Attached files

| file | filename |

|---|---|

| EX-21.1 - EX-21.1 - Daseke, Inc. | a17-8418_1ex21d1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K/A

(Amendment No. 1)

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of The Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): February 27, 2017

DASEKE, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

001-37509 |

|

47-3913221 |

|

15455 Dallas Parkway, Suite 440 |

|

75001 |

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

Registrant’s Telephone Number, Including Area Code: (972) 248-0412

Not applicable

(Former Name or Former Address, If Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

oWritten communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

oSoliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

oPre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

oPre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Explanatory Note

This Amendment No. 1 on Form 8-K/A (this “Amendment”) to the Current Report on Form 8-K of Daseke, Inc., originally filed with the Securities and Exchange Commission (the “SEC”) on March 3, 2017 (the “ Original Form 8-K”), is being filed solely to amend and restate in their entirety Item 2.01 and Item 9.01 in the Original Form 8-K. No other changes have been made to the Original Form 8-K. References to “this Form 8-K” are to the Original Form 8-K as amended by this Amendment.

Introductory Note

On February 27, 2017 (the “Closing Date”), the registrant consummated the previously announced merger of a wholly owned subsidiary of the registrant (“Merger Sub”) with and into Daseke, Inc., with Daseke, Inc. surviving (the “Surviving Company”) as a direct wholly owned subsidiary of the registrant (the “Business Combination”), in accordance with the Agreement and Plan of Merger, dated December 22, 2016 (the “Merger Agreement”), by and among the registrant, HCAC Merger Sub, Inc., Daseke, Inc. and Don R. Daseke, solely in his capacity as the Stockholder Representative (as defined therein).

In connection with the closing of the Business Combination (the “Closing”), the Surviving Company, a direct wholly owned subsidiary of the registrant, changed its name from Daseke, Inc. to Daseke Companies, Inc., and the registrant changed its name from Hennessy Capital Acquisition Corp. II to Daseke, Inc. The registrant (now named Daseke, Inc.) is a holding company and derives all of its operating income from its subsidiary, Daseke Companies, Inc.

Unless the context otherwise requires, “we,” “us,” “our” and the “Company” refer to Daseke, Inc. and its consolidated subsidiaries at and after the Closing, “Daseke” refers to Daseke, Inc. and its consolidated subsidiaries prior to the Closing, and “Hennessy Capital” refers to the registrant prior to the Closing.

In connection with its execution of the Merger Agreement, Hennessy Capital entered into, among other things, backstop and subscription agreements (the “Backstop and Subscription Agreements”) with certain institutional accredited investors (such investors referred to collectively as the “Backstop Commitment Investors”) and preferred subscription agreements with certain institutional accredited investors (collectively, the “Preferred Financing Investors”). In the Backstop and Subscription Agreements, the Backstop Commitment Investors made a commitment (the “Backstop Commitment”) pursuant to which they agreed to purchase an aggregate of up to $35.0 million in shares of Hennessy Capital common stock (as and to the extent requested by Hennessy Capital), through (x) open market or privately negotiated transactions with third parties (including forward contracts), (y) a private placement to occur concurrently with the consummation of the Business Combination at a purchase price of $10.00 per share, or (z) a combination thereof. In the preferred subscription agreements, the Preferred Financing Investors agreed to purchase from Hennessy Capital, concurrent with the consummation of the Closing, 650,000 shares of the Company’s 7.625% Series A Convertible Preferred Stock (the “Series A Preferred Stock”) for an aggregate purchase price of $65.0 million (the “Preferred Financing”).

On February 24, 2017, Hennessy Capital exercised the Backstop Commitment in full, and the Backstop Commitment Investors purchased an aggregate of $35.0 million in shares of Hennessy Capital common stock through open market or privately negotiated transactions with third parties at a purchase price of up to $10.00 per share.

Item 2.01 Completion of Acquisition or Disposition of Assets.

The disclosure set forth under “Introductory Note” above and in Item 2.01 “Completion of Acquisition or Disposition of Assets” in the Company’s Current Report on Form 8-K filed with the SEC on February 27, 2017 is incorporated in this Item 2.01 by reference.

Prior to the Closing, Hennessy Capital was a shell company with no operations, formed as a vehicle to effect a business combination with one or more operating businesses. After the Closing, the Company became a holding company whose assets primarily consist of interests in its direct wholly-owned subsidiary, Daseke

Companies, Inc. and the direct and indirect subsidiaries thereof. The following information is provided about the business of the Company following the consummation of the Business Combination,

Cautionary Note Regarding Forward-Looking Statements

We make forward-looking statements in this Form 8-K, including in the statements incorporated herein by reference. These forward-looking statements relate to expectations for future financial performance, business strategies or expectations for our business. These forward-looking statements are often preceded by, followed by or include the words “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target,” “will” or similar expressions. Specifically, forward-looking statements may include statements relating to:

·the benefits of the Business Combination;

·the future financial performance of the Company following the Business Combination;

·changes in the market for the Company’s services; and

·expansion plans and opportunities, including future acquisitions or additional business combinations.

These forward-looking statements are based on information available as of the date of this Amendment (or, in the case of forward-looking statements incorporated herein by reference, as of the date of they were originally made), and expectations, forecasts and assumptions based on such information, and involve a number of judgments, risks and uncertainties. Accordingly, forward-looking statements should not be relied on as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

·the outcome of any legal proceedings that may be instituted against us following consummation of the Business Combination and the transactions contemplated thereby;

·the inability to maintain the listing of the Company’s common stock and warrants on The Nasdaq Capital Market following the Business Combination;

·the risk that the Business Combination disrupts current plans and operations as a result of the consummation of the transactions contemplated thereby;

·the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition and the Company’s ability to grow and manage growth profitably;

·the possibility that we may be adversely affected by other economic, business or competitive factors;

·changes in applicable laws or regulations; and

·other risks and uncertainties indicated in Hennessy Capital’s definitive proxy statement dated February 6, 2017 (the “Proxy Statement”), including those under “Risk Factors—Risk Factors Relating to Daseke’s Business and Industry” beginning on page 63, as well as those identified under “Risk Factors” in this Item 2.01.

Business

The business of the Company, including a description of its properties, is described in the Proxy Statement in the section entitled “Information About Daseke” beginning on page 229, which is incorporated by reference herein. The business of Hennessy Capital is described in the Proxy Statement in the Section entitled “Information About Hennessy Capital” beginning on page 208, which incorporated by reference herein. The below provides additional information about the Company’s business.

