Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - XG SCIENCES INC | s109452_ex31-1.htm |

| EX-32.1 - EXHIBIT 32.1 - XG SCIENCES INC | s109452_ex32-1.htm |

| EX-10.5 - EXHIBIT 10.5 - XG SCIENCES INC | s109452_ex10-5.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934: |

| For the fiscal year ended: December 31, 2017 | |

| ☐ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934: |

| For the transition period from: |

| XG SCIENCES, INC. | ||||

| (Exact name of registrant

as specified in its charter) |

| Michigan | 333-209131 | 20-4998896 | ||

| (State or other jurisdiction

of incorporation or organization) |

(Commission File No.) | (I.R.S. Employer

Identification No.) |

3101 Grand Oak Drive

Lansing, MI 48911

(Address of principal executive offices) (zip code)

(517) 703-1110

(Issuer Telephone number)

Securities registered under Section 12(b) of the Act: None.

Securities registered under Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐ No ☒

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes ☒ No ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes ☐ No ☒

Indicate by check mark whether the registrant is a large accelerated filer, and accelerated filer, a non-accelerated filer, or a smaller reporting company, and whether the registrant is an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer (Do not check if a smaller reporting company) ☐ | Smaller reporting company ☒ |

Emerging growth company ☒

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

As of June 30, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $13,940,528, based on the price at which the common equity was last sold (i.e., $8.00 per share).

The number of shares outstanding of the registrant’s Common Stock, no par value per share, as of April 2, 2018 was 2,555,275.

1

TABLE OF CONTENTS

2

Note Regarding Forward-Looking Statements:

The information in this Annual Report on Form 10-K contains “forward-looking statements” and information within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) relating to XG Sciences, Inc., a Michigan corporation and its subsidiary, XG Sciences IP, LLC, a Michigan corporation (collectively referred to as “we”, “us”, “our”, “XG Sciences”, “XGS”, or the “Company”), which are subject to the “safe harbor” created by those sections. These forward-looking statements include, but are not limited to, statements concerning our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements.

These forward-looking statements involve known and unknown risks and uncertainties that could cause our actual results, performance or achievements to differ materially from those expressed or implied by the forward-looking statements, including, without limitation, the risks set forth on beginning on page 13 under the section entitled “Risk Factors” herein.

XG Sciences was formed in May 2006 for the purpose of commercializing certain technology to produce graphene nanoplatelets. First isolated and characterized in 2004, graphene is a single layer of carbon atoms configured in an atomic-scale honeycomb lattice. Among many noted properties, monolayer graphene is harder than diamonds, lighter than steel but significantly stronger, and conducts electricity better than copper. Graphene nanoplatelets are particles consisting of multiple layers of graphene. Graphene nanoplatelets have unique capabilities for energy storage, thermal conductivity, electrical conductivity, barrier properties, lubricity and the ability to impart physical property improvements when incorporated into plastics or other matrices.

We believe the unique properties of graphene and graphene nanoplatelets will enable numerous new product applications and the market for such products will quickly grow to be a significant market opportunity. Our business model is to design, manufacture and sell advanced materials we call xGnP® graphene nanoplatelets and value-added products incorporating xGnP® nanoplatelets. We currently have hundreds of customers trialing our products for numerous applications, including, but not limited to lithium ion batteries, lead acid batteries, thermally conductive adhesives, composites, thermal transfer fluids, thermal management and heat transfer, inks and coatings, printed electronics, construction materials, cement, and military uses. We believe our proprietary processes have enabled us to be a low-cost producer of high quality, graphene nanoplatelets and value-added integrated products containing graphene nanoplatelets and that we are well positioned to address a wide range of end-use applications.

Our Customers

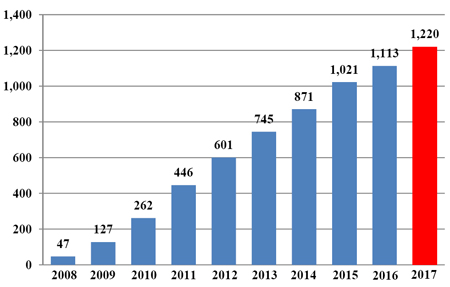

We sell products to customers around the world and have sold materials to over 1,000 customers in 47 countries since 2008. Some of these customers are research organizations and some are commercial organizations. Our customers have included well-known automotive and OEM suppliers around the world (Ford, Johnson Controls, Magna, Honda Engineering) world-scale lithium ion battery manufacturers in the US, South Korea and China (Samsung SDI, LG Chemical, Lishen, A123) and diverse specialty material companies (3M, BASF, Henkel, Dow Chemical, DuPont) as well as leading research centers such as Lawrence Livermore National Laboratory and Oakridge National Laboratory. We have also licensed some of our base manufacturing technology to other companies and we consider technology licensing a component of our business model. Our licensees include POSCO, the fourth largest steel manufacturer in the world by volume of output, and Cabot Corporation (“Cabot”), a leading global specialty chemicals and performance materials company. These licensees further extend our technology through their customer networks. Ultimately, we expect to benefit from royalties on sales of xGnP® nanoplatelets produced and sold by our licensees. As can be seen in the below bar chart, the cumulative number of customers has steadily grown over the last ten years.

3

Cumulative Customers, by Year

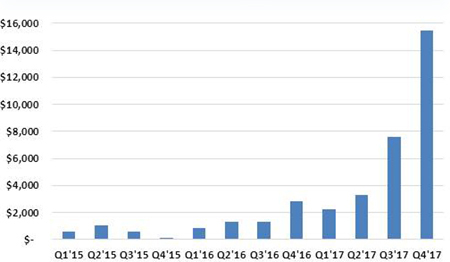

We believe average order size is an indicator of commercial traction. The majority of our customers are still ordering in smaller quantities consistent with their development and engineering qualification work. As can be seen in the chart below, our quarterly average order size was relatively modest until 2017, when a number of customers reached commercial status with different product applications. These data represent orders shipped in the respective quarter and exclude no charge orders targeted mainly for R&D purposes. The data show that the average order size has increased steadily over the last two years, and we believe that it will continue to increase in in 2018 as more customers commercialize products using our materials. As a result of this increasing order size, in 2017 our customer shipments increased by over 600% to almost 18 metric tons of products from the 2.5 metric tons shipped in 2016.

Average Order Size of Fulfilled Orders

Our Products

Bulk Materials. We target our xGnP® nanoplatelets for use in a wide range of large and growing end-use markets. Our proprietary manufacturing processes allow us to produce nanoplatelets with varying performance characteristics that can be tuned to specific end-use applications based on customer requirements. We currently offer four commercial “grades” of bulk graphene nanoplatelet materials, each of which is available in various particle sizes, which allows for surface areas ranging from 50 to 800 square meters per gram of material depending on the product. Other grades may be made available, depending on the needs for specific applications. In addition, we sell our xGnP® graphene nanoplatelets in the form of pre-dispersed mixtures with water, alcohol, or other organic solvents and resins. In addition to selling bulk nanoplatelets, we also offer the following integrated, value-added products that contain our graphene nanoplatelets in various forms.

