Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBIT 21.1 SUBSIDIARIES OF REALNETWORKS 2017 - REALNETWORKS INC | exhibit211-subsidiariesofr.htm |

| EX-32.2 - EXHIBIT 32.2 CFO 906 Q4-17 - REALNETWORKS INC | exhibit322-cfo906q4x17.htm |

| EX-32.1 - EXHIBIT 32.1 CEO 906 Q4-17 - REALNETWORKS INC | exhibit321-ceo906q4x17.htm |

| EX-31.2 - EXHIBIT 31.2 CFO 302 Q4-17 - REALNETWORKS INC | exhibit312-cfo302q4x17.htm |

| EX-31.1 - EXHIBIT 31.1 CEO 302 Q4-17 - REALNETWORKS INC | exhibit311-ceo302q4x17.htm |

| EX-23.1 - EXHIBIT 23.1 CONSENT OF KPMG LLP 2017 - REALNETWORKS INC | exhibit231-kpmgconsent_2017.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Fiscal Year Ended December 31, 2017

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission file number 1-37745

RealNetworks, Inc.

(Exact name of registrant as specified in its charter)

Washington | 91-1628146 | |

(State of incorporation) | (I.R.S. Employer Identification Number) | |

1501 First Avenue South, Suite 600, Seattle, Washington, 98134 | ||

(206) 674-2700

(Address of principal executive offices, zip code, telephone number)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, Par Value $0.001 per share Preferred Share Purchase Rights | The NASDAQ Stock Market The NASDAQ Stock Market | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ | Accelerated filer þ | |||

Non-accelerated filer ¨ | (Do not check if a smaller reporting company) | Smaller reporting company ¨ | ||

Emerging growth company ¨ | ||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the common stock held by non-affiliates of the registrant was $104 million on June 30, 2017, based on the closing price of the common stock on that date, as reported on the Nasdaq Global Select Market. Shares held by each executive officer and director have been excluded in that such persons may be deemed to be affiliates. In the case of 10% or greater shareholders, we have not deemed such shareholders to be affiliates unless there are facts and circumstances which would indicate that such shareholders exercise any control over our company. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s common stock outstanding as of February 23, 2018 was 37,341,387.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant has incorporated by reference the information required by Part III of this Annual Report from its Proxy Statement relating to its 2018 Annual Meeting of Shareholders or an amendment to this Form 10-K, to be filed within 120 days after the end of its fiscal year ended December 31, 2017.

TABLE OF CONTENTS

Page | ||

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

2

PART I.

This Annual Report on Form 10-K and the documents incorporated herein by reference contain forward-looking statements that have been made pursuant to the provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on current expectations, estimates, and projections about RealNetworks’ industry, products, management’s beliefs, and certain assumptions made by management. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” and similar expressions are intended to identify forward-looking statements. All statements contained in this report that do not relate to matters of historical fact should be considered forward-looking statements. Forward-looking statements include statements with respect to:

• | the expected benefits and other consequences of our growth plans, strategic initiatives, and restructurings; |

• | our expected introduction, and related monetization, of new and enhanced products, services and technologies across our businesses; |

• | future revenues, operating expenses, income and other taxes, tax benefits, net income (loss) per diluted share available to common shareholders, acquisition costs and related amortization, and other measures of results of operations; |

• | the effects of our past acquisitions and expectations for future acquisitions and divestitures; |

• | plans, strategies and expected opportunities for future growth, increased profitability and innovation; |

• | the expected financial position, performance, growth and profitability of, and investment in, our businesses and the availability of resources; |

• | the effects of legislation, regulations, administrative proceedings, court rulings, settlement negotiations and other factors that may impact our businesses; |

• | the continuation and expected nature of certain customer relationships; |

• | impacts of competition and certain customer relationships on the future financial performance and growth of our businesses; |

• | our involvement in potential claims, legal proceedings and government investigations, and the potential outcomes and effects of such potential claims, legal proceedings and governmental investigations on our business, prospects, financial condition or results of operations; |

• | the effects of U.S. and foreign income and other taxes on our business, prospects, financial condition or results of operations; and |

• | the effect of economic and market conditions on our business, prospects, financial condition or results of operations. |

These statements are not guarantees of future performance and actual actions or results may differ materially. These statements are subject to certain risks, uncertainties and assumptions that are difficult to predict, including those noted in the documents incorporated herein by reference. Particular attention should also be paid to the cautionary language in Item 1A entitled “Risk Factors.” RealNetworks undertakes no obligation to update publicly any forward-looking statements as a result of new information, future events or otherwise, unless required by law. Readers should, however, carefully review the risk factors included in other reports or documents filed by RealNetworks from time to time with the Securities and Exchange Commission, particularly the Quarterly Reports on Form 10-Q and any Current Reports on Form 8-K.

3

Item 1. | Business |

Overview

RealNetworks creates innovative technology products and services that make it easy to connect with and enjoy digital media. We invented the streaming media category in 1995 and continue to connect consumers with their digital media both directly and through partners, aiming to support every network, device, media type and social network. We provide our digital media products and services to consumers, mobile carriers, device manufacturers and other businesses.

Consumers use our digital media products and services to store, organize, play, manage and enjoy their digital media content, either directly from us or through our distribution partners. Our consumer products and services include our casual games, our ringback tone and messaging tools, and RealPlayer, our widely distributed media player. Our video compression technology is licensed primarily to OEMs, including manufacturers of mobile devices, smart TVs, and set-top boxes. The monetization, distribution, and licensing of our technology products and services are heavily dependent on contracts with third parties, such as mobile carriers and device manufacturers.

We were incorporated in 1994 in the State of Washington. Our common stock is listed on the NASDAQ Stock Market under the symbol “RNWK.”

In this Annual Report on Form 10-K ("10-K") for the year ended December 31, 2017, RealNetworks, Inc., together with its subsidiaries, is referred to as “RealNetworks,” the “Company,” “we,” “us,” or “our.” “RealPlayer,” “RealMedia,” and other trademarks of ours appearing in this report are our property.

Segments

We report revenue and operating income (loss) in three segments: (1) Consumer Media, (2) Mobile Services, and (3) Games. We allocate to our reportable segments certain corporate expenses which are directly attributable to supporting the business, including but not limited to a portion of finance, IT, legal, human resources and headquarters facilities. Remaining expenses, which are not directly attributable to supporting the business, are reported as corporate items. Also reported in our corporate segment are restructuring charges, lease exit and related charges, as well as stock compensation charges.

Consumer Media

In our Consumer Media segment, revenue is primarily derived from the licensing of our portfolio of video codecs. Codecs are an encoding and decoding technology which are designed to reduce the amount of bits required to stream or store media content, and modern codecs achieve significant savings in streaming bandwidth and storage costs. Our latest codec technology, RealMedia High Definition, which we refer to as RealMedia HD or RMHD, offers significant compression advantages over our prior-generation codec, RealMedia Variable Bitrate, or RMVB, which is still widely used. Our codec technologies business is primarily focused in the Chinese market, where RMVB is a popular format and also where we continue to focus most of our efforts to date regarding RMHD.

We continue to develop and innovate our codec technology to meet or exceed user demands for increasing compression efficiency and visual quality. We license our codec technology to a variety of electronic equipment, microchip, and integrated circuit manufacturers who embed our codec in their products, including mobile devices, laptops, smart TVs and other devices. To ensure a robust ecosystem for our codec technologies, we also promote the use of our codec technology to producers of media content and users of RealPlayer, thus encouraging the widespread adoption by device manufacturers.

We also generate revenue through online sales to consumers of our PC-based RealPlayer subscription products, including our SuperPass service, which provides consumers with access to digital entertainment content for a monthly fee. The RealPlayer media player, our enduring yet continually evolving software product, includes features and services that enable consumers to discover, play, download, manage and edit digital video, stream audio and video, download and save photos and videos from the web, transfer and share content on social networks, and edit their own photo and video content. As part of our RealPlayer download process, we also offer distribution of third-party software products to consumers, which generates additional revenue.

Mobile Services

Mobile Services consists of the various digital media services we provide to mobile and online service providers as software as a service (SaaS) offerings. Included in our SaaS offerings are our messaging products, which include our intercarrier messaging service and our recently introduced text message management, anti-spam, and classification product, Kontxt, and our ringback tone service. We provide these services to a large number of mobile carriers around the world, although a significant portion of our revenue for this segment results from contracts with a few mobile carriers. Also included in this segment is our RealTimes platform, which we offer to mobile carriers for incorporation in their hosted cloud solutions.

4

We also offer business intelligence, subscriber management and billing for the carriers who make our offerings available to their customers.

Our intercarrier messaging platform enables operators to send and receive SMS messages worldwide between networks and service providers, regardless of network technology, typically processing billions of SMS messages per day between users on hundreds of different networks. We earn revenue from our intercarrier messaging service based on a revenue-sharing arrangement with one service partner. During the fourth quarter of 2017, we introduced our next-generation mobile messaging platform, Kontxt, which evaluates message streams sent from an application to a person (A2P) and classifies those messages into various categories. This allows network operators and other service providers to create policies for prioritization and delivery of messages and blocking spam and fraudulent messages, resulting in more efficient text message delivery.

Our ringback tone services enable callers to hear subscriber-selected music or messages instead of the traditional electronic ringing sound while waiting for the person they have called to answer. We primarily offer ringback tone services via mobile carriers, where, in return for providing, operating and managing the ringback tone service for the carrier customers, we generally enter into revenue-sharing arrangements with the carriers based on monthly subscription fees, content download fees or a combination of such fees paid by subscribers.

Our photo and video sharing platform, RealTimes, is offered to wireless carriers for integration in their hosted cloud solutions. Within our Mobile Services group, we focus on leveraging current and prospective wireless carrier relationships to increase integration of the RealTimes platform.

In December 2017, we exited our low-margin music on demand service in Korea. As the profits generated from this business had significantly declined over time, we did not seek renewal of the sole contract for this service. Accordingly, this business is reported as discontinued operations in our financial statements for the periods disclosed in this 10-K.

Games

Our Games segment is focused on the development, publishing, and distribution of casual games, which are offered via mobile devices, digital downloads, and subscription play. Casual games typically have simple graphics, rules and controls, are quick to learn, and often include time-management, board, card, puzzle, word and hidden-object games. In the mobile market, we are focused on creating a large and diverse portfolio of products that combine casual game play and storytelling. We call this product line GameHouse Original Stories (Original Stories). Our Original Stories are based on a series of characters including Emily (Delicious Franchise), Amanda (Heart's Medicine) and Angela (Fabulous). The portfolio continues to grow as new characters and story lines are developed. Original Stories are primarily developed by our in-house game studios or through partnerships with external game developers for both mobile and PC play. Also offered to our customers are games licensed to us by third parties.

Our mobile games are digitally distributed through third-party application storefronts, such as the Apple App Store and Google Play, and are principally offered in North America, Europe and Latin America. As they are released, new games are typically introduced to consumers through offering a free trial before purchase on an individual basis. After reaching a certain level in game play, consumers then have the option to purchase the full game. In addition to the sale of mobile games, we also generate revenue through advertising shown to consumers during play.

PC consumers can access and play both our Original Stories and hundreds of third party games through individual purchases or a subscription service offered through our GameHouse and Zylom websites, and through websites owned or managed by third parties. Consistent with our mobile offerings, we typically introduce new games by offering a free trial before purchase on an individual basis or as part of one of our subscription services.

See Note 19. Segment Information, in this 10-K for additional details on our segments and geographic concentrations.

Napster (formerly branded as Rhapsody)

At December 31, 2017, we owned approximately 42% of the issued and outstanding stock of Napster. Since the Rhapsody streaming music service has been re-branded as Napster, all references to Napster in this Annual Report on Form 10-K will refer to Rhapsody International, Inc., d/b/a Napster. See Note 4. Napster Joint Venture, in this 10-K for additional details. Napster provides music products and services that enable consumers to have access to digital music content from a variety of devices. The Napster unlimited subscription service offers unlimited access to a catalog of tens of millions of music tracks by way of on-demand streaming and conditional downloads. Napster also operates a radio-like service, branded as "UnRadio" in the U.S., through which users can listen to online radio stations based on selected artists or genres and download favorite tracks played on those stations for offline playback. Napster currently offers music services worldwide (under the Napster brand) and generates revenue primarily through subscriptions to its music services either directly to consumers or through distribution partners, such as mobile carriers.

5

Customers

Our customers include consumers and businesses located throughout the world. Sales to customers outside the U.S., primarily in Europe and Asia, were 48%, 49% and 49% of our revenue during the years ended December 31, 2017, 2016 and 2015, respectively. See Note 19. Segment Information, for details on geographic concentrations and see Note 6. Allowance for Doubtful Accounts Receivable and Sales Returns, for details on customer revenue concentrations.

Research and Development

We devote a substantial portion of our resources to developing new products, enhancing existing products, expanding and improving our fundamental technology, and strengthening our technological expertise in all our businesses. During the years ended December 31, 2017, 2016, and 2015, we expended 38%, 37% and 47%, respectively, of our revenue on research and development activities.

Sales, Marketing and Distribution

Our marketing programs are aimed at increasing brand awareness of our products and services and stimulating demand. We use a variety of methods to market our products and services, including paid search advertising, affiliate marketing programs, electronic and other online media, and email offers to qualified potential and existing customers, and providing product specific information through our websites. We also cross-market products and services offered by some of our businesses through the RealPlayer and Games marketing and distribution channels. We have subsidiaries and offices in several countries that market and sell our products outside the U.S.

