Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Aberdeen Standard Precious Metals Basket ETF Trust | gltr-20171231xex32_2.htm |

| EX-32.1 - EX-32.1 - Aberdeen Standard Precious Metals Basket ETF Trust | gltr-20171231xex32_1.htm |

| EX-31.2 - EX-31.2 - Aberdeen Standard Precious Metals Basket ETF Trust | gltr-20171231xex31_2.htm |

| EX-31.1 - EX-31.1 - Aberdeen Standard Precious Metals Basket ETF Trust | gltr-20171231xex31_1.htm |

| EX-23.1 - EX-23.1 - Aberdeen Standard Precious Metals Basket ETF Trust | gltr-20171231xex23_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number: 001-34917

ETFS PRECIOUS METALS BASKET TRUST

(Exact name of registrant as specified in its charter)

|

New York |

27-2780046 |

|

(State or other jurisdiction of |

(I.R.S. Employer |

|

incorporation or organization) |

Identification No.) |

|

|

|

|

c/o ETF Securities USA LLC |

|

|

405 Lexington Avenue |

|

|

New York, NY |

10174 |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code:

(646) 846 3130

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of each class |

|

|

Name of each exchange on which registered |

|

|

ETFS Physical PM Basket Shares |

NYSE Arca |

||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months.

Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

Accelerated filer |

☒ |

|

|

Non accelerated filer |

☐ |

Smaller reporting company |

☐ |

|

|

|

Emerging growth company |

☐ |

||

If an emerging growth company, indicate by check mark if the registrant had elected not to use the extend transition period for complying with any new or revised financial accounting standards pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes ☐ No ☒

Aggregate market value of the registrant’s shares outstanding based upon the closing price of a share on June 30, 2017 as reported by the NYSE Arca, Inc. on that date: $324,292,500.

As of February 21, 2018, ETFS Precious Metals Basket Trust has 5,800,000 ETFS Physical PM Basket Shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None.

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains various “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and within the Private Securities Litigation Reform Act of 1995, as amended. Forward-looking statements usually include the words, “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “projects,” “understands” and other words suggesting uncertainty. We remind readers that forward-looking statements are merely predictions and therefore inherently subject to uncertainties and other factors and involve known and unknown risks that could cause the actual results, performance, levels of activity, or our achievements, or industry results, to be materially different from any future results, performance, levels of activity, or our achievements expressed or implied by such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Trust undertakes no obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Additional significant uncertainties and other factors affecting forward-looking statements are presented in the Risk Factors section herein.

TABLE OF CONTENTS

|

|

|

|

|

|

1 | |

|

|

1 | |

|

|

2 | |

| 3 | ||

| 13 | ||

| 21 | ||

|

|

21 | |

|

|

22 | |

|

|

22 | |

|

|

23 | |

|

|

24 | |

|

|

22 | |

|

|

24 | |

|

|

24 | |

| 25 | ||

|

25 |

||

|

|

25 | |

|

|

26 | |

|

|

27 | |

|

|

30 | |

|

|

31 | |

|

|

40 | |

|

|

40 | |

|

|

40 | |

|

|

40 | |

|

|

|

|

|

|

41 | |

|

|

41 | |

|

|

43 | |

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

44 |

|

Item 7A. Quantitative and Qualitative Disclosures about Market Risk |

|

47 |

|

|

48 | |

|

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

48 |

|

|

49 | |

|

|

51 | |

|

|

|

|

|

|

52 | |

|

Item 10. Directors, Executive Officers and Corporate Governance |

|

52 |

|

|

52 | |

|

|

53 | |

|

Item 13. Certain Relationships and Related Transactions, and Director Independence |

|

53 |

|

|

53 | |

|

|

|

|

|

|

54 | |

|

|

54 | |

|

|

54 |

The purpose of the ETFS Precious Metals Basket Trust (the “Trust”) is to own, in an agreed proportion, gold, silver, platinum and palladium (collectively, “Bullion”) transferred to the Trust in exchange for shares issued by the Trust (“Shares”). Each Share represents a fractional undivided beneficial interest in and ownership of the Trust. The assets of the Trust are anticipated to consist solely of Bullion. The Trust was formed on October 18, 2010 when an initial deposit of Bullion was made in exchange for the issuance of two Baskets (a “Basket” consists of 50,000 Shares).

The sponsor of the Trust is ETF Securities USA LLC (the “Sponsor”). The trustee of the Trust is The Bank of New York Mellon (the “Trustee”) and the custodian is JPMorgan Chase Bank N.A., London Branch (the “Custodian”).

The Trust’s Shares at redeemable value increased from $261,511,595 at December 31, 2016 to $361,931,979 at December 31, 2017, the Trust’s fiscal year end. Outstanding Shares in the Trust increased from 4,500,000 Shares at December 31, 2016 to 5,600,000 Shares at December 31, 2017.

The Trust is not managed like a corporation or an active investment vehicle. The Trust has no directors, officers or employees. It does not engage in any activities designed to obtain a profit from or to improve the losses caused by changes in the price of gold, silver, platinum and palladium. The Bullion held by the Trust will only be delivered to pay the remuneration due to the Sponsor (the “Sponsor’s Fee”), distributed to Authorized Participants (defined below) in connection with the redemption of Baskets or sold (1) on an as-needed basis to pay Trust expenses not assumed by the Sponsor, (2) in the event the Trust terminates and liquidates its assets, or (3) as otherwise required by law or regulation.

The Trust is not registered as an investment company under the Investment Company Act of 1940 and is not required to register under such act. The Trust does not and will not hold or trade in commodities futures contracts, “commodity interests” or any other instruments regulated by the Commodity Exchange Act (the “CEA”), as administered by the Commodity Futures Trading Commission (the “CFTC”). The Trust is not a commodity pool for purposes of the CEA and the Shares are not “commodity interests” and neither the Sponsor nor the Trustee is subject to regulation as a commodity pool operator or a commodity trading advisor in connection with the Shares. The Trust has no fixed termination date.

The Sponsor of the registrant maintains an Internet website at www.etfsecurities.com, through which the registrant’s annual reports on Form 10-K, quarterly reports on Form 10-Q, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, are made available free of charge as soon as reasonably practicable after they have been filed or furnished to the Securities and Exchange Commission (the “SEC”). Additional information regarding the Trust may also be found on the SEC’s EDGAR database at www.sec.gov.

1

The investment objective of the Trust is for the Shares to reflect the performance of the price of physical gold, silver, platinum and palladium in the proportions held by the Trust, less the expenses of the Trust’s operations. The Trust holds Bullion in a ratio such that, for every 0.03 ounces of gold, it holds 1.1 ounces of silver, 0.004 ounces of platinum and 0.006 ounces of palladium. The Shares are intended to constitute a simple and cost-effective means of making an investment similar to an investment in physical Bullion. An investment in physical Bullion requires expensive and sometimes complicated arrangements in connection with the assay, transportation, warehousing and insurance of the metal. Traditionally, such expense and complications have resulted in investments in physical Bullion being efficient only in amounts beyond the reach of many investors.

The Shares are intended to provide institutional and retail investors with a simple and cost-efficient means, with minimal credit risk, of gaining investment benefits similar to those of holding physical Bullion. The Shares offer an investment that:

•Is Easily Accessible. The Shares trade on the NYSE Arca and provide institutional and retail investors with indirect access to the Bullion markets. The Shares are bought and sold on the NYSE Arca like any other exchange-listed securities. The close of the NYSE Arca trading session is 4:00 PM New York time.

•Is Relatively Cost Effective. The Sponsor expects that, for many investors, costs associated with buying and selling the Shares in the secondary market and the payment of the Trust’s ongoing expenses will be lower than the costs associated with buying and selling Bullion and storing and insuring Bullion in a traditional allocated Bullion account.

•Has Minimal Credit Risk. The Shares represent an interest in physical Bullion owned by the Trust (other than an amount held in unallocated form which is not sufficient to make up a whole bar or plate or ingot or which is held temporarily to effect a creation or redemption of Shares). Physical Bullion of the Trust in the Custodian’s possession is not subject to borrowing arrangements with third parties. Other than the Bullion temporarily being held in an unallocated Bullion account with the Custodian, the physical Bullion of the Trust is not subject to counterparty or credit risks. See “Risk Factors—Bullion held in the Trust’s unallocated Bullion account and any Authorized Participant’s unallocated Bullion account is not segregated from the Custodian’s assets....” This contrasts with most other financial products that gain exposure to Bullion through the use of derivatives that are subject to counterparty and credit risks.

Investing in the Shares does not insulate the investor from certain risks, including price volatility. See “Risk Factors.”