Overview

The Company is a leading consolidator of the open deck freight market in North America and, of the 50 largest U.S. trucking companies, Daseke was one of the fastest-growing companies in 2015.(1) Through its acquisition of nine operating companies, the Company believes it has become the largest owner of open deck equipment(2) and

(1) Journal of Commerce, April 2016

(2) CCJ Top 250, September 2016

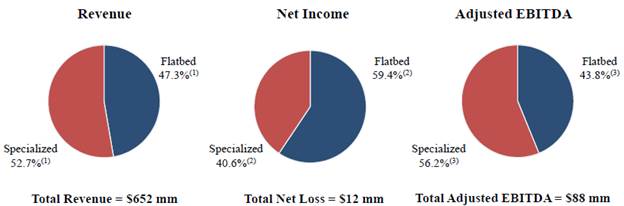

the second largest provider of open deck transportation and logistics solutions by revenue in North America.(3) From 2009 to 2016, Daseke grew revenue from $30 million to $652 million at a compound annual growth rate (“CAGR”) of 55%. Although net loss increased from $0.4 million to $12.3 million from 2009 to 2016, Adjusted EBITDA grew from $6 million to $88 million at a CAGR of 47%.(4)

The Company operates an “asset right” business model that combines strategic equipment ownership with complementary asset-light operations, which maximizes scale, growth, flexibility and profitability. Asset-based operations have the benefit of providing shippers with certainty of delivery and continuity of operations, which is often a customer requirement. Alternatively, the Company’s asset-light operations offer flexibility and scalability to meet customers’ dynamic needs and have lower fixed costs, lower capital expenditure requirements and higher returns on invested capital. The Company’s asset-light operations provide the ability to expand during periods of high demand with minimal incremental investment and the ability to contract during times of lower demand with limited redundancy costs or under-utilized assets. The Company’s asset-light service solutions consist of owner-operator transportation and freight brokerage, which generated approximately 34% of Daseke’s freight and brokerage revenue in 2016.

The Company’s open deck fleet consists of approximately 2,900 tractors and 6,300 trailers, which allows it to serve the largest national customers throughout North America. In 2016, Daseke’s company and owner-operator drivers drove approximately 247 million miles. The Company provides solutions that can broadly be classified under three categories:

· Company freight (66% of Daseke’s 2016 freight and brokerage revenue) are loads that are fulfilled by company-owned equipment. As of December 31, 2016, Daseke operated a fleet of 2,300 company-owned tractor units and 6,300 trailers, supported by 2,100 company drivers.

· Owner-operator freight (20% of Daseke’s 2016 freight and brokerage revenue) consists of loads transported by independent contractors who provide asset-light capacity to the Company under exclusive arrangements. As of December 31, 2016, Daseke’s owner-operators operated a fleet of 600 tractor units.

· Freight brokerage (14% of Daseke’s 2016 freight and brokerage revenue) refers to non-asset services in which the Company arranges for third-party transportation and logistics companies under non-exclusive contractual arrangements to haul freight that does not fit within its network or economic objectives. The Company leverages relationships with a large and diverse group of more than 5,000 third-party carriers to provide scalable capacity and reliable service to its customers.

The Company provides these solutions through two reportable segments: Flatbed Solutions and Specialized Solutions.

· Flatbed Solutions focuses on delivering transportation and logistics solutions that principally require the use of flatbed and retractable-sided transportation equipment. The Company’s Flatbed Solutions segment hauls construction products, building materials, roofing, aluminum, iron and steel, among other products. As of December 31, 2016, Daseke’s Flatbed Solutions segment operated 1,600 tractors and 2,900 trailers. Daseke’s Flatbed Solutions segment generated revenue of $310 million in 2016.

· Specialized Solutions focuses on delivering transportation and logistics solutions that principally include super heavy haul, high-value customized, over-dimensional, step deck and removable gooseneck (RGN) solutions. Many of the shippers served by the Company’s Specialized Solutions segment require highly

(3) “Top 100 For-Hire Carriers,” 2016 Transport Topics

(4) Adjusted EBITDA is not a recognized measure under accounting principles that are generally accepted in the United States of America. For a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk—Non-GAAP Financial Measures.”

engineered solutions and customized equipment to meet their unique transportation needs. Examples of the products the Company’s Specialized Solutions segment haul include aviation parts, wind turbines, agricultural equipment, building and construction equipment, manufacturing equipment and industrial machinery. As of December 31, 2016, Daseke’s Specialized Solutions segment operated 1,300 tractors and 3,400 trailers. Daseke’s Specialized Solutions segment generated revenue of $346 million in 2016.

Below are charts that show the contribution of each reportable segment to Daseke’s consolidated total revenue, net income (loss) and Adjusted EBITDA for 2016. Adjusted EBITDA is not a recognized measure under accounting principles generally accepted in the United States (“GAAP”). For a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net loss, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk—Non-GAAP Financial Measures” below.

(1) Percentages are calculated based on revenues of each segment, inclusive of $2.1 million and $2.4 million of intersegment revenues for the Flatbed Solutions segment and the Specialized Solutions segment, respectively. Such intersegment revenues are eliminated in Daseke’s consolidated results.

(2) Percentages are calculated based on the net income of each segment, without including $14.6 million of unallocated corporate overhead in either the numerator or denominator.

(3) Percentages are calculated based on the Adjusted EBITDA of each segment, without including $2.8 million of unallocated corporate overhead in either the numerator or denominator.

Operations

Revenue Equipment. As of December 31, 2016, Daseke operated 2,300 company-owned tractors with an average age of 2.2 years. Daseke also had under contract 600 tractors owned and operated by independent contractors as of December 31, 2016. Daseke also operated 6,300 trailers as of December 31, 2016.

Customers. The Company believes that it provides one of the most comprehensive transportation and logistics solutions offerings in the open deck industry. The Company delivers a diverse offering of transportation and logistics solutions to approximately 3,600 customers across 49 U.S. states, Canada and Mexico through two reportable segments: Flatbed Solutions and Specialized Solutions. In 2016, Daseke’s Flatbed Solutions segment provided transportation and logistics solutions to more than 1,900 customers, and Daseke’s Specialized Solutions segment provided unique, value-added transportation and logistics solutions to more than 2,100 customers. See Note 20 of Daseke’s audited consolidated financial statements included in this Form 8-K for information on its two reportable segments.

A material portion of the Company’s revenue is generated from its major customers, the loss of one or more of which could have a material adverse effect on its business. In 2016, no customer of the Flatbed Solutions segment or the Specialized Solutions segment accounted for more than 10% of its consolidated total revenue.

Employees and Independent Contractors

As of December 31, 2016, there were approximately 2,892 full-time employees in Daseke’s total employee headcount of approximately 2,900, which includes approximately 2,100 drivers. The Company is not a party to any collective bargaining agreements.

The Company also contracts with owner-operator drivers to provide and operate tractors, which provide additional revenue equipment capacity. Independent contractors own their own tractors and are responsible for all associated expenses, including financing costs, fuel, maintenance, insurance and highway use taxes. As of December 31, 2016, Daseke had 600 independent contractors, who accounted for approximately 23% of total miles in 2016.

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available to the public through the Internet at the SEC’s website at http://www.sec.gov. You may also read and copy any document we file with the SEC at the SEC’s public reference room at 100 F Street, N.E. Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information about its public reference facilities and their copy charges.

We also make available free of charge on our Internet website http://investor.daseke.com all of the documents that we file with the SEC as soon as reasonably practicable after we electronically file those documents with the SEC. Information contained on our website is not incorporated by reference into this Form 8-K, and you should not consider information contained on our website as part of this Form 8-K.

Risk Factors

Risk factors related to the Company’s business, operations and industry and ownership of our common stock are described in the Proxy Statement in the section entitled “Risk Factors” beginning on page 63, which is incorporated by reference herein. The below provides additional risk factors. These risk factors are not exhaustive. We may face additional risks and uncertainties that are not presently known to us, or that we currently deem immaterial, which may also impair our business. The risk factors should be read in conjunction with the financial statements and notes to the financial statements included elsewhere in this Form 8-K.

The Company may not be able to generate sufficient cash to service all of its indebtedness and may be forced to take other actions to satisfy its obligations under applicable debt instruments, which may not be successful.

