Attached files

| file | filename |

|---|---|

| 8-K - Entegra Financial Corp. | e17286_enfc-8k.htm |

May 2017 Annual Shareholder Meeting

The discussions included in this document may contain “forward - looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 , including Section 21 E of the Securities Exchange Act of 1934 and Section 27 A of the Securities Act of 1933 . Such statements involve known and unknown risks, uncertainties and other factors that may cause actual results to differ materially . For the purposes of these discussions, any statements that are not statements of historical fact may be deemed to be “forward - looking statements . ” Such statements are often characterized by the use of qualifying words such as “expects,” “anticipates,” “believes,” “estimates,” “plans,” “projects,” or other statements concerning opinions or judgments of the Company and its management about future events . The accuracy of such forward looking statements could be affected by factors including, but not limited to, the financial success or changing conditions or strategies of the Company’s customers or vendors, fluctuations in interest rates, actions of government regulators, the availability of capital and personnel or general economic conditions . These forward looking statements express management’s current expectations, plans or forecasts of future events, results and condition, including financial and other estimates . Additional factors that could cause actual results to differ materially from those anticipated by forward looking statements are discussed in the Company’s filings with the Securities and Exchange Commission, including without limitation its annual report on Form 10 - K, quarterly reports on Form 10 - Q and current reports on Form 8 - K . The Company undertakes no obligation to revise or update these statements following the date of this presentation . Forward Looking Statements 2

Statements included in this document include non - GAAP financial measures and should be read along with the accompanying tables in the GAAP Appendix to our quarterly earnings release, which provide a reconciliation of non - GAAP financial measures to GAAP financial measures . This document discusses financial measures, such as core return on average equity, core return on average assets, core diluted earnings per share and core efficiency ratio, which are non - GAAP measures . We believe that such non - GAAP measures are useful because they enhance the ability of investors and management to evaluate and compare the Company’s operating results from period to period in a meaningful manner . Non - GAAP measures should not be considered as an alternative to any measure of performance as promulgated under GAAP . Investors should consider the Company’s performance and financial condition as reported under GAAP and all other relevant information when assessing the performance or financial condition of the Company . Non - GAAP measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of the Company’s results or financial condition as reported under GAAP . Non - GAAP Measurements 3

All financial numbers included in this presentation are shown in thousands ( 000 ’s) unless otherwise noted, excluding per share data and percentages . Financial Basis 4

Who We Are 5

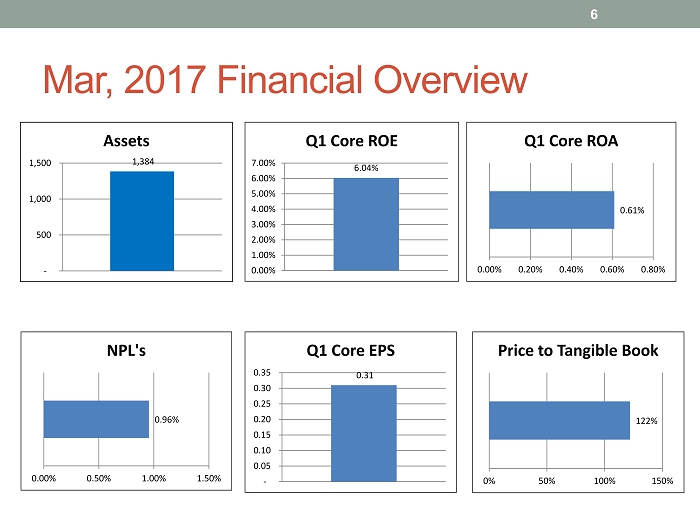

Mar, 2017 Financial Overview 6 1,384 - 500 1,000 1,500 Assets 6.04% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% Q1 Core ROE 0.61% 0.00% 0.20% 0.40% 0.60% 0.80% Q1 Core ROA 0.96% 0.00% 0.50% 1.00% 1.50% NPL's 0.31 - 0.05 0.10 0.15 0.20 0.25 0.30 0.35 Q1 Core EPS 122% 0% 50% 100% 150% Price to Tangible Book

What’s In A Name? Integrity (Noun) “the quality of being honest and having strong moral principles ; moral uprightness . ” 7

95 Years of History … And Counting 8

17 Branch Footprint 9

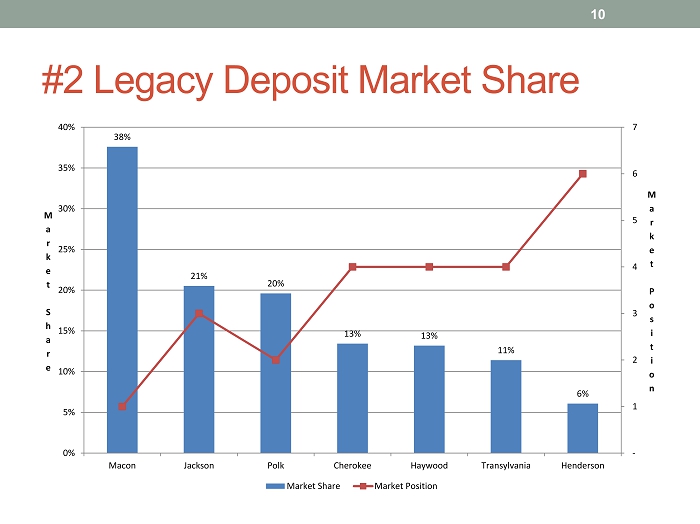

#2 Legacy Deposit Market Share 10 38% 21% 20% 13% 13% 11% 6% - 1 2 3 4 5 6 7 0% 5% 10% 15% 20% 25% 30% 35% 40% Macon Jackson Polk Cherokee Haywood Transylvania Henderson M a r k e t P o s i t i o n M a r k e t S h a r e Market Share Market Position

Major Employers 11

Charter Conversion 12

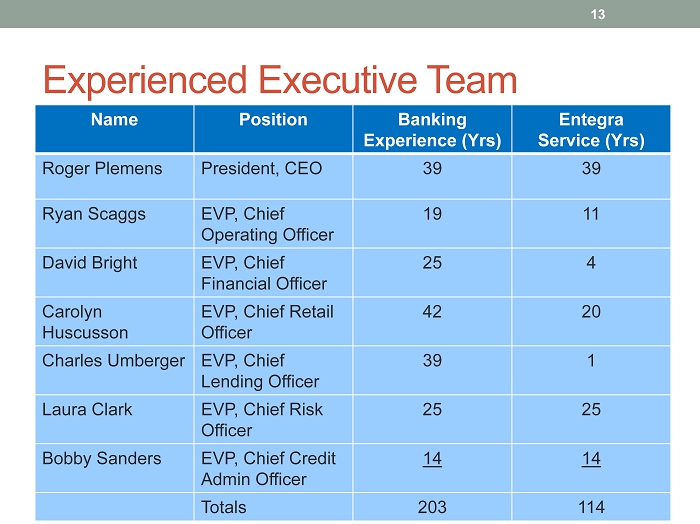

Experienced Executive Team Name Position Banking Experience ( Yrs ) Entegra Service ( Yrs ) Roger Plemens President, CEO 39 39 Ryan Scaggs EVP, Chief Operating Officer 19 11 David Bright EVP, Chief Financial Officer 25 4 Carolyn Huscusson EVP, Chief Retail Officer 42 20 Charles Umberger EVP, Chief Lending Officer 39 1 Laura Clark EVP, Chief Risk Officer 25 25 Bobby Sanders EVP, Chief Credit Admin Officer 14 14 Totals 203 114 13

Solid Stock Performance 14 $100 $120 $140 $160 $180 $200 $220 $240 $260 10/1/2014 12/31/2014 12/31/2015 12/31/2016 03/31/2017 Index Value Performance Graph Entegra Financial Corp. NASDAQ Composite Index NASDAQ Bank Index

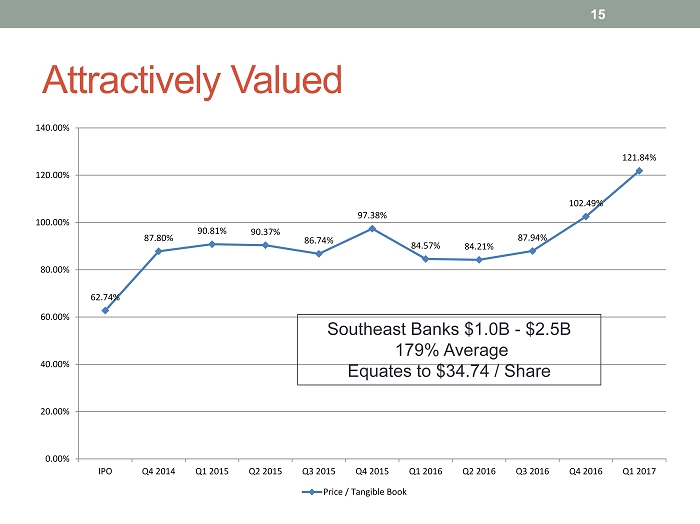

62.74% 87.80% 90.81% 90.37% 86.74% 97.38% 84.57% 84.21% 87.94% 102.49% 121.84% 0.00% 20.00% 40.00% 60.00% 80.00% 100.00% 120.00% 140.00% IPO Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Price / Tangible Book Attractively Valued Southeast Banks $1.0B - $2.5B 179% Average Equates to $34.74 / Share 15

Research Coverage 16

Strategy Summary 17

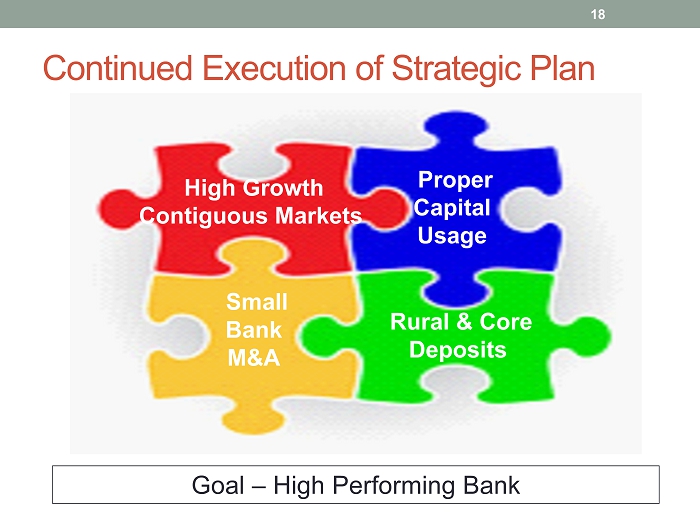

Continued Execution of Strategic Plan High Growth Contiguous Markets Small Bank M&A Rural & Core Deposits Proper Capital Usage Goal – High Performing Bank 18

Diverse Footprint 19 Rural Deposit Markets High Growth Lending Markets

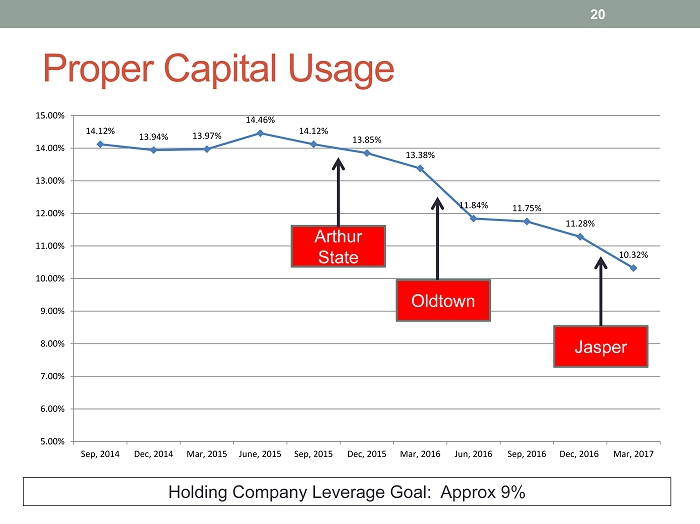

14.12% 13.94% 13.97% 14.46% 14.12% 13.85% 13.38% 11.84% 11.75% 11.28% 10.32% 5.00% 6.00% 7.00% 8.00% 9.00% 10.00% 11.00% 12.00% 13.00% 14.00% 15.00% Sep, 2014 Dec, 2014 Mar, 2015 June, 2015 Sep, 2015 Dec, 2015 Mar, 2016 Jun, 2016 Sep, 2016 Dec, 2016 Mar, 2017 Proper Capital Usage Holding Company Leverage Goal: Approx 9% Arthur State Oldtown Jasper 20

Disciplined Acquisitions December, 2015 2 Branches - $40M April, 2016 Whole Bank - $110M First Quarter, 2017 2 Branches - $150M 21 ASB ASB OLD STEA

Strategic De Novo Activity Mortgage LPO July, 2016 LPO - Jan, 2015 Branch – Oct, 2015 $50M 22

Financial Overview 23

Bank Capital Ratios Capital Levels Remain Well Above Regulatory Guidelines 24 10.09% 15.06% 15.06% 16.15% 5.00% 6.50% 8.00% 10.00% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% 16.00% 18.00% Leverage CET I RBC Tier 1 RBC Total RBC Actual Well-Capitalized

Steady Asset Growth CAGR – 18% 25 1,114,528 1,078,537 1,021,777 874,706 769,939 784,893 903,648 1,031,416 1,292,877 1,384,305 - 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017

815,959 770,448 715,313 615,540 560,717 521,874 540,479 624,072 744,361 759,150 - 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000 900,000 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017 Continued Focus on Loan Growth CAGR – 12% 26

Lower ADC Risk Profile 27 27.0% 24.7% 21.5% 18.3% 13.6% 13.0% 9.7% 9.2% 8.1% 9.1% 47.5% 47.0% 47.8% 50.0% 53.2% 55.2% 53.2% 49.7% 46.2% 45.9% 22.1% 25.4% 28.0% 29.4% 31.0% 29.6% 32.8% 34.4% 39.1% 38.7% 3.4% 2.9% 2.7% 2.2% 2.2% 2.3% 4.3% 6.8% 6.7% 6.4% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0% 120.0% 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017 ADC Res RE Comm RE C&I / Other

ADC / CRE Concentrations CRE Concentrations Remain Well Below Regulatory Guidance 28 61% 168% 100% 300% 0% 50% 100% 150% 200% 250% 300% 350% ADC Total CRE Entegra Reg Guidance

Diversified CRE Portfolio 29 5.3% 12.0% 4.3% 17.0% 3.1% 7.4% 23.6% 4.1% 3.5% 19.6% Churches Hotels Medical Office Office Recreation Restaurant Retail Storage Warehouse Other

1 - 4 Family Portfolio – Primarily 1 st Mtg 30 90.4% 9.6% First Mortgage Subordinated Mortgage

Growing Deposits w / Minimal Brokered 31 53,508 53,063 50,858 55,145 59,610 70,114 86,244 121,062 139,136 153,740 662,497 737,345 747,561 695,687 615,488 614,112 616,873 595,555 690,877 818,971 - 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000 200,000 - 200,000 400,000 600,000 800,000 1,000,000 1,200,000 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017 B r o k e r e d D e p o s i t s T o t a l D e p o s i t s Noninterest Interest Brokered Deposit

Focus on Core Deposits Core Deposits = Total Deposits Less Certificates of Deposits 29% 71% Dec, 2008 Core Non-Core 32 64% 36% Mar, 2017 Core Non-Core

Core Deposit Benefits 33 2.04% 1.55% 1.22% 0.95% 0.86% 0.72% 0.59% 0.55% 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% - 500 1,000 1,500 2,000 2,500 3,000 3,500 2010 2011 2012 2013 2014 2015 2016 Q1 2017 C o s t o f D e p o s i t s F e e I n c o m e Fee Income Cost of Deposits

Improving Earnings 34 3.91% 3.26% 3.05% 5.30% 4.71% 3.86% 5.15% 4.65% 7.26% 6.04% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Core ROE

Margin Driving Higher Earnings 35 24,463 25,872 27,421 34,488 38,472 3.42% 3.32% 3.11% 3.28% 3.30% 2.95% 3.00% 3.05% 3.10% 3.15% 3.20% 3.25% 3.30% 3.35% 3.40% 3.45% - 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 2013 2014 2015 2016 Q1 2017 N e t I n t M a r g i n ( % ) N e t I n t I n c o m e Net Int Income Margin

Disciplined Expense Control 36 79.6% 83.6% 83.1% 70.1% 72.6% 77.3% 72.4% 73.3% 68.4% 71.61% 50.0% 55.0% 60.0% 65.0% 70.0% 75.0% 80.0% 85.0% 90.0% Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Core Efficiency

Credit Losses Continue to Decline Credit Losses = Net Charge - Offs + REO Losses 37 3,400 25,937 24,629 31,282 13,005 9,237 5,610 212 529 800 - 500 1,000 1,500 2,000 2,500 - 5,000 10,000 15,000 20,000 25,000 30,000 35,000 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017 R E O E x p e n s e s C r e d i t L o s s e s Credit Losses REO Expenses

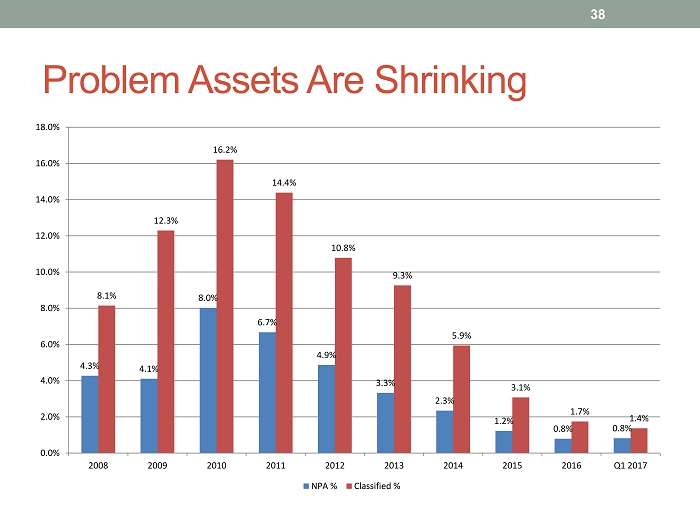

Problem Assets Are Shrinking 38 4.3% 4.1% 8.0% 6.7% 4.9% 3.3% 2.3% 1.2% 0.8% 0.8% 8.1% 12.3% 16.2% 14.4% 10.8% 9.3% 5.9% 3.1% 1.7% 1.4% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 2017 NPA % Classified %

