Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SMITH A O CORP | d8k.htm |

Baird 2009 Industrial Conference Exhibit 99.1 |

2 This presentation contains statements

that we believe are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements generally can

be identified by the use of words such as “may,” “will,”

“expect,” “intend,” “estimate,” “anticipate,” “believe,” “continue,” “guidance”, or words of similar meaning. These forward-looking statements are subject to risks and uncertainties that

could cause actual results to differ materially from those anticipated as of the date of

this release. Factors that could cause such a variance include the following: significant volatility in raw material prices; competitive pressures on the company’s

businesses; inability to implement pricing actions; negative impact of future pension

contributions on the company’s cash flow; instability in the company’s electric motor and water products markets; further weakening in housing construction; further weakening in

commercial construction; timing of any recoveries in housing or commercial construction;

a slowdown in the Chinese economy; expected restructuring savings realized; further

adverse changes in customer liquidity and general economic and capital market conditions; the impact of acquisition accounting or non-GAAP financial measures on the company’s financial statements

or difficulties in closing on and integrating the proposed China acquisition, and

realizing future growth and profit expectations. Forward-looking statements

included in this press release are made only as of the date of this presentation, and the company is under no obligation to update these statements to reflect subsequent events or

circumstances. All subsequent written and oral forward-looking statements

attributed to the company, or persons acting on its behalf, are qualified entirely by

these cautionary statements. This presentation contains certain non-GAAP financial

measures as that term is defined by the SEC. Non-GAAP financial measures are

generally identified by “Adjusted” (Adj.), “Non-GAAP” or “Before Restructuring”. Forward Looking Statements |

3 Investment Case • Leader in Commercial and Residential Water Heaters • 2009 Margin Expansion, in spite of Significant Volume Declines • Strong Balance Sheet and Cash Flow • China/Asia • Energy Efficient Products |

4 $1.00 $1.25 $1.50 $1.75 $2.00 $2.25 $2.50 $2.75 $3.00 $3.25 2007 2008 2009 GAAP Forecast 2009 Non- GAAP forecast 2009 EPS Forecast $2.70 $2.85 $.15 Range $2.60 - $2.75 $2.95 - $3.13 $.18 Range |

5 Sales 1,481.9 $ 1,796.3 $ (314.4) $ -18% Net Earnings 67.0 $ 75.2 $ (8.2) $ -11% EPS 2.21 $ 2.48 $ (0.27) $ -11% (in millions, except per share) 2009 2008 change % chg. Financial Results – 9 months YTD Earnings and EPS are Non-GAAP |

6 Water Products 1,012.8 $ 1,105.0 $ (92.2) $ -8% Electrical Products 472.0 694.9 (222.9) -32% Intersegment (2.9) (3.6) 0.7 Total Sales 1,481.9 $ 1,796.3 $ (314.4) $ -18% Segment Sales – 9 months YTD 2009 2008 change % chg. (in millions) |

7 Water Products 104.3 $ 105.1 $ (0.8) $ -1% Electrical Products 27.4 44.3 (16.9) -38% Corporate (35.8) (36.9) 1.1 3% Total Operating Profit 95.9 $ 112.5 $ (16.6) $ -15% Margin Water Products 10.3% 9.5% Electrical Products 5.8% 6.4% Operating Profit – 9 months YTD 2009 2008 change % chg. (in millions, except margins) |

8 • Operating cash flow of $198 million • Expect operating cash flow of approximately $190 to $200 million in 2009 • Balance Sheet remains strong • Debt to Capital ratio of 24% 197. 8 75.0 0 20 40 60 80 100 120 140 160 180 200 Nine Month Cash Flow from Operations 9/30/08 9/30/09 |

9 A. O. Smith *EBITDA Excludes $8.7M for restructuring $1.4B $.9B Water Products Electrical Products* Sales EBITDA 31% 69% |

10 0 200 400 600 800 1000 1200 1400 1600 2004 2005 2006 2007 2008 2009 thru Sept 0% 2% 4% 6% 8% 10% 12% Sales EBIT Margin Water Products – Sales & Earnings |

11 U. S. Water Heater Market Segment 0% 10% 20% 30% 40% 50% Tankless Residential Market Commercial Market 0% 10% 20% 30% 40% 50% 60% Standard Commercial |

