Attached files

| file | filename |

|---|---|

| EX-10.1 - EXHIBIT 10.1 AMENDMENT TO S&O AGREEMENT - Delek US Holdings, Inc. | dk-10qxex101soamendmentx03.htm |

| EX-32.2 - EXHIBIT 32.2 CFO CERTIFICATION - Delek US Holdings, Inc. | dk-ex322xcfocertificationx.htm |

| EX-32.1 - EXHIBIT 32.1 CEO CERTIFICATION - Delek US Holdings, Inc. | dk-ex321xceocertificationx.htm |

| EX-31.2 - EXHIBIT 31.2 CFO CERTIFICATION - Delek US Holdings, Inc. | dk-ex312xcfocertificationx.htm |

| EX-31.1 - EXHIBIT 31.1 CEO CERTIFICATION - Delek US Holdings, Inc. | dk-ex311xceocertificationx.htm |

| EX-10.8 - EXHIBIT 10.8 PAGE EMPLOYMENT AGREEMENT - Delek US Holdings, Inc. | dk-10qxex108pageemployment.htm |

| EX-10.7 - EXHIBIT 10.7 CAGLE EMPLOYMENT AGREEMENT - Delek US Holdings, Inc. | dk-10qxex107cagleemploymen.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the quarterly period ended March 31, 2017 | ||||

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to | ||

Commission file number 001-32868

DELEK US HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

Delaware | 52-2319066 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

7102 Commerce Way | ||

Brentwood, Tennessee | 37027 | |

(Address of principal executive offices) | (Zip Code) | |

(615) 771-6701

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o | Emerging growth company o | ||||

(Do not check if a smaller reporting company) | ||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

At May 4, 2017, there were 62,029,238 shares of common stock, $0.01 par value, outstanding (excluding securities held by, or for the account of, the Company or its subsidiaries).

TABLE OF CONTENTS

Exhibit 2.1 | |

Exhibit 2.2 | |

Exhibit 2.3 | |

Exhibit 10.1 | |

Exhibit 10.2 | |

Exhibit 10.3 | |

Exhibit 10.4 | |

Exhibit 10.5 | |

Exhibit 10.6 | |

Exhibit 10.7 | |

Exhibit 10.8 | |

Exhibit 31.1 | |

Exhibit 31.2 | |

Exhibit 32.1 | |

Exhibit 32.2 | |

EX-101 INSTANCE DOCUMENT | |

EX-101 SCHEMA DOCUMENT | |

EX-101 CALCULATION LINKBASE DOCUMENT | |

EX-101 LABELS LINKBASE DOCUMENT | |

EX-101 PRESENTATION LINKBASE DOCUMENT | |

2

Part I.

FINANCIAL INFORMATION

Item 1. | Financial Statements |

Delek US Holdings, Inc.

Condensed Consolidated Balance Sheets (Unaudited)

(In millions, except share and per share data)

March 31, 2017 | December 31, 2016 | |||||||

ASSETS | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 591.4 | $ | 689.2 | ||||

Accounts receivable | 325.8 | 265.9 | ||||||

Accounts receivable from related party | 1.5 | 0.1 | ||||||

Inventories, net of inventory valuation reserves | 397.4 | 392.4 | ||||||

Other current assets | 51.2 | 49.3 | ||||||

Total current assets | 1,367.3 | 1,396.9 | ||||||

Property, plant and equipment: | ||||||||

Property, plant and equipment | 1,602.7 | 1,587.6 | ||||||

Less: accumulated depreciation | (512.9 | ) | (484.3 | ) | ||||

Property, plant and equipment, net | 1,089.8 | 1,103.3 | ||||||

Goodwill | 12.2 | 12.2 | ||||||

Other intangibles, net | 26.3 | 26.7 | ||||||

Equity method investments | 360.0 | 360.0 | ||||||

Other non-current assets | 102.4 | 80.7 | ||||||

Total assets | $ | 2,958.0 | $ | 2,979.8 | ||||

LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

Current liabilities: | ||||||||

Accounts payable | $ | 503.6 | $ | 494.6 | ||||

Accounts payable to related party | 2.9 | 1.8 | ||||||

Current portion of long-term debt | 84.4 | 84.4 | ||||||

Obligation under Supply and Offtake Agreement | 130.2 | 124.6 | ||||||

Accrued expenses and other current liabilities | 197.8 | 229.8 | ||||||

Total current liabilities | 918.9 | 935.2 | ||||||

Non-current liabilities: | ||||||||

Long-term debt, net of current portion | 740.5 | 748.5 | ||||||

Environmental liabilities, net of current portion | 6.0 | 6.2 | ||||||

Asset retirement obligations | 5.3 | 5.2 | ||||||

Deferred tax liabilities | 75.7 | 76.2 | ||||||

Other non-current liabilities | 29.2 | 26.0 | ||||||

Total non-current liabilities | 856.7 | 862.1 | ||||||

Stockholders’ equity: | ||||||||

Preferred stock, $0.01 par value, 10,000,000 shares authorized, no shares issued and outstanding | — | — | ||||||

Common stock, $0.01 par value, 110,000,000 shares authorized, 67,224,463 shares and 67,150,352 shares issued at March 31, 2017 and December 31, 2016, respectively | 0.7 | 0.7 | ||||||

Additional paid-in capital | 653.6 | 650.5 | ||||||

Accumulated other comprehensive loss | (19.5 | ) | (20.8 | ) | ||||

Treasury stock, 5,195,791 shares, at cost, as of both March 31, 2017 and December 31, 2016 | (160.8 | ) | (160.8 | ) | ||||

Retained earnings | 523.9 | 522.3 | ||||||

Non-controlling interest in subsidiaries | 184.5 | 190.6 | ||||||

Total stockholders’ equity | 1,182.4 | 1,182.5 | ||||||

Total liabilities and stockholders’ equity | $ | 2,958.0 | $ | 2,979.8 | ||||

See accompanying notes to condensed consolidated financial statements

3

Delek US Holdings, Inc.

Condensed Consolidated Statements of Income (Unaudited)

(In millions, except share and per share data)

Three Months Ended | ||||||||

March 31, | ||||||||

2017 | 2016 | |||||||

Net sales | $ | 1,182.2 | $ | 886.1 | ||||

Operating costs and expenses: | ||||||||

Cost of goods sold | 1,035.7 | 815.8 | ||||||

Operating expenses | 61.2 | 69.0 | ||||||

Insurance proceeds — business interruption | — | (42.4 | ) | |||||

General and administrative expenses | 26.5 | 29.0 | ||||||

Depreciation and amortization | 29.0 | 28.3 | ||||||

Total operating costs and expenses | 1,152.4 | 899.7 | ||||||

Operating income (loss) | 29.8 | (13.6 | ) | |||||

Interest expense | 13.6 | 13.2 | ||||||

Interest income | (1.0 | ) | (0.3 | ) | ||||

(Income) loss from equity method investments | (3.1 | ) | 18.0 | |||||

Other expense, net | — | 0.6 | ||||||

Total non-operating expenses, net | 9.5 | 31.5 | ||||||

Income (loss) from continuing operations before income tax expense (benefit) | 20.3 | (45.1 | ) | |||||

Income tax expense (benefit) | 5.0 | (23.6 | ) | |||||

Income (loss) from continuing operations | 15.3 | (21.5 | ) | |||||

Discontinued operations: | ||||||||

Loss from discontinued operations | — | (3.9 | ) | |||||

Income tax benefit | — | (1.5 | ) | |||||

Loss from discontinued operations, net of tax | — | (2.4 | ) | |||||

Net income (loss) | 15.3 | (23.9 | ) | |||||

Net income attributed to non-controlling interest | 4.1 | 5.3 | ||||||

Net income (loss) attributable to Delek | $ | 11.2 | $ | (29.2 | ) | |||

Basic earnings (loss) per share: | ||||||||

Income (loss) from continuing operations | $ | 0.18 | $ | (0.43 | ) | |||

Loss from discontinued operations | — | (0.04 | ) | |||||

Total basic earnings (loss) per share | $ | 0.18 | $ | (0.47 | ) | |||

Diluted earnings (loss) per share: | ||||||||

Income (loss) from continuing operations | $ | 0.18 | $ | (0.43 | ) | |||

Loss from discontinued operations | — | (0.04 | ) | |||||

Total diluted earnings (loss) per share | $ | 0.18 | $ | (0.47 | ) | |||

Weighted average common shares outstanding: | ||||||||

Basic | 61,978,072 | 62,132,007 | ||||||

Diluted | 62,589,210 | 62,132,007 | ||||||

Dividends declared per common share outstanding | $ | 0.15 | $ | 0.15 | ||||

See accompanying notes to condensed consolidated financial statements

4

Delek US Holdings, Inc.

