Attached files

| file | filename |

|---|---|

| EX-10.14I - EXHIBIT 10.14I - Ingevity Corp | ex1014inon-employeedirecto.htm |

| EX-32.2 - EXHIBIT 32.2 - Ingevity Corp | ex322-q42016.htm |

| EX-32.1 - EXHIBIT 32.1 - Ingevity Corp | ex321-q42016.htm |

| EX-31.2 - EXHIBIT 31.2 - Ingevity Corp | ex312-q42016.htm |

| EX-31.1 - EXHIBIT 31.1 - Ingevity Corp | ex311-q42016.htm |

| EX-23.1 - EXHIBIT 23.1 - Ingevity Corp | ex231-q42016.htm |

| EX-21.1 - EXHIBIT 21.1 - Ingevity Corp | ex211-q42016.htm |

| EX-10.14H - EXHIBIT 10.14H - Ingevity Corp | ex1014hnon-employeedirecto.htm |

| EX-10.14G - EXHIBIT 10.14G - Ingevity Corp | ex1014gnon-employeedirecto.htm |

| EX-10.17 - EXHIBIT 10.17 - Ingevity Corp | ex1017ingevitycorporationn.htm |

| EX-10.16 - EXHIBIT 10.16 - Ingevity Corp | ex1016ingevitycorporationn.htm |

| EX-10.15 - EXHIBIT 10.15 - Ingevity Corp | ex1015ingevitycorporationd.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________

FORM 10-K

_______________________________________________________________________

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-37586

__________________________________________________________________________

INGEVITY CORPORATION

(Exact name of registrant as specified in its charter)

__________________________________________________________________________

Delaware | 47-4027764 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

5255 Virginia Avenue | ||

North Charleston, South Carolina 29406 | ||

(Address of principal executive offices) (Zip code) | ||

(Registrant’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class: | Name of Each Exchange on Which Registered: | |

Common Stock ($0.01 par value) | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Yes | No | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ¨ | x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. | ¨ | x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | x | ¨ |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that registrant was required to submit and post such files.) | x | ¨ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K of any amendment to this Form 10-K. | x | |

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): | ||

Large Accelerated Filer o | Accelerated Filer o | |

Non-Accelerated Filer x | Smaller reporting company o | |

Indicate by check mark whether the Registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes o No x

At June 30, 2016, the aggregate market value of common stock held by non-affiliates of the Registrant was $1,433,127,614. The market value held by non-affiliates excludes the value of those shares held by executive officers and directors of the Registrant.

The Registrant had 42,125,358 shares of common stock, $0.01 par value, outstanding at February 28, 2017.

Documents Incorporated by Reference | |||

Portions of the Company's 2017 Annual Meeting Proxy Statement are incorporated by reference into Part III of this report. | |||

Ingevity Corporation

Form 10-K

INDEX

Page No. | ||||

2

Item 1. Business

General

Ingevity’s business originated as part of the operations of its initial parent company, Westvaco Corporation, a paper and packaging company, using co-products of the kraft pulping process, primarily crude tall oil ("CTO") and lignin, as well as hardwood sawdust. Ingevity operated as a division of Westvaco Corporation and its corporate successors, including MeadWestvaco Corporation and WestRock Company, since 1964. Ingevity separated from WestRock Company on May 15, 2016.

Ingevity Corporation was incorporated in Delaware on March 27, 2015. The address of Ingevity’s principal executive offices is 5255 Virginia Avenue, North Charleston, South Carolina 29406. Ingevity maintains a website at www.ingevity.com. Ingevity’s website and the information contained in or connected to the website will not be deemed to be incorporated in this document, and you should not rely on any such information in making an investment decision.

Ingevity

Ingevity is a leading global manufacturer of specialty chemicals and high performance activated carbon materials. We provide innovative solutions to meet our customers’ unique and demanding requirements through proprietary formulated products. Our deep technical expertise and experience, flexible manufacturing, distinctive chemistry, global reach and focus on innovation and application development provide our customers with the ability to enhance their own products and competitive position in the markets they serve.

Ingevity’s specialty chemical products serve as critical inputs used in a variety of high performance applications, including asphalt paving, oil exploration and production, agrochemicals, adhesives, lubricants and printing inks. We are also the leading global manufacturer of activated carbon used in gasoline vapor emission control systems in cars, trucks, motorcycles and boats, with over 750 million units installed globally, having supplied products in this application for over 30 years. Our products meet highly specialized, complex customer needs in the industries in which they are used. As customer applications become more demanding, Ingevity’s products become increasingly specialized and represent a critical component of our customers’ products, typically at a modest input cost relative to the customer’s overall product cost. This value creation - significant performance impact versus relatively low input cost - provides some measure of stability as customers may be reluctant to face the performance risk potentially associated with switching over to competitors’ offerings.

With a history of innovation spanning 100 years, we have grown into a global leader in the markets we serve with over $900 million in sales in 2016, serving customers in approximately 65 countries from our United States and China manufacturing facilities. Our global engineering, technical, sales and application support teams closely collaborate with our customers, and, importantly, with their customers. With our deep technical expertise and experience in our customers’ applications and end markets, we have the capacity and flexibility to anticipate and respond to changing market conditions and customer demands and to develop proactive solutions that provide our customers - and therefore us - with a distinct competitive advantage. Additionally, the quality and diversity of our product portfolio, and the flexibility of our manufacturing assets, gives us the capability to direct our resources towards their most profitable and attractive uses and geographies in response to changing market conditions.

We participate in attractive, higher growth sectors of the global specialty chemicals industry. The broadly defined specialty chemicals industry is expected to experience a 3.5% compound annual growth rate ("CAGR") from 2015 through 2020, according to IHS, Inc., a leading provider and analyst of industry information for, among other things, the chemical industry. Ingevity focuses on targeted markets within that space that are expected to outpace the broader specialty chemicals market growth rate, supported by long-term secular growth trends in infrastructure preservation and development, innovation in unconventional oil exploration and production and increasing global food production demands. We also participate in more commoditized sectors, where we sell our functional chemistries, including tall oil fatty acid ("TOFA") and biofractions, directly into the marketplace with low differentiation, and where we sell certain activated carbons for use in some purification processes. Additionally, our specialized automotive carbon business, which engineers, manufactures and sells wood-based activated carbon used in gasoline vapor emission control systems, is expected to benefit from increasingly stringent vehicle emission standards worldwide that our products are uniquely designed and qualified to meet. The annual global sales of light duty vehicles (i.e. passenger and light commercial vehicles) that are powered with gasoline are forecast to grow from approximately 71 million to approximately 90 million vehicles (+28%) from 2015 to 2025. All of this growth is expected to occur outside of the United States and Canada in countries and regions where gasoline vapor emission standards significantly lag the modern, highly effective standards of the United States and Canada. This

3

provides significant upside potential in addition to the already favorable macroeconomic growth trends of the global automotive industry.

We report in two business segments, Performance Materials and Performance Chemicals. Our Performance Materials segment consists of our carbon technologies business which primarily produces automotive carbon products used in gasoline vapor emission control systems. Our Performance Chemicals segment primarily addresses applications in three product families: pavement technologies, oilfield technologies and industrial specialties.

