Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - CROWN CRAFTS INC | ex_114943.htm |

| EX-32.1 - EXHIBIT 32.1 - CROWN CRAFTS INC | ex_114942.htm |

| EX-31.2 - EXHIBIT 31.2 - CROWN CRAFTS INC | ex_114941.htm |

| EX-31.1 - EXHIBIT 31.1 - CROWN CRAFTS INC | ex_114940.htm |

| EX-23.1 - EXHIBIT 23.1 - CROWN CRAFTS INC | ex_114939.htm |

| EX-21.1 - EXHIBIT 21.1 - CROWN CRAFTS INC | ex_114938.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________

Form 10-K

(Mark One)

|

☑ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

| For the fiscal year ended April 1, 2018 |

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 1-7604

Crown Crafts, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

58-0678148 |

|

(State of Incorporation) |

(I.R.S. Employer Identification No.) |

|

916 S. Burnside Ave. |

|

|

Gonzales, Louisiana |

70737 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant's Telephone Number, including area code: (225) 647-9100

Securities registered pursuant to Section 12(b) of the Act:

| Title of class | Name of exchange on which registered |

| Common Stock, $0.01 par value | The NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☑ |

| Non-Accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller Reporting Company | ☐ |

| Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

The approximate aggregate market value of the voting stock held by non-affiliates of the registrant as of September 29, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter) was $55.5 million.

As of May 10, 2018, 10,069,558 shares of the registrant’s common stock were outstanding.

Documents Incorporated by Reference:

Portions of the registrant’s Proxy Statement for its 2018 Annual Meeting of Stockholders are incorporated into Part III hereof by reference.

|

Page |

||

|

Item 1. |

3 |

|

|

Item 1A. |

6 |

|

|

Item 1B. |

11 |

|

|

Item 2. |

11 |

|

|

Item 3. |

11 |

|

|

Item 4. |

11 |

|

|

Item 5. |

12 |

|

|

Item 6. |

14 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

15 |

|

Item 7A. |

21 |

|

|

Item 8. |

21 |

|

|

Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. |

21 |

|

Item 9A. |

22 |

|

|

Item 9B. |

22 |

|

|

Item 10. |

23 |

|

|

Item 11. |

23 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. |

23 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence. |

23 |

|

Item 14. |

23 |

|

|

Item 15. |

24 |

|

Cautionary Notice Regarding Forward-Looking Statements

Certain of the statements made herein under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere, including information incorporated herein by reference to other documents, are “forward-looking statements” within the meaning of, and subject to the protections of, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include statements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, assumptions, estimates, intentions and future performance and involve known and unknown risks, uncertainties and other factors, many of which may be beyond our control and which may cause the actual results, performance or achievements of Crown Crafts, Inc. to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements.

All statements other than statements of historical fact are statements that could be forward-looking statements. You can identify these forward-looking statements through our use of words such as “may,” “anticipate,” “assume,” “should,” “indicate,” “would,” “believe,” “contemplate,” “expect,” “estimate,” “continue,” “plan,” “point to,” “project,” “predict,” “could,” “intend,” “target,” “potential” and other similar words and expressions of the future. These forward-looking statements may not be realized due to a variety of factors, including, without limitation, those described in Part I, Item 1A. “Risk Factors,” and elsewhere in this report and those described from time to time in our future reports filed with the Securities and Exchange Commission (the “SEC”) under the Exchange Act.

All written or oral forward-looking statements that are made by or are attributable to us are expressly qualified in their entirety by this cautionary notice. Our forward-looking statements apply only as of the date of this report or the respective date of the document from which they are incorporated herein by reference. We have no obligation and do not undertake to update, revise or correct any of the forward-looking statements after the date of this report, or after the respective dates on which such statements otherwise are made, whether as a result of new information, future events or otherwise.

Description of Business

Crown Crafts, Inc. (the “Company”) was originally formed as a Georgia corporation in 1957. The Company was reincorporated as a Delaware corporation in 2003. The Company’s executive offices are located at 916 South Burnside Avenue, Gonzales, Louisiana 70737, its telephone number is (225) 647-9100 and its internet address is www.crowncrafts.com.

The Company operates indirectly through its wholly-owned subsidiaries, Hamco, Inc. (“Hamco”), Crown Crafts Infant Products, Inc. (“CCIP”) and Carousel Designs, LLC (“Carousel”), in the infant, toddler and juvenile products segment within the consumer products industry. The infant, toddler and juvenile products segment consists of infant and toddler bedding and blankets, bibs, soft bath products, disposable products, developmental toys and accessories. Sales of the Company’s products are generally made directly to retailers, which are primarily mass merchants, mid-tier retailers, juvenile specialty stores, value channel stores, grocery and drug stores, restaurants, wholesale clubs and internet-based retailers, as well as directly to consumers through www.babybedding.com. The Company’s products are marketed under a variety of Company-owned trademarks, under trademarks licensed from others and as private label goods.

The Company's fiscal year ends on the Sunday nearest to or on March 31. References herein to “fiscal year 2018” or “2018” represent the 52-week period ended April 1, 2018, “fiscal year 2017” or “2017” represent the 52-week period ended April 2, 2017, and references to “fiscal year 2016” or “2016” represent the 53-week period ended April 3, 2016.

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act available free of charge on its website at www.crowncrafts.com as soon as reasonably practicable after such material has been electronically filed with the SEC. These reports are also available without charge on the SEC’s website at www.sec.gov.

Competition

The infant and toddler consumer products industry is highly competitive. The Company competes with a variety of distributors and manufacturers (both branded and private label), including large infant and juvenile product companies and specialty infant and juvenile product manufacturers, on the basis of quality, design, price, brand name recognition, service and packaging. The Company’s ability to compete depends principally on styling, price, service to the retailer and continued high regard for the Company’s products and trade names.

Trademarks, Copyrights and Patents

The Company considers its intellectual property to be of material importance to its business. Sales of products marketed under the Company’s trademarks, including NoJo®, Neat Solutions®, Carousel Designs® and Sassy®, accounted for 30%, 23%, and 23% of the Company’s total gross sales during fiscal years 2018, 2017 and 2016, respectively. Protection for these trademarks is obtained through domestic and foreign registrations. The Company also markets designs which are subject to copyrights and design patents owned by the Company.

International Sales

Sales to customers in countries other than the U.S. represented 3% of the Company’s total gross sales during each of fiscal years 2018, 2017 and 2016, which included 0.4% of sales to the customers set forth below that represented at least 10% of the Company’s gross sales during fiscal year 2018. International sales are based upon the location that predominately represents what the Company believes to be the final destination of the products delivered to the Company’s customers.

Products

The Company's primary focus is on infant, toddler and juvenile products, including the following:

|

● |

infant and toddler bedding |

|

● |

blankets and swaddle blankets |

|

● |

nursery and toddler accessories |

|

● |

room décor |

|

● |

reusable and disposable bibs |

|

● |

burp cloths |

|

● |

hooded bath towels and washcloths |

|

● |

reusable and disposable placemats and floor mats |

|

● |

disposable toilet seat covers and changing mats |

|

● |

developmental toys |

|

● |

feeding and care goods |

|

● |

other infant, toddler and juvenile soft goods |

Recent Acquisitions

Carousel: On August 4, 2017, Carousel Acquisition, LLC, a newly formed subsidiary of the Company, acquired substantially all of the assets and business, and assumed certain specified liabilities, of a privately held manufacturer and online retailer of premium infant and toddler bedding and nursery décor based in Douglasville, Georgia, which was at that time named Carousel Designs, LLC (the “Carousel Acquisition”). On August 11, 2017, the seller of such assets having relinquished its rights to its name as part of the terms of the acquisition transaction, Carousel Acquisition, LLC changed its name to Carousel Designs, LLC. To complete the Carousel Acquisition, Carousel paid $8.7 million from cash on hand and also paid off capital leases amounting to $845,000 that were associated with certain acquired fixed assets.

