Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - RETAIL PROPERTIES OF AMERICA, INC. | ex-9916x30x21.htm |

| 8-K - 8-K - RETAIL PROPERTIES OF AMERICA, INC. | rpai-20210803.htm |

Exhibit 99.2

T A B L E O F C O N T E N T S

| 1 | E A R N I N G S R E L E A S E.......................................................................... | ||||||||||||||||

| 2 | |||||||||||||||||

F I N A N C I A L S U M M A R Y | |||||||||||||||||

| Condensed Consolidated Balance Sheets................................................. | |||||||||||||||||

| Condensed Consolidated Statements of Operations................................ | |||||||||||||||||

| Funds From Operations Attributable to Common Shareholders, Operating FFO Attributable to Common Shareholders and Additional Information....................................................................... | |||||||||||||||||

| Supplemental Financial Statement Detail................................................. | |||||||||||||||||

| Same Store Net Operating Income............................................................ | |||||||||||||||||

| Capitalization............................................................................................. | |||||||||||||||||

| Covenants.................................................................................................. | |||||||||||||||||

| Summary of Indebtedness........................................................................ | |||||||||||||||||

| 3 | |||||||||||||||||

T R A N S A C T I O N S U M M A R Y | |||||||||||||||||

| Development Projects............................................................................... | |||||||||||||||||

| Acquisitions and Dispositions.................................................................... | |||||||||||||||||

| 4 | |||||||||||||||||

P O R T F O L I O S U M M A R Y | |||||||||||||||||

| Retail Market Summary............................................................................. | |||||||||||||||||

| Retail Operating Portfolio Occupancy....................................................... | |||||||||||||||||

| Top Retail Tenants..................................................................................... | |||||||||||||||||

| Retail Leasing Activity Summary................................................................ | |||||||||||||||||

| Retail Lease Expirations............................................................................. | |||||||||||||||||

| 5 | |||||||||||||||||

O T H E R I N F O R M A T I O N | |||||||||||||||||

| COVID-19 Disclosure – Tenant Resiliency and Rent Collections................ | |||||||||||||||||

| COVID-19 Disclosure – Supplemental Base Rent and Uncollectible Lease Income Information......................................................................... | |||||||||||||||||

| Non-GAAP Financial Measures and Reconciliations.................................. | |||||||||||||||||

Retail Properties of America, Inc. | 2021 Spring Road, Suite 200 | Oak Brook, Illinois 60523 | 855.247.RPAI | www.rpai.com

RETAIL PROPERTIES OF AMERICA, INC. REPORTS

SECOND QUARTER AND YEAR TO DATE 2021 RESULTS

Oak Brook, IL – August 3, 2021 – Retail Properties of America, Inc. (NYSE: RPAI) (the “Company”) today reported financial and operating results for the quarter and six months ended June 30, 2021.

FINANCIAL RESULTS

For the quarter ended June 30, 2021, the Company reported:

▪Net income attributable to common shareholders of $15.4 million, or $0.07 per diluted share, compared to net loss attributable to common shareholders of $(7.3) million, or $(0.04) per diluted share, for the same period in 2020;

▪Funds from operations (FFO) attributable to common shareholders of $56.9 million, or $0.27 per diluted share, compared to $36.1 million, or $0.17 per diluted share, for the same period in 2020;

▪Operating funds from operations (Operating FFO) attributable to common shareholders of $56.9 million, or $0.27 per diluted share, compared to $36.1 million, or $0.17 per diluted share, for the same period in 2020;

▪Approximately $6 million recorded within lease income, equating to $0.03 per diluted share, due to reversals of uncollectible lease income, primarily consisting of amounts received during the second quarter of 2021 from cash-basis and vacated tenants that pertain to periods prior to the second quarter of 2021;

▪Cash collections as of July 26, 2021 of 98% of billed second quarter 2021 base rent, up from 96% of billed first quarter 2021 base rent as previously reported;

▪Cash collections as of June 30, 2021 of 95% of previously deferred base rent that was due during the second quarter of 2021; and

▪Cash-basis tenants as of June 30, 2021 represent 9% of annualized base rent (ABR), down from 11% of ABR as of March 31, 2021.

For the six months ended June 30, 2021, the Company reported:

▪Net income attributable to common shareholders of $20.1 million, or $0.09 per diluted share, compared to $15.0 million, or $0.07 per diluted share, for the same period in 2020;

▪FFO attributable to common shareholders of $109.2 million, or $0.51 per diluted share, compared to $98.6 million, or $0.46 per diluted share, for the same period in 2020;

▪Operating FFO attributable to common shareholders of $109.3 million, or $0.51 per diluted share, compared to $93.5 million, or $0.44 per diluted share, for the same period in 2020; and

▪Approximately $11 million recorded within lease income, equating to $0.05 per diluted share, due to reversals of uncollectible lease income, primarily consisting of amounts received during the first half of 2021 from cash-basis and vacated tenants that pertain to periods prior to 2021.

Subsequent to quarter end, as previously announced, the Company entered into a definitive Agreement and Plan of Merger with Kite Realty Group Trust (Kite Realty Group), pursuant to

n Retail Properties of America, Inc.

T: 855.247.RPAI

www.rpai.com 2021 Spring Road, Suite 200

Oak Brook, IL 60523

which RPAI will merge with and into a subsidiary of Kite Realty Group, with the subsidiary surviving the merger. Immediately following the closing of the merger, such subsidiary will merge with and into Kite Realty Group, L.P., the operating partnership of Kite Realty Group, so that all of the assets of Kite Realty Group will be owned at or below the operating partnership level. The board of directors of the Company and the board of trustees of Kite Realty Group unanimously approved the transaction. The parties expect the transaction to close during the fourth quarter of 2021, subject to the satisfaction of customary closing conditions, including the approval of both the Company’s and Kite Realty Group’s shareholders.

OPERATING RESULTS

For the quarter ended June 30, 2021, the Company’s portfolio results were as follows:

▪32.7% increase in same store net operating income (NOI) over the comparable period in 2020;

▪Retail portfolio occupancy: 91.8% at June 30, 2021, up 30 basis points from 91.5% at March 31, 2021 and down 180 basis points from 93.6% at June 30, 2020;

▪Retail portfolio percent leased, including leases signed but not commenced: 93.4% at June 30, 2021, up 70 basis points from 92.7% at March 31, 2021 and down 150 basis points from 94.9% at June 30, 2020;

▪Retail portfolio leased to occupied spread percentage: 160 basis points at June 30, 2021, up 40 basis points from 120 basis points at March 31, 2021 and up 30 basis points from 130 basis points at June 30, 2020, representing approximately $8.3 million in ABR and $26.32 in ABR per square foot;

▪Total retail portfolio ABR per occupied square foot of $19.37 at June 30, 2021, up 0.5% from $19.28 ABR per occupied square foot at March 31, 2021 and down 0.4% from $19.45 ABR per occupied square foot at June 30, 2020;

▪904,000 square feet of retail leasing transactions comprised of 113 new and renewal leases;

▪A blended re-leasing spread of positive 5.0%, comprised of comparable cash leasing spreads of 12.7% on new leases and 2.8% on renewal leases;

