Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT

UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(FEE REQUIRED)

For the fiscal year ended December 31, 2019

☐ TRANSACTION REPORT

UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

(NO FEE REQUIRED)

For the transaction period from ________ to ________

Commission file number 000-50385

GrowLife, Inc.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

|

90-0821083

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

|

(I.R.S.

Employer Identification No.)

|

5400 Carillon Point

Kirkland, WA 98033

(Address

of principal executive offices and zip code)

(866) 781-5559

(Registrant’s

telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the

Securities Exchange Act of 1934 during the preceding 12 months (or

for such shorter period that the registrant was required to file

such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every

Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-T (§232.405 of this chapter)

during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large

accelerated filer, an accelerated filer, a non-accelerated filer,

smaller reporting company, or an emerging growth company. See the

definitions of “large accelerated filer,”

“accelerated filer”, “smaller reporting

company”, and “emerging growth company” in Rule

12b-2

|

Large

accelerated filer

|

☐

|

Accelerated

filer

|

☐

|

|

Non-accelerated

filer (Do not check if a smaller reporting company)

|

☐

|

Smaller

reporting company

|

☒

|

|

Emerging

growth company

|

☐

|

|

|

If an emerging growth company, indicate by check mark if the

registrant has elected not to use the extended transition period

for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange

Act. ☐

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange

Act). Yes ☐ No ☒

As of June 30, 2019 (the last business day of our most recently

completed second fiscal quarter), based upon the last reported

trade on that date, the aggregate market value of the voting and

non-voting common equity held by non-affiliates (for this purpose,

all outstanding and issued common stock minus stock held by the

officers, directors and known holders of 10% or more of the

Company’s common stock) was $23,254,528.

As of

April 1, 2020, there were

29,282,602 shares of the issuer’s common stock, $0.0001 par

value per share, outstanding.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

The following discussion, in addition to the other information

contained in this report, should be considered carefully in

evaluating us and our prospects. This report (including without

limitation the following factors that may affect operating results)

contains forward-looking statements (within the meaning of Section

27A of the Securities Act of 1933, as amended ("Securities Act")

and Section 21E of the Securities Exchange Act of 1934, as amended

("Exchange Act") regarding us and our business, financial

condition, results of operations and prospects. Words such as

"expects," "anticipates," "intends," "plans," "believes," "seeks,"

"estimates" and similar expressions or variations of such words are

intended to identify forward-looking statements, but are not the

exclusive means of identifying forward-looking statements in this

report. Additionally, statements concerning future matters such as

revenue projections, projected profitability, growth strategies,

development of new products, enhancements or technologies, possible

changes in legislation and other statements regarding matters that

are not historical are forward-looking statements.

Forward-looking statements in this report reflect the good faith

judgment of our management and the statements are based on facts

and factors as we currently know them. Forward-looking statements

are subject to risks and uncertainties and actual results and

outcomes may differ materially from the results and outcomes

discussed in the forward-looking statements. Factors that could

cause or contribute to such differences in results and outcomes

include, but are not limited to, those discussed below and in

"Management's Discussion and Analysis of Financial Condition and

Results of Operations" as well as those discussed elsewhere in this

report. Readers are urged not to place undue reliance on these

forward-looking statements which speak only as of the date of this

report. We undertake no obligation to revise or update any

forward-looking statements in order to reflect any event or

circumstance that may arise after the date of this

report.

TABLE OF CONTENTS

|

|

|

Page

|

|

PART 1

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART

II

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART

III

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART

IV

|

|

|

|

|

|

|

|

|

|

|

PART I

ITEM 1. DESCRIPTION OF BUSINESS

THE COMPANY AND OUR BUSINESS

Forward-looking

statements in this report reflect the good-faith judgment of our

management, and the statements are based on facts and factors as we

currently know them. Forward-looking statements are subject to

risks, uncertainties and actual results, and outcomes may differ

materially from the results and outcomes discussed in the

forward-looking statements. Factors that could cause or contribute

to such differences in results and outcomes include, but are not

limited to, those discussed below as well as those discussed

elsewhere in this report (including in Part II, Item 1A (Risk

Factors)). Readers are urged not to place undue reliance on these

forward-looking statements because they speak only as of the date

of this report. We undertake no obligation to revise or update any

forward-looking statements in order to reflect any event or

circumstance that may arise after the date of this

report.

On

October 9, 2019, we approved the reduction of authorized capital

stock, whereby the total number of our authorized common stock

decreased from 6,000,000,000 by a ratio of 1 for 50, to 120,000,000

shares. On November 20, 2019, we filed

a Certificate of Amendment of Certificate of Incorporation with the

Secretary of State of the State of Delaware. As a result of

the reduction, we have an aggregate 130,000,000 authorized shares

consisting of : (i) 120,000,000 shares of common stock, par value

$0.0001 per share, and (ii) 10,000,000 shares of preferred stock,

par value $0.0001 per share.

The reverse stock split of 1 for 150 was effective at the open of

business on November 27, 2019 whereupon the shares of common stock

began trading on a split-adjusted basis. Our CUSIP number for our

common stock changed to 39985X203. All warrant, option, share and per

share information in this Form 10-K gives retroactive effect to the

1-for-150 reverse split with all numbers rounded up to the nearest

whole share.

THE COMPANY AND OUR BUSINESS

GrowLife,

Inc. (“GrowLife” or the “Company”) is

incorporated under the laws of the State of Delaware and is

headquartered in Kirkland, Washington. We were founded in 2012 with

the Closing of the Agreement and Plan of Merger with SGT Merger

Corporation.

FINANCIAL PERFORMANCE

First,

our 2019 revenue of $8.2 million as compared to $4.6 million for

last year ending December 31, 2018, overall grew about 80% over the

prior year.

Second,

gross profits, or revenue after our cost of sales, was reported at

$2.5 million for the year ending December 31, 2019 as compared to

last year’s $468,000, a 432% year-over-year increase. This is

attributed to the acquisition of the EZ-CLONE Enterprises Inc.

(“EZ-CLONE”) line of products, which brought in

significantly higher margins along with our continuing GrowLife

business revenue, resulting in blended gross margin of 30.2%, up

from 10.2%.

Finally,

the Company continues to generate growth by investing in its

EZ-CLONE acquisition, sales and marketing efforts and a result

reported a loss for the year ending December 31, 2019. We

believe that expansion spending is necessary in a high-growth

market such as the cannabis, hemp and CBD-related

businesses.

As of

December 31, 2019, we had closed all of our retail stores which we

had previously operated in Portland, Maine, Encino, California and

Calgary, and Canada online sales. During 2019 we also divested from

the flooring division located in Grand Prairie, Texas. As a result

of these changes, we expect to reduce losses and cash outflows by

up to $100,000 per month starting October 1, 2019. During the

quarter ended September 30, 2019, we recorded a restructuring

expense of $306,000 for the closure of the flooring division

related to the equipment write down and $250,000 for the closure of

the retail stores, related leases and online sales.

