Attached files

| file | filename |

|---|---|

| 8-K - SWK Holdings Corp | e17544_swkh-8k.htm |

Collaborative Approach to Life Science Financing

Forward - looking and Cautionary Statements Statements in this presentation that are not strictly historical, and any statements regarding events or developments that we be lieve or anticipate will or may occur in the future are "forward - looking" statements within the meaning of the federal securities laws. There are a number of important fact ors that could cause actual results, developments and business decisions to differ materially from those suggested or indicated by such forward - looking statements an d you should not place undue reliance on any such forward - looking statements. Additional information regarding the factors that may cause actual results to differ mat erially from these forward - looking statements is available in our SEC filings, including our 2016 Annual Report on Form 10 - K and our Quarterly Reports on Form 10 - Q for subsequent periods. The Company does not assume any obligation to update or revise any forward - looking statement, whether as a result of new information , future events and developments or otherwise. Our specialty finance and asset management businesses are conducted through separate subsidiaries and the Company conducts its operations i n a manner that is excluded from the definition of an investment company and exempt from registration and regulation under the Investment Compan y A ct of 1940. This presentation is neither an offer to sell nor a solicitation of any offer to buy any securities, investment product or in ves tment advisory services, including such services offered by SWK Advisors LLC. This presentation does not contain all of the information necessary to make an investment decision, including, but not limited to, the risks, fees and investment strategies of investing in life science investments. Any offering is made only pursuant to the relevant information memorandum, a relevant subscription agreement or investment management agreement, and SWK Advisors LLC’s Form ADV, all of which must be read in their entirety. All investors must be “accredited investors” and/or “qualified purchasers” as defined in the securities laws before they can invest with SW K Advisors LLC. Life science securities may rely on milestone payments and/or a royalty stream from an underlying drug, device, or product which may or may not have received approval of the Food and Drug Administration (“FDA”). If the underlying drug, device, or product does not receive FDA approval, it could negatively impact the securities, including the payments of principal and/or interest. In addition, the introduction of new drugs, devices, or products onto the market could negatively impact the securities, since that may decrease sales and/or prices of the underlying drug, device, or product. Changes to Medicare reimbursement or third party payor pricing could negatively impact the securities, since they could negatively impact the prices and/or sales of the underlying drug, device, or product. There is also risk that the licensing agreement that governs the payment of royalties may terminate, which could negatively impact the securities. There is also the risk that litigation involving the underlying drug, device, or product could negatively impact the securities, including payments of principal and/or interest on any securities. 2

CORPORATE OVERVIEW

SWK Holdings Overview • SWK provides custom financing solutions for commercial - stage healthcare companies and royalty owners • Deploy balance sheet capital into secured financing portfolio ̶ Market capitalization at 11/30/17 was $ 140mm, 65% of 9/30/17 stockholders equity of $ 217mm • SWK targets $5mm to $20mm financings , a market niche it believes is largely ignored by larger market participants and generates attractive full - cycle returns • SWK targets unlevered, mid - teens return on capital ̶ 9/30/17 portfolio effective yield: 14.0% * • Life science business launched in 2012; since inception of business strategy SWK has completed financings with 26 different parties deploying $ 374mm of capital, including partner co - investments • Financings with 18 parties in current portfolio; ten exits since inception • Business focus is secured financings and royalty monetizations , but will selectively consider equity - like opportunities • Corporate goals: ̶ Increase book value per share at a 10%+ CAGR ̶ Be recognized as partner of choice for life science companies and inventors seeking $20mm or less ̶ Generate current income to utilize SWK’s substantial NOL asset, $ 405mm at 9/30/17 • Experienced and aligned management and Board 4 CORPORATE OVERVIEW *Effective yield is the rate at which income is expected to be recognized pursuant to the Company’s revenue recognition policies , if all payments are received pursuant to the terms of the finance receivable; excludes warrants

Why Life Science Finance? • Achieve high current yield from investment in non - correlated assets ̶ Invest in royalty, revenue, equity & debt interests from healthcare companies, research institutions and inventors ̶ Structured debt: high coupon drives current yield and warrants provide equity upside; backed by collateral value and lender rights in downside scenario ̶ Royalties: strong underlying existing cash flow profile without material exposure to corporate costs • Access to capital is challenging for small/medium sized life science companies ̶ Unlike larger private - lending verticals, few participants exist for sub - $20mm life science financings ̶ Traditional alternatives to primary equity and convertible debt typically highly dilutive and difficult to execute • Life science products are highly portable among marketing organizations ̶ Approved & marketed products and/or royalty streams are valuable collateral regardless of corporate cash burn ̶ Small products often do not justify stand - alone sales force costs and can be highly accretive to larger companies ̶ Once ingrained into therapeutic practice, many products continue to ‘sell’ themselves • Revenues are predictable and have low correlation to economic growth and macro factors ̶ Product launch curves are relatively stable with much supporting data from comparables ̶ Given long approval times, competition is often identifiable up to a decade in advance • Mitigate FDA & clinical trial risk by focusing on commercial opportunities ̶ Diligence focuses on product necessity, intellectual property exclusivity, regulatory moat, competitive threats, reimbursement, and marketer ability and financial stability 5 CORPORATE OVERVIEW

Experienced Team • SWK’s investment professionals have extensive experience financing life science companies • CEO Winston Black has been active in life science structured finance asset class since 2007 when he helped manage a multi - billion dollar healthcare portfolio for a large investment firm and helped develop the royalty financing market • CEO Winston Black has financed life science companies for more than a decade and has experience in operations, public markets investing, and restructurings • Management has experience investing across the capital structure and understands various stakeholders’ incentives • The team has a broad network of clinical, financial, and legal experts • Experienced financial, accounting, and legal team combining in - house resources with veteran outsourced providers • SWK is 69% owned by Carlson Capital, a multi - billion dollar, Dallas - based asset manager ̶ Two Carlson representatives are on SWK’s Board of Directors • SWK’s Board of Directors provides wealth of investment, operational and corporate governance experience 6 CORPORATE OVERVIEW