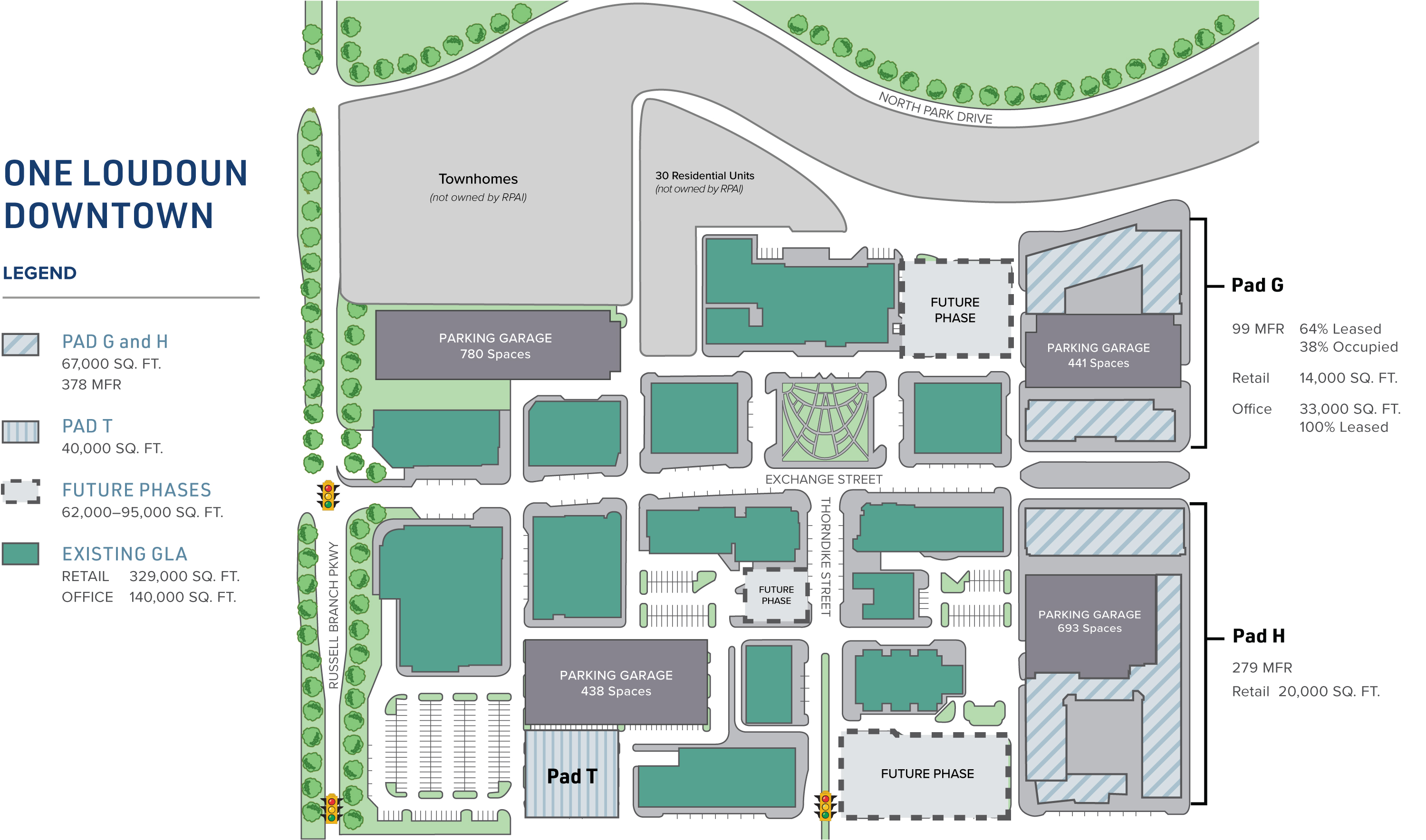

▪Signed leases at One Loudoun Downtown for an additional 42 of Pad G’s 99 multi-family rental units, branded Vyne, which were 64% leased and 38% occupied at June 30, 2021; and

▪Signed a lease representing an additional 26% of Pad G’s 33,000 square feet of office space, branded One Endicott, which was 100% leased at June 30, 2021.

For the six months ended June 30, 2021, the Company’s portfolio results were as follows:

▪13.0% increase in same store NOI over the comparable period in 2020;

▪1,591,000 square feet of retail leasing transactions comprised of 226 new and renewal leases; and

▪A blended re-leasing spread of positive 5.3%, comprised of comparable cash leasing spreads of 15.2% on new leases and 2.9% on renewal leases.

INVESTMENT ACTIVITY

Expansions and Redevelopments

The Company continues to make progress on the execution of its active expansion and redevelopment projects and invested $29.9 million during the first half of 2021 primarily at Circle East, One Loudoun Downtown, The Shoppes at Quarterfield and Southlake Town Square, with the vast majority of this investment related to the One Loudoun Downtown Pads G & H expansion project.

ii

Active Projects

One Loudoun Downtown

During the quarter, the Company and KETTLER, its joint venture partner for the multi-family component of the mixed-use expansion of Pads G & H at One Loudoun Downtown located in the Washington, D.C. metropolitan statistical area (MSA), signed leases for an additional 42 of Pad G’s 99 multi-family rental units, branded Vyne, which were 64% leased and 38% occupied at June 30, 2021. The Company also signed a lease representing an additional 26% of Pad G’s 33,000 square feet of office space, branded One Endicott, which was 100% leased at June 30, 2021.

At Pad H, which includes 279 multi-family rental units, construction continues to progress, including in-unit installation of final finishes and appliances as well as interior amenity finishes.

The aggregate One Loudoun Downtown Pads G & H expansion project, which includes 378 multi-family rental units as well as 67,000 square feet of commercial gross leasable area, remains on track to stabilize in Q2 – Q3 2022.

Circle East

During the quarter, the Company signed Brightside Boutique for in-line space at its 82,000 square foot Circle East mixed-use project located in Towson, MD within the Baltimore MSA, bringing the project to 29% leased. Madison Reed, another in-line tenant, opened during the quarter.

Other Projects

At the 100% leased, single-tenant pad development at Southlake Town Square, the tenant commenced rent payment on July 1, 2021. The Company continues construction at The Shoppes at Quarterfield reconfiguration, which is 100% leased, with targeted stabilization in Q1 – Q2 2022.

Acquisitions

Subsequent to quarter end, the Company closed on the acquisition of Arcadia Village, a 100% leased neighborhood center located in the Phoenix MSA, for a gross purchase price of $21.0 million.

BALANCE SHEET

As of June 30, 2021, the Company had no outstanding unsecured debt principal due until November 2023, a fully undrawn $850.0 million unsecured revolving line of credit and approximately $917.0 million in total available liquidity, compared to $888.0 million as of March 31, 2021, and $727.3 million as of June 30, 2020.

Additionally, as of June 30, 2021, the Company had $1.8 billion of gross consolidated indebtedness with a weighted average contractual interest rate of 4.19% and a weighted average maturity of 5.4 years, up from 4.1 years as of June 30, 2020, and a net debt to quarterly annualized adjusted EBITDAre ratio of 5.6x.

Subsequent to quarter end, as previously announced, the Company closed on the amendment and extension of its $850.0 million unsecured revolving line of credit (Unsecured Revolving Line of Credit). This amendment and extension maintains the Company’s existing $850.0 million borrowing capacity, financial covenants, including the 6.50% capitalization rate used to calculate certain financial covenants, and leverage-based grid pricing as well as:

▪Expands the available accordion feature, enabling the Company to increase borrowing capacity by up to $750.0 million to a total of $1.6 billion, subject to lender approval;

iii

▪Incorporates a sustainability metric, based on targeted greenhouse gas emission reductions, which permits the Company to reduce the applicable grid-based spread by one basis point annually upon attainment;

▪Improves ratings-based grid pricing by 10-15 basis points from the previous ratings-based grid across various points on the investment grade ratings spectrum;

▪Extends the maturity date from April 22, 2022 to January 8, 2026; and

▪Includes retention of two six-month extension options, exercisable at the Company’s sole election.

Also subsequent to quarter end, the Company closed on the amendment of its $150.0 million term loan due 2026, improving leverage-based and ratings-based grid pricing, resulting in a 40-basis point reduction in the current applicable leverage-based pricing spread.

DIVIDEND

As previously announced on May 27, 2021, the Company’s board of directors declared a second quarter dividend for its outstanding Class A common stock of $0.075 per share, up from the $0.07 per share declared for the first quarter of 2021. The second quarter dividend of $0.075 per share, which totaled $16.1 million, was paid on July 9, 2021, to Class A common stockholders of record on June 25, 2021.

As previously announced on July 26, 2021, the Company’s board of directors declared a third quarter dividend for its outstanding Class A common stock of $0.075 per share. The dividend of $0.075 per share will be paid on October 8, 2021, to Class A common stockholders of record on October 1, 2021.

2021 GUIDANCE

In light of the Company’s proposed merger with Kite Realty Group previously announced, the Company will no longer provide guidance and it is not affirming past guidance.

The Company will no longer hold a webcast conference call to discuss its quarterly results and operating performance.

SUPPLEMENTAL INFORMATION

The Company has posted supplemental financial and operating information and other data in the INVEST section of its website.

ABOUT RPAI

Retail Properties of America, Inc. is a REIT that owns and operates high quality, strategically located open-air shopping centers, including properties with a mixed-use component. As of June 30, 2021, the Company owned 100 retail operating properties in the United States representing 19.7 million square feet. The Company is publicly traded on the New York Stock Exchange under the ticker symbol RPAI. Additional information about the Company is available at www.rpai.com.

iv

SAFE HARBOR LANGUAGE

The statements and certain other information contained in this press release, which can be identified by the use of forward-looking terminology such as “believes,” “expects,” “may,” “should,” “intends,” “plans,” “estimates” or “anticipates” and variations of such words or similar expressions or the negative of such words, constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbors created thereby. These forward-looking statements reflect the Company’s current views about its plans, intentions, expectations, strategies and prospects, which are based on the information currently available to the Company and on assumptions it has made. Although the Company believes that its plans, intentions, expectations, strategies and prospects as reflected in or suggested by those forward-looking statements are reasonable, the Company can give no assurance that such plans, intentions, expectations or strategies will be attained or achieved. Furthermore, these forward-looking statements should be considered as subject to the many risks and uncertainties that exist in the Company’s operations and business environment. Such risks and uncertainties could cause actual results to differ materially from those projected. These uncertainties include, but are not limited to, economic, business and financial conditions, and changes in the Company’s industry and changes in the real estate markets in particular, economic and other developments in markets where the Company has a high concentration of properties, the Company’s business strategy, the Company’s projected operating results, rental rates and/or vacancy rates, frequency and magnitude of defaults on, early terminations of or non-renewal of leases by tenants, bankruptcy, insolvency or general downturn in the business of a major tenant or a significant number of smaller tenants, adverse impact of e-commerce developments and shifting consumer retail behavior on tenants, interest rates or operating costs, the discontinuation of London Interbank Offered Rate (LIBOR), real estate and zoning laws and changes in real property tax rates, real estate valuations, the Company’s leverage, the Company’s ability to generate sufficient cash flows to service outstanding indebtedness and make distributions to shareholders, changes in the dividend policy for the Company’s Class A common stock, the Company’s ability to obtain necessary outside financing, the availability, terms and deployment of capital, general volatility of the capital and credit markets and the market price of the Company’s Class A common stock, risks generally associated with real estate acquisitions and dispositions, including the Company’s ability to identify and pursue acquisition and disposition opportunities, risks generally associated with redevelopment, including the impact of construction delays and cost overruns and related impact on the Company’s estimated investments in such redevelopment, the Company’s ability to lease redeveloped space, the Company’s ability to identify and pursue redevelopment opportunities and the risk that it takes longer than expected for development assets to stabilize or that the Company does not achieve its estimated returns on such investments, the Company’s ability to enter into new leases or renew leases on favorable terms, pandemics or other public health crises, such as the COVID-19 pandemic, and the related impact on (i) the Company’s ability to manage its properties, finance its operations and perform necessary administrative and reporting functions and (ii) the ability of the Company’s tenants to operate their businesses, generate sales and meet their financial obligations, including the obligation to pay rent and other charges as specified in their leases, risks associated with the proposed merger with Kite Realty Group, including the Company’s ability to consummate the proposed merger on the proposed terms or on the anticipated timeline at all, including risks and uncertainties relating to securing the necessary shareholder approvals and satisfaction of other closing conditions to consummate the proposed merger and the occurrence of any event, change or other circumstance that could give rise to the termination of the merger agreement, the Company’s ability to create long-term shareholder value, regulatory changes and other risk factors, including those detailed in the sections of the Company’s most recent Forms 10-K and 10-Q filed with the SEC titled “Risk Factors,” which you should interpret as heightened as a result of the numerous and ongoing adverse impacts of COVID-19. The extent to which COVID-19 impacts the Company and its tenants will depend on future developments, which are highly uncertain and cannot be predicted with confidence, including the scope, severity and duration of the pandemic, the actions taken to contain the pandemic or mitigate its impact, including the adoption of available COVID-19 vaccines, and the direct and indirect economic effects of the pandemic and containment measures, among others. The Company assumes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

