Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - XpresSpa Group, Inc. | v462079_ex32.htm |

| EX-31.2 - EXHIBIT 31.2 - XpresSpa Group, Inc. | v462079_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - XpresSpa Group, Inc. | v462079_ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - XpresSpa Group, Inc. | v462079_ex23-1.htm |

| EX-21 - EXHIBIT 21 - XpresSpa Group, Inc. | v462079_ex21.htm |

| EX-10.27 - EXHIBIT 10.27 - XpresSpa Group, Inc. | v462079_ex10-27.htm |

| EX-3.1 - EXHIBIT 3.1 - XpresSpa Group, Inc. | v462079_ex3-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___ to ___

Commission file number 001-34785

FORM Holdings Corp.

(Exact name of registrant as specified in its charter)

| Delaware | 20-4988129 |

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

780 Third Avenue, 12th Floor New York, NY |

10017 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (212) 309-7549

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $0.01 per share | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer ", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |

|

Non-accelerated filer |

¨ | Smaller reporting company | x | |

| [Do not check if a smaller reporting company] | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the registrant's common stock held by non-affiliates of the registrant (without admitting that any person whose shares are not included in such calculation is an affiliate), computed by reference to the closing sale price of such shares on The NASDAQ Stock Market LLC on June 30, 2016 was $28,369,000.

As of March 30, 2017, 19,198,454 shares of the registrant's common stock are outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents (or parts thereof) are incorporated by reference into the following parts of this Annual Report on Form 10-K: Certain information required in Part III of this Annual Report on Form 10-K is incorporated from the Registrant’s Proxy Statement for the 2017 Annual Meeting of Stockholders.

Table of Contents

3

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements relating, among other matters, to our anticipated financial performance, future revenues or earnings, business prospects, projected ventures, new products and services, anticipated market performance and similar matters.

These risks and uncertainties, many of which are beyond our control, include:

| • | the impact of our business and asset acquisitions on our operations and operating results including our ability to realize the expected value and benefits of such acquisitions; |

| • | our ability to develop and introduce new products and/or develop intellectual property; |

| • | our ability to protect and maintain our intellectual property rights; |

| • | our ability to raise additional capital to fund our operations and business plan and the effects that such financing may have on the value of the equity instruments held by our stockholders; |

| • | our ability to retain key members of our management team; |

| • | general economic conditions and level of consumer and corporate spending on technology, consumer electronics, health and wellness, and travel; |

| • | our ability to hire a skilled labor force and the costs associated with that labor; |

| • | with regard to our retail businesses, our ability to secure new locations, maintain existing ones, and ensure continued customer traffic at those locations; |

| • | our ability to protect our customers’ financial data and other personal information; |

| • | the loss of one or more of our significant suppliers or vendors; |

| • | unexpected trends in the travel, health and wellness, mobile phone, telecom computing, and consumer electronics industries and potential technology and service obsolescence; |

| • | market acceptance, quality, pricing, availability and useful life of our products and/or services, as well as the mix of our products and services sold; |

| • | lawsuits, claims, and investigations that may be filed against us and other events that may adversely affect our reputation; |

| • | our ability to license and monetize our patents, including litigation outcomes; and |

| • | competitive conditions within our industries. |

Forward-looking statements may appear throughout this Annual Report on Form 10-K, including, without limitation, the following sections: Item 1 “Business,” Item 1A “Risk Factors,” and Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements generally can be identified by words such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “projects,” “will be,” “will continue,” “will likely result,” and similar expressions. These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, which could cause our actual results to differ materially from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Annual Report on Form 10-K, and in particular, the risks discussed under the caption “Risk Factors” in Item 1A of this report and those discussed in other documents we file with the Securities and Exchange Commission (“SEC”). We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

All references in this Annual Report on Form 10-K to “we,” “us” and “our” refer to FORM Holdings Corp. (prior to May 5, 2016, known as “Vringo, Inc.”), unless the context requires otherwise.

4

Overview

FORM Holdings Corp (“FORM” or the “Company”) focuses on acquiring and building companies that would benefit from:

| • | additional capital; |

| • | exposure to visibility from the public markets; |

| • | talent recruiting; |

| • | rebranding; and |

| • | implementation of best practices. |

Our management team is committed to executing on our strategy. Our focus is on travel, health and wellness, and technology. We limit our scope by only looking at companies with a clear path for growth.

Segments

We currently have four operating segments:

| • | XpresSpa |

| • | Group Mobile |

| • | FLI Charge |

| • | Intellectual property |

Our Strategy and Outlook

XpresSpa

We acquired XpresSpa on December 23, 2016. XpresSpa is a leading airport retailer of spa services and related products. It is a well-recognized and popular airport spa brand with approximately 50% market share in the United States and nearly three times the number of domestic locations as its closest competitor. It provides nearly 700,000 services per year. As of December 31, 2016, XpresSpa operated 53 total locations in 40 terminals and 22 airports in three countries, the United States, Netherlands, and United Arab Emirates. XpresSpa also sells wellness and travel products through its internet site, www.xpresspa.com. Key services and products include:

| • | massage services for the neck, back, feet and whole body; |

| • | nail care, such as pedicures, manicures and polish changes; |

| • | travel products such as neck pillows, blankets, massage tools and eye masks. |

5

For over a decade, increased security requirements have led travelers to spend more time at the airport. In addition, in anticipation of the long and often stressful security lines, travelers allow for more time to get through security and, as a result, often experience increased downtime prior to boarding. Consequentially, travelers at large airport hubs spend approximately 75 minutes in the terminal after passing through security.

XpresSpa was developed to address the stress and idle time spent at the airport, allowing travelers to spend this time productively, by relaxing and focusing on personal care and wellness. We believe that XpresSpa is well positioned to benefit from consumers’ growing interest in health and wellness and increasing demand for spa services and related wellness products.

In addition, a confluence of microeconomic events has created favorable conditions for the expansion of retail concepts at airports, in particular, retail concepts that attract higher spending from air travelers. The competition for airplane landings has forced airports to lower landing fees, which in turn has necessitated augmenting their retail offerings to offset budget shortfalls. Infrastructure projects at airports across the country, again intended to make an airport more desirable to airlines, require funding from bond issuances that in turn rely upon, in part, the expected minimum rent guarantees and expected income from concessionaires.

Equally as important to the industry growth is XpresSpa’s flexible retail format. XpresSpa opens multiple locations annually, which have ranged in size from 300 square feet to 3,000 square feet, with a typical size of 1,000 to 1,200 square feet. XpresSpa is able to adapt its operating model to almost any size location available in space constrained airports. This increased flexibility compared to other retail concepts allows XpresSpa to operate multiple stores within an airport, from which it enjoys synergies due to shared labor between stores.

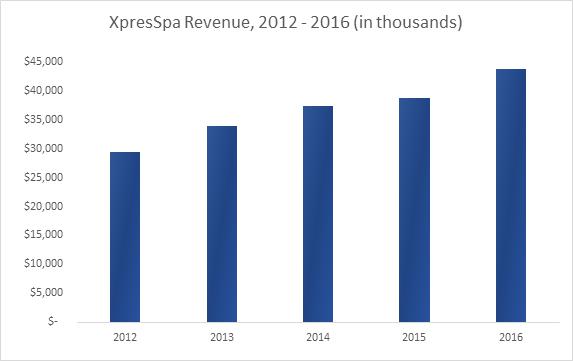

XpresSpa’s total revenues have increased 49% from approximately $29,353,000 in 2012 to $43,820,000 in 2016, largely as a result of the growth in the number of spas, from 28 in January 2012 to 53 in December 2016.