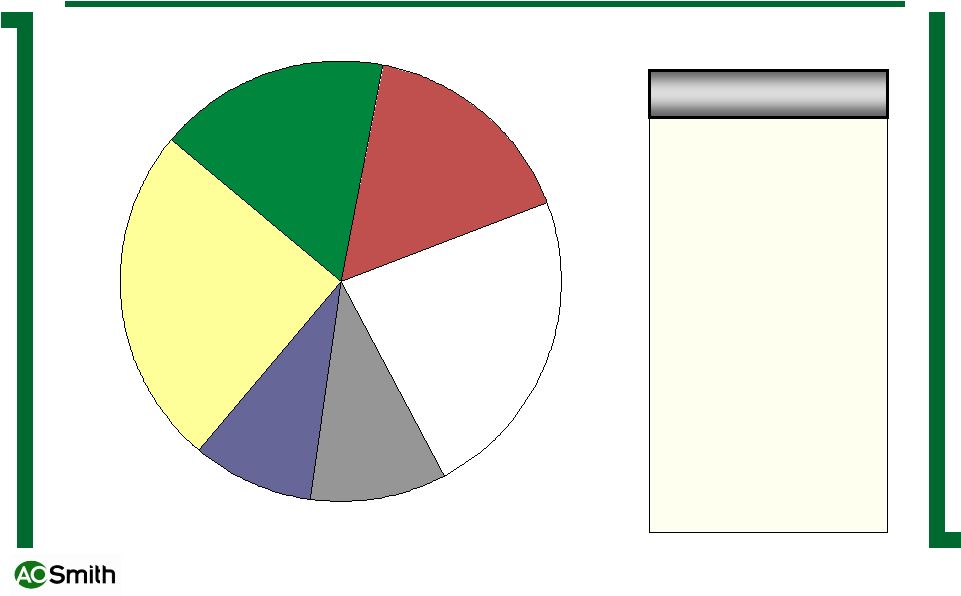

12 NA Commercial 11% NA Residential 74% China 15% Water Products End Markets |

13 0 100 200 300 400 500 600 700 800 900 1000 2004 2005 2006 2007 2008 2009 thru Septmber 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% Sales EBIT Margin Electrical Products–Sales & Earnings EBIT Margin shown is Non-GAAP |

14 HVAC & R 17% Pump 16% Distribution 23% General Industries 10% China/Asia 9% Hermetic 25% Trane Carrier Scroll Tech York Copeland Pentair Waterway Hayward Broan Grainger Johnstone SCP Major Customers Electrical Products Market Segments Served |

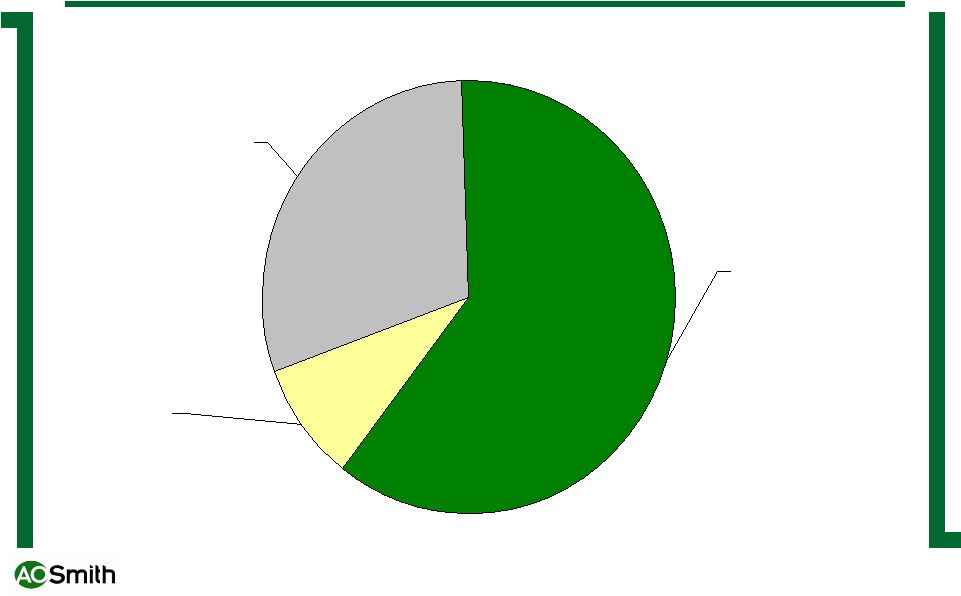

15 Electrical Products End Markets China 9% NA Residential 61% NA Commercial 30% |

16 China/Asia now 13% of Sales and Growing 0 50 100 150 200 250 300 2003 2004 2005 2006 2007 2008 Electrical Products Water Products Sales have grown 35% (CAGR) over the last 5 years |

17 Mega Trends - China Data: (The Value of China's Emerging Middle Class) Share of Chinese Urban Households, % |

18 China Motor Manufacturing Commercial hermetic motors for air conditioning & refrigeration $0 $20 $40 $60 $80 $100 $120 2004 2005 2006 2007 2008 Suzhou Yueyang |

19 • Since 1995 • Products designed for Chinese consumers • Experienced Chinese managers • Double digit margin • Strong retail presence • Consistent strong growth • Doubled capacity to 2M units - 2010 Nanjing, China |

