Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - REX ENERGY CORP | d508630d8k.htm |

| EX-99.4 - EX-99.4 - REX ENERGY CORP | d508630dex994.htm |

| EX-99.3 - EX-99.3 - REX ENERGY CORP | d508630dex993.htm |

| EX-99.2 - EX-99.2 - REX ENERGY CORP | d508630dex992.htm |

CORPORATE PRESENTATION January 2018 Exhibit 99.1 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Disclosures 2 Forward Looking Statements Statements in this presentation that are not historical facts are “forward-looking statements” within the

meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We believe these statements and the assumptions and estimates contained in this presentation are reasonable based

on information that is currently available to us. However, management’s assumptions and the company’s future performance are subject to a wide range of business risks and uncertainties, both known and unknown, and we cannot assure

that the company can or will meet the goals, expectations and projections included in this presentation. Any number of factors could cause our actual results to be materially different from those expressed or implied in our forward

looking statements, including (without limitation): economic conditions in the United States and globally; domestic and global supply and demand for oil, natural gas liquids (“NGLs”) and natural gas; realized prices for oil,

natural gas and NGLs and volatility of those prices; the adequacy and availability of capital resources, credit and liquidity, including, but not limited to, access to additional borrowing capacity and our inability to generate sufficient cash flow from

operations to fund our capital expenditures and meet working capital needs; our ability to comply with restrictions imposed by our term loan credit agreement, secured and unsecured indentures, and other existing and future financing arrangements;

our ability to service our outstanding indebtedness; impairments of our natural gas, NGL and condensate asset values due to declines in commodity prices; conditions in the domestic and global capital and credit markets and their

effects on us; new or changing government regulations, including those relating to environmental matters, permitting or other aspects of our operations; the willingness and ability of the Organization of Petroleum Exporting Countries

to set and maintain oil price and production controls; the geologic quality of our properties with regard to, among other things, the existence of hydrocarbons in economic quantities; uncertainties inherent in the estimates of our natural

gas, NGL and condensate reserves; our ability to increase natural gas, NGL and condensate production and income through exploration and development; drilling and operating risks; counterparty credit risks; the success of our drilling

techniques in both conventional and unconventional reservoirs; the success of the secondary and tertiary recovery methods we utilize or plan to employ in the future; the number of potential well locations to be drilled, the cost to

drill, and the time frame within which they will be drilled; the ability of contractors to timely and adequately perform their drilling, construction, well stimulation, completion and production services; the availability of equipment, such as

drilling rigs, and infrastructure, such as transportation pipelines, processing and midstream services; the effects of adverse weather or other natural disasters on our operations; competition in the oil and gas industry in general, and specifically

in our areas of operation; changes in our drilling plans and related budgets; the success of prospect development and property acquisition; the success of our business and financial strategies and hedging strategies; uncertainties related to

the legal and regulatory environment for our industry, and our own legal proceeding and their outcome; and our ability to maintain the listing of our securities on the NASDAQ Capital Market or any other exchange on which our securities trade.

Further information on the risks and uncertainties that may affect our business is available in the company’s filings with the SEC, and we strongly encourage readers to review and understand those risks. We do not assume or undertake

any obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Presentation of Information The estimates of reserves in this presentation are based on a reserve report of our independent external reserve engineers

as of December 31, 2017. We believe the data we prepared and supplied to our external reservoir engineers in connection with their preparation of the December 31, 2017 reserve report, and the assumptions, forecasts, and estimates

contained therein, are reasonable; however we cannot assure that they will prove to have been correct. Estimates of reserves can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. In this presentation,

references to Rex Energy, Rex, REXX, the Company, we, our and us refer to Rex Energy Corporation and its subsidiaries. Unless otherwise noted, all references to acreage holdings are as of December 01, 2017 and are rounded to the

nearest hundred. All financial information excludes discontinued operations unless otherwise noted. All estimates of internal rate of return (IRR) are before tax. Hydrocarbon Volumes The SEC permits publicly-reporting oil and gas companies to disclose “proved reserves” in their filings with

the SEC. “Proved reserves” are estimates that geological and engineering data demonstrate with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions. SEC rules also permit

the disclosure of “probable” and “possible” reserves. Rex Energy discloses proved reserves but does not disclose probable or possible reserves. We may use certain broader terms such as “resource potential,” “EUR”

(estimated ultimate recovery of resources, defined below) and other descriptions of volumes of potentially recoverable hydrocarbons throughout this presentation. These broader classifications do not constitute “reserves” as defined by the SEC

and we do not attempt to distinguish these classifications from probable or possible reserves as defined by SEC guidelines. In addition, we are prohibited from disclosing hydrocarbon quantities that do not constitute reserves in documents filed with

the SEC. The company defines EUR as the cumulative oil and gas production expected to be economically recovered from a reservoir or individual well from initial production until the end of its useful life. Our estimates of

EURs and resource potential have been prepared internally by our engineers and management without review by independent engineers. These estimates are by their nature more speculative than estimates of proved, probable and possible

reserves and accordingly are subject to substantially greater uncertainty of being actually realized. We include these estimates to demonstrate what we believe to be the potential for future drilling and production by the company.

Ultimate recoveries will be dependent upon numerous factors including actual encountered geological conditions, the impact of future oil and gas pricing, exploration and development costs, and our future drilling decisions and budgets

based upon our future evaluation of risk, returns and the availability of capital and, in many areas, the outcome of negotiation of drilling arrangements with holders of adjacent or fractional interest leases. Estimates of resource

potential and other figures may change significantly as development of our resource plays provide additional data and therefore quantities that may ultimately be recovered will likely differ materially from these estimates.

Potential Drilling Locations

Our estimates of potential drilling locations are prepared

internally by our engineers and management and are based upon a number of assumptions inherent in the estimating process. Management, with the assistance of engineers and other professionals, as necessary, conducts a topographical analysts of our unproved prospective acreage to identify

potential well pad locations using operationally approved designs and considering several factors, which may include but are not limited to access roads, terrain, well azimuths, and well pad sizes. For our operations in Pennsylvania, we then

calculate the number of horizontal well bores for which the company appears to control sufficient acreage to drill the lateral wells from each potential well pad location to arrive at an estimated number of net potential drilling locations.