NON-GAAP FINANCIAL MEASURES

As defined by the National Association of Real Estate Investment Trusts (NAREIT), an industry trade group, Funds From Operations (FFO) means net income attributable to common shareholders computed in accordance with generally accepted accounting principles (GAAP), excluding the Company’s share of (i) depreciation and amortization related to real estate, (ii) gains from sales of real estate assets, (iii) gains and losses from change in control and (iv) impairment write-downs of real estate assets and investments in entities directly attributable to decreases in the value of real estate held by the entity. The Company has adopted the NAREIT definition in its computation of FFO attributable to common shareholders. The Company believes that, subject to the following limitations, FFO attributable to common shareholders provides a basis for comparing its performance and operations to those of other real estate investment trusts (REITs). The Company believes that FFO attributable to common shareholders, which is a supplemental non-GAAP financial measure, provides an additional and useful means to assess the operating performance of REITs. FFO attributable to common shareholders does not represent an alternative to (i) “Net income” or “Net income attributable to common shareholders” as an indicator of the Company’s financial performance, or (ii)

v

“Cash flows from operating activities” in accordance with GAAP as a measure of the Company’s capacity to fund cash needs, including the payment of dividends.

The Company also reports Operating FFO attributable to common shareholders, which is defined as FFO attributable to common shareholders excluding the impact of discrete non-operating transactions and other events which the Company does not consider representative of the comparable operating results of its real estate operating portfolio, which is its core business platform. Specific examples of discrete non-operating transactions and other events include, but are not limited to, the impact on earnings from gains or losses associated with the early extinguishment of debt or other liabilities, litigation involving the Company, including gains recognized as a result of settlement and costs to engage outside counsel related to litigation with former tenants, the impact on earnings from executive separation and the excess of redemption value over carrying value of preferred stock redemption, which are not otherwise adjusted in the Company’s calculation of FFO attributable to common shareholders. The Company believes that Operating FFO attributable to common shareholders, which is a supplemental non-GAAP financial measure, provides an additional and useful means to assess the operating performance of REITs. Operating FFO attributable to common shareholders does not represent an alternative to (i) “Net income” or “Net income attributable to common shareholders” as an indicator of the Company’s financial performance, or (ii) “Cash flows from operating activities” in accordance with GAAP as a measure of the Company’s capacity to fund cash needs, including the payment of dividends. Comparison of the Company’s presentation of Operating FFO attributable to common shareholders to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

The Company also reports Net Operating Income (NOI), which it defines as all revenues other than (i) straight-line rental income (non-cash), (ii) amortization of lease inducements, (iii) amortization of acquired above and below market lease intangibles and (iv) lease termination fee income, less real estate taxes and all operating expenses other than lease termination fee expense and non-cash ground rent expense, which is comprised of amortization of right-of-use lease assets and amortization of lease liabilities. NOI consists of Same Store NOI and NOI from Other Investment Properties. Same Store NOI represents NOI from the Company’s same store portfolio consisting of 100 retail operating properties acquired or placed in service and stabilized prior to January 1, 2020. NOI from Other Investment Properties represents NOI primarily from (i) properties acquired or placed in service during 2020 and 2021, (ii) the multi-family rental units at Plaza del Lago and One Loudoun Downtown – Pad G, (iii) Circle East, which is in active redevelopment, (iv) One Loudoun Downtown – Pads G & H, which are in active development, (v) Carillon, a redevelopment project where the Company halted plans for vertical construction during 2020 in response to macroeconomic conditions due to the impact of the COVID-19 pandemic. During the three months ended June 30, 2021, the Company announced plans to commence construction on a medical office building at Carillon in the second half of 2021, (vi) The Shoppes at Quarterfield, which is in active redevelopment, (vii) land held for future development, (viii) investment properties that were sold or classified as held for sale during 2020 and 2021, (ix) the net income from the Company’s wholly owned captive insurance company, and (x) noncontrolling interests. The Company believes that NOI, Same Store NOI and NOI from Other Investment Properties, which are supplemental non-GAAP financial measures, provide an additional and useful operating perspective not immediately apparent from “Net income” or “Net income attributable to common shareholders” in accordance with GAAP. The Company uses these measures to evaluate its performance on a property-by-property basis because they allow management to evaluate the impact that factors such as lease structure, lease rates and tenant base have on the Company’s operating results. NOI, Same Store NOI and NOI from Other Investment Properties do not represent alternatives to “Net income” or “Net income attributable to common shareholders” in accordance with GAAP as indicators of the Company’s financial performance. Comparison of the Company’s presentation of NOI, Same Store NOI and NOI from Other Investment Properties to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

As defined by NAREIT, EBITDA for real estate (EBITDAre) means net income (loss) computed in accordance with GAAP, plus (i) interest expense, (ii) income tax expense, (iii) depreciation and amortization, (iv) impairment charges on investment property and (v) impairment charges on investments in unconsolidated affiliates if caused by a decrease in the value of depreciable property in the affiliate, plus or minus (i) gains from sales of investment property, including gains (or losses) on change in control, and (ii) adjustments to reflect the entity’s share of EBITDAre of unconsolidated affiliates. The Company reports Adjusted EBITDAre, which excludes the impact of certain discrete non-operating transactions and other events such as gain on litigation settlement. The Company believes that Adjusted EBITDAre is useful because it allows investors and management to evaluate and compare the Company’s performance from period to period in a meaningful and consistent manner in addition to standard financial measurements under GAAP. EBITDAre and Adjusted EBITDAre are supplemental non-GAAP financial measures and should not be considered alternatives to “Net income” or “Net income attributable to common shareholders” as indicators of the Company’s financial performance. Comparison of the Company’s presentation of EBITDAre and Adjusted EBITDAre to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

vi

Net Debt to Adjusted EBITDAre is a supplemental non-GAAP financial measure and represents (i) the Company’s total debt principal, which excludes unamortized discount and capitalized loan fees, less (ii) cash and cash equivalents divided by (iii) Adjusted EBITDAre for either the prior three months, annualized or the trailing twelve months (Annualized Adjusted EBITDAre). The Company believes that this ratio is useful because it provides investors with information regarding its total debt principal net of cash and cash equivalents, which could be used to repay debt, compared to its performance as measured using Annualized Adjusted EBITDAre. Comparison of the Company’s presentation of Net Debt to Adjusted EBITDAre to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

CONTACT INFORMATION

Michael Gaiden

Senior Vice President – Finance

Retail Properties of America, Inc.

(630) 634-4233

vii

Retail Properties of America, Inc.

Condensed Consolidated Balance Sheets

(amounts in thousands, except par value amounts)

(unaudited)

| June 30, 2021 | December 31, 2020 | ||||||||||

| Assets | |||||||||||

| Investment properties: | |||||||||||

| Land | $ | 1,073,449 | $ | 1,075,037 | |||||||

| Building and other improvements | 3,610,901 | 3,590,495 | |||||||||

| Developments in progress | 182,979 | 188,556 | |||||||||

| 4,867,329 | 4,854,088 | ||||||||||

| Less: accumulated depreciation | (1,572,604) | (1,514,440) | |||||||||

Net investment properties (includes $93,186 and $74,314 from consolidated variable interest entities, respectively) | 3,294,725 | 3,339,648 | |||||||||

| Cash and cash equivalents | 67,245 | 41,785 | |||||||||

| Accounts receivable, net | 69,494 | 73,983 | |||||||||

| Acquired lease intangible assets, net | 60,666 | 66,799 | |||||||||

| Right-of-use lease assets | 41,855 | 42,768 | |||||||||

| Assets associated with investment properties held for sale | 13,800 | — | |||||||||

Other assets, net (includes $647 and $354 from consolidated variable interest entities, respectively) | 67,973 | 72,220 | |||||||||

| Total assets | $ | 3,615,758 | $ | 3,637,203 | |||||||

| Liabilities and Equity | |||||||||||

| Liabilities: | |||||||||||

Mortgages payable, net (includes unamortized discount of $(428) and $(450), respectively, and unamortized capitalized loan fees of $(160) and $(192), respectively) | $ | 90,374 | $ | 91,514 | |||||||

Unsecured notes payable, net (includes unamortized discount of $(6,044) and $(6,473), respectively, and unamortized capitalized loan fees of $(6,912) and $(7,527), respectively) | 1,187,044 | 1,186,000 | |||||||||

Unsecured term loans, net (includes unamortized capitalized loan fees of $(2,105) and $(2,441), respectively) | 467,895 | 467,559 | |||||||||