As of February 28, 2017, the Company had approximately $295.0 million of indebtedness outstanding. Its ability to make scheduled payments on or to refinance its indebtedness obligations depends on its financial condition and operating performance, which are subject to prevailing economic and competitive conditions and certain financial, business and other factors beyond its control. The Company may not be able to maintain a level of cash flows from operating activities sufficient to permit it to pay the principal, premium, if any, and interest on its indebtedness.

If the Company’s cash flows and capital resources are insufficient to fund debt service obligations, the Company may be forced to reduce or delay investments and capital expenditures, sell assets, seek additional capital or restructure or refinance indebtedness. The Company’s ability to restructure or refinance indebtedness will depend on the condition of the capital markets and its financial condition at such time. Any refinancing of indebtedness could be at higher interest rates and may require the Company to comply with more onerous covenants, which could further restrict business operations. The terms of existing or future debt instruments may restrict the Company from adopting some of these alternatives. In addition, any failure to make payments of interest and principal on outstanding indebtedness on a timely basis would likely result in a reduction of the Company’s credit rating, which could harm its ability to incur additional indebtedness. In the absence of sufficient cash flows and capital resources, the Company could face substantial liquidity problems and might be required to dispose of material assets or operations to meet debt service and other obligations. However, the proceeds of any such disposition may not be adequate to meet any debt service obligations then due.

The Company’s leverage and debt service obligations may adversely affect its financial condition, results of operations, business prospects and ability to make payments on its debt obligations.

As of February 28, 2017, the Company had approximately $295.0 million of indebtedness outstanding. The Company’s level of indebtedness could adversely affect it in several ways, including the following:

· require the Company to dedicate a substantial portion of its cash flow from operations to service its existing debt, thereby reducing the cash available to finance its operations and other business activities;

· limit management’s discretion in operating its business and its flexibility in planning for, or reacting to, changes in its business and the industry in which it operates;

· increase its vulnerability to downturns and adverse developments in its business and the economy generally;

· limit its ability to access the capital markets to raise capital on favorable terms or to obtain additional financing for working capital, capital expenditures or acquisitions or to refinance existing indebtedness;

· place restrictions on its ability to obtain additional financing, make investments, lease equipment, sell assets and engage in business combinations;

· make it more likely that a reduction in its borrowing base following a periodic redetermination could require it to repay a portion of its then-outstanding bank borrowings;

· make it vulnerable to increases in interest rates as indebtedness under the Company’s credit facilities may vary with prevailing interest rates;

· place it at a competitive disadvantage relative to competitors with lower levels of indebtedness in relation to their overall size or less restrictive terms governing their indebtedness; and

· make it more difficult for it to satisfy its obligations under its debt instruments and increase the risk that it may default on its debt obligations.

Increases in interest rates could adversely affect the Company’s business.

The Company’s business and operating results can be harmed by factors such as the availability, terms of and cost of capital, increases in interest rates or a reduction in credit rating. These changes could cause the Company’s cost of doing business to increase and limit its ability to pursue acquisition opportunities. For example, as of February 28, 2017, outstanding borrowings under the Term Loan Facility (as defined in the Original Form 8-K) was $250 million, and a 1.0% increase in interest rates would result in an increase in annual interest expense of approximately $2.5 million, assuming the $250 million in debt is outstanding for the full year, before the effects of income taxes. Recent and continuing disruptions and volatility in the global financial markets may lead to a contraction in credit availability impacting its ability to finance its operations. The Company requires continued access to capital. A significant reduction in cash flows from operations or the availability of credit could materially and adversely affect its ability to achieve its planned growth and operating results.

The Company derives a material portion of its revenue from its major customers, the loss of one or more of which could have a material adverse effect on its business.

A material portion of the Company’s revenue is generated from its major customers, the loss of one or more of which could have a material adverse effect on the Company’s business. In 2016 and 2015, Daseke’s top ten customers, based on revenue, accounted for approximately 23% and 33%, respectively, of Daseke’s revenue, and Daseke’s largest customer accounted for approximately 8% of its revenue in both 2016 and 2015. A material portion of the Company’s freight is from customers in the building materials industry, and as such, the Company’s results may be more susceptible to trends in construction cycles, which are affected by numerous factors, including rates of infrastructure spending, real estate equity values, interest rates and general economic conditions, than carriers that do not have this concentration.

Economic conditions and capital markets may adversely affect the Company’s customers and their ability to remain solvent. The Company’s customers’ financial difficulties can negatively impact the Company’s results of operations and financial condition and the Company’s ability to comply with the covenants in its debt agreements,

especially if they were to delay or default on payments to the Company. Generally, the Company does not have contractual relationships that guarantee any minimum volumes with customers, and the Company cannot assure you that customer relationships will continue as presently in effect. A reduction in, or termination of, the Company’s services by one or more of its major customers could have a material adverse effect on the Company’s business and operating results.

The Company’s contractual agreements with its owner-operators expose it to risks that it does not face with its company drivers.

The Company relies, in part, upon independent contractor owner-operators to perform the services for which it contracts with customers. Approximately 20% of Daseke’s freight was carried by independent contractor owner-operators in 2016. The Company’s reliance on independent contractor owner-operators creates numerous risks for the Company’s business. For example, the Company provides financing to certain of its independent contractor owner-operators purchasing tractors from the Company. If owner-operators operating the tractors the Company financed default under or otherwise terminate the financing arrangement and the Company is unable to find a replacement owner-operator, the Company may incur losses on amounts owed to it with respect to the tractor in addition to any losses it may incur as a result of idling the tractor. Further, if the Company is unable to provide such financing in the future, due to liquidity constraints or other restrictions, the Company may experience a shortage of owner-operators available to it.

If the Company independent contractor owner-operators fail to meet the Company contractual obligations or otherwise fail to perform in a manner consistent with the Company’s requirements, the Company may be required to use alternative service providers at potentially higher prices or with some degree of disruption of the services that the Company provides to customers. If the Company fails to deliver on time, if its contractual obligations are not otherwise met, or if the costs of its services increase, then the Company’s profitability and customer relationships could be harmed.

The financial condition and operating costs of the Company’s independent contractor owner-operators are affected by conditions and events that are beyond the Company’s control and may also be beyond their control. Adverse changes in the financial condition of the Company’s independent contractor owner-operators or increases in their equipment or operating costs could cause them to seek higher revenues or to cease their business relationships with the Company. The prices the Company charges its customers could be impacted by such issues, which may in turn limit pricing flexibility with customers, resulting in fewer customer contracts and decreasing the Company’s revenues.

Independent contractor owner-operators typically use tractors, trailers and other equipment bearing the Company’s trade names and trademarks. If one of the Company’s independent contractor owner-operators is subject to negative publicity, it could reflect on the Company and have a material adverse effect on the Company’s business, brand and financial performance. Under certain laws, the Company could also be subject to allegations of liability for the activities of its independent contractor owner-operators.

Owner-operators are third-party service providers, as compared to company drivers who are employed by the Company. As independent business owners, the Company’s owner-operators may make business or personal decisions that conflict with the Company’s best interests. For example, if a load is unprofitable, route distance is too far from home or personal scheduling conflicts arise, an owner-operator may deny loads of freight from time to time. In these circumstances, the Company must be able to timely deliver the freight in order to maintain relationships with customers.