For our operations in Ohio, we calculate the number of horizontal well bores that may be drilled from the potential well pad and multiply this by the company’s net working interest percentage of the proposed unit and arrive at an estimate

number of net potential drilling locations. In both cases, we then divide the unproved prospective acreage by the number of net potential drilling locations to arrive at an average well spacing. Management uses these estimates to, among

other things, evaluate our acreage holdings and formulate plans for drilling. Any number of factors could cause the number of wells we actually drill to vary significantly form these estimates, including, without limitation, the

availability of capital, drilling and production costs, commodity prices, availability of drilling services and equipment, lease expirations and regulatory approvals. DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Executive Summary DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

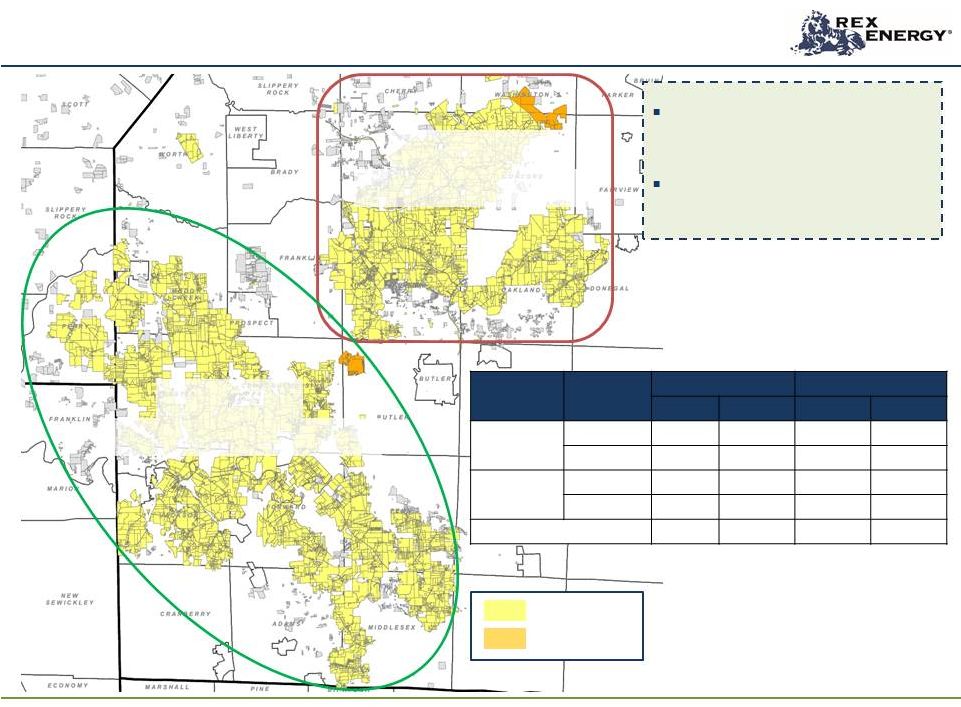

Company Overview

4

Appalachian Basin

Net

Acreage

~98,000

Warrior North

Net

Acreage

~11,800

Butler Operated

Net

Acreage

~76,000

Non-Operated

Net

Acreage

~10,200

Production

(1)

3Q17A

182.0 Mmcfe/d

4Q17E

~205.1

Mmcfe/d

4Q17E Exit Rate

~215.2 Mmcfe/d

2017E

~184.1 Mmcfe/d

2018E

250.0 –

260.0 Mmcfe/d

2019E

285.0 –

295.0 Mmcfe/d

Capital

Expenditures

(1)

2017 Net Operational

Capex

~$133.5 million

2018 Net Operational Capex

$105.0 -

$125.0 million

Estimated Production Growth Rate

35% -

45%

2019 Net Operational Capex

$60.0

-

$75.0

million

Estimated Production Growth Rate

10% -

20%

Total

Proved Reserves

2017 Base Proved Reserves/$PV10

3,848 Bcfe/$892.4 MM

2017 PDP Reserves/$PV10

969 Bcfe/$504.6

MM

Rex Energy is a pure-play Appalachian Basin focused company

targeting wet- gas windows in the Pennsylvania

Marcellus and Ohio Utica Shales (1)

Estimates based on Growth Plan

|

Investment Highlights 5 Best in Class Human Capital Safety is Rex Energy’s #1 priority Core team has been together for six years Rex’s success is directly correlated to its employees’ success

Focused on developing and retaining our existing

talent Ability to run 2-3 rig program with

current team High Quality Acreage

Position Highly contiguous acreage position in the

Appalachian Basin Large multi-year inventory of

~900+ gross/690 net liquids-rich drilling locations Average Working Interest: 74%; Average NRI: 63% 99% of acreage held by production Ready for multi-well pad development Multiple horizons: Upper Devonian, Marcellus and Utica formations

Current HBP holds all depths –

Marcellus, Upper Devonian Burkett, Dry Gas Utica and

Rhinestreet formations

Prolific

Resource

Proven formations: Marcellus, Upper Devonian and

Utica Derisked

existing acreage with over 200 gross wells placed into sales as

of 12/31/2017 Year-End 2017 PDP Reserves: 969

Bcfe; PV10: $504.6 million Year-End 2017 Base

Proved Reserves: 3,848 Bcfe; PV10: $892.4 million

Cost and Capital Efficiency Improvements

HBP acreage allows for flexibility in choosing future locations

to drill and complete Capital spend is focused on

best areas of the assets to maximize returns

Enhanced completion design and longer laterals results in

maximized financial returns Established supply

chain program that ensures Rex is getting the best value possible from its service providers Drilling and Completion Enhancements Average drilling days reduced to 11.1 days in 2017 vs. 16.6 days in 2014 while increasing lateral length by ~2,600’

during same period

Increased completion stages per day: 5.5 stages/day in 2017 vs.

4.1 stages/day in 2016; more recent jobs 7-10 stages / day Conducted a comprehensive performance analysis with third party engineering firm on over 160 wells to produce a more

optimal completion design

Comprehensive water management plans

Marketing and Processing Strategy

Recent NGL marketing agreement with BP allows for consistent

liquids cash flow and eliminates seasonality

Diversified marketing strategy and active hedging minimizes

exposure to large fluctuations in commodity prices and gas basis differentials Anchor/shipper with MarkWest facilities in Butler County Extensive Geology and Reservoir Insight Drilled over 220 wells in the Appalachian Basin Large inventory of logs and cores performed over the past six years

Developed best practices for optimal drilling performance and

completion techniques Minimal science required to

unlock optimal value DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Rex has secured ~928 gross/ ~690 net “wet gas” locations

Leasing additional infill acres in Moraine East potentially adds

~160 locations In addition to the “wet gas”

locations identified above, Rex has secured

approximately 400 dry gas Utica locations in the Butler Legacy and

Moraine East areas

Current HBP holds all depths –

Marcellus, Upper Devonian, Utica & Rhinestreet

“Wet Gas” Acreage and Well Counts

Area

Formation

Acres

Well Count

Gross

Net

Gross

Net

Legacy

Marcellus

63,000

44,300

251

177

Burkett

63,000

44,300

318

222

Moraine

East

Marcellus

36,000

31,700

175

141

Burkett

36,000

31,700

154

125

Warrior North

Utica

13,000

11,800

30

25

Total

211,000

163,800

928

690

“Stacked Pay” Effect

6

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Management Profiles

Tom Stabley –

President & Chief Executive Officer

Co-founder of Rex Energy in 2003 –

managed various partnerships

that eventually were consolidated into Rex Energy

Guided the company through reorganization and consolidation that

resulted in Rex Energy’s IPO in 2007 Over 20

years of expertise in capital markets, financial reporting, corporate finance and strategic planning Robert Ovitz – Chief Operating Officer Joined Rex Energy in 2014 Over 30 years of extensive technical experience in drilling, completions and HSE as well as leading and managing business

organizations within the E&P

space Prior to joining Rex, he was a Senior

Operations Manager for Noble Energy in the Appalachian Basin where he built Noble Energy’s operational team and presence in the basin

Curt Walker –

Chief Financial Officer

Joined Rex Energy in 2007

Over 15 years experience in accounting, financial reporting,

corporate finance and strategic planning Previous

experience with YRC Worldwide, a Fortune 500 company

Dave

Pratt –

Senior Vice President & Exploration Manager

Joined Rex Energy in 2008

Over 30 years experience as a senior geologist working on

projects located throughout the United States

Previous experience in geology with Cabot Oil & Gas, Texaco,

Sohio Petroleum and Ensource & Enstar Mike Eck

– Senior Vice President, Risk

Management Joined Rex Energy in 2010

Over 18 years experience in risk management, process

re-engineering and audit Responsible for the

oversight of Rex Energy’s HSE function, Procurement department and Internal Audit group F. Scott Hodges – Senior Vice President, Land & Business Development Joined Rex Energy in 2010 Over 20 years experience in acquisition and management of mineral and surface rights and business development

Previous experience as Regional Land Manager for Consol Energy

from 1997 - 2010

Mike

Endler –

Vice President, Basin Manager

Joined Rex Energy in 2011

Over 15 years experience in engineering and

operations Previous experience in consulting for

the oil and gas industry, specializing in surface facilities and water management Registered Professional Engineer Darren Springinatic – Senior Director, Marketing Joined Rex Energy in 2012 Over 15 years experience in oil and gas marketing in the U.S. and Canada

Previous experience in oil and gas marketing with Bonavista

Petroleum and Hunt Oil Abhinav Sharma

–

Director, Reservoir Engineering

Joined Rex Energy in 2010

Over 10 years experience in reservoir engineering

Masters in Petroleum Engineering from University of Texas,

Austin 7 |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

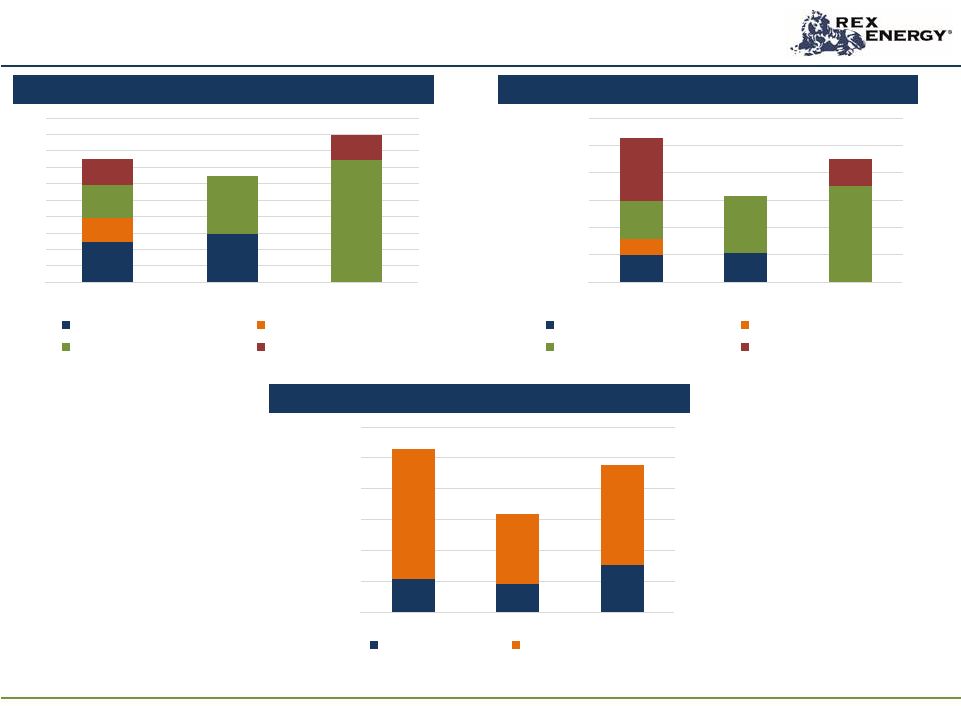

8

Production (Mmcfe/d)

(1)

LOE ($/Mcfe)

Key Metrics: 2014 –

2020E

Cash G&A ($/Mcfe)

154.4

183.8

195.3

180.0 –

190.0

250.0 –

260.0

280.0 –

300.0

290.0 –

310.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

2014

2015

2016

2017E

2018E

2019E

2020E

$1.94

$1.84

$1.78

$1.77 -

$1.82

$1.55 -

$1.60

$1.52 -

$1.57

$1.51 -

$1.56

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2014

2015

2016

2017E

2018E

2019E

2020E

$0.82

$0.75

$0.54

$0.23 -

$0.28

$0.15 -

$0.20

$0.14 -

$0.19

$0.14 -

$0.19

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

2014

2015

2016

2017E

2018E

2019E

2020E

(1)

