Attached files

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES ACT OF 1934

For the transition period from ________ to ________

Commission File Number: 001-36615

GWG HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 26-2222607 | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) |

325 North St. Paul Street, Suite 2650

Dallas, TX 75201

(Address of principal executive offices, including zip code)

(612) 746-1944

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock | GWGH | Nasdaq Capital Market |

Securities registered pursuant to Section 12(g) of the Act

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates was $21,845,565 as of June 28, 2019 (the last business day of the registrant’s most recently completed second fiscal quarter), based on a total of 2,878,352 shares of common stock held by non-affiliates and a closing price of $7.14 as reported on the Nasdaq Capital Market on June 28, 2019. For purposes of this computation, all officers, directors, and 10% beneficial owners of the registrant are deemed to be affiliates. Such determination should not be deemed to be an admission that such officers, directors or 10% beneficial owners, are or were, in fact, affiliates of the registrant.

As of March 24, 2020, GWG Holdings, Inc. had 33,035,249 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

GWG HOLDINGS, INC.

Index to Form 10-K

for the Fiscal Year Ended December 31, 2019

i

Organizational Structure

Our business was originally organized in February 2006. We added our current parent holding company, GWG Holdings, Inc. (“GWG Holdings”), in March 2008, and in September 2014 we consummated an initial public offering of our common stock on The Nasdaq Capital Market where our stock trades under the ticker symbol “GWGH.”

GWG Holdings conducts its life insurance secondary market business through a wholly owned subsidiary, GWG Life, LLC (“GWG Life”), and GWG Life’s wholly owned subsidiaries, GWG Life Trust and GWG DLP Funding IV, LLC. GWG Holdings’ indirect interests in loans collateralized by cash flows from alternative assets are held by The Beneficient Company Group, L.P. (“Ben LP,” including all of the subsidiaries it may have from time to time — “Beneficient”) and its general partner, Beneficient Management, L.L.C. (“Beneficient Management”). As a result of the Investment and Exchange Agreements described in the section below entitled “The Beneficient Transaction”, GWG Holdings reported the results of Ben LP and its subsidiaries on a consolidated basis beginning on the transaction date of December 31, 2019. All of these entities are legally organized in the state of Delaware, other than GWG Life Trust, which is governed by the laws of the state of Utah. Unless the context otherwise requires or we specifically so indicate, all references in this report to “we,” “us,” “our,” “our Company,” “GWG,” or the “Company” refer to these entities collectively. Our headquarters are located in Dallas, Texas.

On November 11, 2019, GWG Holdings contributed the common stock and membership interests of its previously-wholly owned subsidiaries Life Epigenetics Inc. (“Life Epigenetics”) and youSurance General Agency, LLC (“youSurance”) to a legal entity, InsurTech Holdings, LLC (“InsurTech Holdings”) in exchange for a membership interest in InsurTech Holdings. On March 2, 2020, InsurTech Holdings changed its name to FOXO BioScience LLC. Although we currently own 100% of the equity of InsurTech Holdings, we do not have a controlling financial interest in InsurTech Holdings because the managing member has substantive participating rights. Therefore, we account for our ownership interest in InsurTech Holdings as an equity method investment. Life Epigenetics was formed to commercialize epigenetic technology for the longevity industry. youSurance seeks to offer life insurance directly to customers utilizing epigenetic technology.

Beneficient was formed in 2003 but began its alternative asset business in September 2017. Beneficient operates primarily through its subsidiaries, which provide Beneficient’s products and services. These subsidiaries include: (i) Beneficient Capital Company, L.L.C. (“BCC”), through which Beneficient offers loans and liquidity products; (ii) Beneficient Administrative and Clearing Company, L.L.C. (“BACC”), through which Beneficient provides services for fund and trust administration and plans to provide custody services; (iii) Pen Indemnity Insurance Company, LTD (“Pen”), through which Beneficient plans to offer insurance services; and (iv) Ben Markets Management Holdings, L.P., formerly called ACE Portal, L.L.C. (“ACE”), through which Beneficient plans to provide an online portal for direct access to Beneficient’s financial services and products.

Our Company

We are a financial services company committed to transforming the alternative asset industry with disruptive and innovative products and services. In 2018 and 2019 GWG consummated a series of transactions (as more fully described below) with Beneficient that has resulted in a significant reorientation of our business and capital allocation strategy towards an expansive and diverse exposure to alternative assets. As part of this reorientation, we also changed our Board of Directors and executive management team.

While we are continuing our work to maximize the value of our secondary life insurance business, we do not anticipate purchasing additional life insurance policies in the secondary market and have increased capital allocated toward providing liquidity to a broader range of alternative assets, primarily through investments in Beneficient. We believe Beneficient’s operations will generally produce higher risk-adjusted returns than those we can achieve from life insurance policies acquired in the secondary market. Furthermore, although we believe that our portfolio of life insurance policies is a meaningful component of a growing diversified alternative asset portfolio, we continue to explore strategic alternatives for our life insurance portfolio aimed at maximizing its value, including a possible sale, refinancing or recapitalization of our life insurance portfolio.

Page 1

We completed our transactions with Beneficient to provide us with a significant increase in assets and common shareholder equity. In addition, our transactions with Beneficient provide us with the opportunity for a diversified source of future earnings within the alternative asset industry. As GWG and Beneficient expand their strategic relationship, we believe the Beneficient transactions will transform GWG from a niche provider of liquidity to owners of life insurance to, as GWG and Beneficient expand their strategic relationship, a full-scale provider of trust and liquidity products and services to owners of a broad range of alternative assets.

Beneficient, through its subsidiaries, plans to operate three potentially high value, high margin lines of business:

| ● | Private Trust Lending & Liquidity Products. Through BCC, Beneficient provides a unique suite of private trust, lending and liquidity products focused on bringing liquidity to owners of professionally managed alternative assets. Beneficient’s innovative liquidity solutions are designed to serve mid-to-high net worth (“MHNW”) individuals, small-to-mid sized (“STM”) institutions, and asset managers who have historically possessed few attractive options to access early liquidity from their alternative assets. Beneficient targets MHNW clients with $5 million to $30 million in net worth and STM institutional clients typically holding less than $1 billion in assets. |

| ● | Trust and Custody Services. Through BACC and (subject to capitalization) through Pen, Beneficient plans, in the future, to market retirement funds, custody and clearing of alternative assets, and trustee and insurance services for covering risks attendant to owning or managing alternative assets. |

| ● | Financial Technology. Through ACE, Beneficient plans to provide online portals and financial technologies for the trading and financing of alternative assets. |

Beneficient’s existing and planned products and services are designed to support the tax and estate planning objectives of its MHNW clients, facilitate a diversification of assets or simply provide administrative management and reporting solutions tailored to the goals of the investor who owns alternative investments.

The Beneficient Transactions

The Exchange Transaction

On January 12, 2018, GWG Holdings and GWG Life entered into a Master Exchange Agreement (as amended, the “Master Exchange Agreement”) with Beneficient, MHT Financial SPV, LLC, a Delaware limited liability company (“MHT SPV”), and various related trusts (the “Seller Trusts”). The material terms and conditions of the initial Master Exchange Agreement were described in GWG Holdings’ Current Report on Form 8-K (the “January 2018 Form 8-K”) filed with the Securities and Exchange Commission (“SEC”) on January 18, 2018.