2

Overview of the Bullion Industry

Introduction

This section provides a brief introduction to the gold, silver, platinum and palladium industries by looking at some of the key participants, detailing the primary sources of demand and supply and, with respect to the gold and silver industries, outlining the role of the “official” sector (i.e., central banks) in the markets.

In this annual report, the term “ounces” refers to fine troy ounces (with respect to gold only) and troy ounces (with respect to silver, platinum and palladium).

The Gold Industry

Market Participants

The participants in the world gold market may be classified in the following sectors: the mining and producer sector, the banking sector, the official sector, the investment sector, and the manufacturing sector. A brief description of each follows.

Mining and Producer Sector

This group includes mining companies that specialize in gold and silver production, mining companies that produce gold as a by-product of other production (such as a copper or silver producer), scrap merchants and recyclers.

Banking Sector

Gold bullion banks provide a variety of services to the gold market and its participants, thereby facilitating interactions between other parties. Services provided by the gold bullion banking community include traditional banking products as well as mine financing, physical gold purchases and sales, hedging and risk management, inventory management for industrial users and consumers, and gold deposit and loan instruments.

The Official Sector

The official sector encompasses the activities of the various central banking operations of gold-holding countries. According to statistics released by the World Gold Council, central banks are estimated to hold approximately 33,000 tonnes (when used in this annual report “tonne” refers to one metric tonne, which is equivalent to 1,000 kilograms or 32,151 troy ounces) of gold reserves, or approximately 20% of existing above-ground stocks. Since September 2009, the European Central Bank and 18 other central banks have operated under the Central Bank Gold Agreement (“CBGA”). The CBGA maintains a cap on lending and derivatives activities and allows a maximum level of sales of 400 tonnes per year, with an overall total of no more than 2,000 tonnes permitted during the five-year life of the CBGA.

The Investment Sector

This sector includes the investment and trading activities of both professional & private investors and speculators. These participants range from large hedge and mutual funds to day-traders on futures exchanges, and retail-level coin collectors.

The Manufacturing Sector

The fabrication and manufacturing sector represents all the commercial and industrial users of gold for whom gold is a daily part of their business. The jewelry industry is a large user of gold. Other industrial users of gold include the electronics and dental industries.

3

World Gold Supply and Demand 2007-2016

The following table sets forth a summary of the world gold supply and demand for the period from 2007 to 2016 and is based on information reported by GFMS Ltd.

|

|

||||||||||

|

(tonnes) |

2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|

Supply |

||||||||||

|

Mine production |

2,538 | 2,467 | 2,651 | 2,775 | 2,868 | 2,883 | 3,077 | 3,172 | 3,209 | 3,222 |

|

Scrap |

1,029 | 1,388 | 1,765 | 1,743 | 1,704 | 1,700 | 1,303 | 1,158 | 1,172 | 1,268 |

|

Net Hedging Supply |

(432) | (357) | (234) | (106) | 18 | (40) | (39) | 108 | 21 | 21 |

|

Total Supply |

3,135 | 3,498 | 4,182 | 4,412 | 4,590 | 4,543 | 4,341 | 4,438 | 4,402 | 4,511 |

|

|

||||||||||

|

Demand |

||||||||||

|

Jewelry Fabrication |

2,474 | 2,355 | 1,866 | 2,083 | 2,091 | 2,061 | 2,610 | 2,469 | 2,395 | 1,891 |

|

Industrial Fabrication |

492 | 479 | 426 | 480 | 471 | 429 | 421 | 403 | 365 | 354 |

|

Electronics |

345 | 334 | 295 | 346 | 343 | 307 | 300 | 290 | 258 | 254 |

|

Dental & Medical |

58 | 56 | 53 | 48 | 43 | 39 | 36 | 34 | 32 | 30 |

|

Other Industrial |

89 | 89 | 78 | 86 | 85 | 83 | 85 | 79 | 75 | 70 |

|

Net Official Sector |

(484) | (235) | (34) | 77 | 457 | 544 | 409 | 466 | 436 | 257 |

|

Retail Investment |

448 | 937 | 866 | 1,263 | 1,616 | 1,407 | 1,873 | 1,163 | 1,162 | 1,057 |

|

Bars |

238 | 667 | 562 | 946 | 1,247 | 1,056 | 1,444 | 886 | 876 | 787 |

|

Coins |

210 | 270 | 304 | 317 | 369 | 351 | 429 | 277 | 286 | 270 |

|

Physical Demand |

2,930 | 3,536 | 3,124 | 3,903 | 4,635 | 4,441 | 5,313 | 4,501 | 4,358 | 3559 |

|

|

||||||||||

|

Physical Surplus/Deficit |

205 | (38) | 1,058 | 509 | (45) | 102 | (972) | (63) | 44 | 952 |

|

|

||||||||||

|

ETF Inventory Build |

253 | 321 | 623 | 382 | 185 | 279 | (880) | (155) | (125) | 524 |

|

Exchange Inventory Build |

(10) | 34 | 39 | 54 | (6) | (10) | (98) | 1 | (48) | 86 |

|

Net Balance |

(38) | (393) | 396 | 73 | (224) | (167) | 6 | 91 | 217 | 342 |

|

|

||||||||||

|

Source: GFMS |

The following are some of the main characteristics of the gold market illustrated by the table:

One factor which separates gold from other precious metals is that there are large above-ground stocks which can be quickly mobilized. As a result of gold’s liquidity, gold often acts more like a currency than a commodity.

Over the past ten years, (new) mine production of gold has experienced a modest rise of about 2.8% per annum, increasing 2% in 2015. Of the three sources of supply, mine production accounts for nearly 71% of total supply in 2016. Recycled gold volumes have ranged from 1,029 tonnes to 1,765 tonnes over the past 10 years.

On the demand side, jewelry is clearly the greatest source of demand however jewelry’s contribution to demand has fallen from 84% in 2007 to 53% of demand in 2016. Industrial demand has been relatively constant, contributing between 8% to 17% of total demand.

Exchange traded product inventory build had seen strong growth until 2009, more than doubling between 2006 and 2009, before tapering and eventually seeing outflows between 2013 and 2015 as the price of gold fell by 36% in that time frame. Gold ETF inventory build resumed strong growth in 2016. During the 2013 price crash, retail coin and bar demand rose to a 10-year high as retail investors, especially from China, were enticed by the falling prices. ETP inventory resumed building in 2016 after three continuous years of outflows.

4

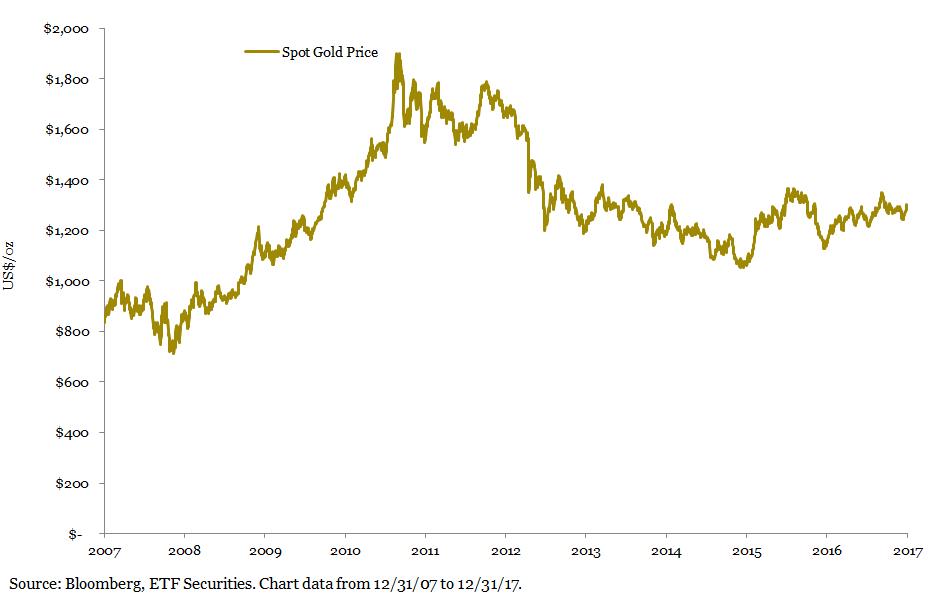

Historical Chart of the Price of Gold

The price of gold is volatile and fluctuations are expected to have a direct impact on the value of the Shares. However, movements in the price of gold in the past are not a reliable indicator of future movements. Movements may be influenced by various factors, including announcements from central banks regarding a country’s reserve gold holdings, agreements among central banks, political uncertainties around the world, and economic concerns.