Corporate Milestones 7 Pre - 2012 2012 2013 2014 2015 2016 2017 • Predecessor Kana Software assets sold to Kay Technologies; $450 million+ NOLs remained at sale • SWK exists as public shell • Winston Black and Brett Pope hired to launch life science technology finance strategy • Holmdel formed and acquired U.S. marketing rights to InnoPran XL • $113MM raised through private placement and rights offering • Ended year with $102MM income producing assets • Team rebuilt and investment process improved • Ended year with $143MM income producing assets • Winston Black named CEO • 1/10 effective reverse stock split • Ended year with $108MM income producing assets • Holmdel sold – 3.5x CoC return CORPORATE OVERVIEW • Ended year with $37.2MM income producing assets

Value Creation Strategy • Deploy balance sheet capital into secured financing portfolio ̶ $5mm to $20mm loan and royalty market sports attractive, low - to - mid teens yields ̶ SWK has established reputation as a go - to capital provider for this underserved market ̶ Majority of financings structured with warrants or other upside features • Evaluate and pursue product acquisition opportunities ̶ Leverage SWK contacts, infrastructure, and lessons learned from Holmdel success ̶ Potential to use greater percentage of NOLs • Secure additional capital to boost ROE ̶ SWK targets a 10%+ ROE ̶ SWK currently has no leverage while similarly sized BDCs often sport 50% to 75% debt/equity leverage ̶ SWK will selectively consider other forms of outside capital including asset management arrangements • Selectively consider new capital deployment opportunities ̶ SWK’s core competency is life science finance but is willing to consider other capital deployment options that could utilize the company’s substantial NOLs • SWK believes this strategy can achieve a 10%+ book value per share CAGR 8 CORPORATE OVERVIEW

*Private warrants carried at zero cost Portfolio Overview: 9/30/17 9 Royalty 23% First Lien 69% Second Lien 6% Equity 1% Public Warrants 1% • GAAP Value: $ 168.4MM • Finance Receivables: $ 163.7MM • Marketable Securities: $3.3MM • Public Warrants: $1.4MM * Portfolio Value • Actively Financed Entities: 18 • Avg. GAAP Balance per Entity: $9.2MM • Total Unfunded Commitments: $8.3MM • Non - Accrual Balance: $19.0MM Metrics CORPORATE OVERVIEW

SWK Key Statistics 10 * Defined as finance receivables, marketable investments and investment in unconsolidated entity less non - controlling interests ** Eliminates provision for income taxes and non - cash mark - to - market changes on warrant assets and liability; see reconciliation on page 44 CORPORATE OVERVIEW

SWK Targets Low - to - Mid Teens Effective Yields 11 *Includes non - accruals; Excludes warrants **Includes non - accruals; Effective yield is the rate at which income is expected to be recognized pursuant to the Company’s revenue recognition policies, if all payments are received pursuant to the terms of the finance receivable; excludes warrants CORPORATE OVERVIEW

SWK Employs a Lean Cost Structure 12 • SWK is internally managed and does not engage outside advisors to fulfill the investment function • Management receives a fixed salary and participates in a bonus pool based on the Company’s annual pre - tax profit CORPORATE OVERVIEW 0.0% 0.5% 1.0% 1.5% 2.0% $2.0 $2.5 $3.0 $3.5 $4.0 Over the Past Two Years, G&A Expense Has Averaged 1.5% of Total Assets ($ in millions) LTM G&A Expense (mm) LTM G&A Expenses % of Avg. Total Assets

INVESTMENT PROCESS

Underwriting Process Overview Sourcing Initial Analysis and Screening Detailed Diligence Preliminary Term Submission Investment Committee Approval and Term Sheet Monitoring Legal Documentation 14 • Financing prospects are sourced via proprietary network and brokers • Initial diligence focuses on medical and commercial viability, corporate financial performance, and management credibility • Assuming prospect passes first screen, SWK undertakes multi - week diligence process using primary research coupled with third - party consultants to generate an independent assessment of collateral value • SWK underwrites to maximum of 40% LTVs • SWK creates scenarios to stress test valuation and cash flow forecasts • Assuming justified by diligence, SWK submits preliminary terms • Post acceptance of preliminary terms, SWK formally presents investment presentation to committee for approval • Post investment committee approval, SWK submits a formal term sheet • Term sheet has “outs” for IP review and other detailed diligence • SWK works with top - tier law firm to paper legal documentation • Time to close from initial contact is generally six weeks to three months • Ongoing monitoring of investment performance through borrower financial review, prescription volume monitoring, industry trends, etc. INVESTMENT PROCESS

Sourcing • SWK has a well - developed and diversified sourcing network ̶ SWK balances proprietary opportunities with deal flow from trusted, boutique investment banks and brokers • SWK typically faces limited competition due to proprietary sourcing network and focus on sub - $20mm financings • The seven deals completed in 2016 were sourced from a variety of relationships: 15 Boutique HC Ibanks Private equity relationship Prior financing discussion Co - lender relationship Board relationship In - bound due to SWK being public INVESTMENT PROCESS

