Attached files

| file | filename |

|---|---|

| EX-32.2 - U.S. GOLD CORP. | ex32-2.htm |

| EX-32.1 - U.S. GOLD CORP. | ex32-1.htm |

| EX-31.2 - U.S. GOLD CORP. | ex31-2.htm |

| EX-31.1 - U.S. GOLD CORP. | ex31-1.htm |

| EX-23.1 - U.S. GOLD CORP. | ex23-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended April 30, 2018.

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to _______________.

Commission file number: 1-08266

| U.S. GOLD CORP |

| (Exact name of registrant as specified in its charter) |

| Nevada | 22-1831409 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

| 1910 E. Idaho Street, Suite 102-Box 604, Elko, NV | 89801 | |

| Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (800) 557-4550

Securities registered pursuant to section 12(b) of the Act:

| Title of each class | Name of exchange on which registered | |

| Common Stock, $.001 Par Value | NASDAQ Stock Market LLC |

Securities registered pursuant to section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in the definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer a smaller reporting company or an emerging growth company.

See definition of “accelerated filer,” “large accelerated filer,” “smaller reporting company” and “Emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [X] Emerging growth Company [ ]

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial standards provided pursuant to section 13 of the exchange act [ ]

Indicate by check mark whether the registrant is a shell-company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the Common Stock held by non-affiliates of the registrant calculated on the basis of the closing price as of the last business day of the registrant’s most recently completed second quarter, October 31, 2017, was $15,842,437.

The number of shares of Common Stock outstanding on July 30, 2018, was 17,619,084 shares.

DOCUMENTS INCORPORATED BY REFERENCE:

None

U.S. GOLD CORP

INDEX

| 2 |

FORWARD-LOOKING STATEMENTS

Some information contained in or incorporated by reference into this Annual Report on Form 10-K may contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995. These statements include statements relating to our plans to conduct geographic surveys and determine the scope of our drilling program during our fiscal year ended April 30, 2019, the conclusions of a pre-feasibility study and related studies, expectations and the timing and budget for exploration and future development of our properties, our planned expenditures during our fiscal year ended April 30, 2019, our estimates of the cost of future permitting changes and additional bonding requirements, future exploration plans, our expected cash needs, our ability to fund our business with our current cash reserves based on our currently planned activities and statements concerning our financial condition, our plans with respect to future financing options, our anticipation of future environmental impacts, business and operating strategies, and operating and legal risks.

We use the words “anticipate,” “continue,” “likely,” “estimate,” “expect,” “may,” “could,” “will,” “project,” “should,” “believe” and similar expressions to identify forward-looking statements. Statements that contain these words discuss our future expectations and plans, or state other forward-looking information. Although we believe the expectations and assumptions reflected in those forward-looking statements are reasonable, we cannot assure you that these expectations and assumptions will prove to be correct. Our actual results could differ materially from those expressed or implied in these forward-looking statements as a result of various factors described in this annual report on Form 10-K the Risk Factors in Item 1A of this Annual Report.

Many of these factors are beyond our ability to control or predict. Although we believe that the expectations reflected in our forward-looking statements are based on reasonable assumptions, such expectations may prove to be materially incorrect due to known and unknown risk and uncertainties. You should not unduly rely on any of our forward-looking statements. These statements speak only as of the date of this Annual Report on Form 10-K. Except as required by law, we are not obligated to publicly release any revisions to these forward-looking statements to reflect future events or developments. All subsequent written and oral forward-looking statements attributable to us and persons acting on our behalf are qualified in their entirety by the cautionary statements contained in this section and elsewhere in this Annual Report on Form 10-K.

Overview

U.S. Gold Corp., formerly known as Dataram Corporation (the “Company”), was incorporated under the laws of the State of Nevada and was originally incorporated in the State of New Jersey in 1967. Effective June 26, 2017, the Company changed its legal name to U.S. Gold Corp. from Dataram Corporation. On May 23, 2017, the Company merged with Gold King Corp. (“Gold King”), in a transaction treated as a reverse acquisition and recapitalization, and the business of Gold King became the business of the Company. The Company is a gold and precious metals exploration company pursuing exploration and development opportunities primarily in Nevada and Wyoming. None of the Company’s properties contain proven and probable reserves, and all of the Company’s activities on all of its properties are exploratory in nature.

We are an exploration stage company that owns certain mining leases and other mineral rights comprising the Copper King Project in Wyoming and the Keystone Project in Nevada.

Copper King Project

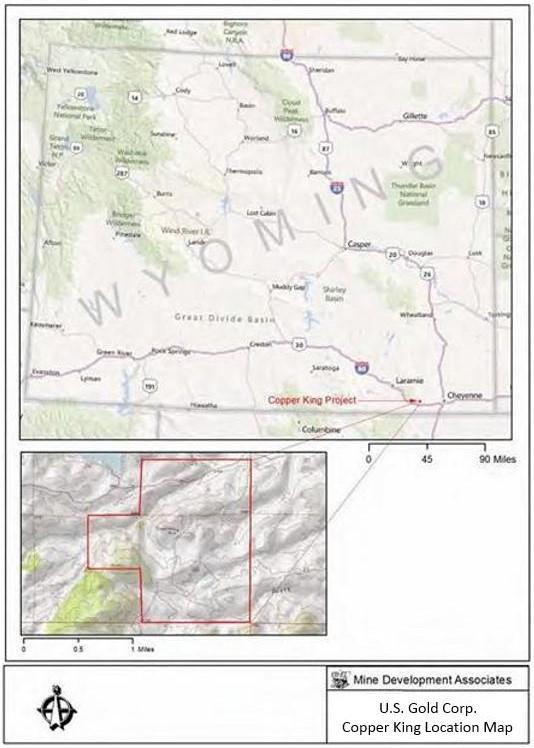

The Copper King Project (the “Copper King Project”) consists of certain mining leases and other mineral rights comprising the Copper King gold and copper development project located in the Silver Crown Mining District of southeast Wyoming.

| 3 |

Location and Access

The Copper King Project is located in southeastern Wyoming, approximately 32km west of the city of Cheyenne, on the southeastern margin of the Laramie Range. The property covers about five square kilometers that include the S½ Section 25, NE¼ Section 35, and all of Section 36, T.14N., R.70W.,Sixth Principal Meridian. Access to within 1.5km of the property is provided by paved and maintained gravel roads. An easement agreement providing access for exploration and other minimal impact activities has been negotiated with Ferguson Ranch Inc. on the S½ Section 25, T14N, R70W, and the W½ Section 30, T14N, R69W. The fee for this easement is $10,000 per year, renewable each year prior to July 11.

The Copper King property covers 453 contiguous hectares (approximately five square kilometers) that include the S½ of Section 25, NE¼ Section 35, and all of Section 36, T.14N., R.70W. The project is entirely located on land owned and administered by the State of Wyoming. There are no federal lands within or adjoining the Copper King land position. Curt Gowdy State Park lies northwest of the property, partially within Section 26. The state park’s southeastern boundary is approximately 300m northwest of the property and approximately 900m northwest of the mineralized area. The Copper King property position consists of two State of Wyoming Metallic and Non-metallic Rocks and Minerals Mining Leases.

Figure 1 – Copper King Project Location and Boundaries

| 4 |

Title to Copper King Project

USG’s rights to the Copper King Project arise under two State of Wyoming mineral leases:

1) State of Wyoming Mining Lease No. 0-40828

Township 14 North, Range 70 West, 6th P.M., Laramie County, Wyoming:

Section 36: All

2) State of Wyoming Mining Lease No. 0-40858

Township 14 North, Range 70 West, 6th P.M., Laramie County, Wyoming:

Section 25: S/2

Section 35: NE/4

Ownership of the mineral rights remains in the possession of the State of Wyoming as conveyed to the State by the United States, evidenced by 1942 patents for Section 36, and 1989 Order confirming title to Section 25 and 35. The State of Wyoming issued Mineral Leases for the mineral rights to Wyoming Gold Mining Company, Inc. (“Wyoming Gold”) in 2013 and 2014. These leases were assigned to us on June 23, 2014.

Lease 0-40828 was renewed in February 2013 for a second ten-year term and Lease 0-40858 was renewed for its second ten-year term in February 2014. Each lease requires an annual payment of $2.00 per acre.

The following production royalties must be paid to the State of Wyoming, although once the project is in operation, the Board of Land Commissioners has the authority to reduce the royalty payable to the State:

| FOB Mine Value per Ton | Percentage Royalty | |||

| $00.00 to $50.00 | 5 | % | ||

| $50.01 to $100.00 | 7 | % | ||

| $100.01 to $150.00 | 9 | % | ||

| $150.01 and up | 10 | % | ||

History of Prior Operations and Exploration on the Copper King Project

Limited exploration and mining were conducted on the Copper King property in the late 1880s and early 1900s. Approximately 300 tons of material was reported to have been produced from a now inaccessible 160 foot-deep shaft with two levels of cross-cuts. A few small adits and prospect pits with no significant production are scattered throughout the property.

Since 1938, at least nine historic (pre-Strathmore Minerals Corp.) drilling campaigns by at least seven companies plus the U.S. Bureau of Mines have been conducted at Copper King. The current project database contains 91 drill holes totaling 37,500 feet that were drilled before Wyoming Gold acquired the property. All but six of the drill holes are within the current resource area. Other work conducted at Copper King by previous companies has included ground and aeromagnetic surveys as well as induced polarization surveys along with geochemical sampling, geologic mapping, and a number of metallurgical studies.

Wyoming Gold conducted an exploration drill program in 2007 and 2008. Thirty-five diamond core drill holes were completed for a total of 25,500 feet. The exploration permit, 360DN, has been terminated and the bond released. The focus of that work was to confirm and potentially expand the mineralized body outlined in the previous drill campaigns, increase the geologic and geochemical database leading to the creation of the current geologic model and resource estimate, and to provide material for further metallurgical testing. The Copper King assay database for some 120 holes contains 8,357 gold assays and 8,225 copper assays. At least 10 different organizations or individuals conducted metallurgical studies on the gold-copper mineralization at the request of prior operators between 1973 and 2009. It was concluded that the process with the highest potential to yield good extractions of gold and copper would likely be flotation, followed by cyanidation of the flotation tailings. Core is stored in two public storage facilities; one is AAA in Cheyenne, Wyoming and the other is Absaroka in Dubois, Wyoming.

| 5 |

Geological Summary of the Copper King Project

The Copper King Project is underlain by Proterozoic rocks that make up the southern end of the Precambrian core of the Laramie Range. Metavolcanic and metasedimentary rocks of amphibolite-grade metamorphism are intruded by the 1.4 billion year old Sherman Granite and related felsic rocks. Within the project area, foliated granodiorite is intruded by aplitic quartz monzonite dikes, thin mafic dikes and younger pegmatite dikes. Shear zones with cataclastic foliation striking N60°E to N60°W are found in the southern part of the Silver Crown district, including at Copper King. The granodiorite typically shows potassium enrichment, particularly near contacts with quartz monzonite. Copper and gold mineralization occurs primarily in unfoliated to mylonitic granodiorite. The mineralization is associated with a N60°W-trending shear zone and disseminated and stockwork gold-copper deposits in the intrusive rocks. Some authors have categorized it as a Proterozoic porphyry gold-copper deposit. Hydrothermal alteration is overprinted on retrograde greenschist alteration and includes a central zone of silicification, followed outward by a narrow potassic zone, surrounded by propylitic alteration. Higher-grade mineralization occurs within a central core of thin quartz veining and stockwork mineralization that is surrounded by a zone of lower-grade disseminated mineralization. Disseminated sulfides and native copper with stockwork malachite and chrysocolla are present at the surface, and chalcopyrite, pyrite, minor bornite, primary chalcocite, pyrrhotite, and native copper are present at depth. Gold occurs as free gold.

Estimated Resources from the Technical Report dated December 5, 2017

The Copper King resource contains oxide, mixed oxide-sulfide, and sulfide rock types. At the stated cutoff grade 0.015oz AuEq/ton, approximately 80% of the resource is sulfide material with the remaining 20% split evenly between the oxide and mixed rock types. There is consistent distribution of gold and copper, albeit generally low-grade, throughout this potential open-pit deposit.

Table 1.1 Summary Tables of Copper King Resources 1

Total Measured and Indicated Resource:

| Au-equiv. Cutoff | ||||||||||||||||||||||||||||||||

| oz AuEq/ton | g AuEq/t | tons | Tonnes | oz Au/ton | g Au/t | oz Au | % Cu | lbs Cu | ||||||||||||||||||||||||

| 0.015 | 0.51 | 59,750,000 | 54,200,000 | 0.015 | 0.53 | 926,000 | 0.187 | 223,000,000 | ||||||||||||||||||||||||

Total Inferred Resource:

| Au-equiv. Cutoff | ||||||||||||||||||||||||||||||||

| oz AuEq/ton | g AuEq/t | tons | Tonnes | oz Au/ton | g Au/t | oz Au | % Cu | lbs Cu | ||||||||||||||||||||||||

| 0.015 | 0.51 | 15,620,000 | 14,170,000 | 0.011 | 0.38 | 174,000 | 0.200 | 62,530,000 | ||||||||||||||||||||||||

Using the individual metal grades of each block, the AuEq grade is calculated using the following formula: g AuEq/t = g Au/t + (2.057143 * %Cu). This formula is based on prices of US$1,275.00 per ounce gold, and US$2.80 per pound copper.

1 Technical Report on the Copper King Project Laramie County, Wyoming, Effective Date December 5, 2017, prepared for U.S. Gold Corp. by Mine Development Associates, authors Paul Tietz and Neil Prenn.

| 6 |

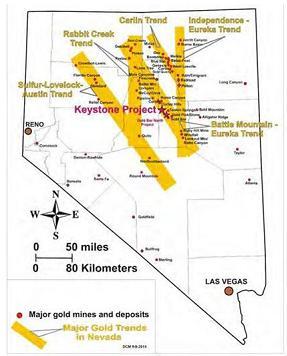

Keystone Project

Location

The Keystone Project consists of 650 unpatented lode mining claims situated in Eureka County, Nevada. The claims making up the Keystone Project are situated in Eureka County, Nevada in Sections 2-4 and 9-11, Township 23 North, Range 48 East, and Sections 22-28, and 33-36 Township 24 North, all Range 48 East of the Mount Diablo Meridian.

Figure 2 – Location of Keystone Project and Major Gold Trends in Nevada

| 7 |

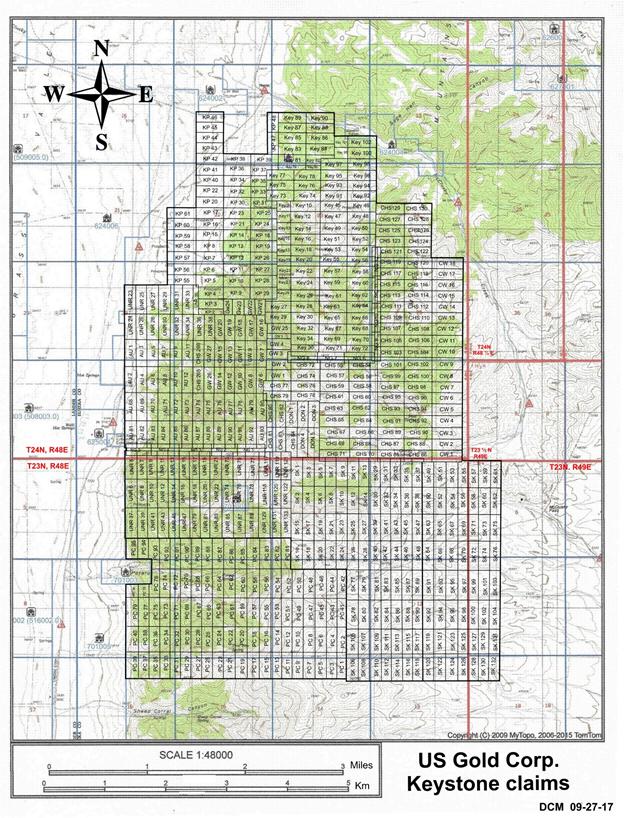

Figure 3 – Keystone Project Claim Boundaries

| 8 |

The Keystone Project may be accessed by improved roads. Navigation through the interior of the project is by off-road vehicle.

Title and Ownership for Keystone Project

The Keystone Project consists of unpatented mining claims located on federal land administered by the U.S. Bureau of Land Management (“BLM”). An annual maintenance fee of $155.00 per claim per year must be paid to the Nevada BLM by September 1 of each year, and failure to make the payment on time renders the claims void.

In addition, the State of Nevada requires the claimant to file an Affidavit and Notice of Intent to Hold in the appropriate county by November 1 of each year. However, the failure to timely record an Affidavit does not affect a forfeiture of the claims, as does the failure to pay the federal claim maintenance fees by September 1. Instead, in the event of a conflict with a junior locator, the senior claimant must prove his intent to maintain the claims. This can generally be accomplished by producing a receipt showing payment of the federal claim maintenance fees to the BLM.

The federal claim maintenance fees are prospective and are paid for the ensuing assessment year. For example, the payments made on June 29, 2015 relate to the 2015-2016 assessment year running from September 1, 2015 to September 1, 2016. By comparison, the Nevada filings are retrospective, describing the assessment year just ended or about to end.

Congress has extended the claim maintenance requirements through 2016. It will therefore be necessary for us to perform the following acts in order to maintain the claims in 2016-2017 and each year thereafter: (1) on or before September 1 of each year, we must pay a maintenance fee of $155.00 per claim to the Nevada BLM, and (2) on or before November 1 of each year we must record an Affidavit and Notice of Intent to Hold in Eureka County.

We acquired the mining claims comprising the Keystone Project on May 27, 2016 from Nevada Gold Ventures, LLC (“Nevada Gold”) and Americas Gold Exploration, Inc. (“Americas Gold”) under the terms of the Purchase and Sale Agreement. Some of the Keystone claims are subject to pre-existing net smelter royalty (“NSR”) obligations. In addition, under the terms of the Purchase and Sale Agreement, Nevada Gold retained additional NSR rights of 0.5% with regard to certain claims and 3.5% with regard to certain other claims. The unpatented mining claims comprising the Keystone Project, with applicable NSR obligations, are as follows:

| 1. | Acquired 100% from Americas Gold; subject to a one percent (1%) NSR held by Wolfpack Gold Nevada Corp.; a two percent (2.0%) NSR with respect to precious metals and one percent (1.0%) NSR with respect to all other metals and minerals held by Orion Royalty Company, LLC; and a one-half percent (0.5%) NSR to Nevada Gold. |

[#] unpatented lode mining claims situated in Eureka County, Nevada, in Sections 33 and 34, Township 24 North, Range 48 East, and Sections 3, 4, 9, and 10, Township 23 North, Range 48 East, Mount Diablo Base Line and Meridian.

| 2. | Acquired 100% from Americas Gold; subject to a three and one-half percent (3.5%) NSR to Nevada Gold |

[#] unpatented lode mining claims situated in Eureka County, Nevada, in Sections 27, 28 and 35, Township 24 North, Range 48 East, and Sections 2 and 3, Township 23 North, Range 48 East, Mount Diablo Base Line and Meridian.

| 3. | Acquired 100% from Nevada Gold; subject to a three and one-half percent (3.5%) NSR to Nevada Gold |

[#] unpatented lode mining claims situated in Eureka County, Nevada, in Sections 2 & 11, Township 23 North, Range 48 East, Mount Diablo Base Line and Meridian.

| 9 |

| 4. | Acquired 50% from Nevada Gold, 50% from Americas Gold, subject to a three and one-half percent (3.5%) NSR to Nevada Gold |

[#] unpatented lode mining claims, alphabetically ordered, situated in Eureka County, Nevada, in Sections 22, 23, 24, 25, 26, 27, 28, 33, 34, 35 & 36, Township 24 North, Range 48 East, Mount Diablo Base Line and Meridian.

Under the terms of the Purchase and Sale Agreement, we may buy down 1% of the NSR owed to Nevada Gold at any time through the fifth anniversary of the closing date for $2,000,000. In addition, we may buy down an additional 1% of the NSR owed to Nevada Gold anytime through the eighth anniversary of the closing date for $5,000,000.

History of Prior Operations and Exploration on the Keystone Project

No comprehensive, modern-era, model-driven exploration has ever been conducted on the Keystone Project. Newmont drilled 6 holes in the old base metal and silver Keystone mine area in 1967, and encountered low grade (+/- 0.02 opt) gold intercepts. Chevron staked the property in 1981-1983 and drilled 27 shallow drill holes, continued by an agreement with USMX that drilled an additional 19 shallow holes; significant amounts of low grade and anomalous gold were intersected, but results were considered uneconomic, and the project dropped. In 1988 and 1989, Phelps Dodge acquired a southern portion of the district and drilled 6 holes, one of which total depth in gold mineralization, and was subsequently deepened in 1990 resulting in over 200’ of low grade gold mineralization. About this time Coral Resources acquired a northern portion of the property and drilled 21 shallow holes to follow-up previous drill intercepts. 1995-1997, Golden Glacier, a junior company, acquired the north end of the district, and Uranerz a portion of the southern area; 6 holes were drilled in the north and only 2 holes in the south, respectively. The entire district was dropped by all parties.

In 2004 with the discovery of Cortez Hills and escalating gold prices, Nevada Pacific Gold, Great American Minerals (Don McDowell), and Tone Resources (Dave Mathewson) competed in claim staking the entire district. Subsequently, Don McDowell, founder of Great American Minerals approached Placer Dome (prior to Barrick acquisition) who discovered Pipeline and Cortez Hills, and who correctly recognized the Keystone district potential. Placer Dome entered into separate joint venture agreements with Nevada Pacific and Great American. The following year Barrick Gold bought Placer Dome and dropped all Placer Dome’s Nevada exploration projects and joint ventures, including Keystone. In 2006, Nevada Pacific and Tone were purchased by USG. USG, now McEwen Mining, drilled 35 holes mostly near the north end of the district; targeting the range front pediment and the historic Keystone Mine.

Geological Potential of the Keystone Project

To date, a technical report has not been prepared on the Keystone Project. Keystone is positioned on the prolific Cortez gold trend, one of the world’s leading gold producing regions. The Keystone Project is centered on a granitic intrusion that warped the local Paleozoic stratigraphy into a dome, allowing for exposure of highly favorable Devonian, Carboniferous (Mississippian-Pennsylvania) and Permo-Triassic rocks including key likely host rocks for mineralization, the silty carbonate strata of the Horse Creek Formation and the Wenban limestone, as well as possible sandy clastic units of the Diamond Peak Formation. The Horse Canyon and Wenban rocks are the primary host rocks at the nearby Cortez Hills Mine and Gold Rush deposit currently operated by Barrick Gold.

| 10 |

Competition

We do not compete directly with anyone for the exploration or removal of minerals from our property as we hold all interest and rights to the claims. Readily available commodities markets exist in the U.S. and around the world for the sale of minerals. Therefore, we will likely be able to sell minerals that we are able to recover. We will be subject to competition and unforeseen limited sources of supplies in the industry in the event spot shortages arise for supplies such as explosives or large equipment tires, and certain equipment such as bulldozers and excavators and services, such as contract drilling that we will need to conduct exploration. If we are unsuccessful in securing the products, equipment and services we need, we may have to suspend our exploration plans until we are able to secure them.

Compliance with Government Regulation

We will be required to comply with all regulations, rules and directives of governmental authorities and agencies applicable to the exploration of minerals in the United States generally. We will also be subject to the regulations of the BLM with respect to mining claims on federal lands.

Future exploration drilling on any of our properties that consist of BLM land will require us to either file a Notice of Intent (NOI) or a Plan of Operations with the BLM, depending upon the amount of new surface disturbance that is planned. A Notice of Intent is required for planned surface activities that anticipate less than 5.0 acres of surface disturbance, and usually can be obtained within a 30 to 60 day time period. Currently, we are working off 5 separate NOIs at Keystone. A Plan of Operations will be required if there is greater than 5.0 acres of new surface disturbance involved with the planned exploration work. A Plan of Operations can take several months to be approved, depending on the nature of the intended work, the level of reclamation bonding required, the need for archeological surveys and other factors as may be determined by the BLM. We filed our Environmental Assessment with the BLM in Q1, 2018. We expect to receive the Finding of No Significant Impact by the end of Q3, 2018. Once approved, this Plan of Operations will give us 200 acres of surface disturbance and greatly expand our exploration potential.

Environmental Permitting Requirements

Various levels of governmental controls and regulations address, among other things, the environmental impact of mineral mining and exploration operations and establish requirements for reclamation of mineral mining and exploration properties after exploration operations have ceased. With respect to the regulation of mineral mining and exploration, legislation and regulations in various jurisdictions establish performance standards, air and water quality emission limits and other design or operational requirements for various aspects of the operations, including health and safety standards. Legislation and regulations also establish requirements for reclamation and rehabilitation of mining properties following the cessation of operations and may require that some former mining properties be managed for long periods of time after mining activities have ceased.

Our activities are subject to various levels of federal and state laws and regulations relating to protection of the environment, including requirements for closure and reclamation of mineral exploration properties. Some of the laws and regulations include the Clean Air Act, the Clean Water Act, the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), the Emergency Planning and Community Right-to-Know Act, the Endangered Species Act, the Federal Land Policy and Management Act, the National Environmental Policy Act, the Resource Conservation and Recovery Act, and related state laws in Nevada. Additionally, much of our property is subject to the federal General Mining Law of 1872, which regulates how mining claims on federal lands are located and maintained.

The State of Nevada, where we focus our mineral exploration efforts, requires mining projects to obtain a Nevada State Reclamation Permit pursuant to the Mined Land Reclamation Act (the “Nevada MLR Act”), which establishes reclamation and financial assurance requirements for all mining operations in the state. New and expanding facilities are required to provide a reclamation plan and financial assurance to ensure that the reclamation plan is implemented upon completion of operations. The Nevada MLR Act also requires reclamation plans and permits for exploration projects that will result in more than five acres of surface disturbance on private lands.

| 11 |

For the fiscal years ended April 30, 2018 and April 30, 2017, compliance costs for the Company regarding environmental permitting requirements and consultancy were $188,433 and $12,667 respectively, for an aggregate for fiscal years ended April 30, 2018 and April 30, 2017 of $201,100, payable to Amec Foster Wheeler plc (now “Wood Group” as of October, 2017).

Employees

As of July 20, 2018, we have 5 full-time employees and no part-time employees.

Gold Bar North

In August 2017, the Company closed on a transaction under a purchase and sale agreement executed in June 2017 with Nevada Gold Ventures LLC and the Buyer pursuant to which Nevada Gold Ventures LLC sold and the Buyer purchased all right, title and interest in the Gold Bar North Property, a gold development project located in Eureka County, Nevada (see Note 3). The purchase price for the Gold Bar North Property was: (a) cash payment in the amount of $20,479 which was paid in August 2017 and (b) 15,000 shares of common stock of the Company which were issued in August 2017. The Company valued these common shares at the fair value of $35,850 or $2.39 per common share based on the quoted trading price on the date of grant. Mr. David Mathewson, the Company’s Chief Geologist, is the managing member of Nevada Gold Ventures LLC. Gold Bar North consists of 49 unpatented lode mining claims situated in Eureka County, Nevada, The Company is currently focusing the majority of its limited resources on exploration activities at the Copper King and Keystone properties.

| 12 |

| 13 |

We will require significant additional capital to fund our business plan.

We will be required to expend significant funds to determine if proven and probable mineral reserves exist at our properties, to continue exploration and if warranted, develop our existing properties and to identify and acquire additional properties to diversify our properties portfolio. We have spent and will be required to continue to expend significant amounts of capital for drilling, geological and geochemical analysis, assaying and feasibility studies with regard to the results of our exploration. We may not benefit from some of these investments if we are unable to identify commercially exploitable mineralized material.

Our ability to obtain necessary funding for these purposes, in turn, depends upon a number of factors, including the status of the national and worldwide economy and the price of gold. Capital markets worldwide have been adversely affected by substantial losses by financial institutions, caused by investments in asset-backed securities. We may not be successful in obtaining the required financing or, if we can obtain such financing, such financing may not be on terms that are favorable to us. Failure to obtain such additional financing could result in delay or indefinite postponement of further mining operations or exploration and development and the possible partial or total loss of our potential interest in our Properties.

We have a limited operating history on which to base an evaluation of our business and prospects.

Since our inception we have had no revenue from operations. We have no history of producing metals from any of our properties. Our properties are exploration stage properties. Advancing properties from exploration into the development stage requires significant capital and time, and successful commercial production from a property, if any, will be subject to completing feasibility studies, permitting and construction of the mine, processing plants, roads, and other related works and infrastructure. As a result, we are subject to all of the risks associated with developing and establishing new mining operations and business enterprises including:

| ● | completion of feasibility studies to verify reserves and commercial viability, including the ability to find sufficient gold mineral reserves to support a commercial mining operation; | |

| ● | the timing and cost, which can be considerable, of further exploration, preparing feasibility studies, permitting and construction of infrastructure, mining and processing facilities; | |

| ● | the availability and costs of drill equipment, exploration personnel, skilled labor and mining and processing equipment, if required; | |

| ● | the availability and cost of appropriate smelting and/or refining arrangements, if required; | |

| ● | compliance with environmental and other governmental approval and permit requirements; | |

| ● | the availability of funds to finance exploration, development and construction activities, as warranted; | |

| ● | potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants which may delay or prevent development activities; | |

| ● | potential increases in exploration, construction and operating costs due to changes in the cost of fuel, power, materials and supplies; and | |

| ● | potential shortages of mineral processing, construction and other facilities related supplies. |

The costs, timing and complexities of exploration, development and construction activities may be increased by the location of our properties and demand by other mineral exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if commenced, development, construction and mine start-up. Accordingly, our activities may not result in profitable mining operations and we may not succeed in establishing mining operations or profitably producing metals at any of our properties.

| 14 |

We have a history of losses and expect to continue to incur losses in the future.

We have incurred losses since inception, have negative cash flow from operating activities and expect to continue to incur losses in the future. We incurred the following losses from continuing operations during each of the following periods:

| ● | $7,827,000 for the year ended April 30, 2018; and | |

| ● | $4,148,000 for the year ended April 30, 2017. |

We expect to continue to incur losses unless and until such time as one of our properties enters into commercial production and generate sufficient revenues to fund continuing operations. We recognize that if we are unable to generate significant revenues from mining operations and dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition.

Exploring for gold is an inherently speculative business.

Natural resource exploration and exploring for gold in particular is a business that by its nature is very speculative. There is a strong possibility that we will not discover gold or any other resources which can be mined or extracted at a profit. Although the Copper King Project has known gold deposits, the deposits may not be of the quality or size necessary for us to make a profit from actually mining it. Few properties that are explored are ultimately developed into producing mines. Unusual or unexpected geological formations, geological formation pressures, fires, power outages, labor disruptions, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are just some of the many risks involved in mineral exploration programs and the subsequent development of gold deposits.

Our directors and executive officers lack significant experience or technical training in exploring for precious and base metal deposits and in developing mines.

Most of our directors and executive officers lack significant experience or technical training in exploring for precious and base metal deposits and in developing mines. Accordingly, although our Chief Geologist has significant experience with early stage gold and base metal exploration, our management may not be fully aware of many of the other specific requirements related to working within this industry. Their decisions and choices may not take into account standard engineering or managerial approaches that mineral exploration companies commonly use. Consequently, our operations, earnings, and ultimate financial success could suffer irreparable harm due to some of our management’s lack of experience in the mining industry.

We will need to obtain additional financing to fund our Copper King, Keystone and Gold Bar North exploration programs.

We may not have sufficient capital to fund our future exploration programs for the Copper King Project, the Keystone Project or the Gold Bar North Project as they are currently planned or to fund the acquisition and exploration of new properties. We will require additional funding to continue our planned future exploration programs. Management estimates that we will require up to $2,500,000 in order to fund our Fiscal Year 2019 combined planned exploration and development programs. Our inability to raise additional funds on a timely basis could prevent us from achieving our business objectives and could have a negative impact on our business, financial condition, results of operations and the value of our securities.

| 15 |

We do not know if our properties contain any gold or other minerals that can be mined at a profit.

Although the properties on which we have the right to explore for gold are known to have deposits of gold, there can be no assurance such deposits can be mined at a profit. Whether a gold deposit can be mined at a profit depends upon many factors. Some but not all of these factors include: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; operating costs and capital expenditures required to start mining a deposit; the availability and cost of financing; the price of gold, which is highly volatile and cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land use, importing and exporting of minerals and environmental protection.

Our Copper King Project and Keystone Property are in the exploration stage.

Copper King has estimated mineral resources identified, but there has not been a mineral reserve estimation in accordance with SEC Industry Guide 7. There are currently no estimates of gold mineralization at the Keystone Property available in historical data obtained during the property purchase. There is no assurance that we can establish the existence of any mineral reserves on Copper King or Keystone in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from the properties and if we do not do so we will lose all of the funds that we expend on exploration. If we do not discover any mineral reserves in a commercially exploitable quantity, the exploration component of our business could fail.

We have not established that our Copper King or Keystone Property contains any mineral reserve according to recognized reserve guidelines, nor can there be any assurance that we will be able to do so. A mineral reserve is defined by the SEC in its Industry Guide 7 as that part of a mineral deposit, which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a “reserve” that meets the requirements of the SEC’s Industry Guide 7 is extremely remote; in all probability our mineral Properties do not contain any “reserves” and any funds that we spend on exploration could be lost. Even if we do eventually discover a mineral reserve on our Properties, there can be no assurance that they can be developed into producing mines and extract those minerals. Both mineral exploration and development involve a high degree of risk and few mineral properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the mineral deposit to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral deposit unprofitable.

We do not have proven or probable reserves, and there is no assurance that the quantities of precious metals we might produce in the future will be sufficient to recover our investment and operating costs.

We do not have proven or probable reserves. Substantial expenditures are required to acquire existing gold properties with established reserves or to establish proven or probable reserves through drilling, analysis and engineering. Any sums expended for additional drilling, analysis and engineering may not establish proven or probable reserves on our properties. We drill in connection with our mineral exploration and not with the purpose of establishing proven and probable reserves. While we estimate the amount of mineralized material we believe exists on our Copper King property, our calculations are subject to uncertainty due to several factors, including the quantity and grade of the mineralized material, metal prices and recoverability of minerals in the mineral recovery process. There is a great degree of uncertainty attributable to the calculation of any mineralized material, particularly where there has not been significant drilling, mining and processing. Until the mineralized material located on our properties is actually mined and processed, the quantity and quality of the mineralized material must be considered as an estimate only. In addition, the estimated value of such mineralized material (regardless of the quantity) will vary depending on metal prices. Any material change in the estimated value of mineralized material may negatively affect the economic viability of our properties. In addition, there can be no assurance that we will achieve the same recoveries of metals contained in the mineralized material as in small-scale laboratory tests or that we will be able to duplicate such results in larger scale tests under on-site conditions or during potential production. There can be no assurance that our exploration activities will result in the discovery of sufficient quantities of mineralized material to recover our investment and operating costs.

| 16 |

We have no history of producing metals from our current mineral properties and there can be no assurance that we will successfully establish mining operations or profitably produce precious metals.

We have no history of producing metals from our current properties. We do not produce gold and do not currently generate operating earnings. While we seek to move our projects and properties into production, such efforts will be subject to all of the risks associated with establishing new mining operations and business enterprises, including:

| ● | the timing and cost, which are considerable, of the construction of mining and processing facilities; | |

| ● | the ability to find sufficient gold reserves to support a profitable mining operation; | |

| ● | the availability and costs of skilled labor and mining equipment; | |

| ● | compliance with environmental and other governmental approval and permit requirements; | |

| ● | the availability of funds to finance construction and development activities; | |

| ● | potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants that may delay or prevent development activities; and | |

| ● | potential increases in construction and operating costs due to changes in the cost of labor, fuel, power, materials and supplies. |

It is common in new mining operations to experience unexpected problems and delays during construction, development and mine start-up. In addition, our management will need to be expanded. This could result in delays in the commencement of mineral production and increased costs of production. Accordingly, we cannot assure you that our activities will result in profitable mining operations or that we will successfully establish mining operations.

Estimates of mineral resources are subject to evaluation uncertainties that could result in project failure.

Our exploration and future mining operations, if any, are and would be faced with risks associated with being able to accurately predict the quantity and quality of mineral resources/reserves within the earth using statistical sampling techniques. Estimates of mineral resource/reserve on our properties would be made using samples obtained from appropriately placed trenches, test pits and underground workings and intelligently designed drilling. There is an inherent variability of assays between check and duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. Additionally, there also may be unknown geologic details that have not been identified or correctly appreciated at the current level of accumulated knowledge about our properties. This could result in uncertainties that cannot be reasonably eliminated from the process of estimating mineral resources/reserves. If these estimates were to prove to be unreliable, we could implement an exploitation plan that may not lead to commercially viable operations in the future.

Any material changes in mineral resource/reserve estimates and grades of mineralization will affect the economic viability of placing a property into production and a property’s return on capital.

As we have not completed feasibility studies on our Copper King, Keystone and Gold Bar North Properties and have not commenced actual production, mineral resource estimates may require adjustments or downward revisions. In addition, the grade ultimately mined, if any, may differ from that indicated by our preliminary economic assessment and drill results. Minerals recovered in small scale tests may not be duplicated in large scale tests under on-site conditions or in production scale.

The mineral resource estimates contained in this Annual Report have been determined based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for gold or copper may render portions of our potential mineralization and resource estimates uneconomic and result in reduced reported mineralization or adversely affect any commercial viability determinations we may reach. Any material reductions in estimates of mineralization, or of our ability to extract this mineralization, could have a material adverse effect on our share price and the value of our Properties.

| 17 |

We may not be able to obtain all required permits and licenses to place any of our properties into future potential production.

Our current and future operations, including development activities and commencement of production, if warranted, require permits from governmental authorities and such operations are and will be governed by laws and regulations governing prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. Companies engaged in mineral property exploration and the development or operation of mines and related facilities generally experience increased costs, and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. We cannot predict if all permits which we may require for continued exploration, development or construction of mining facilities and conduct of mining operations will be obtainable on reasonable terms, if at all. Costs related to applying for and obtaining permits and licenses may be prohibitive and could delay our planned exploration and development activities. Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions.

Parties engaged in mining operations may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations. Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on our operations and cause increases in capital expenditures or production costs or reduction in levels of production at producing properties or require abandonment or delays in development of new mining properties.

We are subject to significant governmental regulations, which affect our operations and costs of conducting our business.

Our current and future operations are and will be governed by laws and regulations, including:

| ● | laws and regulations governing mineral concession acquisition, prospecting, development, mining and production; | |

| ● | laws and regulations related to exports, taxes and fees; | |

| ● | labor standards and regulations related to occupational health and mine safety; and | |

| ● | environmental standards and regulations related to waste disposal, toxic substances, land use and environmental protection. |

Companies engaged in exploration activities often experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. Failure to comply with applicable laws, regulations and permits may result in enforcement actions, including the forfeiture of mineral claims or other mineral tenures, orders issued by regulatory or judicial authorities requiring operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or costly remedial actions. We may be required to compensate those suffering loss or damage by reason of our mineral exploration activities and may have civil or criminal fines or penalties imposed for violations of such laws, regulations and permits. Existing and possible future laws, regulations and permits governing operations and activities of exploration companies, or more stringent implementation, could have a material adverse impact on our business and cause increases in capital expenditures or require abandonment or delays in exploration.

| 18 |

Our business is subject to extensive environmental regulations that may make exploring, mining or related activities prohibitively expensive, and which may change at any time.

All of our operations are subject to extensive environmental regulations that can substantially delay exploration and mine development and make exploration and mine development expensive or prohibit it altogether. We may be subject to potential liabilities associated with the pollution of the environment and the disposal of waste products that may occur as the result of exploring and other related activities on our properties. We may have to pay to remedy environmental pollution, which may reduce the amount of money that we have available to use for exploration, mine development, or other activities, and adversely affect our financial position. If we are unable to fully remedy an environmental problem, we might be required to suspend operations or to enter into interim compliance measures pending the completion of the required remedy. If a decision is made to mine our properties and we retain any operational responsibility for doing so, our potential exposure for remediation may be significant, and this may have a material adverse effect upon our business and financial position. We have not purchased insurance for potential environmental risks (including potential liability for pollution or other hazards associated with the disposal of waste products from our exploration activities) and such insurance may not be available to us on reasonable terms or at a reasonable price. All of our exploration and, if warranted, development activities will be subject to regulation under one or more local, state and federal environmental impact analyses and public review processes. It is possible that future changes in applicable laws, regulations and permits or changes in their enforcement or regulatory interpretation could have significant impact on some portion of our business, which may require our business to be economically re-evaluated from time to time. These risks include, but are not limited to, the risk that regulatory authorities may increase bonding requirements beyond our financial capability. Inasmuch as posting of bonding in accordance with regulatory determinations is a condition to the right to operate under specific federal and state operating permits, increases in bonding requirements could prevent operations even if we are in full compliance with all substantive environmental laws.

Regulations and pending legislation governing issues involving climate change could result in increased operating costs, which could have a material adverse effect on our business.

A number of governments or governmental bodies have introduced or are contemplating regulatory changes in response to various climate change interest groups and the potential impact of climate change. Legislation and increased regulation regarding climate change could impose significant costs on us, our venture partners and our suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting and other costs to comply with such regulations. Any adopted future climate change regulations could also negatively impact our ability to compete with companies situated in areas not subject to such limitations. Given the emotion, political significance and uncertainty around the impact of climate change and how it should be dealt with, we cannot predict how legislation and regulation will affect our financial condition, operating performance and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by us or other companies in our industry could harm our reputation. The potential physical impacts of climate change on our operations are highly uncertain, and would be particular to the geographic circumstances in areas in which we operate. These may include changes in rainfall and storm patterns and intensities, water shortages, changing sea levels and changing temperatures. These impacts may adversely impact the cost, production and financial performance of our operations.

| 19 |

We may be denied the government licenses and permits which we need to explore on our properties. In the event that we discover commercially exploitable deposits, we may be denied the additional government licenses and permits which we will need to mine our properties.

Exploration activities usually require the granting of permits from various governmental agencies. For example, exploration drilling on unpatented mineral claims requires a permit to be obtained from the United States BLM, which may take several months or longer to grant the requested permit. Depending on the size, location and scope of the exploration program, additional permits may also be required before exploration activities can be undertaken. Prehistoric or Indian grave yards, threatened or endangered species, archeological sites or the possibility thereof, difficult access, excessive dust and important nearby water resources may all result in the need for additional permits before exploration activities can commence. As with all permitting processes, there is the risk that unexpected delays and excessive costs may be experienced in obtaining required permits. The needed permits may not be granted at all. Delays in or our inability to obtain necessary permits will result in unanticipated costs, which may result in serious adverse effects upon our business.

The values of our properties are subject to volatility in the price of gold and any other deposits we may seek or locate.

Our ability to obtain additional and continuing funding, and our profitability in the unlikely event we ever commence mining operations or sell the rights to mine, will be significantly affected by changes in the market price of gold. Gold prices fluctuate widely and are affected by numerous factors, all of which are beyond our control. Some of these factors include the sale or purchase of gold by central banks and financial institutions; interest rates; currency exchange rates; inflation or deflation; fluctuation in the value of the United States dollar and other currencies; speculation; global and regional supply and demand, including investment, industrial and jewelry demand; and the political and economic conditions of major gold or other mineral producing countries throughout the world, such as Russia and South Africa. The price of gold or other minerals have fluctuated widely in recent years, and a decline in the price of gold could cause a significant decrease in the value of our properties, limit our ability to raise money, and render continued exploration and development of our properties impracticable. If that happens, then we could lose our rights to our properties and be compelled to sell some or all of these rights. Additionally, the future development of our properties beyond the exploration stage is heavily dependent upon the level of gold prices remaining sufficiently high to make the development of our properties economically viable. You may lose your investment if the price of gold decreases. The greater the decrease in the price of gold, the more likely it is that you will lose money.

Our property titles may be challenged and we are not insured against any challenges, impairments or defects to our mineral claims or property titles. We have not fully verified title to our properties.

Our unpatented Keystone claims were created and maintained in accordance with the federal General Mining Law of 1872. Unpatented claims are unique U.S. property interests and are generally considered to be subject to greater title risk than other real property interests because the validity of unpatented claims is often uncertain. This uncertainty arises, in part, out of the complex federal and state laws and regulations under the General Mining Law. We have obtained a title report on our Keystone claims, but cannot be certain that all defects or conflicts with our title to those claims have been identified. Further, we have not obtained title insurance regarding our purchase and ownership of the Keystone claims. Defending any challenges to our property titles may be costly, and may divert funds that could otherwise be used for exploration activities and other purposes. In addition, unpatented claims are always subject to possible challenges by third parties or contests by the federal government, which, if successful, may prevent us from exploiting our discovery of commercially extractable gold. Challenges to our title may increase its costs of operation or limit our ability to explore on certain portions of our properties. We are not insured against challenges, impairments or defects to our property titles, nor do we intend to carry extensive title insurance in the future.

| 20 |

The value of our property and any other deposits we may seek or locate is subject to volatility in the price of gold.

Our ability to obtain additional and continuing funding, and our profitability if and when we commence mining or sell our rights to mine, will be significantly affected by changes in the market price of gold and other mineral deposits. Gold and other minerals prices fluctuate widely and are affected by numerous factors, all of which are beyond our control. The price of gold may be influenced by:

| ● | fluctuation in the supply of, demand and market price for gold; | |

| ● | mining activities of our competitors; | |

| ● | sale or purchase of gold by central banks and for investment purposes by individuals and financial institutions; | |

| ● | interest rates; | |

| ● | currency exchange rates; | |

| ● | inflation or deflation; | |

| ● | fluctuation in the value of the United States dollar and other currencies; | |

| ● | global and regional supply and demand, including investment, industrial and jewelry demand; and | |

| ● | political and economic conditions of major gold or other mineral-producing countries. |

The price of gold and other minerals have fluctuated widely in recent years, and a decline in the price of gold or other minerals could cause a significant decrease in the value of our property, limit our ability to raise money, and render continued exploration and development of our property impracticable. If that happens, then we could lose our rights to our property or be compelled to sell some or all of these rights. Additionally, the future development of our mining properties beyond the exploration stage is heavily dependent upon gold prices remaining sufficiently high to make the development of our property economically viable.

Possible amendments to the General Mining Law and other environmental regulations could make it more difficult or impossible for us to execute our business plan.

In recent years, the U.S. Congress has considered a number of proposed amendments to the General Mining Law, as well as legislation that would make comprehensive changes to the law. Although no such comprehensive legislation has been adopted to date, there can be no assurance that such legislation will not be adopted in the future. If adopted, such legislation, if it includes concepts that have been part of previous legislative proposals, could, among other things, (i) limit on the number of millsites that a claimant may use, discussed below, (ii) impose time limits on the effectiveness of plans of operation that may not coincide with mine life, (iii) impose more stringent environmental compliance and reclamation requirements on activities on unpatented mining claims and millsites, (iv) establish a mechanism that would allow states, localities and Native American tribes to petition for the withdrawal of identified tracts of federal land from the operation of the General Mining Law, (v) allow for administrative determinations that mining would not be allowed in situations where undue degradation of the federal lands in question could not be prevented, (vi) impose royalties on gold and other mineral production from unpatented mining claims or impose fees on production from patented mining claims, and (vii) impose a fee on the amount of material displaced at a mine. Further, such legislation, if enacted, could have an adverse impact on earnings from our operations, could reduce estimates of any reserves we may establish and could curtail our future exploration and development activity on our unpatented claims.

| 21 |

Our ability to conduct exploration, development, mining and related activities may also be impacted by administrative actions taken by federal agencies. With respect to unpatented millsites, for example, the ability to use millsites and their validity has been subject to greater uncertainty since 1997. In November of 1997, the Secretary of the Interior (appointed by President Clinton) approved a Solicitor’s Opinion that concluded that the General Mining Law imposed a limitation that only a single five-acre millsite may be claimed or used in connection with each associated and valid unpatented or patented lode mining claim. Subsequently, however, on November 7, 2003, the new Secretary of the Interior (appointed by President Bush) approved an Opinion by the Deputy Solicitor which concluded that the mining laws do not impose a limitation that only a single five-acre millsite may be claimed in connection with each associated unpatented or patented lode mining claim. Current federal regulations do not include the millsite limitation. There can be no assurance, however, that the Department of the Interior will not seek to re-impose the millsite limitation at some point in the future.

In addition, a consortium of environmental groups has filed a lawsuit in the United District Court for the District of Columbia against the Department of the Interior, the Department of Agriculture, the BLM, and the U.S. Forest Service (“USFS”), asking the court to order the BLM and USFS to adopt the five-acre millsite limitation. That lawsuit also asks the court to order the BLM and the USFS to require mining claimants to pay fair market value for their use of the surface of federal lands where those claimants have not demonstrated the validity of their unpatented mining claims and millsites. If the plaintiffs in that lawsuit were to prevail, that could have an adverse impact on our ability to use our unpatented millsites for facilities ancillary to our exploration, development and mining activities, and could significantly increase the cost of using federal lands at our properties for such ancillary facilities.

In 2009, the U.S. Environmental Protection Agency (“EPA”) announced that it would develop financial assurance requirements under CERCLA Section 108(b) for the hard rock mining industry. On January 29, 2016, the U.S. District Court for the District of Columbia issued an order requiring that if the EPA intended to prepare such regulations, it had to do so by December 1, 2016. The EPA did comply with that order by issuing draft proposed regulations on December 1, 2016. The EPA subsequently issued its proposed rule on January 11, 2017. Under the proposed rule, owners and operators of facilities subject to the rule have been required, among other things, to (i) notify the EPA that they are subject to the rule; (ii) calculate a level of financial responsibility for their facility using a formula provided in the rule; (iii) obtain a financial responsibility instrument, or qualify to self-assure, for the amount of financial responsibility; (iv) demonstrate that they had obtained such evidence of financial responsibility; and (v) update and maintain financial responsibility until the EPA released the owner or operator from the CERCLA Section 108(b) regulations. As drafted, those additional financial assurance obligations could have been in addition to the reclamation bonds and other financial assurances we have and would be required to have in place under current federal and state laws. If such requirements had been retained in the final rule, they could have required significant additional expenditures on financial assurance, which could have had a material adverse effect on the our future business operations.

However, after an extended public comment period, the EPA decided on December 1, 2017 not to adopt the proposed rule, and not to impose additional financial assurance obligations on the hard rock mining industry. It is possible that one or more non-governmental organizations will file lawsuits challenging that decision.

Market forces or unforeseen developments may prevent us from obtaining the supplies and equipment necessary to explore for gold and other minerals.

Gold exploration, and mineral exploration in general, is a very competitive business. Competitive demands for contractors and unforeseen shortages of supplies and/or equipment could result in the disruption of our planned exploration activities. Current demand for exploration drilling services, equipment and supplies is robust and could result in suitable equipment and skilled manpower being unavailable at scheduled times for our exploration program. Fuel prices are extremely volatile as well. We will attempt to locate suitable equipment, materials, manpower and fuel if sufficient funds are available. If we cannot find the equipment and supplies needed for our various exploration programs, we may have to suspend some or all of them until equipment, supplies, funds and/or skilled manpower become available. Any such disruption in our activities may adversely affect our exploration activities and financial condition.

| 22 |

We may not be able to maintain the infrastructure necessary to conduct exploration activities.

Our exploration activities depend upon adequate infrastructure. Reliable roads, bridges, power sources and water supply are important factors which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect our exploration activities and financial condition.

We rely on contractors to conduct a significant portion of our operations and construction projects.

A significant portion of our operations and construction projects are currently conducted in whole or in part by contractors. As a result, our operations are subject to a number of risks, some of which are outside our control, including:

| ● | negotiating agreements with contractors on acceptable terms; |

| ● | the inability to replace a contractor and its operating equipment in the event that either party terminates the agreement; |

| ● | reduced control over those aspects of operations which are the responsibility of the contractor; |

| ● | failure of a contractor to perform under its agreement; |

| ● | interruption of operations or increased costs in the event that a contractor ceases its business due to insolvency or other unforeseen events; |

| ● | failure of a contractor to comply with applicable legal and regulatory requirements, to the extent it is responsible for such compliance; and |

| ● | problems of a contractor with managing its workforce, labor unrest or other employment issues. |

In addition, we may incur liability to third parties as a result of the actions of our contractors. The occurrence of one or more of these risks could adversely affect our results of operations and financial position.

Our exploration activities and any future mine development may be adversely affected by the local climate or seismic events, which could prevent us from gaining access to our property year-round.

Earthquakes, heavy rains, snowstorms, and floods could result in serious damage to or the destruction of facilities, equipment or means of access to our property, or may otherwise prevent us from conducting exploration activities on our property. There may be short periods of time when the unpaved portion of the access road is impassible in the event of extreme weather conditions or unusually muddy conditions. During these periods, it may be difficult or impossible for us to access our property, make repairs, or otherwise conduct exploration or mine development activities on them.

We may be unable to secure surface access or purchase required surface rights.

Although the Company acquires the rights to some or all of the minerals in the ground subject to the mineral tenures that it acquires, or has a right to acquire, in most cases it does not thereby acquire any rights to, or ownership of, the surface to the areas covered by such mineral tenures. In such cases, applicable mining laws usually provide for rights of access to the surface for the purpose of carrying on mining activities, however, the enforcement of such rights through the courts can be costly and time consuming. It is necessary to negotiate surface access or to purchase the surface rights if long-term access is required. There can be no guarantee that, despite having the right at law to access the surface and carry on exploration and future potential mining activities, we will be able to negotiate satisfactory agreements with any such existing landowners/occupiers for such access or purchase of such surface rights, and therefore we may be unable to carry out planned exploration and future potential mining activities. In addition, in circumstances where such access is denied, or no agreement can be reached, we may need to rely on the assistance of local officials or the courts in such jurisdiction the outcomes of which cannot be predicted with any certainty. Our inability to secure surface access or purchase required surface rights could materially and adversely affect our timing, cost or overall ability to develop any mineral deposits we may locate.

| 23 |

Joint ventures and other partnerships may expose us to risks.

We may enter into future joint ventures or partnership arrangements with other parties in relation to the exploration, development and production of a certain portion of the Copper King, Keystone and Gold Bar North Properties in which we have an interest. Joint ventures can often require unanimous approval of the parties to the joint venture or their representatives for certain fundamental decisions such as an increase or reduction of registered capital, merger, division, dissolution, amendments of consenting documents, and the pledge of joint venture assets, which means that each joint venture party may have a veto right with respect to such decisions which could lead to a deadlock in the operations of the joint venture. Further, we may be unable to exert control over strategic decisions made in respect of such properties. Any failure of such other companies to meet their obligations to us or to third parties, or any disputes with respect to the parties’ respective rights and obligations, could have a material adverse effect on the joint ventures or their properties and therefore could have a material adverse effect on our results of operations, financial performance, cash flows and the price of the Common Shares.

We may experience difficulty attracting and retaining qualified management to meet the needs of our anticipated growth, and the failure to manage our growth effectively could have a material adverse effect on our business and financial condition.

We are dependent on a relatively small number of key employees, including our President and Chief Executive Officer, our Chief Operating Officer and our Chief Geologist. The loss of any officer could have an adverse effect on us. We have no life insurance on any individual, and we may be unable to hire a suitable replacement for them on favorable terms, should that become necessary.

We may have exposure to greater than anticipated tax liabilities.

Our future income taxes could be adversely affected by earnings being lower than anticipated in jurisdictions that have lower statutory tax rates and higher than anticipated in jurisdictions that have higher statutory tax rates, changes in the valuation of our deferred tax assets or liabilities, or changes in tax laws, regulations, or accounting principles, as well as certain discrete items. We are subject to review or audit by tax authorities. As a result, we may in the future receive assessments in multiple jurisdictions on various tax-related assertions. Any adverse outcome of such a review or audit could have a negative effect on our operating results and financial condition. In addition, the determination of our provision for income taxes and other tax liabilities requires significant judgment, and there could be situations where the ultimate tax determination is uncertain. Although we believe our estimates are reasonable, the ultimate tax outcome may differ from the amounts recorded in our financial statements and may materially affect our financial results in the period or periods for which such determination is made.

Risks Related to Ownership of Our Common Stock

If we fail to establish and maintain an effective system of internal control, we may not be able to report our financial results accurately or to prevent fraud. Any inability to report and file our financial results accurately and timely could harm our reputation and adversely impact the trading price of our common stock and our ability to file registration statements pursuant to registration rights agreements and other commitments.

Effective internal control is necessary for us to provide reliable financial reports and prevent fraud. If we cannot provide reliable financial reports or prevent fraud, we may not be able to manage our business as effectively as we would if an effective control environment existed, and our business and reputation with investors may be harmed. As a result of our small size, any current internal control deficiencies may adversely affect our financial condition, results of operation and access to capital. As of April 30, 2018, management has concluded that our internal controls over financial reporting were not effective.

| 24 |

Public company compliance may make it more difficult to attract and retain officers and directors.