Condensed Consolidated Statements of Comprehensive Income (Unaudited)

(In millions)

Three Months Ended March 31, | |||||||||

2017 | 2016 | ||||||||

Net income (loss) attributable to Delek | $ | 11.2 | $ | (29.2 | ) | ||||

Other comprehensive income (loss): | |||||||||

Commodity contracts designated as cash flow hedges: | |||||||||

Unrealized losses, net of ineffectiveness (gains) losses of $(2.2) million and $1.0 million for the three months ended March 31, 2017 and 2016, respectively | (6.0 | ) | (6.8 | ) | |||||

Realized losses reclassified to cost of goods sold | 7.8 | 7.3 | |||||||

Gain on cash flow hedges, net | 1.8 | 0.5 | |||||||

Income tax expense | (0.6 | ) | (0.2 | ) | |||||

Net comprehensive income on commodity contracts designated as cash flow hedges | 1.2 | 0.3 | |||||||

Foreign currency translation gain (loss) | — | 0.2 | |||||||

Other comprehensive income (loss) from equity method investments, net of tax (expense) benefit of a nominal amount and $0.1 million for the three months ended March 31, 2017 and 2016, respectively | 0.1 | (0.2 | ) | ||||||

Total other comprehensive income | 1.3 | 0.3 | |||||||

Comprehensive income (loss) attributable to Delek | $ | 12.5 | $ | (28.9 | ) | ||||

See accompanying notes to condensed consolidated financial statements

5

Delek US Holdings, Inc.

Condensed Consolidated Statements of Cash Flows (Unaudited)

(In millions)

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

Cash flows from operating activities: | ||||||||

Net income (loss) | $ | 15.3 | $ | (23.9 | ) | |||

Adjustments to reconcile net income (loss) to net cash (used in) provided by operating activities: | ||||||||

Depreciation and amortization | 29.0 | 28.3 | ||||||

Amortization of deferred financing costs and debt discount | 0.9 | 1.1 | ||||||

Accretion of asset retirement obligations | 0.1 | — | ||||||

Amortization of unfavorable contract liability | (1.5 | ) | — | |||||

Deferred income taxes | (1.4 | ) | (11.6 | ) | ||||

(Income) loss from equity method investments | (3.1 | ) | 18.0 | |||||

Dividends from equity method investments | 5.1 | 5.0 | ||||||

Equity-based compensation expense | 3.8 | 4.1 | ||||||

Income tax benefit of equity-based compensation | — | 0.1 | ||||||

Loss from discontinued operations | — | 2.4 | ||||||

Changes in assets and liabilities, net of acquisitions: | ||||||||

Accounts receivable | (61.3 | ) | 19.1 | |||||

Inventories and other current assets | (10.4 | ) | 3.0 | |||||

Fair value of derivatives | 2.0 | (1.3 | ) | |||||

Accounts payable and other current liabilities | (3.1 | ) | 33.5 | |||||

Obligation under Supply and Offtake Agreement | 5.6 | (7.6 | ) | |||||

Non-current assets and liabilities, net | (23.1 | ) | (0.8 | ) | ||||

Cash (used in) provided by operating activities - continuing operations | (42.1 | ) | 69.4 | |||||

Cash provided by operating activities - discontinued operations | — | 2.5 | ||||||

Net cash (used in) provided by operating activities | (42.1 | ) | 71.9 | |||||

Cash flows from investing activities: | ||||||||

Equity method investment contributions | (1.7 | ) | (14.8 | ) | ||||

Purchases of property, plant and equipment | (19.0 | ) | (12.6 | ) | ||||

Proceeds from sales of assets | — | 0.2 | ||||||

Cash used in investing activities - continuing operations | (20.7 | ) | (27.2 | ) | ||||

Cash used in investing activities - discontinued operations | — | (7.0 | ) | |||||

Net cash used in investing activities | (20.7 | ) | (34.2 | ) | ||||

Cash flows from financing activities: | ||||||||

Proceeds from long-term revolvers | 208.6 | 86.0 | ||||||

Payments on long-term revolvers | (179.2 | ) | (79.7 | ) | ||||

Payments on term debt | (37.7 | ) | (12.7 | ) | ||||

Proceeds from product financing agreements | — | 42.5 | ||||||

Repayments of product financing agreements | (6.0 | ) | — | |||||

Taxes paid due to the net settlement of equity-based compensation | (0.7 | ) | (0.2 | ) | ||||

Income tax benefit of equity-based compensation | — | (0.1 | ) | |||||

Repurchase of common stock | — | (2.8 | ) | |||||

Repurchase of non-controlling interest | (4.0 | ) | — | |||||

Distribution to non-controlling interest | (6.4 | ) | (5.7 | ) | ||||

Dividends paid | (9.6 | ) | (9.4 | ) | ||||

Deferred financing costs paid | — | (0.2 | ) | |||||

Cash (used in) provided by financing activities - continuing operations | (35.0 | ) | 17.7 | |||||

Cash used in financing activities - discontinued operations | — | (7.7 | ) | |||||

Net cash (used in) provided by financing activities | (35.0 | ) | 10.0 | |||||

Net (decrease) increase in cash and cash equivalents | (97.8 | ) | 47.7 | |||||

Cash and cash equivalents at the beginning of the period | 689.2 | 302.2 | ||||||

Cash and cash equivalents at the end of the period | $ | 591.4 | $ | 349.9 | ||||

Less cash and cash equivalents of discontinued operations at the end of the period | — | 7.1 | ||||||

Cash and cash equivalents of continuing operations at the end of the period | $ | 591.4 | $ | 342.8 | ||||

Delek US Holdings, Inc.

Condensed Consolidated Statements of Cash Flows (Unaudited)(Continued)

(In millions)

Three Months Ended March 31, | ||||||||

2017 | 2016 | |||||||

Supplemental disclosures of cash flow information: | ||||||||

Cash paid during the period for: | ||||||||

Interest, net of capitalized interest of a nominal amount and $0.1 million in the 2017 and 2016 periods, respectively | $ | 17.9 | $ | 16.5 | ||||

Income taxes | $ | 12.9 | $ | 0.1 | ||||

Non-cash investing activities: | ||||||||

Decrease in accrued capital expenditures | $ | (3.8 | ) | $ | (10.0 | ) | ||

See accompanying notes to condensed consolidated financial statements

6

Delek US Holdings, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

1. Organization and Basis of Presentation

Delek US Holdings, Inc. is the sole shareholder or owner of membership interests of Delek Refining, Inc. ("Refining"), Delek Finance, Inc., Delek Marketing & Supply, LLC, Lion Oil Company ("Lion Oil"), Delek Renewables, LLC, Delek Rail Logistics, Inc., Delek Logistics Services Company, Delek Helena, LLC, and Delek Land Holdings, LLC. Unless otherwise indicated or the context requires otherwise, the terms "we," "our," "us," "Delek" and the "Company" are used in this report to refer to Delek US Holdings, Inc. and its consolidated subsidiaries. Delek is listed on the New York Stock Exchange under the symbol "DK."

In August 2016, we entered into a definitive equity purchase agreement (the "Purchase Agreement") with Compañía de Petróleos de Chile COPEC S.A. and its subsidiary, Copec Inc., a Delaware corporation (collectively, "COPEC"). Under the terms of the Purchase Agreement, Delek has agreed to sell, and COPEC has agreed to purchase, 100% of the equity interests in Delek's wholly-owned subsidiaries MAPCO Express, Inc., MAPCO Fleet, Inc., Delek Transportation, LLC, NTI Investments, LLC and GDK Bearpaw, LLC (collectively, the “Retail Entities”) for cash consideration of $535 million, subject to customary adjustments (the “Retail Transaction”). The Retail Transaction closed in November 2016.

As a result of the Purchase Agreement, we met the requirements under the provisions of Accounting Standards Codification ("ASC") 205-20, Presentation of Financial Statements - Discontinued Operations ("ASC 205-20") and ASC 360, Property, Plant and Equipment ("ASC 360"), to report the results of the Retail Entities as discontinued operations and to classify the Retail Entities as a group of assets held for sale. See Note 4 for further information regarding the Retail Entities.

Having classified the Retail Entities as assets held for sale, the condensed consolidated statements of income for the three months ended March 31, 2016 have been reclassified to reflect the results of the Retail Entities as income from discontinued operations, net of taxes.

Our condensed consolidated financial statements include the accounts of Delek and its consolidated subsidiaries. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with U.S. Generally Accepted Accounting Principles ("GAAP") have been condensed or omitted, although management believes that the disclosures herein are adequate to make the financial information presented not misleading. Our unaudited condensed consolidated financial statements have been prepared in conformity with GAAP applied on a consistent basis with those of the annual audited financial statements included in our Annual Report on Form 10-K filed with the Securities and Exchange Commission ("SEC") on February 28, 2017 (the "Annual Report on Form 10-K") and in accordance with the rules and regulations of the SEC. These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and the notes thereto for the year ended December 31, 2016 included in our Annual Report on Form 10-K.

