Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Cactus, Inc. | whd-20171231ex32204bc81.htm |

| EX-32.1 - EX-32.1 - Cactus, Inc. | whd-20171231ex3215dd730.htm |

| EX-31.2 - EX-31.2 - Cactus, Inc. | whd-20171231ex3124d7e8f.htm |

| EX-31.1 - EX-31.1 - Cactus, Inc. | whd-20171231ex31143747d.htm |

| EX-21.1 - EX-21.1 - Cactus, Inc. | whd-20171231ex2115c4eb1.htm |

| EX-3.2 - EX-3.2 - Cactus, Inc. | whd-20171231ex32b2defed.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10‑K

(Mark One)

☑ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 001‑38390

Cactus, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

35‑2586106 |

|

(State or other jurisdiction |

(I.R.S. Employer |

|

|

|

|

Cobalt Center 920 Memorial City Way, Suite 300 Houston, Texas |

77024 |

|

(Address of principal executive offices) |

(Zip code) |

(713) 626‑8800

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Common Stock, par value $0.01 per share |

New York Stock Exchange |

|

(Title of each class) |

(Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☑

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10‑K or any amendment to this Form 10‑K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

|

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

|

Non-accelerated filer |

☑ |

Smaller reporting company |

☐ |

|

(Do not check if a smaller reporting company) |

Emerging growth company |

☑ |

|

If an emerging growth company indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes ☐ No ☑

As of June 30, 2017, the last business day of the registrant’s most recently completed second quarter, there was no public market for the registrant’s common stock. The registrant’s common stock began trading on the New York Stock Exchange on February 8, 2018.

As of March 13, 2018, the registrant had 26,450,000 shares of Class A Common Stock, $0.01 par value per share, and 48,439,772 shares of Class B Common Stock, $0.01 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The Company’s definitive proxy statement relating to the annual meeting of shareholders (to be held June 20, 2018) will be filed with the Securities and Exchange Commission within 120 days after the close of the Company’s fiscal year ended December 31, 2017 and is incorporated by reference in Part III to the extent described herein.

|

ii |

||

|

iv |

||

|

|

|

|

|

|

1 | |

|

|

|

|

| 1 | ||

| 12 | ||

| 32 | ||

| 33 | ||

| 33 | ||

| 34 | ||

|

|

|

|

|

|

34 | |

|

|

|

|

| 34 | ||

| 35 | ||

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

36 | |

| 52 | ||

| 54 | ||

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

83 | |

| 83 | ||

| 84 | ||

|

|

|

|

|

|

85 | |

|

|

|

|

| 85 | ||

| 85 | ||

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

85 | |

|

Certain Relationships and Related Transactions, and Director Independence |

85 | |

| 85 | ||

|

|

|

|

|

|

86 | |

|

|

|

|

| 86 | ||

| 88 | ||

|

|

89 | |

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10‑K (this “Annual Report”) contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). When used in this Annual Report, the words “could,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project” and similar expressions are intended to identify forward‑looking statements, although not all forward‑looking statements contain such identifying words. These forward‑looking statements are based on our current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. When considering forward‑looking statements, you should keep in mind the risk factors and other cautionary statements described under the heading “Item 1A. Risk Factors” included in this Annual Report. These forward‑looking statements are based on management’s current belief, based on currently available information, as to the outcome and timing of future events.

Forward‑looking statements may include statements about:

|

· |

demand for our products and services, which is affected by, among other things, changes in the price of, and demand for, crude oil and natural gas in domestic and international markets; |

|

· |

the level of growth in number of rigs and well count; |

|

· |

the level of fracturing activity and the availability of fracturing equipment and pressure pumping services; |

|

· |

the size and timing of orders; |

|

· |

availability of raw materials; |

|

· |

expectations regarding raw materials, overhead and operating costs and margins; |

|

· |

availability of skilled and qualified workers; |

|

· |

potential liabilities arising out of the installation, use or misuse of our products; |

|

· |

the possibility of cancellation of orders; |

|

· |

our business strategy; |

|

· |

our financial strategy, operating cash flows, liquidity and capital required for our business; |

|

· |

our future revenue, income and operating performance; |

|

· |

the termination of relationships with major customers or suppliers; |

|

· |

warranty and product liability claims; |

|

· |

laws and regulations, including environmental regulations, that may increase our costs, limit the demand for our products and services or restrict our operations; |

|

· |

disruptions in the political, regulatory, economic and social conditions domestically or internationally; |

ii

|

· |

increased import tariffs assessed on products from China or imported raw materials used in the manufacture of our goods in the United States; |

|

· |

a failure of our information technology infrastructure or any significant breach of security; |

|

· |

potential uninsured claims and litigation against us; |

|

· |

our dependence on the continuing services of certain of our key managers and employees; |

|

· |

the lack of a public market for our securities; and |

|

· |

plans, objectives, expectations and intentions contained in this Annual Report that are not historical. |

We caution you that these forward‑looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the operation of our business. These risks include, but are not limited to the risks described in this Annual Report under “Item 1A. Risk Factors.”

Should one or more of the risks or uncertainties described in this Annual Report occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward‑looking statements.

All forward‑looking statements, expressed or implied, included in this Annual Report are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward‑looking statements that we or persons acting on our behalf may issue.

Except as otherwise required by applicable law, we disclaim any duty to update any forward‑looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this Annual Report.

iii

EMERGING GROWTH COMPANY STATUS

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as we are an emerging growth company, unlike public companies that are not emerging growth companies under the JOBS Act, we will not be required to:

|

· |

provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes‑Oxley Act of 2002; |

|

· |

comply with any new requirements adopted by the Public Company Accounting Oversight Board (the “PCAOB”) requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; |

|

· |

provide certain disclosure regarding executive compensation required of larger public companies or hold shareholder advisory votes on the executive compensation required by the Dodd‑Frank Wall Street Reform and Consumer Protection Act (the “Dodd‑Frank Act”); or |

|

· |

obtain shareholder approval of any golden parachute payments not previously approved. |

We will cease to be an emerging growth company upon the earliest of the:

|

· |

last day of the fiscal year in which we have $1.07 billion or more in annual revenues; |

|

· |

date (after being subject to Section 13(a) or Section 15(d) of the Exchange Act for a period of at least twelve calendar months) on which we become a “large accelerated filer” (the fiscal year‑end on which the total market value of our common equity securities held by non‑affiliates is $700 million or more as of June 30); |

|

· |

date on which we issue more than $1.0 billion of non‑convertible debt over a three‑year period; or |

|

· |

last day of the fiscal year following the fifth anniversary of our initial public offering. |

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards, but we have irrevocably opted out of the extended transition period and, as a result, we will adopt new or revised accounting standards on the relevant dates in which adoption of such standards is required for other public companies.