6

XpresSpa regularly measures comparable store sales, which it defines as current period sales from stores opened more than 12 months compared to those same stores’ sales in the prior year period (“Comp Store Sales”). The measurement of Comp Store Sales on a daily, weekly, monthly and year-to-date basis provides an additional perspective on XpresSpa’s total sales growth when considering the influence of new unit contribution. A reconciliation between Comp Store Sales, which is a non-GAAP measure commonly used in the retail industry, and total revenue as reported on the financial statements is presented below:

| (In Thousands) | 2012 | 2013 | 2014 | 2015 | 2016 | |||||||||||||||

| Comp Store Sales | $ | 21,461 | $ | 26,569 | $ | 31,441 | $ | 34,060 | $ | 38,943 | ||||||||||

| Non-Comp Store Sales | 7,892 | 7,326 | 5,906 | 4,783 | 4,877 | |||||||||||||||

| Total Revenue | $ | 29,353 | $ | 33,895 | $ | 37,347 | $ | 38,843 | $ | 43,820 | ||||||||||

XpresSpa believes that its operating metrics represent an attractive return on invested capital and, as a result, is pursuing new locations at airports and terminals around the country. Historically, XpresSpa has won approximately four out of every five requests for proposal (“RFP”) in which it has participated.

Group Mobile

We acquired Group Mobile on October 15, 2015. Group Mobile provides total hardware solutions, including rugged laptops, tablets, and handheld computers. Group Mobile also markets rugged mobile printers, vehicle computer docking and mounting gear, power accessories, wireless communication products, antennas, carrying cases and other peripherals, accessories and add-ons needed to maximize productivity in a mobile- or field-computing environment. Group Mobile’s professional service offerings are evolving into project lifecycle services including technology consultations, development and deployment, project and asset management, equipment installation, break-fix, hardware service technical support, 24-7 helpdesk and more.

Group Mobile is aggressively pursuing sales of Law Enforcement In-Vehicle “Video and Body-Worn” camera solutions to meet the complex mobile technology demands of thousands of law enforcement agencies and officers in the United States market. Key to the Group Mobile long-term strategy is the complete professional services, post deployment services and lifecycle management of Group Mobile offerings to bring stability to the customer mobile technology platforms.

Group Mobile purchases rugged mobile computing equipment and complementary products from its primary distribution and manufacturing partners and sells them to enterprises, resellers, and retail customers. Our primary customers range from corporations to local governments, emergency first responders and healthcare organizations. We believe that the market for rugged mobile computing products is trending towards an increase in the volume of unit sales combined with declining unit prices as the business transitions from primarily being comprised of laptops to one primarily comprised of rugged tablets. As this transition has occurred, Group Mobile is seeing shortened product life cycles and industry specific devices for segments such as healthcare. Group Mobile sets sale prices based on the market supply and demand characteristics for each particular product. Group Mobile is highly dependent on the end-market demand for rugged mobile computing products, which is influenced by many factors including the introduction of new IT products by Original Equipment Manufacturers (“OEM”), replacement cycles for existing rugged mobile computing products, overall economic growth, local and state budgets, and general business activity.

Product costs represent the single largest expense and product inventory is one of the largest working capital investments for Group Mobile. Group Mobile’s primary suppliers include Synnex Corporation, Ingram Micro Inc., Xplore Technologies Corporation, and Motion Computing, which, combined, represent approximately 81% of Group Mobile’s inventory purchases. We have reseller agreements with most of our OEM and distribution partners. These agreements usually provide for nonexclusive resale and distribution rights. The agreements are generally short-term, subject to periodic renewal, and often contain provisions permitting termination by either our supplier or us without cause upon relatively short notice. Furthermore, product procurement from the OEM suppliers is a highly complex process and, as such, efficient and effective purchasing operations are critical to Group Mobile’s success.

7

FLI Charge

FLI Charge is an early stage company that designs, develops, licenses, manufactures and markets power transfer and charging solutions. FLI Charge is currently working with partners in several verticals to bring products to market. These verticals include education, office, hospitality, power tools, automotive and consumer electronics, among others.

The FLI Charge ecosystem consists of powered surfaces and enablement chips that seamlessly transfer power to electronic devices. FLI Charge surfaces are connected to a power source or battery. The surfaces have conductive contact strips that provide power and are constantly monitored by control circuitry that immediately halts power transfer if an unapproved load or short-circuit condition is detected. FLI Charge-enabled devices are embedded with the FLI Charge contact enablement that consists of four contact points, known as the FLI Charge “constellation.” The constellation is designed to make an immediate and continuous electrical connection with the contact strips regardless of the device’s position or orientation on the surface. The enablement monitors the power coming from the surface and ensures that the correct amount of power goes to the device. Once an approved FLI Charge device is placed on a surface, power is transferred immediately to charge or power the device.

There are several competing charging technologies on the market or under development today. The most popular competing technology is inductive wireless charging, in which magnetic induction uses a magnetic coil to create resonance, which can transmit energy over a relatively short distance. The amount of power delivered is a function of the size of the coils, and the coils must be aligned and paired within a typical distance of less than one inch. Products utilizing magnetic induction have been available for 10+ years in products such as rechargeable electronic toothbrushes and pace makers. The leading inductive technologies deliver a maximum of 20 watts. Other competing technologies include magnetic resonance, RF harvesting, laser and ultrasound.

FLI Charge launched its consumer product line on Indiegogo, a crowdfunding platform, on June 15, 2016; the campaign was completed on August 15, 2016. FLI Charge delivered products to the participants in the fourth quarter of 2016.

Intellectual Property

Our intellectual property operating segment is engaged in the innovation, development and monetization of intellectual property. Our portfolio consists of patents and patent applications covering ad-insertion, wireless power, and mobile technologies.

We are currently focused on monetizing our technology portfolio through a variety of value enhancing initiatives including, but not limited to, licensing, litigation and strategic partnerships. We are currently asserting patents in litigation related to ad-insertion and remote monitoring.

Recent Developments

XpresSpa Acquisition

On August 8, 2016, we signed an agreement to acquire XpresSpa. On December 23, 2016, we completed the acquisition of XpresSpa for a total purchase consideration of $37,400,000, which includes:

| (a) | $1,734,000 in cash which was invested on August 8, 2016. |

| (b) | 2,500,000 shares of FORM common stock, par value $0.01 per share (“FORM Common Stock”). |

| (c) | 494,792 shares of our newly designated Series D Convertible Preferred Stock, par value $0.01 per share, (“FORM Preferred Stock”) with an aggregate initial liquidation preference of $23,750,000. |

8

Pursuant to the terms of the agreement governing the XpresSpa acquisition, in February 2017, in view of unexpected expenses, the parties mutually agreed to reduce the purchase price consideration and, as a result, the total number of shares of FORM Preferred Stock was decreased from 494,792 shares to 491,427 shares with an aggregate initial liquidation preference of $23,588,000, which are initially convertible into 3,931,416 shares of FORM Common Stock, at a conversion price of $6.00 per share. Each holder of FORM Preferred Stock shall be entitled to vote on an as converted basis.

| (d) | Five-year warrants to purchase 2,500,000 shares of FORM Common Stock, at an exercise price of $3.00 per share, each subject to adjustment in the event of a stock split, dividend or similar events. |

230,208 shares of FORM Preferred Stock, with an estimated fair value of $11,050,000, were placed into an escrow that will be subject to release over an 18 month period once certain conditions are satisfied. The escrow will be used to obtain necessary lease consents from the airports and to cover potential liabilities that may arise after the acquisition, but pertain to the activities before the acquisition.