Unsecured revolving line of credit | — | — | |||||||||

Accounts payable and accrued expenses | 64,912 | 78,692 | |||||||||

| Distributions payable | 16,110 | 12,855 | |||||||||

| Acquired lease intangible liabilities, net | 58,687 | 61,698 | |||||||||

| Lease liabilities | 84,095 | 84,628 | |||||||||

Liabilities associated with investment properties held for sale | 526 | — | |||||||||

Other liabilities (includes $3,103 and $3,890 from consolidated variable interest entities, respectively) | 62,854 | 72,127 | |||||||||

| Total liabilities | 2,032,497 | 2,055,073 | |||||||||

| Commitments and contingencies | |||||||||||

| Equity: | |||||||||||

Preferred stock, $0.001 par value, 10,000 shares authorized, none issued or outstanding | — | — | |||||||||

Class A common stock, $0.001 par value, 475,000 shares authorized, 214,798 and 214,168 shares issued and outstanding as of June 30, 2021 and December 31, 2020, respectively | 215 | 214 | |||||||||

| Additional paid-in capital | 4,522,790 | 4,519,522 | |||||||||

| Accumulated distributions in excess of earnings | (2,921,415) | (2,910,383) | |||||||||

| Accumulated other comprehensive loss | (22,827) | (31,730) | |||||||||

| Total shareholders’ equity | 1,578,763 | 1,577,623 | |||||||||

| Noncontrolling interests | 4,498 | 4,507 | |||||||||

| Total equity | 1,583,261 | 1,582,130 | |||||||||

| Total liabilities and equity | $ | 3,615,758 | $ | 3,637,203 | |||||||

| 2nd Quarter 2021 Supplemental Information | 1 | |||||||

Retail Properties of America, Inc.

Condensed Consolidated Statements of Operations

(amounts in thousands, except per share amounts)

(unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

| Lease income | $ | 121,239 | $ | 96,803 | $ | 240,619 | $ | 215,498 | |||||||||||||||

| Expenses: | |||||||||||||||||||||||

| Operating expenses | 17,180 | 14,843 | 35,245 | 31,257 | |||||||||||||||||||

| Real estate taxes | 17,799 | 17,916 | 36,733 | 36,449 | |||||||||||||||||||

| Depreciation and amortization | 41,815 | 43,755 | 89,682 | 83,928 | |||||||||||||||||||

| Provision for impairment of investment properties | — | — | — | 346 | |||||||||||||||||||

| General and administrative expenses | 10,374 | 8,491 | 21,492 | 17,656 | |||||||||||||||||||

| Total expenses | 87,168 | 85,005 | 183,152 | 169,636 | |||||||||||||||||||

| Other (expense) income: | |||||||||||||||||||||||

| Interest expense | (18,776) | (19,360) | (37,528) | (36,406) | |||||||||||||||||||

| Gain on litigation settlement | — | — | — | 6,100 | |||||||||||||||||||

| Other income (expense), net | 92 | 215 | 161 | (546) | |||||||||||||||||||

| Net income (loss) | 15,387 | (7,347) | 20,100 | 15,010 | |||||||||||||||||||

| Net loss attributable to noncontrolling interests | 9 | — | 9 | — | |||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 15,396 | $ | (7,347) | $ | 20,109 | $ | 15,010 | |||||||||||||||

| Earnings (loss) per common share – basic and diluted: | |||||||||||||||||||||||

| Net income (loss) per common share attributable to common shareholders | $ | 0.07 | $ | (0.04) | $ | 0.09 | $ | 0.07 | |||||||||||||||

| Weighted average number of common shares outstanding – basic | 213,813 | 213,337 | 213,732 | 213,276 | |||||||||||||||||||

| Weighted average number of common shares outstanding – diluted | 214,069 | 213,337 | 214,209 | 213,276 | |||||||||||||||||||

| 2nd Quarter 2021 Supplemental Information | 2 | |||||||

Retail Properties of America, Inc.

Funds From Operations (FFO) Attributable to Common Shareholders,

Operating FFO Attributable to Common Shareholders and Additional Information

(amounts in thousands, except per share amounts)

(unaudited)

| FFO attributable to common shareholders and Operating FFO attributable to common shareholders (a) | |||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Net income (loss) attributable to common shareholders | $ | 15,396 | $ | (7,347) | $ | 20,109 | $ | 15,010 | |||||||||||||||

| Depreciation and amortization of real estate (b) | 41,508 | 43,422 | 89,048 | 83,260 | |||||||||||||||||||

| Provision for impairment of investment properties | — | — | — | 346 | |||||||||||||||||||

| FFO attributable to common shareholders | $ | 56,904 | $ | 36,075 | $ | 109,157 | $ | 98,616 | |||||||||||||||

FFO attributable to common shareholders per common share outstanding – diluted | $ | 0.27 | $ | 0.17 | $ | 0.51 | $ | 0.46 | |||||||||||||||

| FFO attributable to common shareholders | $ | 56,904 | $ | 36,075 | $ | 109,157 | $ | 98,616 | |||||||||||||||

| Impact on earnings from the early extinguishment of debt, net | — | — | 64 | — | |||||||||||||||||||

| Gain on litigation settlement | — | — | — | (6,100) | |||||||||||||||||||

| Other (c) | 5 | — | 33 | 1,011 | |||||||||||||||||||

| Operating FFO attributable to common shareholders | $ | 56,909 | $ | 36,075 | $ | 109,254 | $ | 93,527 | |||||||||||||||

Operating FFO attributable to common shareholders per common share outstanding – diluted | $ | 0.27 | $ | 0.17 | $ | 0.51 | $ | 0.44 | |||||||||||||||

| Weighted average number of common shares outstanding – diluted | 214,069 | 213,337 | 214,209 | 213,276 | |||||||||||||||||||

| Dividends declared per common share | $ | 0.075 | $ | — | $ | 0.145 | $ | 0.165625 | |||||||||||||||

| Dividends paid per common share | $ | 0.070 | $ | 0.165625 | $ | 0.130 | $ | 0.33125 | |||||||||||||||

| Additional Information (d) | |||||||||||||||||||||||

| Lease-related expenditures (e) | |||||||||||||||||||||||

| Same store | $ | 7,198 | $ | 8,426 | $ | 16,595 | $ | 19,613 | |||||||||||||||

| Other investment properties | $ | 7 | $ | 6 | $ | 7 | $ | 15 | |||||||||||||||

| Capital expenditures (f) | |||||||||||||||||||||||

| Same store | $ | 4,307 | $ | 8,476 | $ | 6,436 | $ | 14,096 | |||||||||||||||

| Other investment properties | $ | 230 | $ | 183 | $ | 397 | $ | 906 | |||||||||||||||

| Predevelopment costs | $ | 341 | $ | 202 | $ | 702 | $ | 504 | |||||||||||||||

| Straight-line rental income, net (g) | $ | 787 | $ | (1,284) | $ | 1,207 | $ | (943) | |||||||||||||||

Amortization of above and below market lease intangibles and lease inducements | $ | 462 | $ | 1,343 | $ | 1,264 | $ | 1,900 | |||||||||||||||

| Non-cash ground rent expense, net | $ | 212 | $ | 212 | $ | 424 | $ | 545 | |||||||||||||||

Adjusted EBITDAre (a) | $ | 75,978 | $ | 55,768 | $ | 147,310 | $ | 129,590 | |||||||||||||||

(a)Refer to pages 21 – 24 for definitions and reconciliations related to FFO attributable to common shareholders, Operating FFO attributable to common shareholders and Adjusted EBITDAre.

(b)Includes $7,527 of accelerated depreciation recorded in connection with the write-off of assets taken out of service due to the demolition of a retail outparcel at the Company’s Tacoma South investment property during the six months ended June 30, 2021.

(c)Primarily consists of the impact on earnings from litigation involving the Company, including costs to engage outside counsel related to litigation with former tenants, which is included within “Other income (expense), net” in the condensed consolidated statements of operations.

(d)The same store portfolio consists of 100 retail operating properties. Refer to pages 21 – 24 for definitions and reconciliations of non-GAAP financial measures.

(e)Consists of payments for tenant improvements, lease commissions and lease inducements and excludes development projects, which are included within “Developments in progress” in the condensed consolidated balance sheets.

(f)Capital expenditures consist of payments for building, site and other improvements, net of anticipated recoveries, and exclude development projects, which are included within “Developments in progress” in the condensed consolidated balance sheets. Predevelopment costs consist of payments related to future redevelopment and expansion projects incurred before each project is considered active and are included within “Other assets, net” in the condensed consolidated balance sheets.

(g)Includes changes in allowances for doubtful straight-line receivables of $484 and $(1,636) for the three months ended June 30, 2021 and 2020, respectively, and $(2,127) and $(2,671) for the six months ended June 30, 2021 and 2020, respectively, driven by the Company’s cash-basis tenant population. As of June 30, 2021, approximately 9.0% of the Company’s tenants, based on annualized base rent (ABR) of the operating portfolio, are being accounted for on the cash basis of accounting.

| 2nd Quarter 2021 Supplemental Information | 3 | |||||||

Retail Properties of America, Inc.