For a description of the qualifications and other requirements applicable to emerging growth companies and certain elections that we have made due to our status as an emerging growth company, see “Risk Factors—Risks Related to Our Class A Common Stock—For as long as we are an emerging growth company, we will not be required to comply with certain reporting requirements, including those relating to disclosure about our executive compensation, that apply to other public companies.”

iv

You should read this entire report carefully, including the risks described under Part 1, Item 1A. Risk Factors and our consolidated financial statements and the notes to those consolidated financial statements included elsewhere in this Annual Report on Form 10‑K. Except as otherwise indicated or required by the context, all references in this Annual Report to the “Company,” “Cactus,” “we,” “us” and “our” refer to (i) Cactus Wellhead, LLC (“Cactus LLC”) and its consolidated subsidiaries prior to the completion of our initial public offering and (ii) Cactus, Inc. (“Cactus Inc.”) and its consolidated subsidiaries (including Cactus LLC) following the completion of our initial public offering on February 12, 2018, unless we state otherwise or the context otherwise requires. References in this Annual Report to “Cadent” are to Cadent Energy Partners II, L.P., an affiliate of Cadent Energy Partners. References in this Annual Report to “Cactus WH Enterprises” are to Cactus WH Enterprises, LLC. Cadent, Cactus WH Enterprises and Mr. Lee Boquet are collectively referred to herein as the “Pre-IPO Owners.”

Overview

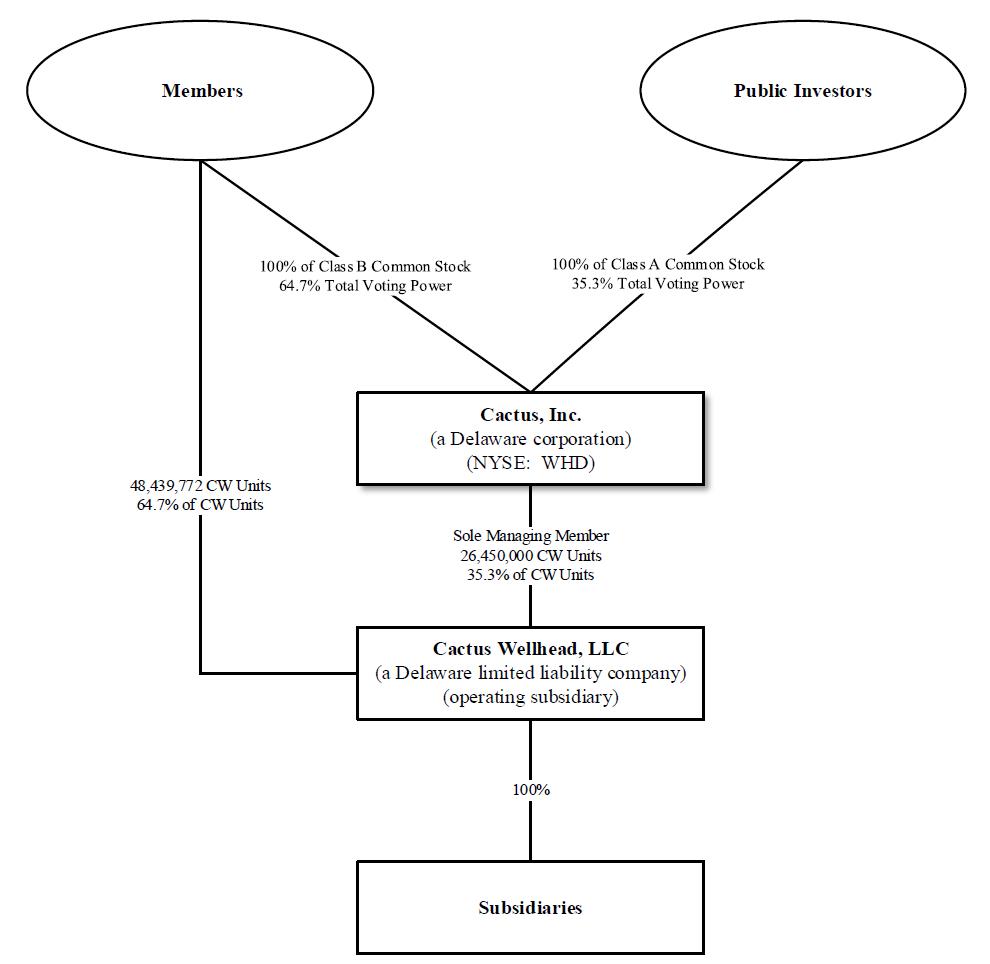

Cactus Inc. was incorporated as a Delaware corporation on February 17, 2017 for the purpose of completing an initial public offering of equity (our “IPO”) and related transactions. On February 12, 2018, in connection with our IPO, Cactus Inc. became a holding company whose sole material assets are units in Cactus LLC (“CW Units”). Cactus Inc. became the managing member of Cactus LLC and is responsible for all operational, management and administrative decisions relating to Cactus LLC’s business.

On February 12, 2018, we completed our initial public offering of 23,000,000 shares of Class A common stock, par value $0.01 per share (“Class A Common Stock”), at a price to the public of $19.00 per share. We received net proceeds of $405.8 million after deducting underwriting discounts and commissions and estimated offering expenses of our IPO. On February 14, 2018 we completed the sale of an additional 3,450,000 shares of Class A Common Stock pursuant to the exercise in full by the underwriters of their option to purchase additional shares of Class A Common Stock (the “Option”), resulting in $61.6 million of additional net proceeds. We contributed all of the net proceeds of the IPO to Cactus LLC in exchange for CW Units. Cactus LLC used (i) $251.0 million of the net proceeds to repay all of the borrowings outstanding under its term loan facility, including accrued interest and (ii) $216.4 million to redeem CW Units from certain direct and indirect owners of Cactus LLC.

We design, manufacture, sell and rent a range of highly‑engineered wellheads and pressure control equipment. Our products are sold and rented principally for onshore unconventional oil and gas wells and are utilized during the drilling, completion (including fracturing) and production phases of our customers’ wells. In addition, we provide field services for all of our products and rental items to assist with the installation, maintenance and handling of the wellhead and pressure control equipment.

Organizational Structure

In connection with the completion of the IPO, Cactus Inc. became the sole managing member of Cactus LLC and is responsible for all operational, management and administrative decisions relating to Cactus LLC’s business and consolidates the financial results of Cactus LLC and its subsidiaries. The Limited Liability Company Operating Agreement of Cactus LLC was amended and restated as the First Amended and Restated Limited Liability Company Operating Agreement of Cactus LLC (the “Cactus Wellhead LLC Agreement”) to, among other things, admit Cactus Inc. as the sole managing member of Cactus LLC.

1

In connection with our IPO, we completed a series of reorganization transactions, including the following:

|

(a) |

all of the membership interests in Cactus LLC were converted into a single class of CW Units; |

|

(b) |

Cactus Inc. contributed the net proceeds of the IPO to Cactus LLC in exchange for 23,000,000 CW Units; |

|

(c) |

Cactus LLC used the net proceeds of the IPO that it received from Cactus Inc. to repay the borrowings outstanding, plus accrued interest, under its term loan facility and to redeem 8,667,841 CW Units from the owners thereof; |

|

(d) |

Cactus Inc. issued and contributed 51,747,768 shares of its Class B common stock, par value $0.01 per share (“Class B Common Stock”) equal to the number of outstanding CW Units held by the Pre-IPO Owners following the redemption described in (c) above to Cactus LLC; |

|

(e) |

Cactus LLC distributed to each of the Pre-IPO Owners that continued to own CW Units following the IPO one share of Class B Common Stock for each CW Unit such Pre-IPO Owner held following the redemption described in (c) above; |

|

(f) |

Cactus Inc. contributed the net proceeds from the exercise of the Option to Cactus LLC in return for 3,450,000 additional CW Units; and |

|

(g) |

Cactus LLC used the net proceeds from the Option to redeem 3,450,000 CW Units from the owners thereof, and Cactus Inc. canceled a corresponding number of shares of Class B Common Stock. |

In connection with the IPO, Cactus Inc. granted 0.7 million restricted stock unit awards, which will vest over one to three years, to certain directors, officers and employees of Cactus.

