Attached files

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON,

DC 20549

FORM 10-K

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal period ended December 31, 2017

or

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________ to ________

Commission File Number 333 - 192877

QPAGOS

(Exact Name of Registrant as Specified in Its Charter)

Nevada |

33 - 1230229 | |

(State

or Other Jurisdiction of |

(I.R.S.

Employer |

Paseo

del la Reforma 404 Piso 15 PH

Col. Juarez, Del. Cuauhtémoc

Mexico, D.F. C.P. 06600

(Address of principal executive offices) (Zip Code)

+52

(55) 55 - 110 - 110

(Registrant’s telephone number, including area

code)

Securities registered pursuant to Section 12(b) of the Act: |

Name of each exchange on which registered | |

(Title of Class) |

None |

Securities registered pursuant to Section 12 (g) of the Act: Common Stock, $0.0001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the issuer: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of issuer’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every interactive data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated file, a non-accelerated file, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

Non-accelerated filer |

☐ |

Smaller reporting company |

☒ |

(Do not check if a smaller reporting company) |

Emerging growth company |

☒ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s common stock held by non-affiliates of the Registrant as of June 30, 2017, (the last business day of the registrants most recently completed second quarter) was approximately $17,635,566 based on $0.32, the price at which the registrants common stock was last sold on June 30, 2017.

As of April 13, 2018, the issuer had 77,383,966 shares of common stock outstanding.

Documents incorporated by reference: None

FORM 10-K

TABLE OF CONTENTS

Special Note Regarding Forward-Looking Statements

Many of the matters discussed within this Annual Report on Form 10-K (“Annual Report”) contain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) on our current expectations and projections about future events. In some cases, you can identify forward-looking statements by terminology such as “may,” “should,” “potential,” “continue,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “estimates,” and similar expressions. These statements are based on our current beliefs, expectations, and assumptions and are subject to a number of risks and uncertainties, many of which are difficult to predict and generally beyond our control, that could cause actual results to differ materially from those expressed, projected or implied in or by the forward-looking statements. Such risks and uncertainties include the risks noted under Part 1. “Business”, and Part II, Item 7”, “Management’s Discussion and Analysis of Financial Conditions and Results of Operations”, but are also contained elsewhere. We do not undertake any obligation to update any forward-looking statements. Unless the context requires otherwise, references to “we,” “us,” “our,” and “Qpagos,” refer to Qpagos and its subsidiaries. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, or at all. We do not undertake any obligation to update any forward-looking statements.

Company Overview

We are a provider of next generation physical and virtual payment services that we introduced to the Mexican market in the third quarter of 2014. We have a ten-year renewable exclusive license agreement for the use of technology that can be used to perform services that are similar to services that have been successfully deployed with this technology in several European, Asian, North and South American countries.

We provide an integrated network of kiosks, terminals and payment channels that enable consumers to deposit cash, convert it into a digital form and remit the funds to any merchant in our network quickly and securely. We help consumers and merchants connect more efficiently in markets and consumer segments, such as Mexico, that are largely cash-based and lack convenient alternatives for consumers to pay for goods and services in physical, online and mobile environments. For example, we license technology that can be used to pay bills, add minutes to mobile phones, purchase transportation tickets, shop online, buy digital services or send money to a friend or relative.

Our current focus is on Mexico which remains a cash-dominated society for retail consumer payments with approximately 80% of the value of personal payments exchanged in cash (Bank of Mexico). The penetration of electronic payment services, such as credit and debit cards and point of sale terminals, significantly lags behind more developed economies. We believe that opportunities for our services in Mexico are vast. With over 109 million mobile subscribers in Mexico, 85% of which are under prepaid plans, the mobile sector was a $13 billion business in 2017 as reported by the Competitive Intelligence Unit (the “CIU”). We believe that there is opportunity for growth in the Mexican market and we have expanded to service providers beyond the mobile telephone operators to service providers of electricity, transportation, utilities, municipal services and taxes, consumer credit installments, insurance premiums, and many more. Altogether as of the end of the first quarter of 2018 our platform had integrated over 140 such services, including the National Lottery’s; Pronosticos.

Our primary strategy in Mexico to date has been the attraction of service providers as well as the deployment of kiosks through Redpag Electrónicos S.A.P.I. de C.V., our kiosk management subsidiary and the sale of kiosks to the country’s leading financial institutions and retailers. During the years ended December 31, 2017 and 2016, we generated net revenues of $3,941,273 and $2,691,896, respectively, an increase of 1,249,397 or 46.4% from our operations in Mexico. Our primary source of revenue are fees we receive for processing payments made by consumers to service providers. We also generate revenue from non-payment services such as kiosk sales. We currently have in excess of 140 service providers integrated into our payment gateway, which includes all mobile phone providers in Mexico as well as most utility companies, and several financial and entertainment services as well as government payments. As of December 31, 2017, QPAGOS had deployed over 216 kiosks and terminals and service an additional 440 kiosks of an independent distributor. QPAGOS kiosks and terminals can be found at convenience stores, next to metro stations, retail stores, municipalities airport, education centers, shopping malls, in large cities as well as many small and rural towns.

We believe that QPAGOS platform provides simple and intuitive user interfaces, convenient access and best-in-class services. QPAGOS runs its network and processes its transactions using a proprietary, advanced technology platform that leverages the latest virtualization, analytics and security technologies to create a fast, highly reliable, secure and redundant system. We believe that the breadth and reach of this network, along with the proprietary nature of its technology platform, differentiate us from our competitors and allow us to effectively manage and update our services and realize significant operating leverage with growth in volumes.

1

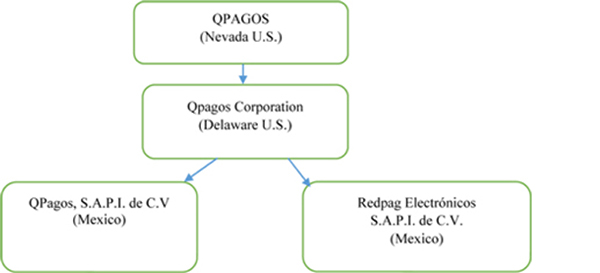

QPAGOS Corporate History and Background

Our current corporate structure is as follows:

QPAGOS was incorporated on September 25, 2013 under the laws of the State of Nevada originally under the name Asiya Pearls, Inc. On May 27, 2016, Asiya Pearls, Inc. filed a Certificate of Amendment to its Articles of Incorporation to change its name from Asiya Pearls, Inc. to QPAGOS.

Qpagos Corporation was incorporated on May 1, 2015 under the laws of Delaware under the name Qpagos Corporation as the holding company for its two 99.9% owned operating subsidiaries, QPagos, S.A.P.I. de C.V. and Redpag Electrónicos S.A.P.I. de C.V. Each of these entities were incorporated in November 2013 in Mexico.

