Attached files

| file | filename |

|---|---|

| EX-99.2 - EXHIBIT 99.2 - SEACOAST BANKING CORP OF FLORIDA | tv499800_ex99-2.htm |

| EX-99.1 - EXHIBIT 99.1 - SEACOAST BANKING CORP OF FLORIDA | tv499800_ex99-1.htm |

| 8-K - FORM 8-K - SEACOAST BANKING CORP OF FLORIDA | tv499800_8k.htm |

Exhibit 99.3

Q2 - 2018 Earnings Presentation Contact: (email) Chuck.Shaffer@SeacoastBank.com (phone) 772.221.7003 (web) www.SeacoastBanking.com

Cautionary Notice Regarding Forward - Looking Statements 2 This press release contains "forward - looking statements" within the meaning, and protections, of Section 27 A of the Securities Act of 1933 and Section 21 E of the Securities Exchange Act of 1934 , including, without limitation, statements about future financial and operating results, cost savings, enhanced revenues, economic and seasonal conditions in our markets, and improvements to reported earnings that may be realized from cost controls, tax law changes, and for integration of banks that we have acquired, or expect to acquire, as well as statements with respect to Seacoast's objectives, strategic plans, including Vision 2020 , expectations and intentions and other statements that are not historical facts . Actual results may differ from those set forth in the forward - looking statements . Forward - looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions, and involve known and unknown risks, uncertainties and other factors, which may be beyond our control, and which may cause the actual results, performance or achievements of Seacoast to be materially different from future results, performance or achievements expressed or implied by such forward - looking statements . You should not expect us to update any forward - looking statements . You can identify these forward - looking statements through our use of words such as “may,” “will,” “anticipate,” “assume,” “should,” “support”, “indicate,” “would,” “believe,” “contemplate,” “expect,” “estimate,” “continue,” “further”, “point to,” “project,” “could,” “intend” or other similar words and expressions of the future . These forward - looking statements may not be realized due to a variety of factors, including, without limitation : the effects of future economic and market conditions, including seasonality ; governmental monetary and fiscal policies, as well as legislative, tax and regulatory changes ; changes in accounting policies, rules and practices ; the risks of changes in interest rates on the level and composition of deposits, loan demand, liquidity and the values of loan collateral, securities, and interest sensitive assets and liabilities ; interest rate risks, sensitivities and the shape of the yield curve ; the effects of competition from other commercial banks, thrifts, mortgage banking firms, consumer finance companies, credit unions, securities brokerage firms, insurance companies, money market and other mutual funds and other financial institutions operating in our market areas and elsewhere, including institutions operating regionally, nationally and internationally, together with such competitors offering banking products and services by mail, telephone, computer and the Internet ; and the failure of assumptions underlying the establishment of reserves for possible loan losses . The risks of mergers and acquisitions, include, without limitation : unexpected transaction costs, including the costs of integrating operations ; the risks that the businesses will not be integrated successfully or that such integration may be more difficult, time - consuming or costly than expected ; the potential failure to fully or timely realize expected revenues and revenue synergies, including as the result of revenues following the merger being lower than expected ; the risk of deposit and customer attrition ; any changes in deposit mix ; unexpected operating and other costs, which may differ or change from expectations ; the risks of customer and employee loss and business disruption, including, without limitation, as the result of difficulties in maintaining relationships with employees ; increased competitive pressures and solicitations of customers by competitors ; as well as the difficulties and risks inherent with entering new markets . All written or oral forward - looking statements attributable to us are expressly qualified in their entirety by this cautionary notice, including, without limitation, those risks and uncertainties described in our annual report on Form 10 - K for the year ended December 31 , 2017 under “Special Cautionary Notice Regarding Forward - Looking Statements” and “Risk Factors”, and otherwise in our SEC reports and filings . Such reports are available upon request from the Company, or from the Securities and Exchange Commission, including through the SEC’s Internet website at http : //www . sec . gov .