Supplemental Financial Statement Detail

(amounts in thousands)

(unaudited)

| Supplemental Balance Sheet Detail | June 30, 2021 | December 31, 2020 | |||||||||

| Developments in Progress | |||||||||||

| Active developments/redevelopments and Carillon (a) | $ | 157,529 | $ | 163,106 | |||||||

| Land held for future development | 25,450 | 25,450 | |||||||||

| Total | $ | 182,979 | $ | 188,556 | |||||||

| Accounts Receivable, Net | |||||||||||

| Accounts receivable, net (b) | $ | 18,232 | $ | 23,905 | |||||||

| Straight-line receivables, net | 51,262 | 50,078 | |||||||||

| Total | $ | 69,494 | $ | 73,983 | |||||||

| Other Assets, Net | |||||||||||

| Deferred costs, net | $ | 39,976 | $ | 37,965 | |||||||

| Restricted cash (c) | 3,876 | 3,544 | |||||||||

| Other assets, net | 24,121 | 30,711 | |||||||||

| Total | $ | 67,973 | $ | 72,220 | |||||||

| Other Liabilities | |||||||||||

| Unearned income | $ | 19,426 | $ | 19,077 | |||||||

| Fair value of derivatives | 22,827 | 31,666 | |||||||||

| Other liabilities | 20,601 | 21,384 | |||||||||

| Total | $ | 62,854 | $ | 72,127 | |||||||

| Supplemental Statement of Operations Detail | Three Months Ended June 30, | Six Months Ended June 30, | |||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Lease Income | |||||||||||||||||||||||

| Base rent (d) (e) (f) | $ | 87,944 | $ | 90,670 | $ | 174,018 | $ | 181,103 | |||||||||||||||

| Percentage and specialty rent (f) | 633 | 450 | 1,157 | 1,325 | |||||||||||||||||||

| Tenant recoveries (e) (f) | 24,413 | 23,823 | 50,441 | 49,565 | |||||||||||||||||||

| Lease termination fee income | 759 | 252 | 1,438 | 376 | |||||||||||||||||||

| Other lease-related income | 1,468 | 1,044 | 2,777 | 2,549 | |||||||||||||||||||

| Uncollectible lease income, net (f) (g) | 4,773 | (19,495) | 8,317 | (20,377) | |||||||||||||||||||

| Straight-line rental income, net (h) | 787 | (1,284) | 1,207 | (943) | |||||||||||||||||||

Amortization of above and below market lease intangibles and lease inducements | 462 | 1,343 | 1,264 | 1,900 | |||||||||||||||||||

| Total | $ | 121,239 | $ | 96,803 | $ | 240,619 | $ | 215,498 | |||||||||||||||

| Operating Expense Supplemental Information | |||||||||||||||||||||||

| Non-cash ground rent expense, net | $ | 212 | $ | 212 | $ | 424 | $ | 545 | |||||||||||||||

| General and Administrative Expense Supplemental Information | |||||||||||||||||||||||

| Non-cash amortization of stock-based compensation | $ | 1,970 | $ | 2,221 | $ | 4,776 | $ | 4,454 | |||||||||||||||

| Additional Supplemental Information | |||||||||||||||||||||||

| Capitalized compensation costs – development and capital projects | $ | 1,130 | $ | 970 | $ | 2,255 | $ | 1,968 | |||||||||||||||

| Capitalized internal leasing incentives | $ | 106 | $ | 42 | $ | 163 | $ | 102 | |||||||||||||||

| Capitalized interest | $ | 1,254 | $ | 736 | $ | 2,546 | $ | 1,521 | |||||||||||||||

(a)As of June 30, 2021, the Company has active redevelopments at Circle East, One Loudoun Downtown, The Shoppes at Quarterfield and Southlake Town Square. See page 9 for further details.

(b)Amount as of June 30, 2021 and December 31, 2020, includes $3,771 and $9,934, respectively, representing deferrals, both signed and agreed in principle, net of related amounts reserved.

(c)Consists of funds restricted through lender or other agreements.

(d)Refer to page 20 for novel coronavirus (COVID-19) supplemental base rent reconciliations for the three months ended June 30, 2021.

(e)Base rent and tenant recoveries are presented gross of any uncollected amounts related to cash-basis tenants. Such uncollected amounts are reflected within “Uncollectible lease income, net.”

(f)The 2020 presentation has been updated to reflect consistent presentation with 2021.

(g)Uncollectible lease income, net includes (i) the change in reserve related to receivables associated with tenants accounted for on the cash basis of accounting, (ii) the impact of executed lease concessions that did not meet deferral accounting treatment, however, were agreed in previous periods; as a result, the impact of these anticipated concessions was included within the reserve for uncollectible lease income until executed, (iii) the net change in the general reserve for those receivables that are not considered probable of collection, and (iv) the estimated impact for lease concessions that have been agreed in principle with the tenant that are not expected to meet deferral accounting treatment, however, such agreements were not executed as of period end. Refer also to page 20.

(h)Includes changes in allowances for doubtful straight-line receivables of $484 and $(1,636) for the three months ended June 30, 2021 and 2020, respectively, and $(2,127) and $(2,671) for the six months ended June 30, 2021 and 2020, respectively. As of June 30, 2021, approximately 9.0% of the Company’s tenants, based on ABR of the operating portfolio, are being accounted for on the cash basis of accounting.

| 2nd Quarter 2021 Supplemental Information | 4 | |||||||

Retail Properties of America, Inc.

Same Store Net Operating Income (NOI)

(dollar amounts in thousands)

(unaudited)

| Same store portfolio (a) | |||||||||||||||||

Based on Same store portfolio as of June 30, 2021 | |||||||||||||||||

| 2021 | 2020 | Change | |||||||||||||||

| Number of retail operating properties in same store portfolio | 100 | 100 | — | ||||||||||||||

| Occupancy | 91.8 | % | 93.6 | % | (1.8) | % | |||||||||||

| Percent leased (b) | 93.4 | % | 94.8 | % | (1.4) | % | |||||||||||

| Annualized base rent (ABR) per occupied square foot | $ | 19.48 | $ | 19.54 | (0.3) | % | |||||||||||

| Same Store NOI (c) | |||||||||||||||||||||||||||||||||||

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||||||||||||||

| 2021 | 2020 | Change | 2021 | 2020 | Change | ||||||||||||||||||||||||||||||

| Base rent (d) (e) (f) | $ | 86,107 | $ | 88,755 | $ | 170,174 | $ | 177,122 | |||||||||||||||||||||||||||

| Percentage and specialty rent (f) | 644 | 448 | 1,164 | 1,311 | |||||||||||||||||||||||||||||||

| Tenant recoveries (e) (f) | 23,713 | 23,558 | 49,636 | 48,880 | |||||||||||||||||||||||||||||||

| Other lease-related income | 1,319 | 1,050 | 2,604 | 2,518 | |||||||||||||||||||||||||||||||

| Uncollectible lease income, net (f) (g) | 4,269 | (19,344) | 8,026 | (20,179) | |||||||||||||||||||||||||||||||

| Property operating expenses (h) | (16,361) | (14,639) | (33,458) | (30,359) | |||||||||||||||||||||||||||||||

| Real estate taxes | (17,154) | (17,625) | (36,111) | (35,848) | |||||||||||||||||||||||||||||||

| Same Store NOI (c) | $ | 82,537 | $ | 62,203 | 32.7 | % | $ | 162,035 | $ | 143,445 | 13.0 | % | |||||||||||||||||||||||

(a)The Company’s same store portfolio consists of 100 retail operating properties acquired or placed in service and stabilized prior to January 1, 2020 and excludes the following:

▪properties acquired or placed in service and stabilized during 2020 and 2021;

▪the multi-family rental units at Plaza del Lago and One Loudoun Downtown – Pad G;

▪Circle East, which is in active redevelopment;

▪One Loudoun Downtown – Pads G & H, which are in active development;

▪Carillon, a redevelopment project where the Company halted plans for vertical construction during 2020 in response to macroeconomic conditions due to the impact of the COVID-19 pandemic. During the three months ended June 30, 2021, the Company announced plans to commence construction on a medical office building at Carillon in the second half of 2021;

▪The Shoppes at Quarterfield, which is in active redevelopment;

▪land held for future development;

▪investment properties that were sold or classified as held for sale during 2020 and 2021;

▪the net income from our wholly owned captive insurance company; and

▪noncontrolling interests.

(b)Includes leases signed but not commenced.

(c)Refer to pages 21 – 24 for definitions and reconciliations of non-GAAP financial measures. Comparison of the Company’s presentation of Same Store NOI to similarly titled measures for other REITs may not necessarily be meaningful due to possible differences in definition and application by such REITs.

(d)Refer to page 20 for COVID-19 supplemental same store base rent reconciliations for the three months ended June 30, 2021.

(e)Base rent and tenant recoveries are presented gross of any uncollected amounts related to cash-basis tenants. Such uncollected amounts are reflected within “Uncollectible lease income, net.”

(f)The 2020 presentation has been updated to reflect consistent presentation with 2021.

(g)Uncollectible lease income, net includes (i) the change in reserve related to receivables associated with tenants accounted for on the cash basis of accounting, (ii) the impact of executed lease concessions that did not meet deferral accounting treatment, however, were agreed in previous periods; as a result, the impact of these anticipated concessions was included within the reserve for uncollectible lease income until executed, (iii) the net change in the general reserve for those receivables that are not considered probable of collection, and (iv) the estimated impact for lease concessions that have been agreed in principle with the tenant that are not expected to meet deferral accounting treatment, however, such agreements were not executed as of period end. Refer also to page 20.

(h)Consists of all property operating items included within “Operating expenses” in the condensed consolidated statements of operations, which include all items other than (i) lease termination fee expense and (ii) non-cash ground rent expense, which is comprised of right-of-use lease assets and amortization of lease liabilities.

| 2nd Quarter 2021 Supplemental Information | 5 | |||||||

Retail Properties of America, Inc.