The FORM Preferred Stock is senior to the FORM Common Stock and the terms of the FORM Preferred Stock contain no restrictions on our ability to issue additional senior preferred securities or our ability to issue additional preferred securities in the future. We have the right, but not the obligation, upon ten trading days’ notice to convert the outstanding shares of FORM Preferred Stock into FORM Common Stock at the then applicable conversion ratio, at any time or from time to time, if the volume weighted average price per share of the FORM Common Stock exceeds $9.00 for over any 20 days in a 30 consecutive trading day period. The term of the FORM Preferred Stock is seven years, after which time we can repay the holders in shares of FORM Common Stock or cash at our election. If we elect to make a payment, or any portion thereof, in shares of FORM Common Stock, the number of shares deliverable (the “Base Shares”) will be based on the volume weighted average price per share of the FORM Common Stock for the 30 trading days prior to the date of calculation (the “Base Price”) plus an additional number of shares of FORM Common Stock (the “Premium Shares”), calculated as follows: (i) if the Base Price is greater than $9.00, no Premium Shares shall be issued, (ii) if the Base Price is greater than $7.00 and equal to or less than $9.00, an additional number of shares equal to 5% of the Base Shares shall be issued, (iii) if the Base Price is greater than $6.00 and equal to or less than $7.00, an additional number of shares equal to 10% of the Base Shares shall be issued, (iv) if the Base Price is greater than $5.00 and equal to or less than $6.00, an additional number of shares equal to 20% of the Base Shares shall be issued and (v) if the Base Price is less than or equal to $5.00, an additional number of shares equal to 25% of the Base Shares shall be issued. The FORM Preferred Stock will accrue interest at 9% per annum.

Assignment of Infrastructure Patent Portfolio

On December 5, 2016, we entered into an agreement with Nokia Corporation (“Nokia”) to assign Nokia rights related to certain patents previously purchased from Nokia. The carrying value of the patents assigned to Nokia prior to the agreement was $1,186,000, which offset the $1,750,000 of royalty payable and resulted in a gain of $564,000 on the disposal of assets, which is included in general and administrative expense in the consolidated statements of operations and comprehensive loss. We retained selected patents previously purchased from Nokia with a carrying value of $50,000 as of December 31, 2016 that are no longer subject to any royalty payments to Nokia.

Senior Secured Notes

As of December 31, 2016, we no longer had an outstanding balance for our Senior Secured Convertible Notes (the “Notes”), as the Notes were repaid in full during the year. The details of our significant transactions during 2016 pertaining to the Notes are described below.

On March 9, 2016, we and the holders (the “Investors”) of our $12,500,000 Notes, which we originally issued in a registered direct offering on May 4, 2015, entered into an exchange note agreement (the “Exchange Note Agreement”). Pursuant to the Exchange Note Agreement, we issued to the Investors an aggregate of 703,644 shares of our common stock, par value $0.01 per share, in exchange for the reduction of $1,267,000 of the outstanding aggregate principal amount of the Notes and $49,000 of accrued interest. As a result, the outstanding aggregate principal amount under the Notes was reduced from $3,016,000 to $1,749,000 as of March 9, 2016.

9

In addition, on March 9, 2016, with the consent of each of the Investors, we agreed to amend the Notes. Pursuant to the Amended and Restated Senior Secured Notes (the “Amended Notes”) and the Indenture dated May 4, 2015, as supplemented by a First Supplemental Indenture dated May 4, 2015 and further supplemented by a Second Supplemental Indenture (the “Second Supplemental Indenture”) dated March 9, 2016: (i) the Amended Notes are no longer convertible into shares of our common stock and are payable by us on the Maturity Date (as defined below) in cash only, (ii) the Maturity Date of the Amended Notes was extended to June 30, 2017 (the “Maturity Date”), (iii) we discontinued the payment of principal prior to the Maturity Date (subject to certain exceptions), (iv) the interest rate increased from 8% to 10% per annum and accrues on the outstanding aggregate principal amount of the Amended Notes, payable monthly, and (v) we will pay to the Investors on the Maturity Date 102% of the outstanding aggregate principal amount of the Amended Notes. We also agreed to maintain a cash balance (including cash equivalents) of not less than $2,900,000.

We also agreed to reduce the exercise price of the warrants to purchase an aggregate of 537,500 shares of our common stock pursuant to the initial agreement (the “May 2015 Warrants”) from $10.00 to $3.00 per share and we agreed to remove from the May 2015 Warrants certain anti-dilution features. Other terms of the May 2015 Warrants remained the same. Furthermore, in connection with the Amended Notes, we paid a restructuring fee of $50,000 to the Investors.

On July 1, 2016, we repaid in full the Amended Notes that were due on June 30, 2017, including a 15% fee for early repayment. We used an aggregate of $2,011,000 of cash on hand for repayment of the Amended Notes. As a result of the repayment in full of the Amended Notes, all liens on our assets, including intellectual property, were released by the Investors.

Impairment of Patents

Our name change and repositioning as a holding company was deemed a triggering event, which required our patent assets to be tested for impairment. In performing this impairment test, we determined that the patent portfolios, which together represent an asset group, were subject to impairment testing. In the first step of the impairment test, we utilized our projections of future undiscounted cash flows based on our existing plans for the patents. As a result, it was determined that our projections of future undiscounted cash flows were less than the carrying value of the asset group. Accordingly, we performed the second step of the impairment test to measure the potential impairment by calculating the asset group’s fair value as of May 6, 2016. As a result, following amortization for the month of April, we recorded an impairment charge of $11,937,000, which resulted in a new carrying value of $1,526,000 on May 6, 2016. Following the impairment, we reevaluated the remaining useful life of the patent assets and concluded that there were no changes.

Stockholder Rights Plan

On March 18, 2016, we announced that our Board of Directors adopted a stockholder rights plan in the form of a Section 382 Rights Agreement designed to preserve our tax assets. As a part of the plan, our Board of Directors declared a dividend of one preferred-share-purchase right for each share of our common stock outstanding as of March 29, 2016. Effective on March 18, 2016, if any group or person acquires 4.99% or more of our outstanding shares of common stock, or if a group or person that already owns 4.99% or more of our common stock acquires additional shares representing 0.5% or more of our common stock, then, subject to certain exceptions, there would be a triggering event under the plan. The rights would then separate from our common stock and would be adjusted to become exercisable to purchase shares of our common stock having a market value equal to twice the purchase price of $9.50, resulting in significant dilution in the ownership interest of the acquiring person or group. Our Board of Directors has the discretion to exempt any acquisition of our common stock from the provisions of the plan and has the ability to terminate the plan prior to a triggering event. In connection with this plan, we filed a Certificate of Designation of Series C Junior Preferred Stock with the Secretary of State of Delaware on March 18, 2016.