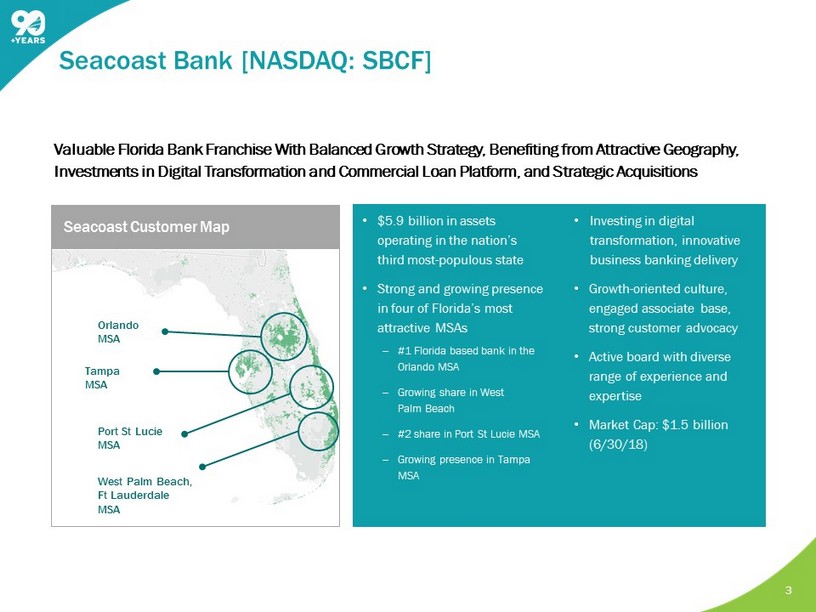

• $5.9 billion in assets operating in the nation’s third most - populous state • Strong and growing presence in four of Florida’s most attractive MSAs ‒ #1 Florida based bank in the Orlando MSA ‒ Growing share in West Palm Beach ‒ #2 share in Port St Lucie MSA ‒ Growing presence in Tampa MSA • Investing in digital transformation, innovative business banking delivery • Growth - oriented culture, engaged associate base, strong customer advocacy • Active board with diverse range of experience and expertise • Market Cap: $1.5 billion (6/30/18) Valuable Florida Bank Franchise With Balanced Growth Strategy, Benefiting from Attractive Geography, Investments in Digital Transformation and Commercial Loan Platform, and Strategic Acquisitions 3 Seacoast Bank [NASDAQ: SBCF ] Orlando MSA West Palm Beach, Ft Lauderdale MSA Port St Lucie MSA Tampa MSA Seacoast Customer Map

4 Seacoast’s Differentiated Strategy Experienced Board & Management Team Comprehensive Customer Servicing Model Track Record of Value - Creating Acquisitions Expanding Analytical & Digital Capabilities Well - Positioned to Benefit From Florida Market Focused on Controls

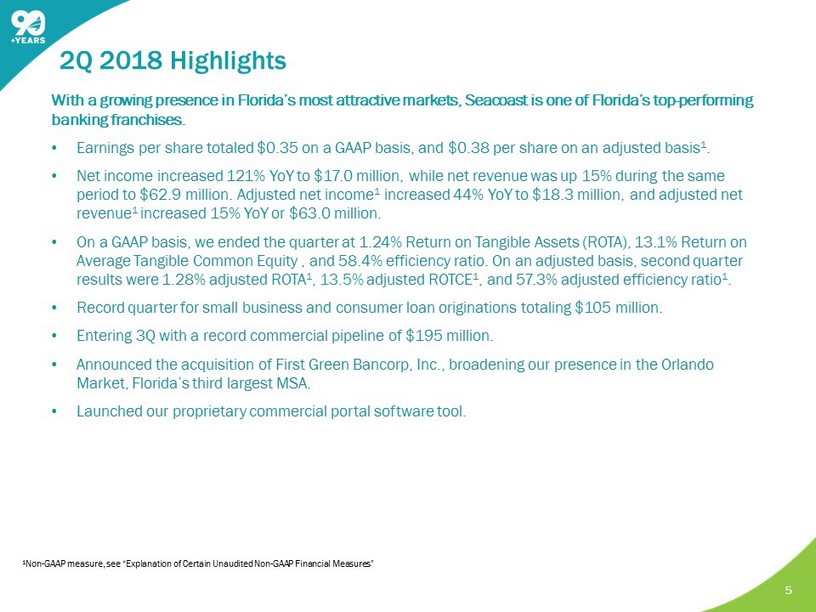

5 2 Q 2018 Highlights With a growing presence in Florida’s most attractive markets, Seacoast is one of Florida’s top - performing banking franchises. • Earnings per share totaled $0.35 on a GAAP basis, and $0.38 per share on an adjusted basis 1 . • Net income increased 121% YoY to $17.0 million, while net revenue was up 15% during the same period to $62.9 million. Adjusted net income 1 increased 44% YoY to $18.3 million, and adjusted net revenue 1 increased 15% YoY or $63.0 million. • On a GAAP basis, we ended the quarter at 1.24% Return on Tangible Assets (ROTA), 13.1% Return on Average Tangible Common Equity , and 58.4% efficiency ratio. On an adjusted basis, second quarter results were 1.28% adjusted ROTA 1 , 13.5% adjusted ROTCE 1 , and 57.3% adjusted efficiency ratio 1 . • Record quarter for small business and consumer loan originations totaling $105 million. • Entering 3Q with a record commercial pipeline of $195 million . • Announced the acquisition of First Green Bancorp, Inc., broadening our presence in the Orlando Market, Florida’s third largest MSA. • Launched our proprietary commercial portal software tool. 1 Non - GAAP measure, see “Explanation of Certain Unaudited Non - GAAP Financial Measures ”

Notable Items Impacting Results by $0.05 per share in the Second Quarter 6 • $0.5 million reduction in accretion from discounts on acquired loans quarter over quarter . • Experienced higher prepayments quarter over quarter on the nonacquired originated loan portfolio which reduced loan growth by 3 %. • Recognized $1.7 million in net charge offs in the quarter . • Recognized $0.3 million in losses on the sale of other real estate owned during the quarter.

First Green Bank Acquisition: Continuation of “Land and Expand” M&A Strategy in Orlando FL 7 High - Quality Expansion In Attractive Market • Expands footprint in Orlando, Florida’s 3rd largest MSA • Significantly strengthens Seacoast’s position as the #1 community bank by deposit market share in the Orlando MSA, increasing deposits 49% to over $1.4 billion • High growth potential as Seacoast executes its integration and digital marketing playbook • Solidifies presence along attractive, high growth I - 4 corridor Anticipated Positive Financial Results • 10%+ core EPS accretion in both 2019 and 2020 • 25%+ internal rate of return • Tangible book value d ilution earn - back of under one year (crossover method) Adds Scale in Orlando MSA, Strengthens Florida Franchise Overall • Branch location overlap creates immediate operating synergy opportunities • Opens First Green’s customer base and prospect list to Seacoast’s expanded products and services • Expands Seacoast’s loan portfolio and maintains prudent level of diversification

8 ($ in thousands) • Net interest income 1 totaled $50.3 million, up $0.4 million or 1 % from the prior quarter and $6.0 million or 14% from the prior year quarter. • Net interest margin was 3.77% in the current quarter compared to 3.80% in the prior quarter and 3.84% in the second quarter of 2017. • The impact of purchased loan accretion on total net interest margin represented 16 basis points in the current quarter, versus 20 in the prior quarter and 25 in the second quarter of 2017. 1 Calculated on a fully taxable equivalent basis using amortized cost . Net Interest Income and Margin $44,320 $45,903 $48,402 $49,853 $50,294 3.84% 3.74% 3.71% 3.80% 3.77% 3.59% 3.54% 3.49% 3.60% 3.61% $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 $45,000 $50,000 $55,000 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Net Interest Income Net Interest Margin NIM, excluding accretion on acquired loans

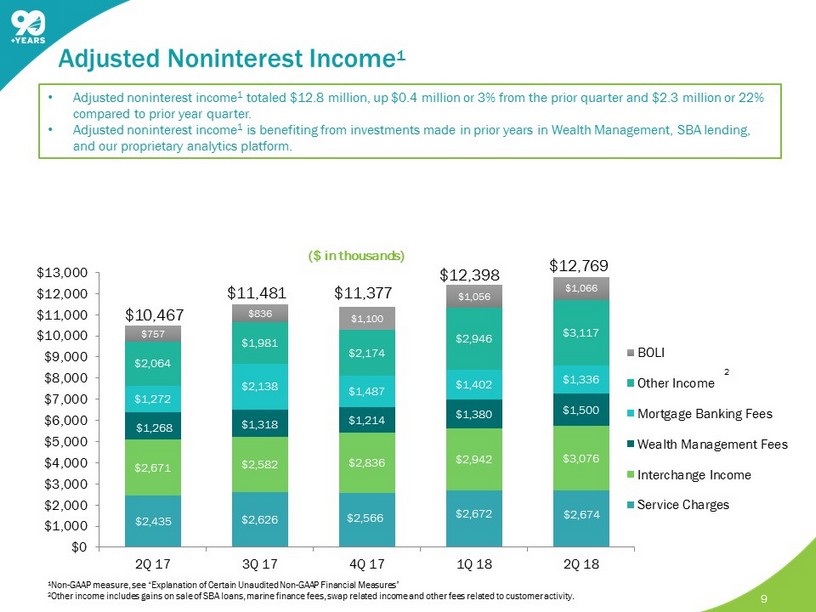

9 $2,435 $2,626 $2,566 $2,672 $2,674 $2,671 $2,582 $2,836 $2,942 $3,076 $1,268 $1,318 $1,214 $1,380 $1,500 $1,272 $2,138 $1,487 $1,402 $1,336 $2,064 $1,981 $2,174 $2,946 $3,117 $757 $836 $1,100 $1,056 $1,066 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000 $10,000 $11,000 $12,000 $13,000 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 BOLI Other Income Mortgage Banking Fees Wealth Management Fees Interchange Income Service Charges 2 $10,467 • Adjusted noninterest income 1 totaled $12.8 million, up $0.4 million or 3% from the prior quarter and $2.3 million or 22% compared to prior year quarter. • Adjusted noninterest income 1 is benefiting from investments made in prior years in Wealth Management, SBA lending, and our proprietary analytics platform. $11,481 $11,377 $12,398 $12,769 Adjusted Noninterest Income 1 1 Non - GAAP measure, see “Explanation of Certain Unaudited Non - GAAP Financial Measures” 2 Other income includes gains on sale of SBA loans, marine finance fees, swap related income and other fees related to customer ac tivity. ($ in thousands)

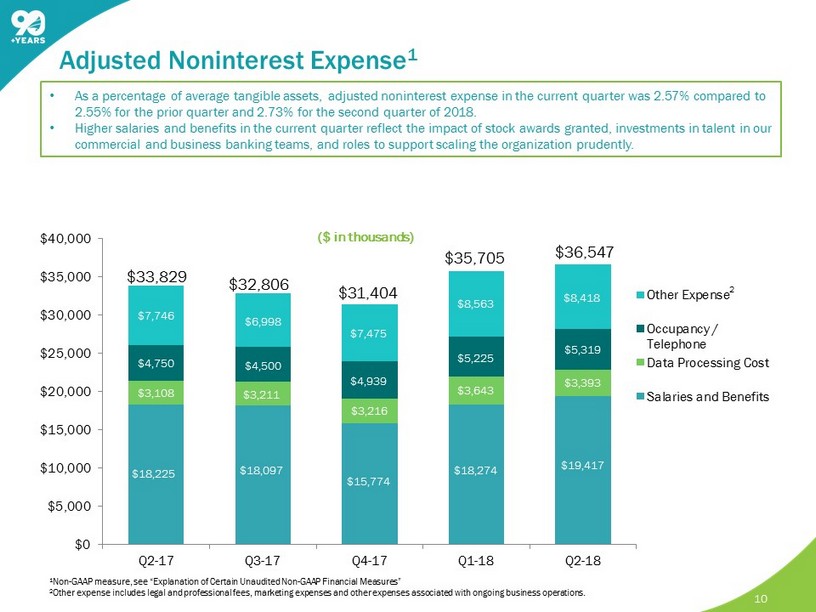

10 $18,225 $18,097 $15,774 $18,274 $19,417 $3,108 $3,211 $3,216 $3,643 $3,393 $4,750 $4,500 $4,939 $5,225 $5,319 $7,746 $6,998 $7,475 $8,563 $8,418 $0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 Q2-17 Q3-17 Q4-17 Q1-18 Q2-18 Other Expense Occupancy / Telephone Data Processing Cost Salaries and Benefits 2 $36,547 $33,829 $32,806 $31,404 $35,705 • As a percentage of average tangible assets, adjusted noninterest expense in the current quarter was 2.57% compared to 2.55% for the prior quarter and 2.73% for the second quarter of 2018. • Higher salaries and benefits in the current quarter reflect the impact of stock awards granted, investments in talent in our commercial and business banking teams, and roles to support scaling the organization prudently . 1 Non - GAAP measure, see “Explanation of Certain Unaudited Non - GAAP Financial Measures ” 2 Other expense includes legal and professional fees, marketing expenses and other expenses associated with ongoing business op era tions. Adjusted Noninterest Expense 1 ($ in thousands)

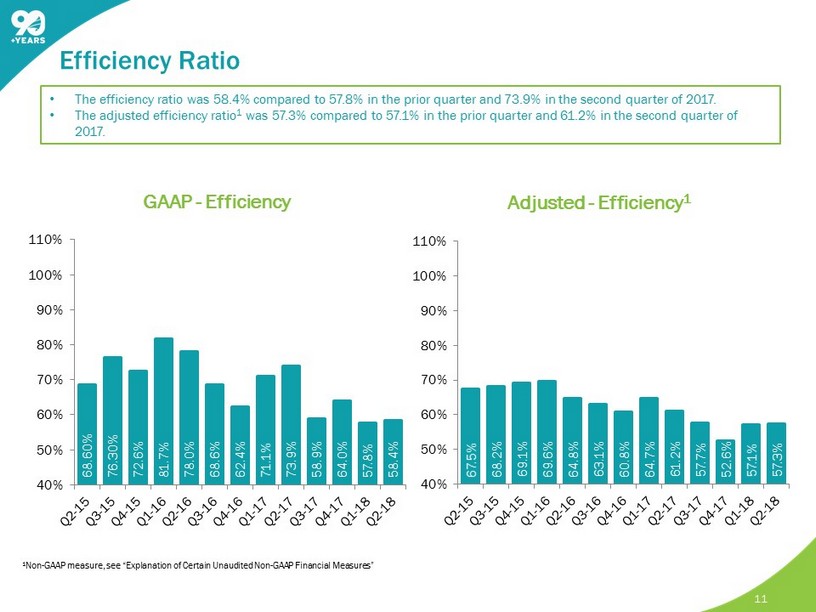

11 68.60% 76.30% 72.6% 81.7% 78.0% 68.6% 62.4% 71.1% 73.9% 58.9% 64.0% 57.8% 58.4% 40% 50% 60% 70% 80% 90% 100% 110% GAAP - Efficiency 67.5% 68.2% 69.1% 69.6% 64.8% 63.1% 60.8% 64.7% 61.2% 57.7% 52.6% 57.1% 57.3% 40% 50% 60% 70% 80% 90% 100% 110% Adjusted - Efficiency 1 1 Non - GAAP measure, see “Explanation of Certain Unaudited Non - GAAP Financial Measures ” • The efficiency ratio was 58.4% compared to 57.8% in the prior quarter and 73.9% in the second quarter of 2017. • The adjusted efficiency ratio 1 was 57.3% compared to 57.1% in the prior quarter and 61.2% in the second quarter of 2017. Efficiency Ratio

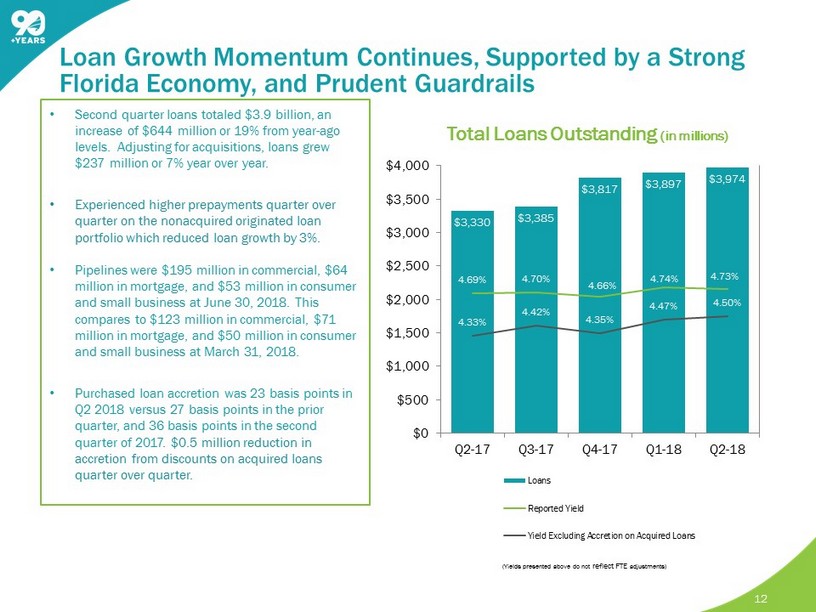

12 Total Loans Outstanding (in millions) • Second quarter loans totaled $3.9 billion, an increase of $644 million or 19% from year - ago levels. Adjusting for acquisitions, loans grew $237 million or 7% year over year . • Experienced higher prepayments quarter over quarter on the nonacquired originated loan portfolio which reduced loan growth by 3%. • Pipelines were $195 million in commercial, $64 million in mortgage, and $53 million in consumer and small business at June 30, 2018 . This compares to $123 million in commercial, $71 million in mortgage, and $50 million in consumer and small business at March 31, 2018. • Purchased loan accretion was 23 basis points in Q2 2018 versus 27 basis points in the prior quarter, and 36 basis points in the second quarter of 2017. $0.5 million reduction in accretion from discounts on acquired loans quarter over quarter. $3,330 $3,385 $3,817 $3,897 $3,974 4.69% 4.70% 4.66% 4.74% 4.73% 4.33% 4.42% 4.35% 4.47% 4.50% $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 Q2-17 Q3-17 Q4-17 Q1-18 Q2-18 Loans Reported Yield Yield Excluding Accretion on Acquired Loans Loan Growth Momentum Continues, Supported by a Strong Florida Economy, and Prudent Guardrails (Yields presented above do not reflect FTE adjustments)

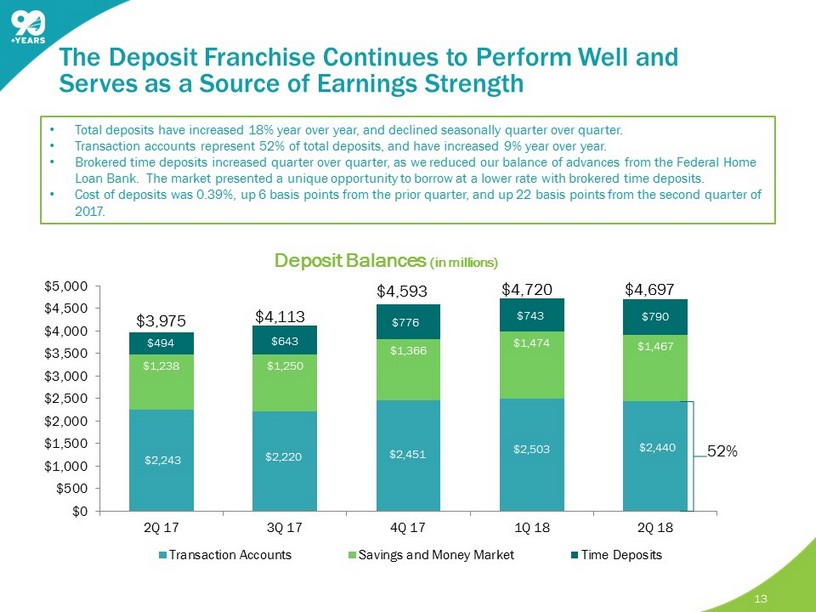

13 • Total deposits have increased 18% year over year, and declined seasonally quarter over quarter. • Transaction accounts represent 52% of total deposits, and have increased 9 % year over year. • Brokered time deposits increased quarter over quarter, as we reduced our balance of advances from the Federal Home Loan Bank. The market presented a unique opportunity to borrow at a lower rate with brokered time deposits. • Cost of deposits was 0.39%, up 6 basis points from the prior quarter, and up 22 basis points from the second quarter of 2017. $2,243 $2,220 $2,451 $2,503 $2,440 $1,238 $1,250 $1,366 $1,474 $1,467 $494 $643 $776 $743 $790 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500 $5,000 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Transaction Accounts Savings and Money Market Time Deposits Deposit Balances (in millions) $4,697 $3,975 $4,113 $4,593 52% $4,720 The Deposit Franchise Continues to Perform Well and Serves as a Source of Earnings Strength

14 (1) Beta calculated using the change in deposit costs 2Q18 vs 2Q17 divided by the 75bps change in Fed Funds rate from June 30, 2017 to June 30, 2018 Average Deposit Balances and Cost Our focus on organic growth and relationship - based funding, in combination with our innovative analytics platform, supports a well - diversified low - cost deposit portfolio. 33% 32% 31% 31% 31% 1% 5% 6% 5% 5% 10% 9% 11% 12% 12% 22% 22% 21% 21% 22% 24% 23% 22% 22% 21% 10% 9% 9% 9% 9% 2Q17 3Q17 4Q17 1Q18 2Q18 Savings Int Bearing Demand Money Market Time Deposits Brokered Deposits Non-Int Bearing Cost of Deposits Deposit Mix 0.39 % 2Q17 - 2Q18 Interest Bearing Deposits Cumulative Beta (1) Savings 7 bps Interest Bearing Demand 12 bps Money Market 38 bps Time Deposits 71 bps Brokered CDs 54 bps Total Interest Bearing 33 bps Total Deposits 22 bps Fed Funds Change 75 bps 0.33 % 0.29 % 0.22 % 0.17 %

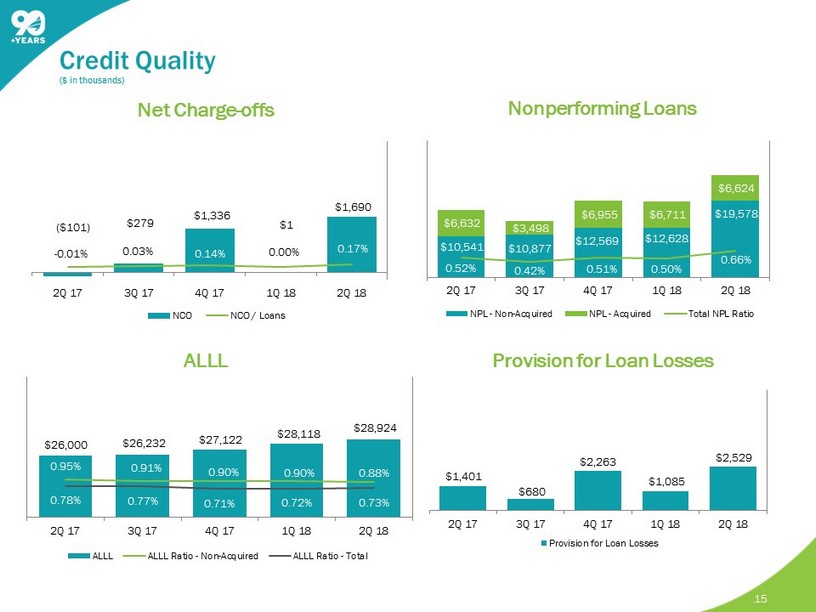

15 Net Charge - offs Nonperforming Loans ALLL $26,000 $26,232 $27,122 $28,118 $28,924 0.95% 0.91% 0.90% 0.90% 0.88% 0.78% 0.77% 0.71% 0.72% 0.73% 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 ALLL ALLL Ratio - Non-Acquired ALLL Ratio - Total Provision for Loan Losses $279 ($101) $1,336 $1 $1,690 - 0.01% 0.03% 0.14% 0.00% 0.17% 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 NCO NCO / Loans $10,541 $10,877 $12,569 $12,628 $19,578 $6,632 $3,498 $6,955 $6,711 $6,624 0.52% 0.42% 0.51% 0.50% 0.66% 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 NPL - Non-Acquired NPL - Acquired Total NPL Ratio Credit Quality ($ in thousands) $1,401 $680 $2,263 $1,085 $2,529 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Provision for Loan Losses

Maintaining Strong Capital to Support Balanced Growth Opportunities 16 Tangible Book Value / Book Value Per Share $10.55 $10.95 $11.15 $11.39 $11.67 $13.29 $13.66 $14.70 $14.94 $15.18 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Tangible Book Value Per Share Book Value Per Share 11.2% 12.8% 13.5% 14.8% 13.5% 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Adjusted Return on Tangible Common Equity 1 14.5% 14.8% 14.2% 15.0% 15.2% 13.8% 14.1% 13.6% 14.4% 14.5% 2Q 17 3Q 17 4Q 17 1Q 18 2Q 18 Total Risk Based Capital Tier 1 Ratio Total Risk Based and Tier 1 Capital Tangible Common Equity / Tangible Assets 8.9% 9.1% 9.3% 9.3% 9.6% 2Q 17 3Q 17 4Q 17 1Q 18 2Q18 1 Non - GAAP measure, see “Explanation of Certain Unaudited Non - GAAP Financial Measures.”

Reiterating Vision 2020 Objectives 17 • We remain confident in our ability to achieve our Vision 2020 targets announced early last year. We continue to monitor the impact of the Tax Cuts and Jobs Act of 2017 and believe the impact of this important legislation will more fully materialize in the marketplace moving forward. Additionally, we announced the acquisition of First Green Bancorp, Inc., which is expected to close early in the fourth quarter. We believe both the Tax Cuts and Jobs Act of 2017 and the acquisition of First Green Bancorp, Inc. reinforce our ability to achieve these objectives. Vision 2020 Targets Return on Tangible Assets 1.30%+ Return on Tangible Common Equity 16%+ Efficiency Ratio Below 50%

Investor Presentation Charles M. Shaffer Executive Vice President Chief Financial Officer (772) 221 - 7003 Chuck.Shaffer@seacoastbank.com INVESTOR RELATIONS www.SeacoastBanking.com NASDAQ: SBCF 18 18 Contact Details: Seacoast Banking Corporation of Florida

19

This presentation contains financial information determined by methods other than Generally Accepted Accounting Principles (“GAAP”) . The financial highlights provide reconciliations between GAAP net income and adjusted net income, GAAP income and adjusted pretax, preprovision income . Management uses these non - GAAP financial measures in its analysis of the Company’s performance and believes these presentations provide useful supplemental information, and a clearer understanding of the Company’s performance . The Company believes the non - GAAP measures enhance investors’ understanding of the Company’s business and performance and if not provided would be requested by the investor community . These measures are also useful in understanding performance trends and facilitate comparisons with the performance of other financial institutions . The limitations associated with operating measures are the risk that persons might disagree as to the appropriateness of items comprising these measures and that different companies might calculate these measures differently . The Company provides reconciliations between GAAP and these non - GAAP measures . These disclosures should not be considered an alternative to GAAP . Explanation of Certain Unaudited Non - GAAP Financial Measures 20

( Q2 17 – Q2 18) GAAP to Non - GAAP Reconciliation 21 (Dollars in thousands except per share data) Second Quarter: 2018 First Quarter: 2018 Fourth Quarter: 2017 Third Quarter: 2017Second Quarter: 2017 Net income (loss) 16,964 18,027 13,047 14,216 7,676 Gain on sale of VISA Stock 0 0 (15,153) 47 (21) Securities (gains)/losses, net 48 102 (112) 47 (21) Total Adjustments to Revenue 48 102 (15,265) 47 (21) Merger related charges 695 470 6,817 491 5,081 Amortization of intangibles 1,004 989 963 839 839 Business continuity expenses - Hurricane Irma 0 0 0 352 0 Branch reductions and other expense initiatives 0 0 0 (127) 1,876 Total Adjustments to Noninterest Expense 1,699 1,459 7,780 1,555 7,796 Tax impact of adjustments (433) (538) 3,147 (673) (2,786) Effect of change in corporate tax rate 0 248 8,552 0 0 Adjusted Net Income 18,268 19,298 17,261 15,145 12,665 Earnings per diluted share, as reported 0.35 0.38 0.28 0.32 0.18 Adjusted earnings per diluted share 0.38 0.40 0.37 0.35 0.29 Average shares outstanding (000) 47,974 47,688 46,473 43,792 43,556 Revenue 62,928 62,058 74,868 57,183 54,644 Total Adjustments to Revenue 48 102 (15,265) 47 (21) Adjusted Revenue 62,976 62,160 59,603 57,230 54,623 Noninterest Expense 38,246 37,164 39,184 34,361 41,625 Total Adjustments to Noninterest Expense 1,699 1,459 7,780 1,555 7,796 Adjusted Noninterest Expense 36,547 35,705 31,404 32,806 33,829 Foreclosed property expense and net (gain)/loss on sale 405 192 (7) (296) 297 Net Adjusted Noninterest Expense 36,142 35,513 31,411 33,102 33,532

GAAP to Non - GAAP Reconciliation ( Q2 17 – Q2 18) 22 (Dollars in thousands) Second Quarter: 2018 First Quarter: 2018 Fourth Quarter: 2017 Third Quarter: 2017Second Quarter: 2017 Adjusted Revenue 62,976 62,160 59,603 57,230 54,623 Impact of FTE adjustment 87 91 174 154 164 Adjusted Revenue on a fully taxable equivalent basis 63,063 62,251 59,777 57,384 54,787 Adjusted Efficiency Ratio 57.3% 57.1% 52.6% 57.7% 61.2% Average Assets 5,878,035 5,851,688 5,716,230 5,316,119 5,082,002 Less average goodwill and intangible assets (166,393) (167,136) (149,432) (118,364) (114,563) Average Tangible Assets 5,711,642 5,684,552 5,566,798 5,197,755 4,967,439 Return on Average Assets (ROA) 1.16% 1.25% 0.91% 1.06% 0.61% Impact of removing average intangible assets and related amortization 0.08% 0.09% 0.06% 0.06% 0.05% Return on Tangible Average Assets (ROTA) 1.24% 1.34% 0.97% 1.12% 0.66% Impact of other adjustments for Adjusted Net Income 0.04% 0.04% 0.26% 0.04% 0.36% Adjusted Return on Average Tangible Assets 1.28% 1.38% 1.23% 1.16% 1.02% Average Shareholders' Equity 709,674 695,240 657,100 587,919 567,448 Less average goodwill and intangible assets (166,393) (167,136) (149,432) (118,364) (114,563) Average Tangible Equity 543,281 528,104 507,668 469,555 452,885 Return on Average Shareholders' Equity 9.6% 10.5% 7.9% 9.6% 5.4% Impact of removing average intangible assets and related amortization 3.5% 3.9% 2.8% 2.9% 1.9% Return on Average Tangible Common Equity (ROTCE) 13.1% 14.4% 10.7% 12.5% 7.3% Impact of other adjustments for Adjusted Net Income 0.4% 0.4% 2.8% 0.3% 3.9% Adjusted Return on Average Tangible Common Equity 13.5% 14.8% 13.5% 12.8% 11.2%