Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Enveric Biosciences, Inc. | ex32_2.htm |

| EX-32.1 - EXHIBIT 32.1 - Enveric Biosciences, Inc. | ex32_1.htm |

| EX-31.2 - EXHIBIT 31.2 - Enveric Biosciences, Inc. | ex31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - Enveric Biosciences, Inc. | ex31_1.htm |

| EX-23.1 - EXHIBIT 23.1 - Enveric Biosciences, Inc. | ex23_1.htm |

| EX-21.1 - EXHIBIT 21.1 - Enveric Biosciences, Inc. | ex21_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2017

|

Commission file number 001-38286

|

AMERI Holdings, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

|

95-4484725

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

100 Canal Pointe Boulevard, Suite 108,

Princeton, New Jersey

|

08540

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: 732-243-9250

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange On Which Registered

|

|

|

Common Stock $0.01 par value per share

|

The NASDAQ Stock Market LLC

|

|

|

Warrants to Purchase Common Stock

|

The NASDAQ Stock Market LLC

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the last 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

☐

|

Accelerated filer

|

☐

|

|

Non-accelerated filer

|

☐ (Do not check if a smaller reporting company)

|

Smaller reporting company

|

☒

|

|

Emerging growth company

|

☒

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting equity held by non-affiliates of the registrant as of June 30, 2017 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $8.7 million based on the closing bid price of the registrant’s common stock of $6.51 per share on that date. All executive officers and directors of the registrant and all 10% or greater stockholders have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant.

As of March 29, 2018, 18,790,998 shares of the registrant’s common stock were issued and outstanding.

Portions of the registrant’s definitive Proxy Statement for its Annual Meeting of Stockholders, which will be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2017, are incorporated by reference into Part III of this Annual Report on Form 10-K.

AMERI Holdings, Inc.

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2017

|

Item 1.

|

1

|

|

|

Item 1A.

|

9 | |

|

Item 1B.

|

27 | |

|

Item 2.

|

27 | |

|

Item 3.

|

27 | |

|

Item 4.

|

27 | |

|

Item 5.

|

28 | |

|

Item 6.

|

31 | |

|

Item 7.

|

31 | |

|

Item 7A.

|

41 | |

|

Item 8.

|

41 | |

|

Item 9.

|

41 | |

|

Item 9A.

|

41 | |

|

Item 9B.

|

42 | |

|

Item 10.

|

43 | |

|

Item 11.

|

43 | |

|

Item 12.

|

43 | |

|

Item 13.

|

43 | |

|

Item 14.

|

43 | |

|

Item 15.

|

44 | |

|

F-1

|

|

PART I

|

This annual report contains forward-looking statements. These statements relate to either future events or our future financial performance. In some cases, you may be able to identify forward-looking statements by terms such as “may,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential” or “continue,” the negative of these terms or other synonymous terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors,” that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Any forward-looking statements made by or on our behalf are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend, and we do undertake any obligation, to revise or update any of the forward-looking statements to match actual results. Readers are urged to carefully review and consider the various disclosures made in this report, which aim to inform interested parties of the risks factors that may affect our business, financial condition, results of operations and prospects.

Our financial statements are stated in United States Dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles (GAAP).

As used in this annual report, the terms “we,” “us,” “our” and similar references refer to AMERI Holdings Inc., and its subsidiaries together, unless the context indicates otherwise.

Our Company

We specialize in delivering SAP cloud, digital and enterprise services to clients worldwide.

SAP is a leader in providing enterprise resource planning (“ERP”) software and technologies to enterprise customers worldwide. We deliver a wide range of solutions and services across multiple domains and industries. Our services center around SAP and include technology consulting, business intelligence, cloud services, application development/integration and maintenance, implementation services, infrastructure services, and independent validation services, all of which can be delivered as a set of managed services or on an on-demand service basis, or a combination of both.

Our SAP focus allows us to provide technological solutions to a broad and growing base of clients. We are headquartered in Princeton, NJ, and have offices across the United States, which are supported by offices in India. Our model inverts the conventional global delivery model wherein offshore information technology (“IT”) service providers are based abroad and maintain a minimal presence in the United States. With a strong SAP focus, our client partnerships anchor around SAP cloud and digital services. In 2017, we signed a strategic partnership agreement with NEC America to offer SAP S/4 HANA (a next generation enterprise system) migration services. This partnership will allow us to offer our clients a broader spectrum of services. We pursue an acquisition strategy that seeks to disrupt the established business model of offshore IT service providers.

Our primary business objective is to provide our clients with a competitive advantage by enhancing their business capabilities and technologies with our expanding consulting services portfolio, which is aided by our business acquisitions. Our strategic acquisitions allow us to bring global service delivery, SAP S/4 HANA, SAP Business Intelligence, SAP Success Factors, SAP Hybris and high-end SAP consulting capabilities to a broader geographic market and customer base. We continue to leverage our growing geographical footprint and technical expertise to simultaneously expand our service and product offering. With each acquisition, our goal is to identify business synergies that will allow us to bring new services and products from one subsidiary to customers at our other subsidiaries. While we generate revenues from the consulting businesses of each of our acquired subsidiaries, we believe that additional revenues will be generated through new business relationships and services developed through our business combinations.

Background

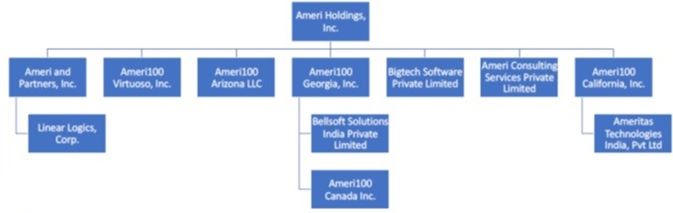

We were incorporated under the laws of the State of Delaware in February 1994 as Spatializer Audio Laboratories, Inc., which was a shell company immediately prior to our completion of a “reverse merger” transaction on May 26, 2015, in which we caused Ameri100 Acquisition, Inc., a Delaware corporation and our newly created, wholly owned subsidiary, to be merged with and into Ameri and Partners Inc. (“Ameri and Partners”), a Delaware corporation (the “Merger”). As a result of the Merger, Ameri and Partners became our wholly owned subsidiary with Ameri and Partners’ former stockholders acquiring a majority of the outstanding shares of our common stock. The Merger was consummated under Delaware law, pursuant to an Agreement of Merger and Plan of Reorganization, dated as of May 26, 2015 (the “Merger Agreement”), and in connection with the Merger we changed our name to AMERI Holdings, Inc. and do business under the brand name “Ameri100”.

Ameri Holdings, Inc., along with its eleven subsidiaries, Ameri and Partners, Inc., Ameri Consulting Service Private Ltd., Ameri100 Georgia Inc. (“Ameri Georgia”), Bellsoft India Solutions Private Ltd., Ameri100 Canada Inc. (formerly BSI Global IT Solutions Inc.), Linear Logics, Corp., Ameri100 Virtuoso Inc. (“Virtuoso”), Ameri100 Arizona LLC (“Ameri Arizona”), Bigtech Software Private Limited (“Bigtech”), Ameri100 California Inc. (“Ameri California) and Ameritas Technologies India Private Limited, provides SAP cloud, digital and enterprise services to clients worldwide.