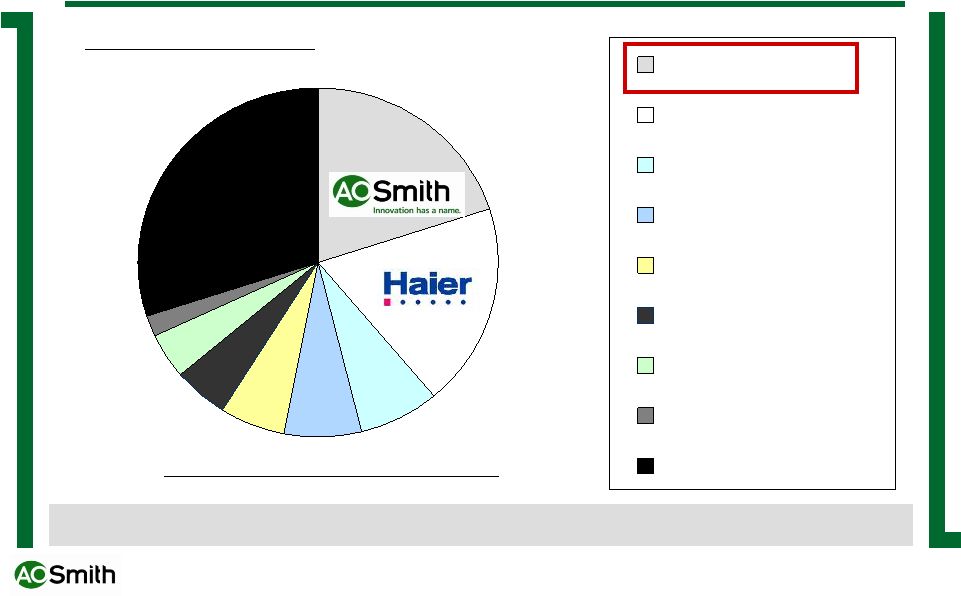

20 A. O. Smith 20% Haier 19% Makro 7% Wanhe 7% Ariston 6% Rinnai 5% Noritz 4% Siemens 2% > 100 Others 30% > 100 Others 30% Leading Electric Brands: A.O. Smith, Haier, Ariston, Siemens Leading Gas Instantaneous Brands: Makro, Wanhe, Rinnai, Noritz Source: GFK-2009 (by Value) Leading residential brands measured in currency; Tier One Market China Residential Share |

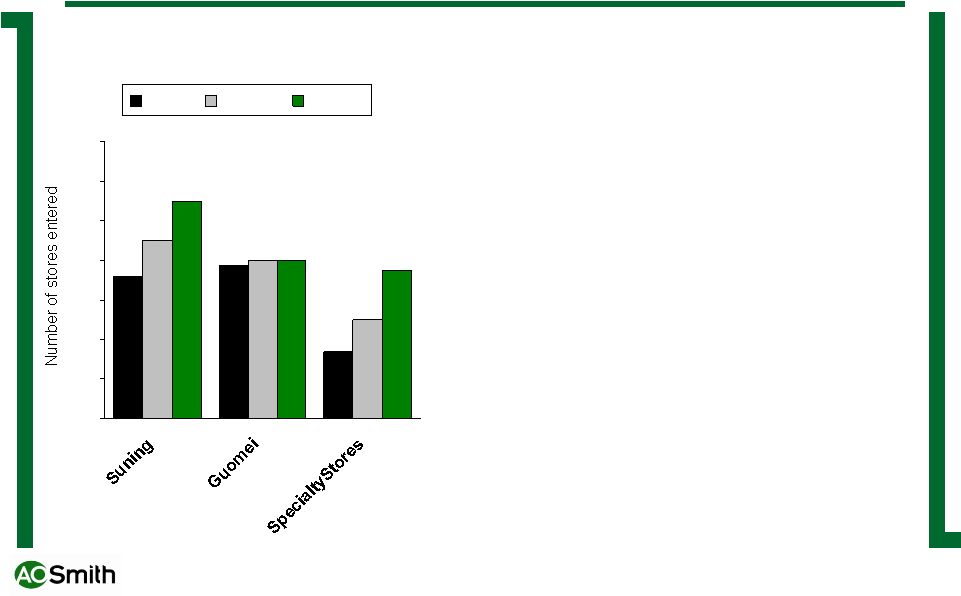

21 Retail channel Expansion 2008 to 2010 900 800 500 721 335 777 1100 750 0 200 400 600 800 1000 1200 1400 2008 2009P 2010P Distribution Channel Expansion • Suning currently has 800 stores and plans to reach 900 stores by year end • Guomei is down sizing for store efficiencies • We have been assisting distributors opening specialty stores, and developing service oriented dealers network |