The following chart illustrates the movements in the price of an ounce of gold in U.S. Dollars from December 2007 to December 2017:

The gold price tends to rise during periods of low real interest rates and high monetary expansion, as they are often associated with currency debasement and systemic financial failures. The decline in the U.S. Dollar against other currencies, a surge in investment demand in commodities as an asset class generally, and the low level of forward selling by mining companies have all contributed to the increase in the gold price between 2004 and 2011. The gold price peaked at US$1,900 per ounce in September 2011 as successive Euro leader summits, bailouts and bond stability funds failed to staunch both sovereign debt and banking sector solvency concerns in Europe. 2016 proved to be a stellar year for gold rising 8.4%, ending 3 years of negative price returns. Additionally, the trends of 3 years of investor outflows in global ETFs and net negative investor sentiment in gold futures positioning reversed in 2016 and continued through 2017. Low real interest rates, tepid economic growth, and rising policy uncertainty were key tailwinds for gold that sparked a return of investor interest. Gold prices rose 13.1% in 2017 closing at $1,303 per troy ounce.

5

The Silver Industry

Market Participants.

The participants in the world silver market may be classified in the following sectors: the mining and producer sector, the banking sector, the official sector, the investment sector, and the manufacturing sector. A brief description of each follows.

Mining and Producer Sector.

This group includes mining companies that specialize in silver and silver production, mining companies that produce silver as a by-product of other production (such as a copper or gold producer), scrap merchants and recyclers.

Banking Sector.

Bullion banks provide a variety of services to the silver market and its participants, thereby facilitating interactions between other parties. Services provided by the bullion banking community include traditional banking products as well as mine financing, physical silver purchases and sales, hedging and risk management, inventory management for industrial users and consumers and silver leasing.

The Official Sector.

There are no official statistics published by the International Monetary Fund, Bank of International Settlements, or national banks on silver holdings by national governments. The main reason for this is that silver is generally not recognized as a reserve asset. Consequently, there are very limited silver stocks held by governments. According to GFMS Limited in World Silver Survey 2017, at the end of 2016, government-held silver bullion stocks total 89.1 million ounces.

The Investment Sector.

This sector includes the investment and trading activities of both professional and private investors and speculators. These participants range from large hedge and mutual funds to day-traders on futures exchanges, and retail-level coin collectors.

The Manufacturing Sector.

The fabrication and manufacturing sector represents all the commercial and industrial users of silver. Industrial applications comprise the largest use of silver. The jewelry and silverware sector is the second largest, followed by the photographic industry (although the latter has been declining over a number of years as a result of the spread of digital photography).

6

World Silver Supply and Demand 2007-2016

The following table sets forth a summary of the world silver supply and demand for the period from 2007 to 2016 and is based on information reported by the World Silver Survey 2017, published by Thomson Reuters GFMS.

|

|

||||||||||

|

(in millions of ounces) |

2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|

Supply |

||||||||||

|

Mine Production |

668 | 685 | 717 | 753 | 758 | 792 | 824 | 869 | 891 | 886 |

|

Net Government Sales |

43 | 31 | 16 | 44 | 12 | 7 | 8 |

- |

- |

- |

|

Scrap |

204 | 200 | 200 | 226 | 260 | 254 | 191 | 165 | 141 | 140 |

|

Net Hedging Supply |

(24) | (9) | (17) | 50 | 12 | (47) | (35) | 17 | 8 | (18) |

|

Total Supply |

891 | 907 | 916 | 1,074 | 1,043 | 1,006 | 988 | 1,051 | 1,040 | 1,007 |

|

|

||||||||||

|

Demand |

||||||||||

|

Jewelry |

182 | 178 | 177 | 190 | 192 | 187 | 222 | 228 | 228 | 207 |

|

Coins & Bars |

62 | 197 | 93 | 148 | 208 | 159 | 241 | 234 | 291 | 207 |

|

Silverware |

60 | 58 | 53 | 52 | 47 | 44 | 59 | 61 | 63 | 52 |

|

Industrial Fabrication |

646 | 642 | 528 | 634 | 661 | 600 | 605 | 596 | 570 | 562 |

|

Electrical & Electronics |

263 | 272 | 227 | 301 | 291 | 267 | 266 | 263 | 246 | 234 |

|

Brazing Alloys & Solders |

59 | 62 | 54 | 61 | 63 | 61 | 64 | 67 | 62 | 55 |

|

Photography |

117 | 98 | 76 | 68 | 61 | 54 | 51 | 49 | 47 | 45 |

|

Photovoltaic |

- |

- |

- |

- |

76 | 58 | 56 | 52 | 57 | 77 |

|

Ethylene Oxide |

8 | 7 | 5 | 9 | 6 | 5 | 8 | 5 | 10 | 10 |

|

Other Industrial |

200 | 203 | 166 | 195 | 164 | 155 | 161 | 161 | 148 | 141 |

|

ETP Inventory Build |

55 | 101 | 157 | 130 | (24) | 55 | 3 | 2 | (18) | 47 |

|

Exchange Inventory Build |

22 | (7) | (15) | (7) | 12 | 62 | 9 | (5) | 13 | 80 |

|

Total Demand |

1,026 | 1,169 | 993 | 1,145 | 1,097 | 1,108 | 1,137 | 1,115 | 1,146 | 1,155 |

|

|

||||||||||

|

Net Balance |

(135) | (262) | (77) | (71) | (54) | (102) | (149) | (64) | (107) | (148) |

|

|

||||||||||

|

Source: World Silver Survey 2017 |

The following are some of the main characteristics of the silver market illustrated by the table:

Like gold, silver has also been used as a currency in the past. However, the main differences between gold and silver is that 53% of gold is used for jewelry and 49% of silver fabrication demand is industrial uses.

New mine production accounts for approximately 88% of total silver supply. Recycled silver accounts for around 14% of total supply. Recycled silver totalled 140 million ounces in 2016, marking the fourth consecutive time recycling has fallen below 200 million ounces in 10 years. The total of producer hedging, government sales and implied “net disinvestment” has been in decline but together account for the balance of total supply.

Industrial applications and jewelry demand accounted for 67% of total demand in 2016. Photography has been taking a lower share of overall silver demand falling from 11% in 2007 to 4% in 2016, while all other industrial applications have remained in the range of 45% to 51% over the past 10 years. Jewelry and silverware have remained relatively constant at 230 to 290 million ounces per annum. Investment in coins and bars have grown more than three-fold in the past 10 years rising from 62 million ounces in 2007 to 207 million ounces in 2016.

7

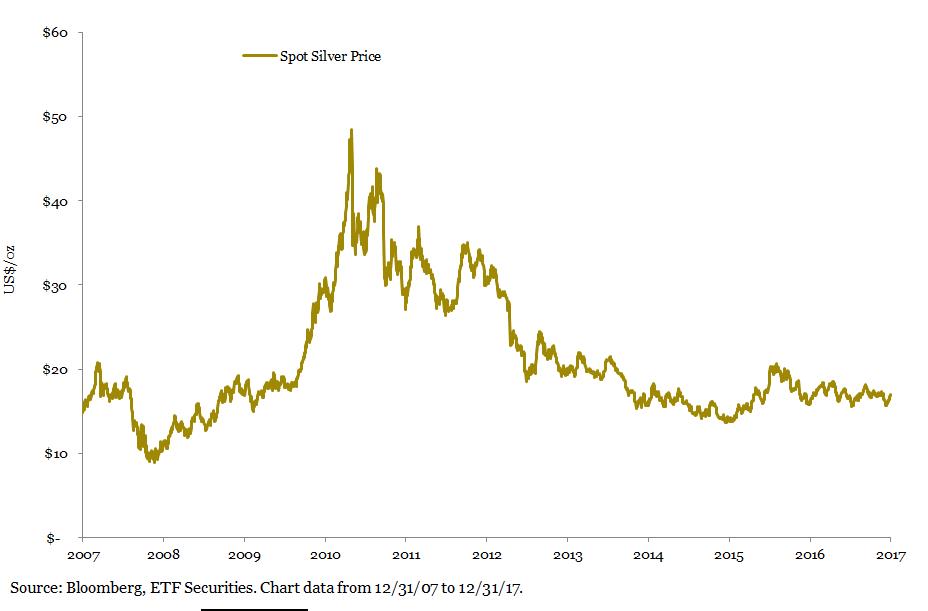

Historical chart of the price of Silver

The price of silver is volatile and fluctuations are expected to have a direct impact on the value of the Shares. However, movements in the price of silver in the past are not a reliable indicator of future movements. Movements may be influenced by various factors, including announcements from central banks regarding a country’s reserve silver holdings, agreements among central banks, political uncertainties around the world, and economic concerns. The following chart illustrates the movements in the price of an ounce of silver in dollars from December 2007 to December 2017 and is based on information provided by Bloomberg:

Between 2003 and 2011, the price of silver increased due to a number of factors. Among such factors are the decline in the U.S. Dollar against other currencies, a surge in investment demand in commodities as an asset class generally, strength in fabrication demand, and the low level of forward selling by mining companies. Since the global financial crisis that started in 2008, investors have increasingly been using silver as a store of value to counter the effects of an increase in paper money by major reserve currency central banks. However, since 2011, when prices peaked at $48.44 per ounce, prices have trended downwards, albeit with multiple upwards rallies (that have often lasted several months). The rise in the value of the U.S. Dollar, sluggish industrial growth and a tame inflation environment (which has led some investors to revise their expectations of the effects of monetary expansion) are some of the drivers behind the fall in silver prices since 2011. In 2017 silver prices rose 6.4%, closing at $16.90 per ounce, driven by its correlation to gold and rising global industrial activity.