1

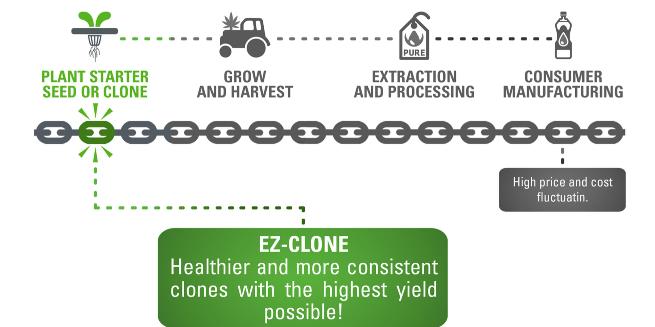

GROWLIFE’S EVOLUTION

GrowLife

is the customer’s champion, always focused on where we can

add value to their success. When we asked cultivators over the

years how we can best help them, at first it was with access to the

best products. So the Company grew, through acquisitions, to seven

retail stores and an e-commerce site with 12,000 products to reach

areas where our stores could not. Then, large-scale cultivation

operations required consultative engagements, and a direct sales

team with professional growing expertise was added. As a result,

less retail traffic led us to close many stores and turn a few into

distribution hubs. Then, the industry saw consolidation and major

price drops where cost of operations became the biggest

demand.

GrowLife

set the goal of increasing margins and revenue through an

acquisition needed to offset the low margins and reduce high debt

financing. We also began researching Cube, an initiative to lower

production costs of dry weight Cannabis Flower to $0.50 per gram

for our customers. We went from a reseller company to a technology

company, which required more capital and more acquisitions. In

2018, our gross margins were cut in half and losses grew to about

the same as our revenue.

In

2019, with the EZ-CLONE acquisition, we achieved our goals by

raising gross margins to over 30% and revenue to over $8 million.

We also reached our Cube goal of producing $0.50 per gram.

Cube’s greatest cost savings came from space management,

which led to labor, energy and waste efficiencies. We have posted

our operating manual online and are providing the materials in an

open source manner. We will sell the higher margin materials and

avoid carrying expensive Cube inventory in order to focus on our

clone business.

GROWLIFE’S FUTURE

GrowLife’s Goal

Be the nation’s leading supplier of plant clones

that grow plant-based medicines through systems, services and

partnerships.

In

2019, billions of plants were grown to serve the demand of the

plant-based medicines, more commonly referred to as the Cannabis

and CBD markets. The source of propagation, or initial planting, is

seeding or cloning (starters). The leader in cloning systems is

EZ-CLONE. The economics have favored seeds until recently where

controlling genetics, gender and yield to control the crop output,

focus on certain geographic locations equipped with tobacco

infrastructure are becoming a strategic investment.

GrowLife Mission

Measure its success by its customer’s success;

serving cultivators of all sizes as a reliable business partner and

its shareholders with value and trust.

Our

EZ-CLONE systems come in many sizes for different size customers.

We seek and partner with the best genetics and propagators in the

country. And, we make the best long-term decisions for our

shareholders to deliver value,

including maintaining management continuity to best serve them.

Promptly and diligently taking action to qualify the Company for

re-uplist back to the OTCQB from the Pink Sheets is an example of

the Company’s commitment to its shareholders.

GrowLife’s Vision

Our clones are the essential factor for our customers

now

and in the long-term in today’s Hemp CBD and tomorrow’s

Cannabinoid Industry.

In

2019, we grew greatly by supplying EZ-CLONE, our leading cloning

systems, to our cultivators across the country as we prepared to

supply Hemp CBD clones. In 2020 we plan to supply millions of

EZ-CLONEZ clones to CBD farmers. We seek to continue to deliver on

our mission with our shareholders as the CBD clone

industry grows and our

role in it.

2

WHY CLONES ARE THE GAME CHANGER

Toward

the end of 2018, we announced the majority acquisition of EZ-CLONE

Enterprises Inc. EZ-CLONE is the industry-leading supplier of

commercial-grade cloning and propagation equipment. This was a part

of this strategic positioning plank to shift from reselling other

products and control our own destiny, with locking in on an

essential component in the cultivator’s supply

chain.

Cannabis

cultivators have been cloning their favorite strains from mother

plants for decades, using various outdated conventional methods,

like tabletop growing. These methods are extremely labor and space

intensive. As the demand for cannabis and CBD-rich hemp increases

through further legalization, so will the demand for more and more

starters, whether clones or seeds. And while cloning is the

preferred method of production for many growers, cloning can be

time and labor intensive, and takes a lot of space in most grow

facilities.

In late

2017, EZ-CLONE developed its Commercial Pro System, which is one of

the largest and most efficient aeroponic cloning systems on the

market. It is commercially scalable and allows cultivators to clone

high volumes of plants in a timeframe as short as 10 days, with the

least amount of human and environmental resources consumed than

ever previously seen. These systems decrease the need for resources

such as labor and planting area, and we estimate that cultivators

reduce their costs by over 20% per plant using CLONEs vs.

seed, while simultaneously

producing the highest-quality plants possible. This system is so

unique, we recently announced a patent issuance on this system and

hope to secure further intellectual property protection on EZ-CLONE

products in the coming months and years.

In

addition to the Commercial Pro System, the EZ-CLONE product line

has systems of all sizes designed for any size grow room or

facility, consumable products such as EZ-CLONE’s Rooting

Compound, Cloning Collars, Clear Rez and other items needed to

operate these systems. Since our acquisition, we have added a

subscription-based service to provide monthly shipments to

cultivators with everything necessary to clone in our systems, as

well as struck a deal with technology company Emerald Metrics to

add multi-spectral imaging add-ons to

our Commercial Pro Systems that allow growers to see the health of

their clones through any computer or mobile device.

We

believe this illustrates how GrowLife is positioned as an innovator

of this industry-leading cloning solution, to capitalize not only

on the emerging cannabis industry but now the exploding hemp CBD

industry. Cloning in the Cannabis industry where genetics is

important can still be managed with seeds, but when it comes to CBD where genetic

and gender control dictates yield of revenue and crop regulatory

compliance is determined by exact genetic make-up, cloning becomes

essential.

WHY CLONES

To

position GrowLife as the industry leader in clones, we believe that

we need to deliver both systems and the highest quality clones in

the growing hemp and CBD industry. This puts us ahead of trends,

and to be the primary source of clones as well as propagation

machinery and consumables for the booming CBD-rich hemp

industry.

3

CBD VALUE CHAIN OPPORTUNITY

We see

the greatest opportunity for our Company in further positioning

ourselves as the industry leader in plant cloning, and more

specifically, as the leader in cloning of hemp plants grown for CBD

extraction. Hemp production was legalized in December 2018 in the

United States, subject to certain federal and state restrictions,

creating a completely new market opportunity where countless

farmers are switching their operations to hemp. Some conservative

reports estimate that more than 500 million hemp plants were

planted in 2019, with farmers looking to grow hemp to provide raw

materials to the exploding CBD market. Unfortunately, a lot of hemp

growers do not understand the intricacies of growing hemp,

especially for CBD extraction. Not all hemp plants can be used to

create CBD products. Plants need to be rich in CBD, not THC, be the

correct gender, and be healthy and large enough to process. In

order to achieve this, the only way to start plants is by using

genetically modified and feminized seeds or through

cloning.

