Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - STORE CAPITAL Corp | s001732x1_8k.htm |

Exhibit 99.1

Disclaimer This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Such forward-looking statements include, without limitation, statements concerning our business and growth strategies, investment, financing and leasing activities and trends in our business, including trends in the market for long-term, triple-net leases of freestanding, single-tenant properties. Words such as “expects,” “anticipates,” “intends,” “plans,” “likely,” “will,” “believes,” “seeks,” “estimates,” and variations of such words and similar expressions are intended to identify such forward-looking statements. Such statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from the results of operations or plans expressed or implied by such forward-looking statements. Although we believe that the assumptions underlying the forward-looking statements contained herein are reasonable, any of the assumptions could be inaccurate, and therefore such statements included in this presentation may not prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or any other person that the results or conditions described in such statements or our objectives and plans will be achieved. Furthermore, actual results may differ materially from those described in the forward-looking statements and may be affected by a variety of risks and factors including, without limitation, the risks described in our Annual Report on Form 10-K for the fiscal year ended December 31, 2016 and subsequent quarterly reports on form 10-Q.Forward-looking statements set forth herein speak only as of the date hereof, and we expressly disclaim any obligation or undertaking to update or revise any forward-looking statement contained herein, to reflect any change in our expectations with regard thereto, or any other change in events, conditions or circumstances on which any such statement is based, except to the extent otherwise required by law.THIS PRESENTATION CONTAINS HISTORICAL PERFORMANCE INFORMATION REGARDING STORE CAPITAL, AS WELL AS OTHER COMPANIES PREVIOUSLY MANAGED BY OUR SENIOR EXECUTIVE TEAM. SUCH PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS.This presentation contains references to our copyrights, trademarks and service marks and to those belonging to other entities. Solely for convenience, copyrights, trademarks, trade names and service marks referred to in this presentation may appear without the © or ® or TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these copyrights, trademarks, trade names and service marks. We do not intend our use or display of other companies’ trade names, copyrights, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.Definitions and footnotes for data provided herein are provided in the appendix section of this presentation. Unless otherwise indicated, data provided herein is dated as of march 31, 2017. 2

STORE Capital Snapshot NYSE: STOR; U.S. PROFIT-CENTER REAL ESTATE ~35-YEAR SUCCESSFUL LEADERSHIP TRACK RECORD $4.1B EQUITY MARKET CAP; 4.9% DIVIDEND YIELD16% DIVIDEND INCREASE FROM 2014 TO 20161,750 PROPERTIES LEASED TO 369 CUSTOMERS ~75% OF LEASE CONTRACTS INVESTMENT-GRADE QUALITY1 “STORE Capital is completely distinctive, constructed deliberately on foundational building blocks based upon our decades of highly successful investment experience to make this the absolute best platform we have ever created.” -- Christopher Volk, CEO 3

Dedicated to real estate net-lease profit-center property investmentsMarket leader in profit-center net-lease solutionsAddressing one of nation’s largest real estate market opportunitiesAmongst fastest-growing real estate net-lease companies1 Why is that so important?Tenants need their profit-center real estate in order to conduct business, making our rent contracts senior to other financial obligations Which is the unique payment source?Profitability from the operations of each investment How do STORE properties differ from other commercial real estate assets?Three sources of payment support instead of two PROPERTY VALUE CORPORATE CREDIT UNIT-LEVEL PROFITABILITY STORE is Single Tenant Operational Real Estate | foundational distinction | defining our investment asset class shapes everything we do. 4

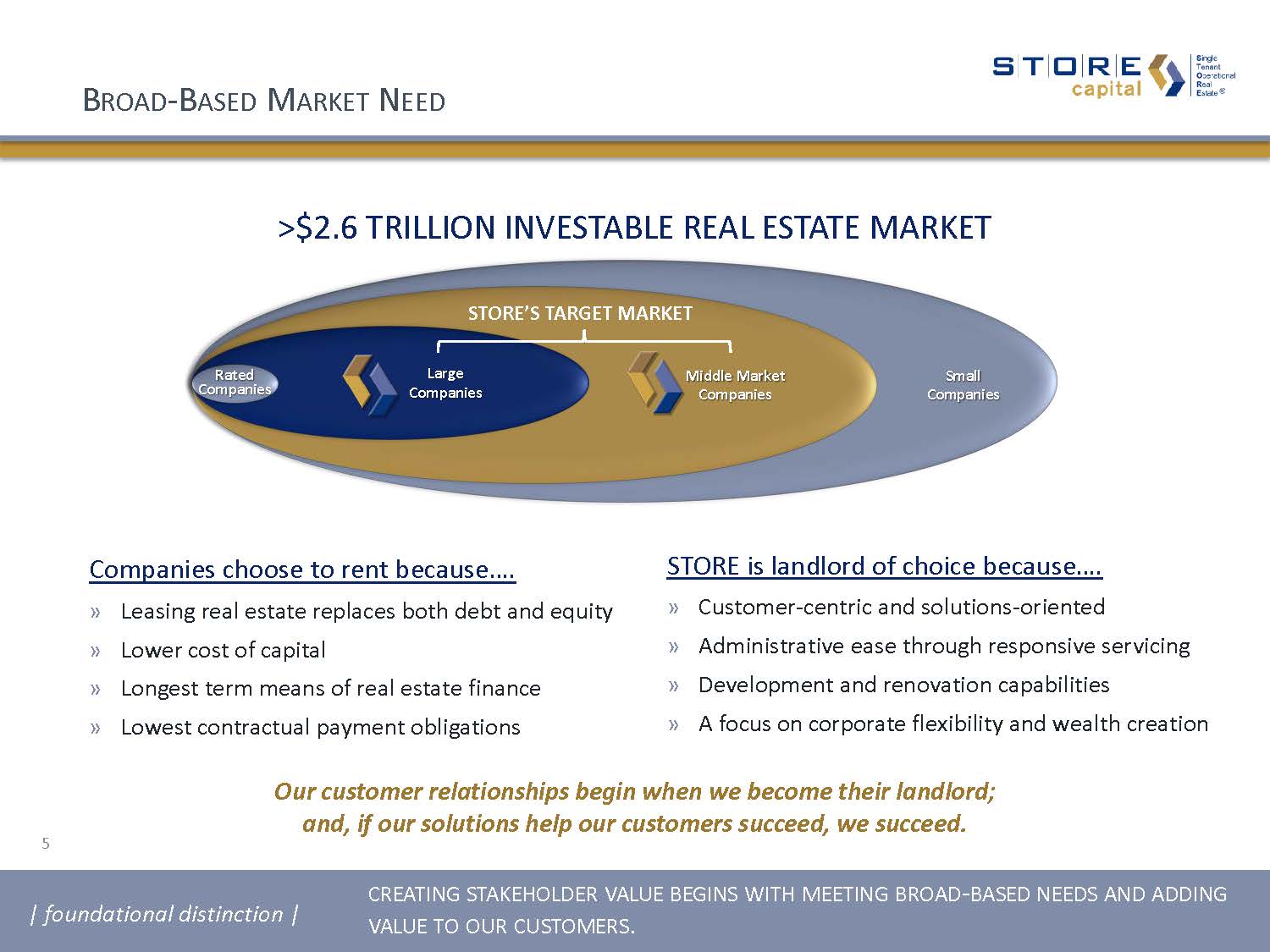

Broad-Based Market Need 5 Companies choose to rent because….Leasing real estate replaces both debt and equityLower cost of capitalLongest term means of real estate financeLowest contractual payment obligations STORE is landlord of choice because….Customer-centric and solutions-orientedAdministrative ease through responsive servicing Development and renovation capabilitiesA focus on corporate flexibility and wealth creation Our customer relationships begin when we become their landlord; and, if our solutions help our customers succeed, we succeed. | foundational distinction | creating stakeholder value begins with meeting broad-based needs and adding value to our customers. 5 >$2.6 TRILLION INVESTABLE REAL ESTATE MARKET Small Companies Middle Market Companies Large Companies Rated Companies STORE’s Target market

Internal OwnershipDirect calling efforts on thousands of companies and financial sponsors ~80% ~20% B2B Benefits + Higher Lease Rates+ Lower Real Estate Prices+ Longer Lease Terms+ Smaller Transaction Sizes + Greater Investment Diversity+ Stronger Contracts Our unique platform has multiple origination channels enabling us to efficiently cover a very large market opportunity.All channels result in a B2B approach. | foundational distinction | a hallmark of store is our origination platform, which is essential to superior investment returns and lower investment risk. “B2B” Origination Platform Virtual SalesforceTenant introductions through intermediary relationships = Value for Stockholders 6

Investment Portfolio Built “Brick by Brick” quarterly net new customers and transactions unprecedented granularity | foundational distinction | transaction flow ownership enables organic growth and unparalleled portfolio diversity. 7 customer revenue distribution1 % Of Total Rent & Interest 369 customers | ~ 17 net new customers quarterly 1,750 properties | ~ 76 net new properties quarterly ~ 590 contracts | ~ 30 transactions closed quarterlyAverage transaction size below $9 millionRepeat customers about one-third of new business <$5M $5 -$20M $20 -$50M $50 -$200M $200 -$500M $500M -$1B >$1B ~ 70% of customers have revenues over $50 millionMedian tenant revenues ~ $47 millionWeighted average tenant revenues ~$696 million strong tenant revenue profiles