Platinum Group Metals

Platinum and palladium are the two best known metals of the six platinum group metals (“PGMs”). Platinum and palladium have the greatest economic importance and are found in the largest quantities. The other four—iridium, rhodium, ruthenium and osmium—are produced only as co-products of platinum and palladium.

PGMs are found primarily in South Africa and Russia. South Africa is the world’s leading platinum producer and one of the largest palladium producers. Russia is the largest producer of palladium and most production is concentrated in the Norilsk region. All of South Africa’s production is sourced from the Bushveld Igneous Complex, which hosts the world’s largest resource of PGMs. Together, South Africa and Russia accounted for 77% of platinum and palladium mine supply in 2016.

8

Platinum

World Platinum Supply and Demand 2007-2016

The following table sets forth a summary of the world platinum supply and demand from 2007 to 2016 and is based on information reported by Johnson Matthey, Platinum 2017 Report.

|

|

||||||||||

|

(thousands of ounces) |

2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|

Supply |

||||||||||

|

South Africa |

5,070 | 4,515 | 4,635 | 4,635 | 4,860 | 4,110 | 4,208 | 3,547 | 4,571 | 4,392 |

|

Russia |

915 | 805 | 785 | 825 | 835 | 801 | 736 | 700 | 670 | 723 |

|

North America |

325 | 325 | 260 | 200 | 350 | 306 | 318 | 339 | 316 | 338 |

|

Zimbabwe |

170 | 180 | 230 | 280 | 340 | 337 | 410 | 401 | 401 | 489 |

|

Others |

120 | 115 | 115 | 110 | 100 | 126 | 163 | 156 | 151 | 161 |

|

Total Supply |

6,600 | 5,940 | 6,025 | 6,050 | 6,485 | 5,680 | 5,835 | 5,143 | 6,109 | 6,103 |

|

|

||||||||||

|

Demand by Application |

||||||||||

|

Autocatalyst |

4,145 | 3,655 | 2,185 | 3,075 | 3,185 | 3,158 | 3,000 | 3,103 | 3,264 | 3,318 |

|

Chemical |

420 | 400 | 290 | 440 | 470 | 452 | 528 | 523 | 539 | 545 |

|

Electrical |

255 | 230 | 190 | 230 | 230 | 176 | 218 | 225 | 229 | 235 |

|

Glass |

470 | 315 | 10 | 385 | 515 | 153 | 100 | 212 | 160 | 242 |

|

Investment |

170 | 555 | 660 | 655 | 460 | 450 | 871 | 277 | 451 | 620 |

|

Jewelry |

2,110 | 2,060 | 2,810 | 2,420 | 2,475 | 2,783 | 3,028 | 2,897 | 2,824 | 2,446 |

|

Medical & Biomedical |

230 | 245 | 250 | 230 | 230 | 223 | 214 | 214 | 215 | 217 |

|

Petroleum |

205 | 240 | 210 | 170 | 210 | 112 | 159 | 165 | 142 | 143 |

|

Other |

265 | 290 | 190 | 300 | 320 | 395 | 433 | 438 | 447 | 461 |

|

Total Gross Demand |

8,270 | 7,990 | 6,795 | 7,905 | 8,095 | 7,902 | 8,551 | 8,054 | 8,271 | 8,227 |

|

|

||||||||||

|

Recycling |

||||||||||

|

Autocatalyst |

(935) | (1,130) | (830) | (1,085) | (1,240) | (1,120) | (1,206) | (1,272) | (1,110) | (1,152) |

|

Electrical |

- |

(5) | (10) | (10) | (10) | (22) | (24) | (27) | (29) | (32) |

|

Jewellery |

(655) | (695) | (565) | (735) | (810) | (895) | (790) | (762) | (574) | (738) |

|

Total Recycling |

(1,590) | (1,830) | (1,405) | (1,830) | (2,060) | (2,037) | (2,020) | (2,061) | (1,713) | (1,922) |

|

|

||||||||||

|

Total Net Demand |

6,680 | 6,160 | 5,390 | 6,075 | 6,035 | 5,865 | 6,531 | 5,993 | 6,558 | 6,305 |

|

|

||||||||||

|

Movements in Stocks |

(80) | (220) | 635 | (25) | 450 | (185) | (696) | (850) | (449) | (202) |

|

|

||||||||||

|

Source: Johnson Matthey PGM Market Report 2017 |

The following are some of the main characteristics of the platinum market illustrated by the table:

The main supplier of platinum is South Africa, providing over 70% of total mine supply over the past five years. Russia is the second largest supplier of platinum. Its share of world mine production has averaged around 13% of total mine supply over the past ten years. Recovery of platinum from autocatalysts is the other main source of supply and provided around 14% of total supply in 2016. This source of supply increases along with autocatalyst production.

Over the past decade, jewelry demand for platinum peaked at 41% of total demand in 2009. Jewelry demand has since declined to 30% total demand in 2016. Autocatalyst demand for platinum accounted for around 40% of total demand at the end of 2016, at around its 5-year average. Investment demand accounted for 8% of the total in 2016, up from 5% in 2015.

9

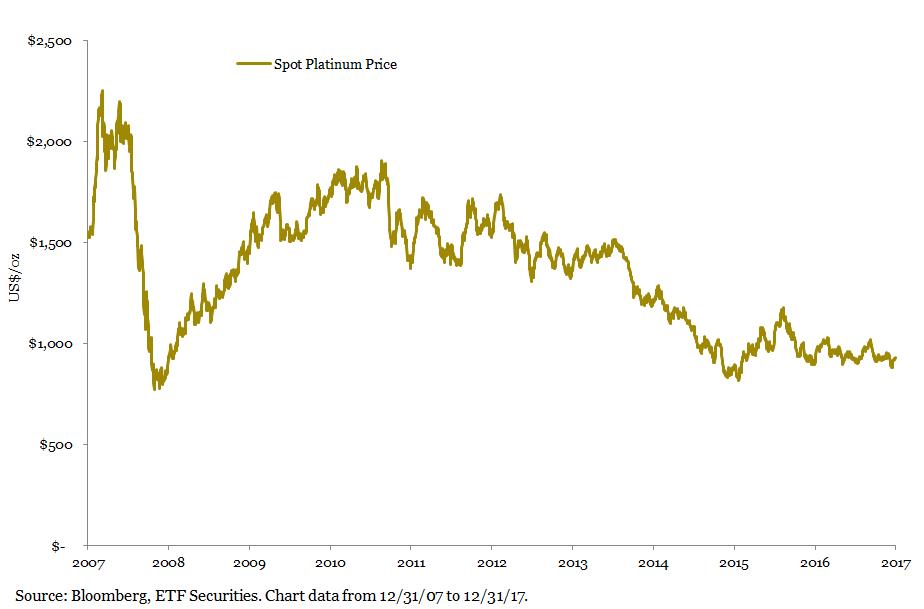

Historical Chart of the Price of Platinum

The price of platinum is volatile and fluctuations are expected to have a direct impact on the value of the Shares. However, movements in the price of platinum in the past are not a reliable indicator of future movements.

The following chart illustrates the movements in the price of an ounce of platinum in U.S. Dollars from December 2007 to December 2017 and is based on information provided by Bloomberg.