While

there are many forecasts where the CBD industry will be billions of

dollars, there is a distinction between CBD and industrial hemp,

retail and planting, etc. We believe these forecasts can be

influenced by many factors such as the quality and availability of

certain genetics and distribution, which provides access to markets

normally not available such as the growing eco-system at this

market’s stage. We believe analysts will continue to raise

their CBD forecasts for the upcoming years, and more large

companies from the personal care and beverage industries will debut

CBD products and demand for raw hemp-based CBD will grow

accordingly.

Additionally,

we are seeing many hemp growers losing crop viability due to the

way they are starting plants. Some are losing crops to

cross-pollination and some are even being burned down by the DEA

when they have too high of levels of THC. We believe this is a

testament as to how much demand for hemp crops will continue to

grow, and growers will continue to search for the best way to grow

hemp to avoid these issues. And we see that cloning is the best way

to ensure a healthy crop with the proper CBD/THC content. We plan

to be the hemp CBD champion with our standard operating procedures

(SOP), superior genetics and large-scaled propagated clones. We

have made strides to reach hemp farmers and educate them on the

benefits of cloning, launching our resource and sales channel at

EZCLONEHemp.com, attending hemp-focused trade shows and ramping up

our sales force in hemp-heavy states, where traditional agricultural is

making the switch to hemp. We hand pick the best seeds with the

best genetics to produce the best clones.

4

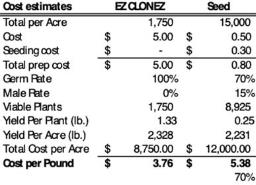

EZ-CLONEZ ECONOMICS

|

To make

a compelling case to farmers the cost of clone versus seeds must

work. The table shows an example of how an EZ-CLONEZ clone, if

priced at $5.00, would compare to a seed priced at $0.50, when

fully factored.

The

case shows a clone is 30% less than seeds. When purchased in

greater quantities, the pricing is lower and therefore savings may

be greater. Additional factors of the clones, which are not

included, that farmers can look into are greater yields and

consistency from genetics and acre density in certain climate areas

that may increase revenue for greater return.

Overall,

our EZ-CLONEZ business development consultants have over 100 years

of combined cultivation experience to assure the right clone,

genetics and SOP are provided.

|

|

SUMMARY

With

our strategic investment in EZ-CLONE, we have positioned ourselves

to capitalize on expanding market opportunity. Where EZ-CLONE was

able to create a quality product with steady growth, GrowLife has

grown it and continues to expand it with clones into the Hemp CBD

market. Whether it be system or plants, GrowLife will provide the

best clones in the market to our customers.

We

believe with the revenue growth and increased margins described,

our fundamentals are strong, our positioning is focused and our

strategy is true. To put it is simply, we are ready and prepared to

make our place in one of the largest shifts in mainstream wellness

and agriculture in history.

Employees

As of

December 31, 2019, we had twenty six full-time and part-time

employees. Marco Hegyi, our Chief Executive Officer, is based in

Kirkland, Washington. Mark E. Scott, our Chief Financial Officer,

is based primarily in Seattle, Washington. We have approximately 12

full and part time employees located throughout the United States

who operate our businesses. In addition, we employ 12 full-time and

part-time employees at EZ-CLONE in Sacramento, CA. None of our

employees are subject to a collective bargaining agreement or

represented by a trade or labor union. We believe that we have a

good relationship with our employees.

Key Partners

In

2019, we saw thousands of customers purchase through hundreds of

retailers who purchased our EZ-CLONE products from our

distributors, Hawthorne and Hydrofarm, as well as directly from us

across varying states. In 2020, we see this retail walk-in

purchasing sales strategy to serving cultivation facilities, online

selling and direct sales to continue to serve our customers across

the nation.

Our key

suppliers include manufacturers for the production of our EZ-CLONE

products. All the products purchased and resold are applicable to

indoor growing for organics, greens, and plant-based medicines. In

2020 we have a new team of genetics and propagation partners who

are facilitating the production of our EZ-CLONEZ clones in select

states.

Competition

Covering

two countries across all cultivator segments creates competitors

that also serve as partners. Large commercial cultivators have

found themselves willing to assume their own equipment support by

buying large volume, purchased

directly from certain suppliers and distributors such as Hawthorne

and Hydrofarm. Other key competitors on the retail side consist of

local and regional hydroponic resellers of indoor growing

equipment. On the e-commerce business, GrowersHouse.com,

Hydrobuilder.com and smaller online resellers using Amazon and eBay

e-commerce market systems.

In the

EZ-CLONEZ business, we expect

the seed and many small clone providers in the Hemp CBD market to

provide alternative to our products and compete with our products.

Our propagation partners have been selected to have the capacity to

serve large-scale farmers seeking to fulfill the demand for

millions of clones.

5

Intellectual Property and Proprietary Rights

Our

intellectual property consists of brands and their related

trademarks and websites, customer lists and affiliations, product

know-how and technology, and marketing intangibles.

Our

other intellectual property is primarily in the form of trademarks

and domain names. We also hold rights to several website addresses

related to our business including websites that are actively used

in our day-to-day business such as www.shopgrowlife.com,

www.growlifeinc.com,

and www.greners.com.

We have

applied for two patents related to the vertical room Cube product

previously discussed.

We have

a policy of entering into confidentiality and non-disclosure

agreements with our employees, some of our vendors and customers as

necessary.

On

October 15, 2018, we closed the Purchase and Sale Agreement with

EZ-CLONE Enterprises, Inc., a California corporation. EZ-CLONE is

the manufacturer of

multiple award-winning products specifically designed for the

commercial cloning and propagation stage of indoor plant

cultivation including cannabis, food, and other hydroponic farming.

The total purchase price was $4 million of which $1,500,000 is

payable in cash and $2.5 million payable in stock. At closing, we

paid 51% of this amount totaling $2,040,000 via a (i) a cash

payment of $645,000; and (ii) the issuance of 715,385 restricted

shares of our common stock valued $1,395,000.

The

October 15, 2018 agreement called for the Company, upon delivery of

the remaining 49% of EZ Clone stock, to acquire such stock within

one year for $1,960,000, payable as follows: (i) a cash payment of

$855,000; and (ii) the issuance of Company’s common stock at

a value of $1,105,000. On November 5, 2019, we amended the purchase

agreement with one 24.5% owner obligating the Company to purchase

the remaining 49% of stock by agreeing to a 20% extension fee

($171,000) of the $855,000 cash payable at the earlier of the

closing of $2,000,000 in funding or nine months (July 2020). As of

December 31, 2019, the $171,000 extension fee has not been paid and

we continue in discussion with the shareholders about paying of the

remaining purchase price payable.