The Company’s total assets include goodwill and indefinite-lived intangibles. If the Company determines that these items have become impaired in the future, net income could be materially and adversely affected.

As of December 31, 2016, Daseke had recorded goodwill of $89.0 million and indefinite-lived intangible assets of $30.1 million, net of accumulated amortization. Goodwill represents the excess of cost over the fair market value of net assets acquired in business combinations. In accordance with Financial Accounting Standards Board

Accounting Standards Codification, Topic 350, “Intangibles — Goodwill and Other,” the Company tests goodwill and indefinite-lived intangible assets for potential impairment annually and between annual tests if an event occurs or circumstances change that would more likely than not reduce the fair value below its carrying amount. Any excess in carrying value over the estimated fair value is charged to the Company’s results of operations. Further, the Company may never realize the full value of its intangible assets. Any future determination requiring the write-off of a significant portion of intangible assets could have an adverse effect on the Company’s financial condition and results of operations. If there are changes to the methods used to allocate carrying values, if management’s estimates of future operating results change, if there are changes in the identified reporting units or if there are changes to other significant assumptions, the estimated carrying values and the estimated fair value of the Company’s goodwill and long-lived assets could change significantly, and could result in future non-cash impairment charges, which could materially impact its results of operations and financial condition for any such future period.

Selected Historical Consolidated Financial and Other Data of Daseke

The following selected historical consolidated financial information is provided to assist in the analysis of Daseke financial performance. The table below provides Daseke’s revenue, net income (loss), Adjusted EBITDA and free cash flow for the years ended December 31, 2016, 2015, 2014, 2013, 2012, 2011, 2010 and 2009 on a historical basis. The historical revenue, net income (loss), Adjusted EBITDA and free cash flow for the years ended December 31, 2013, 2012, 2011, 2010 and 2009 are derived from Daseke’s audited historical consolidated financial statements not included in this Form 8-K. The historical revenue, net income (loss), Adjusted EBITDA and free cash flow for the years ended December 31, 2016, 2015 and 2014 are derived from Daseke’s audited historical consolidated financial statements included elsewhere in this Form 8-K.

|

|

|

Year Ended December 31, |

| ||||||||||||||||||||||

|

(in thousands) |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

|

2012 |

|

2011 |

|

2010 |

|

2009 |

| ||||||||

|

Total revenue |

|

$ |

651,802 |

|

$ |

678,845 |

|

$ |

542,711 |

|

$ |

206,543 |

|

$ |

119,520 |

|

$ |

49,958 |

|

$ |

39,760 |

|

$ |

30,324 |

|

|

Net income (loss) |

|

$ |

(12,279 |

) |

$ |

3,263 |

|

$ |

1,300 |

|

$ |

(2,976 |

) |

$ |

3,151 |

|

$ |

2,976 |

|

$ |

1,263 |

|

$ |

(381 |

) |

|

Adjusted EBITDA(1) |

|

$ |

88,240 |

|

$ |

97,304 |

|

$ |

70,346 |

|

$ |

23,905 |

|

$ |

19,179 |

|

$ |

9,289 |

|

$ |

7,330 |

|

$ |

6,455 |

|

|

Free cash flow (1) |

|

$ |

56,571 |

|

$ |

30,335 |

|

$ |

(332 |

) |

$ |

3,180 |

|

$ |

(412 |

) |

$ |

4,942 |

|

$ |

5,754 |

|

$ |

5,907 |

|

(1) Adjusted EBITDA and free cash flow are not recognized measures under GAAP. For a definition of Adjusted EBITDA and free cash flow and a reconciliation of Adjusted EBITDA and free cash flow to net income (loss), see “Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk—Non-GAAP Financial Measures” below.

The following table sets forth selected historical consolidated financial and other data as of and for the years ended December 31, 2016, 2015 and 2014. Such financial data are derived from Daseke’s audited consolidated financial statements included elsewhere in this Form 8-K. The historical results presented below and above are not necessarily indicative of the results to be expected for any future period and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk” below and Daseke’s audited consolidated financial statements and the related notes appearing elsewhere in this Form 8-K.