QPagos, S.A.P.I. de C.V. was formed to process payment transactions for service providers it contracts with, and Redpag Electrónicos S.A.P.I. de C.V. was formed to deploy and operate kiosks as a distributor.

On August 31, 2015, QPAGOS Corporation entered into various agreements with the shareholders of Qpagos and Redpag to give effect to a reverse merger transaction (the “Reverse Merger’’). Pursuant to the Reverse Merger, the majority of the shareholders of Qpagos and Redpag effectively received shares in Qpagos Corporation, through various consulting and management agreements entered into with Qpagos Corporation and sold an effective 99.996% and 99.990% of the outstanding shares in Qpagos and Redpag, respectively to Qpagos Corporation. The series of transactions closed effective August 31, 2015. Upon the close of the Reverse Merger, Qpagos Corporation became the parent of Qpagos and Redpag and assumed the operations of these two companies as its sole business.

On May 12, 2016, Qpagos Corporation entered into an Agreement and Plan of Merger (the “Merger Agreement”) with QPAGOS and QPAGOS Merge, Inc., a Delaware corporation and wholly owned subsidiary of QPAGOS (“Merger Sub”). Pursuant to the Merger Agreement, on May 12, 2016 Qpagos Corporation and Merger Sub merged (the “Merger”), and Qpagos Corporation continued as the surviving corporation of the Merger and became a wholly owned subsidiary of QPAGOS. As a result of the Merger, each outstanding share of Qpagos Corporation common stock was converted into the right to receive two shares of QPAGOS common stock as set forth in the Merger Agreement. Under the terms of the Merger Agreement, we issued, and Qpagos Corporation stockholders received in a tax-free exchange, shares of our common stock such that Qpagos Corporation stockholders owned approximately 91% of our company immediately after the Merger. In addition, each outstanding warrant of Qpagos Corporation was assumed by us and converted into a warrant to acquire a number of shares of our common stock equal to twice the number of shares of common stock of Qpagos Corporation subject to the warrant immediately before the effective time of the Merger at an exercise price per share of Company common stock equal to 50% of the warrant exercise price for Qpagos Corporation common stock. There are no outstanding stock options of Qpagos Corporation.

Our principal offices are located at Paseo del la Reforma 404 Piso 15 PH, Col. Juarez, Del. Cuauhtémoc, Mexico, D.F. C.P. 06600, and our telephone number at that office is +52 (55) 55–110–110. We also have offices in the United States that are located at 1900 Glades Road, Suite 280, Boca Raton, Florida 33431. We maintain an Internet website at www.qpagos.com. Neither this website nor the information on this website is included or incorporated in, or is a part of, this prospectus or any supplement to the prospectus.

2

Our Strategy

Our mission is to leverage the experience and success of other global companies in our industry, and establish ourselves as the leading developer and supplier of state-of-the-art electronic payment solutions to Mexican merchants and service providers across all consumer services sectors, such as: fixed and mobile telephone operators, internet services providers, cable, entertainment, public and municipal services such as electricity, water and gas, financial and travel services. Our near-term strategy includes:

| ● | Positioning ourselves as the leading consumer payment solutions provider for all service providers that rely on electronic payments for their collection needs. |

| ● | Establishing a successful distributor network based on a competitive distribution model for entrepreneurs that look at our self-service kiosks as a profitable business opportunity, as well as retail chains and retail banks that need to expedite electronic payments that are clogging teller lines through the assistance of self-service kiosks. |

| ● | Supporting distributors and franchisees through training, point of sale marketing materials, and an ever-increasing amount of payment services, many of which are regional in nature. |

| ● | Developing a Franchising Model through the creation and expansion of one-stop payment services stores which cater to the vast need for a digital payment solution in Mexico. |

| ● | Developing a motivated and effective management team. |

Implications of Being an Emerging Growth Company

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and therefore we intend to take advantage of certain exemptions from various public company reporting requirements, including not being required to have our internal controls over financial reporting audited by our independent registered public accounting firm pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and any golden parachute payments. We may take advantage of these exemptions until we are no longer an “emerging growth company.” In addition, the JOBS Act provides that an “emerging growth company” can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have elected to use the extended transition period for complying with new or revised accounting standards under the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates. We will remain an “emerging growth company” until the earlier of (1) the last day of the fiscal year: (a) following the fifth anniversary of the completion of this offering; (b) in which we have total annual gross revenue of at least $1.07 billion; or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeded $700.0 million as of the prior June 30th , and (2) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period. References herein to “emerging growth company” have the meaning associated with that term in the JOBS Act.

Our Business Model

Our primary source of revenue are fees we receive for processing payments.

During 2017 we processed approximately 2,102,065 payment transactions, compared to 1,624,931 in 2016, an increase of 29.4%.

For the year ended December 31, 2017, these transactions generated $3,941,273 in net revenue, of which approximately $3,343,833 (2016: 2,182,907) is net revenue derived from the operations of QPagos S.A.P.I. de C.V. and $597,440 (2016: $508,989) is net revenue derived from the operations of Redpag. We earn a gross profit of approximately 5.9% (2016: 7.5%) on airtime sales on kiosks operated by Redpag and approximately 0.1% gross profit on wholesale operations by which we provide air time and services to other non-kiosk distributors. We also earn commissions on payment services we provide to end-users through our kiosks and kiosks operated by third parties. This fee is either a transactional based fee of between USD$0.50 and USD$0.75 per transaction or a percentage of the transaction value. Certain service providers require that we receive the entire fee solely from the customers.

Our agents (our distributors) buy kiosks or terminals from us for approximately $6,000. The agent retains a portion of the fees that we derive from the service providers for services performed at the kiosks. Typically, 65% to 70% of the fees we receive from service providers are shared with the agent that has purchased the kiosk, and we retain 30–35% of such fees.

In addition, for certain high traffic public areas, such as malls and shopping centers, government agencies and large retailers who want to monetize high traffic areas, we pay the owner of the space a rental fee for the use of the space, and revenue share a smaller % of the commission, typically 10%. We also generate monthly rental fees for collocating our kiosks in municipal offices and integrating their services into our platform.

3

Additionally, when a distributor integrates their services into QPagos platform, for transactions done at their kiosks we may charge a transaction fee that may average $0.10, while that same transaction may generate up to $0.50 when done in other kiosks in Qpagos network.

4

Partners-Service Providers

Our current focus has been on the prepaid mobile telephone market. In Mexico, 85% of the more than 109 million mobile subscribers are under prepaid programs, thus millions of people make payments into these plans on a frequent basis. We currently have integrated over 140 service providers, including all principal mobile operators in Mexico, major utilities and the national lottery system “Pronosticos”. Among these. Also, QPagos, S.A.P.I. de C.V has integrated 9 of Mexico’s 32 states in its payment platform, and citizens of these states can now pay at our kiosks, municipal services, such as car registration, property taxes, traffic tickets, etc.