Our condensed consolidated financial statements include Delek Logistics Partners, LP ("Delek Logistics"), a variable interest entity. As the general partner of Delek Logistics, we have the sole ability to direct the activities of Delek Logistics that most significantly impact its economic performance. We are also considered to be the primary beneficiary for accounting purposes and are Delek Logistics' primary customer. As Delek Logistics does not derive an amount of gross margin material to us from third parties, there is limited risk to Delek associated with Delek Logistics' operations. However, in the event that Delek Logistics incurs a loss, our operating results will reflect Delek Logistics' loss, net of intercompany eliminations, to the extent of our ownership interest in Delek Logistics.

In the opinion of management, all adjustments necessary for a fair presentation of the financial condition and the results of operations for the interim periods have been included. All significant intercompany transactions and account balances have been eliminated in consolidation. All adjustments are of a normal, recurring nature. Operating results for the interim period should not be viewed as representative of results that may be expected for any future interim period or for the full year.

Certain prior period amounts have been reclassified in order to conform to the current year presentation.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

New Accounting Pronouncements

In January 2017, the Financial Accounting Standards Board (the "FASB") issued guidance that eliminates Step 2, which required a comparison of the implied fair value of goodwill of the reporting unit with the carrying amount of that goodwill for that reporting unit, from the goodwill impairment test. It also eliminates the requirements for any reporting unit with a zero or negative carrying amount to perform a qualitative assessment and, if it fails that qualitative assessment, to perform Step 2 of the goodwill impairment test. An entity still has the option to perform the qualitative assessment for a reporting unit to determine if the quantitative impairment test is necessary. This guidance is effective for annual

7

or any interim goodwill impairment tests in fiscal years beginning after December 15, 2019. Early adoption is permitted for interim or annual goodwill impairment tests performed on testing dates after January 1, 2017. We expect to adopt this guidance on or before the effective date and are currently evaluating the impact that adopting this new guidance will have on our business, financial condition and results of operations.

In January 2017, the FASB issued guidance clarifying the definition of a business in order to assist entities with evaluating when a set of transferred assets and activities is considered a business. In general, we expect that the revised definition will result in fewer acquisitions being accounted for as business combinations than under the current guidance. This guidance is effective for fiscal years beginning after December 15, 2017, and interim periods within those fiscal years. Early adoption is permitted under certain circumstances. We expect to adopt this guidance on or before the effective date and are currently evaluating the impact that adopting this new guidance will have on our business, financial condition and results of operations.

In March 2016, the FASB issued guidance that simplifies several aspects of the accounting for share-based payment award transactions, including the accounting for excess tax benefits and deficiencies, classification of awards as either equity or liabilities and classification of excess tax benefits on the statement of cash flows. This guidance is effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years and can be early adopted for any interim or annual financial statements that have not yet been issued. We prospectively adopted this guidance on the effective date and the adoption did not have a material impact on our business, financial condition or results of operations.

In July 2015, the FASB issued guidance requiring entities to measure FIFO or average cost inventory at the lower of cost and net realizable value. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. This guidance does not change the measurement of inventory measured using LIFO or the retail inventory method. This guidance is effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. We adopted this guidance on the effective date and the adoption did not have a material impact on our business, financial condition or results of operations.

In May 2014, the FASB issued guidance regarding “Revenue from Contracts with Customers,” to clarify the principles for recognizing revenue. The core principle of the new guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The guidance also requires improved interim and annual disclosures that enable the users of financial statements to better understand the nature, amount, timing, and uncertainty of revenues and cash flows arising from contracts with customers. The new guidance is effective for annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period, and can be adopted retrospectively. Early adoption is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period. We expect to adopt this guidance on January 1, 2018. We have formed a project implementation team as well as a project time-line to evaluate this new standard. We have reviewed and gained an understanding of the new revenue recognition accounting guidance and completed our revenue stream scoping process. We have preliminarily elected to use the modified retrospective adoption method to apply this standard, under which the cumulative effect of initially applying the new guidance will be recognized as an adjustment to the opening balance of retained earnings in the first quarter of 2018. We are still evaluating the impact that adopting this standard will have on our business processes, systems and controls, and interpretative and industry specific guidance is still developing.

2. Delek Logistics

Delek Logistics is a publicly traded limited partnership that was formed by Delek to own, operate, acquire and construct crude oil and refined products logistics and marketing assets. A substantial majority of Delek Logistics' assets are integral to Delek’s refining and marketing operations. As of March 31, 2017, we owned a 61.2% limited partner interest in Delek Logistics, consisting of 15,197,571 common units, and a 94.9% interest in Logistics GP, which owns the entire 2.0% general partner interest, consisting of 496,502 general partner units, in Delek Logistics and all of the incentive distribution rights.

We have agreements with Delek Logistics that, among other things, establish fees for certain administrative and operational services provided by us and our subsidiaries to Delek Logistics, provide certain indemnification obligations and establish terms for fee-based commercial logistics and marketing services provided by Delek Logistics and its subsidiaries to us.

8

Delek Logistics is a variable interest entity as defined under GAAP and is consolidated into our condensed consolidated financial statements. With the exception of intercompany balances which are eliminated in consolidation, the Delek Logistics condensed consolidated balance sheets as of March 31, 2017 and December 31, 2016, as presented below, are included in the consolidated balance sheets of Delek (unaudited, in millions).

March 31, 2017 | December 31, 2016 | |||||||

ASSETS | ||||||||

Cash and cash equivalents | $ | — | $ | 0.1 | ||||

Accounts receivable | 23.8 | 19.2 | ||||||

Accounts receivable from related parties | — | 2.8 | ||||||

Inventory | 6.3 | 8.9 | ||||||

Other current assets | 0.8 | 1.1 | ||||||

Property, plant and equipment, net | 248.9 | 251.0 | ||||||

Equity method investments | 103.0 | 101.1 | ||||||

Goodwill | 12.2 | 12.2 | ||||||

Intangible assets, net | 14.2 | 14.4 | ||||||

Other non-current assets | 4.4 | 4.7 | ||||||

Total assets | $ | 413.6 | $ | 415.5 | ||||

LIABILITIES AND DEFICIT | ||||||||

Accounts payable | $ | 13.1 | $ | 10.9 | ||||

Accounts payable to related parties | 0.3 | — | ||||||

Accrued expenses and other current liabilities | 8.9 | 9.8 | ||||||

Revolving credit facility | 392.0 | 392.6 | ||||||

Asset retirement obligations | 3.9 | 3.8 | ||||||

Other non-current liabilities | 14.4 | 11.7 | ||||||

Deficit | (19.0 | ) | (13.3 | ) | ||||

Total liabilities and deficit | $ | 413.6 | $ | 415.5 | ||||

9

3. Equity Method Investments

On May 14, 2015, Delek acquired from Alon Israel Oil Company, Ltd. ("Alon Israel") approximately 33.7 million shares of common stock (the "ALJ Shares") of Alon USA Energy, Inc. (NYSE: ALJ) ("Alon USA") pursuant to the terms of a stock purchase agreement with Alon Israel dated April 14, 2015 (the "Alon Acquisition"). The ALJ Shares represented an equity interest in Alon USA of approximately 48% at the time of acquisition. We acquired the ALJ Shares with a combination of cash, Delek stock and seller-financed debt.

In January 2017, we announced that Delek, Alon USA, Delek Holdco, Inc., a Delaware corporation and wholly owned subsidiary of Delek (“Holdco”), Dione Mergeco, Inc., a Delaware corporation and wholly owned subsidiary of Holdco ("Parent Merger Sub"), and Astro Mergeco, Inc., a Delaware corporation and wholly owned subsidiary of Holdco (“Astro Merger Sub” and, together with Holdco and Parent Merger Sub, the “Holdco Parties”), entered into an Agreement and Plan of Merger, as subsequently amended on February 27 and April 21, 2017, to effect certain technical amendments, (the “Merger Agreement”) pursuant to which (i) Parent Merger Sub will, upon the terms and subject to the conditions thereof, merge with and into Delek (the “Parent Merger”), with Delek surviving as a wholly owned subsidiary of Holdco and (ii) Astro Merger Sub will, upon the terms and subject to the conditions thereof, merge with and into Alon USA (the “Alon Merger” and, together with the Parent Merger, the “Mergers”) with Alon USA surviving as a wholly owned subsidiary of Holdco. In the Parent Merger, each issued and outstanding share of common stock of Delek, par value $0.01 per share (“Delek common stock”), or fraction thereof, will be converted into the right to receive one validly issued, fully paid and non-assessable share of Holdco common stock, par value $0.01 per share (“Holdco common stock”) or such fraction thereof equal to the fractional share of Delek common stock, upon the terms and subject to the conditions set forth in the Merger Agreement. In the Alon Merger, each issued and outstanding share of common stock of Alon USA, par value $0.01 per share (“Alon common stock”), other than Alon common stock held by Delek or any subsidiary of Delek, will be converted into the right to receive 0.504 shares of Holdco common stock, upon the terms and subject to the conditions set forth in the Merger Agreement.

As of March 31, 2017, our investment balance in Alon USA was $257.0 million and the excess of our initial investment over our net equity in the underlying net assets of Alon USA was approximately $11.5 million. This excess is included in equity method investments in our consolidated balance sheet and a portion has been attributed to property, plant and equipment and finite-lived intangible assets. These portions of the excess are being amortized as a reduction to earnings from equity method investments on a straight-line basis over the lives of the related assets. The earnings or losses from this equity method investment reflected in our consolidated statements of income include our share of net earnings or losses directly attributable to this equity method investment, and amortization of the excess of our investment balance over the underlying net assets of Alon USA. As of March 31, 2017, the market value of our ALJ Shares was $410.7 million, based on quoted market prices. There were no indicators of impairment of our investment in Alon USA as of March 31, 2017.

Below is summarized financial information of the financial condition and results of operations of Alon USA (in millions):

Balance Sheet Information | March 31, 2017 | December 31, 2016 | ||||||

Current assets | $ | 507.3 | $ | 486.2 | ||||

Non-current assets | 1,604.9 | 1,624.0 | ||||||

Current liabilities | 504.4 | 445.5 | ||||||

Non-current liabilities | 1,026.5 | 1,082.2 | ||||||

Non-controlling interests | 62.9 | 61.3 | ||||||

Three Months Ended | ||||||||

Income Statement Information | March 31, 2017 | March 31, 2016 | ||||||

Revenue | $ | 1,150.6 | $ | 850.0 | ||||

Gross profit | 177.7 | 114.8 | ||||||

Pre-tax income (loss) | 12.8 | (57.3 | ) | |||||

Net income (loss) | 10.3 | (36.1 | ) | |||||

Net income (loss) attributable to Alon USA | 7.3 | (35.5 | ) | |||||

In March 2015, Delek Logistics entered into two joint ventures that have constructed logistics assets, which will serve third parties and subsidiaries of Delek. Delek Logistics' investment in these joint ventures is being financed through a combination of cash from operations and borrowings under the DKL Revolver (as defined in Note 7). As of March 31, 2017, Delek Logistics' investment balance in these joint ventures was $103.0 million and was accounted for using the equity method. One of the joint venture projects was completed and began operations in September 2016. The other was completed and began operations in January 2017.

10

4. Discontinued Operations and Assets Held for Sale

In August 2016, Delek entered into a Purchase Agreement to sell the Retail Entities to COPEC. As a result of the Purchase Agreement, we met the requirements of ASC 205-20 and ASC 360 to report the results of the Retail Entities as discontinued operations and to classify the Retail Entities as a group of assets held for sale. The fair value assessment of the Retail Entities as of August 27, 2016 did not result in an impairment. We ceased depreciation of these assets as of August 27, 2016. The Retail Transaction closed in November 2016 and we received cash consideration of $378.9 million, net of debt repayments and transaction costs, and retained approximately $62.8 million of net liabilities from the Retail Entities. The Retail Transaction resulted in a gain on sale of the Retail Entities, before income tax, of $134.1 million.

Under the terms of the Purchase Agreement, Lion Oil and MAPCO Express entered into a supply agreement at the closing of the Retail Transaction pursuant to which Lion Oil will supply fuel to retail locations owned by MAPCO Express for a period of 18 months following the closing of the Retail Transaction (the "Fuel Supply Agreement"). We recorded net revenues of $104.1 million and net cash inflows of $99.0 million for the three months ended March 31, 2017 associated with the Fuel Supply Agreement.

Once the Retail Entities were identified as assets held for sale, the operations associated with these properties qualified for reporting as discontinued operations. Accordingly, the operating results, net of tax, from discontinued operations are presented separately in Delek’s condensed consolidated statements of income and the notes to the condensed consolidated financial statements have been adjusted to exclude the discontinued operations. Components of amounts reflected in income from discontinued operations are as follows (in millions):

Three Months Ended | ||||

March 31, 2016 | ||||

Revenue | 219.8 | |||

Cost of goods sold | (175.2 | ) | ||

Operating expenses | (32.9 | ) | ||

General and administrative expenses | (5.7 | ) | ||

Depreciation and amortization | (7.8 | ) | ||

Other operating expense, net | (0.4 | ) | ||

Interest expense | (1.7 | ) | ||

Income from discontinued operations before taxes | (3.9 | ) | ||

Income tax expense (benefit) | (1.5 | ) | ||

Income from discontinued operations, net of tax | $ | (2.4 | ) | |

5. Inventory

Refinery inventory consists of crude oil, work-in-process, refined products and blendstocks which are stated at the lower of cost or market. Cost of inventory for the Tyler refinery is determined under the last-in, first- out ("LIFO") valuation method and costs in excess of market value are charged to cost of goods sold. Cost of inventory for the El Dorado refinery is determined on a first-in, first-out ("FIFO") basis and costs in excess of net realizable value are charged to cost of goods sold.

Logistics inventory consists of refined products which are stated at the lower of FIFO cost or net realizable value.

Carrying value of inventories consisted of the following (in millions):

March 31, 2017 | December 31, 2016 | |||||||

Refinery raw materials and supplies | $ | 185.7 | $ | 145.6 | ||||

Refinery work in process | 35.4 | 37.6 | ||||||

Refinery finished goods | 170.0 | 200.3 | ||||||

Logistics refined products | 6.3 | 8.9 | ||||||

Total inventories | $ | 397.4 | $ | 392.4 | ||||

Due to a lower crude oil and refined product pricing environment experienced since the end of 2014, market prices have declined to a level below the average cost of our inventories. At March 31, 2017, we recorded a pre-tax inventory valuation reserve of $18.9 million, $18.7 million of which related to LIFO inventory, which is subject to reversal in subsequent periods, not to exceed LIFO cost, should market prices recover. At December 31, 2016, we recorded a pre-tax inventory valuation reserve of $16.0 million, all of which related to LIFO inventory, which reversed

11

in the first quarter of 2017, as the inventories associated with the valuation adjustment at the end of 2016 were sold or used. For the three months ended March 31, 2017 and 2016, we recognized net inventory valuation (losses) gains of $(2.9) million and $3.6 million, respectively, which were recorded as a component of cost of goods sold in the consolidated statements of income.

At March 31, 2017 and December 31, 2016, the excess of replacement cost (FIFO) over the carrying value (LIFO) of the Tyler refinery inventories was $1.1 million and $3.5 million, respectively.

Permanent Liquidations

We incurred a permanent reduction in a LIFO layer resulting in liquidation losses in our refinery inventory of a nominal amount and $3.3 million during the three months ended March 31, 2017 and 2016, respectively. These liquidation losses were recognized as a component of cost of goods sold.

6. Crude Oil Supply and Inventory Purchase Agreement

Delek has a Master Supply and Offtake Agreement (the "Supply and Offtake Agreement") with J. Aron & Company ("J. Aron"). Throughout the term of the Supply and Offtake Agreement, which was amended on February 27, 2017 to change, among other things, certain terms related to pricing and an extension of the maturity date to April 30, 2020, Lion Oil and J. Aron will identify mutually acceptable contracts for the purchase of crude oil from third parties and J. Aron will supply up to 100,000 barrels per day ("bpd") of crude oil to the El Dorado refinery. Crude oil supplied to the El Dorado refinery by J. Aron will be purchased daily at an estimated average monthly market price by Lion Oil. J. Aron will also purchase all refined products from the El Dorado refinery at an estimated daily market price, as they are produced. These daily purchases and sales are trued-up on a monthly basis in order to reflect actual average monthly prices. We have recorded a receivable related to this monthly settlement of $1.0 million and $6.9 million as of March 31, 2017 and December 31, 2016, respectively. Also pursuant to the Supply and Offtake Agreement and other related agreements, Lion Oil will endeavor to arrange potential sales by either Lion Oil or J. Aron to third parties of the products produced at the El Dorado refinery or purchased from third parties. In instances where Lion Oil is the seller to such third parties, J. Aron will first transfer title to the applicable products to Lion Oil.

This arrangement is accounted for as a product financing arrangement. Delek incurred fees payable to J. Aron of $2.5 million during each of the three months ended March 31, 2017 and 2016. These amounts are included as a component of interest expense in the condensed consolidated statements of income. Upon any termination of the Supply and Offtake Agreement, including in connection with a force majeure event, the parties are required to negotiate with third parties for the assignment to us of certain contracts, commitments and arrangements, including procurement contracts, commitments for the sale of product, and pipeline, terminalling, storage and shipping arrangements.