|

|

|

Year Ended December 31, |

| |||||||

|

(Dollars in thousands, except share and per share data) |

|

2016 |

|

2015 |

|

2014 |

| |||

|

Consolidated statement of operations data: |

|

|

|

|

|

|

| |||

|

Total revenue |

|

$ |

651,802 |

|

$ |

678,845 |

|

$ |

542,711 |

|

|

Operating expenses: |

|

|

|

|

|

|

| |||

|

Salaries, wages and employee benefits |

|

197,789 |

|

178,703 |

|

132,205 |

| |||

|

Fuel |

|

66,865 |

|

70,296 |

|

88,031 |

| |||

|

Operations and maintenance |

|

96,100 |

|

98,734 |

|

59,274 |

| |||

|

Purchased freight |

|

154,054 |

|

181,985 |

|

150,654 |

| |||

|

Taxes and licenses |

|

9,222 |

|

9,228 |

|

7,304 |

| |||

|

Insurance and claims |

|

19,114 |

|

19,655 |

|

15,446 |

| |||

|

Depreciation and amortization |

|

67,500 |

|

63,573 |

|

48,575 |

| |||

|

(Gain) loss on disposition of revenue property and equipment |

|

(116 |

) |

(2,184 |

) |

934 |

| |||

|

Impairments |

|

2,005 |

|

— |

|

1,838 |

| |||

|

Other operating expenses |

|

28,636 |

|

27,847 |

|

19,631 |

| |||

|

Total operating expenses |

|

641,169 |

|

647,837 |

|

523,892 |

| |||

|

Income from operations |

|

10,633 |

|

31,008 |

|

18,819 |

| |||

|

Interest expense |

|

23,124 |

|

20,602 |

|

15,978 |

| |||

|

Other income |

|

(375 |

) |

(320 |

) |

(243 |

) | |||

|

Total other expense |

|

22,749 |

|

20,282 |

|

15,735 |

| |||

|

Income (loss) before provision for income taxes |

|

(12,116 |

) |

10,726 |

|

3,084 |

| |||

|

Provision for income taxes |

|

163 |

|

7,463 |

|

1,784 |

| |||

|

Net income (loss) |

|

$ |

(12,279 |

) |

$ |

3,263 |

|

$ |

1,300 |

|

|

Dividends declared per preferred share |

|

$ |

75.00 |

|

$ |

75.00 |

|

$ |

75.00 |

|

|

Net income (loss) available to common stockholders |

|

$ |

(17,049 |

) |

$ |

(1,473 |

) |

$ |

272 |

|

|

Basic net income (loss) per common share |

|

$ |

(117.18 |

) |

$ |

(10.13 |

) |

$ |

2.02 |

|

|

Diluted net income (loss) per common share |

|

$ |

(117.18 |

) |

$ |

(10.13 |

) |

$ |

1.94 |

|

|

Basic weighted average common shares outstanding |

|

145,495 |

|

145,495 |

|

134,581 |

| |||

|

Diluted weighted average common shares outstanding |

|

145,495 |

|

145,495 |

|

140,280 |

| |||

|

Consolidated balance sheet data (at end of period): |

|

|

|

|

|

|

| |||

|

Cash |

|

$ |

3,695 |

|

$ |

4,886 |

|

$ |

2,406 |

|

|

Property and equipment, net |

|

$ |

318,747 |

|

$ |

354,535 |

|

$ |

303,515 |

|

|

Total assets |

|

$ |

570,235 |

|

$ |

627,607 |

|

$ |

509,922 |

|

|

Current liabilities |

|

$ |

92,398 |

|

$ |

109,669 |

|

$ |

89,224 |

|

|

Working capital(1) |

|

$ |

36,282 |

|

$ |

42,538 |

|

$ |

41,401 |

|

|

Long-term debt and other long-term liabilities |

|

$ |

374,774 |

|

$ |

397,888 |

|

$ |

313,583 |

|

|

Total stockholders’ equity |

|

$ |

103,063 |

|

$ |

120,050 |

|

$ |

107,115 |

|

|

Other financial data (unaudited): |

|

|

|

|

|

|

| |||

|

Adjusted EBITDA(2) |

|

$ |

88,240 |

|

$ |

97,304 |

|

$ |

70,346 |

|

|

Adjusted EBITDAR(2) |

|

$ |

101,177 |

|

$ |

106,261 |

|

$ |

76,641 |

|

|

Adjusted EBITDA Margin(2) |

|

13.5 |

% |

14.3 |

% |

13.0 |

% | |||

|

Free cash flow(2) |

|

$ |

56,571 |

|

$ |

30,335 |

|

$ |

(332 |

) |

|

Operating ratio |

|

98.4 |

% |

95.4 |

% |

96.5 |

% | |||

|

Adjusted operating ratio(2) |

|

95.6 |

% |

93.0 |

% |

93.4 |

% | |||

|

Operating statistics (unaudited): |

|

|

|

|

|

|

| |||

|

Total miles |

|

246,989,374 |

|

230,923,639 |

|

192,226,156 |

| |||

|

Company-operated tractors |

|

2,304 |

|

2,267 |

|

1,878 |

| |||

|

Owner-operated tractors |

|

609 |

|

702 |

|

735 |

| |||

|

Number of trailers |

|

6,347 |

|

5,977 |

|

5,515 |

| |||

(1) Working capital is defined as current assets (excluding cash) less current liabilities (excluding the current portion of long-term debt).

(2) Adjusted EBITDA, Adjusted EBITDAR, Adjusted EBITDA Margin, free cash flow and adjusted operating ratio are not recognized measures under GAAP. For a definition of Adjusted EBITDA, Adjusted EBITDAR, Adjusted EBITDA Margin, free cash flow and adjusted operating ratio, a reconciliation of Adjusted EBITDA, Adjusted EBITDAR and free cash flow to net income (loss) and a reconciliation of operating ratio to operating ratio, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures About Market Risk—Non-GAAP Financial Measures” below.

Unaudited Pro Forma Condensed Combined Financial Information

The following unaudited pro forma condensed combined financial statements give effect to the Business Combination under the acquisition method of accounting in accordance with Financial Accounting Standards Board (FASB) Accounting Standard Codification (“ASC”) Topic 805, Business Combinations (“ASC 805”). The Business Combination will be accounted for as a reverse merger in accordance with accounting principles generally accepted in the United States of America. Under this method of accounting, Hennessy Capital will be treated as the “acquired” company for financial reporting purposes. This determination was primarily based on Daseke comprising the ongoing operations of the combined company, Daseke’s senior management comprising the senior management of the combined company, and Daseke stockholders having a majority of the voting power of the combined company. For accounting purposes, Daseke will be deemed to be the accounting acquirer in the transaction and, consequently, the transaction will be treated as a recapitalization of Daseke (i.e., a capital transaction involving the issuance of stock by Hennessy Capital for the stock of Daseke). Accordingly, the consolidated assets, liabilities and results of operations of Daseke will become the historical financial statements of the combined company, and

Hennessy Capital’s assets, liabilities and results of operations will be consolidated with Daseke beginning on the acquisition date.

The historical consolidated financial information has been adjusted in these unaudited pro forma condensed combined financial statements to give effect to pro forma events that are (1) directly attributable to the Business Combination and the proposed related financing transactions, (2) factually supportable, and (3) with respect to the statements of operations, expected to have a continuing impact on the post-combination company. The unaudited pro forma condensed combined balance sheet is based on the historical audited consolidated balance sheet of Daseke, and the audited balance sheet of Hennessy Capital, as of December 31, 2016 and has been prepared to reflect the Business Combination and the proposed related financing transactions as if they occurred on December 31, 2016. The unaudited pro forma condensed combined statement of operations for the year ended December 31, 2016 combines the historical results of operations of Daseke together with the historical results for Hennessy Capital for the year ended December 31, 2016, giving effect to the Business Combination and the proposed related financing transactions as if they occurred on January 1, 2016.

The unaudited pro forma condensed combined statement of operations information for the year ended December 31, 2016 was derived from Daseke’s audited consolidated statement of operations and comprehensive loss for the year ended December 31, 2016 and Hennessy Capital’s audited statement of operations for the year ended December 31, 2016 included elsewhere in this Current Report on Form 8-K/A.

On January 5, 2017, Hennessy Capital consummated a transaction in which it received a $5 million release fee in exchange for releasing a party from a non-circumvention agreement with Hennessy Capital that was associated with a planned business combination with a third party that was not consummated. In connection with the receipt of this payment by Hennessy Capital, Hennessy Capital paid down approximately $6.6 million of liabilities accrued in connection with that business combination that did not close. The payment and settlement of these liabilities in January 2017 is not reflected in the unaudited pro forma condensed combined balance sheet because it is not related to the Business Combination.

These unaudited pro forma condensed combined financial statements are for informational purposes only. They do not purport to indicate the results that would actually have been obtained had the Business Combination and the proposed related financing transactions been completed on the assumed date or for the periods presented, or which may be realized in the future. The pro forma adjustments are based on the information currently available and the assumptions and estimates underlying the pro forma adjustments are described in the accompanying notes. Actual results may differ materially from the assumptions within the accompanying unaudited pro forma condensed combined financial information. The combined company will incur additional costs after the Business Combination in order to satisfy its obligations as a fully reporting public company. In addition, we anticipate the adoption of various stock compensation plans or programs (including the Incentive Plan) that are typical for employees, officers and directors of public companies. No adjustment to the unaudited pro forma statement of operations has been made for these items as they are not directly related to the Business Combination and amounts are not yet known.

The unaudited pro forma condensed combined financial information should be read in conjunction with the accompanying notes and the sections entitled “Daseke Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Hennessy Capital Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical financial statements and notes thereto of Daseke and Hennessy Capital, included elsewhere in this Form 8-K or in the Proxy Statement.

The unaudited pro forma condensed combined financial statements have been prepared based on: (i) 11,616,990 shares of Hennessy Capital common stock redeemed at the Closing ($116.2 million) pursuant to Hennessy Capital’s pre-Business Combination certificate of incorporation of Hennessy Capital, (ii) $65.0 million of Series A Preferred Stock issued in connection with Preferred Financing at the Closing and the refinancing of certain Daseke long-term debt with a new $250.0 million term loan.