In the second half of 2008 platinum prices fell sharply (from a high of $2,276 per ounce in March to a low of $814 per ounce at the end of October 2008) as industrial demand collapsed on the back of the global financial crisis. Prices remained weak in the first few months of 2009 as industrial activity continued to slow. As global manufacturing started to turn up in early 2009, platinum prices began to rise. During this period, the prices of a wide range of commodities, equities and other cyclically-oriented assets also began to rebound strongly from the lows of late 2008/early 2009. As it became clear that auto sales in the US and China were rebounding on a sustainable basis, platinum and palladium continued to rise. By the end of 2009, platinum prices had risen to $1,416 per ounce, representing a 63% increase from the beginning of 2009 and 64% of the March 2008 high. The Japanese earthquake in early 2011, coupled with the unfolding of the European financial crisis with Portugal being bailed out, weighed on platinum performance in the second half of 2011. Platinum prices dropped by 26% in the six months to December 2011, from a high of $1,840 per troy ounce in June to a low of $1,369 per troy ounce in December 2011. Continued weakness in the European auto market weighed on platinum performance since then, with prices only partially recovering from 2011 lows. In 2012, platinum prices rose on the back of supply disruptions in South Africa, which accounts for over 70% of world’s supply of platinum. A strike at one of South Africa’s biggest platinum mines caused the price of platinum to rise from $1,387 to $1,709 per ounce in August 2012. At the beginning of 2013, Anglo American Platinum, the world’s biggest producer of the metal, announced its intention to close four mine shafts and its consideration of selling another mine complex as part of a radical overhaul of its South African operations. This statement prompted a strong reaction on platinum prices, which rose from $1,656 to $1,736 per ounce in the days following the announcement, on fears of a further tightening in platinum supply. However, platinum’s correlation to gold weighed on platinum prices in 2013 overall. Prolonged strikes at South African mines in 2014 led to the deepest supply deficit in platinum since 1975 (the earliest date we have supply and demand data). However, that failed to arrest the price slide which saw prices fall 11% in 2014, highlighting the extent of negative sentiment towards industrially-exposed precious metals. Despite autocatalyst demand for platinum increasing in 2015, tightening nitrogen oxide emission standards have led to pessimism about the future demand for platinum-heavy diesel autocatalysts relative to palladium-heavy gasoline autocatalysts. Further pessimistic outlook for South Africa’s economy and its currency the South African Rand weighed on platinum prices throughout 2017. This pessimism was exacerbated by the fraud at Volkswagen that affected mainly diesel cars. Platinum rose 3% in 2017 to $930.5 per ounce reaching a 2017 high of $1,030 per ounce in February 2017 and a low of $880 per ounce in December 2017.

10

Palladium

World Palladium Supply and Demand 2007-2016

The following table sets forth a summary of the world palladium supply and demand for the period from 2007 to 2016 and is based on information reported by Johnson Matthey, Palladium 2017 Report.

|

|

||||||||||

|

(thousands of ounces) |

2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|

Supply |

||||||||||

|

South Africa |

2,765 | 2,430 | 2,370 | 2,640 | 2,560 | 2,359 | 2,465 | 2,125 | 2,684 | 2,574 |

|

Russia |

||||||||||

|

Primary |

3,050 | 2,700 | 2,675 | 2,720 | 2,705 | 2,627 | 2,528 | 2,589 | 2,434 | 2,773 |

|

Stock Sales |

1,490 | 960 | 960 | 1,000 | 775 | 260 | 100 |

- |

- |

- |

|

North America |

990 | 910 | 755 | 590 | 900 | 811 | 831 | 912 | 874 | 894 |

|

Zimbabwe |

135 | 140 | 180 | 220 | 265 | 266 | 322 | 327 | 320 | 392 |

|

Others |

150 | 170 | 160 | 185 | 155 | 162 | 152 | 150 | 142 | 129 |

|

Total Supply |

8,580 | 7,310 | 7,100 | 7,355 | 7,360 | 6,485 | 6,398 | 6,103 | 6,454 | 6,762 |

|

|

||||||||||

|

Demand by Application |

||||||||||

|

Autocatalyst |

4,545 | 4,465 | 4,050 | 5,580 | 6,155 | 6,673 | 7,061 | 7,512 | 7,651 | 7,935 |

|

Chemical |

375 | 350 | 325 | 370 | 440 | 524 | 440 | 358 | 439 | 411 |

|

Dental |

630 | 625 | 635 | 595 | 540 | 510 | 457 | 468 | 475 | 427 |

|

Electrical |

1,550 | 1,370 | 1,370 | 1,410 | 1,375 | 1,190 | 1,070 | 1,014 | 960 | 953 |

|

Investment |

260 | 420 | 625 | 1,095 | (565) | 467 | (8) | 943 | (659) | (646) |

|

Jewelry |

950 | 985 | 775 | 595 | 505 | 442 | 354 | 272 | 223 | 189 |

|

Other |

85 | 75 | 70 | 90 | 110 | 104 | 109 | 111 | 133 | 147 |

|

Total Gross Demand |

8,395 | 8,290 | 7,850 | 9,735 | 8,560 | 9,910 | 9,483 | 10,678 | 9,222 | 9,416 |

|

|

||||||||||

|

Recycling |

||||||||||

|

Autocatalyst |

(1,015) | (1,140) | (965) | (1,310) | (1,695) | (1,675) | (1,905) | (2,158) | (1,891) | (1,990) |

|

Electrical |

(315) | (345) | (395) | (440) | (480) | (443) | (463) | (474) | (475) | (481) |

|

Jewelry |

(235) | (130) | (70) | (100) | (210) | (194) | (157) | (89) | (46) | (20) |

|

Total Recycling |

(1,565) | (1,615) | (1,430) | (1,850) | (2,385) | (2,312) | (2,525) | (2,721) | (2,412) | (2,491) |

|

|

||||||||||

|

Total Net Demand |

6,830 | 6,675 | 6,420 | 7,885 | 6,175 | 7,598 | 6,958 | 7,957 | 6,810 | 6,925 |

|

|

||||||||||

|

Movements in stocks |

1,750 | 635 | 680 | (530) | 1,185 | (1,113) | (560) | (1,854) | (356) | (163) |

|

|

||||||||||

|

Source: Johnson Matthey PGM Market Report 2017 |

The following are some of the main characteristics of the palladium market illustrated by the table:

Russia has traditionally been the largest producer of palladium, providing on average 46% of supply over the past 10 years. However its production has declined and sales of state held stock has dwindled down to zero. In 2016, Russia provided 41% of mine supplies while South Africa produced 38%. South Africa has on average supplied over 35% of production over the past 10 years. North America contributes approximately 12% of mine supply. Recovery of palladium has more than doubled over the past 11 years to account for 27% of overall supply at the end of 2016. Autocatalysts are the largest component of palladium demand, representing close to 84% of total demand in 2016. Palladium investment demand was negative in 2015 and 2016, giving back all of the investment demand in 2014. Jewelry demand for palladium contributed 2% of total demand in 2016, down from 4% in 2006. Other industrial demand (electronics, dentistry and chemical) has fallen from 31% of total demand in 2007 to 21% of total demand in 2016.

11

Historical Chart of the Price of Palladium

The price of palladium is volatile and fluctuations are expected to have a direct impact on the value of the Shares. However, movements in the price of palladium in the past are not a reliable indicator of future movements. The following chart illustrates the movements in the price of an ounce of palladium in U.S. Dollars from December 2007 to December 2017 and is based on information provided by Bloomberg:

Palladium prices fell sharply during the first phase of the global financial crisis, when prices dropped from $579 per ounce in February 2008 to $173 per ounce in October 2008. Prices then rallied almost five-fold until February 2011 to $841/oz, in line with other precious metals that gained favor as investors sought to diversify their assets away from paper currencies that they felt were being debased. Adding to demand for palladium, a number of countries had car scrappage programs, as part of their expenditure programs to counter the recession and to encourage people to replace their old vehicles with newer more environmentally-friendly ones. The rise in Chinese demand for cars and autocatalysts has also provided support for palladium demand in addition to increasing emission controls. Palladium prices have tempered since 2011, but concerns over supply shortages due to labor problems at mines in South Africa and dwindling Russian stocks have provided some price support since mid-2012. Palladium rose to a 13 year high of $907 per ounce in September 2014, a 27% increase from the start of the year. The rally was driven by supply side concerns following the longest strike in South African mining history and escalating tensions between Russia and Ukraine. The strong rally in 2014 was completely unwound in 2015, when South African mine supply resumed back to pre-strike levels and pessimism about industrial demand in China overwhelmed the true tightness in the market. Palladium was the top performer of the precious metals complex through the close of 2017 as it rose 56% this year ending at $1,064 per ounce. Given palladium’s demand is most sensitive to the industrial production cycle palladium may see further support along with industrial metals in anticipation of a rise in US infrastructure spending and recovery in global growth. Expected continued supply deficits, growing demand, and drawdowns in above ground stocks have kept the market balance for palladium favorable.

12

Operation of the Bullion Markets

The global trade in Bullion consists of Over-the-Counter (“OTC”) transactions in spot, forwards, and options and other derivatives, together with exchange-traded futures and options.

Global Over-The-Counter Market

The OTC market trades on a 24-hour per day continuous basis and accounts for most global Bullion trading.

Market makers, as well as others in the OTC market, trade with each other and with their clients on a principal-to-principal basis. All risks and issues of credit are between the parties directly involved in the transaction.

For gold and silver, market makers include the market-making members of the London Bullion Market Association (“LBMA”), the trade association that acts as the coordinator for activities conducted on behalf of its members and other participants in the London bullion market. The thirteen market-making members of the LBMA are: BNP Paribas SA, Citibank N.A. (through its London Branch), HSBC Bank USA, N.A. (London Branch), Goldman Sachs International, ICBC Standard Bank, JPMorgan Chase Bank, The Bank of Nova Scotia-ScotiaMocatta, Société Générale, Merrill Lynch International Bank Limited, Morgan Stanley & Co. International plc, Standard Chartered Bank, Toronto-Dominion Bank and UBS AG.

For platinum and palladium, five market-making members of the London Platinum and Palladium Market (“LPPM”), the trade association that acts as the coordinator for activities conducted on behalf of its members and other participants in the LPPM, are currently participating in the London Metal Exchange Fix (“LME Fix”). The OTC market provides a relatively flexible market in terms of quotes, price, size, destinations for delivery and other factors. Bullion dealers customize transactions to meet clients’ requirements. The OTC market has no formal structure and no open-outcry meeting place.

The main centers of the OTC market are London, Zurich and New York for gold and silver and London, New York, Hong Kong and Zurich for platinum and palladium. Mining companies, central banks, manufacturers of jewelry and industrial products, together with investors and speculators, tend to transact their business through one of these market centers. Centers such as Dubai and several cities in the Far East also transact substantial OTC market business, typically involving jewelry and small bars of gold or silver and small plates or ingots of platinum or palladium (1 kilogram or less) and will hedge their exposure by selling into one of these main OTC centers. Precious metals dealers have offices around the world and most of the world’s major bullion dealers are either members or associate members of the LBMA and/or the LPPM.

In the OTC market for gold, the standard size of trades between market makers ranges between 5,000 and 10,000 ounces. Bid-offer spreads are typically 50 US cents per ounce. Certain dealers are willing to offer clients competitive prices for much larger volumes, including trades over 100,000 ounces, although this will vary according to the dealer, the client and market conditions, as transaction costs in the OTC market are negotiable between the parties and therefore vary widely. Cost indicators can be obtained from various information service providers as well as dealers.

In the OTC market for silver, the standard size of trades between market makers is 100,000 ounces.

In the OTC market for platinum and palladium, the standard size of trades between market makers is 1,000 ounces.

Liquidity in the OTC market can vary from time to time during the course of the 24-hour trading day. Fluctuations in liquidity are reflected in adjustments to dealing spreads—the differential between a dealer’s “buy” and “sell” prices. The period of greatest liquidity in the Bullion markets generally occurs at the time of day when trading in the European time zones overlaps with trading in the United States, which is when OTC market trading in London, New York, Zurich and other centers coincides with futures and options trading on the Commodity Exchange, Inc. (“COMEX”), a designated contract market within the CME Group. This period lasts for approximately four hours each New York business day morning.

13

The Gold Bullion Market

The London Gold Bullion Market

Although the market for physical gold is distributed globally, most OTC market trades are cleared through London. In addition to coordinating market activities, the LBMA acts as the principal point of contact between the market and its regulators. A primary function of the LBMA is its involvement in the promotion of refining standards by maintenance of the “London Good Delivery Lists,” which are the lists of LBMA accredited melters and assayers of gold. The LBMA also coordinates market clearing and vaulting, promotes good trading practices and develops standard documentation.

The terms “loco London” gold and “loco Zurich” gold refer to gold physically held in London and Zurich, respectively, that meets the specifications for weight, dimensions, fineness (or purity), identifying marks (including the assay stamp of a LBMA acceptable refiner) and appearance set forth in “The Good Delivery Rules for Gold and Silver Bars” published by the LBMA. Gold bars meeting these requirements are described in this prospectus from time to time as “London Good Delivery Bars.” The unit of trade in London is the troy ounce, whose gram conversion is: 1,000 grams equals 32.1507465 troy ounces and 1 troy ounce equals 31.1034768 grams. A London Good Delivery bar is acceptable for delivery in settlement of a transaction on the OTC market. Typically referred to as 400-ounce bars, a London Good Delivery bar must contain between 350 and 430 fine troy ounces of gold, with a minimum fineness (or purity) of 995 parts per 1,000 (99.5%), be of good appearance and be easy to handle and stack. The fine gold content of a gold bar is calculated by multiplying the gross weight of the bar (expressed in units of 0.025 troy ounces) by the fineness of the bar. A London Good Delivery bar must also bear the stamp of one of the melters and assayers who are on the LBMA approved list. Unless otherwise specified, the gold spot price always refers to that of a London Good Delivery bar. Business is generally conducted over the phone and through electronic dealing systems.

On March 20, 2015, ICE Benchmark Administration (“IBA”) began administering the operation of an “equilibrium auction,” which is an electronic, tradable and auditable, over-the-counter auction market with the ability to settle trades in US Dollars (“USD”), euros or British Pounds for LBMA-authorized participating gold bullion banks or market makers (“gold participants”) that establishes a reference gold price for that day’s trading. IBA’s equilibrium auction is the gold valuation replacement selected by the LBMA for the London gold fix previously determined by the London Gold Market Fixing Ltd. that was discontinued on March 19, 2015. IBA’s equilibrium auction, like the previous gold fixing process, establishes and publishes fixed prices for troy ounces of gold twice each London trading day during fixing sessions beginning at 10:30 a.m. London time (the LBMA AM Gold Price) and 3:00 p.m. London time (the LBMA PM Gold Price).

Daily during London trading hours the LBMA AM Gold Price and the LBMA PM Gold Price each provide reference gold prices for that day’s trading. Many long-term contracts will be priced either on the basis of the LBMA AM Gold Price or the LBMA PM Gold Price, and market participants will usually refer to one or the other of these prices when looking for a basis for valuations. The LBMA AM Gold Price and the LBMA PM Gold Price, determined according to the methodologies of IBA and disseminated electronically by IBA to selected major market data vendors, such as Thomson Reuters and Bloomberg, are widely used benchmarks for daily gold prices and are quoted by various financial information sources as the London gold fix was previously. The Trust values its gold on the basis of the LBMA PM Gold Price.

The LBMA PM Gold Price is the result of an “equilibrium auction” because it establishes a price for a troy ounce of gold that will clear the maximum amount of bids and offers for gold entered by order-submitting gold participants each day. The opening bid and subsequent bid prices are generated by an algorithm based method, and each auction is actively supervised by IBA staff. There are currently twelve gold participants Bank of China, Bank of Communications, Goldman Sachs International, HSBC Bank USA NA, ICBC Standard Bank, INTL FCStone, Jane Street Global Trading LLC, JP Morgan Chase Bank NA, Koch Supply and Trading LP, Morgan Stanley, The Bank of Nova Scottia – Scotia Mocatta and the Toronto Dominon Bank), and IBA uses ICE’s front-end system, WebICE, as the technology platform that allows direct participants as well as sponsored clients to manage their orders in the auction in real time via their own screens.

The IBA auction process begins with a notice of an auction round issued to gold participants before the commencement of the auction round stating a gold price in U.S. Dollars, at which the auction round will be conducted. An auction round lasts 30 seconds. Gold participants electronically place bid and offer orders at the round’s stated price and indicate whether the orders are for their own account or for the account of clients. Aggregate bid and offer volume will be shown live on WebICE, providing a level playing field for all participants.

14

At the end of the auction round, the IBA system evaluates the equilibrium of the bid and offer orders submitted. If bid and offer orders indicate an imbalance outside of acceptable tolerances established for the IBA system (normally 10,000 oz) (e.g., too many purchase orders submitted compared to sell orders or vice versa), the auction chairman calculates a new auction round price is calculated principally based on the volume weighting of bid and offer orders submitted in the immediately completed auction round. For instance, if the order imbalance indicates that purchase orders (bids) outweigh sales orders (offers) then a new auction round price will be issued that will be increased over that used in the prior auction round. Likewise, the new auction round price will be decreased from the prior round’s price if offers outweigh bids. To clear the imbalance, the IBA system then issues another notice of auction round to gold participants at the newly calculated price. During this next 30 second auction round, gold participants again submit orders, and after it ends, the IBA system evaluates for order imbalances. If order imbalances persist, a new auction price will be calculated and a further auction round will occur. This auction round process continues until an equilibrium within specified tolerances is determined to exist. Once the IBA system determines that orders are in equilibrium within system tolerances, the auction process ends and the equilibrium auction round price becomes the LBMA PM Gold Price.

The LBMA PM Gold Price and all bid and offer order information for all auction rounds become publicly available electronically via IBA instantly after the conclusion of the equilibrium auction. Since April 1, 2015, the LBMA Gold Price has been regulated by the Financial Conduct Authority (“FCA”) in the United Kingdom (“UK”). IBA also has an Oversight Committee, made up of market participants, industry bodies, direct participant representatives, infrastructure providers and IBA. The Oversight Committee allows the LBMA to continue to have significant involvement in the oversight of the auction process, including, among other matters, changes to the methodology and accreditation of direct participants. Additionally, IBA watches over the price discovery process for the LBMA Gold Price and ensures that it meets the International Organization of Securities Commissions’ (IOSCO) Principles for Financial Benchmarks.

The LBMA PM Gold Price is widely viewed as a full and fair representation of all or material market interest at the conclusion of the equilibrium auction. IBA’s LBMA PM Gold Price electronic auction methodology is similar to the non-electronic process previously used to establish the London gold fix where the London gold fix process adjusted the gold price up or down until all the buy and sell orders are matched, at which time the price was declared fixed. Nevertheless, the LBMA PM Gold Price has several advantages over the previous London gold fix. The LBMA PM Gold Price auction process is fully transparent in real time to the gold participants and, at the close of each equilibrium auction, to the general public. The LBMA PM Gold Price auction process is also fully auditable by third parties since an audit trail exists from the time of each notice of an auction round. Moreover, the LBMA PM Gold Price’s audit trail and active, real time surveillance of the auction process by IBA as well as FCA’s oversight of IBA, will deter manipulative and abusive conduct in establishing each day’s LBMA PM Gold Price.

Since March 20, 2015, the Sponsor determined that the London gold fix, which ceased to be published as of March 19, 2015, could no longer serve as a basis for valuing gold bullion received upon purchase of the Trust’s Shares, delivered upon redemption of the Trust’s Shares and otherwise held by the Trust on a daily basis, and that the LBMA PM Gold Price is an appropriate alternative for determining the value of the Trust’s gold each trading day. The Sponsor also determined that the LBMA PM Gold Price fairly represents the commercial value of gold bullion held by the Trust and the “Benchmark Price" (as defined in the Trust Agreement) as of any day will be the LBMA PM Gold Price for such day.

The Zurich Gold Bullion Market

After London, the second principal center for spot or physical gold trading is Zurich. For eight hours a day, trading occurs simultaneously in London and Zurich—with Zurich normally opening and closing an hour earlier than London. During these hours, Zurich closely rivals London in its influence over the spot price because of the importance of the three major Swiss banks—Credit Suisse, Swiss Bank Corporation, and Union Bank of Switzerland (UBS)—in the physical gold market. Each of these banks has long maintained its own refinery, often taking physical delivery of gold and processing it for other regional markets. The loco Zurich bullion specification is the same as for the London bullion market, which allows for gold physically located in Zurich to be quoted loco London and vice versa.

Futures Exchanges

The most significant gold futures exchanges are the COMEX and the Tokyo Commodity Exchange (“TOCOM”). The COMEX is the largest exchange in the world for trading precious metals futures and options and has been trading gold since 1974. The TOCOM has been trading gold since 1982. Trading on these exchanges is based on fixed delivery dates and transaction sizes for the futures and options contracts traded. Trading costs are negotiable. As a matter of practice, only a small percentage of the futures market turnover ever comes to physical delivery of the gold represented by the contracts traded. Both exchanges permit trading on margin. Margin trading can add to the speculative risk involved given the potential for margin calls if the price moves against the contract holder. The COMEX trades gold futures almost continuously (with one short break in the evening) through its CME Globex electronic trading system and clears through its central clearing system. On June 6, 2003, the TOCOM adopted a similar clearance system. In each case, the exchange acts as a counterparty for each member for clearing purposes.

15

Other Exchanges

There are other gold exchange markets, such as the Istanbul Gold Exchange (trading gold since 1995), the Shanghai Gold Exchange (trading gold since 2002), the Hong Kong Chinese Gold & Silver Exchange Society (trading gold since 1918) and the Singapore Mercantile Exchange (trading gold since 2010).

The Silver Market

The London Silver Bullion Market

Although the market for physical silver is distributed globally, most OTC market trades are cleared through London. In addition to coordinating market activities, the LBMA acts as the principal point of contact between the market and its regulators. A primary function of the LBMA is its involvement in the promotion of refining standards by maintenance of the “London Good Delivery Lists,” which are the lists of LBMA accredited melters and assayers of silver. The LBMA also coordinates market clearing and vaulting, promotes good trading practices and develops standard documentation.

The term “loco London” silver refers to silver physically held in London that meets the specifications for weight, dimensions, fineness (or purity), identifying marks (including the assay stamp of a LBMA acceptable refiner) and appearance set forth in “The Good Delivery Rules for Gold and Silver Bars” published by the LBMA. Silver bars meeting these requirements are described in this prospectus from time to time as “Silver Good Delivery Bars.” The unit of trade in London is the troy ounce, whose conversion between grams is: 1,000 grams equals 32.1507465 troy ounces and 1 troy ounce equals 31.1034768 grams. A Silver Good Delivery Bar is acceptable for delivery in settlement of a transaction on the OTC market. A Silver Good Delivery Bar must contain between 750 troy ounces and 1,100 troy ounces of silver with a minimum fineness (or purity) of 999.0 parts per 1,000. A Silver Good Delivery Bar must also bear the stamp of one of the refiners who are on the LBMA-approved list. Unless otherwise specified, the silver spot price always refers to that of a Silver Good Delivery Bar. Business is generally conducted over the phone and through electronic dealing systems.

On July 14, 2017, the LBMA announced that IBA had been selected to be the third-party administrator for the “LBMA Silver Price”. Effective as of October 2, 2017 IBA provides the auction platform and methodology as well as the overall administration and governance for the LBMA Silver Price benchmark. IBA operates an “equilibrium auction”, which is an electronic, tradable and auditable, over-the-counter auction for LBMA-authorized participating silver bullion banks or market makers and sponsored clients of direct participants (“silver participants”) that establishes a reference silver price for that day’s trading, often referred to as the “LBMA Silver Price”. The LBMA Silver Price equilibrium auction operated by CME Group Inc. and Thomson Reuters prior to October 2, 2017 was selected by the LBMA as the silver valuation replacement for the London silver fix previously determined by the London Silver Market Fixing Ltd. that was discontinued on August 14, 2014. The LBMA Silver Price has become a widely used benchmark for daily silver prices and is quoted by various financial information sources as the London silver fix was previously.

The LBMA Silver Price is the result of an “equilibrium auction” because it establishes a price for a troy ounce of Silver Good Delivery Bars that will clear the maximum amount of bids and offers for silver entered by order-submitting silver participants each day. IBA will use ICE’s front-end system, WebICE, as the technology platform that will allow direct participants, as well as sponsored clients of direct participants, to manage their orders in the auction in real time via their own desktops. As the IBA electronic silver auction market develops, IBA expects to admit additional silver participants to the order submission process. The benchmark is published when the auction finishes, typically a few minutes after 12:00 noon (London time).

At the opening of each auction, IBA in the role of auction chairman (“Chairman”) will announce an opening price (in U.S. Dollars), that takes into account current market conditions and begin auction rounds, with an expected duration of at least every 30 seconds each. During each auction round, participants may enter the volume they wish to buy or sell at that price, and such orders will be part of the price formation. Aggregate bid and offer volume will be shown live on WebICE. At the end of each auction round, the total net volume will be calculated. If this “imbalance” is larger than the imbalance tolerance (currently set at 500,000 oz.) then a new price will be set by the Chairman (based on the current market conditions, and the direction and magnitude of the imbalance in the round) and begin a new auction round. If the imbalance is less than the tolerance, then the auction is complete with all volume tradeable at that price. The price will then be set in U.S. Dollars and also converted into other currencies, including Australian Dollars, British Pounds, Canadian Dollars, Euros, Onshore and Offshore Yuan, Indian Rupees, Japanese Yen, Malaysian Ringgit, Russian Rubles, Singapore Dollars, South African Rand, Swiss Francs, New Taiwan Dollars, Thai Baht and Turkish Lira. The auction will be run at 12:00 noon (London time).

During the auction, the price at the start of each round, and the volumes at the end of each round will be available through major market data vendors. As soon as the auction finishes, the final prices and volumes will be available through major market data vendors. IBA will also publish transparency reports, detailing the prices, volumes and times for each round of the auction. These transparency reports will be available through major market data vendors and IBA when the auction finishes. The process can also be observed real-time through a WebICE screen. The auction mechanism will provide a complete audit trail.

16

As of August 1, 2017, there were seven direct participants in the LBMA Silver Price administered by CME Group and Thomson Reuters. As of February 14, 2018 there are nine direct participants participating in the auction process that determines the LBMA Silver Price.

Since April 1, 2015, the LBMA Silver Price has been regulated by the Financial Conduct Authority (“FCA”) in the UK.. IBA is already authorized as a regulated benchmark administrator by the FCA. Under the UK benchmark regulation, the governance structure for a regulated benchmark must include an Oversight Committee, made up of market participants, industry bodies, direct participant representatives, infrastructure providers and the administrator (i.e., IBA). Through the Oversight Committee the LBMA will continue to have significant involvement in the oversight of the auction process, including, among other matters, changes to the methodology and accreditation of direct participants. The price discovery process for the LBMA Silver Price will be subject to surveillance by IBA. IBA has been formally assessed against the IOSCO Principles. In order to meet the IOSCO Principles, the price discovery used for the LBMA Silver Price benchmark will be auditable and transparent.

The LBMA Silver Price is viewed as a full and fair representation of all market interest at the conclusion of the auction. IBA’s auction process is similar to CME Group’s auction process, which in turn was similar to the non-electronic process previously used to establish the London silver fix where the London silver fix process adjusted the silver price up or down until all the buy and sell orders are matched, at which time the price was declared fixed. Nevertheless, the LBMA Silver Price has several advantages over the previous London silver fix. IBA’s auction process will be fully transparent in real-time to direct participants and sponsored clients and, at the close of each auction, to the general public. IBA’s auction process also will be fully auditable since an audit trail exists for every change made in the process. Moreover, the audit trail and active surveillance of the auction process by IBA, as well as the FCA’s oversight of IBA, should deter manipulative and abusive conduct in establishing each day’s LBMA Silver Price.

Since August 15, 2014, the Sponsor determined that the London silver fix, which ceased to be published as of that date, would be an inappropriate basis for valuing silver bullion received upon purchase of the Trust’s Shares, delivered upon redemption of the Trust’s Shares and otherwise held by the Trust on a daily basis, and that the LBMA Silver Price is an appropriate alternative for determining the value of the Trust’s silver each trading day. The Sponsor also determined that the LBMA Silver Price will fairly represent the commercial value of silver bullion held by the Trust and that the “Benchmark Price” (as defined in the Trust Agreement) as of any day will be the LBMA Silver Price for such day.

Futures Exchanges

The most significant silver futures exchanges are the COMEX and the TOCOM. Futures exchanges seek to provide a neutral, regulated marketplace for the trading of derivatives contracts for commodities. Futures contracts are defined by the exchange for each commodity. For each commodity traded, this contract specifies the precise quality and quantity standards. The contract’s terms and conditions also define the location and timing of physical delivery.

An exchange does not buy or sell those contracts, but seeks to offer a transparent forum where members, on their own behalf or on the behalf of customers, can trade the contracts in a safe, efficient and orderly manner. During regular trading hours at the COMEX, the commodity contracts are traded on CME Globex system, an electronic; a verbal auction in which all bids, offers and trades must be publicly announced to all members and, upon execution, centrally cleared. Electronic trading is offered by the exchange almost 24 hours a day (except for a short break in the evening), six days a week.

In addition to the public nature of the pricing, futures exchanges in the United States are regulated at two levels: internal and external governmental supervision. The internal is performed through self-regulation and consists of regular monitoring of the following: the open-outcry process to ensure that it is conducted in conformance with all exchange rules; the financial condition of all exchange member firms to ensure that they continuously meet financial commitments; and the positions of commercial and non-commercial customers to ensure that physical delivery and other commercial commitments can be met, and that pricing is not being improperly affected by the size of any particular customer positions. External governmental oversight is performed by the CFTC, which reviews all the rules and regulations of United States futures exchanges and monitors their enforcement.

The Platinum Market

The Zurich and London Platinum Bullion Market

Although the market for physical platinum is distributed globally, most platinum is stored and most OTC market trades are cleared through Zurich. As of September 1, 2009, London also serves as a center for the clearing of OTC trades in platinum. In addition to coordinating market activities, the LPPM acts as the principal point of contact between the market and its regulators. A primary function of the LPPM is its involvement in the promotion of refining standards by maintenance of the “London/Zurich Good Delivery Lists,” which are the lists of LPPM accredited melters and assayers of platinum. The LPPM also coordinates market clearing and vaulting, promotes good trading practices and develops standard documentation.

17

Platinum is traded generally on a “loco Zurich” basis, meaning the precious metal is physically held in vaults in Zurich or is transferred into accounts established in Zurich. As of September 1, 2009, platinum began trading on a “loco London” basis as well, meaning the precious metal is physically held in vaults in London or is transferred into accounts established in London. The basis for settlement and delivery of a loco Zurich spot trade is payment (generally in U.S. Dollars) two business days after the trade date against delivery. Delivery of the platinum can either be by physical delivery or through the clearing systems to an unallocated account.

The unit of trade in London and Zurich is the troy ounce, whose conversion between grams is: 1,000 grams is equivalent to 32.1507465 troy ounces, and one troy ounce is equivalent to 31.1034768 grams. A good delivery platinum plate or ingot is acceptable for delivery in settlement of a transaction on the OTC market (a “Good Delivery Platinum Plate or Ingot”). A Good Delivery Platinum Plate or Ingot must contain between 32 and 192 troy ounces of platinum with a minimum fineness (or purity) of 999.5 parts per 1,000 (99.95%), be of good appearance, and be easy to handle and stack. The platinum content of a platinum Good Delivery Platinum Plate or Ingot is calculated by multiplying the gross weight by the fineness of the plate or ingot. A Good Delivery Platinum Plate or Ingot must also bear the stamp of one of the melters and assayers who are on the LPPM approved list. Unless otherwise specified, the platinum spot price always refers to the “Good Delivery Standards” set by the LPPM. Business is generally conducted over the phone and through electronic dealing systems.

Since December 1, 2014, the London Metal Exchange (“LME”) has been administering the operation of an electronic platinum bullion price fixing systems (“LMEbullion”) that replicates electronically the manual London platinum fix processes previously employed by the London Platinum and Palladium Fixing Company Ltd (“LPPFCL”) as well as providing electronic market clearing processes for platinum bullion transactions at the fixed prices established by the LME pricing mechanism. The LME’s electronic price fixing processes, like the previous London platinum fix processes, establishes and publishes fixed prices for troy ounces of platinum twice each London trading day during fixing sessions beginning at 9:45 a.m. London time (the “LME AM Fix”) and 2:00 p.m. London time (the “LME PM Fix”). In addition to utilizing the same London platinum fix standards and methods, the LME also supervises the platinum electronic price fixing processes through its market operations, compliance, internal audit and third-party complaint handling capabilities in order to support the integrity of the LME PM Fix. The LME, in administering LMEbullion, uses a pricing methodology that meets the administrative and regulatory needs of platinum market participants, including the International Organization of Securities Commissions’ (IOSCO) Principles for Financial Benchmarks.

Daily during London trading hours the LME AM Fix and the LME PM Fix each provide reference platinum prices for that day’s trading. Many long-term contracts are priced on the basis of either the LME AM Fix or the LME PM Fix, and market participants usually refer to one or the other of these prices when looking for a basis for valuations. The LME AM Fix and the LME PM Fix are viewed as a full and fair representation of all market interest at the conclusion of the electronic price fixing process. The Trust values its platinum on the basis of the LME PM Fix.

The LME PM Fix results from LMEbullion. Formal participation in the LME PM Fix is limited to participating LPPM members, each of which is a bullion dealer. Five LPPM members are currently participating in establishing the LME PM Fix (BASF Metals Limited, Goldman Sachs International, HSBC Bank USA NA, Johnson Matthey plc and ICBC Standard Bank plc). Any other market participant wishing to participate in the trading on the LME PM Fix is required to do so through one of the participating LPPM members.

18

Orders are placed either with one of the participating LPPM members or with another precious metals dealer who will then be in contact with a participating LPPM member during the fixing. The fixing members net-off all orders when communicating their net interest at the fixing. The fix begins with the LMEbullion system suggesting a “trying price,” reflecting the market price prevailing at the opening of the fix. This is relayed by the fixing members to their dealing rooms which have direct communication with all interested parties. Any market participant may enter the fixing process at any time, or adjust or withdraw his order. The platinum price is adjusted up or down until all the buy and sell orders are electronically matched, at which time the price is declared fixed. All fixing orders are transacted on the basis of this fixed price, which is instantly relayed to the market through various media.

The LPPFCL, LBMA and the LME have asserted that the LME’s electronic price fixing processes are similar to the non‑electronic processes previously used to establish the applicable London platinum fix where the London platinum fix process adjusted the platinum price up or down until all the buy and sell orders entered by the participating LPPM members are matched, at which time the price was declared fixed. Nevertheless, the LME PM Fix has several advantages over the previous London platinum fix. The LME’s electronic price fixing processes are fully transparent. The LME asserts that its electronic price fixing processes also will be fully auditable by third parties since an audit trail exists from the beginning of each fixing session. The LME also asserts that the market operation, compliance, internal audit and third-party complaint handling capabilities of the LME will support the integrity of the LME PM Fix.