10

Reverse Stock Split

Unless otherwise noted, the information contained in these consolidated financial statements gives effect to a one-for-ten reverse stock split of our common stock effected on November 27, 2015 (the “Reverse Stock Split”) on a retroactive basis for all periods presented.

Competition

Each of our four reporting segments operates in different competitive environments.

XpresSpa

XpresSpa operates 53 locations, which includes 49 domestic locations and four international locations. Our domestic units operate within many of the largest and most heavily trafficked airports in the United States. The competitive landscape for wellness service providers in airports consists of approximately 110 spas across North America. XpresSpa’s 49 domestic units represent approximately 45% of the total North American market. The balance of the North American market is highly fragmented and is represented largely by small, privately-owned entities that operate one or two locations in a single airport. Only three other market participants operate 10 or more airport locations in the United States. The largest domestic competitor operates 18 locations in eight airports. Outside of North America, this same competitor operates 18 locations in seven international airports.

Group Mobile

Our rugged devices reselling business is regionally focused with the majority of our customers having direct relationships with local sales staff. Most competitors are private companies that have limited infrastructure. We believe that our key competitive advantages are knowledge, service and breadth of products relative to these competitors. As we grow the business, we also believe that we will be able to further improve our service and overall shopping experience.

FLI Charge

There are several competing wire-free power and charging technologies on the market or under development today. The most popular competing technology is inductive wireless charging, in which magnetic induction uses a magnetic coil to create resonance, which can transmit energy over very short distances. Power is delivered as a function of coil size, and coils must be directly paired within a typical distance of less than one inch. Products utilizing magnetic induction have been available for 10+ years and include rechargeable electronic toothbrushes and pace makers. Other competing technologies include magnetic resonance, RF harvesting, laser and ultrasound. Most competitors utilize these competing technologies and not our technology.

As compared to each of the competing wireless technologies above, we believe that our conductive technology exhibits many competitive advantages including:

| • | charge rates/efficiency – FLI Charge pads charge devices nearly as fast as plugging them into a wall outlet; |

| • | multiple devices – FLI Charge pads can charge or power multiple devices at the same time without reducing the charging speed; |

| • | safety – FLI Charge’s technology is as safe as plugging devices into a wall outlet; |

| • | maximum power – FLI Charge pads can supply as much as 150 watts of power, which is enough to charge or power devices with relatively high power requirements such as power tool batteries and flat screen monitors; |

11

| • | positioning freedom – FLI Charge’s technology allows for devices to be placed in any orientation, anywhere on the pad, without sacrificing any charging speed; and |

| • | compatibility – all FLI Charge enabled electronic devices are compatible with all FLI Charge pads. |

Intellectual Property

After a period of intense competition from public and private companies for the acquisition of intellectual property assets, prices have dropped substantially. Due to the many patent sales and divestments over the past few years, many companies continue to seek to monetize intellectual property by licensing their patents to companies in a number of technology sectors. This has occurred in an increasingly challenging and changing legal environment for monetizing patents. Relatively new procedures at the United States Patent and Trademark Office as well as the anticipation of the Unified European Patent Court have created uncertainty as to the value of patent assets.

Employees

As of March 15, 2017, we and our subsidiaries had 673 full-time and 90 part-time employees. XpresSpa had 58 full-time employees in San Francisco International Airport, who are represented by a labor union and are covered by a collective bargaining agreement. XpresSpa had 25 full-time employees in Los Angeles International Airport, who are represented by a labor union and, starting in March 2017, will be covered by a collective bargaining agreement. We consider our relationships with our employees to be good.

Our Company

We were incorporated in Delaware as a corporation on January 9, 2006 and completed an initial public offering in June 2010. On May 6, 2016, we changed our name to FORM Holdings Corp. from Vringo Inc. and concurrently announced our repositioning as a holding company of small and middle market growth companies. Our common stock, par value $0.01 per share, which was previously listed on The NASDAQ Capital Market under the trading symbol “VRNG,” has been listed under the trading symbol “FH” since May 9, 2016. Our principal executive offices are located at 780 Third Avenue, 12th Floor, New York, New York 10017. Our telephone number is (212) 309-7549 and our website address is www.formholdings.com. We also operate the following websites: www.xpresspa.com, www.groupmobile.com and www.flicharge.com. References in this Annual Report on Form 10-K to these website addresses do not constitute incorporation by reference of the information contained on the website. We make our filings with the Securities and Exchange Commission, or the SEC, including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, other reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, and amendments to the foregoing reports, available free of charge on or through our website as soon as reasonably practicable after we file these reports with, or furnish such reports to, the SEC. In addition, we post the following information on our website:

| • | our corporate code of conduct and our insider trading compliance manual; and |

| • | charters for our audit committee, compensation committee, and nominating and corporate governance committee. |

The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers, including us, that file electronically with the SEC. The public can obtain any documents that we file with the SEC at http://www.sec.gov.

12

Our business, financial condition, results of operations and the trading price of our common stock could be materially adversely affected by any of the following risks as well as the other risks highlighted elsewhere in this Annual Report on Form 10-K. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may materially affect our business, financial condition and results of operations.

Risks Related to our Financial Condition and Capital Requirements

We may not be able to raise additional capital. Moreover, additional financing may have an adverse effect on the value of the equity instruments held by our stockholders.

We may choose to raise additional funds in connection with any potential acquisition of operating businesses or other assets. In addition, we may also need additional funds to respond to business opportunities and challenges, including our ongoing operating expenses, protection of our assets, development of new lines of business and enhancement of our operating infrastructure. While we may need to seek additional funding, we may not be able to obtain financing on acceptable terms, or at all. In addition, the terms of our financings may be dilutive to, or otherwise adversely affect, holders of our common stock. We may also seek additional funds through arrangements with collaborators or other third parties. We may not be able to negotiate arrangements on acceptable terms, if at all. If we are unable to obtain additional funding on a timely basis, we may be required to curtail or terminate some or all of our business plans. Any such financing that we undertake will likely be dilutive to our current stockholders.

Global economic conditions may cause counterparties to our negotiations to delay entering into licensing agreements, product purchase agreements or other business arrangements, which could adversely affect our business, financial condition and operating results.

Our business plan depends significantly on worldwide economic conditions, and the United States and world economies have recently experienced fluctuating economic conditions. Uncertainty about global economic conditions poses a risk as businesses may postpone spending in response to tighter credit, negative financial news and declines in income or asset values. This response could have a material negative effect on the willingness of parties to enter into revenue generating agreements in a timely manner. Entering into such agreements is critical to our business plan, and our failure to do so could cause material harm to our business, financial condition and results of operations.

Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited.

As of December 31, 2016, we had federal net operating loss carryforwards (“NOL”s) of $138,915,000 which expire 20 years from the respective tax years to which they relate. Our ability to utilize our NOLs may be limited under Section 382 of the Internal Revenue Code. The limitations apply if an ownership change, as defined by Section 382, occurs. Generally, an ownership change occurs when certain shareholders increase their aggregate ownership by more than 50 percentage points over their lowest ownership percentage in a testing period (typically three years). Additionally, United States tax laws limit the time during which these carryforwards may be utilized against future taxes. As a result, we may not be able to take full advantage of these carryforwards for federal and state tax purposes. Future changes in stock ownership may also trigger an ownership change and, consequently, a Section 382 limitation.

13

Risks Related to our Merger with XpresSpa (the “Merger”)

We may not realize the potential value and benefits created by the Merger.

The success of the Merger will depend, in part, on our ability to realize the expected potential value and benefits created from integrating our existing businesses with XpresSpa’s business, which includes the maximization of the economic benefits of our strategic vision and plans, cash balances (which, in the case of XpresSpa, would be used for the build-out of new airport locations), financial reporting and analysis functions and legal expertise. The integration process may be complex, costly, and time-consuming. The difficulties of integrating the operations of XpresSpa’s business could include, among others:

| · | failure to implement our business plan; |

| · | unanticipated issues in integrating the business of both companies; |

| · | loss of key employees with knowledge of our or XpresSpa’s historical business and operations; |

| · | unanticipated changes in applicable laws and regulations; and |

| · | other unanticipated issues, expenses, or liabilities that could impact, among other things, our ability to realize any expected benefits on a timely basis, or at all. |

We may not accomplish the integration of XpresSpa’s business smoothly, successfully, or within the anticipated costs or time frame. The diversion of the attention of management from our current operations to the integration effort and any difficulties encountered in combining businesses could prevent us from realizing the full expected potential value and benefits to result from the Merger and could adversely affect our business. In addition, the integration efforts could divert our and XpresSpa’s focus and resources from other strategic opportunities and operational matters during the integration process. We are dependent on certain key personnel, and the loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations. Our success and future prospects largely depend on the skills, experience and efforts of our and XpresSpa’s key personnel, including Andrew D. Perlman, our current Chief Executive Officer and Director, and Edward Jankowski, XpresSpa’s Chief Executive Officer. The loss of Mr. Perlman or Mr. Jankowski or other of our or XpresSpa’s executives, or our failure to retain other key personnel, would jeopardize our ability to execute our strategic plan and materially harm our business.

Our success will depend in part on relationships with third parties, which relationships may be affected by third-party preferences or public attitudes about the Merger. Any adverse changes in these relationships could adversely affect our business, financial condition, or results of operations.

Our success is dependent on our ability to maintain and renew our and XpresSpa’s business relationships and to establish new business relationships. There can be no assurance that our management will be able to maintain such business relationships, or enter into or maintain new business contracts and other business relationships, on acceptable terms, if at all. The failure to maintain important business relationships could have a material adverse effect on our business, financial condition, or results of operations.

14

Our business and financial condition could be constrained by XpresSpa’s outstanding debt.

XpresSpa is obligated under the Senior Secured Note payable to Rockmore Investment Master Fund Ltd. (“Rockmore”), a related party, which has an outstanding balance of approximately $6,500,000, with a maturity date of May 1, 2018, with an additional one-year extension if both we and Rockmore consent to such extension. The Senior Secured Note accrues interest of 11.24% per annum. XpresSpa has granted Rockmore a security interest in all of its tangible and intangible personal property to secure its obligations under the Senior Secured Note. After the completion of the Merger the debt remains outstanding as an obligation of XpresSpa, but is guaranteed by us.

Material weaknesses may exist when we report on the effectiveness of our internal controls over financial reporting for purposes of our reporting requirements.

Prior to the Merger, XpresSpa, as a private company, was not subject to Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”). Therefore, XpresSpa’s management and independent auditors were not required to perform an evaluation of XpresSpa’s internal controls over financial reporting as of December 31, 2015 in accordance with the provisions of Sarbanes-Oxley. We are required to provide management’s report on internal control over financial reporting in our Annual Report on Form 10-K, as required by Section 404 of Sarbanes-Oxley. We have not yet assessed the effectiveness of the internal controls for XpresSpa; however, we are not currently aware of any negative indicators.

Because the lack of a public market for XpresSpa’s units makes it difficult to evaluate the fairness of the Merger, XpresSpa’s equity holders may have received or receive consideration in the Merger that is greater than or less than the fair market value of XpresSpa’s units.

The outstanding equity of XpresSpa is privately held and is not traded in any public market. The lack of a public market makes it difficult to determine the fair market value of XpresSpa. Since the amount of our common stock, preferred stock and warrants to be issued to XpresSpa’s equity holders was determined based on negotiations between the parties, it is possible that the value of our common stock, preferred stock and warrants issued or to be issued in connection with the Merger will be greater than the fair market value of XpresSpa. Alternatively, it is possible that the value of the shares of our common stock, preferred stock and warrants issued or to be issued in connection with the Merger will be less than the fair market value of XpresSpa.

The issuance of our securities to XpresSpa equity holders in connection with the Merger diluted the voting power of our current stockholders.

Pursuant to the terms of the Merger Agreement, we issued to XpresSpa unit holders shares of our common stock and warrants to purchase shares of our common stock, and have issued shares of our preferred stock thereto. Without taking into account any shares of our common stock held by XpresSpa equity holders prior to the completion of the Merger but assuming that all shares held in escrow are released to the former equity holders of XpresSpa, the former equity holders of XpresSpa own approximately 18% of our outstanding common stock (or 33% of our outstanding common stock calculated on a fully diluted basis) and our stockholders prior to the Merger own approximately 82% of our outstanding common stock (or 67% of our outstanding common stock calculated on a fully diluted basis). In addition, the holders of our preferred stock have certain voting rights as specified in the Certificate of Designation of Preferences, Rights and Limitations of FORM Preferred Stock. Accordingly, the issuance of shares of our common stock and our preferred stock to XpresSpa equity holders in connection with the Merger reduced the relative voting power of each share of our common stock held by our current stockholders.

15

If we exercise the option to repay the preferred stock issued in connection with the Merger in stock rather than cash, such repayment may result in the issuance of a large number of shares of common stock which may have a negative effect on the trading price of our common stock as well as a dilutive effect.

Pursuant to the terms of the FORM Preferred Stock issued in connection with the Merger, on the seven-year anniversary of the initial issuance date of the shares of FORM Preferred Stock, December 23, 2024, we may repay each share of FORM Preferred Stock, at our option, in cash, by delivery of shares of common stock or through any combination thereof. If we elect to make a payment, or any portion thereof, in shares of common stock, the number of shares deliverable (the “Base Shares”) will be based on the volume weighted average price per share of our common stock for the thirty trading days prior to the date of calculation (the “Base Price”) plus an additional number of shares of common stock (the “Premium Shares”), calculated as follows: (i) if the Base Price is greater than $9.00, no Premium Shares shall be issued, (ii) if the Base Price is greater than $7.00 and equal to or less than $9.00, an additional number of shares equal to 5% of the Base Shares shall be issued, (iii) if the Base Price is greater than $6.00 and equal to or less than $7.00, an additional number of shares equal to 10% of the Base Shares shall be issued, (iv) if the Base Price is greater than $5.00 and equal to or less than $6.00, an additional number of shares equal to 20% of the Base Shares shall be issued and (v) if the Base Price is less than or equal to $5.00, an additional number of shares equal to 25% of the Base Shares shall be issued. Accordingly, if the volume weighted average price per share of our common stock is below $9.00 per share as of the time of repayment and we exercise the option to make such repayment in shares of our common stock, a large number of shares of our common stock may be issued to the holders of the FORM Preferred Stock upon maturity which may have a negative effect on the trading price of our common stock. At the seven year maturity date of the FORM Preferred Stock (which shall be the date that is seven years from the closing date of the Merger), we, at our election, may decide to issue shares of our common stock based on the formula set forth above or to re-pay in cash all or any portion of the FORM Preferred Stock.