Unaudited Pro Forma Condensed Combined Balance Sheet

As of December 31, 2016

(In thousands)

|

|

|

Hennessy |

|

Daseke |

|

Pro Forma |

|

Footnote |

|

Pro Forma |

| ||||

|

ASSETS |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Current assets |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Cash and cash equivalents |

|

$ |

591 |

|

$ |

3,695 |

|

$ |

199,599 |

|

3a |

|

$ |

36,476 |

|

|

|

|

|

|

|

|

184 |

|

3a |

|

|

| ||||

|

|

|

|

|

|

|

236,000 |

|

3a |

|

|

| ||||

|

|

|

|

|

|

|

(293,455 |

) |

3a |

|

|

| ||||

|

|

|

|

|

|

|

(116,170 |

) |

3b |

|

|

| ||||

|

|

|

|

|

|

|

(36,168 |

) |

3c |

|

|

| ||||

|

|

|

|

|

|

|

(23,000 |

) |

3d |

|

|

| ||||

|

|

|

|

|

|

|

200 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

65,000 |

|

3e |

|

|

| ||||

|

Accounts receivable, net |

|

— |

|

54,177 |

|

|

|

|

|

54,177 |

| ||||

|

Current portion of net investment in sales-type leases |

|

— |

|

3,516 |

|

|

|

|

|

3,516 |

| ||||

|

Prepaid expenses and other assets |

|

44 |

|

18,322 |

|

|

|

|

|

18,366 |

| ||||

|

Total current assets |

|

$ |

635 |

|

$ |

79,710 |

|

$ |

32,190 |

|

|

|

$ |

112,535 |

|

|

Cash and investments held in Trust Account |

|

199,783 |

|

— |

|

(199,599 |

) |

3a |

|

— |

| ||||

|

|

|

|

|

|

|

(184 |

) |

3a |

|

|

| ||||

|

Property and equipment, net |

|

— |

|

318,747 |

|

|

|

|

|

318,747 |

| ||||

|

Other intangible assets, net |

|

— |

|

71,653 |

|

|

|

|

|

71,653 |

| ||||

|

Goodwill |

|

— |

|

89,035 |

|

|

|

|

|

89,035 |

| ||||

|

Other long term assets |

|

— |

|

11,090 |

|

|

|

|

|

11,090 |

| ||||

|

TOTAL ASSETS |

|

$ |

200,418 |

|

$ |

570,235 |

|

$ |

(167,593 |

) |

|

|

$ |

603,060 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Current liabilities |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Current maturities of long-term debt |

|

$ |

— |

|

$ |

52,665 |

|

$ |

(52,665 |

) |

3a |

|

$ |

2,500 |

|

|

|

|

|

|

|

|

2,500 |

|

3a |

|

|

| ||||

|

Accounts payable |

|

328 |

|

5,954 |

|

|

|

|

|

6,282 |

| ||||

|

Accrued compensation |

|

— |

|

7,835 |

|

|

|

|

|

7,835 |

| ||||

|

Accrued expenses and taxes |

|

8,062 |

|

16,104 |

|

(2,600 |

) |

3d |

|

21,566 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Accrued insurance and claims and other current liabilities |

|

— |

|

9,840 |

|

|

|

|

|

9,840 |

| ||||

|

Total current liabilities |

|

$ |

8,390 |

|

$ |

92,398 |

|

$ |

(52,765 |

) |

|

|

$ |

48,023 |

|

|

Long-term liabilities |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Deferred underwriters’ fee |

|

7,185 |

|

— |

|

(7,185 |

) |

3d |

|

— |

| ||||

|

Long-term debt, net of current maturities |

|

— |

|

215,230 |

|

(174,347 |

) |

3a |

|

278,500 |

| ||||

|

|

|

|

|

|

|

4,117 |

|

3a |

|

|

| ||||

|

|

|

|

|

|

|

233,500 |

|

3a |

|

|

| ||||

|

Long-term deferred tax liability and other |

|

— |

|

93,101 |

|

|

|

|

|

93,101 |

| ||||

|

Subordinated debt |

|

— |

|

66,443 |

|

(66,443 |

) |

3a |

|

— |

| ||||

|

Common stock subject to possible redemption |

|

179,843 |

|

|

|

(179,843 |

) |

3d |

|

— |

| ||||

|

Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Preferred stock |

|

— |

|

1 |

|

65,000 |

|

3e |

|

65,000 |

| ||||

|

|

|

|

|

|

|

(1 |

) |

3e |

|

|

| ||||

|

Common stock |

|

1 |

|

1 |

|

2 |

|

3c |

|

4 |

| ||||

|

|

|

|

|

|

|

1 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

(1 |

) |

3e |

|

|

| ||||

|

Additional paid-in-capital |

|

14,752 |

|

117,807 |

|

266,651 |

|

3c |

|

$ |

150,959 |

| |||

|

|

|

|

|

|

|

(36,168 |

) |

3c |

|

|

| ||||

|

|

|

|

|

|

|

179,842 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

(9,753 |

) |

3d |

|

|

| ||||

|

|

|

|

|

|

|

(266,653 |

) |

3c |

|

|

| ||||

|

|

|

|

|

|

|

2 |

|

3e |

|

|

| ||||

|

|

|

|

|

|

|

(116,170 |

) |

3b |

|

|

| ||||

|

|

|

|

|

|

|

649 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Accumulated deficit |

|

(9,753 |

) |

(14,694 |

) |

(4,117 |

) |

3a |

|

(32,475 |

) | ||||

|

|

|

|

|

|

|

(16,464 |

) |

3d |

|

|

| ||||

|

|

|

|

|

|

|

200 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

2,600 |

|

3d |

|

|

| ||||

|

|

|

|

|

|

|

9,753 |

|

3e |

|

|

| ||||

|

Accumulated other comprehensive loss |

|

— |

|

(52 |

) |

|

|

|

|

(52 |

) | ||||

|

Total stockholders’ equity |

|

$ |

5,000 |

|

$ |

103,063 |

|

$ |

73,373 |

|

|

|

$ |

183,436 |

|

|

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY |

|

$ |

200,418 |

|

$ |

570,235 |

|

$ |

(167,593 |

) |

|

|

$ |

603,060 |

|

See accompanying notes to unaudited pro forma condensed combined financial information.

Unaudited Pro Forma Condensed Combined Statement of Operations

For the Year Ended December 31, 2016

(In thousands, except for per share information)

|

|

|

Hennessy |

|

Daseke |

|

Pro Forma |

|

Footnote |

|

Pro Forma |

| ||||

|

Net revenue |

|

$ |

— |

|

$ |

651,802 |

|

$ |

— |

|

|

|

$ |

651,802 |

|

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Operations expenses |

|

— |

|

390,617 |

|

|

|

|

|

390,617 |

| ||||

|

Purchased freight |

|

|

|

154,054 |

|

|

|

|

|

154,054 |

| ||||

|

Depreciation and amortization |

|

|

|

67,500 |

|

|

|

|

|

67,500 |

| ||||

|

Selling, general and administrative expenses |

|

9,991 |

|

26,993 |

|

(10,052 |

) |

4a |

|

26,932 |

| ||||

|

Impairment loss |

|

— |

|

2,005 |

|

— |

|

|

|

2,005 |

| ||||

|

Total operating expenses |

|

9,991 |

|

641,169 |

|

(10,052 |

) |

|

|

641,108 |

| ||||

|

Income from operations |

|

(9,991 |

) |

10,633 |

|

10,052 |

|

|

|

10,694 |

| ||||

|

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

| ||||

|

Interest and other income |

|

508 |

|

375 |

|

(508 |

) |

4b |

|

375 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Interest and financing costs |

