Attached files

| file | filename |

|---|---|

| EX-23 - EX-23 - STORE CAPITAL Corp | stor-20141231xex23.htm |

| EX-21 - EX-21 - STORE CAPITAL Corp | stor-20141231ex214763bd0.htm |

| EX-32.1 - EX-32.1 - STORE CAPITAL Corp | stor-20141231ex32158b356.htm |

| EX-32.2 - EX-32.2 - STORE CAPITAL Corp | stor-20141231ex32254f3c4.htm |

| EX-31.2 - EX-31.2 - STORE CAPITAL Corp | stor-20141231ex312fb527a.htm |

| EX-31.1 - EX-31.1 - STORE CAPITAL Corp | stor-20141231ex311fe6aa9.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

or

|

◻ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File No. 001-36739

STORE CAPITAL CORPORATION

(Exact name of registrant as specified in its charter)

|

Maryland |

|

45-2280254 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

8501 East Princess Drive, Suite 190, Scottsdale, Arizona 85255

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (480) 256-1100

Securities Registered Pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock, $0.01 par value |

|

New York Stock Exchange |

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ◻ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ◻

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ◻ No ◻

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

◻ |

Accelerated filer |

◻ |

|

|

|

|

|

|

Non-accelerated filer |

☒ |

Smaller reporting company |

◻ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ◻ No ☒

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of a share of the registrant’s common stock on November 18, 2014 as reported on the New York Stock Exchange on such date, was approximately $616,687,500. The registrant has elected to use November 18, 2014, which was the initial trading date on the New York Stock Exchange, as the calculation date because on June 30, 2014 (the last business day of the registrant’s most recently completed second fiscal quarter), the registrant was a privately held company. Shares of the registrant’s common stock held by each executive officer, director and beneficial owner of more than 5% of the outstanding common stock have been excluded from the calculation, as such persons may be deemed to be affiliates. This determination of affiliate status should not be deemed conclusive for any other purpose. As of March 6, 2015, there were 115,210,809 shares of the registrant’s common stock outstanding.

Documents Incorporated by Reference

Portions of Part III of this Form 10-K are incorporated by reference from the registrant’s definitive proxy statement for its 2015 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission no later than 120 days after the end of the registrant’s fiscal year.

TABLE OF CONTENTS

In this Annual Report on Form 10-K (the “Annual Report”), we refer to STORE Capital Corporation, a Maryland corporation, as “we,” “us,” “our,” “the Company” or “S|T|O|R|E,” unless we specifically state otherwise or the context indicates otherwise.

Forward-Looking Statements

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements include, without limitation, statements concerning our business and growth strategies, investment, financing and leasing activities and trends in our business, including trends in the market for long-term, triple-net leases of freestanding, single-tenant properties. Words such as “expects,” “anticipates,” “intends,” “plans,” “likely,” “will,” “believes,” “seeks,” “estimates,” and variations of such words and similar expressions are intended to identify such forward-looking statements. Such statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from the results of operations or plans expressed or implied by such forward-looking statements. Although we believe that the assumptions underlying the forward-looking statements contained herein are reasonable, any of the assumptions could be inaccurate, and therefore such statements included in this Annual Report may not prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by us or any other person that the results or conditions described in such statements or our objectives and plans will be achieved. For a further discussion of these and other factors that could impact future results, performance or transactions, see “Item 1A. Risk Factors” elsewhere in this Annual Report.

Forward-looking statements and such risks, uncertainties and other factors speak only as of the date of this Annual Report, and we expressly disclaim any obligation or undertaking to update or revise any forward-looking statement contained herein, to reflect any change in our expectations with regard thereto, or any other change in events, conditions or circumstances on which any such statement is based, except to the extent otherwise required by law.

General

S|T|O|R|E is an internally managed net‑lease real estate investment trust, or REIT, that is the leader in the acquisition, investment and management of Single Tenant Operational Real Estate, or STORE Properties, which is our target market and the inspiration for our name. A STORE Property is a real property location at which a company operates its business and generates sales and profits, which makes the location a profit center and, therefore, fundamentally important to that business.

S|T|O|R|E continues the investment activities of our senior leadership team, which has been investing in single‑tenant operational real estate for over thirty-five years. We are one of the largest and fastest‑growing net‑lease REITs, as demonstrated by the table below, and own a large, well‑diversified portfolio that consists of investments in 947 property locations operated by 226 customers across 46 states as of December 31, 2014. Our customers operate across a wide variety of industries within the service, retail and industrial sectors of the U.S. economy, with restaurants, early childhood education centers, health clubs, movie theaters and sporting goods stores representing the top industries in our portfolio.

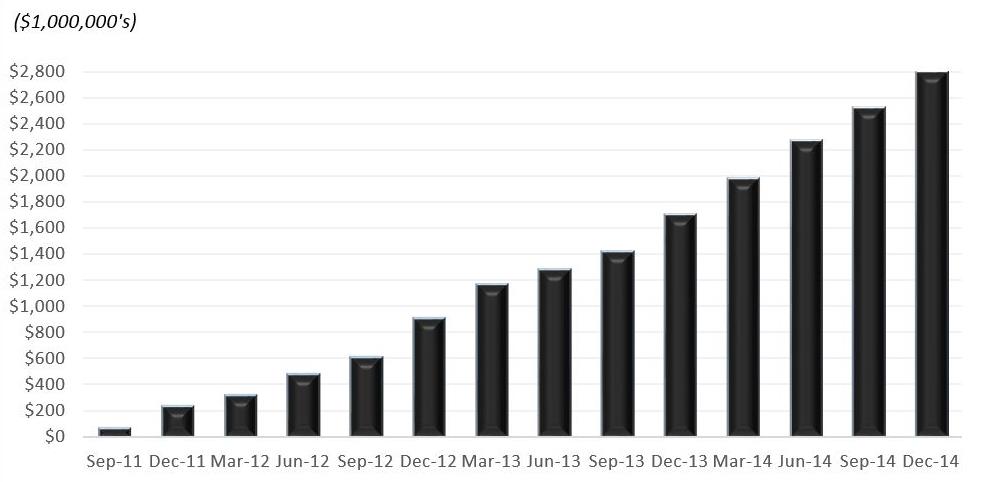

Our Total Investment Portfolio at Quarter End

We have elected to be taxed as a REIT under the Internal Revenue Code, as amended, which we refer to in this Annual Report as the “Code,” commencing with our initial taxable year ended December 31, 2011. To continue to qualify as a REIT, we must continue to meet certain tests which, among other things, generally require that our assets consist primarily of real estate assets, our income be derived primarily from real estate assets, and that we distribute at least 90% of our REIT taxable income (other than our net capital gains) to our stockholders annually.

Although we are a public company, we are a “controlled company” (within the meaning of the rules of the New York Stock Exchange, or NYSE) because a substantial portion of our common stock (approximately 71%) is owned indirectly by certain investment funds managed by Oaktree Capital Management, L.P. Oaktree is a global investment management firm specializing in alternative investments with approximately $91 billion in assets under management as of December 31, 2014.

2014 Highlights

|

· |

On November 21, 2014, we completed our initial public offering, or IPO, of 31,625,000 shares of our common stock, including 4,125,000 shares of common stock sold in connection with the full exercise of the underwriters’ option to purchase additional shares, at a price to the public of $18.50 per share. The shares began trading on the New York Stock Exchange on November 18, 2014 under the ticker symbol “STOR”. Net proceeds from the sale of our common stock were approximately $545.8 million after deducting underwriting discounts and commissions and offering expenses, the majority of which has been used as of December 31, 2014 to pay down outstanding credit facility debt and for portfolio acquisitions. |

|

· |

In September 2014, we entered into a new three-year $300 million unsecured revolving credit facility, which replaced our two existing secured credit facilities that aggregated $300 million. This new facility includes an accordion feature that allows the size of the facility to be increased up to $500 million and provides us more flexibility at a lower cost than our previous facilities. |

|

· |

In May 2014, we issued our fifth series of STORE Master Funding net-lease mortgage notes payable, aggregating $260 million in principal amount. In addition, we added $53 million of traditional mortgage debt in 2014, bringing our total long-term outstanding debt to $1.28 billion at December 31, 2014, up from $992 million at December 31, 2013. Of our total gross investment in real estate of $2.8 billion at year-end,

2 |

approximately $1.85 billion is utilized as collateral for our $1.28 billion of secured debt outstanding, leaving $952 million of real estate assets unencumbered as of December 31, 2014. |

|

· |

For the year ended December 31, 2014, we declared dividends of $0.9898 per common share to our stockholders, which includes a pro-rated dividend per common share of $0.1139, or $1.00 per share on an annualized basis, for the period since the closing of the IPO through December 31, 2014. |

|

· |

During the year ended December 31, 2014, we invested over $1.1 billion in 341 property locations. |

Our Target Market

We are the leader in providing real estate financing solutions principally to middle‑market and larger businesses that own STORE Properties and operate within the broad-based service, retail and industrial sectors of the U.S. economy. Our net‑lease solutions are designed to provide a long‑term, lower‑cost way to improve our customers’ capital structures and, thus, be a preferred alternative to real estate ownership. We estimate the market for STORE Properties to exceed $2.3 trillion in market value and to include more than 1.5 million properties.

We define middle‑market companies as those having approximate annual gross revenues of between $20 million and $300 million, although some of our customers have annual revenues substantially in excess of $300 million. Most of our customers do not have credit ratings, while some have ratings from rating agencies that service insurance companies or fixed‑income investors. Most of these non-rated companies either prefer to be unrated or are simply too small to issue debt rated by a nationally recognized rating agency in a cost‑efficient manner.

Despite the market’s size, the financing marketplace for STORE Properties is highly fragmented, with few participants addressing the long‑term capital needs of middle‑market and larger non-rated companies. While we believe our net‑lease financing solutions can add value to a wide variety of companies, we believe the largest underserved market and, therefore, our greatest opportunity is non-rated, bank‑dependent, middle‑market and larger companies that generally have less access to efficient sources of long‑term capital.

We believe the demand for our net‑lease solutions is even greater today as a result of the current bank regulatory environment. In our view, the increased scrutiny and regulation of the banking industry over the past several years in response to the collapse of the housing and mortgage industries from 2007 to 2009, particularly with the passage of the Dodd‑Frank Wall Street Reform and Consumer Protection Act and the Basel Accords issued by the Basel Committee on Banking Supervision, have made commercial banks even less responsive to the long‑term capital needs of the middle‑market companies we target. These companies have historically depended on commercial banks for their financing.

S|T|O|R|E was formed to capitalize on this market opportunity and address the capital needs of middle‑market and larger non-rated companies by offering them a superior alternative to financing their profit‑center real estate with traditional mortgage or bank debt and their own equity. We believe our opportunities include both gaining market share from the fragmented network of net‑lease capital providers and growing the market by creating demand for our net‑lease solutions that meet the long‑term real estate capital needs of these companies.

Our target market of STORE Properties is divided into three primary sectors and various sub-sectors. The primary sectors and their proportion of our target market are service at 47%, retail at 37% and industrial at 16%. The sub-sectors included within each primary sector are summarized in the table below.

|

Service |

|

Retail |

|

Industrial |

|

Restaurants |

|

Big box retail |

|

Industrial profit-centers |

|

Education |

|

Specialty retail |

|

|

|

Fitness centers |

|

Grocery |

|

|

|

Transportation |

|

Drug stores |

|

|

|

Automotive services |

|

Automotive (new and used) |

|

|

|

Family entertainment |

|

|

|

|

3

Within the sub‑sectors, the market for STORE Properties is further subdivided into a wide variety of industries within the service, retail and industrial sectors, such as:

|

Automotive parts stores |

|

Movie theaters |

|

Cold storage facilities |

|

Office supplies retailers |

|

Department stores |

|

Pet care facilities |

|

Discount stores |

|

Rental centers |

|

Early childhood education |

|

Secondary education |

|

Furniture stores |

|

Supermarkets |

|

Entertainment facilities |

|

Truck stops |

|

Fast food restaurants |

|

Wholesale clubs |

|

Full service restaurants |

|

|

Many of these industries are represented within our diverse property portfolio.

Our Asset Class: STORE Properties

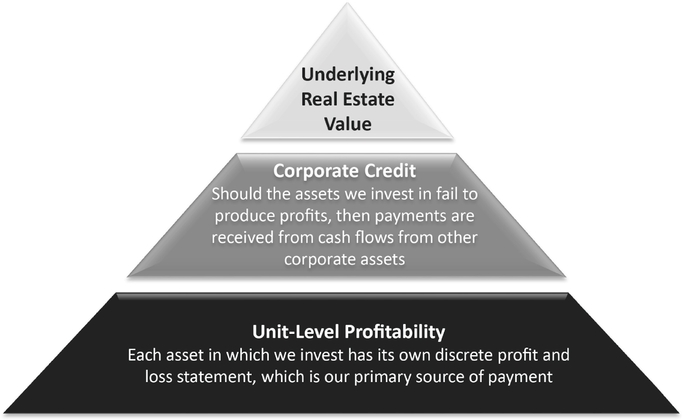

Single Tenant Operational Real Estate, or STORE Properties, is a unique asset class that inspired the formation of S|T|O|R|E and our company name. STORE Properties are profit-center real estate locations on which our tenants conduct their businesses and generate their revenues and profits. The defining characteristic of STORE Properties is the number of payment sources: STORE Properties have three payment sources, whereas all other commercial real estate assets have just two.

|

· |

Unit-Level Profitability: STORE Properties are distinguished by the primary source of their rent payment, which comes directly from the profits produced by the business operations at the real estate locations we own, which we refer to as ‘unit-level profitability.’ While it is a common perception that the tenant is the primary source of the rent payment (as distinguished from the business at the unit itself), the historic pattern we have observed of tenants in corporate insolvencies vacating unprofitable locations and retaining profitable ones is the main indicator of the payment source. Because tenants historically retain profitable locations and vacate unprofitable ones in the event of insolvency, it is fundamentally important for S|T|O|R|E to collect and review the unit-level financial statements of our tenants at our real estate locations, which is a key component of our business model. As of December 31, 2014, we receive unit-level financial statements on over 96% of the properties in our portfolio. Without having access to unit-level financial reporting for the business activities conducted on the properties we own, we would not have an accurate assessment of the essential nature of our real estate to our customer’s business; without this, we would be speculating about the quality of the most important, and primary, payment source. |

|

· |

Tenant Credit Quality. In addition to the unit-level profitability of the business on the real estate we own, there are two other payment sources that are common to all real estate investments. One is tenant credit quality, which serves as an additional, but not primary, source of payment to unit-level profitability. The tenant’s credit can become the primary payment source if our unit is not profitable and the tenant is required to divert cash flows from its other units or other resources to pay our rents. However, tenant credit quality tends to be subject to greater volatility over time than unit-level profitability, because tenant credit quality is not only a function of the unit-level profitability of the operations at our locations, but of the profitability of potentially many other existing and new assets owned and operated by our tenant. Corporate financial health is also a function of many other decisions, such as capital structure or growth strategies, as well as conditions in the marketplace for the tenant’s products and services, which can change over time and which may have profound impacts on tenant creditworthiness. |

|

· |

Real Estate Residual Value. The other payment source that is common to all real estate investments (and is the third of our three payment sources) is the residual value of the underlying real estate, which gives us the opportunity to receive rents from other substitute tenants in the event our asset becomes vacant. For S|T|O|R|E, this means more than just looking at broad lease rate and transaction comparables. Studies we have done underscore the importance of investing in properties at or below their as-new replacement costs. We also review the local markets in which our properties are located and seek to have rents that are at or

4 |

below prevailing market rents on a per square foot basis for comparable properties. Taking these steps protects S|T|O|R|E and our customers by making it easier for us to assign, sell or sublease properties that our customers may want to sell, reposition or vacate as part of their capital efficiency strategy. |

The following diagram illustrates the three sources of payment that are common among STORE Properties:

The S|T|O|R|E Credit Pyramid

The investment, management and capitalization competencies we have developed over more than thirty-five years, like our credit pyramid, arise from the distinctive characteristics of the large asset class of STORE Properties we address.

Our Competitive Strengths

Our objective is to build upon our market‑leading platform for the acquisition, investment and management of STORE Properties that simultaneously creates value for stockholders and customers through our five corporate competencies. Each member of our senior leadership team is primarily responsible for one of our five competencies, which are described below:

|

· |

Investment Origination. S|T|O|R|E Capital was formed to fill a need for efficient long-term real estate capital for middle-market and larger customers. We do this principally by creating lease contracts that address our customers’ needs and create strong alignments of interest that benefit our stockholders. By creating demand for our services, and not simply taking market share or aggregating assets, we have maintained a large pipeline of investment opportunities ever since we commenced operations in 2011. As a result, approximately 75% of our investments (by dollar volume) have been originated by our internal origination team through direct customer relationships using our form financing documents. Our objective is to be both selective and achieve higher rates of return than our stockholders could achieve if they sought to acquire profit-center real estate on their own. At the same time, our solutions-oriented approach strives to create superior value for our customers over other financing options they may have to capitalize their businesses. |

|

· |

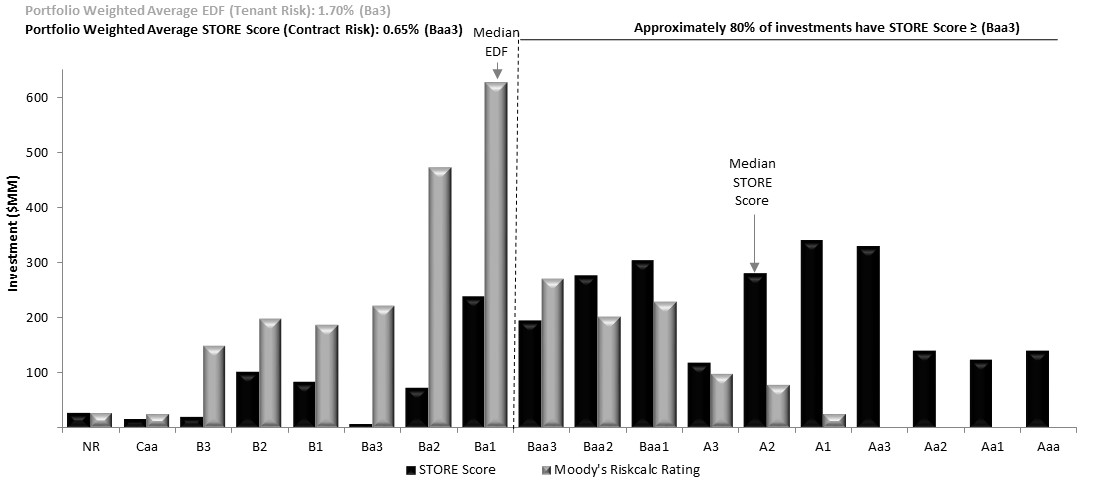

Investment Underwriting. Our methods of risk evaluation have been developed by our senior leadership team over thirty-five years, more than $12 billion and over 8,000 STORE Property investments. Our investment underwriting approach centers on evaluations of unit-level and corporate-level financial performance, together with detailed real estate valuation assessments. These three areas represent our credit pyramid, which is reflective of the characteristics of the STORE Property asset class. At S|T|O|R|E,

5 |

we have combined our underwriting approach with our portfolio management systems to capture tenant credit ratings and lease contract ratings (referred to as a S|T|O|R|E Score) as tools to monitor ongoing portfolio performance. Our collective experience has enabled us to develop sophisticated risk evaluation tools and insights that are designed to offer greater risk-adjusted investment results than those available to most real estate investors. |

The following table compares our tenant credit ratings (determined using Moody’s Riskcalc) with the STORE Score:

|

· |

Investment Documentation. For over thirty-five years, we have learned that lease contracts, and not tenant credit quality, are the principal determinants of investment risk. Part of contract creation is embodied in the investment underwriting process, which focuses on the following factors: the prices we pay for the real estate; the unit-level profitability of the businesses operated on our real estate; the rents and escalations we receive; and the support offered to the investment by tenant credit quality. These factors are ultimately incorporated into our contracts and supported by third party diligence, including appraisals, property condition reports, environmental reports and other diligence. Finally, the contracts we create foster alignments of interest through the use of features such as master leases and bankruptcy-remote investment structures. Altogether, our documentation process, like our approach to underwriting, has evolved over decades and offers investors in S|T|O|R|E a value that most could not create for themselves. |

|

· |

Portfolio Management. Net-lease real estate investment portfolios require active management in order to realize superior risk-adjusted rates of return. With a diversified portfolio, we have developed highly effective approaches that place greater focus on the minority of investments that have a higher risk potential to experience future problems. For over thirty-five years, we have learned how to monitor unit-level profit and loss statements, tenant corporate financial statements and the timely payment of property taxes and insurance in order to gauge portfolio quality. S|T|O|R|E represents our third, and most highly developed, servicing platform. We are virtually paperless, have access to granular or highly detailed information on our portfolio from virtually anywhere and are highly scalable. Having such systems helps us effectively monitor and reduce tenant credit risk at the property level. And when combined with our high degree of financial and operating flexibility, we are able to realize better stockholder risk-adjusted rates of return on our invested capital. |

|

· |

Financial Reporting and Treasury. We consider and evaluate our corporate financing strategies with the same emphasis as our real estate investment strategies. Borrowings must prudently improve stockholder returns; they must be structured to provide portfolio flexibility and minimize our exposure to changes in long-term interest rates; they must be structured to optimize our cost of financing that will enhance investor

6 |

rates of return; and finally, a liability strategy should contribute to corporate governance by enhancing corporate flexibility. Our senior leadership team has extensive experience with diverse liability strategies. Today, we are one of the few REITs to employ our own A+ rated borrowing source. Our senior leadership team developed our master funding conduit strategy in 2005, which is ideally suited to finance diverse portfolios of profit-center real estate, such as ours. The strategies we implement are designed to add value to our investors by offering a more efficient means to finance real estate than they could otherwise do on their own. At the same time, the flexibility we derive from our liability strategies can also result in important flexibility for our customers. |

Our Business and Growth Strategies

Our objective is to continue to create stockholder value through sustained investment and management activities designed to grow distributable cash flows and deliver attractive risk-adjusted rates of return from a growing, diverse portfolio of STORE Properties. To accomplish this, our principal business and growth strategies are as follows:

|

· |

Continue to Focus on Middle‑Market Companies Operating STORE Properties. We believe we have selected the most attractive investment opportunity within the net‑lease market, STORE Properties, and targeted the most attractive customer type within that market, middle‑market and larger non-rated companies. We focus on this market given its strong fundamentals and outsized growth potential. Within the net‑lease market for STORE Properties, our value proposition is most compelling to middle‑market, bank‑dependent companies who are not rated by any nationally recognized rating agency due to their size or capital markets preferences, but who have strong credit metrics and operate within broad-based industries having the potential for sustained relevance. |

|

· |

Realize Stable Income and Internal Growth. We seek to make investments that generate strong and stable current income as a result of the difference, or spread, between the rate we earn on our assets and the rate we pay on our liabilities (primarily our long‑term debt). We augment that income with internal growth. We seek to realize superior internal growth through a combination of (1) a target dividend payout ratio that permits a level of free cash flow reinvestment and (2) cash generated from the 1.7% weighted average annual escalation of base rent and interest in our portfolio (as of December 31, 2014). We benefit from contractual rent escalations, as nearly 97% of our leases and loans (by annualized base rent and interest) have escalations that are either fixed (23%) or based on the Consumer Price Index, or CPI (74%). We believe this will enable strong dividend growth without relying exclusively on future common stock issuances to fund new portfolio investments. |

|

· |

Capitalize on Direct Origination Capabilities for External Growth. As the market leader in STORE Property investment originations, we plan to complement our internal growth with continued new investments that are funded through future equity issuances and borrowings to expand our platform and raise investor cash flows. |

|

· |

Actively Manage our Balance Sheet to Maximize Capital Efficiency. We seek to select funding sources designed to lock in long‑term investment spreads and limit interest rate sensitivity. We also seek to maintain a prudent balance between the use of debt (which includes our own STORE Master Funding program, commercial mortgage-backed securities, or CMBS, borrowings, insurance borrowings, bank borrowings and possibly preferred stock issuances) and equity financing. As of December 31, 2014, the long‑term, non‑recourse debt of our consolidated special purpose entities had an aggregate outstanding principal balance of $1.3 billion, a weighted average maturity of 6.9 years and a weighted average interest rate of 4.9%. On an annualized basis, our fourth quarter adjusted debt to earnings before interest, taxes, depreciation and amortization, or EBITDA, was under 6x and, as we move forward as a public company, we are targeting a ratio of between 6x and 7x. |

|

· |

Increase our portfolio diversity. As of December 31, 2014, we had invested $2.8 billion in 947 property locations, substantially all of which are profit centers for our customers. Our portfolio is highly diversified with 226 customers operating 208 different brand names, or business concepts, across 46 states and over 65 industry groups. None of our customers represented more than 4% of our portfolio as of

7 |

December 31, 2014, based on annualized base rent and interest. Our portfolio’s diversity decreases the impact on us of an adverse event affecting a specific customer, industry or region, thereby increasing the stability of our cash flows. Additional acquisitions in the future will further increase the diversity of our portfolio and, from time to time, we may sell properties in our portfolio to improve overall portfolio credit quality or diversity. |

Competition

We face competition in the acquisition and financing of STORE Properties from numerous investors, including traded and non‑traded public REITs, private equity investors and institutional investment funds, some of which have greater financial resources than we do, a greater ability to borrow funds to acquire properties and the ability to accept more risk. We also believe that competition for real estate financing comes from middle‑market business owners themselves, many of whom have had a historic preference to own, rather than lease, the real estate they use in their businesses. The competition we face may increase the demand for STORE Properties and, therefore, reduce the number of suitable acquisition opportunities available to us or increase the price we must pay to acquire STORE Properties. This competition will increase if investments in real estate become more attractive relative to other forms of investment.

Employees

As of December 31, 2014, we had 50 full‑time employees, all of whom are located in our single office in Scottsdale, Arizona. None of our employees are subject to a collective bargaining agreement. We consider our employee relations to be good.

Principal Executive Offices

Our principal offices are located at 8501 East Princess Drive, Suite 190, Scottsdale, Arizona 85255. We currently occupy approximately 14,000 square feet of space leased from an unaffiliated third party. We believe that our offices are adequate for our present and currently planned future operations and that adequate additional space will be available if needed in the future.

Insurance

Our leases and loan agreements typically require our tenants and borrowers to maintain insurance of the types and in the amounts that are usual and customary for similar commercial properties, including commercial general liability, fire and extended loss insurance provided by reputable companies, with commercially reasonable exclusions, deductibles and limits, all as verified by our independent insurance consultant.

Separately, we purchase contingent liability insurance, in excess of our tenants’ and borrowers’ liability coverage, to provide us with additional security in the event of a catastrophic claim. Also, we purchase property coverage, on a case-by-case basis, where we believe such additional insurance is warranted.

Regulation

Our properties are subject to various laws and regulations, including regulations relating to fire and safety requirements, ordinances and affirmative and negative covenants and in some instances, common area obligations. Our tenants and borrowers have primary responsibilities for compliance with these requirements pursuant to our lease and loan agreements. We believe that each of our tenants and borrowers have the necessary permits and approvals to operate and conduct their businesses on our properties.

Environmental Matters

General. All real property and the operations conducted on real property are subject to federal, state and local laws and regulations relating to human health and the environment. Certain of these laws and regulations may impose joint and several liability on certain statutory classes of persons, including owners or operators, for the costs of investigation or remediation of contaminated properties, regardless of fault or the legality of the original disposal.

8

These laws and regulations apply to past and present business operations of our tenants and borrowers and the use, storage, handling and contracting for recycling or disposal of hazardous substances or wastes. Our tenants and borrowers are obligated to comply with environmental laws. Our leases and loans typically impose obligations on our tenants and borrowers to indemnify us from all or most compliance costs we may experience as a result of the environmental conditions on our properties. If a tenant or borrower fails to, or cannot, comply we may be required to pay such costs. We are not aware of any environmental condition with respect to any of our properties which would have a material adverse effect on our business, financial condition or results of operations. We cannot predict whether new or more stringent laws relating to the environment will be enacted in the future or how such laws will impact the operations of businesses at our properties. Costs associated with an environmental event could be substantial.

Superlien Laws. Under the laws of many states, contamination on a site may give rise to a lien on the site for clean‑up costs. In several states, such a lien has priority over all existing liens, including those of existing mortgages. In these states, the lien of a mortgage may lose its priority to such a “superlien.”

CERCLA. The federal Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended, or CERCLA, imposes strict liability on present and past “owners” and “operators” of a contaminated site for the costs of clean‑up. A secured lender may be liable as an “owner” or “operator” of a contaminated site if agents or employees of the lender have participated in the management of such site or in the operations of the tenant. Excluded from CERCLA’s definition of “owner” or “operator” however, is a person “who without participating in the management of the facility, holds indicia of ownership primarily to protect his security interest”. This is the so called “secured creditor exemption.” With respect to most of the assets in our investment portfolio, we are the owner of the real property. However, with respect to a few of the assets in our investment portfolio, we are not the owner of the property but have a mortgage loan on the property. In both instances, we believe we meet the secured creditor exemption.

Liability is not limited to the original or unamortized principal balance of a loan or to the value of the site securing a loan. CERCLA provides substantial protection to lenders by defining the activities in which a lender can engage and still have the benefit of the secured creditor exemption. In order for a lender to be deemed to have participated in the management of a site, the lender must actually participate in the operational affairs of the site or our tenant or borrower. CERCLA provides that “merely having the capacity to influence, or unexercised right to control” operations does not constitute participation in management. A lender may lose the protection of the secured creditor exemption only if it exercises decision‑making control over our tenant’s or borrower’s environmental compliance and hazardous substance handling and disposal practices, or assumes responsibility for substantially all operational functions at the site or overall management encompassing day‑to‑day decision making with regard to environmental compliance. CERCLA also provides that a lender will continue to have the benefit of the secured creditor exemption even if it forecloses on a site, purchases it at a foreclosure sale or accepts a deed‑in‑lieu of foreclosure provided that the lender seeks to sell the site at the earliest practicable commercially reasonable time on commercially reasonable terms.

Certain Other Federal and State Laws. Many states have statutes similar to CERCLA, and not all of those statutes provide for a secured creditor exemption. In addition, under federal law, there is potential liability relating to hazardous wastes and underground storage tanks under the Federal Resource Conservation and Recovery Act, or RCRA. The definition of “hazardous substances” under CERCLA specifically excludes petroleum products. Subtitle I of RCRA governs underground petroleum storage tanks. The protections accorded to lenders under CERCLA are also accorded to the holders of security interests in underground petroleum storage tanks if the lender does not participate in management of the underground storage tanks and is not otherwise engaged in petroleum production, refining or marketing. It should be noted, however, that liability for cleanup of petroleum contamination may be governed by state law, which may not provide for any specific protection for secured creditors.

In a few states, transfers of some types of sites are conditioned upon cleanup of contamination prior to transfer. In these cases, a lender that becomes the owner of a site through foreclosure, deed in lieu of foreclosure or otherwise, may be required to clean up the contamination before selling or otherwise transferring the site.

Also, certain federal, state and local laws govern the removal, encapsulation or disturbance of asbestos‑containing materials, or ACMs, in the event of the remodeling, renovation or demolition of a building. Such

9

laws, as well as common law standards, may impose liability for releases of ACMs and may provide for third parties to seek recovery from owners or operators of sites for personal injuries associated with such releases.

Beyond statute‑based environmental liability, there exist common law causes of action (for example, actions based on nuisance or on toxic tort resulting in death, personal injury or damage to site) related to hazardous environmental conditions on a site. While it may be more difficult to hold a lender liable in such cases, unanticipated or uninsured liabilities of our tenant or borrower may jeopardize the tenant’s or borrower’s ability to meet its lease or loan obligations.

Additional Considerations. The cost of remediating hazardous substance contamination at a site can be substantial. If a lender becomes liable, it can bring an action for contribution against the owner or operator who created the environmental hazard, but that individual or entity may be without substantial assets.

If a lender forecloses on a mortgage secured by a site on which business operations are subject to environmental laws and regulations, the lender will be required to operate the site in accordance with those laws and regulations. Such compliance may result in substantial expense.

In addition, a lender may be obligated to disclose environmental conditions on a site to government entities and/or to prospective buyers (including prospective buyers at a foreclosure sale or following foreclosure). Such disclosure may decrease the amount that prospective buyers are willing to pay for the affected site, sometimes substantially, and thereby decrease the ability of the lender to recoup its investment in a loan upon foreclosure.

Emerging Growth Company Status

We currently qualify as an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We plan to take advantage of these exemptions for our 2015 proxy statement.

In addition, an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended, or the Securities Act, for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for all public companies which are not emerging growth companies. Our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

We could remain an “emerging growth company” for up to five years after our IPO, or until the earliest of (i) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (ii) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of shares of our common stock that are held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three year period.

Available Information

We electronically file with the Securities and Exchange Commission our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, pursuant to Section 13(a) of the Exchange Act. You may obtain a free copy of our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments to those reports on the day of filing with the SEC on our website at www.storecapital.com, or by sending an email message to info@storecapital.com.

10

There are many factors that affect our business and the results of our operation, some of which are beyond our control. The following is a description of important factors that may cause our actual results of operations in future periods to differ materially from those currently expected or discussed in forward-looking statements set forth in this Annual Report. Forward-looking statements and such risks, uncertainties and other factors speak only as of the date of this Annual Report, and we expressly disclaim any obligation or undertaking to update or revise any forward-looking statement contained herein, to reflect any change in our expectations with regard thereto, or any other change in events, conditions or circumstances on which any such statement is based, except to the extent otherwise required by law.

Risks Related to Our Business

Our business depends on our customers successfully operating their businesses on real estate we own or finance for them, and their failure to do so could materially and adversely affect our business. Substantially all of our properties are leased by customers operating a business at those locations where sales and profits are generated for their businesses. We underwrite and evaluate investment risk based on our belief that the most important, and primary, source of payment for our leases and loans is unit‑level profitability. While a tenant may have other sources of payment to meet its obligations, we believe the success of our investments materially depends upon whether our customers successfully operate their businesses, and thus generate unit‑level profitability, at the location or locations we are acquiring or financing. Our customers may be adversely affected by many factors beyond our control that might render one or more of their locations uneconomic. These factors include poor management, changing demographics, a downturn in general economic conditions or changes in consumer trends that decrease demand for our customers’ products or services. The occurrence of any of these may cause our customers to fail to pay rent when due, fail to pay real estate taxes when due, fail to pay insurance premiums when due, become insolvent or declare bankruptcy, any of which could materially and adversely affect our business.

Our investments are and are expected to continue to be concentrated in the single‑tenant, middle‑market sector, and if the demand of single‑tenant, middle‑market companies for net‑lease financing fails to increase or decreases, or if the supply of net‑lease financing increases in this sector, we could be materially and adversely affected. Our target market is middle‑market companies that operate their businesses out of one or more locations that generate unit‑level profitability for the business. Historically, many companies prefer to own, rather than lease, the real estate they use in their businesses. A failure to increase demand for our products by, among other ways, failing to convince middle‑market companies to sell and lease back their STORE Properties, or a decrease in the demand of middle‑market companies to rent STORE Properties or an increase in the availability of STORE Properties for rent could materially and adversely affect us.

If we do not have sufficient access to debt and equity, we will be unable to continue to grow by acquiring STORE Properties. As a REIT, we are required to distribute at least 90% of our REIT taxable income, determined without regard to the dividends‑paid deduction and excluding any net capital gain, each year to our stockholders. As a result, our ability to retain earnings to fund acquisitions or make any capital expenditures, if required, will be limited. Our long‑term ability to grow through additional investments will be limited if we cannot obtain additional debt or equity financing. We cannot guarantee that debt or equity financing will be available to us in the future, or that we will be able to obtain it on favorable terms.

