Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - CCO HOLDINGS LLC | ccoh12312017exh-322.htm |

| EX-32.1 - EXHIBIT 32.1 - CCO HOLDINGS LLC | ccoh12312017exh-321.htm |

| EX-31.2 - EXHIBIT 31.2 - CCO HOLDINGS LLC | ccoh12312017exh-312.htm |

| EX-31.1 - EXHIBIT 31.1 - CCO HOLDINGS LLC | ccoh12312017exh-311.htm |

| EX-12.1 - EXHIBIT 12.1 - CCO HOLDINGS LLC | ccoh12312017exh-121.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

FORM 10-K

______________

(Mark One) | ||

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2017 | ||

or | ||

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Transition Period From to

Commission File Number: | 001-37789 |

333-112593-01 | |

CCO Holdings, LLC

CCO Holdings Capital Corp.

(Exact name of registrant as specified in its charter)

Delaware | 86-1067239 | |

Delaware | 20-0257904 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

400 Atlantic Street Stamford, Connecticut 06901 | (203) 905-7801 | |

(Address of principal executive offices including zip code) | (Registrant’s telephone number, including area code) | |

Securities registered pursuant to section 12(b) of the Act: None

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrants have submitted electronically and posted on their corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrants were required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

Large accelerated filer o Accelerated filer o Non-accelerated filer x Smaller reporting company o

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

All of the issued and outstanding shares of capital stock of CCO Holdings Capital Corp. are held by CCO Holdings, LLC. All of the limited liability company membership interests of CCO Holdings, LLC are held by CCH I Holdings, LLC (a subsidiary of Charter Communications, Inc., a reporting company under the Exchange Act). There is no public trading market for any of the aforementioned limited liability company membership interests or shares of capital stock.

CCO Holdings, LLC and CCO Holdings Capital Corp. meet the conditions set forth in General Instruction I(1)(a) and (b) to Form 10-K and are therefore filing with the reduced disclosure format.

Number of shares of common stock of CCO Holdings Capital Corporation outstanding as of December 31, 2017: 1

Documents Incorporated By Reference: None

CCO HOLDINGS, LLC

CCO HOLDINGS CAPITAL CORP.

FORM 10-K — FOR THE YEAR ENDED DECEMBER 31, 2017

FORM 10-K — FOR THE YEAR ENDED DECEMBER 31, 2017

TABLE OF CONTENTS

Page No. | ||||

This annual report on Form 10-K is for the year ended December 31, 2017. The United States Securities and Exchange Commission (“SEC”) allows us to “incorporate by reference” information that we file with the SEC, which means that we can disclose important information to you by referring you directly to those documents. Information incorporated by reference is considered to be part of this annual report. In addition, information that we file with the SEC in the future will automatically update and supersede information contained in this annual report. In this annual report, “CCO Holdings,” “we,” “us” and “our” refer to CCO Holdings, LLC and its subsidiaries.

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS:

This annual report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), regarding, among other things, our plans, strategies and prospects, both business and financial including, without limitation, the forward-looking statements set forth in Part I. Item 1. under the heading “Business” and in Part II. Item 7. under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this annual report. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions, including, without limitation, the factors described in Part I. Item 1A. under “Risk Factors” and in Part II. Item 7. under the heading, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this annual report. Many of the forward-looking statements contained in this annual report may be identified by the use of forward‑looking words such as “believe,” “expect,” “anticipate,” “should,” “planned,” “will,” “may,” “intend,” “estimated,” “aim,” “on track,” “target,” “opportunity,” “tentative,” “positioning,” “designed,” “create,” “predict,” “project,” “initiatives,” “seek,” “would,” “could,” “continue,” “ongoing,” “upside,” “increases” and “potential,” among others. Important factors that could cause actual results to differ materially from the forward-looking statements we make in this annual report are set forth in this annual report and in other reports or documents that we file from time to time with the SEC, and include, but are not limited to:

•our ability to efficiently and effectively integrate acquired operations;

• | our ability to sustain and grow revenues and cash flow from operations by offering video, Internet, voice, mobile, advertising and other services to residential and commercial customers, to adequately meet the customer experience demands in our markets and to maintain and grow our customer base, particularly in the face of increasingly aggressive competition, the need for innovation and the related capital expenditures; |

• | the impact of competition from other market participants, including but not limited to incumbent telephone companies, direct broadcast satellite operators, wireless broadband and telephone providers, digital subscriber line (“DSL”) providers, fiber to the home providers, video provided over the Internet by (i) market participants that have not historically competed in the multichannel video business, (ii) traditional multichannel video distributors, and (iii) content providers that have historically licensed cable networks to multichannel video distributors, and providers of advertising over the Internet; |

• | general business conditions, economic uncertainty or downturn, unemployment levels and the level of activity in the housing sector; |

• | our ability to obtain programming at reasonable prices or to raise prices to offset, in whole or in part, the effects of higher programming costs (including retransmission consents); |

• | our ability to develop and deploy new products and technologies including mobile products, our cloud-based user interface, Spectrum Guide®, and downloadable security for set-top boxes, and any other cloud-based consumer services and service platforms; |

• | the effects of governmental regulation on our business including costs, disruptions and possible limitations on operating flexibility related to, and our ability to comply with, regulatory conditions applicable to us as a result of the Time Warner Cable Inc. and Bright House Networks, LLC Transactions; |

• | any events that disrupt our networks, information systems or properties and impair our operating activities or our reputation; |

• | the ability to retain and hire key personnel; |

• | the availability and access, in general, of funds to meet our debt obligations prior to or when they become due and to fund our operations and necessary capital expenditures, either through (i) cash on hand, (ii) free cash flow, or (iii) access to the capital or credit markets; and |

• | our ability to comply with all covenants in our indentures and credit facilities, any violation of which, if not cured in a timely manner, could trigger a default of our other obligations under cross-default provisions. |

All forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by this cautionary statement. We are under no duty or obligation to update any of the forward-looking statements after the date of this annual report.

ii

PART I

Item 1. Business.

Introduction

We are the second largest cable operator in the United States and a leading broadband communications services company providing video, Internet and voice services to approximately 27.2 million residential and business customers at December 31, 2017. In addition, we sell video and online advertising inventory to local, regional and national advertising customers and fiber-delivered communications and managed information technology (“IT”) solutions to large enterprise customers. We also own and operate regional sports networks and local sports, news and community channels and sell security and home management services in the residential marketplace.

CCO Holdings is a holding company whose principal assets are the equity interests in its operating subsidiaries. CCO Holdings is a direct subsidiary of CCH I Holdings, LLC, which is an indirect subsidiary of Charter Communications, Inc. (“Charter”), Charter Communications Holdings, LLC (“Charter Holdings”) and Spectrum Management Holding Company, LLC.

Our core strategy is to deliver high quality products at competitive prices, combined with outstanding service. This strategy, combined with simple, easy to understand pricing and packaging, is central to our goal of growing our customer base while also selling more services to each customer. We expect to execute this strategy by managing our operations in a consumer-friendly, efficient and cost-effective manner. Our operating strategy includes insourcing much of our customer care and field operations workforces, which results in higher quality service transactions. While an insourced operating model can increase field operations and customer care costs associated with each service transaction, the higher quality nature of insourced labor service transactions significantly reduces the volume of service transactions per customer, more than offsetting the higher investment made in each service transaction. As we reduce the number of service transactions and recurring costs per customer relationship, we effectively pass those savings on to our customers in the form of products and prices that we believe provide more value than what our competitors offer. The combination of offering competitively priced products and high quality service, allows us to increase the number of customers we serve over our fixed network and increase the number of products we sell to each customer, while at the same time reducing the number of service transactions per relationship, improving customer satisfaction and reducing churn, which results in lower costs to acquire and serve customers. We are also reducing our operating costs per customer relationship by providing customers with the ability to communicate with us through a variety of new forums that they may favor over telephonic communications. These forums include our customer website, mobile device applications, online chat and social media, which are less costly for us to provide than direct telephonic communications. Ultimately, our operating strategy enables us to offer high quality, competitively priced services profitably, while continuing to invest in new products and services.

Our principal executive offices are located at 400 Atlantic Street, Stamford, Connecticut 06901. Our telephone number is (203) 905-7800, and Charter has a website accessible at www.charter.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and all amendments thereto, are available on Charter's website free of charge as soon as reasonably practicable after they have been filed. The information posted on Charter's website is not incorporated into this annual report.

The Transactions

On May 18, 2016, the transactions contemplated by the Agreement and Plan of Mergers dated as of May 23, 2015 (the “Merger Agreement”), by and among Time Warner Cable Inc. ("Legacy TWC"), Charter Communications, Inc. prior to the closing of the Merger Agreement (“Legacy Charter”), CCH I, LLC, previously a wholly owned subsidiary of Legacy Charter and certain other subsidiaries of CCH I, LLC were completed (the “TWC Transaction,” and together with the Bright House Transaction described below, the “Transactions”). As a result of the TWC Transaction, CCH I, LLC became the new public parent company that holds the operations of the combined companies and was renamed Charter Communications, Inc.

Also, on May 18, 2016, Legacy Charter and Advance/Newhouse Partnership (“A/N”), the former parent of Bright House Networks, LLC (“Legacy Bright House”), completed their previously announced transaction, pursuant to a definitive Contribution Agreement (the “Contribution Agreement”), under which Charter acquired Legacy Bright House (the “Bright House Transaction”). Pursuant to the Bright House Transaction, Charter became the owner of the membership interests in Legacy Bright House and the other assets primarily related to Legacy Bright House (other than certain excluded assets and liabilities and non-operating cash).

In connection with the TWC Transaction, Legacy Charter and Liberty Broadband completed their previously announced transactions pursuant to their investment agreement, in which Liberty Broadband purchased shares of Charter Class A common

1

stock to partially finance the cash portion of the TWC Transaction consideration, and in connection with the Bright House Transaction, Liberty Broadband purchased shares of Charter Class A common stock (the "Liberty Transaction"). See Note 3 to the accompanying consolidated financial statements contained in “Part II. Item 8. Financial Statements and Supplementary Data,” for more information on the Transactions.

2

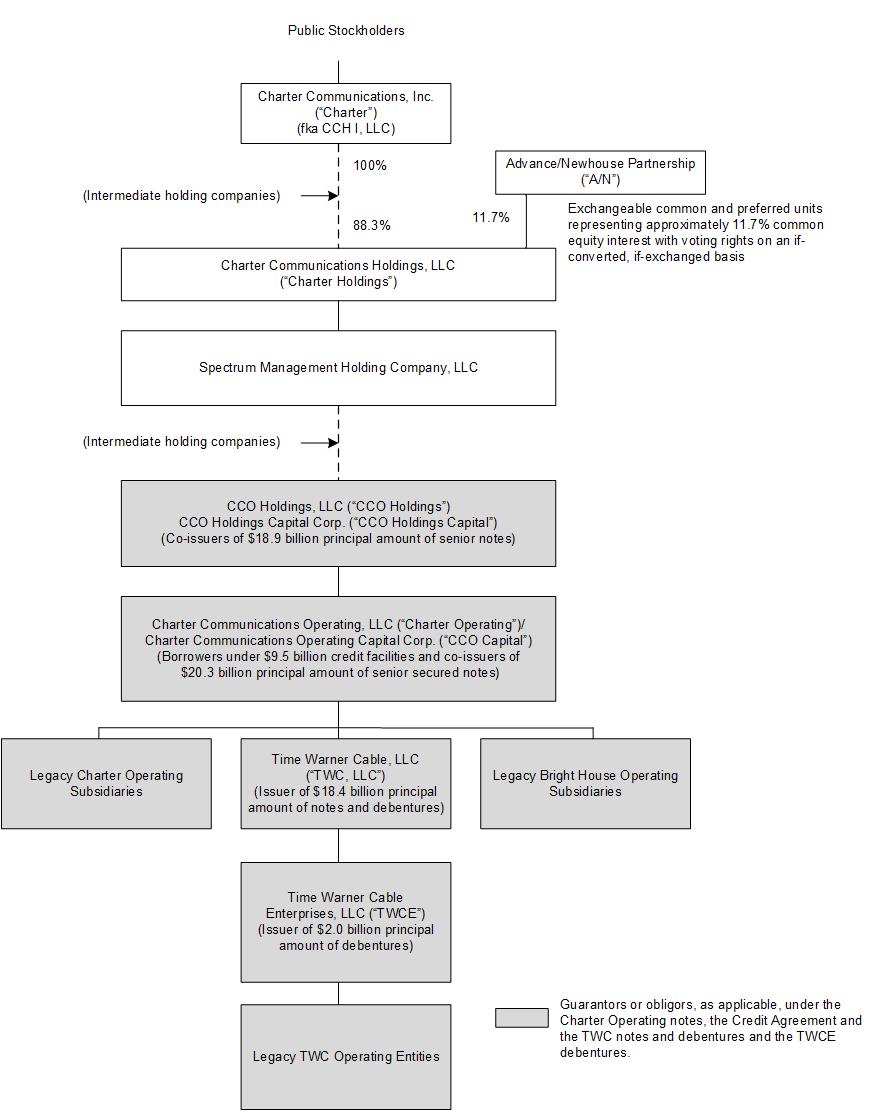

Corporate Entity Structure

The chart below sets forth our entity structure and that of our direct and indirect parents and subsidiaries. The chart does not include all of our affiliates and subsidiaries and, in some cases, we have combined separate entities for presentation purposes. The equity ownership percentages shown below are approximations. Indebtedness amounts shown below are principal amounts as of December 31, 2017. See Note 9 to the accompanying consolidated financial statements contained in “Part II. Item 8. Financial Statements and Supplementary Data,” which also includes the accreted values of the indebtedness described below.

3

Products and Services

We offer our customers subscription-based video services, including video on demand (“VOD”), high definition (“HD”) television, and digital video recorder (“DVR”) service, Internet services and voice services. As of December 31, 2017, 74% of our footprint was all-digital enabling us to offer more HD channels, faster Internet speeds and better video picture quality and we intend to transition the remaining portions of our Legacy TWC and Legacy Bright House footprints to all-digital. Our video, Internet, and voice services are offered to residential and commercial customers on a subscription basis, with prices and related charges based on the types of service selected, whether the services are sold as a “bundle” or on an individual basis, and the equipment necessary to receive our services. Bundled services are available to substantially all of our passings, and approximately 59% of our customers subscribe to a bundle of services.