Our Industry

Background

We operate in an intensely competitive IT outsourcing services industry, which competes on quality, service and costs. Though we are able to differentiate our company on all of these axes, our India-based capabilities ensure that labor arbitrage is our fundamental differentiator. Most offshore IT services providers have undertaken a “forward integration” to boost their capabilities and presence in their client geographies (large offshore presence with a small local presence). Conversely, large U.S. system integrators focus on “backward integration” to scale and boost their offshore narrative (offshore being the “back office” for the local operations). Today, the IT services industry is marked by the following characteristics:

|

Characteristic

|

Description

|

|

|

Mature Market

|

●

|

Most large global companies have already outsourced what they wanted to outsource.

|

|

Commoditized Business Model

|

●

|

North America and Europe continue to be the markets with attractive spending potential. However, increased regulations and visa dependencies prove to be a major drawback of the model.

|

|

●

|

The benefits realized from the business model are largely based on labor arbitrage, productivity benefits and portfolio restructuring. These contours have changed due to commoditization.

|

|

|

Insourcing

|

●

|

Extremely rapid changes in technology are forcing IT services–traditionally an outsourcing business—to adopt an insourcing model.

|

|

Rapid Technology Shifts

|

●

|

Cloud services, robotic process automation, artificial intelligence and internet of things are increasingly in demand as part of outsourcing engagements. Smart robots increasingly operate in the cloud, and a ‘labor-as-a-service’ approach has emerged, as clients and providers find that intelligent tools and virtual agents can be easily and flexibly hosted on cloud platforms.

|

|

●

|

Social media, cloud computing, mobility and big data will continue to be mainstays for any IT ecosystem.

|

|

|

●

|

The convergence of cloud computing, virtualization (applications and infrastructure) and utility computing is around the corner. The ability of a vendor to offer an integrated basket of services on a SaaS model, will be a key differentiator.

|

|

|

●

|

Enterprises are becoming more digital. There is a strong convergence of human and machine intelligence thanks to drivers like advanced sensors and machine learning. Operations and technology are converging.

|

|

|

Contracts & Decision Making

|

●

|

Large multi-year contracts will be renegotiated and broken down into shorter duration contracts and will involve multiple vendors rather than sole sourcing.

|

|

●

|

The ability to demonstrate value through Proof of Concepts (POCs) and willingness to offer outcome based pricing are becoming critical considerations for decision making, Requests for Proposal (RFP)-driven decisions are increasingly rare.

|

|

The SAP Industry

SAP as an ERP and Cloud product has become an industry by itself. The core SAP enterprise offering has been reinforced with cloud-based products that make the entire SAP ecosystem extremely attractive from our perspective due to the following attributes:

| ● |

The alignment of SAP to enterprises is extremely strong. Given the reliance of enterprises on applications, clients tend to make long-term bets on SAP as an enterprise solution.

|

| ● |

According to the September 2014 “HfS Blueprint Report” from by HfS Research Ltd., the SAP market is a multi-billion-dollar market that is very fragmented (there are over 5,000 consulting firms), with the three largest service providers capturing an increasing share of the market.

|

| ● |

A significant number of SAP customers must move to S/4 HANA by 2025).

|

Our Approach

Our solutions deliver significant business efficiency outcomes through turnkey projects, consulting and offshore services. We have adopted a “strategic acquisition model”, pursuant to which we acquire companies that support our goals. These businesses are realigned as parts of a viable and profitable operating model. We believe that our strategic service portfolio, deep industry experience and strong global talent pool offer a compelling proposition to clients. In 2017 we acquired ATCG Technology Solutions, Inc., which has become our wholly-owned subsidiary Ameri California. In 2016, we acquired three companies: Virtuoso, L.L.C. and DC&M Partners, L.L.C.in the U.S. (now Virtuoso and Ameri Arizona, respectively) and Bigtech in India. These strategic acquisitions have brought offshore delivery, SAP S/4 HANA, SAP SuccessFactors, SAP Hybris and high-end SAP consulting capabilities to our service portfolio.

Our Portfolio of Service Offerings

Our portfolio of service offerings expanded significantly in 2016 and 2017 with our acquisitions of Ameri Georgia, Ameri Arizona, Ameri California, Virtuoso and Bigtech. We expect our future service offerings to evolve as we continue to pursue our acquisitive growth strategy.

Our current portfolio of services is divided into three categories:

Cloud Services

An increasing trend in the IT services market is the adoption of cloud services. Historically, clients have resorted to on-premise software solutions, which required capital investments in infrastructure and data centers. Cloud services enable clients to build and host their applications at much lower costs. Our services offerings leverage the low cost and flexibility of cloud computing.

We have expertise in deploying SAP’s public, private and hybrid cloud services, as well as SAP S/4 HANA, SAP SuccessFactors and SAP Hybris cloud migration services. Our teams are experienced in the rapid delivery of cloud services. We perform SAP application and cloud support and SAP cloud development. Additionally, we provide cloud automation solutions that focus on business objectives and organizational growth.

Digital Services

We have developed several cutting-edge mobile solutions, including Simple Advance Planning and Optimization (“APO”), the SAP IBP/S&OP Mobile Analytics App and the Langer Index. The Simple APO mobile application (app) provides sales professionals with real-time collaboration capabilities and customer data, on their mobile devices. It increases the efficiency of the sales process and the accuracy of customer needs forecasting. The SAP IBP mobile app enables the real-time management and analysis of sales and operations planning (S&OP) related data from mobile devices. SAP is an implementation partner for this app. SAP has recognized the app’s value to the ecosystem, as S&OP apps are complex and difficult to design. The Langer Index is a mobile-supported, web-based assessment system for collecting and analyzing IT organizational effectiveness.

We are also active in robotic process automation (“RPA”), which leverages the capability of artificially intelligent software agents for business process automation. We have expertise in automating disparate and redundant data entry tasks by configuring software robots that seamlessly integrate with existing software systems. We also provide RPA solutions for reporting and analysis and deliver insights into business functions by translating large data into structured reports. Lastly, we have a working partnership with Blue Prism, a leading RPA solutions provider, which makes it possible for us to automate up to one-third of all standard back-office operations.

Enterprise Services

We design, implement and manage Business Intelligence (“BI”) and analytics solutions. BI helps our clients navigate the market better by identifying new trends and by targeting top-selling products. We also enable clients to use BI for generating instant financial reports and analytics of customer, product and cost information over time. In addition, we provide solutions for metadata repository, master data management and data quality. Finally, we determine BI demands across various platforms.

Other key enterprise services that we offer include consulting services for global and regional SAP implementations, SAP/IT solution advisory and architectural services, project management services, IT/ERP strategy and vendor selection services. Often clients have relied on us to deliver services in non-SAP packages, as well.