Upon the expiration of the Supply and Offtake Agreement on April 30, 2020, or upon any earlier termination, Delek will be required to repurchase the consigned crude oil and refined products from J. Aron at then prevailing market prices. At March 31, 2017, Delek had 2.5 million barrels of inventory consigned from J. Aron, and we have recorded liabilities associated with this consigned inventory of $130.2 million in the condensed consolidated balance sheet.

7. Long-Term Obligations and Notes Payable

Outstanding borrowings under Delek’s existing debt instruments are as follows (in millions):

March 31, 2017 | December 31, 2016 | |||||||

DKL Revolver | $ | 392.0 | $ | 392.6 | ||||

Wells Term Loan(1) | 57.7 | 63.6 | ||||||

Wells Revolving Loan | 30.0 | — | ||||||

Reliant Bank Revolver | 17.0 | 17.0 | ||||||

Promissory Notes | 105.0 | 130.0 | ||||||

Lion Term Loan Facility(2) | 223.2 | 229.7 | ||||||

824.9 | 832.9 | |||||||

Less: Current portion of long-term debt and notes payable | 84.4 | 84.4 | ||||||

$ | 740.5 | $ | 748.5 | |||||

12

(1) | The Wells Term Loan is net of deferred financing costs of $0.1 million as of both March 31, 2017 and December 31, 2016 and debt discount of $0.5 million as of both March 31, 2017 and December 31, 2016. |

(2) | The Lion Term Loan Facility is net of deferred financing costs of $2.7 million and $3.0 million, respectively, and debt discounts of $1.0 million and $1.1 million, respectively, at March 31, 2017 and December 31, 2016. |

DKL Revolver

Delek Logistics has a $700.0 million senior secured revolving credit agreement with Fifth Third Bank, as administrative agent, and a syndicate of lenders (the "DKL Revolver"). Delek Logistics and each of its existing subsidiaries are borrowers under the DKL Revolver. The DKL Revolver contains a dual currency borrowing tranche that permits draw downs in U.S. or Canadian dollars and an accordion feature whereby Delek Logistics can increase the size of the credit facility to an aggregate of $800.0 million, subject to receiving increased or new commitments from lenders and the satisfaction of certain other conditions precedent.

The obligations under the DKL Revolver are secured by a first priority lien on substantially all of Delek Logistics' tangible and intangible assets. Additionally, a subsidiary of Delek provides a limited guaranty of Delek Logistics' obligations under the DKL Revolver. The guaranty is (i) limited to an amount equal to the principal amount, plus unpaid and accrued interest, of a promissory note made by Delek in favor of the subsidiary guarantor (the "Holdings Note") and (ii) secured by the subsidiary guarantor's pledge of the Holdings Note to the DKL Revolver lenders. As of March 31, 2017, the principal amount of the Holdings Note was $102.0 million.

The DKL Revolver will mature on December 30, 2019. Borrowings under the DKL Revolver bear interest at either a U.S. base rate, Canadian prime rate, LIBOR, or a Canadian Dealer Offered Rate, in each case plus applicable margins, at the election of the borrowers and as a function of draw down currency. The applicable margin, in each case, varies based upon Delek Logistics' leverage ratio, which is defined as the ratio of total funded debt to EBITDA for the most recently ended four fiscal quarters. At March 31, 2017, the weighted average borrowing rate was approximately 3.6%. Additionally, the DKL Revolver requires Delek Logistics to pay a leverage ratio dependent quarterly fee on the average unused revolving commitment. As of March 31, 2017, this fee was 0.50% per year. As of March 31, 2017, Delek Logistics had $392.0 million of outstanding borrowings under the credit facility, as well as letters of credit issued of $7.5 million. Unused credit commitments under the DKL Revolver, as of March 31, 2017, were $300.5 million.

Wells ABL

Our subsidiary, Delek Refining, Ltd., has an asset-based loan credit facility with Wells Fargo Bank, National Association, as administrative agent, and a syndicate of lenders, which was amended and restated on September 29, 2016 (the "Wells ABL"). The Wells ABL consists of (i) a $450.0 million revolving loan (the "Wells Revolving Loan"), which includes a $45.0 million swing line loan sub-limit and a $200.0 million letter of credit sub-limit, (ii) a $70.0 million term loan (the "Wells Term Loan"), and (iii) an accordion feature which permits an increase in the size of the revolving credit facility to an aggregate of $725.0 million, subject to additional lender commitments and the satisfaction of certain other conditions precedent. The Wells Revolving Loan matures on September 29, 2021 and the Wells Term Loan matures on September 29, 2019. The Wells Term Loan is subject to repayment in level principal installments of approximately $5.8 million per quarter, with the final installment due on September 29, 2019. As of March 31, 2017, under the Wells ABL, we had letters of credit issued totaling approximately $92.4 million, $30.0 million in borrowings outstanding under the Wells Revolving Loan and $58.3 million outstanding under the Wells Term Loan. The obligations under the Wells ABL are secured by (i) substantially all the assets of Refining and its subsidiaries, with certain limitations, (ii) guaranties provided by the general partner of Delek Refining, Ltd., as well as by the parent of Delek Refining, Ltd., Delek Refining, Inc. (iii) a limited guarantee provided by Delek in an amount up to $15.0 million and (iv) a limited guarantee provided by Lion Oil in an amount equal to the sum of the face amount of all letters of credit issued on behalf of Lion Oil under the Wells ABL and any loans made by Refining or its subsidiaries to Lion Oil. Under the facility, revolving loans and letters of credit are provided subject to availability requirements which are determined pursuant to a borrowing base calculation as defined in the credit agreement. The borrowing base as calculated is primarily supported by cash, certain accounts receivable and certain inventory. Borrowings under the Wells Revolving Loan and Wells Term Loan bear interest based on separate predetermined pricing grids which allow us to choose between base rate loans or LIBOR rate loans. At March 31, 2017, the weighted average borrowing rate was approximately 4.7% under the Wells Term Loan and 4.5% under the Wells Revolving Loan. Additionally, the Wells ABL requires us to pay a quarterly unused credit commitment fee. As of March 31, 2017, this fee was approximately 0.38% per year. Unused borrowing base availability, as calculated and reported under the terms of the Wells ABL credit facility, as of March 31, 2017, was approximately $155.8 million.

Reliant Bank Revolver

We have a revolving credit agreement with Reliant Bank, which was amended on May 26, 2016 (the "Reliant Bank Revolver"). The Reliant Bank Revolver provides for unsecured loans of up to $17.0 million. As of March 31, 2017, we had $17.0 million outstanding under this facility. The Reliant Bank Revolver matures on June 28, 2018, and bears interest at a fixed rate of 5.25% per annum. The Reliant Bank Revolver requires us to pay a quarterly fee of 0.50% per year on the average available revolving commitment. As of March 31, 2017, we had no unused credit commitments under the Reliant Bank Revolver.

13

Promissory Notes

On April 29, 2011, Delek entered into a $50.0 million promissory note (the "Ergon Note") with Ergon, Inc. ("Ergon") in connection with the closing of our acquisition of Lion Oil. As of March 31, 2017, $10.0 million was outstanding under the Ergon Note. The Ergon Note requires Delek to make annual amortization payments of $10.0 million each, commencing April 29, 2013. The Ergon Note matures on April 29, 2017. Interest under the Ergon Note is computed at a fixed rate equal to 4.0% per annum.

On May 14, 2015, in connection with the closing of the Company’s acquisition of the ALJ Shares, the Company issued the Alon Israel Note in the amount of $145.0 million, which was payable to Alon Israel. The Alon Israel Note bears interest at a fixed rate of 5.5% per annum and requires five annual principal amortization payments of $25.0 million beginning in January 2016 followed by a final principal amortization payment of $20.0 million at maturity on January 4, 2021. In October 2015, we prepaid the first annual principal amortization payment in the amount of $25.0 million, along with all interest due on the prepaid amount. On December 22, 2015, Alon Israel assigned the remaining $120.0 million of principal and all accrued interest due under the Alon Israel Note to assignees under four new notes in substantially the same form and on the same terms as the Alon Israel Note (collectively, the "Alon Successor Notes"). The $120.0 million in total principal of the four Alon Successor Notes collectively require the same principal amortization payments and schedule as under the Alon Israel Note, with payments due under each Alon Successor Note commensurate to such note's pro rata share of $120.0 million in assigned principal. As of March 31, 2017, a total principal amount of $95.0 million was outstanding under the Alon Successor Notes.

