARD-LOOKING STATEMENTS. ACTUAL RESULTS COULD DIFFER MATERIALLY FROM SUCH PROJECTIONS. IN OUR PRIVATE PLACEMENT MEMORANDUM DATED OCTOBER 28, 2009, WE HAVE INCLUDED IMPORTANT FACTORS IN THE “RISK FACTORS” SECTION OF THE MEMORANDUM THAT WE BELIEVE COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THE PROJECTIONS THAT WE MAKE. OUR FORWARD-LOOKING STATEMENTS DO NOT REFLECT THE POTENTIAL IMPACT OF ANY FUTURE ACQUISITIONS, MERGERS, DISPOSITIONS, JOINT VENTURES OR INVESTMENTS WE MAY MAKE. YOU SHOULD READ OUR PRIVATE PLACEMENT MEMORANDUM COMPLETELY AND WITH THE UNDERSTANDING THAT OUR ACTUAL FUTURE RESULTS MAY BE MATERIALLY DIFFERENT FROM WHAT WE EXPECT. WE DO NOT ASSUME ANY OBLIGATION TO UPDATE ANY FORWARD-LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE, EXCEPT AS REQUIRED BY LAW.

2009 Projections Vystar Corporation FY 2009 Actual Results Projected Q1 Q2 Q3 Q4 Total Net Product Sales $ 11 $ 1 $ 6 $ 32 $ 50 Licensing Revenue - - - - - Total Net Revenue 11 1 6 32 50 Gross Margin - Product 3 (1) - 6 8 Gross Margin - Licensing - - - - - Operating expenses 511 560 485 474 2,030 Net Income (Loss) $ (508) $ (561) $ (485) $ (468) $ (2,022) Cash Balance, End of Period $ 1,253 $ 1,345 $ 722 $ 409 $ 409 Sales, in tonnes: 3.5 0.5 2.7 16.0 22.7 Product Sales 3.5 0.5 2.7 16.0 22.7 Licensing Sales - - - - -

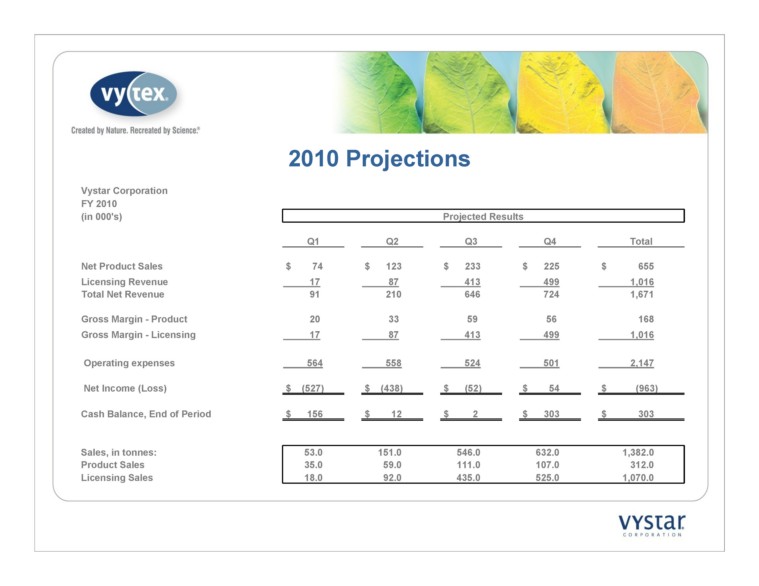

2010 Projections Vystar Corporation FY 2010 Projected Results Q1 Q2 Q3 Q4 Total Net Product Sales $ 74 $ 123 $ 233 $ 225 $ 655 Licensing Revenue 17 87 413 499 1,016 Total Net Revenue 91 210 646 724 1,671 Gross Margin - Product 20 33 59 56 168 Gross Margin - Licensing 17 87 413 499 1,016 Operating expenses 564 558 524 501 2,147 Net Income (Loss) $ (527) $ (438) $ (52) $ 54 $ (963) Cash Balance, End of Period $ 156 $ 12 $ 2 $ 303 $ 303 Sales, in tonnes: 53.0 151.0 546.0 632.0 1,382.0 Product Sales 35.0 59.0 111.0 107.0 312.0 Licensing Sales 18.0 92.0 435.0 525.0 1,070.0

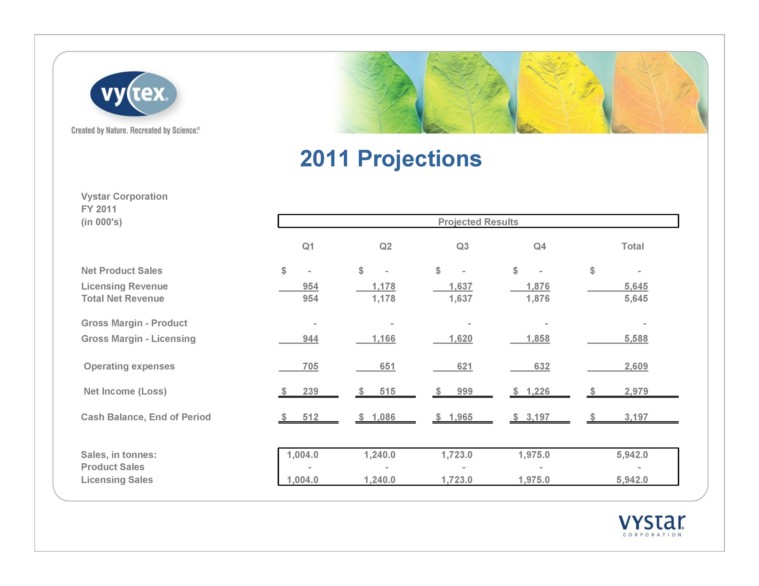

2011 Projections Vystar Corporation FY 2011 Projected Results Q1 Q2 Q3 Q4 Total Net Product Sales $ - $ - $ - $ - $ - Licensing Revenue 954 1,178 1,637 1,876 5,645 Total Net Revenue 954 1,178 1,637 1,876 5,645 Gross Margin - Product - - - - - Gross Margin - Licensing 944 1,166 1,620 1,858 5,588 Operating expenses 705 651 621 632 2,609 Net Income (Loss) $ 239 $ 515 $ 999 $ 1,226 $ 2,979 Cash Balance, End of Period $ 512 $ 1,086 $ 1,965 $ 3,197 $ 3,197 Sales, in tonnes: 1,004.0 1,240.0 1,723.0 1,975.0 5,942.0 Product Sales - - - - - Licensing Sales 1,004.0 1,240.0 1,723.0 1,975.0 5,942.0

Vystar Offering (Refer to PPM) Offer Up to 1,000,000 Shares of

Common Stock and Warrants to

Purchase up to

1,000,000 Shares of

Common Stock Offering Offer Total Shares

Outstanding Offer Price Offering Price $2.00 per Share $2,000,000 Warrants 500,000 at $1.50/share Exercisable within 12

months 500,000 at $3.25/share Exercisable within 24 months 12,787,274

Why Invest in Vystar? Large Global Market 40,000 products

made with

natural rubber

latex $2.6B market Fully Commercialized Address Allergenicity

Concerns Virtually

undetectable

levels of

antigenic protein Endorsed by

American Latex

Allergy Association Green

Footprint All natural, renewable

resource Biodegradable No VOCs No known human

carcinogens FDA 510(k)

Clearances Highly prized

510(k) clearance

for lowest

antigenic protein

claim on market