Estimates based on Growth Plan

|

Joint Ventures DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Joint Venture Summary 10 Benefit Street Partners (BSP) $175.0 million in initial consideration with $134.0 million committed and funded to date BSP’s initial capital and well commitment has ended BSP has elected into an additional seven JV AMI wells to date at a working interest of 15% - 20% ArcLight All 32 wells have been drilled and placed into service $67.6 million contributed 17.5% reverts to Rex upon ArcLight achieving hurdle rate Sumitomo Through JV, Sumitomo has 30% interest in Legacy Butler AMI Other interests in non-operated areas Joint Venture Summary ($ in millions) Benefit Street Partners ArcLight Sumitomo Date March 2016 March 2015 August 2010 Type Joint Exp./Dev. Agreement Drilling Participation & Exploration Area Moraine East/Warrior North Legacy Butler/Moraine East Legacy Butler AMI Yes Wellbore Only Yes # of wells participated 47 32 139 Acres (Gross/Net) Warrior North: 6,679/1,336 ME: 36,668/5,985 -- Butler Legacy: 63,000/18,700 Partners WI% Initial Wells – 65% 35.0% 30.0% Consideration $175.0 -- -- Commitment $134.0 -- -- Contributed to Date $134.0 $67.6 -- Int. Reversion N/A IRR/ROI hurdle rates N/A Other BSP earned assigned of 15%-20% in acreage located within each unit -- -- DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Appalachia Benchmarking DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Marcellus Performance Benchmarking 12 EUR (Bcfe) / 1,000 ft. 3.18 3.25 2.15 2.40 2.71 2.46 2.16 2.00 2.95 2.40 2.52 4.40 2.66 1.60 Butler Central Butler South Moraine East Core Highly Rich Gas/Cond. Highly Rich Gas Rich Gas Dry Gas SW PA Wet SW PA Rich SW PA Dry Lower SW PA Condensate Source: Company presentations and filings, TPH Research, Wall Street consensus estimates as compiled by

FaceSet as of 12/14/2017

Note: Rex calculations based on November 2017 IR presentation.

Peers based on most recently disclosed Marcellus estimates Peers include AR, CNX, COG, ECR, EQT, and RRC REXX Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 D&C ($MM) / 1,000 ft. $0.89 $0.87 $0.92 $0.93 $0.93 $0.93 $0.93 $0.82 $0.86 $0.69 $0.94 $0.84 $0.86 Butler Legacy Moraine East Core Highly Rich Gas/Cond. Highly Rich Gas Rich Gas Dry Gas SW PA Wet SW PA Rich SW PA Dry Lower SW PA Condensate Median: $0.92 Median: 2.49 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Operational & Financial Benchmarking

(1)

13

2017E-2018E Production Growth

39%

17%

21%

14%

18%

28%

31%

18%

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Median:

18%

% Liquids (Reserve Based)

43%

7%

39%

35%

3%

7%

15%

18%

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Median:

15%

Production Investment Rate ($/Mcfed)

(2)

Inventory Life –

Years

(3)

$647

$2,203

$1,314

$1,586

$1,530

$1,366

$1,765

$2,475

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Median:

$1,586

37

23

18

19

29

6

15

12

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Median:

18

Source: TPH Research, Wall Street consensus estimates as compiled

by FactSet of 12/14/2017

Note: Rex forecasts and inventory calculations based on November

2017 IR Presentation Peers include AR, CNX, COG,

ECR, EQT, GPOR and RRC (1)

Based on Growth Plan projections

(2)

2018E

Capex spend/(2018E production less 2017E declined production).

Assumes 20% base decline for 2017E (3)

For Rex, based on 25 wells per year.

|

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Operational & Financial Benchmarking

(1)

14

Hedge Profile (% of 2018E Production)

(2)

56%

38%

73%

39%

1%

63%

74%

47%

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

2018E PDP

Hedge Profile:

64%

Median:

47%

In-Basin Sales Exposure (% of 2018E NG Production)

54%

48%

26%

54%

77%

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Median:

51%

G&A Burden (2018E G&A/Mcfe)

$0.17

$0.14

$0.13

$0.19

$0.07

$0.12

$0.12

$0.29

REXX

Peer 1

Peer 2

Peer 3

Peer 4

Peer 5

Peer 6

Peer 7

Median:

$0.13

Source: Company presentations and filings, TPH Research, Wall

Street consensus estimates as compiled by FactSet

as of 12/14/2017

Peers include AR, CNX, COG, ECR, EQT, GPOR and RRC

(1)

Based on Growth Plan projections

(2)

Includes volumes from all derivatives

|

Butler Operated Area DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Legacy Area Moraine East Rex 70%/Sumitomo 30% Rex ~85%/BSP ~15% Area Lease Status Acres Well Count Gross Net Gross Net Legacy HBP/HBO 62,500 43,950 564 395 Pending 500 350 5 4 Moraine East HBP/HBO 35,000 30,700 329 266 Pending 1,000 1,000 -- -- Total: 99,000 76,000 898 665 Butler Operated Area Currently control 898 potential “wet gas” locations in the Butler Operated Area ~99% of these locations are held by production/operations HBP/HBO Pending 16 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Gas pipeline from Moraine East Field Rex Energy Regional Office MarkWest Gas Processing Facilities Fresh Water Impoundment

Legacy Butler Operated Area

17

Contiguous acreage position of ~63,000 gross/44,300

net acres

Average working interest: 70%

Sumitomo JV: 30% WI in all wells

ArcLight: 35% WI in 16 wells (will revert to 17.5%)

Gross/Net Potential Locations: 569/399 based on 800’

spacing

Currently have 139 wells placed into sales:

127 Marcellus

10 Upper Devonian Burkett

2 Utica

Recent 5-day average wellhead inlet of 180

MMcf/d MarkWest

provides gas gathering and processing services

Total capacity: 410 MMcf/d

Capacity dedicated to Rex: 285 MMcf/d (inclusive

of JV partners); currently at 267 MMcf/d

Gas from Moraine East field flows into MarkWest

processing facility via Stonehenge pipeline

Four-Well Wilson Pad

Three extended laterals produced

at an average 5-day sales rate of

11.3 Mmcfe/d and 30-day sales

rate of 11.0 Mmcfe/d

Wells are still exhibiting strong

pressures

Legend:

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Enhanced Performance – Butler Legacy (1) Central 9.7 Bcfe EUR (80% ethane) 11.7 Bcfe EUR (80% ethane) 15.6 Bcfe EUR (80% ethane) 15.7 Bcfe EUR (80% ethane) 17.0 Bcfe EUR (80% ethane) 8.9 Bcfe EUR (55% ethane) 10.7 Bcfe EUR (55% ethane) 14.4 Bcfe EUR (55% ethane) 14.5 Bcfe EUR (55% ethane) 15.9 Bcfe EUR (55% ethane) 2013 2014 2015 2016 2017 Completion Reduced Cluster Spacing Reduced Cluster Spacing Reduced Cluster Spacing Reduced Cluster Spacing Reduced Cluster Spacing Gross Avg. 30- Day Wellhead Gas IP (Mcf/d) 3,175 3,683 4,736 4,458 4,234 1 Yr. Decline 50% 48% 44% 40% 33% Lateral Length 4,000’ 4,000’ 5,000’ 5,000’ 5,000 Stages / Spacing 27 / 150’ 33 / 150’ 33 / 150’ 33 / 150’ 33 / 150’ Frac Sand (#/ft) 1,800 2,000-2,200 2,200-2,500 2,200-2,500 2,200-2,500 All-In Cost $5.9 million $5.7 million $4.8 million $4.8 million $5.2 million WH EUR (bcf)/1,000’ 1.43 1.44 1.86 1.88 2.71 (1) See note on Hydrocarbon Volumes and disclaimers at beginning of presentation