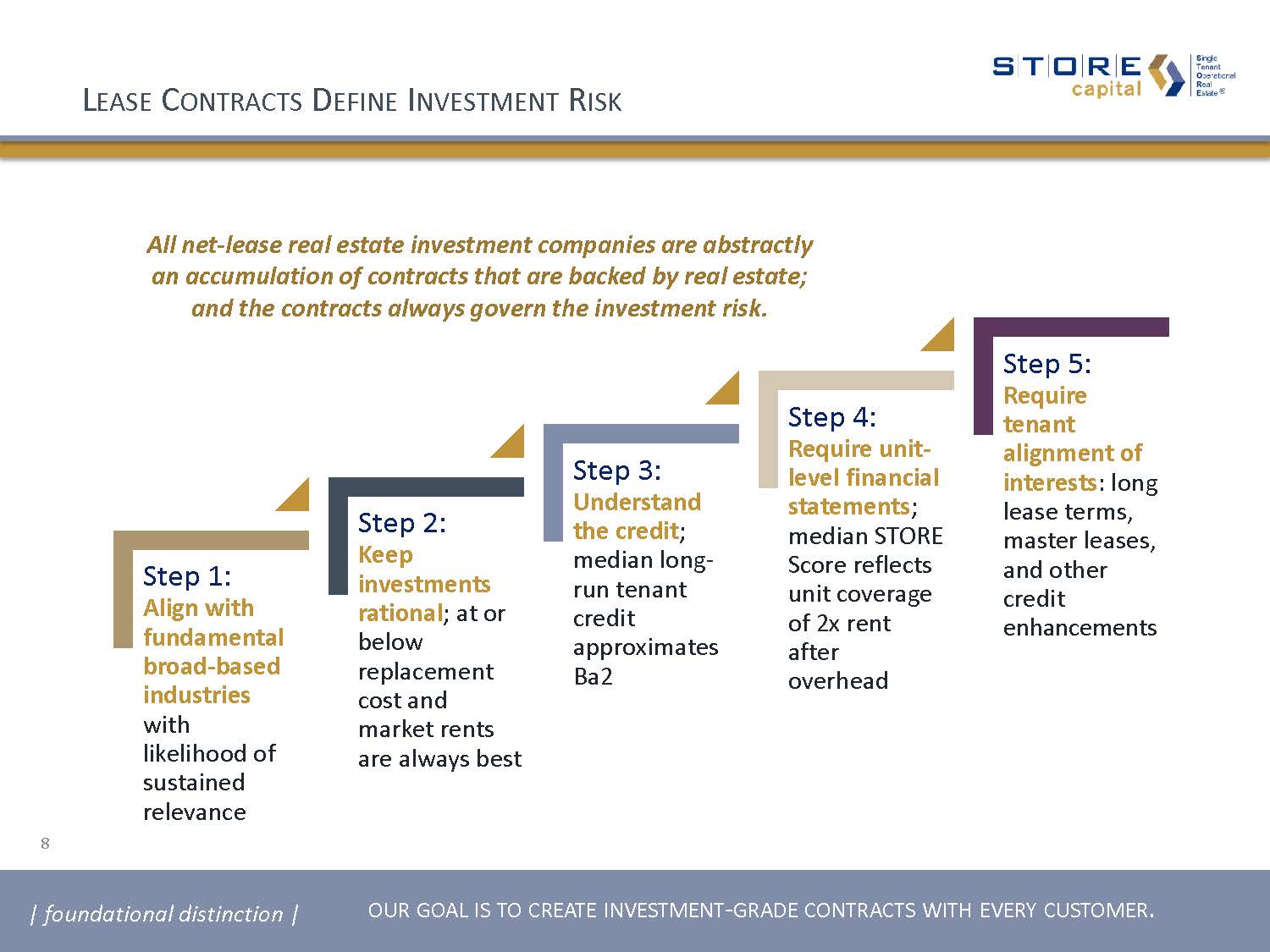

Lease Contracts Define Investment Risk All net-lease real estate investment companies are abstractly an accumulation of contracts that are backed by real estate; and the contracts always govern the investment risk. | foundational distinction | our goal is to create investment-grade contracts with every customer. 8

Capital Structure Leadership | foundational distinction | an effective capital structure must be established at the outset. 9 Effective Liquidity Management$500 million unsecured multi-year revolving credit facilityAccess to A+ asset-backed / BBB- unsecured borrowingsVirtually all borrowings are long-term and fixed rate Effective Asset/Liability ManagementIntelligent, laddered investment-grade borrowingsTarget long-term annual debt maturities below 2.5% of assetsMinimize gap between free cash flow1 and debt maturities strategic liability management ($MM) Our structural aim is to have the annual gap between our free cash flow after dividends and our annual debt maturities be 1.5% of assets or less. The smaller the gap, the less interest rate sensitive is our balance sheet. Median debt maturities

Complementary Investment-Grade Debt Options growing unencumbered asset pool ($MM) store master funding S&P rated A+Dedicated asset-backed securities conduit unsecured term borrowings | foundational distinction | multiple complementary investment-grade borrowing sources are integral to a long-term capital markets strategy designed to optimize cost of capital. S&P rated BBB-, positive outlookFitch Ratings rated BBB-, positive outlook Q3 2011 Q1 2017 10 Non-recourse with minimal covenantsComplete portfolio management flexibilityEfficient leverage of 70%BBB rated notes retained for flexibilityEnables superior unsecured debt ratiosProvides leading term borrowing diversity Select Ratios BBB+/Baa1 Net Lease Average1 STORE Unencumbered Asset Target2 STORE Unencumbered Asset Actual3 Unencumbered assets/unsecured debt ~3x ~3.5x 4.6x Debt/EBITDA ~5x ~4x 3.3x Debt service coverage ~4x ~5.5x 7.4x Investment-grade borrowing diversity with resultant improved unsecured credit metrics.

11 Internal Growth Strategy Lease Escalation Frequency % Base Rent and Interest1 Weighted Average Annual Escalation Rate1,2 Annually 67% 1.8% Every 5 years 28% 1.8% Other escalation frequencies 3% 2.1% Flat 2% N/A Total / Weighted Average 100% 1.8% lease escalations dividends Market-leading dividend increases 8.0% in 20157.4% in 2016Market-leading and growing dividend protection370% payout ratio in 201568% payout ratio in 2016 Annual Lease Escalations AFFO Per Share Growth 1.00% 1.53% 1.25% 1.91% 1.50% 2.29% 1.80% 2.75% 2.00% 3.05% + ReinvestedCash Flows 65.0% 67.0% 75.0% 80.0% 2.76% 2.59% 1.90% 1.48% = EstimatedInternal Growth > 5% | foundational distinction | portfolio lease escalations and retained and reinvested cash flows drive significant internal growth. 11 estimated internal growth4 AFFO Payout Ratio AFFO Per Share Growth

12 Unrivaled Leadership Experienced….Built & managed three net-lease real estate investment companiesInvested over $15 billion in profit-center real estate (9,100+ properties)Consistently outperformed broader REIT market returns over multiple decades1Navigated platforms through multiple economic cycles & interest rate environmentsThought leadership through primary and published research Groundbreaking….Investment-grade corporate net-lease rating (1995)Net-lease real estate master trust conduit (2005)NYSE-listed public company sales (2001 & 2007)Private institutional investor sponsorship (1999 & 2011) | foundational distinction | a progression of innovation and thought leadership over three decades. 12 Senior leaders working together between 10 and 35 years. 1980 Q1 2017 > $15 B CUMULATIVE ACQUISITIONS

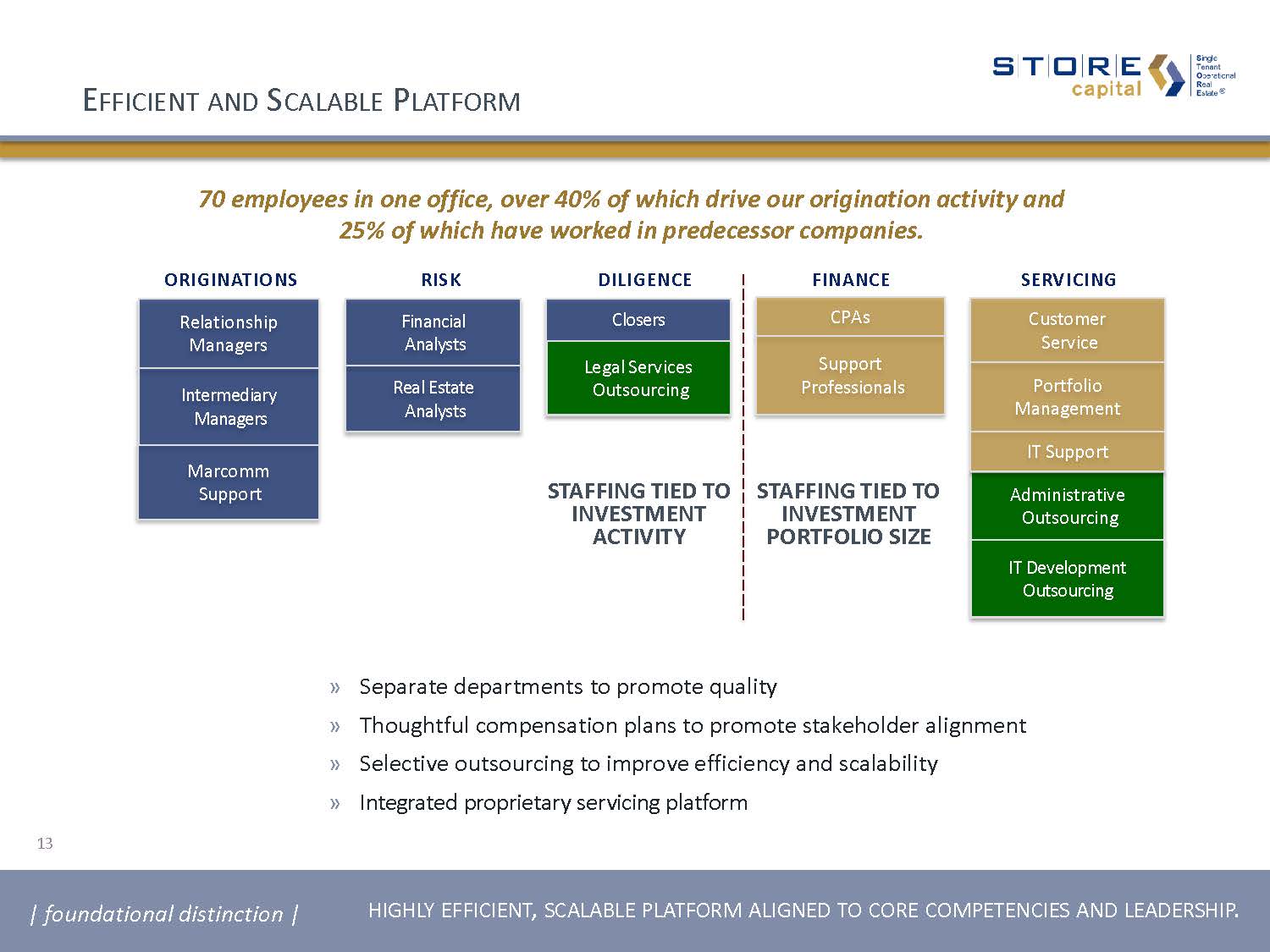

70 employees in one office, over 40% of which drive our origination activity and 25% of which have worked in predecessor companies. originations servicing diligence finance risk RelationshipManagers Intermediary Managers Closers Financial Analysts Real Estate Analysts CPAs Support Professionals Customer Service Portfolio Management Administrative Outsourcing IT Development Outsourcing IT Support Legal Services Outsourcing Marcomm Support Separate departments to promote qualityThoughtful compensation plans to promote stakeholder alignmentSelective outsourcing to improve efficiency and scalability Integrated proprietary servicing platform Efficient and Scalable Platform | foundational distinction | highly efficient, scalable platform aligned to core competencies and leadership. staffing tied to investment activity staffing tied to investment portfolio size 13

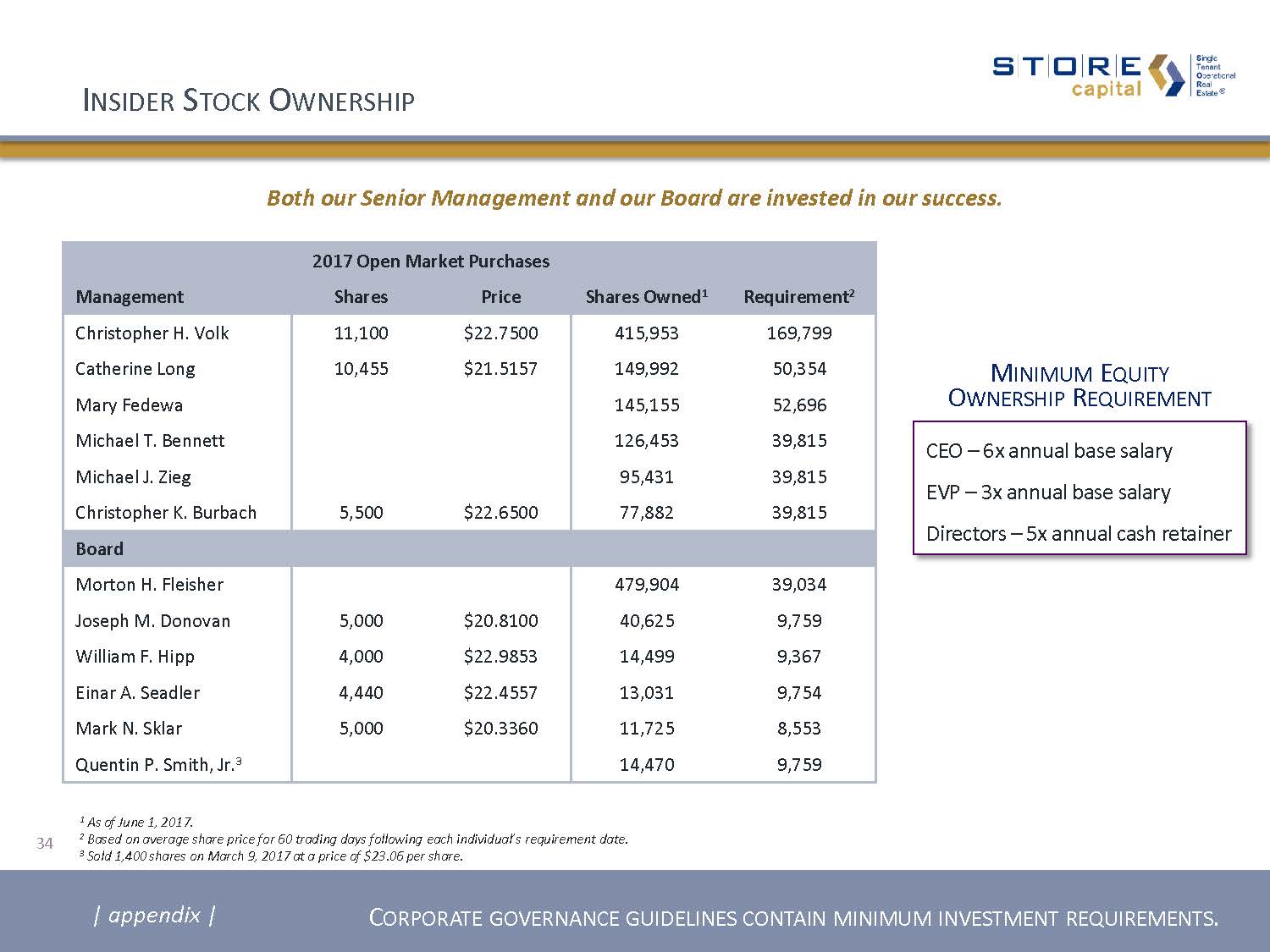

Best in Class Corporate Governance leading board governance leading stockholder disclosure Full tenant credit quality distributionFull contract quality distributionFull tenant size distributionLease contract escalationsProperty appraised replacement costsPortfolio master leasesLeading unit-level performance disclosureProperty sales gain over costsGround lease investmentsNN vs NNN leases With our leading stockholder disclosure and board governance practices, we provide corporate governance that is “best in class” in the net-lease sector. | foundational distinction | our transparency reflects our superior tenant reporting requirements and robust it platform. 14 Non-Staggered Board? Yes Opt-Out of State Anti-Takeover Provisions¹ and poison pills? All Stockholder Rights Plan (SRP) Today? No Investment Committee of the Board of Directors Approves all investments over 1% of assets Future Implementation of SRP Subject to Stockholder Approval? Yes Independent Board, Committees and Chairman Yes Stock Ownership Guidelines for Executive Officers and Independent Directors* Yes * Executive Officers and Directors already exceed stock ownership guidelines and over 45,000 shares of STORE stock were purchased by Executive Officers and Directors in 2017, see page 34.