Lion Term Loan

Our subsidiary, Lion Oil, has a term loan credit facility with Fifth Third Bank, as administrative agent, and a syndicate of lenders, which was amended and restated on May 14, 2015 in connection with the Company’s closing of the Alon Acquisition to, among other things, increase the total loan size from $99.0 million to $275.0 million (the "Lion Term Loan"). The Lion Term Loan requires Lion Oil to make quarterly principal amortization payments of approximately $6.9 million each, commencing on September 30, 2015, with a final balloon payment due at maturity on May 14, 2020. The Lion Term Loan is secured by, among other things, (i) substantially all the assets of Lion Oil and its subsidiaries (excluding inventory and accounts receivable), (ii) all shares in Lion Oil, (iii) any subordinated and common units of Delek Logistics held by Lion Oil, and (iv) the ALJ Shares. Additionally, the Lion Term Loan is guaranteed by Delek and the subsidiaries of Lion Oil. Interest on the unpaid balance of the Lion Term Loan is computed at a rate per annum equal to LIBOR or a base rate, at our election, plus the applicable margins, subject in each case to an all-in interest rate floor of 5.50% per annum. As of March 31, 2017, approximately $226.9 million was outstanding under the Lion Term Loan and the weighted average borrowing rate was 5.65%.

Restrictive Covenants

Under the terms of our Wells ABL, DKL Revolver, Reliant Bank Revolver and Lion Term Loan, we are required to comply with certain usual and customary financial and non-financial covenants. Further, although we were not required to comply with separate fixed charge coverage ratio financial covenants under the Wells ABL and the Lion Term Loan during the three months ended March 31, 2017, we may be required to comply with these covenants at times when certain trigger thresholds are met, as defined in each of the Wells ABL and Lion Term Loan agreements. We believe we were in compliance with all covenant requirements under each of our credit facilities as of March 31, 2017.

Certain of our credit facilities contain limitations on the incurrence of additional indebtedness, making of investments, creation of liens, dispositions of property, making of restricted payments and transactions with affiliates. Specifically, these covenants may limit the payment, in the form of cash or other assets, of dividends or other distributions, or the repurchase of shares with respect to the equity of our subsidiaries. Additionally, certain of our credit facilities limit our ability to make investments, including extensions of loans or advances to, or acquisitions of equity interests in, or guarantees of obligations of, any other entities.

8. Other Assets and Liabilities

The detail of other current assets is as follows (in millions):

Other Current Assets | March 31, 2017 | December 31, 2016 | |||||

Prepaid expenses | $ | 14.2 | $ | 14.0 | |||

Short-term derivative assets (see Note 15) | 3.4 | 6.8 | |||||

Income and other tax receivables | 14.5 | 19.2 | |||||

RINs Obligation surplus (see Note 14) | 15.0 | 4.9 | |||||

Other | 4.1 | 4.4 | |||||

Total | $ | 51.2 | $ | 49.3 | |||

14

The detail of other non-current assets is as follows (in millions):

Other Non-Current Assets | March 31, 2017 | December 31, 2016 | |||||

Prepaid tax asset | $ | 58.7 | $ | 59.5 | |||

Deferred financing costs | 7.5 | 8.2 | |||||

Long-term income tax receivables | 10.2 | 7.5 | |||||

Supply and Offtake receivable | 20.2 | — | |||||

Long-term derivative assets (see Note 15) | 0.1 | — | |||||

Other | 5.7 | 5.5 | |||||

Total | $ | 102.4 | $ | 80.7 | |||

The detail of accrued expenses and other current liabilities is as follows (in millions):

Accrued Expenses and Other Current Liabilities | March 31, 2017 | December 31, 2016 | |||||

Income and other taxes payable | $ | 103.9 | $ | 115.7 | |||

Short-term derivative liabilities (see Note 15) | 17.1 | 26.1 | |||||

Interest payable | 4.4 | 9.6 | |||||

Employee costs | 5.8 | 7.3 | |||||

Environmental liabilities (see Note 16) | 1.0 | 1.0 | |||||

Product financing agreements | — | 6.0 | |||||

RINs Obligation deficit (see Note 14) | — | 25.6 | |||||

Other | 65.6 | 38.5 | |||||

Total | $ | 197.8 | $ | 229.8 | |||

The detail of other non-current liabilities is as follows (in millions):

Other Non-Current Liabilities | March 31, 2017 | December 31, 2016 | |||||

Long-term derivative liabilities (see Note 15) | $ | 23.0 | $ | 17.3 | |||

Other | 6.2 | 8.7 | |||||

Total | $ | 29.2 | $ | 26.0 | |||

9. Stockholders' Equity

Changes to equity during the three months ended March 31, 2017 are presented below (in millions, except per share amounts):

Delek Stockholders' Equity | Non-Controlling Interest in Subsidiaries | Total Stockholders' Equity | ||||||||||

Balance at December 31, 2016 | $ | 991.9 | $ | 190.6 | $ | 1,182.5 | ||||||

Net income | 11.2 | 4.1 | 15.3 | |||||||||

Net unrealized gain on cash flow hedges, net of income tax expense of $0.6 million and ineffectiveness gain of $2.2 million | 1.2 | — | 1.2 | |||||||||

Other comprehensive income from equity method investments, net of income tax expense of a nominal amount | 0.1 | — | 0.1 | |||||||||

Common stock dividends ($0.15 per share) | (9.6 | ) | — | (9.6 | ) | |||||||

Distribution to non-controlling interest | — | (6.4 | ) | (6.4 | ) | |||||||

Repurchase of non-controlling interest | — | (4.0 | ) | (4.0 | ) | |||||||

Equity-based compensation expense | 3.6 | 0.2 | 3.8 | |||||||||

Taxes due to the net settlement of equity-based compensation | (0.7 | ) | — | (0.7 | ) | |||||||

Other | 0.2 | — | 0.2 | |||||||||

Balance at March 31, 2017 | $ | 997.9 | $ | 184.5 | $ | 1,182.4 | ||||||

Dividends

During the three months ended March 31, 2017, our Board of Directors declared the following dividends:

Date Declared | Dividend Amount Per Share | Record Date | Payment Date | |||

February 27, 2017 | $0.15 | March 15, 2017 | March 29, 2017 | |||

Stock Repurchase Program

In December 2016, our Board of Directors authorized a share repurchase program for up to $150.0 million of Delek common stock. Any share repurchases under the repurchase program may be implemented through open market transactions or in privately negotiated transactions, in accordance with applicable securities laws. The timing, price, and size of repurchases will be made at the discretion of management and will depend on prevailing market prices, general economic and market conditions and other considerations. The repurchase program does not obligate us to acquire any particular amount of stock and does not expire. There were no shares repurchased during the three months ended March 31, 2017.

10. Income Taxes

Under ASC 740, Income Taxes (“ASC 740”), companies are required to apply an estimated annual tax rate to interim period results on a year-to-date basis; however, the estimated annual tax rate should not be applied to interim financial results if a reliable estimate cannot be made. In this situation, the interim tax rate should be based on actual year-to-date results. Based on our current projections, which have fluctuated as a result of changes in crude oil prices and the related crack spreads, we believe that using actual year-to-date results to compute our effective tax rate will produce a more reliable estimate of our tax expense or benefit. As such, we recorded a tax provision for the three months ended March 31, 2017 and 2016 based on actual year-to-date results, in accordance with ASC 740.

Our effective tax rate was 24.6% for the three months ended March 31, 2017, compared to 52.3% for the three months ended March 31, 2016. The decrease in our effective tax rate in the three months ended March 31, 2017 was primarily due to the expiration of provisions for certain tax credits and incentives that expired as of December 31, 2016 and have not been extended by Congress, as well as the impact of pre-tax income in the three months ended March 31, 2017, compared to a pre-tax loss in the three months ended March 31, 2016.

15

11. Equity-Based Compensation

Delek US Holdings, Inc. 2006 and 2016 Long-Term Incentive Plans

Compensation expense for Delek equity-based awards amounted to $3.3 million ($2.1 million, net of taxes) and $3.6 million ($2.3 million, net of taxes) for the three months ended March 31, 2017 and 2016, respectively. These amounts, excluding amounts related to discontinued operations of $0.4 million for the three months ended March 31, 2016, are included in general and administrative expenses in the accompanying condensed consolidated statements of income.

As of March 31, 2017, there was $25.1 million of total unrecognized compensation cost related to non-vested share-based compensation arrangements, which is expected to be recognized over a weighted-average period of 1.8 years.

We issued 74,111 and 40,466 shares of common stock as a result of exercised stock options, stock appreciation rights, and vested restricted stock units during the three months ended March 31, 2017 and 2016, respectively. These amounts do not include shares withheld to satisfy employee tax obligations related to the exercises and vestings. Such withheld shares totaled 61,845 and 12,183 shares during the three months ended March 31, 2017 and 2016, respectively.