4

Composites. These consist of compositions of specially designed xGnP® graphene nanoplatelets formulated in pre-dispersed mixtures that can be easily dispersed in various polymers. Our integrated composites portfolio includes pre-compounded resins derived from a range of thermoplastics as well as mother batches of resins and xGnP® nanoplatelets and their combination with resins and fibers for use in various end-use applications that may include industrial, automotive and sporting goods and which have demonstrated efficacy in standard injection molding, compression molding, blow molding and 3-D processes, to name but a few. In addition, we offer various bulk materials with demonstrated efficacy in plastic composites to impart improved physical performance to such matrices, which may be supplied as dry powders or as aqueous or solvent-based dispersions or cakes. We have also targeted use of our graphene nanoplatelets as an additive in cement mixtures, which we believe results in improved barrier resistance, durability, toughness and corrosion protection. Our GNP® Concrete Additive promotes the formation of more uniform and smaller grain structure in the cement. This fine-grain and uniform structure gives concrete improvements in flexural and compressive strength. In addition, the embedded graphene nanoplatelets will stop cracks from forming and retard crack propagation, should any cracks form – the combination of which will improve lifetime and durability of cement.

Energy Storage Materials. These consist of specialty advanced materials that have been formulated for specific applications in the energy storage segment. Chief among these is our proprietary, specially formulated silicon-graphene composite material (also referred to as “SiG” or “XG SiG®”) for use in lithium-ion battery anodes. XG SiG® targets the never-ending need for higher battery capacity and longer life. In several customer trials, our SiG material has demonstrated the potential to increase battery energy storage capacity by 3-5x what is currently available with conventional lithium ion batteries today. Additionally, we offer various bulk materials for use as conductive additives for cathodes and anodes in lithium-ion batteries, as an additive to anode slurries for lead-carbon batteries, as a component in coatings for current collectors in lithium-ion batteries and we are investigating the use of our materials as part of other battery components.

Inks and Coatings. These consist of specially-formulated dispersions of xGnP® together with solvents, binders, and other additives to make electrically or thermally conductive products designed for printing or coating and which are showing promise in diverse customer applications such as advanced packaging, electrostatic dissipation and thermal management. We also offer a set of standardized ink formulations suitable for printing. These inks offer the capability to print electrical circuits or antennas and may be suitable for other electrical or thermal applications as well. All of these formulations can be customized for specific customer requirements.

Thermal Management Materials. These consist mainly of two types of products, our XG Leaf® sheet products and various thermal interface materials (“TIM”) in the form of custom greases or pastes. XG Leaf® is a family of sheet products ideally suited for use in thermal management in portable electronics, which may include cell phones, tablets and notebook PC’s. As these devices continue to adopt faster electronics, higher data management capabilities, brighter displays with ever increasing definition, they generate more and more heat. Managing that heat is a key requirement for the portable electronics market and our XG Leaf® product line is well suited to address the need. These sheets are made using special formulations of xGnP® graphene nanoplatelets as precursors, along with other materials for specific applications. There are several different types of XG Leaf® available in various thicknesses, depending on the end-use requirements for thermal conductivity, electrical conductivity, or resistive heating. Our custom XG TIM® greases and pastes are also designed to be used in various high temperature environments. Additionally, we offer various bulk materials for use as active components in liquids, coatings and plastic composites to impart improved thermal management performance to such matrices.

Our Focus Areas

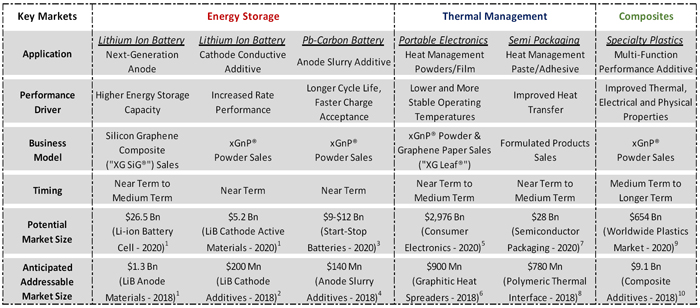

We believe we are a “platform play” in advanced materials, because our proprietary processes allow us to produce varying grades of graphene nanoplatelets that can be mapped to a variety of applications in many market segments. However, we are prioritizing our efforts in specific areas and with specific customers that we believe represent opportunities for either relatively near-term revenue or especially large and attractive markets. At this time, we are focused on three high priority areas: Energy Storage, Thermal Management and Composites. The following table shows examples of the types of applications we are pursuing, the expecting timing of revenue and the addressable market size of selected market opportunities.

5

XGS Market/Application Focus Areas & 2018 Market Size

| (1) Avicenne Energy, “The Worldwide Rechargeable Battery Market 2014 - 2025”, 24th Edition - V3, July 2015. |

| (2) Avicenne Energy, The Battery Show; Novi, MI; September 2017. |

| (3) Avicenne Energy, The Battery Show; Novi, MI; September 2017. & Internal Estimates. |

| (4) ArcActive via Nanalyze, April 3, 2015. |

| (5) ArcActive via Nanalyze, April 3, 2015 & Internal Estimates. |

| (6) Future Markets Insights, “Consumer Electronics Market: Global Industry Analysis and opportunity Assessment 2015 - 2020”, May 8, 2015. |

| (7) Prismark, “Market Assessment: Thin Carbon-Based Heat Spreaders”, August 2014. |

| (8) Reporterlink.com, “Semiconductor & IC Packaging Materials Market…”, May 2014. |

| (9) Prismark, 2015. |

| (10) Grand View Research, “Global Plastics Market Analysis…”, August 2014. |

| (11) From (10) and internal estimates: 2018 = 305 million tons of plastic, if 10% of the market adopted xGnP® to enhance their properties, and at only 1% by weight as an additive, then in 2018 305,000 tons or 305,000,000 kilos of xGnP® would be required. At $30 a Kg - the value is $9.1 Bn per year. |

Commercialization Process

Because graphene is a new material, most of our customers are still developing applications that use our products. Commercialization is a process, the exact timing of which is often difficult to predict. It starts with our own internal R&D to validate performance for an identified market or customer-specific need. Our customers then validate the performance of our materials and determine whether our products can be incorporated into their manufacturing processes. This is initially done at pilot production scale levels. Our customers then have to introduce products that incorporate our materials to their own customers to validate performance. After their customers have validated performance, our customers will then move to commercial scale production. Every customer goes through the same process, but will do so at varying speeds, depending on the customer, the product application and the end-use market. Thus, we are not always able to predict when our customers will begin ordering commercial volumes of our materials or predict their expected volumes over time. However, as customers move through the process, we generally receive feedback and gain greater insights regarding their commercialization plans. The following are examples of where our products are providing value to our customers at levels that are either in commercial production or we believe will warrant their use on a commercial basis:

| ● | Callaway Golf Company incorporated our graphene nanoplatelets into the outer core of their Chrome Soft golf balls, resulting in a new class of golf ball that enables higher driving speeds, greater distance and increased control, which is allowing Calloway to command a premium price for their golf balls in the marketplace, and | |

| ● | Lead acid battery manufacturer demonstrating approximately 90% improvement in measured cycle life, appreciable improvement in capacity and charge acceptance and without any loss in water retention performance, and | |

| ● | Light emitting diode module and product company demonstrated approximately 50% improvement in thermal management capability when compared to existing commercial thermal management products, translating into a 15% improvement in thermal management at the device level, and |