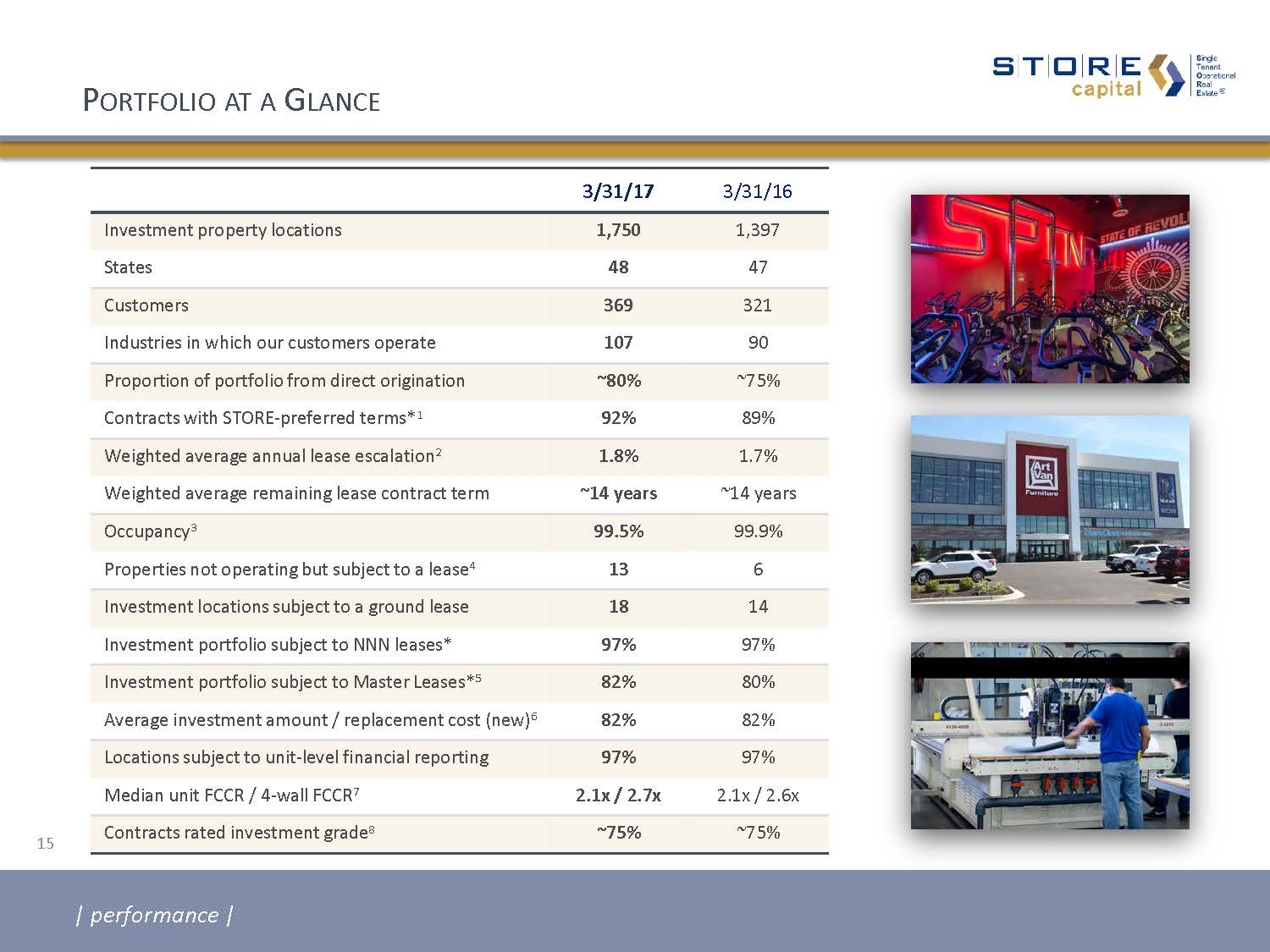

Portfolio at a Glance 3/31/17 3/31/16 Investment property locations 1,750 1,397 States 48 47 Customers 369 321 Industries in which our customers operate 107 90 Proportion of portfolio from direct origination ~80% ~75% Contracts with STORE-preferred terms*1 92% 89% Weighted average annual lease escalation2 1.8% 1.7% Weighted average remaining lease contract term ~14 years ~14 years Occupancy3 99.5% 99.9% Properties not operating but subject to a lease4 13 6 Investment locations subject to a ground lease 18 14 Investment portfolio subject to NNN leases* 97% 97% Investment portfolio subject to Master Leases*5 82% 80% Average investment amount / replacement cost (new)6 82% 82% Locations subject to unit-level financial reporting 97% 97% Median unit FCCR / 4-wall FCCR7 2.1x / 2.7x 2.1x / 2.6x Contracts rated investment grade8 ~75% ~75% | performance | 15

2016 Key Achievements Generated a total return to shareholders of 11.5%, versus 8.6% for the MSCI U.S. REIT Index1Invested $1.2 billion at an initial weighted average cap rate of 7.9%2Grew comparable revenues by 32.2% and Adjusted Funds from Operations (AFFO) by 34.0%Grew comparable AFFO per share by 10.1% and raised our dividend 7.4%Increased dividend protection3 and internal growth potential with a conservative 68.3% payout ratio Reviewed more than $8 billion and maintained a pipeline of more than $7 Billion in investment opportunities4Acquired over 360 properties, grew our customer count by 19% and added over 20 industry groups5Added a corporate bbb-, positive outlook credit rating from Standard & Poor’s Ratings ServicesLowered our target leverage range to 5.75x – 6.25x Funded Debt to EBITDAMaintained approximately 75% of our lease contracts investment-grade in quality | performance | 16

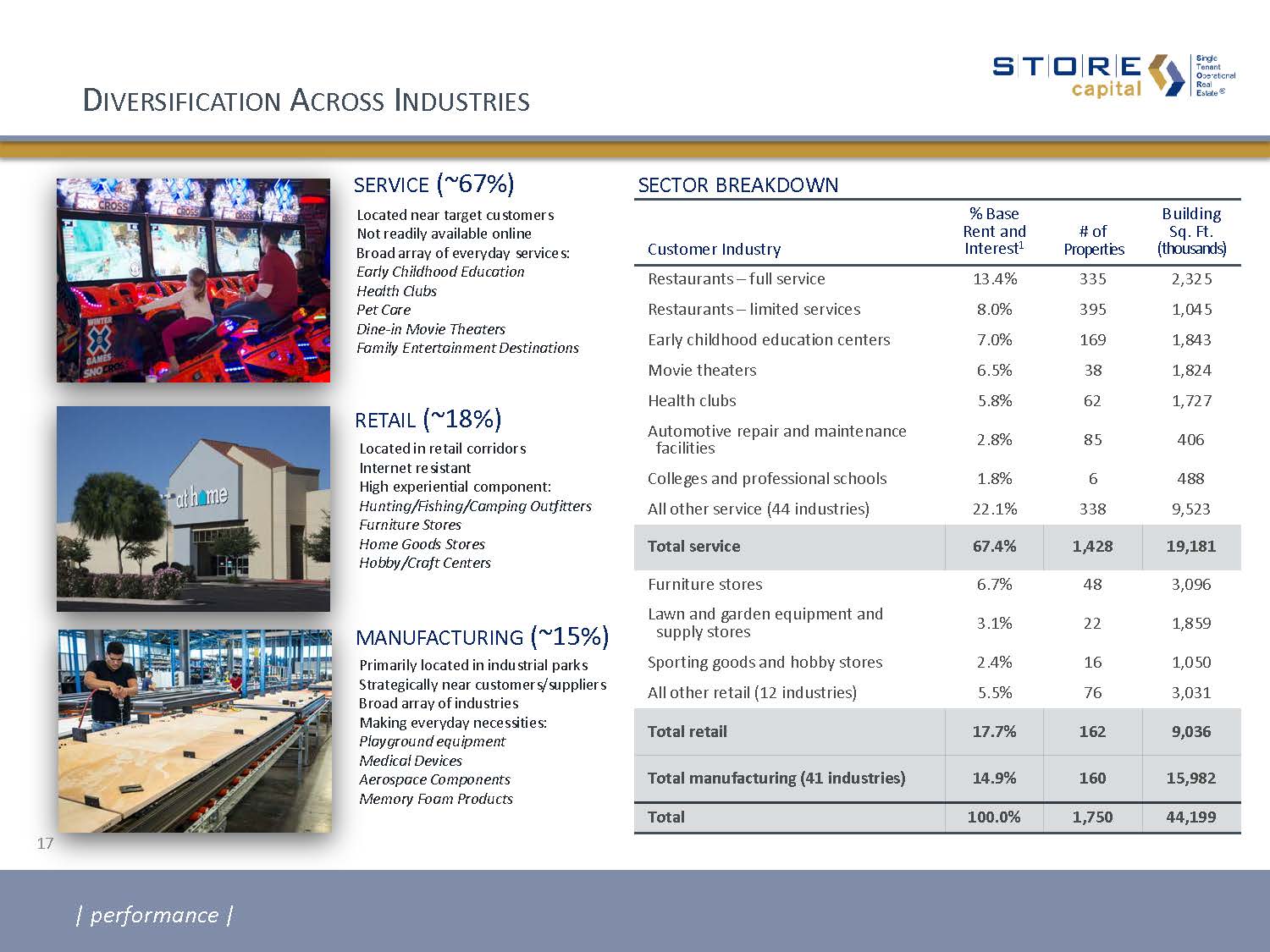

Diversification Across Industries Customer Industry % Base Rent and Interest1 # of Properties Building Sq. Ft. (thousands) Restaurants – full service 13.4% 335 2,325 Restaurants – limited services 8.0% 395 1,045 Early childhood education centers 7.0% 169 1,843 Movie theaters 6.5% 38 1,824 Health clubs 5.8% 62 1,727 Automotive repair and maintenance facilities 2.8% 85 406 Colleges and professional schools 1.8% 6 488 All other service (44 industries) 22.1% 338 9,523 Total service 67.4% 1,428 19,181 Furniture stores 6.7% 48 3,096 Lawn and garden equipment and supply stores 3.1% 22 1,859 Sporting goods and hobby stores 2.4% 16 1,050 All other retail (12 industries) 5.5% 76 3,031 Total retail 17.7% 162 9,036 Total manufacturing (41 industries) 14.9% 160 15,982 Total 100.0% 1,750 44,199 sector breakdown | performance | 17 Located near target customers Not readily available onlineBroad array of everyday services:Early Childhood EducationHealth ClubsPet CareDine-in Movie TheatersFamily Entertainment Destinations Located in retail corridorsInternet resistantHigh experiential component:Hunting/Fishing/Camping OutfittersFurniture StoresHome Goods StoresHobby/Craft Centers Primarily located in industrial parksStrategically near customers/suppliersBroad array of industries Making everyday necessities:Playground equipmentMedical DevicesAerospace ComponentsMemory Foam Products service (~67%) retail (~18%) manufacturing (~15%)

