Attached files

| file | filename |

|---|---|

| 10-K - FORM 10-K - ARKANOVA ENERGY CORP. | form10k.htm |

| EX-32.1 - EXHIBIT 32.1 - ARKANOVA ENERGY CORP. | exhibit32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - ARKANOVA ENERGY CORP. | exhibit31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - ARKANOVA ENERGY CORP. | exhibit31-1.htm |

![]()

January 18, 2017

Mr. Pierre Mulacek

Provident Energy of Montana, LLC

3809 Juniper Trace, Suite 201

Austin, Texas 78738

|

Subject: |

Reserve Estimate and Financial Forecast as to Provident Energy of Montana, LLC’s Interests in the Two Medicine Cut Bank Sand Unit, Cut Bank Field, Glacier and Pondera Counties, Montana |

Dear Mr. Mulacek:

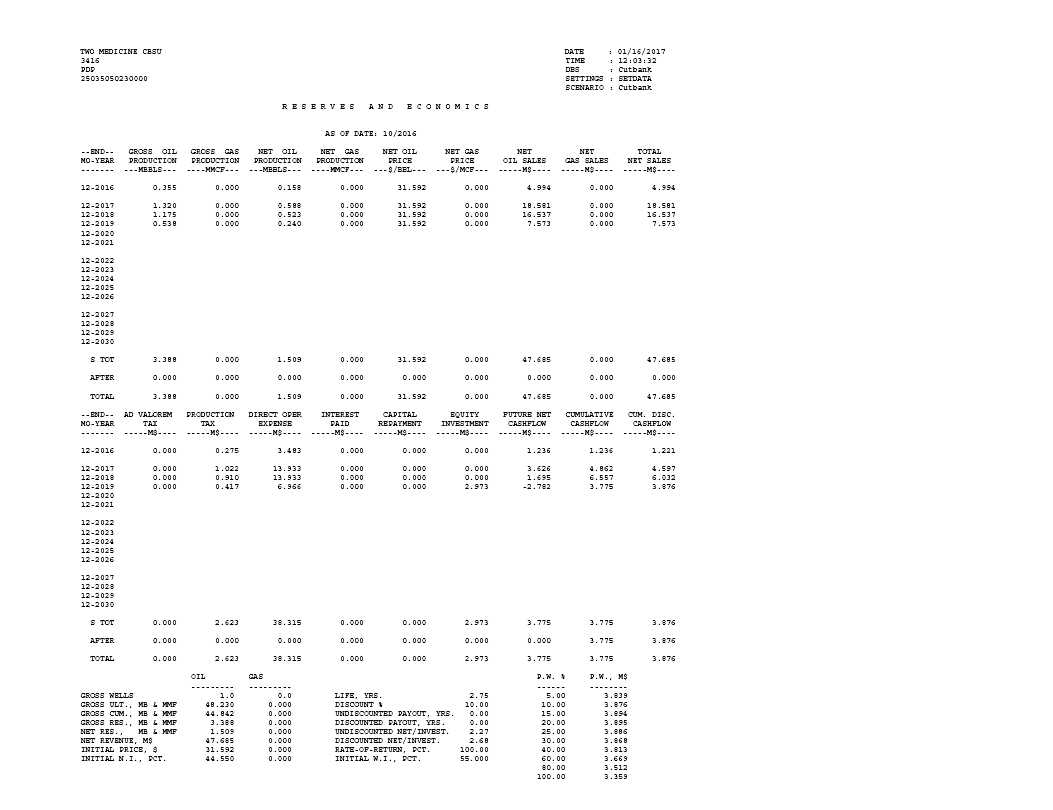

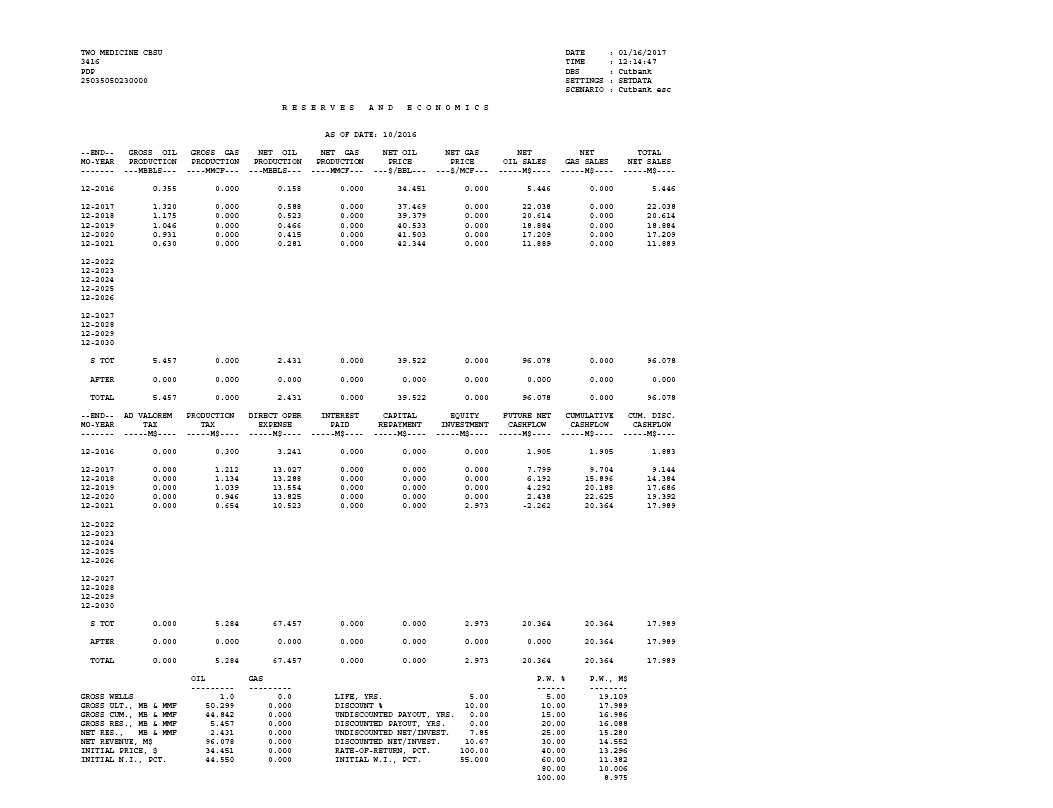

As per your request, Gustavson Associates, LLC., has conducted an independent reserve evaluation and estimated the future net revenue attributable as to Provident Energy of Montana, LLC’s interests in the Two Medicine Cut Bank Sand Unit (TMCBSU), Cut Bank Field, Glacier and Pondera Counties, Montana. It is our understanding that Provident Energy of Montana, LLC plans to include this report as part of a filing with the United States Securities and Exchange Commission (SEC). Therefore, this report is focused on Proved reserves and cash flow projections deriving there from. Estimates and projections have been made as of September 30, 2016. Reserves have been estimated in accordance with the US Securities and Exchange Commission’s (SEC) definitions and guidelines.