6

| ● | Automotive parts supplier demonstrating improvements in thermal stability for polymer composites incorporating our materials, allowing for approximately 20% higher operating temperatures, a 50% improvement in strength at the elevated temperature and a 17% improvement in noise and vibration isolation, and | |

| ● | Industrial refrigeration equipment supplier demonstrating improved heat transfer efficiency and energy savings when our xGnP® graphene nanoplatelets are incorporated as a component in the thermal-transfer fluids, and | |

| ● | Construction company demonstrating less than one weight percent of our product in construction material composites improves flexural strength by more than 30%, and | |

| ● | Plastics composite part manufacturer demonstrating 7-30% improvement in strength and 40% improvement in modulus when used in sheet molding compound, and | |

| ● | Engineering design firm for automotive manufacturers found approximately 20% reduction in operating temperature and in thermal uniformity when XG Leaf® replaces standard cooling fins in lithium ion battery packs, and | |

| ● | Plastic composite parts manufacturer demonstrating 25% increase in tensile strength and 15% improvement in flex modulus for a high-density polyethylene composite. |

The process of “designing-in” new materials is relatively complex and involves the use of relatively small amounts of the new material in laboratory and engineering development for an extended period of time. Following successful development, customers that incorporate our materials into their products will then order much larger quantities of material to support commercial production. Although our customers are under no obligation to report to us on the usage of our materials, some have indicated that they have introduced or will soon introduce commercial products that use our materials. Thus, while many of our customers are currently purchasing our materials in kilogram (one or two pound) quantities, some are now ordering at multiple ton quantities and we believe many will require tens of tons or even hundreds of tons of material when they commercialize products that incorporate our materials. We also believe that those customers already in production will increase their order volume as demand increases and others will begin to move into commercial volume production as they gain more experience in working with our materials and engage with their customers. For example, we shipped a 1 metric ton order in the fourth quarter of 2016 to a customer who is currently moving into larger scale production and had previously used smaller quantities. In the first half of 2017 we shipped 3.4 metric tons of product for various end-use customers and in the second half of 2017 we shipped just shy of 14 metric tons and we received orders in the fourth quarter that exceeded capacity. This demand profile is further evidence that we are transitioning into higher-volume production. Based on customer forecasts and management estimates, we expect to ship from 100 to 200 metric tons in 2018.

2018 Expected Revenue

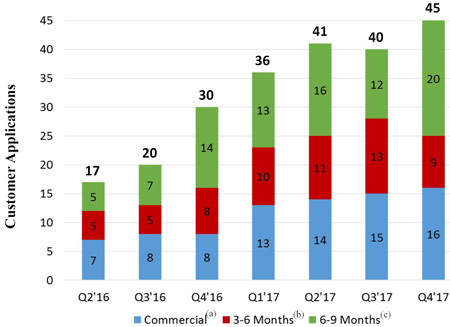

We are tracking the commercial and development status of more than 75 different customer applications using our materials with some customers pursuing multiple applications. As of December 31, 2017, we had sixteen specific customer applications where our materials are incorporated into our customers’ products and such customers are actively promoting or selling these products to their own customers. In addition, we have another nine customer applications where our customers have indicated that they expect to begin shipping product incorporating our materials in the next 3 – 6 months, and we have another twenty customer applications where our customers have indicated an intent to commercialize in the next 6 – 9 months. We are also working with numerous additional customers that have not yet indicated an exact date for commercialization, but we believe have the potential to contribute to revenue in 2018. The following graphic demonstrates the trend over the past 7 quarters as an increasing number of customers indicate their intent to commercialize applications and move into actively selling or promoting products for future sales. We anticipate that the average order size for these customers will increase throughout 2018 as their demand grows. As a result, we believe we will begin shipping significantly greater quantities of our products, and thus continue scaling revenue in 2018. Based on the status of current discussions with customers and their feedback on the performance of our materials in their products, we believe we will be able to recognize approximately $10 – $20 million of revenue in 2018, although this cannot be assured.

7

| (a) | Customer applications where our materials are used in customer products and they are actively promoting or selling them to their customers. |

| (b) | Customer applications where our customers are indicating that they expect to begin shipping products incorporating our materials in the next 3-6 months. |

| (c) | Customer applications where our customers are indicating an intent to commercialize in the next 6-9 months. |

Addressable Markets

The markets that we serve are large and rapidly growing. For example, as shown in the figure below, Avicenne Energy (The Battery Show, Novi MI, September 2017) estimates that the market for materials used in lithium ion batteries is currently approximately $10.4 billion and with a double-digit compound annual growth rate. We believe our ability to address next generation battery materials represents a significant opportunity for us.

8

According to Prismark Partners, LLC, a leading electronics industry consulting firm specializing in advanced materials, the 2018 market for finished graphitic heat spreaders as sold to the OEM and EMS companies with adhesive, PET, and/or copper backing for selected portable applications is expected to reach $900 million in 2018. The market has been in a significant expansion period driven by the demand for portable devices. In a press release dated October 17, 2017, Gartner, Inc., a leading research organization, estimated the 2018 global smartphone market at more than 1.6 billion units and worldwide combined shipments of devices (PC’s, tablets, ultraphones and mobile devices were expected to exceed 2.35 billion units in 2018). Every cell phone has some form of thermal management system, and we believe many of the new smart phones and other portable devices being developed can benefit from the thermal management properties of our XG Leaf® product line. In November 2017, International Data Corporation (IDC) in their Worldwide Quarterly Tablet Tracker estimated the global shipment of tablets in the third quarter at 40 million units (Q1 at 36.2 million units and Q2 at 37.9 million units). Thus, we believe our XG Leaf® product line is well positioned to address a very large and rapidly growing market.

Our Intellectual Property

Some of our proprietary manufacturing processes were developed at Michigan State University (MSU) and licensed to us in 2006. We license two U.S. patents and patent applications from MSU. On August 8, 2016, we signed an agreement acquiring an exclusive license to Metna’s background IP for use of graphene nanoplatelets as additives to concrete mixtures. For purposes of the agreement, Metna’s background IP relates to the U.S. Patent 8,951,343. Also, on August 8, 2016, we entered into a second agreement for an exclusive license related to all Metna’s background technology and foreground technology, including any jointly-owned foreground technology where the end use is known to be any graphite additive dispersed in concrete mixtures. Over time, our scientists and engineers have made many further discoveries and inventions that are embodied in the form of (as of December 31, 2017): eight additional U.S. patents, 10 foreign patents, 16 additional U.S. patent applications, and numerous trade secrets. For each patent application filed in the U.S., we make a determination on the nature and value of the patent. For many of the applications filed in the U.S., additional filings are made in other countries such as the European Union, Japan, South Korea, China, Taiwan or other applicable countries. As of December 31, 2017, we maintained 35 international patent applications. These filings and analyses are made on a case-by-case basis. Typically, patents that are defensive in nature are not filed abroad, while those that are protective of active XGS products or applications are filed in relevant countries abroad. Our general IP strategy is to keep as trade secrets those manufacturing processes that are difficult to enforce should they be disclosed and to seek patent coverage for other manufacturing processes, materials derived from those processes, unique combinations of materials and end uses of materials containing graphene nanoplatelets. We believe that the combination of our rights under the MSU license, our patents and patent applications, and our trade secrets create a strong intellectual property position.