Our products and services are marketed through direct and indirect channels. We use public relations, trade shows, events and speaking opportunities to market our products and services. We also use a variety of online channels, including social media, to promote and sell our products and services directly.

In our Consumer Media business, we market and sell our various RealPlayer services directly through our own websites such as Real.com, as well as indirectly through third party distribution partners. We also employ a sales team in China which works with distribution partners on marketing of our codec technologies.

Our Mobile Services sales, marketing and business development team works closely with many of our enterprise, infrastructure, wireless, broadband and media customers to identify new business opportunities for our entertainment applications, services and systems. Through ongoing communications with the product and marketing divisions of our customers, we tailor our SaaS offerings to their strategic needs and the needs of their subscribers.

Our games are marketed directly from our GameHouse and Zylom websites and through third-party distribution channels, such as application storefronts, search engines, online portals, and content publishers.

Customer Support

Customer support is integral to the provision of nearly all of our consumer products and services. Consumers who purchase and use our consumer software products and services can get assistance primarily via the Internet or email, depending on the product or service. For most of our consumer products, we contract with third-party outsource support vendors to provide the primary staffing for our first-tier customer support globally. We also provide various support service options for our business customers and for software developers using our software products and associated services. Support service options include online support services and on-site support personnel covering technical and business-related support topics.

Competition

The market for software and services for digital media delivery over the Internet and wireless networks is intensely competitive. Many of our current and potential competitors have longer operating histories, greater name recognition or brand awareness, more employees or significantly greater resources than we do.

In our Consumer Media segment, our codec technology faces competition from other next-generation video codecs, and many of our competitors have come together in patent pools to market and license competing codecs. In order to be successful, we must withstand the inherent market penetration that arises when multiple companies promote a shared codec solution. Our RealPlayer media player also continues to face competition from alternative streaming media playback applications which have obtained very broad market penetration.

In our Mobile Services segment, our SaaS business competes with a large and diverse number of domestic and international companies, and each of our SaaS offerings tends to face competitors specific to that product or service. Our SaaS business continues to experience significant competitive pricing pressure from carriers and the proliferation of smartphone applications and services, some of which do not depend on our carrier customers for distribution to consumers. Many of our SaaS services require a high degree of integration with carrier or service provider networks and thus require a high degree of

6

operational expertise. In addition, our ability to enhance services with new features as the digital entertainment market evolves is critical to our competitive position, as is our knowledge of the consumer environment to which these services are targeted.

Our Games business competes with a variety of distributors and publishers of casual games for PC and mobile platforms. Our in-house game development studios compete with other developers and publishers of mobile games based on our ability to create high quality games that resonate with consumers, and our ability to secure broad distribution.

Intellectual Property

As of December 31, 2017, we had 19 U.S. patents, 23 South Korean patents, 11 patents in other countries and more than 25 pending patent applications worldwide relating to various aspects of our technology. We regularly analyze our patent portfolio and prepare additional patent applications on current and anticipated features of our technology in various jurisdictions across the world, or sell or abandon patents or applications that are no longer relevant or valuable to our operations.

In addition to our patent portfolio, we have assembled, over time, an international portfolio of trademarks and service marks that covers certain of our products and services. We also have applications pending for additional trademarks and service marks in jurisdictions around the world, and have several unregistered trademarks. Many of our marks begin with the word “Real” (such as RealPlayer). We are aware of other companies that use “Real” in their marks alone or in combination with other words, and we do not expect to be able to prevent all third-party uses of the word “Real” for all goods and services.

Our ability to compete across our businesses partly depends on the superiority, uniqueness and value of the technology that we both develop and license from third parties. To protect our proprietary rights, we rely on a combination of patent, trademark, copyright and trade secret laws, confidentiality agreements with our employees and third parties, and protective contractual provisions. These efforts to protect our intellectual property rights may not be effective in preventing misappropriation of our technology, or may not prevent the development and design by others of products or technologies similar to or competitive with those we develop.

Employees

At December 31, 2017, we had approximately 456 employees, of which 140 were based in the Americas, 109 were based in Asia, and 207 were based in Europe. None of our employees are subject to a collective bargaining agreement.

Position on Charitable Responsibility

In periods when we have achieved sustained profitability, we intend to donate 5% of our net income to charitable organizations, which will reduce our net income for those periods. The non-profit RealNetworks Foundation, established in 2001, manages a substantial portion of our charitable giving efforts. Through the Foundation, we support our employees' philanthropic efforts by matching their donations of time and money to charitable organizations.

Available Information

Our corporate Internet address is www.realnetworks.com. We make available free of charge on www.investor.realnetworks.com our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments to these reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC). However, the information found on our corporate website is not part of this or any other report.

Item 1A. | Risk Factors |

You should carefully consider the risks described below together with all of the other information included in this 10-K. The risks and uncertainties described below are not the only ones facing our company. Additional risks and uncertainties not presently known to us or that we presently deem less significant may also impair our business operations. If any of the following risks actually occurs, our business, financial condition or operating results, and the trading price of our common stock, could be materially harmed.

Our restructuring efforts and growth plans are ambitious and could be unsuccessful, which would have a material adverse effect on our business and financial results.

For the past several years, we have taken steps to reduce costs and increase profitability by restructuring our businesses and streamlining our operations. We have also developed new products and technologies and funded initiatives intended to create or support growth in our businesses and financial results. These restructuring efforts and growth initiatives have impacted all segments of our organization.

7

The simultaneous execution of all of these activities is complex and ambitious, thereby imposing increased pressure on our reduced human and capital resources, requiring us to allocate limited resources among our diverse business units. These efforts may cause uncertainty around the future direction of our product and service offerings and growth prospects.

Given the ambitious nature of our restructuring and streamlining efforts and our growth initiatives, there is substantial risk that we may be unsuccessful in managing the potential strain on our resources, our cash reserves may be insufficient to fully implement our plans, our growth initiatives may not gain adequate momentum, or the combination of our streamlining efforts and growth initiatives may not prove to be profitable. In any such case, our business would suffer, and our operational and financial results would be negatively impacted to a significant degree. Our stock price would suffer as a result.

We need to successfully monetize our new products and services in order to sustain and grow our businesses, and manage our cash resources.

In order to sustain our current level of business and to implement our growth plans, we must successfully monetize our new products and services, including through existing and new relationships with distribution partners. Our digital media products and services must be attractive and useful to subscribers and consumers, whether direct from us or through our distribution partners. The successful acceptance and monetization of these products and services, therefore, is subject to unpredictable and volatile factors beyond our control, including end-user preferences, competing products and services, the rapid pace of change in the market and the effectiveness of our distribution channels. Any failure by us to timely and accurately anticipate consumers’ changing needs and wants, emerging technological trends or changes in the competitive landscape for our products and services could result in a failure to monetize our new products or the loss of market opportunities.

