Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒

|

|

Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

|

|

|

For the fiscal year ended March 31, 2018.

|

|

☐

|

|

Transition report pursuant to Section 13 or 15(d) of the Exchange Act of 1934

For the transition period from _____ to _____

|

Commission file number: 001-32830

INDIA GLOBALIZATION CAPITAL, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

(State or other jurisdiction of

incorporation or organization)

|

|

20-2760393

(I.R.S. Employer

Identification No.)

|

|

4336 Montgomery Avenue, Bethesda, Maryland

(Address of Principal Executive Offices)

|

20814

(Zip Code)

|

(301) 983-0998

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Common Stock

|

|

NYSE American LLC

|

|

(Title of each class)

|

|

(Name of each exchange on which registered)

|

Securities registered pursuant to Section 12(g) of the Act:

Common Stock Purchase Warrants

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☑ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☑ Yes ☐ No

Indicate by check mark disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

|

Accelerated filer ☐

|

|

Non-accelerated filer ☐

|

(Do not check if a smaller reporting company)

|

Smaller reporting company ☑

|

|

Emerging growth company☐

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☑ No

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of September 29, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter was $8,376,895 based on the last reported sale price of the registrant’s common stock (its only outstanding equity security) of $0.36 per share on that date. All executive officers and directors of the registrant and all 10% or greater stockholders have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant.

31,028,473 shares of our common stock were issued and outstanding as of June 15, 2018.

DOCUMENTS INCORPORATED BY REFERENCE

None

INDIA GLOBALIZATION CAPITAL, INC.

FORM 10-K

FOR THE FISCAL YEAR ENDED MARCH 31, 2018

|

|

|

Page

|

|

PART I

|

|

|

|

|

|

|

|

Item 1.

|

5

|

|

|

Item 1A.

|

13

|

|

|

Item 1B.

|

19

|

|

|

Item 2.

|

20

|

|

|

Item 3.

|

20

|

|

|

Item 4

|

20

|

|

|

|

|

|

|

PART II

|

|

|

|

|

|

|

|

Item 5.

|

21

|

|

|

Item 6.

|

21

|

|

|

Item 7.

|

22

|

|

|

Item 8.

|

27

|

|

|

Item 9.

|

54

|

|

|

Item 9A.

|

54

|

|

|

Item 9B.

|

55

|

|

|

|

|

|

|

PART III

|

|

|

|

|

|

|

|

Item 10.

|

56

|

|

|

Item 11.

|

59

|

|

|

Item 12.

|

63

|

|

|

Item 13.

|

64

|

|

|

Item 14.

|

65

|

|

|

PART IV

|

|

|

|

|

|

|

|

Item 15.

|

67

|

|

|

Item 16.

|

68

|

|

|

69

|

FORWARD-LOOKING STATEMENTS AND IMPORTANT FACTORS

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. This report and the documents incorporated in this report by reference contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Additionally, we or our representatives may, from time to time, make other written or verbal forward-looking statements. In this report and the documents incorporated by reference, we discuss plans, expectations and objectives regarding our business, financial condition and results of operations. Without limiting the foregoing, statements that are in the future tense, and all statements accompanied by terms such as “believe,” “project,” “expect,” “trend,” “estimate,” “forecast,” “assume,” “intend,” “plan,” “target,” “anticipate,” “outlook,” “preliminary,” “will likely result,” “will continue” and variations of them and similar terms are intended to be “forward-looking statements” as defined by federal securities laws. This document contains statements and claims that are not approved by the FDA. These statements and claims are in compliance with state laws, specifically in states where medical cannabis is approved, and Alzheimer's and other diseases are approved conditions for treatment with cannabis. We caution you not to place undue reliance on forward-looking statements, which are based upon assumptions, expectations, plans and projections. Forward-looking statements are subject to risks and uncertainties, including those identified in the “Risk Factors” included in this report and in the documents incorporated by reference that may cause actual results to differ materially from those expressed or implied in the forward-looking statements. Forward-looking statements speak only as of the date when they are made. Except as required by federal securities law, we do not undertake any obligation to update forward-looking statements to reflect events, circumstances, changes in expectations or the occurrence of unanticipated events after the date of those statements. We intend that all forward-looking statements made will be subject to safe harbor protection of the federal securities laws pursuant to Section 27A of the Securities Act and Section 21E of the Exchange Act.

Forward-looking statements are based upon, among other things, our assumptions with respect to:

| · |

our ability to successfully register patents, create and market new products and services, including but not limited to trading in Hong Kong and other part of south Asia, leasing equipment in India, and achieve customer acceptance in the industries we serve;

|

| · |

our ability to accurately predict the future demand for our products and services;

|

| · |

competition in using phytocannabinoids for alternative, pharmaceutical, and nutraceutical therapies;

|

| · |

federal and state legislation and administrative policy regulating phytocannabinoids;

|

| · |

our ability (based in part on regulatory concerns) to license our products to processors that can produce pharmaceutical grade phytocannabinoids;

|

| · |

our ability to obtain and protect patents for the use of phytocannabinoids in our formulations;

|

| · |

current and future economic and political conditions, in specifically but not limited to North America, Malaysia, and India; and

|

| · |

other assumptions described in this prospectus supplement underlying or relating to any forward-looking statements.

|

You should consider the limitations on, and risks associated with, forward-looking statements and not unduly rely on the accuracy of predictions contained in such forward-looking statements. As noted above, these forward-looking statements speak only as of the date when they are made. Moreover, in the future, we may make forward-looking statements through our senior management that involve the risk factors and other matters described in this report, as well as other risk factors subsequently identified, including, among others, those identified in our filings with the SEC in our quarterly reports on Form 10-Q and our current reports on Form 8-K.

PART I

Unless the context requires otherwise, all references in this report to “IGC,” “the Company,” “we,” “our” and “us” refer to India Globalization Capital, Inc., together with the subsidiaries listed on the Company’s Annual Report on Form 10-K. We exclude our investments and minority non-controlling interests, and any information provided by them is not incorporated by reference in this report, and you should not consider it a part of this report.

Company Background

We are a Maryland corporation formed in April 2005. Our principal office in the U.S. is in Bethesda, Maryland, in addition we have a facility in Washington State. Our back office is in Kochi, Kerala India. In addition, many of our staff and advisors work from their home offices. We maintain our main website at www.igcinc.us and our telephone number is +1-301-983-0998. The information contained on any of our websites is not incorporated by reference in this report, and you should not consider it a part of this report unless we specifically refer to it. Our operational subsidiaries are in Hong Kong, India and Malaysia. Our filings are available on www.sec.gov.

For more on corporate history, please check our websites at (i) www.igcinc.us and (ii) www.igcpharma.com.

Our Business

The Company’s main focus is to develop and commercialize cannabinoid based alternative therapies for indications such as Alzheimer’s disease, Parkinson’s disease, and pain. Its lead product is Hyalolex, an alternative oral therapy for the treatment of symptoms associated with Alzheimer’s disease. The Company has filed several patents for its pipeline of products including ones for the treatment of Parkinson’s Central Nervous System related disorders, eating disorders, and seizures in cats and dogs. The commercialization of Hyalolex through medical dispensaries is expected to commence in the second half of calendar 2018. Since its inception, the Company operates a legacy business that involves trading commodities and heavy equipment rental.

In addition, the Company plans to leverage its technology and cannabis expertise to build meaningful solutions to address issues facing the cannabis industry using distributed ledgers inherent in blockchain technology. These would include addressing issues such as product identification assurance (PIA) and product origin assurance, transactional difficulties, and inadequate product labeling. Please see Note 1 in the Financial statements for further information.

Business Segments and Revenue Contribution

The Company has two business segments: legacy infrastructure, and medical cannabis based alternative therapies. The legacy business has two drivers a) trading of infrastructure commodities like steel, and iron ore, among others and b) rental of heavy equipment. The legacy infrastructure business contributed 100% of the revenue in fiscal year 2017 and fiscal year 2018. In fiscal year 2017, our lead product Hyalolex was in its research and development phase and in fiscal 2018 we began production in anticipation of commercialization in the second half of 2018.

|

Segments

|

Fiscal Year Ended

March 31, 2018

|

|||

|

Legacy infrastructure

|

$

|

2,192,590

|

||

|

Alternative therapies

|

-

|

|||

|

Total IGC

|

$

|

2,192,590

|

||

Segment 1: Legacy Infrastructure

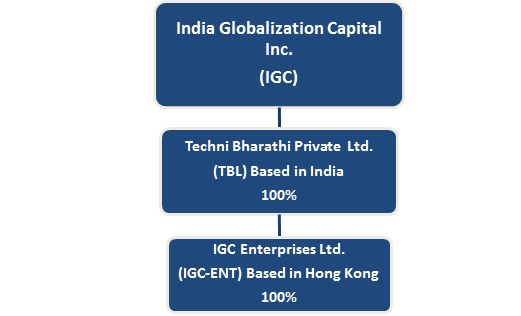

Since our inception, we have participated in various aspects of the infrastructure industry. During the fiscal year 2018, we streamlined our legacy infrastructure business to infrastructure commodity trading, and heavy equipment rental. We trade infrastructure commodities like steel and iron ore, among others, and we rent heavy equipment. Our subsidiary, Techni Bharathi Private Ltd (“TBL”) in India is responsible for heavy equipment rental, and its subsidiary IGC Enterprises Ltd. in Hong Kong is responsible for infrastructure trading.

For the rental business, we supply equipment and operators to construction companies. This business is very small and limited to the city of Kochi in Kerala, India. In fiscal year 2018 we have three customers all of which are construction companies. For the trading business we have four customers and no principal supplier. We are opportunistic and will buy from any of the South Asian countries. In fiscal 2018 our suppliers are companies based in India and Hong Kong. For the level of business and the value of each trade, the number of customers we have is adequate and does not constitute inordinate customer risk. Revenue from our legacy infrastructure business including heavy equipment rental and commodity trading is less than 1% based on revenue of both the rental and trading markets. This business is highly competitive, and our differentiation is based primarily on price and industry knowledge of commodity requirements for infrastructure projects. Our strategy in fiscal 2019 for the legacy business is to maintain annual revenue of $3-$5 million and focus on growing margin by reducing the cost of money and by modest investments in heavy equipment.

The pricing for steel and iron ore are heavily influenced by tariffs and demand for infrastructure development. In fiscal year 2018, steel prices although down from fiscal 2017, fluctuated in a relatively narrow band as did iron ore prices. We do not hedge or take long term positions on commodities. We limit our exposure by contractually ensuring that every purchase has a vetted legitimate buyer and ensuring rapid closing of transactions. On a transaction basis, this business does not require special government approvals. We have the requisite business licenses that allow us to operate in this segment.

In the fiscal years ending March 31, 2018 and 2017, we funded our subsidiary TBL $75,000 and $43,000 for working capital, respectively. For the trading business our sales team is in Hong Kong and the sales cycle lasts between two and three months. For our equipment leasing business our sales team is in Kochi, India, where the sales cycle lasts around two months. In Malaysia, through our subsidiary Cabaran Ultima, we operated a real estate management business. During the fiscal year 2018, we decided to exit this business and as of March 31, 2018, we have accounted for our investment in Cabaran Ultima as “Investment Held for Sale” at a fair value of $147,500. We hope to sell Cabaran Ultima during fiscal year 2019. Please see Note-22, “Investment Held for Sale” for more information.

Segment 2: Alternative therapies (Complementary and Alternative Medicine, “CAM”)

We focus on the development and commercialization of cannabinoid-based combination therapies. Cannabinoids are chemical compounds that exert a range of effects on the body, including impacting the immune response, gastrointestinal maintenance and motility, muscle functioning, and nervous system response and functioning. Phytocannabinoids are cannabinoids that occur naturally in the cannabis plant. Phytocannabinoids are abundant in the viscous resin produced by glandular structures called trichomes. There are over 480 different compounds in the cannabis plant. Many of them have been identified as cannabinoids. Of these, THC (delta-9-tetrahydrocannabinol) is the main psychoactive component in the plant with many therapeutic uses. The other broadly pursued non-psychoactive phytocannabinoid, CBD (Cannabidiol), is pleiotropic influencing many pathways in humans, dogs, and cats, and may be used to provide relief to a variety of symptoms including pain, seizures, and eating disorders. In medical applications, cannabinoids are extracted from the cannabis plant using a variety of well-established technologies, including using CO2, butane, alcohol, among others, as solvents. The refined extracted material is isolated for specific active ingredients like THC and CBD, among others, and used in formulations as the primary or secondary active ingredient.

Our work and strategy are to use cannabinoids synergistically with other active ingredients that in many cases have been established to treat specific conditions. We seek, through the synergies for our combination therapies, to decrease side effects, increase bio-availability, and enhanced efficacy. This strategy in some cases leads to “new and improved” products, and in others it results in totally novel products with surprising results, as in the case of Hyalolextm.

We have filed eight provisional patents with the United States Patent and Trademark Office (“USPTO”), in the phytocannabinoid-based combination therapy space, for the indications of pain, medical refractory epilepsy, and cachexia. In addition, in May 2017, we acquired an exclusive license to a patent filed by the University of South Florida Research Foundation entitled “Cannabidiol and Synthetic Dronabinol for treatment of Alzheimer’s Disease.”

Hyalolextm

Hyalolextm is not approved by the Federal Drug Administration (FDA), and therefore is not considered an approved pharmaceutical drug. It is a Complimentary Alternative Medicine (“CAM”).

The name of IGC’s lead product Hyalolextm, is based on the Greek roots hyalo and lex that broadly mean clear, clarity, glass-like, and words, reading, respectively. In Alzheimer’s cell lines, Alzheimer’s animal models, and in some human studies the active ingredients in Hyalolextm have been shown to alleviate many of the symptoms associated with Alzheimer’s. Patients with Alzheimer’s suffer from a variety of symptoms including dementia, anxiety, agitation, and sleep disorder, among others. These symptoms often result in hard-to-manage patients and caregiver distress. As set out below, about 30% of the overall cost of managing Alzheimer’s patients is attributed to caregiver cost. We believe that our product can reduce caregiver distress by helping to better manage patients.

Market Overview of Alzheimer’s Disease

Alzheimer’s is known as America’s most expensive disease. The estimated cost in 2017 to Medicare and Medicaid was about $175 billion. There are currently over 5.3 million Americans with Alzheimer’s disease (“AD”) and around 35 million worldwide. The cost of Alzheimer’s is skyrocketing as the baby-boomers age: the number of AD patients is expected to double over the next 20 years and the direct costs are expected to exceed $450 billion in the next 12 years. Although the speed of progression can vary, the average life expectancy following diagnosis is believed to be between three and nine years. It is the most common cause of dementia among older adults. Currently, no treatment can stop or reverse the progression of the disease and there is still no accepted cure for AD.

Data for Hyalolextm

Our research into cannabinoid-based combination therapies led us to work done at the University of South Florida using cannabinoids on Alzheimer’s disease. The professor working on this unique approach was featured on CNN on Dr. Sanjay Gupta’s show Weed 2. The work, specifically, reported several novel findings that were subsequently filed as a patent. In the fiscal year 2018, IGC acquired exclusive rights to the data and the patent filing. The research reported that micro-dosing of the cannabinoid THC, in combination with another naturally occurring compound, works synergistically to reduce the buildup of plaques and tangles, through allegedly new pathways. These results were shown using Alzheimer’s cell lines. Plaques and tangles are hallmarks of Alzheimer’s disease. It is known that patients get plaques and tangles between 15 to 20 years before any Alzheimer’s related symptoms manifest. The work further showed, on Alzheimer’s cell lines, that micro dosing of THC can increase the functioning of mitochondria. The findings are unique as all previous research showed the opposite effect at higher doses, for example, loss of mitochondrial functioning.

We claim that the novelty is two-fold: one, that micro dosing of THC affects the brain radically differently from normal dosing that is prescribed (FDA approved Dronabinol) or consumed by individuals; the second is that micro doses of THC can synergistically work with other naturally occurring compounds to increase efficacy and reduce side effects. For example, the research showed that at these therapeutic micro-doses, THC is non-toxic to neurons, a finding that is contrary to massive amounts of research and data showing that THC is neuro-toxic at normally ingested levels. The research was extended to include a Morris Water Maze test for measuring spatial memory impairment on Alzheimer’s mice. It was found that Alzheimer’s mice treated with THC were significantly better at negotiating the water maze than untreated mice. Of course, as expected, neither group were anywhere close to the performance of healthy mice. Preliminary findings have also reported that THC can play a role in triggering neurogenesis, the growth and development of nervous tissue.

After a great deal of in-depth research and experiments, our team created an oral formulation, a medicinal syrup, by adding excipients and synergistic ingredients. The formulation has evolved into market-ready Hyalolextm to help patients suffering from Alzheimer’s disease.

Marketing plan for Hyalolextm

Hyalolextm is formulated for a dose of 1 ml either two or three times a day. It is currently available in 30 ml bottles. We plan to derive revenue by licensing the technology, data, research, brand, and selling the excipients and non-cannabinoid compounds to resellers in various states. As the final product contains a controlled substance, although in micro-doses, it can only be manufactured by a state licensed entity that conforms to all relevant state regulations. The reseller will have the product manufactured and delivered to state licensed dispensaries where they can be sold consistent with state laws governing the sale of products containing cannabinoids. The product will only be available to patients in medical states that are registered through specific state sanctioned programs.

To ensure compliance and product assurance we are developing a QR code (Quick Response code) supported system that will track the product and allow patients to access information about the product and also provide feedback. To this, we plan to add a backend based on blockchain technology that will go much further in ensuring compliance, product authenticity and product origin.

Growth and Expansion Strategy

Our growth and expansion strategies are to commercialize and license Hyalolextm in states and countries where we can legally enter the market. Our immediate plans are to commercialize Hyalolextm in 10 states starting with Puerto Rico, Maryland, District of Columbia, and California.

Sales, Distribution and Marketing

We plan to license Hyalolextm to resellers in medical states and other countries. Under the licensing agreement, the U.S. based reseller will market and manufacture Hyalolextm and, either directly or indirectly, distribute the product to medical dispensaries where it can be sold. Individuals with medical cards approved by the state will have access to the product.

Manufacturing and Supply

Hyalolextm is manufactured in each medical state separately, by a licensed processor (manufacturer). The manufacturer then sells the products to dispensaries that in turn sell the product to the end user. The active ingredients are manufactured (grown and extracted) within the state, procured within the state, processed within the state, distributed within the state, and sold to individuals with medical cards within the state. The state programs are strictly controlled and licensed. For example, in each state entities must undergo background checks and obtain a license to grow, process, and/or operate a medical dispensary. Individuals that desire to purchase products from dispensaries must obtain a medical card and, in most states, register with the state as a patient. Further, medical states use software platforms to track plants, extracts, and products very closely to ensure compliance. In addition, all products are tested by an independent state licensed lab, on a batch basis, for cannabinoid profiles and a host of other measurements that are specific to individual states.

Other products: IGC-501, Serosapse, Caesafin, and Natrinol

Other products that we have in the pipeline are IGC-501 for indications of neuropathic pain; Serosapse for indications of Parkinson’s and other Central Nervous System (CNS) disorders; Caesafin for seizures in cats and dogs; and Natrinol for indications of cancer and AIDS induced nausea and vomiting. None of these are FDA approved and they are not considered to be pharmaceutical drugs. They fall in the category of complimentary alternative medicines or CAMS.

Overview and Target Market for Other Products

The pain management market represents a significant component of the healthcare system. In September 2012, The Journal of Pain reported that the annual estimated national cost of pain ranges from $560 billion to $635 billion. This figure exceeds the entire cost of the nation’s priority health conditions. Additionally, The American Pain Society recommends that pain be made more visible and be categorized as the fifth vital sign, recognizing that terminal illnesses are often accompanied by unbearable levels that are so severe and difficult to treat that death seems preferable. According to the Arthritis Foundation, arthritis has been particularly problematic for women; since 1999 there has been a 22% increase in the number of women who attribute their disability to arthritis. Current treatment protocols such as the utilization of opioid-based drug therapies present several challenges and may result in debilitating consequences that affect patients’ day-to-day functioning and patients’ productivity. Commonly reported side effects include hallucinations, constipation, sedation, nausea, respiratory depression, and dysphoria. Our patent filing is based on a novel therapy that uses extracts from the cannabis plant for the treatment of psoriatic arthritis and scleroderma pain. The therapy uses a cream that is applied to the joints using a variety of delivery mechanisms including a bio-adhesive patch.

There are over one million adults suffering from Parkinson’s disease (PD) in the U.S. PD is the second most common neurodegenerative disorder worldwide with an estimated 1% of adults over 60 suffering from the disease. The market for curing the disease is very large. We are testing products for end points associated with Parkinson’s disease like REM sleep disorder, anxiety, and dyskinesia. The PD treatment market is expected to reach $5.69 billion by 2022 from $4.24 billion in 2017, at a CAGR of 6.1%. The market is being driven by the growth in aging population and the associated increase in the prevalence of Parkinson’s disease and government funding for research. (Ref: https://www.marketsandmarkets.com/PressReleases/parkinson-disease-treatment.asp).

Approximately 50 million people worldwide are affected by epilepsy (Sanders, 2003). Epilepsy is thought to be due to multiple factors that include the alteration of many ion channels like sodium, potassium, and NMDA (N-Methyl-d-aspartate) and neurotransmitters like GABA (gamma amino butyric acid). It is believed, for example, that to maximally control epilepsy, modulation of one or more of these channels and receptors is required and that monotherapy is adequate in up to 25% of patients. The onset of epileptic seizures can be life threatening, including long-term implications (Lutz, 2004) such as mental health problems, cognitive deficits and morphological changes (Swann, 2004, Avoli et. al., 2005). The onset of epilepsy also greatly affects lifestyle as sufferers live in fear of consequential injury or the inability to perform daily tasks (Fisher et. al., 2000). The scientific community (1980 Cunha et. al., 1986 Ames, 1990 Trembly et. al. recent testing by GW Pharmaceuticals, among others) have shown that Cannabidiol (CBD) has anti-convulsive properties in humans. Other studies (Davis and Ramsey) have shown that tetrahydrocannabinol (THC) can also help reduce seizures. Three of our patent filings involving novel therapies use phytocannabinoid extracts from cannabis, in combination with other generic drugs, to treat medical refractory epilepsy in humans and seizures in dogs and cats.

Cachexia is a condition that accompanies severe illness such as cancer and results in the weakness and wasting away of the body. Cachexia physically weakens patients to the extent that response to standard treatments is poor. In the U.S., it is estimated that a population of approximately 1.3 million are experiencing cachexia associated with cancer, multiple sclerosis, Parkinson’s disease, HIV/AIDS, and other progressive illnesses. Cachexia is secondary to an underlying disease such as cancer or AIDS and is a positive risk factor for death. As an example, cancer induced anorexia cachexia is responsible for about 20% of all cancer deaths. Our patent filing involves a novel therapy that uses phytocannabinoids to stimulate senses (smell and taste) with a combination of drugs to stimulate appetite. Our approach addresses the veterinarian market as dogs and cats also suffer from pain, epilepsy, and cachexia and getting a product to market for the veterinarian industry is significantly less time consuming than getting products approved for human healthcare. There are 160 million domesticated dogs and cats in the U.S. and about 1% suffer from seizures. Our veterinarian product uses combination therapy for the treatment of seizures in dogs and cats.

QR code-based blockchain PIA

The Company has developed and deployed a QR code-based system that allows patients to access a website with specific information on our alternative medicine products. Each QR code is specific to a state and displays information specific to that state. We are in the process of creating a mobile optimized version that will expand the product information available to patients to include location of dispensaries that carry our products, based on zip code, and in turn also allow us to gather information through surveys and obtain feedback from patients.

As the number of states in which the product is available increases, we expect to expand the backend to a blockchain that allows for inputs directly from growers, processors, and dispensaries. This information will collectively display product identification, and product origination, by providing the patient with information regarding the origin, chemicals, and processes used to manufacture the product. We expect to expand the QR code-based system in several phases over fiscal 2019.

Research and Development

In the fiscal years 2017 and 2018, IGC identified combinations of Tetrahydrocannabinol (THC) and the non-psychoactive, medically useful compound Cannabidiol (CBD) to address symptoms of Parkinson’s disease and other diseases. The costs associated with this work is mostly in-house research. For example, looking for combinations of plant extracts that could work and data to support the claims that certain combinations and formulations can alleviate symptoms associated with diseases. The estimated amount spent for research and development was approximately $114,000 and $137,000 in the fiscal years 2017 and 2018, respectively. All research and development costs are expensed in the quarter in which they are incurred.

Competition

The development of phytocannabinoid-based therapies is currently not very competitive. The largest amount of research in this area is done in Israel. The most significant research and FDA approved trials are done by one large pharmaceutical company, and to a lesser extent, by two other large firms. In the United States, there is very little wide spread research while most of the research is concentrated in Israel. This is mostly because the United States Drug Enforcement Administrating (“DEA”) classifies phytocannabinoid extracts as a Schedule 1 drug. This means that phytocannabinoids are characterized as substances with “high potential for abuse” and with “no currently accepted medical use.” Further, any study conducted in the US must be registered and approved by the DEA and raw materials purchased through the National Institute of Drug Abuse (NIDA).

We view competition in two ways. First, we compete with about fifteen publicly listed companies and two private companies that have articulated a business plan to develop phytocannabinoid-based therapies, two large publicly-listed and well-funded pharmaceutical companies, and three small listed companies. There are several microcap companies trading on the OTC market and two private ones that also competing in this space. We have limited competition in the areas of Alzheimer’s, Parkinson’s, and seizures for dogs and cats using phytocannabinoid- based therapies. In the field of epilepsy in humans there is significant competition and so we are focused on seizures in dogs and cats where there is limited competition. Second, we have competition from non-phytocannabinoid-based therapies: there is severe competition in all areas that we are working on including for example Alzheimer’s, with almost all the massive and well- financed pharmaceutical companies and four pure play listed companies working on the disease, albeit all of them without the use of phytocannabinoids.

Competitive Advantage

We believe that there are three factors coalescing to create entrepreneurial opportunities in the cannaceutical industry. The first is deregulation of the industry. This is taking place in the U.S., Canada, Germany, and other parts of the world. We believe that during any major deregulation, it takes several years for market equilibrium to be achieved. Most large companies don’t react quickly and that creates entrepreneurial opportunities, including as a first mover. The second factor is that the plant has cannabinoids that work on several pathways, in humans and animals, and that these cannabinoids can potentially be used to treat many diseases and aliments. The third factor is a rising awareness and demand for natural products including natural complementary and alternative medicines.

Our competitive advantage with products such as Hyalolextm emerges from the following: a) first to market, b) proprietary data, c) patent filings, d) deep understanding of synergies, e) several years of research, f) a pipeline of other products, and f) a well differentiated strategy. Apart from these competitive advantages specific to Hyalolextm, our management has experience and deep knowledge of deregulating industries; access to foreign markets where testing has less regulatory hurdles; access to intellectual property experts; access to a network of doctors and PhDs; knowledge of FDA trials, extraction techniques, and plant strains.

Core Business Competencies

Our core competencies include the following:

|

•

|

A network of doctors, PhDs, and intellectual property legal experts that have a sophisticated understanding of drug discovery, research, FDA filings, intellectual protection and product formulation.

|

|

•

|

Knowledge of various cannabis strains, their phytocannabinoid profile, extraction methodology, and impact on various pathways.

|

|

•

|

Knowledge of cannabinoid-based combination therapies.

|

Patents, Development Pipeline, and Licenses

The success of most of our product candidates will depend in large part on our ability to:

|

•

|

obtain and maintain patent and other legal protections for the proprietary technology, inventions, and improvements we consider important to our business;

|

|

•

|

prosecute our patent applications and defend our issued patents;

|

|

•

|

preserve the confidentiality of our trade secrets; and

|

|

•

|

operate without infringing the patents and proprietary rights of third parties.

|

We intend to continue to seek appropriate patent protection for certain of our product candidates, drug delivery systems, molecular modifications, as well as other proprietary technologies and their uses by filing patent applications in the United States and selected other countries. We intend for these patent applications to cover, where possible, claims for medical uses, processes for preparation, processes for delivery and formulations.

Although, the Company believes the registration of patents is an important part of its business strategy and its success depends in part on such registration, the Company cannot guarantee that such patent filings will result in a successful registration with the USPTO. Please see Item 1A, Risk Factors.

The table below provides a status of the patent filings:

|

Formulation

|

Indication

|

Provisional Filing

|

PCT Filing

|

Subsequent Activity

|

|

IGC-501

|

Pain

|

9/16/14

|

9/16/15

|

US National Case Filed on 6/15/16

|

|

IGC-502

|

Seizures

|

1/25/15

|

1/14/16

|

US National Case Filed on 6/15/16

|

|

IGC-503

|

Seizures

|

4/1/15

|

3/25/16

|

PCT Application Published on 10/6/16

|

|

IGC-504

|

Eating Disorders

|

8/12/15

|

8/11/16

|

US and National Filing on 2/12/18

|

|

IGC-505

|

Seizures

|

6/15/16

|

6/15/16

|

US National Filing Anticipated on 12/15/18

|

|

IGC-506

|

Eating Disorders

|

2/28/17

|

2/27/18

|

US and National Filing Anticipated on 8/28/19

|

|

IGC-507

IGC-AD1

|

Alzheimer’s Disease

|

7/30/2015

|

Anticipated in 2018

|

US and National Filing Anticipated in 2018

|

|

IGC-508

|

CNS Disorders

|

3/29/2018

|

Anticipated in 2019

|

US and National Filing Anticipated in 2019

|

Technology and Intellectual Property

We have intellectual property attorneys that file patents or provisional patent applications, copyright, trademark and trade secret laws of general applicability, employee confidentiality, and invention assignment agreements, and other intellectual property protection methods to safeguard our technology, research and development. The Company holds all rights to the patents that have been filed by us with the USPTO.

Governmental Regulations and Approvals

Marijuana is a Schedule I controlled substance and possession, manufacturing, and growing are all illegal under federal law. Even in those states in which the use of marijuana has been legalized for medical and or recreational use, it remains a violation of federal law.

A Schedule I controlled substance is defined as a substance that has no currently accepted medical use in the United States, a lack of safety for use under medical supervision and a high potential for abuse. The Department of Justice defines Schedule 1 controlled substances as “the most dangerous drugs of all the drug schedules with potentially severe psychological or physical dependence.” If the federal government decides to enforce the Controlled Substances Act in Colorado with respect to marijuana, persons that are charged with distributing, possessing with intent to distribute, or growing marijuana could be subject to fines and terms of imprisonment, the maximum being life imprisonment and a $50 million fine.

In the United States, 29 states, Guam, Puerto Rico and District of Columbia have allowed (subject to licensing) the cultivation, processing and sale of cannabis. The state laws are in conflict with the federal Controlled Substances Act, which makes marijuana use and possession illegal on a national level.

The previous administration under President Obama had effectively stated that it was not an efficient use of resources to direct federal law enforcement agencies to prosecute those lawfully abiding by state-designated laws allowing the use and distribution of medical cannabis. In this regard, the prior DOJ Deputy Attorney General of the Obama administration issued a memorandum (the “Cole Memo”) to all United States Attorneys providing updated guidance to federal prosecutors concerning cannabis enforcement under the CSA.

The Cole Memo noted that the Department of Justice is committed to using its investigative and prosecutorial resources to address the most significant threats in the most effective, consistent, and rational way. In furtherance of those objectives, the Cole Memo provided guidance to Department of Justice attorneys and law enforcement to focus their enforcement resources on persons or organizations whose conduct interferes with any one or more of the following in preventing:

|

·

|

the distribution of cannabis to minors;

|

|

·

|

revenue from the sale of cannabis from going to criminal enterprises, gangs and cartels;

|

|

·

|

the diversion of cannabis from states where it is legal under state law in some for to other states;

|

|

·

|

state-authorized cannabis activity from being used as a cover or pretext for the trafficking of other illegal drugs or other illegal activity;

|

|

·

|

violence and the use of firearms in the cultivation and distribution of cannabis;

|

|

·

|

drugged driving and the exacerbation of other adverse public health consequences associated with cannabis use;

|

|

·

|

the growing of cannabis on public lands and the attendant public safety and environmental dangers posed by cannabis production on public lands; and

|

|

·

|

cannabis possession or use on federal property.

|

On January 4, 2018, the U.S. Attorney General Jeff Sessions issued the Sessions Memo stating that the Cole Memo was rescinded effectively immediately. In particular, Mr. Sessions stated that “prosecutors should follow the well-established principles that govern all federal prosecutions,” which require “federal prosecutors deciding which cases to prosecute to weigh all relevant considerations, including federal law enforcement priorities set by the Attorney General, the seriousness of the crime, the deterrent effect of criminal prosecution, and the cumulative impact of particular crimes on the community.” Mr. Sessions went on to state in the memorandum that “previous nationwide guidance specific to marijuana is unnecessary and is rescinded, effective immediately.”

It is unclear at this time whether the Sessions Memo indicates that the Trump administration will strongly enforce the federal laws applicable to cannabis or what types of activities will be targeted for enforcement.

However, on March 31, 2018 President Trump signed a $1.3 trillion budget bill that includes a provision that prevents the Justice Department, including the Drug Enforcement Administration, from using funds to arrest or prosecute patients, caregivers and businesses that are acting in compliance with state medical marijuana laws. This provision, known as the Rohrabacher-Blumenauer Amendment, prohibits the Justice Department from using federal funds to interfere with state medical marijuana programs.

Our business is impacted by state regulators some of whom must approve our products for sale in their dispensaries. For example, the Washington DC Department of Health must approve Hyalolextm before it can be manufactured and sold in Washington DC. Some states also require that marketing material be reviewed. We face scrutiny by the NYSE American regarding our products, including the modes of operation. FDA has been regulating CBD companies and this could possibly expand to other cannabis derivatives as well. Compliance with federal, state, and local laws and regulations is expensive requiring attorneys and experts, however such compliance is not expected to have, an adverse effect on our capital expenditures, competitive position, financial condition, or results of operations.

Employees and Consultants

As of March 31, 2018, we employed 16 employees and a total work force of approximately 26 including employees, seasonal contract workers, and advisors in the United States, India, and Malaysia. These numbers include both the legacy and the alternative therapy segments.

Reclassification

In fiscal year 2018, land valued at $5.2 million was previously recorded as investment under non-current asserts. This land has been reclassified as Property, Plant, and Equipment under non-current assets as we are pursuing options to monetize this asset. In the fiscal year 2018, a Note Payable in the amount of $1.8 Million was reclassified to current liabilities from non-current liabilities. Please see “Note 7 – Note Payable and Loans – Others” in Part II, Item 8 in our Consolidated Financial Statements contained herein for more information.

Operating Subsidiaries

The following chart presents our Company’s current direct and indirect consolidated operating subsidiaries.

Available Information

The Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are filed with the Securities and Exchange Commission (the “SEC”). The Company is subject to the informational requirements of the Exchange Act and files or furnishes reports, proxy statements and other information with the SEC. Such reports and other information filed by the Company with the SEC are available free of charge on the Company’s website at www.igcinc.us when such reports are available on the SEC’s website. The public may read and copy any materials filed by the Company with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov. The contents of these websites are not incorporated into this filing. Further, the Company’s references to the URLs for these websites are intended to be inactive textual references only.

You should carefully consider the following risk factors, together with all of the other information included in this report in evaluating our company and our common stock. If any of the following risks and uncertainties develops into actual events, they could have a material adverse effect on our business, financial condition or results of operations. In that case, the trading price of our common stock and other securities also could be adversely affected. We make various statements in this section, which constitute “forward-looking statements.” See “Forward-Looking Statements.”

Risks Related to Our Business and Expansion Strategy

Our cannaceutical strategy makes it difficult to find, retain, and attract management.

The environment we work in is heavily regulated and we have experience in regulated industries. However, this industry is not just heavily regulated, it is also heavily scrutinized. This takes a massive toll on management and makes it very difficult to attract and retain talent. Management spends a great deal of time and money explaining and justifying actions, strategy, and business plans to regulators. A myriad of complex factors including regulations regarding money laundering, inter-state commerce, DOJ, FDA, NYSE, SEC, state laws, among others, affect every decision. Navigating this complex set of landmines and staying focused on generating shareholder value is an arduous task and there can be no assurance that we will be successful in steering clear of all the potential issues, any of which could adversely impact the stock price or lead to delisting from the NYSE American.

Our cannaceutical strategy makes it difficult to raise money as a public company.

Despite having no direct involvement in selling cannabis or any controlled substances, despite being listed on a national exchange, and despite being current on SEC filings, the Company is often considered a “cannabis company” with all the nuances that accompany that label, including being blacklisted by banks, investments banks, and by the largest clearing services company. Due to the near-monopoly nature of some of these institutions like clearing houses, it makes it very difficult for the Company to raise money, deposit share certificates, or even have investment banking relationships. While we believe that we will be able to raise the capital we need to continue our operations, there can be no assurance that we will be successful in these efforts or will be able to raise enough capital for planned expansion.

We have a history of operating losses and there can be no assurance that we can again achieve or maintain profitability.

Our short-term focus is to become profitable by marketing our products. However, we have had a history of operating losses. For the fiscal year ended 2018 and 2017, we have a net loss of $1,786,274 and $1,852,861, respectively. Accordingly, there can be no guarantee that our efforts will be successful. Continue losses will require us to seek additional financing. No assurance can be given the we can raise any such financing and such financing could be dilutive to our shareholders.

We expect to acquire companies and we are subject to evolving and often expensive corporate governance regulations and requirements. Our failure to adequately adhere to these requirements, and comply with them with regard to acquired companies, some of which may be non-reporting entities, or the failure or circumvention of our controls and procedures could seriously harm our business and affect our status as a reporting company listed on a national securities exchange.

As a public reporting company whose shares are listed for trading on the NYSE American, we are subject to various regulations. Compliance with these evolving regulations is costly and requires a significant diversion of management time and attention, particularly with regard to our disclosure on controls and procedures and our internal control over financial reporting. As we have made and continue to make acquisitions in foreign countries, our internal controls and procedures may not be able to prevent errors or fraud in the future. We cannot guarantee that we can establish internal controls over financial reporting immediately on companies that we acquire. Thus, faulty judgments, simple errors or mistakes, or the failure of our personnel to enforce controls over acquired companies or to adhere to established controls and procedures, may make it difficult for us to ensure that the objectives of our control systems are met. A failure of our controls and procedures to detect other than inconsequential errors or fraud could seriously harm our ability to continue as a reporting company listed on a national securities exchange.

We may engage in strategic transactions that could impact our liquidity, increase our expenses and present significant distractions to our management, and which ultimately may not be successful.

From time to time we may consider strategic transactions, such as acquisitions of companies, asset purchases and out-licensing or in-licensing of products, product candidates or technologies, particularly those arrangements that seek to leverage other organizations’ internal platforms or competencies for the benefit of our products or potential products. Additional potential transactions that we may consider include a variety of different business arrangements, including spin-offs, strategic partnerships, joint ventures, restructurings, divestitures, business combinations and investments. Any such transaction may require us to incur non-recurring or other charges, may increase our near and long-term expenditures and may pose significant integration challenges or disrupt our management or business, which could adversely affect our operations and financial results. For example, these transactions may entail numerous operational and financial risks, including:

|

•

|

exposure to unknown or unanticipated liabilities, including foreign laws we are unfamiliar with;

|

|

•

|

disruption of our business and diversion of our management’s time and attention in order to develop acquired products, product candidates or technologies;

|

|

•

|

incurrence of substantial debt or dilutive issuances of equity securities to pay for acquisitions, which we may not be able to obtain on favorable terms, if at all;

|

|

•

|

higher than expected acquisition and integration costs;

|

|

•

|

write-downs of assets or goodwill or impairment charges;

|

|

•

|

increased amortization expenses;

|

|

•

|

difficulty and cost in combining the operations and personnel of any acquired businesses with our operations and personnel;

|

|

•

|

entering into a long-term relationship with a partner that proves to be unreliable or counterproductive;

|

|

•

|

impairment of relationships with key suppliers or customers of any acquired businesses due to changes in management and ownership; and

|

|

•

|

inability to retain key employees of any acquired businesses. Accordingly, although there can be no assurance that we will undertake or successfully complete any transactions of the nature described above, any transactions that we do complete could have a material adverse effect on our business, results of operations, financial condition and prospects if we are unable to execute on the planned objectives or capitalize on the relationship in the manner that was originally contemplated.

|

We have a limited senior management team size that may hamper our ability to effectively manage a publicly traded company and manage acquisitions and that may harm our business.

Since we operate in several foreign countries, we use consultants, including lawyers and accountants, to help us comply with regulatory requirements and public company compliance on a timely basis. As we expand, we expect to increase the size of our senior management. However, we cannot guarantee that in the interim period our senior management can adequately manage the requirements of a public company and the integration of acquisitions, and any failure to do so could lead to the imposition of fines, penalties, harm our business, status as a reporting company and our listing on the NYSE American.

Our expansion is dependent on laws pertaining to the legal cannabis industry.

We expect to acquire companies and hire management in the areas that we have identified. These include, among others, bio-pharmaceuticals with a focus on capitalizing on specific niches within these areas such as phytocannabinoid-based therapies. Entry into any of these areas requires special knowledge of the industry and products. In the event that we are perceived to be entering the legal cannabis sector, even indirectly or remotely, we could be subject to increased scrutiny by regulators because, among other things, marijuana is a Schedule-1 controlled substance and is illegal under federal law. Our failure to adequately manage the risk associated with these businesses and adequately manage the requirements of the regulators can adversely affect our business, our status as a reporting company and our listing on the NYSE American. Further, any adverse pronouncements from regulators about businesses related to the legal cannabis sector could adversely affect our stock price if we are perceived to be in a company in the cannabis sector.

Our company is in a very new and highly regulated industry. Significant and unforeseen changes in policy may have material impacts on our business.

Continued development in the phytocannabinoids industry is dependent upon continued state legislative authorization of cannabis as well as legislation and regulatory policy at the federal level. The federal Controlled Substances Act currently makes cannabis use and possession illegal on a national level. While there may be ample public support for legislative authorization, numerous factors impact the legislative process. Any one of these factors could slow or halt use and handling of cannabis in the United States or in other jurisdictions, which would negatively impact our development of phytocannabinoid-based therapies and our ability to test and productize these therapies.

Many U.S. state laws are in conflict with the federal Controlled Substances Act. While we do not intend to distribute or sell cannabis in the United States, it is unclear whether regulatory authorities in the United States would object to the registration or public offering of securities in the United States by our company, to the status of our company as a reporting company, or even to investors investing in our company if we engage in legal cannabis production and supply pursuant to the laws and authorization of the jurisdiction where the activity takes place. In addition, the status of cannabis under the Controlled Substances Act may have an adverse effect on federal agency approval of pharmaceutical use of phytocannabinoid products. Any such objection or interference could delay indefinitely or increase substantially the costs to access the equity capital markets, test our therapies, or create products from these phytocannabinoid-based therapies.

Banks and clearing houses may make it difficult for us to trade and clear our stock because they believe we are in the cannabis industry.

Continued development of the cannabis industry is dependent upon continued legislative authorization of cannabis. While there may be plenty public support for legislative authorization, several factors impact the legislative process. Additionally, many U.S. state laws are in conflict with the federal Controlled Substances Act, which makes cannabis use and possession illegal on a national level. While we do not intend to harvest, distribute, or sell cannabis in the United States, our presence in the pharmaceutical space can be misunderstood as being in the sale and distribution part of the cannabis industry. This could lead banks, regulators and others to mislabel our company. As such our stock could suffer if investors are unable to deposit their shares with a broker dealer and have those share clear.

Our business is dependent on continuing relationships with clients and strategic partners.

Our business requires developing and maintaining strategic alliances with contractors that undertake turnkey contracts for infrastructure development projects and with government organizations. The business and our results could be adversely affected if we are unable to maintain continuing relationships and pre-qualified status with key clients and strategic partners.

Currency fluctuations may reduce our assets and profitability.

We have assets located in foreign countries that are valued in foreign currencies. Fluctuation of the U.S. dollar relative to the foreign currency may adversely affect our assets and profit.

Our business relies heavily on our management team and any unexpected loss of key officers may adversely affect our operations.

The continued success of our business is largely dependent on the continued services of our key employees. The loss of the services of certain key personnel, without adequate replacement, could have an adverse effect on our performance. Our senior management, as well as the senior management of our subsidiaries, plays a significant role in developing and executing the overall business plan, maintaining client relationships, proprietary processes and technology. While no one is irreplaceable, the loss of the services of any would be disruptive to our business.

Our quarterly revenue, operating results and profitability will vary.

Factors that may contribute to the variability of quarterly revenue, operating results or profitability include:

| • |

Fluctuations in revenue due to seasonality of the market place, which results in uneven revenue and operating results over the year;

|

| • |

Additions and departures of key personnel; and

|

| • |

Strategic decisions made by us and our competitors, such as acquisitions, divestitures, spin-offs, joint ventures, strategic investments and changes in business strategy.

|

We may not successfully register the provisional patents with the United States Patent and Trademark Office

We have filed eight provisional patents with the United States Patent and Trademark Office (“USPTO”), in the combination therapy space, for the indications of pain, medical refractory epilepsy, eating disorders, and cachexia as part of our intellectual property strategy focused on the phytocannabinoid-based health care industry. There is no guarantee that our applications will result in a successful registration with the USPTO. If we are unsuccessful in registering patents, our ability to create a valuable line of products can be adversely affected. This in turn may have a material and adverse impact on the trading price of our common stock.

We may face risks relating to Health Care Privacy and Security Laws

We may be subject to various privacy and security regulations, including but not limited to HIPAA, as amended by HITECH, and their respective implementing regulations, including the related final published omnibus rule. HIPAA mandates, among other things, the adoption of uniform standards for the electronic exchange of information in common health care transactions, as well as standards relating to the privacy and security of individually identifiable health information, which require the adoption of administrative, physical and technical safeguards to protect such information. Among other things, HITECH makes HIPAA’s privacy and security standards directly applicable to “business associates” — independent contractors or agents of covered entities that receive or obtain protected health information in connection with providing a service on behalf of a covered entity. HITECH also increased the civil and criminal penalties that may be imposed against covered entities, business associates and possibly other persons, and gave state attorneys general new authority to file civil actions for damages or injunctions in federal courts to enforce the federal HIPAA laws and seek attorney’s fees and costs associated with pursuing federal civil actions. In addition, state laws govern the privacy and security of health information in certain circumstances, some of which are more stringent then HIPAA and many of which differ from each other in significant ways and may not have the same effect, thus complicating compliance efforts. Failure to comply with these laws, where applicable, can result in the imposition of significant civil and criminal penalties.

We are dependent on numerous third parties in our supply chain for the commercialization of Hyalolextm, and if we fail to maintain our supply and manufacturing relationships with these third parties or fail to develop new relationships with other third parties, we may be unable to continue to commercialize Hyalolextm or to develop other product candidates.

We rely on a number of third parties for the commercial supply of Hyalolextm and the supply of certain of our product candidates. Our ability to commercially supply Hyalolextm and to develop our product candidates depend, in part, on our ability to successfully obtain the materials for our products and outsource most, if not all of the aspects of their manufacturing, at competitive costs, in accordance with regulatory requirements and in sufficient quantities for commercialization and clinical testing. If we fail to develop and maintain supply relationships with these third parties, we may be unable to continue to commercialize Hyalolextm or certain of our other product candidates. We do not own or operate manufacturing facilities for Hyalolextm and currently lack the licensing to manufacture Hyalolextm directly.

Some of our lines of business will rely on third-party service providers to host and deliver services and data, and any interruptions or delays in these hosted services, security or privacy breaches, or failures in data collection could expose us to liability claims, increased costs, reduced revenue, and harm our business and reputation.

Our lines of business and services, but especially our development of cannabis-based combination therapies for products, including Hyalolextm for Alzheimer’s disease, and other products for Parkinson’s disease, chronic pain, post-traumatic stress disorder, and eating disorders and our long-term development of blockchain technologies to solve critical issues facing the Cannabis industry, rely on services hosted and controlled directly by our suppliers and distributors and their third-party service providers. We do not have redundancy for all of our systems, many of our critical applications reside in only one of our data centers, and our disaster recovery planning may not account for all eventualities. These facts could cause reputational harm, loss of customers and future business, thereby reducing our revenue.

Our suppliers and distributors and their third-party service providers hold customer data, some of which is hosted in third-party facilities. A security incident at those facilities or ours may compromise the confidentiality, integrity or availability of customer data. Unauthorized access to customer data stored on our computers or networks may be obtained through break-ins, breaches of our secure network by an unauthorized party, employee theft or misuse or other misconduct. It is also possible that unauthorized access to customer data may be obtained through inadequate use of security controls by customers. Accounts created with weak passwords could allow cyber-attackers to gain access to customer data. If there were an inadvertent disclosure of customer information, or if a third party were to gain unauthorized access to the information we possess on behalf of our customers, our operations could be disrupted, our reputation could be damaged, and we could be subject to claims or other liabilities. In addition, such perceived or actual unauthorized disclosure of the information we collect, or breach of our security could damage our reputation, result in the loss of customers and harm our business.

Hardware or software failures or errors in our systems or those of our suppliers and distributors or their third-party service providers, could result in data loss or corruption, cause the information that we collect to be incomplete or contain inaccuracies that our customers regard as significant or cause us to fail to meet committed service levels. Furthermore, our ability to collect and report data may be delayed or interrupted by several factors, including access to the Internet, the failure of our network or software systems or security breaches. In addition, computer viruses or other malware may harm our systems, causing us to lose data, and the transmission of computer viruses or other malware could expose us to litigation. We may also find, on occasion, that we cannot deliver data and reports in near real time because of several factors, including failures of our network or software. If we supply inaccurate information or experience interruptions in our ability to capture, store and supply information in near real time or at all, our reputation could be harmed, and we could lose customers, or we could be found liable for damages or incur other losses.

The states in which we and our distributers and suppliers and their service providers operate require that we maintain certain information about our customers and transactions. If we fail to maintain such information, we could be in violation of state laws.

Risks Related to Ownership of Our Common Stock

Our accounting personnel may make unintentional errors.

Given our small size and foreign operations, a small unrectified mistake in the preparation of financial statements and the maintenance of our books and records in accordance with U.S. GAAP and SEC rules and regulations may constitute a material weakness in our internal controls over financial reporting. For more information, please see Item 9A, “Controls and Procedures.”

Future sales of common stock by us could cause our stock price to decline and dilute your ownership in our company.

There are currently 11,656,668 outstanding public warrants to purchase 1,165,667 shares of our common stock at an exercise price of $50.00 a share. We also have outstanding option to buy 650,000 shares, expiring between October 31, 2022 and October 31, 2023, with a weighted average exercise price of $0.34. We are not restricted from issuing additional shares of our common stock or preferred stock, including any securities that are convertible into or exchangeable for, or that represent the right to receive, common stock or preferred stock or any substantially similar securities. The market price of our common stock could decline as a result of sales of a large number of shares of our common stock by us in the market or the perception that such sales could occur. If we raise funds by issuing additional securities in the future or the outstanding warrants or stock options to purchase our common stock are exercised, the newly-issued shares will also dilute your percentage ownership in our company.

The market price for our common stock may be volatile.

The trading volume in our common stock may fluctuate and cause significant price variations to occur. Fluctuations in our stock price may not be correlated in a predictable way to our performance or operating results. Our stock price may fluctuate as a result of a number of events and factors such as those described elsewhere in this “Risk Factors” section, events described in this report, and other factors that are beyond our control. In addition, the stock market, in general, has historically experienced significant price and volume fluctuations. Our common stock has also been volatile, with our 52-week price range being at a low of $0.30 and a high of $1.63 per share. These fluctuations are often unrelated to the operating performance of particular companies. These broad market fluctuations may cause declines in the market price of our common stock. In addition, it is possible, given our current trading price, that we may fail to comply with the minimum trading price required to trade our shares on the NYSE American.

Our publicly-filed reports are subject to review by the SEC, and any significant changes or amendments required as a result of any such review may result in material liability to us and may have a material adverse impact on the trading price of our common stock.

The reports of publicly-traded companies are subject to review by the SEC from time to time for the purpose of assisting companies in complying with applicable disclosure requirements, and the SEC is required to undertake a comprehensive review of a company’s reports at least once every three years under the Sarbanes-Oxley Act of 2002. SEC reviews may be initiated at any time. We could be required to modify, amend, or reformulate information contained in prior filings as a result of an SEC review, as well as state in filings that we have inadequate control or expertise over financial reporting. Any modification, amendment, or reformulation of information contained in such reports could be significant and result in material liability to us and have a material and adverse impact on the trading price of our common stock.

We do not anticipate declaring any cash dividends on our common stock.

We have never declared or paid cash dividends on our common stock and do not plan to pay any cash dividends in the near future. Our current policy is to retain all funds and earnings for use in the operation and expansion of our business. In addition, the terms of our debt agreement prohibit the payment of cash dividends or other distributions on any of our capital stock except dividends payable in additional shares of capital stock.

Maryland anti-takeover provisions and certain anti-takeover effects of our Charter and Bylaws may inhibit a takeover at a premium price that may be beneficial to our stockholders.

Maryland anti-takeover provisions and certain anti-takeover effects of our charter and bylaws may be utilized, under some circumstances, as a method of discouraging, delaying or preventing a change of control of our company at a premium price that would be beneficial to our stockholders. For more detailed information about these provisions, please see “Anti-takeover Law, Limitations of Liability and Indemnification” as following:

Business Combinations

Under the Maryland General Corporation Law, some business combinations, including a merger, consolidation, share exchange or, in some circumstances, an asset transfer or issuance or reclassification of equity securities, are prohibited for a period of time and require an extraordinary vote. These transactions include those between a Maryland corporation and the following persons (a “Specified Person”):

| • |

an interested stockholder, which is defined as any person (other than a subsidiary) who beneficially owns 10% or more of the corporation’s voting stock, or who is an affiliate or an associate of the corporation who, at any time within a two-year period prior to the transaction, was the beneficial owner of 10% or more of the voting power of the corporation’s voting stock; or an affiliate of an interested stockholder.

|

A person is not an interested stockholder if the board of directors approved in advance the transaction by which the person otherwise would have become an interested stockholder. The board of directors of a Maryland corporation also may exempt a person from these business combination restrictions prior to the time the person becomes a Specified Person and may provide that its exemption be subject to compliance with any terms and conditions determined by the board of directors. Transactions between a corporation and a Specified Person are prohibited for five years after the most recent date on which such stockholder becomes a Specified Person. After five years, any business combination must be recommended by the board of directors of the corporation and approved by at least 80% of the votes entitled to be cast by holders of voting stock of the corporation and two-thirds of the votes entitled to be cast by holders of shares other than voting stock held by the Specified Person with whom the business combination is to be effected, unless the corporation’s stockholders receive a minimum price as defined by Maryland law and other conditions under Maryland law are satisfied.

A Maryland corporation may elect not to be governed by these provisions by having its board of directors exempt various Specified Persons, by including a provision in its charter expressly electing not to be governed by the applicable provision of Maryland law or by amending its existing charter with the approval of at least 80% of the votes entitled to be cast by holders of outstanding shares of voting stock of the corporation and two-thirds of the votes entitled to be cast by holders of shares other than those held by any Specified Person. Our Charter does not include any provision opting out of these business combination provisions.

Control Share Acquisitions