Attached files

| file | filename |

|---|---|

| EX-32 - CERTIFICATION UNDER USC 1350 - COMMUNICATIONS SYSTEMS INC | csi170730_ex32.htm |

| EX-31.2 - CERTIFICATION OF CFO - COMMUNICATIONS SYSTEMS INC | csi170730_ex31-2.htm |

| EX-31.1 - CERTIFICATION OF CEO - COMMUNICATIONS SYSTEMS INC | csi170730_ex31-1.htm |

| EX-23 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - COMMUNICATIONS SYSTEMS INC | csi170730_ex23.htm |

| EX-21 - SUBSIDIARIES OF COMMUNICATIONS SYSTEMS, INC. - COMMUNICATIONS SYSTEMS INC | csi170730_ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

Commission File Number: 001-31588

COMMUNICATIONS SYSTEMS, INC.

(Exact name of registrant as specified in its charter)

| Minnesota | 41-0957999 | |

| (State or other jurisdiction | (Federal Employer | |

| of incorporation or organization) | Identification No.) |

10900 Red Circle Drive, Minnetonka, MN 55343

(Address of principal executive offices and zip code)

Registrant’s telephone number, including area code: (952) 996-1674

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $.05 par value | NASDAQ | |

| Preferred Stock Purchase Rights |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐ NO ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company.

See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☐ | Non-Accelerated Filer ☐ | Smaller Reporting Company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant was approximately $48,934,000 based upon the closing sale price of the Company’s common stock on the NASDAQ on June 30, 2016.

As of March 1, 2017 there were outstanding 8,883,535 shares of the Registrant’s common stock.

| Documents Incorporated by Reference: | Portions of the Company’s Proxy Statement for its Annual Meeting of Shareholders to be held on May 24, 2017 are incorporated by reference into Part III of this Form10-K. |

PART I

| ITEM 1. | BUSINESS |

(a) GENERAL DEVELOPMENT OF BUSINESS

Communications Systems, Inc. (herein collectively referred to as “CSI,” “our,” “we” or the “Company”) is a Minnesota corporation organized in 1969 that operates directly and through its subsidiaries located in the United States (U.S.), Costa Rica, and the United Kingdom (U.K.). CSI is principally engaged through its Suttle, Inc. (“Suttle”) subsidiary and business unit in the manufacture and sale of connectivity infrastructure products for broadband and voice communications, and through its Transition Networks, Inc. (“Transition Networks” or “Transition”) subsidiary and business unit in the manufacture and sale of core media conversion products, Ethernet switches, and other connectivity and data transmission products. Through its JDL Technologies, Inc. (“JDL Technologies” or “JDL”) business unit, CSI provides technology solutions including virtualization, managed services, wired and wireless network design and implementation, HIPAA-compliant IT services, and converged infrastructure configuration and deployment. Through its Net2Edge Limited (“Net2Edge”) UK-based business unit, the Company develops, manufactures and sells products that enable telecommunications carriers to connect legacy networks to high-speed services.

The Company maintains a website at www.commsystems.com. Our annual reports on Form 10-K, our quarterly reports on Form 10-Q and our periodic reports on Form 8-K (and any amendments to these reports) are available free of charge by linking from our website to the Securities and Exchange Commission website.

(b) FINANCIAL INFORMATION ABOUT INDUSTRY SEGMENTS

The Company classifies its businesses into four segments:

| ● | Suttle, which manufactures connectivity infrastructure products for broadband and voice communications; |

| ● | Transition Networks, which designs and markets media conversion products, Ethernet switches, and other connectivity and data transmission products; |

| ● | JDL Technologies, which is an IT managed services provider and value-added reseller; and |

| ● | Net2Edge, which develops, manufactures and sells products to connect legacy networks to high-speed services. |

Non-allocated general and administrative expenses are separately accounted for as “Other” in the Company’s segment reporting. Intersegment revenues are eliminated upon consolidation. Further information regarding these segments, including customer and industry concentration, is set forth in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in Note 12 of the Notes to Consolidated Financial Statements under Item 8.

(c) NARRATIVE DESCRIPTION OF BUSINESS

(1) Information Regarding Business Segments

(i) Suttle, Inc.

Suttle, based in Minnetonka, Minnesota, manufactures and markets a broad range of products that support broadband and telephone service under the Suttle brand name in the United States and internationally. Products are deployed from the last mile of the carrier network into the premise/enterprise to meet the unique needs of hybrid/fiber/copper networks. The Company’s customer-oriented approach provides right-sized solutions that leverage existing infrastructure and protect investments as markets and technologies grow and change. With over 100 years of knowledge and experience, Suttle is a reliable partner, delivering innovative, flexible, easy-to-use solutions, lower cost of ownership, and solid customer support. The Company manufactures 71% of its products at its plants in Hector, Minnesota (Suttle, Inc.) and San Jose, Costa Rica (Suttle Costa Rica, S.A.). The other 29% are purchased from offshore contract manufacturers. Segment sales were $42,076,000 in 2016 and $50,082,000 in 2015. On January 24, 2017, the Company announced it was closing its Suttle Costa Rica production facility and consolidating production into its Minnesota facilities.

2

Products

Suttle’s products include Structured Cabling Products (enclosure systems to support premise distribution of broadband and other connectivity networks); FTTx Products (fiber optic management and connectivity solutions for access and premise networks); Modular Connecting Products (connecting products for copper telecommunications networks) and DSL Products (products that support broadband connectivity to copper networks).

Products for the Edge of the Network:

Suttle’s solutions for the last mile of the carrier’s network, i.e. the “Edge,” are designed to operate in challenging environments yet be easily accessible, extend the life of the existing network, enhance data speeds, and prevent loss of bandwidth at the point of use.

Suttle products are designed to work indoor and outdoor and feature flexibility and scalability in real world applications for both copper and fiber networks. Suttle’s FutureLinkTM solutions offer a range of products including terminals, patch-and-splice and splitter enclosures.

Products for the Connected Home/Business:

Suttle provides service distribution products for cost-effective solutions using existing and new structured wiring. These products reduce installation time and labor costs, and increase the provider’s return on investment. In addition to reducing a service provider’s up-front costs, Suttle’s high throughput solutions help eliminate potential bottlenecks to “future-proof” the installation, reducing future costs.

The MediaMAXTM brand provides for reliable brownfield and greenfield premise connectivity to meet the increasing demand for wired and wireless high-speed service throughout the home and business. Designed to optimize installation cost while maximizing coverage and bandwidth at the point of use for multiple deployment topologies, this brand includes a premise connectivity and distribution system, featuring plastic modular enclosures and tool-less, snap-in modules to minimize wireless interference. MediaMAXTM brand product replaces Suttle’s SOHOTM brand products, which have been Suttle’s primary premise distribution products for approximately the last 10 years.

Another key feature of MediaMAX is installation cost and time saving tool-less technology available in jacks and modules. Rounding out the inside the premise/enterprise offering are faceplates and wall plates that accommodate hybrid/fiber, copper and coax connections for higher speed, tool-less connectivity and lower cost of ownership.

Markets and Marketing

Suttle markets its outside plant and premise distribution products globally to telecommunications companies, service providers, residential builders, and low-voltage installers through distributors and the Company’ sales staff. Suttle has a solid history of offering long-term solutions to some of the largest global providers by understanding customers’ needs and providing innovative solutions coupled with strong customer support. Suttle reaches its targeted customers through a variety of marketing media including trade shows, associations, advertising, social media, and the Suttle website.

Suttle recently changed its domain name for electronic communications to SuttleSolutions.com to emphasize our focus on end-to-end customer oriented solutions for communication service providers.