Government Regulation

Currently,

there are thirty three states plus the District of Columbia that

have laws and/or regulation that recognize in one form or another

legitimate medical uses for cannabis and consumer use of cannabis

in connection with medical treatment. There are currently ten

states and the District of Columbia that allow recreational use of

cannabis. As of December 31, 2019, the policy and regulations of

the Federal government and its agencies is that cannabis has no

medical benefit and a range of activities including cultivation and

use of cannabis for personal use is prohibited on the basis of

federal law and may or may not be permitted on the basis of state

law. Active enforcement of the current federal regulatory position

on cannabis on a regional or national basis may directly and

adversely affect the willingness of customers of GrowLife to invest

in or buy products from GrowLife. Active enforcement of the current

federal regulatory position on cannabis may thus indirectly and

adversely affect revenues and profits of the GrowLife

companies.

All

this being said, many reports show that the majority of the

American public is in favor of making medical cannabis available as

a controlled substance to those patients who need it. The need and

consumption will then require cultivators to continue to provide

safe and compliant crops to consumers. The cultivators will then

need to build facilities and use consumable products, which

GrowLife provides.

6

OUR COMMON STOCK

On

October 17, 2017, we were informed by Alpine Securities Corporation

(“Alpine”) that Alpine has demonstrated compliance with

the Financial Industry Regulatory Authority (“FINRA”)

Rule 6432 and Rule 15c2-11 under the Securities Exchange Act of

1934. We filed an amended application with the OTC Markets to list

the Company’s common stock on the OTCQB and begin to trade on

this market as of March 20, 2018. As

of March 4, 2019, we began to trade on the Pink Sheet stocks

system. Our bid price had

closed below $0.01 for more than 30 consecutive calendar

days. As of March 17, 2020, we commenced trading on the

OTCQB Market ("OTCQB") after successfully up-listing from the OTC

Pink Market.

PRIMARY RISKS AND UNCERTAINTIES

We are

exposed to various risks related to legal proceedings, our need for

additional financing, the sale of significant numbers of our

shares, the potential adjustment in the exercise price of our

convertible debentures and a volatile market price for our common

stock. These risks and uncertainties are discussed in more detail

below in Part I, Item 1A.

WEBSITE ACCESS TO UNITED STATES SECURITIES AND EXCHANGE COMMISSION

REPORTS

We file annual and quarterly reports, proxy statements and other

information with the Securities and Exchange Commission ("SEC").

You may read and copy any document we file at the SEC's Public

Reference Room at 100 F Street, N.E., Washington D.C. 20549. Please

call the SEC at 1-800-SEC-0330 for further information on the

public reference room. The SEC maintains a website at

http://www.sec.gov that contains reports, proxy and information

statements and other information concerning filers. We also

maintain a web site at http://www.growlifeinc.com that provides

additional information about our Company and links to documents we

file with the SEC. The Company's charters for the Audit Committee,

the Compensation Committee, and the Nominating Committee; and the

Code of Conduct & Ethics are also available on our website. The

information on our website is not part of this Form

10-K.

ITEM 1A. RISK FACTORS

There are certain inherent risks which will have an effect on our

development in the future and the most significant risks and

uncertainties known and identified by our management are described

below.

Risks

Related to Pandemics

The effects of the recent COVID-19 coronavirus pandemic are not

immediately known, but may adversely affect our business, results

of operations, financial condition, liquidity, and cash

flow.

Presently,

the impact of COVID-19 has not shown any imminent adverse effects

on our business, especially since states across the United

States—including California—has deemed cannabis

businesses as “essential,” allowing our business to

continue its operations. This notwithstanding, it is still unknown

and difficult to predict what adverse effects, if any, COVID-19 can

have on our business, or against the various aspects of

same.

As of

the date of this Annual Report, COVID-19 coronavirus has been

declared a pandemic by the World Health Organization, has been

declared a National Emergency by the United States Government and

has resulted in several states being designated disaster zones.

COVID-19 coronavirus caused significant volatility in global

markets. The spread of COVID-19 coronavirus has caused public

health officials to recommend precautions to mitigate the spread of

the virus, especially as to travel and congregating in large

numbers. In addition, certain states and municipalities have

enacted, and additional cities are considering, quarantining and

“shelter-in-place” regulations which severely limit the

ability of people to move and travel and require non-essential

businesses and organizations to close.

It is

unclear how such restrictions, which will contribute to a general

slowdown in the global economy, will affect our business, results

of operations, financial condition and our future strategic

plans.

Recent

shelter-in-place and essential-only travel regulations could

negatively impact our customers. In addition, while our products

are manufactured in the United States, we still could experience

significant supply chain disruptions due to interruptions in

operations at any or all of our suppliers’ facilities or

downline suppliers. If we experience significant delays in

receiving our products we will experience delays in fulfilling

orders and ultimately receiving payment, which could result in loss

of sales and a loss of customers, and adversely impact our

financial condition and results of operations. The current status

of COVID-19 coronavirus closures and restrictions could also

negatively impact our ability to receive funding from our existing

capital sources as each business is and has been affected

uniquely.

In

addition, our headquarters are located in Kirkland, Washington

which was also recently subject of large COVID-19 outbreak. In

response, Washington State governor, Jay Inslee, mandated a minimum

2 week stay at home order with exceptions only for essential

businesses. While these restrictions are relatively recent as of

the date of this Annual Report, it is unclear at this time how

these restrictions will be amended as the pandemic evolves. We

believe that since we are an essential business, we are hopeful

that COVID-19 closures will have only a limited effect on our

operations and revenues.

7

Risks Related to Securities Markets and Investments in Our

Securities

General securities market uncertainties resulting from the COVID-19

pandemic.

Since

the outset of the pandemic the United States and worldwide national

securities markets have undergone unprecedented stress due to the

uncertainties of the pandemic and the resulting reactions and

outcomes of government, business and the general population. These

uncertainties have resulted in declines in all market sectors,

increases in volumes due to flight to safety and governmental

actions to support the markets. As a result, until the pandemic has

stabilized, the markets may not be available to the Company for

purposes of raising required capital. Should we not be able

to obtain financing when required, in the amounts necessary to

execute on our plans in full, or on terms which are economically

feasible we may be unable to sustain the necessary capital to

pursue our strategic plan and may have to reduce the planned future

growth and/or scope of our operations.

Risks Related to Our Business

Risks Associated with Securities Purchase Agreements with

Chicago Venture Partners, L.P.

(“Chicago Venture”), Iliad Research and Trading,

L.P. (“Iliad”) and Odyssey Research and Trading, LLC,

(“Odyssey”).

The

Securities Purchase Agreements with Chicago Venture, Illiad and

Odyssey will terminate if we file protection from its creditors, a

Registration Statement on Form S-1 is not effective, and our market

capitalization or the trading volume of our common stock does not

reach certain levels. If terminated, we will be unable to draw down

all or substantially all of Notes.