9

Our Manufacturing Capacity

We have developed and scaled-up capacity for two proprietary manufacturing processes — one based on chemical intercalation of graphite and subsequent exfoliation and classification; and the second based on a high-shear mechanical process which also employs graphite as the starting material. In March 2012, we took possession of a production facility under terms of a long-term lease and moved our headquarters to this new location. Initial production commenced in this facility in September 2012. Currently, this facility is capable of producing approximately 30 – 50 tons per year of intercalated materials (depending on product mix) if operated on a continuous basis We expect to streamline certain process steps in 2018 to roughly double the capacity output for our chemical intercalation processes. We also operate a separate production facility in leased manufacturing space which is used for the production of certain graphene nanoplatelets derived from a high-shear mechanical process and also other specialty materials. This facility is capable of producing approximately 30 – 60 tons per year of materials (depending on product mix) if operated on a continuous basis. In October 2017, we signed a lease for a new 64,000 square foot manufacturing facility which will be the site for expansion of our mechanical exfoliation capacity. It is our intent to consolidate equipment into the new facility and to add next-generation tooling to meet our estimated 2018 demand. Following consolidation, we will close the older facility. We expect to increase capacity in 2018 to four times that of our capacity at the end of 2017. We believe these manufacturing facilities will be sufficient to meet demands for the majority of our bulk materials for a number of years, with suitable additions of capital equipment as warranted. However, additional manufacturing capabilities for certain value-added products and certain bulk materials remain to be developed and may require the acquisition of additional facilities. In particular, the production processes for XG Leaf®, XG SiG® and our conductive inks will require additional capital and may require additional facilities to meet expected future customer demand.

Many of the Company’s products are new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. Although we believe we will continue to scale our production capability and revenue rapidly in 2018, we have not yet demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. For additional information please see “Risk Factors” herein.

Our Lead Investors

Since inception and through December 31, 2017, we have raised approximately $40 million of capital through the issuance of equity and equity-linked securities, $4 million through licensing fees and $6 million through the issuance of certain lease and senior debt obligations. Notable investors and licensees in the Company include:

| ● | Hanwha Chemical Corporation – $3 million equity investment (December 2010) | |

| ● | Aspen Advanced Opportunity Fund and affiliates – $20+ million in various equity investments (2010 – Current) | |

| ● | POSCO Corporation – $5.2 million in equity investments/license agreement (June 2011 and March 2014) | |

| ● | Samsung Ventures – $3 million equity investment (January 2014) | |

| ● | The Dow Chemical Company – $5 million drawn on a $10 million senior debt financing (December 2016 - 2017) |

Our Competitive Strengths

We believe that we are a leader in the emerging global market for graphene nanoplatelets. The following competitive strengths distinguish us in our industry:

Our know-how and ability to tailor our products for use in multiple applications. Many of our products and product-development activities target use of our xGnP® graphene nanoplatelets in various matrices to form composite products that are then used by our customers. We have extensive knowledge of how to tailor our products to deliver performance as composite products in various applications and we also have knowledge of how to tailor other components of a composite to adjust the performance of the composite for use in various applications.

The strength of our intellectual property. Because of our focus on manufacturing process development, we believe we have one of the world’s strongest internal knowledge bases in graphene nanoplatelet manufacturing, with most of our proprietary knowledge maintained as trade secrets to avoid the disclosures required by patenting. The 28 US patents and patent applications that we are currently managing (including those under license from MSU and Metna) and 45 international patents and patent applications add value by protecting specific equipment, or high-value end-user product applications. The fact that two global companies have evaluated and licensed our production technology provides independent evidence of our technology’s effectiveness.

10

The breadth of our product offering. To our knowledge, we have the broadest product offering in our industry. In addition to offering four standard grades of bulk graphene nanoplatelet materials in a range of diameters and surface areas, we offer four different grades of XG Leaf® in multiple thicknesses, two different grades of silicon-graphene composite materials, three standard ink formulations, and optional custom dispersions and formulations of our bulk materials. We also offer an XG TIM™ thermal interface material and a newly introduced GNP® Cement Additive product.

The low-cost nature of our manufacturing processes. We believe our manufacturing processes are the lowest-cost approaches to the manufacturing graphene nanoplatelets (subject to economies of scale) based on our internal modelling of competitive processes as well as our analysis of alternative technologies.

Our corporate partners. Three global corporations (Samsung, POSCO, and Hanwha Chemical) have invested over $11 million in XGS, giving us a significant global reach as well as the ability to leverage the assets of our partners. In addition, The Dow Chemical Company has extended $10 million in senior debt financing, of which we have drawn down $5 million.

Our licensees will accelerate our entry into large markets. Cab3ot Corporation, the largest U.S.-based manufacturer of carbon particles, and POSCO, one of the world’s largest steel producers, have licensed parts of our production technology. We believe these licensees will help us distribute our products and value-added products made with our xGnP® nanoplatelets more rapidly than we could do on our own.

The number of development partners that are working with our materials. As of December 31, 2017, we had supplied materials to 280 universities or government laboratories in 41 different countries around the world. A recent search of the U.S. patent database revealed 574 citations of XG Sciences in patents filed by other organizations. These other organizations include Goodrich Corporation, PPG Industries, ExxonMobil Research & Engineering, Toray, Solvay, Honda, Eastman Kodak, Baker Hughes, GM, Rohm and Haas and Sekisui Chemical.

The number of commercial customers purchasing and working with our materials. As of December 31, 2017, we have supplied materials to 983 commercial companies around the world (in addition to universities and research laboratories) who are assessing their performance and potentially designing them into products. We have more than 75 active development relationships where we are working with end-use customers to design products for commercial use. We believe that these relationships will continue to expand.

As a result of these factors, we believe XGS is a leader in the emerging global market for graphene nanoplatelets. Other independent observers have agreed with this assessment. For example, Lux Research, in a July 2015 release listed XGS as a leading player in its review of the graphene industry. Further, Lux analysts wrote: “XG’s march of strategic relationship announcements — Hanwha Chemical in December 2010, POSCO in June 2011, and Cabot in November 2011 — arguably give it the strongest partnership portfolio in the space, and its recent expansion (see the May 7, 2012 LRMJ) makes it one of the low cost and capacity leaders.”

Our Financing History

Since our inception, we have incurred annual losses every year and have accumulated a deficit from operations of $(47,692,116) through December 31, 2017 and $(41,188,851) through December 31, 2016. As of December 31, 2017, and December 31, 2016, our total stockholder’s equity was $1,172,900 and $2,523,578, respectively.

From December 31, 2015 through April 7, 2016, we entered into private placement bridge financings with 15 investors, seven of whom are members or affiliates of members of our board of directors (“Board of Directors” or “Board”), totaling $1,124,750 (the “Bridge Financings”). The investors in the Bridge Financings received common stock warrant coverage of 30% for investments made prior to December 31, 2015 with an exercise price of $8.00 per share, and 20% coverage thereafter with an exercise price of $10.00 per share. In June of 2016, we repaid outstanding principal of $750,000 plus accrued interest of $27,032 to the Bridge Financing Investors. In December of 2016, we repaid the remaining $374,750 of outstanding principal plus accrued interest of $21,253. Members of the Board and their affiliates provided $800,000 of the principal for such Bridge Financings and re-invested all the principal plus additional funds of $1,013,032 to purchase 226,629 shares of the Company’s common stock during 2016.