Our Distribution Network

QPagos, S.A.P.I. de C.V is developing a distribution network along several verticals, principally: (i) an agent network of independent businesses with high customer traffic in which our kiosks can be deployed; (ii) retailers that seek to decongest teller lines and shift service payments to self-service kiosks, (iii) banks and other financial intermediaries that want to extend geographic collection points to their customers, while also improving the experience of their customers when making payments at branches, (iv) government municipalities that want to bring service payments closer to their citizens; (v) other electronic payments distributors who we wholesale our services to, and (vi) our own distributor Redpag Electrónicos with its growing network in Mexico City and adjoining states.

Agents who own kiosks and terminals are responsible for placing, operating and servicing them in high-traffic, convenient retail locations. Several of our agents are mid-sized businesses which we believe provides them with insight into local market dynamics. The agency agreements that we enter into are usually for an indefinite term and may be unilaterally terminated by either party. Our agent contracts do not have exclusivity clauses. We usually cap these fees, and normally award the agents a percentage of the merchant fees. No one agent represented a material amount of our revenue, and we do not view ourselves as being dependent upon any one agent.

Our retail and institutional clients and prospects include large retail and convenience store chains, whose tellers are being congested by service payments and who would like to move these frequent transactions to the front of their stores. We are also in field trials with large financial institutions that want to expedite collections of their financial services as well as expand their hours of operation and geographic reach; and state, government and local municipalities that want to provide their citizens easy access to payments. We recently concluded our trials with a 1,900 plus branch financial institution who is seeking to reduce transaction costs, and improve customer experience by reducing lines with our kiosks. We look forward to consolidating this market opportunity during 2018.

Research and Development Expenditure

We continuously develop our product offering and make technical improvements to our software, these expenses are incurred primarily as consulting fees paid to third party developers. In this area for example we have developed mobile applications to allow customers to access the same menu of service payments in our kiosks through their mobile devices as well as developing complex applications such as the National Lottery’s Pronosticos. We have spent approximately $80,000 for each of the years ended December 31, 2017 and 2016 on research and new product development.

Marketing

We participate in several local events and exhibitions and provide promotional materials to distributors and retailers. We have also engaged in public relations campaigns geared towards corporate and institutional businesses, which has resulted in discussions with large box retailers such as Walmart, OXXO, Casa Ley, 7-Eleven, Circle K and several others. We have participated frequently in several International Franchising Exhibitions in Mexico City, Guadalajara, Puebla, Ciudad Juarez and Monterrey, and yearly in ANTAD Guadalajara Exhibition, the association that groups the country’s mayor retail chains.

Our Technology

We run our network and process our transactions using the proprietary, advanced technology platform that we license, which leverages the latest virtualization, analytics and security technologies to create a fast, highly reliable, secure and redundant system. We believe that the breadth and reach of our network, along with the proprietary nature of the technology platform that we license, differentiates us from our competitors and allow us to effectively manage and update our services and realize significant operating leverage with growth in volumes.

We have adapted our technology to be device agnostic and today consumers can access our payment services through multiple devices, such as POS, Mobile, PC and self-service kiosks.

Competition

The payment services industry is highly competitive, and our continued growth depends on our ability to compete effectively. Although we do not face direct competition in exactly the same line of business, as no major self-service electronic payment kiosk vendors with a payments platform exists in Mexico today, we do face competition from teller-assisted operations at a variety of financial and non-financial business groups, including a few small regional players. These competitors include retail banks, non-traditional payment service providers, such as retailers and mobile network operators, traditional kiosk and terminal operators and electronic payment system operators, as well as other companies that provide various forms of payment services, including electronic payment and payment processing services. Competitors in our industry seek to differentiate themselves by features and functionalities such as speed, convenience, network size, accessibility, hours of operation, reliability and price. A significant number of our competitors have greater financial, technological and marketing resources than we have, operate robust networks and could decide to develop their own self-service kiosks solutions instead of buying from Qpagos.

5

We believe that the most serious competition comes from bricks and mortar locations since the bulk of the mobile top-up business is done at major retail chains such as Walmart, Soriana, Chedraui and convenience stores such as OXXO and 7-Eleven. For example, Monterrey-based OXXO, owned by Coca-Cola bottler FEMSA, with over 14,000 stores is the largest retailer network in Mexico with daily visits of over 8 million people. Because of this high concentration of customers, OXXO has become one of the primary destinations to top up prepaid phones as well as paying utility bills and other services. These brick and mortar retailers are also our key target market for QPAGOS as they are experiencing congestion at their in-person teller operations and are also exploring the alternative of expediting payments through the use of self-service kiosks. We are currently in dialogues with several of these retailers which want to address teller congestion caused by the large number of customers seeking to make bill payments which affects both their customers and their core business as a retailer.

Seasonality

We do not expect that our business will experience significant seasonality.

Government and Environmental Regulation and Laws

Currently our business is not impacted by government regulation. We may in the future be subject to a variety of regulations aimed at preventing money laundering and financing criminal activity and terrorism, financial services regulations, payment services regulations, consumer protection laws, currency control regulations, advertising laws and privacy and data protection laws and therefore expect to experience periodic investigations by various regulatory authorities in connection with the same, which may sometimes result in monetary or other sanctions being imposed on us. Many of these laws and regulations are constantly evolving and are often unclear and inconsistent with other applicable laws and regulations, making compliance challenging and increasing our related operating costs and legal risks. In particular, there has been increased public attention and heightened legislation and regulations regarding money laundering and terrorist financing. We may have to make significant judgment calls in applying anti-money laundering legislation and risk being found in non-compliance with such laws.

If local authorities in Mexico choose to enforce specific interpretations of the applicable legislation that differ from ours or enact new laws, we may be found to be in violation and subject to penalties or other liabilities. This could also limit our ability in effecting such payments going forward and may increase our cost of doing business.

In addition, there is significant uncertainty regarding future legislation on taxation of electronic payments in Mexico, including the place where taxation may be generated. Subsequent legislation and regulation and interpretations thereof, litigation, court rulings, or other events could expose us to increased costs, liability and reputational damage that could have a material adverse effect on our business, financial condition and results of operations.

Employees

As of December 31, 2017, QPAGOS had 2 full time employees, which are its chief executive officer and chief operating officer, and 27 full-time contractors provided to it by an outsourcing company and designated to perform services for its Mexican subsidiaries Qpagos and Redpag. Qpagos Corporation had no part-time employees. None of these employees are subject to collective bargaining agreements. Qpagos Corporation does not have employment agreements with any employees other than its Chief Executive Officer, Gaston Pereira and its Chief Operating Officer, Andrey Novikov. See “Executive Compensation.” Qpagos Corporation also enters into consulting arrangements for IT and operational services.