Moreover, in order to grow our businesses, we must make long-term investments, develop or obtain appropriate intellectual property and commit significant resources before knowing whether the products and services that we are developing or have introduced will meet the demands of a large enough group of consumers. We may not realize a sufficient return, or may experience losses, on these investments, thereby straining our limited cash resources and negatively affecting our ability to pursue other growth or strategic opportunities.

Sustaining and growing our businesses, and managing our cash resources, are subject to these risks inherent in developing, distributing and monetizing our new products and services. Our failure to manage these risks could negatively impact our financial results to a significant degree.

Furthermore, products and services may be subject to legal challenge. Responding to any such claims may require us to enter into royalty and licensing agreements on unfavorable terms, require us to stop distributing or selling, or to redesign our products or services, or to pay damages, any of which could constrain our growth plans and cash resources.

Our businesses face substantial competitive challenges that may prevent us from being successful in those businesses, and may negatively impact future growth in those businesses.

Many of our current and potential competitors in our businesses have longer operating histories, greater name or brand recognition, more employees and significantly greater resources than we do. In addition, current and potential competitors may include relatively new businesses that develop or use innovative technologies, products or features that could disrupt the market for technologies, products or features we currently market or are seeking to develop. In attempting to compete with any or all of these competitors, we may experience some or all of the following consequences, any of which would adversely affect our operating results and the trading price of our stock:

• | reduced prices or margins, |

• | loss of current and potential customers, or partners and potential partners who distribute our products and services or who provide content that we distribute to our customers, |

• | changes to our products, services, technologies, licenses or business practices or strategies, |

• | lengthened sales cycles, |

• | inability to meet demands for more rapid sales or development cycles, |

• | industry-wide changes in content distribution to customers or in trends in consumer consumption of digital media products and services, |

• | pressure to prematurely release products or product enhancements, or |

• | degradation in our stature or reputation in the market. |

The market for our Mobile Services business is highly competitive and evolving rapidly. Increased use of smartphones has resulted in a proliferation of applications and services that compete with our SaaS services. For example, our ringback tones solution faces competition from alternative kinds of applications and services that carriers can deploy or offer to their

8

subscribers, or that consumers can acquire independently of their carrier. Increased competition has in the past resulted in pricing pressure, forcing us to lower the selling price of our services. We expect this pricing pressure to continue to materially harm our operating results and financial condition.

Our Consumer Media technologies for media playback and production (RealPlayer, RealMedia VB and RealMedia HD) compete with alternative media playback technologies and audio and video content formats that have obtained broad market penetration. RealMedia VB and RealMedia HD are codecs, technology that enables compression and decompression of the media content in a (usually proprietary) format. We license our codec technology primarily to computer, smartphone and other mobile device manufacturers, and also to other partners that can support our efforts to build a strong ecosystem, like content providers and integrated circuit developers. To compete effectively, codec technologies must appeal to, and be adopted for use by, a wide range of parties: producers and providers of media content, consumers of media content, and device manufacturers who pre-load codec technologies into their devices. Promoting adoption of our codec technologies to a wide and diverse target market is a complex undertaking. Whether our current or future technologies and formats for producing, streaming or playing back media content, including related codec technology, will be widely and successfully adopted is highly uncertain. If we are unable to compete successfully, our Consumer Media business could continue to decline.

The branded services in our Games business compete with other developers, aggregators and distributors of mobile, online, and downloadable games. Our competitors vary in size and capabilities, which present us with a range of competitive factors and conditions to address. Some of these competitors have high volume distribution channels and greater financial resources than we do. Our Games business also competes with many other smaller companies that may be able to more quickly or efficiently adjust to market conditions. We also face significant price competition in the casual games market, and some of our competitors may be able to offer games for free, or reduce prices more aggressively than us. We expect competition to continue to intensify in this market from these and other competitors. Our games development studios compete primarily with other developers of mobile, online, and downloadable games, and must continue to develop popular and high-quality game titles. Our Games business must also continue to execute on opportunities to expand the play of our games on a variety of non-PC platforms, including mobile, in order to maintain our competitive position and to grow the business.

The distribution and license of our technology products and services are governed by contracts with third parties, the terms of which subject us to significant risks that could negatively impact our revenue, expenses and assumption of liability related to such contracts.

In our Consumer Media and Mobile Services segments, we distribute and license most of our technology products and services pursuant to contracts with third parties, such as mobile carriers and their partners, online service providers, and OEMs and device manufacturers, many of whom may have stronger negotiating leverage due to their size and reach. These contracts govern the calculation of revenue generated and expenses incurred, how we recognize revenue and expenses in our financial statements, and the allocation of risk and liabilities arising from the product or service or distribution thereof. Terms impacting revenue, over which we may have limited if any control, may involve revenue sharing arrangements, end user pricing, usage levels, and exclusivity, all of which materially affect the level of revenue that we may realize from the relationship. Moreover, contract terms around marketing and promotion of our products and other expense allocation could result in us bearing higher expenses or achieving weaker performance than we had anticipated from the relationship.

In addition, although our contracts with third parties are typically for a fixed duration, they could be terminated early; and they may be renegotiated on less favorable terms or may not be renewed at all by the other party. We must, therefore, seek additional contracts with third parties on an ongoing basis to sustain and grow our business. We expect to face continuing and increased competition for the technology products and services we provide, and there is no assurance that the parties with which we currently have contracts will continue or extend current contracts on the same or more favorable terms, or that we will obtain alternative or additional contracts for our technology products and services. The loss of existing contracts, the failure to enter new contracts, or the deterioration of terms in our contracts with third parties could materially harm our operating results and financial condition.

Nearly all of our contracts in which we provide to another party services or rights to use our technology include some form of obligation by us to indemnify the other party for certain liabilities and losses incurred by them, including liabilities resulting from third party claims for damages that arise out of the use of our technology. These indemnification terms provide us with certain procedural safeguards, including the right to control the defense of the indemnified party. We have in the past incurred costs to defend and settle such claims. Claims against which we may be obligated to defend others pursuant to our contracts could in the future result in payments that could materially harm our business and financial results.

9

We may not be successful in maintaining revenue associated with the distribution of our legacy digital media products.

Maintaining and growing the distribution of digital media products through our websites and our other distribution channels has historically been an important revenue driver for our business, including growth through the introduction of new products and services distributed through these channels. Consumers are not downloading and using our digital media products consistent with past usage, so our ability to generate revenue from those products has been, and we expect will be continue to be, reduced, leading to lower than expected adoption of newly introduced products and services. This will also impair the growth and development of related revenue streams from these market segments, including the distribution of third-party products and sales of our subscription services. Historically, most of our revenue from the distribution of third-party products was derived from a single contract, and the terms of this relationship have significantly deteriorated over the years. Our distribution revenue has been, and will continue to be, materially negatively impacted by these factors.

Our operating results are difficult to predict and may fluctuate, which may contribute to continued weakness in our stock price.

The trading price for our common stock has a history of volatility. As a result of the rapidly changing markets in which we compete, our operating results may fluctuate or continue to decline from period to period, which may contribute to further volatility or continued weakness of our stock price.

In past periods, our operating results have been affected by personnel reductions and related restructuring charges, lease exit and related charges, other one-time events, and impairment charges for certain of our equity investments, goodwill and other long-lived assets. In addition to these factors, the general difficulty in forecasting our operating results and metrics could result in actual results that differ significantly from expected results, again causing further volatility and continued weakness in our stock price.

Certain of our product and service investment decisions (for example, research and development and sales and marketing efforts) are based on predictions regarding business and the markets in which we compete. Fluctuations in our operating results, particularly when experienced beyond what we expected, could cause the trading price of our stock to fluctuate. Weakness in our operating performance is likely to cause continued weakness in our stock price.

Any impairment to our goodwill and definite-lived assets could result in a significant charge to our earnings.

In accordance with accounting principles generally accepted in the United States ("GAAP"), we test goodwill for possible impairment on an annual basis or more frequently in the event of certain indications of possible impairment. We review definite-lived assets for impairment whenever events or changes in circumstances indicate the carrying amount of such assets may not be recoverable. These events or circumstances could include a significant change in the business climate, including a significant sustained decline in a reporting unit’s market value, changes in our operating plans and forecasts, legal factors, operating performance indicators, competition, sale or disposition of a significant portion of our business, a significant sustained decline in our market capitalization and other factors. If we were to determine that an impairment had occurred, we would be required to record an impairment charge, which could have a significant negative, and unpredicted, impact on our financial results. The total carrying value of our goodwill and definite-lived assets as of December 31, 2017 was $17 million.

Continued loss of revenue from our subscription services may continue to harm our operating results.

Our operating results have been and may continue to be adversely impacted by the loss of subscription revenue related to our more traditional products and services. Subscribers may cancel their subscriptions to our services for many reasons, including a perception that they do not use the services sufficiently or that the service does not provide enough value, a lack of attractive or exclusive content generally or as compared with competitive service offerings, or because customer service issues are not satisfactorily resolved. Revenue from our SuperPass subscription service, for example, has continued to decline over several periods, due to changes in consumer preferences and changes on our part to focus on other products and services we offer, and we expect these trends to continue.

Government regulation of the Internet is evolving, and unfavorable developments could have an adverse effect on our operating results.

We are subject to regulations and laws specific to the marketing, sale and delivery of goods and services over the Internet. These laws and regulations, which continue to evolve, cover taxation, user privacy, data collection and protection, copyrights,

10

electronic contracts, sales procedures, automatic subscription renewals, credit card processing procedures, consumer protections, digital games distribution, broadband Internet access and content restrictions. We cannot guarantee that we have been or will be fully compliant in every jurisdiction, as it is not entirely clear how existing laws and regulations governing issues such as privacy, taxation and consumer protection apply or will be enforced with respect to the products and services we sell through the Internet. Moreover, as Internet commerce continues to evolve, increasing regulation and/or enforcement efforts by federal, state and foreign agencies and the prospects for private litigation claims related to our data collection, privacy policies or other e-commerce practices become more likely. In addition, the adoption of any laws or regulations or the imposition of other legal requirements that adversely affect our ability to market, sell, and deliver our products and services could decrease our ability to offer or customer demand for our service offerings, resulting in lower revenue. Future regulations, or changes in laws and regulations or their existing interpretations or applications, could also require us to change our business practices, raise compliance costs or other costs of doing business and result in additional historical or future liabilities for us, resulting in adverse impacts on our business and our operating results.

As a consumer-facing business, we receive complaints from our customers regarding our consumer marketing efforts and our customer service practices. Some of these customers may also complain to government agencies, and from time to time, those agencies have made inquiries to us about these practices. In addition, we may receive complaints or inquiries directly from governmental agencies that have not been prompted by consumers. In May of 2012, we resolved an investigation and complaint filed against us by the Washington State Office of the Attorney General, or Washington AG, relating to our consumer marketing practices through the entry of a consent decree filed in King County, Washington Superior Court. While we resolved that matter, we cannot provide assurance that the Washington AG or other governmental agencies will not bring future claims regarding our marketing, or consumer services or other practices.

We face financial and operational risks associated with doing business in non-U.S. jurisdictions and operating a global business, that have in the past and could in the future have a material adverse impact on our business, financial condition and results of operations.

A significant portion of our revenue is derived from sales outside of the U.S. and most of our employees are located outside of the U.S.. Consequently, our business and operations depend significantly on global and national economic conditions and on applicable trade regulations and tariffs. The growth of our business is also dependent in part on successfully managing our international operations. Our non-U.S. sales, purchases and operations are subject to risks inherent in conducting business abroad, many of which are outside our control, including the following:

• | periodic local or geographic economic downturns and unstable political conditions; |

• | price and currency exchange controls; |

• | fluctuation in the relative values of currencies; |

• | difficulty in repatriating money, whether as a result of tax laws or otherwise; |

• | compliance with current and changing tax laws, and the coordination of compliance with U.S. tax laws and the laws of any of the jurisdictions in which we do business; |

• | difficulties protecting intellectual property; |

• | compliance with labor laws and other laws governing employees; |

• | local labor disputes; |

• | changes in trading policies, regulatory requirements, tariffs and other barriers, or the termination or renegotiation of existing trade agreements; |

• | impact of changes in immigration or other policies impacting our ability to attract, hire, and retain key talent; and |

• | difficulties in managing a global enterprise, including staffing, collecting accounts receivable, and managing suppliers, distributors and representatives. |

Because consumers may consider the purchase of our digital entertainment products and services to be a discretionary expenditure, their decision whether to purchase our products and services may be influenced by macroeconomic factors that affect consumer spending such as unemployment, access to credit, negative financial news, and declines in income. In addition, mobile telecommunication carriers and other business partners may reduce their business or advertising spending with us or for our products and services they distribute to users in the face of adverse macroeconomic conditions, such as financial market volatility, government austerity programs, tight credit, and declines in asset values. We have in the past recorded material asset impairment charges due in part to weakness in the global economy, and we may need to record additional impairments to our assets in future periods in the event of renewed weakness and uncertainty in the global or a relevant national economy. Accordingly, any significant weakness in the national and/or global economy could materially impact our business, financial condition and results of operations in a negative manner.

Our international operations involve risks inherent in doing business globally, including difficulties in managing operations due to distance, language, and cultural differences, local economic conditions, different or conflicting laws and

11

regulations, taxes, and exchange rate fluctuations. The functional currency of our foreign subsidiaries is typically the local currency of the country in which each subsidiary operates. We translate our subsidiaries’ revenues into U.S. dollars in our financial statements, and continued volatility in foreign exchange rates, particularly if the U.S. dollar strengthens against the euro, may result in lower reported revenue or net assets in future periods. If we do not effectively manage any of the risks inherent in running our international businesses, our operating results and financial condition could be harmed.

Our business is conducted in accordance with existing international trade relationships, and trade laws and regulations. Changes in geopolitical relationships and laws or policies governing the terms of foreign trade could create uncertainty regarding our ability to operate and conduct commercial relationships in affected jurisdictions, which could have a material adverse effect on our business and financial results. Additionally, our global operations may also be adversely affected by political events, domestic or international terrorist events and hostilities or complications due to natural or human-caused disasters. These uncertainties could have a material adverse effect on the continuity of our business and our results of operations and financial condition.

Napster could continue to recognize losses, or we may modify our relationship with Napster in ways which could negatively impact our results of operations and financial condition or the perceived value of our common stock.

On March 31, 2010, we completed the restructuring of our digital audio music service joint venture, Rhapsody America LLC, now doing business under the Napster brand. As a result of the restructuring, we no longer have operational control over Napster and Napster’s operating performance is no longer consolidated with our consolidated financial statements. We disclose only limited strategic, business and financial information regarding Napster in our financial statements and disclosures, in accordance with GAAP. Napster has generated accounting losses since its inception, and we have recognized our share of such losses on our investment in its convertible preferred stock. We continue to track additional losses incurred by Napster whether or not we recognize them, but in certain circumstances, which have occurred in the past and may occur again in the future, proper accounting treatment may cause us to recognize additional losses on our investment in Napster. Consequently, Napster's past or future performance may continue to have an adverse effect on our financial condition, results of operations, or perceived value. See Note 4. Napster Joint Venture, in this 10-K, for further discussion of our relationship with Napster, including information about the accounting treatment related to the investment in Napster.

As a significant shareholder of Napster we have been in the past and may be in the future faced with a decision as to whether or not it is in the long term interest of RealNetworks to take certain actions with respect to Napster, such as extending a loan, making a further equity investment or providing an additional financial guarantee (as we did during the fourth quarter of 2017), any of which could reduce our available cash or liquidity, and any such action could result in the recognition of additional losses associated with our investment in Napster. The extent of any such potential action is likely to be influenced by whether Napster is able to secure and maintain adequate funding, experiences further declines in its operating results, or is unsuccessful in growing or improving its business or financial condition. Some or all of our decisions or actions related to Napster could have, or increase the risk to us of, an adverse effect on our financial condition, results of operations, liquidity or perceived value.

We depend on timely financial information from Napster in order to timely prepare and file our periodic SEC reports.

Given the current proportion of the outstanding equity of Napster that we hold, we need to receive Napster’s unaudited quarterly financial statements and related information in order to timely prepare our quarterly consolidated financial statements and also to report certain of Napster’s financial results, as may be required, in our quarterly reports on Form 10-Q. In addition, under certain circumstances, we may be required to include Napster’s annual audited financial statements in our 10-K in future periods. As we no longer exert operational control over Napster, we cannot guarantee that Napster will deliver its financial statements and related information to us in a timely manner, or at all, or that the unaudited financial statement information provided by Napster will not contain inaccuracies that are material to our reported results. Any failure to timely obtain Napster’s quarterly financial statements or to include its audited financial statements in our future 10-Ks, if required, could cause our reports to be filed in an untimely manner, which would preclude us from utilizing certain registration statements and could negatively impact our stock price. See Note 4. Napster Joint Venture, for further information related to our investment in Napster.

The continued loss of key personnel, or difficulty recruiting and retaining them, could significantly harm our business or jeopardize our ability to meet our growth objectives.

Our success depends substantially on the contributions and abilities of certain key executives and employees. We have experienced a significant amount of executive-level turnover in the past several years, which has had and could continue to

12

have a negative impact on our ability to retain key employees. We cannot provide assurance that we will effectively manage these recent or future executive-level transitions, which may impact our ability to retain key executives and employees and which could harm our business and operations to the extent there is customer or employee uncertainty arising from such transitions.

Our success is also substantially dependent upon our ability to identify, attract and retain highly skilled management, technical and sales personnel. Qualified individuals are in high demand and competition for such qualified personnel in our industry, particularly engineering talent, is extremely intense, and we may incur significant costs to attract or retain them. Changes in immigration or other policies in the U.S. or other jurisdictions that make it more difficult to hire and retain key talent, or to assign individuals to any of our locations as needed to meet business needs, could adversely affect our ability to attract key talent or deploy individuals as needed, and thereby adversely affect our business and financial results. In addition, our ability to attract and retain personnel has been and may continue to be made more difficult by the uncertainty created by our executive-level turnover and by our continued restructuring efforts, which have involved reductions in our workforce. There can be no assurance that we will be able to attract and retain the key personnel necessary to sustain our business or support future growth.

Acquisitions and divestitures involve costs and risks that could harm our business and impair our ability to realize potential benefits from these transactions.

As part of our business strategy, we have acquired and sold technologies and businesses in the past and expect that we will continue to do so in the future. The failure to adequately manage transaction costs and address the financial, legal and operational risks raised by acquisitions and divestitures of technology and businesses could harm our business and prevent us from realizing the benefits of these transactions. In addition, we may identify and acquire target companies, but those companies may not be complementary to our current operations and may not leverage our existing infrastructure or operational experience, which may increase the risks associated with completing acquisitions.

Transaction-related costs and financial risks related to completed and potential future purchase or sale transactions may harm our financial position, reported operating results, or stock price. Previous acquisitions have resulted in significant expenses, including amortization of purchased technology, amortization of acquired identifiable intangible assets and the incurrence of charges for the impairment of goodwill and other intangible assets, which are reflected in our operating expenses. New acquisitions and any potential additional future impairment of the value of purchased assets, including goodwill, could have a significant negative impact on our future operating results. In compliance with GAAP, we evaluate these assets for impairment at least annually. Factors that may be considered a change in circumstances, indicating that our goodwill or definite-lived assets may not be recoverable, include reduced future revenue and cash flow estimates due to changes in our forecasts, and unfavorable changes to valuation multiples and discount rates due to changes in the market. If we were to conclude that any of these assets were impaired, we would have to recognize an impairment charge that could significantly impact our financial results.

Purchase and sale transactions also involve operational risks that could harm our existing operations or prevent realization of anticipated benefits from a transaction. These operational risks include:

• | difficulties and expenses in assimilating the operations, products, technology, information systems, and/or personnel of the acquired company; |

• | retaining key management or employees of the acquired company; |

• | entrance into unfamiliar markets, industry segments, or types of businesses; |

• | operating, managing and integrating acquired businesses in remote locations or in countries in which we have little or no prior experience; |

• | diversion of management time and other resources from existing operations; |

• | impairment of relationships with employees, affiliates, advertisers or content providers of our business or acquired business; and |

• | assumption of known and unknown liabilities of the acquired company, including intellectual property claims. |

We may be unable to adequately protect our proprietary rights or leverage our technology assets, and may face risks associated with third-party claims relating to intellectual property rights associated with our products and services.

Our ability to compete across our businesses partly depends on the superiority, uniqueness and value of our technology, including both internally developed technology and technology licensed from third parties. To protect our proprietary rights, we rely on a combination of patent, trademark, copyright and trade secret laws, confidentiality agreements with our employees and third parties, and protective contractual provisions. Our efforts to protect our intellectual property rights may not assure our

13

ownership rights in our intellectual property, protect or enhance the competitive position of our products, services and technology, or effectively prevent misappropriation of our technology.

From time to time we receive claims and inquiries from third parties alleging that our technology used in our business may infringe the third parties’ proprietary rights. These claims, even if not meritorious, could force us to make significant investments of time, attention and money in defense, and give rise to monetary damages, penalties or injunctive relief against us. We may be forced to litigate, to enforce or defend our patents, trademarks or other intellectual property rights, or to determine the validity and scope of other parties' proprietary rights in intellectual property. To resolve or avoid such disputes, we may also be forced to enter into royalty or licensing agreements on unfavorable terms or redesign our product features, services and technology to avoid actual or claimed infringement of misappropriation or technology. Any such dispute would likely be costly and distract our management, and the outcome of any such dispute (such as additional licensing arrangements or redesign efforts) could fail to improve our business prospects or otherwise harm our business or financial results.

Nearly all of our contracts by which we provide to another party services or rights to use our technology include some form of obligation by us to indemnify the other party for certain liabilities and losses incurred by them, including liabilities resulting from third party claims for damages that arise out of the use of our technology. Also, in 2012 we sold most of our patents, including patents that covered streaming media, to Intel Corporation, in a contract by which we agreed to indemnify Intel for certain third-party infringement claims against these patents up to the purchase price we received in the sale. Claims against which we may be obligated to defend others pursuant to our contracts expose us to the same risks and adverse consequences described above regarding claims we may receive directly alleging that our trademarks or technology used in our business may infringe a third party's proprietary rights.

Disputes regarding the validity and scope of patents or the ownership of technologies and rights associated with streaming media, digital distribution, and online businesses are common and likely to arise in the future. We also routinely receive challenges to our trademarks and other proprietary intellectual property that we are using in our business activities. We are likely to continue to receive claims of third parties against us, alleging contract breaches, infringement of copyrights or patents, trademark rights, trade secret rights or other proprietary rights, or alleging unfair competition or violations of privacy rights.

We believe that our patent portfolio before the sale to Intel may have in the past discouraged third parties from bringing infringement or other claims against us relating to the use of our technologies in our business. Accordingly, we cannot predict whether the sale of these patent assets to Intel will result in additional infringement or other claims against us from third parties.

Our business and operating results will suffer and we may be subject to market risk and legal liability if our systems or networks fail, become unavailable, unsecured or perform poorly so that current or potential users do not have adequate access to our products, services and websites.

Our ability to provide our products and services to our customers and operate our business depends on the continued operation and security of our information systems and networks and those of our service providers. A significant or repeated reduction in the performance, security or availability of our information systems and network infrastructure or that of our service providers could harm our ability to conduct our business, and harm our reputation and ability to attract and retain users, customers, advertisers and content providers. Many of our products are interactive Internet applications that by their very nature require communication between a client and server to operate.

We sell many of our products and services through online sales transactions directly with consumers, and their credit card information is collected and stored by our payment processors. The systems of our third party service providers may not prevent future improper access or disclosure of credit card information or personally identifiable information. We have an extensive privacy policy concerning the collection, use and disclosure of user data involved in interactions between our client, third party payment providers, and server products. A security breach that leads to disclosure of consumer account information, or any failure by us to comply with our posted privacy policy or existing or new privacy legislation, could harm our reputation, impact the market for our products and services, or subject us to litigation. We have on occasion experienced system errors and failures that caused interruption in availability of products or content or an increase in response time. Problems with our systems and networks, or the third party systems and networks that we utilize, could result from a failure to adequately maintain and enhance these systems and networks, natural disasters and similar events, power failures, intentional actions to disrupt systems and networks and many other causes. Many of our services do not currently have fully redundant systems or a formal disaster recovery plan, and we may not have adequate business interruption insurance to compensate us for losses that may occur from a system outage.

14

Changes in regulations applicable to the Internet and e-commerce that increase the taxes on the services we provide could materially harm our business and operating results.

As Internet commerce continues to evolve, increasing taxation by state, local or foreign tax authorities becomes more likely. For example, taxation of electronically delivered products and services or other charges imposed by government agencies may also be imposed. We believe we collect transactional taxes and are compliant and current in all jurisdictions where we believe we have a collection obligation for transaction taxes. Any regulation imposing greater taxes or other fees for products and services could result in a decline in the sale of products and services and the viability of those products and services, harming our business and operating results. A successful assertion by one or more states or foreign tax authorities that we should collect and remit sales or other taxes on the sale of our products or services could result in substantial liability for past sales.

In those countries where we have a tax obligation, we collect and remit value added tax, or VAT, on sales of “electronically supplied services” provided to European Union residents. The collection and remittance of VAT subjects us to additional currency fluctuation risks.

Changes in accounting standards and subjective assumptions, estimates, and judgments by management related to complex accounting matters could significantly affect our financial results or financial condition.

We prepare our financial statements in conformity with GAAP. These accounting principles are subject to interpretation or changes by the Financial Accounting Standards Board ("FASB") and the SEC, and new accounting pronouncements and varying interpretations of accounting standards and practices have occurred in the past and are expected to occur in the future. Moreover, our financial statements require the application of judgments and estimates regarding a wide range of matters that are relevant to our business, such as revenue recognition, asset impairment and fair value determinations, stock-based compensation, equity method accounting, and intangible asset valuations. Changes in accounting standards or practices, or in our judgments and estimates underlying accounting standards and practices, could harm our operating results and/or financial condition. An example of a new accounting pronouncement is Accounting Standards Update ("ASU") 2014-09 related to revenue recognition. As discussed in Note 2 to the accompanying notes to the consolidated financial statements, ASU 2014-09 will change the way we recognize revenue and will impact the timing of revenue recognition. In addition, subjective judgments and estimates are often necessary in our accounting for investments, such as Napster. Changes to existing accounting rules or to our judgments and estimates underlying those rules could materially impact our reported operating results and financial condition.

We may be subject to additional income tax assessments and changes in applicable tax regulations could adversely affect our financial results.

We are subject to income taxes in the U.S. and numerous foreign jurisdictions. Significant judgment is required in determining our worldwide provision for income taxes, income taxes payable, and net deferred tax assets. In the ordinary course of business, there are many transactions and calculations where the ultimate tax determination is uncertain. Although we believe our tax estimates are reasonable, the final determination of tax audits and any related litigation could be materially different than that which is reflected in our historical financial statements. An audit or litigation can result in significant additional income taxes payable in the U.S. or foreign jurisdictions which could have a material adverse effect on our financial condition and results of operations.

Our Chairman of the Board and Chief Executive Officer beneficially owns approximately 36% of our stock, which gives him significant control over certain major decisions on which our shareholders may vote or which may discourage an acquisition of us.

Robert Glaser, our Chairman of the Board and Chief Executive Officer, beneficially owns approximately 36% of our common stock. As a result, Mr. Glaser and his affiliates will have significant influence to:

• | elect or defeat the election of our directors; |

• | amend or prevent amendment of our articles of incorporation or bylaws; |

• | effect or prevent a merger, sale of assets or other corporate transaction; and |

• | control the outcome of any other matter submitted to the shareholders for vote. |

The stock ownership of Mr. Glaser may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of RealNetworks, which in turn could reduce our stock price or prevent our shareholders from realizing a premium over our stock price.

15

Provisions of our charter documents, shareholder rights plan, and Washington law could discourage our acquisition by a third party.

Our articles of incorporation provide for a strategic transactions committee of the board of directors. Without the prior approval of this committee, and subject to certain limited exceptions, the board of directors does not have the authority to:

• | adopt a plan of merger; |

• | authorize the sale, lease, exchange or mortgage of assets representing more than 50% of the book value of our assets prior to the transaction or on which our long-term business strategy is substantially dependent; |

• | authorize our voluntary dissolution; or |

• | take any action that has the effect of any of the above. |

Mr. Glaser has special rights under our articles of incorporation to appoint or remove members of a strategic transactions committee at his discretion that could make it more difficult for RealNetworks to be sold or to complete another change of control transaction without Mr. Glaser’s consent. RealNetworks has also entered into an agreement providing Mr. Glaser with certain contractual rights relating to the enforcement of our charter documents and Mr. Glaser’s roles and authority within RealNetworks. These rights and his role as Chairman of the Board of Directors, together with Mr. Glaser’s significant beneficial ownership, create unique potential for concentrated influence of Mr. Glaser over potentially material transactions involving RealNetworks and decisions regarding the future strategy and leadership of RealNetworks.

We have adopted a shareholder rights plan, which was amended and restated in December 2008, and amended in April 2016, which provides that shares of our common stock have associated preferred stock purchase rights. The exercise of these rights would make the acquisition of RealNetworks by a third party more expensive to that party and has the effect of discouraging third parties from acquiring RealNetworks without the approval of our board of directors, which has the power to redeem these rights and prevent their exercise.

Washington law imposes restrictions on some transactions between a corporation and certain significant shareholders. The foregoing provisions of our charter documents, shareholder rights plan, our agreement with Mr. Glaser, and Washington law, as well as our charter provisions that provide for a classified board of directors and the availability of “blank check” preferred stock, could have the effect of making it more difficult or more expensive for a third party to acquire, or of discouraging a third party from attempting to acquire, control of us. These provisions may therefore have the effect of limiting the price that investors might be willing to pay in the future for our common stock.

Item 1B. | Unresolved Staff Comments |

None.

Item 2. | Properties |

Our corporate and administrative headquarters and certain research and development and sales and marketing personnel are located at our facility in Seattle, Washington.

We lease properties primarily in the following locations that are utilized by all of our business segments, unless otherwise noted below, to house our research and development, sales and marketing, and general and administrative personnel:

Location | Area leased (sq. feet) | Lease expiration | ||

Seattle, Washington (1) | 86,000 | August 2024, with an option to renew for two five-year periods | ||

Eindhoven, Netherlands (2) | 23,000 | June 2022 | ||

(1) | As of December 31, 2017, we have reduced our use of the facility by 69%. The space which we no longer occupy is currently under sublease for all or a portion of the remaining lease term. For further information, please see Note 11. Lease Exit and Related Charges in this 10-K. |

(2) | This facility is utilized only by our Games segment. |

In addition, we lease smaller facilities in the U.S. and foreign countries, some of which support the operations of all of our business segments while others are dedicated to a specific business segment. We believe that our properties are in good

16

condition, adequate and suitable for the conduct of our business. For additional information regarding our obligations under leases, see Note 17. Commitments and Contingencies, in this 10-K.

Item 3. | Legal Proceedings |

See Note 17. Commitments and Contingencies, in this 10-K.

Item 4. | Mine Safety Disclosures |

Not applicable.

17

PART II.

Item 5. | Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

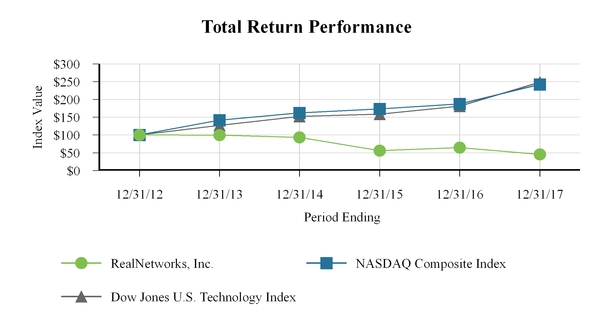

Our common stock is traded on The NASDAQ Stock Market under the symbol RNWK.

The high and low intraday sales prices for our common stock were as follows:

Years Ended December 31, | ||||||||||||||||

2017 | 2016 | |||||||||||||||

High | Low | High | Low | |||||||||||||

First Quarter | $ | 5.45 | $ | 4.50 | $ | 4.43 | $ | 3.04 | ||||||||

Second Quarter | 4.84 | 4.11 | 4.65 | 4.00 | ||||||||||||

Third Quarter | 4.92 | 3.90 | 5.10 | 3.97 | ||||||||||||

Fourth Quarter | 5.00 | 3.40 | 5.14 | 4.09 | ||||||||||||

As of January 31, 2018, there were approximately 179 holders of record of our common stock. Most shares of our common stock are held by brokers and other institutions on behalf of shareholders.