In December 2016, we entered into a draw loan note and agreement (the “Dow Facility”) with The Dow Chemical Company (“Dow”) which provides us with up to $10 million of secured debt financing at an interest rate of 5% per year, drawable at our request under certain conditions. We received $2 million at closing and an additional $1 million on each of July 18, 2017, September 22, 2017 and December 4, 2017, respectively. After December 1, 2017, an additional $5 million becomes available if we have raised $10 million of equity capital after October 31, 2016.

11

The Dow Facility is senior to most of our other debt and is secured by all of our assets (Dow is subordinate only to the capital leases with AAOF, see Note 13 to the financial statements). The loan matures on December 1, 2021 (subject to certain mandatory prepayments based on our equity financing activities). Interest is payable beginning January 1, 2017 although we elected to capitalize interest through January 1, 2019. Dow received warrant coverage of one share of common stock for each $40 in loans received by us, equating to 20% warrant coverage, with an exercise price of $8.00 per share for the warrants issued at closing of the initial $2 million draw. After the initial closing, the strike price of future warrants issued are subject to adjustment if we sell shares of common stock at a lower price. As of December 31, 2017, we had issued 125,000 warrants to Dow, all with an exercise price of $8.00 per share, which are exercisable on or before the expiration date of December 1, 2023.

The Dow warrants meet the criteria for classification within stockholders’ equity. Proceeds were allocated between the debt and the warrants at their relative fair value. During the year ended December 31, 2017, amortization expense of $161,702 was recognized resulting in a carrying value of $4,794,596 for the Dow Loan as of December 31, 2017.

During each of the years ended December 31, 2017 and 2016, we issued 28,560 shares of Series A Preferred Stock to Aspen Advanced Opportunity Fund as payment under the terms of a Master Leasing Agreement for lease financing obligations.

We filed a Registration Statement on Form S-1 (File No. 333-209131) with the SEC on April 11, 2016 which was declared effective by the SEC on April 13, 2016 (the “Registration Statement”). The Registration Statement registered up to 3,000,000 shares of common stock at a fixed price of $8.00 per share to the general public in a self-underwritten offering (the “Offering” or our “IPO”). Post-Effective Amendment No. 1 to the Registration Statement was declared effective August 26, 2016, Post-Effective Amendment No. 2 was declared effective August 31, 2016, Post-Effective Amendment No. 3 was declared effective January 17, 2017, and Post-Effective Amendments No. 4 and No. 5 were dated April 12, 2017. Post-Effective Amendment No. 5 was declared effective April 14, 2017. Although we are currently selling shares of our common stock in our IPO pursuant to an effective Registration Statement, we have not yet listed the company for trading on any exchanges.

As of December 31, 2017, the Company has sold 966,832 shares under the Registration Statement at a price of $8.00 per share for proceeds of $7,734,656.

As of December 31, 2017, we had cash on hand of $2,845,798 and at March 30, 2018 cash on hand of $2,285,182. We believe our cash is sufficient to fund our operations through March 2019 when taking into account various sources of funding and cash received from continued commercial sales transactions. We intend that the primary means for raising funds will be through our Offering of common stock and the additional $5 million of proceeds from the Dow Facility available to us after we have raised $10 million of equity capital as measured in the period beginning on November 1, 2016, however we can make no assurances that we will raise $10 million of equity capital and access the additional $5 million under the Dow Facility. At March 30, 2018 we have raised $6,149,024 towards this $10,000,000 requirement. Taking into account the cash position at March 30, noted above, an additional $3.85 million in proceeds from the Offering, which would allow us to draw up to $5 million from the Dow Facility, we believe that we can fund our operations including planned capital expenditures through March 31, 2019. In addition, two of our shareholders have committed to provide up to $4.5 million in funding for the twelve-month period ended March 31, 2019 to the extent the Company has been unable to raise such funds from other third parties.

As a result of the Bridge Financings and the IPO, the conversion price of our Series A Preferred Stock was adjusted to $6.40 per share.

Pursuant to the Certificate of Designation for the Series A, as amended, all then-outstanding shares of Series A will automatically convert into shares of common stock upon the listing of the Company’s common stock on a Qualified National Exchange (a securities exchange registered with the SEC under Section 6(a) of the Securities Exchange Act of 1934, as amended (“Exchange Act”), such as the NASDAQ Capital Market or the New York Stock Exchange, or (ii) the quotation of our common stock on the OTCQB or OTCQX marketplaces operated by OTC Markets Group, Inc. (“OTC Markets”), and the act of achieving such listing or quotation is referred to hereafter as a “Public Listing” in this report). As a result, there will only be one class of equity securities outstanding — common stock — after we achieve a Public Listing. Prior to any such listing, the Series A may be voluntarily converted into shares of common stock at the then-current conversion rate (current rate for the Series A Preferred Stock is 1.875 for 1).

Public Listing

In order to achieve a Public Listing, we will have to meet certain initial listing qualifications of the Qualified National Exchange or the OTC Markets on which we are seeking the Public Listing. In addition, we will need to have market makers agree to make a market in our common stock and file a FINRA Form 15c211 with the SEC on our behalf before we can achieve a Public Listing, and we will also need to remain current in our quarterly and annual filings with the SEC. Although we intend to seek a Public Listing in 2018, we cannot make any assurances that our common stock will ever be quoted or traded on Qualified National Exchange or the OTC Markets or that any market for our common stock will develop.

12

Employees

As of December 31, 2017, we had 41 full-time employees and 1 part-time employee. 16 of these employees were contract employees who may generally be hired as permanent employees after 3 – 6 months. Employees include the following four senior managers that report to the CEO: Chief Commercial Officer, Vice President of Operations, Vice President of Research & Development, and Controller. The Company employs a total of 6 full-time scientists and technicians in its R&D group, including the Vice President of Research & Development.

Corporate Information

XG Sciences, Inc. was incorporated on May 23, 2006 in the State of Michigan and is organized as a “C” corporation under the applicable laws of the United States and State of Michigan. We do not currently have any affiliated companies or joint venture partners, and we have one wholly owned subsidiary called XG Sciences IP, LLC. This subsidiary was created in 2014 for the purpose of holding our intellectual property. Our headquarters and principal executive offices are located at 3101 Grand Oak Drive, Lansing, Michigan, 48911 and our telephone number is (517) 703-1110.

Our website address is http://www.xgsciences.com, although the information contained in, or that can be accessed through, our website is not part of this filing. You may also contact Dr. Philip L. Rose, our Chief Executive Officer via email at p.rose@xgsciences.com.

Risks Relating to Our Business and Industry

We have a limited operating history, an accumulated deficit and a stockholders’ deficit, making it difficult for you to evaluate our business and your investment.

XG Sciences, Inc. was incorporated on May 23, 2006, and is an advanced materials company. We sell bulk nanomaterials or products made with these materials to other companies for incorporation into their products. To date, there has been limited incorporation of our materials or products into customer products that are released for commercial sale. Because there is a limited demonstrated history of commercial success for our products, it is difficult to evaluate whether our products will ultimately be successful in the market. It is possible that larger and or extended commercial success may never happen and that we will never achieve the level of revenues necessary to sustain our business or continue to attract additional financing.

Many of our products represent new products that have not yet been fully developed and for which manufacturing operations have not yet been fully scaled. This means that investors are subject to all of the risks incident to the creation and development of multiple new products and their associated manufacturing processes.

As of December 31, 2017, and December 31, 2016, we have an accumulated deficit from operations of $(47,767,544) and $(41,188,851), respectively. As of December 31, 2017, and December 31, 2016, our total stockholder’s equity was $1,097,472 and $2,523,578, respectively. The deficit reflects net losses in each period since our inception incurred through development of nanomaterials without the presence of a large-scale market to generate substantial revenues to cover development costs and generate a profit. We have never paid a dividend. Also, since inception, we have not generated sufficient revenues to cover our fixed expenses or sustain our business in any financial reporting period. Nor have we demonstrated the capability to produce sufficient materials to generate the ongoing revenues necessary to sustain our operations in the long-term. There can be no assurance that we will ever produce a profit.

Because we are subject to these uncertainties, there may be risks that management has failed to anticipate and you may have a difficult time evaluating our business and your investment in our Company. Our ability to become profitable depends primarily on our ability to successfully commercialize our products in the future. Even if we successfully develop and market our products, we may not generate sufficient or sustainable revenue to achieve or sustain profitability, which could cause us to cease or curtail operations. In such case, you would likely lose all or a significant part of your investments.

13

We will need to raise substantial additional capital in the future to fund our operations and we may be unable to raise such funds when needed and on acceptable terms, which could have a materially adverse effect on our business.

Developing, manufacturing and selling nanomaterials in commercially-viable quantities requires substantial funding. As of December 31, 2017, and March 30, 2018, we had cash on hand of $2,845,798 and $2,285,182, respectively. We believe our cash is sufficient to fund our operations for the next twelve months (through March 2019) when taking into account various sources of funding and cash received from continued commercial sales transactions. We intend that the primary means for raising funds will be through our Offering and the additional $5 million of proceeds from the Dow Facility available to us after we have raised $10 million of equity capital as measured in the period beginning on November 1, 2016, however we can make no assurances that we will raise $10 million of equity capital and access the additional $5 million under the Dow Facility. There can be no assurance that we will be able to raise additional equity capital subsequent equity offerings or that the terms and conditions of any future financings will be workable or acceptable to us and our stockholders. Our continuation as a going concern is dependent upon continued financial support from our shareholders, our ability to obtain necessary equity and/or debt financing to continue operations, and the attainment of profitable operations. In the event that we are not able to raise substantial additional funds in the future on terms that are acceptable or adjust our business model accordingly, we may be forced to curtail or cease operations and you could lose all or a significant part of your investment.

We have limited experience in the higher volume manufacturing that will be required to support profitable operations, and the risks associated with scaling to larger production quantities may be substantial.

We have limited experience manufacturing our products. We have established small-scale commercial or pilot-scale production facilities for our bulk powders, thermal interface materials (“XG TIM®” or TIM), XG Leaf® and SiG materials. In order to develop the capacity to produce much higher volumes, it will be necessary to produce multiples of existing processes or engineer new production processes in some cases.

We are in the process of building out a new 64,000 square foot manufacturing facility in Mason, MI, but there can be no assurance that this new facility will be opened on time or as planned. There is no guarantee that we will be able to economically scale-up our production processes to the levels required. If we are unable to scale-up our production processes and facilities to support sustainable sales levels, the Company may be forced to curtail or cease operations and you could lose all or a significant part of your investment.

Projection of fixed monthly expenses and operating losses for the near future means that investors may not earn a return on their investment or may lose their investment.

Because of the nature of our business, we project considerable fixed expenses that will lead to projected monthly deficits for the near future. Fixed manufacturing expenses to maintain production facilities, compensation expenses for scientists and other critical personnel, and ongoing rent and utilities amount to several hundred thousand dollars per month, and we believe that such expenses are required as a precursor to significant customer sales. However, there can be no assurance that monthly sales will ever reach a sufficient level to cover the cost of ongoing monthly expenses and if they do, are maintained for a sustainable period of time. If sufficient regular monthly sales are not generated to cover these fixed expenses, we will continue to experience monthly cash flow deficits which, if not eliminated, will require continuing new investment in the Company. If monthly cash flow deficits continue beyond levels that investors find tolerable, we may not be able to raise additional funds and may be forced to curtail or cease operations and you could lose all or a significant part of your investment.

We have a long and complex sales cycle and have not demonstrated the ability to operate successfully in this environment.

It has been our experience since our inception that the average sales cycle for our products can range from one to seven years from the time a customer begins testing our products until the time that they could be successfully used in a commercial product. The product introduction timing will vary based on the target market, with automotive uses typically being toward the long end and consumer electronics toward the shorter end. We have a limited track record of success in completing customer development projects, which makes it difficult for investors to fully evaluate the likelihood of our future success. The sales and development cycle for our products is subject to customer budgetary constraints, internal acceptance procedures, competitive product assessments, scientific and development resource allocations, and other factors beyond our control. If we are not able to successfully accommodate these factors to enable customer development success, we will be unable to achieve sufficient sales to reach profitability. In this case, we may not be able to raise additional funds and may be forced to curtail or cease operations and you could lose all or a significant part of your investment.

We could be adversely affected by our exposure to customer concentration risk.

We are subject to customer concentration risk as a result of our reliance on a relatively small number of customers for a significant portion of our revenues. In 2017 we had one customer (a commercial customer) whose purchases accounted for 53% of product revenue and in 2016 we had one customer (one of our licensees) whose purchases accounted for 24% of total product revenues. Due to the nature of our business and the relatively large size of many of the applications our customers are developing, we anticipate that we will be dependent on a relatively small number of customers for the majority of our revenues for the next several years. It is possible that only one or two customers could place orders sufficient to utilize most or all of our existing manufacturing capacity. In this case, there would be a risk of significant loss of future revenues if one or more of these customers were to stop ordering our materials, which could in turn have a material adverse effect on our business and on your investment.

14

Our revenues often fluctuate significantly based on one-off orders from customers or from the recognition of grant revenues which vary from period-to-period, which may materially impact our financial results from period to period.

Because of the potential for large revenue swings from one-time, large orders or grants it may be difficult to accurately forecast the needs for inventory, working capital, and other financial resources from period-to-period. Such orders would require a significant short-term increase in our production capacity and would require the financial resources to add staff and support the associated working capital. If such large, one-time orders were not handled smoothly, customer confidence in us as a viable supplier could be reduced and we might not succeed in capturing the additional larger orders that may be reflected in our business plan.

We operate in an advanced technology arena where hypothesized properties and benefits of our products may not be achieved in practice, or in which technological change may alter the attractiveness of our products.

Because there is no sustained history of successful use of our products in commercial applications, there is no assurance that broad successful commercial applications may be broadly technically feasible. Many of the scientific and engineering data related to our products has been generated in our own laboratories or in laboratory environments at our customers or third-parties, like universities and national laboratories. It is well known that laboratory data is not always representative of commercial applications.