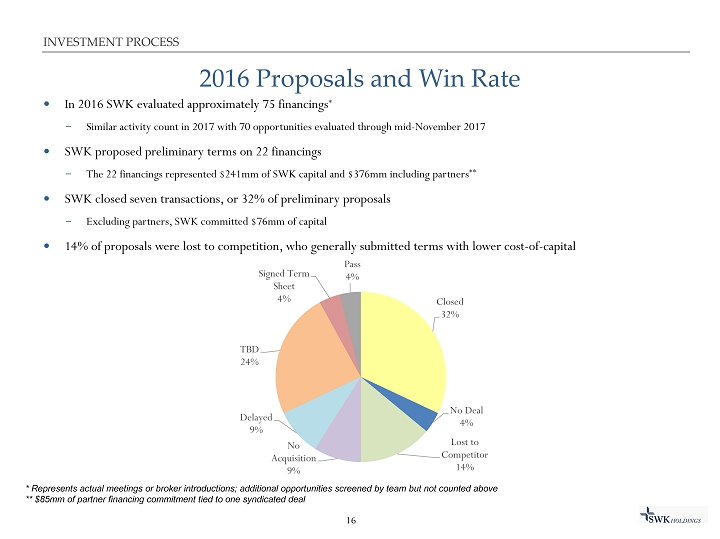

2016 Proposals and Win Rate • In 2016 SWK evaluated approximately 75 financings * ̶ Similar activity count in 2017 with 70 opportunities evaluated through mid - November 2017 • SWK proposed preliminary terms on 22 financings ̶ The 22 financings represented $241mm of SWK capital and $376mm including partners ** • SWK closed seven transactions, or 32% of preliminary proposals ̶ Excluding partners, SWK committed $76mm of capital • 14% of proposals were lost to competition, who generally submitted terms with lower cost - of - capital * Represents actual meetings or broker introductions; additional opportunities screened by team but not counted above ** $85mm of partner financing commitment tied to one syndicated deal 16 Closed 32% No Deal 4% Lost to Competitor 14% No Acquisition 9% Delayed 9% TBD 24% Signed Term Sheet 4% Pass 4% INVESTMENT PROCESS

Diligence Process • SWK’s diligence process is anchored by the “four Cs” of credit analysis: Collateral, Character, Capacity, and Capital • Collateral value is ascertained through analysis of medical and commercial need, market size, IP, and potential strategic buyers and historical transaction valuations • Character is validated through a review of management’s historical track record and current incentives, multiple meetings, and independent channel checks • Capacity to service debt is confirmed through scenario financial modeling of base, downside, and management cases • Capital analysis focuses on company’s ability to raise funds from existing shareholders, public market offerings, or strategic partnerships 17 INVESTMENT PROCESS

CURRENT PORTFOLIO

9/30/17 Portfolio Overview Financing (Month Closed) Type Primary Product Product Marketer Funded Amount / Principal GAAP Value Effective Rate Besivance (4/2013) Royalty Ophthalmic antibiotic Valeant $6.0mm $2.9mm N/A Cambia (4/2013 & 6/2015) Royalty NSAID migraine treatment Depomed $8.5mm $ 8.0mm N/A Forfivo XL (7/2016) Royalty Depressive disorder treatment Alvogen $6.0mm $5.4mm N/A Narcan (12/2016) Royalty Opioid overdose treatment Adapt $17.5mm $17.1mm N/A Secured Royalty (7/2013) Royalty Women’s health Duchesnay $3.0mm $1.5mm 11.5 %* Tissue Regeneration Therapeutics (6/2013) Royalty Umbilical cord banking Various $3.3mm $ 3.7mm N/A ABT (1/2016) First Lien PET biomarker generator Self $6.4mm $6.4mm Prime + 3.25% ABT (10/2014) Second Lien Royalty PET biomarker generator Self $10.0mm $10.9mm N/A * B&D Dental (12/2013) First Lien Dental consumables Self $8.1mm $8.1mm LIBOR +13.0 %* B&D Dental (3/2017) Equipment Financing Dental consumables Self $0.1mm $0.1mm 16.3% 19 *Non - accrual; default interest rate may apply CURRENT PORTFOLIO

9/30/17 Portfolio Overview (Continued) Financing (Month Closed) Type Primary Product Product Marketer Funded Amount / Principal GAAP Value Coupon Rate Celonova (7/2017) First Lien Medical device Self and Boston Scientific $7.5mm $ 7.4mm LIBOR (2.0% floor) +11.0% DxTerity Diagnostics (7/2015) First Lien Diagnostics Self $7.5mm $ 7.4mm LIBOR (1.0% floor) +12.25% Hooper Holmes (5/2017) First Lien Health and wellness Self $6.5mm $ 5.7mm LIBOR (1.0% floor) +12.5% Hooper Holmes (5/2017) Revolving Health and wellness Self $2.0mm $2.0mm LIBOR (1.0% floor) +12.5% Hooper Holmes (8/2017 ) First Lien Health and wellness Self $2.0mm $2.0mm LIBOR (1.0% floor) +12.5% Imprimis Pharmaceticals (7/2017) First Lien Pharmacy Self $9.7mm $ 9.1mm LIBOR (1.5% floor) +10.5% Keystone Dental (5/2016) First Lien Dental implants Self $20.0mm $19.9mm LIBOR (1.0% floor) +12.0% Orametrix (12/2016) First Lien Orthodontic consumables Self $8.5mm $8.4mm LIBOR (1.0% floor) +11.0% Parnell Pharmaceuticals (11/2016 ) First Lien Animal health Self $13.5mm $ 14.6mm 13.0% 20 CURRENT PORTFOLIO