On December 23, 2023, upon the maturity of the FORM Preferred Stock, when determining whether to repay the FORM Preferred Stock in cash or shares of common stock, we expect to consider a number of factors, including our cash position, the price of our common stock and our capital structure at such time. Because we do not have to make a determination as to which option to elect until 2023, it is impossible to predict whether it is more or less likely to repay in cash, stock or a portion of each.

The price of our common stock after the Merger may be affected by factors different from those which affected our shares prior to the Merger.

Our business differs from the business of XpresSpa and, accordingly, our results of operations and the trading price of our common stock following the completion of the Merger may be significantly affected by factors different from those that affected our independent results of operations, as we now conduct activities not undertaken by us prior to the Merger.

16

If any of the events described in ‘‘Risks Related to our Merger with XpresSpa or ‘‘Risks Related to our Business Operations’’ regarding XpresSpa occur, those events could cause the potential benefits of the Merger not to be realized.

Following the completion of the Merger, our current executive officers and certain XpresSpa executive officers and our directors and certain XpresSpa directors direct our business and operations. Additionally, XpresSpa’s business is expected to be an important part of our business following the Merger. As a result, the risks described below in the sections entitled ‘‘Risks Related to our Merger with XpresSpa” or “Risks Related to our Business Operations” regarding XpresSpa herein are among our significant risks. To the extent any of the events described below in either section occur, those events could cause the potential benefits of the Merger not to be realized and the market price of our common stock to decline.

Risks Related to our Business Operations

Future acquisitions or business opportunities could involve unknown risks that could harm our business and adversely affect our financial condition and results of operations.

We strive to be a diversified holding company that owns interests in a number of different businesses. We have in the past, and may in the future, acquire businesses or make investments, directly or indirectly through our subsidiaries, that involve unknown risks, some of which will be particular to the industry in which the investment or acquisition targets operate, including risks in industries with which we are not familiar or experienced. Although we intend to conduct appropriate business, financial and legal due diligence in connection with the evaluation of future investment or acquisition opportunities, there can be no assurance that our due diligence investigations will identify every matter that could have a material adverse effect on us. We may be unable to adequately address the financial, legal and operational risks raised by such investments or acquisitions, especially if we are unfamiliar with the relevant industry. The realization of any unknown risks could expose us to unanticipated costs and liabilities and prevent or limit us from realizing the projected benefits of the investments or acquisitions, which could adversely affect our financial condition, liquidity, results of operations, and trading price.

We may be unsuccessful in identifying suitable acquisition candidates, which may negatively impact our growth strategy.

There can be no assurance given that we will be able to implement our strategy and identify suitable acquisition candidates or consummate future acquisitions on acceptable terms. Our failure to successfully identify suitable acquisition candidates or consummate future acquisitions on acceptable terms could have an adverse effect on our prospects, business activities, cash flow, financial condition, results of operations and stock price.

Anti-takeover provisions of Delaware law, provisions in our charter and bylaws and our stockholder rights plan could prevent or frustrate attempts by stockholders to change our board of directors or current management and could make a third-party acquisition of control of us difficult.

We are a Delaware corporation and, as such, certain provisions of Delaware law could prevent or frustrate attempts by stockholders to change the board of directors or current management, or could delay, discourage or make more difficult a third-party acquisition of control of us, even if the change in control would be beneficial to stockholders or the stockholders regard it as such. We are subject to the provisions of Section 203 of the DGCL, which prohibits certain “business combination” transactions (as defined in Section 203) with an “interested stockholder” (defined in Section 203 as a 15% or greater stockholder) for a period of three years after a stockholder becomes an “interested stockholder,” unless the attaining of “interested stockholder” status or the transaction is pre-approved by our Board of Directors, the transaction results in the attainment of at least an 85% ownership level by an acquirer or the transaction is later approved by our Board of Directors and by our stockholders by at least a 66 2/3 percent vote of our stockholders other than the “interested stockholder,” each as specifically provided in Section 203. We have also adopted a shareholder rights plan in the form of the Rights Agreement, designed to help protect and preserve our substantial tax attributes primarily associated with our NOLs and research tax credits under Sections 382 and 383 of the Internal Revenue Code and related United States Treasury regulations. Although this is not the purpose of the Rights Agreement, it could have the effect of making it uneconomical for a third party to acquire us on a hostile basis.

17

These provisions of the DGCL, our certificate of incorporation and bylaws, and the Rights Agreement may delay, discourage or make more difficult certain types of transactions in which our stockholders might otherwise receive a premium for their shares over the current market price, and might limit the ability of our stockholders to approve transactions that they think may be in their best interest.

Our confidential information may be disclosed by other parties.

We routinely enter into non-disclosure agreements with other parties, including but not limited to vendors, law firms, parties with whom we are engaged in negotiations, and employees. However, there exists a risk that those other parties will not honor their contractual obligations to not disclose our confidential information. This may include parties who breach such obligations in the context of confidential settlement offers and/or negotiations. In addition, there exists a risk that, upon such breach and subsequent dissemination of our confidential information, third parties and potential licensees may seek to use such confidential information to their advantage and/or to our disadvantage including in legal proceedings in which we are involved. Our ability to act against such third parties may be limited, as we may not be in privity of contract with such third parties.

We and our subsidiaries have been, are, and may become involved in litigation that could divert management’s attention and harm our businesses.

Litigation often is expensive and diverts management’s attention and resources, which could adversely affect our businesses. We may be exposed to claims against us even if no wrongdoing has occurred. Responding to such claims, regardless of their merit, can be time-consuming, costly to defend, disruptive to our management’s attention and to our resources, damaging to our reputation and brand, and may cause us to incur significant expenses. Even if we are indemnified against such costs, the indemnifying party may be unable to uphold its contractual obligations.

XpresSpa is reliant on international and domestic airplane travel, and the time that airline passengers spend in United States airports post-security. A decrease in airline travel, a decrease in the desire of customers to buy spa services and products, or decreased time spent in airports would negatively impact XpresSpa’s revenues.

XpresSpa depends upon a large number of airplane travelers with the psychographic propensity for health and wellness, and in particular spa treatments and products, spending significant time post-Transportation Security Administration (“TSA”) security clearance check points.