Top 10 Customers1 18 AMC Entertainment (NYSE:AMC), is the largest movie exhibition company in the world with approximately 1,000 theatres and 11,000 screens across the globe. The company operates in 44 states and approximately 52% of the U.S. population lives within 10 miles of an AMC theater. Gander Mountain operates the nation’s largest retail network specializing in hunting, fishing, camping, marine and outdoor lifestyle products. It offers product line through the Company’s website, catalog and over 100 retail locations across 26 states. Cadence Education is a Morgan Stanley Global PE owned company and is one of the premier early childhood educators in the U.S. The Company’s national platform of more than 150 schools has the capacity to serve more than 20,000 students across 20 states. Mills Fleet Farm is a full-service merchant with more than 35 locations in four mid-western states, offering a broad assortment of goods from hunting gear to lawn, garden and farm supplies. In 2016 Mills was purchased by the PE firm KKR & Co. RMH Franchise Holdings is the second largest Applebee’s franchisee, operating 170+ units in 15 states. The company is a top 100 multi-unit franchisee company in the United States and was formed in 2012 with the backing of PE firms including ACON Investments. Dufresne Spencer Group is an Ashley Furniture HomeStore franchisee that currently operates over 35 Ashley Furniture HomeStores throughout 9 states in the Southeast. Dufresne Spencer Group was ranked No. 35 in 2016 Furniture Today's Top 100 Furniture Stores. O'Charley's operates over 300 casual dining restaurants, over 200 of which are branded as O’Charley’s. O'Charley's is a wholly owned subsidiary of American Blue Ribbon Holdings, which is majority owned by Fidelity National Financial. Freedom Roads / Camping World Holdings (NYSE: CWH) operates the largest national network of recreational vehicle dealerships and retail parts & accessories stores with over 120 locations. Camping World offers the largest selection of products, service and installation in the RV industry. % Base Rent and Interest2 3.1% 2.4% 2.1% 2.0% 2.0% 1.5% 1.3% 1.1% 1.1% 1.1% | performance | 17.7% Total Top 10 Customers Art Van Furniture is the Midwest’s largest furniture retailer and America’s largest independent furniture retailer. Founded in 1959, the company operates more than 100 stores throughout five Midwestern states, including Art Van Furniture franchise locations as well as Art Van mattress and flooring stores. Automotive Remarketing Group, Inc., dba America’s Auto Auction is one of the fastest growing auto auction companies in the nation. Today the company operates 21 successful auction locations nationwide. The Company is a wholesale auto auction company offering a full spectrum of remarketing services for both buyers and sellers of used vehicles.

Diversification Across Geographies1 | performance | 19

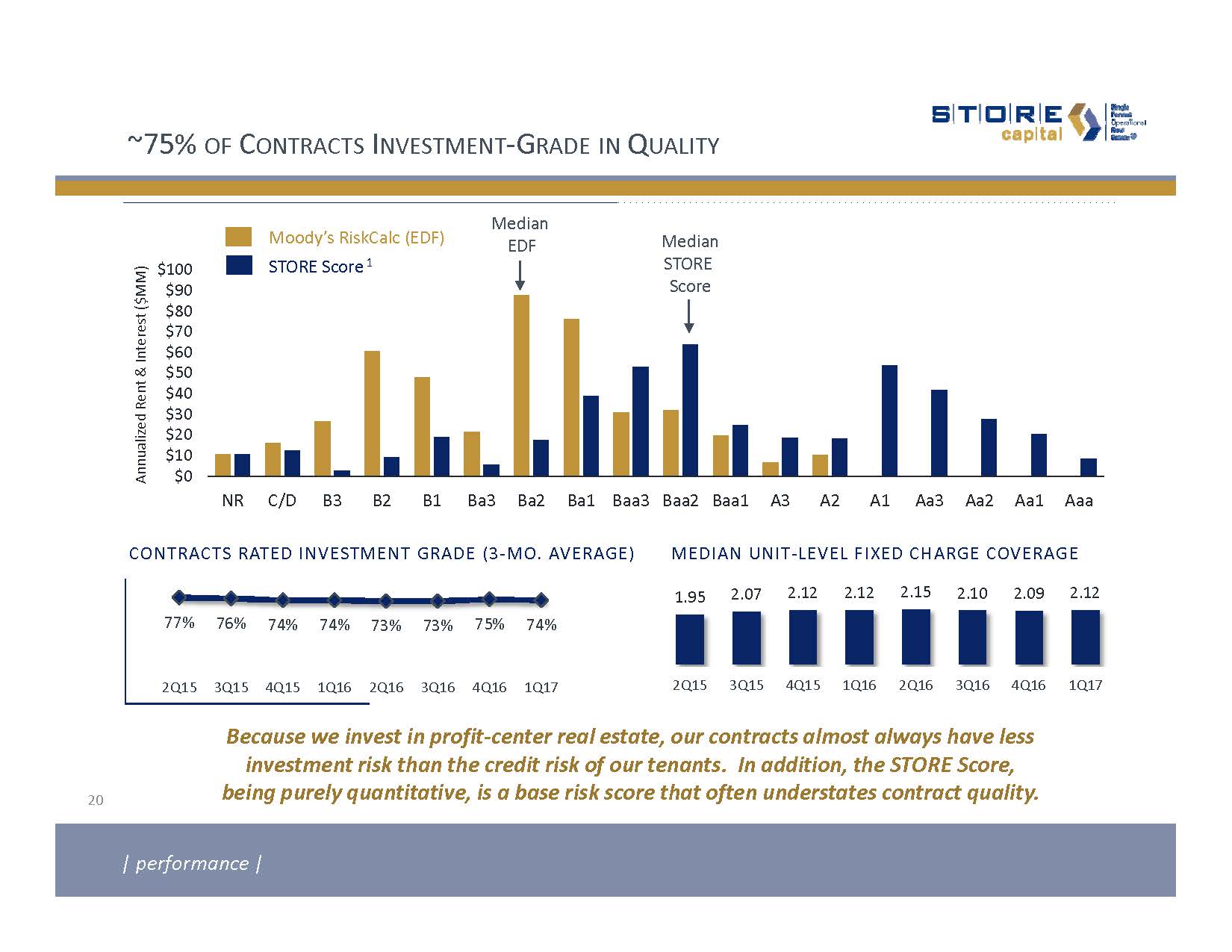

~75% of Contracts Investment-Grade in Quality Because we invest in profit-center real estate, our contracts almost always have less investment risk than the credit risk of our tenants. In addition, the STORE Score, being purely quantitative, is a base risk score that often understates contract quality. | performance | Moody’s RiskCalc (EDF) STORE Score 1 20 CONTRACTS RATED INVESTMENT GRADE (3-MO. AVERAGE) MEDIAN UNIT-LEVEL FIXED CHARGE COVERAGE Median EDF MedianSTORE Score

| performance | PIPELINE VELOCITY ($B) Total Pipeline1 Deals Reviewed1 Cumulative Annual Acquisitions 2012 2013 2014 2015 2016 PIPELINE SECTOR DISTRIBUTION AS OF 3/31/17 Investment Pipeline Activity 21 | performance | $0.7 $0.8 $1.1 $1.2 $1.2

22 NOI, AFFO AND NET INCOME ($MM)2 Growth and Performance | performance | PER SHARE GROWTH NET INCOME:16.4% DIVIDENDS:8.6% AFFO:10.1% Average Annual Growth Rate ACQUISITION VOLUME ($MM)1 GROSS RATE OF RETURN 3 5.6% 4.1%4 4.7% 4.4% 4.1% 9.7% 8.3% 8.1% 7.9% 8.0% 10.0% 9.8% 9.7% 9.5% 7.7% 3.7%

Total Return Built on Both Yield & Growth | performance | 23 500 companies 21 companies(4%) 5 companies(1%) Only 1% of companies in the S&P 500 have STORE’s combination of dividend yield and EPS growth offering a superior investment opportunity. 300% Price-to-Total Return Discount S&P 500 INDEX2 S&P Multiple 26.6 x Dividend Yield 2.0% 4Q15A - 4Q16A EPS Growth 5.3% Total Return 7.3% PEGY 3.6 x STORE CAPITAL AFFO Multiple 14.6 x Dividend Yield 4.9% 4Q15A – 4Q16A AFFO Growth Rate 7.5% Total Return 12.4% STOR PEGY 1.2 x

Margins of Safety Portfolio QualityApproximately 75% investment-gradeMaster leases 82% of the time97% property-level financial statementsMarket-leading investment diversityInvestments average 82% of replacement costInvestment yields above NAV auction yields Financial StrengthA highly protected dividendMarket-leading internal growth1 Multiple investment-grade borrowing optionsConservative leverage and flexible balance sheet | performance | 24

Distinction market-leading investment approach in underserved market exceeding $2.6 trillion 1. predominantly investment-grade quality net-lease contract portfolio 2. market-leading diversified capital markets strategy 3. secure dividends and dividend growth 4. margins of safety for our shareholders in everything we do 5. leadership team with 35-year history and a multiple-decade record of outperformance1 6. | performance | 25

Appendix

27 Historic Dividend/AFFO per share Performance 1 Steady AFFO per share1 growth commensurate with dividend per share growth allows us to maintain a low payout ratio. Our low AFFO payout ratio means we have excess cash flow after dividends to reinvest in new real estate acquisitions, which drives internal growth. 2 71% 67% | appendix|

FFCA (NYSE: FFA) 1994 - 2001 Spirit Finance (NYSE: SFC) 2003 - 2007 STORE Holdings (Oaktree) 2011 - 2016 Management Team Performance | appendix | Management has unparalleled expertise in creating successful STORE investment platforms in a variety of market environments. 28 $4.9 billion Invested Average Cap Rate – 10.3%Average 10-year US Treasury – 6.2%Asset-Backed and Unsecured DebtRated BBB by S&P, Baa2 by Moody’sAverage Occupancy – 98+%Sold to GE Capital $3.5 billion InvestedAverage Cap Rate – 8.7%Average 10-year US Treasury – 4.4%Asset-Backed DebtNo corporate credit ratingAverage Occupancy – 99+%Sold to consortium of investors $4.4 billion InvestedAverage Cap Rate – 8.3%Average 10-year US Treasury – 2.3%Asset-Backed and Unsecured DebtRated BBB- by S&P, BBB- by FitchAverage Occupancy – 99+%Founding shareholders sold shares in public market

| appendix | 29 1994 2016 Stable and Attractive Lease Rates and Risk-Adjusted Returns Low lease rate volatility and strong investment spreads have resulted in superior risk-adjusted returns. S|T|O|R|E and predecessors’ average Lease Rates vs. 10-Year Treasuries Excess Return relative to Market Risk 2

Most Diversified Tenant Base Source: Latest publicly available financial information as of December 31, 2016. ¹ Includes: Agree Realty Corporation; EPR Properties; Lexington Realty Trust; Spirit Realty Capital, Inc.; VEREIT, Inc.; and W. P. Carey Inc. (weighted average lease term in years) Longest Lease Term Lowest Near-Term Renewal Exposure (% top 5 tenants, based on current annual rent) (% expirations by period, based on current annual rent) | appendix | Our net-lease portfolio has long contract terms and very high tenant diversification. High Quality Portfolio 30

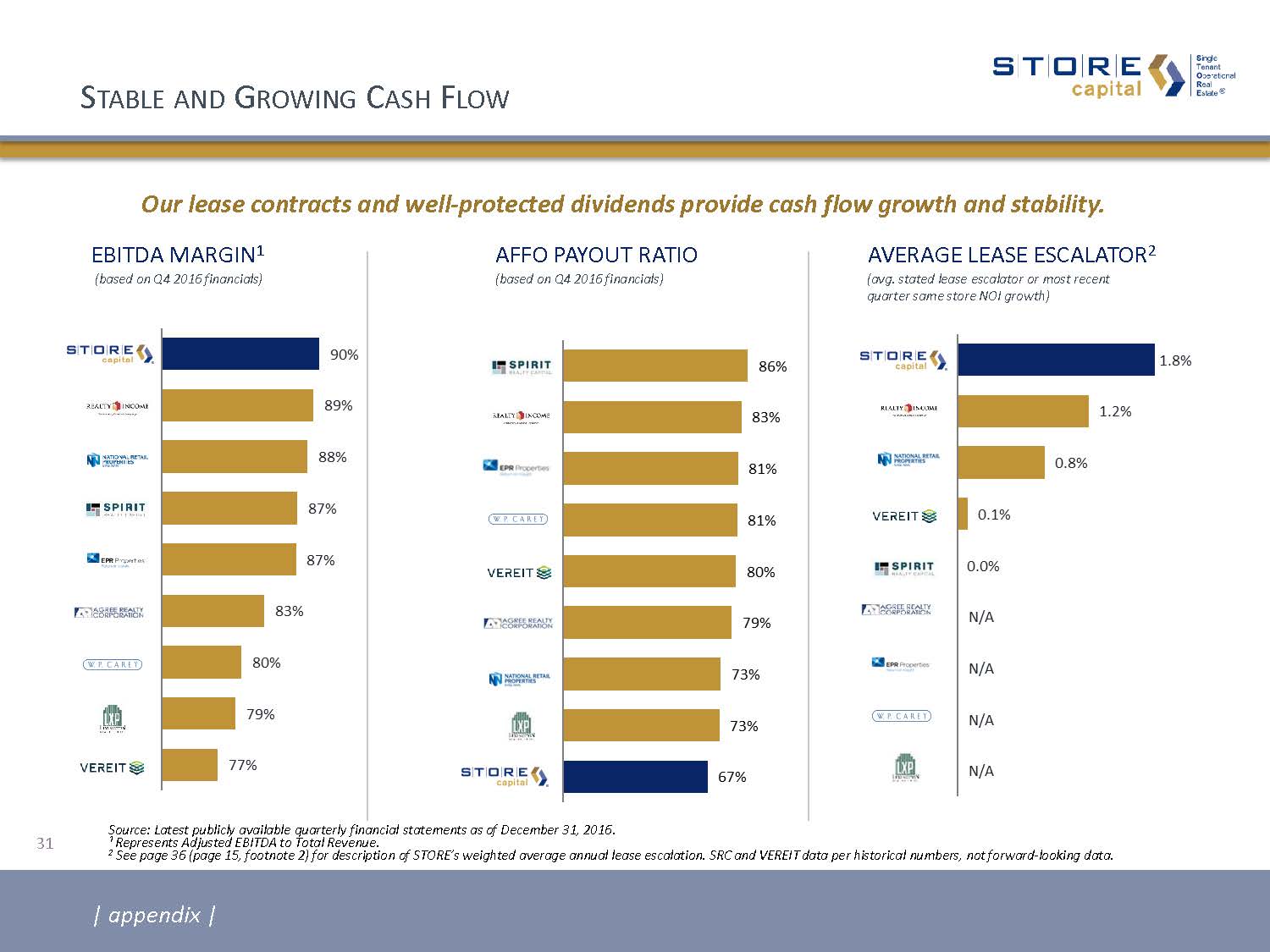

ebitda margin1 Average Lease escalator2 Source: Latest publicly available quarterly financial statements as of December 31, 2016. ¹ Represents Adjusted EBITDA to Total Revenue.2 See page 36 (page 15, footnote 2) for description of STORE’s weighted average annual lease escalation. SRC and VEREIT data per historical numbers, not forward-looking data. (based on Q4 2016 financials) affo payout ratio (avg. stated lease escalator or most recent quarter same store NOI growth) (based on Q4 2016 financials) Stable and Growing Cash Flow Our lease contracts and well-protected dividends provide cash flow growth and stability. | appendix | 31

MARY FEDEWAEVP – Acquisitions & DirectorCo-Founder; Executive Vice President – Acquisitions, Assistant Secretary and Assistant Treasurer since Company’s inception; Director since August 2016Former Managing Director of Acquisitions at Spirit; former Senior Vice President of GE Franchise Finance (successor company to FFCA)>20 years of experience in a broad range of financial servicesRecognized as a Woman of Influence in 2016 by Real Estate Forum magazine 32 Executive Management Team | appendix | CHRISTOPHER H. VOLKPresident, CEO & DirectorCo-Founder; CEO and Director since Company’s inception in May 2011Former Co-Founder, CEO and Director of Spirit Finance Corporation (“Spirit”); former President and Director of Franchise Finance Corporation of America (“FFCA”)>30 years of experience in structuring, managing and financing commercial real estate companiesLed largest ever real estate limited partnership roll-up transaction of its time in 1994 in formation of FFCA; oversaw issuance of FFCA's unsecured debt rating in 1995, the first unsecured debt rating ever issued to a net-lease REIT; led creation of first commercial real estate master trust debt conduit in the United States designed to finance net-lease assets in 2005 at Spirit CATHERINE LONGCFO, EVP & TreasurerCo-Founder; Executive Vice President – CFO, Treasurer and Assistant Secretary since Company’s inceptionFormer CFO and Treasurer of Spirit; former Principal Accounting Offer of FFCA>30 years of accounting, operating and financial management expertise Named CFO of the Year in 2008 by Arizona chapter of Financial Executives International CHRISTOPHER K. BURBACHEVP – UnderwritingExecutive Vice President – Underwriting since February 2012Former Vice President of Investment Management at Spirit; former CEO of VM ManagementBroad range of experience in credit, underwriting and financial analysis MICHAEL J. ZIEGEVP – Portfolio ManagementCo-Founder; Executive Vice President – Portfolio Management, Assistant Secretary and Assistant Treasurer since Company’s inceptionFormer Senior Vice President – Portfolio Management at Spirit; former partner of Kutak RockAlmost 20 years of experience in commercial real estate, spanning finance, transaction structuring, credit, and asset management and recovery MICHAEL T. BENNETTEVP – General Counsel, Chief Compliance Officer & SecretaryCo-Founder; Executive Vice President—General Counsel, Chief Compliance Officer, Corporate Secretary and Assistant TreasurerFormer Senior Vice President of Spirit; former General Counsel of Farmer Mac (NYSE:AGM)>30 years of legal, transactional and operational experience in real estate and finance industriesNamed best in-house attorney at the Arizona Corporate Counsel Awards in 2017 by Az Business magazine

33 Board of Directors | appendix | MORTON H. FLEISCHERChairmanChairman since inception in May 2011. Former Co-Founder and Chairman of Spirit and FFCA MARY FEDEWAEVP – Acquisitions & DirectorCo-Founder of S|T|O|R|E; EVP – Acquisitions since inception in May 2011; director since 2016 William F. HippDirectorDirector since 2016. Former head of real estate for Key Bank, BankBoston and FleetBoston with over 35 years in commercial banking Einar A. SeadlerDirectorDirector since 2016. Founder and President of EAS Advisors LLC; Former Managing Director of Accenture Strategy Joseph M. DonovanDirectorDirector since 2014. Chairman of Fly Leasing Limited (NYSE: FLY); Director of Institutional Financial Markets Inc. (AMEX: IFMI) Mark N. SklarDirectorDirector since August 2016. Founding partner and Director of DMB and its affiliated companies Quentin P. Smith, JrDirectorDirector since 2014. Founder and President of Cadre Business Advisors LLC; Director of Banner Health System CHRISTOPHER H. VOLKCEO & DirectorCo-Founder of S|T|O|R|E; CEO and Director since inception in May 2011. Former Co-Founder, CEO and Director of Spirit and President and Director of FFCA

34 Insider Stock Ownership Corporate governance guidelines contain minimum investment requirements. Both our Senior Management and our Board are invested in our success. 2017 Open Market Purchases Management Shares Price Shares Owned1 Requirement2 Christopher H. Volk 11,100 $22.7500 415,953 169,799 Catherine Long 10,455 $21.5157 149,992 50,354 Mary Fedewa 145,155 52,696 Michael T. Bennett 126,453 39,815 Michael J. Zieg 95,431 39,815 Christopher K. Burbach 5,500 $22.6500 77,882 39,815 Board Morton H. Fleisher 479,904 39,034 Joseph M. Donovan 5,000 $20.8100 40,625 9,759 William F. Hipp 4,000 $22.9853 14,499 9,367 Einar A. Seadler 4,440 $22.4557 13,031 9,754 Mark N. Sklar 5,000 $20.3360 11,725 8,553 Quentin P. Smith, Jr.3 14,470 9,759 CEO – 6x annual base salaryEVP – 3x annual base salaryDirectors – 5x annual cash retainer Minimum Equity Ownership Requirement 1 As of June 1, 2017.2 Based on average share price for 60 trading days following each individual’s requirement date.3 Sold 1,400 shares on March 9, 2017 at a price of $23.06 per share. | appendix |

35 Footnotes Page 31 Reflects the percentage of our contracts that have a STORE Score that is investment grade. We measure the credit quality of our portfolio on a contract-by-contract basis using the STORE Score, which is a proprietary risk measure reflective of both the credit risk of our tenants and the profitability of the operations at the properties.Page 41 Based on percentage growth of our investment portfolio for the year ended December 31, 2016.Page 71 Excludes customers, representing approximately 4.4% of annualized base rent and interest, that do not report corporate revenues. Page 91 Free cash flow approximates Adjusted Funds from Operations less dividends paid.Page 10:1 Based on average of ratios of Realty Income and National Retail Properties as of March 31, 2017.2 In addition to improved unencumbered asset ratios, unsecured lenders additionally benefit from the support of significant cash flows after debt service from assets subject to secured borrowings as well as a growing pool of unencumbered BBB rated Master Funding notes. 3 Ratios as of March 31, 2017; Unencumbered EBITDA based on NOI from Unencumbered Assets less an allocation of general and administrative expenses based on assets. Page 11: 1 Shown as of March 31, 2017, by % of annualized base rent and interest (annualized based on rates in effect on March 31, 2017, for all leases, loans and direct financing receivables in place as of that date). Excludes contracts representing less than 0.3% of annualized base rent and interest where there are no further escalations remaining in the current lease term and there are no extension options.2 Represents the weighted average annual escalation rate of the entire portfolio as if all escalations occurred annually. For escalations based on a formula including CPI, assumes the stated fixed percentage in the contract or assumes 1.5% if no fixed percentage is in the contract. For contracts with no escalations remaining in the current lease term, assumes the escalation in the extension term. 3 Dividend protection refers to the percentage difference between our AFFO per share and our dividend per share. The wider the relative gap between AFFO per share and dividends per share, the greater the implied dividend protection. All dividends are declared at the discretion of our Board of Directors and future dividends will depend upon our actual funds from operations, financial condition and capital requirements, the annual distribution requirements under the REIT provisions of the Code and other factors.4 S|T|O|R|E defines internal growth as the combination of high average lease escalators and a low AFFO payout ratio, which allows us to reinvest a growing amount of free cash flow back into our business. Page 12:1 See chart, page 28. | appendix |

Footnotes | appendix | 36 5 The percentage of investment portfolio subject to master leases represents the percentage of the investment portfolio in multiple properties with a single customer subject to master leases. Based on annualized base rent and interest, 83% of the investment portfolio involves multiple properties with a single customer, whether or not subject to a master lease.6 The average investment amount/replacement cost (new) represents the ratio of purchase price to replacement cost (new) at acquisition.7 S|T|O|R|E calculates unit fixed charge coverage ratio generally as the ratio of (i) the unit’s EBITDAR, less a standardized corporate overhead expense based on estimated industry standards, to (ii) the unit’s total fixed charges, which are its lease expense, interest expense and scheduled principal payments on indebtedness. The 4-Wall coverage ratio refers to a unit’s FCCR before taking into account standardized corporate overhead expense.8 The proportion of investment contracts rated investment grade represents the percentage of our contracts that have a STORE Score that is investment grade. We measure the credit quality of our portfolio on a contract-by-contract basis using the STORE Score, which is a risk measure reflective of both the credit risk of our tenants and the profitability of the operations at the properties. Page 16:1 Source: Bloomberg. Represents total return over period from January 1, 2016 through December 31, 2016. Past performance is not necessarily an indicator of future performance.2 Represents acquisitions of real estate and investment in loans receivable between January 1, 2016 and December 31, 2016.3 See footnote 3 to page 11 on page 35. Page 14:1 Our Board of Directors has opted out of the control share acquisition statute and business combination provisions in the Maryland General Corporation Law (called the “Maryland Unsolicited Takeover Law” or “MUTA”) and we may not opt back in to these provisions without stockholder approval.Page 15: * Based on annualized base rent and interest.1 Represents the percentage of our lease contracts that were created by S|T|O|R|E or contain preferred contract terms such as unit-level financial reporting, triple-net lease provisions and, when applicable, master lease provisions.2 Weighted average annual lease escalation represents the weighted average annual escalation rate of the entire portfolio as if all escalations occurred annually. For escalations based on a formula including CPI, assumes the stated fixed percentage in the contract orassumes 1.5% if no fixed percentage is in the contract. For contracts with no escalations remaining in the current lease term, assumes the escalation in the extension term. Calculation excludes contracts representing less than 0.3% of annualized base rent and interest where there are no further escalations remaining in the current lease term and there are no extension options.3 S|T|O|R|E defines occupancy as a property being subject to a lease or loan contract. 4 The number of properties not currently operating but subject to a lease represents the number of our investment locations that have been closed by the tenant but remain subject to a lease.

Footnotes | appendix | 37 4 S|T|O|R|E’s pipeline during the year ended December 31, 2016. See slide 21 for more information about S|T|O|R|E's pipeline, including its composition. S|T|O|R|E may never acquire properties in its pipeline for a variety of reasons as described in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2016.5 For the year ended December 31, 2016.Page 17:1 Data as of March 31, 2017, by % of annualized base rent and interest (annualized based on rates in effect on March 31, 2017, for all leases, loans and direct financing receivables in place as of that date).Page 18:1 Data based on information available on customer websites, news releases and/or SEC filings.2 See footnote 1 to page 17 above.Page 19:1 Based on annualized base rent and interest.Page 20:1 We measure the credit quality of our portfolio on a contract-by-contract basis using the STORE Score, which is a proprietary risk measure reflective of both the credit risk of our tenants and the profitability of the operations at our properties. The STORE Score is a quantitative measurement of contract risk computed by multiplying tenant default probabilities (using Moody’s RiskCalc) and estimated store closure probabilities (using a simple algorithm we developed that has closure probabilities ranging from 100% to 10%, depending on unit-level profitability). Qualitative features can also impact investment risk, such as low property investment amounts, favorabletenant debt capital stacks, the presence of third party guarantors, or other factors. Such qualitative factors may serve to further mitigate investment risk.Page 21:1 Four period moving average.Page 22:1 Represents acquisitions of real estate and investment in loan and direct financing receivables.2 Refer to pages 39 through 44 for definitions of these non-GAAP financial measures and reconciliation to GAAP net income.3 Gross Return represents initial cap rate plus weighted average annual lease escalators. Gross returns do not represent the actual returns we may earn on properties.4 S|T|O|R|E did not enter into any new debt in Q1 2016. Rate shown is weighted average rate for new long-term debt issued in April 2016.Page 23:Source: IBES Thomson Reuters. Data as of February 3, 2017.1 Represents 3-year historical normalized diluted EPS growth of five companies: CME Group Inc., Entergy Corporation, Host Hotels & Resorts, The Southern Company and Welltower Inc.2 Market data as of March 31, 2017; P/E multiple based on Goldman Sachs Research and EPS growth based on Goldman Sachs Research estimates.Page 24:1 See footnote 4 to page 11 on page 35.

Footnotes | appendix | 38 Page 25:1 Based on annualized total returns earned by management’s prior investment vehicles while operating as a public company, compared to annualized total returns on the MSCI US REIT Index during the same periods. The past performance of these investment vehicles is not an indicator of S|T|O|R|E’s future performance, and S|T|O|R|E’s performance may be significantly less favorable than the past performance data included in this presentation. Moreover, some of the past performance data covers periods with economic characteristics and cycles and interest rate environments that are significantly different from those S|T|O|R|E faces today and may face in the future.Page 27:¹ See previously filed Form 8-K’s for reconciliations of GAAP net income to AFFO for each quarterly period.2 AFFO per share is sensitive to the timing and amount of real estate acquisitions and capital markets activities during the year, as well as to the spread achieved between the lease rates on new acquisitions and the interest rates on borrowings used to finance those acquisitions. See Page 43 for further discussion regarding use of AFFO.Page 29:Source: Green Street Advisors, U.S. Treasury, Company data and with respect to FFCA and Spirit, publicly available SEC company filings¹ Risk for each sector measured as the standard deviation of capitalization rates during the periods of operation of FFCA, Spirit and S|T|O|R|E from January 1994 to December 2016. 2 The Sharpe Ratio measures the ratio of excess returns to risk, using the spread between capitalization or lease rates and the 10-year U.S. Treasury yields to measure excess returns, and using the standard deviation of returns to measure risk. All ratios are calculated using capitalization or lease rate data during which FFCA and Spirit were publicly traded companies and the period since S|T|O|R|E’s inception. The ratio is calculated based on historical data from January 1994 to September 2014, and future returns and risk may not be consistent with this historical data.

GAAP Reconciliations: Net Income to NOI Year EndedDecember 31, Three Months EndedMarch 31, $ millions 2014 2015 2016 2016 2017 NET INCOMELess: (Gain) loss on dispositions of real estateLess: Income from discontinued operations, net of tax $48.1(4.5)(1.1) $83.8(1.3)- $123.3(13.2)- $24.80.3- $31.4(3.7)- INCOME FROM CONTINUING OPERATIONSAdjustmentsIncome tax expenseDepreciation and amortizationGeneral and administrativeTransaction costsInterestSelling stockholder costsProvision for impairment of real estate $42.50.257.019.52.868.0- - $82.40.388.628.01.281.8-1.0 $110.10.4119.634.00.5105.20.81.7 $25.10.126.58.60.223.40.8- $27.70.135.210.2-29.6-4.3 NET OPERATING INCOME $190.0 $283.2 $372.3 $84.7 $107.2 | appendix | 39

GAAP Reconciliations: Net Income to FFO and AFFO Year EndedDecember 31, Three Months EndedMarch 31, $ millions 2014 2015 2016 2016 2017 NET INCOME Depreciation and amortization of real estate assets Provision for impairment of real estate (Gain) loss on dispositions of real estate $ 48.156.7-(5.5) $ 83.888.31.0(1.3) $123.3119.11.7(13.2) $24.826.4-0.3 $31.435.14.3(3.7) FUNDS FROM OPERATIONS (FFO) $ 99.4 $171.7 $230.9 $51.5 $67.0 Adjustments:Straight-line rental revenue, netTransaction costsNon-cash equity-based compensationNon-cash interest expenseAmortization of lease-related intangibles and costsSelling stockholder costs (2.4)2.82.37.10.7- (2.0)1.24.76.51.4- (2.3)0.57.07.31.70.8 (0.5)0.21.71.70.40.8 (1.2)-1.92.00.2- ADJUSTED FUNDS FROM OPERATIONS (AFFO) $109.9 $183.5 $245.8 $55.8 $70.0 | appendix | 40

GAAP Reconciliations: Debt to Adjusted Debt $ millions As ofMarch 31, 2017 Credit FacilityUnsecured long-term debt, netSecured long-term debt, net $ - 569.9 1,958.4 TOTAL DEBT $2,528.4 Adjustments:Unamortized net debt discountUnamortized deferred financing costsCash and cash equivalentsRestricted cash deposits held for the benefit of lenders 0.4 38.3 (103.3) (42.9) ADJUSTED DEBT $2,420.8 | appendix | 41

GAAP Reconciliations: Net Income to Adjusted EBITDA $ millions Three Months Ended March 31, 2017 NET INCOME $ 31.4 Adjustments:InterestDepreciation and amortizationIncome tax expense 29.635.20.1 EBITDA $ 96.4 Adjustments:Provision for impairment of real estateGain on dispositions of real estate 4.3(3.7) ADJUSTED EBITDA $ 96.9 Estimated additional Adjusted EBITDA for the quarter had all leases and loans in place as of March 31, 2017 been in place as of January 1, 2017 3.9 ADJUSTED EBITDA – CURRENT ESTIMATED RUN RATE $ 100.8 ANNUALIZED ADJUSTED EBITDA – CURRENT ESTIMATED RUN RATE $403.2 ADJUSTED DEBT / ANNUALIZED ADJUSTED EBITDA – CURRENT ESTIMATED RUN RATE 6.0x | appendix | 42

Supplemental Reporting Measures Funds from Operations, or FFO, and Adjusted Funds from Operations, or AFFO Our reported results are presented in accordance with U.S. generally accepted accounting principles, or GAAP. We also disclose Funds from Operations, or FFO, and Adjusted Funds from Operations, or AFFO, both of which are non‑GAAP measures. We believe these two non‑GAAP financial measures are useful to investors because they are widely accepted industry measures used by analysts and investors to compare the operating performance of REITs. FFO and AFFO do not represent cash generated from operating activities and are not necessarily indicative of cash available to fund cash requirements; accordingly, they should not be considered alternatives to net income as a performance measure or to cash flows from operations as reported on a statement of cash flows as a liquidity measure and should be considered in addition to, and not in lieu of, GAAP financial measures. We compute FFO in accordance with the definition adopted by the Board of Governors of the National Association of Real Estate Investment Trusts, or NAREIT. NAREIT defines FFO as GAAP net income, excluding gains (or losses) from extraordinary items and sales of depreciable property, real estate impairment losses and depreciation and amortization expense from real estate assets, including the pro rata share of such adjustments of unconsolidated subsidiaries. To derive AFFO, we modify the NAREIT computation of FFO to include other adjustments to GAAP net income related to certain non‑cash revenues and expenses that have no impact on our long-term operating performance, such as straight‑line rents, amortization of deferred financing costs and stock‑based compensation. In addition, in deriving AFFO, we exclude certain other costs not related to ongoing operations, such as the amortization of lease-related intangibles and, historically, transaction costs associated with acquiring real estate subject to existing leases. FFO is used by management, investors and analysts to facilitate meaningful comparisons of operating performance between periods and among our peers primarily because it excludes the effect of real estate depreciation and amortization and net gains on sales, which are based on historical costs and implicitly assume that the value of real estate diminishes predictably over time, rather than fluctuating based on existing market conditions. Management believes that AFFO provides more useful information to investors and analysts because it modifies FFO to exclude certain additional non-cash revenues and expenses such as straight‑line rents, amortization of deferred financing costs and stock‑based compensation as such items may cause short-term fluctuations in net income but have no impact on long-term operating performance. Additionally, in deriving AFFO, we exclude certain other costs, such as the amortization of lease-related intangibles and, historically, transaction costs associated with acquiring real estate subject to existing leases. We believe that these costs are not an ongoing cost of the portfolio in place at the end of each reporting period and, for these reasons, we add back the portion expensed when computing AFFO. Similarly, in 2016 we excluded the offering expenses incurred on behalf of our selling stockholder, STORE Holding, when it exited all of its holdings of STORE Capital common stock, as those costs are not related to our ongoing operations. As a result, we believe AFFO to be a more meaningful measurement of ongoing performance that allows for greater performance comparability. Therefore, we disclose both FFO and AFFO and reconcile them to the most appropriate GAAP performance metric, which is net income. STORE Capital’s FFO and AFFO may not be comparable to similarly titled measures employed by other companies. | appendix | 43

Supplemental Reporting Measures (Continued) EBITDA, Adjusted EBITDA, Annualized Adjusted EBITDA and Adjusted DebtEBITDA represents earnings before interest, taxes, depreciation and amortization.Adjusted EBITDA represents EBITDA modified to include other adjustments to GAAP net income for transaction costs, non-cash impairment charges and gains/losses on dispositions of real estate and certain other expenses not related to ongoing operations. Annualized Adjusted EBITDA is calculated by multiplying Adjusted EBITDA for the quarter by four. Annualized Adjusted EBITDA – Current Estimated Run Rate is calculated based on an estimated Adjusted EBITDA as if all leases and loans in place as of March 31, 2017 had been in place as of January 1, 2017; then annualizing the Adjusted EBITDA for the quarter by multiplying it by four. You should not unduly rely on this metric as it is based on several assumptions and estimates that may prove to be inaccurate. Our actual reported Adjusted EBITDA for future periods may be significantly less than that implied by our reported Annualized Adjusted EBITDA – Current Estimated Run Rate for a variety of reasons.Adjusted Debt represents our outstanding debt obligations excluding unamortized deferred financing costs and net debt premium, further reduced for cash and cash equivalents and restricted cash deposits held for the benefit of lenders. We believe excluding unamortized deferred financing costs and net debt premium, cash and cash equivalents and restricted cash deposits held for the benefit of lenders provides an estimate of the net contractual amount of borrowed capital to be repaid which we believe is a beneficial disclosure to investors and analysts. Adjusted Debt to Annualized Adjusted EBITDA Adjusted Debt to Annualized Adjusted EBITDA, or leverage, is a supplemental non-GAAP financial measure we use to evaluate the level of borrowed capital being used to increase the potential return of our real estate investments. We calculate leverage by dividing Adjusted Debt by Annualized Adjusted EBITDA. Because our portfolio growth level is significant to the overall size of the Company, we believe that presenting this leverage metric on a run rate basis is more meaningful than presenting the metric for the historical quarterly period, and we refer to this metric as Adjusted Debt to Annualized Adjusted EBITDA—Current Estimated Run Rate. Leverage should be considered as a supplemental measure of the level of risk to which stockholder value may be exposed. Our computation of leverage may differ from the methodology employed by other companies, and, therefore, may not be comparable to other measures. | appendix | 44