Likewise, we operate in a market that is subject to rapid technological change. Part of our business strategy is to monitor such change and take steps to remain technologically current, but there is no assurance that such strategy will be successful. If we are not able to adapt to new advances in materials sciences, or if unforeseen technologies or materials emerge that are not compatible with our products and services or that could replace our products and services, our revenues and business prospects would likely be adversely affected. Such an occurrence may have severe consequences, including the potential for our investors to lose all or a significant part of their investment.

Competitors that are larger and better funded may cause us to be unsuccessful in selling our products.

The Company operates in a market in which there are competitors. Global research is being conducted by substantially larger companies who have greater financial, personnel, technical, and marketing resources. There can be no assurance that our strategy of offering better materials based on our proprietary graphene nanoplatelets will be able to compete with other companies, many of whom will have significantly greater resources, on a continuing basis. In the event that we cannot compete successfully, we may be forced to cease our curtail operations and investors may lose all or a significant part of their investment.

We are dependent on key employees.

Our operations and development are dependent upon the experience and knowledge of Philip L. Rose, our Chief Executive Officer. If he was to resign or be terminated, our business would be adversely affected in the short term, and his departure could disrupt the business enough to endanger your investment. We also depend on Dr. Liya Wang, Vice President of Research & Development, Bamidele Ali, Chief Commercial Officer, Scott Murray, Vice President of Operations, and Dr. Hiroyuki Fukushima, Technical Director. If the services of any of these individuals should become unavailable, our business operations might be adversely affected. We do not hold any “Key Person” insurance, and if several of these individuals became unavailable at the same time, our ability to continue normal business operations might be adversely affected, to the extent that revenue or profits could be diminished and you could lose all or a significant part of your investment.

Our success depends in part on our ability to protect our intellectual property rights, and our inability to enforce these rights could have a material adverse effect on our competitive position.

We rely on the patent, trademark, copyright and trade-secret laws of the United States and the countries where we do business to protect our intellectual property rights. We may be unable to prevent third parties from using our intellectual property without our authorization. The unauthorized use of our intellectual property could reduce any competitive advantage we have developed, reduce our market share or otherwise harm our business. In the event of unauthorized use of our intellectual property, litigation to protect or enforce our rights could be costly, and we may not prevail.

15

Many of our technologies are not covered by any patent or patent application, and our issued and pending U.S. and non-U.S. patents may not provide us with any competitive advantage and could be challenged by third parties. Our inability to secure issuance of our pending patent applications may limit our ability to protect the intellectual property rights these pending patent applications were intended to cover. Our competitors may attempt to design around our patents to avoid liability for infringement and, if successful, our competitors could adversely affect our market share. Furthermore, the expiration of our patents may lead to increased competition.

Our pending trademark applications may not be approved by the responsible governmental authorities and, even if these trademark applications are granted, third parties may seek to oppose or otherwise challenge these trademark applications. A failure to obtain trademark registrations in the United States and in other countries could limit our ability to protect our products and their associated trademarks and impede our marketing efforts in those jurisdictions.

In addition, effective patent, trademark, copyright and trade secret protection may be unavailable or limited in some foreign countries. In some countries, we do not apply for patent, trademark or copyright protection. We also rely on unpatented proprietary manufacturing expertise, continuing technological innovation and other trade secrets to develop and maintain our competitive position. Although we generally enter into confidentiality agreements with our employees and third parties to protect our intellectual property, these confidentiality agreements are limited in duration and could be breached and may not provide meaningful protection of our trade secrets or proprietary manufacturing expertise. Adequate remedies may not be available if there is an unauthorized use or disclosure of our trade secrets and manufacturing expertise. In addition, others may obtain knowledge about our trade secrets through independent development or by legal means. The failure to protect our processes, apparatuses, technology, trade secrets and proprietary manufacturing expertise, methods and compounds could have a material adverse effect on our business by jeopardizing critical intellectual property.

Where a product formulation or process is kept as a trade secret, third parties may independently develop or invent and patent products or processes identical to our trade-secret products or processes. This could have an adverse impact on our ability to make and sell products or use such processes and could potentially result in costly litigation in which we might not prevail.

We could face intellectual property infringement claims that could result in significant legal costs and damages and impede our ability to produce key products, which could have a material adverse effect on our business, financial condition and results of operations.

If we are unable to implement and maintain effective internal control over financial reporting, our stock could be less attractive to potential investors.

We are required to establish and maintain appropriate internal controls over financial reporting, subject to exemptions that we avail ourselves to under the JOBS Act discussed below. Failure to establish such controls, or any failure of such controls once established, could adversely impact our public disclosures regarding our business, financial condition or results of operations. Any failure of our controls could also prevent us from maintaining accurate accounting records and discovering accounting errors and financial frauds. Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and the standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. In the year ended December 31, 2017, we identified material weaknesses in our internal controls over financial reporting related to a limited number of accounting personnel which does not provide for an adequate segregation of duties and the lack of a chief financial officer. We plan to create positions to segregate duties consistent with control objectives in our accounting department.

In addition, management’s assessment of internal controls over financial reporting may identify material weaknesses and conditions that need to be addressed in our internal controls over financial reporting or other matters that may raise concerns for investors in the future. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting, disclosure of management’s assessment of our internal controls over financial reporting, or at such time as we are no longer subject to exemptions under the JOBS Act, disclosure of our independent registered public accounting firm’s report on management’s assessment of our internal controls over financial reporting may have an adverse impact on our ability to sell our common stock.

16

Future adverse regulations could affect the viability of the business.

Our bulk products have been approved for sale in the United States by the U.S. Environmental Protection Agency after a detailed review of our products and production processes for our H, M, R and C grade materials. In most cases, as far as we are aware, there are no current regulations elsewhere in the world that prevent or prohibit the sale of our products. Nevertheless, the sale of nano-materials is a subject of regulatory discussion and review in many countries around the world. In some cases, there is a discussion of potential testing requirements for toxicity or other health effects of nano-materials before they can be sold in certain jurisdictions. If such regulations are enacted in the future, our business could be adversely affected because of the requirement for expensive and time-consuming tests or other regulatory compliance. If nano-materials are found to be toxic, such finding could have a material impact on our business and on the production and sale of our products. There can be no assurance that future regulations might not severely limit or even prevent the sale of our products in major markets, in which case our financial prospects might be severely limited, causing investors to lose all or a significant part of their investment.

Compliance with changing regulation of corporate governance and public disclosure will result in additional expenses and will divert time and attention away from revenue generating activities.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Sarbanes-Oxley Act of 2002 and related SEC regulations, have significantly increased the costs and risks associated with accessing the public markets and public reporting. Our management team will need to invest significant management time and financial resources to comply with both existing and evolving standards for public companies, which will lead to increased general and administrative expenses and a diversion of management time and attention from revenue generating activities to compliance activities, which could have an adverse effect on our business.

Given our limited resources, we may not effectively manage our growth.

There is no guarantee that we have the resources, financial or operational, required to manage our growth. This is particularly true as we expand facilities and manufacture our products on a greater commercial scale. Furthermore, rapid growth in our operations may place a significant strain on our management, administrative, operational and financial infrastructure. The inability to adequately manage our growth could have a material and adverse effect on our business, financial condition or results of operations, thus resulting in a lower quoted price of our common stock.