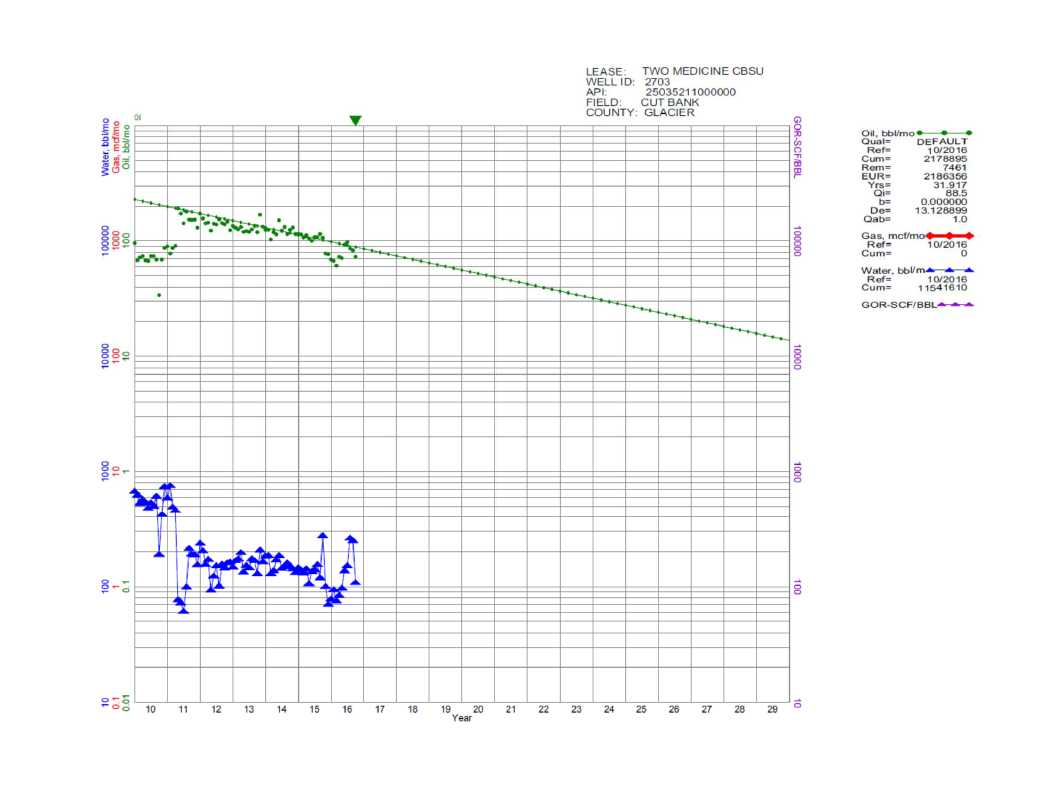

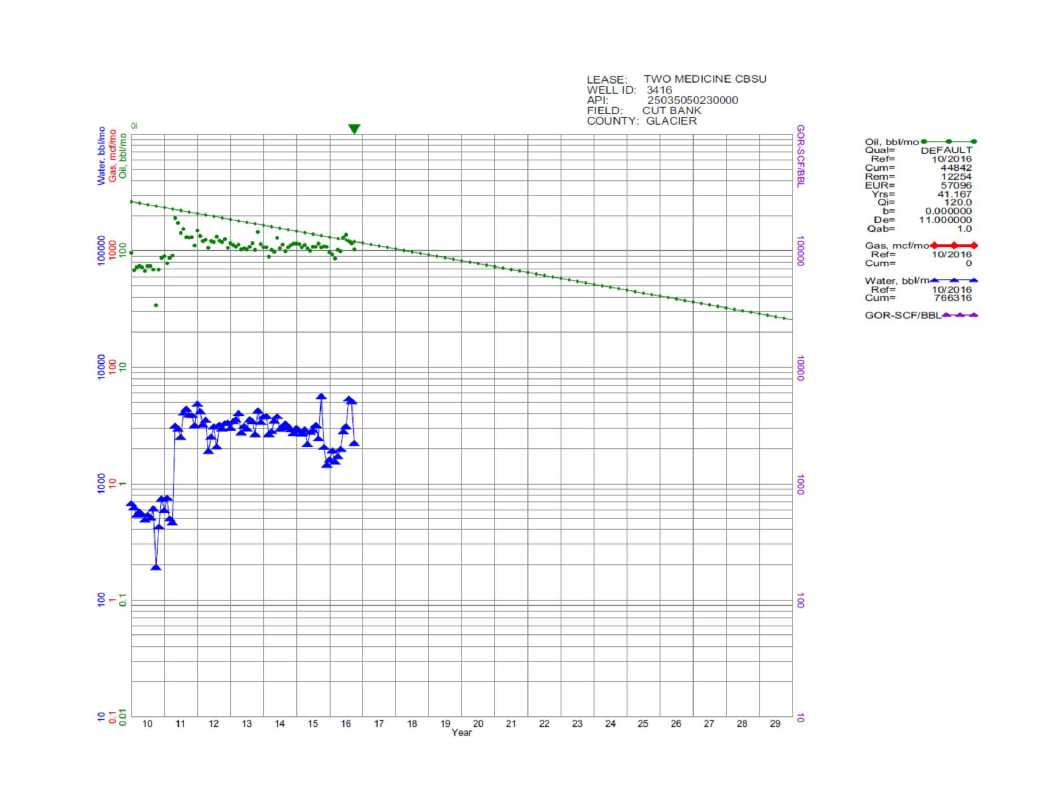

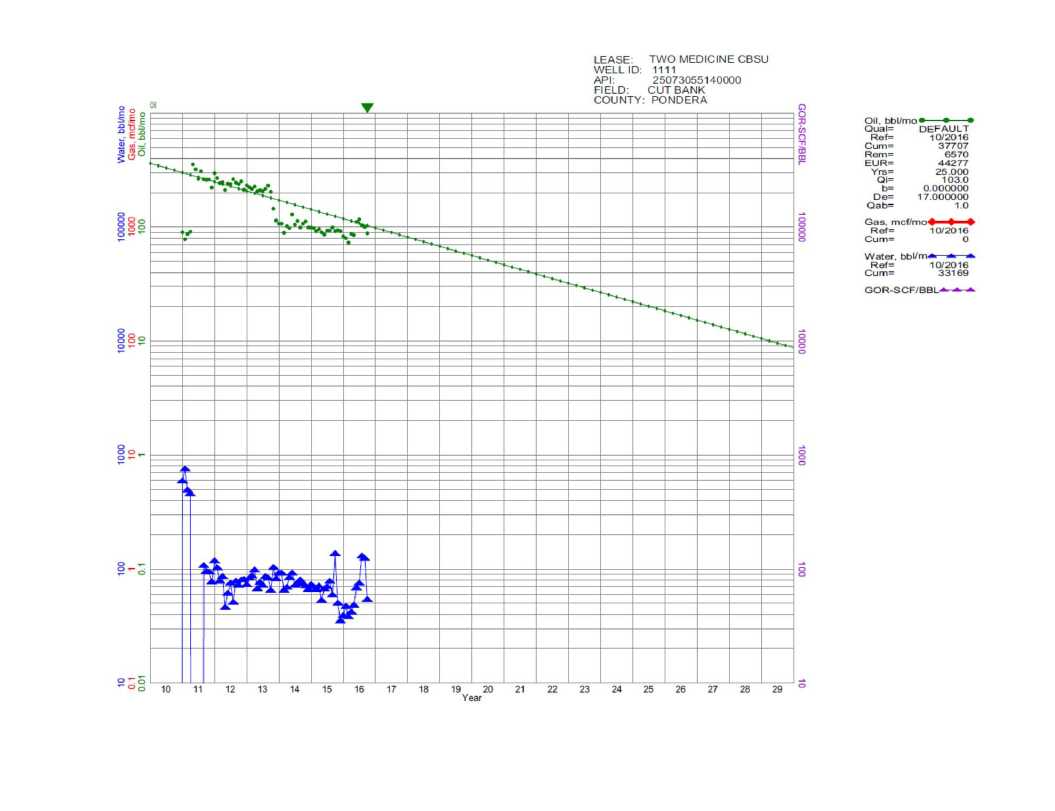

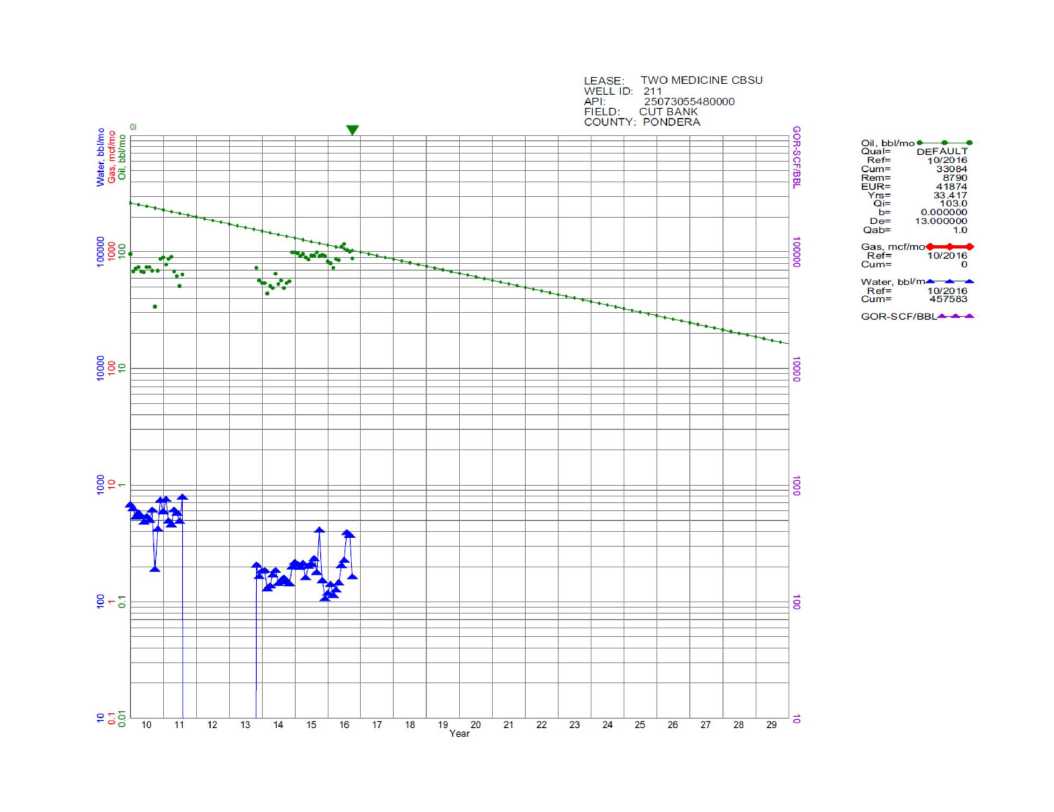

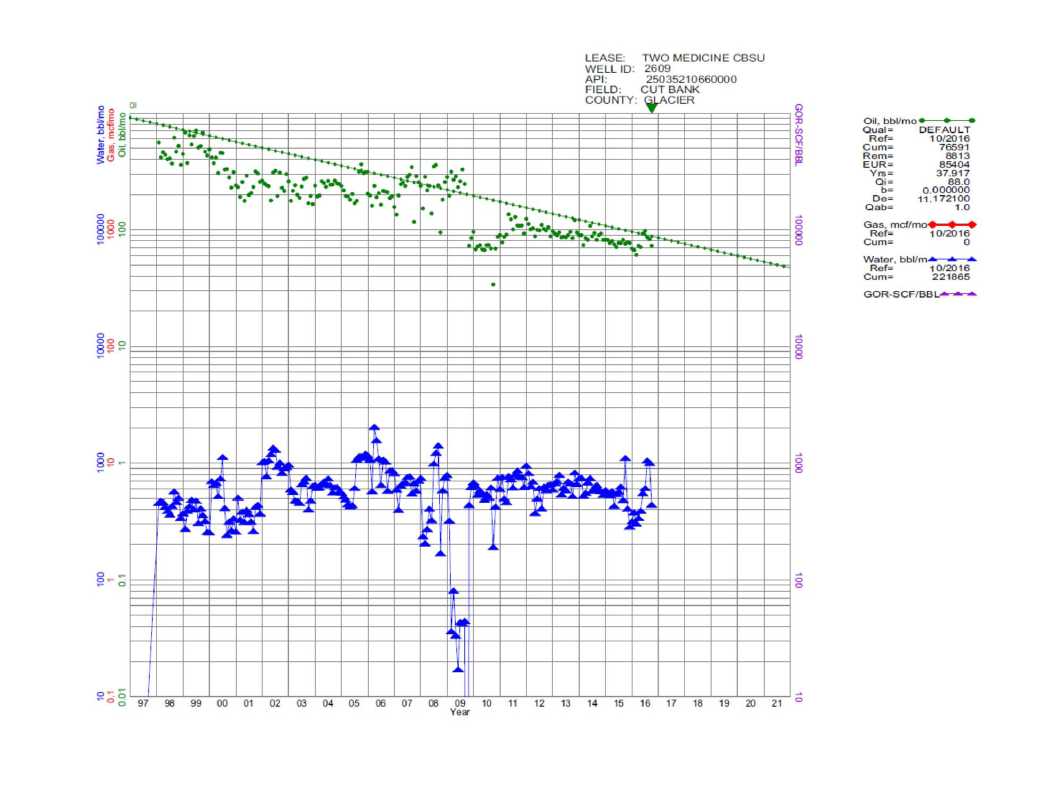

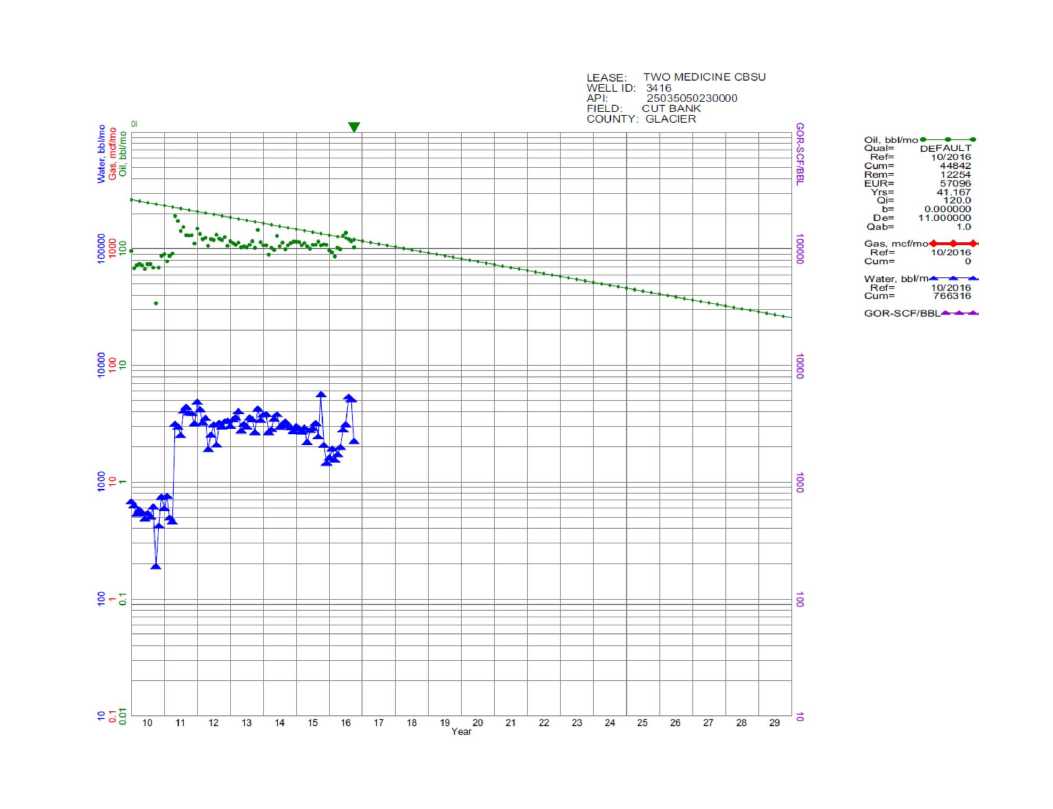

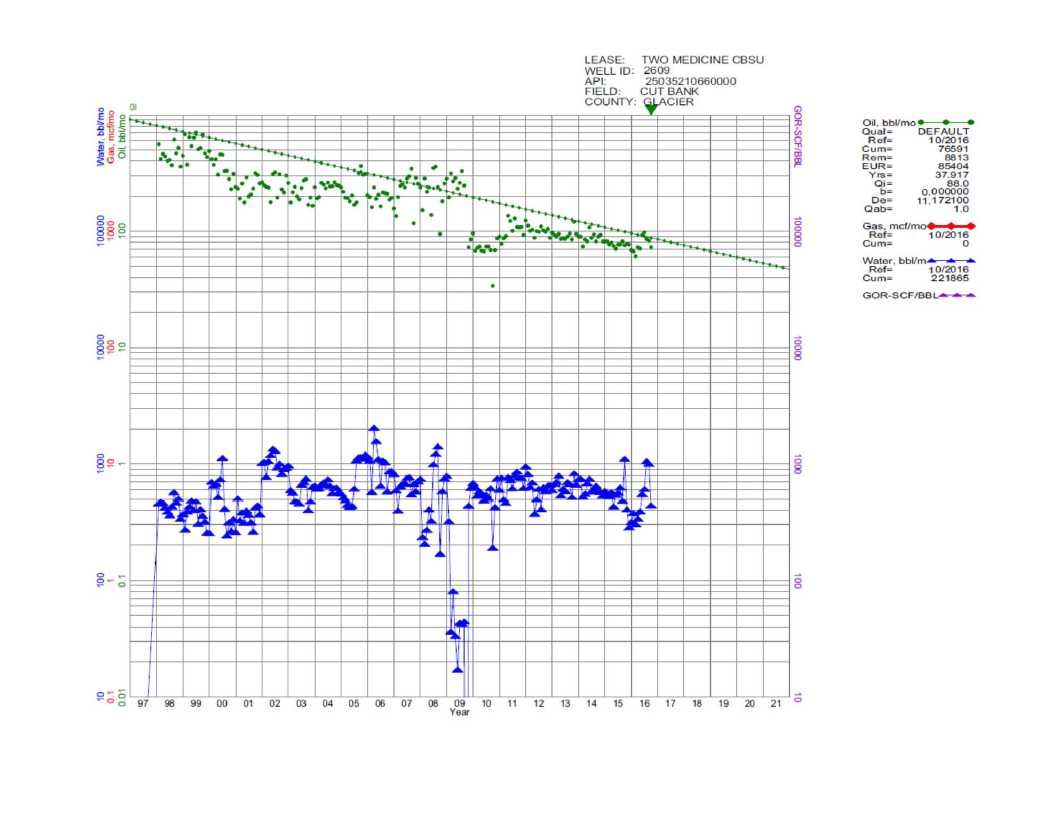

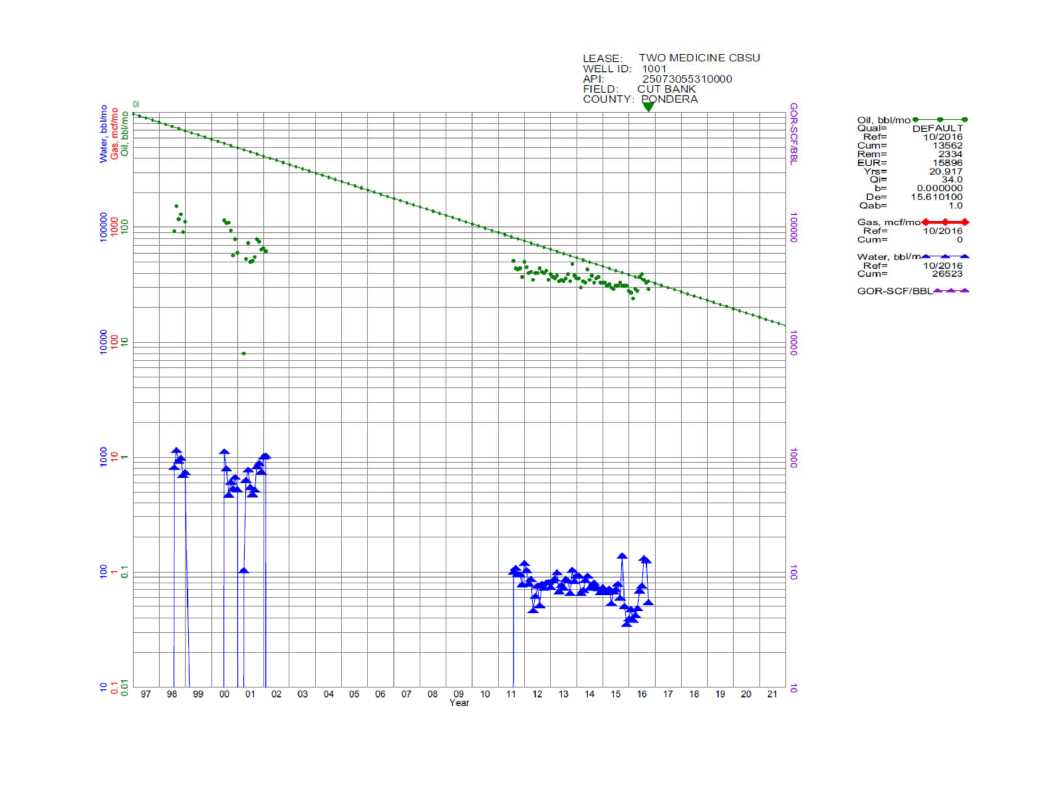