In this Annual Report, we refer to the owners of CW Units (along with their permitted transferees) as “CW Unit Holders.” CW Unit Holders also own one share of our Class B Common Stock for each CW Unit such CW Unit Holders own. After giving effect to our IPO and the related transactions, Cactus Inc. owns an approximate 35.3% interest in Cactus LLC, and the CW Unit Holders own an approximate 64.7% interest in Cactus LLC. These ownership percentages are based on 26,450,000 shares of Class A Common Stock and 48,439,772 shares of Class B Common Stock issued and outstanding as of March 13, 2018.

2

The following diagram indicates our simplified ownership structure.

Our Company

We design, manufacture, sell and rent a range of highly‑engineered wellheads and pressure control equipment. Our products are sold and rented principally for onshore unconventional oil and gas wells and are utilized during the drilling, completions (including fracturing) and production phases of our customers’ wells. In addition, we provide field services for all of our products and rental items to assist with the installation, maintenance and handling of the wellhead and pressure control equipment.

3

Our principal products include our Cactus SafeDrill™ wellhead systems, frac stacks, zipper manifolds and production trees that we design and manufacture. Every oil and gas well requires a wellhead, which is installed at the onset of the drilling process and which remains with the well through its entire productive life. The Cactus SafeDrill™ wellhead systems employ technology which allows technicians to land and secure casing strings more safely from the rig floor reducing the need to descend into the cellar. We believe we are a market leader in the application of such technology, with thousands of our products sold and installed across the United States since 2011. During the completion phase of a well, we rent frac stacks, zipper manifolds and other high‑pressure equipment that are used for well control and for managing the transmission of frac fluids and proppants during the hydraulic fracturing process. These severe service applications require robust and reliable equipment. For the subsequent production phase of a well, we sell production trees that regulate hydrocarbon production, which are installed on the wellhead after the frac tree has been removed. In addition, we provide mission‑critical field services for all of our products and rental items, including 24‑hour service crews to assist with the installation, maintenance and safe handling of the wellhead and pressure control equipment. Finally, we provide repair services for all of the equipment that we sell or rent.

Our innovative wellhead products and pressure control equipment are developed internally. We believe our close relationship with our customers provides us with insight into the specific issues encountered in the drilling and completions processes, allowing us to provide them with highly tailored product and service solutions. We have achieved significant market share, as measured by the percentage of total active U.S. onshore rigs that we follow (which we define as the number of active U.S. onshore drilling rigs to which we are the primary provider of wellhead products and corresponding services during drilling), and brand name recognition with respect to our engineered products, which we believe is due to our focus on safety, reliability, cost effectiveness and time saving features. We optimize our products for pad drilling (i.e., the process of drilling multiple wellbores from a single surface location) to reduce rig time and provide operators with significant efficiencies that translate to cost savings at the wellsite.

Our manufacturing and production facilities are located in Bossier City, Louisiana and Suzhou, China. While both facilities can produce our full range of products, our Bossier City facility has advanced capabilities and is designed to support time‑sensitive and rapid turnaround orders, while our facility in China is optimized for longer lead time orders and outsources its machining requirements. Both our United States and China facilities are licensed to the latest API 6A specification for both wellheads and valves and API Q1 and ISO9001:2015 quality management systems.

We operate 14 service centers in the United States, which are strategically located in the key oil and gas producing regions, including the Permian, SCOOP/STACK, Marcellus, Utica, Eagle Ford, Bakken and other active oil and gas regions in the United States. We also have one service center in Eastern Australia. These service centers support our field services and provide equipment assembly and repair services.

Our History

We began operating in August 2011, following the formation of Cactus LLC by Scott Bender and Joel Bender, who have owned or operated wellhead manufacturing businesses since the late 1970s, and by Cadent, as its equity sponsor. We acquired our primary manufacturing facility in Bossier City, Louisiana from one of our Pre-IPO Owners in September 2011 and established our other production facility, located in Suzhou, China, in December 2013. Since we began operating, we have grown to 14 U.S. service centers located in Texas, Louisiana, Colorado, Wyoming, New Mexico, Oklahoma, Pennsylvania and North Dakota. In July 2014, we formed Cactus Wellhead Australia Pty, Ltd and established a service center to develop the market for our products in Eastern Australia.

Suppliers and Raw Materials

Forgings, castings and bar stock represent the principal raw materials used in the manufacture of our products and rental equipment. In addition, we require accessory items (such as elastomers, ring gaskets, studs and nuts) and machining services. We purchase these items and services from over 250 vendors, both in the United States and China.

4

For the years ended December 31, 2017, 2016 and 2015, approximately $33.4 million, $10.8 million and $18.1 million, respectively, of machined component purchases were made from a vendor located in China, representing approximately 22%, 20% and 27%, respectively, of our total third party vendor purchases of raw materials, finished products, equipment, machining and other services. Although we have historically made purchases from this vendor pursuant to a long term contract, such contract expired at the end of 2016. We are currently purchasing from this vendor on terms substantially similar to those contained in the expired agreement. We expect to negotiate a new agreement with such vendor on terms similar to those in the expired agreement. Although our relationships with our existing vendors, including the Chinese vendor referred to above, are important to us, we do not believe that we are substantially dependent on any individual vendor to supply our required materials or services. The materials and services essential to our business are normally readily available and, where we use one or a few vendors as a source of any particular materials or services, we believe that we can, within a reasonable period of time, make satisfactory alternative arrangements in the event of an interruption of supply from any vendor.

We believe that our materials and services vendors have the capacity to meet additional demand should we require it.

Impact of Section 232 of the Trade Expansion Act of 1962 (“Section 232”)

On March 8, 2018, the President of the United States issued two proclamations imposing tariffs on imports of certain steel and aluminum products, effective March 23, 2018. The decision was made in response to the Department of Commerce’s findings and recommendations in its reports of its investigations into the impact of imported steel and aluminum on the national security of the United States pursuant to Section 232. Specifically, the President has imposed a 25% global tariff on certain imported steel mill products and a 10% global tariff on certain imported aluminum products from all countries except Canada and Mexico. The tariffs could cause the cost of raw materials to increase, although the impact to us of Section 232 remains uncertain.