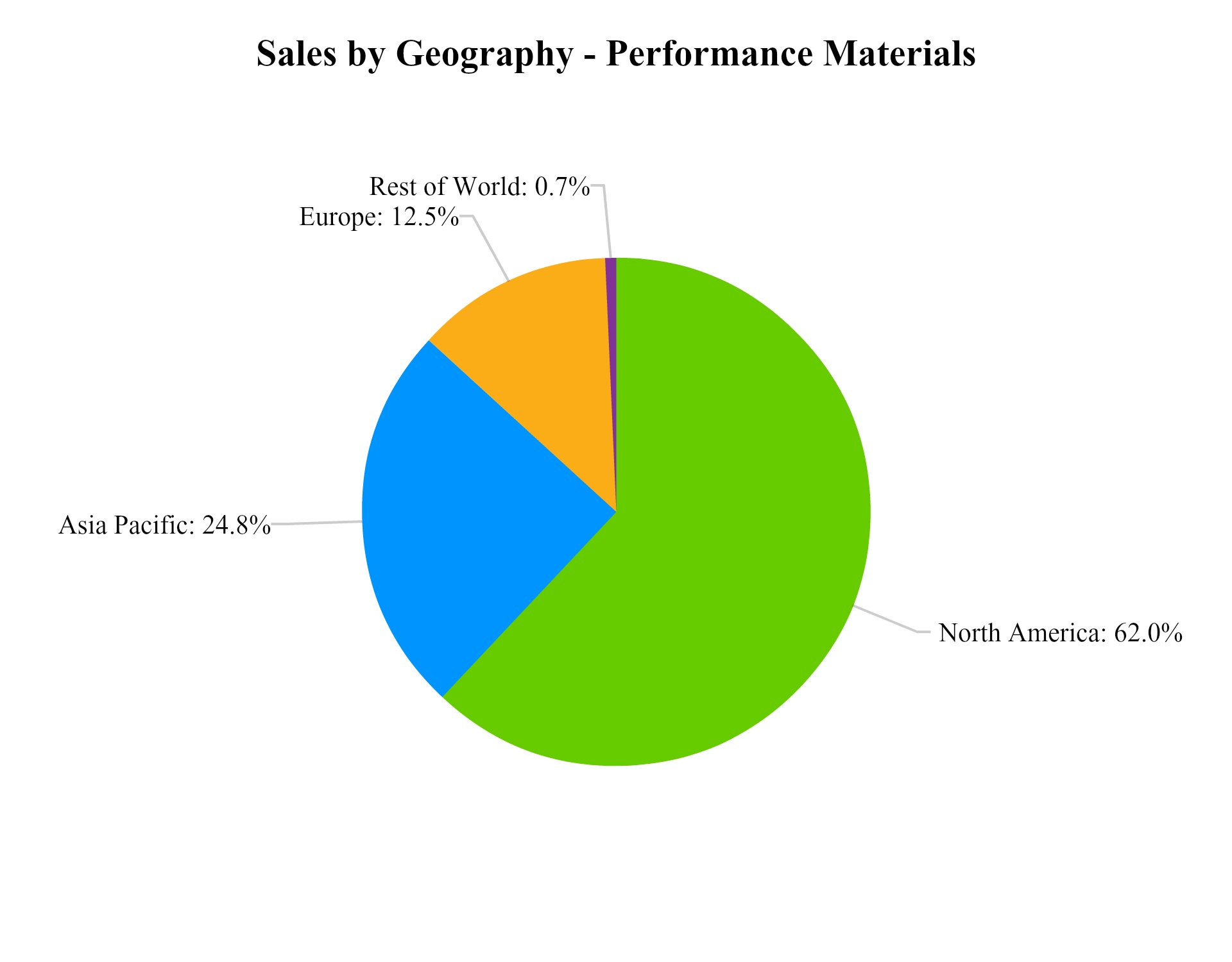

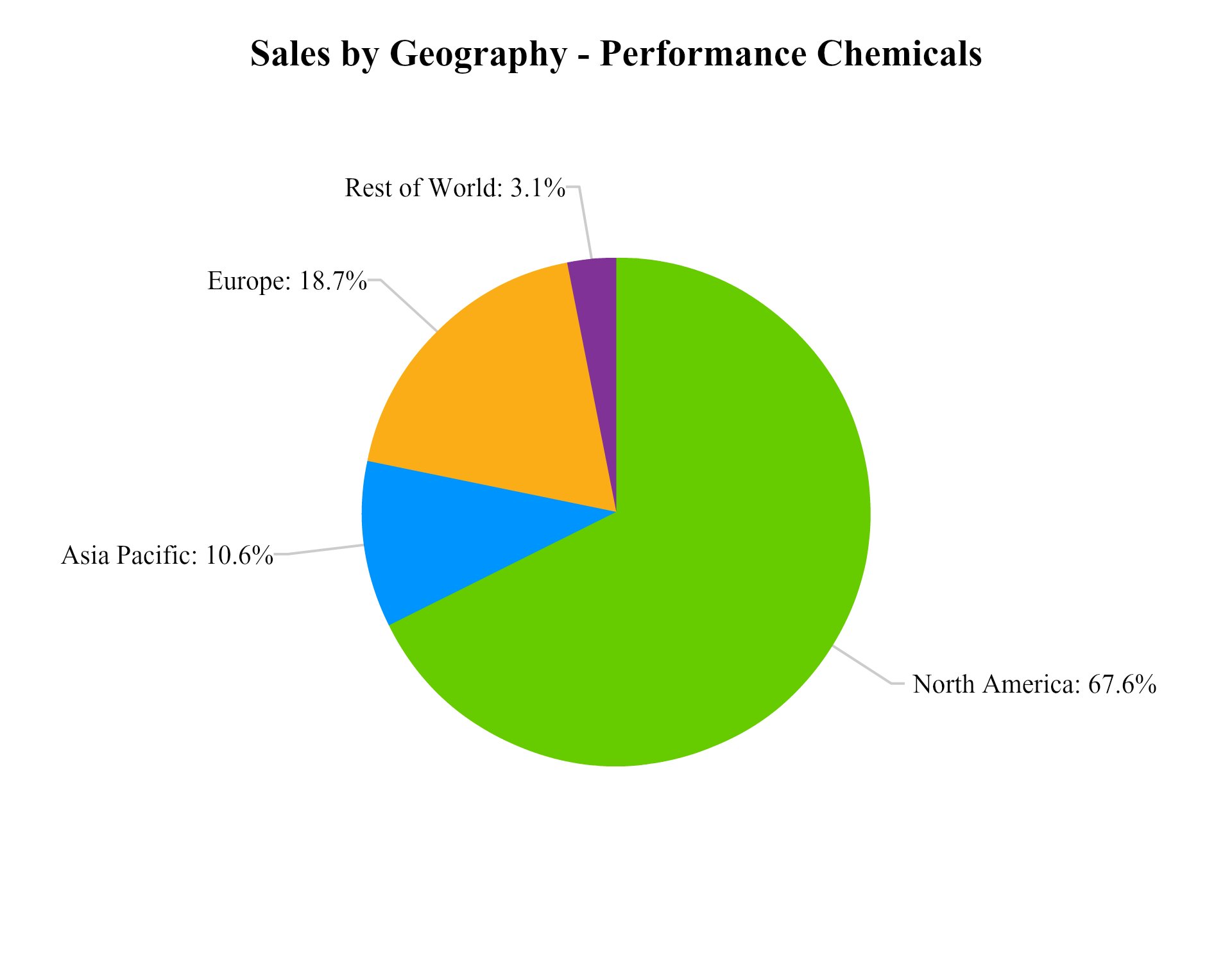

The chart below illustrates our revenue by segment, product family and sales by geography in 2016. For more information about our U.S. and foreign operations, see Note 19 of Notes to the Consolidated Financial Statements.

Performance Materials | Performance Chemicals | |||

Product Families | Carbon Technologies | Pavement Technologies | Oilfield Technologies | Industrial Specialties |

Primary End Uses | Automotive gasoline vapor emissions control Process purification | Pavement preservation Adhesion promotion Warm mix asphalt technology | Well service additives Production and downstream chemicals | Adhesives Agrochemicals Lubricants Publication inks Industrial intermediates |

2016 Revenue | $301 million | $607 million | ||

Sales are assigned to geographic areas based on location to which product was shipped to a third party.

Our Core Strengths

Ingevity is committed to continued value creation for its customers and stockholders by focusing on its core strengths:

Leading Global Market Positions

We are a leader in the global pine chemicals industry, further distinguished by our focus on target markets that offer the potential for profitable growth, supported by long-term secular growth trends in infrastructure preservation and development, innovation in unconventional oil exploration and production and increasing global food production demands. Our products serve

4

as critical inputs used in a variety of high performance applications, including asphalt paving, oil exploration and production, agrochemicals, lubricants and printing inks. The quality and diversity of our product portfolio, and the flexibility of our manufacturing assets, gives us the capability to direct our differentiated products towards their most profitable and attractive uses and geographies.