Our

ability to require Chicago Venture, Illiad and Odyssey to fund the

Notes is at mutual discretion, subject to certain limitations.

Chicago Venture, Illiad and Odyssey are obligated to fund if each

of the following conditions are met; (i) the average and median

daily dollar volumes of our common stock for the twenty (20) and

sixty (60) trading days immediately preceding the funding date are

greater than $100,000; (ii) our market capitalization on the

funding date is greater than $17,000,000; (iii) we are not in

default with respect to share delivery obligations under the note

as of the funding date; and (iv) we are current in our reporting

obligations.

There

is no guarantee that we will be able to meet the foregoing

conditions or any other conditions under the Securities Purchase

Agreements and/or Notes or that we will be able to draw down any

portion of the amounts available under the Securities Purchase

Agreements and/or Notes.

If we

not able to draw down all amounts possible under the Securities

Purchase Agreements or if the Securities Purchase Agreements are

terminated, we may be forced to curtail the scope of our operations

or alter our business plan if other financing is not available to

us.

Risks Associated with EZ-CLONE Enterprises, Inc.

On

October 15, 2018, we closed the Purchase and Sale Agreement with

EZ-CLONE. EZ-CLONE is the

manufacturer of multiple award-winning products specifically

designed for the commercial cloning and propagation stage of indoor

plant cultivation including cannabis, food, and other hydroponic

farming. The total purchase price was $4 million of which

$1,500,000 is payable in cash and $2.5 million payable in stock. At

closing, we paid 51% of this amount totaling $2,040,000 via

a (i) a cash payment of $645,000; and (ii) the issuance of 715,385

restricted shares of our common stock valued

$1,395,000.

The

October 15, 2018 agreement called for the Company, upon delivery of

the remaining 49% of EZ Clone stock, to acquire such stock within

one year for $1,960,000, payable as follows: (i) a cash payment of

$855,000; and (ii) the issuance of Company’s common stock at

a value of $1,105,000. On November 5, 2019, we amended the purchase

agreement with one 24.5% owner obligating the Company to purchase

the remaining 49% of stock by agreeing to a 20% extension fee

($171,000) of the $855,000 cash payable at the earlier of the

closing of $2,000,000 in funding or nine months (July 2020). As of

December 31, 2019, the $171,000 extension fee has not been paid and

we continue in discussion with the shareholders about paying of the

remaining purchase price payable.

Our acquisition of EZ-Clone thus far has been positive for our

overall results of operations. Additionally, we have spent a

significant amount of time and effort modifying our business plans

and focuses toward the clone industry. If we fail to close on the

remaining 49% of EZ-Clone we may experience direct consequences

including, but not limited to, claims for breach of contract for

failure to close on a contractual obligation.

8

Our common stock.

On

October 17, 2017, we were informed by Alpine Securities Corporation

(“Alpine”) that Alpine has demonstrated compliance with

the Financial Industry Regulatory Authority (“FINRA”)

Rule 6432 and Rule 15c2-11 under the Securities Exchange Act of

1934. We filed an amended application with the OTC Markets to list

the Company’s common stock on the OTCQB and begin to trade on

this market as of March 20, 2018. As

of March 4, 2019, we began to trade on the OTC Pink Sheet stocks

system because our bid price

had closed below $0.01 for more than 30 consecutive calendar

days. As of March 17, 2020, we commenced trading on the

OTCQB Market ("OTCQB") after successfully up-listing from the OTC

Pink Market.

This

action had a material adverse effect on our business, financial

condition and results of operations. If we are unable to obtain

additional financing when it is needed, we will need to restructure

our operations, and divest all or a portion of our

business.

We have been involved in Legal Proceedings.

We have

been involved in certain disputes and legal proceedings as

discussed in the section title “Legal Proceedings”. In

addition, as a public company, we are also potentially susceptible

to litigation, such as claims asserting violations of securities

laws. Any such claims, with or without merit, if not resolved,

could be time-consuming and result in costly litigation. There can

be no assurance that an adverse result in any future proceeding

would not have a potentially material adverse on our business,

results of operations or financial condition.

We may engage in acquisitions, mergers, strategic alliances, joint

ventures and divestures that could result in final results that are

different than expected.

In the normal course of business, we engage in discussions relating

to possible acquisitions, equity investments, mergers, strategic

alliances, joint ventures and divestitures. Such transactions are

accompanied by a number of risks, including the use of significant

amounts of cash, potentially dilutive issuances of equity

securities, incurrence of

debt on potentially unfavorable terms as well as impairment

expenses related to goodwill and amortization expenses related to

other intangible assets, the possibility that we may pay too much

cash or issue too many of our shares as the purchase price for an

acquisition relative to the economic benefits that we ultimately

derive from such acquisition, and various potential difficulties

involved in integrating acquired businesses into our

operations.

From time to time, we have also engaged in discussions with

candidates regarding the potential acquisitions of our product

lines, technologies and businesses. If a divestiture such as this

does occur, we cannot be certain that our business, operating

results and financial condition will not be materially and

adversely affected. A successful divestiture depends on various

factors, including our ability to effectively transfer liabilities,

contracts, facilities and employees to any purchaser; identify and

separate the intellectual property to be divested from the

intellectual property that we wish to retain; reduce fixed costs

previously associated with the divested assets or business; and

collect the proceeds from any divestitures.

If we do not realize the expected benefits of any acquisition or

divestiture transaction, our financial position, results of

operations, cash flows and stock price could be negatively

impacted.

Our proposed business is dependent on laws pertaining to the

marijuana industry.

Continued

development of the marijuana industry is dependent upon continued

legislative authorization of the use and cultivation of marijuana

at the state level. Any number of factors could slow or

halt progress in this area. Further, progress, while

encouraging, is not assured. While there may be ample

public support for legislative action, numerous factors impact

the legislative process. Any one of these factors could

slow or halt use of marijuana, which would negatively impact our

proposed business.

Currently,

thirty three states and the District of Columbia allow its citizens

to use medical cannabis. Additionally, ten states and

the District of Columbia have legalized cannabis for adult

use. The state laws are in conflict with the federal

Controlled Substances Act, which makes marijuana use and possession

illegal on a national level. The Obama administration previously

effectively stated that it is not an efficient use of resources to

direct law federal law enforcement agencies to prosecute those

lawfully abiding by state-designated laws allowing the use and

distribution of medical marijuana. The Trump

administration position is unknown. However, there is no

guarantee that the Trump administration will not change current

policy regarding the low-priority enforcement of federal

laws. Additionally, any new administration that follows

could change this policy and decide to enforce the federal laws

strongly. Any such change in the federal

government’s enforcement of current federal laws could cause

significant financial damage to us and its

shareholders.

Further,

while we do not harvest, distribute or sell marijuana, by supplying

products to growers of marijuana, we could be deemed to be

participating in marijuana cultivation, which remains illegal under

federal law, and exposes us to potential criminal liability, with

the additional risk that our business could be subject to civil

forfeiture proceedings.

The marijuana industry faces strong opposition.