|

— |

|

(23,124 |

) |

(18,200 |

) |

4c |

|

(19,700 |

) | ||||

|

|

|

|

|

|

|

21,624 |

|

4c |

|

|

| ||||

|

Total other income (expense) |

|

508 |

|

(22,749 |

) |

2,916 |

|

|

|

(19,325 |

) | ||||

|

Income (loss) before income taxes |

|

(9,483 |

) |

(12,116 |

) |

12,968 |

|

|

|

(8,631 |

) | ||||

|

Provision (benefit) for income taxes |

|

|

|

(163 |

) |

(1,362 |

) |

4c |

|

(1,525 |

) | ||||

|

Net income (loss) |

|

(9,483 |

) |

(12,279 |

) |

11,606 |

|

|

|

(10,156 |

) | ||||

|

Less: Dividends to preferred stockholders |

|

— |

|

(4,770 |

) |

4,770 |

|

4d |

|

— |

| ||||

|

Net income (loss) available to common stockholders |

|

$ |

(9,483 |

) |

$ |

(17,049 |

) |

$ |

16,376 |

|

|

|

$ |

(10,156 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Earnings (loss) per share available to common stockholders |

|

$ |

(1.46 |

) |

|

|

|

|

|

|

$ |

(0.27 |

) | ||

|

Weighted average shares outstanding — Basic and diluted |

|

6,490,000 |

|

|

|

31,226,000 |

|

5a |

|

37,716,000 |

| ||||

See accompanying notes to unaudited pro forma condensed combined financial information.

NOTES TO UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

1. Description of Transaction

Pursuant to the Merger Agreement and the transactions contemplated thereby, on February 27, 2017, Hennessy Capital consummated the acquisition of all of the outstanding capital stock of Daseke through a merger of a wholly owned subsidiary of the Company with and into Daseke, with Daseke surviving such merger as a direct wholly owned subsidiary of the Company.

The aggregate merger consideration paid upon the closing of the Business Combination (the “Closing Merger Consideration”) was $266.7 million comprised of an aggregate of 26,665,330 newly issued shares of Hennessy Capital common stock at a value of $10.00 per share. The Closing Merger Consideration was determined pursuant to the Merger Agreement and equaled the sum of (i) (a) $626 million, plus (b) approximately $1.8 million of adjusted Daseke cash, minus (c) approximately $341.2 million of Daseke indebtedness, approximately $0.3 million of unpaid income taxes, and approximately $36.2 million (the “Main Street and Prudential Consideration”) for payment to Main Street Capital II, LP, Main Street Mezzanine Fund, LP and Main Street Capital Corporation (collectively, “Main Street”) and Prudential Capital Partners IV, L.P., Prudential Capital Partners (Parallel Fund) IV, L.P. and Prudential Capital Partners Management Fund IV, L.P. (collectively, “Prudential”) and approximately $4.2 million of transaction fees and expenses, in each case estimated as of the end of the day immediately preceding the closing date, divided by (d) $10.00, plus (ii) the 2,079,042 shares forfeited by the HCAC Sponsor in the Sponsor Share Forfeiture (as defined and further discussed below). Pursuant to the letter agreement, dated December 22, 2016, among Hennessy Capital, Daseke, The Walden Group, Main Street and Prudential regarding, among other things, the conditional waiver of Main Street’s and Prudential’s respective put rights on their shares of Daseke common stock in exchange for aggregate consideration in an amount equal to the Main Street and Prudential Consideration in accordance with the terms and conditions of such agreement, Hennessy Capital repurchased all Daseke shares held by Main Street and Prudential immediately prior to closing for aggregate cash consideration of approximately $36.2 million. All other Daseke stockholders received all-stock consideration upon closing of the Business Combination consisting of newly issued shares of Hennessy Capital common stock (at a value of $10.00 per share) with an aggregate value equal to the Closing Merger Consideration.

In addition, the Merger Agreement contains an earn-out provision pursuant to which we may potentially issue up to 15 million additional shares of our common stock to Daseke stockholders for the achievement of specified share price thresholds and annualized Adjusted EBITDA (giving effect to acquisitions and as defined in the Merger Agreement) targets for the fiscal years ending December 31, 2017, 2018 and 2019 (the “Earn-Out Consideration”). The Earn-Out Consideration is payable entirely in newly issued shares of Hennessy Capital common stock.

In order to ensure sufficient funds (after redemptions) to refinance certain existing Daseke indebtedness, pay transaction fees and expenses and use for general corporate purposes, at closing, the Company sold 650,000 shares of its Series A Preferred Stock in a private placement for an aggregate purchase price of $65.0 million (referred to herein as the “Preferred Financing”) and consummated a $350.0 million debt financing (the “Debt Financing”), consisting of a $250.0 million senior secured term loan that was fully drawn at closing and a $100.0 million delayed drawn term loan that may be drawn within a 12-month period from closing of the Business Combination. At closing, the Company also refinanced its existing revolving credit facility with the ABL Facility.

In addition, Hennessy Capital received commitments from investors in the Backstop Commitment to purchase up to $35.0 million in shares of Company common stock (as and to the extent requested by Hennessy Capital) to help ensure that the Company received sufficient funds from our trust account after redemptions to (among other things) fund the payment of the Main Street and Prudential Consideration. On February 24, 2017, Hennessy Capital exercised the Backstop Commitment in full, and the Backstop Commitment investors purchased an aggregate of $35.0 million in shares of Hennessy Capital common stock through open market or privately negotiated transactions with third parties at a purchase price of up to $10.00 per share.

In order to facilitate the Business Combination, HCAC Sponsor forfeited more than half of its founder shares (resulting in 1,848,043 remaining founder shares held by HCAC Sponsor) for the benefit of Daseke stockholders and, to a lesser extent, for the benefit of investors in the Backstop Commitment and in connection with the payment of certain deferred underwriting discounts and fees to the underwriters (the “Underwriters”) of

Hennessy Capital’s July 2015 initial public offering (the “IPO”). Prior to the closing of the Business Combination, HCAC Sponsor forfeited to the Company 2,079,042 founder shares, and the Company issued an equivalent number of newly issued shares of Hennessy Capital common stock to Daseke stockholders as part of the Closing Merger Consideration (which Sponsor forfeiture and new issuance to Daseke stockholders is referred to collectively herein as the “Sponsor Share Forfeiture”). In addition, prior to closing, HCAC Sponsor forfeited 391,892 founder shares in connection with the Backstop Commitment and an additional 231,000 founder shares in connection with the payment of deferred underwriting discounts and fees to the Underwriters. At closing, in addition to the shares issued to Daseke stockholders as part of the Closing Merger Consideration, the Company also issued 419,669 newly issued shares of Company common stock (including 27,777 shares issued in consideration for the reduction of certain financial advisory fees) in the aggregate to the Backstop Commitment investors (such shares are referred to in the Backstop and Subscription Agreements and the Proxy Statement as “Utilization Fee Shares”).

Following the consummation of the Business Combination on February 27, 2017, there were 37,715,960 shares of Company common stock issued and outstanding, including 26,665,330 shares issued to former Daseke stockholders pursuant to the Merger Agreement and 8,342,918 “public” shares (issued in the IPO) of Company common stock remaining outstanding following redemptions.