Capitalization

(amounts in thousands, except share price and ratio)

| Capitalization Data | |||||||||||

| June 30, 2021 | December 31, 2020 | ||||||||||

| Equity Capitalization | |||||||||||

| Common stock shares outstanding (a) | 214,798 | 214,168 | |||||||||

| Common stock share price | $ | 11.45 | $ | 8.56 | |||||||

| Total equity capitalization | $ | 2,459,437 | $ | 1,833,278 | |||||||

| Debt Capitalization | |||||||||||

| Mortgages payable (b) | $ | 90,962 | $ | 92,156 | |||||||

| Unsecured notes payable (c) | 1,200,000 | 1,200,000 | |||||||||

| Unsecured term loans (d) | 470,000 | 470,000 | |||||||||

| Unsecured revolving line of credit | — | — | |||||||||

| Total debt capitalization | $ | 1,760,962 | $ | 1,762,156 | |||||||

| Total capitalization at end of period | $ | 4,220,399 | $ | 3,595,434 | |||||||

Net income for the trailing twelve months ended June 30, 2021 was $19,661, comprised of net income (loss) of $15,387, $4,713, $1,849 and $(2,288) for the three months ended June 30, 2021, March 31, 2021, December 31, 2020 and September 30, 2020, respectively.

Calculation of Net Debt to Adjusted EBITDAre Ratio (e)

Trailing Twelve Months Ended June 30, 2021 | Three Months Ended | |||||||||||||||||||

| June 30, 2021 | December 31, 2020 | |||||||||||||||||||

| Total debt principal at period end | $ | 1,760,962 | $ | 1,760,962 | $ | 1,762,156 | ||||||||||||||

| Less: consolidated cash and cash equivalents at period end | (67,245) | (67,245) | (41,785) | |||||||||||||||||

| Total net debt at period end | $ | 1,693,717 | $ | 1,693,717 | $ | 1,720,371 | ||||||||||||||

Adjusted EBITDAre | $ | 271,936 | (f) | $ | 303,912 | (g) | $ | 243,812 | (g) | |||||||||||

Net Debt to Adjusted EBITDAre | 6.2x | (f) | 5.6x | (g) | 7.1x | (g) | ||||||||||||||

(a)Excludes performance restricted stock units and options outstanding, which could potentially convert into common stock in the future.

(b)Mortgages payable excludes mortgage discount of $(428) and $(450) and capitalized loan fees of $(160) and $(192), net of accumulated amortization, as of June 30, 2021 and December 31, 2020, respectively.

(c)Unsecured notes payable excludes discount of $(6,044) and $(6,473) and capitalized loan fees of $(6,912) and $(7,527), net of accumulated amortization, as of June 30, 2021 and December 31, 2020, respectively.

(d)Unsecured term loans exclude capitalized loan fees of $(2,105) and $(2,441), net of accumulated amortization, as of June 30, 2021 and December 31, 2020, respectively.

(e)Refer to pages 21 – 24 for definitions and reconciliations of non-GAAP financial measures.

(f)For purposes of this ratio calculation, the trailing twelve months ended EBITDAre was used.

(g)For purposes of this ratio calculation, annualized three months ended EBITDAre was used.

| 2nd Quarter 2021 Supplemental Information | 6 | |||||||

Retail Properties of America, Inc.

Covenants

| Unsecured Revolving Line of Credit, Term Loans Due 2023, 2024 and 2026 and Notes Due 2024, 2026, 2028 and 2029 (a) | ||||||||||||||

| Covenant | June 30, 2021 | |||||||||||||

| Leverage ratio (b) (c) | Unsecured revolving line of credit, Term Loans Due 2023, 2024 and 2026 and Notes Due 2026, 2028 and 2029: | ≤ 60.0% | 36.1 | % | ||||||||||

| Notes Due 2024: | ≤ 60.0% | 37.8 | % | |||||||||||

| Secured leverage ratio (b) (c) | Unsecured revolving line of credit and Term Loans Due 2023, 2024 and 2026: | ≤ 45.0% | 1.8 | % | ||||||||||

| Notes Due 2024, 2026, 2028 and 2029: | ≤ 40.0% | |||||||||||||

| Fixed charge coverage ratio (b) (d) | ≥ 1.50x | 3.6x | ||||||||||||

| Interest coverage ratio (b) (e) | ≥ 1.50x | 3.7x | ||||||||||||

| Unencumbered leverage ratio (b) (c) | ≤ 60.0% | 36.4 | % | |||||||||||

| Unencumbered interest coverage ratio (b) | ≥ 1.75x | 4.1x | ||||||||||||

| Notes Due 2025 and 2030 (f) | |||||||||||

| Covenant | June 30, 2021 | ||||||||||

| Leverage ratio (g) | ≤ 60.0% | 36.0 | % | ||||||||

| Secured leverage ratio (g) | ≤ 40.0% | 1.8 | % | ||||||||

| Debt service coverage ratio (b) (h) | ≥ 1.50x | 3.7x | |||||||||

| Unencumbered assets to unsecured debt ratio | ≥ 150% | 280 | % | ||||||||

(a)For a complete listing of all covenants related to the Company’s unsecured revolving line of credit as well as covenant definitions, refer to the Fifth Amended and Restated Credit Agreement filed as Exhibit 10.2 to the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2018, filed on May 2, 2018, the First Amendment to the Fifth Amended and Restated Credit Agreement filed as Exhibit 10.1 to the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2020, filed on May 6, 2020 and the Sixth Amended and Restated Credit Agreement that will be filed as Exhibit 10.1 to the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2021, dated August 4, 2021. For a complete listing of all covenants as well as covenant definitions related to the Company’s Term Loan Due 2023, refer to the credit agreement filed as Exhibit 10.1 to the Company’s Current Report on Form 8-K, dated November 29, 2016, the First Amendment to the Term Loan Agreement filed as Exhibit 10.4 to the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2018, filed on August 1, 2018, the Second Amendment to the Term Loan Agreement filed as Exhibit 10.10 to the Company’s Annual Report on Form 10-K for the year ended December 31, 2018, filed on February 13, 2019, and the Third Amendment to the Term Loan Agreement filed as Exhibit 10.2 to the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2020, filed on May 6, 2020. For a complete listing of all covenants as well as covenant definitions related to the Company’s Term Loan Due 2024 and Term Loan Due 2026, refer to the Term Loan Agreement filed as Exhibit 10.1 to the Company’s Current Report on Form 8-K, dated July 23, 2019, the First Amendment to the Term Loan Agreement filed as Exhibit 10.3 to the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2020, filed on May 6, 2020 and the Second Amendment to the Term Loan Agreement that will be filed as Exhibit 10.2 to the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2021, dated August 4, 2021. For a complete listing of all covenants related to the Company’s 4.58% senior unsecured notes due 2024 (Notes Due 2024) as well as covenant definitions, refer to the Note Purchase Agreement filed as Exhibit 10.1 to the Company’s Current Report on Form 8-K, dated May 22, 2014. For a complete listing of all covenants related to the Company’s 4.08% senior unsecured notes due 2026 and 4.24% senior unsecured notes due 2028 (Notes Due 2026 and 2028) as well as covenant definitions, refer to the Note Purchase Agreement filed as Exhibit 10.1 to the Company’s Current Report on Form 8-K, dated October 5, 2016. For a complete listing of all covenants related to the Company’s 4.82% senior unsecured notes due 2029 (Notes Due 2029) as well as covenant definitions, refer to the Note Purchase Agreement filed as Exhibit 10.1 to the Company’s Current Report on Form 8-K, dated April 9, 2019.

(b)Covenant calculation includes operating results, or a derivation thereof, based on the most recent four fiscal quarters of activity.

(c)Based upon a capitalization rate of 6.50% as specified in the Company’s debt agreements.

(d)Applies only to the Company’s unsecured revolving line of credit, Term Loan Due 2023, Term Loan Due 2024, Term Loan Due 2026, Notes Due 2026 and 2028 and Notes Due 2029. This ratio is based upon consolidated debt service, including interest expense and principal amortization, excluding interest expense related to defeasance costs and prepayment premiums.

(e)Applies only to the Notes Due 2024, Notes Due 2026 and 2028 and Notes Due 2029.

(f)For a complete listing of all covenants related to the Company’s 4.00% senior unsecured notes due 2025 (Notes Due 2025) as well as covenant definitions, refer to the First Supplemental Indenture filed as Exhibit 4.2 to the Company’s Current Report on Form 8-K, dated March 12, 2015, and the Second Supplemental Indenture filed as Exhibit 4.1 to the Company’s Current Report on Form 8-K, dated July 21, 2020. For a complete listing of all covenants related to the Company’s 4.75% senior unsecured notes due 2030 (Notes Due 2030) as well as covenant definitions, refer to the Third Supplemental Indenture filed as Exhibit 4.1 to the Company’s Current Report on Form 8-K, dated August 25, 2020.

(g)Based upon the book value of Total Assets as defined in the First Supplemental Indenture referenced in footnote (f) above.

(h)Based upon interest expense and excludes principal amortization. This ratio is calculated on a pro forma basis with the assumption that debt and property transactions occurred on the first day of the preceding four-quarter period.

| 2nd Quarter 2021 Supplemental Information | 7 | |||||||

Retail Properties of America, Inc.

Summary of Indebtedness as of June 30, 2021

(dollar amounts in thousands)

| Description | Balance | Interest Rate (a) | Maturity Date | WA Years to Maturity | Type | |||||||||||||||||||||||||||

| Consolidated Indebtedness | ||||||||||||||||||||||||||||||||

| Peoria Crossings | $ | 24,131 | 4.82 | % | 04/01/22 | 0.8 years | Fixed/Secured | |||||||||||||||||||||||||

| Gateway Village | 31,434 | 4.14 | % | 01/01/23 | 1.5 years | Fixed/Secured | ||||||||||||||||||||||||||

| Northgate North | 23,932 | 4.50 | % | 06/01/27 | 5.9 years | Fixed/Secured | ||||||||||||||||||||||||||

| The Shoppes at Union Hill | 11,465 | 3.75 | % | 06/01/31 | 9.9 years | Fixed/Secured | ||||||||||||||||||||||||||

| Mortgages payable (b) | 90,962 | 4.37 | % | 3.5 years | ||||||||||||||||||||||||||||

| Senior notes – 4.58% due 2024 | 150,000 | 4.58 | % | 06/30/24 | 3.0 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Senior notes – 4.00% due 2025 | 350,000 | 4.00 | % | 03/15/25 | 3.7 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Senior notes – 4.08% due 2026 | 100,000 | 4.08 | % | 09/30/26 | 5.3 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Senior notes – 4.24% due 2028 | 100,000 | 4.24 | % | 12/28/28 | 7.5 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Senior notes – 4.82% due 2029 | 100,000 | 4.82 | % | 06/28/29 | 8.0 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Senior notes – 4.75% due 2030 | 400,000 | 4.75 | % | 09/15/30 | 9.2 years | Fixed/Unsecured | ||||||||||||||||||||||||||

| Unsecured notes payable (b) | 1,200,000 | 4.42 | % | 6.3 years | ||||||||||||||||||||||||||||

| Unsecured credit facility revolving line of credit | — | 1.20 | % | (c) | 04/22/22 | (d) | 0.8 years | Variable/Unsecured | ||||||||||||||||||||||||

| Term Loan Due 2023 | 200,000 | 4.10 | % | (e) | 11/22/23 | 2.4 years | Fixed/Unsecured | |||||||||||||||||||||||||

| Term Loan Due 2024 | 120,000 | 2.88 | % | (f) | 07/17/24 | 3.0 years | Fixed/Unsecured | |||||||||||||||||||||||||

| Term Loan Due 2026 | 150,000 | 3.37 | % | (g) (h) | 07/17/26 | 5.0 years | Fixed/Unsecured | |||||||||||||||||||||||||

| Unsecured term loans (b) | 470,000 | 3.56 | % | 3.4 years | ||||||||||||||||||||||||||||

| Total consolidated indebtedness | $ | 1,760,962 | 4.19 | % | 5.4 years | |||||||||||||||||||||||||||

Consolidated Debt Maturity Schedule as of June 30, 2021 | ||||||||||||||||||||||||||||||||||||||||||||

| Year | Fixed Rate (b) | WA Rates on Fixed Debt | Variable Rate | WA Rates on Variable Debt (c) | Total | % of Total | WA Rates on Total Debt (a) | |||||||||||||||||||||||||||||||||||||

| 2021 | $ | 1,215 | 4.08 | % | $ | — | — | $ | 1,215 | 0.1 | % | 4.08 | % | |||||||||||||||||||||||||||||||

| 2022 | 26,641 | 4.81 | % | — | 1.20 | % | 26,641 | 1.5 | % | 4.81 | % | |||||||||||||||||||||||||||||||||

| 2023 | 231,758 | 4.10 | % | — | — | 231,758 | 13.2 | % | 4.10 | % | ||||||||||||||||||||||||||||||||||

| 2024 | 271,737 | 3.83 | % | — | — | 271,737 | 15.4 | % | 3.83 | % | ||||||||||||||||||||||||||||||||||

| 2025 | 351,809 | 4.00 | % | — | — | 351,809 | 20.0 | % | 4.00 | % | ||||||||||||||||||||||||||||||||||

| 2026 | 251,884 | 3.66 | % | — | — | 251,884 | 14.3 | % | 3.66 | % | ||||||||||||||||||||||||||||||||||

| 2027 | 21,410 | 4.46 | % | — | — | 21,410 | 1.2 | % | 4.46 | % | ||||||||||||||||||||||||||||||||||

| 2028 | 101,229 | 4.23 | % | — | — | 101,229 | 5.7 | % | 4.23 | % | ||||||||||||||||||||||||||||||||||

| 2029 | 101,274 | 4.81 | % | — | — | 101,274 | 5.8 | % | 4.81 | % | ||||||||||||||||||||||||||||||||||

| 2030 | 401,324 | 4.75 | % | — | — | 401,324 | 22.8 | % | 4.75 | % | ||||||||||||||||||||||||||||||||||

| Thereafter | 681 | 3.75 | % | — | — | 681 | — | % | 3.75 | % | ||||||||||||||||||||||||||||||||||

| Total | $ | 1,760,962 | 4.19 | % | $ | — | 1.20 | % | $ | 1,760,962 | 100.0 | % | 4.19 | % | ||||||||||||||||||||||||||||||

(a)Interest rates presented exclude the impact of the discount and capitalized loan fee amortization. As of June 30, 2021, the Company’s overall weighted average interest rate for consolidated debt including the impact of the discount and capitalized loan fee amortization was 4.44%.

(b)Mortgages payable excludes mortgage discount of $(428) and capitalized loan fees of $(160), net of accumulated amortization, as of June 30, 2021. Unsecured notes payable excludes discount of $(6,044) and capitalized loan fees of $(6,912), net of accumulated amortization, as of June 30, 2021. Unsecured term loans exclude capitalized loan fees of $(2,105), net of accumulated amortization, as of June 30, 2021. In the consolidated debt maturity schedule, maturity amounts for each year include scheduled principal amortization payments.

(c)Represents interest rate as of June 30, 2021, however, the revolving line of credit was not drawn as of June 30, 2021.

(d)Subsequent to June 30, 2021, the Company entered into its sixth amended and restated unsecured credit agreement that extended the maturity date of the unsecured revolving line of credit to January 8, 2026 with the option to extend for two additional six-month periods at the Company’s election, subject to (i) customary representations and warranties, including, but not limited to, the absence of an event of default as defined in the amended unsecured credit agreement and (ii) payment of an extension fee equal to 0.075% of the revolving line of credit capacity. The sixth amended and restated unsecured credit agreement also includes a sustainability metric based on targeted greenhouse gas emission reductions, which permits the Company to reduce the applicable grid-based spread by one basis point annually upon attainment.

(e)Reflects $200,000 of LIBOR-based variable rate debt that has been swapped to a fixed rate of 2.85% plus a credit spread based on a leverage grid ranging from 1.20% to 1.85% through November 22, 2023. The applicable credit spread was 1.25% as of June 30, 2021.

(f)Reflects $120,000 of LIBOR-based variable rate debt that has been swapped to a fixed rate of 1.68% plus a credit spread based on a leverage grid ranging from 1.20% to 1.70% through July 17, 2024. The applicable credit spread was 1.20% as of June 30, 2021.

(g)Reflects $150,000 of LIBOR-based variable rate debt that has been swapped to a fixed rate of 1.77% plus a credit spread based on a leverage grid ranging from 1.50% to 2.20% through July 17, 2026. The applicable credit spread was 1.60% as of June 30, 2021.

(h)Subsequent to June 30, 2021, the Company amended the pricing terms of the Term Loan Due 2026, which will bear interest at a rate of LIBOR plus a credit spread based on a leverage grid ranging from 1.20% to 1.70%. In accordance with the amended term loan agreement, the Company may elect to convert to an investment grade pricing grid. In addition, the amendment also includes the sustainability metric discussed above.

| 2nd Quarter 2021 Supplemental Information | 8 | |||||||

Retail Properties of America, Inc.

Development Projects as of June 30, 2021

(dollar amounts in thousands)

| Property Name and Metropolitan Statistical Area (MSA) | Estimated Project Commercial GLA | Estimated Project Multi-Family Rental Units (MFR) | JV / Air Rights | Estimated Net RPAI Project Investment (a) | Net RPAI Project Investment Inception to Date | Estimated Incremental Return on Investment (b) | Targeted Stabilization (c) | Property Included in Same Store Portfolio (d) | Project Description | |||||||||||||||||||||||||||||||||||||||||||||||

| Active Projects | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Circle East (e) (Baltimore MSA) | 82,000 | 370 | MFR: Air rights sale | $46,000–$48,000 | $ | 28,929 | (f) | 7.0%–8.0% | Q3–Q4 2022 | No (e) | Mixed-use redevelopment that will include dual-sided street level retail with approx. 370 third party-owned MFR above. Project is 29% leased | |||||||||||||||||||||||||||||||||||||||||||||

One Loudoun Downtown – Pads G & H (Washington, D.C. MSA) | 67,000 | 378 | MFR: 90%/10% JV | $125,000–$135,000 (g) | $ | 95,546 | (g) | 6.0%–7.0% | Q2–Q3 2022 | No (h) | Vacant pad development to densify and enhance existing mixed-use asset in Loudoun County. Pad G’s MFR is 64% leased and Pad G’s office GLA is 100% leased. See site plan on page 12 | |||||||||||||||||||||||||||||||||||||||||||||

The Shoppes at Quarterfield (Baltimore MSA) | 58,000 | — | n/a | $9,700–$10,700 | $ | 4,266 | 10.0%–11.0% | Q1–Q2 2022 (i) | No | Reconfiguration of site and building, which represents 94% of the property’s GLA. 37% of the project’s GLA was delivered to the grocer anchor in Q4 2020. Project is 100% leased | ||||||||||||||||||||||||||||||||||||||||||||||

(a)Net project investment represents the Company’s estimated share of the project costs, net of proceeds from land sales, sales of air rights, reimbursement from third parties and excludes contributions from project partners, as applicable.

(b)Estimated Incremental Return on Investment (ROI) generally reflects only the unleveraged incremental NOI generated by the project upon stabilization and is calculated as incremental NOI divided by net project investment. Incremental NOI is the difference between NOI expected to be generated by the stabilized project and the NOI generated prior to the commencement of active redevelopment, development or expansion of the space. ROI does not include peripheral impacts, such as the impact on future lease rollover at the property or the impact on the long-term value of the property.

(c)Targeted stabilization represents the projected date of the redevelopment reaching 90% occupancy, but generally no later than one year from the completion of major construction activity.

(d)The Company’s same store portfolio consists of retail operating properties acquired or placed in service and stabilized prior to January 1, 2020. A property is removed from the Company’s same store portfolio if the project is considered to significantly impact the existing property’s NOI and activities have begun in anticipation of the project. Expansions and pad developments are generally not considered to significantly impact the existing property’s NOI, and therefore, the existing properties have not been removed from the Company’s same store portfolio if they otherwise met the criteria to be included in the Company’s same store portfolio as of June 30, 2021.

(e)Circle East is the Company’s rebranded redevelopment at Towson Circle (which has been excluded from the Company’s same store portfolio due to the ongoing redevelopment).

(f)Net project investment inception to date is net of proceeds of $11,820 received in the first quarter of 2018 from the sale of air rights to a third party to develop the MFR.

(g)Project investment includes an allocation of infrastructure costs.

(h)The property is comprised of the redevelopment project (which has been excluded from the Company’s same store portfolio due to the ongoing redevelopment) and the remaining retail operating portion of the property (which is included in the Company’s same store portfolio as of June 30, 2021).

(i)During the three months ended December 31, 2020, the Company delivered the grocer anchor space to ALDI, which represents approximately 37% of the GLA under redevelopment. ALDI’s rent commenced during the fourth quarter of 2020.

The Company cannot guarantee that (i) ROI will be generated at the percentage listed or at all, (ii) total actual net investment associated with these projects will be equal to the total estimated net project investment, (iii) project commencement or stabilization will occur when anticipated or (iv) that the Company will ultimately complete any or all of these projects. The ROI and total estimated net project investment reflect the Company’s best estimate based upon current information, may change over time and are subject to certain conditions which are beyond the Company’s control, including, without limitation, general economic conditions, market conditions and other business factors.

| 2nd Quarter 2021 Supplemental Information | 9 | |||||||

Retail Properties of America, Inc.

Development Projects as of June 30, 2021 (continued)

(dollar amounts in thousands)

The Company has identified the following potential development, redevelopment, expansion and pad development opportunities to develop or redevelop significant portions of the property, add stand-alone buildings, convert previously under-utilized space or develop additional commercial GLA at existing properties. Executing on these opportunities may be subject to certain conditions that are beyond the Company’s control, including, without limitation, government approvals, tenant consents as well as general economic, market and other conditions and, therefore, the Company can provide no assurances that any of the development, redevelopment, expansion and pad development opportunities (i) will be executed on, (ii) will commence when anticipated or (iii) will ultimately be realized.

| Property Name | MSA | Included in Same store portfolio (a) | Entitled Commercial GLA (b) | Entitled MFR (b) | Developable Acreage | |||||||||||||||||||||||||||

| Future Projects – Entitled (b) | ||||||||||||||||||||||||||||||||

| One Loudoun Uptown – land held for future development | Washington, D.C. | No | 2,800,000 | 32 | ||||||||||||||||||||||||||||

| Carillon (c) | Washington, D.C. | No | 1,200,000 | 3,000 | 50 | |||||||||||||||||||||||||||

| One Loudoun Downtown – Pad T | Washington, D.C. | Yes | 40,000 | |||||||||||||||||||||||||||||

| One Loudoun Downtown – future phases (d) | Washington, D.C. | Yes | 62,000 – 95,000 | |||||||||||||||||||||||||||||

| Main Street Promenade | Chicago | Yes | 62,000 | 47 | ||||||||||||||||||||||||||||

| Downtown Crown | Washington, D.C. | Yes | 42,000 | |||||||||||||||||||||||||||||

| Reisterstown Road Plaza | Baltimore | Yes | 8,000 – 12,000 | |||||||||||||||||||||||||||||

| Gateway Plaza | Dallas | Yes | 8,000 | |||||||||||||||||||||||||||||

| Edwards Multiplex – Ontario, CA | Riverside-San Bernardino | Yes | 3,000 | |||||||||||||||||||||||||||||

| Property Name | MSA | Included in Same store portfolio (a) | Estimated Project Commercial GLA | Estimated Project MFR | ||||||||||||||||||||||

| Development, Redevelopment, Expansion and Pad Development Opportunities | ||||||||||||||||||||||||||

| Southlake Town Square | Dallas | Yes | 271,000 | |||||||||||||||||||||||

| Merrifield Town Center II (e) | Washington, D.C. | Yes | 80,000 – 100,000 | 350 – 400 | ||||||||||||||||||||||

| Tysons Corner (e) | Washington, D.C. | Yes | 50,000 – 75,000 | 350 – 450 | ||||||||||||||||||||||

| Plaza del Lago – future phase | Chicago | Yes | 20,600 | |||||||||||||||||||||||

| Lakewood Towne Center | Seattle | Yes | 10,500 | |||||||||||||||||||||||

| Humblewood Shopping Center | Houston | Yes | 5,000 | |||||||||||||||||||||||

| Watauga Pavilion | Dallas | Yes | 5,000 | |||||||||||||||||||||||

(a)See footnote (d) on page 9 regarding the Company’s same store portfolio.

(b)Project may require additional discretionary design or other approvals in certain jurisdictions.

(c)During 2020, in response to macroeconomic conditions due to the impact of the COVID-19 pandemic, the Company halted plans for vertical construction at Carillon and terminated the joint ventures related to the multi-family rental portion and the medical office building portion of phase one of the redevelopment. During the three months ended June 30, 2021, the Company announced plans to commence construction on a medical office building at Carillon in the second half of 2021.

(d)One Loudoun Downtown – future phases include three vacant parcels that have been identified as future pad development opportunities of up to 95,000 square feet of commercial GLA.

(e)Project may require demolition of a portion of the property’s existing GLA.

| 2nd Quarter 2021 Supplemental Information | 10 | |||||||

Retail Properties of America, Inc.

Development Projects as of June 30, 2021 (continued)

(dollar amounts in thousands)

| Property Name and MSA | Project Commercial GLA | Project MFR | Estimated Net RPAI Project Investment (a) | Net RPAI Project Investment Inception to Date | Estimated Incremental Return on Investment (a) | Stabilization (a) | Property Included in Same Store Portfolio (a) | Project Description | ||||||||||||||||||||||||||||||||||||||||||

| Completed Redevelopment Projects | ||||||||||||||||||||||||||||||||||||||||||||||||||

Reisterstown Road Plaza (Baltimore MSA) | 40,500 | — | $ | 10,294 | $ | 10,294 | 11.5% | Q4 2018 | Yes | Reconfigured existing space and facade renovation; redevelopment GLA is 100% leased and 100% occupied | ||||||||||||||||||||||||||||||||||||||||

Plaza del Lago – MFR (Chicago MSA) | — | 18 | $ | 1,395 | $ | 1,395 | 8.5% | Q2 2020 | No (b) | Reconfiguration of 18 MFR; major construction was completed in Q2 2019 | ||||||||||||||||||||||||||||||||||||||||

Southlake Town Square – Pad (Dallas MSA) | 4,000 | — | $2,000–$2,500 | $ | 2,154 | 12.0%–15.0% | Q3 2021 | Yes | Vacant pad development. Project is 100% leased | |||||||||||||||||||||||||||||||||||||||||

| Property Name and MSA | Project Commercial GLA | Net RPAI Investment (a) | Incremental Return on Investment (a) | Completion | Property Included in Same Store Portfolio (a) | Project Description | ||||||||||||||||||||||||||||||||

| Completed Expansions and Pad Developments | ||||||||||||||||||||||||||||||||||||||

Lake Worth Towne Crossing – Parcel (Dallas MSA) | 15,030 | $ | 2,872 | 11.3% | Q4 2015 | Yes | 15,030 sq. ft. multi-tenant retail | |||||||||||||||||||||||||||||||

Parkway Towne Crossing (Dallas MSA) | 21,000 | $ | 3,468 | 9.9% | Q3 2016 | Yes | 21,000 sq. ft. multi-tenant retail | |||||||||||||||||||||||||||||||

Heritage Square (Seattle MSA) | 4,200 | $ | 1,507 | 11.2% | Q3 2016 | Yes | 4,200 sq. ft. redevelopment of outparcel for new tenant, Corner Bakery | |||||||||||||||||||||||||||||||

Pavilion at King’s Grant (Charlotte MSA) | 32,500 | $ | 2,470 | 14.7% | Q2 2017 | Yes | 32,500 sq. ft. multi-tenant retail | |||||||||||||||||||||||||||||||

Shops at Park Place (Dallas MSA) | 25,040 | $ | 3,956 | 9.1% | Q2 2017 | Yes | 25,040 sq. ft. pad development | |||||||||||||||||||||||||||||||

Lakewood Towne Center (Seattle MSA) | 4,500 | $ | 1,900 | 7.3% | Q3 2017 | Yes | 4,500 sq. ft. pad development | |||||||||||||||||||||||||||||||

(a)See footnote (a), (b), (c) and (d) on page 9 regarding the net RPAI project investment, incremental return on investment, stabilization and same store portfolio, respectively.

(b)The property is comprised of the multi-family rental units, which were placed in service during the three months ended September 30, 2019 and are excluded from the Company’s same store portfolio, and the remaining retail operating portion of the property, which is included in the Company’s same store portfolio as of June 30, 2021.