Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 CERTIFICATION OF OUR CFO PURSUANT TO SECTION 906 - Keurig Dr Pepper Inc. | dps-ex322_20180331.htm |

| EX-32.1 - EXHIBIT 32.1 CERTIFICATION OF OUR CEO PURSUANT TO SECTION 906 - Keurig Dr Pepper Inc. | dps-ex321_20180331.htm |

| EX-31.2 - EXHIBIT 31.2 CERTIFICATION OF OUR CFO PURSUANT TO SECTION 302 - Keurig Dr Pepper Inc. | dps-ex312_20180331.htm |

| EX-31.1 - EXHIBIT 31.1 CERTIFICATION OF OUR CEO PURSUANT TO SECTION 302 - Keurig Dr Pepper Inc. | dps-ex311_20180331.htm |

| EX-12.1 - EXHIBIT 12.1 COMPUTATION OF RATIO OF EARNINGS TO FIXED CHARGES - Keurig Dr Pepper Inc. | dps-ex121_20180331.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED March 31, 2018

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-33829

Delaware | 98-0517725 | |

(State or other jurisdiction of | (I.R.S. employer | |

incorporation or organization) | identification number) | |

5301 Legacy Drive, Plano, Texas | 75024 | |

(Address of principal executive offices) | (Zip code) | |

(972) 673-7000

(Registrant's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer", "accelerated filer", "smaller reporting company", and "emerging growth company" in Rule 12b-2 of the Securities Exchange Act of 1934.

Large Accelerated Filer x | Accelerated Filer o | Non-Accelerated Filer o | Smaller Reporting Company o | Emerging Growth Company o | ||||

(Do not check if a smaller reporting company) | ||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes o No x

As of April 23, 2018, there were 180,221,324 shares of the registrant's common stock, par value $0.01 per share, outstanding.

DR PEPPER SNAPPLE GROUP, INC.

FORM 10-Q

INDEX

Page | ||||

ii

PART I - FINANCIAL INFORMATION

ITEM 1. | Financial Statements (Unaudited) |

DR PEPPER SNAPPLE GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

For the Three Months Ended March 31, 2018 and 2017

(Unaudited)

For the Three Months Ended | ||||||||

March 31, | ||||||||

(in millions, except per share data) | 2018 | 2017 | ||||||

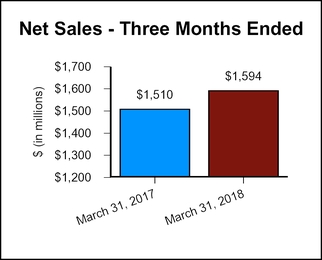

Net sales | $ | 1,594 | $ | 1,510 | ||||

Cost of sales | 681 | 607 | ||||||

Gross profit | 913 | 903 | ||||||

Selling, general and administrative expenses | 626 | 620 | ||||||

Depreciation and amortization | 27 | 25 | ||||||

Other operating expense (income), net | 1 | (28 | ) | |||||

Income from operations | 259 | 286 | ||||||

Interest expense | 41 | 40 | ||||||

Interest income | (1 | ) | (1 | ) | ||||

Other income, net | — | (1 | ) | |||||

Income before provision for income taxes and equity in loss of unconsolidated subsidiaries | 219 | 248 | ||||||

Provision for income taxes | 54 | 71 | ||||||

Income before equity in loss of unconsolidated subsidiaries | 165 | 177 | ||||||

Equity in loss of unconsolidated subsidiaries, net of tax | (6 | ) | — | |||||

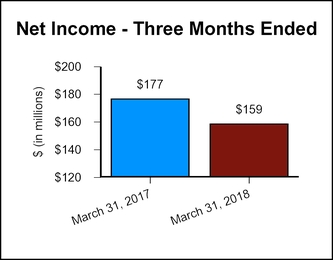

Net income | $ | 159 | $ | 177 | ||||

Earnings per common share: | ||||||||

Basic | $ | 0.88 | $ | 0.97 | ||||

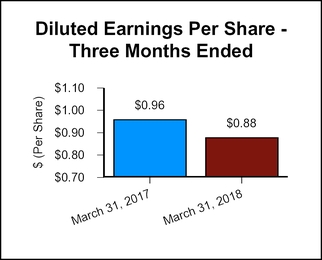

Diluted | 0.88 | 0.96 | ||||||

Weighted average common shares outstanding: | ||||||||

Basic | 179.9 | 183.4 | ||||||

Diluted | 180.8 | 184.6 | ||||||

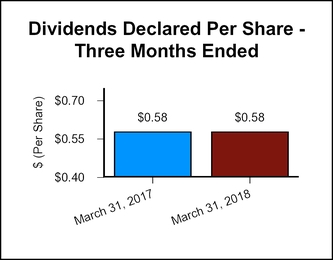

Cash dividends declared per common share | $ | 0.58 | $ | 0.58 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

1

DR PEPPER SNAPPLE GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

For the Three Months Ended March 31, 2018 and 2017

(Unaudited)

For the Three Months Ended March 31, | |||||||

(in millions) | 2018 | 2017 | |||||

Comprehensive income | $ | 178 | $ | 200 | |||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

2

DR PEPPER SNAPPLE GROUP, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

As of March 31, 2018 and December 31, 2017

(Unaudited)

March 31, | December 31, | ||||||

(in millions, except share and per share data) | 2018 | 2017 | |||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 13 | $ | 61 | |||

Restricted cash and restricted cash equivalents | 16 | 18 | |||||

Accounts receivable: | |||||||

Trade, net | 700 | 668 | |||||

Other | 49 | 42 | |||||

Inventories | 243 | 229 | |||||

Prepaid expenses and other current assets | 225 | 99 | |||||

Total current assets | 1,246 | 1,117 | |||||

Property, plant and equipment, net | 1,198 | 1,198 | |||||

Investments in unconsolidated subsidiaries | 36 | 24 | |||||

Goodwill | 3,564 | 3,561 | |||||

Other intangible assets, net | 3,784 | 3,781 | |||||

Other non-current assets | 286 | 279 | |||||

Deferred tax assets | 65 | 62 | |||||

Total assets | $ | 10,179 | $ | 10,022 | |||

Liabilities and Stockholders' Equity | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 377 | $ | 365 | |||

Deferred revenue | 64 | 64 | |||||

Short-term borrowings and current portion of long-term obligations | 383 | 79 | |||||

Income taxes payable | 39 | 11 | |||||

Other current liabilities | 761 | 719 | |||||

Total current liabilities | 1,624 | 1,238 | |||||

Long-term obligations | 4,135 | 4,400 | |||||

Deferred tax liabilities | 623 | 614 | |||||

Non-current deferred revenue | 1,038 | 1,055 | |||||

Other non-current liabilities | 273 | 264 | |||||

Total liabilities | 7,693 | 7,571 | |||||

Commitments and contingencies | |||||||

Stockholders' equity: | |||||||

Preferred stock, $0.01 par value, 15,000,000 shares authorized, no shares issued | — | — | |||||

Common stock, $0.01 par value, 800,000,000 shares authorized, 180,218,713 and 179,743,028 shares issued and outstanding as of March 31, 2018 and December 31, 2017, respectively | 2 | 2 | |||||

Additional paid-in capital | — | — | |||||

Retained earnings | 2,667 | 2,651 | |||||

Accumulated other comprehensive loss | (183 | ) | (202 | ) | |||

Total stockholders' equity | 2,486 | 2,451 | |||||

Total liabilities and stockholders' equity | $ | 10,179 | $ | 10,022 | |||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

DR PEPPER SNAPPLE GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

For the Three Months Ended March 31, 2018 and 2017

(Unaudited)

For the Three Months Ended | |||||||

March 31, | |||||||

(in millions) | 2018 | 2017 | |||||

Operating activities: | |||||||

Net income | $ | 159 | $ | 177 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation expense | 50 | 49 | |||||

Amortization expense | 9 | 11 | |||||

Amortization of deferred revenue | (16 | ) | (16 | ) | |||

Employee stock-based compensation expense | 10 | 6 | |||||

Deferred income taxes | 20 | 30 | |||||

Gain on step acquisition of unconsolidated subsidiaries | — | (28 | ) | ||||

Unrealized gains on economic hedges | 11 | (5 | ) | ||||

Other, net | 9 | 4 | |||||

Changes in assets and liabilities, net of effects of acquisition: | |||||||

Trade accounts receivable | (30 | ) | 18 | ||||

Other accounts receivable | (7 | ) | 5 | ||||

Inventories | (13 | ) | (16 | ) | |||

Other current and non-current assets | (139 | ) | (85 | ) | |||

Other current and non-current liabilities | (4 | ) | (92 | ) | |||

Trade accounts payable | 17 | 19 | |||||

Income taxes payable | 27 | 20 | |||||

Net cash provided by operating activities | 103 | 97 | |||||

Investing activities: | |||||||

Acquisition of business | (2 | ) | (1,548 | ) | |||

Cash acquired in step acquisition of unconsolidated subsidiaries | — | 3 | |||||

Purchase of property, plant and equipment | (41 | ) | (16 | ) | |||

Purchase of intangible assets | (3 | ) | (1 | ) | |||

Investment in unconsolidated subsidiaries | (19 | ) | (1 | ) | |||

Proceeds from disposals of property, plant and equipment | 1 | 1 | |||||

Other, net | (4 | ) | (7 | ) | |||

Net cash used in investing activities | (68 | ) | (1,569 | ) | |||

Financing activities: | |||||||

Net issuance of commercial paper | 54 | — | |||||

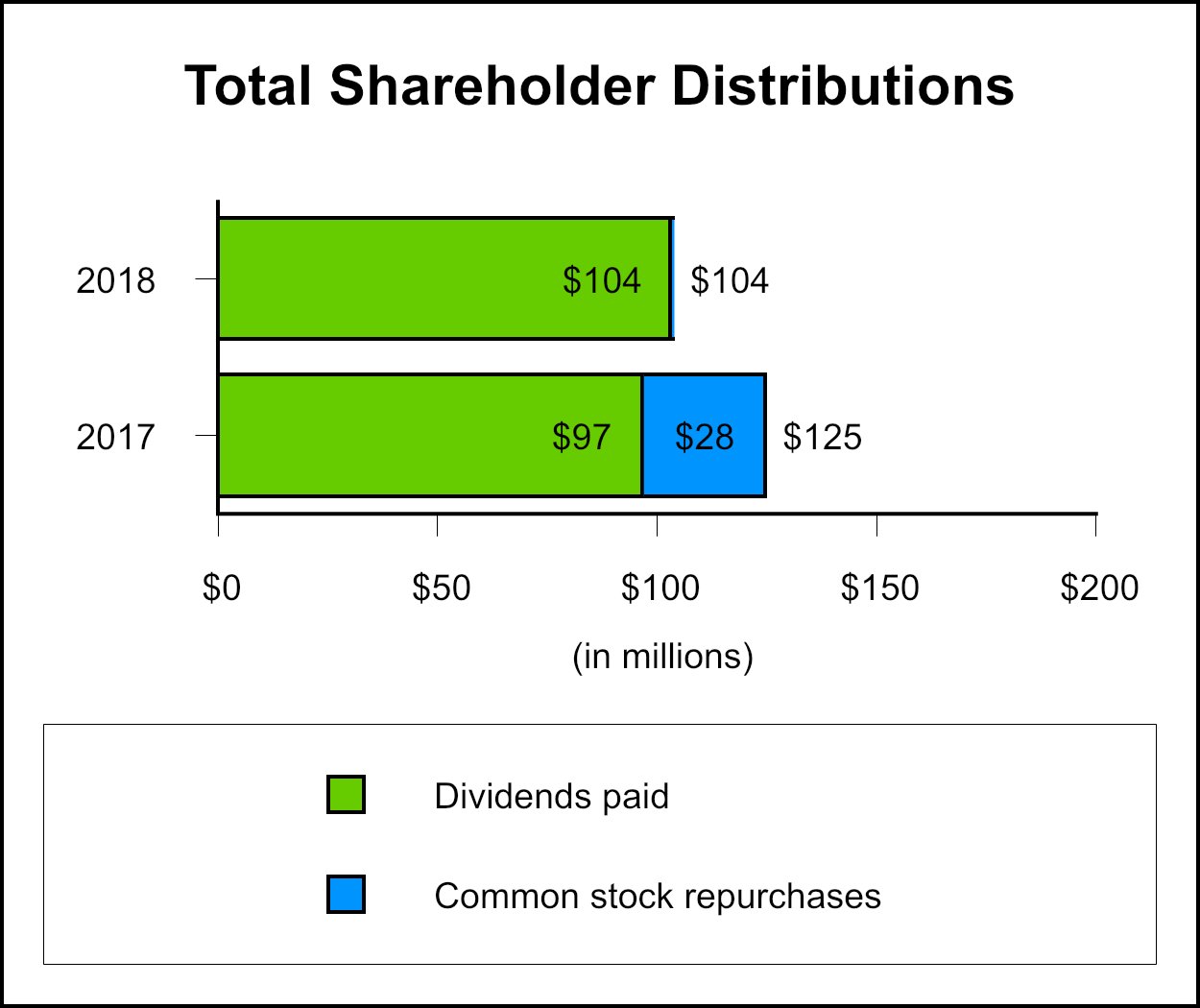

Repurchase of shares of common stock | — | (28 | ) | ||||

Dividends paid | (104 | ) | (97 | ) | |||

Tax withholdings related to net share settlements of certain stock awards | (21 | ) | (30 | ) | |||

Proceeds from stock options exercised | 2 | 17 | |||||

Deferred financing charges paid | — | (1 | ) | ||||

Capital lease payments | (4 | ) | (3 | ) | |||

Net cash used in financing activities | (73 | ) | (142 | ) | |||

Cash, cash equivalents, restricted cash and restricted cash equivalents — net change from: | |||||||

Operating, investing and financing activities | (38 | ) | (1,614 | ) | |||

Effect of exchange rate changes on cash, cash equivalents, restricted cash and restricted cash equivalents | 1 | 3 | |||||

Cash, cash equivalents, restricted cash and restricted cash equivalents at beginning of period | 158 | 1,787 | |||||

Cash, cash equivalents, restricted cash and restricted cash equivalents at end of period | $ | 121 | $ | 176 | |||

See Note 13 for supplemental cash flow information.

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

DR PEPPER SNAPPLE GROUP, INC.

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITY

For the Three Months Ended March 31, 2018

(Unaudited)

Accumulated | ||||||||||||||||||||||

Common Stock | Additional | Other | ||||||||||||||||||||

Issued | Paid-In | Retained | Comprehensive | Total | ||||||||||||||||||

(in millions, except per share data) | Shares | Amount | Capital | Earnings | Loss | Equity | ||||||||||||||||

Balance as of January 1, 2018 | 179.7 | $ | 2 | $ | — | $ | 2,651 | $ | (202 | ) | $ | 2,451 | ||||||||||

Adoption of new accounting standards | — | — | — | (31 | ) | — | (31 | ) | ||||||||||||||

Shares issued under employee stock-based compensation plans and other | 0.5 | — | — | — | — | — | ||||||||||||||||

Net income | — | — | — | 159 | — | 159 | ||||||||||||||||

Other comprehensive income | — | — | — | — | 19 | 19 | ||||||||||||||||

Dividends declared, $0.58 per share | — | — | 1 | (106 | ) | — | (105 | ) | ||||||||||||||

Deemed capital contribution from former shareholders of Bai Brands LLC | — | — | 2 | — | — | 2 | ||||||||||||||||

Stock options exercised and stock-based compensation | — | — | (3 | ) | (6 | ) | — | (9 | ) | |||||||||||||

Balance as of March 31, 2018 | 180.2 | $ | 2 | $ | — | $ | 2,667 | $ | (183 | ) | $ | 2,486 | ||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

5

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. | General |

References in this Quarterly Report on Form 10-Q to "DPS" or "the Company" refer to Dr Pepper Snapple Group, Inc. and all entities included in the unaudited condensed consolidated financial statements.

This Quarterly Report on Form 10-Q refers to some of DPS' owned or licensed trademarks, trade names and service marks, which are referred to as the Company's brands. All of the product names included herein are either DPS' registered trademarks or those of the Company's licensors.

BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("U.S. GAAP") for interim financial information and in accordance with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by U.S. GAAP for complete consolidated financial statements. In the opinion of management, all adjustments, consisting principally of normal recurring adjustments, considered necessary for a fair presentation have been included. These unaudited condensed consolidated financial statements should be read in conjunction with the Company's audited consolidated financial statements and the notes thereto in the Company's Annual Report on Form 10-K for the year ended December 31, 2017 ("Annual Report").

PRINCIPLES OF CONSOLIDATION

DPS consolidates all wholly owned subsidiaries. The Company uses the equity method to account for investments in companies if the investment provides the Company with the ability to exercise significant influence over operating and financial policies of the investee. Consolidated net income includes DPS' proportionate share of the net income or loss of these companies. Judgment regarding the level of influence over each equity method investment includes considering key factors such as ownership interest, representation on the board of directors or similar governing body, participation in policy-making decisions and material intercompany transactions.

The Company is also required to consolidate entities that are variable interest entities (“VIEs”) of which DPS is the primary beneficiary. Judgments are made in assessing whether the Company is the primary beneficiary, including determination of the activities that most significantly impact the VIE’s economic performance.

The Company eliminates from its financial results all intercompany transactions between entities included in the unaudited condensed consolidated financial statements and the intercompany transactions with its equity method investees.

USE OF ESTIMATES

The process of preparing DPS' unaudited condensed consolidated financial statements in conformity with U.S. GAAP requires the use of estimates and judgments that affect the reported amount of assets, liabilities, revenue and expenses. These estimates and judgments are based on historical experience, future expectations and other factors and assumptions the Company believes to be reasonable under the circumstances. These estimates and judgments are reviewed on an ongoing basis and are revised when necessary. Changes in estimates are recorded in the period of change. Actual amounts may differ from these estimates.

FAIR VALUE

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Based upon the transparency of inputs to the valuation of an asset or liability, a three-level hierarchy has been established for fair value measurements. The three-level hierarchy for disclosure of fair value measurements is as follows:

Level 1 - Quoted market prices in active markets for identical assets or liabilities.

Level 2 - Observable inputs such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical or similar assets or liabilities in markets that are not active; and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets.

Level 3 - Valuations with one or more unobservable significant inputs that reflect the reporting entity's own assumptions.

The fair value of senior unsecured notes and marketable securities as of March 31, 2018 and December 31, 2017 are based on quoted market prices for publicly traded securities.

6

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

The Company estimates fair values of financial instruments measured at fair value in the financial statements on a recurring basis to ensure they are calculated based on market rates to settle the instruments. These values represent the estimated amounts DPS would pay or receive to terminate agreements, taking into consideration current market rates and creditworthiness.

As of March 31, 2018 and December 31, 2017, the Company did not have any assets or liabilities measured on a recurring basis without observable market values that would require a high level of judgment to determine fair value (Level 3).

Transfers between levels are recognized at the end of each reporting period. There were no transfers of financial instruments between the three levels of fair value hierarchy during the three months ended March 31, 2018 and 2017.

Refer to Notes 6, 7, 12 and 13 for additional information.

RECLASSIFICATIONS

Pension and other post-retirement benefit plan expenses of $1 million were reclassified from selling, general & administrative ("SG&A") expenses to other income, net, for the three months ended March 31, 2017, as a result of the retrospective adoption of Accounting Standard Update ("ASU") 2017-07, Compensation - Retirement Benefits (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost ("ASU 2017-07"). Refer to Recently Adopted Provisions of U.S. GAAP below.

RECENTLY ISSUED ACCOUNTING STANDARDS

Effective in 2019

In February 2016, the Financial Accounting Standards Board ("FASB") issued ASU 2016-02, Leases (Topic 842) ("ASU 2016-02"). The ASU replaces the prior lease accounting guidance in its entirety. The underlying principle of the new standard is the recognition of lease assets and lease liabilities by lessees for substantially all leases, with an exception for leases with terms of less than twelve months. The standard also requires additional quantitative and qualitative disclosures. In January 2018, the FASB issued ASU 2018-01, Leases (Topic 842) - Land Easement Practical Expedient for Transition to Topic 842, which provides an optional transition practical expedient that allows companies to not evaluate (under Topic 842) existing or expired land easements that were not previously accounted for as leases (under Topic 840).

Topic 842 is effective for interim and annual reporting periods beginning after December 15, 2018, and early adoption is permitted. Topic 842 requires a modified retrospective approach, which includes several optional practical expedients. The Company intends to adopt the standard during the quarter ending March 31, 2019. The Company has assembled a cross functional project management team, selected a software provider and has begun the implementation of the software. The Company anticipates the impact of Topic 842 will be significant to its Consolidated Balance Sheet due to the amount of the Company's lease commitments.

In August 2017, the FASB issued ASU 2017-12, Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities ("ASU 2017-12"). The objective of the ASU is to improve the financial reporting of hedging relationships in order to better portray the economic results of an entity’s risk management activities in its financial statements and to make certain targeted improvements to simplify the application of hedge accounting guidance. ASU 2017-12 is effective for interim and annual reporting periods beginning after December 15, 2018, and early adoption is permitted. The Company is currently evaluating the impact of ASU 2017-12 on the Company's consolidated financial statements.

In February 2018, the FASB issued ASU 2018-02, Income Statement - Reporting Comprehensive Income (Topic 220) ("ASU 2018-02"). The objective of the ASU is to allow a reclassification from accumulated comprehensive income (loss) to retained earnings for stranded tax effects resulting from the Tax Cuts and Jobs Act ("TCJA") and will improve the usefulness of information reported to financial statement users. ASU 2018-02 is effective for interim and annual reporting periods beginning after December 15, 2018, and early adoption is permitted. The Company is currently evaluating the impact of ASU 2018-02 on the Company's consolidated financial statements.

7

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

RECENTLY ADOPTED PROVISIONS OF U.S. GAAP

As of January 1, 2018, the Company adopted Revenue from Contracts with Customers (Topic 606) ("ASC 606"). The new guidance sets forth a new five-step revenue recognition model which replaces the prior revenue recognition guidance in its entirety and is intended to eliminate numerous industry-specific pieces of revenue recognition guidance that have historically existed in U.S. GAAP. The underlying principle of the new standard is that a business or other organization will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects what it expects to receive in exchange for the goods or services. The standard also requires more detailed disclosures and provides additional guidance for transactions that were not addressed completely in the prior accounting guidance. The Company adopted the standard using the modified retrospective method and recognized the cumulative effect of initially applying the standard, which was primarily driven by the acceleration of certain customer incentives, as a $35 million reduction to the opening balance of retained earnings. The Company expects that the impact to net income of the new standard will be immaterial on an ongoing annual basis; however, the Company does anticipate that the new standard will have an impact on its net sales in interim periods due to timing. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. Refer to Note 3 for additional information regarding the Company's adoption of ASC 606.

As of January 1, 2018, the Company adopted ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other than Inventory ("ASU 2016-16"). ASU 2016-16 requires entities to recognize the income tax consequences of intra-entity transfers of assets other than inventories when such transfers occur. The ASU was adopted on a modified retrospective basis through a cumulative-effect adjustment, which resulted in an increase to the opening balance of retained earnings of approximately $4 million as of January 1, 2018.

As a result of the adoption of ASC 606 and ASU 2016-16, retained earnings decreased approximately $31 million as of January 1, 2018.

As of January 1, 2018, the Company adopted ASU 2017-07, which requires employers who offer defined benefit pension plans or other post-retirement benefit plans to report the service cost component within the same income statement caption as other compensation costs arising from services rendered by employees during the period. The ASU also requires the other components of net periodic benefit cost to be presented separately from the service cost component, in a caption outside of a subtotal of income from operations. Additionally, the ASU provides that only the service cost component is eligible for capitalization. As a result of the adoption, the Company reclassified $1 million from selling, general and administrative expenses to other non-operating expense, net for the three months ended March 31, 2017.

As of January 1, 2018, the Company adopted ASU 2016-01, Financial Instruments - Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities ("ASU 2016-01"), which makes several targeted improvements to U.S. GAAP. Among other things, ASU 2016-01 eliminates the cost method of accounting and investments in equity securities which were previously accounted for under the cost method must now be measured at fair value, with changes in fair value recognized in net income, under guidance in the newly added Topic 321, Investments - Equity Securities, to the Accounting Standards Codification. Equity instruments that do not have readily determinable fair values may be measured at cost less impairment, plus or minus changes resulting from observable price changes in orderly transactions for identical or similar investments of the same issuer. The Company also adopted ASU 2018-03, Technical Corrections and Improvements to Financial Instruments—Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities, which provides clarification on certain guidance issued under ASU 2016-01. The Company holds two investments in equity securities which were accounted for under the cost method of accounting prior to January 1, 2018, which do not have readily determinable fair values. The adoption of these standards did not have a material impact on such investments or the Company's consolidated financial statements.

2. Acquisitions and Investments in Unconsolidated Subsidiaries

ANNOUNCEMENT OF PROPOSED MERGER WITH MAPLE PARENT HOLDINGS CORP.

On January 29, 2018, DPS entered into an Agreement and Plan of Merger (the "Merger Agreement") by and among DPS, Maple Parent Holdings Corp. (“Maple”) and Salt Merger Sub, Inc., a wholly-owned subsidiary of DPS (“Merger Sub”), whereby Merger Sub will be merged with and into Maple, with Maple surviving the merger as a wholly-owned subsidiary of the Company (the “Maple Merger”). For financial reporting and accounting purposes, Maple will be the acquirer of DPS upon completion of the Maple Merger.

Maple is the indirect parent of Keurig Green Mountain, Inc. ("Keurig"), through which Maple conducts all of its operations. Keurig is a leading producer of specialty coffee and innovative single serve brewing systems. The combined businesses will create Keurig Dr Pepper Inc., a new beverage company of scale with a portfolio of iconic consumer brands and expanded distribution capability to reach virtually every point-of-sale in North America.

8

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

In consideration for the Maple Merger, each share of common stock of Maple issued and outstanding immediately prior to the closing of the Maple Merger (the “Effective Time”) shall be converted into the right to receive a number of fully paid and nonassessable shares of common stock of DPS determined pursuant to an exchange ratio set forth in the Merger Agreement (the “Acquisition Shares”).

The Merger Agreement provides that DPS will declare a special cash dividend equal to $103.75 per share, subject to any withholding of taxes required by law, payable to holders of its common stock as of the record date for the special dividend, which shall be the business day immediately prior to the completion of the Maple Merger (such special dividend, together with the Maple Merger, the "Maple Transaction").

As a result of the Maple Transaction, the equityholders of Maple as of immediately prior to the Effective Time will own approximately 87% of DPS' common stock following the closing and the stockholders of DPS as of immediately prior to the Effective Time will own approximately 13% on a fully diluted basis.

The completion of the Maple Transaction requires the approval of the holders of DPS' common stock of (i) an amendment to DPS’ certificate of incorporation to increase the number of authorized shares of common stock and to change DPS' name to "Keurig Dr Pepper Inc." and (ii) the issuance of the Acquisition Shares pursuant to the Merger Agreement (collectively, the "Stockholder Approvals").

In addition to the Stockholder Approvals, the completion of the Maple Transaction will depend upon a number of conditions being satisfied or waived, including, among others, obtaining all required regulatory approvals, authorization of the listing on the New York Stock Exchange of the Acquisition Shares, the absence of any injunction prohibiting the consummation of the Maple Transaction and absence of any legal requirements enacted by any court or other governmental entity since the date of the Merger Agreement that remain in effect prohibiting consummation of the Maple Transaction. The obligation of each party to consummate the Maple Transaction is also conditioned on the other party’s representations and warranties being true and correct (subject to certain materiality exceptions) and the other party having performed in all material respects its obligations under the Merger Agreement.

The Merger Agreement may be terminated at any time prior to the Effective Time, whether before or after receipt of the Stockholder Approvals or the effectiveness of the Maple stockholder consent or Merger Sub stockholder consent, by the mutual written consent of the parties, by either Maple or DPS if the closing of the Maple Transaction does not occur by October 29, 2018 or the Stockholder Approvals are not obtained or a final and nonappealable government order prohibiting the closing of the Maple Transaction is in place, or by Maple or DPS in connection with certain breaches of the Merger Agreement by DPS or Maple, respectively.

If the Merger Agreement is terminated by DPS as a result of DPS accepting a superior proposal and entering into an alternative acquisition agreement, by Maple if our Board changes its recommendation to stockholders to approve the Stockholder Approvals or fails to reaffirm such recommendation following receipt or public announcement of a competing acquisition proposal within five business days after Maple's request to do so, or by either DPS or Maple because the closing does not occur by October 29, 2018 and there is an acquisition proposal outstanding at the time of such termination and within twelve months of termination of the Merger Agreement DPS consummates or enters into an agreement with respect to an acquisition proposal, DPS shall pay to Maple a termination fee in the amount of $700 million. If the Merger Agreement is terminated by DPS because Maple is unable to obtain required financing on the terms required by the Merger Agreement, Maple shall pay to DPS a reverse termination fee in the amount of $700 million.

Upon completion of the Maple Transaction:

• | all unvested stock options, restricted stock units ("RSUs") and performance share units ("PSUs") will vest immediately as a result of the Change in Control (as defined in the terms of each individual award agreement); and |

• | the $500 million revolving line of credit (the "Revolver") will be terminated as a result of the Change in Control (as defined in the Company's unsecured credit agreement (the "Credit Agreement"). |

The Company has an agreement with a financial advisor in relation to the pending Maple Transaction. The Company agreed to pay a fee of approximately $50 million, $5 million of which was for the delivery of the fairness opinion during the first quarter of 2018, and the remaining portion of which will be paid upon, and subject to, consummation of the Maple Transaction.

9

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

BAI BRANDS MERGER UPDATE

On January 31, 2018, the purchase price allocation for the merger with Bai Brands LLC ("Bai Brands") ("Bai Brands Merger") was finalized. There were no changes from the preliminary purchase price allocation as of December 31, 2017, as disclosed in our Annual Report.

In February 2018, the arbitration between the Company and the former shareholders of Bai Brands was completed and the working capital adjustment, which was agreed upon during the year ended December 31, 2017, was released from restricted cash. The remaining non-current restricted cash and corresponding non-current holdback liability, net of any claims, are anticipated to be released approximately four years after the acquisition date, subject to certain administrative conditions and resolution of certain indemnification obligations.

The following table provides a rollforward of the holdback placed in escrow from December 31, 2017 to March 31, 2018:

(in millions) | Indemnification Escrow | Unrecognized Compensation Costs | Total Holdback Liability | |||||||||

Balance as of December 31, 2017 | $ | 79 | $ | 7 | $ | 86 | ||||||

Recognized compensation costs | — | (2 | ) | (2 | ) | |||||||

Balance as of March 31, 2018 | $ | 79 | $ | 5 | $ | 84 | ||||||

TRANSACTION AND INTEGRATION EXPENSES

The following table provides information about the Company's transaction and integration expenses incurred during the three months ended March 31, 2018 and 2017:

For the Three Months Ended March 31, | ||||||||

(in millions) | 2018 | 2017 | ||||||

Maple Transaction | $ | 12 | $ | — | ||||

Bai Brands Merger | 1 | 19 | ||||||

Total transaction and integration expenses incurred | $ | 13 | $ | 19 | ||||

INVESTMENTS IN UNCONSOLIDATED SUBSIDIARIES

On January 5, 2018, the Company acquired a 5.1% interest in Core Nutrition, LLC ("Core") for $18 million. The investment is accounted for as an equity method investment as the Company is deemed to have the ability to exercise significant influence through a more than minor interest in the investee in accordance with U.S. GAAP.

3. Revenues

The Company recognizes revenue when obligations under the terms of a contract with the customer are satisfied. Branded product sales, which include carbonated soft drinks ("CSDs"), non-carbonated beverages ("NCBs") and allied brand sales, occur once control is transferred upon delivery to the customer's facility. Contract manufacturing sales occur once control is transferred, either upon shipment or at the time the finished goods are ready for shipment and billed to the customer, based upon the terms of the contract with the customer. Revenue is measured as the amount of consideration the Company expects to receive in exchange for transferring goods. The amount of consideration the Company receives and revenue the Company recognizes varies with changes in customer incentives the Company offers to its customers and their customers. Sales taxes and other similar taxes are excluded from revenue. Costs associated with shipping and handling activities, such as merchandising, are included in SG&A expenses as revenue is recognized.

The Company entered into arrangements during 2010 to license the manufacturing and distribution of certain brands to PepsiCo, Inc. ("PepsiCo") and The Coca-Cola Company ("Coca-Cola") and to sell and deliver all concentrates used in the manufacture of licensed beverages under these arrangements as PepsiCo and Coca-Cola place orders for these concentrates. In these cases, the Company first determined whether the arrangements represented separate performance obligations. The primary requirements to meet the separate performance obligation criteria is whether the performance obligation is capable of being distinct and distinct in the context of the contract. As the sale of the manufacturing and distribution rights and the ongoing sales of concentrate would not have economic benefit to the customer on its own or together with other resources that are available to the customer and the promises are not capable of being distinct, only one performance obligation was identified for these arrangements. The one-time nonrefundable cash receipts from PepsiCo and Coca-Cola were therefore recorded as deferred revenue and are recognized as net sales ratably over time during the estimated 25-year life of the customer relationship.

10

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

The adoption of ASC 606 resulted in an immaterial impact to the individual financial statement line items of the Company's unaudited Condensed Consolidated Statements of Income during the three months ended March 31, 2018.

For the three months ended March 31, 2018, the Company recognized $16 million of net sales that were included in deferred revenue at the beginning of the respective periods, which relates to the PepsiCo and Coca-Cola arrangements primarily within the Beverage Concentrates operating segment.

Information about the Company's net sales by reporting segment and portfolio for the three months ended March 31, 2018 and 2017 is as follows:

(in millions) | Beverage Concentrates | Packaged Beverages | Latin America Beverages | Total | |||||||||||

For the three months ended March 31, 2018: | |||||||||||||||

Carbonated soft drinks ("CSDs")(1) | $ | 280 | $ | 477 | $ | 76 | $ | 833 | |||||||

Non-carbonated beverages ("NCBs")(2) | 3 | 477 | 36 | 516 | |||||||||||

Contract manufacturing(3) | — | 69 | 1 | 70 | |||||||||||

Allied brand sales(4) | — | 147 | — | 147 | |||||||||||

Other(5) | 20 | 8 | — | 28 | |||||||||||

Net sales | $ | 303 | $ | 1,178 | $ | 113 | $ | 1,594 | |||||||

For the three months ended March 31, 2017:(6) | |||||||||||||||

CSDs(1) | $ | 271 | $ | 462 | $ | 66 | $ | 799 | |||||||

NCBs(2) | 3 | 449 | 32 | 484 | |||||||||||

Contract manufacturing(3) | — | 60 | — | 60 | |||||||||||

Allied brand sales(4) | — | 139 | — | 139 | |||||||||||

Other(5) | 20 | 8 | — | 28 | |||||||||||

Net sales | $ | 294 | $ | 1,118 | $ | 98 | $ | 1,510 | |||||||

__________________

(1) | Represents product sales of owned CSD brands within our portfolio and the net sales recognized ratably under the PepsiCo and Coca-Cola arrangements. Product sales include the sale of beverage concentrates, syrup and packaged beverages. |

(2) | Represents product sales of owned NCB brands within our portfolio. Product sales primarily include packaged beverages. |

(3) | Net sales from contract manufacturing, bottling beverages and other products for private label owners or others. |

(4) | Allied brand sales represent product distribution of third party brands. |

(5) | Other sales include miscellaneous revenues, such as royalties. |

(6) | Prior period amounts were not adjusted for the adoption of the new revenue recognition guidance under ASC 606. |

Information about the Company's net sales by reporting segment and geography for the three months ended March 31, 2018 and 2017 is as follows:

(in millions) | Beverage Concentrates | Packaged Beverages | Latin America Beverages | Total | |||||||||||

For the three months ended March 31, 2018: | |||||||||||||||

United States ("U.S.") | $ | 284 | $ | 1,146 | $ | — | $ | 1,430 | |||||||

Canada | 19 | 32 | — | 51 | |||||||||||

Latin America and other(1) | — | — | 113 | 113 | |||||||||||

Net sales | $ | 303 | $ | 1,178 | $ | 113 | $ | 1,594 | |||||||

For the three months ended March 31, 2017:(2) | |||||||||||||||

U.S. | $ | 277 | $ | 1,089 | $ | — | $ | 1,366 | |||||||

Canada | 17 | 29 | — | 46 | |||||||||||

Latin America and other(1) | — | — | 98 | 98 | |||||||||||

Net sales | $ | 294 | $ | 1,118 | $ | 98 | $ | 1,510 | |||||||

__________________

(1) | Other includes immaterial net sales in geographical locations outside of U.S., Latin America and Canada. |

(2) | Prior period amounts were not adjusted for the adoption of the new revenue recognition guidance under ASC 606. |

11

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

4. | Goodwill and Other Intangible Assets |

CHANGE IN THE COMPANY'S OPERATING SEGMENTS AND REPORTING UNITS

As of January 1, 2018, due to changes to the information reviewed by the chief operating decision maker and limited availability of discrete financial information, the Company has determined that Bai no longer meets the criteria to be considered an operating segment. Therefore, as of January 1, 2018, the Company has three operating segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. There is no change to the Company's reportable segments, as previously Bai and Packaged Beverages Excluding Bai were aggregated into the Packaged Beverages reportable segment.

The Company has additionally concluded that Bai meets the criteria to be considered a component of the Packaged Beverages segment. However, as the economic characteristics of Bai and Warehouse Direct ("WD") are similar, the Company has aggregated Bai and WD into a single reporting unit as of January 1, 2018.

GOODWILL

Changes in the carrying amount of goodwill by reporting unit are as follows:

(in millions) | Beverage Concentrates | WD Reporting Unit(1) | DSD Reporting Unit(1) | Bai(1) | Latin America Beverages | Total | |||||||||||||||||

Balance as of December 31, 2017 | |||||||||||||||||||||||

Goodwill | $ | 1,733 | $ | 1,222 | $ | 189 | $ | 568 | $ | 29 | $ | 3,741 | |||||||||||

Accumulated impairment losses | — | — | (180 | ) | — | — | (180 | ) | |||||||||||||||

1,733 | 1,222 | 9 | 568 | 29 | 3,561 | ||||||||||||||||||

Foreign currency impact | — | — | — | — | 3 | 3 | |||||||||||||||||

Reclassifications(2) | — | 568 | — | (568 | ) | — | — | ||||||||||||||||

Balance as of March 31, 2018 | |||||||||||||||||||||||

Goodwill | 1,733 | 1,790 | 189 | — | 32 | 3,744 | |||||||||||||||||

Accumulated impairment losses | — | — | (180 | ) | — | — | (180 | ) | |||||||||||||||

$ | 1,733 | $ | 1,790 | $ | 9 | $ | — | $ | 32 | $ | 3,564 | ||||||||||||

(1) | As of January 1, 2018, the Packaged Beverages operating segment is comprised of three reporting units, the Direct Store Delivery ("DSD") system, WD and Bai. |

(2) | As of January 1, 2018, due to changes in the Company's operating segments and reporting units, the goodwill associated with the Bai operating segment was reclassified to the WD reporting unit. Refer to Change in the Company's Operating Segments and Reporting Units above. |

12

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

INTANGIBLE ASSETS OTHER THAN GOODWILL

The net carrying amounts of intangible assets other than goodwill are as follows:

March 31, 2018 | December 31, 2017 | ||||||||||||||||||||||

Gross | Accumulated | Net | Gross | Accumulated | Net | ||||||||||||||||||

(in millions) | Amount | Amortization | Amount | Amount | Amortization | Amount | |||||||||||||||||

Intangible assets with indefinite lives: | |||||||||||||||||||||||

Brands(1) | $ | 3,697 | $ | 3,697 | $ | 3,694 | $ | 3,694 | |||||||||||||||

Distribution rights | 32 | 32 | 32 | 32 | |||||||||||||||||||

Intangible assets with definite lives: | |||||||||||||||||||||||

Customer relationships | 106 | $ | (80 | ) | 26 | 106 | $ | (79 | ) | 27 | |||||||||||||

Non-compete agreements | 22 | (3 | ) | 19 | 22 | (2 | ) | 20 | |||||||||||||||

Distribution rights | 21 | (11 | ) | 10 | 18 | (10 | ) | 8 | |||||||||||||||

Brands | 29 | (29 | ) | — | 29 | (29 | ) | — | |||||||||||||||

Bottler agreements | 19 | (19 | ) | — | 19 | (19 | ) | — | |||||||||||||||

Total | $ | 3,926 | $ | (142 | ) | $ | 3,784 | $ | 3,920 | $ | (139 | ) | $ | 3,781 | |||||||||

____________________________

(1) | Indefinite lived brand assets increased $3 million as a result of foreign currency translation. |

Amortization expense for intangible assets with definite lives for the three months ended March 31, 2018 and 2017 was $3 million and $2 million, respectively.

Amortization expense of these intangible assets over the remainder of 2018 and the next four years is expected to be as follows:

Remainder of 2018 | For the Years Ended December 31, | ||||||||||||||||||

(in millions) | 2019 | 2020 | 2021 | 2022 | |||||||||||||||

Projected amortization expense for intangible assets with definite lives | $ | 13 | $ | 14 | $ | 9 | $ | 7 | $ | 5 | |||||||||

IMPAIRMENT TESTING

The Company conducts impairment tests on goodwill and all indefinite lived intangible assets annually or more frequently if circumstances indicate that the carrying amount of an asset may not be recoverable. DPS did not identify any circumstances that indicated that the carrying amount of any goodwill or any indefinite lived intangible asset may not be recoverable as of March 31, 2018.

5. Income Taxes

The legislation commonly referred to as the Tax Cuts and Jobs Act (the "TCJA") was enacted on December 22, 2017. The TCJA reduced the U.S. federal statutory tax rate from 35% to 21% effective January 1, 2018, repealed the domestic manufacturing deduction effective January 1, 2018 and made changes to the international tax rules.

13

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

The effective tax rates for the three months ended March 31, 2018 and 2017 were 24.7% and 28.6%, respectively. The following is a reconciliation of the provision for income taxes computed at the U.S. federal statutory tax rate to the provision for income taxes reported in the unaudited Condensed Consolidated Statements of Income:

For the Three Months Ended March 31, 2018 | For the Three Months Ended March 31, 2017 | ||||||||||||

(in millions) | Amount | Percentage | Amount | Percentage | |||||||||

Statutory federal income tax(1) | $ | 46 | 21.0 | % | $ | 87 | 35.0 | % | |||||

State income taxes, net(2) | 10 | 4.6 | % | 8 | 3.2 | % | |||||||

US federal domestic manufacturing benefit(3) | — | — | % | (6 | ) | (2.4 | )% | ||||||

Impact of non-US operations(4) | 1 | 0.5 | % | (1 | ) | (0.4 | )% | ||||||

Stock-based compensation benefit(5) | (5 | ) | (2.3 | )% | (18 | ) | (7.3 | )% | |||||

Other | 2 | 0.9 | % | 1 | 0.5 | % | |||||||

Total income tax provision | $ | 54 | 24.7 | % | $ | 71 | 28.6 | % | |||||

____________________________

For the three months ended March 31, 2018, the TCJA

(1) | reduced the U.S. federal statutory tax rate from 35% to 21%. |

(2) | decreased the federal income tax benefit from the deduction of state income taxes from 35% to 21%. |

(3) | repealed the U.S. federal domestic manufacturing deduction. |

(4) | caused the impact of non-U.S. operations to switch from an income tax benefit to an income tax detriment due to the lower U.S. federal statutory tax rate. |

(5) | reduced the tax benefit from stock-based compensation due to the lower U.S. federal statutory tax rate; additionally, the pre-tax windfall in the current period was less than the prior period. |

On December 22, 2017, the SEC staff issued Staff Accounting Bulletin (“SAB”) 118, Income Tax Accounting Implications of the Tax Cuts and Jobs Act (“SAB 118”), which provides guidance on accounting for the impact of the TCJA, in effect allowing an entity to use a methodology similar to the measurement period in a business combination for tax impacts effective in the fourth quarter of 2017. Pursuant to the provisions of SAB 118, as of March 31, 2018, the Company has not completed its accounting for the tax effects of the TCJA. The Company recorded a reasonable estimate of the impact from the TCJA, but is still analyzing the TCJA and refining our calculations. Additionally, future guidance from the Internal Revenue Service, SEC, or the FASB could result in changes to our accounting for the tax effects of the TCJA.

6. | Long-term Obligations and Borrowing Arrangements |

The following table summarizes the Company's long-term obligations:

March 31, | December 31, | ||||||

(in millions) | 2018 | 2017 | |||||

Senior unsecured notes | $ | 4,212 | $ | 4,230 | |||

Capital lease obligations | 186 | 183 | |||||

Subtotal | 4,398 | 4,413 | |||||

Less - current portion | (263 | ) | (13 | ) | |||

Long-term obligations | $ | 4,135 | $ | 4,400 | |||

The following table summarizes the Company's short-term borrowings and current portion of long-term obligations:

Fair Value Hierarchy Level | March 31, 2018 | December 31, 2017 | |||||||||||||||

(in millions) | Carrying Value | Fair Value | Carrying Value | Fair Value | |||||||||||||

Commercial paper | 1 | $ | 120 | $ | 120 | $ | 66 | $ | 66 | ||||||||

Current portion of long-term obligations: | |||||||||||||||||

Senior unsecured notes | 2 | 249 | 249 | — | — | ||||||||||||

Capital lease obligations(1) | N/A | 14 | 13 | ||||||||||||||

Short-term borrowings and current portion of long-term obligations | $ | 383 | $ | 369 | $ | 79 | $ | 66 | |||||||||

____________________________

(1) | Capital lease obligations are specifically excluded from the calculation of fair value under U.S. GAAP. |

14

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

SENIOR UNSECURED NOTES

The Company's senior unsecured notes (collectively, the "Notes") consisted of the following carrying values and estimated fair values that are not required to be measured at fair value in the Consolidated Balance Sheets are as follows:

(in millions) | Fair Value Hierarchy Level | March 31, 2018 | December 31, 2017 | |||||||||||||||||||

Issuance | Maturity Date | Rate | Carrying Value | Fair Value | Carrying Value | Fair Value | ||||||||||||||||

2019 Notes | January 15, 2019 | 2.60% | 2 | $ | 250 | $ | 249 | $ | 250 | $ | 251 | |||||||||||

2020 Notes | January 15, 2020 | 2.00% | 2 | 250 | 245 | 250 | 248 | |||||||||||||||

2021-A Notes | November 15, 2021 | 3.20% | 2 | 250 | 247 | 250 | 255 | |||||||||||||||

2021-B Notes | November 15, 2021 | 2.53% | 2 | 250 | 242 | 250 | 249 | |||||||||||||||

2022 Notes | November 15, 2022 | 2.70% | 2 | 250 | 239 | 250 | 248 | |||||||||||||||

2023 Notes | December 15, 2023 | 3.13% | 2 | 500 | 481 | 500 | 504 | |||||||||||||||

2025 Notes | November 15, 2025 | 3.40% | 2 | 500 | 477 | 500 | 508 | |||||||||||||||

2026 Notes | September 15, 2026 | 2.55% | 2 | 400 | 354 | 400 | 378 | |||||||||||||||

2027 Notes | June 15, 2027 | 3.43% | 2 | 500 | 470 | 500 | 501 | |||||||||||||||

2038 Notes | May 1, 2038 | 7.45% | 2 | 125 | 174 | 125 | 179 | |||||||||||||||

2045 Notes | November 15, 2045 | 4.50% | 2 | 550 | 528 | 550 | 588 | |||||||||||||||

2046 Notes | December 15, 2046 | 4.42% | 2 | 400 | 379 | 400 | 424 | |||||||||||||||

Principal amount | $ | 4,225 | $ | 4,085 | $ | 4,225 | $ | 4,333 | ||||||||||||||

Unamortized premiums, discounts, and debt issuance costs | (12 | ) | (13 | ) | ||||||||||||||||||

Adjustments to carrying value for interest rate swaps(1) | (1 | ) | 18 | |||||||||||||||||||

Carrying amount | $ | 4,212 | $ | 4,230 | ||||||||||||||||||

____________________________

(1) | Refer to Note 7 for additional information on the Company's interest rate swaps. |

The indentures governing the Notes, among other things, limit the Company's ability to incur indebtedness secured by principal properties, to enter into certain sale and leaseback transactions and to enter into certain mergers or transfers of substantially all of DPS' assets. The Notes are guaranteed by all of the Company's existing and future direct and indirect subsidiaries that guarantee any of the Company's other indebtedness. As of March 31, 2018, the Company was in compliance with all financial covenant requirements of the Notes.

The fair value amounts of long term debt were based on current market rates available to the Company. The difference between the fair value and the carrying value represents the theoretical net premium or discount that would be paid or received to retire all debt and related unamortized costs to be incurred at such date. The carrying amount includes the unamortized discounts and issuance costs on the issuance of debt and impact of interest rate swaps designated as fair value hedges and other hedge related adjustments. Refer to Note 7 for additional information regarding the notes subject to fair value hedges.

BORROWING ARRANGEMENTS

Commercial Paper Program

The following table provides information about the Company's weighted average borrowings under its commercial paper program for the three months ended March 31, 2018 and 2017:

For the Three Months Ended | ||||||||

March 31, | ||||||||

(in millions, except percentages) | 2018 | 2017 | ||||||

Weighted average commercial paper borrowings(1) | $ | 115 | $ | 6 | ||||

Weighted average borrowing rates | 1.95 | % | 1.03 | % | ||||

____________________________

(1) | Borrowings during the period had maturities of 90 days or less. |

Upon execution of the Merger Agreement on January 29, 2018, the Company became limited to a maximum aggregate amount of commercial paper outstanding of $200 million, unless it obtains Maple's approval. Refer to Note 2 for additional information about the Merger Agreement.

15

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

Unsecured Credit Agreement

The following table provides amounts utilized and available under the "Revolver" as of March 31, 2018:

(in millions) | Amount Utilized | Balances Available | |||||

Revolver | $ | — | $ | 380 | |||

Letters of credit | — | 75 | |||||

As of March 31, 2018, the Company was in compliance with all financial covenant requirements relating to the Credit Agreement.

Shelf Registration Statement

The Company filed a "well-known seasoned issuer" shelf registration statement with the SEC, effective September 2, 2016, which registered an indeterminate amount of securities for future sales. The Company's Board of Directors (the "Board") authorizes the amount of securities that the Company may issue. As of March 31, 2018, $450 million remained authorized to be issued under the Board's authorization.

Letters of Credit Facilities

In addition to the portion of the Revolver reserved for issuance of letters of credit, the Company has incremental letters of credit facilities. Under these facilities, $120 million is available for the issuance of letters of credit, $60 million of which was utilized as of March 31, 2018 and $60 million of which remains available for use.

7. Derivatives

DPS is exposed to market risks arising from adverse changes in:

•interest rates;

•foreign exchange ("FX") rates; and

• | commodity prices affecting the cost of raw materials and fuels. |

The Company manages these risks through a variety of strategies, including the use of interest rate contracts, FX forward contracts, commodity forward and future contracts and supplier pricing agreements. DPS does not hold or issue derivative financial instruments for trading or speculative purposes.

The Company formally designates and accounts for certain interest rate contracts and foreign exchange forward contracts that meet established accounting criteria under U.S. GAAP as either fair value or cash flow hedges. For derivative instruments that are designated and qualify as cash flow hedges, the effective portion of the gain or loss on the derivative instruments is recorded, net of applicable taxes, in Accumulated Other Comprehensive Loss ("AOCL"), a component of Stockholders' Equity in the unaudited Condensed Consolidated Balance Sheets. When net income is affected by the variability of the underlying transaction, the applicable offsetting amount of the gain or loss from the derivative instrument deferred in AOCL is reclassified to net income and is reported as a component of the unaudited Condensed Consolidated Statements of Income. For derivative instruments that are designated and qualify as fair value hedges, the effective change in the fair value of the instrument, as well as the offsetting gain or loss on the hedged item attributable to the hedged risk, are recognized immediately in current-period earnings. For derivatives that are not designated or are de-designated as a hedging instrument, the gain or loss on the instrument is recognized in earnings in the period of change. Cash flows from derivative instruments designated in a qualifying hedging relationship are classified in the same category as the cash flows from the hedged items.

Certain interest rate contracts qualify for the "shortcut" method of accounting for hedges under U.S. GAAP. Under the shortcut method, the hedges are assumed to be perfectly effective and no ineffectiveness is recorded in earnings. For all other designated hedges, the Company assesses whether the derivative instrument is effective in offsetting the changes in fair value or variability of cash flows at the inception of the derivative contract. DPS measures hedge ineffectiveness on a quarterly basis throughout the designated period. Changes in the fair value of the derivative instrument that do not effectively offset changes in the fair value of the underlying hedged item throughout the designated hedge period are recorded in earnings each period.

If a fair value or cash flow hedge were to cease to qualify for hedge accounting, or were terminated, the derivatives would continue to be carried on the balance sheet at fair value until settled and hedge accounting would be discontinued prospectively. If the underlying hedged transaction ceases to exist, any associated amounts reported in AOCL would be reclassified to earnings at that time.

16

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

INTEREST RATES

Fair Value Hedges

The Company is exposed to the risk of changes in the fair value of certain fixed-rate debt attributable to changes in interest rates and manages these risks through the use of receive-fixed, pay-variable interest rate swaps. Any ineffectiveness is recorded as interest during the period incurred. The following table presents information regarding these interest rate swaps and the associated hedging relationships:

Impact to the carrying value | ||||||||||||||||||

($ in millions) | Method of | of long-term debt | ||||||||||||||||

Hedging | Number of | measuring | Notional | March 31, | December 31, | |||||||||||||

Period entered | relationship | instruments | effectiveness | value | 2018 | 2017 | ||||||||||||

November 2011 | 2019 Notes | 2 | Short cut method | $ | 100 | $ | (1 | ) | $ | — | ||||||||

November 2011 | 2021-A Notes | 2 | Short cut method | 150 | (3 | ) | (1 | ) | ||||||||||

November 2012 | 2020 Notes | 5 | Short cut method | 120 | (3 | ) | (2 | ) | ||||||||||

December 2016 | 2021-B Notes | 2 | Short cut method | 250 | (7 | ) | (4 | ) | ||||||||||

December 2016 | 2023 Notes | 2 | Short cut method | 150 | (6 | ) | (3 | ) | ||||||||||

January 2017 | 2022 Notes | 4 | Regression | 250 | 8 | 17 | ||||||||||||

June 2017 | 2038 Notes | 1 | Regression | 50 | 11 | 11 | ||||||||||||

$ | 1,070 | $ | (1 | ) | $ | 18 | ||||||||||||

FOREIGN EXCHANGE

Cash Flow Hedges

The Company's Canadian and Mexican businesses purchase certain inventory through transactions denominated and settled in United States ("U.S.") dollars, a currency different from the functional currency of those businesses. These inventory purchases are subject to exposure from movements in exchange rates. During the three months ended March 31, 2018 and 2017, the Company utilized FX forward contracts designated as cash flow hedges to manage the exposures resulting from changes in these foreign currency exchange rates. The intent of these FX contracts is to provide predictability in the Company's overall cost structure. These FX contracts, carried at fair value, have maturities between one and nine months as of March 31, 2018. The Company had outstanding FX forward contracts with notional amounts of $49 million and $48 million as of March 31, 2018 and December 31, 2017, respectively.

COMMODITIES

Economic Hedges

DPS centrally manages the exposure to volatility in the prices of certain commodities used in its production process and transportation through forward and future contracts. The intent of these contracts is to provide a certain level of predictability in the Company's overall cost structure. During the three months ended March 31, 2018 and 2017, the Company held forward and future contracts that economically hedged certain of its risks. In these cases, a natural hedging relationship exists in which changes in the fair value of the instruments act as an economic offset to changes in the fair value of the underlying items. Changes in the fair value of these instruments are recorded in earnings throughout the term of the derivative instrument and are reported in the same line item of the unaudited Condensed Consolidated Statements of Income as the hedged transaction. Unrealized gains and losses are recognized as a component of unallocated corporate costs until the Company's operating segments are affected by the completion of the underlying transaction, at which time the gain or loss is reflected as a component of the respective segment's operating profit ("SOP"). The total notional values of derivatives related to economic hedges of this type were $185 million and $199 million as of March 31, 2018 and December 31, 2017, respectively.

17

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

FAIR VALUE OF DERIVATIVE INSTRUMENTS

The following table summarizes the fair value hierarchy and the location of the fair value of the Company's derivative instruments designated as hedging instruments within the unaudited Condensed Consolidated Balance Sheets as of March 31, 2018 and December 31, 2017:

(in millions) | Fair Value Hierarchy Level | Balance Sheet Location | March 31, 2018 | December 31, 2017 | |||||||

Assets: | |||||||||||

Interest rate contracts | 2 | Prepaid expenses and other current assets | $ | — | $ | 3 | |||||

FX forward contracts | 2 | Prepaid expenses and other current assets | — | 2 | |||||||

Interest rate contracts | 2 | Other non-current assets | 12 | 16 | |||||||

Liabilities: | |||||||||||

Interest rate contracts | 2 | Other current liabilities | 8 | 3 | |||||||

FX forward contracts | 2 | Other current liabilities | 1 | — | |||||||

Interest rate contracts | 2 | Other non-current liabilities | 12 | 8 | |||||||

The following table summarizes the fair value hierarchy and the location of the fair value of the Company's derivative instruments not designated as hedging instruments within the unaudited Condensed Consolidated Balance Sheets as of March 31, 2018 and December 31, 2017:

(in millions) | Fair Value Hierarchy Level | Balance Sheet Location | March 31, 2018 | December 31, 2017 | |||||||

Assets: | |||||||||||

Commodity contracts | 2 | Prepaid expenses and other current assets | $ | 21 | $ | 27 | |||||

Commodity contracts | 2 | Other non-current assets | 12 | 17 | |||||||

Liabilities: | |||||||||||

Commodity contracts | 2 | Other non-current liabilities | 1 | — | |||||||

The fair values of commodity contracts, interest rate contracts and FX forward contracts are determined based on inputs that are readily available in public markets or can be derived from information available in publicly quoted markets. The fair value of commodity contracts are valued using the market approach based on observable market transactions, primarily underlying commodities futures or physical index prices, at the reporting date. Interest rate contracts are valued using models based primarily on readily observable market parameters, such as LIBOR forward rates, for all substantial terms of the Company's contracts and credit risk of the counterparties. The fair value of FX forward contracts are valued using quoted forward FX prices at the reporting date. Therefore, the Company has categorized these contracts as Level 2.

18

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

IMPACT OF CASH FLOW HEDGES

The following table presents the impact of derivative instruments designated as cash flow hedging instruments under U.S. GAAP to the unaudited Condensed Consolidated Statements of Income and Comprehensive Income:

(in millions) | Amount of Loss Recognized in Other Comprehensive Loss ("OCI") | Amount of Loss Reclassified from AOCL into Income | Location of Loss Reclassified from AOCL into Income | ||||||

For the three months ended March 31, 2018: | |||||||||

Interest rate contracts | $ | — | $ | (2 | ) | Interest expense | |||

FX forward contracts | (1 | ) | — | Cost of sales | |||||

Total | $ | (1 | ) | $ | (2 | ) | |||

For the three months ended March 31, 2017: | |||||||||

Interest rate contracts | $ | — | $ | (2 | ) | Interest expense | |||

FX forward contracts | (5 | ) | — | Cost of sales | |||||

Total | $ | (5 | ) | $ | (2 | ) | |||

For the three months ended March 31, 2018 and 2017, no hedge ineffectiveness was recognized in earnings with respect to derivative instruments designated as cash flow hedges. During the next 12 months, the Company expects to reclassify pre-tax net losses of $11 million from AOCL into net income.

IMPACT OF FAIR VALUE HEDGES

The following table presents the impact of derivative instruments designated as fair value hedging instruments under U.S. GAAP to the unaudited Condensed Consolidated Statements of Income:

(in millions) | Amount of Gain Recognized in Income | Location of Gain Recognized in Income | ||||

For the three months ended March 31, 2018: | ||||||

Interest rate contracts | $ | 1 | Interest expense | |||

For the three months ended March 31, 2017: | ||||||

Interest rate contracts | $ | 4 | Interest expense | |||

For the three months ended March 31, 2018 and 2017, no hedge ineffectiveness was recognized in earnings with respect to derivative instruments designated as fair value hedges for each period.

19

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

IMPACT OF ECONOMIC HEDGES

The following table presents the impact of derivative instruments not designated as hedging instruments under U.S. GAAP to the unaudited Condensed Consolidated Statements of Income:

(in millions) | Amount of Gain (Loss) Recognized in Income | Location of Gain (Loss) Recognized in Income | ||||

For the three months ended March 31, 2018: | ||||||

Commodity contracts(1) | $ | (8 | ) | Cost of sales | ||

Commodity contracts(1) | 3 | SG&A expenses | ||||

Total | $ | (5 | ) | |||

For the three months ended March 31, 2017: | ||||||

Commodity contracts(1) | $ | 21 | Cost of sales | |||

Commodity contracts(1) | (13 | ) | SG&A expenses | |||

Interest rate contracts(2) | 1 | Interest expense | ||||

Total | $ | 9 | ||||

(1) | Commodity contracts include both realized and unrealized gains and losses. |

(2) | Represents gains on the interest rate contracts related to the 2022 Notes prior to re-designation of hedging relationship in January 2017. |

The Company has exposure to credit losses from derivative instruments in an asset position in the event of nonperformance by the counterparties to the agreements. Historically, DPS has not experienced credit losses as a result of counterparty nonperformance. The Company selects and periodically reviews counterparties based on credit ratings, limits its exposure to a single counterparty under defined guidelines and monitors the market position of the programs upon execution of a hedging transaction and at least on a quarterly basis.

8. Stock-Based Compensation

The Company's Omnibus Stock Incentive Plan of 2009 ( "DPS Stock Plan") provides for various long-term incentive awards, including stock options, RSUs and PSUs.

Stock-based compensation expense is recorded in SG&A expenses in the unaudited Condensed Consolidated Statements of Income. The components of stock-based compensation expense are presented below:

For the Three Months Ended March 31, | |||||||

(in millions) | 2018 | 2017 | |||||

Total stock-based compensation expense | $ | 10 | $ | 6 | |||

Income tax benefit recognized in the Statements of Income | (2 | ) | (2 | ) | |||

Stock-based compensation expense, net of tax | $ | 8 | $ | 4 | |||

20

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

STOCK OPTIONS

The table below summarizes stock option activity for the three months ended March 31, 2018:

Stock Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term (Years) | Aggregate Intrinsic Value (in millions) | |||||||||

Outstanding as of January 1, 2018 | 1,372,606 | $ | 82.83 | 7.86 | $ | 20 | ||||||

Exercised | (23,510 | ) | 77.15 | 1 | ||||||||

Forfeited or expired | (3,519 | ) | 93.52 | |||||||||

Outstanding as of March 31, 2018 | 1,345,577 | 82.90 | 7.62 | 48 | ||||||||

Exercisable as of March 31, 2018 | 938,886 | 78.19 | 7.19 | 38 | ||||||||

As of March 31, 2018, there was $4 million of unrecognized compensation cost related to unvested stock options granted under the DPS Stock Plan that is expected to be recognized over a weighted average period of 1.26 years.

RESTRICTED STOCK UNITS

The table below summarizes RSU activity for the three months ended March 31, 2018. The fair value of RSUs is determined based on the number of units granted and the grant date price of the Company's common stock.

RSUs | Weighted Average Grant Date Fair Value | Weighted Average Remaining Contractual Term (Years) | Aggregate Intrinsic Value (in millions) | |||||||||

Outstanding as of January 1, 2018 | 942,124 | $ | 88.44 | 0.82 | $ | 91 | ||||||

Granted | 432,538 | 116.13 | ||||||||||

Vested and released | (501,852 | ) | 84.24 | 58 | ||||||||

Forfeited | (6,745 | ) | 92.86 | |||||||||

Outstanding as of March 31, 2018 | 866,065 | 104.67 | 1.79 | 103 | ||||||||

As of March 31, 2018, there was $80 million of unrecognized compensation cost related to unvested RSUs granted under the DPS Stock Plan that is expected to be recognized over a weighted average period of 1.78 years.

During the three months ended March 31, 2018, 501,852 shares subject to previously granted RSUs vested. A majority of these vested RSUs were net share settled. The Company withheld 144,882 shares based upon the Company's closing stock price on the vesting date to settle the employees' minimum statutory obligation for applicable income and other employment taxes. Subsequently, the Company remitted the required funds to the appropriate taxing authorities.

PERFORMANCE SHARE UNITS

The table below summarizes PSU activity for the three months ended March 31, 2018. The fair value of PSUs is determined based on the number of units granted and the grant date price of the Company's common stock.

PSUs | Weighted Average Grant Date Fair Value | Weighted Average Remaining Contractual Term (Years) | Aggregate Intrinsic Value (in millions) | |||||||||

Outstanding as of January 1, 2018 | 329,490 | $ | 51.69 | 0.98 | $ | 32 | ||||||

Vested and released | (92,589 | ) | 67.35 | 11 | ||||||||

Forfeited | (21,972 | ) | 67.11 | |||||||||

Outstanding as of March 31, 2018 | 214,929 | 45.66 | 1.25 | 25 | ||||||||

As of March 31, 2018, there was $6 million of unrecognized compensation cost related to unvested PSUs granted under the DPS Stock Plan that is expected to be recognized over a weighted average period of 1.25 years.

21

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

During the three months ended March 31, 2018, 92,589 units subject to previously granted PSUs vested. A majority of these vested PSUs were net share settled. The Company withheld 27,373 shares based upon the Company's closing stock price on the vesting date to settle the employees' minimum statutory obligation for the applicable income and other employment taxes. Subsequently, the Company remitted the required funds to the appropriate taxing authorities.

9. Earnings Per Share

Basic earnings per share ("EPS") is computed by dividing net income by the weighted average number of common shares outstanding for the period. Diluted EPS reflects the assumed conversion of all dilutive securities. The following table presents the basic and diluted EPS and the Company's basic and diluted shares outstanding:

For the Three Months Ended March 31, | |||||||

(in millions, except per share data) | 2018 | 2017 | |||||

Basic EPS: | |||||||

Net income | $ | 159 | $ | 177 | |||

Weighted average common shares outstanding | 179.9 | 183.4 | |||||

Earnings per common share — basic | $ | 0.88 | $ | 0.97 | |||

Diluted EPS: | |||||||

Net income | $ | 159 | $ | 177 | |||

Weighted average common shares outstanding | 179.9 | 183.4 | |||||

Effect of dilutive securities: | |||||||

Stock options | 0.3 | 0.3 | |||||

RSUs | 0.5 | 0.7 | |||||

PSUs | 0.1 | 0.2 | |||||

Weighted average common shares outstanding and common stock equivalents | 180.8 | 184.6 | |||||

Earnings per common share — diluted | $ | 0.88 | $ | 0.96 | |||

Stock options, RSUs, PSUs and dividend equivalent units ("DEUs") totaling 0.1 million and 0.5 million shares were excluded from the diluted weighted average shares outstanding for the three months ended March 31, 2018 and 2017, respectively, as they were not dilutive.

Under the terms of our RSU and PSU agreements, unvested RSU and PSU awards contain forfeitable rights to dividends and DEUs. Because the DEUs are forfeitable, they are defined as non-participating securities. As of March 31, 2018, there were 22,526 DEUs, which will vest at the time that the underlying RSU or PSU vests.

As of March 31, 2018, the Company's Board has authorized a total aggregate share repurchase plan of $5 billion. The Company's share repurchase program was suspended during negotiation of the Maple Transaction, and it remains suspended as of March 31, 2018 under the terms of the Merger Agreement. The Company therefore did not repurchase any shares during the three months ended March 31, 2018. The Company repurchased and retired 0.3 million shares of common stock valued at approximately $28 million for the three months ended March 31, 2017.

22

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

10. Accumulated Other Comprehensive Loss

The following tables provide a summary of changes in the balances of each component of AOCL, net of taxes:

(in millions) | Foreign Currency Translation | Change in Pension Liability | Cash Flow Hedges | Accumulated Other Comprehensive Loss | |||||||||||

Balance as of January 1, 2017 | $ | (164 | ) | $ | (37 | ) | $ | (28 | ) | $ | (229 | ) | |||

OCI before reclassifications | 16 | 1 | (7 | ) | 10 | ||||||||||

Amounts reclassified from AOCL | — | 4 | 13 | 17 | |||||||||||

Net current year OCI | 16 | 5 | 6 | 27 | |||||||||||

Balance as of December 31, 2017 | (148 | ) | (32 | ) | (22 | ) | (202 | ) | |||||||

OCI before reclassifications | 18 | — | (2 | ) | 16 | ||||||||||

Amounts reclassified from AOCL | — | 1 | 2 | 3 | |||||||||||

Net current period OCI | 18 | 1 | — | 19 | |||||||||||

Balance as of March 31, 2018 | $ | (130 | ) | $ | (31 | ) | $ | (22 | ) | $ | (183 | ) | |||

The following table presents the amount of loss reclassified from AOCL into the unaudited Condensed Consolidated Statements of Income:

For the Three Months Ended March 31, | |||||||||

(in millions) | Location of Loss Reclassified from AOCL into Income | 2018 | 2017 | ||||||

Loss on cash flow hedges: | |||||||||

Interest rate contracts | Interest expense | $ | (2 | ) | $ | (2 | ) | ||

Foreign exchange forward contracts | Cost of sales | — | — | ||||||

Total | (2 | ) | (2 | ) | |||||

Income tax benefit | — | (1 | ) | ||||||

Total | $ | (2 | ) | $ | (1 | ) | |||

Defined benefit pension and post-retirement plan items: | |||||||||

Amortization of actuarial losses, net | Other income, net | $ | (1 | ) | $ | (1 | ) | ||

Total | (1 | ) | (1 | ) | |||||

Income tax benefit | — | — | |||||||

Total | $ | (1 | ) | $ | (1 | ) | |||

Total reclassifications | $ | (3 | ) | $ | (2 | ) | |||

23

DR PEPPER SNAPPLE GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited, Continued)

11. | Inventories |

Inventories consisted of the following:

March 31, | December 31, | ||||||

(in millions) | 2018 | 2017 | |||||

Raw materials | $ | 79 | $ | 81 | |||