9/30/17 Portfolio Overview (Continued) 21 Financing (Month Closed) Type Primary Product Product Marketer Funded Amount / Principal GAAP Value Coupon Rate Soluble Systems (6/2015) First Lien Wound care Self $ 14.8mm $ 14.8mm LIBOR (1.0% floor) +10.25% Tenex Health (7/2016) First Lien Sports medicine treatment Self $6.0mm $5.7mm LIBOR (1.0% floor) +12.0% Thermedx (5/2016) First Lien Fluid management device Hill - Rom $3.5mm $4.0mm N/A Cancer Genetics (10/2015) Public Equity Diagnostics Self N/A $1.8mm N/A Hooper Holmes (3/2016) Public Equity Health and wellness Self N/A $ 0.05mm N/A Public Warrants (Various) Warrants Various Various N/A $1.4mm N/A CURRENT PORTFOLIO

REALIZATIONS AND CASE STUDIES

Portfolio Realizations • SWK has exited ten financings for a total 1.2x CoC return and 12% weighted average IRR ̶ Eight resulted in positive realizations with a cumulative 1.4x CoC and weighted average 26% IRR ̶ SynCardia position was sold to distressed private equity firm with SWK recouping 58% of principal ̶ Response Genetics was taken through Chapter 11 and sold to a strategic buyer for cash and CGIX stock o Based on the 11/30/17 value of SWK’s CGIX stock, Response Genetics recovery has totaled 58% of principal 23 REALIZATIONS AND CASE STUDIES $ in 000s Investments Origination Payoff Cost Proceeds CoC IRR Notes Nautilus 12/05/12 12/17/13 22,500$ 28,269$ 1.3x 26% Parnell 01/23/14 06/27/14 25,000 27,110 1.1x 21% PDI 10/31/14 12/22/15 20,000 25,028 1.3x 23% Tribute 08/08/13 02/05/16 14,000 18,367 1.3x 16% Excludes value of warrants Galil 10/31/14 06/15/16 12,500 16,601 1.3x 21% Nanosphere 05/14/15 06/30/16 10,000 14,362 1.4x 48% Excludes value of final potential earn-out Syncardia First 12/13/13 06/24/16 12,790 8,524 0.7x -34% Syncardia Second 12/13/13 06/24/16 5,910 3,255 0.6x -58% Syncardia Preferred 09/15/14 06/24/16 1,500 - 0.0x -100% Response Genetics 07/30/14 10/07/15 12,257 7,056 0.6x -33% Includes 11/30/17 value of CGIX equity Holmdel 12/20/12 02/23/17 6,000 20,920 3.5x 63% Hooper 04/17/15 05/12/17 5,000 6,801 1.4x 21% Excludes value of warrants Total Realized / Wtd. Avg 147,457$ 176,291$ 1.2x 12%

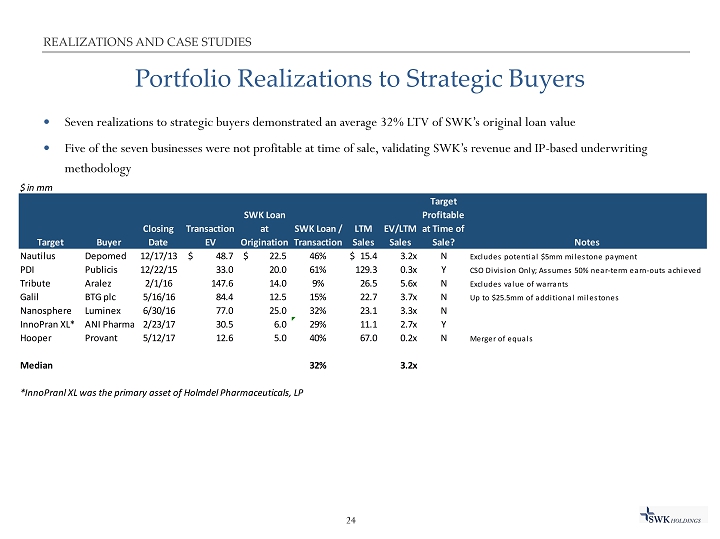

Portfolio Realizations to Strategic Buyers • Seven realizations to strategic buyers demonstrated an average 32% LTV of SWK’s original loan value • Five of the seven businesses were not profitable at time of sale, validating SWK’s revenue and IP - based underwriting methodology 24 REALIZATIONS AND CASE STUDIES $ in mm Target Buyer Closing Date Transaction EV SWK Loan at Origination SWK Loan / Transaction LTM Sales EV/LTM Sales Target Profitable at Time of Sale? Notes Nautilus Depomed 12/17/13 48.7$ 22.5$ 46% 15.4$ 3.2x N Excludes potential $5mm milestone payment PDI Publicis 12/22/15 33.0 20.0 61% 129.3 0.3x Y CSO Division Only; Assumes 50% near-term earn-outs achieved Tribute Aralez 2/1/16 147.6 14.0 9% 26.5 5.6x N Excludes value of warrants Galil BTG plc 5/16/16 84.4 12.5 15% 22.7 3.7x N Up to $25.5mm of additional milestones Nanosphere Luminex 6/30/16 77.0 25.0 32% 23.1 3.3x N InnoPran XL* ANI Pharma 2/23/17 30.5 6.0 29% 11.1 2.7x Y Hooper Provant 5/12/17 12.6 5.0 40% 67.0 0.2x N Merger of equals Median 32% 3.2x *InnoPranl XL was the primary asset of Holmdel Pharmaceuticals, LP