Delek Logistics GP, LLC 2012 Long-Term Incentive Plan

Compensation expense for Delek Logistics GP equity-based awards was $0.4 million ($0.3 million, net of taxes) for both the three months ended March 31, 2017 and 2016. These amounts are included in general and administrative expenses in the accompanying condensed consolidated statements of income.

As of March 31, 2017, there was $1.2 million of total unrecognized compensation cost related to non-vested share-based compensation arrangements, which is expected to be recognized over a weighted-average period of 1.6 years.

12. Earnings (Loss) Per Share

Basic and diluted earnings per share are computed by dividing net income (loss) by the weighted average common shares outstanding. The common shares used to compute Delek’s basic and diluted earnings (loss) per share are as follows:

Three Months Ended | ||||||

March 31, | ||||||

2017 | 2016 | |||||

Weighted average common shares outstanding | 61,978,072 | 62,132,007 | ||||

Dilutive effect of equity instruments | 611,138 | — | ||||

Weighted average common shares outstanding, assuming dilution | 62,589,210 | 62,132,007 | ||||

Outstanding common share equivalents totaling 1,934,173 and 2,981,508 were excluded from the diluted earnings per share calculation for the three months ended March 31, 2017 and 2016, respectively, as these common share equivalents did not have a dilutive effect under the treasury stock method. These amounts include outstanding common share equivalents totaling 208,933 that were excluded from the diluted earnings per share calculation due to the net loss for the three months ended March 31, 2016.

13. Segment Data

Prior to August 2016, we aggregated our operating units into three reportable segments: refining, logistics and retail. However, in August 2016, Delek entered into a Purchase Agreement to sell the Retail Entities, which consist of all of the retail segment and a portion of the corporate, other and eliminations segment, to COPEC. As a result of the Purchase Agreement, we met the requirements of ASC 205-20, Presentation of Financial Statements - Discontinued Operations and ASC 360, Property, Plant and Equipment, to report the results of the Retail Entities as discontinued operations and to classify the Retail Entities as a group of assets held for sale. The operating results for the Retail Entities, in all periods presented, have been reclassified to discontinued operations and are no longer reported as retail segment.

Our corporate activities, results of certain immaterial operating segments, our equity method investment in Alon USA and intercompany eliminations are reported in the corporate, other and eliminations segment. Decisions concerning the allocation of resources and assessment of operating performance are made based on this segmentation. Management measures the operating performance of each of the reportable segments based on the segment contribution margin.

Segment contribution margin is defined as net sales less cost of sales and operating expenses, excluding depreciation and amortization. Operations which are not specifically included in the reportable segments are included in the corporate and other category, which primarily consists of operating expenses, depreciation and amortization expense and interest income and expense associated with our corporate headquarters.

The refining segment processes crude oil and other purchased feedstocks for the manufacture of transportation motor fuels, including various grades of gasoline, diesel fuel, aviation fuel, asphalt and other petroleum-based products that are distributed through owned and third-party product terminals. The refining segment has a combined nameplate capacity of 155,000 bpd, including the 75,000 bpd Tyler refinery and the 80,000 bpd El Dorado refinery. The refining segment also owns and operates two biodiesel facilities involved in the production of biodiesel fuels and related activities.

Our refining segment has a services agreement with our logistics segment, which, among other things, requires the refining segment to pay service fees based on the number of gallons sold at the Tyler refinery and a sharing of a portion of the margin achieved in return for providing marketing, sales and customer services. This intercompany transaction fee was $4.3 million and $3.9 million during the three months ended March 31, 2017 and 2016, respectively. Additionally, the refining segment pays crude transportation, terminalling and storage fees to the logistics segment for the utilization of pipeline, terminal and storage assets. These fees were $31.2 million and $31.0 million during the three months ended March 31, 2017 and 2016, respectively. The logistics segment also sold $1.1 million and $1.5 million of Renewable Identification Numbers ("RINs") to the refining segment during the three months ended March 31, 2017 and 2016, respectively. The refining segment recorded sales and fee revenues from the logistics segment of $9.0 million during the three months ended March 31, 2017, and recorded sales and fee revenues from the logistics segment and the Retail Entities, the operations of which are included in discontinued operations, in the amount of $91.4 million during the three months ended March 31, 2016. All inter-segment transactions have been eliminated in consolidation.

Our logistics segment owns and operates crude oil and refined products logistics and marketing assets. The logistics segment generates revenue and contribution margin by charging fees for gathering, transporting and storing crude oil and for marketing, distributing, transporting and storing intermediate and refined products.

16

The following is a summary of business segment operating performance as measured by contribution margin for the period indicated (in millions):

Three Months Ended March 31, 2017 | ||||||||||||||||

(In millions) | Refining | Logistics | Corporate, Other and Eliminations | Consolidated | ||||||||||||

Net sales (excluding intercompany fees and sales) | $ | 1,090.5 | $ | 92.9 | $ | (1.2 | ) | $ | 1,182.2 | |||||||

Intercompany fees and sales | 9.0 | 36.6 | (45.6 | ) | — | |||||||||||

Operating costs and expenses: | ||||||||||||||||

Cost of goods sold | 984.3 | 92.6 | (41.2 | ) | 1,035.7 | |||||||||||

Operating expenses | 50.8 | 10.3 | 0.1 | 61.2 | ||||||||||||

Segment contribution margin | $ | 64.4 | $ | 26.6 | $ | (5.7 | ) | 85.3 | ||||||||

General and administrative expenses | 26.5 | |||||||||||||||

Depreciation and amortization | 29.0 | |||||||||||||||

Operating income | $ | 29.8 | ||||||||||||||

Total assets | $ | 1,994.1 | $ | 413.6 | $ | 550.3 | $ | 2,958.0 | ||||||||

Capital spending (excluding business combinations) | $ | 10.8 | $ | 2.8 | $ | 1.6 | $ | 15.2 | ||||||||

Three Months Ended March 31, 2016 | ||||||||||||||||

Refining | Logistics | Corporate, Other and Eliminations(4) | Consolidated | |||||||||||||

Net sales (excluding intercompany fees and sales) | $ | 735.9 | $ | 67.7 | $ | 0.5 | $ | 804.1 | ||||||||

Intercompany fees and sales(1) | 91.4 | 36.4 | (45.8 | ) | 82.0 | |||||||||||

Operating costs and expenses: | ||||||||||||||||

Cost of goods sold | 787.9 | 66.8 | (38.9 | ) | 815.8 | |||||||||||

Operating expenses | 58.3 | 10.5 | 0.2 | 69.0 | ||||||||||||

Insurance proceeds - business interruption | (42.4 | ) | — | — | (42.4 | ) | ||||||||||

Segment contribution margin | $ | 23.5 | $ | 26.8 | $ | (6.6 | ) | 43.7 | ||||||||

General and administrative expenses | 29.0 | |||||||||||||||

Depreciation and amortization | 28.3 | |||||||||||||||

Operating loss | $ | (13.6 | ) | |||||||||||||

Total assets(2) | $ | 1,937.9 | $ | 379.2 | $ | 979.7 | $ | 3,296.8 | ||||||||

Capital spending (excluding business combinations)(3) | $ | 3.3 | $ | 1.1 | $ | 2.1 | $ | 6.5 | ||||||||

(1) | Intercompany fees and sales for the refining segment include revenues from the Retail Entities of $82.0 million during the three months ended March 31, 2016, the operations of which are reported in discontinued operations. |

(2) | Assets held for sale of $463.8 million are included in the corporate, other and eliminations segment as of March 31, 2016. |

(3) | Capital spending excludes capital spending associated with the Retail Entities of $3.4 million during the three months ended March 31, 2016. |

(4) | The corporate, other and eliminations segment operating results for the three months ended March 31, 2016 have been restated to reflect the reclassification of the Retail Entities to discontinued operations. |

17

Property, plant and equipment and accumulated depreciation as of March 31, 2017 and depreciation expense by reporting segment for the three months ended March 31, 2017 are as follows (in millions):

Refining | Logistics | Corporate, Other and Eliminations | Consolidated | |||||||||||||

Property, plant and equipment | $ | 1,213.6 | $ | 345.2 | $ | 43.9 | $ | 1,602.7 | ||||||||

Less: Accumulated depreciation | (391.8 | ) | (96.3 | ) | (24.8 | ) | (512.9 | ) | ||||||||

Property, plant and equipment, net | $ | 821.8 | $ | 248.9 | $ | 19.1 | $ | 1,089.8 | ||||||||

Depreciation expense | $ | 21.8 | $ | 4.9 | $ | 1.9 | $ | 28.6 | ||||||||

In accordance with ASC 360, Delek evaluates the realizability of property, plant and equipment as events occur that might indicate potential impairment. There were no indicators of impairment of our property, plant and equipment as of March 31, 2017.