Corporate Information

Our principal offices are located at Paseo del la Reforma 404 Piso 15 PH, Col. Juarez, Del. Cuauhtémoc, Mexico, D.F. C.P. 06600, and our telephone number at that office is +52 (55) 55–110–110. We also have offices in the United States that are located at 1900 Glades Road, Suite 265, Boca Raton, Florida 33431. We maintain an Internet website at www.qpagos.com. Neither this website nor the information on this website is included or incorporated in, or is a part of, this Form 10-K.

Available Information

Our principal offices are located at Paseo del la Reforma 404 Piso 15 PH, Col. Juarez, Del. Cuauhtémoc, Mexico, D.F. C.P. 06600, and our telephone number at that office is +52 (55) 55–110–110. We also have offices in the United States that are located at 1900 Glades Road, Suite 280, Boca Raton, Florida 33431. We maintain an Internet website at www.qpagos.com. We have included our website address as a factual reference and do not intend it to be an active link to our website. We make available on our website, www.qpagos.com our Annual Reports on Form 10-K, quarterly Reports on Form 10-Q and Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. These reports are available free of charge through the investor relations page of our internet website as soon as reasonably practicable after those reports are filed with the SEC.

6

As a smaller reporting company, we are not required to provide disclosure regarding risk factors.

Item 1B. Unresolved Staff Comments

None

Qpagos leases approximately 1,600 square feet in Mexico City at Paseo de la Reforma 404, where its corporate offices are located. The lease is for a term of 36 months with a three-month termination clause. The current lease commenced in December 16, 2016, expires in December 16, 2019 and provides for an aggregate annual rent of approximately $40,519 per annum. We also lease space on a month-to month basis for our data servers at a monthly rate of $1,680. In addition, Qpagos leases warehouse space on a month-to-month basis for $625 per month. We believe these facilities are in good condition and adequate to meet our current and anticipated requirements.

From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties and an adverse result in these or other matters may arise from time to time that may harm our business. We are currently not aware of any such legal proceedings or claims that we believe will have a material adverse effect on our business, financial condition or operating results.

Item 4. Mine Safety Disclosures

Not applicable.

7

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchase of Equity Securities

From November 3, 2014 to July 4, 2016, our common stock has been traded on the OTC Pink Markets under the symbol “ASYP” but no trading took place during this time. Since July 5, 2016 our common stock has traded on the OTCQB and our symbol was changed to “QPAG” on June 2, 2016. The range of high and low sales prices for the period from July 5, 2016 thru March 31, 2018 is presented below:

| High | Low | |||||||

| YEAR ENDED DECEMBER 31, 2016 | ||||||||

| First Quarter | $ | — | $ | — | ||||

| Second Quarter | $ | — | $ | — | ||||

| July 5, 2016 (Third Quarter) | $ | 1.31 | $ | 0.55 | ||||

| Fourth quarter | $ | 0.94 | $ | 0.25 | ||||

| YEAR ENDED DECEMBER 31, 2017 | ||||||||

| First Quarter | $ | 0.55 | $ | 0.18 | ||||

| Second Quarter | $ | 0.49 | $ | 0.285 | ||||

| Third Quarter | $ | 0.40 | $ | 0.13 | ||||

| Fourth Quarter | $ | 0.35 | $ | 0.15 | ||||

| YEAR ENDED DECEMBER 31, 2018 | ||||||||

| First Quarter | $. | 0.25 | $ | 0.13 | ||||

| Second Quarter through April 13, 2018 | $ | 0.40 | $ | 0.18 | ||||

The last reported sale price of our common stock on the OTCQB on April 13, 2018, was $0.40 per share. As of April 13, 2018, there were approximately 49 holders of record of our common stock.

Dividend Policy

We have not paid any cash dividends on our common stock to date, and we have no intention of paying cash dividends in the foreseeable future. Whether we declare and pay dividends is determined by our Board of Directors at their discretion, subject to certain limitations imposed under Nevada corporate law. The timing, amount and form of dividends, if any, will depend on, among other things, our results of operations, financial condition, cash requirements and other factors deemed relevant by our Board of Directors.

Equity Compensation Plan Information

See Item 11 – Executive Compensation for equity compensation plan information.

Recent Sales of Unregistered Securities

Other than as set forth below or as previously disclosed in our filings with the Securities and Exchange Commission, we did not sell any equity securities during the year ended December 31, 2017 in transactions that were not registered under the Securities Act.

On October 3, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $48,880 to Strategic IR Corp. (“Strategic”) The note has a maturity date of October 3, 2018 and a coupon of eight percent (8%) per annum. We have the right to prepay the note without penalty for the first 180 days. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

On October 11, October 12 and October 26, 2017, we received three installments of $50,000 each from Vladimir Skigin totaling $150,000 and issued a Convertible Promissory Note in the aggregate principal amount of $150,000 to him. The note has a maturity date of October 10, 2018 and a coupon of 8% per annum. We have the right to prepay the note within the first 180 days at a premium of 110% of the sum of the accrued interest and principal. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

On October 23, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $14,298 to Strategic. The note has a maturity date of October 23, 2018 and a coupon of eight percent (8%) per annum. We have the right to prepay the note without penalty for the first 180 days. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

On October 31, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $50,000 to Viktoria Akhmetova. The note has a maturity date of October 20, 2018 and a coupon of eight percent (8%) per annum. We have the right to prepay the note within the first 180 days at a premium of 110% of the sum of the accrued interest and principal. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

8

On November 14, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $53,000 to Power Up Lending Group LTD. The note has a maturity date of August 30, 2018 and a coupon of eight percent (8%) per annum. We have the right to prepay the note without penalty for the first 180 days. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

On November 29, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $75,000 to JSJ Investments, Inc. The note has a maturity date of November 29, 2018 and a coupon of eight percent (8%) per annum. We have the right to prepay the note without penalty for the first 180 days. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

On November 27,2017 and December 13, 2017, we issued 203,516 and 168,466 shares of our common stock upon conversion of notes. The issuance was exempt from registration pursuant to section 3(a)(9) of the Securities Act. The shares were issued in exchange for the notes and no compensation was paid by the security holder in connection with the solicitation of the exchange.

On December 14, 2017, we issued a Convertible Promissory Note in the aggregate principal amount of $78,000 to Labrys Fund, LP. The note has a maturity date of June 14, 2018 and a coupon of eight percent (8%) per annum. In connection with the issuance of the note, we were required to issue 231,931 shares of common stock as a commitment fee valued at $76,537. The shares are returnable to us if no Event of Default has occurred prior to the date the note is fully repaid. Management had determined that it is probable that we would meet the conditions under the note and therefore it is more likely than not that we would not be in Default as defined in the note. As a result, management has concluded that it was probable that the shares would be returned and therefore the value of the 231,931 shares was not recorded. We have the right to prepay the note without penalty for the first 180 days. The outstanding principal amount of the note is convertible at any time and from time to time at the election of the holder into shares of our common stock at a conversion price equal to 60% of the average of the lowest three trading bid prices during the previous ten (10) trading days, including the date the notice of conversion is received.