18

17.3 Bcfe

EUR

(80% ethane)

16.2 Bcfe

EUR

(55% ethane)

2017

Reduced

Cluster

Spacing

5,535

36%

5,000

33 / 150’

2,200-2,500

$5.2 million

3.01

South

st

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Legacy Butler Marcellus Economics (1) Marcellus Economics (55% Ethane Recovery) (2) (1) See note on Hydrocarbon Volumes and disclaimers at beginning of presentation.

(2)

Economics reflect

55% ethane recovery.

(3)

Average 5-year C3+ differential approx. 52% of Oil, C2

differential approx. is 19% of Oil. (4)

Historical price differentials applied to Condensate. Gas price

differential dependent on future development plans and futures price differentials to Rex markets. (5) Strip Pricing as of 11.13.2017 – Oil: 2018: $56.63, 2019: $54.04, 2020: $52.47, 2021: $51.81 , 2022: $51.75 // Gas: 2018: $3.02, 2019: $2.92, 2020: $2.86, 2021: $2.87, 2022: $2.88 (6) 2016 EUR adjusted for net reserves 19 Butler Central 3rd Party YE16 Butler Central 3rd Party YE17 Butler South 3rd Party YE16 Butler South 3rd Party YE17 All-in Well Cost $6.0 million $6.0 million $6.0 million $6.0 million Lateral Length 6,700 ft 6,700 ft 6,700 ft 6,700 ft BCFE/1000ft (6) (55% C2) 2.21 3.18 2.12 3.25 % Liquids (55% C2) 35% 35% 28% 28% EUR (Bcfe) (6) 80% / 55% C2 15.8 14.8 22.8 21.3 15.1 14.2 23.1 21.7 IRR (3,4,5) $3.00 NYMEX Oil Price: 2017+: $60 34% 38% 25% 34% $3.00 NYMEX Oil Price: 2017+: $55 30% 33% 23% 30% $3.25 NYMEX Oil Price: 2017+: $55 36% 39% 29% 38% Strip Pricing 28% 31% 20% 28% Avg. 30-day sales rate (MMcfe/d) 8.0 – 11.0 8.0 – 11.0 8.0 – 11.0 8.0 – 11.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 0 2,000 4,000 6,000 8,000 10,000 12,000 0 10 20 30 40 50 60 Production Month Butler South -3rd Party YE16 Butler South -3rd Party YE17 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Butler Central -3rd Party YE16

Butler Central -3rd Party YE17

|

Production linearly adjusted to 5,000ft equivalent lateral

Plotted above are 28 representative wells in Butler

Central with RCS completions Butler Central Type Curve

Evolution- Adjusted

20

100

1,000

10,000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

Months

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Production linearly adjusted to 5,000ft equivalent lateral

Plotted above are 17 representative wells in Butler

South with RCS completions Butler

South

Type

Curve

Evolution-

Adjusted

21

100

1,000

10,000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

Months

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Moraine East DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Legend: Gas Pipeline (Stonehenge) Perm. In-Ground Waterline Stonehenge - high pressure discharge line to MarkWest processing facility Renick Impoundment Fleeger-2 Impoundment Oakland Twp. Impoundment Stonehenge – Renick Compressor Station Lake Oneida – primary water source Estimated current total to MarkWest: Legacy Butler - 180 MMcfd Moraine East - 87 MMcfd 267 MMcfd Moraine East Area 23 Contiguous acreage position of ~36,000 gross/31,700 net acres Average working interest: 85% Gross/Net Potential Locations: 329/266 based on 800’

spacing

Leasing additional acreage adds ~160 potential gross

locations

Currently have 37 wells placed into sales:

30 Marcellus

7 Upper Devonian Burkett

Recent 5-day average wellhead inlet of 87

MMcf/d Gas gathering and field compression by

provided by Stonehenge

Gas from Moraine East field flows into MarkWest

processing facility via Stonehenge pipeline

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Moraine East Area – Recent Developments 24 Three-well Manuel pad Drilled to an average lateral length of ~6,750 feet Placed into sales in 4Q17 Two-well Frye pad Drilled to an average lateral length of ~6,300 feet 24-hour sales rate per well of 9.4 Mmcfe/d On a per lateral foot basis, highest rates achieved in Moraine

East

30-day sales rate per well of 8.5 Mmcfe/d

Six-well Shields pad

24-hour sales rate per well of 9.2 Mmcfe/d

30-day sales rate per well of 7.9 Mmcfe/d

In-line with economic projections for 2017 Moraine East

program

Four-well Mackrell

pad

Drilled to an average lateral length of ~7,630

24-hour sales rate per well of 8.4 Mmcfe/d

Four-well Baird pad

24-hour sales rate of 10.1 Mmcfe/d

Two Marcellus wells produced at an average 24-hour sales

rate per well of 12.1 Mmcfe/d

Baird 4H produced 213 bbls/d of condensate, representing the

highest condensate rate achieved in the Butler

Operated Area 30-day sales rate of 7.3

Mmcfe/d Upcoming

developments

Fourth compressor station expected to be in service in early

January 2018

Four-well Kern pad expected to be placed into sales in March

2018 Average lateral length of

8,500’ 100% working interest

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Moraine East Sample Unit Development 25 Initial Development 2 nd Wave of Development 3 rd Wave of Development Future Development 3 wave of development will require new pad site Focus on one of the units (ie: southwest unit) Drill 8-12 wells with avg lateral length 6,000 - 7,000 feet Repeat process for next unit (ie: southeast unit) Initial development of 4 PDP Wells ~4,000 acres are held by production (HBP) within the units Initial wells hold all depths and formation Infrastructure designed to support future development Future development of the remaining ~20-40 wells will follow a similar process Using existing pads and infrastructure will provide strong capital efficiencies Anticipate developing 8 – 12 wells at a time 2 wave of development will focus on one of the units (ie: northeast unit) Use existing pad sites Drill 8-12 wells with avg lateral length 6,000 - 7,000 feet Repeat process for next unit (ie: southeast unit) nd rd DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Achievable Performance Improvements in ME 26 After analyzing the production data from existing

Moraine East wells the latest 2017 wells have been

completed with optimized completion

techniques. Proppant loading, stage size,

water ratio, treatment rates, and other

variables have been optimized to improve

performance of latest wells. These latest

wells have been placed at optimized lateral

spacing of ~800 ft. In the past, the Moraine East

adjacent wells were spaced between 600 to

750 ft. Performance of longer

laterals is being tested in the Shields

and Mackrell pads. One of the wells is

greater than 10,000 ft.