The following pro forma information has been prepared based on: (i) 11,616,990 shares of Hennessy Capital common stock redeemed at closing (for a total cash payment of $116.2 million) pursuant to the terms of Hennessy Capital’s pre-Business Combination certificate of incorporation; (ii) 26,665,330 shares of Company common stock issued to former Daseke stockholders pursuant to the Merger Agreement; (iii) 419,669 shares of Company common stock issued to the Backstop Commitment investors; (iv) 650,000 shares of 7.625% Series A Convertible Preferred Stock of the Company issued in connection with the Preferred Financing for aggregate proceeds of $65.0 million; (v) the cash payment of Company and Hennessy Capital transaction fees and expenses including approximately $36.2 million of Main Street and Prudential Consideration and (vi) the payment of approximately $296.4 million of existing Daseke indebtedness (including approximately $1.8 million of interest and penalties) from, among other sources, the net proceeds of the Closing Date Term Loan.

2. Basis of Presentation

The Business Combination will be accounted for as a reverse merger in accordance with accounting principles generally accepted in the United States of America. Under this method of accounting, Hennessy Capital will be treated as the “acquired” company for financial reporting purposes. This determination was primarily based on Daseke comprising the ongoing operations of the combined company, Daseke’s senior management comprising the senior management of the combined company and Daseke stockholders having a majority of the voting power of the combined company. For accounting purposes, Daseke will be deemed to be the accounting acquirer in the transaction and, consequently, the transaction will be treated as a recapitalization of Daseke (i.e., a capital transaction involving the issuance of stock by Hennessy Capital for the stock of Daseke). Accordingly, the consolidated assets, liabilities and results of operations of Daseke will become the historical financial statements of the combined company, and Hennessy Capital’s assets, liabilities and results of operations will be consolidated with Daseke beginning on the Closing Date.

The unaudited pro forma condensed combined balance sheet as of December 31, 2016 was derived from Daseke’s audited consolidated balance sheet, and Hennessy Capital’s audited balance sheet, each as of December 31, 2016. The unaudited pro forma condensed combined balance sheet as of December 31, 2016 assumes that the Business Combination and the related proposed financing transactions were completed on December 31, 2016.

The unaudited pro forma condensed combined statement of operations information for the year ended December 31, 2016 was derived from Daseke’s audited consolidated statement of operations and comprehensive loss for the year ended December 31, 2016 and Hennessy Capital’s audited statement of operations for the year ended December 31, 2016 and gives pro forma effect to the Business Combination and the related proposed financing transactions as if they had occurred on January 1, 2016.

3. Unaudited Pro Forma Condensed Combined Balance Sheet Adjustments

The pro forma adjustments to the unaudited combined pro forma balance sheet consist of the following:

(a) Reflects cash funding and debt repayment as follows: (i) the transfer of $199.6 million from HennessyCapital’s trust account, (ii) the transfer of $184 thousand from Hennessy Capital’s trust account for the payment of taxes and working capital, (iii) the proceeds from the new $250.0 million term loan facility, net of approximately $14.0 million of financing costs including original issue discount of approximately $3.5 million and placement fees and expenses of approximately $10.5 million, and reflecting approximately $2.5 million as current portion of long-term debt, (iv) the repayment of approximately $293.4 million of the existing $338.4 million of debt together with the write off of deferred financing costs of approximately $4.1 million. Excluded from the repayment is approximately $45.0 million of equipment financing and real estate debt that remains outstanding.

(b) Represents 11,616,990 common shares ($116.2 million) redeemed on the closing date.

(c) Reflects the payment of purchase price as follows: $266.7 million in fair value of approximately 26,665,000 shares of common stock valued at $10.00 per share and, payment of approximately $36.2 million for the payment of the Main Street and Prudential Consideration.

The Merger Agreement contains an earn-out provision pursuant to which the Company may issue up to 15 million additional shares of its common stock to Daseke stockholders for the achievement of specified share price thresholds and annualized Adjusted EBITDA (giving effect to acquisitions and as defined in the Merger Agreement) targets for the fiscal years ending December 31, 2017, 2018 and 2019. The earn-out shares are to be issued contingent on future performance of the post combination company and, therefore, have not been recorded in the unaudited pro forma condensed combined financial statements.

(d) Reflects other transaction effects including: (i) the payment of transaction costs associated with the Business Combination which are estimated to be approximately $37.0 million in total for both parties, including approximately $14.0 million of financing costs associated with the Debt Financing (including approximately $3.5 million of original issue discount on the Debt Financing) and approximately $7.2 million of deferred underwriting discounts and fees from the IPO (“IPO fees”) which were due upon consummation of the Business Combination, less the waiver of approximately $0.65 million of IPO fees and (ii) the elimination of 18,932,591 shares of common stock subject to possible redemption. This adjustment reflects the elimination of Hennessy Capital’s retained earnings and Daseke’s par value of common and preferred stock upon consummation of the Business Combination. Also includes the adjustment to cash, accrued expenses and retained earnings for transaction expenses paid or accrued at December 31, 2016 including approximately $0.2 million of cash, and approximately $2.6 million of transaction costs included in accrued expenses (including $1.6 million at Hennessy Capital and $1.0 million at Daseke).

(e) Represents the issuance of 650,000 shares of Series A Preferred Stock at a per share purchase price of $100, for gross proceeds in the amount of $65.0 million. Each share of Series A Preferred Stock will be convertible into shares of common stock at a conversion price of $11.50. The unaudited pro forma combined balance sheet does not assume conversion of the Series A Preferred Stock. If the Series A Preferred Stock were to be converted into shares of common stock, the impact on the unaudited pro forma condensed unaudited balance sheet as of December 31, 2016 would be as follows:

|

|

|

(in thousands of dollars) |

| ||||

|

Line item |

|

Pro Forma |

|

Adjusted for the |

| ||

|

Convertible preferred stock |

|

$ |

65,000 |

|

$ |

— |

|

|

Common stock |

|

$ |

4 |

|

$ |

4 |

|

|

Additional paid-in-capital |

|

$ |

150,959 |

|

$ |

215,959 |

|

|

Stockholders’ equity |

|

$ |

183,436 |

|

$ |

183,436 |

|

4. Notes and Adjustments to Unaudited Pro Forma Condensed Combined Statements of Operations

The pro forma adjustments to the unaudited condensed combined pro forma statements of operations consist of the following:

(a) Elimination of Hennessy Capital’s costs to locate a potential acquisition target, and costs of the Business Combination incurred by Hennessy Capital ($9.1 million) and Daseke (1.0 million) at December 31, 2016.

(b) Elimination of interest income on the Hennessy Capital trust assets.

(c) Addition of incremental interest expense on the Debt Financing, entered into in connection with the Business Combination calling for an aggregate commitment of up to $350.0 million, $250 million of which was drawn on at Closing and the remainder, $100 million, is a delayed draw down term loan, as well as a $70.0 million asset-based revolving credit facility. The interest rate on the Debt Financing is LIBOR (with a floor of 1%) plus 5.5% and was approximately 6.5% at Closing. Therefore, the condensed combined pro forma statement of operations contains an adjustment for approximately $18.2 million annually representing approximately $16.2 million of annual interest at 6.5% on the pro forma outstanding debt of approximately $250.0 million plus approximately $2.0 million of annual amortization of approximately $14.0 million of original issue discount on, and financing costs of, the Debt Financing assuming the debt was outstanding at January 1, 2016. Each 0.125% change in the interest rate would generate an approximately $313 thousand change in interest expense.