Proved Developed Producing (PDP) reserves have been assigned to three of the 36 currently producing wells in the Cut Bank Field under the flat pricing scenario, with five wells economic under the escalated price scenario. The remaining wells were found to be uneconomic under current operating conditions.

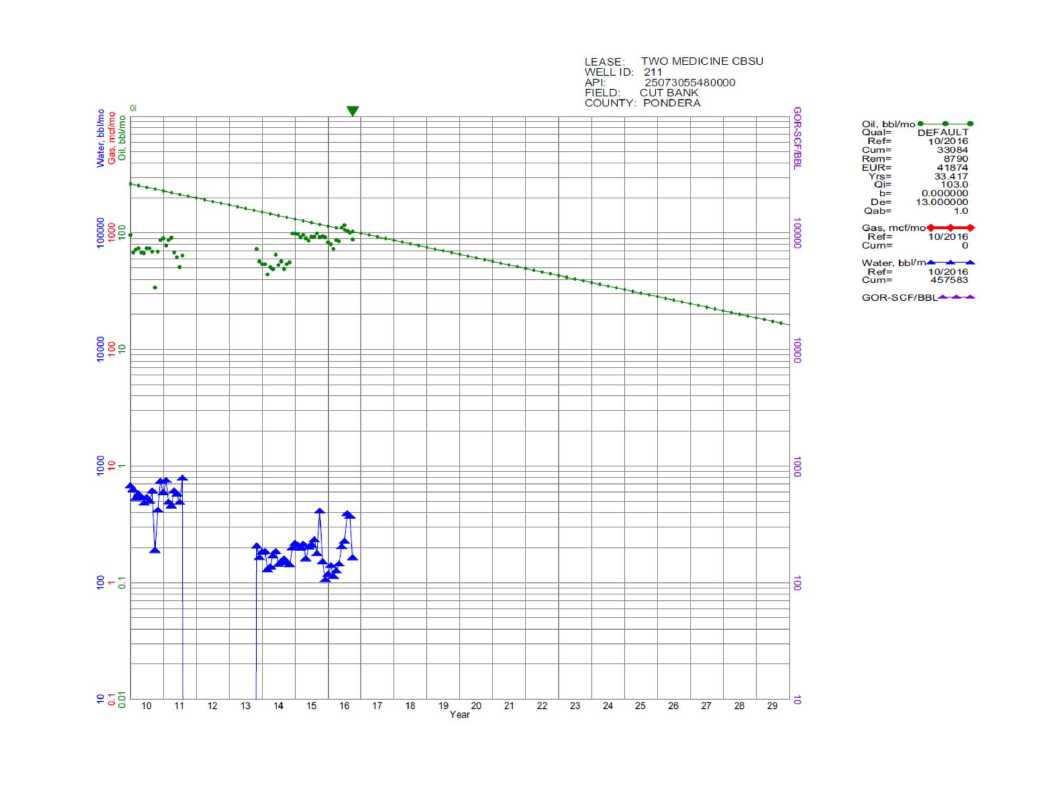

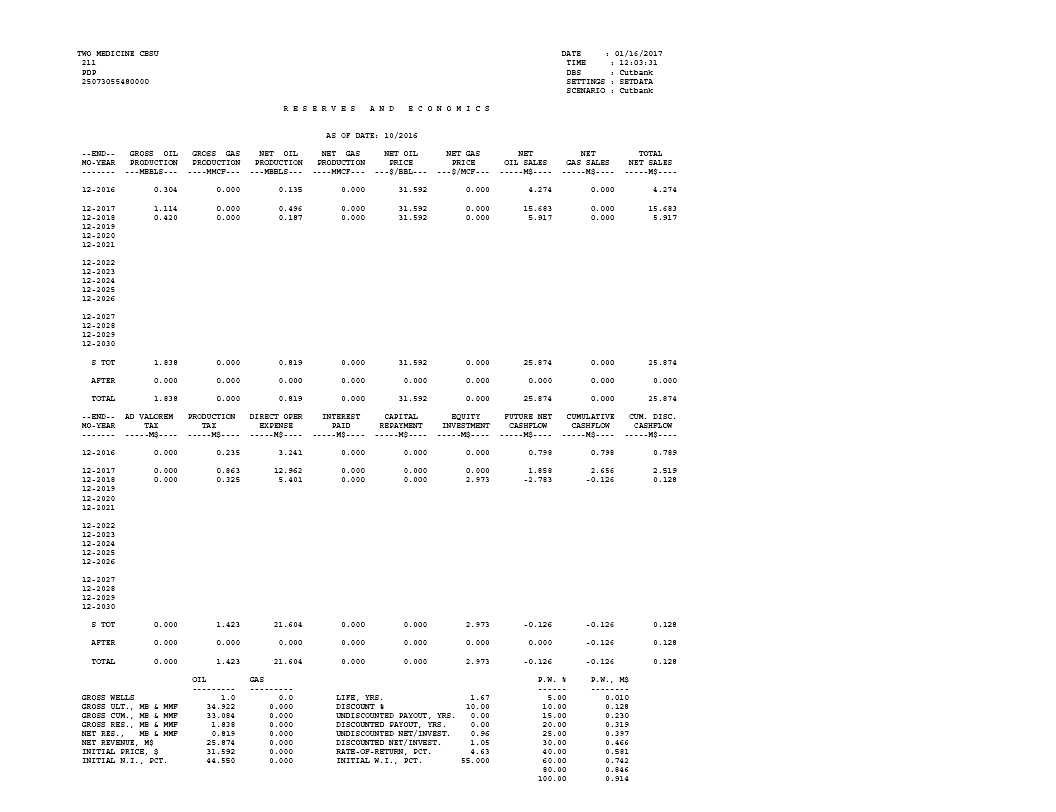

The operator has indicated that they have no further plans for workovers or drilling; therefore, no Proved Undeveloped reserves have been assigned. Waterflood was re-started in the unit in October 2014, and initial response has been seen. This Consultant’s estimates of net reserves and future net revenues for the total of the wells in which Provident Energy of Montana, LLC currently holds an interest described herein, as of September 30, 2016, are shown in Table 1 below. Reserve estimates and production rate projections were based on the extrapolation of established performance trends.