On August 10, 2018, GWG Holdings, GWG Life, Beneficient, MHT SPV, and the Seller Trusts entered into a Third Amendment to Master Exchange Agreement (the “Third Amendment”). Pursuant to the Third Amendment, the parties agreed to consummate the transactions contemplated by the Master Exchange Agreement in two closings. The Third Amendment also generally deleted MHT SPV as a party to the Master Exchange Agreement. The material terms and conditions of the Third Amendment to Master Exchange Agreement were described in GWG Holdings’ Current Report on Form 8-K (the “August 2018 Form 8-K”) filed with the SEC on August 14, 2018. The transactions contemplated by the Master Exchange Agreement, as amended, are referred to throughout this Report as the “Exchange Transaction.”

On the first closing date, which took place on August 10, 2018 (the “Initial Transfer Date”):

| ● | in consideration for GWG Holdings and GWG Life entering into the Master Exchange Agreement and consummating the transactions contemplated thereby, Ben LP, as borrower, entered into a commercial loan agreement (the “Commercial Loan Agreement”) with GWG Life, as lender, providing for a loan in a principal amount of $200.0 million (the “Commercial Loan”); |

| ● | Ben LP delivered to GWG a promissory note (the “Exchangeable Note”) in the principal amount of $162.9 million; |

| ● | Ben LP purchased 5,000,000 shares of GWG’s Series B Convertible Preferred Stock, par value $0.001 per share and having a stated value of $10 per share (the “Series B”), for cash consideration of $50.0 million, which shares were subsequently transferred to the Seller Trusts; |

Page 2

| ● | the Seller Trusts delivered to GWG 4,032,349 common units of Ben LP at an assumed value of $10 per common unit; |

| ● | GWG issued to the Seller Trusts Seller Trust L Bonds due 2023 (the “Seller Trust L Bonds”) in an aggregate principal amount of $403.2 million, as more fully described below; |

| ● | GWG and the Seller Trusts entered into a registration rights agreement with respect to the Seller Trust L Bonds received by the Seller Trusts; and |

| ● | GWG and Beneficient entered into a registration rights agreement with respect to the Ben LP common units received and to be received by GWG. |

Under the Master Exchange Agreement, at the final closing (the “Final Closing” and the date on which the final closing occurred, the “Final Closing Date”), which occurred on December 28, 2018:

| ● | in accordance with the Master Exchange Agreement, and based on the net asset value of alternative asset financings as of the Final Closing Date, effective as of the Initial Transfer Date, (i) the principal amount of the Commercial Loan was reduced to $182.0 million, (ii) the principal amount of the Exchangeable Note was reduced to $148.2 million, and (iii) the principal amount of the Seller Trust L Bonds was reduced to $366.9 million; |

| ● | the Seller Trusts refunded to GWG $0.8 million in interest paid on the Seller Trust L Bonds related to the Seller Trust L Bonds that were issued as of the Initial Transfer Date but cancelled, effective as of the Initial Transfer Date, on the Final Closing Date; |

| ● | the accrued interest on the Commercial Loan and the Exchangeable Note was added to the principal amount of the Commercial Loan, as a result of which the principal amount of the Commercial Loan as of the Final Closing Date was $192.5 million; |

| ● | the Seller Trusts transferred to GWG an aggregate of 21,650,087 common units of Ben LP and GWG received 14,822,843 common units of Ben LP in exchange for the Exchangeable Note, upon completion of which GWG owned (including the 4,032,349 common units received by GWG on the Initial Transfer Date) 40,505,279 common units of Ben LP; |

| ● | Ben LP issued to GWG an option (the “Option Agreement”) to acquire the number of common units of Ben LP, interests or other property that would be received by a holder of Preferred Series A Subclass 1 Unit Accounts of Beneficient Company Holdings, L.P. (“BCH”), an affiliate of Ben LP; and |

| ● | GWG issued to the Seller Trusts 27,013,516 shares of GWG common stock (including shares issued upon conversion of the Convertible Preferred Stock). |

On the Final Closing Date, GWG and the Seller Trusts also entered into a registration rights agreement with respect to the shares of GWG common stock owned by the Seller Trusts, an orderly marketing agreement and a stockholders’ agreement. The material terms of these agreements were described in our Information Statement on Schedule 14C filed with the SEC on December 6, 2018, and in our Current Report on Form 8-K filed with the SEC on January 4, 2019.

The Expanded Strategic Relationship

In the second quarter of 2019, we completed an expansion of the strategic relationship with Beneficient, which was a transformational event for both organizations that is expected to create a unified platform uniquely positioned to provide an expanded suite of products, services and resources for investors and the financial professionals who assist them. GWG and Beneficient intend to collaborate extensively and capitalize on one another’s capabilities, relationships and services.

On April 15, 2019, Jon R. Sabes, the Company’s former Chief Executive Officer and a former director, and Steven F. Sabes, the Company’s former Executive Vice President and a former director, entered into a Purchase and Contribution Agreement (the “Purchase and Contribution Agreement”) with, among others, Ben LP. The Purchase and Contribution Agreement was summarized in our Current Report on Form 8-K filed with the SEC on April 16, 2019.

Page 3

The closing of the transactions contemplated by the Purchase and Contribution Agreement (the “Purchase and Contribution Transaction”) occurred on April 26, 2019. Prior to or in connection with such closing:

| ● | Messrs. Jon and Steven Sabes sold and transferred all of the shares of the Company’s common stock held directly and indirectly by them and their immediate family members (approximately 12% of the Company’s outstanding common stock in the aggregate); specifically, Messrs. Jon and Steven Sabes (i) sold an aggregate 2,500,000 shares of Company common stock to BCC for $25.0 million in cash and (ii) contributed the remaining 1,452,155 shares of Company common stock to AltiVerse Capital Markets, L.L.C., a Delaware limited liability company (“AltiVerse”) (which is a limited liability company owned by an entity related to Beneficient’s founders, including Brad K. Heppner (GWG’s Chairman and Beneficient’s Chief Executive Officer and Chairman) and an entity related to Thomas O. Hicks (one of Beneficient’s current directors and a director of GWG)), in exchange for certain equity interests in AltiVerse. |

| ● | Our bylaws were amended to increase the maximum number of directors of the Company from nine to 13, and the actual number of directors comprising the Board was increased from seven to 11. The size of the Board has since been reduced and currently consists of nine directors. |

| ● | All seven members of the Company’s Board of Directors prior to the closing resigned as directors of the Company, and 11 individuals designated by Beneficient were appointed as directors of the Company, leaving two board seats vacant after the closing. |

| ● | Jon R. Sabes resigned from all officer positions he held with the Company and all of its subsidiaries prior to the closing, other than his position as Chief Executive Officer of the Company’s technology focused wholly owned subsidiaries, Life Epigenetics and youSurance. |

| ● | Steven F. Sabes resigned from all officer positions he held with the Company and all of its subsidiaries prior to the closing, except as Chief Operating Officer of Life Epigenetics. |

| ● | The resignations of Messrs. Jon and Steven Sabes included a full waiver and forfeit of (i) any severance that may be payable by the Company or any of its subsidiaries in connection with such resignations or the Purchase and Contribution Transaction and (ii) all equity awards of the Company currently held by either of them. |

| ● | Murray T. Holland, a trust advisor of the Seller Trusts, was appointed as Chief Executive Officer of the Company. |

| ● | The Company entered into performance share unit agreements with certain employees of the Company pursuant to which such employees would receive a bonus under certain terms and conditions, including, among others, that such employees remain employed by the Company or one of its subsidiaries (or, if no longer employed, such employment was terminated by the Company other than for cause, as such term is defined in the performance share unit agreement) for a period of 120 days following the closing. |

| ● | The stockholders’ agreement that was entered into on the Final Closing Date was terminated by mutual consent of the parties thereto. |

| ● | BCC and AltiVerse executed and delivered a Consent and Joinder to the Amended and Restated Pledge and Security Agreement dated October 23, 2017 by and among the Company, GWG Life, LLC, Messrs. Jon and Steven Sabes and the Bank of Utah, which provides that the shares of the Company’s common stock acquired by BCC and AltiVerse pursuant to the Purchase and Contribution Agreement will continue to be pledged as collateral security for the Company’s obligations owing in respect of the L Bonds issued under our Amended and Restated Indenture, dated as of October 23, 2017, as amended and supplemented. |

Among other things, the Purchase and Contribution Agreement contemplated that after the closing, the parties will seek to enter into an agreement pursuant to which the Company will, in certain circumstances, have the right to appoint a majority of the board of directors of the general partner of Beneficient, resulting in the Company and Beneficient being consolidated from a financial reporting perspective. The Company and Beneficient will also seek to enter into an agreement pursuant to which the Company will offer and distribute (through a FINRA registered managing broker-dealer) Beneficient’s liquidity products and services. The Company intends to reduce capital allocated to life insurance assets while it works with Beneficient to build a larger diversified portfolio of alternative asset investment products.

A copy of the Purchase and Contribution Agreement is included in our Annual Report on Form 10-K filed with the SEC on July 9, 2019 as Exhibit 99.3.

Page 4

The Investment and Exchange Agreements

On December 31, 2019, the Company, Ben LP, BCH, and Beneficient Management entered into a Preferred Series A Unit Account and Common Unit Investment Agreement (the “Investment Agreement”).

Pursuant to the Investment Agreement, the Company transferred $79.0 million to Ben LP in return for 666,667 common units of Ben LP and a Preferred Series A Subclass 1 Unit Account of BCH.

In connection with the Investment Agreement, the Company obtained the right to appoint a majority of the board of directors of Beneficient Management, the general partner of Ben LP. As a result, the Company obtained control of Ben LP and began reporting the results of Ben LP and its subsidiaries on a consolidated basis beginning on the transaction date of December 31, 2019. The Company’s right to appoint a majority of the board of directors of Beneficient Management will terminate in the event (i) the Company’s ownership of the fully diluted equity of Ben LP (excluding equity issued upon the conversion or exchange of Preferred Series A Unit Accounts of BCH held as of December 31, 2019 by parties other than the Company) is less than 25%, (ii) the Continuing Directors of the Company cease to constitute a majority of the board of directors of the Company, or (iii) certain bankruptcy events occur with respect to the Company. The term “Continuing Directors” means, as of any date of determination, any member of the board of directors of the Company who: (1) was a member of the board of directors on December 31, 2019; or (2) was nominated for election or elected to the board of directors with the approval of a majority of the Continuing Directors who were members of the board of directors at the time of such nomination or election.

Following the transaction, and as agreed upon in the Investment Agreement, the Company was issued an initial capital account balance for the Preferred Series A Subclass 1 Unit Account of $319.0 million. The other holders of the Preferred Series A Subclass 1 Unit Accounts are an entity related to the founders of Ben LP and an entity related to one of GWG’s and Beneficient’s directors (the “Related Entities”), and the aggregate capital accounts of all holders of the Preferred Series A Subclass 1 Unit Accounts after giving effect to the investment by the Company is $1.6 billion. The Company’s Preferred Series A Subclass 1 Unit Account is the same class of preferred security as held by the Related Entities. In the event the Related Entities exchange their Preferred Series A Subclass 1 Unit Account for securities of the Company, the Company’s Preferred Series A Subclass 1 Unit Account would be converted into common units of Ben LP (so neither the Company nor the founders would hold Preferred Series A Subclass 1 Unit Accounts).

Also, on December 31, 2019, in a transaction related to the Investment Agreement, GWG Holdings transferred its interest in the Preferred Series A Subclass 1 Unit Account to its wholly owned subsidiary, GWG Life.

In addition, on December 31, 2019, the Company, Ben LP and the holders of common units of Ben LP (the “Common Units”) entered into an Exchange Agreement (the “Exchange Agreement”) pursuant to which the holders of Common Units from time to time have the right, on a quarterly basis, to exchange their Common Units for common stock of the Company. The exchange ratio in the Exchange Agreement is based on the ratio of the capital account associated with the Common Units to be exchanged to the market price of the Company’s common stock based on the volume weighted average price of the Company’s common stock for the five consecutive trading days prior to the quarterly exchange date. The Exchange Agreement is intended to facilitate the marketing of Ben LP’s products to holders of alternative assets.

The Exchange Transaction, the Purchase and Contribution Transaction, and the Investment and Exchange Agreements are referred to collectively as the “Beneficient Transactions.”

Segment Financial Information

We have two reportable segments: 1) Investment in Beneficient and 2) Secondary Life Insurance.

GWG segment information is included in Note 20, Segment Reporting, to the consolidated financial statements included in Item 8 of Part II of this Form 10-K.

Market Opportunity

Alternative Asset Liquidity Products and Services

The market demand for liquidity from owners of alternative assets is attributable to the outstanding net asset value of illiquid alternative assets (“NAV”) held by U.S. investors. Using data from various published industry reports from 2017 to 2019, certain widely accepted commercial private-equity databases, and applying its own proprietary assumptions and calculations (“Ben Estimates”), Beneficient estimates that total outstanding NAV held by U.S. investors exceeded $4.0 trillion in 2019 (up from an estimated $3.0 trillion in 2018).

Page 5

According to at least one industry report from Preqin from 2018, total outstanding NAV in the hands of U.S. investors grew at a 12.1% compound annual growth rate (CAGR) for the ten years ended 2018 and was forecasted to grow at an 8% CAGR through 2023 as a result of continued increases in capital committed to the alternative asset class.

According to Ben Estimates, the large U.S. institutions representing approximately 54% of the NAV have consistently sought liquidity on approximately 1.85% to 2.25% of their outstanding NAV. Based on Ben Estimates, this has led to an annual demand for liquidity of nearly $50 billion in recent years.

A primary group not included in this demand is the MHNW investor who holds investments of $5 million to $30 million compared to a large institution’s holdings in the hundreds of millions or billions of dollars. Intermediary brokers will often not represent the MHNW individuals (or STM institutional investors). According to Ben Estimates, MHNW investors hold over $700.0 billion in NAV, yet MHNW investors have only been able to access liquidity representing less than 0.5% of the NAV held by them each year, compared to the average 2% achieved by the large institutional owners, representing 54% of the market.

Based on these amounts, Beneficient estimates that MHNW investors would seek liquidity of 3% of their outstanding NAV each year if liquidity was made available to them, or a slightly greater percentage than that of large U.S. institutions. As a result, and according to Ben Estimates, the estimated market demand for liquidity by MHNW individuals would have exceeded $20.0 billion in 2019.

Secondary Life Insurance Market

The market for life insurance is large. According to the American Council of Life Insurers Fact Book 2018 (ACLI), consumers owned approximately $12.0 trillion in face value of individual life insurance policy benefits in the United States in 2017. In that same year, the ACLI reports that individual consumers purchased an aggregate of $3.1 trillion of new individual life insurance policy benefits. This figure includes all types of individual life policies, including term insurance and permanent insurance known as whole life and universal life.

The life insurance secondary market primarily serves consumers, 65 years and older, and their families who own life insurance.

The secondary market for life insurance exists as a result of consumer lapse behaviors and surrender values far below economic value offered to consumers for their life insurance by the issuing insurance carriers. The ACLI reports that the annual lapse and surrender rate for individual life insurance policies is 5.7% of the in-force face value of benefits, amounting to over $680 billion in face value of policy benefits lapsed and surrendered in 2017 alone.

In 2017, the National Association of Insurance Commissioners (“NAIC”) issued a policy bulletin in support of products we provide. The bulletin described these products as “innovative private market solutions for financing Americans’ long-term care needs.” The NAIC, citing the Company’s August 25, 2016 presentation, discussed how consumers could exchange the market value of their life insurance policies for products designed to fund long-term care expenses.

Primary Life Insurance Market and Technology (“Insurtech”)

The opportunity to apply technology to transform the insurance industry is significant. The application of technology to the insurance industry, commonly referred to as “insurtech”, provides opportunities for new entrants into the traditional insurance marketplace that have the potential to significantly disrupt the insurance industry’s historical approach to assessing and selecting acceptable underwriting risks.

As discussed in the Organizational Structure section above, on November 11, 2019, GWG contributed the common stock and membership interests of its previously wholly-owned subsidiaries, Life Epigenetics and youSurance, to InsurTech Holdings. This transaction affected a reorganization such that InsurTech owns only two direct subsidiaries, Life Epigenetics and youSurance, which hold all insurtech assets, and one indirect subsidiary, Scientific Testing Partners, LLC, a wholly owned subsidiary of Life Epigenetics. In connection with the transaction, GWG Holdings contributed $2.1 million in cash to InsurTech Holdings during the fourth quarter of 2019 and is committed to contribute an additional $17.9 million to the entity over the next two years.

Page 6

Business Strategies

1. Liquidity for Alternative Assets

As a result of the Beneficient Transactions, we are now uniquely positioned to provide liquidity and related services to investors holding a full range of illiquid alternative assets. We will continue to work to create the most value for holders of alternative assets, the financial professionals who advise them and for our shareholders.

Beneficient provides private trust solutions, including a unique suite of lending and liquidity products focused on bringing liquidity to owners of alternative assets. Beneficient’s innovative liquidity solutions are designed to serve MHNW individuals, STM institutions, and asset managers who have historically possessed few attractive options to access early liquidity from their alternative assets. Beneficient targets MHNW individual clients with $5 million to $30 million in investments and institutional clients typically holding less than $1 billion in assets.

Beneficient’s products can also support tax and estate planning objectives, facilitate a diversification of assets or provide administrative management and reporting solutions tailored to the goals of the investor. In the future, Beneficient plans to offer insurance services covering risks associated with owning or managing alternative assets.

Our life insurance secondary market business is designed to serve consumers 65 years or older owning life insurance. We seek to earn non-correlated yield from life insurance policies that we purchased in the secondary market. Since inception, we have purchased over $3.2 billion in face value of policy benefits from consumers for over $620 million, as compared to the $52 million in surrender value offered by insurance carriers on those same policies. Our products provide unique and valuable services to the senior consumers that we serve.

The goal of our secondary life insurance business has been to build a profitable, large and well-diversified portfolio of life insurance assets. We believe that scale and diversification are key factors and risk mitigation strategies to provide consistent cash flows and reliable investment returns. We believe that we have reached the goal in terms of portfolio size and diversification. As described elsewhere, we do not anticipate making additional investments in the life settlements portfolio as we believe Beneficient’s operations will generally produce higher risk-adjusted returns than those we can achieve from life insurance policies acquired in the secondary market.

2. Developing a World Class Financial Services Distribution Platform

GWG has developed a large and sophisticated financial services product distribution platform. Today, this platform consists of over one hundred independent broker-dealers and several thousand “independent” financial advisors (“Retail Distribution”) who sell the Company’s investment products. “Independent” in this context refers to broker-dealers that accommodate financial advisors who carry securities licenses and need back-office support for services, such as compliance and trade execution, but allow their advisors wide latitude in how they conduct business. Since inception, GWG has raised over $1.52 billion of debt and equity capital to support our secondary market of life insurance business and related expenditures.

We believe that we are well positioned to continue to grow our Retail Distribution for several reasons:

| ● | There is a trend of financial professionals leaving large full-service broker-dealers to become “independent”; |

| ● | Newly independent financial professionals and their clients demand a high level of customer service and access to innovative and value added products; |

| ● | The significant demand for liquidity from owners of alternative assets by US investors; |

| ● | Our expanded relationship with Beneficient will attract more and larger broker dealers to our platform due to our increased size and market capitalization as well as the increase in products offered; and |

| ● | By using capital to provide liquidity products to our current customers, and as they begin to realize the benefit of these products, we will able to raise more capital and attract additional broker dealers into our selling group. |

3. Commercializing Advanced Epigenetic Technology for Primary Life Insurance Markets

We believe life insurance underwriting will be transformed due to advancements in science and technology. As part of that transformational change, we believe the science of epigenetics will serve as a foundational science to this advancement for the life insurance industry by achieving more accurate and automated underwriting.

Page 7

As discussed in the Organizational Structure section above, on November 11, 2019, GWG contributed the common stock and membership interests of its previously wholly-owned subsidiaries, Life Epigenetics and youSurance, to InsurTech Holdings. We believe that as a separate entity (rather than as a small subsidiary of a large financial services holding company), the InsurTech Holdings businesses can reach their maximum potential in terms of marketing and branding, attraction of talent, appropriate peer group comparisons and, ultimately, return to its owners. The Company will retain substantially all of the economics of InsurTech Holdings.

Secondary Life Insurance Assets

Our portfolio of life insurance policies, owned by our subsidiaries as of December 31, 2019, is summarized below:

Life Insurance Portfolio Summary

| Total life insurance portfolio face value of policy benefits (in thousands) | $ | 2,020,973 | ||

| Average face value per policy (in thousands) | $ | 1,756 | ||

| Average face value per insured life (in thousands) | $ | 1,883 | ||

| Weighted average age of insured (years) | 82.4 | |||

| Weighted average life expectancy (LE) estimate (years) | 7.2 | |||

| Total number of policies | 1,151 | |||

| Number of unique lives | 1,073 | |||

| Demographics | 74% Male; 26% Female | |||

| Number of smokers | 48 | |||

| Largest policy as % of total portfolio face value | 0.7 | % | ||

| Average policy as % of total portfolio | 0.1 | % | ||

| Average annual premium as % of face value | 3.3 | % |

Our portfolio of life insurance policies, owned by our subsidiaries as of December 31, 2019, organized by the insured’s current age and the associated number of policies and policy benefits, is summarized below:

Distribution of Policies and Policy Benefits by Current Age of Insured

| Percentage of Total | ||||||||||||||||||||||

| Min Age | Max Age | Number of Policies | Policy | Number of Policies | Policy Benefits | Wtd. Avg. LE (years) | ||||||||||||||||

| 95 | 101 | 17 | $ | 34,402 | 1.5 | % | 1.7 | % | 2.2 | |||||||||||||

| 90 | 94 | 145 | 283,442 | 12.6 | % | 14.0 | % | 3.3 | ||||||||||||||

| 85 | 89 | 238 | 556,090 | 20.7 | % | 27.5 | % | 5.0 | ||||||||||||||

| 80 | 84 | 251 | 463,047 | 21.8 | % | 22.9 | % | 7.7 | ||||||||||||||

| 75 | 79 | 224 | 347,952 | 19.4 | % | 17.2 | % | 9.8 | ||||||||||||||

| 70 | 74 | 205 | 264,496 | 17.8 | % | 13.1 | % | 11.0 | ||||||||||||||

| 60 | 69 | 71 | 71,544 | 6.2 | % | 3.6 | % | 11.4 | ||||||||||||||

| Total | 1,151 | $ | 2,020,973 | 100.0 | % | 100.0 | % | 7.2 | ||||||||||||||

Page 8

Our portfolio of life insurance policies, owned by our subsidiaries as of December 31, 2019, organized by the insured’s estimated life expectancy estimates and associated policy benefits, is summarized below:

Distribution of Policies by Current Life Expectancies of Insured

| Percentage of Total | ||||||||||||||||||

| LE (Months) | Max LE (Months) | Number of Policies | Policy (in thousands) | Number of Policies | Policy Benefits | |||||||||||||

| 0 | 47 | 281 | $ | 447,313 | 24.4 | % | 22.1 | % | ||||||||||

| 48 | 71 | 223 | 389,264 | 19.4 | % | 19.3 | % | |||||||||||

| 72 | 95 | 214 | 408,932 | 18.6 | % | 20.2 | % | |||||||||||

| 96 | 119 | 191 | 334,356 | 16.6 | % | 16.6 | % | |||||||||||

| 120 | 143 | 121 | 187,760 | 10.5 | % | 9.3 | % | |||||||||||

| 144 | 179 | 97 | 180,742 | 8.4 | % | 8.9 | % | |||||||||||

| 180 | 240 | 24 | 72,606 | 2.1 | % | 3.6 | % | |||||||||||

| Total | 1,151 | $ | 2,020,973 | 100.0 | % | 100.0 | % | |||||||||||

We rely on the payment of policy benefit claims by life insurance companies as a significant source of cash inflow. The life insurance assets we own represent obligations of third-party life insurance companies to pay the benefit amount under the policy upon the mortality of the insured. As a result, we manage this credit risk exposure by generally purchasing policies issued by insurance companies with investment-grade ratings from Standard & Poor’s, and diversifying our life insurance portfolio among a number of insurance companies.

The yield to maturity on bonds issued by life insurance carriers reflects, among other things, the credit risk (risk of default) of such insurance carrier. We follow the yields on certain publicly traded life insurance company bonds because this information is part of the data we consider when valuing our portfolio of life insurance policies for our financial statements.

The average yield to maturity of publicly traded life insurance company bonds data we consider as inputs to our life insurance portfolio valuation process was 2.67% as of December 31, 2019. We believe that this average yield to maturity reflects, in part, the financial market’s judgment that credit risk is low with regard to these carriers’ financial obligations. The obligations of life insurance carriers to pay life insurance policy benefits ranks senior to all of their other financial obligations, including the senior bonds they issue. The portfolio is backed by over 80 high quality insurance carriers. As of December 31, 2019, 95.7% of the face value benefits of our life insurance policies were issued by insurers having an investment-grade rating (BBB or better) by Standard & Poor’s.

As of December 31, 2019, our ten largest life insurance company credit exposures and the Standard & Poor’s credit rating of their respective financial strength and claims-paying ability is set forth below:

Distribution of Policy Benefits by Top 10 Insurance Companies

| Rank | Policy (in thousands) | Percentage of Policy Benefit Amount | Insurance Company | Ins. Co. S&P Rating | ||||||||

| 1 | $ | 287,492 | 14.2 | % | John Hancock Life Insurance Company | AA- | ||||||

| 2 | 233,338 | 11.5 | % | Lincoln National Life Insurance Company | AA- | |||||||

| 3 | 214,799 | 10.6 | % | AXA Equitable Life Insurance Company | A+ | |||||||

| 4 | 196,164 | 9.7 | % | Transamerica Life Insurance Company | AA- | |||||||

| 5 | 112,503 | 5.6 | % | Metropolitan Life Insurance Company | AA- | |||||||

| 6 | 98,068 | 4.8 | % | American General Life Insurance Company | A+ | |||||||

| 7 | 85,998 | 4.3 | % | Pacific Life Insurance Company | AA- | |||||||

| 8 | 69,976 | 3.5 | % | ReliaStar Life Insurance Company | A | |||||||

| 9 | 64,095 | 3.2 | % | Massachusetts Mutual Life Insurance Company | AA+ | |||||||

| 10 | 60,953 | 3.0 | % | Protective Life Insurance Company | AA- | |||||||

| $ | 1,423,386 | 70.4 | % | |||||||||

Page 9

Beneficient Loans Receivable

Beneficient’s primary operations pertain to its liquidity products whereby Ben LP, through its subsidiaries, extends loans collateralized by cash flows from illiquid alternative assets and provides services to the trustees who administer the collateral. Beneficient’s core business products are its Exchange Trust, LiquidTrust and the InterChange Trust (introduced in 2020). Beneficient’s clients select one of these products and place their alternative assets into the custody trust that is a constituent member of a trust structure called the “ExAlt PlanTM” (comprised of Exchange Trusts, LiquidTrusts, Custody Trusts, Collective Trusts, and Funding Trusts). The ExAlt PlanTM then delivers to Beneficient’s clients the consideration required by the specific product selected by Beneficient’s clients. At the same time, Beneficient, through a subsidiary, extends a loan to the ExAlt PlanTM. The proceeds (cash or securities of Ben LP or its affiliates) of that loan to the ExAlt PlanTM are ultimately paid to the client. The cash flows from the client’s alternative asset support the repayment of the loans plus any related interest and fees.

Beneficient held loans receivable of $232.3 million at December 31, 2019, representing the fair value of loans as a result of the purchase accounting applied in conjunction with the Investment and Exchange Agreements described above. Loans are carried at the principal amount outstanding, plus interest paid in kind. Loans are demand loans with a maturity date of 12 years. Loans bear contractual interest at the greater of 14% or 1-month LIBOR plus 10%, compounded daily. In the event an alternative reference rate is required, the secured overnight financing rate (SOFR) would replace LIBOR, as contemplated in our loan agreements. The primary source of repayment for the loans and related fees is cash flows from the alternative assets collateralizing the loans. Interest income on loans is accrued on the principal amount outstanding and interest compounds on a daily basis.

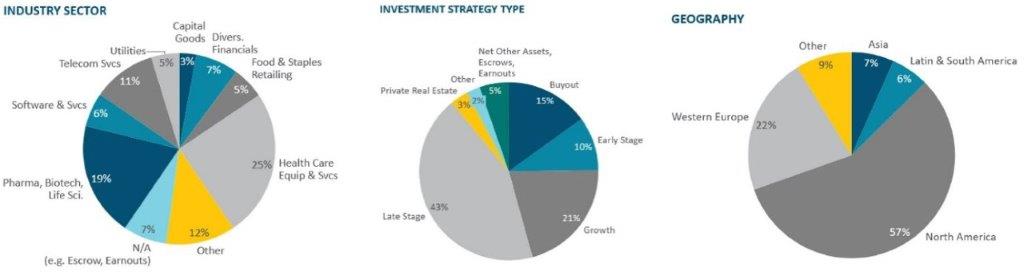

As of December 31, 2019, Beneficient’s loan portfolio had exposure to 117 professionally managed alternative investment funds, comprised of 362 underlying investments, and approximately 96 percent of Beneficient’s loan portfolio was backed by investments in private companies. Beneficient’s loan portfolio diversification spans across these industry sectors, investment strategy types and geographic regions:

Assets in the collateral portfolio consist primarily of interests in alternative investment vehicles (also referred to as “funds”) that are managed by a group of U.S. and non-U.S. based alternative asset management firms that invest in a variety of financial markets and utilize a variety of investment strategies. The vintages of the funds in the collateral portfolio as of December 31, 2019 ranged from 1998 to 2011.

As Beneficient grows its loan portfolio, Beneficient will monitor the diversity of its collateral portfolio through the use of concentration guidelines. These guidelines were established, and will be periodically updated, through a data driven approach based on asset type, fund manager, vintage of fund, industry segment and geography to manage portfolio risk. Beneficient will refer to these guidelines when making decisions about new financing opportunities; however, these guidelines will not restrict Beneficient from entering into financing opportunities that would result in Beneficient having exposure outside of its concentration guidelines. In addition, changes to Beneficient's collateral portfolio may lag changes to the concentration guidelines. As such, Beneficient’s collateral portfolio may, at any given time, have exposures that are outside of its concentration guidelines to reflect, among other things, attractive financing opportunities, limited availability of assets, or other business reasons. Given Beneficient’s limited operating history, the collateral portfolio, as of December 31, 2019, had exposure to certain alternative investment vehicles and investments in private companies that were outside of those guidelines.

Classifications by industry sector, investment strategy type and geography reflect classification of investments held in funds or companies held directly in the collateral portfolio. Investments reflect the assets listed by the general partner of a fund as held by the fund and have a positive or negative net asset value. Typical assets include portfolio companies, limited partnership interests in other funds, and net other assets, which are a fund’s cash and other current assets minus liabilities.

Industry sector is based on Global Industry Classification Standard (GICS®) Level 2 classification (also known as “Industry Group”) of companies held in the collateral portfolio by funds or directly, subject to certain adjustments by us. “Other” classification is not a GICS® classification. “Other” classification reflects companies in the GICS® classification categories of Automobiles & Components, Banks, Commercial & Professional Services, Consumer Durables & Apparel, Consumer Services, Energy, Food, Beverage & Tobacco, Household & Personal Products, Insurance, Materials, Media & Entertainment, Real Estate, Retailing, Semiconductors & Semiconductors Equipment, Tech Hardware & Equipment, and Transportation. N/A includes investments assets that we have determined do not have an applicable GICS Level 2 classification, such as Net Other Assets and investments that are not operating companies.

Investment strategy type reflects classifications based on each fund’s current investment strategy stage as determined by us. “Other Strategy Types” include private debt strategies, natural resources strategies, and hedge funds.

Geography reflects classifications determined by us based on each underlying investment. “Other” geography classification includes Israel, Australia, Eastern Europe.

Page 10

Competitive and Regulatory Framework

Competition

We encounter significant competition from numerous companies in the products and services we provide and seek to develop in the alternative assets industry. Many of these competitors have greater financial and other resources than we do and may have significantly lower cost of funds than us because they have access to insured deposits or greater access to the capital markets, for example. They may also have greater market share in the markets in which we operate. These factors could adversely affect our business, results of operations and financial condition and our ability to implement our growth strategies.

In addition, as we enter new markets, we expect to experience significant competition from incumbent market participants. Our ability to compete in these markets will be dependent upon our ability to deliver value-added products and services to the customers we serve. These factors also could adversely affect our business, results of operations and financial condition and our ability to implement our growth strategies.

Government Regulation

Our life insurance secondary market business is highly regulated at the state level with respect to the life insurance industry, and at the federal level with respect to the issuance of our securities offerings. At the state level, states generally subject us to laws and regulations requiring us to obtain specific licenses or approvals to purchase life insurance policies in those states. State statutes typically provide state regulatory agencies with significant powers to interpret, administer and enforce the laws relating to the life insurance industry. Under this authority, state regulators have broad discretionary power and may impose new licensing and other requirements, and interpret or enforce existing regulatory requirements in new and different ways. Any of these new requirements, interpretations or enforcement directives could be materially adverse to our industry.

Beneficient has applied for trust charters from the Texas Department of Banking and intends to carry on much of its business through two subsidiary trust companies. Because Beneficient’s current business plans are based in part on obtaining regulatory charters to operate as regulated trust companies, a failure to obtain such charters may materially and adversely impact its financial performance and prospects, which would likely diminish our ability to affect parts of our business plan and growth strategies. Furthermore, a failure to obtain the trust charters may trigger an impairment assessment related to the assets of Beneficient, including goodwill recognized in connection with the Investment and Exchange Agreements (see Note 5 to our consolidated financial statements for further details of the accounting for the change in control).

The state regulatory landscape for the use of genetic and epigenetic testing in life insurance underwriting is such that genetic and epigenetic testing is generally permitted. A few states require informed consent for use of genetic testing in life insurance underwriting. Epigenetic testing is distinguishable from genetic testing and we believe epigenetic testing does not raise the ethical issue found with genetic testing of denying insurance coverage to applicants based on immutable inherited characteristics. While well-informed policymakers and regulators should have little reason to consider expanding current definitions of genetic testing to include epigenetic testing, or to increase restrictions on life insurance underwriting using epigenetic test results, we can provide no such assurances.

Other changes to the current genetic and epigenetic regulatory framework, including the imposition of additional or new regulations, could arise at any time during the development or marketing of InsurTech Holdings’ epigenetic based products. This may negatively affect the ability of InsurTech Holdings to obtain or maintain applicable regulatory clearance or approval of its products. In addition, regulatory authorities, such as the Food and Drug Administration (FDA), may introduce new requirements that may change the regulatory requirements for InsurTech Holdings or its customers, or both.

Although the federal securities laws and regulations do not directly affect life insurance, in some cases the purchase of a variable life insurance policy may constitute a transaction involving a “security” that is governed by federal securities laws. While we presently hold few variable life insurance policies, our holding of a significant amount of such policies in the future could cause our Company or one of our subsidiaries to be characterized as an “investment company” under the federal Investment Company Act of 1940. The application of that law to all or part of our businesses — whether due to our purchase of life insurance policies or to the expansion of the definition of “securities” under federal securities laws — could require us to comply with detailed and complex regulatory requirements, and cause us to fall out of compliance with certain covenants under our second amended and restated senior credit facility with LNV Corporation. Such an outcome could negatively affect our business, results of operations and financial condition and our ability to implement our growth strategies.

We hold licenses to purchase life insurance policies in 38 states and can also purchase in seven unregulated states. We have also historically purchased life insurance policies from other secondary market participants.

Health Insurance Portability and Accountability Act (HIPAA)

HIPAA requires that holders of medical records maintain such records and implement procedures designed to assure the privacy of patient records. In order to carry out our business, we receive medical records and obtain a release to share such records with a defined group of persons, take on the responsibility for preserving the privacy of that information, and use the information only for purposes related to the life insurance policies we own.

Page 11

The Genetic Information Nondiscrimination Act of 2008 (GINA)

GINA is a federal law that protects people from genetic discrimination in health insurance and employment. GINA prohibits health insurers from: (i) requesting, requiring, or using genetic information to make decisions about eligibility for health insurance; or (ii) making decisions on the health insurance premium, contribution amounts, or coverage terms they offer to consumers. In addition, GINA makes it against the law for health insurers to consider family history or a genetic test result, a preexisting condition, require a genetic test, or use any genetic information, to discriminate coverage, even if the health insurance company did not mean to collect such genetic information.

GINA does not apply to the life insurance, long-term care or annuity industries. The life insurance, long-term care or annuity industries operate on medical-evidenced underwriting principles in which specific medical conditions are taken into account when assessing and pricing risk. The regulation of genomic data is relatively new, and we believe it is likely that regulation will increase and grow more complex in the foreseeable future. We cannot, however, predict what any new law or regulation would specifically involve or how it might affect our industry, our business, or our future plans.

Patents, trademarks, licenses

On March 19, 2018, Life Epigenetics filed provisional patents for the application of the use of epigenetic technology against the identification of tobacco and alcohol usage. Life Epigenetics continues to advance its intellectual property protection of these alcohol and tobacco focused technologies.

On December 17, 2018, Life Epigenetics secured the exclusive evaluation and option agreement for patent pending “Phenotypic Age and DNA Methylation Based Biomarkers for Life Expectancy and Morbidity” technology from The Regents of the University of California to commercialize advanced epigenetic technology for the life insurance industry.

Life Epigenetics has filed additional patents for a machine learning model trained to classify risk using DNA epigenetic data, a machine learned epigenetic status estimator, and a machine learning model trained to determine biochemical stat and/or medical conditions using DNA epigenetic data.

We believe epigenetics will be commercialized to improve upon many traditional factors used in the life insurance underwriting process with greater accuracy, speed and convenience. To that end, Life Epigenetics is engaged in several research and development efforts to further validate, refine and expand its epigenetic testing capabilities. In particular, Life Epigenetics conducted a research study comprised of approximately 1,300 participants in which biological samples, as well as medical records and prescription transaction history records, detailed health history, and DNA methylation analysis were conducted. Life Epigenetics measured the results of each participant’s diagnostic indicators against insurance risk classes, disease states, biomarker levels, and prescription medication statuses. The results demonstrate that epigenetics can be used to effectively estimate tobacco use, cardiovascular disease, hypertension, kidney disease, diabetes, obesity, and alcohol and drug abuse.

Beneficient has registered trademarks for its LiquidTrust product described in the “Beneficient Loans Receivable” section above and its ACE portal described in the “Organizational Structure” section above. Beneficient also has trademarks pending registration on a number of its other liquidity products and trust services, also described in the “Beneficient Loans Receivable” section above, including, its ExAlt PlanTM, Exchange Trust and Interchange Trust.

Employees

We employed approximately 130 employees as of the date of the filing of this Form 10-K.

Properties

Our principal executive offices are currently located at 325 North St. Paul Street, Dallas, Texas 75201. GWG and Beneficient collectively lease 33,652 square feet of space for a lease term expiring on July 31, 2021. GWG also retains the lease of its legacy executive offices located at 220 South Sixth Street, Suite 1200, Minneapolis, Minnesota 55402. At that location, GWG leases 17,687 square feet of space for a lease term expiring in 2025. We believe these facilities are adequate for our current needs and that suitable additional space will be available as needed.

Page 12

Company Website Access and SEC Filings

Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are filed with the SEC. We are subject to the informational requirements of the Exchange Act and file or furnish reports, proxy statements and other information with the SEC.

Our general website address is www.gwgh.com. Our website has additional information about our Company, its mission and our business. Our website also has tools that could be used by our clients and potential clients, financial advisors and investors. Beneficient’s website address is www.trustben.com and has additional information about Beneficient, its mission and its business. We maintain the website www.gwglife.com for consumers and life insurance professionals seeking our life insurance secondary market products and services. InsurTech Holdings also maintains the websites www.lifeegx.com and www.yousurance.com for its initiatives of commercializing epigenetic testing and underwriting personalized life insurance policies based on this testing. The information contained on or accessible through the foregoing websites is not part of this Annual Report on Form 10-K.

Our business involves a number of challenges and risks. In addition to the other information in this report, you should consider carefully the following risk factors in evaluating us and our business. The risks described below are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also affect our business, financial condition, operating results, or prospects.

Risks Related to Our Secondary Life Insurance Business and Industry

Material changes in the secondary life insurance market, a relatively new and evolving market, may adversely affect our operating results, business prospects, the value of our common stock and our ability to repay our debt obligations.

The success of our business and our ability to satisfy our debt obligations depends in part on the continued development of the secondary market for life insurance, including the accuracy of actuarial forecasting, the solvency of life insurance companies to pay the face value of the life insurance benefits and the demand for life insurance investments, all of which will critically impact our performance. The life insurance secondary market may be impacted by a variety of factors such as the interpretation of existing laws and regulations (including laws relating to insurable interests), the passage of new legislation and regulations, mortality improvement rates, updated actuarial methodologies, and mortality tables. Importantly, all of the factors that we believe could most significantly affect the life insurance secondary market are beyond our control. Any material and adverse change in the life insurance secondary market could adversely affect our operating results, our access to capital, the value of our common stock, our ability to repay our various debt and other obligations, and our business prospects and viability. Because of this, an investment in our securities involves greater risk as compared to investments offered by companies with more diversified business operations in more established or predictable markets.

The valuation of our life insurance policy assets on our balance sheet requires us to make material assumptions that may ultimately prove to be incorrect. If our assumptions prove incorrect, we could suffer significant losses that materially and adversely affect our results of operations.

One of our principal assets is a portfolio of life insurance policies purchased in the secondary market, comprising approximately 62% and 50% of our total assets, excluding goodwill, as of December 31, 2019 and 2018, respectively. Those assets are considered “Level 3” fair value measurements under Accounting Standards Codification 820, Fair Value Measurements and Disclosures (“ASC 820”), as there is currently no active market where we are able to observe quoted prices for identical assets. As a result, our determination of “fair value” for those assets on our balance sheet incorporates significant inputs that are not observable. Fair value is defined as an exit price representing the amount that would be received if assets were sold or that would be paid to transfer a liability in an orderly transaction between market participants at the measurement date. As such, fair value is a market-based measurement determined based on the assumptions market participants would use in pricing an asset or liability. A sale of the portfolio or a portion of the portfolio in an other than orderly transaction would likely occur at less than the fair value of the respective life insurance policies.

A Level 3 fair value measurement is inherently uncertain and could create additional volatility in our financial statements that is not necessarily related to the performance of our underlying assets. As of both December 31, 2019 and 2018, we estimated the fair value discount rate for our life insurance portfolio to be 8.25%. Life expectancy estimates are also a significant component within our fair value measurement. If in the future we determine that a higher discount rate is required to ascribe fair value to a similarly situated portfolio of life insurance policies or that life expectancy estimates materially differ from actuarial estimates and/or our projections, we could experience significant losses materially affecting our results of operations. In addition, significant losses of this nature would likely at some point cause our common stock to decline in value and cause us to be out of compliance with borrowing covenants contained in our various borrowing agreements. This could in turn result in acceleration of our second amended and restated senior credit facility with LNV Corporation, L Bonds and Seller Trust L Bonds, which we may not be able to repay. As a result, we may be forced to seek additional debt or equity financing to repay such debt amounts, and additional financing may not be available on terms acceptable to us, if at all.

If we are unable to repay our debt when it comes due, then our senior lender or the holders of our L Bonds and Seller Trust L Bonds, or both, would have the right to foreclose on our assets. For further disclosure relating to the risks associated with the valuation of our assets, see the risk factors below “If actuarial assumptions we obtain from third-party providers . . . .” and “Inaccuracies in the life expectancy estimates we use for small face policies . . . .”

Page 13

Actual results from our life insurance portfolio may not match our projected results, which could adversely affect our ability to service our existing portfolio and meet our debt obligations.

Our business partially relies on achieving actual results that are materially in line with the results we expect to attain from our investments in life insurance policy assets. In this regard, we believe that the larger the portfolio of life insurance we own, the greater the likelihood that we will achieve our expected results. To our knowledge, rating agencies generally suggest that portfolios of life insurance policies contain enough policies on individual lives to achieve actuarial stability in receiving expected cash flows. For instance, in a life insurance securitization methodology published in 2016, A.M. Best Company concluded that at least 300 lives are necessary to achieve actuarial stability, while Standard & Poor’s has indicated that stability is unlikely to be achieved with less than 1,000 lives. As of December 31, 2019, we owned $2.0 billion in face value of life insurance policies covering 1,073 unique lives.

However, even if our life insurance portfolio is actuarially stable, we still may experience differences between the projection models we use and actual mortalities, which generally has been the case over the past several years. Differences between our expectations and actual mortality results could have a materially adverse effect on our operating results and cash flow. In such a case, we may face liquidity problems, including difficulties servicing our remaining portfolio of policies and servicing our outstanding debt obligations. Continued or material failures to meet our expected results could decrease the attractiveness of our securities in the eyes of potential investors, thereby making it even more difficult to obtain capital needed to service and grow the portfolio — to the extent we allocate capital to life insurance policy purchases, and service our existing debt.

Our investments in life insurance policies have inherent risks, including fraud and legal challenges to the validity of the policies, which we will be unable to eliminate and which may adversely affect our results of operations.

When we purchase a life insurance policy, we face certain risks associated with insurance fraud and other legal challenges to the validity of the policy. For example, to the extent the insured is not aware of the existence of the policy, the insured does not exist, or the insurance company does not recognize the policy, the insurance company may cancel or rescind the policy thereby causing the loss of an investment in that policy. In addition, if an insured’s medical records have been altered in such a way as to shorten a life expectancy as reported, this may cause us to overpay for the related policy. Finally, we may experience legal challenges from insurance companies claiming that the insured failed to have an insurable interest at the time the policy was originally purchased or that the policy owner made fraudulent disclosures to the insurer at the time the policy was purchased (e.g., disclosures pertaining to the health status of the insured or the existence or sources of premium financing), or challenges from the beneficiaries of an insurance policy claiming that the sale of the policy to us was invalid.

To mitigate these risks, our origination practices and underwriting procedures include a current verification of coverage from the insurance company, a complete due-diligence investigation of the insured and accompanying medical records, a review of the life insurance policy application, and a requirement that the policy has been in force for at least two years. We also conduct a legal review of any premium financing associated with the policy to determine if an insurable interest existed at the time of its issuance. Nevertheless, these steps will not eliminate the risk of fraud or legal challenges to the life insurance policies we purchase. Furthermore, changes in laws or regulations or the interpretation of existing laws or regulations, may prove our due-diligence and risk-mitigation efforts inadequate. If a significant face amount of policies were invalidated for reasons of fraud or any other reason, our results of operations would be materially adversely affected.

Our ownership of life insurance policies issued by insurers that are unable to pay claims presented to them could have a materially adverse effect on our results of operation, our financial condition, or even our overall prospects.

We currently rely on the payment of policy claims by insurers as our most significant source of revenue collection. In essence, the life insurance assets we own represent the obligations of insurers to pay the benefit amount under the relevant policy upon the mortality of the insured. As a result, in our business, we face the “credit risk” that a particular insurer will be financially unable to pay claims when and as they become due. Depending on how many policies we own that are issued by insurers having financial difficulties at the time a claim is presented for payment, this risk could be significant enough to have a materially adverse effect on our results of operation, our financial condition, or even our overall prospects.

Page 14

To mitigate this credit risk, we generally purchase policies issued only by insurers with an investment-grade credit rating from one or more of Standard & Poor’s, Moody’s, or A.M. Best Company. As of December 31, 2019, 95.7% of the face value benefits of our life insurance policies were issued by insurers having an investment-grade rating (BBB or better) by Standard & Poor’s. We also review our exposure to credit risk associated with our portfolio of life insurance policies when estimating its fair value. In evaluating the policies’ credit risk, we consider items such as insurance company solvency, credit risk indicators, and general economic conditions. Notwithstanding our efforts to mitigate credit risk exposure and to reflect this risk in our portfolio valuation, we cannot predict with any certainty whether a particular insurer will be in a financial position to satisfy amounts that it owes under life insurance policies it has issued when a claim for payment is presented.

We have relied materially on information provided or obtained by third parties in the acquisition of life insurance policies. Any misinformation or negligence in the course of obtaining information could materially and adversely affect the value of the policies we own, our results of operation and the value of our securities.

Our acquisition of each life insurance policy is negotiated based on variables and particular facts that are unique to the policy itself and the health of the insured. The facts we obtain about the policies and the insured at the time when the policy was applied for and obtained are based on the insured’s factual representations to the insurance company, and the facts the insurance company separately obtains in the course of its own due-diligence examination, such as facts concerning the health of the insured and whether or not there is an insurable interest present when the policy was issued. Any misinformation or negligence in the course of obtaining information relating to a policy or insured could materially and adversely impact the value of the policies we own and could in turn adversely affect our results of operations and the value of our securities.

Although we do not anticipate purchasing additional life insurance policies, our life insurance business continues to be subject to state regulation and changes in those laws and regulations, or changes in their interpretation, could negatively affect our results of operation and financial condition.

When we purchase a life insurance policy, we are subject to state insurance regulations. Over the past number of years, we have seen a dramatic increase in the number of states that have adopted legislation and regulations from model laws promulgated by either the National Association of Insurance Commissioners (“NAIC”) or by the National Conference of Insurance Legislators (NCOIL). These laws are essentially consumer protection statutes responding to abuses that arose early in the development of our industry, some of which may persist. Today, almost every state has adopted some version of either the NAIC or NCOIL model laws, which generally require the licensing of purchasers of and brokers for life insurance policies, the filing and approval of purchase agreements, and the disclosure of transaction fees. These laws also require various periodic reporting requirements and prohibit certain business practices deemed to be abusive. State statutes typically provide state regulatory agencies with significant powers to interpret, administer, and enforce the laws relating to the purchase of life insurance policies. Under statutory authority, state regulators have broad discretionary power and may impose new licensing requirements, interpret or enforce existing regulatory requirements in different ways, or issue new administrative rules, any of which could be generally adverse to the industry and potentially the value of our life insurance policy assets.

If federal regulators or courts conclude that the purchase of life insurance in the secondary market constitutes, in all cases, a transaction in securities, we could be in violation of existing covenants under our second amended and restated senior credit facility with LNV Corporation, which could result in significantly diminished access to capital. We could also face increased operational expenses. The materialization of this risk could adversely affect our operating results and financial condition, our ability to repay our debt, and possibly threaten the viability of our business.

On occasion, the SEC has attempted to regulate the purchase of non-variable universal life insurance policies as transactions in securities under federal securities laws. In July 2010, the SEC issued a Staff Report of its Life Settlement Task Force. In that report, the Staff recommended that certain types of purchased insurance policies be classified as securities. The SEC has not taken any position on the Staff Report, and there is no indication if the SEC will take any action to implement the recommendations of the Staff Report. In addition, there have been several federal court cases in which transactions involving the purchase and fractionalization of life insurance policies have been held to be transactions in securities under the federal Securities Act of 1933.

Page 15

We believe that the matters discussed in the Staff Report and existing case law do not impact our current business model because our purchases of life insurance policies are distinguishable from those cases that have been held by courts, and advocated by the Staff Report, to be transactions in securities. For example, neither we nor any of our affiliates are involved in the fractionalization of life insurance policies, and we presently do not purchase significant amounts of variable life insurance policies. As a practical matter, if all or a majority of our life insurance policies were deemed to be “securities” under federal securities laws, either through an expansion of the definition of what constitutes a “security,” the expansion of the types of transactions in life insurance policies that would constitute transactions in “securities,” or the elimination or limitation of available exemptions and exceptions (whether by statutory change, regulatory change, or administrative or court interpretation), then we or one or more of our affiliated entities could become subject to the federal Investment Company Act of 1940. This outcome would likely have a material and negative effect on our Company by imposing additional regulations and rules to our governance structure, operations, and our capital structure. In particular, this outcome would likely cause us to be in violation of existing covenants under our second amended and restated senior credit facility with LNV Corporation requiring us not to operate or be characterized as an “investment company” under the Investment Company Act of 1940. This breach would likely adversely affect our liquidity and increase our cost of capital and operational expenses, all of which would adversely affect our operating results. Such an outcome could also threaten our ability to satisfy our obligations as they come due and the viability of our business.

If actuarial assumptions we obtain from third-party providers and rely on to calculate our expected returns on our investments in life insurance policies change, our operating results and cash flow could be adversely affected, as well as the value of our collateral and our ability to service our debt obligations.