14. Fair Value Measurements

The fair values of financial instruments are estimated based upon current market conditions and quoted market prices for the same or similar instruments. Management estimates that the carrying value approximates fair value for all of Delek’s assets and liabilities that fall under the scope of ASC 825, Financial Instruments ("ASC 825").

Delek applies the provisions of ASC 820, Fair Value Measurements ("ASC 820"), which defines fair value, establishes a framework for its measurement and expands disclosures about fair value measurements. ASC 820 applies to our commodity derivatives that are measured at fair value on a recurring basis. The standard also requires that we assess the impact of nonperformance risk on our derivatives. Nonperformance risk is not considered material to our financial statements at this time.

ASC 820 requires disclosures that categorize assets and liabilities measured at fair value into one of three different levels depending on the observability of the inputs employed in the measurement. Level 1 inputs are quoted prices in active markets for identical assets or liabilities. Level 2 inputs are observable inputs other than quoted prices included within Level 1 for the asset or liability, either directly or indirectly through market-corroborated inputs. Level 3 inputs are unobservable inputs for the asset or liability reflecting our assumptions about pricing by market participants.

Over the counter ("OTC") commodity swaps, physical commodity purchase and sale contracts and interest rate swaps and caps are generally valued using industry-standard models that consider various assumptions, including quoted forward prices, spot prices, interest rates, time value, volatility factors and contractual prices for the underlying instruments, as well as other relevant economic measures. The degree to which these inputs are observable in the forward markets determines the classification as Level 2 or 3. Our contracts are valued based on exchange pricing and/or price index developers such as Platts or Argus and are, therefore, classified as Level 2.

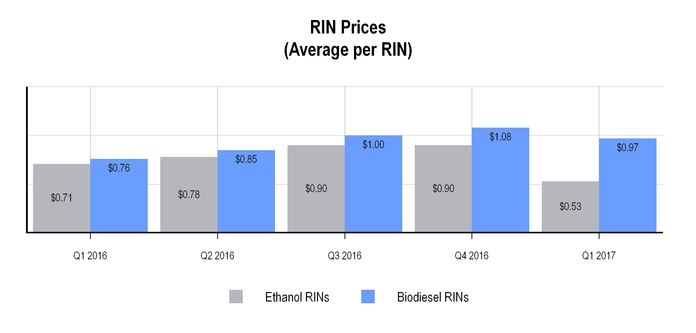

The U.S. Environmental Protection Agency ("EPA") requires certain refiners to blend biofuels into the fuel products they produce pursuant to the EPA’s Renewable Fuel Standard - 2. Alternatively, credits called RINs, which may be generated and/or purchased, can be used to satisfy this obligation instead of physically blending biofuels ("RINs Obligation"). Our RINs Obligation surplus or deficit is based on the amount of RINs we must purchase, net of amounts internally generated and purchased and the price of those RINs as of the balance sheet date. The RINs Obligation surplus or deficit is categorized as Level 2 and is measured at fair value based on quoted prices from an independent pricing service.

On March 1, 2017, the El Dorado refinery received approval from the EPA for a small refinery exemption from the requirements of the renewable fuel standard for the 2016 calendar year. This waiver resulted in a reduction of our RINs Obligation and related cost of goods sold of approximately $47.5 million for the three months ended March 31, 2017.

From time to time, Delek enters into future commitments to purchase or sell RINs at fixed prices and quantities, which are used to manage the costs associated with our RINs Obligation. These future RIN commitment contracts meet the definition of derivative instruments under ASC 815, Derivatives and Hedging ("ASC 815"). They are categorized as Level 2, and are measured at fair value based on quoted prices from an independent pricing service. Changes in the fair value of these future RIN commitment contracts are recorded in cost of goods sold on the consolidated statements of income.

We have elected to account for our J. Aron step-out liability at fair value in accordance with ASC 825, as it pertains to the fair value option. This standard permits the election to carry financial instruments and certain other items similar to financial instruments at fair value on the balance sheet, with all changes in fair value reported in earnings. Our J. Aron step-out liability is categorized as Level 2, and is measured at fair value using market prices for the consigned crude oil and refined products we are required to repurchase from J. Aron at the end of the term of the Supply and Offtake Agreement.

18

The fair value hierarchy for our financial assets and liabilities accounted for at fair value on a recurring basis at March 31, 2017 and December 31, 2016, was as follows (in millions):

As of March 31, 2017 | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Assets | ||||||||||||||||

OTC commodity swaps | $ | — | $ | 28.5 | $ | — | $ | 28.5 | ||||||||

RINs Obligation surplus | — | 15.0 | — | 15.0 | ||||||||||||

Total assets | — | 43.5 | — | 43.5 | ||||||||||||

Liabilities | ||||||||||||||||

OTC commodity swaps | — | (70.6 | ) | — | (70.6 | ) | ||||||||||

RIN commitment contracts | — | (3.4 | ) | — | (3.4 | ) | ||||||||||

J. Aron step-out liability | — | (130.2 | ) | — | (130.2 | ) | ||||||||||

Total liabilities | — | (204.2 | ) | — | (204.2 | ) | ||||||||||

Net liabilities | $ | — | $ | (160.7 | ) | $ | — | $ | (160.7 | ) | ||||||

As of December 31, 2016 | ||||||||||||||||

Level 1 | Level 2 | Level 3 | Total | |||||||||||||

Assets | ||||||||||||||||

OTC commodity swaps | $ | — | $ | 53.1 | $ | — | $ | 53.1 | ||||||||

RINs Obligation surplus | — | 4.9 | — | 4.9 | ||||||||||||

Total assets | — | 58.0 | — | 58.0 | ||||||||||||

Liabilities | ||||||||||||||||

OTC commodity swaps | — | (103.6 | ) | — | (103.6 | ) | ||||||||||

RIN commitment contracts | — | (0.8 | ) | — | (0.8 | ) | ||||||||||

RINs Obligation deficit | — | (25.6 | ) | — | (25.6 | ) | ||||||||||

J. Aron step-out liability | — | (144.8 | ) | — | (144.8 | ) | ||||||||||

Total liabilities | — | (274.8 | ) | — | (274.8 | ) | ||||||||||

Net liabilities | $ | — | $ | (216.8 | ) | $ | — | $ | (216.8 | ) | ||||||

The derivative values above are based on analysis of each contract as the fundamental unit of account as required by ASC 820. Derivative assets and liabilities with the same counterparty are not netted where the legal right of offset exists. This differs from the presentation in the financial statements which reflects our policy under the guidance of ASC 815-10-45, wherein we have elected to offset the fair value amounts recognized for multiple derivative instruments executed with the same counterparty and where the legal right of offset exists. As of March 31, 2017 and December 31, 2016, $8.9 million and $14.7 million, respectively, of cash collateral was held by counterparty brokerage firms and has been netted with the net derivative positions with each counterparty.

15. Derivative Instruments

We use derivatives to reduce normal operating and market risks with the primary objective of reducing the impact of market price volatility on our results of operations. As such, our use of derivative contracts is aimed at:

• | limiting the exposure to price fluctuations of commodity inventory above or below target levels at each of our segments; |

• | managing our exposure to commodity price risk associated with the purchase or sale of crude oil, feedstocks and finished grade fuel products at each of our segments; and |

• | limiting the exposure to interest rate fluctuations on our floating rate borrowings. |

We primarily utilize OTC commodity swaps, generally with maturity dates of three years or less, and interest rate swap and cap agreements to achieve these objectives. OTC commodity swap contracts require cash settlement for the commodity based on the difference between a

19

fixed or floating price and the market price on the settlement date. As of March 31, 2017, there are no interest rate swap or cap agreements outstanding. At this time, we do not believe there is any material credit risk with respect to the counterparties to these contracts.

From time to time, we also enter into future commitments to purchase or sell RINs at fixed prices and quantities, which are used to manage the costs associated with our RINs Obligation. These future RIN commitment contracts meet the definition of derivative instruments under ASC 815, and are recorded at estimated fair value in accordance with the provisions of ASC 815. Changes in the fair value of these future RIN commitment contracts are recorded in cost of goods sold on the consolidated statements of income.

In accordance with ASC 815, certain of our OTC commodity swap contracts have been designated as cash flow hedges and the effective portion of the change in fair value between the execution date and the end of period has been recorded in other comprehensive income. The effective portion of the fair value of these contracts is recognized in income at the time the positions are closed and the hedged transactions are recognized in income.

From time to time, we also enter into futures contracts with supply vendors that secure supply of product to be purchased for use in the normal course of business at our refining segment. These contracts are priced based on an index that is clearly and closely related to the product being purchased, contain no net settlement provisions and typically qualify under the normal purchase exemption from derivative accounting treatment under ASC 815.