It is

believed by many that large, well-funded businesses may have a

strong economic opposition to the marijuana industry. We

believe that the pharmaceutical industry clearly does not want to

cede control of any product that could generate significant

revenue. For example, medical marijuana will likely

adversely impact the existing market for the current

“marijuana pill” sold by mainstream pharmaceutical

companies. Further, the medical marijuana industry could

face a material threat from the pharmaceutical industry, should

marijuana displace other drugs or encroach upon the pharmaceutical

industry’s products. The pharmaceutical industry

is well funded with a strong and experienced lobby that eclipses

the funding of the medical marijuana movement. Any

inroads the pharmaceutical industry could make in halting or

impeding the marijuana industry harm our business, prospects,

results of operation and financial condition.

9

Marijuana remains illegal under Federal

law.

Marijuana

is a Schedule-I controlled substance and is illegal under federal

law. Even in those states in which the use of marijuana

has been legalized, its use remains a violation of federal

law. Since federal law criminalizing the use of

marijuana preempts state laws that legalize its use, strict

enforcement of federal law regarding marijuana would harm our

business, prospects, results of operation and financial

condition.

Raising additional capital to implement our business plan and pay

our debts will cause dilution to our existing stockholders, require

us to restructure our operations, and divest all or a portion of

our business.

We need

additional financing to implement our business plan and to service

our ongoing operations and pay our current debts. There can be no

assurance that we will be able to secure any needed funding, or

that if such funding is available, the terms or conditions would be

acceptable to us.

If we

raise additional capital through borrowing or other debt financing,

we may incur substantial interest expense. Sales of additional

equity securities will dilute on a pro rata basis the percentage

ownership of all holders of common stock. When we raise more equity

capital in the future, it will result in substantial dilution to

our current stockholders.

If we

are unable to obtain additional financing when it is needed, we

will need to restructure our operations, and divest all or a

portion of our business.

Closing of bank and merchant processing accounts could have a

material adverse effect on our business, financial condition and/or

results of operations.

As a

result of the regulatory environment, we have experienced the

closing of several of our bank and merchant processing accounts

since March 2014. We have been able to open other bank accounts.

However, we may have other banking accounts closed. These factors

impact management and could have a material adverse effect on our

business, financial condition and/or results of

operations.

Federal regulation and enforcement may adversely affect the

implementation of medical marijuana laws and regulations may

negatively impact our revenues and profits.

Currently,

there are thirty three states plus the District of Columbia that

have laws and/or regulation that recognize in one form or another

legitimate medical uses for cannabis and consumer use of cannabis

in connection with medical treatment. Many other states are

considering legislation to similar effect. As of the date of this

writing, the policy and regulations of the Federal government and

its agencies is that cannabis has no medical benefit and a range of

activities including cultivation and use of cannabis for personal

use is prohibited on the basis of federal law and may or may not be

permitted on the basis of state law. Active enforcement of the

current federal regulatory position on cannabis on a regional or

national basis may directly and adversely affect the willingness of

customers of GrowLife to invest in or buy products from GrowLife

that may be used in connection with cannabis. Active enforcement of

the current federal regulatory position on cannabis may thus

indirectly and adversely affect revenues and profits of the

GrowLife companies.

Our history of net losses has raised substantial doubt regarding

our ability to continue as a going concern. If we do not continue

as a going concern, investors could lose their entire

investment.

Our

history of net losses has raised substantial doubt about our

ability to continue as a going concern, and as a result, our

independent registered public accounting firm included an

explanatory paragraph in its report on our financial statements as

of and for the years ended December 31, 2019 and 2018 with

respect to this uncertainty. Accordingly, our ability to continue

as a going concern will require us to seek alternative financing to

fund our operations. This going concern opinion could materially

limit our ability to raise additional funds through the issuance of

new debt or equity securities or otherwise. Future reports on our

financial statements may include an explanatory paragraph with

respect to our ability to continue as a going concern.

We have a history of operating losses and there can be no assurance

that we can again achieve or maintain profitability.

We have

experienced net losses since inception. As of December 31, 2019, we

had an accumulated deficit of $148.5 million. There can be no assurance

that we will achieve or maintain profitability.

10

We are subject to corporate governance and internal control

reporting requirements, and our costs related to compliance with,

or our failure to comply with existing and future requirements,

could adversely affect our business.

We must

comply with corporate governance requirements under the

Sarbanes-Oxley Act of 2002 and the Dodd–Frank Wall Street

Reform and Consumer Protection Act of 2010, as well as additional

rules and regulations currently in place and that may be

subsequently adopted by the SEC and the Public Company Accounting

Oversight Board. These laws, rules, and regulations continue to

evolve and may become increasingly stringent in the future. We are

required to include management’s report on internal controls

as part of our annual report pursuant to Section 404 of the

Sarbanes-Oxley Act. We strive to continuously evaluate and improve

our control structure to help ensure that we comply with Section

404 of the Sarbanes-Oxley Act. The financial cost of compliance

with these laws, rules, and regulations is expected to remain

substantial.

We

cannot assure you that we will be able to fully comply with these

laws, rules, and regulations that address corporate governance,

internal control reporting, and similar matters. Failure to comply

with these laws, rules and regulations could materially adversely

affect our reputation, financial condition, and the value of our

securities.

Our inability or failure to effectively manage our growth could

harm our business and materially and adversely affect our operating

results and financial condition.

Our

strategy envisions growing our business. We plan to expand our

product, sales, administrative and marketing organizations. Any

growth in or expansion of our business is likely to continue to

place a strain on our management and administrative resources,

infrastructure and systems. As with other growing businesses, we

expect that we will need to further refine and expand our business

development capabilities, our systems and processes and our access

to financing sources. We also will need to hire, train, supervise

and manage new and retain contributing employees. These processes

are time consuming and expensive, will increase management

responsibilities and will divert management attention. We cannot

assure you that we will be able to:

|

|

●

|

expand

our products effectively or efficiently or in a timely

manner;

|

|

|

●

|

allocate

our human resources optimally;

|

|

|

●

|

meet

our capital needs;

|

|

|

●

|

identify

and hire qualified employees or retain valued employees;

or

|

|

|

●

|

incorporate

effectively the components of any business or product line that we

may acquire in our effort to achieve growth.

|

Our

operating results may fluctuate significantly based on customer

acceptance of our products. As a result, period-to-period

comparisons of our results of operations are unlikely to provide a

good indication of our future performance. Management expects that

we will experience substantial variations in our net sales and

operating results from quarter to quarter due to customer

acceptance of our products. If customers don’t accept our

products, our sales and revenues will decline, resulting in a

reduction in our operating income.

Customer

interest for our products could also be impacted by the timing of

our introduction of new products. If our competitors introduce new

products around the same time that we issue new products, and if

such competing products are superior to our own, customers’

desire for our products could decrease, resulting in a decrease in

our sales and revenues. To the extent that we introduce new

products and customers decide not to migrate to our new products

from our older products, our revenues could be negatively impacted

due to the loss of revenue from those customers. In the event that

our newer products do not sell as well as our older products, we

could also experience a reduction in our revenues and operating

income.

If we do not successfully generate additional products and

services, or if such products and services are developed but not

successfully commercialized, we could lose revenue

opportunities.

Our

future success depends, in part, on our ability to expand our

product and service offerings. To that end we have engaged in the

process of identifying new product opportunities to provide

additional products and related services to our customers. The

process of identifying and commercializing new products is complex

and uncertain, and if we fail to accurately predict

customers’ changing needs and emerging technological trends

our business could be harmed. We may have to commit significant

resources to commercializing new products before knowing whether

our investments will result in products the market will accept.

Furthermore, we may not execute successfully on commercializing

those products because of errors in product planning or timing,

technical hurdles that we fail to overcome in a timely fashion, or

a lack of appropriate resources. This could result in competitors

providing those solutions before we do and a reduction in net sales

and earnings.

The

success of new products depends on several factors, including

proper new product definition, timely completion and introduction

of these products, differentiation of new products from those of

our competitors, and market acceptance of these products. There can

be no assurance that we will successfully identify new product

opportunities, develop and bring new products to market in a timely

manner, or achieve market acceptance of our products or that

products and technologies developed by others will not render our

products or technologies obsolete or noncompetitive.

11

Our future success depends on our ability to grow and expand our

customer base. Our failure to achieve such growth or

expansion could materially harm our business.

To

date, our revenue growth has been derived primarily from the sale

of our products and through the purchase of existing businesses.

Our success and the planned growth and expansion of our business

depend on us achieving greater and broader acceptance of our

products and expanding our customer base. There can be no assurance

that customers will purchase our products or that we will continue

to expand our customer base. If we are unable to effectively market

or expand our product offerings, we will be unable to grow and

expand our business or implement our business strategy. This could

materially impair our ability to increase sales and revenue and

materially and adversely affect our margins, which could harm our

business and cause our stock price to decline.

If we

incur substantial liability from litigation, complaints, or

enforcement actions resulting from misconduct by our distributors,

our financial condition could suffer. We will require that our

distributors comply with applicable law and with our policies and

procedures. Although we will use various means to address

misconduct by our distributors, including maintaining these

policies and procedures to govern the conduct of our distributors

and conducting training seminars, it will still be difficult to

detect and correct all instances of misconduct. Violations of

applicable law or our policies and procedures by our distributors

could lead to litigation, formal or informal complaints,

enforcement actions, and inquiries by various federal, state, or

foreign regulatory authorities against us and/or our distributors.

and could consume considerable amounts of financial and other

corporate resources, which could have a negative impact on our

sales, revenue, profitability and growth prospects. As we are

currently in the process of implementing our direct sales

distributor program, we have not been, and are not currently,

subject to any material litigation, complaint or enforcement action

regarding distributor misconduct by any federal, state or foreign

regulatory authority.

Our

future manufacturers could fail to fulfill our orders for products,

which would disrupt our business, increase our costs, harm our

reputation and potentially cause us to lose our

market.

We may

depend on contract manufacturers in the future to produce our

products. These manufacturers could fail to produce products to our

specifications or in a workmanlike manner and may not deliver the

units on a timely basis. Our manufacturers may also have to obtain

inventories of the necessary parts and tools for production. Any

change in manufacturers to resolve production issues could disrupt

our ability to fulfill orders. Any change in manufacturers to

resolve production issues could also disrupt our business due to

delays in finding new manufacturers, providing specifications and

testing initial production. Such disruptions in our business and/or

delays in fulfilling orders would harm our reputation and would

potentially cause us to lose our market.

Our inability to effectively protect our intellectual property

would adversely affect our ability to compete effectively, our

revenue, our financial condition and our results of

operations.

We may

be unable to obtain intellectual property rights to effectively

protect our business. Our ability to compete effectively may be

affected by the nature and breadth of our intellectual property

rights. While we intend to defend against any threats to our

intellectual property rights, there can be no assurance that any

such actions will adequately protect our interests. If we are

unable to secure intellectual property rights to effectively

protect our technology, our revenue and earnings, financial

condition, and/or results of operations would be adversely

affected.

We may

also rely on nondisclosure and non-competition agreements to

protect portions of our technology. There can be no assurance that

these agreements will not be breached, that we will have adequate

remedies for any breach, that third parties will not otherwise gain

access to our trade secrets or proprietary knowledge, or that third

parties will not independently develop the technology.

We do

not warrant any opinion as to non-infringement of any patent,

trademark, or copyright by us or any of our affiliates, providers,

or distributors. Nor do we warrant any opinion as to invalidity of

any third-party patent or unpatentability of any third-party

pending patent application.

Our industry is highly competitive and we have less capital and

resources than many of our competitors, which may give them an

advantage in developing and marketing products similar to ours or

make our products obsolete.

We are

involved in a highly competitive industry where we may compete with

numerous other companies who offer alternative methods or

approaches, may have far greater resources, more experience, and

personnel perhaps more qualified than we do. Such resources may

give our competitors an advantage in developing and marketing

products similar to ours or products that make our products

obsolete. There can be no assurance that we will be able to

successfully compete against these other entities.

Transfers of our securities may be restricted by virtue of state

securities “blue sky” laws, which prohibit trading

absent compliance with individual state laws. These restrictions

may make it difficult or impossible to sell shares in those

states.

Transfers

of our common stock may be restricted under the securities or

securities regulations laws promulgated by various states and

foreign jurisdictions, commonly referred to as "blue sky" laws.

Absent compliance with such individual state laws, our common stock

may not be traded in such jurisdictions. Because the securities

held by many of our stockholders have not been registered for

resale under the blue sky laws of any state, the holders of such

shares and persons who desire to purchase them should be aware that

there may be significant state blue sky law restrictions upon the

ability of investors to sell the securities and of purchasers to

purchase the securities. These restrictions may prohibit the

secondary trading of our common stock. Investors should consider

the secondary market for our securities to be a limited

one.

12

We are dependent on key personnel.

Our

success depends to a significant degree upon the continued

contributions of key management and other personnel, some of whom

could be difficult to replace. We do not maintain key man life

insurance covering our officers. Our success will depend on the

performance of our officers and key management and other personnel,

our ability to retain and motivate our officers, our ability to

integrate new officers and key management and other personnel into

our operations, and the ability of all personnel to work together

effectively as a team. Our failure to retain and recruit

officers and other key personnel could have a material adverse

effect on our business, financial condition and results of

operations.

We have limited insurance.

We have

no directors’ and officers’ liability insurance and

limited commercial liability insurance policies. Any significant

claims would have a material adverse effect on our business,

financial condition and results of

operations.

Risks Related to our Common Stock

Chicago Venture, Illiad and Odyssey could have significant

influence over matters submitted to stockholders for

approval.

As a

result of funding from Chicago Venture, Iliad and Odyssey as

previously detailed, they exercise significant control over

us.

While

there are limits on the ownership by each party, ff these companies

were to choose to act together, they would be able to significantly

influence all matters submitted to our stockholders for approval,

as well as our officers, directors, management and affairs. For

example, these companies, if they choose to act together, could

significantly influence the election of directors and approval of

any merger, consolidation or sale of all or substantially all of

our assets. This concentration of voting power could delay or

prevent an acquisition of us on terms that other stockholders may

desire.

Trading in our stock is limited by the SEC’s penny stock

regulations.

Our

stock is categorized as a penny stock. The SEC has adopted Rule

15g-9 which generally defines "penny stock" to be any equity

security that has a market price (as defined) less than US$ 5.00

per share or an exercise price of less than US $5.00 per share,

subject to certain exclusions (e.g., net tangible assets in excess

of $2,000,000 or average revenue of at least $6,000,000 for the

last three years). The penny stock rules impose additional sales

practice requirements on broker-dealers who sell to persons other

than established customers and accredited investors. The penny

stock rules require a broker-dealer, prior to a transaction in a

penny stock not otherwise exempt from the rules, to deliver a

standardized risk disclosure document in a form prepared by the

SEC, which provides information about penny stocks and the nature

and level of risks in the penny stock market. The broker-dealer

also must provide the customer with current bid and offer

quotations for the penny stock, the compensation of the

broker-dealer and its salesperson in the transaction, and monthly

account statements showing the market value of each penny stock

held in the customer's account. The bid and offer quotations, and

the broker-dealer and salesperson compensation information, must be

given to the customer orally or in writing prior to effecting the

transaction and must be given to the customer in writing before or

with the customer's confirmation. In addition, the penny stock

rules require that prior to a transaction in a penny stock not

otherwise exempt from these rules, the broker-dealer must make a

special written determination that the penny stock is a suitable

investment for the purchaser and receive the purchaser's written

agreement to the transaction. Finally, broker-dealers may not

handle penny stocks under $0.10 per share.

These

disclosure requirements reduce the level of trading activity in the

secondary market for the stock that is subject to these penny stock

rules. Consequently, these penny stock rules would affect the

ability of broker-dealers to trade our securities if we become

subject to them in the future. The penny stock rules also could

discourage investor interest in and limit the marketability of our

common stock to future investors, resulting in limited ability for

investors to sell their shares.

FINRA sales practice requirements may also limit a

shareholder’s ability to buy and sell our stock.

In

addition to the “penny stock” rules described above,

FINRA has adopted rules that require that in recommending an

investment to a customer, a broker-dealer must have reasonable

grounds for believing that the investment is suitable for that

customer. Prior to recommending speculative low priced securities

to their non-institutional customers, broker-dealers must make

reasonable efforts to obtain information about the customer’s

financial status, tax status, investment objectives and other

information. Under interpretations of these rules, FINRA believes

that there is a high probability that speculative low priced

securities will not be suitable for at least some customers. The

FINRA requirements make it more difficult for broker-dealers to

recommend that their customers buy our common stock, which may

limit your ability to buy and sell our stock and have an adverse

effect on the market for our shares.

13

The market price of our common stock may be volatile.

The

market price of our common stock has been and is likely in the

future to be volatile. Our common stock price may fluctuate in

response to factors such as:

|

●

|

Halting of trading by the SEC or FINRA.

|

|

●

|

Announcements

by us regarding liquidity, legal proceedings, significant

acquisitions, equity investments and divestitures, strategic

relationships, addition or loss of significant customers and

contracts, capital expenditure commitments, loan, note payable and

agreement defaults, loss of our subsidiaries and impairment of

assets,

|

|

●

|

Issuance

of convertible or equity securities for general or merger and

acquisition purposes,

|

|

●

|

Issuance

or repayment of debt, accounts payable or convertible debt for

general or merger and acquisition purposes,

|

|

●

|

Sale of

a significant number of shares of our common stock by

shareholders,

|

|

●

|

General

market and economic conditions,

|

|

●

|

Quarterly

variations in our operating results,

|

|

●

|

Investor

relation activities,

|

|

●

|

Announcements

of technological innovations,

|

|

●

|

New

product introductions by us or our competitors,

|

|

●

|

Competitive

activities, and

|

|

●

|

Additions

or departures of key personnel.

|

These

broad market and industry factors may have a material adverse

effect on the market price of our common stock, regardless of our

actual operating performance. These factors could have a material

adverse effect on our business, financial condition, and/or results

of operations.

The sale of a significant number of our shares of common stock

could depress the price of our common stock.

Sales

or issuances of a large number of shares of common stock in the

public market or the perception that sales may occur could cause

the market price of our common stock to decline. As of December 31,

2019, there were approximately (i) 28,677,147 shares of common

stock outstanding; (ii) stock option grants for the purchase of

550,000 shares of common stock at average exercise price of $1.491

per share; (iii) warrants to purchase an aggregate of we had

warrants to purchase an aggregate of 2,418,834 shares of common

stock with expiration dates between November 2021

and October 2028 at an exercise price of $3.465 per

share; (iv) and unknown number of

common shares to be issued under the Chicago Venture, Iliad and St.

George financing agreements.

These

stock option grant, warrant and contingent shares could result in

further dilution to common stockholders and may affect the market

price of the common stock.

Significant

shares of common stock are held by our principal shareholders,

other Company insiders and other large shareholders. As affiliates

as defined under Rule 144 of the Securities Act or Rule 144 of the

Company, our principal shareholders, other Company insiders and

other large shareholders may only sell their shares of common stock

in the public market pursuant to an effective registration

statement or in compliance with Rule 144.

These

stock option grant, warrant and contingent shares could result in

further dilution to common stockholders and may affect the market

price of the common stock.

Some of our convertible debentures and warrants may require

adjustment in the conversion price.

Our

Convertible Notes Payable may require an adjustment in the current

conversion price of $0.221 per share if we issue common stock,

warrants or equity below the price that is reflected in the

convertible notes payable. Our warrant with St. George may require

an adjustment in the exercise price. The conversion price of the

convertible notes and warrants will have an impact on the market

price of our common stock. Specifically, if under the terms of the

convertible notes the conversion price goes down, then the market

price, and ultimately the trading price, of our common stock will

go down. If under the terms of the convertible notes the conversion

price goes up, then the market price, and ultimately the trading

price, of our common stock will likely go up. In other words, as

the conversion price goes down, so does the market price of our

stock. As the conversion price goes up, so presumably does the

market price of our stock. The more the conversion price goes down,

the more shares are issued upon conversion of the debt which

ultimately means the more stock that might flood into the market,

potentially causing a further depression of our stock.

14

We do not anticipate paying any cash dividends on our capital stock

in the foreseeable future.

We have

never declared or paid cash dividends on our capital stock. We

currently intend to retain all of our future earnings, if any, to

finance the growth and development of our business, and we do not

anticipate paying any cash dividends on our capital stock in the

foreseeable future. In addition, the terms of any future debt

agreements may preclude us from paying dividends. As a result,

capital appreciation, if any, of our common stock will be your sole

source of gain for the foreseeable future.