5757 Central Ave. Suite D Boulder, Co. 80301 USA 1-303-443-2209 FAX 1-303-443-3156 http://www.gustavson.com

Mr. Pierre Mulacek

January 18, 2017

Page 2

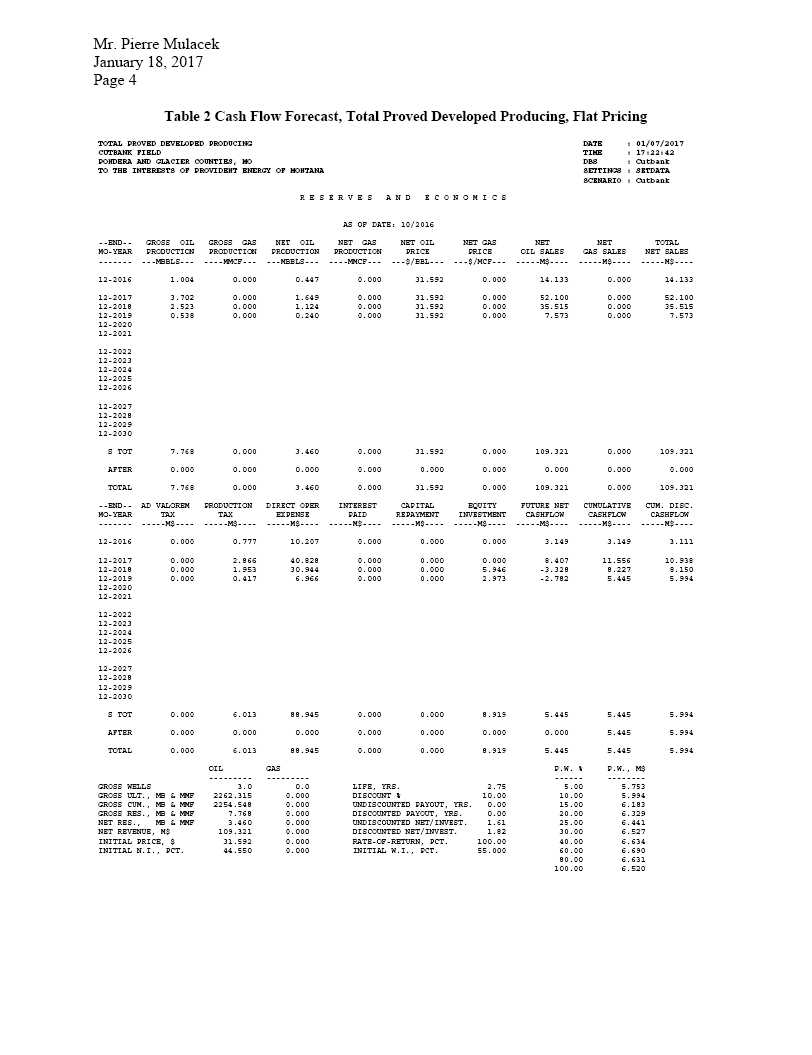

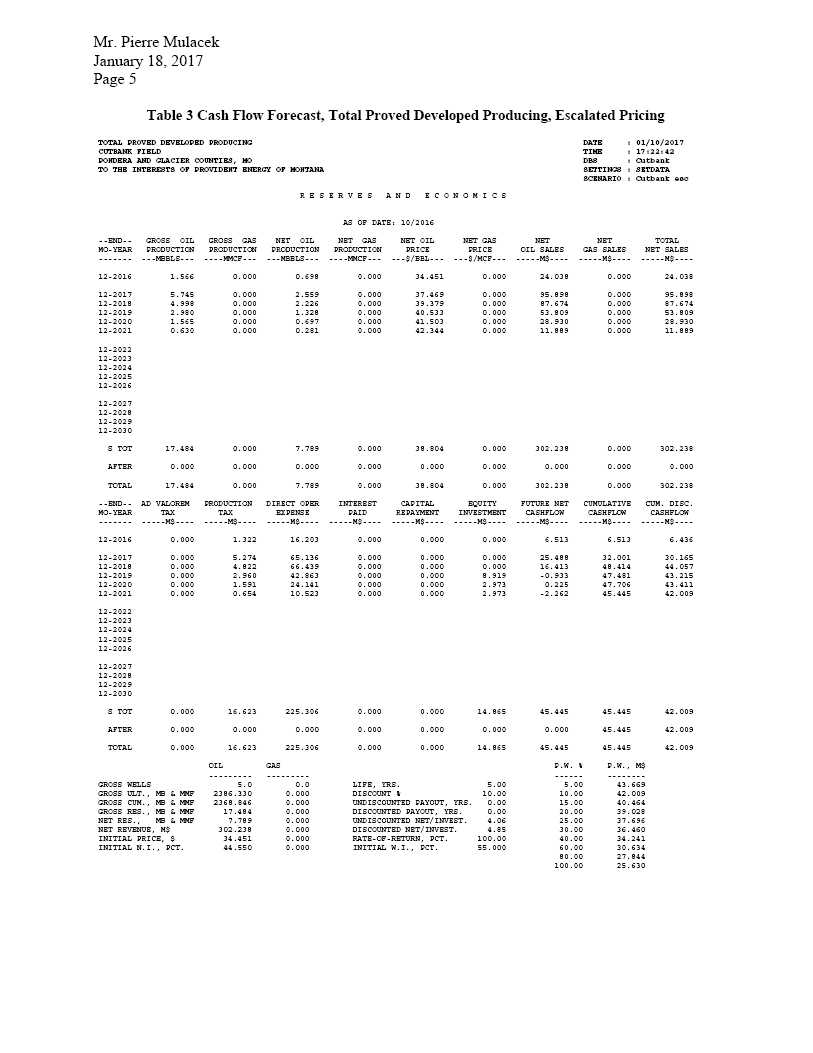

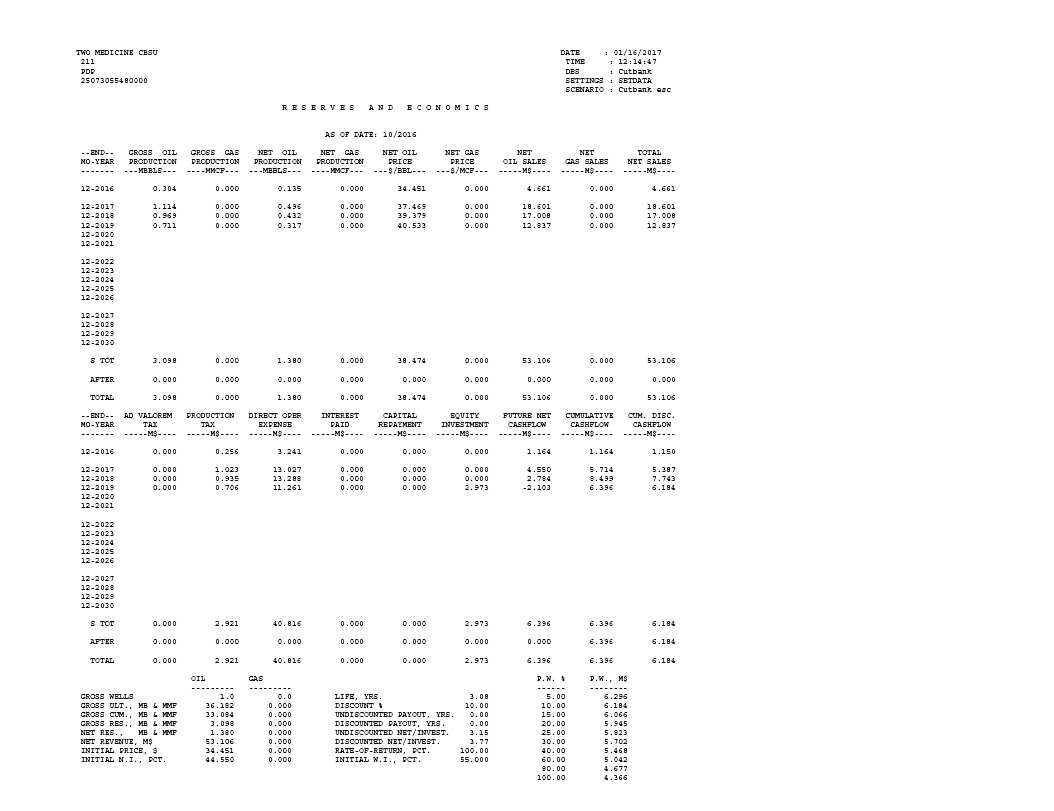

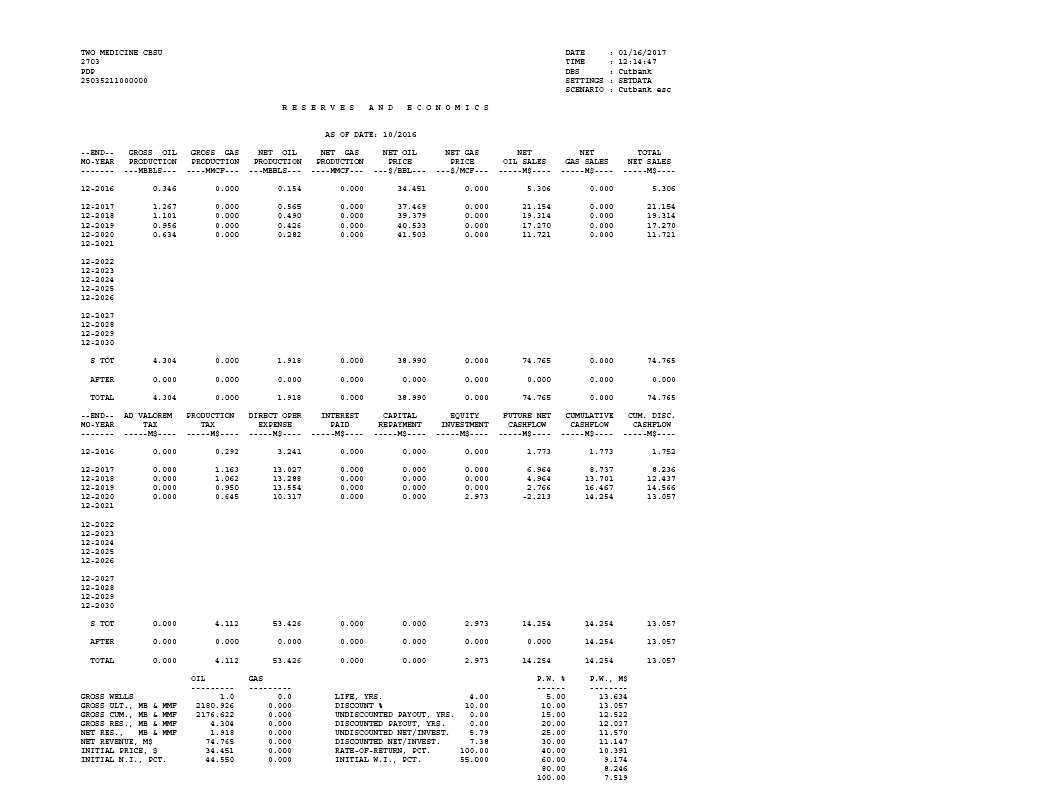

Table 1 Reserves and Cash Flow Summary

| Reserve Category | Estimated Net Reserves | Estimated Future Net Revenue* | |

| Oil (BBL) | Undiscounted

($) |

Discounted at

10% ($) | |

| Proved Developed Producing, Flat Pricing | 3,460 | 5,445 | 5,994 |

| Proved Developed Producing, Escalated Pricing | 7,789 | $45,445 | $42,009 |

*Before deduction of Federal Income Tax

For the flat pricing scenario, the lease operating cost used in this analysis was $1964 per well per month based on the average cost reported by the client. Oil prices were based on the average price paid to the client from the first day of each month in the previous twelve months. This was found to be $41.35. Costs and prices were held flat.

For the escalated pricing scenario, oil prices were based on the Nymex futures prices for the ten days preceding the effective date. The oil prices were then adjusted for local differentials which came out to be -23.6% from the West Texas Intermediate (WTI) price. The $1964 per well per month costs were escalated at 2% per year for 7 years and held flat thereafter.

Estimated future net revenue reflects the deductions of severance and ad valorem taxes and operating costs. Since all of the wells were found to qualify as stripper wells with a production rate of less than 10 barrels of oil per day, the severance tax rate of 5.5% was utilized (compared with 9.0% for wells with over 10 Bbl of daily oil production). Federal income taxes and other indirect costs have not been deducted. A per well abandonment cost of $5,405 was applied at the end of economic life for each well. These costs were all charged against the Proved Developed Producing (PDP) reserves. A detailed assessment of potential environmental liabilities has not been performed; thus, these estimated costs could vary. It is our understanding that Provident Energy of Montana, LLC’s interest in the property is 55 % working interest and 44.55 % net revenue interest.