Frye wells, which were the last set of wells to be

completed in Moraine East, suggest that

the casing pressure is holding steady for

longer and the productivity of these

wells is superior to wells completed with

previous generation techniques.

Peak monthly production rates on per foot basis for

2017 ME wells are higher than earlier

generation completion wells at lower

choke size. With these optimized

techniques, Rex hopes to unlock more

reserves in the future wells in ME. 8 Gray

wells in the planning phase to be D&C in 2018.

Optimized Completions

Earlier Gen. Completions

0.48

0.45

0.49

0.55

0.46

0.46

0.70

0

10

20

30

40

50

60

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Fleeger

Gray

Renick

Fleeger-2

Shields

Mackrell

Frye

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Moraine East Economics (1) Marcellus Economics (55% Ethane Recovery) (2) (1) See note on Hydrocarbon Volumes and disclaimers at beginning of presentation.

(2)

Economics reflect

55% ethane recovery.

(3)

Average 5-year C3+ differential approx. 52% of Oil, C2

differential approx. is 19% of Oil. (4)

Historical price differentials applied to Condensate. Gas price

differential dependent on future development plans and futures price differentials to Rex markets. (5) Strip Pricing as of 11.13.2017 – Oil: 2018: $56.63, 2019: $54.04, 2020: $52.47, 2021: $51.81 , 2022: $51.75 // Gas: 2018: $3.02, 2019: $2.92, 2020: $2.86, 2021: $2.87 , 2022: $2.88 (6) 2016 EUR adjusted for net reserves 27 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 0 10 20 30 40 50 60 Production Month ME 3rd Party YE16 ME 3rd Party YE17 REX ME 2017 Program ME 3rd Party YE16 ME 3rd Party YE17 Rex ME 2017 Program All-in Well Cost $6.5 million $6.5 million $6.5 million Lateral Length 7,500 ft 7,500 ft. 7,500 ft. BCFE/1000ft (6) (55% C2) 1.34 1.74 2.15 % Liquids (55% C2) 39% 40% 39% EUR (Bcfe) (6) 80% / 55% C2 10.7 10.0 13.9 13.0 17.3 16.1 IRR (3,4,5) $3.00 NYMEX Oil Price: 2017+: $60 20% 21% 26% $3.00 NYMEX Oil Price: 2017+: $55 17% 18% 23% $3.25 NYMEX Oil Price: 2017+: $55 20% 21% 26% Strip Pricing 15% 16% 21% Avg. 30-day sales rate (MMcfe/d ) 6.5 - 9.5 5.0 – 8.0 5.0 – 8.0 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Production linearly adjusted to a 6,000ft equivalent lateral and adjusted for downtime

Average lateral length of existing wells is 6,600 ft.

Average lateral length for 2017 wells is 7,500 ft Wells production flattening since the onset of compression. New production behavior since

compression. PDP

Wells

(North

ME)

are

currently

tracking

1.94

bcfe/1000ft

type

curve.

More

data

needed

to

define

EUR

with

certainty.

Moraine East vs. Type Curve

Compression commencement

month for first 12 wells

28

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 Month DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Warrior North DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Warrior North Area 30 Contiguous acreage position of ~13,000 gross/11,800 net acres Average working interest: 95% Gross/Net Potential Locations: 30/25 based on 800’ spacing Currently have 25 wells placed into sales Gas gathering and field compression by provided by BlueRacer; gas processed at Natrium facility NGLs marketed by BlueRacer Wells average ~70% liquids production Strong optionality to condensate production TPL-7 BlueRacer gathering pipeline Three-well Jenkins pad placed into sales on 12/26/2017; 100% WI Seven-well Goebeler pad expected to be placed into sales in April 2018; 71% WI DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

(1) See note on Hydrocarbon Volumes and disclaimers at beginning of presentation.

(2)

Economics reflect

55% ethane recovery.

(3)

Historical price differentials applied to Condensate. Futures

differentials applied for gas production for all scenarios. (4) Average 5-year C3+ differential approx. 56% of Oil, C2 differential approx. is 15% of Oil.

(5)

Strip

Pricing

as

of

11.13.2017

–

Oil:

2018:

$56.63,

2019:

$54.04,

2020:

$52.47,

2021:

$51.81

,

2022:

$51.75

//

Gas:

2018:

$3.02,

2019:

$2.92,

2020:

$2.86,

2021:

$2.87

,

2022:

$2.88.

(6)

2016 EUR adjusted for net reserves

Warrior North Economics

(1)

3rd Party

YE16

3rd Party

YE17

Life Yield=54

3rd Party

YE17

Life Yield=60

Rex Upside

Case 2017

All-in Well Cost

$6.8 million

$6.8 million

$6.8 million

$6.8 million

Lateral Length

6,500 ft

6,500 ft

6,500 ft

6,500 ft

BCFE/1000ft

(6)

1.03

1.05

1.07

1.42

%

Liquids

51%

49%

50%

51%

EUR (MMBOE)

(6)

1.11

1.14

1.16

1.53

IRR

(3,4,5)

$60

52%

35%

43%

55%

40%

27%

33%

44%

43%

29%

35%

46%

40%

26%

32%

43%

Avg. 30-day sales rate (MBOE/d)

1.3 –

1.7

1.2 –

1.6

1.2 –

1.6

1.2 –

1.6

Warrior North Economics (55% Ethane Recovery)

(2)

31

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800 0 10 20 30 40 50 60 Production Month 3rd Party YE16 Rex Upside Case 2017 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

3rd Party YE17 LY=54 |

Transportation & Marketing DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Appalachian Basin Takeaway 33 Natural Gas Currently selling natural gas in the Gulf Coast and Northeast local

markets (DOMSP & TETCO)

Natural Gas Liquids (NGLs)

NGL’s are currently being sold in domestic markets

Upon Mariner East 2 commencement, a portion of Rex

NGL’s will be sold into international

markets Ethane

Rex sells ethane into international and domestic ethane

markets Canada (Mariner West), Europe (Mariner East)

and Mt. Belview (ATEX)