Ingevity is the leading global manufacturer of activated carbon used in gasoline vapor emission control systems in cars, trucks, motorcycles and boats. This business is expected to benefit from increasingly stringent vehicle emission standards worldwide that our products are uniquely designed and qualified to meet. The annual global sales of light duty vehicles (i.e. passenger and light commercial vehicles) that are powered with gasoline are forecast to grow from approximately 71 million to approximately 90 million vehicles (+28%) from 2015 to 2025. Most of this growth is expected to occur outside of the United States and Canada in countries and regions where gasoline vapor emission standards significantly lag the modern, highly effective standards of the United States and Canada. This provides significant upside potential in addition to the already favorable macroeconomic growth trends of the global automotive industry.

Flexible Manufacturing Capabilities Optimize Asset Utilization

The quality and diversity of our product portfolio, and the flexibility of our manufacturing assets, gives us the capability to direct our resources to their most profitable uses and geographies.

Our Performance Chemical assets include multipurpose chemical reactors that are capable of manufacturing products of varying chemistries that can serve multiple markets. For example, in our South Carolina facility, the newest reactor that was commissioned in 2015 is capable of producing products for pavement, oilfield and adhesives applications, while our Louisiana assets can be redirected with relative ease among various applications including asphalt, oilfield, adhesives and inks.

Our Performance Materials assets, which primarily produce automotive grade carbon, are also capable of producing a number of other activated carbon products for food, water, beverage and chemical purification applications, maximizing the productivity of these assets.

Deep Technical Expertise and Product Innovation Capability and Experience

We have deep technical expertise and market knowledge and insights, derived from customer relationships and research and development capabilities, that enable our innovation capacity. Innovation efforts are led and supported by our teams of technical experts and industry veterans, many of whom are considered the foremost experts in their fields, spread throughout our organization in key positions from product development to manufacturing to sales. Each of our business units has its own development and application laboratories that work in partnership with our customers to refine existing products and develop new innovative products that will drive value for Ingevity and our customers.

With our technical expertise and product innovation capability and experience, and by working closely with our customers, our technical experts can quickly offer application solutions that address our customers’ most difficult challenges. For example, when our road contractor customers vary the aggregate and/or asphalt to be used in a particular job mix, they call on our expertise to quickly reformulate the Ingevity additive chemistry needed for the revised mix, so that they can meet the original job specifications on time, regardless of the change. Our ability to swiftly understand and address our customers’ performance needs allows Ingevity to maintain and grow its partnerships with its customer base.

Unique Decades-Long Track Record of Automotive Carbon Products Meeting Emission Compliance Standards

Current U.S. federal and California regulatory standards and the recently promulgated China 6 nation standards require that gasoline vapor control devices remain effective for the entire life of the vehicles on which they are installed. Ingevity has a substantial, decades-long track record of providing life-of-vehicle product performance in a properly designed gasoline vapor control system. Our unique capability to engineer a very specific nanoscale porosity into the carbons on a large commercial scale allows the system designers to minimize the system’s size based on our carbon's ability to remain highly effective over a vehicle’s lifetime. Given the imperative for automotive manufacturers to produce vehicles capable of meeting these long-term requirements, or potentially face expensive recalls and unfavorable publicity, there is an increased risk to use the products of other producers who do not have a comparable, proven history and technical capability, particularly given the significant costs associated with non-compliance should a competitor’s product fail to maintain its effectiveness over vehicle lifetimes.

5

Global Manufacturing and Supply Chain Reach

We have a global reach which allows us to effectively service multinational customers through a combination of our manufacturing facilities located in the United States and China and local talent strategically placed around the globe. In addition, our technology centers located in the United States, China, Europe and India give us the ability to service our customers throughout these regions, and provide us with market insights that allow us to develop customized solutions for local and regional markets. Our global engineering, technical, sales and application support teams serve customers in approximately 65 countries. Our global reach enables us to more effectively serve - and be the business partner of choice to - multinational companies that look to partners who can meet their needs on a consistent basis wherever they do business.

This capability also allows us to take advantage of future market trends. For example, our oilfield technology business has in the past been primarily focused on the North American market. Our global reach will allow us to pursue growth opportunities outside of the United States, particularly in the Middle East, which has not undergone as significant an output decline during the recent global slowdown in the oil and gas exploration industry.

Collaborative Customer and End User Relationships Drive Profitable Growth Opportunities

We take a partnership approach with our customers, investing resources to deeply understand their customers’ markets so that we can provide technologically advanced, tailored solutions that allow our customers to maintain a competitive advantage in the markets they serve. Our knowledge of our customers’ end markets provides us with insights that enable us to develop solutions that address opportunities or challenges and create value for our customers. For example, through our relationships with several automobile manufacturers (original equipment manufacturers, or “OEMs”) (often, our customers’ customer), we learned that certain vehicles were having trouble passing emissions certification tests based on a small amount of volatile organic compounds ("VOCs") migrating from the engine via the vehicles’ air intake systems. To address this issue, we developed several generations of activated carbon-based solutions, including activated carbon honeycombs and engineered activated carbon sheets, that manage these emissions while minimizing pressure drop in the air intake system - a key performance advantage to the OEMs. This drove demand for our product by addressing the needs of our customers’ customer. We believe this approach - driving demand for our products by developing solutions for our customers’ end markets - has been and will continue to be a significant driver of profitable growth.

Education of Government and Regulatory Bodies on Scientifically Based Policies and Specifications

Many of our customers’ markets are subject to increasing regulatory standards and mandates. For example, more stringent air quality standards drive reductions in automotive emissions or the use of recycled materials in the case of pavement technologies. With our technical expertise and experience, our teams are a valued resource and work directly with government and regulatory bodies, in support of our customers, as experts in their field to educate regulators about existing and innovative technologies that support their objectives or solve specific challenges. As the trend continues in mature and emerging markets towards more advanced solutions, we believe the ability to leverage our expertise to educate, advocate and promote sensible regulatory solutions will benefit our customers while driving incremental value within those markets. For example, Ingevity has globally recognized expertise in the highly specialized field of automotive gasoline vapor emissions. While tailpipe emissions on vehicles are well recognized, understood and regulated, gasoline vapor emissions from vehicles have been lightly regulated in many countries outside the United States and Canada. Our experts have educated authorities in other countries to help them understand and quantify the magnitude of these emissions and evaluate the highly effective solutions currently in use in the United States and Canada that can reduce these gasoline vapor emissions to “near zero” levels at a relatively low cost per vehicle.

Our engagement with regulators allows us to then work with our customers in order to help them respond and adapt to evolving and varying regulatory standards. For example, because of the stringent and differing regulatory compliance standards applicable to the global oilfield industry, our oilfield customers often turn to us over smaller, less sophisticated vendors in order to help them manage the complexities of compliance risk in chemical distribution and use throughout the world.

Highly Engaged, Performance and Safety-Driven Culture

We have assembled a highly talented, collaborative, committed and creative team which drives the success of our business. We believe in empowerment and accountability and encourage our employees to think boldly. Our collective ambition is keenly focused on creating value for today and tomorrow. Further, we are committed to protecting human health and the environment while using resources in a responsible and sustainable manner: as a long-standing member of the American Chemistry Council (ACC), we subscribe to the Guiding Principles of the American Chemistry Council’s Responsible Care® program - a global chemical industry performance initiative that is implemented in the United States through the ACC. Our ISO 9001, ISO/TS 16949

6

and Responsible Care® Certifications are internationally recognized measures of consistent superior performance and responsibility to health, safety, security and the environment. We believe this track record is something that further differentiates us from our competitors.

Long-term Secured Raw Material Supply

At the time of the separation from WestRock, we entered into a long-term supply agreement with them pursuant to which we purchase all of the crude tall oil ("CTO") output from WestRock’s existing kraft mills, subject to certain exceptions. This relationship with WestRock is strategically important to our Performance Chemicals business due to the limited supply of CTO globally, of which we believe a significant portion is already under long-term supply agreements with other consumers of CTO. We believe this increment of supply, in conjunction with other contracted sources of CTO, will allow us to serve customer demand. See also “Risk Factors - Our Performance Chemicals segment is highly dependent on CTO which is limited in supply; lack of access to sufficient CTO would impact our ability to produce CTO-based products.”

Our Plans for Additional Growth

We have a demonstrated history of profitable growth. Looking ahead, we believe we will accelerate our growth while maintaining our profitability by taking the following steps as a newly independent public company:

Expand Sales to Existing Customers and into New Geographies

We believe we are well positioned to organically expand our sales through a combination of continued global sales growth, leveraging our significant application knowledge to apply our existing products to new applications and capitalizing on the investments we have made in our global sales, technical centers and distribution network. Our global reach allows us to effectively compete in new geographies, delivering proven innovative solutions where opportunities to apply our technologies exist. We continue to leverage our significant application knowledge and intimate customer relationships to target opportunities where we know our products perform and to create demand for our products by driving value for our customers.

We intend to continue to strengthen our position in emerging markets where we believe there are significant opportunities for growth. Opportunities include the expansion of sales of our pavement products into areas increasingly in need of newly paved roads and increased sales of activated carbon solutions driven by anticipated regulatory changes in global automotive vapor emissions control standards. As a result, we completed construction of a new Performance Materials facility in China during the fourth quarter of 2015. The total project spending was roughly $100 million. This facility produces products for our automotive emissions control applications. We began selling products from this facility in 2016.

Increase our Offering of Specialized, Higher Margin Products

We employ a world-class team of engineering, technical, sales and application specialists, along with experienced industry professionals, which provide us with deep technical knowledge and the ability to be a leading provider of specialty products in the markets we serve. We have the experience and capability to further develop and expand upon the products we currently produce, further differentiating them into higher value, increasingly specialized products, or developing new applications and end uses.

We have a history of success in product development and differentiation. For example, our oilfield technologies business transitioned from providing basic TOFA to our customers to the development and marketing of specialized tall oil emulsifiers and corrosion inhibitors. We also grew our pavement technologies from asphalt chemicals into specialized additives used in ultra-thin paving technologies.

We believe that there is significant upside in further developing and expanding upon products produced from TOFA, displacing some of our lower margin business where we sell TOFA directly to certain customers. This will have the added benefit of improved insulation from the cyclical nature of the direct natural fats and oils market of which TOFA is a part. Over the next few years, our goal is to meaningfully increase the portion of our sales of specialized, higher value products derived from TOFA, including addressing new markets or opportunities to upgrade TOFA into product categories where we might not participate today.

Additionally, we search to supply the right chemistry for the applications within our market segments regardless of the raw materials required. Applying our unique insights into the end use applications of our products, our team searches to find novel solutions, outside of our current CTO-based materials, to problems and our team also works to create the supply chain needed to provide those products to our customers. As an example, we have developed and now manufacture and sell product solutions in our pavement technologies business that are TOFA and hydrocarbon based.

7

Innovate to Enable Our Customers to Adapt to Increasingly Stringent Regulatory Standards

We are a valued resource with government and regulatory agencies around the world, from California to China, including national, regional and local environmental regulatory bodies. We work directly with such bodies, in support of our customers, to help them develop sensible standards based on the availability of technological solutions that make such standards commercially achievable. As standards are adopted and become increasingly demanding, the products that can be used to achieve compliance with such standards become increasingly technologically complex to design and manufacture on a commercial level. Our ability to meet these complexities provides Ingevity with a distinctive commercial edge — as our customers in many applications depend on us to help them meet their compliance standards. For example, when paving contractors were having difficulty meeting the Florida Department of Transportation’s initiative to use more recycled tire rubber, the pavement technologies group developed an innovative delivery system, Evoflex RMA, and educated contractors on how to use it to achieve the desired environmental and performance benefits. We also work closely with automotive companies and their suppliers to ensure that they understand and can meet increasingly stringent vehicle emission standards.

Invest Organically and Selectively Pursue Acquisitions that Further Strengthen Our Product Portfolio

We plan to continue to invest capital organically in attractive cost reduction projects and in capacity expansions as necessary to meet demand growth. For example, in 2016, in order to meet the growing demand for our honeycomb products that help meet the U.S. and Canadian Tier 3 regulation, we began a capital expansion at our Purification Cellutions, LLC, Waynesboro, Georgia honeycomb extrusion joint venture facility to effectively double the capacity output by year end 2017. As demand for these products grows, we will continue to evaluate additional capacity expansion as needed.

In addition, we intend to pursue value-creating acquisitions that represent attractive opportunities in our target markets as well as in high-value niche applications that complement our current product portfolio and capabilities. We continue seeking to add product lines and portfolios, as well as marketing and manufacturing alliances, that will play an important role in strengthening our leadership positions. We are pursuing acquisitions both domestically and globally.

Segments

Performance Materials

We engineer, manufacture and sell wood-based, chemically activated carbon products, produced through a highly technical and specialized process primarily for use in gasoline vapor emission control systems in cars, trucks, motorcycles and boats. We have produced and sold activated carbon for over 100 years, including over 30 years for the automotive application. We are the global leader in this automotive application, with over 750 million units installed globally since we entered this application. We also produce a number of other activated carbon products for food, water, beverage and chemical purification applications, to maximize the productivity of our manufacturing assets.

Our automotive carbon products capture gasoline vapor emissions that would otherwise be released into the atmosphere as VOCs which contain hazardous air pollutants and can photochemically react to form ozone and secondary organic aerosols, a form of PM2.5, which themselves form haze. These gasoline vapor emissions (which are distinct from tailpipe emissions) are released primarily (i) during refueling, (ii) when a vehicle is parked during the daytime, as a result of evaporation and expansion of vapors in the fuel tank in warmer daytime temperatures and (iii) as “running loss”, as a result of evaporation and expansion of vapors in the fuel tank from increased temperatures as a result of operation of the vehicle.

Our automotive carbon products are typically part of vehicle based gasoline vapor emissions control systems which can range from systems equipped with an approximately one liter carbon canister that captures one day of diurnal parking emissions, to more sophisticated Onboard Refueling Vapor Recovery (“ORVR”), running loss and multiday diurnal parking systems with a two to three liter carbon canister that captures over 98% of the gasoline vapor emissions.

The captured gasoline vapors are then largely purged from the carbon and directed to the engine where they are used as supplemental power for the vehicle. In this way, our automotive carbon products are part of a system that provides for both environmental control and energy recovery. We estimate that, in 2016, our products collectively prevented over 20,000 metric tons of VOC emissions each day from being lost to the atmosphere and returned the equivalent of 8 million gallons of gasoline each day to supplementally power vehicles.

Environmental standards drive the implementation of gasoline vapor emission control systems by automotive manufacturers. While tailpipe emissions on vehicles are well recognized, understood and regulated, gasoline vapor emissions from

8

vehicles have been lightly regulated in many countries outside the United States and Canada. For those countries that have not significantly regulated gasoline vapor emissions, enacting more stringent regulations represents a low-cost, high-return opportunity to address their air quality issues. The annual global sales of light duty vehicles (i.e. passenger and light commercial vehicles) that are powered with gasoline are forecast to grow from approximately 71 million to approximately 90 million vehicles (+28%) from 2015 to 2025. All of this growth is expected to occur outside of the United States and Canada in countries and regions where gasoline vapor emission standards significantly lag the modern, highly effective standards of the United States and Canada. Adoption of modern gasoline vapor emission standards in these regions would have significant, positive environmental and energy efficiency impacts and provide significant upside growth potential for our automotive carbon business.

The United States and Canada have led the world in recognizing and addressing the harm to air quality caused by gasoline vapor emissions, and in early 2014 enacted regulatory standards that will further reduce these emissions to “near zero” levels by phasing in Tier 3 evaporative emission standards through 2022, which will result in significant increases in the use of our canister “bleed emissions” system patent over that same period. The Tier 3 phase in schedule requires compliance to the standard as follows: 40% of model year 2017's vehicles, 60% of model year 2018's, 80% of model year 2020's and 100% of model year 2022's. The most commonly applied embodiment of the patent uses our activated carbon in the main part of the canister and our activated carbon honeycomb(s) as a “scrubber” on the outlet side of the canister to reduce the canister's emissions to "near zero." Our “canister bleed emissions” patent expires in April 2022. The honeycombs are manufactured though an activated carbon ceramic extrusion process at our joint venture facility, Purification Cellutions, LLC, located in Waynesboro, Georgia. We financially consolidate this joint venture, of which we have a 70 percent ownership and operating responsibility. The other 30 percent interest is owned by a U.S. based third party and the partner's income is represented in our noncontrolling interest elimination.

Most other countries outside the United States and Canada have significantly lagged in the adoption of regulatory standards that would reduce these gasoline vapor emissions, focusing instead on regulating the more “visible” tailpipe emissions. These other countries are using a gasoline vapor emission standard that is functionally equivalent to a 1981 U.S. regulatory standard. As a result, in Europe, Asia and South America, gasoline vapor emissions are the primary source of automotive VOC emissions. China recently promulgated a new national standard, China 6, that is functionally equivalent to the 2009 alignment of U.S. Tier 2 with California LEV II. This new national standard, containing ORVR and multi-day diurnal parking emission controls, is scheduled to be fully phased in by July 2020 with the potential for earlier implementation in several large municipal regions.

As recognized experts in the field of gasoline vapor emission control, Ingevity has been working with regulatory bodies and relevant third parties in China, Japan, Mexico, Brazil and the European Union to help them understand and move towards more effective regulatory standards similar to those in place in the United States and Canada. Regulatory indications of adoption and implementation of more stringent vapor emissions standards outside of the United States and Canada include the following:

•The European Commission (“EC”) has adopted more stringent gasoline vapor emission regulations with its Euro 6c standard, implementing in September 2019. This new standard is more stringent than the current standards and includes a 2-day diurnal parking emission test that will generally result in a 30-70% increase in canister capacities and a shift in some volumes to pellets and high activity carbon.

•On December 23, 2016, the China Ministry of Environmental Protection and the China State Administration of Quality Supervision, Inspection, and Quarantine released its China 6 National Standard on the Limits and Measurement Methods for Emissions from Light-Duty Vehicles (GB 18352 6-2016). In the new standard, diurnal control is increased to 48-hours, running loss conditions are simulated, and ORVR is added. Emissions limits are also reduced and will be similar to those in U.S. Tier 2. As a result, canister volumes are expected to increase by 2 to 3 times and the majority of the canisters are expected to shift to high activity carbons and pellets. This new standard implements nationally on July 1, 2020 and will likely be adopted earlier by some regions and municipalities.

•Sao Paulo, Brazil is experiencing tremendous ozone problems and needs VOC reductions for air quality improvement. CONAMA is the national authority with responsibility for establishing new vehicle emissions standards in Brazil and is presided over by the Minister of Environment. Sao Paulo is Brazil's most populous metropolitan area, and its state environmental authority, CETESB, has the role of creating and recommending motor vehicle standards to the federal government. CETESB desires to upgrade their evaporative emission standards, including technologies such as ORVR, and have CONAMA add these new requirements to the next phase of vehicle standards, called Proconve 7. They must first get an approval and recommendation from AEA (Brazil’s Association of Automotive Engineers) and ABNT (Brazil Association for Technical Norms) before also seeking action by IBAMA. IBAMA is Brazil's federal environment protection agency with responsibility for the execution, regulation, and control of environmental policies.

9

The AEA has been working to finalize a set of test procedures that includes ORVR for addition to Proconve 7, and the procedures are now in review by ABNT.

•South Korea is currently phasing in some U.S. Tier 2 diurnal parking emission standards, which generally require activated carbon canister volumes greater than 1.3 liters and an increased use of pelletized carbon. In 2018, South Korea will begin phasing in portions of the U.S. Tier 3 “near zero” full vehicle diurnal parking emission standards that will favor the use of low emission and air induction system diurnal parking emission activated carbon technologies.

See also “Risk Factors - Adverse conditions in the automotive market may adversely affect demand for our automotive carbon products,” and “Risk Factors - If increasingly more stringent air quality standards worldwide are not adopted, our growth could be impacted.”

Current regulatory standards in the United States and Canada require that gasoline vapor control devices remain effective for the entire life of the vehicles on which installed. The end of lifetime requirements for most vehicles is 10 years or 120,000 miles, but will increase to 15 years or 150,000 miles for a large segment of these U.S. vehicles. China 6 standards also include a lifetime requirement of 160,000 kilometers or 12 years. Ingevity has a substantial, decades long track record of providing life-of-vehicle product performance based on our unique capability to engineer a very specific nanoscale porosity into the carbons on a large commercial scale. Given the imperative for automotive manufactures to produce vehicles capable of meeting these long term requirements, or potentially face expensive recalls and unfavorable publicity, there is an increased risk to use other producers who do not have a comparable, proven history, particularly given the significant costs associated with non-compliance should a competitor’s offering fail to maintain effectiveness over vehicle lifetimes. Additionally, because these gasoline vapor control systems are certified as “environmental devices” for models currently in production, it is difficult and costly to replace our products within the vehicle’s control system with a competitive product during the vehicle’s model/platform production life due to the high cost of recertification.

As a result of decades of innovation and production, Ingevity is able to produce products that are effective in smaller amounts than competitors’ offerings, meaning less product is required - which results in savings through the use of a smaller and less costly canister in the overall emissions control system. Continued innovation and manufacturing know how should allow this advantage to continue even as competitors improve their product offerings.

Ingevity is further uniquely positioned to capitalize on the opportunity afforded by the adoption of these modern vapor emission regulatory standards, which will, as a practical matter (given current technology), require manufacturers of light duty vehicles in these countries to incrementally install advanced gasoline vapor control technology with carbon capable of meeting the new regulatory standards. Based on the regulatory trends and expected growth in vehicles, Ingevity management estimates that the revenue for its automotive emissions products could double within five to seven years from 2015. Ingevity, through its proprietary technology, trade secrets and confidential manufacturing know-how, has unparalleled capability and expertise to manufacture the high performance activated carbon products required to meet these regulatory standards, as well as more stringent standards likely to be imposed in the years to come. These same capabilities and expertise will help Ingevity to maintain its position in the United States and Canada automotive markets as they advance their standard to “near zero” gasoline vapor emission levels.

We also produce a number of other activated carbon products for food, water, beverage and chemical purification applications, to maximize the productivity of our manufacturing assets.

In 2016, our Performance Materials segment provided sales of $301.0 million and segment operating profit of $106.9 million. For further information on measures of profitability used by managers of the business and its segments, refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations of Ingevity."

Production

Activated carbon is an amorphous form of carbon characterized by a high volume of nanoscale pores. “Activation” refers to the process of developing these pores. The size, shape and volume of the pore structure and the surface chemistry of the pore are critical for driving performance in various applications.

Activated carbons are typically produced from either a thermal or chemical process utilizing a wide variety of carbonaceous raw materials. The thermal process, the most widely used activation process, uses rotary kilns or multi-hearth furnaces to carbonize and activate the raw material. This process operates at a much higher temperature and at a lower yield than the chemical activation process. Typical raw materials include bituminous coal, lignite and coconuts. Thermally activated carbons are usually used for

10

“catch and dispose” applications, whereby the carbon is used to capture certain compounds and the carbon product is then disposed of or thermally regenerated.

Ingevity employs a more specialized activation process, whereby chemical catalysts (most often phosphoric acid or zinc chloride) and various heating methods are used to facilitate the development of porosity. This process operates at a lower temperature and typically has higher yields than a thermal process. Carbons produced by this method typically have larger pores than thermally activated carbons and can be used in both “catch and dispose” applications and “catch and release” applications, whereby the carbon is used to capture and temporarily hold on to certain compounds which are then released in a controlled manner under specific operating conditions.

We use hardwood sawdust to produce chemically activated carbon, which, because of its higher pore volume, pore structure and high surface area, is well-matched for a variety of applications and ideally suited for the “catch and release” automotive application of capturing and reusing gasoline vapor emissions.

We further process activated carbon after it is activated into different forms using a variety of extrusion processes. One of our extrusion processes is to use activated carbon and various binders to make a formed pellet. Pelleted carbon is typically used in canister applications where a low pressure drop system is required such as ORVR.

Another extrusion process we employ is with our honeycomb "scrubber". We utilize an activated carbon infused ceramic extrusion process. These honeycomb "scrubbers" are used with the Company's patented system to reduce the canister's emissions to "near zero" and are manufactured at our joint venture facility, Purification Cellutions, LLC, located in Waynesboro, Georgia.

Customers

We sell our automotive products to over 60 customers around the globe. We are the trusted source of these products for many of the world’s largest automotive parts manufacturers, including Aisan Industry, Delphi Automotive, MAHLE, and many other large and small component manufacturers throughout the global supply chain. Our relationship with many of our customers and their customers - the vehicle manufacturers themselves (including every one of the top 15 global automotive manufacturers) - have been in place for most of our history in this application. No one customer within our Performance Materials segment represents more than 10% of the segment's net sales. Ingevity also produces activated carbon products for food, water, beverage and chemical purification applications, which are sold to nearly 90 customers throughout the world.

We operate primarily through a direct sales force in North America and our other major markets and also have a smaller, focused network of agents and distributors that have established a strong direct sales and marketing presence.

Competition

In automotive carbon, Ingevity has a unique decades-long track record of providing life-of-vehicle performance, with over 750 million units installed. Given the imperative for automotive manufacturers to produce vehicles for the United States and Canadian markets capable of meeting life-of-vehicle emission standards, or potentially face expensive recalls and unfavorable publicity, our automotive carbon products provide our customers the low-risk choice in this high performance application. Our competitors in the automotive application include Cabot Corp., Kuraray, and several Chinese manufacturers. Our process purification business competes mainly in the United States in the food, beverage, chemical and water purification applications. Our competitors in this segment include Cabot, Calgon Carbon, Osaka Gas/Jacobi Carbons and several domestic U.S. manufacturers and distributors of imported products.

Performance Chemicals

Ingevity’s Performance Chemicals segment develops, manufactures and sells a wide range of specialty chemicals primarily derived from co-products of the kraft pulping process. Products include performance chemicals derived from pine chemicals used in asphalt paving, adhesives, agrochemical dispersants, printing inks, lubricants, oilfield exploration and production and other diverse industrial uses. Our application expertise is often called upon to provide unique solutions to our customers that maximize resource efficiency. We have a broad and diverse customer base in this segment. In 2016, our top ten customers accounted for approximately 38% of our segment revenue; the next 100 customers made up approximately 39% of our segment revenue.

The primary raw material used in our Performance Chemicals segment is CTO. Our flexible manufacturing processes allow us to take advantage of our steady availability of CTO supply and respond to changing customer and market demands, which enables us to fully utilize our manufacturing assets.

11

Our Performance Chemicals business serves customers globally from two manufacturing locations in the United States.

In 2016, our Performance Chemicals segment delivered sales of $607.3 million and segment operating profit of $56.7 million. For further information on measures of profitability used by managers of the business and its segments, refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations of Ingevity."

Production

Most of our performance chemicals are derived from CTO, a co-product of the kraft pulping process, where pine is used as the source of the pulp. CTO is produced by acidulating black liquor soap skimmings ("BLSS"), which are recovered during the kraft pulping process. Consumers of CTO can purchase BLSS from pulping mills that do not have acidulation capacity (in which case the BLSS will need to be acidulated into CTO), and purchase CTO from pulping mills that do have acidulation capacity. The CTO is further separated by distillation into tall oil rosin ("TOR"), TOFA and other biofractions. As such products are further refined or chemically modified, higher value derivative products are created, making their way into a wide variety of industrial and consumer goods. We also produce performance chemicals derived from lignin, also a co-product of the kraft pulping process. TOR and TOFA are sold directly to customers in some instances, or, along with lignin, further refined or chemically modified into higher value derivative products.

Our differentiated performance chemicals are engineered to meet specific industry standards and customer requirements.

Pavement Technologies

Our pavement technologies group supplies a broad line of innovative additives, systems and technologies for road construction, resurfacing, preservation, maintenance and recycling globally. As a specialty asphalt additive supplier for over 50 years, we have a long history of work with transportation agencies, university research consortiums, paving contractors and asphalt refiners around the world to design, develop and implement innovative additives and novel paving systems that protect existing roadways and enhance the performance of new road construction.

Our pavement technologies team combines broad downstream technical, application and construction experience with a strong direct sales and marketing presence. Our combined expertise in the disciplines of chemistry and civil engineering provides a comprehensive understanding of the relationship between molecular structure of our chemistries and their impact on the performance of pavement systems. This allows us to develop products customized to local markets and consistently deliver cost-effective solutions for our clients. We also introduce and commercialize new technologies globally through consulting relationships with ministries and departments of transportation to stimulate customer demand for our products.

We supply over 100 asphalt additive products and technologies to approximately 500 customers under numerous well-known industry brands such as Evotherm®, Ralumac® and Indulin®. Technology centers located in the United States, China, Europe and India give us the ability to service our customers throughout these regions, and provide us with market insights that allow us to develop customized solutions for local and regional markets.

We are a global leader in the rapidly expanding Warm Mix Asphalt (“WMA”) enhanced paving segment with our Evotherm® family of products, with over 200,000 lane miles of Evotherm® asphalt having been placed into service in the United States. Evotherm’s® unique chemistry allows paving at temperatures up to 100 degrees Fahrenheit lower than traditional hot mix asphalt (which typically runs between 300 and 325 degrees Fahrenheit), and lower than temperatures achieved by competing WMA technologies. The product, which is added during the mixing of rock aggregate and liquid asphalt, requires no other modification to the paving process. Performance benefits of the Evotherm® product include extending the paving season into colder weather conditions, enabling service to more distant jobsites, accelerating project completion and improving worker safety. According to industry standard predictive lab tests, roads constructed with Evotherm® technology have improved aggregate adhesion properties and longer pavement life. Evotherm® carries environmental benefits as well, reducing production-related CO2 emissions up to 20 - 35% and lowering jobsite emissions by reducing the fumes typically associated with hot mix asphalt paving. Evotherm® also delivers significant savings per ton of mix, making this an attractive product during times of constrained municipal resources and budgets.

According to the National Asphalt Paving Association, WMA paving technology is used annually in 30% of all new highway construction in the U.S. The relevant advantages of WMA paving, and of Evotherm® in particular, are expected to lead to growth, both in the United States and internationally. The product is already gaining market acceptance in China and Europe, with over 30,000 kilometers placed in service in Europe and over 25,000 kilometers placed in service in China. We believe additional

12

growth opportunities exist in Europe, Latin America and elsewhere in Asia, addressable through our existing distribution capabilities in each of these regions.

Customers

We supply over 100 asphalt additive products and technologies to approximately 500 customers under numerous well-known industry brands such as Evotherm®, Ralumac® and Indulin®. Technology centers located in the United States, China, Europe and India create market insights for product development customized to local and regional markets.

Competition

We compete on the basis of deep knowledge of our customers’ business and extensive insights into road building technologies and trends globally. We use these strengths to develop consulting relationships with government departments of transportation, facilitating new technology introduction into key markets around the world. Our combined expertise in the disciplines of chemistry and civil engineering provides a comprehensive understanding of the relationship between molecular structure of our chemistries and their impact on the performance of pavement systems. This allows us to develop products customized to local markets and to consistently deliver cost-effective solutions for our customers. Our primary competitors in pavement technologies are AkzoNobel, Arkema and ArrMaz.

Oilfield Technologies

Our oilfield technologies group produces and sells a wide range of innovative specialty chemical products for the global oilfield industry, including well service additives and chemical solutions for production and downstream applications.

Well Service Additives. Our well service additive products are formulated to increase emulsion stability and aid in fluid loss control for oil-based drilling fluids. Other additives include rheology modifiers, which are used to improve the viscosity properties of oil-based fluids, and are typically used in deep water or cold temperature applications and wetting agents, which provide improved wetting of solids and aid in the efficiency of the drilling process. This family of products aids in accessing difficult to reach oil and gas reserves, both on and offshore around the globe.

Production and Downstream. Our production and downstream products serve as corrosion inhibitors or their components. Crude oil and natural gas production is characterized by variable production rates and unpredictable changes due to the nature of the produced fluids including but not limited to water and salt content. Our corrosion inhibitors maximize production rates by reducing equipment downtime from corrosion of key equipment and pipe.

Customers

We sell our oilfield technologies to over 60 customers around the globe. Our relationships with our top ten customers have been in place for more than ten years, and we work extremely closely with our customers on their product requirements.

Competition

We compete on the basis of our ability to understand our customers’ applications and deliver solutions that aid in their improvement of the exploration and production of oil and gas for the end users. Additionally, this application expertise coupled with our strong understanding of CTO-based chemistry allows for rapid development of solutions to challenges in the field. Our scale and flexibility of manufacturing are the final piece that helps deliver the creativity, expedience and peace of mind the customers in oilfield require from their best suppliers. Our competitors include Georgia-Pacific, Lamberti, Kraton and several others.

Industrial Specialties

Our industrial specialties group manufactures specialty chemicals - including adhesive tackifiers, agrochemical dispersants, lubricant additives, corrosion inhibitors and ink resins - used in industrial settings. Our technical expertise and formulation capabilities allow us to develop innovative products to meet our customers’ various needs.

Adhesives. We are a leading global supplier of tackifier resins which provide superior adhesion to difficult-to-bond materials to the adhesives industry. Adhesive applications for our products include construction, product assembly, packaging, pressure sensitive labels and tapes, hygiene products and road markings.

Agrochemicals. We produce dispersants for crop protection products as well as other naturally derived products for agrochemicals. Crop protection formulations are highly engineered, highly regulated and cover a range of different formulation

13

types, from liquids to solids. We deliver a wide range of dispersants that are high performing and consistent. In addition, our crop protection products are approved for use as inert ingredients in agrochemicals by regulatory agencies throughout the world.

Lubricants. We supply lubricant additives and corrosion inhibitors for the metalworking and fuel additives markets. Our lubricant products are multi-functional additives that contribute to lubricity, wetting, corrosion inhibition, emulsification and general performance improvement. Our products are valued because of their ease in handling, robust performance and improved formulation stability.

Printing Inks. We are a leading supplier of ink resins from renewable resources to the global graphic arts industry for the preparation of printing inks. Our products improve gloss, drying speed, viscosity, adhesion and rub resistance of the finished ink to the substrate. We produce a wide array of resins, typically specifically tailored to a customer’s use, which can vary by application, pigment type, end use, formulation and manufacturing and printing process.

Intermediates. Our functional chemistries are sold across a diverse range of industrial markets including, among others, paper chemicals, textile dyes, rubber, cleaners, mining and nutraceuticals.

Customers

We sell our industrial specialty chemicals to approximately 500 customers around the globe. We have an over twenty-year relationship with many of our significant customers in this business. We work extremely closely with our customers on their product requirements.

Competition

In industrial specialties, our customers select the product that provides the best balance of performance, consistency and price. Reputation and commitment to our customer’s industry are also valued by our customers and allow us to win business when other factors are equal. In our adhesives business, our products compete against other tackifiers, including other TOR-based tackifiers as well as tackifiers produced from gum rosin and hydrocarbon starting materials. In addition, the choice of polymer used in an adhesive formulation drives the selection of tackifier. In agrochemicals, the selection of a dispersant is made early in the product development cycle and the formulator has a choice among Ingevity’s sulfonated lignin products, lower quality lignosulfonates and other surfactants such as naphthalene sulfonates. In lubricants, we compete against other producers of distilled tall oil and additives. In inks, our products compete against other resins that can be derived from TOR, gum rosin and, to a lesser extent, hydrocarbon sources. In our intermediates business, our TOFA competes against widely available fats and oils derived from soy, rapeseed, palm, cotton and tallow sources.

Competitors are different depending on the product, application and region and include Kraton, Georgia-Pacific, Eastman Chemical, ExxonMobil, Borregaard, Lawter, Respol/Forchem, as well as several others.

Capital Expenditures

On average steady-state required spending on continuity capital (e.g., maintenance, safety health and environment, and regulatory) for the business is estimated to be equal to or slightly less than annual Depreciation and Amortization (“D&A”) expense. In any given year, however, continuity capital spending can vary significantly from the average given the nature of some required projects. In addition to continuity capital spending, we would expect to invest additional capital as attractive opportunities for high rate of return cost reduction or expansionary projects warrant. This spending amount may also vary significantly on a year to year basis depending on factors such as timing of project spending and the opportunities at hand.

Raw Materials and Energy

Performance Chemicals. The primary raw material used in our performance chemicals segment is CTO. The availability of CTO is directly linked to the production output of kraft mills using pine as their source of pulp. As a result, there is a finite global supply of CTO - with global demand for kraft pulp driving the global supply of CTO, rather than demand for CTO itself. Most of the CTO made available for sale by its producers is covered by long-term supply agreements, further constraining availability.

At the time of the Separation, we entered into a long-term supply agreement with WestRock pursuant to which we purchase all of the CTO output from WestRock’s existing kraft mills, subject to certain exceptions. Beginning in 2025, either party may provide a notice to the other party terminating the agreement five years from the date of such notice. Beginning one year after

14

such notice, the quantity of products provided by WestRock under the agreement will be gradually reduced over a four-year period based on the schedule set forth in the agreement. In addition, from 2022 until 2025, either party may provide one-year notice to remove a kraft mill as a supply source. The two largest kraft mills under the agreement currently are expected to supply approximately 19.5 to 21.5% and 18.5% to 20.0%, respectively, of the total amount of products expected to be supplied under our agreement with WestRock. In the event that WestRock exercises its right to terminate our supply agreement with them or remove a kraft mill as a supply source, we may be able to obtain substitute supplies of CTO from other suppliers, spot purchases or a new contract with WestRock. This agreement includes pricing terms based on market prices. Under this agreement, based on WestRock’s current output, we expect to source approximately 45% to 55% of our CTO requirements for the maximum operating rates of our facilities. We also have agreements with other suppliers to satisfy substantially all of the balance of our expected requirements of CTO through 2018.

We believe that we are well positioned to have sufficient CTO required for our operations. However, if any of our suppliers (including WestRock) fail to meet their respective demands under our supply agreements or we are otherwise unable to procure an adequate supply of CTO, we would be unable to produce the quantity of products that we have historically produced. In addition, if WestRock exercises its rights to terminate the agreement or remove a kraft mill as a supply source, and we are unable to arrange a substitute supply of CTO, we would be unable to continue to produce the same quantity of products. In the event that WestRock exercises its right to terminate our supply agreement with them or remove a kraft mill as a supply source, we may be able to obtain substitute supplies of CTO from other suppliers, spot purchases or a new contract with WestRock. Additionally, there are other pressures on the availability of CTO. Some kraft pulp mills may choose to consume their production of CTO to meet their energy needs rather than sell the CTO to third parties. Furthermore, weather conditions have in the past and may in the future affect the availability and quality of pine trees used in the kraft pulping process and therefore the availability of CTO meeting our quality standards. See “Risk Factors - Our Performance Chemicals segment is highly dependent on CTO which is limited in supply; lack of access to sufficient CTO would impact our ability to produce CTO-based products.”

Also, regulatory incentives and mandates in Europe for the use of biofuel have placed additional pressure on CTO availability. See “Risk Factors - The European Union’s Directive 2009/28 on the promotion of the use of energy from renewable resources ("Renewable Energy Directive" or "RED") and similar legislation in the United States and elsewhere may incentivize the use of CTO as a feedstock for production of alternative fuels.”

Finally, CTO as a raw material may be subject to significant pricing pressures. See “Risk Factors - Pricing for CTO is subject to particular pricing pressures by reason of limited supply and competing demands for end use, and we may be limited in our ability to pass on increased costs to our customers,” and “Risk Factors - The Company's oilfield technologies business is significantly affected by trends in oil and natural gas prices that affect the level of exploration, development and production activity.”

The other key raw materials used in the Performance Chemicals business are nonylphenol, pentaerythritol and ethylene amines. These are sourced where possible through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

Performance Materials. The primary raw material (by volume) used in in the manufacture of our activated carbon is hardwood sawdust. Sawdust is readily available, and is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing.

We also consume phosphoric acid, which is used to chemically activate the hardwood sawdust. This phosphoric acid is sourced through multiple suppliers to protect against supply disruptions and to maintain competitive pricing. The market price of phosphoric acid is affected by the global agriculture market as the majority of global phosphate rock production is used for fertilizer production and only a portion of that production is used to manufacture purified phosphoric acid. In the recent past, there have been price run-ups in phosphoric acid due to increased phosphate rock demands in global agriculture, which have in turn negatively affected our business.

Energy. Our manufacturing processes require a significant amount of energy. In particular, we are dependent on natural gas to fuel our carbon activation processes and are therefore subject to the market fluctuations in the price of natural gas. Although we believe that we currently have a stable supply of and infrastructure for natural gas sufficient for our operations, we are subject to volatility in the market price of natural gas.

15

Environment

Our operations are subject to extensive regulation by federal, state and local authorities, as well as regulatory authorities with jurisdiction over the foreign operations of Ingevity, including relating to the discharge of materials into the environment and the handling, disposal and clean-up of waste materials, and otherwise relating to the protection of the environment. It is not possible to quantify with certainty the material effects that compliance with these regulations may have upon the capital expenditures, earnings or competitive position of Ingevity, but it is anticipated that such compliance will not have a material adverse effect on any of the foregoing. For a further discussion, see “Risk Factors - Our business involves hazards associated with chemical manufacturing, storage, transportation and disposal,” and “Risk Factors - The Company's operations are subject to a wide range of general and industry specific environmental laws and regulations.” Environmental regulation and legal proceedings have the potential for involving significant costs and liability for the Ingevity.

Backlog

In general, we do not manufacture our products against a backlog of orders and do not consider backlog to be a significant indicator of the level of future sales activity. Production and inventory levels are based on the level of incoming orders as well as projections of future demand. Therefore, we believe that backlog information is not material to understanding our overall business and should not be considered a reliable indicator of our ability to achieve any particular level of revenue or financial performance.

Intellectual Property

Intellectual property, including patents, closely guarded trade secrets and highly proprietary manufacturing know-how, as well as other proprietary rights, is a critical part of maintaining our technology leadership and competitive edge. Our business strategy includes filing patent and trademark applications where appropriate for proprietary developments, as well as protecting our trade secrets. We actively create, protect and enforce our intellectual property rights. The protection afforded by our patents and trademarks varies based on country, scope and coverage, as well as the availability of legal remedies. Although our intellectual property taken as a whole is material to the business, other than our “canister bleed emissions” patent, which is part of our automotive business and expires in April 2022, there is no individual patent or trademark the loss of which could have a material adverse effect on the business. The most commonly applied embodiment of the “canister bleed emissions” patent uses our activated carbon in the main part of the canister and our activated carbon honeycomb(s) from our joint venture, Purification Cellutions, LLC, facility, as a “scrubber” on the outlet side of the canister to reduce the canister's emissions to "near zero." Our Evotherm® Warm Mix Asphalt technology is supported by numerous global patents. See “Risk Factors - If we are unable to adequately protect our intellectual property, we may lose significant competitive advantages,” and “Risk Factors - We are subject to cyber-security risks related to our intellectual property and certain other data."

Research and Development

We employ a world-class team of engineering and scientific professionals, many of whom hold Ph.D. degrees and are considered some of the foremost experts in their fields, with deep knowledge of our customers’ markets. We spent $8 million, $7 million and $8 million for the years ended December 31, 2016, 2015 and 2014, respectively, on research and development which was expensed as incurred.

Seasonality

There are a variety of seasonal dynamics that impact our businesses, though none materially affect financial results, except in the case of the pavement technologies business, where roughly 75% of its revenue is generated between April and September. From a supply perspective, this seasonality is effectively managed through pre-season inventory build then active inventory management throughout the year.

Employees

We currently employ approximately 1,500 employees, of whom 78% are employed in the United States and 22% are employed internationally. Approximately 26% are represented by labor unions, domestic and international, under various collective bargaining agreements. We engage in negotiations with labor unions for new collective bargaining agreements from time to time based upon expiration dates of agreements and statutory requirements. We consider our relationships with employees to be generally good.

The collective bargaining agreement with the Covington Paperworkers Union (“CPU”) representing approximately 125 production and maintenance employees in our Covington, Virginia facility also covered production employees of the adjoining

16

WestRock paper mill. Similarly, the collective bargaining agreement with the International Brotherhood of Electrical Workers (“IBEW”) for WestRock's electrical and instrument technicians also represented eight hourly employees working at our Covington facility. These shared collective bargaining arrangements have been separated subsequent to the Separation.

Ingevity is currently negotiating independently with the bargaining committee for the CPU and the IBEW, respectively. The agreement with CPU expired on December 1, 2016 while the agreement with IBEW expired on January 15, 2017. The provisions of both agreements remain in effect under an “evergreen clause” and notice provisions. The two negotiations are proceeding in good faith by all parties with additional dates set for further discussion in the near future. See “Risk Factors - Work stoppages and other labor relations matters may have an adverse effect on our financial condition and results of operations.”

The Separation

Prior to the separation, we operated as a reporting segment of WestRock, which was formed upon the combination (the “Merger”) of MeadWestvaco Corporation (“MWV”) and Rock-Tenn Company (“Rock-Tenn”). The Merger was completed on July 1, 2015.

Prior to the Merger, we operated as a reporting segment of MWV, which announced on January 8, 2015 that it intended to separate its specialty chemicals business through a pro rata distribution of common stock to its stockholders. Upon the completion of the Merger, WestRock announced its continued plans to complete the separation.

On May 15, 2016 (the "Distribution Date"), WestRock Company (“WestRock”) completed the previously announced separation of the business comprising WestRock's Specialty Chemicals reporting segment, and certain other assets and liabilities, into Ingevity, a separate and distinct public company (herein referred to as the "Separation"). The Separation was completed by way of a distribution of all of the then outstanding shares of common stock of Ingevity through a dividend in kind of Ingevity's common stock (par value $0.01) to holders of record of WestRock common stock (par value $0.01) as of the close of business of May 4, 2016 (the "Record Date").

On the Distribution Date, each holder of WestRock's common stock received one share of Ingevity's common stock for every six shares of WestRock's common stock held on the Record Date. The Separation was completed pursuant to a Separation and Distribution Agreement and other agreements with WestRock related to the Separation, including an Employee Matters Agreement ("EMA"), a Tax Matters Agreement, a Transition Services Agreement and an Intellectual Property Agreement (collectively, the "Separation Agreements"), each of which was filed as an exhibit to our Current Report on Form 8-K, filed with the Securities and Exchange Commission on May 16, 2016. The Separation Agreements govern the relationship among Ingevity and WestRock following the Separation and provide for the allocation of various assets, liabilities, rights and obligations. The Separation Agreements also include arrangements for transition services to be provided by WestRock to Ingevity. For a discussion of each agreement, see the section entitled "Certain Relationships and Related Party Transactions - Agreements with WestRock Related to the Spin-Off" in our Information Statement filed as Exhibit 99.1 ("Information Statement") to our Registration Statement on Form 10, as amended, filed with the Securities and Exchange Commission on April 26, 2016 ("Registration Statement"). The Separation Agreements were entered into on May 14, 2016.

The Registration Statement was declared effective by the SEC on April 25, 2016, and Ingevity's common stock began "regular-way" trading on the New York Stock Exchange ("NYSE") on May 16, 2016 under the symbol "NGVT".

Availability of Reports Filed with the Securities and Exchange Commission

Our interest website is www.ingevity.com. We make available, free of charge through our website, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended ("Exchange Act"), as soon as reasonably practicable after such documents are electronically filed with, or furnished to, the SEC. The information on our website is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K or incorporated by reference in this Annual Report on Form 10-K or any other filings we make with the SEC.

17

EXECUTIVE OFFICERS OF THE REGISTRANT

The executive officers of Ingevity Corporation, the offices they currently hold, their business experience over the past five years and their ages are as follows: