Attached files

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☑ ANNUAL REPORT UNDER

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the fiscal year ended December 31, 2019

------------------------------------------------------

Commission File Number 0-11808

SANARA MEDTECH INC.

(Exact

name of Registrant as specified in its charter)

|

Texas

|

|

59-2219994

|

|

(State or other jurisdiction of incorporation or

organization)

|

|

(I.R.S. Employer Identification No.)

|

|

1200

Summit Ave, Suite 414, Fort Worth, Texas 76102

|

|

(Address

of principal executive offices)

(817)

529-2300

(Registrant’s telephone number, including area

code)

|

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the

Act:

Common

Stock $ .001 par value

Indicate

by check mark if the registrant is a well-known seasoned issuer, as

defined in Rule 405 of the Securities Act. ☐ Yes ☑ No

Indicate

by check mark if the registrant is not required to file reports

pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate

by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934 during the preceding 12 months (or for such

shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for

the past 90 days. ☑ Yes ☐ No

Indicate

by check mark whether the registrant has submitted electronically

every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (§ 232.405 of this

chapter) during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such

files). ☑ Yes ☐ No

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging growth company. See the definitions of

“accelerated filer,” “large accelerated

filer” and “smaller reporting company” in

Rule 12b-2 of the Exchange Act.

|

Large

accelerated filer

☐

|

|

Accelerated

filer

☐

|

|

Non-accelerated

filer

☑

|

|

Smaller

reporting company

☑

|

Emerging

growth company

☐

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether registrant is a shell company (as defined in

Rule 12b-2 of the Exchange Act). Yes ☐

No ☑

The

aggregate market value of the voting and non-voting common equity

held by non-affiliates of the registrant as of June 30, 2019 based

on the $5.51 closing price as of such date was approximately

$6,526,022

As of

February 21, 2020, 6,023,732 shares of the Issuer’s $.001 par

value common stock were issued and outstanding.

SANARA MEDTECH INC.

Form 10-K

For the Year Ended December 31, 2019

|

|

|

Page

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LETTER FROM THE

EXECUTIVE CHAIRMAN AND VICE CHAIRMAN

To Our

Shareholders:

2019

was a pivotal year for our Company with continued growth and

substantial progression in the execution of our long-term strategic

plan including our six areas of strategic focus.

2019 Performance

With an

increase in revenues of 34% over 2018, Sanara delivered

double-digit revenue growth for the seventh consecutive year. Total

revenues increased to $11.8 million for 2019 compared to revenues

of $8.8 million for 2018.

To be

poised for future growth, in 2019, we invested in expanding our

sales force and independent distribution network in geographic

areas that hadn’t been covered as well as the related support

infrastructure. In addition, we increased our clinical study to

prove out our product evidence-based healing and value

proposition.

You

will find more detail on all these areas in this

report.

Organization

In

August 2019, we doubled the size of our Board from three directors

to six, including two individuals new to the Company: Kenneth E.

Thorpe, Ph.D. and Ann Beal Salamone, M.S. Both Dr. Thorpe and Ms.

Salamone have extensive health care experience and very

distinguished and successful careers. Dr. Thorpe currently is Chair

of the Department of Health Policy & Management at Emory

University, Atlanta, Georgia and is a frequent national presenter

on issues of health care reform, financing, and insurance. Ms.

Salamone is a member of the National Academy of Engineering and

currently serves as Chairman of the Board of Rochal Industries LLC

based in San Antonio, Texas, and is one of the principal inventors

of Rochal’s many wound care products.

Management Update

In 2019

we implemented one of our strategic plan initiatives to manage our

operations in two distinct divisions: (1) Surgical and (2) Wound

Care. In May, Zachary B. Fleming was appointed to the position of

President, Surgical. Mr. Fleming joined the Company as Vice

President of Sales in November 2017, and successfully led the

surgical team to achieve sales growth of forty percent in 2018 and

thirty-eight percent in 2019. Also, in Mayof 2019, Shawn M. Bowman

was appointed to the position of President, Wound Care. Mr. Bowman

joined the Company as Vice President and General Manager, Wound

Care in September 2018. He has eighteen years of key experience in

the medical device, biologics and pharmaceutical industries. As a

result of their managerial skills and achievements, Mr. Fleming and

Mr. Bowman were appointed Co-Chief Operating Officers in January of

2020 in addition to maintaining their positions as Presidents of

their respective operating divisions.

In

January 2020, the Company engaged Don Stelly to provide operational

expertise in support of the expansion of our wound and skin care

business. Prior to his engagement by Sanara, Mr. Stelly was the

President and Chief Operating Officer of LHC Group, Inc., a

national provider of in-home healthcare and brings a wealth of

experience in the post-acute care setting.

Operations Update

Driving

innovation with new product development and a commercial pipeline

is key to improving patient outcomes. In line with our six focus

areas of wound and skin care which are: debridement, biofilm

management, hydrolyzed collagen, advanced biologics, adjunct

products for Negative Pressure Wound Therapy, and oxygen delivery

systems for the wound bed, the Company introduced the following

products in 2019:

●

PULSAR II™

Advanced Wound Irrigation System (AWI™), a portable, no

touch, painless, hydro-mechanical debridement system that removes

bacteria and necrotic tissue without disrupting healthy

tissue;

●

BIAKŌS™

Antimicrobial Skin & Wound Cleanser, a patented wound

cleansing spray that disrupts extracellular polymeric substances to

eradicate biofilm; and

●

HYCOL™, an

additive free Type I bovine collagen that provides hydrolyzed

collagen fragments to the wound bed that are a fraction of the size

of native collagen.

2020 Events

As we

move forward, the Company will aggressively pursue its mission to

improve patient outcomes through evidence-based healing solutions.

The Company is well positioned to increase its sales of the current

products as a result of its expanded sales force and distribution

capabilities.

In the first quarter of 2020, the Company’s

BIAKŌS™ Antimicrobial Skin & Wound Gel received FDA

clearance. This product, developed by our primary new product

developer, Rochal Industries, is currently going through the

manufacturing and commercialization process and is expected

to launch later this year. We are also in discussions with various

parties to license, acquire, and/or partner in new product

opportunities related to our six focus areas of wound and skin

care.

The

Company continued its record sales in the first two months of 2020,

but, with the unforeseen impact of the COVID-19 virus to the global

economy we expect a downturn in our business primarily due to the

delay in elective surgeries. We are committed to ensuring that our

customers and patients continue to have access to our products

during this difficult time. To manage this situation, we are taking

steps to cut costs, manage cash-flow, and continue to generate

revenue from both our wound care and surgical

businesses.

Sincerely,

Ron

Nixon

Executive

Chairman

J.

Michael Carmena

Vice

Chairman

2

PART I

Item 1. BUSINESS

Background

The

terms “Sanara MedTech,” “we,” “the

Company,” “SMTI,” “our,” and

“us” as used in this report refer to Sanara MedTech

Inc. and its subsidiaries. The Company

was organized on December 14, 2001, as a Texas corporation under

the name eAppliance Innovations, Inc. In June of 2002, MB Software

Corporation, a public corporation formed under the laws of

Colorado, merged with the Company and the Company changed its name

to MB Software Corporation as part of the merger. In May of 2008,

the Company changed its name to Wound Management Technologies,

Inc. In May of 2019, the Company changed its name to Sanara

MedTech Inc.

The

Company’s business is developing, marketing, and distributing

wound and skin care products to physicians, hospitals, clinics and

post-acute care settings. Our products are primarily sold in the

North American advanced wound care and surgical tissue repair

markets. Sanara MedTech products include CellerateRX® Surgical

Activated Collagen® Adjuvant (CellerateRX); HYCOL™

Hydrolyzed Collagen (HYCOL); BIAKŌS™ Antimicrobial Skin

& Wound Cleanser (BIAKŌS AWC); and PULSAR II™

Advanced Wound Irrigation System (AWI™).

The

Company’s exclusive license to sell and distribute

CellerateRX products in the human health care market (excluding

dental and retail) expired on February 27, 2018. The license

permitted the Company to continue to sell and distribute products

through August 27, 2018. Subsequent to the expiration of the

license agreement between the Company and Applied Nutritionals,

LLC, an affiliate of The Catalyst Group, Inc. (Catalyst) acquired

an exclusive license to distribute CellerateRX products in the

United States, Canada and Mexico.

Effective August 28, 2018, the Company consummated definitive

agreements that continued the Company’s operations to market

the its principal products, CellerateRX, through a 50% ownership

interest in a newly formed limited liability company, Cellerate,

LLC. The remaining 50% ownership interest was held by an affiliate

of Catalyst. As part of this transaction, the Company issued a

convertible promissory note to the affiliate of Catalyst which

converted into shares of common stock at an adjusted price of $9.00

per share. Cellerate, LLC conducted operations with an exclusive

sublicense from Catalyst’s affiliate to distribute

CellerateRX products in the United States, Canada and Mexico (the

sublicense was subsequently amended to include worldwide

distribution rights). On March 15, 2019, the Company executed and

closed an agreement with Catalyst to acquire Catalyst’s 50%

equity interest in Cellerate, LLC. After closing the acquisition,

the Company owned 100% of Cellerate, LLC, and as a wholly owned

subsidiary began reporting its financial results on a consolidated

basis beginning March 15, 2019. The Company acquired the remaining

50% equity interest in Cellerate, LLC in exchange for the issuance

of 1,136,815 shares of the Company’s newly created Series F

Convertible Preferred Stock.

The

Cellerate Acquisition was accounted for as a reverse merger and

recapitalization because, immediately following the completion of

the transaction, Catalyst could obtain effective control of the

Company upon exercise of its convertible preferred stock and

promissory note, both of which could occur at Catalyst’s

option. Additionally, Cellerate, LLC’s officers and senior

executive positions continued on as management of the combined

entity after consummation of the Cellerate

Acquisition.

On

February 7, 2020, the affiliate of Catalyst converted its

promissory note into 179,101 shares of common stock and also

converted its Series F Convertible Preferred Stock into 2,273,630

shares of common stock.

The Products

CellerateRX

products are primarily purchased by hospitals and ambulatory

surgical centers for use by surgeons on surgical wounds. HYCOL

products are available through skilled nursing facilities, wound

care clinics and other medical facilities, and are intended for the

management of full and partial thickness wounds including pressure

ulcers, venous and arterial leg ulcers and diabetic foot ulcers.

HYCOL is currently approved for reimbursement under Medicare Part

B. We believe CellerateRX and HYCOL products are unique in

composition, superior to other products in clinical performance,

and demonstrate the ability to reduce costs associated with the

standards of care for their intended uses.

BIAKŌS

AWC is an FDA cleared, patented product that effectively disrupts

extracellular polymeric substances to eradicate biofilm microbes.

BIAKŌS AWC also provides mechanical removal of debris, dirt,

foreign materials, and microorganisms from wounds including stage

I-IV pressure ulcers, diabetic foot ulcers, post-surgical wounds,

first and second-degree burns as well as grafted and donor sites.

BIAKŌS AWC is effective in killing free-floating microbes,

immature, and mature bacterial biofilms and fungal biofilms. In

addition, BIAKŌS AWC safety studies show that it is

non-cytotoxic, non-irritating, and non-sensitizing to healthy skin

and assists in the normal wound healing process. First sales of

BIAKŌS AWC occurred in July 2019

PULSAR

II™ Advanced Wound Irrigation System (AWI™) is a

portable, no touch, painless, selective hydro-mechanical

debridement system that effectively removes bacteria and necrotic

tissue from wounds without disrupting healthy tissue.

3

New Products, Markets and Services

The

Company received notification of FDA clearance for

BIAKŌS™ Antimicrobial Wound Gel in February 2020 and

expects to launch the product in 2020 to complement its

BIAKŌS™ AWC. Both products are effective against

planktonic microbes as well and immature and mature biofilms. When

used together, the cleanser can be used initially to clean a wound

and disrupt biofilms (removing 99% in 10 minutes). The gel can then

be applied and will remain in the wound for up to 72 hours

eliminating biofilms between normal dressing changes.

The

Company also expects to introduce BIAKŌS™ Antimicrobial

Barrier Film (BIAKŌS ABF) in the latter part of 2020.

BIAKŌS ABF is an FDA cleared, first in-class, antimicrobial

spray-on wound dressing that kills microbes while protecting

underlying tissue, helping to remediate damage and prevent further

infection. This product can be used on macerated skin and

wounds.

Marketing, Sales and Distribution

The

Company’s CellerateRX Surgical products are attracting

increased business from hospitals and surgery centers due to their

recognized benefits including efficacy and economic value. The

surgical products are used in specialty areas including total joint

replacement, spine, orthopedic, trauma, vascular, general, plastic

and reconstructive surgeries and podiatry. The surgical products

are sold through a growing network of surgical specialty

distributors and Company representatives who are credentialed to

demonstrate the products in surgical settings.

The

Company’s advanced wound care products are primarily

distributed to the post-acute care settings including long-term

care facilities, home health, wound care centers, and professional

medical offices. Due to the expansion of our distribution network,

the increasing prevalence of diabetic and decubitus (pressure)

ulcers, and the demonstrated efficacy of our products, we believe

demand for our products will grow significantly in 2020. We believe

our products are unique in composition, superior to other products

in clinical performance, and demonstrate the ability to reduce

costs associated with standard wound management. Our wound care

products are sold by Company representatives supplemented by major

medical-surgical distributors, independent distributors, and

durable medical equipment (DME) distributors.

Staffing

As of

March 26, 2020, the Company has a staff of 40, consisting of 38

full-time employees and 2 part time employees.

Competition

The

wound care market is served by a number of large, multi-product

line companies as well as a number of small companies. Our products

compete with primary dressings, advanced wound care products,

collagen matrices and other biopharmaceutical products.

Manufacturers and distributors of competitive products include

Smith & Nephew plc, Acelity L.P. Inc., Medline Industries,

Inc., ACell Inc., and Integra LifeSciences Holdings Corporation.

Many of our competitors are significantly larger than we are and

have greater financial and personnel resources. We believe,

however, that our products outperform our competitors’

currently available products by improving efficacy, reducing the

cost of patient care, and replacing numerous products with a single

primary dressing.

Available Information

The

Company electronically files reports with the Securities and

Exchange Commission (the “SEC”). The SEC maintains an

Internet site (www.sec.gov) that contains reports, proxy and

information statements, and other information regarding issuers

that file electronically with the SEC. Copies of the

Company’s Annual Report on Form 10-K, Quarterly Reports on

Form 10-Q and Current Reports on Form 8-K and amendments to those

reports filed or furnished to the SEC are also available free of

charge through the Company’s website

(http://www.sanaramedtech.com/), as soon as reasonably practicable

after electronically filing with or otherwise furnishing such

information to the SEC, and are available in print to any

shareholder who requests it.

Item 1A. RISK FACTORS

The

following risk factors should be considered with respect to making

any investment in our securities as such an investment involves a

high degree of risk. You should carefully consider the following

risks and the other information set forth elsewhere in this report,

including the financial statements and related notes, before you

decide to purchase shares of our stock. If any of these risks

occur, our business, financial condition and results of operations

could be adversely affected. As a result, the trading price of our

stock could decline, perhaps significantly, and you could lose part

or all of your investment. As used herein, the word

“business” as used in “material adverse effect on

our business”, “adversely affect our business”

and other similar phrases includes any of (or any combination of)

the Company’s present or future operations, financial

performance, margins, revenues, operating margins, stock value,

competitive position, or other indicators of Company

performance.

4

RISKS RELATED TO HOW WE OPERATE OUR BUSINESS:

We had a history of losses in prior years and may not maintain

profitability as we expand our selling efforts.

The

Company has incurred net losses in most years since we began our

current operations in 2004. We plan to continue making significant

investments in our sales and clinical programs which substantially

increase our operating expenses. Consequently, we will need to

continue our revenue growth to become profitable in the future. We

cannot offer any assurance that we will be able to generate future

sales growth. If we fail to achieve profitability, our stock price

may decline and you may lose part or all of your

investment.

Our revenue growth for a particular period is difficult to predict,

and a shortfall in forecast revenues may harm our operating

results.

Because

we are a relatively small company, our revenue growth and

consequently results of operations are difficult to predict. We

plan our operating expense levels based primarily on forecasted

revenue levels. A shortfall in revenue could lead to operating

results being below expectations as we may not be able to quickly

reduce our fixed expenses in response to short-term revenue

shortfalls. We have experienced fluctuations in revenue and

operating results from quarter to quarter and anticipate that these

fluctuations will continue until we achieve a critical mass with

our product sales. These fluctuations can result from a variety of

factors, including:

●

the

uncertainty surrounding our ability to attract new customers and

retain existing customers;

●

the

length and variability of our sales cycle, which makes it difficult

to forecast the quarter in which our sales will occur;

●

issues

in order fulfillment for our products;

●

the

timing of operating expense relating to the expansion of our

business and operations;

●

the

development of new wound care products or product enhancements by

our competitors;

●

actual

events, circumstances, outcomes and amounts differing from

assumptions and estimates used in preparing our operating plan and

how well we execute our strategy and operating plans.

As a

consequence, operating results for a particular future period are

difficult to predict and prior results are not necessarily

indicative of future results. Any of the foregoing factors, or any

other factors discussed elsewhere herein, could have a material

adverse effect on our business.

If our products do not gain market acceptance, we might not be able

to fund future operations.

Several

factors may affect the market acceptance of our products or any

other products we develop or acquire. These include, but are not

limited to:

●

the

price of our products relative to other products for the same

indications;

●

the

perception by physicians and other members of the healthcare

community of the efficacy and safety of our products for their

indicated applications and treatments;

●

changes

in practice guidelines and the standard of care for the targeted

indication

●

the

effectiveness of our sales and marketing efforts or that of our

independent sales distributors.

Our

ability to effectively promote and sell any approved products may

also depend on pricing and cost-effectiveness, including our

ability to produce a product at a competitive price and our ability

to obtain sufficient third-party coverage or reimbursement, if any.

In addition, our efforts to educate the medical community on the

benefits of our products may require significant resources, may be

constrained by FDA rules and policies on product promotion, and may

never be successful. If our products do not gain market acceptance,

we may not be able to fund future operations, including developing,

testing and obtaining regulatory approval for new product

candidates and expanding our sales and marketing efforts for our

approved products, which would cause our business to

suffer.

5

Disruption of, or changes in, our distribution model or customer

base could harm our sales and margins.

If we

fail to manage the distribution of our products properly, or if the

financial condition or operations of our reseller channels weakens,

there may be a material adverse effect on our business.

Furthermore, a change in the mix of our customers between service

provider and enterprise, or a change in the mix of direct and

indirect sales, could adversely affect our business.

Several

factors could also result in disruption of or changes in our

distribution model or customer base, which could harm our sales and

margins, including the following:

●

in some

instances, we compete with some of our resellers through our direct

sales, which may lead these channel partners to use other suppliers

that do not compete; and

●

some of

our resellers may have insufficient financial resources and may not

be able to withstand changes in business conditions.

If we cannot meet our future capital requirements, our business

will suffer.

We have

a history of operating losses and negative cash flow from operating

activities with the exception of 2016 and 2018. As such, we have

utilized funds from offerings of our securities to fund our

operations. Future results of operations involve significant risks

and uncertainties. Factors that could affect our future operating

results and cause actual results to vary materially from

expectations include, but are not limited to, potential demand for

our products, risks from competitors, regulatory approval of our

new products, technological change, and dependence on key

personnel. Although we have taken steps to improve our overall

liquidity, if our cash flow is insufficient, we may be forced

either to secure additional amounts to our bank line of credit or

seek additional equity financing in order to:

●

fund

operating losses;

●

increase

marketing to address the market for wound care and surgical

products;

●

take

advantage of opportunities, including more rapid expansion or

acquisitions of complementary products or businesses;

●

hire,

train and retain employees;

●

develop

and/or distribute new products; and/or

●

respond

to economic and competitive pressures.

If our

capital needs are met through the issuance of equity or convertible

debt securities, the percentage ownership of our current

shareholders may be reduced which may have a negative impact on the

market price of our common stock. Our future success may be

determined in large part by our ability to obtain additional

financing, and the incurrence of indebtedness would result in

increased debt service obligations which could result in operating

and financing covenants that would restrict our operations. There

can be no assurance that such financing would be available or, if

available, that such financing could be obtained upon terms

acceptable to us. If adequate funds are not available, or are not

available on acceptable terms, our operating results and financial

condition may suffer.

Failure to retain and recruit key personnel would harm our ability

to meet key objectives.

Our

success depends, in large part, on our ability to attract and

retain skilled executive, managerial, sales and marketing

personnel. There can be no assurance that we will be able to find

and attract additional qualified employees or retain any such

executive officers and other key personnel. The inability to hire

qualified personnel or the loss of services of our executive

officers or key personnel may have a material adverse effect on our

business.

Failure to manage our planned growth could harm our

business.

Our

ability to successfully market and sell our wound care products and

implement our business plan requires an effective plan for managing

our future growth. We plan to increase the scope of our operations

at a rapid rate. Future expansion efforts will be expensive and may

strain our internal operating resources. To manage future growth

effectively, we must maintain and enhance our financial and

accounting systems and controls, integrate new personnel and manage

expanded operations. If we do not manage growth properly, it could

harm our operating results and financial condition.

6

We operate in a highly competitive industry and face competition

from large, well-established medical device manufacturers as well

as new market entrants.

Competition

from other medical device companies is significant and could be

significantly affected by new product introductions and other

market activities of industry participants. We compete with other

companies in acquiring rights to products or technologies from

third party developers. Although our products have performed well

in customer evaluations, we are a relatively unknown brand in a

market controlled, in large part, by companies with a large

customer base. We may not, even with strong customer accounts, be

able to establish the credibility necessary to secure large

national customers.

Several

factors may limit the market acceptance of our products, including

the timing of regulatory approvals and market entry relative to

competitive products, the availability of alternative products, and

the price of our products relative to alternative products, the

availability of third-party reimbursement and the extent of

marketing efforts by third party distributors or agents that we

retain. There can be no assurance that our products will receive

market acceptance in a commercially viable period of time, if at

all. Furthermore, there can be no assurance that we can develop

products that are more effective or achieve greater market

acceptance than competitive products, or that our competitors will

not succeed in developing or acquiring products and technologies

that are more effective than those being developed by us, that

would render our products and technologies less competitive or

obsolete.

Our

competitors enjoy several competitive advantages over us, including

but not limited to:

●

large

and established distribution networks in the U.S. and/or in

international markets;

●

greater

financial, managerial and other resources for products research and

development, sales and marketing efforts and protecting and

enforcing intellectual property rights;

●

greater

name recognition;

●

larger

consumer base;

●

more

expansive portfolios of intellectual property rights;

●

greater

experience in obtaining and maintaining regulatory approvals and/or

clearances from the FDA and other regulatory agencies.

The

presence of competition in our market may lead to pricing pressure

which would make it more difficult to sell our products at a

profitable price or may prevent us from selling our products at

all. Our failure to compete effectively would have a material

adverse effect on our business.

Security breaches and other disruptions could compromise our

information and expose us to liability, which would cause our

business and reputation to suffer.

In the

ordinary course of our business, we use networks to collect and

store sensitive data, including intellectual property, proprietary

business information and important information of our customers,

suppliers and business partners, as well as personally identifiable

information of our customers and employees. The secure processing,

maintenance and transmission of this information is critical to our

operations. Despite our security measures, our information

technology and infrastructure may be vulnerable to attacks by

hackers or breached due to employee error, malfeasance or other

disruptions. Any such breach could compromise our networks and the

information stored there could be accessed, publicly disclosed,

lost or stolen. Any such access, disclosure or other loss of

information could result in legal claims or proceedings, liability

under laws that protect the privacy of personal information, and

regulatory penalties. Further, such access, disclosure or loss may

cause disruption of our operations and the services we provide to

customers, damage to our reputation, and cause a loss of confidence

in our products and services, which could adversely affect our

business.

We may not be able to maintain sufficient product liability

insurance to cover claims against

us.

Product

liability insurance for the healthcare industry is generally

expensive to the extent it is available at all. We may not be able

to maintain such insurance on acceptable terms or be able to secure

increased coverage as commercialization of our products progresses,

nor can we be sure that existing or future claims against us will

be covered by our product liability insurance. Moreover, the

existing coverage of our insurance policy or any rights of

indemnification and contribution that we may have may not be

sufficient to offset existing or future claims. A successful claim

against us with respect to uninsured liabilities or in excess of

insurance coverage and not subject to any indemnification or

contribution could have a material adverse effect on our

business.

7

RISKS RELATED TO OUR PRODUCTS:

Competitors could invent products superior to ours and cause our

products and technologies to become obsolete.

The

wound care sector of the medical products industry is characterized

by a multitude of technologies and intense competition. Our

competitors currently manufacture and distribute a variety of

products that are, in many respects, comparable to our products.

Many suppliers of competing products are considerably larger and

have much greater resources than we have. In addition, many

specialized products companies have formed collaborations with

large, established companies to support research, development and

commercialization of wound care products which may be competitive

with ours. Academic institutions, government agencies and other

public and private research organizations are also conducting

research activities and may commercialize wound care products on

their own or through joint ventures. It is possible that these

competitors may develop technologies and products that are more

effective than any we currently have. If this occurs, any of our

products and technology affected by these developments could become

obsolete.

We may have exposure to product liability claims.

Although

we have contractual indemnity from the manufacturer of CellerateRX

for certain liability claims related to its production, we could

face a product liability claim outside of the scope of the

contractual indemnity. We do not have, and do not anticipate

obtaining, contractual indemnification from parties supplying raw

materials or parties marketing the products we sell. In any event,

indemnification from the manufacturer of CellerateRX or from any

other party is limited by the terms of the indemnity and by the

creditworthiness of the indemnifying party. A successful product

liability claim or series of claims brought against us could result

in judgments, fines, damages and liabilities that could have a

material adverse effect on our business. We may incur significant

expense investigating and defending these claims, even if they do

not result in liability. Moreover, even if no judgments, fines,

damages or liabilities are imposed on us, our reputation could

suffer, which could have a material adverse effect on our business.

In the event that we do not have adequate insurance or contractual

indemnification, product liability claims relating to defective

products could have a material adverse effect on our

business.

RISKS RELATED TO INTELLECTUAL PROPERTY:

If we are unable to protect our intellectual property rights

adequately, we may not be able to compete effectively.

Part of our success depends on our ability to protect proprietary

rights to technologies used in certain of our products. We rely on

patents, copyrights, trademarks and trade secret laws to establish

and maintain proprietary rights in our technology and products.

However, these legal means afford only limited protection and may

not adequately protect our rights or permit us to gain or keep a

competitive advantage. Patents and patent applications for the

products we have may not be broad enough to prevent competitors

from introducing similar products into the market. Our patents or

our attempts to enforce them may not necessarily be upheld by the

courts. Efforts to enforce any of our proprietary rights could be

time-consuming and expensive, which could adversely affect our

business and prospects and divert management’s

attention. There can be no assurance that our proprietary

rights will not be challenged, invalidated or circumvented or that

the rights will in fact provide competitive advantages to

us.

We may be found to infringe on intellectual property rights of

others.

Third

parties, including customers, may in the future assert claims or

initiate litigation related to exclusive patent, copyright,

trademark and other intellectual property rights to technologies

and related standards that are relevant to us. These assertions may

emerge over time as a result of our growth and the general increase

in the pace of patent claim assertions, particularly in the U.S.

Because of the existence of a large number of patents in the

healthcare field, the secrecy of some pending patents and the rapid

rate of issuance of new patents, it is not economically practical

or even possible to determine in advance whether a product or any

of its components infringes or will infringe the patent rights of

others. The asserted claims or initiated litigation can include

claims against us or our manufacturers, suppliers or customers

alleging infringement of their proprietary rights with respect to

our existing or future products or components of those products.

Regardless of the merit of these claims, they can be

time-consuming, result in costly litigation and diversion of

technical and management personnel, or require us to develop a

non-infringing technology or enter into license agreements. Where

claims are made by customers, resistance even to unmeritorious

claims could damage customer relationships. There can be no

assurance that licenses will be available on acceptable terms and

conditions, if at all, or that our indemnification by our suppliers

will be adequate to cover our costs if a claim were brought

directly against us or our customers. Furthermore, because of the

potential for high court awards that are not necessarily

predictable, it is not unusual to find even arguably unmeritorious

claims settled for significant amounts. If any infringement or

other intellectual property claim made against us by any third

party is successful, or if we fail to develop non-infringing

technology or license the proprietary rights on commercially

reasonable terms and conditions, our business could be materially

and adversely affected.

8

RISKS RELATED TO REGULATIONS:

Our business is affected by numerous regulations.

Government

regulation by the U.S. FDA and similar agencies in other countries

is a significant factor in the development, manufacturing and

marketing of our products and in the acquisition or licensing of

new products. Complying with government regulations is often time

consuming and expensive and may involve delays or actions adversely

impacting the marketing and sale of our current or future

products.

Following

initial regulatory approval of any products that we may develop, we

will be subject to continuing regulatory review, including review

of adverse (drug or device) experiences or reactions and clinical

results that are reported after our products become commercially

available. This would include results from any post-marketing tests

or continued actions required as a condition of approval. The

manufacturing facilities we use (and may use) to make any of our

products may become subject to periodic review and inspection by

the FDA. If a previously unknown problem with a product or a

manufacturing and laboratory facility used or contracted by us is

discovered, the FDA may impose restrictions on that product or on

the manufacturing facility, including requiring us to withdraw the

product from the market. Any changes to an approved product,

including the way it is manufactured or promoted, often requires

FDA approval before the product, as modified, can be marketed. In

addition, for products we develop in the future, we and our

contract manufacturers may be subject to ongoing FDA requirements

for submission of safety and other post-market information. If we

violate regulatory requirements at any stage, whether before or

after marketing approval is obtained, we may be fined, be forced to

remove a product from the market or experience other adverse

consequences, which would materially harm our financial results.

Additionally, we may not be able to obtain the labeling claims

necessary or desirable for product promotion.

Further,

various healthcare reform proposals have emerged at the federal and

state levels. We cannot predict whether foreign, federal, state or

local healthcare reform legislation or regulation affecting our

business may be proposed or enacted in the future, or what effect

any such legislation or regulation would have on our business. The

implementation of new legislation and regulation may lower

reimbursements for our products or reduce medical procedure

volumes, which would likely adversely affect our business. In

addition, the enacted excise tax may materially and adversely

affect our business.

Distribution

of our products outside the U.S. is subject to extensive government

regulation. These regulations, including the requirements for

approvals or clearance to market; the time required for regulatory

review and the sanctions imposed for violations, vary from country

to country. We do not know whether we will obtain regulatory

approvals in such countries or that we will not be required to

incur significant costs in obtaining or maintaining these

regulatory approvals.

If we fail to obtain or experience significant delays in obtaining

regulatory clearances or approvals to market future medical device

products, we will be unable to commercialize these products until

such clearance or approval is obtained.

The

developing, testing, manufacturing, marketing and selling of

medical devices is subject to extensive regulation by governmental

authorities in the U.S. and other countries. The process of

obtaining regulatory clearance and approval of certain medical

technology products is costly and time consuming. Inherent in the

development of new medical products is the potential for delay

because product testing, including clinical evaluation, is required

before many products can be approved for human use. With respect to

medical devices, such as those that we manufacture and market,

before a new medical device, or a new use of, or claim for, an

existing product can be marketed (unless it is a Class I device),

it must first receive either premarket clearance under Section

510(k) of the Federal Food, Drug and Cosmetic Act or approval of a

premarket approval application, or PMA, from the FDA, unless an

exemption applies. In the 510(k)-clearance process, the FDA must

determine that the proposed device is “substantially

equivalent” to a device legally on the market, known as a

“predicate” device, with respect to intended use,

technology and safety and effectiveness to clear the proposed

device for marketing. Clinical data is sometimes required to

support substantial equivalence. The PMA approval pathway requires

an applicant to demonstrate the safety and effectiveness of the

device for its intended use based, in part, on extensive data

including, but not limited to, technical, preclinical, clinical

trial, manufacturing and labeling data. The premarket approval

process is typically required for devices that are deemed to pose

the greatest risk, such as life-sustaining, life-supporting or

implantable devices. Both the 510(k) and premarket approval

processes can be expensive and lengthy and entail significant user

fees.

Failure

to comply with applicable regulatory requirements can result in,

among other things, suspension or withdrawal of approvals or

clearances, seizure or recall of products, injunctions against the

manufacture, holding, distribution, marketing and sale of a product

and civil and criminal sanctions. Furthermore, changes in existing

regulations or the adoption of new regulations could prevent us

from obtaining, or affect the timing of, future regulatory

approvals. Meeting regulatory requirements and evolving government

standards may delay marketing of our new products for a

considerable period of time, impose costly procedures upon our

activities and result in a competitive advantage to larger

companies that compete against us.

9

We

cannot assure you that the FDA or other regulatory agencies will

clear or approve any products developed by us on a timely basis, if

at all, or, if granted, that clearance or approval will not entail

limiting the indicated uses for which we may market the product,

which could limit the potential market for any of these

products.

Changes to the FDA clearance and approval processes or ongoing

regulatory requirements could make it more difficult for us to

obtain FDA clearance or, approval of new products or comply with

ongoing requirements.

New

government regulations may be enacted and changes in FDA policies

and regulations and, their interpretation and enforcement, could

prevent or delay regulatory clearance or approval of new products.

We cannot predict the likelihood, nature or extent of adverse

government regulation that may arise from future legislation or

administrative action, either in the U.S. or abroad. Therefore, we

do not know whether we will be able to continue to comply with such

regulations or whether the costs of such compliance will have a

material adverse effect on our business. Changes could, among other

things, require different labeling, monitoring of patients,

interaction with physicians, education programs for patients or

physicians, curtailment of necessary supplies, or limitations on

product distribution. These changes, or others required by the FDA

could have an adverse effect on our business, and specifically, on

the sales of these products. The evolving and complex nature of

regulatory science and regulatory requirements, the broad authority

and discretion of the FDA and the generally high level of

regulatory oversight results in a continuing possibility that from

time to time, we will be adversely affected by regulatory actions

despite ongoing efforts and commitment to achieve and maintain full

compliance with all regulatory requirements. If we are not able to

maintain regulatory compliance, we will not be permitted to market

our products and our business would suffer.

Modifications to our current products may require new marketing

clearances or approvals or require us to cease marketing or recall

the modified products until such clearances or approvals are

obtained.

Any

modification to an FDA-cleared product that could significantly

affect its safety or efficacy, or that would constitute a major

change or modification in its intended use, requires a new FDA

510(k) clearance or, possibly, a premarket approval (PMA). The FDA

requires every manufacturer to make its own determination as to

whether a modification requires a new 510(k) clearance or PMA, but

the FDA may review and disagree with any decision reached by the

manufacturer. In the future, we may make additional modifications

to our products after they have received FDA clearance or approval

and, in appropriate circumstances, determine that new clearance or

approval is unnecessary. Regulatory authorities may disagree with

our decisions not to seek new clearance or approval and may require

us to obtain clearance or approval for previous modifications to

our products. If that were to occur for a previously cleared or

approved product, we may be required to cease marketing or recall

the modified device until we obtain the necessary clearance or

approval. Under these circumstances, we may also be subject to

significant regulatory fines or other penalties. If any of the

foregoing were to occur, our financial condition and results of

operations could be negatively impacted.

Changes in reimbursement policies and regulations by governmental

or other third-party payers may have an adverse impact on the use

of our products.

A

significant portion of our wound care products are purchased

principally for the Medicare and Medicaid eligible population by

hospital outpatient clinics, wound care clinics, durable medical

equipment (DME) suppliers and skilled nursing facilities (SNFs),

which typically bill various third-party payers, primarily state

and federal healthcare programs (e.g., Medicare and Medicaid), and

managed care plans, for the products and services provided to their

patients. Although our wound care products are currently eligible

for reimbursement under Medicare Part B, adjustments to our

reimbursement amounts or a change in Centers for Medicare &

Medicaid Services’ (CMS) reimbursement policies could have an

adverse effect on our market opportunities in this area. The

ability of our customers to obtain appropriate reimbursement for

products and services from third-party payers is critical to the

success of our business because reimbursement status affects which

products our customers purchase and the prices they are willing to

pay. In addition, our ability to obtain reimbursement approval in

foreign jurisdictions may affect our ability to expand our product

offerings internationally.

Third-party

payers have adopted, and are continuing to adopt, a number of

policies intended to curb rising healthcare costs. These policies

include the imposition of conditions of payment by foreign, state

and federal healthcare programs as well as private insurance plans,

and the reduction in reimbursement amounts applicable to specific

products and services.

Changes

in healthcare systems in the U.S. or internationally in a manner

that significantly reduces reimbursement for procedures using our

products or denies coverage for these procedures would also have an

adverse impact on the acceptance of our products and the prices

which our customers are willing to pay for them.

10

We and our sales personnel, whether employed by us or by others,

must comply with various federal and state anti-kickback,

self-referral, false claims and similar laws, any breach of which

could cause a material adverse effect on our business.

Our

relationships with physicians, hospitals and the marketers of our

products are subject to scrutiny under various federal

anti-kickback, self-referral, false claims and similar laws, often

referred to collectively as healthcare fraud and abuse laws.

Healthcare fraud and abuse laws are complex, and even minor,

inadvertent violations can give rise to liability, or claims of

alleged violations. Possible sanctions for violation of these fraud

and abuse laws include monetary fines, civil and criminal

penalties, exclusion from federal healthcare programs, including

Medicare, Medicaid, the Veterans Administration, Department of

Defense, Public Health Service (PHS), and forfeiture of amounts

collected in violation of such prohibitions could occur. Certain

states have similar fraud and abuse laws that also authorize

substantial civil and criminal penalties for violations. Any

government investigation or a finding of a violation of these laws

may result in an adverse effect on our business. The federal

Anti-Kickback Statute prohibits any knowing and willful offer,

payment, solicitation or receipt of any form of remuneration in

return for the referral of an individual or the ordering or

recommending of the use of a product or service for which payment

may be made by any federal healthcare program, including

Medicare.

The

scope and enforcement of the healthcare fraud and abuse laws is

uncertain and is subject to rapid change. There can be no assurance

that federal or state regulatory or enforcement agencies will not

investigate or challenge our current or future activities under

these laws. Any state or federal investigation, regardless of the

outcome, could be costly and time-consuming. Additionally, we

cannot predict the impact of any changes in these laws, whether

these changes are retroactive or will have effect on a

going-forward basis only.

If we

engage additional physicians on a consulting basis, the agreements

with these physicians will be structured to comply with all

applicable laws, including the federal ban on physician

self-referrals (commonly known as the “Stark Law”) the

federal Anti-Kickback Statute, state anti-self-referral and

anti-kickback laws. Even so, it is possible that regulatory or

enforcement agencies or courts may view these agreements as

prohibited arrangements that must be restructured or for which we

would be subject to other significant civil or criminal penalties.

Because our strategy includes the involvement of physicians who

consult with us on the design of our products, we could be

materially impacted if regulatory or enforcement agencies or courts

interpret our financial relationships with our physician advisors

who refer or order our products to be in violation of one or more

health care fraud and abuse laws. Such government action could harm

our reputation and the reputations of our physician advisors. In

addition, the cost of noncompliance with these laws could be

substantial because we could be subject to monetary fines and civil

or criminal penalties, and we could also be excluded from state and

federal healthcare programs, including Medicare and Medicaid, for

non-compliance.

RISKS RELATED TO OUR GOVERNING DOCUMENTS OR OUR COMMON

STOCK:

The trading price of the shares of our common stock is highly

volatile, and purchasers of our common stock could incur

substantial losses.

The

market price of our common stock has been and is likely to continue

to be highly volatile and could fluctuate widely in response to

various factors, many of which are beyond our control, including

the following:

●

technological

innovations or new products and services by us or by our

competitors;

●

additions

or departures of key personnel;

●

sales

of our common stock;

●

our

ability to execute our business plan;

●

loss of

any strategic relationship;

●

industry

developments;

●

fluctuations

in stock market prices and trading volumes of similar

companies;

●

economic,

political and other external factors;

●

period-to-period

fluctuations in our financial results;

●

regulatory

developments in the U.S. and foreign countries, both generally or

specific to us and our products; and

●

intellectual

property, product liability or other litigation against us;

and

●

Relatively

low trading volume

Although

publicly traded securities are subject to price and volume

fluctuations, it is likely that our common stock will experience

these fluctuations to a greater degree than the securities of more

established and better capitalized organizations.

11

Our common stock does not have a vigorous trading market and you

may not be able to sell your securities when desired.

Although

there is a public market for our common stock, trading volume has

been historically low, which could impact the stock price and the

ability to sell shares of our common stock. We can give no

assurance that a more active and liquid public market for the

shares of our common stock will develop in the future.

The potential sale of large amounts of common stock may have a

negative effect upon the market value of our shares.

Sales

of a significant number of shares of our common stock in the public

market could harm the market price of our common stock and make it

more difficult for us to raise funds through future offerings of

common stock. As additional shares of our common stock become

available for resale in the public market, the supply of our common

stock will increase, which could decrease the price of our common

stock.

In

addition, future sales of large amounts of common stock could

adversely affect or inhibit our ability to raise

capital.

We have not paid, and we are unlikely to pay cash dividends on our

securities in the near future.

We have

not paid and do not currently intend to pay dividends on our common

stock, which may limit the current return available on an

investment in our stock. Future dividends on our stock, if any,

will depend on our future earnings, capital requirements, financial

condition and such other factors as our management personnel may

consider relevant. Currently, we intend to retain earnings, if any,

to increase our net worth and reserves.

A few of our existing shareholders own a large percentage of our

voting stock and have control over matters requiring stockholder

approval and may delay or prevent a change in control.

Our

directors own and through their affiliates control a large

percentage of our common stock (See “Item 12. Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters”). As a result, our directors and their

affiliates could have the ability to exert substantial influence

over all matters requiring approval by our shareholders, including

the election and removal of directors and any proposed merger,

consolidation or sale of all or substantially all of our assets as

well as other corporate transactions. This concentration of control

could be disadvantageous to other shareholders having different

interests. This significant concentration of share ownership may

adversely affect the trading price for our common stock because

investors sometimes perceive disadvantages in owning stock in

companies with controlling stockholders. In addition, our

Certificate of Formation contains a provision which under the Texas

Business Organizations Code could allow the large shareholders who

own a majority of the common stock to approve certain major

transactions without the approval of other shareholders that

otherwise would be required under Texas corporation

law.

Our Board can authorize the issuance of preferred stock, which

could diminish the rights of holders of our common stock and make a

change of control of the Company more difficult even if it might

benefit our shareholders.

The

Board is authorized to issue shares of preferred stock in one or

more series and to fix the voting powers, preferences and other

rights and limitations of the preferred stock. Accordingly, we may

issue shares of preferred stock with a preference over our common

stock with respect to dividends or distributions on liquidation or

dissolution, or that may otherwise adversely affect the voting or

other rights of the holders of common stock. Issuances of preferred

stock, depending upon the rights, preferences and designations of

the preferred stock, may have the effect of delaying, deterring or

preventing a change of control, even if that change of control

might benefit our shareholders.

FORWARD-LOOKING STATEMENTS:

When

used in this Form 10-K or other filings by the Company with the

Securities and Exchange Commission, in the Company’s press

releases or other public or shareholder communications, or in oral

statements made with the approval of an authorized officer of the

Company’s executive officers, the words or phrases

“would be”, “will allow”, “intends

to”, “will likely result”, “are expected

to”, “will continue”, “is

anticipated”, “estimate”, “project”,

“plan”, “believe” or similar expressions

are intended to identify “forward-looking statements”

within the meaning of the Private Securities Litigation Reform Act

of 1995.

The

Company cautions readers not to place undue reliance on any

forward-looking statements, which speak only as of the date made,

and advises readers that forward-looking statements involve various

risks and uncertainties. Our management believes its assumptions

are based upon reasonable data derived from and known about our

business and operations. No assurances are made that our actual

results of operations or the results of our future activities will

not differ materially from these assumptions. The Company does not

undertake, and specifically disclaims any obligation, to update any

forward-looking statements to reflect occurrences or unanticipated

events or circumstances after the date of such

statement.

12

ITEM 1B. UNRESOLVED STAFF

COMMENTS

None.

ITEM 2. PROPERTIES

The

Company periodically enters into operating lease contracts for

office space and equipment. Arrangements are evaluated at inception

to determine whether such arrangements constitute a lease. In

accordance with the transition guidance of Accounting Standards

Codification (“ASC”) Topic No. 842, such arrangements

are included in our balance sheet as of January 1,

2019.

Right

of use assets, which we refer to as “ROU assets,”

represent the right to use an underlying asset for the lease term,

and lease

liabilities represent the obligation to make lease payments arising

from the lease. Operating lease ROU assets and liabilities were

recognized at the transition date based on the present value of

lease payments over the respective lease terms, with the office

space ROU asset adjusted for deferred rent

liability.

The Company has two operating leases: an office space lease with a

remaining lease term of 54 months and a copier lease with a remaining lease

term of 19 months as of

December 31, 2019. In accordance with

the transition guidance of ASC 842, such arrangements are included

in our balance sheet as of January 1, 2019. All other leases are

short-term leases for which practical expediency has been elected

to not recognize lease assets and lease

liabilities.

In

March 2017, and as amended in March 2018, the Company executed a

new office lease effective April 1, 2019 for office space located

at 1200 Summit Ave., Suite 414, Fort Worth, TX 76102. On July 1,

2019, the Company amended its office lease agreement related to its

current office space located at 1200 Summit Ave., Suite 414, Fort

Worth, TX 76102. The amended lease became effective on August 22,

2019 upon completion by landlord of certain leasehold improvements.

Under the terms of the amended lease agreement, the Company leased

an

additional 1,682 rentable square feet of office space which brought

the total square footage leased to 5,877. The amended lease

agreement extends the original term of the lease for a period of 36

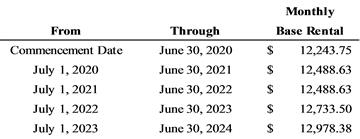

months through June 30, 2024. The monthly base rental payments are

as follows:

As the implicit rate in the leases is not determinable, the

discount rate applied to determine the present value of lease

payments is the borrowing rate on our line of credit. The office

space lease agreement contains no renewal terms, so no lease

liability is recorded beyond the termination date. The copier lease

can be automatically renewed but no lease liability is recorded

beyond the initial termination date as exercising this option is

not reasonably certain.

In

accordance with ASC 842, the Company has recorded lease assets of

$585,251 and a related lease liability of $598,917 as of December

31, 2019. Cash paid for amounts included in measurement of

operating lease liabilities as of December 31, 2019 was

$95,530 The present value

of our operating lease liabilities is shown below.

Maturity of Operating Lease Liabilities

|

|

December 31,

2019

|

|

2020

|

$150,887

|

|

2021

|

151,317

|

|

2022

|

151,333

|

|

2023

|

154,271

|

|

2024

|

77,870

|

|

Total lease

payments

|

685,678

|

|

Less imputed

interest

|

(86,761)

|

|

Present value of

lease liabilities

|

$598,917

|

As of

December 31, 2019, our operating leases have a weighted average

remaining lease term of 4.5 years and a weighted average discount

rate of 6.25%.

ITEM 3. LEGAL PROCEEDINGS

As of

December 31, 2019, and as of this filing date, the Company has no

outstanding legal proceedings.

ITEM 4. MINE SAFETY

DISCLOSURES

This

item is not applicable.

13

PART II

ITEM 5. MARKET FOR REGISTRANT’S

COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF

EQUITY SECURITIES

The

Company’s common stock is traded on OTCQB market of the OTC

Markets Group under the trading symbol “SMTI.” OTCQB is

one of three tiers established by OTC Markets Group, Inc.

Reverse Stock

Split and Reduction of Authorized Capital Stock

On

May 10, 2019, the Company completed a recapitalization of the

Company which included:

(1) a

1-for-100 reverse stock split of the outstanding Common Stock under

which every shareholder received one share of Common Stock for

every 100 shares of Common Stock held;

(2) the

reduction of the authorized capital stock of the Company to

20,000,000 shares of Common Stock and 2,000,000 shares of preferred

stock; and

(3) the

change of the name of the Company from “Wound Management

Technologies, Inc.” to “Sanara MedTech

Inc.”

In

addition, on June 6, 2019 the Company changed the trading symbol of

its Common Stock to “SMTI”. The post-split Common Stock

is traded under the CUSIP number 79957L100. In connection with the

reverse stock split, the Company adjusted the conversion and voting

provisions of the Series F Convertible Preferred Stock by a factor

of 100 and proportionately adjusted the Company's outstanding

employee stock options.

Record Holders

As of

February 21, 2020, there were 207 shareholders of record and there

were 6,023,732 shares of common stock issued and

outstanding.

The

holders of the common stock are entitled to one vote for each share

held of record on all matters submitted to a vote of shareholders.

Holders of the common stock have no preemptive rights and no right

to convert their common stock into any other securities. There is

no redemption or sinking fund provisions applicable to the common

stock.

Dividends

We have

never declared or paid any cash dividends on our common stock and

we do not intend to pay cash dividends in the foreseeable future.

We currently expect to retain any future earnings to fund our

operations and the expansion of our business.

Recent Sales of Unregistered Securities

Set

forth below is information regarding the issuance and sales of the

Company’s securities without registration for the years ended

December 31, 2018, and 2019:

On

March 6, 2018, the Company issued 226,514 shares of Common Stock

for the conversion of $1,200,000 in convertible debt held by

related parties and $385,594 in accrued interest. In February and

March 2018, the Company issued 1,005,677 shares of Common Stock for

the conversion of 85,561 shares of Series C Convertible Preferred

Stock and $1,050,468 of related Series C Preferred Stock

dividends.

On

October 15, 2019, the “Company closed a private placement

offering of 1,204,820 shares of its common stock at a price of

$8.30 per share. All shares were sold by the Company as newly

issued shares. The purchasers in the offering consist of related

party entities to three members of the Company’s Board of

Directors. The transaction was approved by all of the disinterested

Directors of the Company. The price per share was determined by a

special committee of the Board comprised of disinterested Directors

who considered an independent third-party valuation of the offering

price and other relevant information.

ITEM 6. SELECTED FINANCIAL

DATA

As a

smaller reporting company, we are not required to provide this

information.

14

ITEM 7. MANAGEMENT’S DISCUSSION

AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

The

following discussion and analysis contain forward-looking

statements about future revenues, operating results, plans and

expectations. Forward-looking statements are based on a number of

assumptions and estimates that are inherently subject to

significant risks and uncertainties and our results could differ

materially from the results anticipated by our forward-looking

statements as a result of many known or unknown factors, including,

but not limited to, those factors discussed in Part I, Item 1A.

Risk Factors. In addition, the following discussion should be read

in conjunction with Part 1 of this report on Form 10-K as well as

with our consolidated financial statements and the related Notes

contained in Item 8 of this report.

Overview

The

Company’s business is developing, marketing, and distributing

wound and skin care products to physicians, hospitals, clinics and

post-acute care settings. Our products are primarily sold in the

North American advanced wound care and surgical tissue repair

markets. Sanara MedTech products include CellerateRX® Surgical

Activated Collagen® Adjuvant (“CellerateRX”);

HYCOL™ Hydrolyzed Collagen (“HYCOL”);

BIAKŌS™ Antimicrobial Skin & Wound Cleanser

(“BIAKŌS AWC”); and PULSAR II™ Advanced

Wound Irrigation System.

Liquidity and Capital Resources

Cash on

hand at December 31, 2019 was $6,611,928, compared to $176,421 at

December 31, 2018. Based on our current plan of operations, we

believe this amount, when combined with expected cash flows from

operations and amounts available under our revolving credit

facility will be sufficient to fund our growth strategy and to meet

our anticipated cash needs for at least the next twelve

months.

On

October 15, 2019, the Company closed a private placement offering

of 1,204,820 shares of its Common Stock at a price of $8.30 per

share. The $10 million of cash proceeds of the offering are

expected to be used to fund milestone payments under current and

future product license agreements, repayment of indebtedness under

the Company’s bank line of credit, and operating

expenditures, clinical studies and continued expansion of the

Company’s sales force. On October 16, 2019, the Company paid

down the entire balance of the line of credit of $2,200,000 with

cash proceeds received through the private placement stock

offering.

During

2018 and 2019, our principal sources of liquidity have been our

cash generated from operations, cash provided through a bank line

of credit, and more recently, through a private placement offering

discussed above. Cash consists of cash on deposit with banks.

Historically, we have financed our operations primarily from the

sale of debt and equity securities. No financing activities

occurred in 2018.

We

monitor our cash flow, assess our business plan, and make

expenditure adjustments accordingly. If appropriate, we may pursue

limited financing including issuing additional equity and/or

incurring additional debt. Although we have successfully funded our

past operations through additional bank debt and issuance of

equity, there is no assurance that our capital raising efforts will

be able to attract additional necessary capital at prices

attractive to the Company. If we are unable to obtain additional

funding for operations at any time in the future, we may not be

able to continue operations as proposed. This would require us to

modify our business plan, which could curtail various aspects of

our operations.

In

December 2018, and as amended in June 2019, the Company executed