Our Growth Strategy

Our growth strategy is based on customer-driven business expansion and strategic acquisitions of SAP services companies. We introduce specific key account management strategies to grow organically by cross selling and upselling different services across business units. It is our goal to be a leader in the SAP cloud, digital and enterprise services market. We use strategic acquisitions, alliances and partnerships to achieve this goal.

We have complementary near-term and longer-term strategies. In the short-term, we continue to focus on high-end consulting and solutions in the SAP ecosystem. Our medium-term focus will be to make an entry into cloud engagements and SAP HANA. Signing up with NEC America as a strategic partner for the SAP HANA migration will be critical to achieving this objective. Additionally, we plan to gain market share in high-growth areas within the SAP ecosystem such as Hybris, SuccessFactors and BI/BW/SAP S/4 HANA. In the long-term, we plan to identify and acquire firms in the areas of Artificial Intelligence (AI) and robotics to bolster our AIR (AI + Internet of things + robotics) practice. We believe that during each phase of our growth strategy business and market conditions will require our plans to evolve or change, and we plan to be agile in addressing both opportunities and exigencies.

The integration of each of our acquisitions into our business enterprise requires establishing our company’s standard operating procedures at each acquired entity, seamlessly transitioning each acquired entity’s branding to the “Ameri100” brand and assessing any necessity to transition account management. The integration process also requires us to evaluate any product-line expansions made possible by the acquired entity and how to bring new product lines to the broader customer base of the entire Company. With the integration of each acquisition, we face challenges of maintaining cross-company visibility and cooperation, creating a cohesive corporate culture, handling unexpected customer reactions and changes and aligning the interests of the acquired entity’s leadership with the interests of the Company. To date, these challenges have been manageable, and we are becoming more adept at managing integration issues with each new acquisition.

Sales and Marketing

We combine traditional sales with our strength in industries and technology. Our sales function is composed of direct sales and inside sales professionals. Both work closely with our solutions directors to identify potential opportunities within each account. We currently have over 100+ active clients. Using a consultative selling methodology (working with clients to prescribe a solution that suits their need in terms of efficiency, cost and timelines), target prospects are identified and a pursuit plan is developed for each key account. We utilize a blended sales model that combines consultative selling with traditional sales methods. Once the customer has engaged us, the sales, solutions and marketing teams monitor and manage the relationship with the help of customer relationship management software.

Our marketing strategy is to build a strong, sustainable brand image for our company, position us in the SAP arena and facilitate business opportunities. We use a variety of marketing programs across traditional and social channels to target our prospective and current customers, including webinars, targeted email campaigns, co-sponsoring customer events with SAP to create customer and prospect awareness, search engine marketing and advertising to drive traffic to our web properties, and website development to engage and educate prospects and generate interest through white papers, case studies and marketing collateral.

Revenues and Customers

We generate revenue primarily through consulting services performed in the fulfillment of written service contracts. The service contracts we enter into generally fall into two categories: (1) time-and-materials contracts and (2) fixed-price contracts.

When a customer enters into a time-and-materials or fixed-price, (or a periodic retainer-based) contract, we recognize revenue in accordance with an evaluation of the deliverables in each contract. If the deliverables represent separate units of accounting, we then measure and allocate the consideration from the arrangement to the separate units, based on vendor-specific objective evidence of the value for each deliverable.

The revenue under time-and-materials contracts is recognized as services are rendered and performed at contractually agreed upon rates. Revenue pursuant to fixed-price contracts is recognized under the proportional performance method of accounting. We routinely evaluate whether revenue and profitability should be recognized in the current period. We estimate the proportional performance on our fixed-price contracts on a monthly basis utilizing hours incurred to date as a percentage of total estimated hours to complete the project.

For the twelve months ended December 31, 2017 and December 31, 2016, sales to five major customers accounted for approximately 43% and 53% of our total revenue, respectively.

Technology Research and Development

We regard our services and solutions and related software products as proprietary. We rely primarily on a combination of copyright, trademark and trade secret laws of general applicability, employee confidentiality and invention assignment agreements, distribution and software protection agreements and other intellectual property protection methods to safeguard our technology and software products. We have not applied for patents on any of our technology. We also rely upon our efforts to design and produce new applications and upon improvements to existing software products to maintain a competitive position in the marketplace.

We did not make any material expenditures on research or development activities for the twelve months ended December 31, 2017 and December 31, 2016.

Strategic Alliances

Through our Lean Enterprise Architecture Partnership (“LEAP”) methodology, we have strategic alliances with technology specialists who perform services on an as-needed basis for clients. We partner with niche specialty firms globally to obtain specialized resources to meet client needs. Our business partners include executive recruiters, staffing firms and niche technology companies. The terms of each strategic alliance arrangement depend on the nature of the particular partnership. Such alliance arrangements typically set forth deliverables, scope of the services to be delivered, costs of services and terms and conditions of payment (generally 45 to 90 days for payment to be made). Each alliance arrangement also typically includes terms for indemnification of our company, non-solicitation of each partner’s employees by the other partner and dispute resolution by arbitration.

Alliances and partnerships broaden our offerings and make us a one-stop solution for clients. Our team constantly produces services that complement our portfolio and build strategic partnerships. Our partner companies range from digital marketing strategy consulting firms to large infrastructure players.

On any given project we evaluate a client’s needs and make our best effort to meet them with our full-time specialists. However, in certain circumstances, we may need to go outside the Company, and in this case we approach our strategic partners to tap into their pools of technology specialists. Project teams are usually composed of a mix of our full time employees and outside technology specialists. Occasionally, a project team may consist of a Company manager and a few outside technology specialists. While final accountability for any of our projects rests with the Company, the outside technology specialists are incentivized to successfully complete a project with project completion payments that are in addition to hourly billing rates we pay the outside technology specialists.

Competition

The large number of competitors and the speed of technology change make IT services and outsourcing a challenging business. Competitors in this market include systems integration firms, contract programming companies, application software companies, traditional large consulting firms, professional services groups of computer equipment companies and facilities management and outsourcing companies. Examples of our competitors in the IT services industry include Accenture, Cartesian Inc., Cognizant, Hexaware Technologies Limited, Infosys Technologies Limited, Mindtree Limited, RCM Technologies Inc., Tata Consultancy Services Limited, Virtusa, Inc. and Wipro Limited.

We believe that the principal factors for success in the IT services and outsourcing market include performance and reliability; quality of technical support, training and services; responsiveness to customer needs; reputation and experience; financial stability and strong corporate governance; and competitive pricing.