If the number of airline travelers in the United States decreases, if the time that these travelers spend post-TSA security decreases, and/or if travelers ability or willingness to pay for XpresSpa’s products and services diminishes, this could have an adverse effect on XpresSpa’s growth, business activities, cash flow, financial condition and results of operations. Some reasons for these events could include:

| • | terrorist activities impacting either domestic or international travel through airports where XpresSpa operates, causing fear of flying, flight cancellations, or an economic downturn; |

| • | a decrease in business spending that impacts business travel, such as a recession; |

| • | a decrease in consumer spending that impacts United States leisure travel, such as a recession or a stock market downturn or a change in consumer lending regulations impacting available credit for leisure travel; |

| • | an increase in airfare prices that impacts the willingness of United States air travelers to fly, such as an increase in oil prices or heightened taxation from federal or other aviation authorities; |

| • | an increase in airplane accident rates, causing United States travelers to decrease the amount that they fly; |

18

| • | scientific studies that malign the use of spa services or the products used in spa services, such as the impact of certain chemicals and procedures on health and wellness; or |

| • | streamlined TSA security screening checkpoints, which could decrease the wait time at checkpoints and therefore the time air travelers budget for spending time at the airport. |

XpresSpa’s operating results may fluctuate significantly due to certain factors, some of which are beyond its control.

XpresSpa’s operating results may fluctuate from period to period significantly because of several factors, including:

| • | the timing and size of new unit openings, particularly the launch of new terminals; |

| • | passenger traffic and seasonality of air travel; |

| • | changes in the price and availability of supplies; |

| • | macroeconomic conditions, both nationally and locally; |

| • | changes in consumer preferences and competitive conditions; |

| • | expansion to new markets and new locations; and |

| • | increases in infrastructure costs including those costs associated with the build-out of new concession locations and renovating existing concession locations. |

XpresSpa’s operating results may fluctuate significantly as a result of the factors discussed above. Accordingly, results for any period are not necessarily indicative of results to be expected for any other period or for any year.

XpresSpa’s expansion into new airports may present increased risks due to its unfamiliarity with those areas.

XpresSpa’s growth strategy depends upon expanding into markets where it has little or no meaningful operating experience. Those locations may have demographic characteristics, consumer tastes and discretionary spending patterns that are different from those in the markets where its existing operations are located. As a result, new airport terminal operations may be less successful than its concession locations in its current airport terminals. XpresSpa may find it more difficult in new markets to hire, motivate and keep qualified employees who can project its vision, passion and culture. XpresSpa may also be unfamiliar with local laws, regulations and administrative procedures, including the procurement of spa services retail licenses, in new markets which could delay the build-out of new concession locations and prevent it from achieving its target revenues on a timely basis. Operations in new markets may also have lower average revenues or enplanements than in the markets where XpresSpa currently operates. Operations in new markets may also take longer to ramp up and reach expected sales and profit levels, and may never do so, thereby negatively affecting XpresSpa’s results of operations.

XpresSpa currently relies on a skilled, licensed labor force to provide spa services, and the supply of this labor force is finite. If XpresSpa cannot hire adequate staff for its locations, it will not be able to operate.

XpresSpa has approximately 720 employees in its locations. Excluding some dedicated retail staff, the majority of these employees are licensed to perform spa services, and hold such licenses as masseuses, nail technicians, aestheticians, barbers and master barbers. The demand for these licensed technicians has been increasing as more consumers gravitate to health and wellness treatments such as spa services. XpresSpa competes not only with other airport-based spa companies but with spa companies outside of the airport for this skilled labor force. In addition, all staff hired by XpresSpa must pass the background checks and security clearances necessary to work in airport locations. If XpresSpa is unable to attract and retain qualified staff to work in its airport locations, its ability to operate will be impacted negatively.

19

XpresSpa’s labor force could unionize, putting upward pressure on labor costs.

Currently, two XpresSpa locations have a labor force which is unionized. Major players in labor organization, and in particular “Unite Here!” which represents 33,000 employees in the airport concessions and airline catering industries, could target XpresSpa locations for its unionization efforts. In the event of the successful unionization of all of XpresSpa’s labor force, XpresSpa would likely incur additional costs in the form of higher wages, more benefits such as vacation and sick leave, and potentially also higher health care insurance costs.

XpresSpa competes for new locations in airports, and may not be able to secure new locations.

XpresSpa participates in the highly competitive and lucrative airport concessions industry, and as a result competes for retail leases with a variety of larger, better capitalized concessions companies as well as smaller, mid-tier and single unit operators. Frequently, an airport includes a spa concept within its retail product set and, in those instances, XpresSpa competes primarily with BeRelax, Terminal Getaway, Massage Bar and 10 Minute Manicure.

XpresSpa’s leases may be terminated, either for convenience by the landlord or as a result of an XpresSpa default.

XpresSpa has store locations and kiosks in a number of airports in which the landlord, with prior written notice to XpresSpa, can terminate XpresSpa’s lease, including for convenience or as necessary for airport purposes or operations. If a landlord elects to terminate a lease at an airport, XpresSpa may have to shut down one or more store locations at that airport.

Additionally, XpresSpa leases have numerous provisions governing the operation of XpresSpa’s stores. Violation of one or more of these provisions, even unintentionally, may result in the landlord finding that XpresSpa is in default of the lease. Violation of lease provisions may result in fines and, in some cases, termination of a lease.

XpresSpa’s ability to operate depends on the traffic patterns of the terminals in which it operates, and the cessation or disruption of air traveler traffic in these terminals would negatively impact XpresSpa’s addressable market.

XpresSpa depends on a high volume of air travelers in its terminals. It is possible that a terminal in which XpresSpa operates could become subject to a lower volume of air travelers, which would significantly impact traffic near and around XpresSpa locations and therefore its total addressable market. Lower volume in a terminal could be caused by:

| • | terminal construction that results in the temporary or permanent closure of a unit, or adversely impacts the volume or pattern of traffic flows within an airport; |

| • | an airline utilizing an airport in which XpresSpa operates could abandon that airport or an individual terminal in favor of other airports or terminals, or because it is contracting operations; or |

| • | adverse weather conditions could cause damage to the terminal or airport in which XpresSpa operates, resulting in the temporary or permanent closure of a unit. |

20

Failure to comply with minimum airport concession disadvantaged business enterprise participation goals and requirements could lead to lost business opportunities or the loss of existing business.

A number of XpresSpa’s leases contain minimum Airport Concession Disadvantaged Business Enterprise (“ACDBE”) participation requirements, and bidding on or submitting proposals for new concession contracts often requires that XpresSpa meets or uses good faith efforts to meet certain minimum ACDBE participation requirements. If XpresSpa fails to comply with the minimum ACDBE participation requirements, XpresSpa may be held responsible for a breach of contract, which could result in the termination of a lease and impairment of XpresSpa’s ability to bid on or obtain future concession contracts. To the extent that XpresSpa leases are terminated and XpresSpa is required to shut down one or more store locations, there could be a material adverse impact to its business and results of operations.

Continued minimum wage increases would negatively impact XpresSpa’s cost of labor.

XpresSpa compensates its licensed technicians via a formula that includes commissions. As a result, an increase in the minimum wage would increase XpresSpa’s cost of labor.

If XpresSpa is unable to protect its customers’ credit card data and other personal information, XpresSpa could be exposed to data loss, litigation and liability, and its reputation could be significantly harmed.