Downturns in general economic conditions could adversely affect our profitability.

Downturns in general economic conditions can cause fluctuations in demand for our products, product prices, volumes and gross margins. Future economic conditions may not be favorable to our industry. A decline in the demand for our products or a shift to lower-margin products due to deteriorating economic conditions could adversely affect sales of our products and our profitability and could also result in impairments of certain of our assets.

Furthermore, any uncertainty in economic conditions may result in a slowdown to the global economy that could affect our business by reducing the prices that our customers may be able or willing to pay for our products or by reducing the demand for our products.

An increase in the cost of raw materials or electricity might affect our profits.

Any increase in the prices of our raw materials or energy might affect the overall cost of our products. If we are not able to raise our prices to pass on increased costs to our customers, we would be unable to maintain our existing profit margins. Our major cost components include items such as graphite, sulfuric acid, and electricity, which items are normally readily available industrial commodities. During our history as a business, we have not seen any material impact (as defined by GAAP) on our cost structure from fluctuations in raw material or energy costs, but this could change in the future.

Our results of operations could deteriorate if our manufacturing operations were substantially disrupted for an extended period.

Our manufacturing operations are subject to disruption due to extreme weather conditions, floods and similar events, major industrial accidents, strikes and lockouts, adoption of new laws or regulations, changes in interpretations of existing laws or regulations or changes in governmental enforcement policies, civil disruption, riots, terrorist attacks, war, and other events. We cannot assure you that no such events will occur. If such an event occurs, it could have a material adverse effect on us.

Some health effects of nanotechnology are unknown.

There is scientific debate on the health effects of nano-materials such as graphene nanoplatelets, but some scientists believe that certain nano-materials may be hazardous to human health, including the respiratory system if inhaled. Although there is no conclusive evidence of any danger associated with the handling of the Company’s products, there is a theoretical risk of danger to health if an individual is exposed to and/or inhales/ingests some of the Company’s products. The specific health effects of nanoplatelets are unknown and can depend on how they are incorporated and/or bonded to other materials. We carefully evaluate potential health effects of our products and the effects of handling materials on our employees and those who manufacture for us, but as any specific health risks are unknown, we cannot be certain our products present are free of danger to our employees and customers. If nanoplatelets are found to be hazardous to human health, this may adversely affect market acceptance of our products, subject us to additional regulation and have an adverse effect on our business.

17

Defects in our products or poor performance of our customers’ products could result in lost sales and subject us to substantial liability.

We have limited experience with large scale commercialization by our customers of products incorporating our nanoplatelets, and the chance of variability in the performance of our products as shipped may impact the performance of our customers’ products. If our customers’ products incorporating nanoplatelets perform poorly, whether due to design, engineering, production or other reasons, our customers may scale back or cancel orders. In certain cases, if our nanoplatelets are found to be the component that leads to failure or a failure to meet the performance specifications of a customer, we could be required to pay monetary damages. Real or perceived defects in our products could result in claims by our customers for losses they sustain. If our customers make such claims, we may be required, or may choose, for customer relations or other reasons, to expend additional resources to help correct any real or perceived defects. Liability provisions in our terms and conditions of sale may not be enforceable under some circumstances or may not fully or effectively protect us from claims and related liabilities and costs. In addition, regardless of the party at fault, errors of these kinds divert the attention of our engineering personnel from our product development efforts, damage our reputation and the reputation of our products, cause significant customer relations problems and can result in product liability claims. In addition, even claims that ultimately are unsuccessful could result in expenditures of funds in connection with litigation and divert management’s time and other resources. We also may incur costs and expenses relating to a recall of one or more of our products, and the occurrence of such claims could result in the delay or loss of market acceptance of our products and could adversely affect our business, operating results and financial condition.

If product liability lawsuits are brought against us, we may incur substantial liabilities.

We have limited experience with the large-scale manufacturing and distribution of our products. The commercialization of our products and the sale of our products in significant quantities involves exposure to product liability claims. We do not have product liability insurance. If we choose to obtain product liability insurance but cannot obtain sufficient insurance coverage at an acceptable cost or otherwise protect against potential product liability claims, the commercialization of products that we develop may be prevented or inhibited. We cannot predict all of the adverse health events that our products or products may cause. As a result, our [current and] future coverages may not be adequate to protect us from all of the liabilities that we may incur. If losses from product liability claims exceed any insurance coverage, we may incur substantial liabilities that exceed our financial resources. In addition, we may not be able to maintain our product liability insurance at an acceptable cost, if at all, and this insurance may not provide adequate coverage against potential claims or losses. If we are required to pay a product liability claim, we may not have sufficient financial resources and our business and results of operations may be harmed. Whether or not we are ultimately successful in product liability litigation, such litigation could also consume substantial amounts of our financial and managerial resources, and might result in adverse publicity, all of which could have a material adverse effect on our business.

Cybersecurity incidents could disrupt business operations, result in the loss of critical and confidential information, and adversely impact our reputation and results of operations.

Global cybersecurity threats and incidents can range from uncoordinated individual attempts to gain unauthorized access to information technology systems to sophisticated and targeted measures known as advanced persistent threats, directed at the Company, its plants and operations, its products, its customers and/or its third-party service providers. We rely on third party service providers to protect information technology systems, a breach of which could expose our confidential intellectual property, including trade secrets. The failure to protect such intellectual property could create a diminution in the value of our investment in research, development and engineering, and increased cybersecurity protection and remediation costs, which in turn could adversely affect our competitiveness and results of operations. We cannot be sure that our information technology infrastructure is safe from cybersecurity threats. Cybersecurity incidents, depending on their nature and scope, could potentially result in the misappropriation, destruction, corruption or unavailability of critical data and confidential or proprietary information (our own or that of third parties) and the disruption of business operations. The potential consequences of a material cybersecurity incident include reputational damage, claims from and litigation with third parties, fines levied by governmental authorities, and competitive disadvantages in our business.

18

Risks Relating To Our Common Stock

There is a risk of dilution of your percentage ownership of common stock in the Company.

In addition to the shares which we may sell pursuant to our Registration Statement, we have the right to raise additional capital or incur borrowings from third parties to finance its business. We may also implement public or private mergers, business combinations, business acquisitions and similar transactions pursuant to which we would issue substantial additional capital stock to outside parties, causing substantial dilution in the ownership of the Company by our existing stockholders. Subject to certain exceptions (See “Management — Shareholder Side Letter”), our Board of Directors has the authority, without the consent of any of the stockholders, to cause the Company to issue more shares of common stock and/or preferred stock at such price and on such terms and conditions as are determined by the Board in its sole discretion.

The sale of the shares being offered by us in our Registration Statement, as well as the shares of common stock issuable upon the exercise of options and warrants, the shares issuable upon conversion of Series A Preferred Stock (including the shares of Series A Preferred Stock issuable upon the exercise of warrants) and the issuance of additional shares of capital stock by us will dilute your ownership percentage in the Company and could impair our ability to raise capital in the future through the sale of equity securities.

Certain stockholders who are also officers and directors of the Company may have significant control over our management, which may not be in your best interests.