Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - Acushnet Holdings Corp. | golf-20161231ex322668f31.htm |

| EX-32.1 - EX-32.1 - Acushnet Holdings Corp. | golf-20161231ex32103e932.htm |

| EX-31.2 - EX-31.2 - Acushnet Holdings Corp. | golf-20161231ex3124952c6.htm |

| EX-31.1 - EX-31.1 - Acushnet Holdings Corp. | golf-20161231ex3116d0057.htm |

| EX-24.1 - EX-24.1 - Acushnet Holdings Corp. | golf-20161231ex241199151.htm |

| EX-23.1 - EX-23.1 - Acushnet Holdings Corp. | golf-20161231ex23138c82a.htm |

| EX-21.1 - EX-21.1 - Acushnet Holdings Corp. | golf-20161231ex21193b9c9.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☑ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

OR

◻TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934 for the transition period from to

Commission File Number: 001-37935

Acushnet Holdings Corp.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

45-5644353 |

|

(State or other jurisdiction of |

|

|

|

incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

333 Bridge Street

Fairhaven, Massachusetts 02719

(Address of principal executive offices)

(800) 225-8500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Name of each exchange on which registered |

|

Common Stock, par value $0.001 per share |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934. Yes ◻ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ◻

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ◻

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ◻ |

|

Accelerated filer ◻ |

|

Non-accelerated filer ☑ |

|

Smaller reporting company ◻ |

|

|

|

|

|

(Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No ☑

As of June 30, 2016, the last day of the registrant’s most recently completed second quarter, the registrant’s common stock was not publicly traded. The registrant's common stock, $0.001 par value per share, began trading on the New York Stock Exchange on October 28, 2016. As of March 24, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $623.5 million (based upon the closing sale price of the common stock on that date on the New York Stock Exchange).

The number of shares the Registrant's common stock outstanding on March 24, 2017 was 74,451,977.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A relating to the Registrant’s Annual General Meeting of Shareholders, to be held on June 12, 2017, will be incorporated by reference in this Form 10-K in response to Items 10, 11, 12, 13 and 14 of Part III. The definitive proxy statement will be filed with the SEC not later than 120 days after the registrant’s fiscal year ended December 31, 2016.

In this Annual Report on Form 10‑K, the terms “Acushnet,” “we,” “us,” “our” and the “Company” refer to Acushnet Holdings Corp. and its consolidated subsidiaries.

i

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10‑K contains “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which are subject to the “safe harbor” created by that section. These forward-looking statements are included throughout this report, including in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and relate to matters such as our industry, business strategy, goals and expectations concerning our market position, future operations, margins, profitability, capital expenditures, liquidity and capital resources and other financial and operating information. We have used the words “anticipate,” “assume,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “future,” “will,” “seek,” “foreseeable” and similar terms and phrases to identify forward-looking statements in this report.

The forward-looking statements contained in this report are based on management’s current expectations and are subject to uncertainty and changes in circumstances. We cannot assure you that future developments affecting us will be those that we have anticipated. Actual results may differ materially from these expectations due to changes in global, regional or local economic, business, competitive, market, regulatory and other factors, many of which are beyond our control. We believe that these factors include, but are not limited to:

|

· |

a reduction in the number of rounds of golf played or in the number of golf participants; |

|

· |

unfavorable weather conditions may impact the number of playable days and rounds played in a given year; |

|

· |

macroeconomic factors may affect the number of rounds of golf played and related spending on golf products; |

|

· |

demographic factors may affect the number of golf participants and related spending on our products; |

|

· |

a significant disruption in the operations of our manufacturing, assembly or distribution facilities; |

|

· |

our ability to procure raw materials or components of our products; |

|

· |

a disruption in the operations of our suppliers; |

|

· |

cost of raw materials and components; |

|

· |

currency transaction and translation risk; |

|

· |

our ability to successfully manage the frequent introduction of new products; |

|

· |

our reliance on technical innovation and high-quality products; |

|

· |

changes of the Rules of Golf with respect to equipment; |

|

· |

our ability to adequately enforce and protect our intellectual property rights; |

|

· |

involvement in lawsuits to protect, defend or enforce our intellectual property rights; |

|

· |

our ability to prevent infringement of intellectual property rights by others; |

|

· |

recent changes to U.S. patent laws and proposed changes to the rules of the U.S. Patent and Trademark Office; |

|

· |

intense competition and our ability to maintain a competitive advantage in each of our markets; |

ii

|

· |

limited opportunities for future growth in sales of golf balls, golf shoes and golf gloves; |

|

· |

our customers’ financial condition, their levels of business activity and their ability to pay trade obligations; |

|

· |

a decrease in corporate spending on our custom logo golf balls; |

|

· |

our ability to maintain and further develop our sales channels; |

|

· |

consolidation of retailers or concentration of retail market share; |

|

· |

our ability to maintain and enhance our brands; |

|

· |

seasonal fluctuations of our business; |

|

· |

fluctuations of our business based on the timing of new product introductions; |

|

· |

risks associated with doing business globally; |

|

· |

compliance with laws, regulations and policies, including the U.S. Foreign Corrupt Practices Act (the “FCPA”) or other applicable anti-corruption legislation; |

|

· |

our ability to secure professional golfers to endorse or use our products; |

|

· |

negative publicity relating to us or the golfers who use our products or the golf industry in general; |

|

· |

our ability to accurately forecast demand for our products; |

|

· |

a disruption in the service or increase in cost, of our primary delivery and shipping services or a significant disruption at shipping ports; |

|

· |

our ability to maintain our information systems to adequately perform their functions; |

|

· |

cybersecurity risks; |

|

· |

the ability of our eCommerce systems to function effectively; |

|

· |

occurrence of natural disasters or pandemic diseases; |

|

· |

impairment of goodwill and identifiable intangible assets; |

|

· |

our ability to attract and/or retain management and other key employees and hire qualified management, technical and manufacturing personnel; |

|

· |

our ability to prohibit sales of our products by unauthorized retailers or distributors; |

|

· |

terrorist activities and international political instability; |

|

· |

our ability to grow our presence in existing international markets and expand into additional international markets; |

|

· |

tax uncertainties, including potential changes in tax laws, unanticipated tax liabilities and limitations on utilization of tax attributes after any change of control; |

|

· |

adequate levels of coverage of our insurance policies; |

iii

|

· |

product liability, warranty and recall claims; |

|

· |

litigation and other regulatory proceedings; |

|

· |

compliance with environmental, health and safety laws and regulations; |

|

· |

our ability to secure additional capital on terms acceptable to us and potential dilution of holders of our common stock; |

|

· |

our estimates or judgments relating to our critical accounting policies; |

|

· |

our substantial leverage, ability to service our indebtedness, ability to incur more indebtedness and restrictions in the agreements governing our indebtedness; |

|

· |

a sale, foreclosure, liquidation or other transfer of the shares of our common stock owned by Magnus Holdings Co., Ltd. (“Magnus”) as a result of the term loan agreement entered into by Magnus to finance the purchase of shares of our common stock by Magnus in connection with our initial public offering; |

|

· |

the ability of our controlling stockholder to control significant corporate activities, and our controlling stockholder’s interests may conflict with yours; |

|

· |

the pledge by Fila Korea Co., Ltd. (“Fila Korea”) of the common stock of Magnus and any future pledges by Fila Korea of the common stock of Magnus; |

|

· |

the insolvency laws of Korea are different from U.S. bankruptcy laws; |

|

· |

our status as a controlled company; |

|

· |

increased costs and regulatory requirements of operating as a public company; |

|

· |

our ability to maintain effective internal controls over financial reporting; |

|

· |

our ability to pay dividends; |

|

· |

dilution from future issuances or sales of our common stock; |

|

· |

anti-takeover provisions in our organizational documents; and |

|

· |

reports from securities analysts. |

These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, our actual results may vary in material respects from those projected in these forward-looking statements.

Any forward-looking statement made by us in this report speaks only as of the date of this report. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, investments or other strategic transactions we may make. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by any applicable securities laws.

iv

INDUSTRY AND MARKET DATA

Within this annual report on Form 10‑K, we reference information and statistics regarding the golf industry and the golf equipment, wear and gear markets. We have obtained certain of this information and statistics from various independent third-party sources, including independent industry publications, reports by market research firms and other independent sources for the most recent available date. We believe that these external sources and estimates are reliable, but have not independently verified them. Certain of this information and statistics are based on our good faith, reasonable estimates, which are derived from our review of internal surveys and independent sources. In addition, projections, assumptions and estimates of the future performance of the golf industry and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and “Forward-Looking Statements.” These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

WEBSITE DISCLOSURE

We use our website (www.acushnetholdingscorp.com) as a channel of distribution of company information. The information we post through this channel may be deemed material. Accordingly, investors should monitor this channel, in addition to following our press releases, SEC filings and public conference calls and webcasts. In addition, you may automatically receive e-mail alerts and other information about Acushnet Holdings Corp. when you enroll your e-mail address by visiting the “Resources” section of our website at https://www.acushnetholdingscorp.com. The contents of our website are not, however, a part of this report.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

This Annual Report on Form 10‑K includes trademarks, trade names and service marks that we either own or license, such as “Titleist,” “FootJoy,” “Pro V1,” “Pro V1x,” “FJ,” “Pinnacle,” “Scotty Cameron,” and “Vokey Design” which are protected under applicable intellectual property laws. Solely for convenience, trademarks, trade names and service marks referred to in this report may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. This report may also contain trademarks, trade names and service marks of other parties, and we do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

v

Overview

We are the global leader in the design, development, manufacture and distribution of performance‑driven golf products, which are widely recognized for their quality excellence. Driven by our focus on dedicated and discerning golfers and the golf shops that serve them, we believe we are the most authentic and enduring company in the golf industry. Our mission—to be the performance and quality leader in every golf product category in which we compete—has remained consistent since we entered the golf ball business in 1932. Today, we are the steward of two of the most revered brands in golf—Titleist, one of golf’s leading performance equipment brands, and FootJoy, one of golf’s leading performance wear brands. Titleist has been the #1 ball in professional golf for 68 years and FootJoy has been the #1 shoe on the PGA Tour for over six decades.

Our target market is dedicated golfers, who are the cornerstone of the worldwide golf industry. These dedicated golfers are avid and skill‑biased, prioritize performance and commit the time, effort and money to improve their game. We believe our focus on innovation and process excellence yields golf products that represent superior performance and consistent product quality, which are the key attributes sought after by dedicated golfers. Many of the game’s professional players, who represent the most dedicated golfers, prefer our products thereby validating our performance and quality promise, while driving brand awareness. We leverage a pyramid of influence product and promotion strategy, whereby our products are the most played by the best players, creating aspirational appeal for a broad range of golfers who want to emulate the performance of the game’s best players.

Dedicated golfers view premium golf shops, such as on‑course golf shops and golf specialty retailers, as preferred retail channels for golf products of superior performance and product quality. As a result, we have committed to being one of the preferred and trusted partners to premium golf shops worldwide. This commitment provides us a retail environment where our product performance and quality advantage can most effectively be communicated to dedicated golfers. In addition, we also service other qualified retailers that sell golf products to consumers worldwide.

Our vision is to consistently be regarded by industry participants, from dedicated golfers to the golf shops that serve them, as the best golf company in the world. We have established leadership positions across all major golf equipment and golf wear categories under our globally recognized brands.

|

|

#1 ball in golf Golf’s Symbol of Excellence A leading global golf equipment brand |

|

|

#1 shoe in golf #1 glove in golf A leading global golf wear brand |

|

|

#1 wedge on the PGA Tour |

|

|

#1 putter on the PGA Tour |

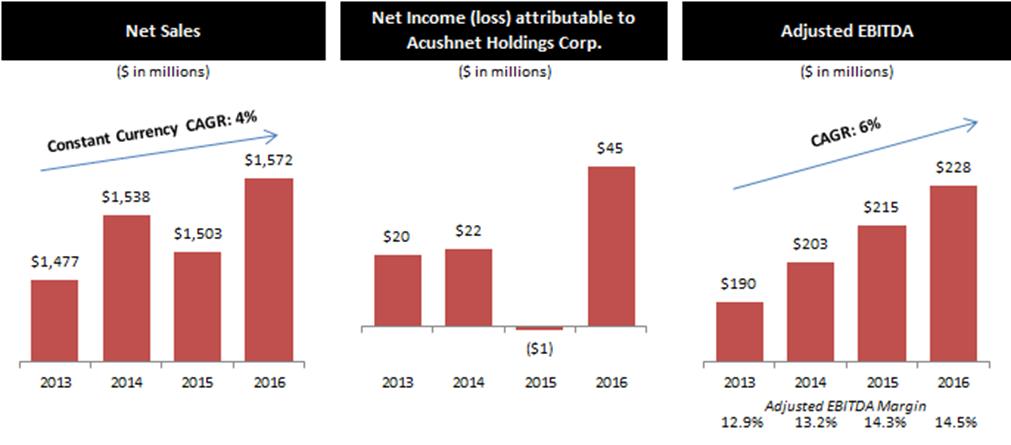

For the year ended December 31, 2016, we recorded net sales of $1,572.3 million, net income attributable to Acushnet Holdings Corp. of $45.0 million and Adjusted EBITDA of $228.4 million. See “Item 6. – Selected Consolidated Financial Data” for a reconciliation of Adjusted EBITDA to net income attributable to Acushnet Holdings Corp., the most directly comparable GAAP financial measure.

6

Our History and Evolution

Founded in Acushnet, Massachusetts by Phil “Skipper” Young in 1910 and incorporated as the Acushnet Process Company, we manufactured rubber‑based products including water bottles, gas masks and bathing caps. Our golf business was established in 1932 when Young, a dedicated golfer himself, missed a critical putt in a golf match. Believing the putt to be well struck, Young took the ball to be x‑rayed, where it was discovered that the ball’s core was off‑center. Following this seminal discovery that many commercially available golf balls frequently had manufacturing inconsistencies, Young set out with Massachusetts Institute of Technology classmate Fred Bommer to develop a superior golf ball. After three years of development, the Titleist golf ball was introduced.

The objective from the very beginning was to produce a golf ball that would set the standard in performance, quality and consistency, and become the preferred choice of dedicated golfers and the preferred trade partners who would serve them. In the early years, many of these preferred trade partners were also some of the first touring golf professionals. Soon the Titleist golf ball was the golf ball of choice wherever competitive golf was played. The core values of serving the game’s dedicated golfer with a superior product, in terms of both performance and quality, and having that superior product validated by the game’s most dedicated golfers and premium golf retailers, have endured for the past eight decades.

In 1976, Acushnet Company was acquired by American Brands, Inc. (the predecessor company of Beam Suntory, Inc. (“Beam”)). We acquired FootJoy in 1985. On July 29, 2011, Acushnet Holdings Corp. (at the time known as Alexandria Holdings Corp.), an entity owned by Fila Korea and certain financial investors, acquired Acushnet Company from Beam. We completed an initial public offering of our common stock in November 2016. See “Notes to Consolidated Financial Statements– Note 2– Summary of Significant Accounting Policies,” for disclosures related to our initial public offering and other related transactions.

Our Core Focus

Dedicated Golfers

Our target market is dedicated golfers, who are avid and skill‑biased, prioritize performance and commit the time, effort and money to improve their game. We believe that dedicated golfers are the most consistent purchasers of golf products and estimate that while they represented only approximately 15% of all United States golfers, they accounted for more than 40% of total rounds played and approximately 70% of all golf equipment and gear spending in the United States during 2016. We also believe dedicated golfers account for an outsize share of golf equipment and gear spending outside the United States and purchase a significant portion of golf wear products worldwide.

Product Platform

Leveraging the success of our golf ball and golf shoe businesses, while maintaining the core values of the Titleist and FootJoy brands, we have strategically entered into product categories such as golf clubs, wedges, putters, golf gloves, golf gear and golf wear with an objective of being the performance and quality leader.

Since the dedicated golfer views each performance product category on its own merits, we have approached each category on its own terms by committing the necessary resources to become the performance and quality leader in each product category where we participate. As a result, we have built an industry leading platform across all performance product categories, driving a market‑differentiating mix of consumable products, which we consider to be golf balls and golf gloves, which collectively represented 40% of our net sales in 2016, and more durable products, which we consider to be golf clubs, golf shoes, golf apparel and golf gear, which collectively represented 60% of our net sales in 2016.

We operate under the following four reportable segments. Financial information for our segments, including sales by geographic area, is included in “Item 7. – Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in “Notes to Consolidated Financial Statements – Note 20 – Segment Information.”

7

Titleist Golf Balls (33% of 2016 net sales)

Titleist is the #1 ball in golf. The Titleist golf ball was founded with a purpose of designing and manufacturing a performance oriented, high quality golf ball that was superior to all other products available in the market. We believe the golf ball is the most important piece of equipment in the game, as it is the only piece of equipment used by every player for every shot. The golf ball is also the most important category for us as it generates the largest portion of our sales and profits. Since its introduction in 2000, the Titleist Pro V1 has been the best‑selling golf ball globally and continues to set the bar in terms of product design, quality and performance. We also design, manufacture and sell other golf balls under the Titleist brand, such as NXT Tour, Velocity and DT TruSoft, as well as under the Pinnacle brand. We have continually improved our golf balls through innovation in materials, construction and manufacturing processes, which has enabled us to build the #1 golf ball franchise in the world.

Titleist Golf Clubs (27% of 2016 net sales)

We design, assemble and sell golf clubs (drivers, fairways, hybrids and irons) under the Titleist brand, wedges under the Vokey Design brand and putters under the Scotty Cameron brand. The mission of our golf club business is to design and develop the best performing golf clubs in the world for dedicated golfers. We believe dedicated golfers do not buy brands across categories but seek out best‑in‑class products in each category. This is the reason we have partnered with dedicated engineers and craftsmen such as Bob Vokey and Scotty Cameron, who understand the nuances, subtleties and impact mechanics of their respective golf club categories. Titleist golf clubs, Vokey Design wedges and Scotty Cameron putters are widely used by professional and competitive amateur players, which validates the products’ performance and quality excellence. We are also committed to a leading club fitting and trial platform to maximize dedicated golfers’ performance experience.

Titleist Golf Gear (9% of 2016 net sales)

We offer a diversified portfolio of Titleist‑branded performance golf gear across the golf bags, headwear, gloves, travel gear, head covers and other golf gear categories. Our golf gear is focused on superior performance and quality excellence, which is the mission of any product bearing the Titleist brand name.

FootJoy Golf Wear (28% of 2016 net sales)

We design, manufacture and sell golf shoes and gloves, and we design and sell performance outerwear, apparel and socks under the FootJoy brand. By offering products with premium materials, superior comfort and fit and authentic designs, FootJoy has become the #1 shoe and #1 glove in golf and a leader in the global performance golf outerwear and the U.S. golf apparel markets. We believe FootJoy is seen by golfers around the world as an authentic and definitive golf brand with a consistent, differentiated focus on performance and quality.

Pyramid of Influence

The game of golf is learned by observation and imitation, and golfers improve their own performance by attempting to emulate highly skilled golfers. Golfers are influenced not only by how other golfers swing but also by what they swing with and what they swing at. This is the essence of golf’s pyramid of influence, which is deeply ingrained in the mindset of the dedicated golfer. At the top of the pyramid is the most dedicated golfer, who attempts to make a living playing the game professionally. Adoption by most of the best golfers, whose professional success depends on their performance, validates the quality, features and benefits of using the best performing products. This, in turn, creates aspirational appeal for golfers who want to emulate the performance of the best players. By virtue of the performance and quality excellence of our products, we believe we are best‑positioned to leverage the pyramid of influence since most of the best players trust and use Titleist and FootJoy products. Our primary marketing strategy is for our products to be the most played by the best players, including both professional and amateur golfers. This strategy has proven to be enduring and effective in the long‑term and is not dependent on the transient success of a few elite players at any given point in time.

Innovation Leadership

We believe innovation is critical to dedicated golfers as they depend on the ability of new and innovative products to drive improved performance. Since we entered the golf ball business in 1932, we believe we have been the

8

design and technology leader in the golf industry with a strategy to develop, implement and protect product and process improvements. We currently employ an R&D team of over 180 scientists, chemists, engineers and technicians. We also introduce new product innovations at a cadence that best aligns with the typical dedicated golfer’s replacement cycle within each product category. We spent $48.8 million, $46.0 million and $44.2 million in 2016, 2015 and 2014, respectively, on R&D.

Operational Excellence

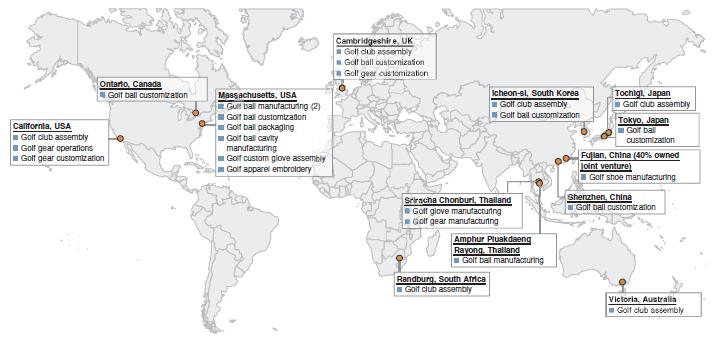

The requirements of the game lead the dedicated golfer to seek out products of maximum performance and consistency. We own or control the design, sourcing, manufacturing, packaging and distribution of our products. In doing so, we are able to exercise control over every step of the manufacturing process and supply chain operations, thereby setting the standard for quality and consistency. Our operational excellence also allows us to continually develop innovative new products, bring those products to market more efficiently and ensure high levels of quality control. We have developed and refined distinct and independently managed supply chains for each of our product categories. Our manufacturing facilities include:

|

· |

three golf ball manufacturing facilities that collectively produce over one million balls per production day; |

|

· |

six golf club assembly facilities; |

|

· |

a joint venture facility to manufacture our golf shoes; and |

|

· |

a facility to manufacture our golf gloves. |

Route to Market Leadership

As one of the preferred partners to premium golf shops, we ensure that the performance benefits derived from using our products are showcased and our products are properly merchandised. We have over 340 sales representatives directly servicing nearly 31,000 accounts in 47 countries and we service over 90 countries in total, directly or through distributors. With an average of almost 20 years of experience, we believe the Titleist U.S. sales team is the largest and most experienced in the industry. Similarly, we believe FootJoy has built the most experienced, highly qualified team in the U.S. golf wear category. As we see our retail partners as a critical connection to dedicated golfers, we place great emphasis on building strong relationships and trust with them. This is the reason our sales associates are expected not simply to be salespeople, but to function as golf experts and enthusiasts in their respective territories, who advise and assist our retail partners to better serve their customers. We help generate golfer demand and sell‑through via in‑shop merchandising, promotions and advertising, and also provide product education to club professionals, coaches and instructors. Lastly, we place a strong focus on consumer engagement, starting with fitting and trial initiatives across our balls, clubs and shoes categories. We offer custom products across categories that we believe are better aligned with golfers’ personal styles, skill levels and preferences.

Market Overview and Opportunity

Market Overview

We estimate that the sport of golf gives rise to a global commercial opportunity of more than $85 billion annually, which captures all spending related to golf. There are over 50 million golfers worldwide playing over 800 million rounds annually on over 32,000 golf courses. Our addressable market comprised of golf equipment, golf wear and golf gear represents approximately $12 billion in retail sales and approximately $8 billion in wholesale sales. The United States accounted for over 40% of our addressable market, followed by Japan and Korea collectively accounting for over 30% of our addressable market, each in 2016.

According to Golf Datatech, LLC, the number of rounds of golf played in the United States has shown modest improvements in both 2015 and 2016. We believe the number of rounds of golf played by our target market of dedicated golfers has remained stable over the past few years.

We view emerging economies, such as the markets in Southeast Asia, as attractive long‑term opportunities based on our assessment through the lens of the five collectively necessary and sufficient conditions for a country to

9

embrace golf: (1) sizeable middle‑class population; (2) educational infrastructure; (3) places to play and practice; (4) professional success that inspires the local golfers; and (5) corporate support.

We believe the golf industry is mainly driven by golfer demographics, dedicated golfers and weather and economic conditions.

Golfer Demographics. Golf is a recreational activity that requires time and money. The golf industry has been principally driven by the age cohort of 30 and above, currently “gen‑x” (age 30 to 49) and “baby boomers” (age 50 to 69), who have the time and money to engage in the sport. In the United States, there are approximately 8.7 million gen‑x golfers and approximately 6.6 million baby boomer golfers, representing approximately 63% of total golfers in the United States. Households headed by gen‑x and baby boomers also claim an approximately 80% share of the total income dollars in the United States. Since a significant number of baby boomers have yet to retire, we anticipate growth in spending from this demographic as it has been demonstrated that rounds of play increase significantly as those in this cohort reach retirement. On average, golfers in the age range of 18 to 34 play 15 rounds per year, whereas those in the age range of 50 to 64 and 65 and above play 29 rounds and 51 rounds per year, respectively. While golf has historically consisted of mostly male players, women accounted for approximately 24% of golfers in the United States in 2015, up from approximately 20% in 2011. Because nearly 40% of beginner golfers in the United States in 2015 were women, we believe that the percentage of women golfers will continue to grow. Beyond the gen‑x and baby boomer generation, another promising development in golf has been the generational shift with millennial golfers making their marks at both professional and amateur levels. Golfers under the age of 30 represented 36% of the World Rank Top 50 and 78% of Rolex World Rank Top 50 Women as of December 31, 2016. The largest single age group of beginners in the United States in 2015 was millennials (age 18 to 29). Further, the number of junior golfers (age 6 to 17) in the United States has grown from approximately 2.5 million golfers in 2010 to approximately 3.0 million golfers in 2015.

Dedicated Golfers. Dedicated golfers are largely gen‑x and baby boomers who have demonstrated the propensity to pay a premium for products that help them perform better. We believe dedicated golfers, who comprise our target market, will continue to be a key driver for the global golf industry. The National Golf Foundation estimates that there were 6.2 million, 6.5 million and 6.4 million “avid” golfers in the United States in 2015, 2014 and 2013, respectively, with “avid” golfers defined as those who play 25 rounds or more per year. We estimate that approximately 60% of these avid golfers in the United States are dedicated golfers.

Weather Conditions. Weather conditions determine the number of playable days in a year and thus influence the amount of time people spend on golf. Weather conditions in most parts of the world, including our primary geographic markets, generally restrict golf from being played year‑round, with many of our on‑course customers closed during the cold weather months. Therefore, favorable weather conditions generally result in more playable days in a given year and thus more golf rounds played, which generally results in increased demand for all golf products.

Economic Conditions. The state of the economy influences the amount of money people spend on golf. Golf equipment, including clubs, balls and accessories, is recreational in nature and is therefore a discretionary purchase for consumers. Consumers are generally more willing to make discretionary purchases of golf products when economic conditions are favorable and when consumers are feeling confident and prosperous.

Our Opportunity

We have demonstrated sustained, resilient and stable revenue and Adjusted EBITDA growth over the past four years, despite challenges related to demographic, macroeconomic and weather related conditions. Our differentiated focus on performance and quality excellence, enduring connections with dedicated golfers and favorable and market‑differentiating mix of consumable and durable products have been the key drivers of our strong performance. We believe this focus positions us to continue to generate industry‑leading performance.

10

Strong Financial Performance

Since 2013, we have driven strong financial performance across our product portfolio in the aggregate and in each of our reportable segments of Titleist golf balls, Titleist golf clubs, Titleist golf gear and FootJoy golf wear. From 2013 to 2016:

|

· |

our net sales increased from $1,477 million to $1,572 million, representing a compound annual growth rate, or CAGR, of 2%, or 4% on a constant currency basis; |

|

· |

our net income attributable to Acushnet Holdings Corp. was $19.6 million in 2013 and $45.0 million in 2016; |

|

· |

our Adjusted EBITDA increased from $190.4 million to $228.4 million, representing a CAGR of 6%; |

|

· |

we achieved 160 basis points of Adjusted EBITDA margin expansion; and |

|

· |

our cash flows provided by operating activities increased from $78.8 million to $105.2 million. |

See “Item 6. – Selected Consolidated Financial Data” for a reconciliation of Adjusted EBITDA to net income (loss) attributable to Acushnet Holdings Corp., the most directly comparable GAAP financial measure. See “Item 7. –Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Key Performance Measures” for a description of how we calculate constant currency information.

Our Competitive Strengths

Steward of Golf’s Most Revered Brands. We have long been the trusted steward of two of golf’s most revered and recognized brands, and have enjoyed the longest running record of market leadership in the golf category. We believe the Titleist and FootJoy brands deliver superior performance and quality excellence in their respective product categories and are widely regarded as the strongest and most identifiable brands among premium golf equipment and golf wear manufacturers. Titleist has been the #1 ball in professional golf for 68 years while FootJoy has been the leading brand on the PGA Tour in golf shoes for over six decades and golf gloves for over three decades. The performance and quality of our brands are validated by the widespread adoption of our products by the world’s best professional and amateur golfers, which generates exceptional brand loyalty among our core customers and drives repeat purchases.

Market‑Leading Portfolio of Products Designed for Dedicated Golfers. The Titleist Pro V1 golf ball was launched in 2000 and in four months became the #1 selling ball on the market, a position it still holds, and is the #1 golf

11

ball played at every level of competitive golf today. We estimate that we held nearly one‑half of the 2015 global top grade wholesale golf ball market, which we estimate was approximately $1.0 billion, including over two‑thirds of the premium performance market segment. Pro V1 models are the longest running #1 of any golf equipment since Golf Datatech began tracking this metric in 1997. It is rare when a brand’s highest priced product in a particular category is also the industry volume leader. In 2016, the number of Titleist balls played on professional tours was more than five times the number of balls of our nearest competitor. Titleist records even higher ball counts at most amateur championships than on the worldwide professional tours, a further testament to the performance and quality of Titleist. Since amateurs are not allowed to receive compensation for the use or endorsement of any brand’s equipment, they freely choose what golf ball they believe will help them shoot their lowest scores. Faithful to the brand promise of the Titleist ball, we believe our golf clubs are also best‑in‑class in terms of performance and quality. Our Vokey Design wedges and Scotty Cameron putters are recognized worldwide as leaders in their respective categories. Our Vokey Design wedges are the most widely used on the PGA Tour. Under our FootJoy brand, we are the #1 shoe in golf, with the leading usage on all of the world’s major professional golf tours and twice as many stock keeping units, or SKUs, as our nearest competitors. FootJoy gloves also have the leading market share, enjoy the #1 position on all the world’s major professional golf tours, and offer the largest selection of golf gloves in the industry. FootJoy is also a global leader in golf outerwear and has a rapidly growing presence in golf apparel.

Favorable Consumable / Durable Mix. We have developed a product portfolio with a favorable mix of consumables and durables, which we believe differentiates us from other pure golf equipment manufacturers. Consumable purchases are largely driven by the number of rounds played, while durable purchases are subject to technology replacement cycles. We believe our favorable product mix is less economically cyclical and more working capital efficient than that of our peers. Our sales reflect a favorable and market‑differentiating mix of consumable products, which we consider to be golf balls and golf gloves, which collectively represented 40% of our net sales in 2016, and more durable products, which we consider to be golf clubs, golf shoes, golf apparel and golf gear, which collectively represented 60% of our net sales in 2016.

Best‑in‑Class Design Innovation. Driven by our commitment to perpetual innovation, we believe we are the innovation leader in the golf industry. Golf’s most regulated and technically‑driven categories are golf balls and golf clubs, and therefore require strong intellectual property to create differentiated products with superior performance and quality. We hold the largest patent portfolio in the golf industry, with over 1,250 active U.S. utility patents in golf balls, close to 350 active U.S. utility patents in golf clubs, wedges and putters and 296 active patents (including ex‑U.S. and design patents) in golf shoes and gloves. As of December 31, 2016, we had 37% and 15% market shares of active golf ball and club patents, respectively. Over 90% of our current products incorporate technologies or designs developed in the last five years. The Titleist Pro V1 franchise is an example of our innovation leadership. We have sold over 130 million dozen Pro V1 and Pro V1x golf balls, generating over $4.5 billion of revenue, since the introduction of the Pro V1 in 2000. We believe our ability to develop and implement innovation drives superior product performance and our patent portfolio allows us to protect our product and process improvements in an industry where success is driven by product performance and quality improvements.

Operational Excellence. Our differentiated manufacturing processes and connectivity between our manufacturing and R&D teams foster integration throughout the design and manufacturing process. This allows us to continually develop innovative new products that we can bring to market efficiently while ensuring consistency and high levels of quality control. Unlike many other golf companies, we own or control the design, sourcing, manufacturing, packaging and distribution of our products. Our vertically integrated approach delivers a consistent product quality and results in very high customer satisfaction. There are over 90 quality checks for Titleist Pro V1 and 120 quality checks that go into Titleist Pro V1x to ensure every ball is worthy of bearing the Titleist brand name. An example of this is our product quality return percentage—for every 10 million Titleist Pro V1 golf balls produced, only one is returned on average. By controlling key aspects of the design and manufacturing processes, we are better able to protect our intellectual property as well as offer customization capabilities and efficient turn times. Furthermore, we are able to provide custom fitted products to individuals in a short timeframe and facilitate regional market customization.

Unparalleled Route to Market Leadership. The foundation of our go‑to‑market strategy is to continue to be the preferred partner for premium golf shops worldwide and to provide customization and fitting that optimize our customers’ post‑purchase experiences. In doing so, we ensure that the performance benefits derived from using our products are showcased and our products are properly merchandised, while deepening our customers’ connections with the Titleist and FootJoy brands. We believe these initiatives, in turn, increase sales and profitability for our retail partners, leading to a mutually beneficial economic relationship. Today, we deploy over 20,000 displays that are

12

designed and adapted to local needs, and there are over 3,500 premium golf shops that exclusively stock or display Titleist balls. By virtue of our strong relationship with retail partners, we are able to build the strong connections with and gain deep understanding of dedicated golfers. We are able to closely track the replacement cycles of our customers’ equipment and effectively market our new products in a timely manner.

Deep Stewardship Culture and Experienced Management Team. Behind our exceptional products and organizational infrastructure lies an authentic and enduring organizational culture validated by the longevity of our management team, sales force and associates. Our management team members, many of whom have dedicated their entire careers to our company, average over 19 years of employment with us. They are supported by a deep and talented team of associates across product categories, functions, markets and geographies, who serve as strong brand and cultural ambassadors. Approximately 50% of our U.S. associates have over ten years of employment with us, highlighting the depth of our talent and future leaders. We are the stewards of our brands, and we are committed to maintaining the culture of excellence that defines us and our products.

Our Growth Strategies

We plan to continue to pursue organic growth initiatives across all product categories, brands, geographies and marketing channels.

Introduce New Products and Extend Market Share Leadership in Equipment Categories. We expect to sustain our strong performance in our core categories of golf balls and golf clubs through several targeted strategies:

|

· |

Titleist Golf Balls. To ensure sustained long‑term market leadership, we are continuously investing in design innovation and refining our sell‑in and sell‑through route to market capabilities and effectiveness in the golf ball product category. We are currently focused on improving our sales team training in product, merchandising, local promotion and selling skills, as well as enhancing trade partnerships in those channels where dedicated golfers shop. To grow our custom golf ball business, we have in place several new initiatives designed to develop strategic partnerships with corporations heavily invested in golf and to drive growth with a particular focus on the areas of corporate, country club, tournament and personalized sales. The 2016 launch of the “My Pro V1 Shop” online golf shop allows golfers to create and purchase their own unique Titleist Pro V1 / Pro V1x golf balls with special play numbers, logos or personalization. We believe the website will increase the likelihood of repeat purchases, thereby strengthening the link with golfers and loyalty to Titleist golf balls. |

|

· |

Titleist Clubs, Wedges and Putters. We intend to continue to launch innovative, performance golf clubs by further leveraging Titleist clubs’ leading R&D platform. We believe concept and specialty products and premium quality digital content will further drive customer awareness and market share gains across all premium club categories. To enhance trial and fitting, we plan to continue our leading consumer connection initiatives, grow our fitting network in opportunistic markets and further promote the utilization of our distinctive fitting operations. We are also executing several initiatives to further elevate Vokey Design wedges and Scotty Cameron putters as golf’s leaders in short‑game performance, technology, craftsmanship, and selection. |

Increase Penetration in Golf Gear and Wear Categories. We intend to build on the brand loyalty that the dedicated golfer has developed for our Titleist ball and club categories and FootJoy shoe and glove categories in order to increase our penetration in the adjacent categories of golf gear and golf wear. We expect to continue to drive growth across these categories by employing the following initiatives:

|

· |

Titleist Golf Gear. We are committed to providing dedicated golfers with golf gear—including golf bags, headwear, gloves, travel gear, head covers and other accessories—of performance and quality excellence that is faithful to the Titleist brand promise. We are making significant investments in design and engineering resources and are leveraging dedicated player research methodologies and insights to drive innovation in this product category. We also plan to expand custom and limited edition product offerings. |

|

· |

FootJoy Women’s Apparel Initiative. We are currently building out a focused, performance‑based FootJoy women’s apparel line consistent with the brand’s successful positioning in men’s apparel. The women’s apparel line, which launched in early 2016, pairs sophisticated performance fabrics and design with |

13

layering technology pioneered by FootJoy to create maximum comfort and protection. By leveraging our existing FootJoy sales force in an adjacent category, we believe we can offer a compelling and authentic solution to female golfers and capitalize on the trend of casual, athletic styling that is driving success in the broader women’s apparel space. |

|

· |

FootJoy eCommerce Launch. We launched a U.S. eCommerce website for FootJoy in 2016. Over 6,000 SKUs are offered across all FootJoy categories, including shoes, gloves and apparel. The eCommerce initiative is expected to yield incremental sales and profitability, enriched data on preferences and trends as well as foster a deeper and more real time connection with the dedicated golfer. |

Strategically Pursue Global Growth. The Titleist and FootJoy brands are both global brands that are well positioned where golf’s growth is anticipated. While we believe that a majority of the near‑term growth will be driven by the developed economies, emerging economies, such as the markets in Southeast Asia, represent longer‑term growth opportunities. To meet future demand, we are ensuring that local capabilities and expertise in sales, customer service, merchandising, online presence, golf education and fitting initiatives are in place to support our operations. We continue to hire local talent across all functions in order to better position the products of Titleist and FootJoy in those markets where participation and popularity of the sport are expected to increase.

Our Products

We design, manufacture and market a broad range of products under the Titleist and FootJoy brands. Both brands are recognized as industry leaders in performance, quality, innovation and design. Our products include golf balls, golf clubs, wedges and putters, golf shoes, golf gloves, golf gear and golf outerwear and apparel.

|

|

||

|

Titleist Golf Balls |

Titleist Golf Clubs, |

Titleist Golf Gear |

|

|

|

|

|

Pro V1 |

Drivers |

Golf bags |

|

Pro V1x |

Fairways |

Headwear |

|

NXT Tour |

Hybrids |

Golf gloves |

|

Velocity |

Irons |

Travel gear |

|

DT TruSoft |

Vokey Design wedges |

Head covers |

|

Pinnacle |

Scotty Cameron putters |

Other golf gear |

|

|

||

|

FootJoy Shoes |

FootJoy Gloves |

FootJoy Outerwear and Apparel |

|

|

|

|

|

Traditional |

Leather construction |

Performance outerwear |

|

Spikeless |

Synthetic |

Performance golf apparel |

|

Athletic |

Leather/synthetic combination |

Golfleisure women’s apparel |

|

Casual |

Specialty |

|

Titleist

We design, manufacture and sell golf balls, golf clubs, wedges and putters and golf gear under the Titleist brand. Net sales of Titleist products for the years ended December 31, 2016, 2015 and 2014 were $1,139.2 million, $1,084.1 million, and $1,116.0 million, respectively, in each case approximately 72% of our total net sales.

Titleist Golf Balls

Titleist is the #1 ball in golf. The 2016 Titleist golf ball product line consisted of six major models, each designed to deliver different performance characteristics, such as distance, flight, short game control, feel and durability.

14

Pro V1 and Pro V1x are designed to be the highest performing and quality golf balls for golfers at every level of the game and best demonstrate Titleist’s design, innovation and technology leadership. The first Pro V1 golf ball was introduced on the PGA Tour in October 2000 and launched to the market in December 2000. It represented the coalescence of three of Titleist’s industry leading technologies: large solid core; multi‑component construction; and high performance, thermoset cast urethane elastomer covers. In its first four months, the Pro V1 golf ball became the best‑selling golf ball and holds that position to this day. During this time, we also set out to create a ball that produced lower driver spin and higher launch characteristics than the Pro V1 while retaining its high performance scoring spin. With its four‑piece, dual core design, the Pro V1x golf ball was introduced in 2003. In 2017, we launched new versions of the Pro V1 and Pro V1x. The New Pro V1 is designed to offer significantly longer distance from faster ball speed and lower long game spin. Advancements in aerodynamics for both Pro V1 and Pro V1x are designed to produce even more consistent flight. We believe these improvements, along with benefits such as our renowned Drop-and-Stop control, soft feel and long lasting durability, make Pro V1 golf balls the best performance choice for all golfers.

We also provide best‑in‑class performance with the NXT Tour, NXT Tour S, Velocity and DT TruSoft models.

By competing at a lower price point, Pinnacle completes a full product offering for us. With two major models, Rush and Soft, Pinnacle golf balls are also available in different optic colors and play numbers. Our Pinnacle Brand competes in the price market segment, which allows the Titleist brand to focus on the premium performance and performance market segments and reduces the need to extend the Titleist brand to the price market segment. This also helps to support the thousands of golf shops that choose to exclusively stock Titleist and Pinnacle golf balls, allowing them to offer golf balls in each market segment which market segments we discussed and defined below.

Titleist and Pinnacle golf balls accounted for $513.9 million, or 33%, $535.5 million, or 36%, and $543.8 million, or 35%, of our total net sales for the years ended December 31, 2016, 2015 and 2014, respectively.

We estimate that we held nearly one‑half of the 2015 global top grade wholesale golf ball market, which we estimate was approximately $1.0 billion, and held leadership positions across the most profitable market segments. The top grade wholesale golf ball market consists of all golf balls sold in the wholesale market excluding range golf balls, practice golf balls or downgraded or repurposed golf balls.

|

· |

The premium performance market segment (which we estimate was approximately $490 million of the 2015 global top grade wholesale golf ball market), which we consider to be golf balls that are designed to maximize total performance across all product attributes, including distance, short game spin and control, feel and durability. Titleist Pro V1 and Pro V1x golf balls led the premium performance segment with over two‑thirds of this market segment. |

|

· |

The performance market segment (which we estimate was approximately $380 million of the 2015 global top grade wholesale golf ball market), which we consider to be golf balls that are designed to prioritize distance, good short game spin and control, feel and durability, while maintaining a lower price point than balls that compete in the premium performance market segment. Titleist NXT Tour, Velocity and DT golf balls led the performance segment with approximately one‑third of this market segment. |

|

· |

The price market segment (which we estimate was approximately $180 million of the 2015 global top grade wholesale golf ball market), which we consider to be golf balls that are designed to prioritize distance, feel and durability, while targeting a more affordable price point than balls that compete in the premium performance and performance market segments. We are a leader in the price market segment. |

15

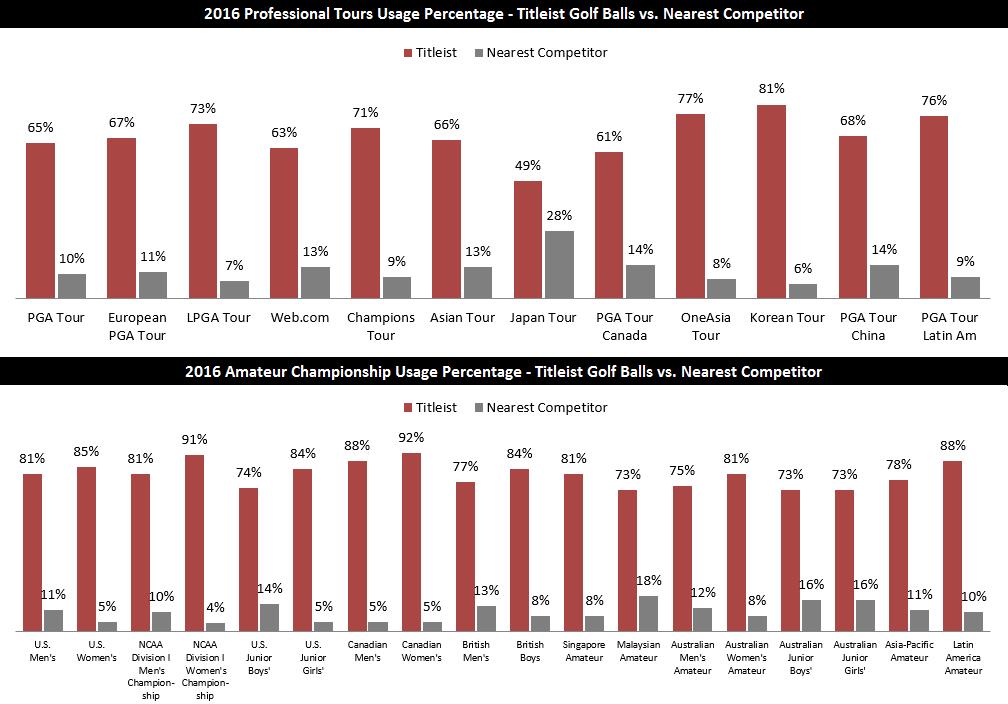

The table below shows the percentage of golfers that used Titleist golf balls as compared to its nearest competitor for specific professional tours and representative amateur championships in 2016.

As shown in the table above, at most amateur championships, Titleist records even higher ball counts than on the worldwide professional tours. Under The Rules of Golf established by the game’s governing bodies, the USGA and R&A, amateurs are not allowed to receive compensation for the use or endorsement of any brand’s equipment. Amateurs freely choose what golf ball they believe will help them shoot their lowest scores. We believe their choice of the Titleist golf ball further validates the superior performance and superior quality of Titleist.

We are also a leader in custom imprinted golf balls. This includes printing high quality reproductions of corporate logos, tournament logos, country club or resort logos, and personalization on Titleist and Pinnacle golf balls. Our service includes design capabilities, special packaging options and fast turnaround times. Custom imprinted golf balls represented over 30% of our global net golf ball sales for the year ended December 31, 2016. The majority of custom imprinting is done for corporate logos as there has long been a strong connection between the business community and golf.

Titleist Golf Clubs, Wedges and Putters

We view and operate the Titleist golf club business in three distinct categories: clubs (which includes drivers, fairways, hybrids and irons), wedges and putters. Our products are generally priced at or above the premium price points in the marketplace, driven by higher‑end technologies (including design, materials and processes) we employ to generate superior quality and performance. We have different models within each category to address the distinct performance needs of our dedicated golfer target audience. Titleist golf clubs, wedges and putters accounted for $431.0 million, or 27%, $388.3 million, or 26%, and $422.4 million, or 27%, of our total net sales for the years ended December 31, 2016, 2015 and 2014, respectively.

16

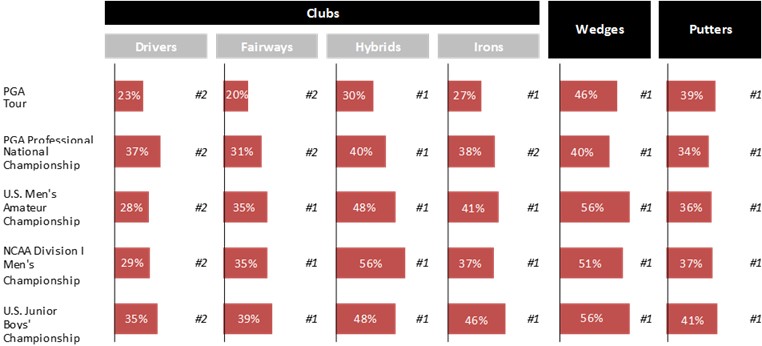

The table below shows the usage percentages and ranks of Titleist golf clubs, wedges and putters on the 2016 PGA Tour and representative 2016 championships in the United States.

Titleist Clubs

Our current global club line consists of the 917 product line of drivers and fairways, the 816 product line of hybrids and the 716 product line of irons. Every product in our club line features premium, tour‑proven stock shafts and grips, complemented by a broad range of custom options.

Titleist 917 drivers and fairways are designed to deliver superior performance through tour‑proven technologies that increase ball speed, decrease spin, and optimize flight without sacrificing forgiveness. We design our drivers and fairways to deliver complete performance with tour‑preferred looks, sound and feel, and we offer the ability to precisely fit individual golfers’ needs.

Titleist 816 hybrids generate long game performance through advanced technology. The advanced features of our hybrids aim to facilitate precision fitting and generate high ball speed, low spin and high launch for increased distance and forgiveness.

Titleist 716 irons are innovative, technologically advanced products designed to deliver distance, forgiveness, proper shot control and feel. While we offer stock set configurations for our iron sets, approximately 56% of our worldwide iron sales are custom fit to help deliver a better fit and performance.

We also sell our VG3 line of clubs, which consist of men’s and women’s drivers, fairways, hybrids and irons offered in Japan only. These products feature design and construction specifically targeted to dedicated golfers in Japan.

Vokey Design Wedges

Bob Vokey champions the Titleist wedge effort by creating high performance wedges to meet the demands of dedicated golfers and the best players in the world. The Vokey Design wedge product offering is a compilation of the most popular wedges resulting from Bob Vokey’s hands‑on work with golf’s best players to develop shapes and soles that address varying techniques and course conditions. In total, we offer 21 unique loft, sole grind and bounce combinations and three unique finishes to create golf’s most complete wedge product performance range. In addition, Vokey’s online Wedgeworks program promotes limited edition models and allows golfers to customize and personalize their wedges. Vokey Design wedges are the most played wedges by tour professionals. In 2016, they accounted for over 46% of all wedges in play on the PGA Tour, where they have been #1 every year since 2004.

17

Scotty Cameron Putters

Scotty Cameron Fine Milled Putters are developed through a specialized and iterative process that blends art and science to create high performance putters. Scotty’s design inspiration begins with studying the best players in the world and working with them to identify the consistent strengths and attributes of their putting. Scotty Cameron encourages a selection process that identifies the putter length, toe flow and appearance to deliver proper balance, shaft flex and feel to golfers and to encourage proper technique. Scotty Cameron putters consist of a range of products for each of these key selection criteria. In 2016, over one‑third of the putters played on the PGA Tour were Scotty Cameron putters, and over the past 21 years, Scotty Cameron putters have helped players win over 1,200 tournaments on the worldwide professional tours.

Using the scottycameron.com website as an information and services hub, we offer loyal brand fans the opportunity to connect more closely with the Scotty Cameron brand. Golfers can customize and personalize their putter(s) in the online Scotty Cameron Custom Shop. Through the popular “Club Cameron” loyalty program and Scotty’s online “Studio Store,” brand fans can purchase unique Scotty Cameron accessories. In 2014, we also opened the Scotty Cameron Gallery in Encinitas, California, and in 2016, we entered into a license agreement whereby a third party opened and operates a similar facility in Tokyo, Japan. Each of these facilities is a premium retail boutique which offers consumers the ability to experience the tour fitting process as well as purchase unique accessory items.

Titleist Golf Gear

Titleist golf gear products are designed and engineered using premium materials, paying particular attention to superior performance, function and style. We focus on the design and development of golf bags, headwear, gloves, travel gear, head covers and other golf gear. We provide personalization and customization within each category of Titleist golf gear, as well as certain licensed products, in order to meet the needs of the dedicated golfer and as part of our service to our accounts. We believe the golf gear business represents a sizable but highly fragmented opportunity with numerous competitors in each product category and geographical market. Titleist golf gear accounted for $136.2 million, or 9%, $129.4 million, or 9%, and $127.9 million, or 8%, of our net sales for the years ended December 31, 2016, 2015 and 2014, respectively.

Titleist golf gear includes:

|

· |

Golf Bags. Our golf bags are designed and engineered with a variety of models possessing distinct features and benefits, including our Tour Staff, Cart and Carry models. The Titleist Tour Staff, Cart and Carry golf bags are leading products sold at premium prices throughout our worldwide distribution network. According to Golf Datatech, our share of U.S. net sales of golf bags from on‑course golf shops and golf specialty retailers was approximately 19% for the year ended December 31, 2016, and our principal competitors in this category include Sun Mountain, Ping and Callaway. |

|

· |

Headwear. Titleist headwear is designed and developed with advanced fabrications and construction to provide performance benefits as well as desirable styling for the dedicated golfer. Our headwear seeks to deliver benefits such as moisture management, UV protections, a secure fit and durability. We offer many unique product models within our headwear lines that include fitted headwear, adjustable headwear, visors and weather protection, including waterproof and cold weather styles. |

|

· |

Golf Gloves. Our Titleist golf glove product portfolio is led by the Players Glove, which is the choice of many leading professionals around the globe and a top model with accounts. We offer a select group of models in most markets that includes the Players Glove, the Players‑Flex Glove and the Perma‑Soft Glove as well as the Players Custom Glove and the Q‑Mark Custom Glove, which are customizable models. The Titleist glove business is strategically aligned with the FootJoy glove business to ensure a comprehensive product portfolio for our accounts and complementary benefit to us. |

|

· |

Travel Gear. Titleist travel gear is offered to serve the business and lifestyle needs of our dedicated golfer audience. Meticulously constructed with premium materials, our different models of travel gear are thoughtfully designed with advanced fabrications and construction to provide functionality, quality and durability. We offer a range of models including golf club travel bags, cabin bags, backpacks, duffel bags and wheeled roller bags, as well as messenger bags and briefcases. |

18

|

· |

Head Covers and Other Golf Gear. Titleist serves the lifestyle and performance needs of our dedicated golfer audience with a variety of other products including head covers, umbrellas, towels, bag covers, shag bags, valuable pouches and cold weather gear. |

FootJoy Golf Wear

FootJoy is one of golf’s leading performance wear brands, which consists collectively of golf shoes, gloves and apparel. FootJoy products accounted for $433.1 million, or 28%, $418.9 million, or 28%, and $421.6 million, or 27%, of our total net sales for the years ended December 31, 2016, 2015 and 2014, respectively.

FootJoy Golf Shoes

FootJoy is the #1 shoe in golf and has been the #1 shoe on the PGA Tour for over six decades. With an exclusive focus on golf, FootJoy shoes are designed, developed and manufactured for all golfers in all golf shoe categories, including traditional, casual, athletic and spikeless. We are the global leader in golf shoes with approximately one‑third of the 2016 global wholesale golf shoe market, which we estimate was approximately $575 million.

The golf shoe category is one of the most demanding of all wearables as golf shoes must perform in all weather conditions, including extreme temperature and moisture exposure; be resistant to pesticides and fungicides; withstand frequent usage and extensive rounds of play; and provide consistent comfort, support and protection to the golfer in an average of over five miles in a walked round. Hence, golf shoes require extensive knowledge and expertise in foot morphology, walking and swing biomechanics, material science and application and sophisticated manufacturing and construction techniques.

Golf shoes are also a style and fashion driven category. FootJoy offers a large assortment of styles to suit the needs and tastes of all golfers. Although it has products that cater to all segments of the value chain, 90% of its 118 styles in the United States golf shoe offering as of December 31, 2015 were in the super premium (greater than $150 MSRP) or premium (greater than $100 MSRP) revenue categories. The breadth and scope of the FootJoy product line is commensurate with its leading sales position. To maintain and grow this leadership position in the category, new product launches and new styles comprise over 60% of its offerings each year in all significant markets around the world.