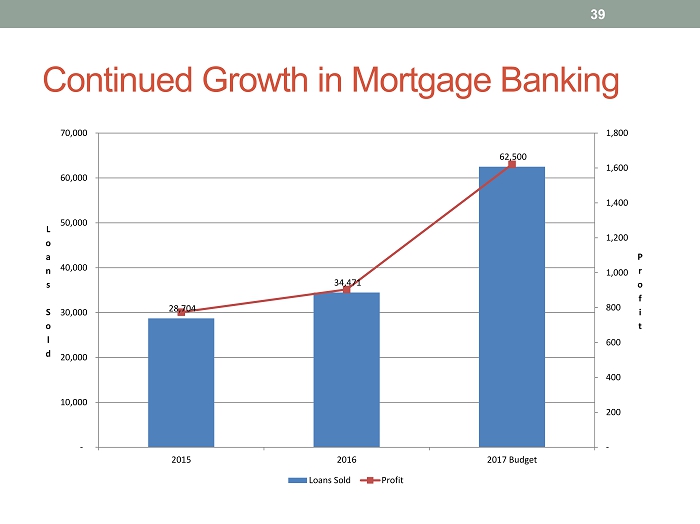

Continued Growth in Mortgage Banking 39 28,704 34,471 62,500 - 200 400 600 800 1,000 1,200 1,400 1,600 1,800 - 10,000 20,000 30,000 40,000 50,000 60,000 70,000 2015 2016 2017 Budget P r o f i t L o a n s S o l d Loans Sold Profit

Summary 40

10% ROE / 1% ROA Goal 41 Reach 9 % leverage Re - mix investment portfolio to loans F ocus on rural & core deposits Small bank M&A at attractive multiples

Summary 95 year o ld bank w/ deep relationships Experienced management team Culture of integrity Attractive entry price Disciplined M&A Growing assets and earnings 42

Summary Strong Carolinas economy Dominant legacy market share Excellent asset quality Disciplined focus on core deposits History of utilizing capital 43

GAAP Appendix 44

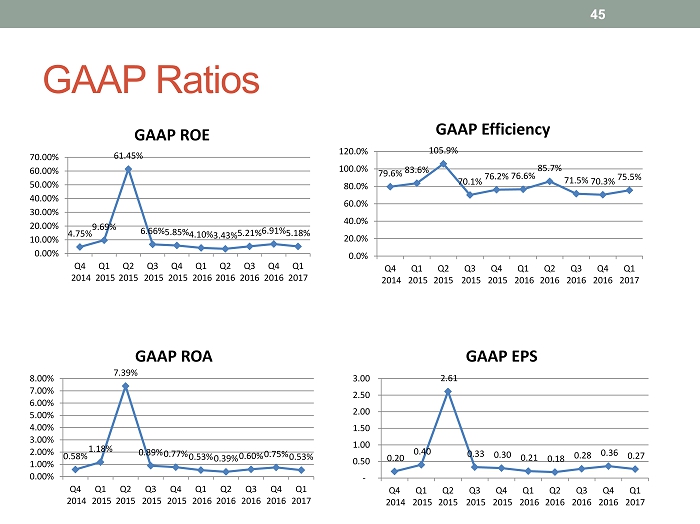

GAAP Ratios 45 4.75% 9.69% 61.45% 6.66% 5.85% 4.10% 3.43% 5.21% 6.91% 5.18% 0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00% Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 GAAP ROE 79.6% 83.6% 105.9% 70.1% 76.2% 76.6% 85.7% 71.5% 70.3% 75.5% 0.0% 20.0% 40.0% 60.0% 80.0% 100.0% 120.0% Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 GAAP Efficiency 0.58% 1.18% 7.39% 0.89% 0.77% 0.53% 0.39% 0.60% 0.75% 0.53% 0.00% 1.00% 2.00% 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 GAAP ROA 0.20 0.40 2.61 0.33 0.30 0.21 0.18 0.28 0.36 0.27 - 0.50 1.00 1.50 2.00 2.50 3.00 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 GAAP EPS