We depend on the asset‑backed securities market and the commercial mortgage‑backed securities market for our long‑term debt financing. We depend on, and we likely will continue to depend on, the asset‑backed securities, or ABS, and the CMBS markets for our long‑term debt financing. Substantially all of the long‑term debt on our balance sheet has been obtained from debt offerings in the ABS and CMBS markets. The ABS debt is issued by bankruptcy remote, special purpose entities that we or our subsidiaries own. These special purpose entities issue multiple series of investment‑grade ABS notes from time to time as additional collateral is added to the collateral pool. Our CMBS debt is generally in the form of first mortgage debt incurred by other special purpose entities that we or our subsidiaries own. Our ABS and CMBS debt is generally non‑recourse. However, there are customary limited exceptions to recourse for matters such as fraud, misrepresentation, gross negligence or willful misconduct, misapplication of payments, bankruptcy and environmental liabilities.

11

In the event of a disruption in the financial markets for ABS or CMBS debt, our ability to obtain long‑term debt may be materially and adversely affected. As a result, we may acquire real estate assets at a lower than anticipated growth rate, or we may be unable to acquire additional real estate assets. In addition, this disruption may affect our return on equity as a result of the decrease in the availability of long‑term debt or leverage for us. Furthermore, a reduction in the difference, or spread, between the rate we earn on our assets and the rate we pay on our liabilities (primarily our long‑term debt), which would occur if the interest rates available to us on future debt issuances increase faster than the lease rates we can charge our customers on STORE Properties we acquire and lease back to them, could have a material and adverse effect on our financial condition.

Failure to mitigate our exposure to interest rate volatility changes may materially and adversely affect us. We attempt to mitigate our exposure to interest rate risk by entering into long‑term fixed-rate financing through the combination of periodic debt offerings under STORE Master Funding, our ABS conduit, through discrete non‑recourse secured borrowings, through insurance company and bank borrowings, by laddering our borrowing maturities and by using leases that generally provide for rent escalations during the term of the lease. However, the weighted average term of our borrowings does not match the weighted average term of our investments, and the methods we employ to mitigate our exposure to changes in interest rates involve risks, including the risk that the debt markets are volatile and tend to reflect the conditions of the then‑current economic climate. Our efforts may not be effective in reducing our exposure to interest rate changes. Failure to effectively mitigate our exposure to changes in interest rates may materially and adversely affect us by increasing our cost of capital and reducing the net returns we earn on our portfolio.

A significant portion of our assets have been pledged to secure the borrowings of our subsidiaries. A significant portion of our investment portfolio consists of assets owned by our consolidated, bankruptcy remote, special purpose entity subsidiaries that have been pledged to secure the long‑term borrowings of those subsidiaries. As of December 31, 2014, the total outstanding principal balance of non‑recourse debt obligations of our consolidated special purpose entity subsidiaries was $1.3 billion, and approximately $1.9 billion in assets held by those subsidiaries had been pledged to secure those borrowings. We or our other consolidated subsidiaries are the equity owners of these special purpose entities, meaning we are entitled to the excess cash flows after debt service and all other required payments are made on the debt of these entities. If our subsidiaries fail to make the required payments on this indebtedness, distributions of excess cash flow to us may be reduced or suspended and the indebtedness may become immediately due and payable. If the subsidiaries are unable to pay the accelerated indebtedness, the pledged assets could be foreclosed upon and distributions of excess cash flow to us may be suspended or terminated. In this case, our ability to make distributions to our stockholders could be materially and adversely affected.

Loss of our key personnel could materially impair our ability to operate successfully. As an internally managed company, our ability to achieve our investment objectives and to make distributions to our stockholders depends upon the performance of our senior leadership team. We rely on our senior leadership team to, among other things, identify and consummate acquisitions, design and implement our financing strategies, manage our investments and conduct our day‑to‑day operations. In particular, our success depends upon the performance of Mr. Volk, our Chief Executive Officer, and other members of our senior leadership team.

We cannot guarantee the continued employment of any of the members of our senior leadership team, who may choose to leave our company for any number of reasons, such as other business opportunities, differing views on our strategic direction or other personal reasons. We rely on the experience, efforts and abilities of these individuals, each of whom would be difficult to replace. The employment agreements we have entered into with each of these executives do not guarantee their continued service to us. The loss of services of one or more members of our senior leadership team, or our inability to attract and retain highly qualified personnel, could adversely affect our business, diminish our investment opportunities and weaken our relationships with lenders, business partners, existing and prospective tenants and industry personnel, all of which could materially and adversely affect us.

We have a limited operating history, and our past experience may not be sufficient to allow us to successfully operate as a public company going forward. We commenced business in May 2011. We cannot assure you that our past experience will be sufficient to successfully operate our company as a publicly traded company, including the requirements to timely meet disclosure requirements of the Securities Exchange Act of 1934, as amended, and comply with the Sarbanes‑Oxley Act. We are required to develop and implement disclosure and control systems and procedures to satisfy our periodic and current reporting requirements under applicable U.S. Securities and Exchange

12

Commission, or SEC, regulations and comply with the NYSE listing standards, and this transition could place a significant strain on our management systems, infrastructure and other resources. Failure to operate successfully as a public company could materially and adversely affect us.

Our success depends in part on the creditworthiness of our customers, and we lease most of our properties to non-rated customers. Our underwriting and risk‑management procedures that we use to evaluate a potential customer’s credit risk may be faulty, deficient or otherwise fail to accurately reflect the risk of our investment. Our customers are mostly middle‑market companies, which generally are not rated by a nationally recognized rating agency. We use external and internal tools to evaluate risk and predict the risk of default. When we review a potential investment, we view our sources of payment to be, in order of priority, unit‑level profitability, tenant credit quality and residual real estate valuation. Additionally, we review a potential customer’s management team and the macroeconomic trends of the industry in which that customer operates. We evaluate the risk of company insolvency using a third‑party model, Moody’s Analytics RiskCalc, which is a model for predicting private company defaults based on Moody’s Analytics Credit Research Database and which provides us an Estimated Default Frequency, or EDF, for each of our customers. We then estimate the risk of lease or loan rejection by assigning a probability of termination based on the unit‑level fixed charge coverage ratio, or unit FCCRs, at the property or properties we own. We then estimate the long‑term default risk of an investment by multiplying the EDF score by our estimated probability that our lease will be rejected in bankruptcy, which we call the “STORE Score.”

Our methods may not adequately assess the risk of an investment. Moody’s Analytics RiskCalc, our methodology of estimating probability of lease rejection and the STORE Score may be inaccurate, incomplete or otherwise fail to adequately assess default risk. An EDF score from Moody’s Analytics RiskCalc is not the same as a published credit rating and lacks the extensive company participation that is typically involved when a rating agency publishes a rating. EDF scores and FCCRs are calculated based on financial information provided to us by our customers and prospective customers without independent verification by us. The probability of lease rejection we assign an investment based on unit FCCR or other factors may be inaccurate. Moreover, the risks we have identified as our principal risks may omit significant risks to our investments. If our underwriting procedures fail to properly assess the unit‑level profitability, tenant or corporate credit risk or real estate value of potential investments, then we may invest in properties that result in tenant defaults, and we may be unable to recover our investment by re‑leasing or selling the related property, which could materially and adversely affect our operating results and financial position.

The bankruptcy or insolvency of any of our tenants could result in the termination of such tenant’s lease and material losses to us. A tenant bankruptcy or insolvency could diminish the rental revenue we receive from that property or could force us to “take back” a property as a result of a default or a rejection of the lease by a tenant in bankruptcy. Any claims against bankrupt tenants for unpaid future rent would be subject to statutory limitations that would likely result in our receipt, if at all, of rental revenues that are substantially less than the contractually specified rent we are owed under their leases. In addition, any claim we have for unpaid past rent will likely not be paid in full. If a tenant becomes bankrupt or insolvent, federal law may prohibit us from evicting such tenant based solely upon such bankruptcy or insolvency. We may also be unable to re‑lease a terminated or rejected space or re‑lease it on comparable or more favorable terms.

Many of our tenants lease multiple properties from us under master leases. Bankruptcy laws afford certain protections to a tenant that may also affect the master lease structure. Subject to certain restrictions, a tenant under a master lease generally is required to assume or reject the master lease as a whole, rather than making the decision on a property‑by‑property basis. This prevents the tenant from assuming only the better performing properties and terminating the master lease with respect to the poorer performing properties. If these tenants are considering filing for bankruptcy protection, we may find it necessary to agree to amend their master leases to remove certain underperforming properties rather than risk the tenant rejecting the entire master lease in bankruptcy. Whether or not a bankruptcy court will require a master lease to be assumed or rejected as a whole depends upon a “facts and circumstances” analysis. A bankruptcy court will consider a number of factors, including the parties’ intent, the nature and purpose of the relevant documents, whether there was separate and distinct consideration for each property included in the master lease, the provisions contained in the relevant documents and applicable state law. If a bankruptcy court allows a master lease to be rejected in part, certain underperforming leases related to properties we own could be rejected by the tenant in bankruptcy, thereby adversely affecting payments derived from the properties. As a result, tenant bankruptcies could materially and adversely affect us.

13

Our financial monitoring, periodic site inspections and selective property sales may fail to mitigate the risk of customer defaults, and if a customer defaults, we may experience difficulty or a significant delay in re‑leasing or selling the property. Our portfolio‑management activities, including financial monitoring, periodic site inspections and selective property sales, may be insufficient to prevent or reduce the frequency of tenant defaults. If a tenant defaults, it will likely cause a significant or complete reduction in our revenue from that property for some time. If a defaulting tenant is unable to recover financially, we may have to re‑lease or sell the property. Re‑leasing or selling properties may take a significant amount of time, during which the property might have a negative cash flow to us and we may incur other related expenses. We may also have to renovate the property, reduce the rent or provide an initial rent abatement or other incentive to attract a potential tenant or buyer before we can re‑lease or sell the property. During this period, we likely will incur ongoing expenses for property maintenance, taxes, insurance and other costs. Therefore, tenant defaults could materially and adversely affect us.

As leases expire, we may be unable to renew those leases or re‑lease the space on favorable terms or at all. Our success depends in part upon our ability to cause our properties to be occupied and generating revenue. As of December 31, 2014, leases and loans representing approximately 10% of our annualized base rent and interest will expire prior to 2025. We cannot guarantee you that we will be able to renew leases or re‑lease space (i) without an interruption in the rental revenue from those properties, (ii) at or above our current rental rates, or (iii) without having to offer substantial rent abatements, tenant improvement allowances, early termination rights or below‑market renewal options. The difficulty, delay and cost of renewing leases, re‑leasing space and leasing vacant space could materially and adversely affect us.

The geographic concentration of our properties could make us vulnerable to an economic downturn, regulatory changes or acts of nature in those areas, resulting in a decrease in our revenues or other negative impacts on our results of operations. As of December 31, 2014, the five states from which we derive the largest amount of our annualized base rent and interest were Texas (13.6%), Illinois (6.9%), Georgia (6.0%), Tennessee (5.9%), and Florida (5.0%). As a result of these concentrations, the conditions of local economies and real estate markets, changes in state or local governmental rules and regulations, acts of nature and other factors in these states could result in a decrease in the demand for the products offered by the businesses operating on the properties in those states, which would have an adverse impact on our customers’ revenues, costs and results of operations, thereby adversely affecting their ability to meet their obligations to us.

As we continue to acquire properties, we may decrease or fail to increase the diversity of our portfolio. We have broad authority to invest in any STORE Property that we may identify in the future. As we continue to acquire properties, our portfolio may become less diverse by tenant, industry or geographic area. If our portfolio becomes less diverse, the trading price of our common stock may fall, as our business will be more sensitive to the bankruptcy or insolvency of fewer tenants, to changes in consumer trends of a particular industry and to a general economic downturn in a particular geographic area.

A decrease in demand for restaurant space or a downturn in the restaurant industry could materially and adversely affect us. As of December 31, 2014, real estate investments operated by customers in the restaurant industry represented approximately 28.1% of the dollar amount of our investment portfolio and 27.9% of our annualized base rent and interest, and, in the future, it is likely we will acquire additional restaurant properties. Because the restaurant industry represents a significant portion of our portfolio, a downturn in the restaurant industry may have a material adverse effect on us.

We have investments in industries that depend upon discretionary spending by consumers. A reduction in the willingness or ability of consumers to use their discretionary income in the businesses of our customers and potential customers could reduce the demand for our net‑lease solutions. Most of our portfolio is leased to or financed with customers operating service or retail businesses on our property locations. Restaurants, early childhood education centers, health clubs, movie theaters and sporting goods stores represent the largest industries in our portfolio; and Gander Mountain, Ashley Furniture HomeStore, Applebee’s, Popeyes Louisiana Kitchen and Starplex Cinemas represent the largest concepts in our portfolio. The success of most of these businesses depends on the willingness of consumers to use discretionary income to purchase their products or services. A downturn in the economy could cause consumers to reduce their discretionary spending, which may have a material adverse effect on us.

14

Some of our tenants are subject to government regulation and rely on government funding, which could adversely impact their ability to make timely lease payments to us. The industries in which some of our tenants operate are subject to government regulation, and these businesses may depend, to various extents, on government funding or reimbursements. For example, tenants in the education industry often rely extensively on local, state and federal government funding for their students’ tuition payments. In addition, tenants in the healthcare and childcare‑related industries typically receive local, state or federal funding, subsidies or reimbursements. The amount and timing of these various fundings, subsidies and reimbursements depend on various factors beyond our or our tenants’ control, including government budgets and policies and political issues. Some of these tenants also must satisfy certain licensure or certification requirements in order to qualify for government funding, subsidies or reimbursements. If these tenants fail to satisfy these requirements or otherwise fail to receive government funding, when and as needed, including as a result of tightened government budgets, revised funding policies or otherwise, their cash flow could be materially affected causing them to default on our leases, which could adversely impact our business. As we continue to grow our investment portfolio, we may continue to invest in these industries and expand our business into other industries that operate in highly regulated environments and rely significantly on payments from government payors. Changes in regulatory requirements or government funding policies affecting our tenants may result in lease defaults, which would reduce our revenues and harm our results of operations and financial position.

We may be unable to identify and complete acquisitions of suitable properties, and the competition for acquisitions may reduce the number of acquisitions we can complete, either of which may impede our growth and the continued diversification of our portfolio. Our ability to continue to acquire suitable properties may be constrained by numerous factors, including the following:

|

· |

Our ability to locate properties with attractive economic terms or lease rates. We target investments that have a difference, or spread, between our cost of capital and the lease rate of the properties we acquire. If that difference, or spread, decreases, our ability to profitably grow our company will decrease. |

|

· |

We compete with numerous investors, including publicly traded and non‑traded REITs, institutional, private equity and individual investors and other investment funds, some of whom have greater financial resources and more favorable capital costs when compared to us. |

|

· |

Since many customers we approach have an historic preference to own, rather than lease, their real estate, our ability to grow requires that we overcome those preferences and convince customers that it is in their best interests to lease, rather than own, their STORE Properties, and we may be unable to do so. |

|

· |

After beginning to negotiate the terms of a transaction and during our real property, legal and financial due‑diligence review with respect to a transaction, we may be unable to reach an agreement with the customer or discover previously unknown matters, conditions or liabilities and may be forced to abandon the opportunity after incurring significant costs and diverting management’s attention. |

|

· |

We may fail to have sufficient equity, adequate capital resources or other financing available to complete acquisitions. |

If any of these risks occur, we may be materially and adversely affected.

Insurance on our properties, which our tenants are typically required to maintain, may not adequately cover all losses, and uninsured losses could materially and adversely affect us. Our leases and loan agreements typically require that our tenants and borrowers maintain insurance of the types and in the amounts that are usual and customary for similar types of commercial property, as reviewed by our independent insurance consultant. Under certain circumstances, however, we may permit certain tenants and borrowers to self‑insure. Depending on the location of the property, losses of a catastrophic nature, such as those caused by earthquakes or floods, may be covered by insurance policies that are held by our tenants with limitations, such as large deductibles or co‑payments that a tenant may not be able to meet.

In addition, factors such as inflation, changes in building codes and ordinances, environmental considerations and others, including terrorism or acts of war, may make any insurance proceeds we receive insufficient to repair or

15

replace a property if it is damaged or destroyed. In that situation, the insurance proceeds we receive may not be adequate to restore our economic position with respect to the affected real property. In the event we experience a substantial or comprehensive loss of any of our properties, we may not be able to rebuild such property to its existing specifications without significant capital expenditures, which may exceed any amounts received pursuant to insurance policies, as reconstruction or improvement of such a property would likely require significant upgrades to meet zoning and building code requirements. The loss of our capital investment in, or anticipated future returns from, our properties due to material uninsured losses could materially and adversely affect us.

Changes in zoning laws may prevent us from restoring a property in the event of a substantial casualty loss. Due to changes, among other things, in applicable building and zoning ordinances and codes, or zoning laws, affecting certain of our properties that have come into effect after the construction of the properties, certain properties may not comply fully with current zoning laws, including use, parking and setback requirements, but may qualify as permitted non‑conforming uses. Such changes may limit our or our tenant’s ability to restore the premises of a property to its previous condition in the event of a substantial casualty loss with respect to the property or the ability to refurbish, expand or renovate such property to remain compliant. If we are unable to restore a property to its prior use after a substantial casualty loss, we may be unable to re‑lease the space at a comparable rent or sell the property at an acceptable price, which may materially and adversely affect us.

Some of our customers operate under franchise or license agreements, which, if terminated or not renewed prior to the expiration of their leases with us, would likely impair their ability to pay us rent. As of December 31, 2014, 20% of our customers operated under franchise or license agreements. Generally, franchise agreements have terms that end earlier than the respective expiration dates of the related leases. In addition, a tenant’s or borrower’s rights as a franchisee or licensee typically may be terminated and the tenant or borrower may be precluded from competing with the franchisor or licensor upon termination. Usually, we have no notice or cure rights with respect to such a termination and have no rights to assignment of any such franchise agreement. This may have an adverse effect on our ability to mitigate losses arising from a default on any of our leases or loans. A franchisor’s or licensor’s termination or refusal to renew a franchise or license agreement would likely have a material adverse effect on the ability of the tenant or borrower to make payments under its lease or loan, which could materially and adversely affect us.

A small percentage of the businesses operating on our properties have limited operating histories, which increases the risk that the tenants operating those businesses may default on rent payments to us. As of December 31, 2014, 29 of the 947 properties in our investment portfolio had been open for less than 12 months or were under construction. The businesses operating on these properties, whether newly constructed or recently opened, may not perform as anticipated, and the tenant may become unable to pay rent to us, which may materially and adversely affect us.

If a tenant defaults under either the ground lease or mortgage loan of a hybrid lease, we may be required to take judicial or administrative action or begin foreclosure proceedings before we can re‑lease or sell the property. As of December 31, 2014, 4.7% of our annualized base rent and interest was derived from hybrid leases. A hybrid lease is a modified sale‑leaseback transaction, where the customer sells us their land, leases the land back from us under a ground lease and we simultaneously make a mortgage loan to the customer secured by the improvements the customer continues to own. If a customer defaults under a hybrid lease, we may: (1) evict the customer under the ground lease and assume ownership of the improvements; or (2) if required by a court, foreclose on the mortgage loan that is secured by the improvements. Under a ground lease, we as ground lessor generally become the owner of the improvements on the land at lease maturity or if the tenant defaults. It is possible that a court could require us to foreclose on the mortgage secured by the improvements rather than simply evicting the defaulting tenant under the ground lease. If foreclosure is required rather than simple eviction, we might encounter delays and expenses in obtaining possession of the land and improvements, which in turn could delay our ability to sell or re‑lease the property in a prompt manner, which could materially and adversely affect us.

We are subject to risks related to owning commercial real estate that could reduce the value of our properties. The value of our investments in commercial real estate is subject to the following risks, among others:

|

· |

changes in local real estate conditions in the markets in which our customers operate; |

16

|

· |

environmental risks related to the presence of hazardous or toxic substances or materials on our properties; |

|

· |

the subjectivity of real estate valuations and changes in such valuations over time; |

|

· |

the illiquidity of real estate compared to other financial assets; |

|

· |

changes in interest rates and the availability of financing; and |

|

· |

changes in the general economic and business climate. |

The occurrence of any of the risks described above may cause the value of our real estate to decline, which could materially and adversely affect us.

Global market and economic conditions may materially and adversely affect us and our tenants. Our business is sensitive to changes in the overall economic conditions that impact our customers’ financial condition and financing practices. Adverse economic conditions such as high unemployment levels, interest rates, tax rates and fuel and energy costs may impact the results of our tenants’ operations, which may impact their ability to meet their obligations to us. During periods of economic slowdown, such as the global and U.S. economic downturn of 2008 and 2009, which resulted in increased unemployment, large‑scale business failures and tight credit markets, demand for real estate may decline, resulting in lower rents we can charge or an increased number of defaults under our existing leases. Accordingly, a decline in economic conditions could materially and adversely affect us.

Illiquidity of real estate investments and restrictions imposed by the Code could significantly impede our ability to respond to adverse changes in the performance of our properties and harm our financial condition. Some of the real estate investments we have made and expect to make in the future may be difficult to sell quickly. Therefore, our ability to promptly sell one or more properties in our portfolio in response to changing economic, financial or investment conditions could be limited. In particular, these risks could arise from weaknesses in or even the lack of an established market for a property, changes in the financial condition or prospects of prospective purchasers, changes in national or international economic conditions, such as the most recent economic downturn, and changes in laws, regulations or fiscal policies of the jurisdiction in which our properties are located.