Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - SHENANDOAH TELECOMMUNICATIONS CO/VA/ | shenex991093029ca.htm |

| EX-32 - EXHIBIT 32 - SHENANDOAH TELECOMMUNICATIONS CO/VA/ | shenex3209302018.htm |

| EX-31.2 - EXHIBIT 31.2 - SHENANDOAH TELECOMMUNICATIONS CO/VA/ | shenex31209302018.htm |

| EX-31.1 - EXHIBIT 31.1 - SHENANDOAH TELECOMMUNICATIONS CO/VA/ | shenex31109302018.htm |

UNITED STATES OF AMERICA

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

FORM 10-Q

(Mark One)

☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2018 | |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from__________ to __________ | |

Commission File No.: 000-09881

SHENANDOAH TELECOMMUNICATIONS COMPANY

(Exact name of registrant as specified in its charter)

VIRGINIA | 54-1162807 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

500 Shentel Way, Edinburg, Virginia 22824

(Address of principal executive offices) (Zip Code)

(540) 984-4141

(Registrant's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☑ | Accelerated filer ☐ | Non-accelerated filer ☐ |

Smaller reporting company☐ | Emerging growth company☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The number of shares of the registrant’s common stock outstanding on November 2, 2018 was 49,558,663.

SHENANDOAH TELECOMMUNICATIONS COMPANY

INDEX

Page Numbers | ||||

PART I. | FINANCIAL INFORMATION | |||

Item 1. | Financial Statements | |||

- | ||||

Item 2. | - | |||

Item 3. | ||||

Item 4. | ||||

PART II. | OTHER INFORMATION | |||

Item 1A. | ||||

Item 2. | ||||

Item 6. | ||||

SHENANDOAH TELECOMMUNICATIONS COMPANY AND SUBSIDIARIES | ||||||||

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS | ||||||||

(in thousands) | ||||||||

September 30, 2018 | December 31, 2017 | |||||||

ASSETS | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 75,207 | $ | 78,585 | ||||

Accounts receivable, net | 59,968 | 54,184 | ||||||

Income taxes receivable | 2,545 | 17,311 | ||||||

Inventory, net | 4,962 | 5,704 | ||||||

Prepaid expenses and other | 63,383 | 17,111 | ||||||

Total current assets | 206,065 | 172,895 | ||||||

Investments | 12,296 | 11,472 | ||||||

Property, plant and equipment, net | 669,709 | 686,327 | ||||||

Other assets: | ||||||||

Intangible assets, net | 381,537 | 380,979 | ||||||

Goodwill | 146,497 | 146,497 | ||||||

Deferred charges and other assets, net | 53,723 | 13,690 | ||||||

Total assets | $ | 1,469,827 | $ | 1,411,860 | ||||

LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

Current liabilities: | ||||||||

Current maturities of long-term debt, net of unamortized loan fees | $ | 84,743 | $ | 64,397 | ||||

Accounts payable | 23,868 | 28,953 | ||||||

Advanced billings and customer deposits | 7,415 | 21,153 | ||||||

Accrued compensation | 6,833 | 9,167 | ||||||

Accrued liabilities and other | 14,756 | 13,914 | ||||||

Total current liabilities | 137,615 | 137,584 | ||||||

Long-term debt, less current maturities, net of unamortized loan fees | 694,045 | 757,561 | ||||||

Other long-term liabilities: | ||||||||

Deferred income taxes | 120,846 | 100,879 | ||||||

Deferred lease | 22,162 | 15,782 | ||||||

Asset retirement obligations | 22,372 | 21,211 | ||||||

Retirement plan obligations | 13,235 | 13,328 | ||||||

Other liabilities | 14,567 | 15,293 | ||||||

Total other long-term liabilities | 193,182 | 166,493 | ||||||

Shareholders’ equity: | ||||||||

Common stock, no par value, authorized 96,000; 49,559 and 49,328 issued and outstanding at September 30, 2018 and December 31, 2017, respectively | — | — | ||||||

Additional paid in capital | 47,350 | 44,787 | ||||||

Retained earnings | 385,045 | 297,205 | ||||||

Accumulated other comprehensive income (loss), net of taxes | 12,590 | 8,230 | ||||||

Total shareholders’ equity | 444,985 | 350,222 | ||||||

Total liabilities and shareholders’ equity | $ | 1,469,827 | $ | 1,411,860 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

3

SHENANDOAH TELECOMMUNICATIONS COMPANY AND SUBSIDIARIES | |||||||||||||||

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS) | |||||||||||||||

(in thousands, except per share amounts) | |||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

Operating revenue: | 2018 | 2017 | 2018 | 2017 | |||||||||||

Service revenue and other | $ | 142,768 | $ | 149,788 | $ | 419,819 | $ | 450,617 | |||||||

Equipment revenue | 15,963 | 1,994 | 49,551 | 8,303 | |||||||||||

Total operating revenue | 158,731 | 151,782 | 469,370 | 458,920 | |||||||||||

Operating expenses: | |||||||||||||||

Cost of services | 47,886 | 48,552 | 146,362 | 145,744 | |||||||||||

Cost of goods sold | 15,036 | 7,282 | 46,007 | 17,232 | |||||||||||

Selling, general and administrative | 27,452 | 42,199 | 86,117 | 125,374 | |||||||||||

Acquisition, integration and migration expenses | — | 1,706 | — | 9,873 | |||||||||||

Depreciation and amortization | 40,028 | 42,568 | 124,632 | 132,297 | |||||||||||

Total operating expenses | 130,402 | 142,307 | 403,118 | 430,520 | |||||||||||

Operating income (loss) | 28,329 | 9,475 | 66,252 | 28,400 | |||||||||||

Other income (expense): | |||||||||||||||

Interest expense | (9,001 | ) | (9,823 | ) | (27,184 | ) | (28,312 | ) | |||||||

Gain (loss) on investments, net | 88 | 202 | 112 | 395 | |||||||||||

Non-operating income (loss), net | 966 | 1,003 | 2,770 | 3,482 | |||||||||||

Income (loss) before income taxes | 20,382 | 857 | 41,950 | 3,965 | |||||||||||

Income tax expense (benefit) | 4,848 | (2,677 | ) | 10,207 | (1,830 | ) | |||||||||

Net income (loss) | 15,534 | 3,534 | 31,743 | 5,795 | |||||||||||

Other comprehensive income (loss): | |||||||||||||||

Unrealized gain (loss) on interest rate hedge, net of tax | 465 | 6 | 4,360 | (770 | ) | ||||||||||

Comprehensive income (loss) | $ | 15,999 | $ | 3,540 | $ | 36,103 | $ | 5,025 | |||||||

Net income (loss) per share, basic and diluted: | |||||||||||||||

Basic net income (loss) per share | $ | 0.31 | $ | 0.07 | $ | 0.64 | $ | 0.12 | |||||||

Diluted net income (loss) per share | $ | 0.31 | $ | 0.07 | $ | 0.63 | $ | 0.12 | |||||||

Weighted average shares outstanding, basic | 49,559 | 49,133 | 49,527 | 49,100 | |||||||||||

Weighted average shares outstanding, diluted | 50,117 | 49,959 | 50,044 | 49,869 | |||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

4

SHENANDOAH TELECOMMUNICATIONS COMPANY AND SUBSIDIARIES | |||||||||||||||||||

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY | |||||||||||||||||||

(in thousands, except share amounts) | |||||||||||||||||||

Shares of Common Stock (no par value) | Additional Paid in Capital | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Total | |||||||||||||||

Balance, December 31, 2017 | 49,328 | $ | 44,787 | $ | 297,205 | $ | 8,230 | $ | 350,222 | ||||||||||

Change in accounting principle - adoption of accounting standard (Note 2) | — | — | 56,097 | — | 56,097 | ||||||||||||||

Net income (loss) | — | — | 31,743 | — | 31,743 | ||||||||||||||

Other comprehensive gain (loss), net of tax of $1,441 | — | — | — | 4,360 | 4,360 | ||||||||||||||

Stock based compensation | 206 | 4,578 | — | — | 4,578 | ||||||||||||||

Stock options exercised | 15 | 104 | — | — | 104 | ||||||||||||||

Common stock issued | — | 18 | — | — | 18 | ||||||||||||||

Shares retired for settlement of employee taxes upon issuance of vested equity awards | (66 | ) | (2,137 | ) | — | — | (2,137 | ) | |||||||||||

Common stock issued to acquire non-controlling interest in nTelos | 76 | — | — | — | — | ||||||||||||||

Balance, September 30, 2018 | 49,559 | $ | 47,350 | $ | 385,045 | $ | 12,590 | $ | 444,985 | ||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

5

SHENANDOAH TELECOMMUNICATIONS COMPANY AND SUBSIDIARIES | ||||||||

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | ||||||||

(in thousands) | ||||||||

Nine Months Ended September 30, | ||||||||

2018 | 2017 | |||||||

Cash flows from operating activities: | ||||||||

Net income (loss) | $ | 31,743 | $ | 5,795 | ||||

Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||

Depreciation | 106,002 | 113,437 | ||||||

Amortization | 18,630 | 18,860 | ||||||

Amortization reflected as rent expense in cost of services | 372 | 2,173 | ||||||

Bad debt expense | 1,362 | 1,479 | ||||||

Stock based compensation expense, net of amount capitalized | 4,578 | 3,053 | ||||||

Waived management fee | 28,164 | 27,068 | ||||||

Deferred income taxes | (1,989 | ) | (12,251 | ) | ||||

(Gain) loss on investments | (112 | ) | (308 | ) | ||||

Net (gain) loss from patronage and equity investments | (2,300 | ) | (2,315 | ) | ||||

Amortization of long-term debt issuance costs | 3,472 | 3,572 | ||||||

Accrued interest and other | 205 | 1,633 | ||||||

Changes in assets and liabilities: | ||||||||

Accounts receivable | (5,492 | ) | 6,418 | |||||

Inventory, net | 741 | 31,604 | ||||||

Income taxes receivable | 14,932 | (8,704 | ) | |||||

Other assets | (13,393 | ) | (162 | ) | ||||

Accounts payable | (1,913 | ) | (30,795 | ) | ||||

Income taxes payable | — | (435 | ) | |||||

Deferred lease | 4,159 | 3,729 | ||||||

Other deferrals and accruals | (361 | ) | (5,146 | ) | ||||

Net cash provided by (used in) operating activities | 188,800 | 158,705 | ||||||

Cash flows from investing activities: | ||||||||

Acquisition of property, plant and equipment | (92,309 | ) | (109,435 | ) | ||||

Proceeds from sale of assets | 540 | 356 | ||||||

Cash distributions (contributions) from investments and other | (1 | ) | 4 | |||||

Sprint expansion | (52,000 | ) | (6,000 | ) | ||||

Net cash provided by (used in) investing activities | (143,770 | ) | (115,075 | ) | ||||

Cash flows from financing activities: | ||||||||

Principal payments on long-term debt | (46,375 | ) | (24,250 | ) | ||||

Proceeds from revolving credit facility borrowings | 15,000 | — | ||||||

Proceeds from credit facility borrowings | — | 25,000 | ||||||

Principal payments on revolving credit facility | (15,000 | ) | — | |||||

Taxes paid for equity award issuances | (2,033 | ) | (5,106 | ) | ||||

Net cash provided by (used in) financing activities | (48,408 | ) | (4,356 | ) | ||||

Net increase (decrease) in cash and cash equivalents | (3,378 | ) | 39,274 | |||||

Cash and cash equivalents, beginning of period | 78,585 | 36,193 | ||||||

Cash and cash equivalents, end of period | $ | 75,207 | $ | 75,467 | ||||

Supplemental Disclosures of Cash Flow Information | ||||||||

Cash payments for: | ||||||||

Interest, net of capitalized interest of $1,187 and $1,266, respectively | $ | 25,067 | $ | 25,934 | ||||

Income tax (refunds received) payments, net | $ | (2,736 | ) | $ | 19,567 | |||

Capital expenditures payable | $ | 11,919 | $ | 3,800 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

6

SHENANDOAH TELECOMMUNICATIONS COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Basis of Presentation

The interim condensed consolidated financial statements of Shenandoah Telecommunications Company and Subsidiaries (collectively, the “Company”) are unaudited. In the opinion of management, all adjustments necessary for a fair presentation of the interim results have been reflected therein in accordance with accounting principles generally accepted in the United States ("GAAP") for interim financial reporting and as required by Rule 10-01 of Regulation S-X. Accordingly, the unaudited condensed consolidated financial statements may not include all of the information and notes required by GAAP for audited financial statements. The information contained herein should be read in conjunction with the audited financial statements included in the Company's Annual Report on Form 10-K for the year ended December 31, 2017.

Immaterial Prior Period Adjustment.

During the three months ended September 30, 2018, the Company determined that the unaudited condensed consolidated financial statements for the three months ended March 31, 2018, and the three and six months ended June 30, 2018, contained an immaterial misstatement. Excess amortization of deferred contract costs that are recognized as a reduction of revenue, as described in Note 2, resulted in an understatement of revenue for the three months ended March 31, 2018, and the three and six months ended June 30, 2018. Additionally, amounts recorded upon the adoption of ASU No. 2014-09, Revenue from Contracts with Customers ("Topic 606", or "the new revenue recognition standard"), on January 1, 2018 were misstated. The Company evaluated the materiality of the prior period adjustment quantitatively and qualitatively, under the SEC’s authoritative guidance on materiality, and concluded that the prior period adjustment was not material to the financial statements of any of the impacted unaudited 2018 periods. The Company elected to correct the prior period adjustment by revising the prior period financial statements.

The cumulative effect of the adjustment made to the consolidated January 1, 2018 balance sheet for the adoption of the new revenue recognition standard was as follows:

As of January 1, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Prepaid expenses and other | $ | 53,688 | $ | (6,701 | ) | $ | 46,987 | ||||

Deferred charges and other assets, net | 29,797 | 14,964 | 44,761 | ||||||||

Deferred income taxes | 119,030 | 2,201 | 121,231 | ||||||||

Retained earnings | 347,240 | 6,062 | 353,302 | ||||||||

The following table presents the effects of the immaterial prior period adjustment on the unaudited condensed consolidated balance sheet as of March 31, 2018 and June 30, 2018:

As of March 31, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Prepaid expenses and other | $ | 64,200 | $ | (5,741 | ) | $ | 58,459 | ||||

Deferred charges and other assets, net | 33,934 | 16,410 | 50,344 | ||||||||

Deferred income taxes | 115,809 | 2,853 | 118,662 | ||||||||

Retained earnings | 352,069 | 7,816 | 359,885 | ||||||||

As of June 30, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Prepaid expenses and other | $ | 64,163 | $ | (4,756 | ) | $ | 59,407 | ||||

Deferred charges and other assets, net | 34,021 | 17,896 | 51,917 | ||||||||

Deferred income taxes | 111,125 | 3,522 | 114,647 | ||||||||

Retained earnings | 359,893 | 9,618 | 369,511 | ||||||||

7

The following tables present the effects of the immaterial prior period adjustment on the unaudited condensed consolidated statements of operations and comprehensive income (loss) for the three months ended March 31, 2018 and the three and six months ended June 30, 2018:

For the Three Months Ended March 31, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Service revenue and other | $ | 134,153 | $ | 2,406 | $ | 136,559 | |||||

Income tax expense (benefit) | 1,176 | 652 | 1,828 | ||||||||

Net income (loss) | 4,829 | 1,754 | 6,583 | ||||||||

Earnings per share - basic | $ | 0.10 | $ | 0.03 | $ | 0.13 | |||||

Earnings per share - diluted | $ | 0.10 | $ | 0.03 | $ | 0.13 | |||||

For the Three Months Ended June 30, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Service revenue and other | $ | 138,021 | $ | 2,471 | $ | 140,492 | |||||

Income tax expense (benefit) | 2,862 | 669 | 3,531 | ||||||||

Net income (loss) | 7,824 | 1,802 | 9,626 | ||||||||

Earnings per share - basic | $ | 0.16 | $ | 0.03 | $ | 0.19 | |||||

Earnings per share - diluted | $ | 0.16 | $ | 0.03 | $ | 0.19 | |||||

For the Six Months Ended June 30, 2018 | |||||||||||

(in thousands) | As Reported | Correction of Error | As Adjusted | ||||||||

Service revenue and other | $ | 272,174 | $ | 4,877 | $ | 277,051 | |||||

Income tax expense (benefit) | 4,038 | 1,321 | 5,359 | ||||||||

Net income (loss) | 12,653 | 3,556 | 16,209 | ||||||||

Earnings per share - basic | $ | 0.26 | $ | 0.07 | $ | 0.33 | |||||

Earnings per share - diluted | $ | 0.25 | $ | 0.07 | $ | 0.32 | |||||

Adoption of New Accounting Principles

There have been no developments related to recently issued accounting standards, including the expected dates of adoption and estimated effects on the Company's unaudited condensed consolidated financial statements and note disclosures, from those disclosed in the Company's 2017 Annual Report on Form 10-K, that would be expected to impact the Company except for the topics discussed below.

The Company adopted ASU No. 2014-09, Revenue from Contracts with Customers ("Topic 606", or "the new revenue recognition standard"), and all related amendments, effective January 1, 2018, using the modified retrospective method as discussed in Note 2, Revenue from Contracts with Customers. The Company recognized the cumulative effect of applying the new revenue recognition standard as an adjustment to the opening balance of retained earnings. The comparative information has not been retrospectively modified and continues to be reported under the accounting standards in effect for those periods.

In February 2016, the Financial Accounting Standards Board (FASB) issued ASU No. 2016-02, Leases (Topic 842), which requires lessees to recognize a right-of-use asset and a lease liability for all leases with terms greater than 12 months. The standard also requires disclosures by lessees and lessors about the amount, timing and uncertainty of cash flows arising from leases, as well as changes in the categorization of rental costs, from rent expense to interest and depreciation expense. Other effects may occur depending on the types of leases and the specific terms of them utilized by particular lessees. The ASU is effective for the Company on January 1, 2019, and early application is permitted. Modified retrospective application is required. The Company expects that the most notable impact to its financial statements upon the adoption of this ASU will be the recognition of a material right-of-use asset and a lease liability for its real estate and equipment leases. The Company is continuing to assess potential impacts that the standard may have on our consolidated financial statements.

8

In February 2018, the FASB issued ASU No. 2018-02, Income Statement - Reporting Comprehensive Income (Topic 220): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income. Under existing U.S. GAAP, the effects of changes in tax rates and laws on deferred tax balances are recorded as a component of income tax expense in the period in which the law was enacted. When deferred tax balances related to items originally recorded in accumulated other comprehensive income are adjusted, certain tax effects become stranded in accumulated other comprehensive income. The amendments in ASU No. 2018-02 allow a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from the 2017 Tax Cuts and Jobs Act. The amendments in this ASU also require certain disclosures about stranded tax effects. The guidance is effective for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. Early adoption in any period is permitted. The Company is currently evaluating the impact of adopting ASU No. 2018-02.

Note 2. Revenue from Contracts with Customers

The Company earns revenue primarily through the sale of our wireless telecommunications services, wireless equipment, and business, residential, and enterprise cable and wireline services that include video, internet, voice, and data services. Revenue earned for the three months ended September 30, 2018 was as follows:

(in thousands) | Wireless | Cable | Wireline | Consolidated | ||||||||||||

Wireless service | $ | 96,299 | $ | — | $ | — | $ | 96,299 | ||||||||

Equipment | 15,666 | 234 | 63 | 15,963 | ||||||||||||

Business, residential and enterprise | — | 29,334 | 10,702 | 40,036 | ||||||||||||

Tower and other | 4,134 | 2,614 | 8,857 | 15,605 | ||||||||||||

Total revenue | 116,099 | 32,182 | 19,622 | 167,903 | ||||||||||||

Internal revenue | (1,263 | ) | (1,266 | ) | (6,643 | ) | (9,172 | ) | ||||||||

Total operating revenue | $ | 114,836 | $ | 30,916 | $ | 12,979 | $ | 158,731 | ||||||||

Revenue earned for the nine months ended September 30, 2018 was as follows:

(in thousands) | Wireless | Cable | Wireline | Consolidated | ||||||||||||

Wireless service | $ | 284,154 | $ | — | $ | — | $ | 284,154 | ||||||||

Equipment | 48,859 | 537 | 155 | 49,551 | ||||||||||||

Business, residential and enterprise | — | 87,931 | 31,906 | 119,837 | ||||||||||||

Tower and other | 10,643 | 7,536 | 26,380 | 44,559 | ||||||||||||

Total revenue | 343,656 | 96,004 | 58,441 | 498,101 | ||||||||||||

Internal revenue | (3,746 | ) | (3,394 | ) | (21,591 | ) | (28,731 | ) | ||||||||

Total operating revenue | $ | 339,910 | $ | 92,610 | $ | 36,850 | $ | 469,370 | ||||||||

Wireless service

The majority of the Company's revenue is earned through providing network access to Sprint under the affiliate agreement, which represents approximately 61% of consolidated revenues for the nine months ended September 30, 2018. Wireless service revenue is variable based on billed revenue to Sprint’s subscribers in the Company's affiliate area, less applicable fees retained by Sprint.

The Company's revenue related to Sprint’s postpaid customers is the amount that Sprint bills its postpaid subscribers, reduced by customer credits, write-offs of receivables, and 8% management and 8.6% service fees. The Company is also charged for the costs of subsidized handsets sold through Sprint’s national channels as well as commissions paid by Sprint to third-party resellers in the Company's service territory.

The Company's revenue related to Sprint’s prepaid customers is the amount that Sprint bills its prepaid subscribers, reduced by costs to acquire and support the customers, based on national averages for Sprint’s prepaid programs, and a 6% management fee.

The Company considers Sprint, rather than Sprint's subscribers, to be the customer under the new revenue recognition standard and the Company's performance obligation is to provide Sprint a series of continuous network access services. The reimbursement to Sprint for the costs of handsets sold through Sprint’s national channels, as well as commissions paid by Sprint to third-party resellers in our service territory represent consideration payable to a customer. These reimbursements are initially recorded as a contract asset and are subsequently recognized as a reduction of revenue over the expected benefit period between 21 and 53 months. Historically, under ASC 605 the customer was considered the subscriber rather than Sprint and as a result, reimbursement

9

payments to Sprint for costs of handsets and commissions were recorded as operating expenses in the period incurred. During 2017, these costs totaled $63.5 million recorded in cost of goods and services, and $16.9 million recorded in selling, general and administrative costs.

On January 1, 2018, upon adoption, the Company recorded a wireless contract asset of approximately $51.1 million. During the three months ended September 30, 2018, payments that increased the wireless contract asset balance totaled $16.4 million and amortization reflected as a reduction of revenue totaled approximately $11.9 million. During the nine months ended September 30, 2018, payments that increased the wireless contract asset balance totaled $44.8 million and amortization reflected as a reduction of revenue totaled approximately $34.1 million. The wireless contract asset balance as of September 30, 2018 was approximately $61.8 million.

Wireless equipment

The Company owns and operates Sprint-branded retail stores within their geographic territory from which the Company sells equipment, primarily wireless handsets, and service to Sprint subscribers. The Company's equipment is predominantly sold to subscribers through Sprint's equipment financing plans. Under the equipment financing plans, Sprint purchases the equipment from the Company and resells the equipment to their subscribers. Historically, under ASC 605, the Company concluded that it was the agent in these equipment financing transactions and recorded revenues net of related handset costs which were approximately $63.8 million in 2017. Under Topic 606 the Company concluded that it is the principal in these equipment financing transactions, as the Company controls and bears the risk of ownership of the inventory prior to sale, and accordingly, revenues and handset costs are recorded on a gross basis, the corresponding cost of the equipment is recorded separately to cost of goods sold.

Business, residential and enterprise

The Company earns revenue in the Cable and Wireline segments from business, residential, and enterprise customers where the performance obligations are to provide cable and telephone network services, sell and lease equipment and wiring services, and lease fiber-optic cable capacity. The Company's arrangements are generally composed of contracts that are cancellable at the customer’s discretion without penalty at any time. As there are multiple performance obligations in these arrangements, the Company recognizes revenue based on the standalone selling price of each distinct good or service. The Company generally recognizes these revenues over time as customers simultaneously receive and consume the benefits of the service, with the exception of equipment sales and home wiring which are recognized as revenue at a point in time when control transfers and when installation is complete, respectively.

Under the new revenue recognition standard, the Company concluded that installation services do not represent a separate performance obligation. Accordingly, installation fees are allocated to services and are recognized ratably over the longer of the contract term or the period the unrecognized portion of the fee remains material to the contract, typically 10 and 11 months for cable and wireline customers, respectively. Historically, the Company deferred these fees over the estimated customer life of 42 months. Additionally, the Company incurs commission and installation costs related to in-house and third-party vendors that were previously expensed as incurred. Under Topic 606, the Company capitalizes and amortizes these commission and installation costs over the expected benefit period which is approximately 44 months, 72 months, and 46 months, for cable, wireline, and enterprise business, respectively.

Tower / Other

Tower revenues consist primarily of tower space leases accounted for under Topic 840, Leases, and Other revenues include network access-related charges for service provided to customers across the segments.

The cumulative effect of the changes made to the consolidated January 1, 2018 balance sheet for the adoption of the new revenue recognition standard were as follows:

10

(in thousands) | Balance at December 31, 2017 | Adjustments due to Topic 606 | Balance at January 1, 2018 | |||||||||

Assets | ||||||||||||

Prepaid expenses and other | $ | 17,111 | $ | 29,876 | $ | 46,987 | ||||||

Deferred charges and other assets, net | 13,690 | 31,071 | 44,761 | |||||||||

Liabilities | ||||||||||||

Advanced billing and customer deposits | 21,153 | (14,302 | ) | 6,851 | ||||||||

Deferred income taxes | 100,879 | 20,352 | 121,231 | |||||||||

Other long-term liabilities | 15,293 | (1,200 | ) | 14,093 | ||||||||

Retained earnings | 297,205 | 56,097 | 353,302 | |||||||||

The impact of the adoption of the new revenue recognition standard on the condensed consolidated statements of operations and comprehensive income (loss) and condensed consolidated balance sheets was as follows:

Three Months Ended September 30, 2018 | ||||||||||||

(in thousands) | As Reported | Balances without Adoption of Topic 606 | Effect of Change Higher/(Lower) | |||||||||

Operating revenue: | ||||||||||||

Service revenue and other | $ | 142,768 | $ | 161,076 | $ | (18,308 | ) | |||||

Equipment revenue | 15,963 | 2,178 | 13,785 | |||||||||

Operating expenses: | ||||||||||||

Cost of services | 47,886 | 48,001 | (115 | ) | ||||||||

Cost of goods sold | 15,036 | 7,870 | 7,166 | |||||||||

Selling, general and administrative | 27,452 | 44,164 | (16,712 | ) | ||||||||

Nine Months Ended September 30, 2018 | ||||||||||||

(in thousands) | As Reported | Balances without Adoption of Topic 606 | Effect of Change Higher/(Lower) | |||||||||

Operating revenue: | ||||||||||||

Service revenue and other | $ | 419,819 | $ | 471,155 | $ | (51,336 | ) | |||||

Equipment revenue | 49,551 | 6,036 | 43,515 | |||||||||

Operating expenses: | ||||||||||||

Cost of services | 146,362 | 146,199 | 163 | |||||||||

Cost of goods sold | 46,007 | 20,316 | 25,691 | |||||||||

Selling, general and administrative | 86,117 | 132,711 | (46,594 | ) | ||||||||

11

As of September 30, 2018 | ||||||||||||

(in thousands) | As Reported | Balances without Adoption of Topic 606 | Effect of Change Higher/(Lower) | |||||||||

Assets | ||||||||||||

Prepaid expenses and other | $ | 63,383 | $ | 27,765 | $ | 35,618 | ||||||

Deferred charges and other assets, net | 53,723 | 17,496 | 36,227 | |||||||||

Liabilities | ||||||||||||

Advanced billing and customer deposits | 7,415 | 23,744 | (16,329 | ) | ||||||||

Deferred income taxes | 120,846 | 97,029 | 23,817 | |||||||||

Other long-term liabilities | 14,567 | 15,759 | (1,192 | ) | ||||||||

Retained earnings | 385,045 | 319,496 | 65,549 | |||||||||

Future performance obligations

On September 30, 2018, the Company had approximately $3.1 million of transaction price allocated to unsatisfied performance obligations, which is exclusive of contracts with original expected duration of one year or less. The Company expects to recognize approximately $0.2 million of this amount as revenue during the remainder of 2018, $0.6 million in 2019, an additional $0.6 million by 2020, and the balance thereafter.

Contract acquisition costs and costs to fulfill contracts

Capitalized contract costs represent contract fulfillment costs and contract acquisition costs which include commissions and installation costs in our Cable and Wireline segments. Capitalized contract costs are amortized on a straight line basis over the contract term plus expected renewals. The Company elected to apply the practical expedient to expense contract acquisition costs when incurred, if the amortization period would be twelve months or less. The amortization of these costs is included in cost of services, and selling, general and administrative expenses. Amounts capitalized were approximately $10.0 million as of September 30, 2018 of which $4.6 million is presented as prepaid expenses and other and $5.4 million is presented as deferred charges and other assets, net. Amortization recognized during the nine months ended September 30, 2018 was approximately $4.1 million.

Note 3. Acquisition

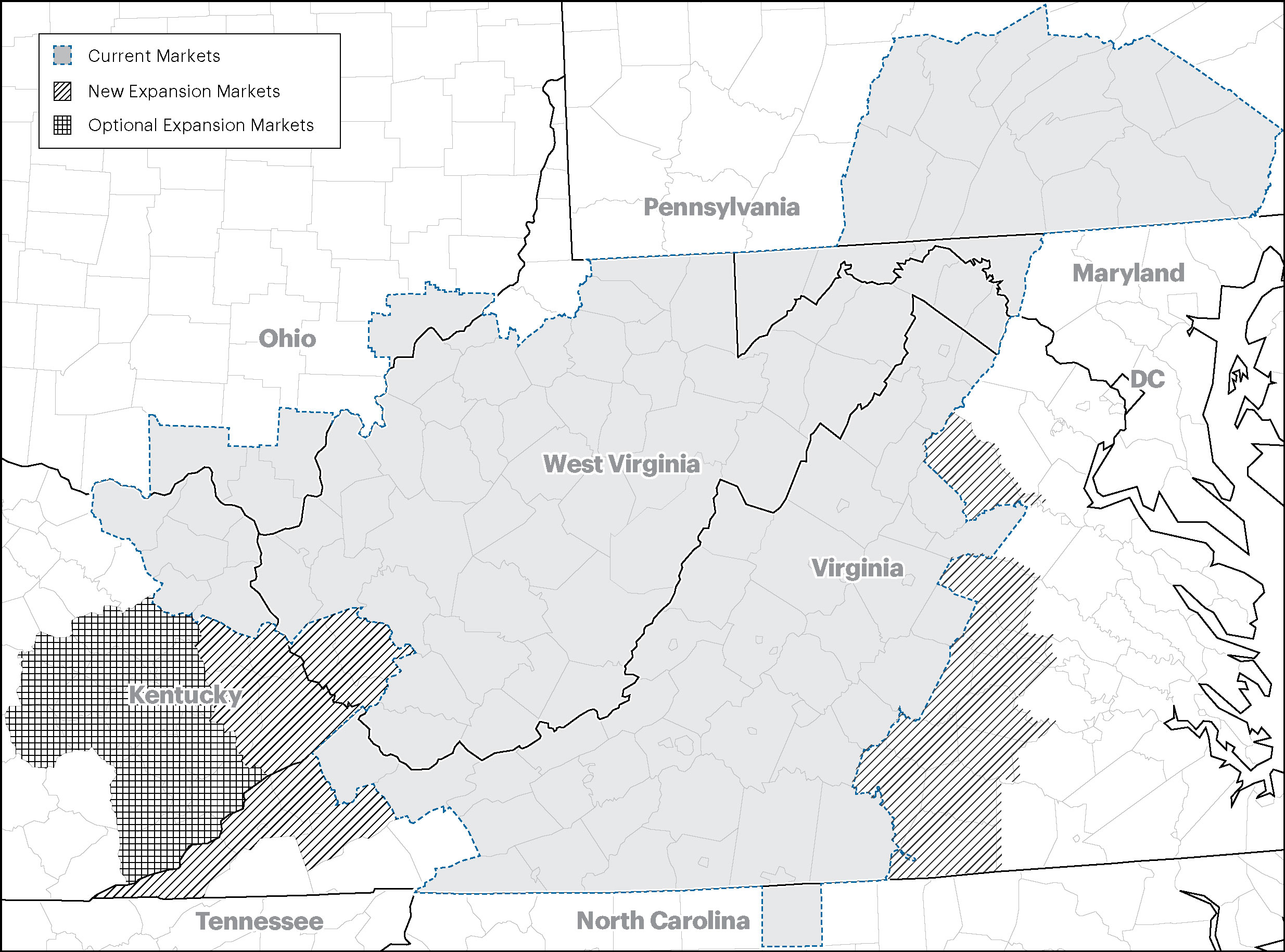

Sprint Territory Expansion: Effective February 1, 2018, the Company signed an expansion agreement with Sprint to expand its wireless service coverage area to include certain areas in Kentucky, Pennsylvania, Virginia and West Virginia, (the “Expansion Area”). The agreement includes certain network build out requirements in the Expansion Area, and the ability to utilize Sprint’s spectrum in the Expansion Area. Pursuant to the expansion agreement, Sprint agreed to, among other things, transition the provision of network coverage in the Expansion Area from Sprint to the Company. The expansion agreement required a payment of $52.0 million for the right to service the Expansion Area pursuant to the Affiliate Agreements plus an additional payment of up to $5.0 million after acceptance of certain equipment at the Sprint cell sites in the Expansion Area. The transaction was accounted for as an asset acquisition.

The Company recorded the following in the wireless segment:

($ in thousands) | Estimated Useful Life (in years) | February 1, 2018 | ||||

Affiliate contract expansion | 12 | $ | 45,148 | |||

Prepayment of tangible assets | 0 | 6,497 | ||||

Off-market leases - favorable | 16.5 | 3,665 | ||||

Off-market leases - unfavorable | 4.2 | (3,310 | ) | |||

Total | $ | 52,000 | ||||

Estimated useful lives are approximate and represent the average of the remaining useful lives as of the acquisition date.

The Company allocated the purchase price to the components identified in the table above based on the relative fair value of each component. The fair value of the components was determined using an income and cost approach.

12

The affiliate contract expansion asset is classified as "Intangible assets, net". The prepayment of tangible assets are classified as "Prepaid expenses and other" within current assets on the Company's balance sheet. The off-market leases - favorable and off-market leases - unfavorable, are classified as "Intangible assets, net" and "Deferred lease", respectively, on the Company's balance sheet.

Note 4. Customer Concentration

Significant Contractual Relationship:

In 1999, the Company executed a Management Agreement (the “Agreement”) with Sprint whereby the Company committed to construct and operate a personal communications service (PCS) network using CDMA air interface technology. The Agreement has been amended numerous times. Under the amended Agreement, the Company is the exclusive PCS Affiliate of Sprint providing wireless mobility communications network products and services on the 800 MHz, 1900 MHz and 2.5 GHz spectrum ranges in its territory across a multi-state area covering large portions of central and western Virginia, south-central Pennsylvania, West Virginia, and portions of Maryland, North Carolina, Kentucky, and Ohio. The Company is authorized to use the Sprint brand in its territory, and operate its network under Sprint’s radio spectrum licenses. As an exclusive PCS Affiliate of Sprint, the Company has the exclusive right to build, own and maintain its portion of Sprint’s nationwide PCS network, in the aforementioned areas, to Sprint’s specifications. The initial term of the Agreement extends through November 2029, with two successive 10-year renewal periods, unless terminated by either party under provisions outlined in the Agreement. Upon non-renewal, the Company may cause Sprint to buy or Sprint may cause the Company to sell, the business at 90% of “Entire Business Value” (EBV) as defined in the Agreement. EBV is defined as i) the fair market value of a going concern paid by a willing buyer to a willing seller; ii) valued as if the business will continue to utilize existing brands and operate under existing agreements; and, iii) valued as if Manager (Shentel) owns the spectrum. Determination of EBV is made by an independent appraisal process.

Amendment to the Affiliate agreement related to the acquisition of the Expansion Area:

Effective with the acquisition of the Expansion Area on February 1, 2018, the Company amended its Agreement with Sprint to expand its wireless service area to include certain areas in Kentucky, Pennsylvania, Virginia and West Virginia. The agreement includes certain network build out requirements in the Expansion Area, and the ability to utilize Sprint’s spectrum in the Expansion Area along with certain other amendments to the Affiliate Agreements. Pursuant to the Expansion Agreement, Sprint agreed to, among other things, transition the provision of network coverage in the Expansion Area from Sprint to the Company.

Note 5. Earnings (Loss) Per Share (EPS)

Basic EPS was computed by dividing net income or loss by the weighted average number of shares of common stock outstanding during the period. Diluted net income (loss) per share was computed under the treasury stock method, assuming the conversion as of the beginning of the period, for all dilutive stock options. Diluted EPS was computed by dividing net income by the sum of the weighted average number of shares of common stock outstanding and potentially dilutive securities outstanding during the period under the treasury stock method. Potentially dilutive securities include stock options and restricted stock units and shares that the Company is contractually obligated to issue in the future.

The following table indicates the computation of basic and diluted earnings per share:

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

(in thousands, except per share amounts) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Calculation of net income (loss) per share: | ||||||||||||||||

Net income (loss) | $ | 15,534 | $ | 3,534 | $ | 31,743 | $ | 5,795 | ||||||||

Weighted average shares outstanding | 49,559 | 49,133 | 49,527 | 49,100 | ||||||||||||

Basic income (loss) per share | $ | 0.31 | $ | 0.07 | $ | 0.64 | $ | 0.12 | ||||||||

Effect of stock options outstanding: | ||||||||||||||||

Basic weighted average shares outstanding | 49,559 | 49,133 | 49,527 | 49,100 | ||||||||||||

Effect from dilutive shares and options outstanding | 558 | 826 | 517 | 769 | ||||||||||||

Diluted weighted average shares outstanding | 50,117 | 49,959 | 50,044 | 49,869 | ||||||||||||

Diluted income (loss) per share | $ | 0.31 | $ | 0.07 | $ | 0.63 | $ | 0.12 | ||||||||

13

The computation of diluted EPS does not include certain unvested awards, on a weighted average basis, because their inclusion would have an anti-dilutive effect on EPS. The awards excluded because of their anti-dilutive effect were as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||

(in thousands) | 2018 | 2017 | 2018 | 2017 | ||||||||

Awards excluded from the computation of diluted net income per share because their inclusion would have been anti-dilutive | 13 | — | 60 | 94 | ||||||||

Note 6. Investments

Other investments, comprised of equity securities which do not have readily determinable fair values, consist of the following:

(in thousands) | 9/30/2018 | 12/31/2017 | |||||

Cost method: | |||||||

CoBank | $ | 7,441 | $ | 6,818 | |||

Other – equity in other telecommunications partners | 784 | 811 | |||||

8,225 | 7,629 | ||||||

Equity method: | |||||||

Other | 575 | 564 | |||||

575 | 564 | ||||||

Total other investments | $ | 8,800 | $ | 8,193 | |||

The CoBank investment is primarily related to patronage distributions of restricted equity and is a required investment related to the Credit Facility. Refer to Note 12, Long-Term Debt, for additional information.

The Company's investments carried at fair value consisted of:

(in thousands) | 9/30/2018 | 12/31/2017 | |||||

Cash and Equivalents | $ | 1,408 | $ | — | |||

Domestic equity funds | 1,675 | 2,856 | |||||

International equity funds | 413 | 423 | |||||

Total investments carried at fair value | $ | 3,496 | $ | 3,279 | |||

Investments carried at fair value were acquired under a rabbi trust arrangement related to the Company’s Supplemental Executive Retirement Plan (SERP). The Company purchases investments in the trust to mirror the investment elections of participants in the SERP. The Company recorded net gains of $0.1 million in both the three months ended September 30, 2018 and 2017. The Company recorded net gains of $0.1 million and $0.3 million in the nine months ended September 30, 2018 and September 30, 2017, respectively. Fair values for these investments are determined using net asset value per share and are not classified in the fair value hierarchy. Gains and losses on the investments in the trust are reflected as increases or decreases in the liability owed to the participants. The increases or decreases to the liability are recorded as pension expense included within "Non-operating income (loss), net" in the Company's consolidated statements of operations.

Note 7. Fair Value Measurements

The following tables present the hierarchy for financial assets and liabilities measured at fair value on a recurring basis:

14

(in thousands) | September 30, 2018 | ||||||||||||||

Balance sheet location: | Level 1 | Level 2 | Level 3 | Total | |||||||||||

Prepaid expenses and other: | |||||||||||||||

Interest rate swaps | $ | — | $ | 5,447 | $ | — | $ | 5,447 | |||||||

Deferred charges and other assets, net: | |||||||||||||||

Interest rate swaps | — | 13,541 | — | 13,541 | |||||||||||

Total | $ | — | $ | 18,988 | $ | — | $ | 18,988 | |||||||

(in thousands) | December 31, 2017 | ||||||||||||||

Balance sheet location: | Level 1 | Level 2 | Level 3 | Total | |||||||||||

Cash equivalents: | |||||||||||||||

Money market funds | $ | 150 | $ | — | $ | — | $ | 150 | |||||||

Prepaid expenses and other: | |||||||||||||||

Interest rate swaps | — | 2,411 | — | 2,411 | |||||||||||

Deferred charges and other assets, net: | |||||||||||||||

Interest rate swaps | — | 10,776 | — | 10,776 | |||||||||||

Total | $ | 150 | $ | 13,187 | $ | — | $ | 13,337 | |||||||

Level 1- Financial assets and liabilities whose values are based on unadjusted quoted prices in active markets for identical assets or liabilities that the reporting entity can access at the measurement date.

Level 2 - Financial assets and liabilities whose values are based on inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly.

Level 3 - Financial assets and liabilities whose values are based on unobservable inputs for the asset or liability.

Financial instruments are defined as cash, or other financial instruments to a third party. The carrying amounts of cash and cash equivalents, accounts receivable, other current assets, investments carried at fair value, accounts payable and accrued liabilities approximate fair value due to their short-term nature. The Company's long-term debt and interest rate swaps approximate fair value because of their floating rate structure.

Derivative financial instruments are recognized as assets or liabilities in the financial statements and measured at fair value on a recurring basis. See Note 10, Derivatives and Hedging, for additional information. The Company measures its interest rate swaps at fair value and recognizes such derivative instruments as either assets or liabilities on the Company’s consolidated balance sheet. Changes in the fair value of swaps are recognized in other comprehensive income, as the Company has designated these swaps as cash flow hedges for accounting purposes. The Company entered into these swaps to manage a portion of its exposure to interest rate movements by converting a portion of its variable rate long-term debt to fixed rate debt.

The Company determines the fair value of its security holdings based on pricing from its vendors. The valuation techniques used to measure the fair value of financial instruments having Level 2 inputs were derived from non-binding consensus prices that are corroborated by observable market data or quoted market prices for similar instruments. Such market prices may be quoted prices in active markets for identical assets (Level 1 inputs) or pricing determined using inputs other than quoted prices that are observable either directly or indirectly (Level 2 inputs).

The Company has certain non-marketable long-term investments for which it is not practicable to estimate fair value, refer to Note 6, Investments, for additional information.

15

Note 8. Property, Plant and Equipment

Property, plant and equipment consisted of the following:

(in thousands) | Estimated Useful Lives | September 30, 2018 | December 31, 2017 | |||||||

Land | $ | 6,568 | $ | 6,418 | ||||||

Buildings and structures | 10 - 40 years | 207,647 | 195,540 | |||||||

Cable and wire | 4 - 40 years | 302,592 | 286,999 | |||||||

Equipment and software | 2 - 17 years | 763,089 | 730,228 | |||||||

Plant in service | 1,279,896 | 1,219,185 | ||||||||

Plant under construction | 74,422 | 62,202 | ||||||||

Total property, plant and equipment | 1,354,318 | 1,281,387 | ||||||||

Less accumulated amortization and depreciation | 684,609 | 595,060 | ||||||||

Property, plant and equipment, net | $ | 669,709 | $ | 686,327 | ||||||

Note 9. Goodwill and Other Intangible Assets

Goodwill consisted of the following:

(in thousands) | September 30, 2018 | December 31, 2017 | |||||

Goodwill - wireless | $ | 146,383 | $ | 146,383 | |||

Goodwill - cable | 104 | 104 | |||||

Goodwill - wireline | 10 | 10 | |||||

Goodwill | $ | 146,497 | $ | 146,497 | |||

Intangible assets consisted of the following:

16

September 30, 2018 | December 31, 2017 | ||||||||||||||||||||||

(in thousands) | Gross Carrying Amount | Accumulated Amortization and Other | Net | Gross Carrying Amount | Accumulated Amortization and Other | Net | |||||||||||||||||

Non-amortizing intangibles: | |||||||||||||||||||||||

Cable franchise rights | $ | 64,334 | $ | — | $ | 64,334 | $ | 64,334 | $ | — | $ | 64,334 | |||||||||||

Railroad crossing rights | 141 | — | 141 | 141 | — | 141 | |||||||||||||||||

Total non-amortizing intangibles | 64,475 | — | 64,475 | 64,475 | — | 64,475 | |||||||||||||||||

Finite-lived intangibles: | |||||||||||||||||||||||

Affiliate contract expansion - wireless | 455,305 | (152,603 | ) | 302,702 | 410,157 | (105,964 | ) | 304,193 | |||||||||||||||

Favorable leases - wireless | 15,816 | (1,754 | ) | 14,062 | 13,103 | (1,222 | ) | 11,881 | |||||||||||||||

Acquired subscribers - cable | 25,265 | (25,213 | ) | 52 | 25,265 | (25,100 | ) | 165 | |||||||||||||||

Other intangibles | 464 | (218 | ) | 246 | 463 | (198 | ) | 265 | |||||||||||||||

Total finite-lived intangibles | 496,850 | (179,788 | ) | 317,062 | 448,988 | (132,484 | ) | 316,504 | |||||||||||||||

Total intangible assets | $ | 561,325 | $ | (179,788 | ) | $ | 381,537 | $ | 513,463 | $ | (132,484 | ) | $ | 380,979 | |||||||||

Affiliate contract expansion is amortized over the expected benefit period and is further reduced by the amount of waived management fees received from Sprint which were $9.6 million and $28.2 million for the three and nine months ended September 30, 2018, respectively. Since May 6, 2016, the date of the non-monetary exchange, waived management fees received from Sprint totaled $88.8 million.

The gross carrying amount of certain intangibles was affected by the expansion of the Company's wireless service coverage area with Sprint. See Note 3, Acquisition for additional information.

Note 10. Derivatives and Hedging

The table below presents the fair value of the Company’s derivative financial instruments as well as its classification on the consolidated balance sheet:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Balance sheet location of derivative financial instruments: | ||||||||

Prepaid expenses and other | $ | 5,447 | $ | 2,411 | ||||

Deferred charges and other assets, net | 13,541 | 10,776 | ||||||

Total derivatives designated as hedging instruments | $ | 18,988 | $ | 13,187 | ||||

The table below summarizes changes in accumulated other comprehensive income (loss) by component:

Nine Months Ended September 30, 2018 | |||||||||||

(in thousands) | Gains (Losses) on Cash Flow Hedges | Income Tax (Expense) Benefit | Accumulated Other Comprehensive Income (Loss), net of taxes | ||||||||

Balance as of December 31, 2017 | $ | 13,187 | $ | (4,957 | ) | $ | 8,230 | ||||

Net change in unrealized gain (loss) | 5,801 | (1,441 | ) | 4,360 | |||||||

Net current period other comprehensive income (loss) | 5,801 | (1,441 | ) | 4,360 | |||||||

Balance as of September 30, 2018 | $ | 18,988 | $ | (6,398 | ) | $ | 12,590 | ||||

The outstanding notional amounts of the cash flow hedge were $395.1 million and $418.3 million as of September 30, 2018 and December 31, 2017, respectively. See Note 7, Fair Value Measurements, for additional information.

17

Note 11. Other Assets and Accrued Liabilities

Prepaid expenses and other, classified as current assets, included the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Prepaid rent | $ | 10,058 | $ | 10,519 | ||||

Prepaid maintenance expenses | 3,546 | 3,062 | ||||||

Interest rate swaps | 5,447 | 2,411 | ||||||

Deferred contract asset | 35,617 | — | ||||||

Other | 8,715 | 1,119 | ||||||

Prepaid expenses and other | $ | 63,383 | $ | 17,111 | ||||

Deferred contract and other costs include amounts reimbursed to Sprint for commissions and device costs, and commissions and installation costs in the Company’s Cable and Wireline segments. The deferred contract and other costs increased due to the adoption of Topic 606. Refer to Note 2, Revenue from Contracts with Customers, for additional information.

Deferred charges and other assets, classified as long-term assets, included the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Interest rate swaps | $ | 13,541 | $ | 10,776 | ||||

Deferred contract asset | 36,260 | — | ||||||

Other | 3,922 | 2,914 | ||||||

Deferred charges and other assets, net | $ | 53,723 | $ | 13,690 | ||||

Deferred contract and other costs include amounts reimbursed to Sprint for commissions and device costs, and commissions and installation costs in the Company’s Cable and Wireline segments. The deferred contract and other costs increased due to the adoption of Topic 606. Refer to Note 2, Revenue from Contracts with Customers, for additional information.

Accrued liabilities and other, classified as current liabilities, included the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Sales and property taxes payable | $ | 3,513 | $ | 3,872 | ||||

Severance accrual | — | 1,028 | ||||||

Asset retirement obligations | 582 | 492 | ||||||

Accrued programming costs | 2,927 | 2,805 | ||||||

Other current liabilities | 7,734 | 5,717 | ||||||

Accrued liabilities and other | $ | 14,756 | $ | 13,914 | ||||

Other liabilities, classified as long-term liabilities, included the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Non-current portion of deferred revenues | $ | 12,659 | $ | 14,030 | ||||

Other | 1,908 | 1,263 | ||||||

Other liabilities | $ | 14,567 | $ | 15,293 | ||||

The Company's asset retirement obligations are included in the balance sheet captions "Asset retirement obligations" and "Accrued liabilities and other". The Company records the fair value of an asset retirement obligation as a liability in the period in which it incurs a legal obligation associated with the retirement and removal of leasehold improvements or equipment. The Company also records a corresponding asset, which is depreciated over the life of the leasehold improvement or equipment. Subsequent to the initial measurement of the asset retirement obligation, the obligation is adjusted at the end of each period to reflect the passage of time and changes in the estimated future cash flows underlying the obligation. The terms associated with its operating leases, and applicable zoning ordinances of certain jurisdictions, define the Company’s obligations which are estimated and vary based on the size and types of the towers.

18

Note 12. Long-Term Debt

Total debt as of September 30, 2018 and December 31, 2017 consisted of the following:

(in thousands) | September 30, 2018 | December 31, 2017 | ||||||

Term loan A-1 | $ | 400,125 | $ | 436,500 | ||||

Term loan A-2 | 390,000 | 400,000 | ||||||

790,125 | 836,500 | |||||||

Less: unamortized loan fees | 11,337 | 14,542 | ||||||

Total debt, net of unamortized loan fees | $ | 778,788 | $ | 821,958 | ||||

Current maturities of long-term debt, net of current unamortized loan fees | $ | 84,743 | $ | 64,397 | ||||

Long-term debt, less current maturities, net of unamortized loan fees | $ | 694,045 | $ | 757,561 | ||||

As of September 30, 2018, the Company's indebtedness totaled approximately $778.8 million, net of unamortized loan fees of $11.3 million, with an annualized overall weighted average interest rate of approximately 4.11%. As of September 30, 2018, the Term Loan A-1 bears interest at one-month LIBOR plus a margin of 2.25%, while the Term Loan A-2 bears interest at one-month LIBOR plus a margin of 2.50%. For September 2018, one-month LIBOR was 2.08%. LIBOR resets monthly.

The Term Loan A-1 required quarterly principal repayments of $6.1 million, which began on September 30, 2016 and continued through June 30, 2017, increased to $12.1 million quarterly from September 30, 2017 through June 30, 2020; then increases to $18.2 million quarterly from September 30, 2020 through March 31, 2021, with the remaining balance due June 30, 2021. The Term Loan A-2 requires quarterly principal repayments of $10.0 million which began on September 30, 2018 and continue through March 31, 2023, with the remaining balance due June 30, 2023.

The 2016 credit agreement also requires the Company to enter into one or more hedge agreements to manage its exposure to interest rate movements. The Company elected to hedge the minimum required under the 2016 credit agreement, and entered into a pay-fixed, receive-variable swap on 50% of the aggregate expected principal balance of the term loans outstanding. The Company will receive one month LIBOR and pay a fixed rate of 1.16%, in addition to the 2.25% initial spread on Term Loan A-1 and the 2.50% initial spread on Term Loan A-2.

The 2016 credit agreement contains affirmative and negative covenants customary to secured credit facilities, including covenants restricting the ability of the Company and its subsidiaries, subject to negotiated exceptions, to incur additional indebtedness and additional liens on their assets, engage in mergers or acquisitions or dispose of assets, pay dividends or make other distributions, voluntarily prepay other indebtedness, enter into transactions with affiliated persons, make investments, and change the nature of the Company’s and its subsidiaries’ businesses.

Indebtedness outstanding under any of the facilities may be accelerated by an Event of Default, as defined in the 2016 credit agreement.

The Facilities are secured by a pledge by the Company of its stock and membership interests in its subsidiaries, a guarantee by the Company’s subsidiaries other than Shenandoah Telephone Company, and a security interest in substantially all of the assets of the Company and the guarantors.

The Company is subject to certain financial covenants to be measured on a trailing twelve month basis each calendar quarter unless otherwise specified. These covenants include:

• | a limitation on the Company’s total leverage ratio, defined as indebtedness divided by earnings before interest, taxes, depreciation and amortization, or EBITDA, of less than or equal to 3.75 to 1.00 from the closing date through December 30, 2018, then 3.25 to 1.00 through December 30, 2019, and 3.00 to 1.00 thereafter; |

• | a minimum debt service coverage ratio, defined as EBITDA minus certain cash taxes divided by the sum of all scheduled principal payments on the Term Loans and scheduled principal payments on other indebtedness plus cash interest expense, greater than 2.00 to 1.00; and |

19

• | maintain a minimum liquidity balance of greater than $25 million. The balance includes amounts available under the revolver facility plus unrestricted cash and cash equivalents on deposit in a deposit account for which a control agreement has been delivered to the administrative agent under the 2016 credit agreement. |

As shown below, as of September 30, 2018, the Company was in compliance with the covenants in its credit agreements.

Actual | Covenant Requirement | |||||

Total leverage ratio | 2.61 | 3.75 or Lower | ||||

Debt service coverage ratio | 3.25 | 2.00 or Higher | ||||

Minimum liquidity balance (in millions) | $ | 149.1 | $25.0 or Higher | |||

Credit Facility Modification: On February 16, 2018, the Company, entered into a Second Amendment to Credit Agreement (the “Second Amendment”) with CoBank, ACB, as administrative agent of its Credit Agreement and the various financial institutions party thereto (the “Lenders”), which modifies the Credit Agreement by (i) reducing the interest rate paid by the Company by 50 basis points with respect to certain loans made by the Lenders to the Company under the Credit Agreement, and (ii) allowing the Company to make charitable contributions to the Shentel Foundation, a Virginia nonstock corporation, of up to $1.5 million in any fiscal year.

Note 13. Income Taxes

The Company files U.S. federal income tax returns and various state and local income tax returns.

The net operating losses acquired in the nTelos acquisition are open to examination from 2002 forward. Income tax filings prior to 2014, excluding the acquired net operating losses, are no longer subject to examination. The Company is not subject to any state or federal income tax audits as of September 30, 2018.

The effective tax rate has fluctuated in recent periods due to the minimal base of pre-tax earnings or losses and has been further impacted by share based compensation tax benefits which are recognized as incurred under the provisions of ASC 740, "Income Taxes".

On December 22, 2017, the Tax Cuts and Jobs Act (the “2017 Tax Act”) was enacted, substantially changing the U.S. tax system. The 2017 Tax Act includes a number of changes to existing U.S. tax laws that impact the Company, most notably a reduction of the U.S. corporate income tax rate from 35 percent to 21 percent for tax years beginning after December 31, 2017. The 2017 Tax Act also provides immediate expensing for certain qualified assets acquired and placed into service after September 27, 2017 as well as prospective changes beginning in 2018, including acceleration of tax revenue recognition, additional limitations on deductibility of executive compensation and limitations on the deductibility of interest.

On December 22, 2017, the SEC staff issued Staff Accounting Bulletin No. 118 (SAB 118) to address the application of U.S. GAAP in situations when a registrant does not have the necessary information available, prepared, or analyzed in reasonable detail to complete the accounting for certain income tax effects of the 2017 Tax Act. The Company recognized the income tax effects of the 2017 Tax Act in its 2017 consolidated financial statements in accordance with SAB No. 118.

As of September 30, 2018, the Company is continuing to evaluate the provisional amounts recorded related to the 2017 Tax Act at December 31, 2017, for related state and local municipality tax matters.

20

Note 14. Segment Reporting

Three Months Ended September 30, 2018

(in thousands) | Wireless | Cable | Wireline | Other | Eliminations | Consolidated | ||||||||||||||||||

External revenue | ||||||||||||||||||||||||

Service revenue | $ | 96,299 | $ | 28,578 | $ | 5,443 | $ | — | $ | — | $ | 130,320 | ||||||||||||

Equipment revenue | 15,666 | 234 | 63 | — | — | 15,963 | ||||||||||||||||||

Other | 2,871 | 2,104 | 7,473 | — | — | 12,448 | ||||||||||||||||||

Total external revenue | 114,836 | 30,916 | 12,979 | — | — | 158,731 | ||||||||||||||||||

Internal revenue | 1,263 | 1,266 | 6,643 | — | (9,172 | ) | — | |||||||||||||||||

Total operating revenue | 116,099 | 32,182 | 19,622 | — | (9,172 | ) | 158,731 | |||||||||||||||||

Operating expenses | ||||||||||||||||||||||||

Cost of services | 32,253 | 14,837 | 9,266 | (12 | ) | (8,458 | ) | 47,886 | ||||||||||||||||

Cost of goods sold | 14,940 | 78 | 19 | (1 | ) | — | 15,036 | |||||||||||||||||

Selling, general and administrative | 11,191 | 5,331 | 1,780 | 9,864 | (714 | ) | 27,452 | |||||||||||||||||

Depreciation and amortization | 30,363 | 6,102 | 3,435 | 128 | — | 40,028 | ||||||||||||||||||

Total operating expenses | 88,747 | 26,348 | 14,500 | 9,979 | (9,172 | ) | 130,402 | |||||||||||||||||

Operating income (loss) | $ | 27,352 | $ | 5,834 | $ | 5,122 | $ | (9,979 | ) | $ | — | $ | 28,329 | |||||||||||

Three Months Ended September 30, 2017

(in thousands) | Wireless | Cable | Wireline | Other | Eliminations | Consolidated | ||||||||||||||||||

External revenue | ||||||||||||||||||||||||

Service revenue | $ | 107,395 | $ | 26,934 | $ | 5,126 | $ | — | $ | — | $ | 139,455 | ||||||||||||

Equipment revenue | 1,742 | 219 | 33 | — | — | 1,994 | ||||||||||||||||||

Other | 2,129 | 1,937 | 6,267 | — | — | 10,333 | ||||||||||||||||||

Total external revenue | 111,266 | 29,090 | 11,426 | — | — | 151,782 | ||||||||||||||||||

Internal revenue | 1,239 | 999 | 8,425 | — | (10,663 | ) | — | |||||||||||||||||

Total operating revenue | 112,505 | 30,089 | 19,851 | — | (10,663 | ) | 151,782 | |||||||||||||||||

Operating expenses | ||||||||||||||||||||||||

Cost of services | 33,825 | 14,858 | 9,796 | — | (9,927 | ) | 48,552 | |||||||||||||||||

Cost of goods sold | 7,216 | 55 | 11 | — | — | 7,282 | ||||||||||||||||||

Selling, general and administrative | 30,099 | 5,358 | 1,706 | 5,772 | (736 | ) | 42,199 | |||||||||||||||||

Acquisition, integration and migration expenses | 1,691 | — | — | 15 | — | 1,706 | ||||||||||||||||||

Depreciation and amortization | 32,929 | 6,192 | 3,249 | 198 | — | 42,568 | ||||||||||||||||||

Total operating expenses | 105,760 | 26,463 | 14,762 | 5,985 | (10,663 | ) | 142,307 | |||||||||||||||||

Operating income (loss) | $ | 6,745 | $ | 3,626 | $ | 5,089 | $ | (5,985 | ) | $ | — | $ | 9,475 | |||||||||||

21

Nine Months Ended September 30, 2018

(in thousands) | Wireless | Cable | Wireline | Other | Eliminations | Consolidated | ||||||||||||||||||

External revenue | ||||||||||||||||||||||||

Service revenue | $ | 284,154 | $ | 85,797 | $ | 16,052 | $ | — | $ | — | $ | 386,003 | ||||||||||||

Equipment revenue | 48,859 | 537 | 155 | — | — | 49,551 | ||||||||||||||||||

Other | 6,897 | 6,276 | 20,643 | — | — | 33,816 | ||||||||||||||||||

Total external revenue | 339,910 | 92,610 | 36,850 | — | — | 469,370 | ||||||||||||||||||

Internal revenue | 3,746 | 3,394 | 21,591 | — | (28,731 | ) | — | |||||||||||||||||

Total operating revenue | 343,656 | 96,004 | 58,441 | — | (28,731 | ) | 469,370 | |||||||||||||||||

Operating expenses | ||||||||||||||||||||||||

Cost of services | 99,491 | 45,118 | 28,441 | — | (26,688 | ) | 146,362 | |||||||||||||||||

Cost of goods sold | 45,749 | 197 | 61 | — | — | 46,007 | ||||||||||||||||||

Selling, general and administrative | 35,693 | 14,940 | 5,183 | 32,344 | (2,043 | ) | 86,117 | |||||||||||||||||

Depreciation and amortization | 95,853 | 18,305 | 10,069 | 405 | — | 124,632 | ||||||||||||||||||

Total operating expenses | 276,786 | 78,560 | 43,754 | 32,749 | (28,731 | ) | 403,118 | |||||||||||||||||

Operating income (loss) | $ | 66,870 | $ | 17,444 | $ | 14,687 | $ | (32,749 | ) | $ | — | $ | 66,252 | |||||||||||

Nine Months Ended September 30, 2017

(in thousands) | Wireless | Cable | Wireline | Other | Eliminations | Consolidated | ||||||||||||||||||

External revenue | ||||||||||||||||||||||||

Service revenue | $ | 323,262 | $ | 80,229 | $ | 15,301 | $ | — | $ | — | $ | 418,792 | ||||||||||||

Equipment revenue | 7,666 | 547 | 90 | — | — | 8,303 | ||||||||||||||||||

Other | 7,467 | 5,736 | 18,622 | — | — | 31,825 | ||||||||||||||||||

Total external revenue | 338,395 | 86,512 | 34,013 | — | — | 458,920 | ||||||||||||||||||

Internal revenue | 3,707 | 2,153 | 24,568 | — | (30,428 | ) | — | |||||||||||||||||

Total operating revenue | 342,102 | 88,665 | 58,581 | — | (30,428 | ) | 458,920 | |||||||||||||||||

Operating expenses | ||||||||||||||||||||||||

Cost of services | 100,745 | 44,956 | 28,357 | — | (28,314 | ) | 145,744 | |||||||||||||||||

Cost of goods sold | 17,084 | 96 | 52 | — | — | 17,232 | ||||||||||||||||||

Selling, general and administrative | 88,201 | 15,083 | 5,065 | 19,139 | (2,114 | ) | 125,374 | |||||||||||||||||

Acquisition, integration and migration expenses | 9,607 | — | — | 266 | — | 9,873 | ||||||||||||||||||

Depreciation and amortization | 104,231 | 18,070 | 9,536 | 460 | — | 132,297 | ||||||||||||||||||

Total operating expenses | 319,868 | 78,205 | 43,010 | 19,865 | (30,428 | ) | 430,520 | |||||||||||||||||

Operating income (loss) | $ | 22,234 | $ | 10,460 | $ | 15,571 | $ | (19,865 | ) | $ | — | $ | 28,400 | |||||||||||

22

A reconciliation of the total of the reportable segments’ operating income (loss) to consolidated income (loss) before taxes is as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

(in thousands) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Total consolidated operating income (loss) | $ | 28,329 | $ | 9,475 | $ | 66,252 | $ | 28,400 | ||||||||

Interest expense | (9,001 | ) | (9,823 | ) | (27,184 | ) | (28,312 | ) | ||||||||

Gain (loss) on investments, net | 88 | 202 | 112 | 395 | ||||||||||||

Non-operating income (loss), net | 966 | 1,003 | 2,770 | 3,482 | ||||||||||||

Income (loss) before income taxes | $ | 20,382 | $ | 857 | $ | 41,950 | $ | 3,965 | ||||||||

As of January 1, 2018, the Company records stock compensation expense to the Other segment. Previously, stock compensation expense was allocated among all of the segments.

Note 15. Subsequent Events

On October 30, 2018, the Company's Board of Directors approved a dividend of $0.27 per common share to be paid on November 30, 2018 to shareholders of record as of the close of business on November 12, 2018. Before dividend reinvestments, the total payout is expected to be approximately $13.4 million.

23

ITEM 2. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

This management’s discussion and analysis includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. When used in this report, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions as they relate to Shenandoah Telecommunications Company or its management are intended to identify these forward-looking statements. All statements regarding Shenandoah Telecommunications Company’s expected future financial position and operating results, business strategy, financing plans, forecasted trends relating to the markets in which Shenandoah Telecommunications Company operates and similar matters are forward-looking statements. We cannot assure you that the Company’s expectations expressed or implied in these forward-looking statements will turn out to be correct. The Company’s actual results could be materially different from its expectations because of various factors, including those discussed below and under the caption “Risk Factors” in the Company’s Annual Report on Form 10-K for its fiscal year ended December 31, 2017. The following management’s discussion and analysis should be read in conjunction with the Company’s Annual Report on Form 10-K for its fiscal year ended December 31, 2017, including the consolidated financial statements and related notes included therein.

General

Overview. Shenandoah Telecommunications Company, (the "Company", "we", "our", or "us"), is a diversified telecommunications company providing integrated voice, video and data communication services including both regulated and unregulated telecommunications services through its wholly owned subsidiaries. These subsidiaries provide wireless personal communications services as a Sprint PCS affiliate, and local exchange telephone services, video, internet and data services, long distance services, fiber optics facilities and leased tower facilities. We organize and strategically manage our operations under the Company's reportable segments that include: Wireless, Cable, Wireline, and Other. See Note 14, Segment Reporting, included with the notes to our consolidated financial statements provided within our 2017 Annual Report on Form 10-K for further information regarding our segments.

Basis of Presentation

The Company adopted ASU No. 2014-09, Revenue from Contracts with Customers (“Topic 606”), effective January 1, 2018, using the modified retrospective method as discussed in Note 2, Revenue from Contracts with Customers. The following tables identify the impact of applying Topic 606 to the Company for the three and nine months ended September 30, 2018:

Three Months Ended September 30, 2018 | |||||||||||||||

Topic 606 Impact - CONSOLIDATED | |||||||||||||||

($ in thousands, except per share amounts) | Prior to Adoption of Topic 606 | Changes in Presentation (1) | Equipment Revenue (2) | Deferred Costs (3) | As Reported 09/30/2018 | ||||||||||

Service revenue and other | $ | 161,076 | $ | (23,174 | ) | $ | — | $ | 4,866 | $ | 142,768 | ||||

Equipment revenue | 2,178 | — | 13,785 | — | 15,963 | ||||||||||

Total operating revenue | 163,254 | (23,174 | ) | 13,785 | 4,866 | 158,731 | |||||||||

Cost of services | 48,001 | — | — | (115 | ) | 47,886 | |||||||||

Cost of goods sold | 7,870 | (6,619 | ) | 13,785 | — | 15,036 | |||||||||

Selling, general & administrative | 44,164 | (16,555 | ) | — | (157 | ) | 27,452 | ||||||||

Depreciation and amortization | 40,028 | — | — | — | 40,028 | ||||||||||

Total operating expenses | 140,063 | (23,174 | ) | 13,785 | (272 | ) | 130,402 | ||||||||

Operating income (loss) | 23,191 | — | — | 5,138 | 28,329 | ||||||||||

Other income (expense) | (7,947 | ) | — | — | — | (7,947 | ) | ||||||||

Income tax expense (benefit) | 3,486 | — | — | 1,362 | 4,848 | ||||||||||

Net income (loss) | $ | 11,758 | $ | — | $ | — | $ | 3,776 | $ | 15,534 | |||||

Earnings (loss) per share | |||||||||||||||

Basic | $ | 0.24 | $ | 0.07 | $ | 0.31 | |||||||||

Diluted | $ | 0.23 | $ | 0.08 | $ | 0.31 | |||||||||

Weighted average shares outstanding, basic | 49,559 | 49,559 | |||||||||||||

Weighted average shares outstanding, diluted | 50,117 | 50,117 | |||||||||||||

24

Nine Months Ended September 30, 2018 | |||||||||||||||

Topic 606 Impact - CONSOLIDATED | |||||||||||||||

($ in thousands, except per share amounts) | Prior to Adoption of Topic 606 | Changes in Presentation (1) | Equipment Revenue (2) | Deferred Costs (3) | As Reported 09/30/2018 | ||||||||||

Service revenue and other | $ | 471,155 | $ | (64,069 | ) | $ | — | $ | 12,733 | $ | 419,819 | ||||

Equipment revenue | 6,036 | — | 43,515 | — | 49,551 | ||||||||||

Total operating revenue | 477,191 | (64,069 | ) | 43,515 | 12,733 | 469,370 | |||||||||

Cost of services | 146,199 | — | — | 163 | 146,362 | ||||||||||

Cost of goods sold | 20,316 | (17,824 | ) | 43,515 | — | 46,007 | |||||||||

Selling, general & administrative | 132,711 | (46,245 | ) | — | (349 | ) | 86,117 | ||||||||

Depreciation and amortization | 124,632 | — | — | — | 124,632 | ||||||||||

Total operating expenses | 423,858 | (64,069 | ) | 43,515 | (186 | ) | 403,118 | ||||||||

Operating income (loss) | 53,333 | — | — | 12,919 | 66,252 | ||||||||||

Other income (expense) | (24,302 | ) | — | — | — | (24,302 | ) | ||||||||

Income tax expense (benefit) | 6,740 | — | — | 3,467 | 10,207 | ||||||||||

Net income (loss) | $ | 22,291 | $ | — | $ | — | $ | 9,452 | $ | 31,743 | |||||

Earnings (loss) per share | |||||||||||||||

Basic | $ | 0.45 | $ | 0.19 | $ | 0.64 | |||||||||

Diluted | $ | 0.45 | $ | 0.18 | $ | 0.63 | |||||||||

Weighted average shares outstanding, basic | 49,527 | 49,527 | |||||||||||||

Weighted average shares outstanding, diluted | 50,044 | 50,044 | |||||||||||||

______________________________________________________

(1) Amounts payable to Sprint for the reimbursement of costs incurred by Sprint in their national sales channel for commissions and device costs for both postpaid and prepaid, and to provide on-going support to their prepaid customers in our territory were historically recorded as expense when incurred. Under Topic 606, these amounts represent consideration payable to our customer, Sprint, and are recorded as a reduction of revenue. In 2017, these amounts were approximately $44.8 million for the postpaid national commissions, previously recorded in selling, general and administrative, $18.7 million for national device costs previously recorded in cost of goods and services, and $16.9 million for the on-going service to Sprint's prepaid customers, previously recorded in selling, general and administrative.

(2) Costs incurred by the Company for the sale of devices under Sprint’s device financing and lease programs were previously recorded net against revenue. Under Topic 606, the revenue and related costs from device sales are recorded gross. These amounts were approximately $63.8 million in 2017.

(3) Amounts payable to Sprint for the reimbursement of costs incurred by Sprint in their national sales channel for commissions and device costs, which historically have been expensed when incurred, are deferred and amortized against revenue over the expected period of benefit of approximately 21 to 53 months. In Cable and Wireline, installation revenues are recognized over a period of approximately 10-11 months. The deferred balance as of September 30, 2018 is approximately $71.9 million and is classified on the balance sheet as current and non-current assets, as applicable.

2018 Developments

Credit Facility Modification: On February 16, 2018, the Company, entered into a Second Amendment to Credit Agreement (the “Second Amendment”) with CoBank, ACB, as administrative agent of its Credit Agreement, described more fully in Note 12, Long-Term Debt, and the various financial institutions party thereto (the “Lenders”), which modifies the Credit Agreement by (i) reducing the interest rate paid by the Company by 50 basis points with respect to certain loans made by the Lenders to the Company under the Credit Agreement, and (ii) allowing the Company to make charitable contributions to Shentel Foundation, a Virginia nonstock corporation, of up to $1.5 million in any fiscal year.