Customers

Suttle’s customers include telephone, CATV, internet service providers and enterprise networks. The Company’s major telephone company customers include AT&T, CenturyLink and Verizon. Suttle serves these major telephone companies directly by Suttle’s sales staff and through a select group of distributors. Sales (including DSL) to the major telephone companies, as a group, both directly and through distribution, represented 90% of Suttle’s sales in 2016 and 79% in 2015.

Other customers include smaller telephone companies, electrical/low-voltage contractors, home builders, and a nationwide network of distributors. Suttle serves these customers primarily through distributors, but also directly through its sales staff. Sales to cable customers and original equipment manufacturers (OEMs) are made through Suttle’ nationwide network of distributors and through the Suttle sales staff. Sales to OEMs and other distributors were 6% of Suttle’s sales in 2016 and 6% in 2015. Sales to international customers and other customers represented 4% of Suttle’s sales in 2016 and 15% in 2015.

3

Competition

Suttle encounters strong competition in all its product lines and competes primarily on the basis of the broad lines of products offered, product performance, quality, price, delivery, and customer support. In addition, distributors of Suttle’s products also market products for one or more of its competitors.

Order Book

Suttle manufactures its products both on a make-to-order basis and on the basis of customer forecasts. Outstanding customer orders at March 1, 2017 were approximately $3,604,000 compared to approximately $3,828,000 at March 1, 2016. New orders are generally filled within 60 days. Suttle does not believe its order book is a significant indicator of longer term future results.

Manufacturing and Sources of Supply

Suttle manufactures its products using plastic or metal parts, wire sub-assemblies, fasteners, brackets, electronic circuit boards, and other components, most of which are fabricated by Suttle. There are multiple sources of supply for the materials and components and the Company is not dependent upon any single supplier, except that Suttle’s corrosion-resistant products use a moisture-resistant gel-filled fig available only from Tyco Electronics Connectivity. Although Suttle has not generally experienced significant problems in obtaining its required supplies, from time to time it experiences spot shortages and longer order lead times are required from its offshore suppliers.

New Product Development; Patents and Intellectual Property

Suttle continually seeks to understand the needs of its customers and both develops new products for evolving customer requirements and enhances existing products to improve its existing product line. For competitive reasons, including duplication of its designs by foreign apparatus manufacturers, Suttle has adopted a policy to seek patent protection on innovative new products. Suttle applied for five patents in 2015, five patents in 2016 and expects to file two patent applications in 2017.

Research and development consists primarily of designing, prototyping, and testing of equipment and supplies associated with developing new products and enhancing existing products. Research and development costs are expensed when incurred and were $2,596,000 in 2016 compared to $4,959,000 in 2015.

Suttle and Suttle Solutions are important trademarks for its business. Suttle regularly supports these brand names by trade advertising and believes they are well known in the marketplace. Other important trademarks include FutureLinkTM brand for the last mile and MDU solutions; MediaMAXTM panels, modules, jacks and wall plates; SpeedStarTM for passive premise connectivity; and CorroShield® brand gel that prevents network corrosion.

(ii) Transition Networks, Inc.

Transition Networks, Inc., based in Minnetonka, Minnesota, designs, assembles and markets media converters, NIDs, network interface cards (NICs), Ethernet switches, Small Form Factor Pluggable modules (SFP), and other connectivity products under the Transition Networks brand names. Transition sells its products through distributors, resellers, integrators, and OEMs. These media converters, NIDs, and Ethernet Switch products allow network operators to transmit voice and data across networks and between copper-wired and fiber-optic equipment. Sales by Transition Networks were $41,093,000 in 2016 compared to $41,469,000 in 2015. International sales accounted for 20% of Transition’s sales, or $8,406,000 in 2016, compared to $10,617,000, or 26% of Transition’s sales in 2015.

Products

Transition Networks designs, assembles and sells media converter devices, NIDs, Ethernet switches and other connectivity products that make it possible to transmit telecommunications signals across networks and between systems using different types of media (for example, between copper and fiber optic networks). These products assist in resolving challenges in the areas of bandwidth constraints, security risks, and distance limitations as networks extend from local area to wide area networks and adapt to ever increasing end-user demands. As enterprise networks are seemingly always in transition, our solutions enable customers to integrate fiber optics into their existing infrastructure as their networks grow, and extend advanced data services to customers at remote locations, including support of wireless networks and its backhaul requirements. Many of our products incorporate features for performing advanced levels of fault management and other benefits to aid in troubleshooting fiber optic and copper network infrastructure. Our growing Power-over-Ethernet (PoE) products provide support of remote devices such as cameras and wireless access points by passing electrical power along with data on Ethernet cabling, eliminating the need for local power in hard to reach locations.

4

Transition Networks products support a wide variety of protocols, including: 10 Gigabit Ethernet, Gigabit Ethernet, Fast Ethernet, Ethernet, T1/E1, DS3, Circuit Emulation Services (TDM or ISDN over Ethernet or IP), RS232, RS485, OC3, OC12, among others. Transition Networks develops product hardware and software internally, and expenses the related costs as they are incurred. In connection with the sale of its hardware products, Transition Networks provides its customers with a variety of software management options including Element Management System (EMS) software for providing superior service provisioning and monitoring of next-generation Carrier Ethernet 2.0 Services. The Company has been developing and marketing Ethernet-based networking products for approximately 30 years. Transition Networks continues to develop products that address the enterprise, service provider, industrial, government, and security markets.

Manufacturing and Sources of Supply

Transition Networks uses contract manufacturers to manufacture its products in different geographical locations. In 2016, 62% of the total value of its products was manufactured in Asia while the remaining 38% was manufactured in the US. Offshore sources of supply are subject to certain risks, including political risk. The Company has alternate sources of supply for its products in different geographical locations and to date has not had problems obtaining necessary product.

Markets and Marketing

Transition Networks’ products are used in a broad array of markets including the federal government, enterprise, service provider, industrial, and surveillance markets. Transition Networks has a broad customer base and its products are used in a variety of applications.

The media conversion product line is used in several applications. The ION and Point System™ chassis-based modular systems are used primarily in telecommunications closets for high-density applications and when multiple protocols need to be supported. Stand-alone media converters are used typically at a workstation or for lower density applications. The line of Ethernet switches is used in last mile access, backhaul, central closet and at the end-user stations. The Carrier Ethernet NID line of products addresses the high quality access requirements for both business services and wireless backhaul data communications and telecommunications applications.

Marketing primarily consists of direct marketing using a sales force, tradeshows, trade magazine advertising, on-line advertising, website, email, social media and public relations activities. Transition Networks also provides and participates in advertising and cooperative marketing campaigns with distribution partners.

The Company’s “Transition Networks” brand name is important to its business and regularly supports this name with trade advertising and believes it to be well known in the marketplace.

Research and Development

Transition Networks develops products for the federal government, enterprise, service provider, security and industrial markets. This includes developing converters for emerging protocols and existing protocols in new markets, as well as new industry standards. Some of these products include remote management devices built on the IEEE® 802.3AH, 802.3AG, ITU-T Y.1731 standards, Metro Ethernet Forum (MEF)® and MEF 2.0 standards, and Power Over Ethernet devices based on the IEEE® 802.3AF and IEEE® 802.3AT standards. Some design efforts are paced by the development of critical components such as integrated circuits and optical transceivers.

Research and development consists primarily of designing, prototyping, and testing of equipment and supplies associated with developing new products and enhancing existing products. Research and development costs are expensed when incurred and were $2,770,000 in 2016 compared to $2,798,000 in 2015.