Customers

We serve over 200 customers representing major independent and other oil and gas companies with operations in the key U.S. oil and gas producing basins including the Permian, Marcellus Shale/Utica, the SCOOP/STACK, the Eagle Ford, the Bakken and other active oil and gas basins, as well as in Australia. For the year ended December 31, 2017, Pioneer Natural Resources represented 11% of our total revenue and no other customer represented 10% or more of our total revenue. For each of the years ended December 31, 2016 and 2015, Devon Energy Corporation represented 12% of our total revenue, and no other customer represented 10% or more of our total revenue.

Manufacturing

Our manufacturing and production facilities are located in Bossier City, Louisiana and Suzhou, China. While both facilities can produce our full range of products, our Bossier City facility has advanced capabilities and is designed to support time‑sensitive and rapid turnaround orders, while China is optimized for longer lead time orders and outsources its machining requirements. Both our U.S. and China facilities are API certified to the API 6A specification for both wellheads and valves and API Q1 and ISO9001:2015 quality management systems.

Our Bossier City facility is configured to provide rapid‑response production of made‑to‑order equipment. Where typical manufacturing facilities are designed to run in batches with different machining processes occurring in stages, this facility uses highly‑capable computer numeric control (“CNC”) machines to perform substantially all machining of the product in a single step. We believe eliminating the setup and queue times between machining processes allows us to offer significantly shorter order‑to‑delivery time for equipment than our competitors, albeit at higher costs than China. Responsiveness to urgent needs strengthens our relationship with key customers.

5

Our Bossier City manufacturing facility also functions as a repair and testing facility with its API 6A PSL3 certification and full QA/QC department. The facility also has the ability to perform hydrostatic testing, phosphate and oiling, copper coating and frac valve remanufacturing.

Our production facility in China is configured to efficiently produce our range of pressure control products and components for less time‑sensitive, higher‑volume orders. All employees in our Suzhou facility are Cactus employees, which we believe is a key factor in ensuring high quality. Our Suzhou facility currently assembles and tests some machined components before shipment to the United States or Australia.

Trademarks and Other Intellectual Property

Trademarks are important to the marketing of our products. We consider the Cactus Wellhead trademark to be important to our business as a whole. Additionally, the SafeDrillTM trademark is complementary to our marketing efforts and brand recognition. These trademarks are registered in the United States.

We also rely on trade secret protection for our confidential and proprietary information. To protect our information, we customarily enter into confidentiality agreements with our employees and suppliers. There can be no assurance, however, that others will not independently obtain similar information or otherwise gain access to our trade secrets.

Cyclicality

We are substantially dependent on conditions in the oil and gas industry, including the level of exploration, development and production activity of, and the corresponding capital spending by, oil and natural gas companies. The level of exploration, development and production activity is directly affected by trends in oil and natural gas prices, which has historically been volatile, and by capital spending discipline imposed by customers.

Declines, as well as anticipated declines, in oil and gas prices could negatively affect the level of these activities and capital spending, which could adversely affect demand for our products and services and, in certain instances, result in the cancellation, modification or rescheduling of existing and expected orders and the ability of our customers to pay us for our products and services. These factors could have an adverse effect on our revenue and profitability.

Seasonality

Our business is not significantly impacted by seasonality, although our fourth quarter has historically been impacted by holidays and our clients’ budget cycles.

Environmental, Health and Safety Regulation

Our operations are subject to domestic (including U.S. federal, state and local) and international regulations with regard to air, land and water quality and other environmental matters. We believe we are in substantial compliance with these regulations. Laws and regulations to minimize and mitigate risks to the environment and to workplace safety continue to be enacted. Changes in standards of enforcement of existing regulations, as well as the enactment and enforcement of new legislation, may require us and our customers to modify, supplement or replace equipment or facilities or to change or discontinue present methods of operation. Our environmental compliance expenditures, our capital costs for environmental control equipment, and the market for our products may change accordingly.

Hazardous Substances and Waste. The Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes, regulate the generation, transportation, treatment, storage, disposal and cleanup of hazardous and non‑hazardous wastes. Under the auspices of the Environmental Protection Agency (“EPA”), the individual states

6

administer some or all of the provisions of RCRA, sometimes in conjunction with their own, more stringent requirements. We are required to manage the transportation, storage and disposal of hazardous and non‑hazardous wastes generated by our operations in compliance with applicable laws, including RCRA.

The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”), also known as the Superfund law, imposes joint and several liability, without regard to fault or legality of conduct, on classes of persons who are considered to be responsible for the release of a hazardous substance into the environment. These persons include the current and former owner or operator of the site where the release occurred, and anyone who disposed of or arranged for the disposal of a hazardous substance released at the site. We currently own, lease, or operate numerous properties used for manufacturing and other operations. We also contract with waste removal services and landfills. In the event of a release from these properties, under CERCLA, RCRA and analogous state laws, we could be required to remove substances and wastes, remediate contaminated property, or perform remedial operations to prevent future contamination even if the releases are not from our operations. In addition, neighboring landowners and other third parties may also file claims for personal injury and property damage allegedly caused by releases into the environment. Any obligations to undertake remedial operations in the future may increase our cost of doing business and may have a material adverse effect on our results of operations and financial condition.

Water Discharges. The Federal Water Pollution Control Act (the “Clean Water Act”) and analogous state laws restrict and control the discharge of pollutants into waters of the United States. Discharges to water associated with our operations require appropriate permits from state agencies and may add material costs to our operations. The adoption of more stringent criteria in the future may also increase our costs of operation. The Clean Water Act and analogous state laws provide for administrative, civil and criminal penalties for unauthorized discharges and, together with the Oil Pollution Act of 1990, impose rigorous requirements for spill prevention and response planning, as well as substantial potential liability for the costs of removal, remediation, and damages in connection with any unauthorized discharges. In addition, in 2015 the EPA and U.S. Army Corps of Engineers (“Corps”) finalized a rule that expanded the scope of waters subject to Clean Water Act jurisdiction. If implemented, this rule may have a material adverse effect on the operation costs of customers, thereby potentially reducing demand for our products. The rule was stayed nationwide in late 2015, however, and the EPA and the Corps have proposed to repeal the rule and reinstate the pre‑2015 rule. In a separate rulemaking, the EPA and the Corps have also proposed to delay the implementation of the 2015 rule until 2019. Neither of these proposals has been finalized and the rule remains stayed by the Sixth Circuit.

Employee Health and Safety. We are subject to a number of federal and state laws and regulations, including OSHA and comparable state statutes, establishing requirements to protect the health and safety of workers. In addition, the OSHA hazard communication standard, the EPA community right‑to‑know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require that information be maintained concerning hazardous materials used or produced in our operations and that this information be provided to employees, state and local government authorities and the public. Substantial fines and penalties can be imposed and orders or injunctions limiting or prohibiting certain operations may be issued in connection with any failure to comply with laws and regulations relating to worker health and safety.

API Certifications. Our manufacturing facility and our production facility are currently certified by the API as being in compliance with API 6A specification for both wellheads and valves and API Q1 and ISO9001:2015 quality management systems. These standards have also been incorporated into regulations adopted by the Bureau of Safety and Environmental Enforcement (“BSEE”) that apply to the oil and gas industries that operate on the outer continental shelf. API’s standards are subject to revision, however, and there is no guarantee that future amendments or substantive changes to the standards would not require us to modify our operations or manufacturing processes to meet the new standards. Doing so may materially affect our operation costs. We also cannot guarantee that changes to the standards would not lead to the rescission of our licenses should we be unable to make the changes necessary to meet the new standards. Furthermore, these facilities are subjected to annual audits by the API. Loss of our API licenses could materially affect demand for these products.