Sassy: On December 15, 2017, Hamco acquired certain assets associated with the Sassy®-branded developmental toy, feeding and baby care product line from Sassy 14, LLC and assumed certain related liabilities (the “Sassy Acquisition”). To complete the Sassy Acquisition, Hamco paid $6.5 million from a combination of cash on hand and the Company’s revolving line of credit.

Government Regulation and Environmental Control

The Company is subject to various federal, state and local environmental laws and regulations, which regulate, among other things, product safety and the discharge, storage, handling and disposal of a variety of substances and wastes, and to laws and regulations relating to employee safety and health, principally the Occupational Safety and Health Administration Act and regulations thereunder. The Company believes that it currently complies in all material respects with applicable environmental, health and safety laws and regulations and that future compliance with such existing laws or regulations will not have a material adverse effect on its capital expenditures, earnings or competitive position. However, there is no assurance that such requirements will not become more stringent in the future or that the Company will not have to incur significant costs to comply with such requirements.

Sales and Marketing

The Company’s products are marketed through a national sales force consisting of salaried sales executives and employees located in Compton, California; Gonzales, Louisiana; Grand Rapids, Michigan; and Bentonville, Arkansas. Products are also marketed by independent commissioned sales representatives located throughout the U.S. Substantially all products are sold to retailers for resale to consumers. The Company's subsidiaries introduce new products throughout the year and participate at the ABC Kids Expo.

Product Sourcing

Foreign and domestic contract manufacturers produce most of the Company’s products, with the largest concentration being in China. The Company makes sourcing decisions on the basis of quality, timeliness of delivery and price, including the impact of ocean freight and duties. Although the Company maintains relationships with a limited number of suppliers, the Company believes that its products may be readily manufactured by several alternative sources in quantities sufficient to meet the Company's requirements. The Company’s management and quality assurance personnel visit the third-party facilities regularly to monitor and audit product quality and to ensure compliance with labor requirements and social and environmental standards. In addition, the Company closely monitors the currency exchange rate. The impact of future fluctuations in the exchange rate or changes in safeguards cannot be predicted with certainty. The Company also produces some of its products domestically at a Company facility located in Douglasville, Georgia.

The Company maintains a foreign representative office located in Shanghai, China, which is responsible for the coordination of production, purchases and shipments, seeking out new vendors and overseeing inspections for social compliance and quality.

The Company’s products are warehoused and distributed from leased facilities located in Compton, California and Douglasville, Georgia.

Product Design and Styling

The Company believes that its creative team is one of its key strengths. The Company’s product designs are primarily created internally and are supplemented by numerous additional sources, including independent artists, decorative fabric manufacturers and apparel designers. Ideas for product design creations are drawn from various sources and are reviewed and modified by the design staff to ensure consistency within the Company’s existing product offerings and the themes and images associated with such existing products. In order to respond effectively to changing consumer preferences, the Company’s designers and stylists attempt to stay abreast of emerging lifestyle trends in color, fashion and design. When designing products under the Company’s various licensed brands, the Company’s designers coordinate their efforts with the licensors’ design teams to provide for a more fluid design approval process and to effectively incorporate the image of the licensed brand into the product. The Company’s designs include traditional, contemporary, textured and whimsical patterns across a broad spectrum of retail price points. Utilizing state of the art computer technology, the Company continually develops new designs throughout the year for all of its product groups. This continual development cycle affords the Company design flexibility, multiple opportunities to present new products to customers and the ability to provide timely responses to customer demands and changing market trends. The Company also creates designs for exclusive sale by certain of its customers under the Company’s brands, as well as the customers’ private label brands.

Employees

At May 10, 2018, the Company had 179 employees, none of whom is represented by a labor union or is otherwise a party to a collective bargaining agreement. The Company attracts and maintains qualified personnel by paying competitive salaries and benefits and offering opportunities for advancement. The Company considers its relationship with its employees to be good.

Customers

The Company's customers consist principally of mass merchants, mid-tier retailers, juvenile specialty stores, value channel stores, grocery and drug stores, restaurants, internet accounts and wholesale clubs. The Company does not enter into long-term or other purchase agreements with its customers. The table below sets forth those customers that represented at least 10% of the Company’s gross sales in fiscal years 2018, 2017, and 2016.

| Fiscal Year | |||||

|

|

2018 |

2017 |

2016 |

||

|

Walmart Inc. |

39% |

42% |

42% |

||

|

Toys "R" Us, Inc. |

15% |

19% |

23% |

||

|

Amazon.com, Inc. |

11% |

* |

* |

||

|

* Amount represented less than 10% of the Company's gross sales for this fiscal year. |

|||||

Licensed Products

Certain products are manufactured and sold pursuant to licensing agreements for trademarks. Also, many of the designs used by the Company are copyrighted by other parties, including trademark licensors, and are available to the Company through copyright license agreements. The licensing agreements are generally for an initial term of one to three years and may or may not be subject to renewal or extension. Sales of licensed products represented 52% of the Company’s gross sales in fiscal year 2018, which included 34% of sales under the Company's license agreements with affiliated companies of The Walt Disney Company (“Disney”), which expire as set forth below:

|

License Agreement |

Expiration |

|

Infant Bedding and Décor |

December 31, 2018 |

|

Infant Feeding and Bath |

December 31, 2019 |

|

Toddler Bedding |

December 31, 2019 |

Seasonality and Inventory Management

There are no significant variations in the seasonal demand for the Company’s products from year to year. Sales are generally higher in periods when customers take initial shipments of new products, as these orders typically include enough products for initial sets for each store and additional quantities for the customer’s distribution centers. The timing of these initial shipments varies by customer and depends on when the customer finalizes store layouts for the upcoming year and whether the customer has any mid-year introductions of products. Sales may also be higher or lower, as the case may be, in periods when customers are restricting internal inventory levels. Consistent with the expected introduction of specific product offerings, the Company carries necessary levels of inventory to meet the anticipated delivery requirements of its customers. Customer returns of merchandise shipped are historically less than 1% of gross sales.

The following risk factors as well as the other information contained in this report and other filings made by the Company with the SEC should be considered in evaluating the Company’s business. Additional risks and uncertainties not presently known to us or that we currently consider immaterial may also impair our business operations. If any of the following risks actually occur, operating results may be affected in future periods.

The loss of one or more of the Company’s key customers could result in a material loss of revenues.

The Company’s top three customers represented approximately 65% of gross sales in fiscal year 2018, which included 15% of sales to Toys “R” Us-Delaware, Inc. (“Toys-Delaware”), an affiliated company of Toys “R” Us, Inc. (“TRU”). On September 18, 2017, TRU and Toys-Delaware filed petitions for relief under Chapter 11 of the U.S. Bankruptcy Code with the U.S. Bankruptcy Court for the Eastern District of Virginia. On March 14, 2018, TRU filed a motion with the Court seeking authority to close all of the remaining Toys-Delaware stores and distribution centers in the U.S., and to otherwise liquidate and wind-down all operations of Toys-Delaware. The Company had ceased all shipments to Toys-Delaware shortly before the liquidation filing was made. The Company anticipates that the loss of future business with Toys-Delaware may be mitigated by a shift to the Company’s other customers.

Although the Company does not enter into contracts with its key customers, it expects its key customers (with the exception of Toys-Delaware) to continue to be a significant portion of its gross sales in the future. The loss of, or a decline in orders from, either or both of the Company’s two remaining top customers could result in a material decrease in the Company’s revenue and operating income.

The loss of one or more of the Company’s licenses could result in a material loss of revenues.

Sales of licensed products represented 52% of the Company’s gross sales in fiscal year 2018, which included 34% of sales associated with the Company’s license agreements with Disney. The Company could experience a material loss of revenues if it is unable to renew its major license agreements or obtain new licenses. The volume of sales of licensed products is inherently tied to the success of the characters, films and other licensed programs of the Company’s licensors. A decline in the popularity of these licensed programs or the inability of the licensors to develop new properties for licensing could also result in a material loss of revenues to the Company. Additionally, the Company’s license agreements with Disney and others require a material amount of minimum guaranteed royalty payments. The failure by the Company to achieve the sales envisioned by the license agreements could result in the payment by the Company of shortfalls in the minimum guaranteed royalty payments, which would adversely impact the Company’s operating results.

The Company’s business is impacted by general economic conditions and related uncertainties affecting markets in which the Company operates.

The Company’s growth is largely dependent upon growth in the birthrate, and in particular, the rate of first births. Economic conditions, including the real and perceived threat of a recession, could lead individuals to decide to forgo or delay having children. Even under optimal economic conditions, shifts in demographic trends and preferences could have the consequence of individuals starting to have children later in life and/or having fewer children. These conditions could result in reduced demand for some of the Company’s products, increased order cancellations and returns, an increased risk of excess and obsolete inventories and increased pressure on the prices of the Company’s products. Also, although the Company’s use of a commercial factor significantly reduces the risk associated with collecting accounts receivable, the factor may at any time terminate or limit its approval of shipments to a particular customer, and the likelihood of the factor doing so may increase due to a change in economic conditions. Such an action by the factor could result in the loss of future sales to the affected customer.

The Company’s success is dependent upon retaining key management personnel.

Certain of the Company’s executive management and other key personnel have been integral to the Company’s operations and the execution of its growth strategy. The departure from the Company of one or more of these individuals, along with the inability of the Company to attract qualified and suitable individuals to fill the Company’s open positions, could adversely impact the Company’s growth and operating results.

The Company may need to write down or write off inventory.

If product programs end before the inventory is completely sold, then the remaining inventory may have to be sold at less than carrying value. The market value of certain inventory items could drop to below carrying value after a decline in sales, at the end of programs, or when management makes the decision to exit a product group. Such inventory would then need to be written down to the lower of carrying or market value, or possibly completely written off, which would adversely affect the Company’s operating results.

Recalls or product liability claims could increase costs or reduce sales.

The Company must comply with the Consumer Product Safety Improvement Act, which imposes strict standards to protect children from potentially harmful products and which requires that the Company’s products be tested to ensure that they are within acceptable levels for lead and phthalates. The Company must also comply with related regulations developed by the Consumer Product Safety Commission and similar state regulatory authorities. The Company’s products could be subject to involuntary recalls and other actions by these authorities, and concerns about product safety may lead the Company to voluntarily recall, accept returns or discontinue the sale of select products. Product liability claims could exceed or fall outside the scope of the Company’s insurance coverage. Recalls or product liability claims could result in decreased consumer demand for the Company’s products, damage to the Company’s reputation, a diversion of management’s attention from its business and increased customer service and support costs, any or all of which could adversely affect the Company’s operating results.

The strength of the Company’s competitors may impact the Company’s ability to maintain and grow its sales, which could decrease the Company’s revenues.

The infant and toddler consumer products industry is highly competitive. The Company competes with a variety of distributors and manufacturers, both branded and private label. The Company’s ability to compete successfully depends principally on styling, price, service to the retailer and continued high regard for the Company’s products and trade names. Several of these competitors are larger than the Company and have greater financial resources than the Company, and some have experienced financial challenges from time to time, including servicing significant levels of debt. Those facing financial pressures could choose to make particularly aggressive pricing decisions in an attempt to increase revenue. The effects of increased competition could result in a material decrease in the Company’s revenues.

The Company’s ability to identify, consummate and integrate acquisitions, divestitures and other significant transactions successfully could have an adverse impact on the Company’s financial results, business and prospects.

As part of its business strategy, the Company has made acquisitions of businesses, divestitures of businesses and assets, and has entered into other transactions to further the interests of the Company’s business and its stockholders. Risks associated with such activities include the following, any of which could adversely affect the Company’s financial results:

|

● |

The active management of acquisitions, divestitures and other significant transactions requires varying levels of Company resources, including the efforts of the Company’s key management personnel, which could divert attention from the Company’s ongoing business operations. |

|

● |

The Company may not fully realize the anticipated benefits and expected synergies of any particular acquisition or investment, or may experience a prolonged timeframe for realizing such benefits and synergies. |

|

● |

Increased or unexpected costs, unanticipated delays or failure to meet contractual obligations could make acquisitions and investments less profitable or unprofitable. |

The Company’s ability to comply with its credit facility is subject to future performance and other factors.

The Company’s ability to make required payments of principal and interest on its debts, to refinance its maturing indebtedness, to fund capital expenditures or to comply with its debt covenants will depend upon future performance. The Company’s future performance is, to a certain extent, subject to general economic, financial, competitive, legislative, regulatory and other factors beyond its control. The breach of any of the debt covenants could result in a default under the Company’s credit facility. Upon the occurrence of an event of default, the Company’s lender could make an immediate demand of the amount outstanding under the credit facility. If a default was to occur and such a demand was to be made, there can be no assurance that the Company’s assets would be sufficient to repay the indebtedness in full.

The Company’s debt covenants may affect its liquidity or limit its ability to pursue acquisitions, incur debt, make investments, sell assets or complete other significant transactions.

The Company’s credit facility contains usual and customary covenants regarding significant transactions, including restrictions on other indebtedness, liens, transfers of assets, investments and acquisitions, merger or consolidation transactions, transactions with affiliates and changes in or amendments to the organizational documents for the Company and its subsidiaries. Unless waived by the Company’s lender, these covenants could limit the Company’s ability to pursue opportunities to expand its business operations, respond to changes in business and economic conditions and obtain additional financing, or otherwise engage in transactions that the Company considers beneficial.

The Company’s inability to anticipate and respond to consumers’ tastes and preferences could adversely affect the Company’s revenues.

Sales are driven by consumer demand for the Company’s products. There can be no assurance that the demand for the Company’s products will not decline or that the Company will be able to anticipate and respond to changes in demand. The Company’s failure to adapt to these changes could lead to lower sales and excess inventory, which could have a material adverse effect on the Company’s financial condition and operating results.

Customer pricing pressures could result in lower selling prices, which could negatively affect the Company’s operating results.

The Company’s customers could place pressure on the Company to reduce the prices of its products. The Company continuously strives to stay ahead of its competition in sourcing, which allows the Company to obtain lower cost products while maintaining high standards for quality. There can be no assurance that the Company could respond to a decrease in sales prices by proportionately reducing its costs, which could adversely affect the Company’s operating results.

Changes in international trade regulations and other risks associated with foreign trade could adversely affect the Company’s sourcing.

The Company sources its products primarily from foreign contract manufacturers, with the largest concentration being in China. Difficulties encountered by these suppliers, such as the instability inherent in operating within an authoritarian political structure, could halt or disrupt production of the Company’s products. The Chinese government could make allegations against the Company of corruption or antitrust violations, or could adopt regulations related to the manufacture of products within China, including quotas, duties, taxes and other charges or restrictions on the exportation of goods produced in China. Alternatively, the U.S. government could impose similar actions on the importation of goods manufactured in China. Any of these actions could result in an increase in the cost of the Company’s products. Also, an arbitrary strengthening of the Chinese currency versus the U.S. Dollar could increase the prices at which the Company purchases finished goods. Any event causing a disruption of the flow of products manufactured on behalf of the Company, whether within the Chinese interior or at the point of embarkation, could result in delays in the receipt of the Company’s inventory and an increase in the cost of the Company’s products. In addition, changes in U.S. customs procedures or delays in the clearance of goods through customs could result in the Company being unable to deliver goods to customers in a timely manner or the potential loss of sales altogether. The occurrence of any of these events could adversely affect the Company’s profitability.

A significant disruption to the Company’s distribution network or to the timely receipt of inventory could adversely impact sales or increase transportation costs, which would decrease the Company’s profits.

Nearly all of the Company’s products are imported from China into the Port of Long Beach in southern California. There are many links in the distribution chain, including the availability of ocean freight, cranes, dockworkers, containers, tractors, chassis and drivers. The timely receipt of the Company’s products is also dependent upon efficient operations at the Port of Long Beach. Any shortages in the availability of any of these links or disruptions in port operations, including strikes, lockouts or other work stoppages or slowdowns, could cause bottlenecks and other congestion in the distribution network, which could adversely impact the Company’s ability to obtain adequate inventory on a timely basis and result in lost sales, increased transportation costs and an overall decrease of the Company’s profits.

Disruptions to the Company’s information technology systems could negatively affect the Company’s results of operations.

The Company’s operations are highly dependent upon computer hardware and software systems, including customized information technology systems and cloud-based applications. The importance of data management and technology to the Company is analogous to the importance of electricity in the past century. The Company also employs third-party systems and software that are integral to its operations. These systems are vulnerable to cybersecurity incidents, including disruptions and security breaches, which can result from unintentional events or deliberate attacks by insiders or third parties, such as cybercriminals, competitors, nation-states, computer hackers and other cyber terrorists. The Company faces an evolving landscape of cybersecurity threats in which evildoers use a complex array of means to perpetrate attacks, including the use of stolen access credentials, malware, ransomware, phishing, structured query language injection attacks and distributed denial-of-service attacks. The Company has implemented security measures to securely maintain confidential and proprietary information stored on the Company’s information systems and continually invests in maintaining and upgrading the systems and applications to mitigate these risks. There can be no assurance that these measures and technology will adequately prevent an intrusion or that a third party that is relied upon by the Company will not suffer an intrusion, that unauthorized individuals will not gain access to confidential or proprietary information or that any such incident will be timely detected and effectively countered. A significant data security breach could result in a disruption to the Company’s operations and could adversely impact its results of operations.

The Company’s sourcing and marketing operations in foreign countries are subject to anti-corruption laws.

The Company’s foreign operations are subject to laws prohibiting improper payments and bribery, including the U.S. Foreign Corrupt Practices Act and similar laws and regulations in foreign jurisdictions, which apply to the Company’s directors, officers, employees and agents acting on behalf of the Company. Failure to comply with these laws could result in damage to the Company’s reputation, a diversion of management’s attention from its business, increased legal and investigative costs, and civil and criminal penalties, any or all of which could adversely affect the Company’s operating results.

The Company could experience adjustments to its effective tax rate or its prior tax obligations, either of which could adversely affect its results of operations.

The Company is subject to income taxes in the many jurisdictions in which it operates, including the U.S., several U.S. states and China. At any particular point in time, several tax years are subject to general examination or other adjustment by these various jurisdictions. In December 2016, the Company received notification from the State of California of its intention to examine the Company’s consolidated income tax returns for the fiscal years ended April 3, 2011, April 1, 2012, March 31, 2013 and March 30, 2014. The ultimate resolution of the examination could include administrative or legal proceedings. Although the Company believes that the calculations and positions taken on its original and amended filed returns are reasonable and justifiable, negotiations or litigation leading to the final outcome of any examination or claim for refund could result in an adjustment to the position that the Company has taken. Such adjustment could result in further adjustment to one or more income tax returns for other jurisdictions, or to income tax returns for prior or subsequent tax years, or both. To the extent that the Company’s reserve for unrecognized tax benefits is not adequate to support the cumulative effect of such adjustments, the Company could experience a material adverse impact on operating results.

The Company’s provision for income taxes is based on its effective tax rate, which in any given financial statement period could fluctuate based on changes in tax laws or regulations, changes in the mix and level of earnings by taxing jurisdiction, changes in the amount of certain expenses within the consolidated statements of income that will never be deductible on the Company’s income tax returns and certain charges deducted on the Company’s income tax returns that are not included within the consolidated statements of income. These changes could cause fluctuations in the Company’s effective tax rate either on an absolute basis, or in relation to varying levels of the Company’s pre-tax income. Such fluctuations in the Company’s effective tax rate could adversely affect its results of operations.

On December 22, 2017, the President of the United States signed into law comprehensive tax legislation commonly referred to as the Tax Cuts and Jobs Act (the “TCJA”), which includes a provision to lower the federal corporate income tax rate to 21% effective as of January 1, 2018. The final impact of the TCJA on the Company may differ from the Company’s estimates, possibly materially, due to such factors as changes in interpretations and assumptions made, related regulations or other guidance that may be issued, and actions taken by the Company in response to the enactment of the TCJA.

The Company could experience losses associated with its intellectual property.

The Company relies upon the fair interpretation and enforcement of patent, copyright, trademark and trade secret laws in the U.S., similar laws in other countries, and agreements with employees, customers, suppliers, licensors and other parties. Such reliance serves to establish and maintain the intellectual property rights associated with the products that the Company develops and sells. However, the laws and courts of certain countries at times do not protect intellectual property rights or respect contractual agreements to the same extent as the laws of the U.S. Therefore, in certain jurisdictions the Company may not be able to protect its intellectual property rights against counterfeiting or enforce its contractual agreements with other parties. In addition, another party could claim that the Company is infringing upon such party’s intellectual property rights, and claims of this type could lead to a civil complaint.

An unfavorable outcome in litigation involving intellectual property could result in any or all of the following: (i) civil judgments against the Company, which could require the payment of royalties on both past and future sales of certain products, as well as plaintiff’s attorneys’ fees and other litigation costs; (ii) impairment charges of up to the carrying value of the Company’s intellectual property rights; (iii) restrictions on the ability of the Company to sell certain of its products; (iv) legal and other costs associated with investigations and litigation; and (v) the Company’s competitive position could be adversely affected.

Economic conditions could result in an increase in the amounts paid for the Company’s products.

Significant increases in the price of raw materials that are components of the Company’s products, including cotton, oil and labor, could adversely affect the amounts that the Company must pay its suppliers for its finished goods. If the Company is unable to pass these cost increases along to its customers, its profitability could be adversely affected.

Government regulation of the Internet and e-commerce is evolving, and unfavorable changes or failure by the Company to adequately comply with new laws and regulations could substantially harm its results of operations.

The Company is subject to laws and regulations governing the Internet and e-commerce. The U.S. Supreme Court is currently deliberating the constitutionality of some of these laws. These regulations and laws include requirements to potentially collect and remit sales tax on orders of the Company’s products that are made through the Internet and are subsequently shipped to customers in thousands of jurisdictions throughout the U.S. within which the Company does not have a routine physical presence. These laws and regulations are often subject to interpretation and application in a manner that is inconsistent from one jurisdiction to another. The Company cannot assure that its practices have complied, are currently complying, or will comply fully and adequately with all such laws and regulations. Any failure to comply with any of these laws or regulations could result in damage to the Company’s reputation or a loss or reduction of orders. If the Company does fully comply with such laws and regulations, its customers could immediately see a significant increase in the total order cost of the Company’s products as such taxes are imposed, which will make the pricing of the Company’s products less competitive. Compliance with such laws and regulations will require a significant investment and continuing costs, as well as efforts of the Company’s key management personnel. Also, the Company at any time could be subjected to examinations by any of the jurisdictions into which the Company may have at one time or another shipped its products, which could result in the assessment upon the Company of a significant accumulation of uncollected taxes, along with penalties and interest. The occurrence of any of these events could adversely affect the Company’s financial position and operating results.

A stockholder could lose all or a portion of his or her investment in the Company.

The Company’s common stock has historically experienced a degree of price variability, and the price could be subject to rapid and substantial fluctuations. The Company’s common stock has also historically been thinly traded, a circumstance that exists when there is a relatively small volume of buy and sell orders for the Company’s common stock at any given point in time. In such situations, a stockholder may be unable to liquidate his or her position in the Company’s common stock at the desired price. Also, as an equity investment, a stockholder’s investment in the Company is subordinate to the interests of the Company’s creditors, and a stockholder could lose all or a substantial portion of his or her investment in the Company in the event of a voluntary or involuntary bankruptcy filing or liquidation.

ITEM 1B. Unresolved Staff Comments

None.

The Company's headquarters are located in Gonzales, Louisiana. The Company rents 17,761 square feet at this location under a lease that expires January 31, 2021. Management believes that its properties are suitable for the purposes for which they are used, are in generally good condition and provide adequate capacity for current and anticipated future operations. The table below sets forth certain information regarding the Company's principal real property as of May 10, 2018.

|

Location |

Use |

Approximate Square Feet |

Owned/ Leased |

|

Gonzales, Louisiana |

Administrative and sales office |

17,761 |

Leased |

|

Compton, California |

Offices, warehouse and distribution center |

157,400 |

Leased |

|

Douglasville, Georgia |

Offices, manufacturing and warehouse |

23,800 |

Leased |

|

Grand Rapids, Michigan |

Product design offices |

3,600 |

Leased |

|

Bentonville, Arkansas |

Sales office |

1,376 |

Leased |

|

Shanghai, People’s Republic of China |

Office |

1,912 |

Leased |

The Company is, from time to time, involved in various legal proceedings relating to claims arising in the ordinary course of its business. Neither the Company nor any of its subsidiaries is a party to any such legal proceeding the outcome of which, individually or in the aggregate, is expected to have a material adverse effect on the Company’s financial position, results of operations or cash flows.

ITEM 4. Mine Safety Disclosures

Not applicable.

ITEM 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Description of Securities

The Company is authorized to issue up to 40,000,000 shares of capital stock, all of which are classified as common stock with a par value of $0.01 per share. On May 10, 2018, there were 12,493,789 shares of the Company’s common stock issued, 10,069,558 of which were outstanding.

Market Information and Price

The Company's common stock is traded on the NASDAQ Capital Market under the symbol “CRWS”. On May 10, 2018, the closing price of the Company’s common stock was $5.85 per share. The table below sets forth the high and low closing price per share of the Company's common stock and the cash dividends per share declared on the Company’s common stock during each quarter of fiscal years 2018 and 2017.

|

|

Closing Price |

Cash Dividends |

||||||||||

|

Quarter |

High | Low | Declared | |||||||||

| Fiscal Year 2018 | ||||||||||||

|

First Quarter |

$ | 8.10 | $ | 6.70 | $ | 0.08 | ||||||

|

Second Quarter |

7.15 | 5.40 | 0.08 | |||||||||

|

Third Quarter |

6.64 | 5.75 | 0.08 | |||||||||

|

Fourth Quarter |

7.45 | 5.90 | 0.08 | |||||||||

|

Fiscal Year 2017 |

||||||||||||

|

First Quarter |

$ | 9.80 | $ | 9.11 | $ | 0.08 | ||||||

|

Second Quarter |

10.20 | 9.66 | 0.08 | |||||||||

|

Third Quarter |

10.24 | 7.60 | 0.48 | |||||||||

|

Fourth Quarter |

8.65 | 7.25 | 0.08 | |||||||||

Holders of Common Stock

As of May 10, 2018, there were approximately 170 registered holders of the Company’s common stock.

Dividends

The Company’s credit facility permits the Company to pay cash dividends on its common stock without limitation, provided there is no default under the credit facility before or as a result of the payment of such dividends.

Securities Authorized for Issuance under Equity Compensation Plans

Refer to “Securities Authorized for Issuance under Equity Compensation Plans” in Item 12. of Part III of this Annual Report on Form 10-K.

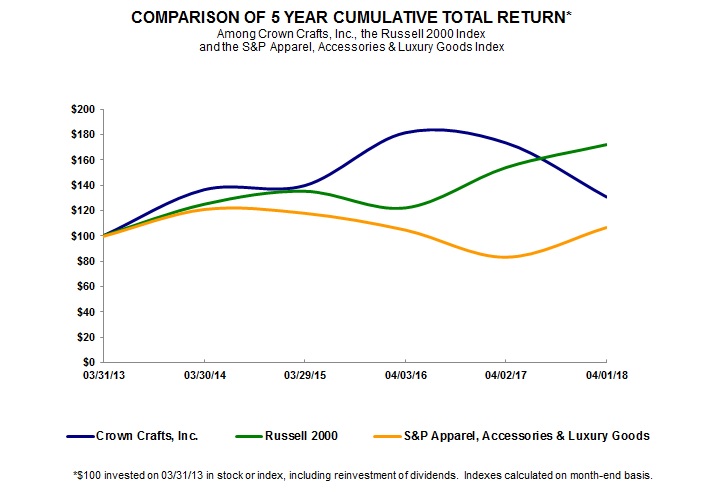

Performance Graph

The following graph (the “Performance Graph”) compares the Company’s cumulative total stockholder return on its common stock for the five-year period ended April 1, 2018 with the cumulative total returns of the Russell 2000 Index and the S&P Apparel, Accessories & Luxury Goods Index for the same period. The Performance Graph tracks the performance of separate $100 investments in the Company’s common stock and the indices on March 31, 2013 through April 1, 2018, with the reinvestment of all dividends.

|

03/31/13 |

03/30/14 |

03/29/15 |

04/03/16 |

04/02/17 |

04/01/18 |

|||||||||||||||||||

|

Crown Crafts, Inc. |

100.00 | 136.37 | 139.66 | 181.51 | 173.47 | 130.62 | ||||||||||||||||||

|

Russell 2000 Index |

100.00 | 124.90 | 135.15 | 121.96 | 153.94 | 172.09 | ||||||||||||||||||

|

S&P Apparel, Accessories & Luxury Goods Index |

100.00 | 121.26 | 118.19 | 104.93 | 83.37 | 106.94 | ||||||||||||||||||

The comparisons in the Performance Graph are based on historical data and are not indicative of, or intended to forecast, the future performance of the Company’s common stock. The Performance Graph will not be deemed to be incorporated by reference into any filing under the Securities Act or the Exchange Act, except to the extent that the Company specifically incorporates the Performance Graph by reference. In addition, the Performance graph will not be deemed to be soliciting material or to be filed with the SEC or subject to Regulation 14A or 14C, other than as provided in Regulation S-K, or to the liabilities of Section 18 of the Exchange Act, except to the extent that the Company specifically requests that the Performance Graph be treated as soliciting material or specifically incorporates it by reference into a filing under the Securities Act or the Exchange Act.

ITEM 6. Selected Financial Data

The information set forth below is not necessarily indicative of the Company’s future financial position or operating results and should be read in conjunction with Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and notes thereto included in this Annual Report on Form 10-K.

|

Fiscal Years |

||||||||||||||||||||

|

2018 |

2017 |

2016 |

2015 |

2014 |

||||||||||||||||

|

|

(amounts in thousands, except per share amounts) |

|||||||||||||||||||

| Operating results: | ||||||||||||||||||||

|

Net sales |

$ | 70,270 | $ | 65,978 | $ | 84,342 | $ | 85,978 | $ | 81,294 | ||||||||||

|

Gross profit |

19,779 | 19,411 | 23,813 | 23,550 | 22,534 | |||||||||||||||

|

Gross profit percentage |

28.1 | % | 29.4 | % | 28.2 | % | 27.4 | % | 27.7 | % | ||||||||||

|

Income from operations |

5,507 | 8,700 | 10,788 | 9,220 | 9,378 | |||||||||||||||

|

Income before income tax expense |

5,421 | 8,796 | 10,744 | 9,160 | 9,346 | |||||||||||||||

|

Income tax expense |

2,400 | 3,224 | 3,915 | 3,442 | 3,575 | |||||||||||||||

|

Net income |

3,021 | 5,572 | 6,829 | 5,718 | 5,771 | |||||||||||||||

|

Basic earnings per share |

$ | 0.30 | $ | 0.56 | $ | 0.68 | $ | 0.57 | $ | 0.59 | ||||||||||

|

Diluted earnings per share |

$ | 0.30 | $ | 0.55 | $ | 0.68 | $ | 0.57 | $ | 0.59 | ||||||||||

|

Cash dividends declared per share |

$ | 0.32 | $ | 0.72 | $ | 0.57 | $ | 0.32 | $ | 0.32 | ||||||||||

|

Financial position at year-end: |

||||||||||||||||||||

|

Cash and cash equivalents |

$ | 215 | $ | 7,892 | $ | 7,574 | $ | 1,807 | $ | 560 | ||||||||||

|

Accounts receivable, net of allowances |

18,498 | 15,614 | 20,796 | 22,370 | 21,712 | |||||||||||||||

|

Inventories |

19,788 | 15,821 | 14,785 | 15,468 | 13,607 | |||||||||||||||

|

Total current assets |

39,754 | 41,110 | 45,732 | 42,519 | 38,069 | |||||||||||||||

|

Finite-lived intangible assets - net |

7,272 | 3,128 | 3,882 | 4,507 | 5,248 | |||||||||||||||

|

Goodwill |

7,125 | 1,126 | 1,126 | 1,126 | 1,126 | |||||||||||||||

|

Total assets |

56,581 | 47,184 | 52,415 | 49,946 | 46,215 | |||||||||||||||

|

Total current liabilities |

6,788 | 7,573 | 12,185 | 10,374 | 10,298 | |||||||||||||||

|

Long-term debt |

9,458 | - | - | - | - | |||||||||||||||

|

Shareholders’ equity |

39,318 | 38,923 | 40,019 | 39,572 | 35,917 | |||||||||||||||

|

Total liabilities and shareholders’ equity |

$ | 56,581 | $ | 47,184 | $ | 52,415 | $ | 49,946 | $ | 46,215 | ||||||||||

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion is intended to provide information concerning certain factors that management considers important in reviewing the Company’s results of operations, financial position, liquidity and capital resources. This discussion should be read in conjunction with the consolidated financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K.

Results of Operations

The following table contains results of operations for fiscal years 2018, 2017 and 2016 and the dollar and percentage changes for those periods (in thousands, except percentages).

|

2017 to 2018 Change |

2016 to 2017 Change |

|||||||||||||||||||||||||||

|

2018 |

$ |

% |

2017 |

$ |

% |

2016 |

||||||||||||||||||||||

|

Net sales by category: |

||||||||||||||||||||||||||||

|

Bedding, blankets and accessories |

$ | 43,486 | $ | 1,105 | 2.6 | % | $ | 42,381 | $ | (16,639 | ) | -28.2 | % | $ | 59,020 | |||||||||||||

|

Bibs, bath, developmental toy, feeding, baby care and disposable products |

26,784 | 3,187 | 13.5 | % | 23,597 | (1,725 | ) | -6.8 | % | 25,322 | ||||||||||||||||||

|

Total net sales |

70,270 | 4,292 | 6.5 | % | 65,978 | (18,364 | ) | -21.8 | % | 84,342 | ||||||||||||||||||

|

Cost of products sold |

50,491 | 3,924 | 8.4 | % | 46,567 | (13,962 | ) | -23.1 | % | 60,529 | ||||||||||||||||||

|

Gross profit |

19,779 | 368 | 1.9 | % | 19,411 | (4,402 | ) | -18.5 | % | 23,813 | ||||||||||||||||||

|

% of net sales |

28.1 | % | 29.4 | % | 28.2 | % | ||||||||||||||||||||||

|

Marketing and administrative expenses |

14,272 | 3,561 | 33.2 | % | 10,711 | (2,314 | ) | -17.8 | % | 13,025 | ||||||||||||||||||

|

% of net sales |

20.3 | % | 16.2 | % | 15.4 | % | ||||||||||||||||||||||

|

Interest expense |

162 | 94 | 138.2 | % | 68 | 10 | 17.2 | % | 58 | |||||||||||||||||||

|

Other income |

76 | (88 | ) | -53.7 | % | 164 | 150 | 1071.4 | % | 14 | ||||||||||||||||||

|

Income tax expense |

2,400 | (824 | ) | -25.6 | % | 3,224 | (691 | ) | -17.7 | % | 3,915 | |||||||||||||||||

|

Net income |

3,021 | (2,551 | ) | -45.8 | % | 5,572 | (1,257 | ) | -18.4 | % | 6,829 | |||||||||||||||||

|

% of net sales |

4.3 | % | 8.4 | % | 8.1 | % | ||||||||||||||||||||||

Net Sales:

Fiscal 2018 Compared with Fiscal 2017

Sales of $70.3 million for 2018 were $4.3 million higher than 2017, an increase of 6.5%. The increase is due to sales that resulted from the Carousel Acquisition and the Sassy Acquisition, which added $5.4 million and $2.1 million of sales during fiscal 2018, respectively, and which amount was offset by a decrease of $4.3 million in sales by CCIP for the same period. A portion of the decrease resulted from reduced product shipments in the current year to a customer that experienced credit problems throughout the year. Also affecting sales is the continuing change in the infant bedding marketplace in which parents are purchasing fewer bedding sets in favor of separates, leading to a lower average price point for the Company’s infant bedding products.

Fiscal 2017 Compared with Fiscal 2016

Sales of $66.0 million for 2017 were lower than 2016, having decreased 21.8%, or $18.4 million. A portion of the sales decrease was due to a Black Friday promotion in 2016 that was not repeated in fiscal year 2017 and reduced product shipments to a customer that experienced credit problems. Additionally, due to the increased value of the U.S. Dollar relative to the Chinese Renminbi, the Company received a series of price reductions from most of its suppliers, which were partially passed along to the Company’s customers. Also affecting sales was the continuing overall sluggish retail environment, coupled with a change in the infant bedding marketplace. Specifically, on the advice of pediatricians, parents are moving more to the concept of a “naked crib”, whereby only a fitted sheet is used in a crib. Bumper pads, sheets, blankets, comforters and other loose bedding and soft objects, such as stuffed toys, wedges and positioners, are recommended to be kept out of the crib. This has resulted in parents purchasing fewer bedding sets in favor of separates and leading to a lower average price point for the Company’s infant bedding products. This trend has been partially offset by the Company’s expanded offerings of separates and infant bedroom décor.

Gross Profit:

Fiscal 2018 Compared with Fiscal 2017

Gross profit increased by $368,000 but decreased from 29.4% of net sales for 2018 to 28.1% of net sales for 2017. The increase in amount is due to higher sales that resulted from the Carousel Acquisition and the Sassy Acquisition, which was offset by a higher level of sales of closeout inventory in the current year at lower margins. Also, sales to Toys-Delaware during the current fiscal year leading up to and continuing through the bankruptcy and liquidation of Toys-Delaware resulted in a shift to a less profitable product mix and shortfalls of minimum guaranteed royalties, which contributed to the decrease in the gross profit percentage.

Fiscal 2017 Compared with Fiscal 2016

Gross profit decreased in amount by $4.4 million but increased as a percentage of net sales from 28.2% to 29.4%. The increase as a percentage of net sales can be attributed to the improved product costs from China, which were the result of favorable exchange rate fluctuations.

Marketing and Administrative Expenses:

Fiscal 2018 Compared with Fiscal 2017

Marketing and administrative expenses increased by $3.6 million for fiscal year 2018 compared with fiscal year 2017. The increase is the result of credit coverage fees of $653,000 and bad debt of $218,000 that did not occur in the prior year and that were associated with the bankruptcy and liquidation of a major retail customer. The Company also incurred higher overall costs during the current year that were associated with the Carousel Acquisition and the Sassy Acquisition, which included $347,000 and $169,000, respectively, in acquisition costs and amortization expense of $183,000 and $56,000, respectively. The current year also included an increase over the prior year of $90,000 in audit fees associated with the Company’s transition from a smaller reporting company to an accelerated filer for SEC purposes.

Fiscal 2017 Compared with Fiscal 2016

Marketing and administrative expenses for fiscal year 2017 declined by $2.3 million compared with fiscal year 2016. The decrease is primarily related to lower overall compensation costs, which declined in fiscal 2017 by $1.4 million as compared with fiscal year 2016.

Income Tax Expense:

Fiscal 2018 Compared with Fiscal 2017

The Company’s overall provision for income taxes increased to 44.3% during 2018 from 36.7% in 2017.

On December 22, 2017, the President of the United States signed into law the TCJA, which includes a provision to lower the federal corporate income tax rate to 21% effective as of January 1, 2018. As the Company’s fiscal year 2018 ended on April 1, 2018, the lower corporate income tax rate was phased in, resulting in a blended federal statutory rate of 30.75% for fiscal year 2018. The Company provides for deferred income taxes based on the difference between the financial statement and tax bases of the Company’s assets and liabilities. The Company’s net deferred income tax assets had previously been recorded based upon the enacted composite federal, state and foreign income tax rate of approximately 37.5% that would have been applied as the financial statement-tax differences began to reverse. Because these differences are now expected to reverse at a composite rate of approximately 24.5%, the Company was required to revalue its net deferred income tax assets. This revaluation resulted in a discrete charge to income tax expense of $377,000 during fiscal year 2018.

Management evaluates items of income, deductions and credits reported on the Company’s various federal and state income tax returns filed and recognizes the effect of positions taken on those income tax returns only if those positions are more likely than not to be sustained. The Company applies the provisions of accounting guidelines that require a minimum recognition threshold that a tax benefit must meet before being recognized in the financial statements. Recognized income tax positions are measured at the largest amount that has a greater than 50% likelihood of being realized. Changes in recognition or measurement are reflected in the period in which the change in judgment occurs.

During fiscal year 2016, an evaluation was made of the Company’s process regarding the calculation of the state portion of its income tax provision. This evaluation resulted in the Company taking a tax position that reflected opportunities for the application of more favorable state apportionment percentages for several prior fiscal years. After considering all relevant information, the Company believes that the technical merits of this tax position would more likely than not be sustained. However, the Company also believes that the ultimate resolution of the tax position will result in a tax benefit that is less than the full amount being sought. Therefore, the Company’s measurement regarding the tax impact of the revised state apportionment percentages resulted in the Company recording a discrete reserve for unrecognized tax benefits during fiscal year 2018 of $113,000, as compared with a reserve of $134,000 during fiscal year 2017. Because the tax impact of the revised state apportionment percentages are measured net of federal income taxes, the provision in the TCJA that lowered the federal corporate income tax rate to 21% required the Company to revalue its reserve for unrecognized tax benefits. This revaluation, which the Company believes is complete, resulted in a net discrete charge to income tax expense of $120,000 during fiscal year 2018.

Income tax expense for fiscal year 2018 included a discrete income tax charge of $37,000 and a discrete income tax benefit of $60,000 to reflect the effect of the tax shortfall and the excess tax benefits, respectively, arising from the vesting of non-vested stock, as compared with $248,000 of net excess tax benefits arising from the effect of such items during fiscal year 2017.

Fiscal 2017 Compared with Fiscal 2016

The Company’s provision for income taxes increased slightly to 36.7% during 2017 from 36.4% in 2016. The Company’s effective tax rate for 2017 was beneficially impacted by the early adoption of revised accounting guidance, which resulted in the recognition of discrete income tax benefits amounting to $248,000 to reflect the effect of net excess tax benefits arising from the exercise of stock options and the vesting of non-vested stock during fiscal year 2017. The Company recorded during 2016 discrete net income tax benefits of approximately $260,000, primarily resulting from the application of more favorable state apportionment percentages to state income tax returns for several prior fiscal years.

Known Trends and Uncertainties

The Company’s financial results are closely tied to sales to the Company’s top three customers, which represented approximately 65% of the Company’s gross sales in fiscal year 2018, including 15% of sales to Toys-Delaware. On September 18, 2017, TRU and Toys-Delaware filed petitions for relief under Chapter 11 of Title 11 of the U.S. Bankruptcy Code with the U.S. Bankruptcy Court for the Eastern District of Virginia. On March 14, 2018, TRU filed a motion with the Court seeking authority to close all of the remaining Toys-Delaware stores and distribution centers in the U.S., and to otherwise discontinue, liquidate and wind-down all U.S. operations of Toys-Delaware. The Company had ceased all shipments to Toys-Delaware shortly before the liquidation filing was made. The Company anticipates that the loss of future business with Toys-Delaware may be mitigated by a shift to the Company’s other customers.

A significant downturn experienced by either or both of the Company’s two remaining top customers could lead to pressure on the Company’s revenues. During fiscal years 2018, 2017 and 2016, the Company at times faced higher raw material costs, as well as increases in labor and transportation costs associated with the Company’s sourcing activities in China. Future increases in these costs could adversely affect the profitability of the Company if it cannot pass the cost increases along to its customers in the form of price increases or if the timing of price increases does not closely match the cost increases. For additional discussion of trends, uncertainties and other factors that could impact the Company’s operating results, refer to “Risk Factors” in Item 1A. of Part I. of this Annual Report on Form 10-K.

Financial Position, Liquidity and Capital Resources

Net cash provided by operating activities decreased from $10.4 million for the fiscal year ended April 2, 2017 to $2.5 million for the fiscal year ended April 1, 2018. In the current year, the Company experienced an increase in its accounts receivable balances that was $8.1 million higher than the decrease in the prior year.

Net cash provided by operating activities decreased from $11.0 million for the fiscal year ended April 3, 2016 to $10.4 million for the fiscal year ended April 2, 2017. In fiscal year 2017, the Company experienced a decrease in its accounts receivable balances that was $3.5 million higher than the decrease in fiscal year 2016. Offsetting this decrease was an increase in inventory in fiscal year 2018 that was $1.7 million higher than fiscal year 2016, as well as net income that was $1.3 million lower in fiscal year 2017 as compared with fiscal year 2016.

Net cash used in investing activities was $15.5 million in fiscal year 2018 compared with $191,000 in fiscal year 2017. The increase in fiscal year 2018 was due primarily to the payment of the purchase price of $8.7 million for the Carousel Acquisition and $6.5 million for the Sassy Acquisition.

Net cash used in investing activities was $191,000 in fiscal year 2017 compared with $324,000 in fiscal year 2016. The decrease in fiscal year 2017 was primarily due to $123,000 used in fiscal year 2016 to purchase certain intangible assets.

Net cash provided by financing activities was $5.3 million in fiscal year 2018 as compared with $9.9 million used in financing activities in the fiscal year 2017, for an overall swing of $15.2 million. The change was primarily associated with net borrowings on the Company’s revolving line of credit during fiscal year 2018 of $9.5 million and a decrease in dividends paid in fiscal year 2018 of $6.5 million as compared with year 2017.

Net cash used in financing activities increased by $5.0 million to $9.9 million in fiscal year 2017. The increase was primarily associated with an increase in dividends paid in fiscal year 2017 of $6.5 million as compared with fiscal year 2016. Offsetting this amount was a $1.9 million decrease in fiscal year 2017 as compared with fiscal year 2016 that were associated with the surrender to the Company’s treasury of a portion of the shares of non-vested stock that vested and from shares issued upon the exercise of options, which was in consideration of the Company remitting the income tax withholding obligations to the appropriate taxing authorities on behalf of the employees of the Company that exercised options and had non-vested stock that vested.

The Company’s future performance is, to a certain extent, subject to general economic, financial, competitive, legislative, regulatory and other factors beyond its control. Based upon the current level of operations, the Company believes that its cash flow from operations and availability on its revolving line of credit will be adequate to meet its liquidity needs.

The Company’s credit facility at April 1, 2018 consisted of a revolving line of credit under a financing agreement with The CIT Group/Commercial Services, Inc. (“CIT”), a subsidiary of CIT Group Inc., of up to $26.0 million, which includes a $1.5 million sub-limit for letters of credit, bearing interest at the rate of prime minus 0.5% or LIBOR plus 2.0%. The financing agreement matures on July 11, 2019 and is secured by a first lien on all assets of the Company. As of April 1, 2018, the Company had elected to pay interest on balances owed under the revolving line of credit under the LIBOR option, which was 3.67% as of April 1, 2018. The financing agreement also provides for the payment by CIT to the Company of interest at the rate of prime as of the beginning of the calendar month minus 2.0%, which was 2.75% as of April 1, 2018, on daily negative balances, if any, held at CIT.

The financing agreement as in effect prior to December 28, 2015 provided for a monthly fee, which was assessed based on 0.125% of the average unused portion of the revolving line of credit, less any outstanding letters of credit (the “Commitment Fee”). The Commitment Fee amounted to $25,000 during fiscal year 2016. The financing agreement was amended on December 28, 2015 to eliminate the Commitment Fee. As of April 1, 2018, there was a balance of $9.5 million owed on the revolving line of credit, there was no letter of credit outstanding and $13.2 million was available under the revolving line of credit based on the Company’s eligible accounts receivable and inventory balances. As of April 2, 2017, there was no balance owed on the revolving line of credit, there was no letter of credit outstanding and $21.4 million was available under the revolving line of credit based on the Company’s eligible accounts receivable and inventory balances.

The financing agreement contains usual and customary covenants for agreements of that type, including limitations on other indebtedness, liens, transfers of assets, investments and acquisitions, merger or consolidation transactions, transactions with affiliates, and changes in or amendments to the organizational documents for the Company and its subsidiaries. The Company believes it was in compliance with these covenants as of April 1, 2018.

To reduce its exposure to credit losses, the Company assigns the majority of its trade accounts receivable to CIT pursuant to factoring agreements, which have expiration dates that are coterminous with that of the financing agreement described above. Under the terms of the factoring agreements, CIT remits customer payments to the Company as such payments are received by CIT.

CIT bears credit losses with respect to assigned accounts receivable from approved shipments, while the Company bears the responsibility for adjustments from customers related to returns, allowances, claims and discounts. CIT may at any time terminate or limit its approval of shipments to a particular customer. If such a termination or limitation occurs, the Company either assumes (and may seek to mitigate) the credit risk for shipments to the customer after the date of such termination or limitation or discontinues shipments to the customer. Factoring fees, which are included in marketing and administrative expenses in the accompanying consolidated statements of income, were $223,000, $395,000 and $556,000 during fiscal years 2018, 2017 and 2016, respectively. There were no advances on the factoring agreements at April 1, 2018 or April 2, 2017.

Contractual Obligations

The Company’s contractual obligations as of April 1, 2018 are as follows (in thousands):

|

Payments due by period |

||||||||||||||||||||

|

|

Total |

2019 |

2020 - 2021 | 2022 - 2023 |

Thereafter |

|||||||||||||||

| Contractual Obligations | ||||||||||||||||||||

|

Purchase obligations |

$ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

|

Long-term debt - principal |

9,458 | - | 9,458 | - | - | |||||||||||||||

|

Long-term debt - estimate of interest |

230 | 180 | 50 | - | - | |||||||||||||||

|

Capital lease obligations |

- | - | - | - | - | |||||||||||||||

|

Operating lease obligations |

3,306 | 1,453 | 1,853 | - | - | |||||||||||||||

|

Minimum guaranteed royalties |

4,418 | 2,894 | 1,524 | - | - | |||||||||||||||

|

Total |

$ | 17,412 | $ | 4,527 | $ | 12,885 | $ | - | $ | - | ||||||||||

Critical Accounting Policies and Estimates

The Company prepares its financial statements to conform with accounting principles generally accepted in the U.S. (“GAAP”) as promulgated by the Financial Accounting Standards Board (“FASB”). References herein to GAAP are to topics within the FASB Accounting Standards Codification (the “FASB ASC”), which the FASB periodically revises through the issuance of an Accounting Standards Update (“ASU”) and which has been established by the FASB as the authoritative source for GAAP recognized by the FASB to be applied by nongovernmental entities.

Use of Estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated balance sheets and the reported amounts of revenues and expenses during the reporting period. The listing below, while not inclusive of all of the Company's accounting policies, sets forth those accounting policies which the Company's management believes embody the most significant judgments due to the uncertainties affecting their application and the likelihood that materially different amounts would be reported under different conditions or using different assumptions.

Revenue Recognition: Sales made directly to consumers are recorded when shipped products have been received by customers. Sales made to retailers are recorded when products are shipped to customers and are reported net of anticipated returns, which are estimated based on historical rates, and other allowances in the accompanying consolidated statements of income. Reserves for returns and other allowances, including cooperative advertising allowances, warehouse allowances, placement fees and volume rebates, are recorded commensurate with sales activity or using the straight-line method, as appropriate, and the cost of such allowances is netted against sales in reporting the results of operations. Shipping costs are included in cost of products sold.