Historical Financing: Holmdel Pharmaceuticals, LP • In December 2012 SWK acquired a limited partnership interest in Holmdel Pharmaceuticals • Holmdel subsequently acquired U.S. marketing rights to InnoPran XL, a non - selective beta blocker with dosing technology to coincide with the body’s natural circadian rhythm • SWK partnered with an accomplished operator that handled marketing, distribution, and reimbursement functions • SWK and a financial partner contributed $13.0mm with the operating partner contributing $1.5mm in cash, an additional product’s cash flows, and operating expertise • SWK’s structure aligned incentives by allowing the operator to increase its share of the economics from 10% to 55% upon achieving return milestones • InnoPran XL sales grew from $5mm in 2012 to $13mm in 2015 • The first milestone was achieved in mid - 2016, more than doubling the operator’s economics • In February 2017, InnoPran XL sold for $30mm; SWK received an $8mm distribution • Investment generated a 3.5x CoC return and 63% IRR • SWK and the operating partner have evaluated purchasing additional assets 25 REALIZATIONS AND CASE STUDIES

Current Financing: Narcan Royalty • Narcan is the only FDA approved, intranasal Naloxone product for the treatment of opioid overdose • Narcan is appropriately priced with revenue growth from expanded distribution, not price hikes • Opiant is a publicly traded drug development company that receives a royalty on Narcan for developing the drug’s unique formulation ̶ Opiant’s novel formulation has a faster time to onset and more convenient and safer administration compared with injectable Naloxone • The product is marketed by Adapt Pharma, a private pharmaceutical company founded by former Azur Pharmaceutical executives with a history of strong sales execution • Opiant needed capital to pursue development programs • At time of monetization, Opiant was a thinly traded OTC stock and management believed the share price did not reflect underlying asset value, thus a share offering was not an attractive option • SWK structured a capped royalty that was smaller than competing proposals by larger royalty investors, and allowed Opiant to retain tail economics • In December 2016 SWK funded $13.8mm in exchange for a royalty that is capped at a 1.5x CoC return ̶ On August 8, 2017 upon achieving $25mm in cumulative sales during two consecutive quarters, SWK funded additional $3.8mm with a 1.5x CoC return cap ̶ SWK will retain a residual royalty ranging from 5% to 10% • Since closing, Narcan sales have exceed original forecasts 26 REALIZATIONS AND CASE STUDIES

Historical Financing: Galil Medical • Galil is a medical device company that delivers innovative cryotherapy solutions for tumor ablation • In 2014 the privately - held company was on the cusp of accelerating revenue growth, but was not yet cash - flow positive and could not tap traditional financing channels • Galil needed additional capital to run clinical trials and expand its sales force • In December 2014, SWK provided a $12.5mm senior secured term loan structured to delay principal repayment until growth initiatives matured ̶ Term loan was structured at a mid - teens cost of capital with a return cap if Galil was sold in first fifteen months • In late 2015, SWK committed to provide additional financing to support Galil’s proposed acquisition of a competitor ̶ The transaction was not consummated, but SWK’s support permitted opportunistic bid • By early 2016, the growth initiatives were bearing fruit and in June 2016 Galil was acquired by BTG plc for $84mm plus up to $26mm in earn - outs • The SWK facility gave Galil capital to grow the business and garner a higher acquisition price while allowing the equity owners to capture maximum upside • SWK facility represented 15% LTV of the take out price • SWK generated a 1.3x cash - on - cash return and 20% IRR 27 REALIZATIONS AND CASE STUDIES

Historical Financing: SynCardia • SynCardia manufactures and markets the only FDA - approved artificial heart • SWK’s original thesis: ̶ Device approved in US and EU; positive efficacy in over 1,300 implants ̶ Device reimbursed at $125,000 in US and $70,000 outside the US ̶ Large and untapped market with over 4,000 patients on US heart transplant waitlist ̶ Funding expected to facilitate marketing to achieve break - even level of implants ̶ Discussions with key heart transplant surgeons validated technology and verified need to exist ̶ Unique positioning and existing sales thought to provide strategic value exceeding investment • December 2013 SWK invested $10mm in two tranches alongside existing first lien lender ̶ Over the next two years SWK invested additional $4mm in company with Syncardia raising ~$30mm in aggregate during that time span • In late 2015 Syncardia failed to complete an IPO, prompting a funding crisis ̶ SWK purchased co - lender’s first lien position for 58% of par and commenced operational restructuring ̶ Restructuring efforts led to cost cuts and implant pre - sales that preserved liquidity • In 4Q15 SWK wrote down the position from ~$20mm to $12.5mm due to failed IPO and challenges • In May 2016 SWK sold entire position to private equity buyer for $7.2mm cash and 5% share in profits once the PE firm received a 3x CoC return • Key lessons learned: ̶ Disparate equity ownership prohibited capital raise under stressed conditions ̶ SWK underappreciated product’s need for engineering improvements to drive sustainable gross margin ̶ SWK underappreciated controversial nature of product with strategics as well as a large portion of physicians 28 REALIZATIONS AND CASE STUDIES

MISCELLANEOUS

SWK Value Proposition to Partners • SWK’s asset base and nimble structure position it to serve the sub - $20mm financing market ̶ Smaller companies often don’t have financial profile to qualify for traditional financing sources ̶ Companies in this niche often have few options outside of a dilutive equity raise ̶ The IPO market is largely closed to companies of this size requiring expensive and difficult private equity sourcing ̶ Many alternative financing sources have grown too large to care about smaller companies ̶ Some historical financing sources have been acquired by regulated financial institutions that due to regulatory constraints cannot lend to unprofitable companies and prohibit SWK - style transactions ̶ Venture lenders often require principal payback over a shorter period than SWK’s structure • SWK structures financings to preserve liquidity and match a growing company’s revenue profile • SWK provides its borrowers with access to its network of capital markets resources and operators • While SWK focuses on the sub - $20mm market, through its RIA arm it can access additional capital to finance larger opportunities 30 MISCELLANEOUS

Financing Structures • Structured debt ̶ Primarily first lien senior secured loans, though will selectively evaluate second lien opportunities ̶ Typically include covenants, prepayment penalties, origination and exit fees, and warrant coverage ̶ Provide working capital to support product commercialization and M&A • Royalties ̶ Companies: fund pipeline development & leverage a lower cost of capital for higher return on investment projects ̶ Institutions: capital planning for operating budgets, funding R&D initiatives, & financial asset diversification ̶ Inventors: financial asset diversification, fund start - up company • Synthetic Royalty ̶ Marketer creates a ‘royalty’ by selling an interest in a future revenue stream earned with a single product or basket of products in exchange for an upfront payment and potential future payments ̶ Ability to structure tiered revenues, reverse tiers, minimum payments, caps, step - downs and buy - out options, similar to a license agreement between innovator and marketer • Hybrid Financing ̶ Combination of royalty and revenue - based financings ̶ Can take on many forms, including structured debt and equity investments • Product acquisition ̶ Target legacy products with established revenue trends, minimal marketing and infrastructure requirements 31 MISCELLANEOUS

Illustration: Royalty Stream Creation Small Biotech enters into marketing collaboration with Big Pharma 1. Small Biotech licenses marketing rights of Drug A to Big Pharma in exchange for upfront payment and a 10% royalty stream 2. Big Pharma markets the drug and begins to pay a 10% royalty stream on the sales of Drug A to Small Biotech. Big Pharma retains the remaining 90% of the sales $ Drugs Customers (Patients) Big Pharma Small Biotech Marketing Rights Upfront Payment + Royalty Stream (10%) 1 2 32 2 1 MISCELLANEOUS

BIOGRAPHIES AND CONTACT INFORMATION

Biographies Winston Black, CEO Mr. Black was appointed CEO in January 2016. He joined SWK as Managing Director in May 2012 from PBS Capital Management, LLC, an investment management business investing in pharmaceutical royalties and healthcare equities that Mr. Black co - founded in 2009. Prior to PBS Capital, Mr. Black was a Senior Portfolio Analyst at Highland Capital Management, L.P. from September 2007 to March 2009 where he managed a portfolio of approximately $2 billion in healthcare investments. Prior to joining Highland, Mr. Black served as COO/Analyst and Chief Compliance Officer at Mallette Capital Management, Inc., a $200 million biotech focused hedge fund. Prior to Mallette Capital, Mr. Black was Vice President, Corporate Development for A TX Communications, Inc. (“ATX”). Mr. Black began his career as an Analyst in the Healthcare and Telecommunications groups at Salomon Smith Barney. Mr. Black received MBAs with distinction from both Columbia Business School and London Business School and received a BA in Economics from Duke University , where he graduated Cum Laude. Charles Jacobson, CFO Charles Jacobson was appointed CFO in September 2012. He serves as the CEO and Managing Director of Pine Hill Group, LLC (“Pine Hill”), a consulting firm which he co - founded in 2007. Pine Hill provides management level finance, accounting and transaction advisory services to middle market public and private companies. Mr. Jacobson serves as Director, Interim CEO and Interim CFO of The PMI Group, Inc., a position he has held since 2017, 2016 and 2015, respectively. Since 2015, Mr. Jacobson serves as CFO and Director of Parkview Capital Credit, Inc., a Business Development Corporation providing mezzanine debt and equity capital to lower middle market companies. From 2012 to 2013, Mr. Jacobson served as CEO and CFO of Pro Capital, LLC (“Pro Cap”), an investment management business specializing in investments of municipal tax liens. Mr. Jacobson also served on Pro Cap’s board of managers from 2012 to 2014. From 2008 to 2011, Mr. Jacobson served as CFO of FS Investment Corporation pursuant to an agreement between Pine Hill and FS Investment Corporation. From 2001 to 2007, Mr. Jacobson worked for ATX, becoming the organization’s senior vice president of finance where he was responsible for managing ATX’s finance organization. Prior to working for ATX, Mr. Jacobson held senior managerial audit positions with Ernst & Young LLP from 1999 to 2000 and with BDO Seidman, LLP from 1996 to 1999, where he was responsible for audit engagements of private, pre - IPO and publicly traded companies in a variety of different industries. Mr. Jacobson began his professional career in 1993 at a regional public accounting firm where he performed audits on governmental entities. Mr. Jacobson is a Certified Public Accountant and holds a B.S. in Accounting from Rutgers University. 34 BIOGRAPHIES AND CONTACT INFO

Biographies Jody Staggs, VP Mr. Staggs joined SWK Holdings as a Senior Analyst in August 2015. Prior to joining SWK, he was Vice President of Investments at Annandale Capital. Prior to joining Annandale, he was the first employee at Alistair Capital, a Dallas - based hedge fund. He previously co - founded PBS Capital Management, LLC, an investment management business investing in pharmaceutical royalties and healthcare equities. Prior to co - founding PBS, he was a Senior Portfolio Analyst at Highland Capital Management, L.P. where he worked on the firm’s healthcare multi - strategy and public equity groups. While at Highland, Mr. Staggs was ranked first out of a class of eight analysts. Mr. Staggs began his career at Raymond James where he was a Senior Equity Research Associate covering healthcare companies and was ranked in the top quartile of all research associates. He was a Walton Scholar and on the Dean’s List at the University of Arkansas where he graduated with a B.A. in Finance. Mr. Staggs has earned the right to use the Chartered Financial Analyst designation. Brannon Morisoli, Senior Analyst Mr. Morisoli joined SWK Holdings as a Senior Analyst in March 2016. Prior to joining SWK, he was an Investment Analyst and Portfolio Manager at a family office. Prior, he was an Investment Analyst for Presidium Group, a real estate private equity firm, where he played an integral role in closing over $100mm in transactions. Mr. Morisoli began his career at Neurografix , a medical technology startup in Santa Monica, CA exploring MRI imaging of peripheral nerves. While with Neurografix , he was published in two leading neurology journals. Mr. Morisoli graduated from UCLA with a B.S., was awarded a fellowship and graduated from the University of Notre Dame with an M.B.A, and was awarded a Samson Fellowship from the University of Wisconsin Law School, where he graduated with a J.D. Mr. Morisoli is an inactive member of the State Bar of Wisconsin. 35 BIOGRAPHIES AND CONTACT INFO

Biographies Yvette Heinrichson, Controller Ms. Heinrichson joined SWK Holdings as Controller in January 2016. Prior to joining SWK, she provided technical GAAP accounting, SEC financial reporting, SOX implementation and process improvement for companies in a number of industries including healthcare/bioscience, technology, real estate, manufacturing, and retail. Prior to her industry experience, she was a financial statement auditor with Deloitte for several years. She holds a B.S. in Business Administration from San Francisco State University and is a Certified Public Accountant with membership in professional associations AICPA, XBRL US, CalCPA , and CFE. She is also XBRL Certified by the AICPA and XBRL US. 36 BIOGRAPHIES AND CONTACT INFO

Biographies – Board of Directors Michael D. Weinberg, Chairman of the Board Mr. Weinberg is Chief Operating Officer of Carlson Capital, L.P. Mr. Weinberg has served in various capacities with Carlson since November 1999. Since April 2007, Mr. Weinberg has served as the managing member of BirdDog Capital, LLC, a holding company involved in retail and restaurant franchises. From January 1996 to November 1999, Mr. Weinberg was Director of Investments at Richmont Capital Partners, L.P., the investment affiliate of privately - held Mary Kay. Mr. Weinberg holds a B.A. degree from the Plan II Liberal Arts Honors Program and a J.D. degree, both from the University of Texas at Austin. Christopher Haga Mr. Haga is a portfolio manager at Carlson. Mr. Haga, joined Carlson in 2003, has 22 years of experience in public and private investing, investment banking and structured finance. His role at Carlson includes public and private investing in financial institutions, energy companies and special situations. Prior to Carlson, Mr. Haga held investment banking and principal investing roles at RBC Capital Markets, Stephens, Inc., Lehman Brothers (London) and Alex. Brown & Sons. Mr. Haga holds a B.S. in Business Administration from the University of North Carolina at Chapel Hill and an M.B.A. from the University of Virginia. D. Blair Baker Mr. Baker is the president of Precept Capital Management, an investment management company based in Dallas, which he founded in 1998. Precept invests across multiple industries and asset types, focusing primarily on publicly - traded securities. His investments in the healthcare sector have included pharmaceutical, medical device, biotech, medical services and medical technology. He has extensive relationships throughout the industry. Mr. Baker previously worked with the advance staff for Vice President George H.W. Bush. Mr. Baker also formed an oil and gas operating company with ongoing operations in the Fort Worth Basin in North Texas. Other relevant prior experience includes Mr. Baker’s position as vice president and securities analyst covering telecommunications equipment companies at Rauscher Pierce Refsnes and as a member of the team at Friess Associates that managed $7 billion of client assets. 37 BIOGRAPHIES AND CONTACT INFO

Biographies – Board of Directors Edward Stead Mr. Stead has served as a senior executive for various companies over an extensive business career. Mr. Stead began his career as a lawyer at IBM from 1973 to 1985. He then served at Apple Computer, Inc. from 1987 until 1996, where he held titles up to and including Senior Vice President, General Counsel and Secretary. At Apple, Mr. Stead led the significant advance of Apple in filing of patented inventions. He also served as EVP, General Counsel and Secretary of Blockbuster, Inc. from 1997 until 2006. Mr. Stead has served on the Legal Advisory Boards of both the NYSE and the NASD. He is currently a member of the American Law Institute. 38 BIOGRAPHIES AND CONTACT INFO

Contact Information • Winston Black: ̶ Phone: 972.687.7251 ̶ Email: wblack@swkhold.com • Jody Staggs: ̶ Phone: 972.687.7252 ̶ Email: jstaggs@swkhold.com • Office address: ̶ 14755 Preston Road, Ste 105 Dallas, TX 75254 • Website: www.swkhold.com 39 BIOGRAPHIES AND CONTACT INFO

FINANCIAL OVERVIEW

Balance Sheets 41 FINANCIAL OVERVIEW $ in 000s Sep-17 Dec-16 Dec-15 Dec-14 ASSETS Cash and cash equivalents 15,975$ 32,182$ 47,287$ 58,728$ Accounts receivable 1,598 1,054 1,127 1,053 Finance receivables 163,719 126,366 99,346 93,347 Marketable investments 3,319 2,621 5,286 4,849 Investment in unconsolidated entities - 6,985 7,988 9,044 Deferred tax asset 32,311 38,471 16,833 20,106 Warrant assets 1,403 1,013 1,900 - Other assets 169 240 720 1,092 Total assets 218,494$ 208,932$ 180,487$ 188,219$ LIABILITIES AND STOCKHOLDERS' EQUITY Accounts payable and accrued liabilities 1,492$ 682$ 788$ 864$ Warrant liability 197 189 259 421 Total liabilities 1,689 871 1,047 1,285 Stockholders' equity: Preferred stock - - - - Common stock 13 13 13 13 Additional paid-in-capital 4,433,511 4,433,289 4,432,926 4,432,482 Accumulated deficit (4,217,507) (4,228,910) (4,257,798) (4,250,428) Accumulated other comprehensive income 788 (87) - - Total SWK Holdings Corp stockholders' equity 216,805 204,305 175,141 182,067 Non-controlling interests in consolidated entities - 3,756 4,299 4,867 Total stockholders' equity 216,805 208,061 179,440 186,934 Total liabilities and stockholders' equity 218,494$ 208,932$ 180,487$ 188,219$

Income Statements 42 FINANCIAL OVERVIEW $ in 000s LTM 9/17 2016 2015 2014 Revenues Finance receivable interest income, including fees 18,850$ 15,747$ 17,265$ 11,542$ Marketable investments interest income - 92 266 360 Income related to investments in unconsolidated entities 11,660 6,219 5,884 5,341 Other 236 322 45 157 Total Revenues 30,746 22,380 23,460 17,400 Costs and expenses: Provision for credit losses 1,659 1,659 10,848 - Impairment expense 6,418 8,077 6,638 - Interest expense (7,243) - 381 579 General and administrative 3,591 2,829 3,378 3,275 Total costs and expenses 4,425 12,565 21,245 3,854 Other income (expense), net Unrealized net (loss) gain on derivatives (1,153) 588 (3,305) (245) Gain on sale of marketable securities 243 - Income (loss) before income taxes 25,411 10,403 (1,090) 13,301 Income tax (benefit) expense (15,478) (21,638) 3,273 (10,303) Consolidated net income 40,889 32,041 (4,363) 23,604 Net income attributable to non-controlling interests 5,769 3,153 3,007 2,839 Net income (loss) attributable to SWK Holdings Corp Stockholders 35,120$ 28,888$ (7,370)$ 20,765$ Net income (loss) per share attributable to SWK Holdings Corp Stockholders Basic 2.70$ 2.22$ (0.57)$ 3.20$ Diluted 2.69$ 2.22$ (0.57)$ 3.20$ Weighted Average Shares Basic 13,031 13,015 12,986 6,486 Diluted 13,035 13,018 12,986 6,492

Cash Flow Statements 43 FINANCIAL OVERVIEW $ in 000s,* LTM 9/17 2016 2015 2014 Cash flows from operating activities: Consolidated net income $40,889 $32,041 ($4,363) $23,604 Adjustments to reconcile net income to net cash provided by operating activities: Income from investments in unconsolidated entity (11,660) (6,219) (5,884) (5,341) Provision for loan credit losses - 1,659 10,848 - Impairment expense 834 8,077 6,638 - Change in fair value of warrants 5,572 (588) 3,305 245 Gain on sale of marketable securities 1,741 - - - Deferred income tax (21,881) (21,638) 3,273 (10,304) Loan discount amortization and fee accretion (2,812) (3,109) (1,778) (448) Interest income in excess of cash collected (1,330) - (1,063) (3,583) Interest paid-in-kind (63) - - - Stock-based compensation 271 363 640 844 Other 17 16 391 145 Changes in operating assets and liabilities: Accounts receivable (708) (457) (74) (525) Other assets (169) (396) (648) (12) Accounts payable and other liabilities 899 (106) (76) 496 Net cash provided by operating activities 11,600 9,643 11,209 5,123 Cash flows from investing activities: Cash distributions from investments in unconsolidated entity 18,895 7,222 6,940 6,722 Cash received for settlement of warrants 1,750 1,405 - - Proceeds from sale of available-for-sale marketable securities (1,014) - - - Net (increase) decrease in finance receivables (30,169) (29,717) (25,849) (60,620) Investment in marketable investments (41,941) - - (1,730) Marketable investment principal payment 94 41 80 - Other (10) (3) (50) (1) Net cash provided by investing activities (52,395) (21,052) (18,879) (55,629) Cash flows from financing activities: Distribution to non-controlling interests (9,662) (3,696) (3,575) (3,584) Net paydown on revolver facility - - - (5,000) Equity offering, net - - - 110,154 Net cash used in financing activities (9,662) (3,696) (3,771) 101,570 Net increase in cash and cash equivalents (50,457) (15,105) (11,441) 51,064 Cash and cash equivalents at beginning of period 66,438 47,287 58,728 7,664 Cash and cash equivalents at end of period 15,975 $32,182 $47,287 $58,728 *numbers may not add due to rounding

Reconciliation of Non - GAAP Adjusted Net Income Attributable to SWK Stockholders The table below eliminates provisions for income taxes, non - cash mark - to - market changes on warrant assets and SWK’s warrant liability, as well as, warrant - related debt issuance costs and stock compensation expense related to SWK’s equity raise. The following tables provide a reconciliation of SWK’s reported (GAAP) income before provision for income tax to SWK’s adjusted net income attributable to SWK Holdings Corporation stockholders (Non - GAAP) for the periods denoted in the table: 44 $ in 000s LTM 9/17 2016 2015 2014 2013 Consolidated net income (loss) 40,889$ 32,041$ (4,363)$ 23,604$ 14,331$ Plus: income tax expense (benefit) (15,478) (21,638) 3,273 (10,303) (9,841) Plus: loss (gain) on fair market value of warrants 1,153 (588) 3,305 245 190 Plus: loss related to Response Genetics warrants - - (802) - - Plus: gain on realized value of warrants - 931 - - - Plus: warrant-related debt issuance costs - - 155 - - Plus: transaction-related stock compensation expense - - - 452 - Adjusted income before provision for income tax 26,564$ 10,746$ 1,568$ 13,998$ 4,680$ Plus: Adjusted provision for income tax - - - - - Non-GAAP consolidated net income 26,564$ 10,746$ 1,568$ 13,998$ 4,680$ Less: Non-GAAP adjusted net income attributable to non-controlling interest (5,769) (3,153) (3,007) (2,839) (1,470) Non-GAAP adjusted net income (loss) attributable to SWK Holdings Corporation Stockholders 20,795$ 7,593$ (1,439)$ 11,159$ 3,211$