Marcus

Hook

Mont Belvieu

Perryville, LA

Freeport LNG

DOMSP

LNG Exports

& Mont Belvieu

Ethane Sales

Ethane &

NGL

Exports

Sarnia, Canada

Ethane Exports

Ethane Markets

NGL Markets

Gas Markets

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Marketing Summary 34 Warrior North Acreage dedication to BlueRacer for gathering and processing Gas is currently being sold into Dominion South (Dominion) and to M2 (TETCO) Rex will have access to Rockies Express, Rover, Leech Express and NEXUS on an interruptible basis Condensate purchased by Marathon Butler (Legacy) Acreage dedication to MarkWest for gathering/processing/compression 285mcf/d of priority capacity rights Gas sold into Dominion South (Dominion) and to the Gulf Coast (Dominion/Texas Gas) 3 ethane markets – Canada (Mariner West), Europe (Mariner East), Gulf Coast (ATEX) Condensate purchased by Marathon Moraine East Acreage dedication to Stonehenge for gathering & compression Gathering, compression can be expanded to over 400mcf/d Tiered volume pricing structure & Tiered minimum volume commitment (MVC) Ability to bank vols to use towards MVC Acreage dedication to MarkWest for processing Gas sold into Dominion South (Dominion) and to the Gulf Coast (Dominion/Texas Gas) 3 ethane markets – Canada (Mariner West), Europe (Mariner East), Gulf Coast (ATEX) Condensate purchased by Marathon DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Butler/Moraine East Map 35 8” MarkWest Ethane Pipeline connecting to Mariner West Mariner West Ethane Pipeline ATEX Ethane Pipeline Mariner East Ethane Pipeline Dominion Transmission Residue Pipeline DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Warrior North Map 36 Berne Plant Rex Energy Acreage Natrium Plant TPL-7 DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Natural Gas LOE vs. Revenue Deduct 37 Dom South vs. Gulf Coast ($0.65) ($0.14) ($0.05) ($0.67) Basis (Variable) Transport (LOE) Basis (Fixed) Transport (LOE) NYMEX $3.00 NYMEX $3.00 $2.21 Net Realized Price $2.28 Net Realized Price Rex residue gas is split 50/50 between two primary markets:

Gulf Coast

130,000 Firm Transportation

$0.67 Average Rate

100,000 Gulf Coast transportation began 11/1/2016, remaining

30,000 came online 4/1/2017. Increase in

LOE’s/decrease in basis began at the end of 2016, incremental increase in LOE/decrease in basis in 04/2017 Full year of Gulf Coast transport LOE/reduced basis will be realized in 2018

2016 Differential ($0.92)/LOE ($1.58). 2017 Differential

(~$0.30)/LOE (~$1.79). Dom South

158,000 Firm Transportation

$0.14 Rate

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Rex/BP NGL Deal Summary Bluestone C3+ NGL Sale • Rex Energy to sell all C3+ NGL products (less ME2 INEOS commitments) out of the Mark

West Bluestone Facility to BP at improved net back pricing. Term

of the deal is January 2018 – March

2021. •

Based on historic NGL price fluctuations, the new improved NGL

fixed differentials should result in increased

revenue over the term of the deal. •

Fixed NGL differentials, eliminate the seasonality out of

pricing, while mitigating the timing of wells being

placed into sales. •

Opportunity to enhance net back pricing with a barrel exchange

agreement. Other Enhancements

• BP assumed credit requirements to Texas Gas Transmission on behalf of Rex Energy.

38

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Reserve Summary DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Projected Reserves YE17 –

Aries Strip Runs

(1,2)

40

(1)

Strip Pricing as of 11.27.2017 –

Oil: 2018: $57.11, 2019: $53.93, 2020: $51.94, 2021: $50.72,

2022: $50.21// Gas: 2018: $2.95, 2019: $2.91, 2020: $2.87, 2021: $2.87, 2022: $2.88 (2) PV10 estimates do not include hedges NPV10 (MM$) Net Reserves (Bcfe) YE17 YE17 PDP $504,584 969 PNP $19,482 32 PUD $365,709 2,765 PROB $2,657 82 Total $892,432 3,848 YE17 Aries Strip Run contains Growth Plan development program along with ~$100MM net capital spend per year

program

until

2029.

Well

count

from

2021

–

2029

varies

from

18-26.

Most

wells

in

the

development

program

from

2021

–

2029

are

infills

that

are

already

proven

from

a

performance

standpoint. |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

$307

$9

$98

$71

$-

$20

$0

Butler

West Lawr

Moraine East

Warrior North

Westmoreland

$503

$9

$229

$131

[CELLRANGE]

$20

[CELLRANGE]

Butler

West Lawr

Moraine East

Warrior North

Westmoreland

(1)

Strip Pricing as of 11.27.2017 –

Oil: 2018: $57.11, 2019: $53.93, 2020: $51.94, 2021: $50.72,

2022: $50.21// Gas: 2018: $2.95, 2019: $2.91, 2020: $2.87, 2021: $2.87, 2022: $2.88 Growth Plan NPV10 Strip (1) by Area ($MM) YE17 PDP Only Growth Plan Run (1) YE17 Total Growth Plan Run (1) 41 892 $MM 505 $MM |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

(1)

Strip Pricing as of 11.27.2017 –

Oil: 2018: $57.11, 2019: $53.93, 2020: $51.94, 2021: $50.72,

2022: $50.21// Gas: 2018: $2.95, 2019: $2.91, 2020: $2.87, 2021: $2.87, 2022: $2.88 YE17 PDP Only Growth Plan Run (1) YE17 Total Growth Plan Run (1) 42 3,848 Bcfe Growth Plan Net Strip (1) Reserves by Area (Bcfe) 969 Bcfe 2,508 Bcfe 11 Bcfe 1,099 Bcfe 196 Bcfe 34 Bcfe Butler West Lawr Moraine East Warrior North Westmoreland 677 Bcfe 11 Bcfe 164 Bcfe 83 Bcfe 34 Bcfe [CELLRANGE] Butler West Lawr Moraine East Warrior North Westmoreland |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Growth Plan Reserves Data Sheet

43

Butler Legacy

Central

Butler Legacy

South

Moraine East

Warrior North

EUR (Bcfe)

21.3

21.7

13.0

6.8

EUR

(Mmboe)

3.6

3.6

2.2

1.1

%

Liquids

35%

28%

40%

49%

Lateral Length (ft.)