7

Climate Change. International, national and state governments and agencies are currently evaluating and/or promulgating legislation and regulations that are focused on restricting emissions commonly referred to as greenhouse gas (“GHG”) emissions. These regulatory measures include, among others, adoption of cap and trade regimes, carbon taxes, increased efficiency standards and incentives or mandates for renewable energy. Consideration of further legislation or regulation may be impacted by the Paris Agreement, which was announced by the Parties to the United Nations Framework Convention on Climate Change in December 2015 and which calls on signatories to set progressive GHG emission reduction goals. Although the United States became a party to the Paris Agreement in April 2016, the Trump administration announced in June 2017 its intention to either withdraw from the Agreement or renegotiate more favorable terms. However, the Paris Agreement stipulates that participating countries must wait four years before withdrawing from the agreement. Despite the planned withdrawal, certain U.S. city and state governments have announced their intention to satisfy their proportionate obligations under the Paris Agreement. These commitments could further reduce demand and prices for fossil fuels produced by our customers. In the United States, the EPA has made findings under the Clean Air Act that GHG emissions endanger public health and the environment, resulting in the EPA’s adoption of regulations requiring construction and operating permit reviews of both existing and new stationary sources with major emissions of GHGs, which reviews require the installation of new GHG emission control technologies. However, in October 2017, the EPA announced a proposal to repeal its regulation of GHG emissions from existing stationary sources. The EPA has also promulgated rules requiring the monitoring and annual reporting of GHG emissions from certain sources, including onshore and offshore oil and natural gas production facilities and onshore oil and natural gas processing, transmission, storage and distribution facilities. In addition, in May 2016, the EPA finalized a rule that set additional emissions limits for volatile organic compounds and established new methane emission standards for certain new, modified or reconstructed equipment and processes in the oil and natural gas source category, including production, processing, transmission and storage activities. In June 2017, the EPA issued an administrative stay of key provisions of the rule, but was promptly ordered by the D.C. Circuit to implement the rule. The EPA also published proposed 60‑day and two‑year stays of certain provisions in June 2017 and published a Notice of Data Availability in November 2017 seeking comment and providing clarification regarding the agency’s legal authority to stay the rule.

It is too early to determine whether, or in what form, further regulatory action regarding greenhouse gas emissions will be adopted or what specific impact a new regulatory action might have on us or our customers. Generally, the anticipated regulatory actions do not appear to affect us in any material respect that is different, or to any materially greater or lesser extent, than other companies that are our competitors. However, to the extent our customers are subject to these or other similar proposed or newly enacted laws and regulations, the additional costs incurred by our customers to comply with such laws and regulations could impact their ability or desire to continue to operate at current or anticipated levels, which would negatively impact their demand for our products and services. In addition, any new laws or regulations establishing cap‑and‑trade or that favor the increased use of non‑fossil fuels may dampen demand for oil and gas production and lead to lower spending by our customers for our products and services. Similarly, to the extent we are or become subject to any of these or other similar proposed or newly enacted laws and regulations, we expect that our efforts to monitor, report and comply with such laws and regulations, and any related taxes imposed on companies by such programs, will increase our cost of doing business and may have a material adverse effect on our financial condition and results of operations. Moreover, any such regulations could ultimately restrict the exploration and production of fossil fuels, which could adversely affect demand for our products.

Hydraulic Fracturing. Many of our customers utilize hydraulic fracturing in their operations. Environmental concerns have been raised regarding the potential impact of hydraulic fracturing on underground water supplies. These concerns have led to several regulatory and governmental initiatives in the United States to restrict the hydraulic fracturing process, which could have an adverse impact on our customers’ completions or production activities. For example, in December 2016, the EPA released its final report on the potential impacts of hydraulic fracturing on drinking water resources, concluding that “water cycle” activities associated with hydraulic fracturing may impact drinking water resources “under some circumstances,” including water withdrawals for fracturing in times or areas of low water availability; surface spills during the management of fracturing fluids, chemicals or produced water; injection of fracturing fluids into wells with inadequate mechanical integrity; injection of fracturing fluids directly into

8

groundwater resources; discharge of inadequately treated fracturing wastewater to surface waters; and disposal or storage of fracturing wastewater in unlined pits. In other examples, the EPA has issued final regulations under the U.S. Clean Air Act governing performance standards, including standards for the capture of air emissions released during hydraulic fracturing, though the EPA is currently reconsidering these standards, and published in June 2016 a final rule prohibiting the discharge of wastewater from hydraulic fracturing operations to publicly owned wastewater treatment plants. Also, the U.S. Bureau of Land Management finalized rules in March 2015 that imposed new or more stringent standards for performing hydraulic fracturing on federal and American Indian lands. While the agency subsequently published a final rule rescinding the 2015 rule in December 2017, this decision could be subject to legal challenge. In addition, in some instances, states and local governments have enacted more stringent hydraulic fracturing restrictions or bans on hydraulic fracturing activities. These and other similar state and foreign regulatory initiatives, if adopted, would establish additional levels of regulation for our customers that could make it more difficult for our customers to complete natural gas and oil wells and could adversely affect the demand for our equipment and services, which, in turn, could adversely affect our results of operations, financial condition and cash flows.

State and federal regulatory agencies have also recently focused on a possible connection between the operation of injection wells used for oil and gas waste disposal and seismic activity. Similar concerns have been raised that hydraulic fracturing may also contribute to seismic activity. When caused by human activity, such events are called induced seismicity. Developing research suggests that the link between seismic activity and wastewater disposal may vary by region, and that only a very small fraction of the tens of thousands of injection wells have been suspected to be, or have been, the likely cause of induced seismicity. In March 2016, the United States Geological Survey identified six states with the most significant hazards from induced seismicity, including Oklahoma, Kansas, Texas, Colorado, New Mexico, and Arkansas. In light of these concerns, some state regulatory agencies have modified their regulations or issued orders to address induced seismicity. Increased regulation and attention given to induced seismicity could lead to greater opposition to, and litigation concerning, oil and gas activities utilizing hydraulic fracturing or injection wells for waste disposal, which could indirectly impact our business, financial condition and results of operations. In addition, these concerns may give rise to private tort suits from individuals who claim they are adversely impacted by seismic activity they allege was induced. Such claims or actions could result in liability for property damage, exposure to waste and other hazardous materials, nuisance or personal injuries, and require our customers to expend additional resources or incur substantial costs or losses. This could in turn adversely affect the demand for our products.

Although we do not conduct hydraulic fracturing, increased regulation and attention given to the hydraulic fracturing process could lead to greater opposition to oil and gas production activities using hydraulic fracturing techniques. In addition, the adoption of new laws or regulations at the federal, state, local or foreign level imposing reporting obligations on, or otherwise limiting, delaying or banning, the hydraulic fracturing process or other processes on which hydraulic fracturing relies, such as water disposal, could make it more difficult to complete oil and natural gas wells, increase our customers’ costs of compliance and doing business, and otherwise adversely affect the hydraulic fracturing services they perform, which could negatively impact demand for our products.

Offshore Drilling. Various new regulations intended to improve offshore safety systems and environmental protection have been issued since 2010 that have increased the complexity of the drilling permit process and may limit the opportunity for some operators to continue deepwater drilling in the U.S. Gulf of Mexico, which could have an adverse impact on our customers’ activities. For example, in April 2016, BSEE published a final blowout preventer systems and well control rule that focuses on blowout preventer requirements and includes reforms in well design, well control, casing, cementing, real‑time well monitoring and subsea containment. Additionally, in July 2016, the Bureau of Ocean Energy Management issued a notice to lessees (“NTL”), effective September 30, 2016, setting out new financial assurance requirements for offshore leases intended to ensure that leaseholders will be able to cover the costs of decommissioning. In January 2017, the Bureau extended the NTL implementation timeline for certain leases by an additional six months. In May 2017, the Bureau began a review of the NTL to determine whether it should be implemented. If these new financial assurance requirements remain in place, they may increase our customers’ operating costs and impact our customers’ ability to obtain leases, thereby reducing demand for our products. Additional regulation includes a third‑party certification requirement promulgated by the Bureau of Safety and Environmental

9

Enforcement (“BSEE”) in September 2016 under which offshore operators must certify through an independent third party that their critical safety and pollution prevention equipment is operational and will function as designed in the most extreme conditions. However, the BSEE published a proposed rule in December 2017 to rescind this requirement, allowing equipment to demonstrate its adequacy through various industry standards, such as those established by the API. Third‑party challenges to industry operations in the U.S. Gulf of Mexico may also serve to further delay or restrict activities. Although our operations are predominately onshore, if the new regulations, policies, operating procedures and possibility of increased legal liability are viewed by our current or future customers as a significant impairment to expected profitability on projects or an unjustifiable increase in risk, they could discontinue or curtail their offshore operations, thereby adversely affecting the demand for our equipment and services, which, in turn could adversely affect our results of operations, financial condition and cash flows.

Chinese Environmental Law. As we have manufacturing operations in the People’s Republic of China (“PRC”), we are regulated by various PRC national and local environmental protection laws, regulations and policies. Chinese PRC environmental laws and regulations include national and local standards governing activities that may impact human health and the environment. These laws and regulations set standards for emissions control, discharges to surface and subsurface water, and the generation, handling, storage, transportation, treatment and disposal of waste materials. Although we believe that our operations are in substantial compliance with current environmental laws and regulations, we may not be able to comply with these regulations at all times as the PRC environmental legal regime is evolving and becoming more stringent. Therefore, if the PRC government imposes more stringent regulations in the future, we will have to incur additional and potentially substantial costs and expenses to comply with new regulations, which may negatively affect our results of operations. If we fail to comply with any of the present or future environmental regulations in any material aspects, we may suffer from negative publicity and may be required to pay substantial fines, suspend or even cease operations.

Companies must register or file an environmental impact report with the appropriate environmental bureau before starting construction or any major expansion or renovation of a new production facility. Before commencing operations, the agency must inspect the new or renovated facility and determine that all necessary equipment has been installed as required by applicable environmental protection requirements.

Chinese PRC authorities have the power to issue fines and penalties for non‑compliance and can also require violators to cease operations until compliance has been restored. We cannot currently predict the extent of future capital expenditures, if any, required for compliance with environmental laws and regulations, which may include expenditures for environmental control facilities.

Insurance and Risk Management

We provide products and systems to customers involved in oil and gas exploration, development and production. We also provide parts, repair services and field services associated with installation at all of our facilities and service centers in the United States and at our facility in Australia, as well as at customer sites. Our operations are subject to hazards inherent in the oil and natural gas industry, including accidents, blowouts, explosions, cratering, fires, oil spills and hazardous materials spills. These conditions can cause personal injury or loss of life, damage to or destruction of property, equipment, the environment and wildlife, and interruption or suspension of operations, among other adverse effects. In addition, claims for loss of oil and natural gas production and damage to formations can occur. If a serious accident were to occur at a location where our equipment and services are being used, it could result in our being named as a defendant to lawsuits asserting significant claims.

We have suffered accidents in the past, and we anticipate that we could experience accidents in the future. In addition to the property and personal losses from these accidents, the frequency and severity of these incidents affect our operating costs and insurability, as well as our relationships with customers, employees and regulatory agencies. Any significant increase in the frequency or severity of these incidents, or the general level of compensation awards, could

10

adversely affect the cost of, or our ability to obtain, workers’ compensation and other forms of insurance and could have other adverse effects on our results of operations and financial condition.

We rely on customer indemnifications and third‑party insurance as part of our risk mitigation strategy. However, our customers may be unable to satisfy indemnification claims against them. In addition, we indemnify our customers against certain claims and liabilities resulting or arising from our provision of goods or services to them. Our insurance may not be sufficient to cover any particular loss or may not cover all losses. We carry a variety of insurance coverages for our operations, and we are partially self‑insured for certain claims, in amounts that we believe to be customary and reasonable. Historically, insurance rates have been subject to various market fluctuations that may result in less coverage, increased premium costs, or higher deductibles or self‑insured retentions.

Our insurance includes coverage for commercial general liability, damage to our real and personal property, damage to our mobile equipment, sudden and accidental pollution liability, workers’ compensation and employer’s liability, auto liability, foreign package policy, excess liability, and directors and officers insurance. Our insurance includes various limits and deductibles or self‑insured retentions, which must be met prior to, or in conjunction with, recovery. To cover potential pollution risks, our commercial general liability policy is endorsed with sudden and accidental coverage and our excess liability policies provide additional limits of liability for covered sudden and accidental pollution losses.

Employees

As of December 31, 2017, we employed over 880 people. Our future success will depend partially on our ability to attract, retain and motivate qualified personnel. We are not a party to any collective bargaining agreements and have not experienced any strikes or work stoppages. We consider our relations with our employees to be satisfactory.

Facilities

Our corporate headquarters is located in Houston, Texas. Please see “Item 2. Properties” for information with respect to our other facilities. We believe that our facilities are adequate for our current operations.

Competition

The markets in which we operate are highly competitive. We believe that we are one of the largest suppliers of wellheads in the United States. We compete with divisions of Schlumberger, Baker Hughes a GE company, Weir and TechnipFMC as well as with a number of smaller companies. We believe that the wellhead market is relatively concentrated, with Cactus, Schlumberger and Baker Hughes representing over 50% of the market. Similar to Cactus, each of Schlumberger, Baker Hughes and TechnipFMC manufacture their own engineered products.

We believe that the rental market for frac stacks and related flow control equipment is more fragmented than the wellhead product market. Cactus does not believe that any individual company represents more than 10% of the market. As is the case in the wellhead market, Cactus, Schlumberger, Baker Hughes and TechnipFMC rent internally engineered and manufactured products. Other competitors generally rent foreign designed and manufactured generic products.