All customer statistics as of December 31, 2017 include the operations of Legacy TWC, Legacy Bright House and Legacy Charter, each of which is based on individual legacy company reporting methodology. These methodologies differ and their differences may be material. Statistical reporting will be conformed over time to a single reporting methodology. The following table summarizes our customer statistics for video, Internet and voice as of December 31, 2017 and 2016 (in thousands except per customer data and footnotes).

Approximate as of | |||||||

December 31, | |||||||

2017 (a) | 2016 (a)(b) | ||||||

Customer Relationships (c) | |||||||

Residential | 25,639 | 24,801 | |||||

Small and Medium Business | 1,560 | 1,404 | |||||

Total Customer Relationships | 27,199 | 26,205 | |||||

Residential Primary Service Units ("PSUs") | |||||||

Video | 16,544 | 16,836 | |||||

Internet | 22,545 | 21,374 | |||||

Voice | 10,427 | 10,327 | |||||

49,516 | 48,537 | ||||||

Monthly Residential Revenue per Residential Customer (d) | $ | 109.75 | $ | 109.57 | |||

Small and Medium Business PSUs | |||||||

Video | 453 | 400 | |||||

Internet | 1,358 | 1,219 | |||||

Voice | 912 | 778 | |||||

2,723 | 2,397 | ||||||

Monthly Small and Medium Business Revenue per Customer (e) | $ | 207.36 | $ | 213.87 | |||

Enterprise PSUs (f) | 114 | 97 | |||||

(a) | We calculate the aging of customer accounts based on the monthly billing cycle for each account. On that basis, as of December 31, 2017 and 2016, customers include approximately 245,800 and 208,400 customers, respectively, whose accounts were over 60 days past due, approximately 19,500 and 15,500 customers, respectively, whose accounts were over 90 days past due, and approximately 12,600 and 8,000 customers, respectively, whose accounts were over 120 days past due. |

(b) | In the second quarter of 2017, we conformed the seasonal customer program in the Legacy Bright House footprint to our program. Prior to the plan change, Legacy Bright House customers enrolling in the seasonal plan were charged a one-time fee and counted as customer disconnects, and as new connects, when moving off the seasonal plan. Under our seasonal plan, residential customers pay a reduced monthly fee while the seasonal plan is active and remain reported as customers. Excluding the impact of customer activity related to Legacy Bright House's previous seasonal plan, residential customer relationships and video, Internet and voice PSUs at December 31, 2016 would have been higher by approximately 10,000, 8,000, 12,000 and 7,000 respectively. |

(c) | Customer relationships include the number of customers that receive one or more levels of service, encompassing video, Internet and voice services, without regard to which service(s) such customers receive. Customers who reside in residential |

4

multiple dwelling units (“MDUs”) and that are billed under bulk contracts are counted based on the number of billed units within each bulk MDU. Total customer relationships excludes enterprise customer relationships.

(d) | Monthly residential revenue per residential customer is calculated as total residential video, Internet and voice annual revenue divided by twelve divided by average residential customer relationships during the respective year. |

(e) | Monthly small and medium business revenue per customer is calculated as total small and medium business annual revenue divided by twelve divided by average small and medium business customer relationships during the respective year. |

(f) | Enterprise PSUs represent the aggregate number of fiber service offerings counting each separate service offering as an individual PSU. |

Residential Services

Video Services

Our video customers receive a package of basic programming which, in our all-digital markets, generally includes a digital set-top box that provides an interactive electronic programming guide with parental controls, access to pay-per-view services, including VOD (available to nearly all of our passings), digital music channels and the option to view certain video services on third party devices. Customers have the option to purchase additional tiers of services including premium channels which provide original programming, commercial-free movies, sports, and other special event entertainment programming. Substantially all of our video programming is available in HD. We also offer certain video packages containing a limited number of channels via our cable television systems.

In the vast majority of our footprint, we offer VOD service which allows customers to select from approximately 35,000 titles at any time. VOD includes standard definition, HD and three dimensional (“3D”) content. VOD programming options may be accessed for free if the content is associated with a customer’s linear subscription, or for a fee on a transactional basis. VOD services are also offered on a subscription basis included in a digital tier premium channel subscription or for a monthly fee. Pay-per-view channels allow customers to pay on a per-event basis to view a single showing of a one-time special sporting event, music concert, or similar event on a commercial-free basis.

Our goal is to provide our video customers with the programming they want, when they want it, on any device. DVR service enables customers to digitally record programming and to pause and rewind live programming. Customers can also use our Spectrum TV application available on mobile devices, residential devices and on our website, to watch up to 250 channels of cable TV, view VOD programming, remotely control digital set-top boxes while in the home and to program DVRs remotely. Customers also have access to programmer authenticated applications and websites (known as TV Everywhere services) such as HBO Go®, Fox Now®, Discovery Go® and WatchESPN®.

In certain markets, we have launched Spectrum Guide®, a network or “cloud-based” user interface that can run on traditional set-top boxes, with a look and feel that is similar to that of the Spectrum TV App. Spectrum Guide® is designed to allow our customers to enjoy a state-of-the-art video experience on the majority of our set-top boxes, including accessing third-party video applications such as Netflix. The guide enables customers to find video content more easily across cable TV channels and VOD options. We plan to continue to deploy Spectrum Guide across our footprint and enhance this technology in 2018 and beyond.

Internet Services

In 2017, we completed our launch of Spectrum pricing and packaging (“SPP”) and now offer an entry level Internet download speed of at least 100 megabits per second (“Mbps”) across 99% of our footprint and 200 Mbps across 17% of our footprint, which among other things, allows several people within a single household to stream HD video content online while simultaneously using our Internet service for non-video purposes. Additionally, leveraging DOCSIS 3.1 technology, we had introduced speed offerings of 940 Mbps ("Spectrum Internet Gig") in 17% of our footprint as of December 31, 2017. Finally, we offer a security suite with our Internet services which, upon installation by customers, provides protection against computer viruses and spyware and includes parental control features.

We offer an in-home WiFi product that provides customers with high performance wireless routers to maximize their in-home wireless Internet experience. Additionally, we offer an out-of-home WiFi service (“Spectrum WiFi”) in most of our footprint to our Internet customers at designated “hot spots.” In 2018, we expect to continue to expand WiFi accessibility to our customers through our network of WiFi hotspots.

5

Voice Services

We provide voice communications services using voice over Internet protocol ("VoIP") technology to transmit digital voice signals over our network. Our voice services include unlimited local and long distance calling to the United States, Canada, Mexico and Puerto Rico, voicemail, call waiting, caller ID, call forwarding and other features and offers international calling either by the minute, or through packages of minutes per month. For customers that subscribe to both our voice and video offerings, caller ID on TV is also available in most areas.

Mobile Services

Our mobile strategy is built on the long-term vision of an integrated fixed/wireless network with differentiated products, and the ability to maximize the potential of our existing cable business. We intend to launch our Spectrum-branded mobile service in 2018 to residential customers via our mobile virtual network operator (“MVNO”) reseller agreement with Verizon Wireless. In the second phase, we plan to use our WiFi network in conjunction with additional unlicensed or licensed spectrum to improve network performance and expand capacity to offer consumers a superior wireless service. In furtherance of this second phase, we have experimental wireless licenses from the Federal Communications Commission ("FCC") that we are utilizing to test next generation wireless services in several markets around the country. We currently plan to only offer our Spectrum mobile service to residential customers subscribing to our Internet service. In the future, we may also offer mobile service to our small and medium business customers on similar terms. We believe Spectrum-branded mobile services will drive more sales of our core products, create longer customer lives and increase profitability and cash flow over time. As we launch our new mobile services, we expect an initial funding period to grow a new product as well as negative working capital impacts from the timing of device-related cash flows when we provide the handset or tablet to customers pursuant to equipment installment plans.