22 Specialty Stores |

23 Hierarchy of Global Drinking Water Needs Source: AO Smith/MBK/2008 Availability Desalinization, Well drilling, Pumping, Point-of-Egress Security, Health, Hygiene Chlorination, Heating/Boiling, Point of Entry Access Infrastructure, Home Plumbing Taste/Convenience Filtration, Bottled water, POU Africa, Middle East, (Water Scarcity) Sustainability water recycling, bottled alternatives Aesthetics soft, carbonated, flavored China, Eastern Europe, India (Water Quality/Health) North America W. Europe (Custom Water) |

24 China Water Purification Landscape • Economic Growth – GDP growth of 8-10% – Retail and appliance sales +20% YOY – Water Purification sales +10-15%/year – Reverse Osmosis and Point of Use sales forecasted at +30% • Improvement of Living Standards – “Feature rich” apartment options – Growing awareness of water health and quality – In home product – 10% market penetration • Declining Water Quality – 70% of source water unsafe to drink • Fragmented market |

25 Chinese Water Purification Terminology • Water Dispenser – free standing unit, dispenses purchased water from jugs, may dispense either hot or cold • Drinking Machines – free standing units that filters tap water and may dispense either hot or cold • Water Jugs – carafe units, typically counter top, that allow gravity filtration of tap water • Water Purifiers/Cleaners – stand alone, or multi- component filtration. Purifiers typically includes RO, typically piped-in and under sink. |

26 Tianlong Acquisition • Acquire leading product in China water purification market • Leverage A. O. Smith brand and water heater presence in appliance stores and building centers • Other benefits: – Existing parallel channels and brands for distribution sales in China – Existing quality manufacturing base for export sales (India)

|

27 Tianlong Profile • Leading supplier of RO systems to the China market – Domestic market share leader – Exports to 30 countries • Market channels – 3200 franchise shops – 8000 mom and pop stores • Product Types – Residential RO machines, RO membranes, filters, water softeners, Commercial/Industrial equipment, Components of residential RO machines • Profitability – Accretive day 1 – ROIC greater than cost of capital in first full year under AOS ownership • 2010 Preliminary Look – Revenues greater than $75 million – Operating margins in upper teens – Accretion: $.10 to $.15 per share |

28 • Bangalore • Establish brand & position product • Develop manufacturing capability – Greenfield manufacturing facility – Indian management team • Focus on storage electric water heaters • Focus on top metropolitan cities India: Currently “Made in China” |

29 Energy Efficiency |

30 0 2000 4000 6000 8000 10000 12000 14000 16000 18000 20000 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 CAGR = 20.8% Cyclone Sales Growth 20% of commercial revenues in 2008 |

31 A. O. Smith Tankless Gas Water Heaters • A comprehensive line of tankless water heaters • Residential and Commercial designs • Indoor and Outdoor installation options • Available in Natural Gas or Propane • Energy Efficient – up to 84% thermal efficiency |

32 Heat Pump Water Heating • Acquisition of AERS – Specialty commercial manufacturer • Additional, new distribution channel • Introducing heat pump water heater in China |

33 Solar Water Heating • Balcony mount system for China • Commercial system for Europe • Residential water heater for North America |

34 New Centurion Pro Pump Motor • Single-Speed, Two-Speed, Three Phase • Improved cooling longer life • Better bearing protection longer life • Better wiring access easier installation • Business – Won 12,000 units ($1.2M) at Hayward – Working with Pentair and Jandy for 2010 season |

35 Energy Efficiency Strategy * Average Selling Price Premium 2 Speed Efficiency Gains of 12% running longer on Low Speeds Operating Savings of 30~65% over Single Speed Motors Variable Speed 90% over Single Speed Flexible – Can be run at Optimum Speed Efficiency range 80% Operating Savings of 30- Motors $70* $125* $425* Traditional Single Speed Single Speed Avg. Efficiency = 68% |

36 AOS Comfort Series |

37 Residential Hermetic Variable Speed • 59 frame IPM for Bristol – Completed in just 3 weeks and delivered March 2 – Seeking IP protection on design – Preliminary tests found 2 SEER point improvement nd |

38 Energy Efficient Products • 40% of China water heater sales are highest energy efficiency rating! • 25% of water products sales exceed minimum energy efficiency standards • 9% of electrical products sales exceed minimum energy efficiency standards |

39 Investment Case • Leader in Commercial and Residential Water Heaters • Margin Expansion, in spite of Significant Volume Declines • Strong Balance Sheet and Cash Flow • China/Asia • Energy Efficient Products |

Thank you! |

41 Investor Contact Patricia Ackerman Vice President, Investor Relations and Treasurer 414-359-4130 packerman@aosmith.com |