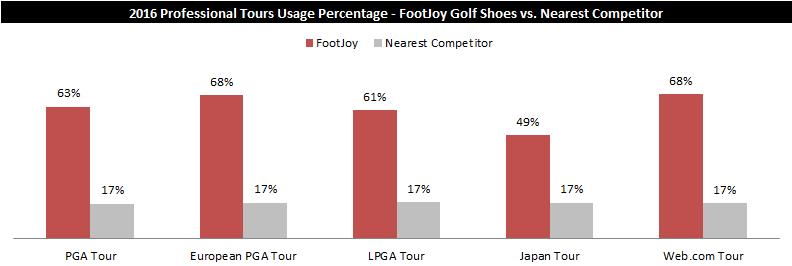

Although FootJoy seeks the greatest use at all levels of the game, it enjoys the leading usage by the most of the best players. The table below shows the percentage of professional golfers that used FootJoy shoes as compared to its nearest competitor for representative professional tours in 2016.

In addition to its stock offerings, FootJoy is a leader in the customization of golf shoe styles and designs. FootJoy’s MyJoys custom golf shoe portal provides individual choices for style, color, personal IDs and team logos that are produced to order for golfers around the world. We believe it is the largest choice offering in the golf shoe category and provides a service and personal expression capability that creates brand loyalty and repeat purchases.

19

FootJoy Gloves

FootJoy is the #1 glove in golf. We are the global leader in golf gloves with approximately one‑third of the 2015 global wholesale golf glove market, which we estimate was approximately $230 million. FootJoy is over three times larger than Titleist in the category, which is the #2 brand worldwide in sales. FootJoy is the leader in sales for all sub‑categories of the glove business, including leather construction, synthetic, leather/synthetic combinations and all specialty gloves including rain and winter specific offerings.

As in the golf shoe category, FootJoy has a long standing leadership position in the glove business that is the result of a deep understanding of golfer needs and expectations for performance, fit, comfort and quality. FootJoy offers the largest variety of glove designs and specifications to meet the needs of all golfers, including high quality, thin leather construction, advanced synthetics and leather/synthetic combinations, and specialty applications such as the world’s leading rain and winter golf gloves. FootJoy has enjoyed leadership of the category since the mid‑1980s and is the market leader in every significant golf market around the world. The table below shows the percentage of professional golfers that used FootJoy and Titleist gloves as compared to their nearest competitor for representative professional tours in 2016.

FootJoy Outerwear and Apparel

FootJoy’s most recent brand extensions have been the entry into the golf outerwear and golf apparel markets. FootJoy’s goal for outerwear is to “make every day playable” and extend the golf season by providing products for rain, wind and cold conditions. FootJoy entered the outerwear category in 1996 with innovative designs and materials and became the leader in net sales in the United States by 2005 and still holds this position today. According to Golf Datatech, our share of U.S. net sales of golf outerwear from on‑course golf shops and golf specialty retailers was approximately 27% for the year ended December 31, 2016, and our principal competitors in this category include Nike, Zero Restriction and Adidas. The brand’s longer term goal is to establish itself as the #1 golf outerwear product worldwide.

The FootJoy outerwear line is predicated on the FootJoy Layering System with three layers: base layer for moisture management, mid layer for temperature control and an outer layer for weather protection. The layer system allows for easy adjustment on the course with maximum comfort and protection. As in its successful golf shoe and glove categories, FootJoy outerwear built its leadership position in the United States by utilizing premium materials and design know‑how to build a complete offering of specialized products to meet the unique needs of the golfer in all weather extremes.

FootJoy fully entered the adjacent category of general golf apparel in 2012 with a tightly focused offering for men in the U.S. market. The line was extended to markets in Europe and Asia in the following years and now enjoys wide appeal and a growing share in most markets around the world. We believe it is one of the fastest growing brands in the men’s general golf apparel market. According to Golf Datatech, our share of U.S. net sales of men’s general golf apparel and outerwear from on‑course golf shops and golf specialty retailers was approximately 11% for the year ended December 31, 2016. The general golf apparel market represents a sizable but highly fragmented opportunity with numerous competitors in each geographical market, including Nike, Adidas and Under Armour.

20

FootJoy more broadly entered the U.S. women’s golf apparel market in early 2016 under the trademark Golfleisure. The styling is appropriate for golf and inspired by the current athleisure segment of women’s apparel in other categories and uses. According to Golf Datatech our share of U.S. net sales of women’s golf apparel and outerwear from on‑course golf shops and golf specialty retailers was approximately 3% for the year ended December 31, 2016, and our principal competitors in this category include Nike, EP Pro and Adidas. Plans include expansion of distribution to other markets in Europe and Asia during 2017.

Product Launch Cycles

We maintain differentiated and disciplined product launch cycles across our portfolio, which has contributed to stable and resilient growth over the long‑run. This approach gives our R&D teams a period of time we believe is necessary to develop superior performing products versus the prior generation models. As a result, we are able to manage our product transitions and inventory from one generation to the next more efficiently and effectively, both internally and with our trade partners.

Product introductions generally stimulate net sales as the golf retail channel takes on inventory of new products. Reorders of these new products then depend on the rate of sell‑through. Announcements of new products can often cause our customers to defer purchasing additional golf equipment until our new products are available. The varying product introduction cycles described below may cause our results of operations to fluctuate as each product line has different volumes, prices and margins.

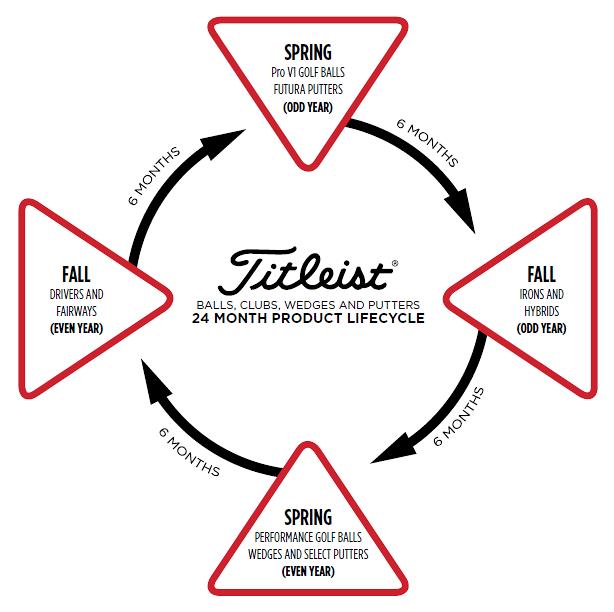

Titleist Golf Balls Segment

We launch new Titleist golf ball models on a two‑year cycle, with new product launches of Pro V1 and Pro V1x, our premium performance models, generally occurring in the first quarter of odd‑numbered years and new product launches of NXT Tour, Velocity and DT, our performance models, generally occurring in the first quarter of even‑numbered years. For new golf ball models, sales occur at a higher rate in the year of the initial launch than in the second year. Given the Pro V1 franchise is our highest volume and our highest priced product, we typically have higher net sales in our Titleist golf ball segment in odd‑numbered years.

Titleist Golf Clubs Segment

We generally launch new Titleist golf club models on a two‑year cycle. Since the fall of 2014, we have generally used the following product launch cycle, and at present we anticipate continuing to use this product launch cycle going forward because we believe it aligns our launches with the purchase habits of dedicated golfers. In general, we launch:

|

· |

drivers and fairways in the fourth quarter of even‑numbered years, which typically results in an increase in sales of drivers and fairways during such quarter because retailers take on initial supplies of these products as stock inventory, with increased sales generated by such new products continuing the following spring or summer of odd‑numbered years; |

|

· |

irons and hybrids in the fourth quarter of odd‑numbered years, with the majority of sales generated by such new products occurring in the following spring or summer of even‑numbered years because a higher percentage of our new irons and hybrids as compared to our drivers and fairways are sold through on a custom fit basis and the spring or summer is when golfers tend to make such custom fit purchases; |