Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - BANC OF CALIFORNIA, INC. | d582337dex991.htm |

| 8-K - 8-K - BANC OF CALIFORNIA, INC. | d582337d8k.htm |

July 26, 2018

2018 Second Quarter Earnings

Investor Presentation

Exhibit 99.2 |

| 1 1 When used in this presentation and in documents filed with or furnished to the Securities and Exchange Commission (the “SEC”),

in press releases or other public stockholder communications, or

in oral statements made with the approval of an authorized executive officer, the words or phrases “believe,” “will,” “should,” “will likely result,” “are expected to,”

“will continue,” “is anticipated,” “estimate,”

“project,” “plans,” or similar expressions are intended to identify “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. You are cautioned not to place undue reliance on any forward-looking statements, which speak

only as of the date made. These statements may relate to

future financial performance, strategic plans or objectives,

revenue, expense or earnings projections, or other financial items of Banc of California Inc. and its affiliates (“BANC,” the “Company,” “we,” “us” or “our”). By their nature, these statements are subject to numerous

uncertainties that could cause actual results to differ

materially from those anticipated in the statements.

Factors that could cause actual results to differ materially from the results

anticipated or projected include, but are not limited to, the following: (i) a pending investigation by the SEC may result in adverse findings, reputational damage, the imposition of sanctions, increased costs and other negative consequences; (ii)

management time and resources may be diverted to address the

pending SEC investigation as well as any related litigation, litigation initiated by stockholders and other litigation; (iii) the costs and effects of litigation, including settlements

and judgments; (iv) our performance may be adversely affected by the management

transition we have recently undergone; (v) the risk that the savings we actually realize from our recently announced reduction in force and planned reduction in use of third party advisors will be less than anticipated and

the risk that the costs associated with the reduction in force

will be greater than anticipated; (vi) risks that the

Company’s merger and acquisition transactions may disrupt current plans and operations and lead to difficulties in customer and employee retention, risks that the costs, fees, expenses and charges related to these transactions could be significantly higher than anticipated

and risks that the expected revenues, cost savings, synergies and

other benefits of these transactions might not be realized to the extent anticipated, within the anticipated timetables, or at all; (vii) risks that funds obtained from capital raising activities will not be utilized efficiently or effectively; (viii) a worsening of current economic conditions, as well as turmoil

in the financial markets; (ix) the credit risks of lending

activities, which may be affected by deterioration in real estate markets and

the financial condition of borrowers, may lead to increased loan and lease delinquencies, losses and nonperforming assets in our loan and lease portfolio, and may result in our allowance for loan and lease losses not being adequate to

cover actual losses and require us to materially increase our

loan and lease loss reserves; (x) the quality and composition of our securities portfolio; (xi) changes in general economic conditions, either nationally or in our market areas, or changes in financial markets; (xii) continuation of or changes in the historically low short-term interest rate environment, changes

in the levels of general interest rates, volatility in the

interest rate environment, the relative differences between

short- and long-term interest rates, deposit interest

rates, our net interest margin and funding sources; (xiii)

fluctuations in the demand for loans and leases, the number of

unsold homes and other properties and fluctuations in commercial and residential real estate values in our market area; (xiv) our ability to develop and maintain a strong core deposit base or other low cost funding sources necessary to fund our activities; (xv) results of

examinations of us by regulatory authorities and the possibility

that any such regulatory authority may, among other things, limit our business activities, require us to change our business mix, increase our allowance for loan and lease losses, write-down asset values or increase our capital levels, or affect our ability to borrow funds or maintain or increase deposits, any

of which could adversely affect our liquidity and earnings; (xvi)

legislative or regulatory changes that adversely affect our business, including, without limitation, changes in tax laws and policies and changes in regulatory capital or other rules, as

well as additional regulatory burdens that result from our growth to over $10

billion in total assets; (xvii) our ability to control operating costs and expenses; (xviii) staffing fluctuations in response to product demand or the implementation of corporate strategies that affect our work force and potential associated charges;

(xix) errors in estimates of the fair values of certain of our

assets and liabilities, which may result in significant changes in valuation; (xx) the network and computer systems on which we depend could fail or experience a security breach; (xxi) our ability to attract and retain key members of our senior management team; (xxii) increased competitive pressures among financial

services companies; (xxiii) changes in consumer spending,

borrowing and saving habits; (xxiv) adverse changes in the securities markets; (xxv) earthquake, fire or other natural disasters affecting the condition of real estate collateral; (xxvi) the availability of resources to address changes in laws, rules or regulations or to respond to regulatory actions; (xxvii)

inability of key third-party providers to perform their

obligations to us; (xxviii) changes in accounting policies and practices, as

may be adopted by the financial institution regulatory agencies or the Financial Accounting Standards Board or their application to our business or final audit adjustments, including additional guidance and interpretation on accounting issues and

details of the implementation of new accounting methods; (xxix)

share price volatility and reputational risks, related to, among other things, speculative trading and certain traders shorting our common shares and attempting to generate negative publicity about us; (xxx) war or terrorist activities; and (xxxi) other economic, competitive, governmental, regulatory, and

technological factors affecting our operations, pricing, products

and services and the other risks described from time to time in other documents that we file with or furnish to the SEC. You should not place undue reliance on forward-looking statements, and we undertake no obligation to update any such statements to reflect circumstances or events that occur after

the date on which the forward-looking statement is

made. Forward-looking Statements

|

2 2 Strong Organic Loan Growth Continuation of Balance Sheet Re-Mix Disciplined Expense Management Held for investment loans grew by $105 million, or 2% QoQ (6% annualized) – Gross loan commitment originations of $765 million at an average production yield of 5.05%

Sold $204 million of performing SFR/MF loans to manage interest rate

risk Second

quarter noninterest expense totaled $62.6 million Non-recurring expenses of $6.4 million including $1.5 million of net legal and professional fees, a

$0.4 million legal settlement expense, $0.5 million charge to write off

certain software models related to DFAST, and $4.0 million

restructure expense associated with the reduction in force

executed on June 26th

Credit and Capital Net charge-offs totaled $738,000, including $372,000 related to performing loan sale

NPAs /Assets of 0.22% and ALLL / Loans increased to 0.81%, up from 0.71% a year ago Total delinquencies (delinquent non-PCI loans to total non-PCI loans) declined to 0.38%

from 0.63% at the end of the prior quarter

Common Equity Tier 1 ratio of 9.90%

Second Quarter 2018 Highlights

Further Progress Towards a Core Commercial Bank Platform

Managing Talent Hired Jim Hazboun as Chief Human Resources Officer Promoted Jason Pendergist to Head of Commercial Banking Reduced securities by $127 million for the quarter, driven by a net decline in collateralized

loan obligation securities (“CLOs”) from sale and call activity

totaling $74 million and the sale of $41 million of commercial

mortgage-backed securities (“CMBS”) Reduced FHLB

advances by $100 million due to improved core deposit growth

1 Held for investment Core deposit balances increased by $357 million, and brokered deposit balances declined

by $332 million

Stabilization of

Core Deposits 1 1 |

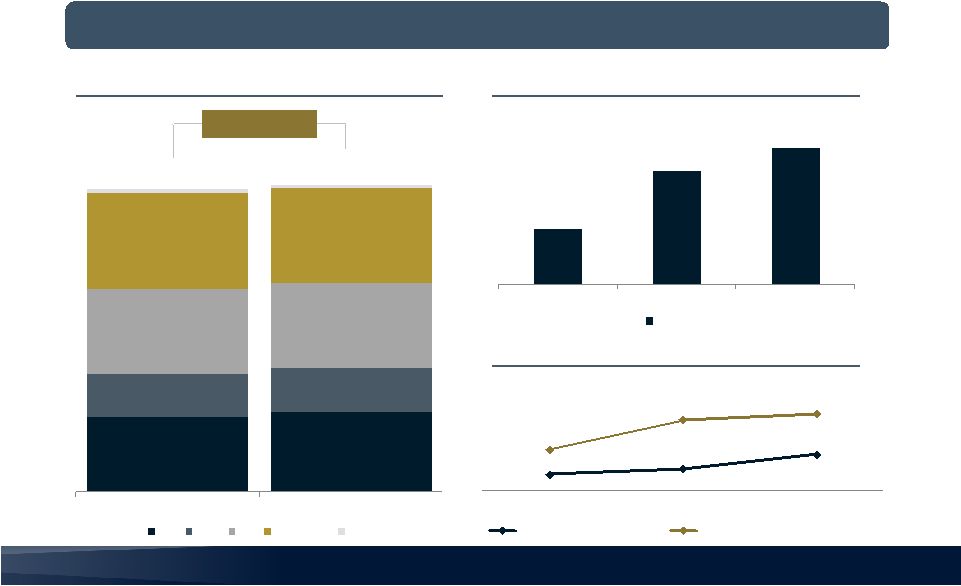

3 3 1 Dollars in millions Total Assets $10,319 ($127) $10,329 $12 $105 1Q18 Cash and Other Securities HFI Loans 2Q18 Strategic Asset Re-Mix Continues Re-Mix of Balance Sheet Toward Core HFI Loans Through Reduced Securities

Q2 Strategic Balance Sheet Re-Mix Activities

1 2 Securities declined by $127 million, including: - Sale of $41 million of CMBS - CLO net runoff of $74 million Increased overall HFI loans by $105 million, or 2% from the prior quarter 1 2 1 |

4 4 BANC Strategic Roadmap: Scorecard Building Core Earnings Power for Sustainable Growth and Returns Over the Long Term

Strategy Components

Tracking Guideposts 1st Half 2018 Results Build Core Deposits Core Deposit Balance Growth Core deposits increased $413 million In Q1, completed the run-off of $207 million of legacy high-rate, high volatility deposits Brokered deposits declined $363 million Amplify Lending Annual Net Loan Growth Loan Originations Securities / Assets (%) HFI loan growth of $377 million, or 11% annualized $1.63 billion of gross loan commitment originations Securities / assets of 22%, down from 25% at YE Normalize Expenses Noninterest Expenses / Average Assets NIE 1 / average assets of 2.21%, down from 2.33% at Q4’17 Continuing to invest in sales and originations while driving efficiencies in support area Creating Stockholder Value ROAA ROATCE Aligned Incentive Plan 0.46% 4.18% 2018 Annual Incentive Plan targets published: Core deposit growth, ROAA, loan growth, adjusted efficiency ratio (%). Additional gating criteria for CET1 ratio (%) and non-performing assets (%). 1 Operating expenses, non-GAAP measure, see reconciliation on slide 8.

2 Non-GAAP measure, see reconciliation on slide 19. 2 1 |

5 5 1 Dollars in millions 2 Core deposits defined as non-brokered deposits Deposit Composition 1 $5,630 $5,685 $6,043 $207 $1,456 $1,425 $1,093 $7,293 $7,110 $7,136 77% 80% 85% 4Q17 1Q18 2Q18 Change 2Q18 vs. 1Q18 $332 $357 Build Core Deposits: Stabilized Core Deposit

Base Core Deposits Increased by $357 Million in the Quarter,

While Brokered Declined by $332 Million BANC

Brokered Institutional Bank (IB) Run-off Core Deposits Core Deposits (% of Deposits) 2 |

6 6 1 Dollars in millions 2 Includes Construction 3 Gross loan commitment originations YTD gross loan production 3 of $1.63 billion at 5.01% average production yield Loans Held for Investment 1 Loans Held for Investment 1 $7,036 1Q18 2Q18 C&I CRE² MF Residential Other 25% 14% 28% 32% +2% Q/Q $6,659 $6,931 $7,036 4Q17 1Q18 2Q18 Period End Amplify Lending: Growing Loan Balances

Loan Production Efforts Driving Higher Loan Balances

B ANC

4.42% 4.48% 4.63% 4.68% 4.99% 5.05% 4Q17 1Q18 2Q18 Portfolio Loan Yields New Production Loan Yields Loan Production Yields Above Loan Portfolio Yields 1% 26% 14% 28% 31% 1% $6,931 |

7 7 $6.7 $7.0 $2.5 $2.3 $0.5 $0.4 $9.7 $9.7 1Q18 2Q18 Loans (HFI) Securities Other Net Interest Margin Stabilized Benefiting from Re-mix of Securities to Loans and Wholesale Funding to Core Deposits

Net Interest Margin Components

3.88% 3.92% 4.04% 4.00% 4.12% 4.35% 3.19% 3.09% 3.15% 3.01% 2.98% 3.01% 0.64% 0.73% 0.80% 0.87% 0.96% 1.15% 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 Earning Asset Yield Net Interest Margin Cost of Deposits Interest Earning Assets 1 1 Average, dollars in billions 2 Includes loans held for sale and other interest-earning assets

3 Dollars in millions, consolidated operations $105.4 $(0.1) $98.9 $1.5 $5.1 1Q18 Securities, HFS, & Other Residential Mortgage - HFI Commercial Loans 2Q18 Interest Income 3 2 |

8 8 1 Loss on investments in alternative energy partnerships create tax credits to offset expense incurred.

2

Continuing operations operating expense less non-recurring

adjustments. Non-GAAP measure: Reconciliation table above.

3 Continuing operations noninterest expense excluding loss on investments in alternative energy partnerships, annualized, over average

consolidated assets. Non-Recurring Adjustments to Continuing

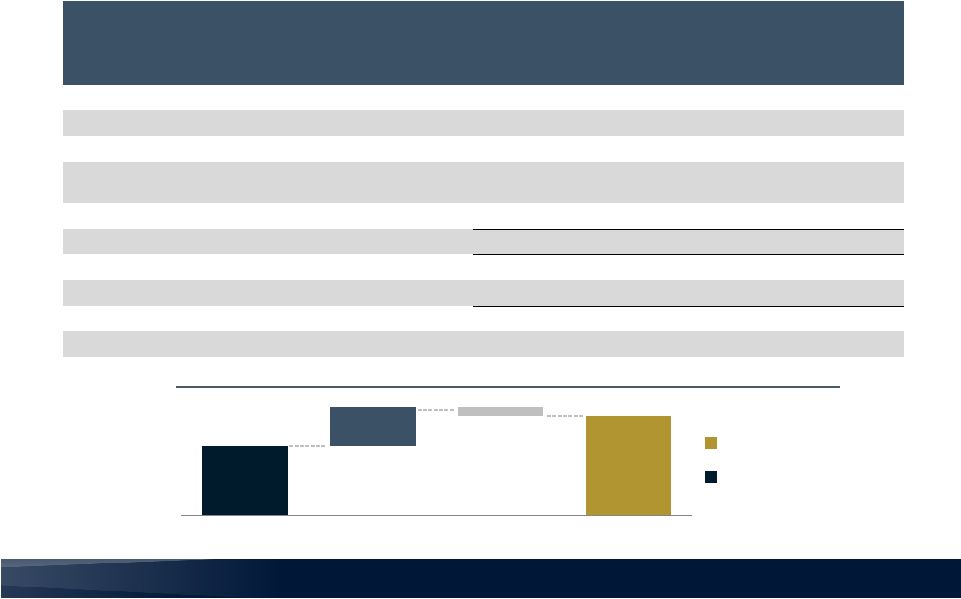

Operations Expenses ($ in

millions) Noninterest Expense - Continuing Operations Q2 non- recurring adjustments Q2 Operating Expense 2 Salaries and employee benefits $ 29.4 $ 29.4 Occupancy and equipment 7.9 7.9 Professional fees 6.3 $ (1.5) 4.8 Data processing 1.7 1.7 Advertising 2.9 2.9 Regulatory assessments 2.2 2.2 Provision (reversal) for loan repurchases (0.2) (0.2) Amortization of intangible assets 0.8 0.8 Restructuring expense 4.0 (4.0) 0.0 All other expense 5.8 (0.9) 4.9 Total Noninterest Expense (ex-loss on investments in alternative energy partnerships) $ 60.7 $ (6.4) $ 54.3 Loss on investments in alternative energy partnerships¹ $ 1.8 Total Noninterest Expense (reported) $ 62.5 Normalize Expenses: Leveraging Expenses

Efficiently Simplifying Operating Model and Delivering

Operational Efficiencies BA

NC 2.12% 2.45% 2.33% 2.37% 4Q17 1Q18 2Q18 2Q18 Operating Long-Term Target <2.00% NIE / Average Assets 3 |

9 9 ($ in millions) Continuing Operations (reported) Q2 adjustments 1 Q2 Operating Earnings from Continuing Operations 2 Normalized Tax Rate at 20% 2 Net interest income $ 72.8 $ 72.8 Provision for loan and lease losses 2.7 2.7 Total noninterest income 8.1 (2.4) 4 5.7 Total noninterest expense (ex-loss on investments in alternative energy partnerships) $ 60.7 $ (6.4) $ 54.3 Loss on investments in alternative energy partnerships³ 1.8 (1.8) --- Total noninterest expense 62.5 (8.2) 54.3 Pre-tax income $ 15.6 $ 5.8 $ 21.5 Income tax expense³

1.8 2.5 4.3 Net income $ 13.9 $ 3.3 $ 17.2 Diluted earnings per total common share $ 0.16 $0.23 1 Includes non-recurring items, loss on investments in alternative energy partnerships, and income tax expense required to reach

a normalized rate of 20%.

2 Non-GAAP measure: Reconciliation table above. 3 Loss on investments in alternative energy partnerships create tax credits to offset expense incurred. 4

Includes $0.3 million benefit from security sales and a $2.1 million legal settlement. Focusing on Core, Sustainable Returns Q2 Including Non-Recurring Items Shown Below $0.16 $0.23 $0.09 2Q18 Reported Adjustments Tax rate normalized at 20% 2Q18 Adjusted Diluted EPS – Continuing Operations Reported Adjusted for non-recurring items ($0.02) |

10 10 Financial Metric Long-Term Strategic Operating Targets 1st Half 2018 Plan Tracking Comments Growth / Balance Sheet: - Loan Growth (HFI)¹ Mid-Teens +11% Loan sales temporarily slowed growth - Deposit Growth (ex-brokered) 2 Low-to-Mid Teens +15% Early Innings of Deposit & Treasury Management Build Out - Securities / Total Assets 15% - 20% 22% Trending Toward Target Operating Metrics: - NIM 3.00% – 3.20% 3.00% Improved earning asset pricing Core deposits better priced than wholesale funding - NIE 3 / Average Assets <2.00% 2.21% Trending Toward Target - Tax Rate 20 – 25% --- Expect FY 2018 Tax Rate Normalization in the 2nd Half Returns: - ROAA 1%+ 0.46% - ROATCE 4 12%+ 4.18% 1 Annualized 2 Annualized ex-brokered, ex-IB run off deposits 3 Continuing operations noninterest expenses excluding loss on investments in alternative energy partnerships, annualized, over average consolidated assets. See page 8 for Non-GAAP reconciliation. 4 Non –GAAP measure, see page 19 for reconciliation.

Creating Stockholder Value: Strategic Target Tracking Focused on Building Core Earnings Power for Sustainable Growth and Returns Over the Long Term

BAN C |

11 11 1.2% 1.6% 2.1% 2.2% 2.3% 2Q17 3Q17 4Q17 1Q18 2Q18 $12.3 $16.0 $21.2 $22.2 $23.0 0.12% 0.16% 0.21% 0.22% 0.22% 2Q17 3Q17 4Q17 1Q18 2Q18 NPAs NPAs/Assets Nonperforming Assets 1 Asset Quality Remains Strong and Stable Disciplined Credit Culture Continues to Drive Strong Asset Quality 1 Dollars in millions, held for investment NPAs / Equity ALLL and NPL Coverage 0.71% 0.72% 0.74% 0.79% 0.81% 468% 367% 255% 258% 254% 2Q17 3Q17 4Q17 1Q18 2Q18 ALLL/Total Loans ALLL/NPLs Total Delinquent Loans / Total Loans 0.38% 0.52% 0.50% 0.63% 0.63% 2Q17 3Q17 4Q17 1Q18 2Q18 |

12 12 Tangible Equity / Tangible Assets 1 9.3% 9.5% 9.4% 9.2% 9.2% 2Q17 3Q17 4Q17 1Q18 2Q18 -1% Solid Capital Ratios Exceeding Basel III Guidelines Tier 1 Risk-Based Capital Ratio Supported by $269 Million of Preferred Equity

Common Equity Tier 1 Ratio (CET1)

9.8% 9.9% 9.9% 9.8% 9.9% 2Q17 3Q17 4Q17 1Q18 2Q18 +1% Tangible Common Equity / Tangible Assets 1 6.7% 6.8% 6.8% 6.6% 6.6% 2Q17 3Q17 4Q17 1Q18 2Q18 -2% Tier 1 Risk-Based Capital Ratio 13.7% 13.8% 13.8% 13.7% 13.8% 2Q17 3Q17 4Q17 1Q18 2Q18 +1% 1 Non-GAAP measure. Reconciliation on slide 19. |

13 13 Appendix |

14 14 Securities Portfolio Yield Benefiting from CLO Quarterly Rate Reset 1 Dollars in millions 2 Based on book value balances of rated securities, data at June 30, 2018 3 Dollars in billions Securities Portfolio Detail 1 Security Type Book Value 1Q18 Book Value 2Q18 Q2 Change Fair Value 2Q18 Book Yield 2Q18 Duration 2Q18 Gov’t & Agency (Agency MBS) $ 495 $ 486 ($ 9) $ 458 2.55% 7.18 CLOs 1,744 1,677 (67) 1,680 4.17% 0.12 CMBS 201 161 (40) 158 3.79% 6.13 Other 1 1 --- 1 n/m n/m Total Securities 2,441 2,325 (116) 2,297 3.81% 2.01 Portfolio Profile 2 AAA / AA 99% A 1% Credit Rating $3.0 $2.8 $2.7 $2.5 $2.3 3.34% 3.46% 3.46% 3.47% 3.78% 2Q17 3Q17 4Q17 1Q18 2Q18 Average Balance Yield Portfolio Average Balances and Yields 3 Agency 21% CLOs 72% CMBS 7% Composition |

15 15 1 All figures from Continuing Operations unless noted; dollars in millions unless noted per share or percentage.

2

Consolidated operations; Efficiency ratio adjusted for including the

pre-tax effect of investments in alternative energy partnerships . 3 Excluding loss on investments in alternative energy partnerships . 4 Non-GAAP measure.

Reconciliation within table above. 5 Non-GAAP measure. Reconciliation on slide 17. ($ in millions) 1 2Q18 1Q18 4Q17 3Q17 2Q17 Total Assets 2 $ 10,319 $ 10,329 $ 10,328 $ 10,280 $ 10,366 Securities 2,297 2,425 2,575 2,756 2,915 Loans Held for Investment 7,036 6,931 6,659 6,227 5,956 Deposits 7,136 7,110 7,293 7,404 8,045 Net Interest Income 72.8 71.4 73.2 75.0 75.5 Provision for Loan and Lease Losses 2.7 19.5 5.1 3.6 2.5 Non Interest Income 8.1 8.6 5.7 18.4 5.7 Noninterest Expense 3,4 60.7 59.8 62.4 67.3 66.6 Loss on Investments in Alternative Energy Partnerships 1.8 n/m 4.0 8.3 9.8 Noninterest Expense – Reported 62.5 59.8 66.4 75.7 76.3 Net Income 13.9 7.1 10.9 18.1 15.1 Diluted Earnings Per Share $ 0.16 $ 0.03 $ 0.11 $ 0.25 $ 0.20 Return on Average Assets 2 0.58% 0.34% 0.44% 0.67% 0.46% Efficiency Ratio 2,5 73.5% 65.7% 75.5% 72.5% 80.5% Preferred Equity Class / Series CUSIP Issue Date Amount Out ($000) Dividend Rate / Coupon (%) First Callable Date Preferred Equity: Non-Cumulative, Perpetual E 05990K874 2/8/2016 125,000 7.00% 3/15/2021 Preferred Equity: Non-Cumulative, Perpetual D 05990K882 4/8/2015 115,000 7.375% 6/15/2020 Preferred Equity: Non-Cumulative, Perpetual C 05990K403 6/12/2013 40,250 8.00% 9/15/2018 Total Preferred Equity $ 280,250 BANC Fast Facts & Preferred Equity Capital Structure |

| 16 16 This presentation contains certain financial measures determined by methods other than in accordance with U.S. generally

accepted accounting principles (GAAP). These measures include noninterest

expense from continuing operations, operating expense from

continuing operations, and diluted earnings per share from continuing operations, adjusted for non-recurring items, each excluding loss on investments in alternative energy partnerships and the latter two also reflecting adjustments for

non- recurring items. Management believes that these

particular measures provide useful supplemental information in understanding our core operating performance. These measures should not be viewed as substitutes for measures determined in accordance

with GAAP, nor are they necessarily comparable to non-GAAP

measures that may be presented by other companies. Reconciliations of these measures to measures determined in accordance with GAAP are contained on slides 8, 9 and 17 of this presentation.

Non-GAAP measures in this presentation also include tangible

equity to tangible assets, tangible common equity to tangible assets, return on average tangible common equity, and adjusted efficiency ratio including the pre-tax effect of investments in alternative

energy partnerships. These particular measures are used by

management in its analysis of the Company's capital strength and the

performance of the Company’s businesses. Banking and financial institution

regulators also exclude goodwill and other intangible assets from

total stockholders' equity when assessing the capital adequacy of a financial institution. Management believes the presentation of these measures excluding the impact of these items provides useful supplemental information that is

essential to

a proper understanding of the capital and financial strength of the Company and the performance of its businesses. These measures

should not be viewed as substitutes for results determined in

accordance with GAAP, nor are they necessarily comparable to non- GAAP measures that may be presented by other companies. Reconciliations of these measures to measures determined in

accordance with GAAP are contained on slides 17-19 of this

presentation. Non-GAAP Financial Information

|

17 17 (in thousands) 2Q18 1Q18 4Q17 3Q17 2Q17 Noninterest expense $ 62,554 $ 59,812 $ 66,424 $ 79,008 $ 98,216 Gain (loss) on investments in alternative energy partnerships, net (1,808) 34 (3,995) (8,348) (9,761) Adjusted noninterest expense $ 60,746 $ 59,846 $ 62,429 $ 70,660 $ 88,455 Net interest income $ 72,953 $ 71,624 $ 73,246 $ 75,953 $ 78,296 Noninterest income 9,168 10,452 6,429 18,827 19,817 Total revenue 82,121 82,076 79,675 94,780 98,113 Tax credit from investments in alternative energy partnerships 1,912 7,323 4,908 8,777 15,681 Deferred tax expense on investments in alternative energy partnerships (211) (769) (859) (1,536) (2,744) Tax effect on tax credit and deferred tax expense 631 2,422 3,004 3,804 8,584 Gain (loss) on investments in alternative energy partnerships, net (1,808) 34 (3,995) (8,348) (9,761) Total pre-tax adjustments for investments in alternative energy partnerships 524 9,010 3,058 2,697 11,760 Adjusted total revenue $ 82,645 $ 91,086 $ 82,733 $ 97,477 $ 109,873 Efficiency ratio 76.17% 72.87% 83.37% 83.36% 100.10% Adjusted efficiency ratio including the pre-tax effect of investments in alternative energy partnerships 73.50% 65.70% 75.46% 72.49% 80.51% Effective tax rate utilized for calculating tax effect on tax credit and deferred tax expense 27.07% 26.98% 42.59% 34.44% 39.89% Non-GAAP Reconciliation Adjusted Efficiency Ratio Including the Pre-tax Effect of Investments in Alternative Energy Partnerships

|

18 18 (in thousands) 2Q18 1Q18 4Q17 3Q17 2Q17 Tangible common equity to tangible assets ratio Total assets $ 10,319,280 $ 10,329,319 $ 10,327,852 $ 10,280,028 $ 10,365,768 Less goodwill (37,144) (37,144) (37,144) (37,144) (37,144) Less other intangible assets (7,683) (8,510) (9,353) (10,219) (11,135) Tangible assets $ 10,274,453 $ 10,283,665 $ 10,281,355 $ 10,232,665 $ 10,317,489 Total stockholders’ equity $ 988,688 $ 993,756 $ 1,012,308 $ 1,013,908 $ 1,006,292 Less goodwill (37,144) (37,144) (37,144) (37,144) (37,144) Less other intangible assets (7,683) (8,510) (9,353) (10,219) (11,135) Tangible equity 943,861 948,102 965,811 966,545 958,013 Less preferred stock (269,071) (269,071) (269,071) (269,071) (269,071) Tangible common equity $ 674,790 $ 679,031 $ 696,740 $ 697,474 $ 688,942 Tangible equity to tangible assets 9.19% 9.22% 9.39% 9.45% 9.29% Tangible common equity to tangible assets 6.57% 6.60% 6.78% 6.82% 6.68% Non-GAAP Reconciliation Tangible Common Equity to Tangible Assets and Tangible Equity to Tangible Assets |

19 19 (in thousands) 1st Half 18 2Q18 1Q18 4Q17 3Q17 2Q17 Return on Tangible Common Equity Average total stockholders’ equity $ 1,010,355 $ 1,000,856 $ 1,019,961 $ 1,014,368 $ 1,005,462 $ 1,014,267 Less average preferred stock (269,071) (269,071) (269,071) (269,071) (269,071) (269,071) Less average goodwill (37,144) (37,144) (37,144) (37,144) (37,144) (37,144) Less average other intangible assets (8,539) (8,110) (8,972) (9,788) (10,760) (11,808) Average tangible common equity $ 695,601 $ 686,531 $ 704,774 $ 698,365 $ 688,487 $ 696,244 Net income $ 23,338 $ 14,780 $ 8,558 $ 11,302 $ 16,949 $ 12,257 Less preferred stock dividends (10,226) (5,113) (5,113) (5,113) (5,112) (5,113) Add amortization of intangible assets 1,670 827 843 866 916 1,056 f intangible assets --- --- --- --- --- --- assets (351) (174) (177) (303) (321) (370) $ 14,431 $ 10,320 $ 4,111 $ 6,752 $ 12,432 $ 7,830 Return on average equity 4.66% 5.92% 3.40% 4.42% 6.69% 4.85% Return on average tangible common equity 4.18% 6.03% 2.37% 3.84% 7.16% 4.51% Effective tax rate utilized for calculating tax effect on amortization and impairment of intangible assets 21.00% 21.00% 21.00% 35.00% 35.00% 35.00% Non-GAAP Reconciliation Return on Average Tangible Common Equity |