Except as otherwise stated, the issuances of the securities were made in reliance on the exemption provided by Section 4(a)(2) of the Securities Act and Regulation D promulgated thereunder for the offer and sale of securities not involving a public offering. The recipients of securities in each of these transactions acquired the securities for investment only and not with a view to or for sale in connection with any distribution thereof, and appropriate legends were affixed to the securities issued in these transactions. Each of the recipients of securities in these transactions was an accredited investor within the meaning of Rule 501 of Regulation D under the Securities Act and had adequate access, through employment, business or other relationships, to information about us.

The issuance of the common stock was made in reliance on the exemption provided by Section 4(a)(2) of the Securities Act for the offer and sale of securities not involving a public offering, promulgated under the Securities Act.

Issuer Purchases of Equity Securities

There were no issuer purchases of equity securities during the fiscal year ended December 31, 2017.

Item 6. Selected Financial Data

Not applicable because we are a smaller reporting company.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with, and is qualified in its entirety by, our audited annual financial statements and the related notes thereto, each of which appear elsewhere in this Report on Form 10-K. This discussion contains certain forward-looking statements that involve risks and uncertainties, as described under the heading “About Forward-Looking Statements” in this Report on Form 10-K. Actual results could differ materially from those projected in the forward-looking statements. For additional information regarding these risks and uncertainties, please see the disclosure under the heading “Risk Factors” elsewhere in this Report on Form 10-K. The Management Discussion and Analysis of Financial Condition and Results of Operations below is based upon only the financial performance of QPAGOS.

Overview and Financial Condition

We are a provider of next generation physical and virtual payment services that we introduced to the Mexican market in the third quarter of 2014. We have a ten-year renewable exclusive license agreement for the use of technology that can be used to perform services that are similar to services that have been successfully deployed with this technology in several European, Asian, North and South American countries.

We provide an integrated network of kiosks, terminals and payment channels that enable consumers to deposit cash, convert it into a digital form and remit the funds to any merchant in our network quickly and securely. We help consumers and merchants connect more efficiently in markets and consumer segments, such as Mexico, that are largely cash-based and lack convenient alternatives for consumers to pay for goods and services in physical, online and mobile environments. For example, we license technology that can be used to pay bills, add minutes to mobile phones, purchase transportation tickets, shop online, buy digital services or send money to third parties.

9

Our current focus is on Mexico which remains a cash-dominated society for retail consumer payments with approximately 80% of the value of personal payments exchanged in cash (Bank of Mexico). The penetration of electronic payment services, such as credit and debit cards and point of sale terminals, significantly lags behind more developed economies. We believe that opportunities for our services in Mexico are vast. With over 109 million mobile subscribers in Mexico, 85% of which are under prepaid plans, mobile top-up alone, was a $13 billion business in 2017 as reported by the Competitive Intelligence Unit (the “CIU”). We believe that there is opportunity for growth in the Mexican market and has expanded to service providers beyond the mobile telephone operators to service provides of electricity, transportation, utilities, municipal services and taxes, consumer credit installments, insurance premiums, and many more. Altogether as of the first quarter of 2018 our platform had integrated over140 such services, including the National Lottery’s Pronosticos.

Our primary strategy in Mexico to date has been the attraction of service providers as well as the deployment of kiosks through Redpag Electrónicos, our kiosk management subsidiary. During the years ended December 31, 2017 and 2016, we generated net revenues of $3,941,273 and $2,691,896, respectively, from our operations in Mexico, a 46.4% increase. Our primary source of revenue are fees we receive for processing payments made by consumers to service providers. We also generate revenue from non-payment services such as kiosk sales. Qpagos Corporation currently has in excess of 140 service providers integrated into its payment gateway, which includes all mobile phone providers in Mexico as well as most utility companies, financial services, entertainment venues and others. As of December 31, 2017, Qpagos Corporation deployed over 228 kiosks and terminals and we service an additional 440 kiosks of independent distributors. Our kiosks and terminals can be found at convenience stores, next to metro stations, retail stores, airport terminals, education centers, and malls in major urban centers, as well as many small and rural towns.

Management Discussion and Analysis of Financial Condition

The discussion and analysis of our financial condition and results of operations are based upon the consolidated financial statements as of December 31, 2017 and 2016, of QPAGOS, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of any contingent liabilities at the financial statement date and reported amounts of revenue and expenses during the reporting period. On an on-going basis we review our estimates and assumptions. The estimates are based on our historical experience and other assumptions that we believe to be reasonable under the circumstances. Actual results are likely to differ from those estimates under different assumptions or conditions.

Results of Operations for the years Ended December 31, 2017 and December 31, 2016

Net revenues in Qpagos Corporation were $3,941,273 and $2,691,896 for the year ended December 31, 2017 and 2016 respectively, an increase of $1,249,377 or 46.4%. Qpagos Corporation operates in Mexico and its functional currency is the Mexican Peso. Qpagos Corporation’s revenue in Mexican Pesos increased to MXN 74,516,037 from MXN 50,308,314 for the year ended December 31, 2017 and 2016, respectively, an increase of MXN 24,207,723 or 48.1%. The increase in revenue in MXN terms is primarily due to an increase in the volume of prepaid airtime sold, directly attributable to the increased activity in its wholesale payments business and we also increased the number of our customers over the prior year. The average US$ exchange rate has strengthened against the MXN over the prior year, from $18.6692 to $18.9066 or 1.3%, which results in a lower revenue growth in US $ terms of approximately $50,116.

Cost of goods sold

Cost of goods sold in Qpagos Corporation was $3,913,953 and $2,595,012 for the years ended December 31, 2017 and 2016, respectively, an increase of $1,318,941 or 50.8%. Qpagos operates in Mexico and its functional currency is the Mexican Peso. Qpagos Corporation’s cost of sales in Mexican Pesos increased to MXN 73,999,501 from MXN 48,467,539 for the year ended December 31, 2017 and 2016, respectively, an increase of MXN 25,531,962 or 52.7%. The increase in cost of sales in MXN terms is primarily due to the increase in the volume of prepaid airtime sold which is directly attributable to the increased activity of its wholesale business during the current year. Cost of goods consists primarily of services acquired from third parties, such as prepaid air time and the cost of the kiosks and any retrofitted components. Also included in cost of sales is depreciation related to those kiosks that are used in the production of income. Depreciation expenses was $36,518 and $37,244, for the years ended December 31, 2017 and 2016, respectively, a decrease of $726. The average US $ exchange rate has strengthened against the MXN over the prior year, from $18.6692 to $18.9066 or 1.3%, which results in a lower cost of sales in US $ terms of approximately $49,762.