5

Transition Networks’ conducts its research and development operations in the United States, at its Minnetonka, Minnesota headquarters location. While this US location has primary engineering and product development responsibility, it will occasionally use third party design services and Original Design Manufacturers (“ODM”) to support specific product design requirements.

Competition

Transition Networks faces strong competition across its entire product line. A large number of competitors exist for high volume products in the Fast Ethernet and Gigabit Ethernet families, as well as the NIDs. Low-cost competitors from China and Taiwan are strongest in (i) Asian, (ii) European, Middle Eastern, and African (“EMEA”) and (iii) South American markets, with limited success in the North American market for the media converter products. Transition Networks also faces new competitors as it enters new markets for industrial products, security market, and higher performance devices for the service provider market.

Order Book

Outstanding customer orders for Transition Networks products were approximately $1,656,000 at March 1, 2017 and $4,485,000 at March 1, 2016. Transition Networks orders are fulfilled on a relatively short-term basis and therefore the Company does not consider the order book as a significant indicator of longer term future results.

(iii) JDL Technologies, Inc.

JDL Technologies, Inc., based in Fort Lauderdale, Florida, is a managed service provider and value-added reseller supplying information technology (“IT”) solutions focused on IT service and support management; network design, deployment and integration; cloud, hosted and virtualized services; and network operations center management. JDL’s 2016 sales were $15,464,000 compared to 2015 sales of $15,672,000. Project revenue totaled $11,854,000 in 2016 or 77% of JDL sales compared to $12,176,000 in 2015 or 78% of JDL sales. Managed service revenues grew to $3,610,000 in 2016 from $3,496,000 in 2015.

Competitive Strategy

The Florida technology market includes a number of managed service providers (“MSPs”) and value-added resellers (“VARs”), and is a microcosm of the burgeoning managed services industry in the U.S. JDL continues to differentiate itself in strategic ways and in early response to market shifts, and is well qualified to help clients optimize their technologies and IT resources in order to meet business objectives and regulatory requirements.

JDL partners with clients to provide complete support for their information technology environments, from servers to applications, to the network, down to the desktop level. Under a typical managed services agreement, JDL maintains corporate IT, resolves issues, supports the client’s user community, and adds new value to the client’s business. JDL’s key avenues for delivering on this commitment—and its competitive advantages—include JDL’s on-premise managed services operations center and secure, state-of-the-art hosted datacenter. The managed services operations center leverages the best available tools, applications, practices and resources to deliver a consistent, quality customer experience. JDL Technologies was named to the 2016 Elite 150 Managed Service Providers in North America, part of The Channel Company’s 2016 MSP 500 list. JDL also holds the MSP Trustmark credential from CompTIA and is a member of the MSP Alliance. JDL’s president and general manager presented a paper at the 2016 MSPWorld Conference hosted by the MSP Alliance.

JDL’s portfolio of technology solutions reflects the regular introduction of new technologies and delivery methodologies and the increasing demand among businesses for innovative solutions to strengthen their competitive edge and address prevailing IT challenges. With its team of professionally certified engineers, more than 475 years of technical experience, and talented leadership, JDL Technologies develops best-of-breed IT solutions that effectively meet these demands. As an example, in 2016 the company’s flagship service for healthcare, HIPAA FastTrack, earned an Information Security award for Innovation in Compliance. To sustain its leading-edge position, JDL also maintains robust partnerships with strategic manufacturers and is a 3CX VoIP Gold Partner, HP Enterprise Gold Partner, Microsoft Gold Partner, eMDs Solution Provider and Citrix Solutions Service Provider.

6

Targeted Vertical Markets

In 2016, JDL Technologies aggressively targeted its primary vertical markets, healthcare and commercial business, through its JDL HealthTechTM and JDL TechWatchTM brands.

Healthcare:

Under the JDL HealthTech brand, JDL continues to penetrate the $1.3 billion healthcare market in Florida, offering an array of services that address HIPAA Security Rule and Privacy Rule compliance requirements, including its flagship cloud-based service, HIPAA FastTrack. JDL’s robust and growing managed services practice supports clients ranging from single-office providers, to multi-location regional specialists, to their regulated suppliers and business associates. A sampling includes:

| - | A national provider of healthcare staffing services and software with locations across the U.S. |

| - | A thriving medical and therapeutic services provider with 15 locations in the Atlanta area |

| - | A pharmaceutical manufacturing and biotesting firm with 900 employees in the U.S. |

Commercial:

JDL Technologies continues to build a solid roster of diverse commercial clients under its JDL TechWatch brand, delivering substantial growth in 2016 in recurring revenues from managed services as well as incremental revenues from additional project work. A sampling of these clients includes:

| - | The largest private international bank in South America |

| - | Several of the largest private investment firms in Florida |

| - | A 60-year-old, well-funded non-profit organization with 19 locations in the continental U.S. |

| - | A Florida personal injury law firm that has won more than $45 million in settlements |

| - | A large family-owned tobacco corporation headquartered in Florida since 1962 |

Education:

JDL Technologies continues to support a multi-year project to provide wireless network services and datacenter upgrades for several hundred public K-12 schools in Florida. The education vertical remains an important element of JDL’s overall market strategy.

Technology Solutions

As a managed service provider and value-added reseller, JDL Technologies specializes in delivering technology solutions that free organizations to focus on the strategic business activities that are critical to their financial success. JDL’s technology solutions encompass an extensive range of networking, virtualization, cloud and infrastructure services, most of which are available under JDL managed services contracts. As technology continues its move to the cloud, JDL aggressively markets its portfolio of cloud-based service offerings to healthcare and commercial business. Its HIPAA FastTrack and Security FastTrack services, provided in the JDL Cloud powered by Citrix, have won awards for product innovation, just as JDL Technologies has been recognized in the industry as a leading Managed Service Provider. JDL engineers are trained and certified in the newest cloud and other technology solutions.

Managed Services:

JDL Technologies continues to expand in breadth and depth as a managed service provider, significantly growing its recurring revenues each year since establishing the program in early 2013. JDL serves a diverse base of clients with locations throughout the United States, offering managed service programs designed specifically for the healthcare and commercial markets. These robust programs meet HIPAA compliance standards and, while the majority of clients are supported remotely, independent of geographic borders, JDL is also able to provide on-site network management and help desk support for key enterprise clients in South Florida. JDL’s managed services include network management, availability assurance, event alerting and incident management services; server, workstation, mobile device and other asset management services; security services including software patching, firewall, antivirus, antimalware and intrusion detection and prevention services; help desk support for client users; SIP trunking, voice over IP and office management services; migration, conversion and vendor management; and technical consulting services and training.

7

Cloud Solutions:

After building its portfolio of cloud service offerings in 2015, JDL has aggressively marketed these services in the healthcare and commercial verticals. Wireless as a service, infrastructure as a service, and Citrix as a service (sold as JDL FastTrack) are among the most popular cloud offerings, with others including backup, storage, voice over IP, firewall and email as cloud or hosted services. The benefits to clients are numerous and include vertical and horizontal scalability, internal bandwidth conservation, and simplification of IT management within client organizations, while JDL benefits from substantial economies of scale and standardization. All JDL cloud offerings are billable as monthly recurring revenue under its managed service model, and JDL is committed to bringing the benefits of cloud services to all clients.

Network Services:

JDL’s roots are in network services, and these services remain central to its role as a managed service provider and value-added reseller. The JDL team has extensive experience and professional certifications in assessing, designing and implementing wired and wireless networks as well as entire technology infrastructures. Networking services also include MPLS, private line and IP communications, network and endpoint security, network tuning and cabling/wiring services. Two large clients are actively leveraging JDL wireless services. The most recent, a pharmaceutical manufacturing and biotesting firm, has deployed wireless as a service in 18 locations across the U.S.

Virtualization:

Using virtualization across an organization’s IT environment delivers greater agility, mobility and efficiency. JDL’s virtualization engineers assess, design, deploy, and manage virtualization programs that ensure user access to any workload, anytime, anywhere, on any device. JDL’s virtualization services encompass desktops, servers, applications, storage, and any combination thereof, including connectivity and software licensing. As JDL clients continue to adopt virtualization, they experience the economies of scale, reduced capital requirements, enhanced security, and disaster recovery protections that are inherent in virtualized environments.

Order Book

Outstanding customer orders and contracts for JDL products and services were approximately $4,132,000 at March 1, 2017 and $6,009,000 at March 1, 2016. The Company does not consider current outstanding orders and contracts as a significant indicator of longer term future results.

(iv) Net2Edge

Net2Edge Limited, based in Basingstoke, Hampshire, United Kingdom, designs, manufactures and markets Carrier Ethernet based Network Access Devices and software under the Liberator™ brand name. Net2Edge™ operates a direct touch sales model and also Markets its products through approved partners and integrators. Net2Edge’s physical products allow network operators to transmit packetized voice and data across networks and between copper-wired and fiber-optic equipment. Software based products currently being developed will launch Net2Edge in to the Software Defined Networking (“SDN”) area and associated Network Function Virtualization (“NFV”) markets. Sales by Net2Edge were $1,873,000 in 2016 and $1,353,000 in 2015.

Products

Net2Edge designs, assembles and sells Ethernet based switches based around the international MEF standards. Those products range from legacy over packet interfaces such as Serial, TDM or ISDN and Native Ethernet from 1G to 10G and beyond. The products are targeted at the telecommunications service providers as Network Interface Devices. By design, the products transmit data from the subscriber enterprise to the provider edge, usually a router. The products are sophisticated, carrying multiple services with definable quality of service metrics over fiber optic paths. These products assist in resolving challenges in the areas of bandwidth constraints, security risks, and distance limitations as networks extend from local area to wide area networks and adapt to ever increasing end user demands. As enterprise networks are seemingly always in transition, our solutions enable customers to integrate multiple services into their existing infrastructure. All Net2Edge products incorporate features for performing advanced levels of fault management and automated provisioning minimizing the administrative burden of the operator.

8

The physical products are further enhanced by software development that will break down the relationship between specialized hardware and the variety of services that can be delivered. This initiative will allow the virtualization of services such as routing and firewalls, providing the operator with freedom of service offered without the need to visit the subscriber’s premise.

Net2Edge products support a wide variety of protocols, including: 10 Gigabit Ethernet, Gigabit Ethernet, Fast Ethernet, Ethernet, T1/E1, DS3, Circuit Emulation Services (TDM or ISDN over Ethernet or IP), RS232, RS485, OC3, OC12, and more. Net2Edge develops product hardware and software internally, and expenses the related costs as they are incurred. In connection with the sale of its hardware products, Net2Edge provides its customers with a variety of software management options including Element Management System (“EMS”) software for providing superior service provisioning and monitoring of next-generation Carrier Ethernet 2.0 Services.

Manufacturing and Sources of Supply

Net2Edge uses contract manufacturers to manufacture its products in the UK. Because some of Net2Edge’s offshore sources of supply are subject to risks, including political, communication and logistic risk, when possible, Net2Edge takes steps to ensure it has multiple suppliers to ensure business continuity.

Markets and Marketing

Net2Edge products are used in a broad array of market sectors including the Government, Enterprise, Utility, Industrial, and Surveillance markets, but as service subscribers to a service provider. Net2Edge has a growing international customer base outside the United Kingdom and customers use its products in a variety of applications.

Net2Edge’s marketing primarily consists of direct marketing using a sales force, tradeshows, trade magazine advertising, on-line advertising, website, email, social media and public relations activities. Net2Edge also provides and participates in advertising and cooperative marketing campaigns with its partners.

The Company’s “Net2Edge” brand name is important to its business. The Company regularly supports this brand name by trade advertising and intends for it to become well known in the marketplace.

Research and Development

Net2Edge develops products for the service provider market including products for emerging protocols and existing protocols in new markets, as well as new industry standards. These products include remote management devices built on the IEEE® 802.3AH, 802.3AG, ITU-T Y.1731 standards, Metro Ethernet Forum (“MEF”)® and MEF 2.0 standards. Some design efforts are paced by the development of critical components such as integrated circuits, System On Chip (“SOC”) silicon and optical transceivers.

Research and development consists primarily of designing, prototyping, testing equipment and supplies associated with enhancing existing products and developing new products. Research and development costs are expensed when incurred and were $621,000 in 2016 and $588,000 in 2015.

Net2Edge conducts its research and development operations out of its Basingstoke, United Kingdom headquarters location. While this UK location has primary engineering and product development responsibility, Net2Edge will occasionally use third party design services and Original Design Manufacturers (“ODM”) to support specific product design requirements.

Competition

Net2Edge faces strong competition across its entire product line. A large number of competitors exist for high volume products. There are low cost competitors from China and Taiwan and established competitors from the USA and Canada. Net2Edge competently competes from a portfolio and specialized development perspective.

9

(2) Employment Levels

As of March 1, 2017 the Company employed 398 people. Of this number, 227 were employed by Suttle (including 71 in Minnesota and 156 in Costa Rica), 93 by Transition Networks, Inc., 19 by Net2Edge in the U.K., 38 by JDL Technologies, Inc., and 21 corporate general and administrative positions. As noted above, in January 2017, the Company announced it was closing the Suttle Costa Rica production facility and consolidating production into its Minnesota facilities.

(3) Executive Officers of Registrant

The executive officers of the Company and their ages at March 1, 2017 are set forth below. See Item 9B of this Form 10-K for additional information on the Company’s management.

| Name | Age | Position1 | ||||

| Roger H.D. Lacey | 66 | Vice-Chairman of the Board and Chief Executive Officer [2014]2 | ||||

| Mark D. Fandrich | 55 | Vice President, Treasurer and Chief Financial Officer [2016]3 | ||||

| Bruce Blackwood | 54 | General Manager, Suttle, Inc. [2007]4 | ||||

| Scott Otis | 55 | General Manager, Transition Networks, Inc. [2013]5 | ||||

| Scott Fluegge | 47 | President and General Manager, JDL Technologies, Inc [2011]6 | ||||

| Kristin A. Hlavka | 35 | Corporate Controller [2011]8 | ||||

| 1 | Dates in brackets indicate year in which officers began serving in such capacity. Executive officers serve at the pleasure of the Board of Directors. |

| 2 | Mr. Lacey has been a director of the Company since 2008, was appointed Vice Chair in September 2013, and was appointed Interim Chief Executive Officer in June 2014. On February 27, 2015 he was appointed as the Company’s Chief Executive Officer. Mr. Lacey was Senior Vice President of Strategy and Corporate Development for 3M Corporation from 2009 until his retirement in 2013. In addition, from 2000 until his retirement, he was 3M Corporation’s Chief Strategy Officer and head of mergers and acquisitions. |

| 3 | Mr. Fandrich was appointed Chief Financial Officer in August 2016. From July 2015 to August 2016, he served as Vice President of Finance of Suttle, Inc.. From April 2004 to July 2015, he was Corporate Controller for The Bergquist Company, a global supplier of thermal interface material. |

| 4 | Mr. Blackwood has served as General Manager of Suttle since December 2007. From July 2001 to November 2007 he served as Suttle’s Vice President of Sales. |

| 5 | Mr. Otis was appointed General Manager of Transition Networks in September 2013. From December 2010 to June 2011 he served as Vice President, Operations - Professional Services for TE Connectivity, Inc. Prior to December 2010, he was the Vice President, Marketing and Business Development – ADC Professional Services. |

| 6 | Mr. Fluegge was appointed Vice President and General Manager of JDL Technologies in December 2011, and was named President and General Manager in September 2013. Prior to this, he was the Vice President of Workload Automation at GSS AMERICA / GSS INFOTECH / INFOSPECTRUM CONSULTING. |

10

| 7 | Ms. Hlavka was appointed Corporate Controller in May 2011. From July 2008 to April 2011, she served as the Assistant Corporate Controller. Prior to July 2008, she was an auditor for Deloitte and Touche LLP. |

(d) FINANCIAL INFORMATION ABOUT FOREIGN AND DOMESTIC OPERATIONS AND EXPORT SALES

Financial information about domestic and foreign operations and export sales may be obtained by reference to Note 12 of the “Notes to Consolidated Financial Statements” under Item 8 herein.

| ITEM 1A. | RISK FACTORS |

Forward Looking Statements

Certain statements contained in this Annual Report on Form 10-K are “forward-looking” statements within the meaning of and in reliance on the Private Securities Litigation Reform Act of 1995, which provides a “safe harbor” for forward-looking statements. Actual events and results may differ materially from those expressed or forecasted in forward-looking statements due to a number of factors. The principal important risk factors that could cause our actual performance and future events and actions to differ materially from these forward-looking statements include, but are not limited to, the risk factors discussed below.

Risks Related to Our Business

The primary markets we serve are highly competitive, and our ability to compete requires continual focus on delivering high-quality, competitively priced products and services and the regular introduction of new products and services that meet evolving customer requirements.

Competition in the markets for voice and data communications products is intense. Our ability to compete with other manufacturers of these products depends primarily on our engineering, manufacturing and marketing skills; the price, quality and reliability of our products; our delivery and service capabilities; and our control of operating expenses. Our JDL subsidiary also experiences intense competition from other providers of IT products and services. We have experienced, and anticipate continuing to experience, pricing pressures from our customers as well as our competitors. The markets we serve are characterized by rapid technological advances and evolving industry standards. These markets can be significantly affected by new product introductions and marketing activities of industry participants. Some of our competitors and potential competitors have greater financial, technological, manufacturing, marketing, and personnel resources than we. Present and future competitors may be able to identify new markets and develop new products that are superior to those developed by us. They may also adapt new technologies faster, devote greater resources to research and development, promote products more aggressively, and price products more competitively than we. We cannot ensure that competition will not intensify or that we will be able to compete effectively in the markets in which we compete.

Our gross margins have declined in recent years, and we face many challenges in maintaining acceptable margins.

Gross margins among our products and services vary and are subject to fluctuation from quarter to quarter. The factors that may affect our gross margins adversely are numerous and include:

| ● | Changes in customer, geographic, or product mix; |

| ● | Our ability to reduce product costs |

| ● | Increases in material or labor costs |

| ● | Expediting costs incurred to meet customer delivery requirements |

| ● | Excess inventory and inventory carrying charges |

11

| ● | Obsolescence charges |

| ● | Changes in shipment volume |

| ● | Changes in component pricing |

| ● | Increased price competition |

| ● | Changes in distribution channels |

| ● | Lower margins on competitive-bid contracts |

| ● | Increased warranty cost and |

| ● | Our ability to manage the impact of foreign currency exchange rate fluctuations. |

Consolidation among our customers has occurred and further consolidation may occur, resulting in the loss of some customers and reducing revenue during the pendency of business combinations and related integration activities.

We believe future consolidation may occur among our customers as they attempt to increase market share and achieve greater economies of scale. Consolidation has affected our business as our customers focus on completing business combinations and integrating their operations. In some instances, customers integrating large-scale acquisitions have reduced their purchases of our products as they integrate.

The business impact to us of significant customer mergers is likely to be unclear until sometime after these transactions are completed. After a consolidation occurs, a customer may choose to reduce the number of vendors from which it purchases equipment and may choose one of our competitors as its preferred vendor. We cannot ensure that we will continue to supply equipment to the surviving communications service provider after a business combination is completed.

Our financial results could be adversely affected if one or more of our key customers substantially reduces orders for our products.

Traditionally, we have derived a large portion of our revenues from a relatively small number of customers, with our top ten customers accounting for 68%, 67% and 72% of net sales for 2016, 2015 and 2014, respectively. In fiscal 2016, 2015, and 2014, one Suttle customer accounted for approximately 12%, 16% and 33% of consolidated sales, respectively. In fiscal 2016 and 2015, a JDL customer accounted for 11% and 11% of our consolidated sales, respectively. The loss of or a substantial reduction in purchases by any one or more of our top customers could have a material adverse effect on our business, financial position and results of operations.

Our market is subject to rapid technological change and, to compete effectively, we must continually introduce new products that achieve market acceptance.

The communications equipment industry is characterized by rapid technological changes, evolving industry standards, changing market conditions, short product life cycles, rapidly changing customer requirements, and frequent new product and service introductions and enhancements. The introduction of products using new technologies or the adoption of new industry standards can make our existing products, or products under development, obsolete or unmarketable. Our future success will depend on our ability to enhance our existing products, to introduce new products to meet changing customer requirements and emerging technologies, and to demonstrate the performance advantages and cost-effectiveness of our products over competing products. Our failure to modify our products to support new alternative technologies or failure to achieve widespread customer acceptance of these modified products could cause us to lose market share and cause our revenues to decline.

We may not predict technological trends or the success of new products in the communications equipment market accurately. New product development often requires forecasting of market trends, development and implementation of new technologies and processes and substantial capital commitments. We do not know whether other new products we develop will gain market acceptance or result in profitable sales.

Some competitors have greater engineering and product development resources. Although we expect to continue to invest significant resources in product development activities, our efforts to achieve and maintain profitability will require us to be selective and focused with our research and development expenditures. If we fail to anticipate or respond in a cost-effective and timely manner to technological developments, changes in industry standards or customer requirements, or if we experience any significant delays in product development or introduction, our business, operating results and financial condition could be affected adversely.

12

We may experience delays in developing and marketing product enhancements or new products that respond to technological change, evolving industry standards and changing customer requirements. We cannot ensure that we will not experience difficulties that could delay or prevent the successful development, introduction, and marketing of these products or product enhancements, or that our new products and product enhancements will adequately meet the requirements of the marketplace and achieve any significant or sustainable degree of market acceptance in existing or additional markets. In addition, the future introductions or announcements of products by us or one of our competitors embodying new technologies or changes in industry standards or customer requirements could render our then-existing products obsolete or unmarketable. We cannot ensure that the introduction or announcement of new product offerings by us or one or more of our competitors will not cause customers to defer their purchase of our existing products, which could cause our revenues to decline.

Our business units are dependent upon federal government spending.

Our JDL Technologies and Transition Networks business units are involved in projects that receive much of their funding from the United States federal government. To the extent that federal government spending is delayed or curtailed by government actions, our revenues and operating results may be adversely affected.

We evaluate and frequently pursue acquisitions, but we may not successfully close these acquisitions and, if these acquisitions are completed, we may have difficulty integrating the acquired businesses with our existing operations.

We regularly consider the acquisition of complementary companies and product lines. We cannot, however, ensure that we will be able to find appropriate candidates for acquisitions, reach agreement to acquire them, or obtain any required shareholder or regulatory approvals needed to close strategic acquisitions, despite the effort and management attention invested.