6,700

6,700

7,500

6,500

Well Cost ($MM)

$6.0

$6.0

$6.5

$6.8

Bcfe/1,000’

3.18

3.25

1.74

1.05

IRR @ Strip Pricing

31%

28%

21%

26%

IRR @ $3.00

gas / $60 oil

38%

34%

26%

35% |

Reserves – Key Takeaways 44 Rex continues to unlock more potential in Legacy Butler, Moraine East and Warrior North

Performed completion study with third party engineering firm to

optimize frac designs for

improvement in IPs and EURs

Currently completing wells with next generation frac

designs in Moraine East and Legacy

Butler

Frye wells, which were completed using optimized design, present

a possibility of upside to current type curves;

Frye’s are currently producing at a higher gas rate on a per foot basis at lower chokes in comparison to other wells Warrior North completion study is currently ongoing As presented in production performance slides, there is possible upside to 2017 type curves in

the near future; many wells in Legacy Butler are above 2017 type

curves Longer laterals in the 2018 drilling program

present the opportunity to improve economics

Currently, Rex’s core assets are nearly fully delineated and

HBP’d, providing the opportunity to

concentrate drilling on the best performing locations to maximize

NPV. DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Financial Strategy & Development Plan DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Financial Strategy 46 Increase cash flow in 2018 to achieve cash flow neutrality in 2019 and 2020 while still

achieving moderate growth (5% -

15%)

Utilize existing rig and completion contracts through current

terms while maintaining efficiencies and minimizing

termination fees Select highest return locations

while continuing to prove and exploit Moraine East

value

Optimize pad density, completion design and lateral length to

achieve strongest return Continue to optimize

existing production Continue strategy to improve key

operational matrix for the company Ability to access

capital markets DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Growth Plan –

Well Activity

47

Well Count Breakdown by Asset Area

Drilling & Completion Capex Breakdown

Capex Breakdown by Asset Area

0 2 4 6 8 10 12 14 16 18 20 2018 2019 2020 Butler Legacy South Butler Legacy Central Moraine East Warrior North $0 $20,000,000 $40,000,000 $60,000,000 $80,000,000 $100,000,000 $120,000,000 2018 2019 2020 Butler Legacy South Butler Legacy Central Moraine East Warrior North $0 $20,000,000 $40,000,000 $60,000,000 $80,000,000 $100,000,000 $120,000,000 2018 2019 2020 Drilling Completions |

DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

Growth Plan Key Metrics: 2017 –

2020

48

EBITDAX Growth ($MM)

LOE/Mcfe

184.1

255.2

288.5

297.3

2017

2018

2019

2020

$1.79

$1.58

$1.54

$1.53

2017

2018

2019

2020

$0.26

$0.18

$0.17

$0.17

2017

2018

2019

2020

$59.2

$123.0

$119.4

$123.0

2017

2018

2019

2020

Production Growth (Mmcfe/d)

Cash G&A/Mcfe |

Financial Projections – Growth Plan 49 2017A 2018E 2019E 2020E Average Daily Production (Mmcfe/d) 184.1 255.2 288.5 297.3 % Liquids Production 38% 45% 46% 46% Key Metrics EBITDAX (000s) $59,176 $122,994 $119,350 $122,968 LOE/Mcfe $1.79 $1.58 $1.54 $1.53 G&A/Mcfe $0.26 $0.18 $0.17 $0.17 Development Plan CAPEX (000s) $133,484 $114,741 $68,469 $95,383 Commodity Price Assumptions Oil $49.97 $56.25 $54.25 $54.00 Natural Gas $3.11 $2.88 $2.80 $2.80 Dominion South Basis Differential ($0.88) ($0.58) ($0.53) ($0.55) C3+ NGLs (% of NYMEX) 62% 58% 52% 52% Cash balance as of December 31, 2017 is $15.2 million. Assumes sale of Westmoreland Non-Op Assets in 2018; estimated annual EBITDAX contribution of $3.5 million.

Term Loan balance as of December 31, 2017 totaled approximately

$189.5 million. Assumes deleveraging

transaction. DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Financial Projections – Reduced Plan 2017A 2018E 2019E 2020E Average Daily Production (Mmcfe/d) 184.1 259.6 255.1 264.8 % Liquids Production 38% 44% 44% 44% Key Metrics EBITDAX (000s) $59,176 $124,841 $96,719 $107,087 LOE/Mcfe $1.79 $1.56 $1.60 $1.56 G&A/Mcfe $0.26 $0.18 $0.19 $0.19 Development Plan CAPEX (000s) $133,484 $69,590 $67,250 $69,953 Commodity Price Assumptions Oil $49.97 $56.25 $54.25 $54.00 Natural Gas $3.11 $2.88 $2.80 $2.80 Dominion South Basis Differential ($0.88) ($0.58) ($0.53) ($0.55) 50 Cash balance as of December 31, 2017 is $15.2 million. Term Loan balance as of December 31, 2017 totaled approximately $189.5 million.

Assumes deleveraging transaction.

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Opportunities and Risks 51 Opportunities and Risks to Plan Achievement Opportunities Risks Most recent base production has exceeded production profile Recent well performance has exceeded current type- curves Continue to drive procurement efficiencies by bundling services and driving competition Maximize efforts to mitigate legacy production declines Continue to employ efficient and lean overhead operations Financial flexibility allows for acceleration while HBP status allows for maximum capital efficiency Commodity prices, ability to participate in improved price environment Ability to access capital markets Availability and consistency of service crews when not running a full 12-month development program Performance and efficiency of processing and midstream operations Commodity prices and ability to hedge at attractive levels

Access to capital markets/ability to refinance delayed

draw term loan

Retaining technical staff and continuity of internal

resources

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |

Appendix: Hedge Positioning DRAFT FRE 408 Settlement Communication; Not admissible for any purpose; For discussion purposes only

|

Hedge Position (1) 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% Natural Gas Oil & Condensate C2 C3+ NGLs Consolidated 2018 2019 2020 Avg. Floor: $2.97 Avg. Floor: $2.73 Avg. Floor: $47.68 Avg. Floor: $47.15 Avg. Floor: $12.93 Avg. Floor: $12.90 Avg. Floor: $33.30 Avg. Floor: $26.15 Avg. Floor: $2.70 Avg. Floor: $52.88 Avg. Floor: $12.79 Avg. Floor: $31.16 (1) Hedging position as of 1/1/2018; percent hedged based on PDP

53

64%

60%

37%

DRAFT

FRE 408 Settlement Communication; Not admissible for any purpose;

For discussion purposes only |