Some of our competitors have significantly greater financial, technical and marketing resources and/or greater name recognition, but we believe we are well positioned to capitalize on the following competitive strengths to achieve future growth:

| · |

well-developed recruiting, training and retention model;

|

| · |

successful service delivery model;

|

| · |

broad referral base;

|

| · |

continual investment in process improvement and knowledge capture;

|

| · |

investment in research and development;

|

| · |

strong corporate governance; and

|

| · |

custom strategic partnerships to provide breadth and depth of services.

|

Employees

As of December 31, 2017, our total headcount was 417, which includes employees and billable subcontractors. We routinely supplement our billable employee staff with billable subcontractors, which totaled 153 at December 31, 2017. Our employees are not part of a collective bargaining arrangement and we believe our relations with our employees are good. We do not have any material employment agreement with our executive officers.

Recent Events and Acquisitions

Public Offering and Uplisting of Common Stock to Nasdaq

On November 21, 2017, we completed an underwritten public offering of 1,475,000 shares of our common stock, at a price of $4.115 per share, and warrants to purchase up to an aggregate of 1,475,000 shares of our common stock, at a price of $0.01 per warrant. The warrants have a per share exercise price of $4.115, were exercisable as of November 21, 2017 and expire five years from that date. The gross proceeds to us from this offering were approximately $6,084,375, before deducting underwriting discounts and commissions and other estimated offering expenses. In connection with the offering, we uplisted our common stock from the OTCQB Marketplace to trading on The Nasdaq Capital Market under the ticker symbol “AMRH”, and we listed the publicly offered warrants for trading on The Nasdaq Capital Market under the ticker symbol “AMRHW”.

On January 24, 2018, we received confirmation from our transfer agent, Corporate Stock Transfer, Inc., which also serves as the warrant agent for the public warrant, that through such date certain holders of warrants had cumulatively exercised warrants for the purchase of a total of 153,060 shares of our common stock, at an exercise price of $4.115 per share, for gross proceeds to us of $629,841.90.

Acquisition of Ameri California

On March 10, 2017, we acquired 100% of the shares of ATCG Technology Solutions, Inc., a Delaware corporation, pursuant to the terms of a Share Purchase Agreement among the Company, Ameri California, all of the stockholders of Ameri California (the “Stockholders”), and the Stockholders’ representative. In July 2017, the name of ATCG Technology Solutions, Inc. was changed to Ameri100 California Inc. Ameri California provides U.S. domestic, offshore and onsite SAP consulting services and has its main office in Folsom, California. Ameri California specializes in providing SAP Hybris, SAP Success Factors and business intelligence services.

The aggregate purchase price for the acquisition of Ameri California was $8,784,533, consisting of:

| (a) |

576,923 shares of our common stock, valued at approximately $3.8 million based on the closing price of our common stock on the closing date of the acquisition;

|

| (b) |

Unsecured promissory notes issued to certain of Ameri California’s selling stockholders for the aggregate amount of $3,750,000 (which notes bear interest at a rate of 6% per annum and mature on June 30, 2018);

|

| (c) |

Earn-out payments in shares of our common stock (up to an aggregate value of $1,200,000 worth of shares) to be paid, if earned, in each of 2018 and 2019 based on certain revenue and earnings before interest taxes, depreciation and amortization (“EBITDA”) targets as specified in the purchase agreement. We estimate those targets will be fully achieved; and

|

| (d) |

An additional cash payment of $55,687 for cash that was left in Ameri California at closing.

|

On February 28, 2018, we entered into an Amendment to 6% Unsecured Promissory Note and Waiver Agreement (the “Amendment”) by and between the Company and Moneta Ventures Fund I, L.P. (“Moneta”). The Amendment amended the terms of the Company’s 6% Unsecured Promissory Note Due June 30, 2018, issued on March 20, 2017, by and between the Company and Moneta (the “Moneta Note”). Among other things, the Amendment provided for the extension of the maturity of the Moneta Note to August 31, 2018, amendment of the payment terms of the Moneta Note, waiver by Moneta of the existence of any Company event of default pursuant to the Moneta Note as of February 28, 2018 and waiver by the Company of certain restrictions with respect to the resale of certain restricted common stock of the Company held by Moneta.

Acquisition of Ameri Arizona

On July 29, 2016, we acquired 100% of the membership interests of DC&M Partners, L.L.C., an Arizona limited liability company, pursuant to the terms of a Membership Interest Purchase Agreement by and among us, Ameri Arizona, all of the members of Ameri Arizona, Giri Devanur and Srinidhi “Dev” Devanur, our former President and Chief Executive Officer and Executive Vice Chairman, respectively. In July 2017, the name of DC&M Partners, L.L.C. was changed to Ameri100 Arizona LLC. Ameri Arizona is an SAP consulting company headquartered in Chandler, Arizona. Ameri Arizona provides its clients with a wide range of information technology development, consultancy and management services with an emphasis on the design, build and rollout of SAP implementations and related products. Ameri Arizona is also an SAP-certified software partner, having launched its SAP reporting, extraction and distribution tool called “IRIS”. Ameri Arizona services clients in diverse industries, including retail, apparel/footwear, third-party logistics providers, chemicals, consumer goods, energy, high-tech electronics, media/entertainment and aerospace.

The aggregate purchase price for the acquisition of Ameri Arizona was $15,816,000, consisting of:

| (a) |

A cash payment in the amount of $3,000,000 at closing;

|

| (b) |

1,600,000 shares of our common stock (valued at approximately $10.4 million based on the $6.51 closing price of our common stock on the closing date of the acquisition), which are to be issued on July 29, 2018 or upon a change of control of our company (whichever occurs earlier); and

|

| (c) |

Earn-out payments of $1,500,000 payable in cash each year to be paid, if earned, through the achievement of annual revenue and gross margin targets in 2017 and 2018.

|

In January 17, 2018, we resolved the payment of all earn-out payments to the former members of Ameri Arizona with respect to the 2016 earn-out period in connection with the Ameri Arizona membership interest purchase agreement, and we have no further payment obligations with respect to the 2016 earn-out period.

Acquisition of Virtuoso

On July 22, 2016, we, through wholly-owned acquisition subsidiaries, acquired all of the outstanding membership interests of Virtuoso, L.L.C., a Kansas limited liability company, pursuant to the terms of an Agreement of Merger and Plan of Reorganization, by and among us, Virtuoso Acquisition Inc., Ameri100 Virtuoso Inc., Virtuoso and the sole member of Virtuoso (the “Sole Member”). Virtuoso is an SAP consulting firm specialized in providing services on SAP S/4 HANA finance, enterprise mobility and cloud migration and is based in Leawood, Kansas. In connection with the merger, Virtuoso’s name was changed to Ameri100 Virtuoso Inc. The Virtuoso acquisition did not constitute a significant acquisition for the Company for purposes of Regulation S-X.

The total purchase price paid to the Sole Member for the acquisition of Virtuoso was $1,831,881, consisting of:

| (a) |

A cash payment in the amount of $675,000 which was due within 90 days of closing and was paid on October 21, 2016;

|

| (b) |

101,250 shares of our common stock at closing, valued at approximately $700,000 based on the $6.51 closing price of our common stock on the closing date of the acquisition; and

|

| (c) |

Earn-out payments in cash and stock of $450,000 and approximately $560,807, respectively, to be paid, if earned, through the achievement of annual revenue and gross margin targets in 2017, 2018 and 2019. Out of the total contingent consideration of approximately $1,000,000, we only considered 50% of the earn-out in the purchase price, mainly due to the reorganization of Virtuoso.

|

As of January 23, 2018, we had resolved all remaining payments under the Virtuoso merger agreement with the former sole-member of Virtuoso and we have no further payment obligations pursuant thereto.

Acquisition of Bigtech Software Private Limited

On June 23, 2016, we entered into a definitive agreement to purchase Bigtech Software Private Limited, a pure-play SAP services company providing a wide range of SAP services including turnkey implementations, application management, training and basis ABAP support. Based in Bangalore, India, Bigtech offers SAP services to improve business operations at companies of all sizes and verticals. The acquisition of Bigtech was effective as of July 1, 2016, and the total consideration for the acquisition of Bigtech was $850,000, consisting of:

| (a) |

A cash payment in the amount of $340,000 which was due within 90 days of closing and was paid on September 22, 2016;

|

| (b) |

Warrants for the purchase of 51,000 shares of our common stock (valued at approximately $250,000 based on the $6.51 closing price of our common stock on the closing date of the acquisition), with such warrants exercisable for two years; and

|

| (c) |

$255,000, which may become payable in cash earn-outs to the sellers of Bigtech, if Bigtech achieves certain pre-determined revenue and EBITDA targets in 2017 and 2018. We estimate the earn-out payments to be earned at 100% of the targets set forth in the purchase agreement.

|

Bigtech’s financial results are included in our condensed consolidated financial results starting July 1, 2016. The Bigtech acquisition did not constitute a significant acquisition for the Company for purposes of Regulation S-X. The valuation of Bigtech was made on the basis of its projected revenues.

Acquisition of Ameri Georgia

On November 20, 2015, we completed the acquisition of Bellsoft, Inc., a consulting company based in Lawrenceville, Georgia with over 175 consultants specialized in the areas of SAP software, business intelligence, data warehousing and other enterprise resource planning services. Following the acquisition, the name of Bellsoft, Inc. was changed to Ameri100 Georgia Inc. (“Ameri Georgia”). Ameri Georgia has operations in the United States, Canada and India. For financial accounting purposes, we recognized September 1, 2015 as the effective date of the acquisition. The total consideration for the acquisition of Ameri Georgia was $9,910,817, consisting of:

| (a) |

A cash payment in the amount of $3,000,000, which was paid at closing;

|

| (b) |

235,295 shares of our common stock issued at closing, valued at approximately $1,000,000 based on the closing price of our common stock on the closing date of the acquisition;

|

| (c) |

$250,000 quarterly cash payments to be paid on the last day of each calendar quarter of 2016;

|

| (d) |

A $1,000,000 cash reimbursement to be paid 5 days following closing to compensate Ameri Georgia for a portion of its approximate cash balance as of September 1, 2015;

|

| (e) |

Approximately $2,910,817 paid within 30 days of closing in connection with the excess of Ameri Georgia’s accounts receivable over its accounts payable as of September 1, 2015; and

|

| (f) |

Earn-out payments of approximately $500,000 a year for 2016 and 2017, if earned through the achievement of annual revenue and EBITDA targets specified in the purchase agreement, subject to downward or upward adjustment depending on actual results.

|

On January 17, 2018, we completed all payment obligations to the former shareholders of Ameri Georgia in connection with the Ameri Georgia share purchase agreement, and we have no further payment obligations pursuant thereto.

Available Information

Our executive office is located at 100 Canal Pointe Boulevard, Suite 108, Princeton, NJ 08540. Our telephone number is (732) 243-9250, our fax number is (732) 243-9254 and our website is www.ameri100.com. We provide free access to various reports that we file with or furnish to the U.S. Securities and Exchange Commission through our website, as soon as reasonably practicable after they have been filed or furnished. These reports include, but are not limited to, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to these reports. Our Securities and Exchange Commission (“SEC”) reports can be accessed through the investors section of our website (http://ameri100.com/page/investors/), and we intend to disclose any changes to or waivers from our Code of Ethics for our Chief Executive Officer and Senior Financial Officers and our Code of Ethics and Business Conduct that would otherwise be required to be disclosed under Item 5.05 of Form 8-K on our website. In addition, the public may read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. We are an electronic SEC filer. The SEC maintains a website that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The internet address of the SEC’s website is http://www.sec.gov. Information on our website does not constitute part of this annual report on Form10-K or any other report we file or furnish with the SEC.

Investors and others should note that we use social media to communicate with our subscribers and the public about our company, our services, new product developments and other matters. Any information that we consider to be material to an evaluation of our company will be included in filings on the SEC EDGAR website and may also be disseminated using our investor relations website (http://ir.ameri100.com/) and press releases.

In addition to the information set forth at the beginning of Management’s Discussion and Analysis entitled “Special Note Regarding Forward-Looking Information”, investors should consider that there are numerous and varied risks, known and unknown, that may prevent us from achieving our goals. If any of these risks actually occur, our business, financial condition or results of operation may be materially and adversely affected. In such case, the trading price of our common stock could decline and investors could lose all or part of their investment.

Risks Relating to Our Business and Industry

We recorded a net loss for the twelve months ended December 31, 2017 and December 31, 2016 and there can be no assurance that our future operations will result in net income.

For the twelve months ended December 31, 2017, and December 31, 2016, we had net revenue of $48.6 million and $36.2 million, respectively, and we had comprehensive net loss of $11.2 million and $2.8 million, respectively. At December 31, 2017, we had stockholders’ equity of approximately $19 million. There can be no assurance that our future operations will result in net income. Our failure to increase our revenues or improve our gross margins will harm our business. We may not be able to sustain or increase profitability on a quarterly or annual basis in the future. If our revenues grow more slowly than we anticipate, our gross margins fail to improve or our operating expenses exceed our expectations, our operating results will suffer. The fee we charge for our solutions and services may decrease, which would reduce our revenues and harm our business. If we are unable to sell our solutions at acceptable prices relative to our costs, or if we fail to develop and introduce new solutions on a timely basis and services from which we can derive additional revenues, our financial results will suffer.

We and our subsidiaries have limited operating histories and therefore we cannot ensure the long-term successful operation of our business or the execution of our business plan.

Our prospects must be considered in light of the risks, expenses and difficulties frequently encountered by growing companies in new and rapidly evolving markets, such as the technology consulting markets in which we operate. We must meet many challenges including:

| · |

establishing and maintaining broad market acceptance of our solutions and services and converting that acceptance into direct and indirect sources of revenue;

|

| · |

establishing and maintaining adoption of our technology solutions in a wide variety of industries and on multiple enterprise architectures;

|

| · |

timely and successfully developing new solutions and services and increasing the functionality and features of existing solutions and services;

|

| · |

developing solutions and services that result in high degree of enterprise client satisfaction and high levels of end-customer usage;

|

| · |

successfully responding to competition, including competition from emerging technologies and solutions;

|

| · |

developing and maintaining strategic relationships to enhance the distribution, features, content and utility of our solutions and services; and

|

| · |

identifying, attracting and retaining talented personnel at reasonable market compensation rates in the markets in which we employ.

|

Our business strategy may be unsuccessful and we may be unable to address the risks we face in a cost-effective manner, if at all. If we are unable to successfully address these risks our business will be harmed.

We face working capital constraints and may not have sufficient working capital in the long term and there is no assurance that we will be able to obtain additional financing, which could negatively impact our business.

We have incurred significant and recurring operational losses as a result of our ongoing acquisition strategy. We have outstanding cash payment obligations related to our past acquisitions of approximately $4.3 million. In addition, under the terms of our Series A Preferred Stock, we are currently obligated to pay approximately $2 million in cash dividends per year on such stock through fiscal year 2019. If our current cash position does not improve significantly, we will not have sufficient cash on hand to meet these obligations. Due to our working capital constraints, we are not current in all payments to all our unsecured noteholders. We are working with certain of our unsecured noteholders to negotiate payment terms until we are able to raise more capital.

Operational streamlining that was completed in 2017 is anticipated to provide cash savings of approximately $1.75 million per year. We believe additional cost-cutting efforts will further reduce cash used in operations. In addition, we believe that we can obtain additional external financing to meet future cash requirements. We raised $1.25 million in March 2017 through the sale of convertible notes and over $6.7 million in gross proceeds through our public offering of common stock and warrants in November 2017.

There can be no assurance that we will be able to secure additional sources of capital or that cost savings will provide sufficient working capital. If we continue to be unable to pay all outstanding payments under our unsecured notes, the unpaid noteholders may take legal action against us, they may accelerate the payment of the principal under the applicable notes, and our senior secured lender may call a cross-default under our existing credit facility, which could result in the acceleration of the obligations thereunder and have a negative impact on our revenue and financial results. Should we be unable to raise sufficient debt or equity capital, we could be forced to cease operations. Our plan regarding these matters is to work to raise additional debt and/or equity financing to allow us the ability to cover our current cash flow requirements and meet our obligations as they become due. There can be no assurances that financing will be available or if available, that such financing will be available under favorable terms.

The economic environment, pricing pressures, and decreased employee utilization rates could negatively impact our revenues and operating results.

Spending on technology products and services is subject to fluctuations depending on many factors, including the economic environment in the markets in which our clients operate.

Reduced ERP spending in response to a challenging economic environment leads to increased pricing pressure from our clients, which may adversely impact our revenue, gross profits, operating margins and results of operations.

In addition to the business challenges and margin pressure resulting from economic slowdown in the markets in which our clients operate and the response of our clients to such slowdown, there is also a growing trend among consumers of ERP services towards consolidation of technology service providers in order to improve efficiency and reduce costs. Our success in the competitive bidding process for new projects or in retaining existing projects is dependent on our ability to fulfil client expectations relating to staffing, delivery of services and more stringent service levels. If we fail to meet a client’s expectations in such projects, this would likely adversely impact our business, revenues and operating margins. In addition, even if we are successful in winning the mandates for such projects, we may experience significant pressure on our operating margins as a result of the competitive bidding process.

Moreover, our ability to maintain or increase pricing is restricted as clients often expect that as we do more business with them, they will receive volume discounts or lower rates. In addition, existing and new customers are also increasingly using third-party consultants with broad market knowledge to assist them in negotiating contractual terms. Any inability to maintain or increase pricing on account of this practice may also adversely impact our revenues, gross profits, operating margins and results of operations.

Uncertain global SAP consulting market conditions may continue to adversely affect demand for our services.

We rely heavily on global demand for ERP services, especially SAP consulting by customers. Any weakness for these ERP services by global customers will adversely affect our revenue projections and hence our profits. SAP AG is adapting itself to the changes in the market especially towards cloud offerings. These changes may lead to SAP losing its market share to other competitors like Oracle, Microsoft, Salesforce and Workday among many other newer players. With these setbacks to SAP, we may face uncertain future due to dramatic changes in the market place which in turn will affect our revenues and profits.

Our success depends largely upon our highly-skilled technology professionals and our ability to hire, attract, motivate, retain and train these personnel.

Our ability to execute projects, maintain our client relationships and acquire new clients depends largely on our ability to attract, hire, train, motivate and retain highly skilled technology professionals, particularly project managers and other mid-level professionals. If we cannot hire, motivate and retain personnel, our ability to bid for projects, obtain new projects and expand our business will be impaired and our revenues could decline.

Increasing worldwide competition for skilled technology professionals and increased hiring by technology companies may affect our ability to hire and retain an adequate number of skilled and experienced technology professionals, which may in turn have an adverse effect on our business, results of operations and financial condition.

In addition, the demands of changes in technology, evolving standards and changing client preferences may require us to redeploy and retrain our technology professionals. If we are unable to redeploy and retrain our technology professionals to keep pace with continuing changes in technology, evolving standards and changing client preferences, this may adversely affect our ability to bid for and obtain new projects and may have a material adverse effect on our business, results of operations and financial condition.

Our strategy to increase our growth through acquisitions may be unsuccessful and could adversely affect our business and results.

As part of our growth strategy, we intend to further acquire other businesses; however, there is no assurance that we will be able to identify appropriate acquisition targets, successfully acquire identified targets or successfully integrate the business of acquired companies to realize the full benefits of the combined businesses.

While we recently acquired Ameri California, Ameri Arizona, Virtuoso and Bigtech in connection with our growth strategy to acquire other businesses, we can provide no assurance that we will identify appropriate acquisition targets, successfully complete any future acquisitions or successfully integrate the business of companies we do acquire. Even if we successfully acquire a business entity, there is no assurance that our combined business will become profitable. The process of completing the integration of acquired businesses could cause an interruption of, or loss of momentum in, the activities of our company and the loss of key personnel. The diversion of management’s attention and any delays or difficulties encountered in connection with the pursuit of business acquisitions and the integration of acquired businesses, and the incurrence of significant, acquisition related costs in connection with proposed and completed acquisitions, could have an adverse effect on our business, financial condition or results of operations.

We face intense competition from other service providers.

We are subject to intense competition in the industry in which we operate which may adversely affect our results of operations, financial condition and cash flows. We operate in a highly competitive industry, which is served by numerous global, national, regional and local firms. Our industry has experienced rapid technological developments, changes in industry standards and customer requirements. The principal competitive factors in the IT markets include the range of services offered, size and scale of service provider, global reach, technical expertise, responsiveness to client needs, speed in delivery of IT solutions, quality of service and perceived value. Many companies also choose to perform some or all of their back-office IT and IT-enabled operations internally. Such competitiveness requires us to keep pace with technological developments and maintains leadership; enhance our service offerings, including the breadth of our services and portfolio, and address increasingly sophisticated customer requirements in a timely and cost-effective manner.

We market our service offerings to large and medium-sized organizations. Generally, the pricing for the projects depends on the type of contract, which includes time and material contracts, annual maintenance contracts (fixed time frame), fixed price contracts and transaction price based contracts. The intense competition and the changes in the general economic and business conditions can put pressure on us to change our prices. If our competitors offer deep discounts on certain services or provide services that the marketplace considers more valuable, we may need to lower prices or offer other favorable terms in order to compete successfully. Any broad-based change to our prices and pricing policies could cause revenues to decline and may reduce margins and could adversely affect results of operations, financial condition and cash flows. Some of our competitors may bundle software products and services for promotional purposes or as a long-term pricing strategy or provide guarantees of prices and product implementations. These practices could, over time, significantly constrain the prices that we can charge for certain services. If we do not adapt our pricing models to reflect changes in customer use of our services or changes in customer demand, our revenues and cash flows could decrease.

Our competitors may have significantly greater financial, technical and marketing resources and greater name recognition and, therefore, may be better able to compete for new work and skilled professionals. Similarly, if our competitors are successful in identifying and implementing newer service enhancements in response to rapid changes in technology and customer preferences, they may be more successful at selling their services. If we are unable to respond to such changes our results of operations may be harmed. Further, a client may choose to use its own internal resources rather than engage an outside firm to perform the types of services we provide. We cannot be certain that we will be able to sustain our current levels of profitability or growth in the face of competitive pressures, including competition for skilled technology professionals and pricing pressure from competitors employing an on-site/offshore business model.

In addition, we may face competition from companies that increase in size or scope as the result of strategic alliances such as mergers or acquisitions. These transactions may include consolidation activity among hardware manufacturers, software companies and vendors and service providers. The result of any such vertical integration may be greater integration of products and services that were once offered separately by independent vendors. Our access to such products and services may be reduced as a result of such an industry trend, which could adversely affect our competitive position. These types of events could have a variety of negative effects on our competitive position and our financial results, such as reducing our revenue, increasing our costs, lowering our gross margin percentage and requiring us to recognize impairments on our assets.

Our business could be adversely affected if we do not anticipate and respond to technology advances in our industry and our clients’ industries.

The IT and global outsourcing and SAP consulting services industries are characterized by rapid technological change, evolving industry standards, changing client preferences and new product introductions. Our success will depend in part on our ability to develop IT solutions that keep pace with industry developments. We may not be successful in addressing these developments on a timely basis or at all. In addition, products or technologies developed by others may not render our services noncompetitive or obsolete. Our failure to address these developments could have a material adverse effect on our business, results of operations, financial condition and cash flows.

A significant number of organizations are attempting to migrate business applications to advanced technologies. As a result, our ability to remain competitive will be dependent on several factors, including our ability to develop, train and hire employees with skills in advanced technologies, breadth and depth of process and technology expertise, service quality, knowledge of industry, marketing and sales capabilities. Our failure to hire, train and retain employees with such skills could have a material adverse impact on our business. Our ability to remain competitive will also be dependent on our ability to design and implement, in a timely and cost- effective manner, effective transition strategies for clients moving to advanced architectures. Our failure to design and implement such transition strategies in a timely and cost-effective manner could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Our operations and assets in India expose us to regulatory, economic, political and other uncertainties in India, which could harm our business.

We have an offshore presence in India where a number of our technical professionals are located. In the past, the Indian economy has experienced many of the problems confronting the economies of developing countries, including high inflation and varying gross domestic product growth. Salaries and other related benefits constitute a major portion of our total operating costs. Many of our employees based in India where our wage costs have historically been significantly lower than wage costs in the United States and Europe for comparably skilled professionals, and this has been one of our competitive advantages. However, wage increases in India or other countries where we have our operations may prevent us from sustaining this competitive advantage if wages increase. We may need to increase the levels of our employee compensation more rapidly than in the past to retain talent. If such events occur, we may be unable to continue to increase the efficiency and productivity of our employees and wage increases in the long term may reduce our profit margins.

Our clients may seek to reduce their dependence on India for outsourced IT services or take advantage of the services provided in countries with labor costs similar to or lower than India.

Clients which presently outsource a significant proportion of their IT services requirements to vendors in India may, for various reasons, including in response to rising labor costs in India and to diversify geographic risk, seek to reduce their dependence on one country. We expect that future competition will increasingly include firms with operations in other countries, especially those countries with labor costs similar to or lower than India, such as China, the Philippines and countries in Eastern Europe. Since wage costs in our industry in India are increasing, our ability to compete effectively will become increasingly dependent on our reputation, the quality of our services and our expertise in specific industries. If labor costs in India rise at a rate that is significantly greater than labor costs in other countries, our reliance on the labor in India may reduce our profit margins and adversely affect our ability to compete, which would, in turn, have a negative impact on our results of operations.

Our business could be materially adversely affected if we do not or are unable to protect our intellectual property or if our services are found to infringe upon or misappropriate the intellectual property of others.

Our success depends in part upon certain methodologies and tools we use in designing, developing and implementing applications systems in providing our services. We rely upon a combination of nondisclosure and other contractual arrangements and intellectual property laws to protect confidential information and intellectual property rights of ours and our third parties from whom we license intellectual property. We enter into confidentiality agreements with our employees and limit distribution of proprietary information. The steps we take in this regard may not be adequate to deter misappropriation of proprietary information and we may not be able to detect unauthorized use of, protect or enforce our intellectual property rights. At the same time, our competitors may independently develop similar technology or duplicate our products or services. Any significant misappropriation, infringement or devaluation of such rights could have a material adverse effect upon our business, results of operations, financial condition and cash flows.

Litigation may be required to enforce our intellectual property rights or to determine the validity and scope of the proprietary rights of others. Any such litigation could be time consuming and costly. Although we believe that our services do not infringe or misappropriate on the intellectual property rights of others and that we have all rights necessary to utilize the intellectual property employed in our business, defense against these claims, even if not meritorious, could be expensive and divert our attention and resources from operating our company. A successful claim of intellectual property infringement against us could require us to pay a substantial damage award, develop non-infringing technology, obtain a license or cease selling the products or services that contain the infringing technology. Such events could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Any disruption in the supply of power, IT infrastructure and telecommunications lines to our facilities could disrupt our business process or subject us to additional costs.

Any disruption in basic infrastructure, including the supply of power, could negatively impact our ability to provide timely or adequate services to our clients. We rely on a number of telecommunications service and other infrastructure providers to maintain communications between our various facilities and clients in India, the United States and elsewhere. Telecommunications networks are subject to failures and periods of service disruption, which can adversely affect our ability to maintain active voice and data communications among our facilities and with our clients. Such disruptions may cause harm to our clients’ business. We do not maintain business interruption insurance and may not be covered for any claims or damages if the supply of power, IT infrastructure or telecommunications lines is disrupted. This could disrupt our business process or subject us to additional costs, materially adversely affecting our business, results of operations, financial condition and cash flows.

System security risks and cyber-attacks could disrupt our information technology services provided to customers, and any such disruption could reduce our expected revenue, increase our expenses, damage our reputation and adversely affect our stock price and the value of our warrants.

Security and availability of IT infrastructure is of the utmost concern for our business, and the security of critical information and infrastructure necessary for rendering services is also one of the top priorities of our customers.

System security risks and cyber-attacks could breach the security and disrupt the availability of our IT services provided to customers. Any such breach or disruption could allow the misuse of our information systems, resulting in litigation and potential liability for us, the loss of existing or potential clients, damage to our reputation and diminished brand value and could have a material adverse effect on our financial condition.

Our network and our deployed security controls could also be penetrated by a skilled computer hacker or intruder. Further, a hacker or intruder could compromise the confidentiality and integrity of our protected information, including personally identifiable information; deploy malicious software or code like computer viruses, worms or Trojan horses, etc. may exploit any security vulnerabilities, known or unknown, of our information system; cause disruption in the availability of our information and services; and attack our information system through various other mediums.

We also procure software or hardware products from third party vendors that provide, manage and monitor our services. Such products may contain known or unfamiliar manufacturing, design or other defects which may allow a security breach or cyber-attack, if exploited by a computer hacker or intruder, or may be capable of disrupting performance of our IT services and prevent us from providing services to our clients.

In addition, we manage, store, process, transmit and have access to significant amounts of data and information that may include our proprietary and confidential information and that of our clients. This data may include personal information, sensitive personal information, personally identifiable information or other critical data and information, of our employees, contractors, officials, directors, end customers of our clients or others, by which any individual may be identified or likely to be identified. Our data security and privacy systems and procedures meet applicable regulatory standards and undergo periodic compliance audits by independent third parties and customers. However, if our compliance with these standards is inadequate, we may be subject to regulatory penalties and litigation, resulting in potential liability for us and an adverse impact on our business.

We are still susceptible to data security or privacy breaches, including accidental or deliberate loss and unauthorized disclosure or dissemination of such data or information. Any breach of such data or information may lead to identity theft, impersonation, deception, fraud, misappropriation or other offenses in which such information may be used to cause harm to our business and have a material adverse effect on our financial condition, business, results of operations and cash flows.

We must effectively manage the growth of our operations, or our company will suffer.

Our ability to successfully implement our business plan requires an effective planning and management process. If funding is available, we intend to increase the scope of our operations and acquire complimentary businesses. Implementing our business plan will require significant additional funding and resources. If we grow our operations, we will need to hire additional employees and make significant capital investments. If we grow our operations, it will place a significant strain on our existing management and resources. If we grow, we will need to improve our financial and managerial controls and reporting systems and procedures, and we will need to expand, train and manage our workforce. Any failure to manage any of the foregoing areas efficiently and effectively would cause our business to suffer.

Our revenues are concentrated in a limited number of clients and our revenues may be significantly reduced if these clients decrease their IT spending.

Our client contracts are based on time and materials expenses. We do not have long-term client contracts. Our client contracts contain standard payment terms, and our clients only pay us for services rendered. We have limited exposure for non-payment by our clients and do not have any unresolved client debts. While our client contracts can be terminated with little or no notice, it is uncommon for our clients to terminate an engagement in the middle of the implementation of services.

For the twelve-month period ended December 31, 2017, sales to five major customers accounted for approximately 43% of our total revenue. Consequently, if our top clients reduce or postpone their IT spending significantly, this may lower the demand for our services and negatively affect our revenues and profitability. Further, any significant decrease in the growth of the financial services or other industry segments on which we focus may reduce the demand for our services and negatively affect our revenues, profitability and cash flows.

Our client contracts can typically be terminated without cause and with little or no notice or penalty, which could negatively impact our revenues and profitability.

Our clients typically retain us on a non-exclusive, project-by-project basis. Many of our client contracts can be terminated with or without cause. Our business is dependent on the decisions and actions of our clients, and there are a number of factors relating to our clients that are outside of our control which might lead to termination of a project or the loss of a client, including:

| · |

financial difficulties for a client;

|

| · |

a change in strategic priorities, resulting in a reduced level of technology spending;

|

| · |

a demand for price reductions; or an unwillingness to accept higher pricing due to various factors such as higher wage costs, higher cost of doing business;

|

| · |

a change in outsourcing strategy by moving more work to the client’s in-house technology departments or to our competitors;

|

| · |

the replacement by our clients of existing software with packaged software supported by licensors;

|

| · |

mergers and acquisitions;

|

| · |

consolidation of technology spending by a client, whether arising out of mergers and acquisitions, or otherwise; and

|

| · |

sudden ramp-downs in projects due to an uncertain economic environment.

|

Our inability to control the termination of client contracts could have a negative impact on our financial condition and results of operations.

Our engagements with customers are typically singular in nature and do not necessarily provide for subsequent engagements.

Our clients generally retain us on a short-term, engagement-by-engagement basis in connection with specific projects, rather than on a recurring basis under long-term contracts. Although a substantial majority of our revenues are generated from repeat business, which we define as revenues from a client who also contributed to our revenues during the prior fiscal year, our engagements with our clients are typically for projects that are singular in nature. Therefore, we must seek out new engagements when our current engagements are successfully completed or terminated, and we are constantly seeking to expand our business with existing clients and secure new clients for our services. In addition, in order to continue expanding our business, we may need to significantly expand our sales and marketing group, which would increase our expenses and may not necessarily result in a substantial increase in business. If we are unable to generate a substantial number of new engagements for projects on a continual basis, our business and results of operations would likely be adversely affected.

Our results of operations may fluctuate from quarter to quarter, which could affect our business, financial condition and results of operations.

Our results of operations may fluctuate from quarter to quarter depending upon several factors, some of which are beyond our control. These factors include the timing and number of client projects commenced and completed during the quarter, the number of working days in a quarter, employee hiring, attrition and utilization rates and the mix of time-and-material projects versus fixed price deliverable projects and maintenance projects during the quarter. Additionally, periodically our cost increases due to both the hiring of new employees and strategic investments in infrastructure in anticipation of future opportunities for revenue growth.

These and other factors could affect our business, financial condition and results of operations, and this makes the prediction of our financial results on a quarterly basis difficult. Also, it is possible that our quarterly financial results may be below the expectations of public market analysts.

We are heavily dependent on our senior management, and a loss of a member of our senior management team could cause our stock price and the value of our warrants to suffer.

If we lose members of our senior management, we may not be able to find appropriate replacements on a timely basis, and our business could be adversely affected. Our existing operations and continued future development depend to a significant extent upon the performance and active participation of certain key individuals. We do not currently maintain key man insurance. If we were to lose any of our key personnel, we may not be able to find appropriate replacements on a timely basis and our financial condition and results of operations could be materially adversely affected.

Our international sales and operations are subject to applicable laws relating to trade, export controls and foreign corrupt practices, the violation of which could adversely affect its operations.