Privacy protection is increasingly demanding, and the use of electronic payment methods and collection of other personal information, including order history, travel history and other preferences, exposes XpresSpa to increased risk of privacy and/or security breaches as well as other risks. The majority of XpresSpa’s sales are by credit or debit cards. Additionally, XpresSpa collects and stores personal information from individuals, including its customers and employees.

XpresSpa may experience security breaches in which credit and debit card information or other personal information is stolen in the future. Although XpresSpa uses secure private networks to transmit confidential information, third parties may have the technology or know-how to breach the security of the customer information transmitted in connection with credit and debit card sales, and its security measures and those of technology vendors may not effectively prohibit others from obtaining improper access to this information. The techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and are often difficult to detect for long periods of time, which may cause a breach to go undetected for an extensive period of time. Advances in computer and software capabilities, new tools, and other developments may increase the risk of such a breach. Further, the systems currently used for transmission and approval of electronic payment transactions, and the technology utilized in electronic payments themselves, all of which can put electronic payment at risk, are determined and controlled by the payment card industry, not by XpresSpa. In addition, contractors, or third parties with whom XpresSpa does business or to whom XpresSpa outsources business operations may attempt to circumvent its security measures in order to misappropriate such information, and may purposefully or inadvertently cause a breach involving such information. If a person is able to circumvent XpresSpa’s security measures or those of third parties, he or she could destroy or steal valuable information or disrupt XpresSpa’s operations. XpresSpa may become subject to claims for purportedly fraudulent transactions arising out of the actual or alleged theft of credit or debit card information, and XpresSpa may also be subject to lawsuits or other proceedings relating to these types of incidents. Any such claim or proceeding could cause XpresSpa to incur significant unplanned expenses, which could have an adverse effect on its business or results of operations. Further, adverse publicity resulting from these allegations could significantly harm its reputation and may have a material adverse effect on it. Although XpresSpa carries cyber liability insurance to protect against these risks, there can be no assurance that such insurance will provide adequate levels of coverage against all potential claims.

Negative social media regarding XpresSpa could result in decreased revenues and impact XpresSpa’s ability to recruit workers.

XpresSpa’s affinity among consumers is highly dependent on their positive feelings about the brand, its customer service and the range and quality of services and products that it offers. A negative customer experience that is posted to social media outlets and is distributed virally could tarnish XpresSpa’s brand and its customers may opt to no longer engage with the brand.

21

XpresSpa employs people in multiple different jurisdictions, and the employment laws of those jurisdictions are subject to change. In addition, its services are regulated through government-issued operating licenses. Noncompliance with applicable laws could result in employee lawsuits or legal action taken by government authorities.

XpresSpa must comply with a variety of employment and business practices laws across the United States, Netherlands, and United Arab Emirates. XpresSpa monitors the laws governing its activities, but in the event it does not become aware of a new regulation or fails to comply with a regulation, it could be subject to disciplinary action by governing bodies and potentially employee lawsuits.

XpresSpa is not currently cash flow positive, and will depend on funding from us to open new locations. In the event that capital is unavailable from us, XpresSpa will not be able to open new locations.

Throughout its operating history, XpresSpa has not generated sufficient cash from operations to fund its new store development. As a result, it will be dependent upon us to fund its new location growth until such time as it can produce enough cash to profitably fund its own location growth.

XpresSpa sources, develops and sells products that may result in product liability defense costs and product liability payments.

The ingredients in XpresSpa’s products contain ingredients that are deemed to be safe by the United States Federal Drug Administration and the Federal Food, Drug and Cosmetics Act. However, there is no guarantee that these ingredients will not cause adverse health effects to some consumers given the wide range of ingredients and allergies amongst the general population. XpresSpa may face substantial product liability exposure for products it sells to the general public or that is uses in its services. Product liability claims, regardless of their merits, could be costly and divert management’s attention, and adversely affect XpresSpa’s reputation and the demand for its products and services. XpresSpa to date has not been named as a defendant in any product liability action.

The mobile and/or rugged computing industry is characterized by rapid technological change, and the success of Group Mobile depends upon the frequent enhancement of existing products and services and timely introduction of new products and services that meet Group Mobile’s customers’ needs.

Customer requirements for mobile computing products and services are rapidly evolving and technological changes in the industry occur rapidly. To keep up with new customer requirements and distinguish Group Mobile from its competitors in the business of reselling rugged devices, Group Mobile must frequently introduce new products and services and enhancements of existing products and services. Enhancing existing products and services and developing new products and services is a complex and uncertain process. Furthermore, Group Mobile may not be able to launch new or improved products or services before its competition launches comparable products or services. Any of these factors could cause Group Mobile’s business or results of operations to suffer.

Group Mobile depends on a small number of OEMs to supply the products and services that it sells and the loss of, or a material change in, a business relationship with a major OEM supplier, could adversely affect our operations, cash flow, and financial position.

Group Mobile’s future success is highly dependent on its relationships with a small number of OEM suppliers. Group Mobile’s primary suppliers include Synnex Corporation, Ingram Micro Inc., Xplore Technologies Corporation, and Motion Computing, which combined represent approximately 81% of Group Mobile’s inventory purchases. OEM supplier agreements typically are short-term and may be terminated without cause upon short notice. The loss or deterioration of our relationship with any of our major OEM suppliers, the authorization by OEM suppliers of additional distributors, the sale of products by OEM suppliers directly to our reseller and retail customers and end-users, or our failure to establish relationships with new OEM suppliers or to expand the distribution and supply chain services that we provide OEM suppliers could adversely affect our operations, cash flows, and financial position. In addition, OEM suppliers may face liquidity or solvency issues that in turn could negatively affect our operations, cash flows, and financial position.

22

Group Mobile’s and FLI Charge’s businesses depend upon their ability to keep pace with the latest technological changes and their failure to do so could make Group Mobile and FLI Charge less competitive in their respective industries.

The market for Group Mobile’s and FLI Charge’s products and services is characterized by rapid change and technological change, frequent new product innovations, changes in customer requirements and expectations and evolving industry standards. Products using new technologies or emerging industry standards could make Group Mobile’s and FLI Charge’s products and services less attractive. Furthermore, Group Mobile’s and FLI Charge’s competitors may have access to technology not available to Group Mobile and FLI Charge, which may enable them to produce products of greater interest to consumers or at a more competitive cost. Failure to respond in a timely and cost-effective way to these technological developments may result in serious harm to Group Mobile’s and FLI Charge’s businesses and operating results. As a result, Group Mobile’s and FLI Charge’s success will depend, in part, on their ability to develop and market product and service offerings that respond in a timely manner to the technological advances available to Group Mobile’s and FLI Charge’s customers, evolving industry standards and changing preferences.

If FLI Charge successfully commercially launches a product, and its product does not achieve widespread market acceptance, it will not be able to generate the revenue necessary to support its business.

Achieving acceptance of a wire-free recharging system as a preferred method to recharge fixed and mobile electronic devices will be crucial to FLI Charge’s continued success. Consumers and commercial customers will not begin to use or increase the use of FLI Charge’s product unless they agree that the convenience of its solution would be worth the additional expense of purchasing the FLI Charge system. FLI Charge has no history of marketing any product and it and its commercialization partners may fail to generate significant interest in the initial commercial products or any other product it or its partners may develop. These and other factors, including the following factors, may affect the rate and level of the market acceptance: