Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - Core-Mark Holding Company, LLC | a2016-exhibit322.htm |

| EX-32.1 - EXHIBIT 32.1 - Core-Mark Holding Company, LLC | a2016-exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - Core-Mark Holding Company, LLC | a2016-exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - Core-Mark Holding Company, LLC | a2016-exhibit311.htm |

| EX-23.1 - EXHIBIT 23.1 - Core-Mark Holding Company, LLC | a2016-exhibit231.htm |

| EX-21.1 - EXHIBIT 21.1 - Core-Mark Holding Company, LLC | a2016-exhibit211.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

x | Annual Report Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended December 31, 2016

o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to .

Commission File Number: 000-51515

Core-Mark Holding Company, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 20-1489747 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

395 Oyster Point Boulevard, Suite 415 South San Francisco, California 94080 | (650) 589-9445 |

(Address of Principal Executive Offices, including Zip Code) | (Registrant's Telephone Number, including Area Code) |

Securities Registered Pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, par value $0.01 per share | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2016, the last business day of the registrant's most recently completed second fiscal quarter: $2,117,773,783

As of February 24, 2017, the registrant had 46,315,364 shares of its common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information called for by Part III of this Form 10-K will be included in an amendment to this Form 10-K or incorporated by reference to the registrant’s 2017 definitive proxy statement to be filed pursuant to Regulation 14A.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2016

TABLE OF CONTENTS

Page | ||

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in this Annual Report on Form 10-K that are not statements of historical fact are forward-looking statements made pursuant to the safe-harbor provisions of the Exchange Act of 1934 and the Securities Act of 1933.

Forward-looking statements in some cases can be identified by the use of words such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “seek,” “anticipate,” “estimate,” “believe,” “could,” “would,” “project,” “predict,” “continue,” “plan,” “propose” or other similar words or expressions. Forward-looking statements are made only as of the date of this Form 10-K and are based on our current intent, beliefs, plans and expectations. They involve risks and uncertainties that could cause actual results to differ materially from historical results or those described in or implied by such forward-looking statements.

A detailed discussion of risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in Part I, Item 1A, “Risk Factors” of this Form 10-K. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

SEC Regulation - Non-GAAP Information

The financial statements in this Annual Report on Form 10-K are prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP"). Core-Mark Holding Company, Inc. ("Core-Mark") uses certain non-GAAP financial measures including Adjusted EBITDA, net income excluding LIFO expense, net sales less excise taxes, remaining gross profit, remaining gross profit margin, remaining gross profit margin less excise taxes and cigarette remaining gross profit per carton. We believe these non-GAAP financial measures provide meaningful supplemental information for investors regarding the performance of our business and facilitate a meaningful period to period evaluation. Management uses these non-GAAP financial measures in order to have comparable financial results to analyze changes in Core-Mark’s underlying business. These non-GAAP measures should be considered as a supplement to, and not as a substitute for, or superior to, financial measures calculated in accordance with GAAP. More information about such measures are included in Item 7 - Adjusted EBITDA and Item 7- Non GAAP Financial Information.

ii

PART I

ITEM 1. BUSINESS

Unless the context indicates otherwise, all references in this Annual Report on Form 10-K to “Core-Mark,” “the Company,” “we,” “us,” or “our” refer to Core-Mark Holding Company, Inc. and its subsidiaries.

Company Overview

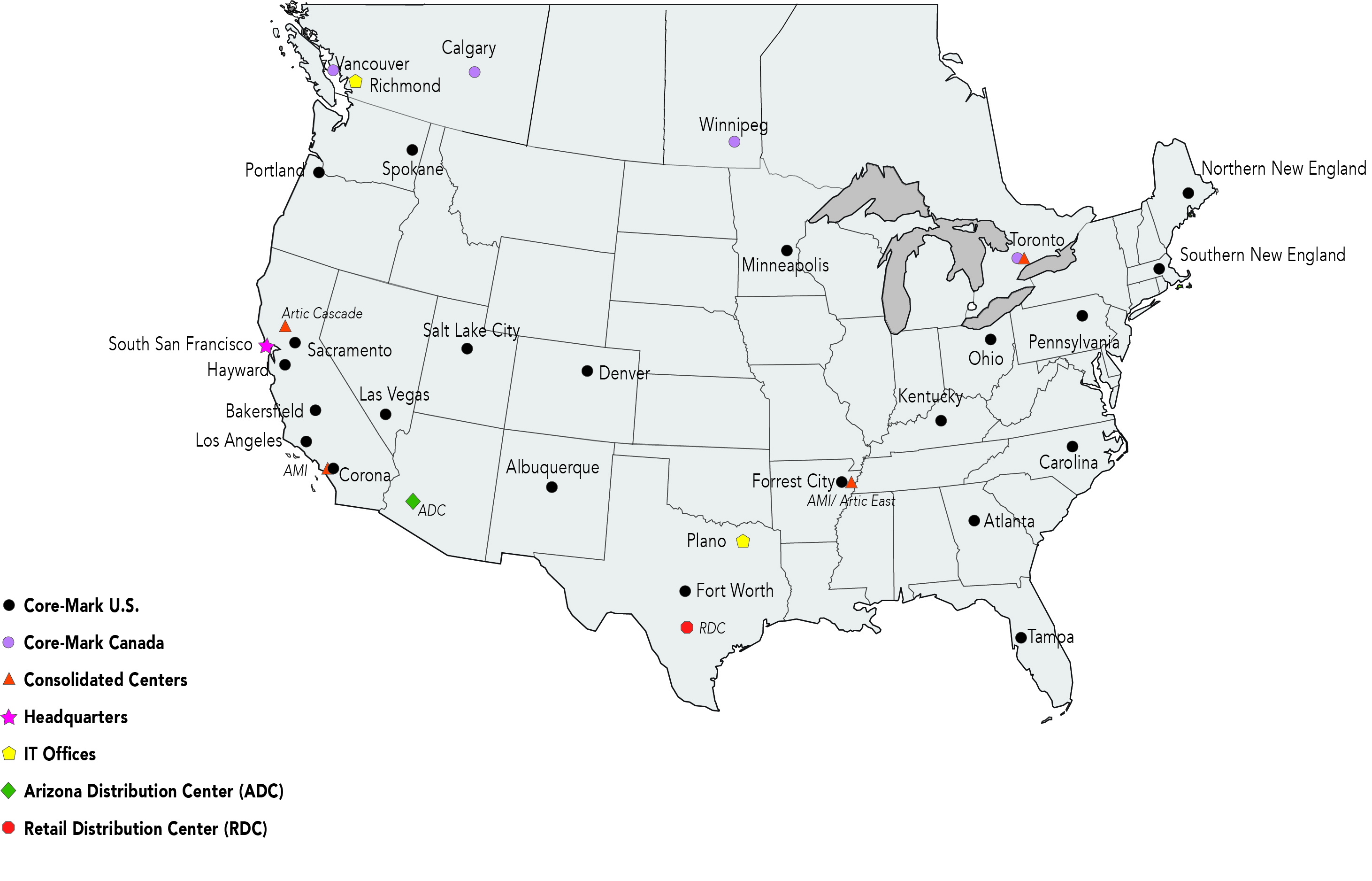

Core-Mark is one of the largest wholesale distributors to the convenience retail industry in North America, providing sales, marketing, distribution and logistics services to over 43,000 customer locations across the United States (U.S.) and Canada through 30 distribution centers (excluding two distribution facilities we operate as a third party logistics provider). Our origins date back to 1888, when Glaser Bros., a family-owned-and-operated candy and tobacco distribution business, was founded in San Francisco, California.

Our mission is to be the most valued marketer of fresh and broad-line supply solutions to the convenience retail industry. While the past century has brought incredible changes to our business and the world in which we operate, our goal is the same today as it was over 125 years ago - to provide customers with the best possible service and to help them grow their sales and profits. We have grown our business organically and through acquisitions which have expanded our distribution network, product selection and customer base.

Core-Mark has become one of two national distributors to the convenience store industry in the U.S. and is the largest in Canada. The national market presence we have established rests primarily with our ability to service customers in every geographic region within the U.S. through 25 distribution centers and servicing customers in Canada with our five Canadian distribution centers.

We operate in an industry where, in 2015, based on the National Association of Convenience Stores ("NACS") State of the Industry ("SOI") report, total in-store sales at convenience retail locations in the U.S. increased 5.8% to approximately $225.8 billion and were generated through approximately 154,000 stores. Over the ten years from 2006 through the end of 2015, U.S. convenience in-store sales have increased by a compounded annual growth rate of approximately 3.3%. Based on the Canadian Convenience Store Association ("CCSA") 2015 Industry report, we estimate that total Canadian in-store sales at convenience locations were approximately CAD$40.0 billion generated through approximately 26,000 stores.

Company Highlights

Net income grew from $26.2 million in 2011 to $54.2 million in 2016, or approximately 16% compounded annually. Our net sales grew from $8.1 billion in 2011 to $14.5 billion in 2016, yielding an annual compounded growth rate of approximately 12%, while our annual Adjusted EBITDA(1) increased from $91.9 million to $152.3 million, or approximately 11%, compounded annually. Our growth has been driven primarily by our business strategies described more fully below. We believe these strategies have positioned us to continue to grow our approximate 6% market share of total in-store sales within the convenience store channel in North America and to take advantage of growth opportunities with other retail store formats. Below are key highlights of 2016:

• | In December 2016, we signed a three-year supply agreement to service approximately 530 Walmart Neighborhood Markets and Supercenter stores in five western states (Arizona, California, New Mexico, Nevada and Utah). We will be the primary distributor to these stores for candy, tobacco and certain snack foods. We expect to begin service under this agreement in May 2017. |

• | In June 2016, we acquired substantially all of the assets of Pine State Convenience, a division of Pine State Trading Company, located in Gardiner, Maine, for cash consideration of approximately $88 million. |

• | In October 2015, we signed a five-year agreement with Murphy U.S.A. to be the primary wholesale distributor to over 1,400 stores located in 24 states across the Southwest, Southeast and Midwest United States. Services under this contract began in the first quarter of 2016. We believe our services have created efficiencies and a strategic supply chain relationship for Murphy U.S.A. |

• | In October 2015, we signed a five-year supply agreement with 7-Eleven, Inc. to service approximately 900 stores in three western regions. We began servicing 7-Eleven in October 2016 and we became the primary wholesale distributor delivering a wide range of products to these stores out of three of our divisions - Las Vegas, NV, Salt Lake City, UT and Sacramento, CA. |

________________________________________

(1) | Adjusted EBITDA is a non-GAAP measure. See reconciliation of Adjusted EBITDA to net income in Item 7- Adjusted EBITDA. |

1

Business Strategy

Our objective is to increase overall return to stockholders by growing our revenues and leveraging operating costs to increase profitability. As one of the largest marketers of fresh and broad-line supply solutions to the convenience retail industry in North America with a track record of effectively selling into other retail channels, we believe we are well-positioned to continue meeting this objective. Our business strategy also includes the following initiatives, designed to further enhance the value we provide to our retail customers:

Vendor Consolidation Initiative ("VCI"). We expect our VCI program will allow us to continue to grow our sales by capitalizing on the highly fragmented supply chain that services the convenience retail industry. A convenience retailer generally receives store merchandise through a large number of direct-store deliveries. This represents a highly inefficient and costly process for retailers. Our VCI program targets inefficiencies in the convenience store supply chain by offering the retailer the ability to receive multiple weekly deliveries for the bulk of their products, including dairy and other merchandise they purchased from direct-store delivery companies. This simplifies the supply chain and provides retailers with an opportunity to improve inventory turns and working capital, reduce operational and transaction costs, and greatly diminish their out-of-stocks.

Fresh Products ("Fresh"). There is an increasing trend among consumers to purchase fresh food from convenience and other retail store formats. To meet this demand, we have modified and upgraded our refrigerated capacity, including investing in chill docks, and tri-temperature ("tri-temp") trailers, which provide the infrastructure to deliver a significant range of chilled items including milk, produce and other fresh foods to retail outlets. We have established partnerships with strategically-located dairies, fresh kitchens and bakeries to further enable us to deliver premium consumer items such as sandwiches, wraps, cut-fruit, parfaits, pastries, doughnuts, bread and home meal replacement solutions. We continue to promote our fresh products through the development of unique and comprehensive marketing and equipment programs that assist the retailer in showcasing their fresh product offering. We believe our investments in infrastructure, combined with our strategically located suppliers and in-house expertise, position us as the leader in providing fresh products and programs to the convenience retail industry. Proper execution of VCI, the cornerstone being dairy distribution, provides Core-Mark the critical mass necessary to offer retailers a multiple weekly delivery platform, which facilitates the proper handling and dating of fresh products. We believe that fresh items are increasingly driving consumer decisions, and will continue to be an important category.

Focused Marketing Initiative ("FMI"). Designed to enhance our relationship with our independent customer base and to further differentiate us in the market place, our FMI program is centered on increasing the sales and profitability of the independent store through improved category insights, optimized retail price strategy and demographic decision-making, along with providing Core-Mark’s marketing solutions to create a comprehensive retail marketing strategy. We believe our innovative approach, which focuses on building a trusted partnership with our customers, has established us as the market leader in providing valuable marketing and supply chain solutions to the convenience retail industry.

Acquisitions and Expansion. We believe there is significant opportunity to increase our market presence and revenue growth through strategic and opportunistic acquisitions and the continued expansion of our credit facility infrastructure. We completed seven acquisitions and added three additional warehouses between 2006 and 2016, which expanded our distribution network, product selection and customer base. We will continue to be opportunistic in pursuing acquisitions that allow further leveraging of our geographic footprint and bring Fresh and VCI to a broader customer base.

Competitive Strengths

We believe we have the following fundamental competitive strengths, which form the foundation for our business strategy:

Innovation and Flexibility. Wholesale distributors typically provide convenience retailers access to a broad product line, the ability to place small quantity orders, inventory management and access to trade credit. Our capability to increase sales and profitability with existing and new customers is based on our ability to deliver consistently high levels of service, innovative marketing programs, technology solutions and logistics support. We believe we are one of the first to recognize emerging trends and to offer retailers our unique strategic solutions such as VCI, Fresh and FMI.

Distribution Capabilities. The wholesale distribution industry is highly fragmented and historically has consisted of a large number of small, privately-owned businesses and a small number of large, full-service wholesale distributors serving multiple geographic regions. Relative to smaller competitors, large national distributors such as Core-Mark benefit from several competitive advantages including: increased purchasing power, the ability to service large national chain accounts, economies of scale in sales and operations, and the resources to invest in information technology and other productivity-enhancing technologies. Our wholesale distributing capabilities provide valuable services to both manufacturers of consumer products and convenience retailers. Manufacturers benefit from our broad retail coverage, inventory management, efficiency in processing small orders and frequency of deliveries. Convenience retailers benefit from our distribution capabilities by gaining access to a broad product line, optimizing inventory management and accessing trade credit.

2

Customers

We service over 43,000 customer locations in 50 states in the U.S. and five Canadian provinces. Our primary customer base consists of traditional convenience stores as well as alternative outlets selling consumer packaged goods. Our traditional convenience store customers include many of the major national and super-regional convenience store operators, as well as independently owned convenience stores. Our alternative outlet customers comprise a variety of store formats, including grocery stores, drug stores, liquor stores, cigarette and tobacco shops, hotel gift shops, military exchanges, college and corporate campuses, casinos, hardware stores, airport concessions and other specialty and small format stores that carry convenience products.

Our top ten customers accounted for 43.2% of our net sales in 2016. Our largest customers were Murphy U.S.A., which the Company began servicing in the first quarter of 2016, and Alimentation Couche-Tard, Inc. ("Couche-Tard"). Murphy U.S.A and Couche-Tard accounted for 12.0% and 11.4% of our total net sales, respectively.

Products

We purchase a variety of brand name and private label products, in excess of 53,000 stock keeping units ("SKUs"), from suppliers and manufacturers. Cigarette products represent less than 5% of our total SKUs purchased. We offer customers a variety of food/non-food products, including fast food, candy, snacks, groceries, fresh products, dairy, bread, beverages, other tobacco products, general merchandise and health and beauty care products.

Below is a comparison of our net sales mix by primary product category for the last three years (in millions):

Year Ended December 31, | ||||||||||||||||||||

2016 | 2015 | 2014 | ||||||||||||||||||

Product Category | Net Sales | % of Net Sales | Net Sales | % of Net Sales | Net Sales | % of Net Sales | ||||||||||||||

Cigarettes | $ | 10,335.7 | 71.1 | % | $ | 7,528.5 | 68.0 | % | $ | 6,942.0 | 67.5 | % | ||||||||

Food (1) | 1,422.5 | 9.8 | 1,251.1 | 11.3 | 1,180.9 | 11.5 | ||||||||||||||

Fresh (1) | 389.8 | 2.7 | 335.0 | 3.0 | 281.1 | 2.7 | ||||||||||||||

Candy | 620.0 | 4.3 | 557.0 | 5.0 | 534.3 | 5.2 | ||||||||||||||

Other tobacco products ("OTP") | 1,133.8 | 7.8 | 870.3 | 8.0 | 827.5 | 8.1 | ||||||||||||||

Health, beauty & general | 446.7 | 3.1 | 368.8 | 3.3 | 361.0 | 3.5 | ||||||||||||||

Beverages | 176.5 | 1.2 | 156.6 | 1.4 | 151.8 | 1.5 | ||||||||||||||

Equipment/other | 4.4 | — | 2.1 | — | 1.5 | — | ||||||||||||||

Total food/non-food products | 4,193.7 | 28.9 | % | 3,540.9 | 32.0 | % | 3,338.1 | 32.5 | % | |||||||||||

Total net sales | $ | 14,529.4 | 100.0 | % | $ | 11,069.4 | 100.0 | % | $ | 10,280.1 | 100.0 | % | ||||||||

(1) | In 2016, the Fresh category was separated from the Food category to better highlight the growth in the Fresh commodity. The 2015 and 2014 presentations have been realigned to reflect these changes. |

Cigarette Products. We purchase cigarette products from major U.S. and Canadian manufacturers. We have no long-term cigarette purchase agreements and buy substantially all of our products on an as-needed basis. Cigarette manufacturers historically offer structured incentive programs to wholesalers based on maintaining market share and executing promotional programs. Net sales of the cigarettes category grew 37.3% in 2016 to $10,335.7 million, accounting for approximately 71.1% of our total net sales and 29.9% of our total gross profit in 2016. We control major purchases of cigarettes centrally to optimize inventory levels and purchasing opportunities, and the daily replenishment of inventory and brand selection is controlled by our distribution centers.

In 2016 our cigarette carton sales in the U.S. and Canada increased 34.5% and 13.8%, respectively, benefiting from market share gains, including the addition of Murphy U.S.A, and the acquisition of Pine State Convenience. In the industry overall, U.S. and Canadian cigarette consumption steadily declined over the last decade. Based on data compiled from the U.S. Department of Agriculture - Economic Research Service and provided by the Tobacco Merchants Association ("TMA"), total cigarette consumption in the U.S declined from 389 billion cigarettes in 2006 to 275 billion cigarettes in 2015, or a compounded annual decline of approximately 3.8%. Total cigarette consumption declined in Canada from 32 billion cigarettes in 2006 to 27 billion cigarettes in 2015, or a compounded annual decline of approximately 1.9% based on statistics provided by the TMA. Although we anticipate overall cigarette consumption will continue to decline, we expect to offset these declines through market share expansion, growth in our non-cigarette categories and incremental gross profit from cigarette manufacturer price increases.

3

We expect cigarette manufacturers will continue to raise prices as carton sales decline in order to maintain or enhance their overall profitability.

Excise taxes are levied on cigarettes and other tobacco products by the U.S. and Canadian federal governments and are also imposed by various states, localities and provinces. We collect state, local, and provincial excise taxes from our customers and remit these amounts to the appropriate authorities based on the credit terms, if applicable, extended by each jurisdiction. Net sales and cost of sales included offsetting amounts related to state, local and provincial excise taxes were approximately $3.0 billion, $2.2 billion and $2.1 billion in 2016, 2015 and 2014, respectively.

Food/Non-food Products. Our food products include fast food, candy, snacks, groceries, beverages and fresh products such as sandwiches, juices, salads, produce, dairy and bread. Our non-food products include cigars, tobacco, health and beauty care products, general merchandise and equipment. Net sales of the combined food/non-food product categories grew 18.4% in 2016 to $4,193.7 million, which was 28.9% of our total net sales driven primarily by incremental sales to existing customers and market share gains including the acquisition of Pine State Convenience. Sales generated from VCI, Fresh and FMI were the primary drivers of the increased sales to existing customers. Gross profit for food/non-food categories grew $59.5 million, or 13.0%, to $516.9 million in 2016, which was 70.1% of our total gross profit. In order to take advantage of the significantly higher margins earned by food/non-food products, two of our key business strategies, VCI and Fresh, focus primarily on the highest margin categories in the food/non-food group. We believe there is an increasing trend toward purchases of fresh food from convenience and other retail store formats. Combined sales of our Food and Fresh categories grew $226.2 million, or 14.3%, to $1,812.3 million. We also believe there is an overall trend toward the increased use of other tobacco products. Sales of OTP increased $263.5 million, or 30.3%, driven primarily by this trend, as well as market share gains. Our strategy is to continue to grow food/non-food products through our VCI, Fresh, and FMI strategies.

Suppliers

We purchase products for resale from approximately 5,000 trade suppliers and manufacturers located across the U.S. and Canada. In 2016, we purchased approximately 79% of our products from our top 20 suppliers, with our top two suppliers, Philip Morris USA, Inc. and R.J. Reynolds Tobacco Company, accounting for approximately 35% and 23% of our purchases, respectively. We coordinate our purchasing from suppliers by negotiating, on a corporate-wide basis, special arrangements to obtain volume discounts and additional incentives, while also taking advantage of promotional and marketing incentives offered to us as a wholesale distributor. In addition, buyers in each of our distribution facilities purchase products directly from the manufacturers, improving product mix and availability for individual markets.

4

Operations

As of December 31, 2016, we operated a network of 30 distribution centers in the U.S. and Canada (excluding two distribution facilities we operate as a third party logistics provider). Twenty-five of our distribution centers are located in the U.S. and five are located in Canada.

The map below depicts the scope of our operations and the names of our distribution centers.

We operate four consolidation centers which buy products from our suppliers in bulk quantities and then re-distribute the products to many of our other distribution centers. The products purchased by our consolidation centers include frozen and chilled items, candy, snacks, beverages, health and beauty care and general merchandise products. We operate two additional facilities as a third party logistics provider. One distribution facility located in Phoenix, Arizona, referred to as the Arizona Distribution Center ("ADC"), is dedicated solely to supporting the logistics and management requirements of one of our major customers, Couche-Tard. The second distribution facility located in San Antonio, Texas, referred to as the Retail Distribution Center ("RDC"), is dedicated solely to supporting another major customer, CST Brands, Inc.

Our proprietary Distribution Center Management System platform provides our distribution centers with the flexibility to adapt rapidly to changing business needs and allows them to provide our customers with necessary information technology requirements and integration capabilities.

Distribution

At December 31, 2016, we had approximately 1,800 transportation department personnel, including delivery drivers, shuttle drivers, routers, training supervisors and managers who focus on achieving safe, on-time deliveries. Our daily orders are picked and loaded nightly in reverse order of scheduled delivery. At December 31, 2016, our distribution fleet primarily consisted of nearly 1,500 leased tractors and trailers with over 500 additional owned trailers. We have made a significant investment over the past few years in upgrading our trailer fleet to tri-temp, which gives us the capability to deliver frozen, chilled and non-refrigerated goods in one delivery. As of December 31, 2016, approximately 97% of our trailers were tri-temp, with the remainder capable of

5

delivering refrigerated and non-refrigerated foods. This provides us the multiple temperature zone capability needed to support our focus on delivering fresh products to our customers. We have transitioned a portion of our truck fleet to Compressed Natural Gas ("CNG"), which allows us to reduce our carbon footprint and lower our transportation costs. As of December 31, 2016, approximately 20% of our trucks ran on CNG. To date, we have opened seven CNG stations, two of which we own, located in Wilkes-Barre, Pennsylvania and Corona, California, and the other five are operated in partnership with U.S. Oil and are located in Aurora, Colorado, Forrest City, Arkansas, Sanford, North Carolina, Atlanta, Georgia and Tampa, Florida under the name GAIN Clean Fuel ("GAIN"). In addition to providing fuel to our fleet, the GAIN stations are also open to other public fleets for fueling.

Competition

Competition within the industry is based primarily on the range and quality of the services provided, price, product selection and the reliability of wholesalers’ logistics as well as proximity to the customer's stores. We operate from a perspective that focuses heavily on flexibility and providing outstanding customer service through our distribution centers, order fulfillment rates, on-time delivery, innovative marketing solutions and merchandising support as well as competitive pricing.

We believe McLane Company, Inc., a subsidiary of Berkshire Hathaway Inc., and Core-Mark are the two largest convenience wholesale distributors (measured by annual sales) in North America. There are two other large companies that cover the eastern half of the U.S: The H.T. Hackney Company and the Eby Brown Company. In addition, there are hundreds of local distributors serving small regional chains and independent convenience retailers. In Canada, in addition to Core-Mark, there is one large national company, Wallace & Carey, Inc., one regional company which services the Manitoba, Saskatchewan and Alberta markets, Pratts Wholesale Limited, and one large national convenience store and grocery wholesaler, Sobeys Inc., aside from Core-Mark, that make up the competitive landscape.

Beyond the traditional wholesale supply channels, we face potential competition from at least three other supply avenues. First, certain manufacturers such as Anheuser-Busch Companies, Inc., MillerCoors LLC, The Coca-Cola Company, Frito-Lay, Inc., a division of PepsiCo, Inc. ("PepsiCo") and PepsiCo deliver their products directly to convenience retailers. Secondly, club wholesalers such as Costco Wholesale Corporation ("Costco") and Sam’s West, Inc. ("Sam’s Club") provide a limited selection of products at generally competitive prices; however, they often have limited delivery options and limited services. Finally, some large convenience retail chains self-distribute products due to the geographic density of their stores and their belief that they can economically service such locations.

We face competition from the diversion into the U.S. and Canadian markets of cigarettes intended for sale outside of such markets, including the sale of cigarettes in non-taxable jurisdictions, inter-state/provincial and international smuggling of cigarettes, the sale of counterfeit cigarettes by third parties, increased imports of foreign low priced brands, the sale of cigarettes by third parties over the internet and by other means designed to avoid collection of applicable taxes. The competitive environment has been characterized by a continued influx of cheap products and tobacco alternatives, including electronic cigarettes that challenge sales of higher priced and fully taxed cigarettes.

Working Capital Practices

We sell products on credit terms to our customers that averaged, as measured by days sales outstanding, about nine days for each of 2016, 2015 and 2014. Credit terms may impact pricing and are competitive within our industry. Many of our customers remit payment electronically, which facilitates efficient and timely monitoring of payment risk. Canadian days sales outstanding in receivables tend to be lower as Canadian industry practice is for shorter credit terms than in the U.S.

We maintain our inventory of products based on the level of sales of the particular product and manufacturer replenishment cycles. The number of days a particular item of inventory remains in our distribution centers varies by product and is principally driven by the turnover of that product and economic order quantities. We typically order and carry in inventory additional amounts of certain critical products to assure high order fulfillment levels for these items. Periodically, we may carry higher levels of inventory to take advantage of anticipated manufacturer price increases. The number of days of cost of sales in inventory averaged about 15 days in 2016, and 16 days in both 2015 and 2014. The cigarette category averaged nine days, ten days, and nine days, in 2016, 2015 and 2014, respectively. The food/non-food categories averaged 27 days in 2016, and 29 days in both 2015 and 2014.

We obtain terms from our vendors and certain taxing jurisdictions based on industry practices, consistent with our credit standing. We take advantage of the full complement of term offerings, which may include enhanced cash discounts for earlier payment or prepayment. Terms for our accounts payable and cigarette and tobacco taxes payable range anywhere from one day prepaid to 60 days credit. Days payable outstanding for both categories, excluding the impact of prepayments, during each of 2016, 2015 and 2014 averaged about 11 days.

6

Employees

The following chart provides a breakdown of our employees by function and geographic region (including employees at our third party logistics facilities) as of December 31, 2016:

TOTAL EMPLOYEES BY BUSINESS FUNCTION

U.S. | Canada | Total | ||||||

Sales and Marketing | 1,465 | 108 | 1,573 | |||||

Warehousing and Distribution | 4,766 | 367 | 5,133 | |||||

Management, Administration, Finance and Purchasing | 834 | 148 | 982 | |||||

Total Categories | 7,065 | 623 | 7,688 | |||||

Three of our distribution centers, Hayward, Las Vegas and Calgary, have employees who are covered by collective bargaining agreements with local affiliates of The International Brotherhood of Teamsters (Hayward and Las Vegas) and the United Food and Commercial Workers International Union (Calgary). Approximately 325 employees, or 4% of our workforce, are unionized. There have been no disruptions in customer service, strikes, work stoppages or slowdowns as a result of union activities, and we believe we have satisfactory relations with our employees.

Regulation

As a distributor of food products in the U.S., we are subject to the Federal Food, Drug and Cosmetic Act and regulations promulgated by the U.S. Food and Drug Administration ("FDA"). In Canada, similar standards related to food and over-the-counter medications are governed by Health Canada. The products we distribute are also subject to federal, state, provincial and local regulation through such measures as the licensing of our facilities, enforcement by state, provincial and local health agencies of relevant standards for the products we distribute and regulation of our trade practices in connection with the sale of our products. Our facilities are inspected periodically by federal, state, provincial and local authorities, including the Occupational Safety and Health Administration ("OSHA") under the U.S. Department of Labor, which require us to comply with certain health and safety standards to protect our employees.

We are also subject to regulation by the U.S. and Canadian Departments of Transportation, which regulate transportation of perishable goods, and similar state, provincial and local agencies. Our distribution centers in the U.S. and Canada are subject to a broad spectrum of federal, state, provincial and local environmental protection statutes including those that govern the emissions to air, soil and water, and the disposal of hazardous substances.

Our policy is to comply with all regulatory and legal requirements and management is not aware of any related issues that may have a material effect upon our business, financial condition or results of operations.

Registered Trademarks

We have registered trademarks including the following: Arcadia Bay®, Arcadia Bay Coffee Company®, Cable Car®, Core-Mark®, Core Solutions Group®, EMERALD®, Java Street®, SmartStock® and Pine State Convenience®.

Segment and Geographic Information

We have two operating segments which aggregate into one reportable segment. We also present certain financial information by segment region -- the U.S. and Canada. See Note 16 - Segment and Geographic Information to our consolidated financial statements.

Seasonality

We typically generate slightly higher net sales and gross profits during the warm weather months (April through September) than in other times throughout the year. We believe this occurs because the convenience store industry tends to be busier due to timing of vacations and increase in travel during this period.

Corporate and Available Information

Our corporate headquarters is located at 395 Oyster Point Boulevard, Suite 415, South San Francisco, California, 94080 and our telephone number is (650) 589-9445.

7

Our internet website address is www.core-mark.com. We provide free access to various reports that we file with or furnish to the U.S. Securities and Exchange Commission ("SEC") through our website, as soon as reasonably practicable after they have been filed or furnished. These reports include, but are not limited to, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports. Our SEC reports can be accessed through the “Investor Relations” section of our website under “Financials and Filings,” or through www.sec.gov. Further, a copy of this Annual Report on Form 10-K is located at the SEC’s Public Reference Room at 100 F Street, NE, Washington D.C. 20549. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.

Also available on our website are printable versions of Core-Mark’s Audit Committee Charter, Compensation Committee Charter, Nominating and Corporate Governance Committee Charter, Code of Business Conduct and Ethics, Corporate Governance Guidelines and Principles and other corporate information. Copies of these documents may also be requested from:

Core-Mark International

395 Oyster Point Blvd, Suite 415

South San Francisco, CA 94080

Attention: Investor Relations

Corporate Governance--Code of Business Conduct and Ethics and Whistle Blower Policy:

Our Code of Business Conduct and Ethics is designed to promote honest, ethical and lawful conduct by all employees, officers and directors and is available on the “Investor Relations” section of our website at www.core-mark.com under “Corporate Governance.”

Additionally, the Audit Committee of the Board of Directors of Core-Mark has established procedures to receive, retain, investigate and act on complaints and concerns of employees, stockholders and others regarding accounting, internal accounting controls and auditing matters, including complaints regarding attempted or actual circumvention of internal accounting controls or complaints regarding violations of our accounting policies. The procedures are also described on our website at www.core-mark.com under “Corporate Governance” in the “Investor Relations” section.

8

ITEM 1A. RISK FACTORS

Our business is subject to a variety of risks. Set forth below are certain of the important risks that we face, the occurrence of which may have a material effect on our business, financial condition or results of operations.

Risks Related to Our Business and Industry

Our ability to operate effectively could be impaired by the risks and costs associated with expansion activities.

Our business has expanded rapidly and market share growth is one of our key company initiatives. To accomplish this growth we have focused on strategic acquisitions and securing large regional and national customers as key elements of success. Any significant expansion activity comes with inherent risks. Acquisitions may entail various risks such as identifying suitable candidates, realizing acceptable rates of return on the investment, identifying potential liabilities, obtaining adequate financing, negotiating acceptable terms and conditions, and successfully integrating operations and converting systems post acquisition. Integrating a large new customer has similar risks of realizing acceptable returns on invested working capital, negotiating acceptable pricing and service levels, while managing resources and business interruptions as we integrate the new business into our current infrastructure. We may realize higher costs, lower margins or fewer benefits than originally anticipated and may experience disruption to our base business in connection with such acquisitions and other new customer integration activities.

We depend on attracting and retaining qualified labor including our senior management and other key personnel.

We substantially depend on the continued services and performance of our senior executive officers as named in our Proxy Statement and other key employees. We do not maintain key person life insurance policies on these individuals, and we do not have employment agreements with any of them. The loss of the services of any of our senior executive officers or other key personnel could harm our business.

We compete with other businesses in each of our markets with respect to attracting and retaining qualified employees. A shortage of qualified employees, especially drivers, in a market could require us to enhance our wage and benefit packages in order to compete effectively in the hiring and retention of qualified employees or to hire more expensive temporary employees. Any such shortage of qualified employees could decrease our ability to effectively serve our customers and might lead to lower profits because of higher labor costs.

Our ability to meet our labor needs is generally subject to numerous other external factors, including prevailing wage rates, changing demographics, health and other insurance costs, and adoption of new or revised employment and labor laws and regulations. These external factors could prevent us from locating, attracting or retaining qualified personnel, which would impact the quality of the services which provide to our customers, and our financial performance may be adversely affected.

We are dependent on the convenience retail industry, and our results of operations could suffer if it experiences an overall decline or consolidation.

The majority of our sales are made under purchase orders and short-term contracts with convenience retail stores which inherently involve significant risks. These risks include declining sales in the convenience retail industry due to general economic conditions, including rising gasoline prices, which may impact “in-store” retail sales, competition from grocery stores and other retail outlets, termination of customer relationships and consolidation of our customer base. Such events could cause us to experience decreases in revenues and put pressure on our margins and increase our credit risk and potential bad debt exposure.

Many of the markets in which we compete are highly competitive and we may lose market share and suffer a decline in sales and profitability in these markets if we are unable to outperform our competition.

Our distribution centers operate in highly competitive markets. We face competition from local, regional and national tobacco and consumable products distributors on the basis of service, price, reliability, delivery schedules, and variety of products offered. We also face competition from club stores and alternate sources that sell consumable products to convenience retailers. Some of our competitors, including McLane Company, Inc. (a subsidiary of Berkshire Hathaway Inc.), have substantial financial resources and long-standing customer relationships. In addition, heightened competition among our existing competitors, or by new entrants into the distribution market, could create additional competitive pressures that may result in the loss of major customers, reduced margins, or have other adverse effects on our business. If we fail to successfully respond to these competitive pressures or to implement our strategies effectively, we may lose market share and our results of operations could suffer.

Our failure to maintain relationships with large customers could potentially harm our business.

We have relationships with many large regional and national convenience and other store chains. While we expect to maintain these relationships for the foreseeable future, any termination, non-renewal or reduction in services that we provide to such customers could cause our revenues and operating results to suffer.

9

We may lose business if manufacturers or large retail customers convert to direct distribution of their products.

In the past, certain large manufacturers and customers have elected to engage in direct distribution or third party distribution of their products and eliminate wholesale distributors such as Core-Mark. If other manufacturers or retail customers make similar elections in the future, our revenues and profits would be adversely affected and there can be no assurance that we will be able to mitigate such losses.

Our business is sensitive to fuel prices and related transportation costs, which could adversely affect our business.

Our operating results are sensitive to, and may be adversely affected by, unexpected increases in fuel or other transportation-related costs, including costs from the use of third party carriers, temporary staff and overtime. Historically, we have been able to pass on a substantial portion of increases in our own fuel or other transportation costs to our customers in the form of fuel or delivery surcharges, but our ability to continue to pass through these increases, is not assured. If we are unable to continue to pass on fuel and transportation-related cost increases to our customers or do not realize the benefits we expect from converting a large percentage of our trucks to operate on natural gas or incur higher expenses if the price of diesel fuel decreases but the price of natural gas does not similarly decrease, our operating results could be negatively affected.

Cigarette and consumable goods distribution is a low-margin business sensitive to inflation and deflation.

We derive most of our revenues from the distribution of cigarettes, other tobacco products, candy, snacks, fast food, groceries, fresh products, dairy, beverages, general merchandise and health and beauty care products. Our industry is characterized by a high volume of sales with low profit margins. Our food/non-food sales are generally priced based on the manufacturer’s cost of the product plus a percentage markup. As a result, our profit levels may be negatively impacted during periods of cost deflation or stagnation for these products, even though our gross profit as a percentage of the price of goods sold may remain relatively constant. In addition, periods of product cost inflation may have a negative impact on our gross profit margins with respect to sales of cigarettes because gross profit on cigarette sales are generally fixed on a cents per carton basis. Therefore, as cigarette prices increase, gross profit generally decreases as a percentage of sales. In addition, if the cost of the cigarettes that we purchase increases due to manufacturer price increases, reduced or eliminated manufacturer discounts and incentive programs or increases in applicable excise tax rates, our inventory carrying costs and accounts receivable could rise, placing pressure on our working capital requirements.

We rely on manufacturer discount and incentive programs and cigarette excise stamping allowances, and any material changes in these programs could adversely affect our results of operations.

We receive payments from the manufacturers on the products we distribute for allowances, discounts, volume rebates and other merchandising and incentive programs. These payments are a substantial contributor to our gross profit. The amount and timing of these payments are affected by changes in the programs by the manufacturers, our ability to sell specified volumes of a particular product, attaining specified levels of purchases by our customers and the duration of carrying a specified product. In addition, we receive discounts from certain taxing jurisdictions in connection with the collection of excise taxes. If the manufacturers or taxing jurisdictions change or discontinue these programs or change the timing of payments, or if we are unable to maintain the volume of our sales required by such programs, our results of operations could be negatively affected.

We depend on relatively few suppliers for a large portion of our products, and any interruptions in the supply of the products that we distribute could adversely affect our results of operations.

We obtain the products we distribute from third party suppliers. At December 31, 2016, we had approximately 5,000 vendors and during 2016 we purchased approximately 79% of our products from our top 20 suppliers, with purchases from our top two suppliers, Philip Morris USA, Inc. and R.J. Reynolds Tobacco Company, representing approximately 35% and 23% of our purchases, respectively. We do not have any long-term contracts with our suppliers committing them to provide products to us. Our suppliers may not provide the products we distribute in the quantities we request on favorable terms, or at all. We are also subject to delays caused by interruption in production due to conditions outside our control, such as slow-downs or strikes by employees of suppliers, inclement weather, transportation interruptions, regulatory requirements and natural disasters. Our inability to obtain adequate supplies of the products we distribute could cause us to fail to meet our contractual and other obligations to our customers and reduce the volume of our sales and profitability.

We may be subject to product liability claims and counterfeit product claims which could materially adversely affect our business.

As a distributor of food and consumer products, we face the risk of exposure to product liability claims in the event that the use of a product sold by us causes injury or illness. In addition, certain products that we distribute may be subject to counterfeiting. Our business could be adversely affected if consumers lose confidence in the safety and quality of the food and other products we distribute. Further, our operations could be subject to disruptions as a result of manufacturer recalls. This risk may increase as we continue to expand our distribution of fresh products. If we do not have adequate insurance, if contractual indemnification

10

from the supplier or manufacturer of the defective, contaminated or counterfeit product is not available, or if a supplier or manufacturer cannot fulfill its indemnification obligations to us, the liability relating to such product claims or disruption as a result of recall efforts could materially adversely impact our results of operations.

We may not be able to achieve the expected benefits from the implementation of marketing initiatives.

We are continuously improving our competitive performance through a series of strategic marketing initiatives. The goal of this effort is to develop and implement a comprehensive and competitive business strategy, addressing the special needs of the convenience industry environment, increasing our market position within the industry and ultimately creating increased stockholder value. Customer acceptance of our new marketing initiatives may not be as anticipated or competitive pressures may cause us to curtail or abandon these initiatives, resulting in lower revenue growth and unachieved cost savings.

Maintaining our brand and reputation is necessary for the success of our business.

Our established brand and reputation within the market largely contributes to our success. Our current and future business could be negatively impacted if we were poorly represented or garnered negative publicity through various media channels, which include but are not limited to, print, broadcast, web-based, and social media. Brand value is based in large part on perceptions of subjective qualities, and even isolated incidents can erode trust and confidence, particularly if they result in adverse publicity, governmental investigations or litigation. Even if the aforementioned situations were unfounded or not material to our business, these events could still diminish demand for our products and services and erode customer confidence. If any of these events were to occur, they could have a negative impact on our results of operations and financial condition.

Our information technology systems may be subject to failure, disruptions, security breaches (such as malware, viruses, hacking or other cyber-attacks) which could compromise our ability to conduct business, seriously harm our business and adversely affect our financial results.

Our business is highly dependent on our enterprise information technology systems. We rely on our information technology systems and our internal information technology staff to maintain the information required to operate our distribution centers and to provide our customers with fast, efficient and reliable deliveries. We have taken steps to increase redundancy in our information technology systems and have disaster recovery plans in place to mitigate events that could disrupt our systems’ service. However, if our systems fail or are not reliable, we may suffer disruptions in service to our customers and our results of operations could suffer.

We may upgrade and replace various components of our proprietary enterprise resource planning ("ERP") system periodically with the goal of maintaining and improving overall functionality, performance and service. As technology-based solutions become more integrated with our service offerings, our ability to service our customers could be impacted, creating additional competitive pressure and causing us to lose market share.

In addition, we retain sensitive data, including intellectual property, proprietary business information and personally identifiable information, in our secure data centers and on our networks. We may face threats to our data centers and networks of unauthorized access, security breaches and other system disruptions. Despite our security measures, our infrastructure may be vulnerable to attacks by experienced hackers or other disruptive events.

Computer malware, viruses, hacking and other cyber-attacks have become more prevalent and may occur on our systems in the future. Intruders may also take the form of parties that attempt to fraudulently induce employees or other users of our systems to disclose sensitive or confidential information or otherwise disrupt operations. Any such security breach may compromise information stored on our networks and may result in significant data losses or theft of intellectual property, proprietary business information or personally identifiable information belonging to us or our customers, business partners or employees. Though it is difficult to determine what, if any, harm may directly result from any specific interruption or attack, any failure to maintain performance, reliability and security affects the availability of our technical infrastructure and technology-based services. Any such failure may harm our reputation and our ability to retain existing customers and attract new customers and could impact our results of operation.

We may be subject to various claims and lawsuits that could result in significant expenditures.

The nature of our business exposes us to the potential for various claims and litigation related to labor and employment, personal injury, property damage, business practices, environmental liability and other matters. Any material litigation or a catastrophic accident or series of accidents could have a material adverse effect on our business, financial position and results of operations and cash flows.

Unions may attempt to organize our employees.

As of December 31, 2016, 325, or approximately 4%, of our employees were covered by collective bargaining agreements with labor organizations, which agreements expire at various times. We cannot assure that we will be able to renew our respective

11

collective bargaining agreements on favorable terms, that employees at other facilities will not unionize or that our labor costs will not increase. In addition, the United States National Labor Relations Board ("NLRB") is becoming more active with the passage of administrative rules that could impact our ability to manage our labor force and wage successful campaigns preventing further unionization of our employees. To the extent we suffer business interruptions as a result of strikes or other work stoppages or slow-downs, or our labor costs increase and we are not able to recover such increases through increased prices charged to customers or offsets by productivity gains, our results of operations could be materially adversely affected.

Employee health benefit costs represent a significant expense to us and may negatively affect our profitability.

With over 5,000 employees and their families participating in our health plans, our expenses relating to employee health benefits are substantial. In past years, we have experienced significant increases in certain of these costs, largely as a result of economic factors beyond our control, including, in particular, ongoing increases in health care costs well in excess of the rate of inflation. Increased participation in our health plans, continued increasing health care costs, as well as changes in laws, regulations and assumptions used to calculate health and benefit expenses, may adversely affect our business, financial position and results of operations. In addition, the Patient Protection and Affordable Care Act ("ACA") may continue to increase our employee healthcare-related costs. We have migrated a significant number of employees to our high deductible plan resulting in a reduction in our claims exposure and offsetting other costs related to ACA. While we have taken steps to minimize the impact of ACA, there is no guarantee our efforts will be successful.

Changes to minimum wage laws and other governmental legislation or regulations could increase our costs substantially.

As of December 31, 2016, we had no employees who were paid under the minimum wage in their respective locations. Several bills have been introduced in the U.S. legislature over the past few years to increase the federal minimum wage. In addition, certain states have adopted or are considering adopting minimum wage statutes that exceed the federal minimum wage rate. Any increases in federal or state minimum wages could require us to increase the wages paid to our minimum wage employees and create pressure to raise wages for other employees who already earn above-minimum wages. If we are unable to pass these additional labor costs on to our customers in the form of increased prices or surcharges, our business and results of operations would be adversely affected.

If we are unable to comply with governmental regulations that affect our business or if there are substantial changes in these regulations, our business could be adversely affected.

As a distributor of food and other consumable products, we are subject to regulation by the FDA, Health Canada and similar regulatory authorities at the federal,state, provincial and local levels. In addition, our employees operate tractor trailers, trucks, forklifts and various other powered material handling equipment and we are therefore subject to regulation by the U.S. and Canadian Departments of Transportation. Our operations are also subject to regulation by OSHA, the U.S. Drug Enforcement Administration and a myriad of other federal, state, provincial and local agencies. Each of these regulatory authorities has broad administrative powers with respect to our operations. Regulations, and the costs of complying with those regulations, have been increasing in recent years. If we fail to adequately comply with government regulations, we could experience increased inspections or audits, regulatory authorities could take remedial action including imposing fines or shutting down our operations or we could be subject to increased compliance costs. If any of these events were to occur, our results of operations would be adversely affected.

Natural disaster damage could have a material adverse effect on our business.

Our headquarters and several of our warehouses in California, and one warehouse located near Vancouver, British Columbia, Canada, are in or near high hazard earthquake zones. We also have operations in areas that have been affected by natural disasters such as hurricanes, tornados, floods, and ice and snow storms. While we maintain insurance to cover us for certain potential losses, our insurance may not be sufficient in the event of a significant natural disaster or payments under our policies may not be received timely enough to prevent adverse impacts on our business. Our customers could also be affected by like events, which could adversely affect our sales and results of operations.

Insurance and claims expenses could have a material adverse effect on us.

We have a combination of both self-insurance and high-deductible insurance programs for the risks arising out of the services we provide and the nature of our operations throughout North America, including claims exposure resulting from personal injury, property damage, business interruption and workers’ compensation. Workers’ compensation, automobile and general liabilities are determined using actuarial estimates of the aggregate liability for claims incurred and an estimate of incurred but not reported claims. Our accruals for insurance reserves reflect certain actuarial assumptions and management judgments, which are subject to a high degree of variability. If the number or severity of claims for which we are retaining risk increases, our financial condition and results of operations could be adversely affected. If we lose our ability to self-insure these risks, our insurance costs could materially increase and we may find it difficult to obtain adequate levels of insurance coverage.

12

Risks Related to the Distribution of Cigarettes and Other Tobacco Products

Our sales volume is largely dependent upon the distribution of cigarettes, sales of which are declining generally.

The distribution of cigarettes is currently a significant portion of our business. In 2016, approximately 71.1% of our net sales (which includes excise taxes) and 29.9% of our gross profit were generated from the distribution of cigarettes. Due to increases in the prices of cigarettes, restrictions on cigarette manufacturers’ marketing and promotions, increases in cigarette regulation and excise taxes, health concerns, increased pressure from anti-tobacco groups, the rise in popularity of tobacco alternatives, including electronic cigarettes, and other factors, cigarette consumption in the U.S. and Canada has been declining gradually over the past few decades. In most instances, tobacco alternatives, such as electronic cigarettes, are not subject to federal, state, provincial and local excise taxes like the sale of conventional cigarettes or other tobacco products. We expect consumption trends of legal cigarette products will continue to be negatively impacted by the factors described above. In addition, we expect rising prices may lead to a higher percentage of consumers purchasing cigarettes through illicit markets, over the internet and by other means designed to avoid payment of cigarette taxes. If we are unable to sell other products to make up for these declines in cigarette unit sales, our operating results may suffer.

Legislation, regulation and other matters are negatively affecting the cigarette and tobacco industry.

The tobacco industry is subject to a wide range of laws and regulations regarding the marketing, distribution, sale, taxation and use of tobacco products imposed by governmental entities. Various jurisdictions have adopted or are considering legislation and regulations restricting displays and marketing of tobacco products, establishing fire safety standards for cigarettes, raising the minimum age to possess or purchase tobacco products, requiring the disclosure of ingredients used in the manufacture of tobacco products, imposing restrictions on public smoking, restricting the sale of tobacco products directly to consumers or other recipients over the internet and other tobacco product regulation. In addition, the FDA has been empowered to regulate changes to nicotine yields and the chemicals and flavors used in tobacco products (including cigars, pipe and e-cigarette products), require ingredient listings be displayed on tobacco products, prohibit the use of certain terms which may attract youth or mislead users as to the risks involved with using tobacco products, as well as limit or otherwise impact the marketing of tobacco products by requiring additional labels or warnings as well as pre-approval by the FDA. Such legislation and related regulation is likely to continue adversely impacting the market for tobacco products and, accordingly, our sales of such products.

In Canada, many provinces have enacted legislation authorizing and facilitating the recovery by provincial governments of tobacco-related health care costs from the tobacco industry by way of lawsuit. Some Canadian provincial governments have either already initiated lawsuits or indicated an intention that such lawsuits will be filed. It is unclear at this time how such restrictions and lawsuits may affect Core-Mark and its Canadian operations.

If excise taxes are increased or credit terms are reduced, our sales of cigarettes and other tobacco products could decline and our liquidity could be negatively impacted.

Cigarettes and tobacco products are subject to substantial excise taxes in the U.S. and Canada. Significant increases in cigarette-related taxes and/or fees have been proposed or enacted and are likely to continue to be proposed or enacted by various taxing jurisdictions within the U.S. and Canada as a means of increasing government revenues. These tax increases negatively impact consumption. Additionally, they may cause a shift in sales from premium brands to discount brands, illicit channels or tobacco alternatives, such as electronic cigarettes, as smokers seek lower priced options.

Taxing jurisdictions have the ability to change or rescind credit terms currently extended for the remittance of tax that we collect on their behalf. If these excise taxes are substantially increased or credit terms are substantially reduced, it could have a negative impact on our liquidity. Accordingly, we may be required to obtain additional debt financing, which we may not be able to obtain on satisfactory terms or at all.

Our distribution of cigarettes and other tobacco products exposes us to potential liabilities.

In June 1994, the Mississippi attorney general brought an action against various tobacco industry members on behalf of the state to recover state funds paid for health care costs related to tobacco use. Most other states sued the major U.S. cigarette manufacturers based on similar theories. In November 1998, the major U.S. tobacco product manufacturers entered into a Master Settlement Agreement ("MSA") with 46 states, the District of Columbia and certain U.S. territories. The other four states--Mississippi, Florida, Texas and Minnesota (non-MSA states)--settled their litigations with the major cigarette manufacturers by separate agreements. The MSA and the other state settlement agreements settled health care cost recovery actions and monetary claims relating to future conduct arising out of the use of, or exposure to, tobacco products, imposed a stream of future payment obligations on major U.S. cigarette manufacturers and placed significant restrictions on the ability to market and sell cigarettes. The payments required under the MSA result in the products sold by the participating manufacturers to be priced at higher levels than non-MSA manufacturers. In addition, the growth in market share of discount brands since the MSA was signed has had an adverse impact on the total volume of the cigarettes that we sell.

13

In connection with the MSA, we were indemnified by most of the tobacco product manufacturers from which we purchased cigarettes and other tobacco products for liabilities arising from our sale of the tobacco products that they supplied to us. Should the MSA ever be invalidated, we could be subject to substantial litigation due to our distribution of cigarettes and other tobacco products, and we may not be indemnified for such costs by the tobacco product manufacturers in the future. In addition, even if we are indemnified by cigarette manufacturers that are parties to the MSA, future litigation awards against such cigarette manufacturers could be so large as to prevent the manufacturers from satisfying their indemnification obligations.

T

Risks Related to Financial Matters, Financing and Foreign Exchange

Changes to federal, state or provincial income tax legislation could have a material adverse effect on our business and results of operations.

From time to time, new tax legislation is adopted by the federal government and various states or other regulatory bodies. Significant changes in tax legislation could adversely affect our business or results of operations in a material way. For example, in the U.S. the federal government has in the past proposed legislation which effectively could limit, or even eliminate, use of the last-in, first-out ("LIFO") inventory method for financial and income tax purposes. Although the final outcome of any such proposals cannot be ascertained, the ultimate financial impact to us of the transition from LIFO to another inventory method could be material to our operating results.

We may not be able to settle our qualified defined benefit pension plan on terms or pricing which is satisfactory to us.

We record a liability associated with the underfunded status of our pension plan when the benefit obligation exceeds the fair value of the plan assets. As of December 31, 2016, our pension plan was 88% funded and our consolidated balance sheet included $4.3 million in pension liabilities related to underfunded pension obligations. On September 14, 2016, our Board of Directors approved termination of our qualified defined-benefit pension plan. We expect to complete the settlement before the end of 2017. Our pension liabilities are expected to be settled through either lump sum payments or purchasing annuities from an insurance Company. We may not be able to consummate the sale or purchase of annuities with counterparties on terms or pricing suitable to us.

There can be no assurance that we will continue to declare cash dividends in the future or in any particular amounts and if there is a reduction in dividend payments, our stock price may be harmed.

Since the fourth quarter of 2011, we have paid a quarterly cash dividend to our stockholders. We intend to continue to pay quarterly dividends subject to capital availability and periodic determinations by our Board of Directors that cash dividends are in the best interest of our stockholders and are in compliance with all applicable laws and agreements to which we are a party. Future dividends may be affected by a variety of factors such as available cash, anticipated working capital requirements, overall financial condition, credit agreement restrictions, future prospects for earnings and cash flows, capital requirements for acquisitions, stock repurchase programs, reserves for legal risks and changes in federal and state income tax laws or corporate laws. Our Board of Directors may, at its discretion, decrease or entirely discontinue the payment of dividends at any time. Any such action could have a material, negative effect on our stock price.

Currency exchange rate fluctuations could have an adverse effect on our revenues and financial results.

We generate a significant portion of our revenues in Canadian dollars, approximately 10% in 2016 and 11% in 2015. We also incur a significant portion of our expenses in Canadian dollars. To the extent that we are unable to match revenues received in Canadian dollars with costs paid in the same currency, exchange rate fluctuations in Canadian dollars could have an adverse effect on our financial results. During times of a strengthening U.S. dollar, our reported sales and earnings from our Canadian operations will be reduced because the Canadian currency will be translated into fewer U.S. dollars. Conversely, during times of a weakening U.S. dollar, our reported sales and earnings from our Canadian operations will be increased because the Canadian currency will be translated into more U.S. dollars. U.S. GAAP requires that foreign currency transaction gains or losses on short-term intercompany transactions be recorded currently as gains or losses within the statement of operations. To the extent we incur losses on such transactions, our net income will be reduced. We currently do not hedge our Canadian foreign currency cash flows.

We may not be able to borrow additional capital to provide us with sufficient liquidity and capital resources necessary to meet our future financial obligations.

We expect that our principal sources of funds will be cash generated from our operations and, if necessary, borrowings under a $600 million revolving credit facility ("Credit Facility") as of December 31, 2016. On November 4, 2016, we entered into a ninth amendment to the Credit Facility which increased our Credit Facility from $450 million to $600 million. The Credit Facility, initially dated as of October 12, 2005, as amended or otherwise modified from time to time, is between us, as Borrowers, the Lenders named therein, and JPMorgan Chase Bank, N.A., as administrative agent. The Credit Facility expires in May 2020. While

14

we believe our sources of liquidity are adequate, we cannot assure that these sources will be available or continue to provide us with sufficient liquidity and capital resources required to meet our future financial obligations, or to provide funds for our working capital, capital expenditures and other needs. As such, additional equity or debt financing sources may be necessary, in addition we may not be able to expand our existing Credit Facility or obtain new financing on terms satisfactory to us.

Our operating flexibility is limited in significant respects by the restrictive covenants in our Credit Facility.

Our Credit Facility imposes restrictions on us that could increase our vulnerability to general adverse economic and industry conditions by limiting our flexibility in planning for and reacting to changes in our business and industry. Specifically, these restrictions place limits on our ability, among other things, to: incur additional indebtedness, pay dividends, issue stock of subsidiaries, make investments, repurchase stock, create liens, enter into transactions with affiliates, merge or consolidate, or transfer and sell our assets. In addition, under our Credit Facility, under certain circumstances we are required to meet a fixed charge coverage ratio. Our ability to comply with this covenant may be affected by factors beyond our control and a breach of the covenant could result in an event of default under our Credit Facility, which would permit the lenders to declare all amounts incurred thereunder to be immediately due and payable and terminate their commitments to make further extensions of credit.

Our actual business and financial results could differ as a result of the accounting methods, estimates and assumptions that we use in preparing our financial statements, which may negatively impact our results of operations and financial condition.

To prepare financial statements in conformity with GAAP, management is required to exercise judgment in selecting and applying accounting methodologies and making estimates and assumptions. These methods, estimates, and assumptions are subject to uncertainties and changes, which affect the reported values of assets and liabilities, revenues and expenses, and disclosures of contingent assets and liabilities. Areas requiring significant estimates by our management include but are not limited to the following: allowance for doubtful accounts, provisions for income taxes, vendor rebates and promotional allowances, valuation of goodwill and long-lived assets, valuation of assets and liabilities in connection with business combinations, valuation of pension assets and obligations, stock-based compensation expense and accruals for estimated liabilities, including litigation and insurance reserves.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our headquarters are located in South San Francisco, California, and consist of approximately 31,800 square feet of leased office space. We also lease approximately 20,000 square feet for use by our information technology and tax personnel in Richmond, British Columbia, approximately 6,000 square feet for use by our information technology personnel in Plano, Texas, and approximately 3,600 and 2,000 square feet of additional office space in Fort Worth, Texas and Phoenix, AZ, respectively. We lease approximately 4.9 million square feet and own approximately 0.6 million square feet of distribution space.

Distribution Center Facilities by City and State of Location(1) | ||

Albuquerque, New Mexico | Hayward, California | Spokane, Washington |

Atlanta, Georgia | Las Vegas, Nevada | Tampa, Florida |

Bakersfield, California | Leitchfield, Kentucky | Whitinsville, Massachusetts |

Corona, California(2) | Los Angeles, California | Wilkes-Barre, Pennsylvania |

Denver, Colorado | Minneapolis, Minnesota | Calgary, Alberta |

Forrest City, Arkansas(3) | Portland, Oregon | Toronto, Ontario |

Fort Worth, Texas | Sacramento, California(4) | Vancouver, British Columbia |

Gardiner, Maine | Salt Lake City, Utah | Winnipeg, Manitoba |

Glenwillow, Ohio | Sanford, North Carolina | Mississauga, Ontario(5) |