We believe that the principal competitive factors in the markets we serve are technical features, equipment availability, work force competency, efficiency, safety record, reputation, experience and price. Additionally, projects are often awarded on a bid basis, which tends to create a highly competitive environment. While we seek to be competitive in our pricing, we believe many of our customers elect to work with us based on product features, safety, performance and quality of our crews, equipment and services. We seek to differentiate ourselves from our competitors

11

by delivering the highest‑quality services and equipment possible, coupled with superior execution and operating efficiency in a safe working environment.

Available Information

We are required to file annual, quarterly and current reports, proxy statements and certain other information with the SEC. Any documents filed by us with the SEC may be inspected without charge at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Copies of these materials may be obtained from such office upon payment of a duplicating fee. Please call the SEC at 1‑800‑SEC‑0330 for further information on the operation of the Public Reference Room.

The SEC maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding registrants that file electronically with the SEC. Any documents filed by us with the SEC, including this Annual Report, can be downloaded from the SEC’s website.

Our principal executive offices are located at Cobalt Center, 920 Memorial City Way, Suite 300, Houston, TX 77024, and our telephone number at that address is (713) 626‑8800. Our website address is www.CactusWHD.com. Our periodic reports and other information filed with or furnished to the SEC are available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this Annual Report and does not constitute a part of this Annual Report.

Investing in our Class A Common Stock involves risks. You should carefully consider the information in this Annual Report, including the matters addressed under “Cautionary Note Regarding Forward‑Looking Statements,” and the following risks before making an investment decision. Our business, financial condition, prospects and results of operations could be materially and adversely affected by any of these risks. Additional risks or uncertainties not currently known to us, or that we deem immaterial, may also have an effect on our business, financial condition, prospects or results of operations. The trading price of our Class A Common Stock could decline due to any of these risks, and you may lose all or part of your investment.

Risks Related to the Oilfield Services Industry and Our Business

Demand for our products and services depends on oil and gas industry activity and expenditure levels, which are directly affected by trends in the demand for and price of crude oil and natural gas.

Demand for our products and services depends primarily upon the general level of activity in the oil and gas industry, including the number of drilling rigs in operation, the number of oil and gas wells being drilled, the depth and drilling conditions of these wells, the volume of production, the number of well completions and the level of well remediation activity, and the corresponding capital spending by oil and natural gas companies. Oil and gas activity is in turn heavily influenced by, among other factors, oil and gas prices worldwide, which have historically been volatile.

Declines, as well as anticipated declines, in oil and gas prices could negatively affect the level of these activities and capital spending, which could adversely affect demand for our products and services and, in certain instances, result in the cancellation, modification or rescheduling of existing and expected orders and the ability of our customers to pay us for our products and services. These factors could have an adverse effect on our revenue and profitability.

12

Factors affecting the prices of oil and natural gas include, but are not limited to, the following:

|

· |

demand for hydrocarbons, which is affected by worldwide population growth, economic growth rates and general economic and business conditions; |

|

· |

changes in sentiment on environmental matters; |

|

· |

costs of exploring for, producing and delivering oil and natural gas; |

|

· |

political and economic uncertainty and sociopolitical unrest; |

|

· |

available excess production capacity within the Organization of Petroleum Exporting Countries (“OPEC”) and the level of oil and gas production by non‑OPEC countries; |

|

· |

oil refining capacity and shifts in end‑customer preferences toward fuel efficiency and the use of natural gas; |

|

· |

technological advances affecting energy consumption; |

|

· |

potential acceleration of the development of alternative fuels; |

|

· |

access to capital and credit markets, which may affect our customers’ activity levels and spending for our products and services; |

|

· |

the relative strength of the U.S. dollar; |

|

· |

changes in laws and regulations related to hydraulic fracturing activities; |

|

· |

changes in environmental laws and regulations (including relating to the use of coal in power plants); and |

|

· |

natural disasters. |

The oil and gas industry has historically experienced periodic downturns, which have been characterized by diminished demand for oilfield services and downward pressure on the prices we charge. The last downturn in the oil and gas industry that began in mid‑2014 resulted in a reduction in demand for oilfield services and adversely affected our financial condition, results of operations and cash flows. Any future downturn or expected downturn could again adversely affect our results of operations, financial condition and cash flows.

The cyclicality of the oil and natural gas industry may cause our operating results to fluctuate.

We derive our revenues from companies in the oil and natural gas exploration and production industry, a historically cyclical industry with levels of activity that are significantly affected by the levels and volatility of oil and natural gas prices. We have experienced and may in the future experience significant fluctuations in operating results as a result of the reactions of our customers to changes in oil and natural gas prices. For example, prolonged low commodity prices during 2015 and 2016, combined with adverse changes in the capital and credit markets, caused many exploration and production companies to reduce their capital budgets and drilling activity. This resulted in a significant decline in demand for oilfield services and adversely impacted the prices we could charge, particularly for rentals of frac equipment.

13

If oil prices or natural gas prices decline, the demand for our products and services could be adversely affected.

The demand for our products and services is primarily determined by current and anticipated oil and natural gas prices and the level of drilling activity and related general production spending in the areas in which we have operations. Volatility or weakness in oil prices or natural gas prices (or the perception that oil prices or natural gas prices will decrease) affects the spending patterns of our customers and may result in the drilling of fewer new wells or lower production spending on existing wells. When this occurs, exploration and production (“E&P”) companies move to significantly cut costs, both by decreasing drilling and completions activity and by demanding price concessions from their service providers. This results in lower demand for our products and services and may cause lower rates and lower utilization of our equipment. If oil prices decline or natural gas prices continue to remain low or decline further, or if there is a reduction in drilling activities, the demand for our products and services and our results of operations could be materially and adversely affected.

Additionally, the commercial development of economically viable alternative energy sources (such as wind, solar, geothermal, tidal, fuel cells and biofuels) could reduce demand for our products and services and create downward pressure on the revenue we are able to derive from such products and services, as they are dependent on oil and natural gas prices.

Anticipated growth in U.S. drilling and completions activity, and our ability to benefit from such anticipated growth, could be adversely affected by any significant constraints in pressure pumping capacity in the industry.

Growth in U.S. drilling and completions activity may be impacted by, among other things, pressure pumping capacity and pricing, which, in turn, is impacted by, among other things, the availability of fracturing equipment, demand for fracturing equipment and fracturing intensity per active rig. Also, longer laterals and higher intensity fracturing result in greater wear and tear to the industry’s fracturing equipment, which has caused and will continue to cause attrition in the supply of fracturing equipment and shortages in the availability of pressure pumping services. In addition, rising fracturing intensity per rig and an overall increase in completions activity has increased the demand for fracturing equipment. During the completion phase of a well, we rent frac stacks, zipper manifolds and other high‑pressure equipment used during the hydraulic fracturing process. For the subsequent production phase of a well, we sell production trees, which are installed on the wellhead after the frac tree has been removed. Any significant additional constraints in the availability of pressure pumping services, fracturing equipment or the ability of fracturing service providers to deliver fracturing services would have an adverse impact on the demand for the products we sell and rent, which could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We design, manufacture, sell, rent and install equipment that is used in oil and gas exploration and production activities, which may subject us to liability, including claims for personal injury, property damage and environmental contamination should such equipment fail to perform to specifications.