We are exploring working with a variety of partners and vendors in a number of operational areas within the wireless space, including: creating common operating platforms; technical standards development and harmonization; device forward and reverse logistics; and emerging wireless technology platforms. The efficiencies created are expected to provide more choice, innovative products and competitive prices for customers. We intend to consider and pursue opportunities in the mobile space which may include entering into joint ventures or partnerships with wireless or cable providers which may require significant investment. There is no assurance we will enter into such arrangements or that if we do, that they will be successful.

Commercial Services

We offer scalable broadband communications solutions for businesses and carrier organizations of all sizes, selling Internet access, data networking, fiber connectivity to cellular towers and office buildings, video entertainment services and business telephone services.

Small and Medium Business

Spectrum Business offers Internet, voice and video services to small and medium businesses over our hybrid fiber coaxial network that are similar to those that we provide to our residential customers. Spectrum Business includes a full range of video programming and entry-level Internet speeds of 100 Mbps downstream and 10 Mbps upstream. Additionally, customers can upgrade their Internet speeds to 200 or 300 Mbps downstream. Spectrum Business also includes a set of business services including web hosting, e-mail and security, and multi-line telephone services with more than 30 business features including web-based service management, that are generally not available to residential customers.

Enterprise Solutions

Spectrum Enterprise offers fiber-delivered communications and managed IT solutions to larger businesses, as well as high-capacity last-mile data connectivity services to wireless and wireline carriers, Internet Service Providers (“ISPs”) and other competitive carriers on a wholesale basis. Spectrum Enterprise's product portfolio includes fiber Internet access, voice trunking services, hosted voice, Ethernet services that privately and securely connect geographically dispersed client locations, and video solutions designed to meet the needs of hospitality, education, and health care clients. In addition, Spectrum Enterprise is beginning market field trials of an innovative Hybrid Software-Defined Wide Area Network that enables businesses to leverage the performance of Ethernet, the ubiquity of Internet connectivity and the flexibility of a software-defined solution to solve a wide array of business communications and networking challenges. Our managed IT portfolio includes Cloud Infrastructure as a Service and Cloud Desktop as a Service, and managed hosting, application, and messaging solutions, along with other related IT and professional services. Our large serviceable footprint allows us to effectively serve business customers with multiple sites across given

6

geographic regions. These customers can benefit from obtaining advanced services from a single provider simplifying procurement and potentially reducing their costs.

Advertising Services

Our advertising sales division, Spectrum Reach®, offers local, regional and national businesses the opportunity to advertise in individual and multiple markets on cable television networks and digital outlets. We receive revenues from the sale of local advertising across various platforms for networks such as MTV®, CNN® and ESPN®. In any particular market, we typically insert local advertising on up to 60 channels. Our large footprint provides opportunities for advertising customers to address broader regional audiences from a single provider and thus reach more customers with a single transaction. Our size also provides scale to invest in new technology to create more targeted and addressable advertising capabilities.

Available advertising time is generally sold by our advertising sales force. In some markets, we have formed advertising interconnects or entered into representation agreements with other video distributors, including, among others, Verizon Communications Inc.’s (“Verizon”) fiber optic service (“FiOS”) and AT&T Inc.’s (“AT&T”) U-verse and DIRECTV platforms, under which we sell advertising on behalf of those operators. In other markets, we enter into representation agreements under which another operator in the area will sell advertising on our behalf. These arrangements enable us and our partners to deliver linear commercials across wider geographic areas, replicating the reach of local broadcast television stations to the extent possible. In addition, we enter into interconnect agreements from time to time with other cable operators, which, on behalf of a number of video operators, sells advertising time to national and regional advertisers in individual or multiple markets.

Additionally, we sell the advertising inventory of our owned and operated local sports, news and lifestyle channels, of our regional sports networks that carry Los Angeles Lakers’ basketball games and other sports programming and of SportsNet LA, a regional sports network that carries Los Angeles Dodgers’ baseball games and other sports programming.

We are in the process of deploying advanced advertising products such as our Audience App, which uses our proprietary set-top box viewership data (all anonymized and aggregated) to optimize linear inventory, and household addressability, which allows for more finite targeting, within various parts of our footprint. These new products will be distributed across more of our footprint in 2018.

Other Services

Regional Sports and News Networks

We have an agreement with the Los Angeles Lakers for rights to distribute all locally available Los Angeles Lakers’ games through 2033. We broadcast those games on our regional sports network, Spectrum SportsNet. We also manage 16 local news channels, including Spectrum News NY1, a 24-hour news channel focused on New York City, 10 local sports channels and one local lifestyle community channel, and we own 26.8% of Sterling Entertainment Enterprises, LLC (doing business as SportsNet New York), a New York City-based regional sports network that carries New York Mets’ baseball games as well as other regional sports programming.

American Media Productions, LLC ("American Media Productions"), an unaffiliated third party, owns SportsNet LA, a regional sports network carrying the Los Angeles Dodgers’ baseball games and other sports programming. In accordance with agreements with American Media Productions, we act as the network’s exclusive affiliate and advertising sales representative and have certain branding and programming rights with respect to the network. In addition, we provide certain production and technical services to American Media Productions. The affiliate, advertising, production and programming agreements continue through 2038.

Security and Home Management

We provide security and home management services to our residential customers in certain markets. Our broadband cable system connects the customer’s in-home system to our emergency response center for traditional security, fire and medical emergency monitoring and dispatch. The service also allows customers to remotely arm or disarm their security system, monitor their home via indoor and outdoor cameras, and remotely operate key home functions, including setting and controlling lights, thermostats and door locks.

Pricing of Our Products and Services

Our revenues are principally derived from the monthly fees customers pay for the services we provide. We typically charge a one-time installation fee which is sometimes waived or discounted in certain sales channels during certain promotional periods.

7

Our SPP generally offers a standardized price for each tier of service, bundle of services, and add-on service, regardless of market and emphasizes triple play bundles of video, Internet and voice services. Our most popular and competitive services are combined in core packages at what we believe are attractive prices. We believe our approach:

• | offers simplicity for customers to understand our offers, and for our employees in service delivery; |

• | drives our ability to package more services at the time of sale, thus increasing revenue per customer; |

• | offers a higher quality and more value-based set of services, including faster Internet speeds, more HD channels, lower equipment fees and a more transparent pricing structure; |

• | drives higher customer satisfaction, lower service calls and churn; and |

• | allows for gradual price increases at the end of promotional periods. |

Our Network Technology and Customer Premise Equipment

Our network includes three key components: a national backbone, regional/metro networks and a “last-mile” network. Both our national backbone and regional/metro network components utilize a redundant Internet Protocol ("IP") ring/mesh architecture. The national backbone component provides connectivity from regional demarcation points to nationally centralized content, connectivity and services. The regional/metro network components provide connectivity between the regional demarcation points and headends within a specific geographic area and enable the delivery of content and services between these network components.

Our last-mile network utilizes a hybrid fiber coaxial cable (“HFC”) architecture, which combines the use of fiber optic cable with coaxial cable. In most systems, we deliver our signals via fiber optic cable from the headend to a group of nodes, and use coaxial cable to deliver the signal from individual nodes to the homes served by that node. For our fiber Internet, Ethernet, carrier wholesale, SIP and PRI Spectrum Enterprise customers, fiber optic cable is extended from individual nodes to the customer’s site. For certain new build and MDU sites, we increasingly bring fiber to the customer site. Our design standard is six strands of fiber to each node, with two strands activated and four strands reserved for spares and future services. This design standard allows these additional strands to be utilized for additional residential traffic capacity, and enterprise customer needs as they arise. We believe that this hybrid network design provides high capacity and signal quality. The design also provides two-way signal capabilities for the support of interactive services.

HFC architecture benefits include:

• | bandwidth capacity to enable traditional and two-way video and broadband services; |

• | dedicated bandwidth for two-way services; and |

• | signal quality and high service reliability. |

Approximately 98% of our estimated passings are served by systems that have bandwidth of 750 megahertz or greater as of December 31, 2017. This bandwidth capacity enables us to offer HD television, DOCSIS-based Internet services and voice services.

An all-digital platform enables us to offer a larger selection of HD channels, faster Internet speeds and better picture quality while providing greater plant security and enabling lower installation and disconnect service truck rolls. We are currently all-digital in 74% of our footprint and intend to transition the remaining portions of our Legacy TWC and Legacy Bright House footprints.

We have been introducing our new set-top box, WorldBox, to consumers in certain markets. The WorldBox design has opened the set-top box market to new vendors and reduced our set-top box costs. WorldBox also includes more advanced features and functionality than older set-top boxes, including faster processing times, IP capabilities with increased speed, additional simultaneous recordings, increased DVR storage capacity, and a greater degree of flexibility for consumers to take Charter-provisioned set-top boxes with them, if and when, they move residences. We have also been introducing our new cloud-based user interface, Spectrum Guide®, to our video customers in certain markets. Spectrum Guide® improves video content search and discovery, and fully enables our on-demand offering. In addition, Spectrum Guide® can function on the majority of our set-top boxes, reducing costs and customer disruption to swap equipment for new functionality.

Management, Customer Operations and Marketing

Our operations are centralized, with senior executives located at several key corporate offices, responsible for coordinating and overseeing operations, including establishing company-wide strategies, policies and procedures. Sales and marketing, network operations, field operations, customer operations, engineering, advertising sales, human resources, legal, government relations, information technology and finance are all directed at the corporate level. Regional and local field operations are responsible for

8

customer premise service transactions and maintaining and constructing that portion of our network which is located outdoors. In 2018, our field operations group continues to focus on standardizing practices, processes, procedures and metrics.

We continue to focus on improving the customer experience through enhanced product offerings, reliability of services, and delivery of quality customer service. As part of our operating strategy, we are committed to investments and hiring plans that continue to insource most of our customer operations workload. In-house domestic call centers handled approximately 75% of our customer service calls and are managed centrally to ensure a consistent, high quality customer experience. Routing calls by particular call types to specific agents that only handle such call types, enables agents to become experts in addressing specific customer needs, thus creating a better customer experience. We also continue to migrate our call centers to full virtualization which allows calls to be routed across our call centers regardless of the location origin of the call, reducing call wait times, and saving costs. A new call center agent desktop interface tool, already used at Legacy Charter, is being developed for Legacy TWC and Legacy Bright House. This new desktop interface tool will enable virtualization of all call centers, regardless of legacy billing platform, and will better serve our customers.

We also provide customers with the opportunity to interact with us through a variety of forums in addition to telephonic communications, including through our customer website, mobile device applications, online chat and social media. Our customer websites and mobile applications enable customers to pay their bills, manage their accounts, order new services and utilize self-service help and support.

We sell our residential and commercial services using a national brand platform known as Spectrum®, Spectrum Business® and Spectrum Enterprise®. These brands reflect our comprehensive approach to industry-leading products, driven by speed, performance and innovation. Our marketing strategy emphasizes the sale of our bundled services through targeted direct response marketing programs to existing and potential customers, and increases awareness and the value of the Spectrum brand. Our marketing organization creates and executes marketing programs intended to grow customer relationships, increase the number of services we sell per relationship, retain existing customers and cross-sell additional products to current customers. We monitor the effectiveness of our marketing efforts, customer perception, competition, pricing, and service preferences, among other factors, in order to increase our responsiveness to our customers and to improve our sales and customer retention. The marketing organization manages the majority of the sales channels including direct sales, on-line, outbound telemarketing and stores.

Programming

We believe that offering a wide variety of video programming choices influences a customer’s decision to subscribe and retain our cable video services. We obtain basic and premium programming, usually pursuant to written contracts from a number of suppliers. Media corporation consolidation has, however, resulted in fewer suppliers and additional selling power on the part of programming suppliers. Our programming contracts are generally for a fixed period of time, usually for multiple years, and are subject to negotiated renewal. Recently, we have begun entering into agreements to co-produce original content which give us the right to provide our customers with certain exclusive content, for a period of time.

Programming is usually made available to us for a license fee, which is generally paid based on the number of customers to whom we make that programming available. Programming license fees may include “volume” discounts and financial incentives to support the launch of a channel and/or ongoing marketing support, as well as discounts for channel placement or service penetration. For home shopping channels, we typically receive a percentage of the revenue attributable to our customers’ purchases. We also offer VOD and pay per view channels of movies and events that are subject to a revenue split with the content provider.

Our programming costs have increased in excess of customary inflationary and cost-of-living type increases. We expect programming costs to continue to increase due to a variety of factors including, annual increases pursuant to our programming contracts, contract renewals with programmers and the carriage of incremental programming, including new services, higher expanded basic video penetration and VOD programming. Increases in the cost of sports programming and the amounts paid for broadcast station retransmission consent have been the largest contributors to the growth in our programming costs over the last few years. Additionally, the demands of large media companies who link carriage of their most popular networks to carriage and cost increases of their less popular networks, has limited our flexibility in creating more tailored and cost-sensitive programming packages for consumers.

Federal law allows commercial television broadcast stations to make an election between “must-carry” rights and an alternative “retransmission-consent” regime. When a station opts for retransmission-consent, we are not allowed to carry the station’s signal without that station’s permission. Continuing demands by owners of broadcast stations for cash payments at substantial increases over amounts paid in prior years in exchange for retransmission consent will increase our programming costs or require us to cease carriage of popular programming, potentially leading to a loss of customers in affected markets.

9

Over the past several years, increases in our video service rates have not fully offset the increases in our programming costs, and with the impact of increasing competition and other marketplace factors, we do not expect the increases in our video service rates to fully offset the increase in our programming costs for the foreseeable future. Although we pass along a portion of amounts paid for retransmission consent to the majority of our customers, our inability to fully pass programming cost increases on to our video customers has had, and is expected in the future to have, an adverse impact on our cash flow and operating margins associated with our video product. In order to mitigate reductions of our operating margins due to rapidly increasing programming costs, we continue to review our pricing and programming packaging strategies.

We currently have programming contracts that have expired and others that will expire at, or before the end, of 2018. We will seek to renew these agreements on terms that we believe are favorable. There can be no assurance, however, that these agreements will be renewed on favorable or comparable terms. To the extent that we are unable to reach agreements with certain programmers on terms that we believe are reasonable, we have been, and may in the future be, forced to remove such programming channels from our line-up, which may result in a loss of customers.

Regions

We operate in geographically diverse areas which are organized in regional clusters. These regions are managed centrally on a consolidated level. Our eleven regions and the customer relationships within each region as of December 31, 2017 are as follows (in thousands):

Regions | Total Customer Relationships | |

Carolinas | 2,668 | |

Central | 2,870 | |

Florida | 2,389 | |

Great Lakes | 2,208 | |

Northeast | 2,970 | |

Northwest | 1,472 | |

NYC | 1,334 | |

South | 2,085 | |

Southern Ohio | 2,093 | |

Texas | 2,736 | |

West | 4,374 | |

Competition

Residential Services

We face intense competition for residential customers, both from existing competitors and, as a result of the rapid development of new technologies, services and products, from new entrants.

Video competition

Our residential video service faces competition from direct broadcast satellite (“DBS”) service providers, which have a national footprint and compete in all of our operating areas. DBS providers offer satellite-delivered pre-packaged programming services that can be received by relatively small and inexpensive receiving dishes. DBS providers offer aggressive promotional pricing, exclusive programming (e.g., NFL Sunday Ticket) and video services that are comparable in many respects to our residential video service. Our residential video service also faces competition from companies with fiber-based networks, primarily AT&T U-verse, Frontier Communications Corporation (“Frontier”) FiOs and Verizon FiOs, which offer wireline video services in approximately 27%, 8% and 4%, respectively, of our operating areas. AT&T also owns DIRECTV, and as a combined company provides video service (via IP or satellite) and voice service (via IP or wireless) across our entire footprint, and delivers video, Internet, voice and mobile services across 45% of our passings. AT&T also announced the acquisition of Time Warner Inc. in October 2016 which is subject to regulatory approval. If approved, it is not yet clear how AT&T will use the various programming and studio assets it would acquire from Time Warner Inc. to benefit its own products on its four video platforms or what potential program access conditions, as part of any regulatory approval, might apply.

10

Our residential video service also faces growing competition from a number of other sources, including companies that deliver linear network programming, movies and television shows on demand and other video content over broadband Internet connections to televisions, computers, tablets and mobile devices. These newer categories of competitors include virtual multichannel video programming distributors (“V-MVPD”) such as DirecTV NOW, Sling TV, Playstation Vue, YouTube TV and Hulu Live, and direct to consumer products offered by programmers that have not traditionally sold programming directly to consumers, such as HBO Now, CBS All Access and Showtime Anytime. Other online video business models have also developed, including, (i) subscription video on demand (“SVOD”) services such as Netflix, Amazon Prime, and Hulu Plus, (ii) ad-supported free online video products, including YouTube and Hulu, some of which offer programming for free to consumers that we currently purchase for a fee, (iii) pay-per-view products, such as iTunes and Amazon Instant, and (iv) additional offerings from wireless providers which continue to integrate and bundle video services and mobile products. Historically, we have generally viewed SVOD online video services as complementary to our own video offering, and we have developed a cloud-based guide that is capable of incorporating video from many online video services currently offered in the marketplace. As the proliferation of online video services grows, however, services from V-MVPDs and new direct to consumer offerings, as well as piracy and password sharing, could negatively impact the growth of our video business.

Internet competition

Our residential Internet service faces competition from the phone companies’ DSL, fiber-to-the-home ("FTTH") and wireless broadband offerings, as well as from a variety of companies that offer other forms of online services, including wireless and satellite-based broadband services. AT&T, Frontier FiOs and Verizon’s FiOs are our primary FTTH competitors. Given the FTTH deployments of our competitors, launches of broadband services offering 1 gigabits per second (“Gbps”) speed have recently grown. Several competitors, including AT&T, Verizon's FiOs and Google, deliver 1 Gbps broadband speed in at least a portion of their footprints which overlap our footprint. DSL service is often offered at prices lower than our Internet services, although typically at speeds much lower than the minimum speeds we offer as part of SPP. Various wireless phone companies are now offering third and fourth generation (3G and 4G) wireless Internet services and some have announced that they intend to offer faster fifth generation (5G) services in the future. Some wireless phone companies offer unlimited data packages to customers. In addition, a growing number of commercial areas, such as retail malls, restaurants and airports, offer WiFi Internet service. Numerous local governments are also considering or actively pursuing publicly subsidized WiFi Internet access networks. These options offer alternatives to cable-based Internet access.

Voice competition

Our residential voice service competes with wireless and wireline phone providers, as well as other forms of communication, such as text messaging on cellular phones, instant messaging, social networking services, video conferencing and email. We also compete with “over-the-top” phone providers, such as Vonage, Skype, magicJack, Google Voice and Ooma, Inc., as well as companies that sell phone cards at a cost per minute for both national and international service. The increase in the number of different technologies capable of carrying voice services and the number of alternative communication options available to customers as well as the replacement of wireline services by wireless have intensified the competitive environment in which we operate our residential voice service. When launched, our mobile service will compete with other wireless providers such as Verizon, AT&T, T-Mobile US, Inc. ("T-Mobile") and Sprint Corporation ("Sprint").

Regional Competitors

In some of our operating areas, other competitors have built networks that offer video, Internet and voice services that compete with our services. For example, in certain markets, our residential video, Internet and voice services compete with Google Fiber, Cincinnati Bell Inc., Hawaiian Telcom, RCN Telecom Services, LLC, Grande Communications Networks, LLC and WideOpenWest Finance, LLC.

Additional competition

In addition to multi-channel video providers, cable systems compete with other sources of news, information and entertainment, including over-the-air television broadcast reception, live events, movie theaters and the Internet. Competition is also posed by fixed wireless and satellite master antenna television systems, or SMATV systems, serving MDUs, such as condominiums, apartment complexes, and private residential communities.

Business Services

We face intense competition across each of our business services product offerings. Our small and medium business video, Internet,

11

networking and voice services face competition from a variety of providers as described above. Our enterprise solutions also face competition from the competitors described above as well as other telecommunications carriers, such as metro and regional fiber-based carriers. We also compete with cloud, hosting and related service providers and application-service providers.

Advertising

We face intense competition for advertising revenue across many different platforms and from a wide range of local and national competitors. Advertising competition has increased and will likely continue to increase as new advertising avenues seek to attract the same advertisers. We compete for advertising revenue against, among others, local broadcast stations, national cable and broadcast networks, radio stations, print media and online advertising companies and content providers.

Security and Home Management

Our IntelligentHome service faces competition from traditional security companies, such as the ADT Corporation, service providers such as Verizon and AT&T, as well as new entrants, such as Vivint, Inc., Alarm.com, Inc. and NEST Labs, Inc.

Seasonality and Cyclicality

Our business is subject to seasonal and cyclical variations. Our results are impacted by the seasonal nature of customers receiving our cable services in college and vacation markets. Our revenue is subject to cyclical advertising patterns and changes in viewership levels. Our advertising revenue is generally higher in the second and fourth calendar quarters of each year, due in part to increases in consumer advertising in the spring and in the period leading up to and including the holiday season. U.S. advertising revenue is also cyclical, benefiting in even-numbered years from advertising related to candidates running for political office and issue-oriented advertising. Our capital expenditures and trade working capital are also subject to significant seasonality based on the timing of subscriber growth, network programs, specific projects and construction.

Regulation and Legislation

The following summary addresses the key regulatory and legislative developments affecting the cable industry and our services for both residential and commercial customers. Cable system operations are extensively regulated by the federal government (primarily the FCC), certain state governments, and many local governments. A failure to comply with these regulations could subject us to substantial penalties. Our business can be dramatically impacted by changes to the existing regulatory framework, whether triggered by legislative, administrative, or judicial rulings. Congress and the FCC have frequently revisited the subject of communications regulation and they are likely to do so again in the future. We could be materially disadvantaged in the future if we are subject to new regulations or regulatory actions that do not equally impact our key competitors. We cannot provide assurance that the already extensive regulation of our business will not be expanded in the future. In addition, we are already subject to Charter-specific conditions regarding certain business practices as a result of the FCC’s approval of the Transactions.

Video Service

Must Carry/Retransmission Consent

There are two alternative legal methods for carriage of local broadcast television stations on cable systems. Federal “must carry” regulations require cable systems to carry local broadcast television stations upon the request of the local broadcaster. Alternatively, federal law includes “retransmission consent” regulations, by which popular commercial television stations can prohibit cable carriage unless the cable operator first negotiates for “retransmission consent,” which may be conditioned on significant payments or other concessions. Popular stations invoking “retransmission consent” have been demanding substantial compensation increases in their recent negotiations with cable operators, thereby significantly increasing our operating costs.

Additional government-mandated broadcast carriage obligations, including those related to the FCC’s newly adopted enhanced technical broadcasting option (Advanced Television Systems Committee 3.0), could disrupt existing programming commitments, interfere with our preferred use of limited channel capacity, and limit our ability to offer services that appeal to our customers and generate revenues.

Cable Equipment

In 1996, Congress enacted a statute requiring the FCC to adopt regulations designed to assure the development of an independent retail market for “navigation devices,” such as cable set-top boxes. As a result, the FCC required cable operators to make a separate offering of security modules (i.e., a “CableCARD”) that can be used with retail navigation devices. Some of the FCC’s rules

12

requiring support for CableCARDs were vacated by the United States Court of Appeals for the District of Columbia in 2013, and another of these rules was repealed by Congress in 2014, but the basic obligation to provide separable security for retail devices remains in place. In 2016, the FCC proposed to replace its CableCARD regime with burdensome new rules that would have required us to make disaggregated “information flows” available to set-top boxes and apps supplied by third parties. That proposal was not adopted, but various parties may continue to advocate alternative regulatory approaches to reduce consumer dependency on traditional operator provided set-top boxes. It remains uncertain whether the FCC or Congress will change the legal requirements related to our set-top boxes and what the impact of any such changes might be.

Privacy and Information Security Regulation

The Communications Act of 1934, as amended (the “Communications Act”) limits our ability to collect, use, and disclose customers’ personally identifiable information for our video, voice, and Internet services, as well as provides requirements to safeguard such information. We are subject to additional federal, state, and local laws and regulations that impose additional restrictions on the collection, use and disclosure of consumer information. Further, the FCC, Federal Trade Commission ("FTC"), and many states regulate and restrict the marketing practices of communications service providers, including telemarketing and sending unsolicited commercial emails.

As a result of the FCC’s 2017 decision to reclassify broadband Internet access service as an “information service,” the FTC once again has the authority, pursuant to its authority to enforce against unfair or deceptive acts and practices, to protect the privacy of Internet service customers, including our use and disclosure of certain customer information. Although one court decision has raised questions regarding the extent of FTC jurisdiction over companies that offer both common carrier services as well as non-common carrier services, that decision has been stayed, pending review by the full Ninth Circuit Court of Appeals.

Our operations are also subject to federal and state laws governing information security. In the event of an information security breach, such rules may require consumer and government agency notification and may result in regulatory enforcement actions with the potential of monetary forfeitures. The FCC, the FTC and state attorneys general regularly bring enforcement actions against companies related to information security breaches and privacy violations.

Various security standards provide guidance to telecommunications companies in order to help identify and mitigate cybersecurity risk. One such standard is the voluntary framework released by the National Institute for Standards and Technologies (“NIST”) in February 2014, in cooperation with other federal agencies and owners and operators of U.S. critical infrastructure. The NIST cybersecurity framework provides a prioritized and flexible model for organizations to identify and manage cyber risks inherent to their business. It was designed to supplement, not supersede, existing cybersecurity regulations and requirements. Several government agencies have encouraged compliance with the NIST cybersecurity framework, including the FCC, which is also considering expansion of its cybersecurity guidelines or the adoption of cybersecurity requirements. NIST recently proposed draft updates to this voluntary framework and is expected to release final revisions in 2018.

After the repeal of the FCC’s 2016 privacy rules through the Congressional Review Act, many states and local authorities have considered legislative or other actions that would impose additional restrictions on our ability to collect, use and disclose certain information. Despite language in the FCC’s December 2017 decision reclassifying broadband Internet access service as an “information service,” that preempts state and local privacy regulations that conflict with federal policy, we expect these state and local efforts to regulate online privacy to continue in 2018. Additionally, several state legislatures are considering the adoption of new data security and cybersecurity legislation that could result in additional network and information security requirements for our business. There are also bills pending in both the U.S. House of Representatives and Senate that could impose new privacy and data security obligations. We cannot predict whether any of these efforts will be successful or preempted, or how new legislation and regulations, if any, would affect our business.

Pole Attachments

The Communications Act requires most utilities owning utility poles to provide cable systems with access to poles and conduits and simultaneously subjects the rates charged for this access to either federal or state regulation. In 2011 and again in 2015, the FCC amended its existing pole attachment rules to promote broadband deployment. The 2011 order allows for new penalties in certain cases involving unauthorized attachments, but generally strengthens the cable industry’s ability to access investor-owned utility poles on reasonable rates, terms, and conditions. Additionally, the 2011 order reduces the federal rate formula previously applicable to “telecommunications” attachments to closely approximate the rate formula applicable to “cable” attachments. The 2015 order continues the reconciliation of rates, effectively closing the remaining “loophole” that potentially allowed for significantly higher rates for telecommunications than for “cable” attachments in certain scenarios, and minimizing the rate consequences of any of our services if deemed “telecommunications” for pole attachment purposes. Utility pole owners have appealed the 2015 order. Neither the 2011 order nor the 2015 order directly affect the rate in states that self-regulate (rather than

13

allow the FCC to regulate pole rates), but many of those states have substantially the same rate for cable and telecommunications attachments.

Some municipalities have enacted “one-touch” make-ready pole attachment ordinances, which permit third parties to alter components of our network attached to utility poles in ways that could adversely affect our businesses. Some of these ordinances have been challenged with differing results. In 2017, the FCC initiated a rulemaking that considers amending its pole attachment rules to permit a “one-touch” make-ready-like process for the poles within its jurisdiction. If adopted, these rules could have a similar effect as the municipal one-touch make-ready ordinances and adversely affect our businesses.

Cable Rate Regulation

Federal law strictly limits the potential scope of cable rate regulation. Pursuant to federal law, all video offerings are universally exempt from rate regulation, except for a cable system’s minimum level of video programming service, referred to as “basic service,” and associated equipment. Rate regulation of basic service and associated equipment operates pursuant to a federal formula, with local governments, commonly referred to as local franchising authorities, primarily responsible for administering this regulation. The majority of our local franchising authorities have never certified to regulate basic service cable rates. In 2015, the FCC adopted an order (which was subsequently upheld on appeal) reversing its historic approach to rate regulation certifications and requiring a local franchise authority interested in regulating cable rates to first make an affirmative showing that there is no “effective competition” (as defined under federal law) in the community. Very few local franchise authorities have filed the necessary rate regulation certification, and the FCC’s 2015 order should make it more difficult for such entities to assert rate regulation in the future.

There have been calls to impose expanded rate regulation on the cable industry. Confronted with rapidly increasing cable programming costs, it is possible that Congress may adopt new constraints on the retail pricing or packaging of cable programming. Any such constraints could adversely affect our operations.

Ownership Restrictions

Federal regulation of the communications field traditionally included a host of ownership restrictions, which limited the size of certain media entities and restricted their ability to enter into competing enterprises. Through a series of legislative, regulatory, and judicial actions, most of these restrictions have been either eliminated or substantially relaxed. Changes in this regulatory area could alter the business environment in which we operate.

Access Channels

Local franchise agreements often require cable operators to set aside certain channels for public, educational, and governmental access programming. Federal law also requires cable systems to designate up to 15% of their channel capacity for commercial leased access by unaffiliated third parties, who may offer programming that our customers do not particularly desire. The FCC adopted revised rules in 2007 mandating a significant reduction in the rates that operators can charge commercial leased access users and imposing additional administrative requirements that would be burdensome on the cable industry. The effect of the FCC’s revised rules was stayed by a federal court, pending a cable industry appeal and an adverse finding by the Office of Management and Budget. Although commercial leased access activity historically has been relatively limited, increased activity in this area could further burden the channel capacity of our cable systems.

Other FCC Regulatory Matters

FCC regulations cover a variety of additional areas, including, among other things: (1) equal employment opportunity obligations; (2) customer service standards; (3) technical service standards; (4) mandatory blackouts of certain network and syndicated programming; (5) restrictions on political advertising; (6) restrictions on advertising in children’s programming; (7) licensing of systems and facilities; (8) maintenance of public files; (9) emergency alert systems; (10) inside wiring and exclusive contracts for MDU complexes; and (11) disability access, including new requirements governing video-description and closed-captioning. Each of these regulations restricts our business practices to varying degrees and may impose additional costs on our operations.

It is possible that Congress or the FCC will expand or modify its regulation of cable systems in the future, and we cannot predict at this time how that might impact our business.

Copyright

Cable systems are subject to a federal copyright compulsory license covering carriage of television and radio broadcast signals.

14

The copyright law provides copyright owners the right to audit our payments under the compulsory license, and we are currently subject to ongoing compulsory copyright audits. The possible modification or elimination of this compulsory copyright license is the subject of continuing legislative proposals and administrative review and could adversely affect our ability to obtain desired broadcast programming.

Copyright clearances for non-broadcast programming services are arranged through private negotiations. Cable operators also must obtain music rights for locally originated programming and advertising from the major music performing rights organizations. These licensing fees have been the source of litigation in the past, and we cannot predict with certainty whether license fee disputes may arise in the future.

Franchise Matters

Our cable systems generally are operated pursuant to nonexclusive franchises, permits, and similar authorizations granted by a municipality or other state or local government entity in order to utilize and cross public rights-of-way. Cable franchises generally are granted for fixed terms and in many cases include monetary penalties for noncompliance and may be terminable if the franchisee fails to comply with material provisions. The specific terms and conditions of cable franchises vary significantly between jurisdictions. Cable franchises generally contain provisions governing cable operations, franchise fees, system construction, maintenance, technical performance, customer service standards, supporting and carrying public access channels, and changes in the ownership of the franchisee. A number of states subject cable systems to the jurisdiction of centralized state government agencies, such as public utility commissions. Although local franchising authorities have considerable discretion in establishing franchise terms, certain federal protections benefit cable operators. For example, federal law caps local franchise fees.

Prior to the scheduled expiration of our franchises, we generally initiate renewal proceedings with the granting authorities. The Communications Act, which is the primary federal statute regulating interstate communications, provides for an orderly franchise renewal process in which granting authorities may not unreasonably withhold renewals. In connection with the franchise renewal process, however, many governmental authorities require the cable operator to make additional costly commitments. Historically, we have been able to renew our franchises without incurring significant costs, although any particular franchise may not be renewed on commercially favorable terms or otherwise. If we fail to obtain renewals of franchises representing a significant number of our customers, it could have a material adverse effect on our consolidated financial condition, results of operations, or our liquidity. Similarly, if a local franchising authority’s consent is required for the purchase or sale of a cable system, the local franchising authority may attempt to impose more burdensome requirements as a condition for providing its consent.

The traditional cable franchising regime has undergone significant change as a result of various federal and state actions. The FCC has adopted rules that streamline entry for new competitors (particularly those affiliated with telephone companies) and reduce certain franchising burdens for these new entrants. The FCC adopted more modest relief for existing cable operators.

At the same time, a substantial number of states have adopted new franchising laws. Again, these laws were principally designed to streamline entry for new competitors, and they often provide advantages for these new entrants that are not immediately available to existing cable operators. In many instances, these franchising regimes do not apply to established cable operators until the existing franchise expires or a competitor directly enters the franchise territory.

Internet Service

In 2015, the FCC determined that broadband Internet access services, such as those we offer, were a form of “telecommunications service” under the Communications Act and, on that basis, imposed rules banning service providers from blocking access to lawful content, restricting data rates for downloading lawful content, prohibiting the attachment of non-harmful devices, giving special transmission priority to affiliates, and offering third parties the ability to pay for priority routing. The 2015 rules also imposed a “transparency” requirement, i.e., an obligation to disclose all material terms and conditions of our service to consumers.

In December 2017, the FCC adopted an order repudiating its treatment of broadband as a “telecommunications service,” reclassifying broadband as an “information service,” and eliminating the 2015 rules other than the transparency requirement, which it eased in significant ways. The FCC also ruled that state regulators may not impose obligations similar to federal obligations that the FCC removed. We expect that various parties will challenge the FCC’s December 2017 ruling in court, and, we cannot predict how any such court challenges will be resolved. Moreover, it is possible that the FCC might further revise its approach to broadband Internet access in the future, or that Congress might enact legislation affecting the rules applicable to the service.

The FCC’s December 2017 ruling does not affect other regulatory obligations on broadband Internet access providers. Notably, broadband providers are obliged by the Communications Assistance for Law Enforcement Act ("CALEA") to configure their networks in a manner that facilitates the ability of law enforcement, with proper legal authorization, to obtain information about

15

our customers, including the content of their Internet communications. The FCC and Congress also are considering subjecting Internet access services to the Universal Service funding requirements. These funding requirements could impose significant new costs on our Internet service. Also, the FCC and some state regulatory commissions direct certain subsidies to telephone companies deploying broadband to areas deemed to be “unserved” or “underserved.” We have opposed such subsidies when directed to areas that we serve. Despite our efforts, future subsidies may be directed to areas served by us, which could result in subsidized competitors operating in our service territories. State and local governmental organizations have also adopted Internet-related regulations. These various governmental jurisdictions are also considering additional regulations in these and other areas, such as privacy, pricing, service and product quality, imposition of local franchise fees on Internet-related revenue and taxation. The adoption of new Internet regulations or the adaptation of existing laws to the Internet could adversely affect our business.

Aside from the FCC’s generally applicable regulations, we have made certain commitments to comply with the FCC’s order in connection with the FCC’s approval of the TWC Transaction and the Bright House Transaction (discussed below).

Voice Service