Gross profit

Gross profit was $27,320 and $96,884 for the years ended December 31, 2017 and 2016, respectively, a decrease of $69,564 or 71.8%. Qpagos Corporations operates in Mexico and our functional currency is the Mexican Peso. The components of gross profit are as follows:

| ● | Gross profit on sales of services decreased from a gross profit of $54,749 to a gross profit of $38,759, for the years ended December 31, 2016 and 2017, respectively, a decrease of $15,990. The decrease in gross profit is primarily due to the mix of our business shifting towards wholesale customers at lower margins and lower growth in our own managed kiosk business. |

10

| ● | Gross profit on kiosk sales decreased from a gross profit of $80,858 to a gross profit of $3,990 for the years ended December 31, 2016 and 2017, respectively, a decrease of $76,868. The decrease is primarily attributable to a delay in an expected order from a large financial institution to 2018. |

| ● | Gross (loss) profit other increased from a gross loss of ($1,479) to a gross profit of $21,089 for the years ended December 31, 2016 and 2017, respectively, an increase of $22,568. The improvement in the gross profit is due to once-off maintenance expenditure incurred on kiosks in the prior year. |

| ● | Included in gross profit is depreciation related to those kiosks that are used in the production of income. Depreciation expenses was $36,518 and $37,244, for the years ended December 31, 2017 and 2016, respectively, a decrease of $726. |

Total expenses

Total expenses in Qpagos Corporation were $2,268,522 and $4,380,182 for the years ended December 31, 2017 and 2016, respectively, a decrease of $2,111,660 or 48.2%.

Total expenses consisted primarily of the following:

| a. | General and administrative expenditure was $2,196,213 and $4,312,107 for the years ended December 31, 2017 and 2016, respectively, a decrease of $2,115,894 or 49.1%. Qpagos Corporation has operations in Mexico and a US holding company presence which incurs some expenditure. |

| i. | The general and administrative expenditure in Mexico decreased to MXN 14,837,629 from MXN 22,731,911 for the years ended December 31, 2017 and 2016, respectively, a decrease of MXN 7,894,282 or 34.7%. The decrease is primarily due to a reduction in payroll expenses of MXN1,261,731, lower marketing related expenses of MXN 483,422, a decrease in consulting expenses of MXN4,099,137 and various other cost saving initiatives. |

| ii. | The general administrative expenses incurred by Qpagos Corporation in the US, amounted to $1,411,392 and $3,084,747 for the years ended December 31, 2017 and 2016, respectively, a decrease of $1,673,355 or 54.2%. The decrease is primarily due to: |

| ● | non-cash compensation of $2,032,275 related to share based consulting agreements in the prior year, offset by; |

| ● | an increase in management fees of $783,321 and $557,358 for the years ended December 31, 2017 and 2016, respectively, an increase of $225,963 or 40.5%, primarily due to compensation paid to our CEO which was absorbed by the Mexican operations in the prior year; |

| ● | a capital raising fee of $303,407 incurred on the issue of convertible notes, the repurchase of some of these notes and various professional fees associated with these notes. |

| ● | Various other cost saving initiatives introduced to reduce the overall overhead burden on the Company. |

Other income

Other (expense) income of the Company was $(166,432) and $788 for the years ended December 31, 2017 and 2016, respectively. Other expense consisted of losses made on the conversion of debt to equity during the year at discounts to market prices, in terms of the various convertible note agreements entered into during the current year.

Interest expense, net

Interest expense, net was $2,071,781 and $54,610 for the years ended December 31, 2017 and 2016, respectively, an increase of $2,017,171. The interest expense in the current year includes the amortization of non-cash debt discount of $1,919,030 and interest expense of $152,751, consisting of interest on the convertible notes, including penalty interest of $45,500 on early note settlements. The debt discount is calculated at note inception based on the fair market value of the underlying equity of variably priced convertible notes and certain warrants. The interest expense in the prior year of $54,610 was incurred on a note payable to an investor.

Change in fair value of derivative liability

The change in fair value of derivative liabilities was $(330,134) and $(36,074) for the years ended December 31, 2017 and 2016, respectively. The movements in derivative liabilities represents the mark-to-market of underlying conversion features of debt and warrant securities and is dependent on the market price of the Company’s stock and the volatility underpinning our stock.

Foreign currency gain (loss)

The foreign currency gain (loss) in Qpagos Corporation was $178,555 and ($357,855) for the years ended December 31, 2017 and 2016, respectively, an increase of $536,410 or 149.9%. The increase is primarily due to a reduction of liabilities denominated in US$’s in our Mexican operations. There were significant intercompany balances between the US holding company and the Mexican subsidiaries which arose during the 2017 year, which were subsequently capitalized.

11

Net loss

We incurred a net loss of $4,630,994 and $4,731,049, for the years ended December 31, 2017 and 2016, respectively, a decrease of $100,055 or approximately 2.1%, primarily due to the lower expenses, discussed above, offset by the non-cash amortization of debt discount during the current year.

Liquidity and Capital Resources

To date, our primary sources of cash have been funds raised from the sale of our securities and the issuance of debt as well as revenue derived from operations.

We incurred an accumulated deficit of $13,388,991 through December 31, 2017 and incurred negative cash flow from operations of $1,907,581 and $1,929,453 for the years ended December 31, 2017 and 2016, respectively. We have spent, and need to continue to spend, substantial amounts in connection with implementing our business strategy, including our planned product development effort and will be required to raise additional funding.

At December 31, 2017, we had cash of $19,028 and a working capital deficit of $4,696,182. We believe that the current cash balances together with revenue anticipated to be generated from operations will not be sufficient to meet our current working capital needs and as mentioned above, we will seek further funding from either equity issues or further debt funding, should we not be successful, we may have to curtail our operations significantly.

During the year ended December 31, 2017, the Company raised $404,916 in notes payable and a further $1,832,253 of short-term convertible debt from the issuance of debt securities, to fund the operations of the business. During 2017, $94,267 in convertible loans were exchanged for 753,424 shares of common stock.

Subsequent to December 31, 2017 we raised the following additional funds:

| ● | An additional $327,500 in variably priced convertible securities with short term maturities of one year or less. |

| ● | An additional $155,500 from an investor in funds that have not been designated as yet. |

During the year ended December 31, 2017, we purchased and capitalized $17,538 in kiosks.

We have notes payable from related parties and convertible notes payable, all with maturities of less than one year. The notes payable from related parties amounts to $349,916 and our convertible notes payable from related parties has an aggregate principal outstanding of $1,152,070 and accrued interest thereon as of December 31, 2017 of $31,231, The convertible notes payable to non-related parties amounted to an aggregate principal of $1,341,964 , and accrued interest thereon of $49,971. Other than the above we have minimal commitments which include a lease of an office facility with a future commitment of $40,500 in each of the years 2018 and 2019.

We entered into an additional ten-year licensing agreement with the Licensor on May 1, 2015, whereby we are committed to pay an annual license fee in quarterly installments of $5,000 ($20,000 per annum) to the Licensor for an exclusive license for the Mexican market of certain revenue payment services.

Our primary financial commitments as of the date hereof are payments owed commitments due under the license agreement is summarized as follows:

|

Amount |

||||

|

2018 |

$ |

20,100 |

||

|

2019 |

20,100 |

|||

|

2020 |

20,100 |

|||

|

2021 |

20,100 |

|||

|

2022 and thereafter |

67,167 |

|||

|

$ |

147,567 |

|||

Capital Expenditures

None.

12

Critical Accounting Policies

| a) | Use of Estimates |

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions, which are evaluated on an ongoing basis, that affect the amounts reported in the consolidated financial statements and accompanying notes. Management bases its estimates on historical experience and on various other assumptions that it believes are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the amounts of revenues and expenses that are not readily apparent from other sources. Actual results could differ from those estimates and judgments. In particular, significant estimates and judgments include those related to: the estimated useful lives for plant and equipment, the fair value of warrants and stock options granted for services or compensation, estimates of the probability and potential magnitude of contingent liabilities, derivative liabilities, the valuation allowance for deferred tax assets due to continuing operating losses, those related to revenue recognition and the allowance for doubtful accounts.

Making estimates requires management to exercise significant judgment. It is at least reasonably possible that the estimate of the effect of a condition, situation or set of circumstances that existed at the date of the consolidated financial statements, which management considered in formulating its estimate could change in the near term due to one or more future confirming events. Accordingly, the actual results could differ significantly from our estimates.

| b) | Contingencies |

Certain conditions may exist as of the date the financial statements are issued, which may result in a loss to us but which will only be resolved when one or more future events occur or fail to occur. Our management assesses such contingent liabilities, and such assessment inherently involves an exercise of judgment.

If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in our consolidated financial statements. If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material would be disclosed. Loss contingencies considered to be remote by management are generally not disclosed unless they involve guarantees, in which case the guarantee would be disclosed.

| c) | Fair Value of Financial Instruments |

We adopted the guidance of Accounting Standards Codification (“ASC”) 820 for fair value measurements which clarifies the definition of fair value, prescribes methods for measuring fair value, and establishes a fair value hierarchy to classify the inputs used in measuring fair value as follows:

Level 1-Inputs are unadjusted quoted prices in active markets for identical assets or liabilities available at the measurement date.

Level 2-Inputs are unadjusted quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets and liabilities in markets that are not active, inputs other than quoted prices that are observable, and inputs derived from or corroborated by observable market data.

Level 3-Inputs are unobservable inputs which reflect the reporting entity’s own assumptions on what assumptions the market participants would use in pricing the asset or liability based on the best available information.

The carrying amounts reported in the balance sheets for cash, accounts receivable, other current assets, other assets, accounts payable, accrued liabilities, and notes payable, approximate fair value due to the relatively short period to maturity for these instruments. The Company has identified the short term convertible notes and certain warrants attached to certain of the notes that are required to be presented on the balance sheets at fair value in accordance with the accounting guidance.

ASC 825–10 “Financial Instruments” allows entities to voluntarily choose to measure certain financial assets and liabilities at fair value (fair value option). The fair value option may be elected on an instrument-by-instrument basis and is irrevocable unless a new election date occurs. If the fair value option is elected for an instrument, unrealized gains and losses for that instrument should be reported in earnings at each subsequent reporting date. We evaluate the fair value of variably priced derivative liabilities on a quarterly basis and report any movements thereon in earnings.

| d) | Accounts Receivable and Allowance for Doubtful Accounts |

Accounts receivable are reported at realizable value, net of allowances for doubtful accounts, which is estimated and recorded in the period the related revenue is recorded. We have a standardized approach to estimate and review the collectability of its receivables based on a number of factors, including the period they have been outstanding. Historical collection and payer reimbursement experience is an integral part of the estimation process related to allowances for doubtful accounts. In addition, we regularly assess the state of our billing operations in order to identify issues, which may impact the collectability of these receivables or reserve estimates. Revisions to the allowance for doubtful accounts estimates are recorded as an adjustment to bad debt expense. Receivables deemed uncollectible are charged against the allowance for doubtful accounts at the time such receivables are written-off. Recoveries of receivables previously written-off are recorded as credits to the allowance for doubtful accounts. There were no recoveries during the years ended December 31, 2017 and 2016.

13

| e) | Inventory |

We primarily value inventories at the lower of cost or net realizable value on a first-in, first-out basis. We identify and write down our excess and obsolete inventories to net realizable value based on usage forecasts, order volume and inventory aging. With the development of new products, we also rationalize our product offerings and will write-down discontinued product to the lower of cost or net realizable value.

| f) | Intangibles |

All of our intangible assets are subject to amortization. We evaluate the recoverability of intangible assets periodically by taking into account events or circumstances that may warrant revised estimates of useful lives or that indicate the asset may be impaired. Where intangibles are deemed to be impaired we recognize an impairment loss measured as the difference between the estimated fair value of the intangible and its book value.

| g) | License Agreements |

License agreements acquired by us are reported at acquisition value less accumulated amortization and impairments.

Amortization

Amortization is reported in the statement of operations and comprehensive loss on a straight-line basis over the estimated useful life of the intangible assets unless the useful life is indefinite. Amortizable intangible assets are amortized from the date that they are available for use. The estimated useful life of the license agreement is five years which is the expected period for which we expect to derive a benefit from the underlying license agreements.

| h) | Long-Term Assets |

Assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to future undiscounted net cash flows expected to be generated by the asset. If such assets are considered impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets.

| i) | Revenue Recognition |

Our revenue recognition policy is consistent with the requirements of Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 605, Revenue Recognition (ASC 605). In general, we record revenue when it is realized, or realizable and earned. We consider revenue to be realized, or realizable and earned when, persuasive evidence of an arrangement exists, the products or services have been approved by the customer after delivery and/or installation acceptance or performance of services; the sales price is fixed or determinable within the contract; and collectability is reasonably assured.

We have the following sources of revenue which is recognized on the basis described below.

| ● | Revenue from the sale of services. |

Prepaid services are acquired from providers and is sold to end-users through kiosks that we own or kiosks that are owned by third parties. We recognize the revenue on the sale of these services when the end-user deposits funds into the terminal and the prepaid service is delivered to the end-user. The revenue is recognized at the gross value, including margin, of the prepaid service to us, net of any value-added tax which is collected on behalf of the Mexican Revenue Authorities.

| ● | Payment processing provided to end-users |

We provide a secure means for end-users to pay for certain services, such as utilities through our kiosks. We earn either a fixed per-transaction fee or a fixed percentage of the service sold. We act as a collection agent and recognize the payment processing fee, net of any value-added taxes collected on behalf of the Mexican Revenue Authorities, when the funds are deposited into the kiosk and the customer has settled his liability or has acquired a prepaid service.

| ● | Revenue from the sale of kiosks. |

We import, assemble and sell kiosks that are used to generate the revenues discussed above. Revenue is recognized on the full value of the kiosks sold, net of any valued added taxation collected on behalf of the Mexican Revenue Authorities, when the customer takes delivery of the kiosk and all the risks and rewards of ownership are passed to the customer.