The impact of future acquisitions on our business, operating results and financial condition is uncertain. In the case of businesses we may acquire in the future, we may have difficulty assimilating these businesses and their products, services, technologies and personnel into our operations. These difficulties could disrupt our ongoing business, distract our management and workforce, increase our expenses and materially adversely affect our operating results and financial condition. Also, we may not be able to retain key management and other critical employees after an acquisition. We may also acquire unanticipated liabilities. In addition to these risks, we may not realize all of the anticipated benefits of these acquisitions.

Our operating results fluctuate from quarter to quarter.

Our operating results are difficult to predict and may fluctuate significantly from quarter to quarter. Fluctuations in our quarterly operating results may be caused by many factors, including the following:

| ● | the volume of customer orders and our ability to fulfill those orders in a timely manner |

| ● | the overall level of capital expenditures by our customers |

| ● | work stoppages and other developments affecting the operations of our customers |

| ● | the timing of and our ability to obtain new customer contracts |

| ● | the timing of revenue recognition |

| ● | the timing of new product and service introductions |

| ● | the availability of products and services |

| ● | market acceptance of new and enhanced versions of our products and services |

| ● | variations in the mix of products and services we sell |

13

| ● | the timing of federal and state government funding of projects |

| ● | the location and utilization of our production capacity and employees and |

| ● | the availability and cost of key components of our products. |

Our expense levels are based in part on expectations of future revenues. If revenue levels in a particular quarter are lower than expected, our operating results will be affected adversely.

We depend on manufacturing relationships and on limited-source suppliers and any disruptions in these relationships may cause damage to our customer relationships.

We procure all parts and certain services involved in the production of our products from, and subcontract much of our product manufacturing to outside firms that specialize in these services. Although most of the components of our products are available from multiple vendors, we have several single-source supplier relationships, either because alternative sources are not available or because the relationship is advantageous to us. We cannot ensure that our suppliers will be able to meet our future requirements for products and components in a timely fashion. In addition, the availability of many of these components to us is dependent in part on our ability to provide our suppliers with accurate forecasts of our future requirements. Delays or lost sales could be caused by other factors beyond our control, including defects in the quality of components or products supplied by others.

We are dependent upon our senior management and other critical employees.

Like all companies, our success is dependent on the efforts and abilities of our senior management personnel and other critical employees, including those in sales, marketing and product development functions. Our ability to attract, retain and motivate these employees is critical to our success. In addition, because we may acquire one or more businesses in the future, our success may depend, in part, upon our ability to retain and integrate our own personnel with personnel from acquired entities that are necessary to the continued success or the successful integration of the acquired businesses.

Managing our inventory is complex and may include write-downs of excess or obsolete inventory.

Managing our inventory of components and finished products is complicated by a number of factors, including the need to maintain a significant inventory of finished goods for orders we anticipate but may not be received. These issues may cause us to purchase and maintain significant amounts of inventory. If this inventory is not used as expected based on anticipated requirements, it may become excess or obsolete. The existence of excess or obsolete inventory can result in sales price reductions or inventory write-downs, which could adversely affect our business and results of operations.

We face risks associated with expanding our sales outside of the United States.

We believe that our future growth depends in part upon our ability to increase sales in international markets. These sales are subject to a variety of risks, including fluctuations in currency exchange rates, tariffs, import restrictions and other trade barriers, unexpected changes in regulatory requirements, longer accounts receivable payment cycles, potentially adverse tax consequences, and export license requirements. In addition, we are subject to the risks inherent in conducting business internationally, including political and economic instability and unexpected changes in diplomatic and trade relationships. We cannot ensure that one or more of these factors will not have a material adverse effect on our business strategy and financial condition.

Goodwill impairment could adversely affect our net income and shareholders’ equity

We are required to test goodwill for impairment annually and between annual tests if events or circumstances indicate that it is more likely than not that the fair value of a reporting unit is less than its carrying amount. We perform our annual impairment test as of April 1 each year. Various risks may cause the fair value of a reporting unit to fall below its carrying amount; these risks could lead to the measurement and recognition of a goodwill impairment. At December 31, 2016, we had recorded goodwill of $1.46 million from our JDL Technologies’ acquisition of Twisted Technologies in June 2015. If JDL Technologies fails to achieve the future revenue and gross margin levels that we expect, we may be forced to recognize a non-cash impairment with respect to the carrying value of this goodwill.

14

Our failure to achieve and maintain effective internal controls could limit our ability to detect and prevent fraud and thereby adversely affect our business and stock price.

We have incurred, and expect to continue to incur, significant continuing costs, including accounting fees and staffing costs, to maintain compliance with the internal control requirements of the Sarbanes-Oxley Act of 2002. Expansion of our business, particularly internationally, would require ongoing changes to our internal control systems, processes and information systems. In addition, if we complete future acquisitions, our ability to integrate operations of the acquired company could affect our continued compliance with the internal control requirements of the Sarbanes-Oxley Act.

We maintain effective internal controls to generate reliable financial reports. All internal control systems, no matter how well designed, have inherent limitations. Even those systems determined to be effective can provide only reasonable assurance with respect to the consolidated financial system preparation and presentation. Our inability to maintain an effective control environment may cause investors to lose confidence in our reported financial information, which could in turn have a material adverse effect on our stock price. While reviewing our internal controls over financial reporting for the year ended December 31, 2016, we determined we had a material weakness as in internal controls related to segregation of duty conflicts. In conducting this review, we also determined that these same segregation of duty conflicts were substantially present at December 31, 2015. Therefore, we have concluded that a material weakness in our internal controls over financial reporting also existed at December 31, 2015. We also determined we had a material weakness in internal controls over financial reporting due to our failure to review, in sufficient detail, our analysis and the basis for our conclusion that our goodwill was not impaired. See Item 9A for further details.

Product defects or the failure of our products to meet specifications could cause us to lose customers and revenue or to incur unexpected expenses.

If our products do not meet our customers’ performance requirements, our customer relationships may suffer. Also, our products may contain defects or fail to meet product specifications. Any failure or poor performance of our products could result in:

| ● | delayed market acceptance of our products |

| ● | delayed product shipments |

| ● | unexpected expenses and diversion of resources to replace defective products or identify and correct the source of errors |

| ● | damage to our reputation and our customer relationships |

| ● | delayed recognition of sales or reduced sales, and |

| ● | product liability claims or other claims for damages that may be caused by any product defects or performance failures. |

Our sales and operations may continue to be impacted adversely by current global economic conditions.

Over the past several years, financial markets globally have experienced periods of extreme disruption. These have included, among other things, extreme volatility in securities prices, severely diminished liquidity and credit availability, ratings downgrades of some investments and declining valuations of others. The frequency, severity and duration of these disruptions in the financial markets and the global economy are unknown. We cannot ensure that there will not be a further deterioration in financial markets and in business conditions generally. These economic developments have adversely affected our business in a number of ways and will likely continue to adversely affect our business during the foreseeable future.

Risks Related to Our Common Stock

Our stock price has been volatile historically and the price of our common stock may fluctuate significantly in the future.

The trading price of our common stock has been and may continue to be subject to wide fluctuations. Our stock price may fluctuate in response to a number of events and factors, such as quarterly variations in operating results, announcements of technological innovations or new products by us or our competitors, the operating and stock price performance of other companies that investors may deem comparable to us, and new reports relating to trends in our markets or general economic conditions.

15

In addition, the stock market in general, and prices for companies in our industry in particular, have experienced extreme volatility that often has been unrelated to the operating performance of these companies. These broad market and industry fluctuations may adversely affect the price of our common stock, regardless of our operating performance.

Anti-takeover provisions in our charter documents, our shareholder rights agreement and Minnesota law could prevent or delay a change in control of our company.

Provisions of our articles of incorporation and bylaws, our shareholder rights agreement (also known as a “poison pill”) and Minnesota law may discourage, delay or prevent a merger or acquisition that a shareholder may consider favorable, and could limit the price that investors are willing to pay for our common stock. These provisions include the following:

| ● | advance notice requirements for shareholder proposals |

| ● | authorization for our Board of Directors to issue preferred stock without shareholder approval |

| ● | authorization for our Board of Directors to issue preferred stock purchase rights upon a third party’s acquisition of 16.5% or more of our outstanding shares of common stock; |

| ● | limitations on business combinations with interested shareholders and |

| ● | a super majority vote by shareholders is required to approve certain corporate actions, including merger transactions. |

Some of these provisions may discourage a future acquisition of our company even though our shareholders would receive an attractive value for their shares, or a significant number of our shareholders believe such a proposed transaction would be in their best interest.

The payment and amount of future dividends is subject to Board of Director discretion and to various risks and uncertainties.

The payment and amount of future quarterly dividends is within the discretion of the Board of Directors and will depend on factors the Board deems relevant at the time declaration of a dividend is considered. These factors include, but are not limited to: available cash; management’s expectations regarding future performance and free cash flow; alternative uses of cash to fund R&D expenditures and capital expenditures required to fund future growth; and, the effect of various risks and uncertainties described in this “Risk Factors” section.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

CSI conducts administrative, manufacturing and engineering functions at the following facilities:

| - | In Minnetonka, Minnesota, the Company owns a 105,000 square foot building where its executive and administrative offices are located. In addition, Transition Networks uses this facility for its warehouse, assembly, engineering and administrative operations, JDL Technologies. uses this facility for some administrative operations, and Suttle uses this facility for its sales, marketing and product development. |

| - | Suttle’s manufacturing is conducted at two locations. At Hector, Minnesota, the Company owns three buildings totaling 109,000 square feet of manufacturing space. The Company leases 40,000 square feet of manufacturing space in San Jose, Costa Rica. |

| - | Net2Edge leases 5,500 square feet of office space in the U.K. for its Transition Networks, EMEA operations. |

16

CSI believes these facilities will be adequate to accommodate its administrative, manufacturing and distribution needs for the foreseeable future.

| ITEM 3. | LEGAL PROCEEDINGS |

The Company is subject to claims and lawsuits that have been filed in the ordinary course of business. From time to time, the Company brings suit against others to enforce contract rights or property rights, or to collect debts in the ordinary course of business. Management believes that the resolution or settlement of any pending litigation will not have a material adverse effect on the results of operations or liquidity of the Company.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASE OF EQUITY SECURITIES |

(a) MARKET INFORMATION

The Company’s common stock trades on the NASDAQ under the trading symbol JCS.

The table below presents the price range of high and low trades of the Company’s common stock for each quarterly period indicated as reported by NASDAQ for 2016 and 2015.

| 2016 | 2015 | ||||||||||||||||

| High | Low | High | Low | ||||||||||||||

| First | $ | 8.16 | $ | 5.56 | $ | 12.40 | $ | 10.08 | |||||||||

| Second | 7.49 | 6.06 | 11.78 | 10.40 | |||||||||||||

| Third | 7.42 | 4.63 | 10.86 | 8.13 | |||||||||||||

| Fourth | 5.40 | 3.41 | 9.22 | 7.25 | |||||||||||||

(b) HOLDERS

At March 1, 2017 there were approximately 562 registered holders of record of Communications Systems, Inc. common stock.

(c) DIVIDENDS

Communications Systems, Inc. paid regular quarterly dividends to its shareholders on the dates and at the rates indicated below:

| Payment Date | Dividend per Share | |||

| January 1, 2017 | $ | .04 | ||

| October 1, 2016 | .04 | |||

| July 1, 2016 | .16 | |||

| April 1, 2016 | .16 | |||

| January 1, 2016 | .16 | |||

| October 1, 2015 | .16 | |||

| July 1, 2015 | .16 | |||

| April 1, 2015 | .16 | |||

| January 1, 2015 | .16 | |||

17

The payment of future dividends will be determined at the discretion of the Board of Directors.

(d) INFORMATION REGARDING EQUITY COMPENSATION PLANS

The following table presents information about the Company’s equity compensation plans, under which equity securities of the Company are authorized for issuance, as of December 31, 2016:

Securities Authorized for Issuance Under Equity Compensation Plans

| Number of shares | Number of shares of | |||||||||

| of common stock | common stock remaining | |||||||||

| to be issued upon | available for future | |||||||||

| exercise of | Weighted-average | issuance under equity | ||||||||

| outstanding | exercise price of | compensation plans | ||||||||

| options, warrants | outstanding options | (excluding shares in | ||||||||

| Plan Category (1) | and rights | warrants and rights | column (a)) | |||||||

| Equity compensation plans approved by security holders: | ||||||||||

| 1992 Stock Plan-Employee Plan | 10,230 | $ | 14.15 | — | ||||||

| 1992 Stock Plan-Nonemployee Director Plan | 63,000 | $ | 10.82 | — | ||||||

| 1990 Employee Stock Purchase Plan | 6,156 | $ | 3.94 | 76,865 | ||||||

| 2011 Executive Incentive Compensation Plan | 1,026,094 | $ | 9.87 | 836,323 | ||||||

| Equity compensation plans not approved by security holders: | ||||||||||

| None | ||||||||||

| (1) | The Company does not have individual compensation arrangements involving the grant of options, warrants and rights. |

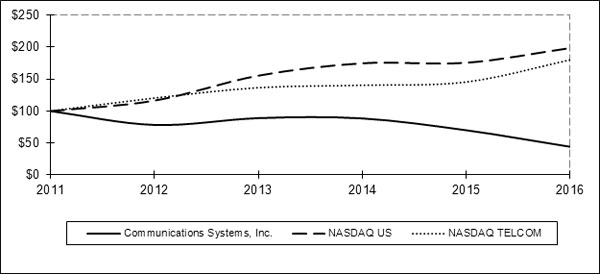

| (e) | FIVE YEAR PERFORMANCE GRAPH |

The following graph presents, at the end of each of the Company’s last five fiscal years, the cumulative total return on the common stock of the Company as compared to the cumulative total return reported for the NASDAQ (U.S.), and the NASDAQ Telecommunications Index. Company information and each index assume the investment of $100 on the last business day before January 1, 2011 and the reinvestment of all dividends.

18

Comparison of Five-Year Cumulative Total Return

| Company or Index | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||

| Communications Systems, Inc. | $ | 100.000 | $ | 78.335 | $ | 88.999 | $ | 88.544 | $ | 70.022 | $ | 44.305 | ||||||||||||

| NASDAQ US | 100.000 | 100.312 | 116.793 | 155.899 | 175.326 | 176.169 | ||||||||||||||||||

| NASDAQ TELCOM | 100.000 | 105.626 | 127.317 | 144.379 | 148.323 | 153.652 | ||||||||||||||||||

(f) RECENT SALES OF UNREGISTERED SECURITIES

Not applicable.

(g) PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS

During the three months ended December 31, 2016 the Company repurchased shares of stock as follows:

ISSUER PURCHASES OF EQUITY SECURITIES

| Period | Total Number of Shares (or Units) Purchased (1) | Average Price Paid per Share (or Unit) | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs (2) | ||||||||||||

| October 2016 | — | $ | — | — | 411,910 | |||||||||||

| November 2016 | 281 | 4.28 | — | 411,910 | ||||||||||||

| December 2016 | — | — | — | 411,910 | ||||||||||||

| Total | 281 | $ | 4.28 | — | 411,910 | |||||||||||

| (1) | The shares in this column represent shares that were surrendered to us by plan participants to satisfy withholding tax obligations related to share-based compensation. |

| (2) | Shares represent remaining amount of a 500,000 share repurchase authorization approved by the Company’s Board in October 2008 and publicly announced in November 2008. |

19

| ITEM 6. | SELECTED FINANCIAL DATA |

The following selected financial data has been derived from our consolidated financial statements and should be read in conjunction with the Consolidated Financial Statements and related notes thereto set forth in Item 8 and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K.

COMMUNICATIONS SYSTEMS, INC. AND SUBSIDIARIES

SELECTED FINANCIAL INFORMATION

(in thousands, except per share amounts)

| Year Ended December 31 | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

| Selected Income Statement Data | ||||||||||||||||||||

| Sales | $ | 99,353 | $ | 107,670 | $ | 119,071 | $ | 131,320 | $ | 104,250 | ||||||||||

| Costs and Expenses: | ||||||||||||||||||||

| Cost of sales | 72,771 | 76,123 | 76,913 | 86,421 | 62,753 | |||||||||||||||

| Selling, general and administrative expenses | 35,186 | 40,830 | 38,628 | 36,743 | 38,101 | |||||||||||||||

| Additional minimum pension liability adjustments1 | (4,148 | ) | — | — | — | — | ||||||||||||||

| Pension settlement costs | — | 1,222 | — | — | — | |||||||||||||||

| Impairment loss | — | — | — | 5,850 | — | |||||||||||||||

| Restructuring expense | — | — | 238 | 1,149 | — | |||||||||||||||

| Total Costs and Expenses | 103,809 | 118,175 | 115,779 | 130,163 | 100,854 | |||||||||||||||

| Operating (Loss) Income | (4,456 | ) | (10,505 | ) | 3,292 | 1,157 | 3,396 | |||||||||||||

| Other (Expense) Income, Net1 | (3,400 | ) | 104 | (112 | ) | (53 | ) | 2 | ||||||||||||

| (Loss) Income Before Income Taxes | (7,856 | ) | (10,401 | ) | 3,180 | 1,104 | 3,398 | |||||||||||||

| Income Tax (Benefit) Expense | 257 | (753 | ) | 1,219 | 2,061 | 1,160 | ||||||||||||||

| Net (Loss) Income | $ | (8,113 | ) | $ | (9,648 | ) | $ | 1,961 | $ | (957 | ) | $ | 2,238 | |||||||

| Basic Net (Loss) Income Per Share | $ | (0.92 | ) | $ | (1.11 | ) | $ | 0.23 | $ | (0.11 | ) | $ | 0.26 | |||||||

| Diluted Net (Loss) Income Per Share | $ | (0.92 | ) | $ | (1.11 | ) | $ | 0.23 | $ | (0.11 | ) | $ | 0.26 | |||||||

| Cash Dividends Declared Per Share | $ | 0.40 | $ | 0.64 | $ | 0.64 | $ | 0.64 | $ | 0.64 | ||||||||||

| Average Diluted Shares Outstanding | 8,832 | 8,720 | 8,640 | 8,531 | 8,519 | |||||||||||||||

| Selected Balance Sheet Data | ||||||||||||||||||||

| Total Assets | $ | 73,177 | $ | 87,916 | $ | 100,286 | $ | 103,533 | $ | 112,535 | ||||||||||

| Property, Plant and Equipment, Net | 15,719 | 17,468 | 18,153 | 14,941 | 14,475 | |||||||||||||||

| Long-term Liabilities | 176 | 290 | 1,271 | 1,838 | 3,298 | |||||||||||||||

| Stockholders’ Equity | 61,633 | 72,185 | 86,020 | 88,622 | 93,995 | |||||||||||||||

1 As part of the settlement of our pension plan, the Company recorded $4.1 million in pension liability gains previously recorded in accumulated other comprehensive income within operating expenses during 2016. Additionally, the Company recognized $4.2 million in foreign currency translation losses within Other (Expense) Income due to the substantial liquidation of our Austin Taylor subsidiary in the U.K.

20

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Overview

Communications Systems, Inc. provides physical connectivity infrastructure products and services for global deployments of broadband networks through the following business units:

Suttle

Founded in 1910, Suttle provides network solutions that meet service providers’ needs at the edge of the network and inside the home/business. Suttle’s product portfolio incorporates technology, leveraging existing infrastructure, and laying the foundation for future growth. Products are designed to comply with the most stringent industry standards. Quality management systems are ISO 9001 and TL9000 certified. Suttle’s newest brands are FutureLinkTM and MediaMAX™. FutureLinkTM provides high-speed connectivity solutions in the last mile of a network. The FutureLinkTM Stackable Fiber Interface Terminal (SFIT)—among other platforms that feature grow-as-you-go capability—is part of Suttle’s FTTx solution. MediaMAX™ is designed for gigabit services for the connected home/business. MediaMAX™ optimizes installation cost while maximizing coverage and high-bandwidth.

Transition Networks

With over 30 years of growth and expertise in hardware and software development, Transition Networks offers customers the ability to affordably integrate the benefits of fiber optics into any data network, in any application, and in any environment. Offering support for multiple protocols, any interface, and a multitude of hardware platforms, Transition Networks’ portfolio gives customers the power to deliver and manage network traffic reliably over fiber. Transition Networks distributes hardware-based connectivity solutions exclusively through a network of resellers in over 90 countries.

JDL Technologies

JDL Technologies provides technology services and infrastructure to the commercial, healthcare and education market segments. The company’s portfolio of technology solutions includes managed services, virtualization and cloud solutions, wired and wireless network design and implementation services, and converged infrastructure configuration and deployment. JDL has provided many of these technology services to the School Board of Broward County, Florida, the sixth largest public school district in the U.S., for more than a decade, and also provides these services to a number of commercial and healthcare clients.

Net2Edge

Net2Edge has been created to focus on the service provider/communications markets. Designing, manufacturing and marketing Carrier Ethernet based Network Access Devices and software that will revolutionize the near future evolution to the next wave of network modernization. Carrier Ethernet is the standard universal service provider delivery system based on the internationally recognized MEF service standards. Net2Edge has created significant market differentiation by enabling legacy services over Carrier Ethernet Access Devices. Service providers all over the world still have vast old networks which are expensive to operate, maintain and manage yet have millions of subscribers. Net2Edge helps resolve that challenge by bringing these legacy services in to the 21st century network.

Key 2016 Developments

| ● | The Company’s 2016 sales were $99.4 million, a 8% decrease from 2015 sales of $107.7 million. |

| ● | The Company’s 2016 net loss was $8.1 million, or ($0.92) per diluted share, compared to net loss of $9.6 million or ($1.11) per diluted share in fiscal 2015. |

| ● | At 2016 year end, the Company had cash, cash equivalents and investments of $16.2 million and positive working capital of $44.0 million compared to cash, cash equivalents and investments of $21.3 million and working capital of $46.4 million at December 31, 2015. |

| ● | Suttle sales decreased 16% to $42.1 million in 2016 from $50.1 million in 2015, primarily due to a decrease in international sales and in sales to its largest telecommunications customer. Suttle had an operating loss of $8.6 million in 2016 compared to an operating loss of $6.4 million in 2015. |

| ● | Transition Networks sales decreased 1% to $41.1 million in 2016 from $41.4 million in 2015. Transition had operating income of $0.3 million in 2016 compared to an operating loss of $1.2 million in 2015. |

21

| ● | Sales by JDL Technologies decreased 1% to $15.5 million in 2016 from $15.7 million in 2015. JDL had operating income of $1.9 million in 2016 compared to operating income of $1.2 million in 2015. |