We provide products and systems to customers involved in oil and gas exploration, development and production. Some of our equipment is designed to operate in high‑temperature and/or high‑pressure environments, and some equipment is designed for use in hydraulic fracturing operations. We also provide parts, repair services and field services associated with installation at all of our facilities and service centers in the United States and at our facility in Australia, as well as at customer sites. Because of applications to which our products and services are exposed, particularly those involving high pressure environments, a failure of such equipment, or a failure of our customer to maintain or operate the equipment properly, could cause damage to the equipment, damage to the property of customers and others, personal injury and environmental contamination and could lead to a variety of claims against us that could have an adverse effect on our business and results of operations.

We indemnify our customers against certain claims and liabilities resulting or arising from our provision of goods or services to them. In addition, we rely on customer indemnifications, generally, and third‑party insurance as part

14

of our risk mitigation strategy. However, our insurance may not be adequate to cover our liabilities. In addition, our customers may be unable to satisfy indemnification claims against them. Further, insurance companies may refuse to honor their policies, or insurance may not generally be available in the future, or if available, premiums may not be commercially justifiable. We could incur substantial liabilities and damages that are either not covered by insurance or that are in excess of policy limits, or incur liability at a time when we are not able to obtain liability insurance. Such potential liabilities could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We may be unable to employ a sufficient number of skilled and qualified workers to sustain or expand our current operations.

The delivery of our products and services requires personnel with specialized skills and experience. Our ability to be productive and profitable will depend upon our ability to attract and retain skilled workers. In addition, our ability to expand our operations depends in part on our ability to increase the size of our skilled labor force. The demand for skilled workers is high, the supply is limited, and the cost to attract and retain qualified personnel has increased. During industry downturns, skilled workers may leave the industry, reducing the availability of qualified workers when conditions improve. In addition, a significant increase in the wages paid by competing employers could result in increases in the wage rates that we must pay. If we are not able to employ and retain skilled workers, our ability to respond quickly to customer demands or strong market conditions may inhibit our growth, which could have a material adverse effect on our business, results of operations and financial condition.

Political, regulatory, economic and social disruptions in the countries in which we conduct business could adversely affect our business or results of operations.

In addition to our facilities in the United States, we operate one production facility in China and have a facility in Australia that sells and rents equipment as well as provides parts, repair services and field services associated with installation. Instability and unforeseen changes in any of the markets in which we conduct business could have an adverse effect on the demand for, or supply of, our products and services, our results of operations and our financial condition. These factors include, but are not limited to, the following:

|

· |

nationalization and expropriation; |

|

· |

potentially burdensome taxation; |

|

· |

inflationary and recessionary markets, including capital and equity markets; |

|

· |

civil unrest, labor issues, political instability, terrorist attacks, cyber‑terrorism, military activity and wars; |

|

· |

supply disruptions in key oil producing countries; |

|

· |

tariffs, trade restrictions, trade protection measures associated with Section 232 or price controls; |

|

· |

foreign ownership restrictions; |

|

· |

import or export licensing requirements; |

|

· |

restrictions on operations, trade practices, trade partners and investment decisions resulting from domestic and foreign laws and regulations; |

15

|

· |

changes in, and the administration of, laws and regulations; |

|

· |

inability to repatriate income or capital; |

|

· |

reductions in the availability of qualified personnel; |

|

· |

foreign currency fluctuations or currency restrictions; and |

|

· |

fluctuations in the interest rate component of forward foreign currency rates. |

We are dependent on a relatively small number of customers in a single industry. The loss of an important customer could adversely affect our results of operations and financial condition.

Our customers are engaged in the oil and natural gas E&P business primarily in the United States and Australia. Historically, we have been dependent on a relatively small number of customers for our revenues. For the year ended December 31, 2017, Pioneer Natural Resources represented 11% of our total revenue, and no other customer represented more than 10% of our total revenue. For each of the years ended December 31, 2016 and 2015, Devon Energy Corporation represented 12% of our total revenue, and no other customer represented more than 10% of our total revenue.

Our business, financial condition, prospects and results of operations could be materially adversely affected if an important customer ceases to engage us for our services on favorable terms or at all or fails to pay or delays in paying us significant amounts of our outstanding receivables.

Additionally, the E&P industry is characterized by frequent consolidation activity. Changes in ownership of our customers may result in the loss of, or reduction in, business from those customers, which could materially and adversely affect our business, results of operations and financial condition.

Customer credit risks could result in losses.

The concentration of our customers in the energy industry may impact our overall exposure to credit risk as customers may be similarly affected by changes in economic and industry conditions. In addition, laws in some jurisdictions outside of the U.S. in which we operate could make collection difficult or time consuming. We perform ongoing credit evaluations of our customers and do not generally require collateral in support of our trade receivables. While we maintain reserves for potential credit losses, we cannot assure such reserves will be sufficient to meet write‑offs of uncollectible receivables or that our losses from such receivables will be consistent with our expectations.

To the extent one or more of our key customers commences bankruptcy proceedings, our contracts with these customers may be subject to rejection under applicable provisions of the United States Bankruptcy Code, or may be renegotiated. Further, during any such bankruptcy proceeding, prior to assumption, rejection or renegotiation of such contracts, the bankruptcy court may temporarily authorize the payment of value for our services less than contractually required, which could also have a material adverse effect on our business, results of operations, financial condition and cash flows.

Delays in obtaining, or inability to obtain or renew, permits or authorizations by our customers for their operations could impair our business.

In most states, our customers are required to obtain permits or authorizations from one or more governmental agencies or other third parties to perform drilling and completions activities, including hydraulic fracturing. Such permits or approvals are typically required by state agencies but can also be required by federal and local governmental agencies

16

or other third parties. The requirements for such permits or authorizations vary depending on the location where such drilling and completions activities will be conducted. As with most permitting and authorization processes, there is a degree of uncertainty as to whether a permit will be granted, the time it will take for a permit or approval to be issued and the conditions which may be imposed in connection with the granting of the permit. In some jurisdictions, such as New York State and within the jurisdiction of the Delaware River Basin Commission, certain regulatory authorities have delayed or suspended the issuance of permits or authorizations while the potential environmental impacts associated with issuing such permits can be studied and appropriate mitigation measures evaluated. In Texas, rural water districts have begun to impose restrictions on water use and may require permits for water used in drilling and completions activities. Permitting, authorization or renewal delays, the inability to obtain new permits or the revocation of current permits could cause a loss of revenue and potentially have a materially adverse effect on our business, results of operations and financial condition.

We may lose money on fixed‑price contracts.

From time to time, we agree to provide products and services under relatively short term fixed‑price contracts. Under these contracts, we are typically responsible for cost overruns. Our actual costs and any gross profit realized on these fixed‑price contracts may vary from the estimated amounts on which these contracts were originally based. There is inherent risk in the estimation process, including significant unforeseen technical and logistical challenges or longer than expected deployment times in the case of rentals. Depending on the size of a project, variations from estimated contract performance could have an adverse impact on our results of operations, financial condition and cash flows.

Increased costs, or lack of availability, of raw materials and other components may result in increased operating expenses and adversely affect our results of operations and cash flows.