14

We do not enter into any leasing of kiosks arrangements with customers and we do not generate any revenues from merchants who access our terminals as yet.

| j) | Share-Based Payment Arrangements |

Generally, all forms of share-based payments, including stock option grants, restricted stock grants and stock appreciation rights are measured at their fair value on the awards’ grant date, based on the estimated number of awards that are ultimately expected to vest. Share-based compensation awards issued to non-employees for services rendered are recorded at either the fair value of the services rendered or the fair value of the share-based payment, whichever is more readily determinable. The expense resulting from share-based payments is recorded in operating expenses in the consolidated statement of operations.

Prior to our reverse merger which took place on May 12, 2016, all share-based payments were based on management’s estimate of market value of our equity. The factors considered in determining managements estimate of market value includes, assumptions of future revenues, expected cash flows, market acceptability of our technology and the current market conditions. These assumptions are complex and highly subjective, compounded by the business being in its early stage of development in a new market with limited data available.

Where equity transactions with arms-length third parties, who had applied their own assumptions and estimates in determining the market value of our equity, had taken place prior to and within a reasonable time frame of any share-based payments, the value of those share transactions have been used as the fair value for any share-based equity payments.

Where equity transactions with arms-length third parties, included both shares and warrants, the value of the warrants have been eliminated from the unit price of the securities using a Black-Scholes valuation model to determine the value of the warrants. The assumptions used in the Black Scholes valuation model includes market related interest rates for risk-free government issued treasury securities with similar maturities; the expected volatility of our common stock based on companies operating in similar industries and markets; our estimated stock price; the expected dividend yield of the Company and; the expected life of the warrants being valued.

Subsequent to our reverse merger which took place on May 12, 2016, we had utilized the market value of our common stock as quoted on the NASDAQ OTCQB, as an indicator of the fair value of our common stock in determining share- based payment arrangements.

Off Balance Sheet Arrangements

None.

Contractual Obligations

|

Payments due by period |

||||||||||||||||||||

|

Total |

Less than 1

|

1 -3 years |

3 - 5 years |

More than 5

|

||||||||||||||||

|

Operating lease obligations |

$ |

71,782 |

$ |

35,891 |

$ |

35,891 |

$ |

— |

$ |

— |

||||||||||

|

Licenses |

$ |

147,567 |

$ |

20,100 |

$ |

60,300 |

$ |

60,300 |

$ |

6,867 |

||||||||||

|

$ |

219,349 |

$ |

55,991 |

$ |

96,191 |

$ |

60,300 |

$ |

6,867 |

|||||||||||

Inflation

The effect of inflation on the Company’s operating results was not significant.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Not applicable because we are a smaller reporting company.

15

Item 8. Financial Statements and Supplemental Data

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To

the Board of Directors and Stockholders of

QPAGOS

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of QPAGOS and subsidiaries as of December 31, 2017 and 2016, and the related consolidated statements of operations and comprehensive loss, statement of changes in stockholders’ (deficit) equity, and cash flows for each of the years in the two-year period ended December 31, 2017, and the related notes (collectively referred to as the notes to consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2017 and 2016, and the consolidated results of its operations and its cash flows for each of the years in the two-year period ended December 31, 2017, in conformity with accounting principles generally accepted in the United States of America.

The Company’s Ability to Continue as a Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 3 to the consolidated financial statements, the Company has incurred a loss since inception and has not generated sufficient revenue to cover its operating expenditures, raising substantial doubt about the Company’s ability to continue as going concern. Management’s evaluation of the events and conditions and management’s plans regarding these matters are also described in Note 3. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

| /s/ RBSM LLP |

| We have served as the Company’s auditor since 2014. |

| Henderson, NV |

| April 17, 2018 |

F-1

QPAGOS

December 31,

|

December 31,

|

|||||||

Assets |

||||||||

Current Assets |

||||||||

Cash |

$ |

19,028 |

$ |

46,286 |

||||

Accounts receivable |

59,628 |

79,943 |

||||||

Inventory |

504,794 |

350,273 |

||||||

Recoverable IVA taxes and credits |

215,990 |

353,780 |

||||||

Other current assets |

288,687 |

279,878 |

||||||

Total Current Assets |

1,088,127 |

1,110,160 |

||||||

Non-Current Assets |

||||||||

Plant and equipment, net |

160,301 |

231,328 |

||||||

Intangibles, net |

125,417 |

168,417 |

||||||

Investment – related party |

3,000 |

3,000 |

||||||

Other assets |

6,950 |

9,847 |

||||||

Total Non-Current Assets |

295,668 |

412,592 |

||||||

Total Assets |

$ |

1,383,795 |

$ |

1,522,752 |

||||

Liabilities and Stockholders’ (Deficit) Equity |

||||||||

Current Liabilities |

||||||||

Accounts payable |

$ |

446,032 |

$ |

320,487 |

||||

Loans payable – Related parties |

349,916 | — | ||||||

Notes payable |

— |

323,462 |

||||||

Notes payable – related parties |

— |

203,288 |

||||||

Convertible debt, net of unamortized discount of $652,563 and $75,888, respectively |

724,776 |

1,180 |

||||||

Convertible debt – related parties, net of unamortized discount of $338,709 |

859,190 |

— |

||||||

Derivative liability |

3,277,621 |

113,074 |

||||||

IVA and other taxes payable |

7,178 |

166,108 |

||||||

Advances from customers |

119,597 |

132,133 |

||||||

Total Current Liabilities |

5,784,310 |

1,259,732 |

||||||

Total Liabilities |

5,784,310 |

1,259,732 |

||||||

Stockholders’ (Deficit) Equity |

||||||||

Preferred stock, $0.0001 par value; 25,000,000 shares authorized, no preferred shares issued and outstanding at December 31, 2017 and 2016, respectively |

— |

— |

||||||

Common stock, $0.0001 par value; 100,000,000 shares authorized, 56,207,424 and 55,454,000 shares issued and outstanding as of December 31, 2017 and December 31, 2016, respectively. |

5,620 |

5,545 |

||||||

Additional paid-in-capital |

8,494,502 |

8,284,522 |

||||||

Accumulated deficit |

(13,388,191 |

) |

(8,757,197 |

) | ||||

Accumulated other comprehensive income |

487,554 |

730,150 |

||||||

Total Stockholders’ (Deficit) Equity |

(4,400,515 |

) |

263,020 |

|||||