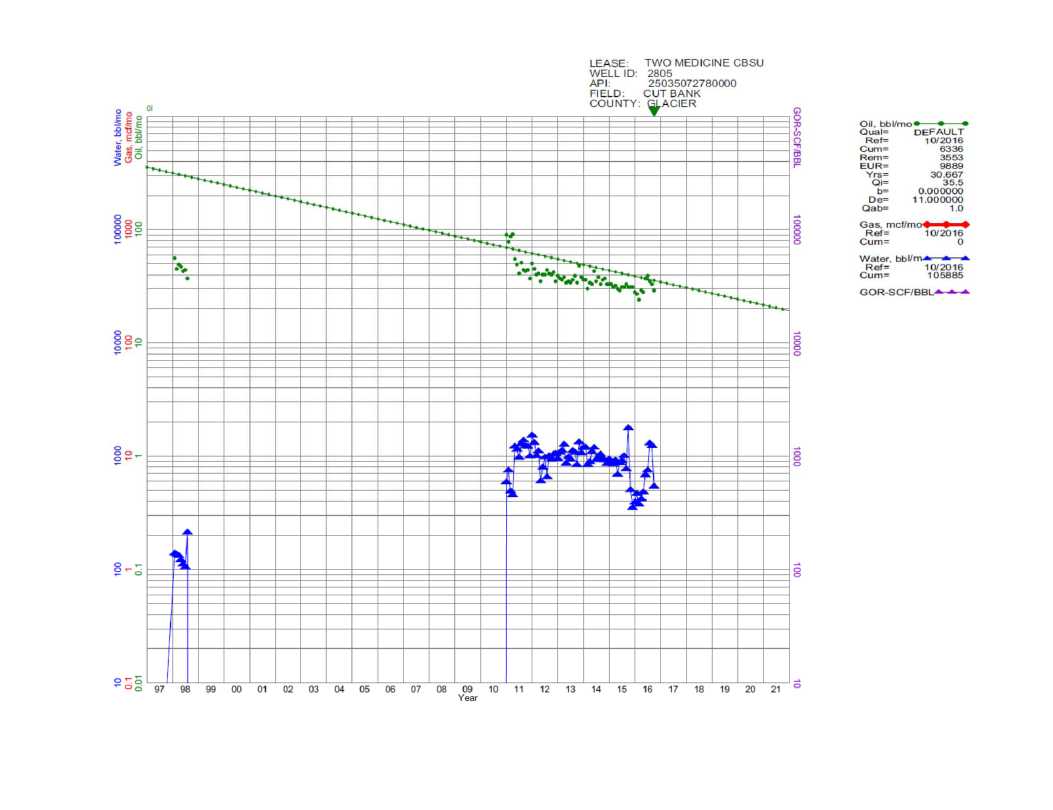

The summary cash flow forecasts by category are included as Table 2 and Table 3. Note that due to the economic parameters, 33 producing wells were found to be uneconomic under current conditions. Appendix A illustrates the decline curve forecasts and cash flows for the 3 economic PDP wells and the waterflood PDNP reserves. The decline curves for the 3 uneconomic wells are shown in Appendix B.

Limiting Conditions and Disclaimers

Reserve estimates presented in this report were based on data and records obtained from Provident Energy of Montana, LLC, Big Bear, IHS Energy, and the Montana Oil and Gas Conservation Division.

Mr. Pierre Mulacek

January 18, 2017

Page 3

Gustavson Associates, LLC, holds neither direct nor indirect financial interest in the subject properties, in Provident Energy of Montana, LLC, or in any other affiliated companies.

The accuracy of any reserve estimate is a function of available data and of geological and engineering interpretation and judgment. While the reserve estimate presented herein is believed to be reasonable, it should be viewed with the understanding that subsequent reservoir performance, changes in pricing structure or market demand may justify its revision.

All data utilized in the preparation of this report are available for examination in our offices. Please contact us if we can be of assistance. We appreciate the opportunity to be of service and look forward to further serving Provident Energy of Montana, LLC.

Very truly yours,

GUSTAVSON ASSOCIATES, LLC.

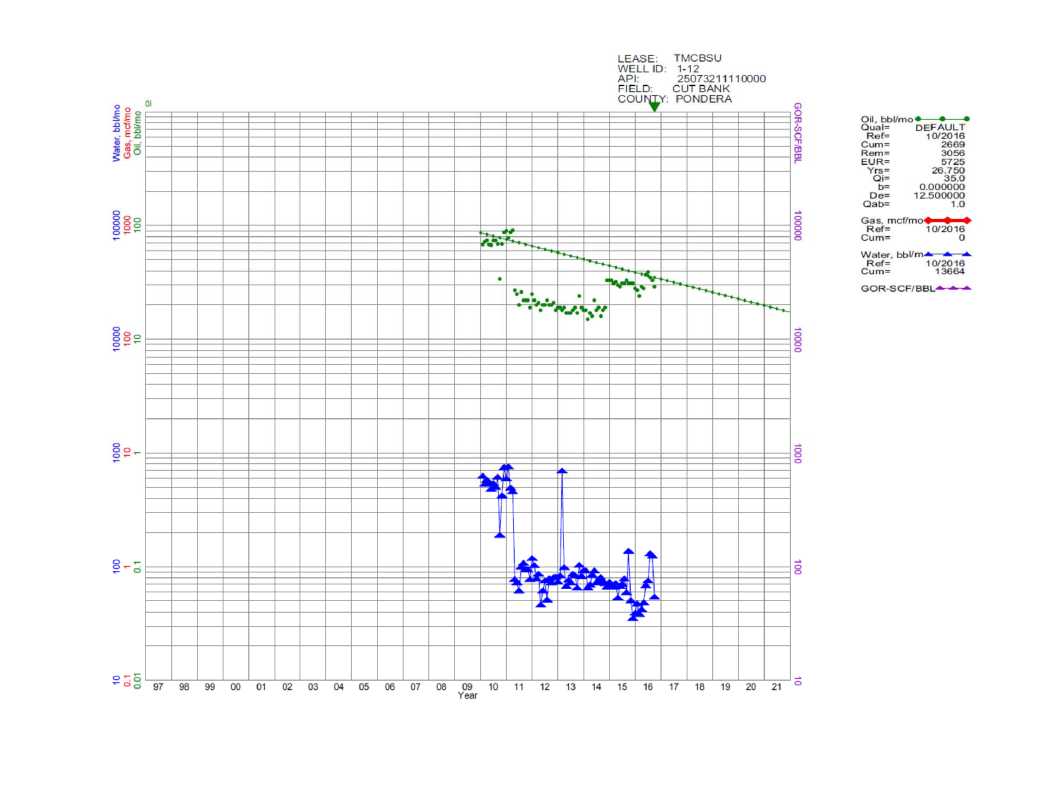

APPENDIX A

DECLINE CURVE FORECASTS

&

WELL CASH FLOWS

Flat Pricing

![]()

Escalated Pricing

![]()

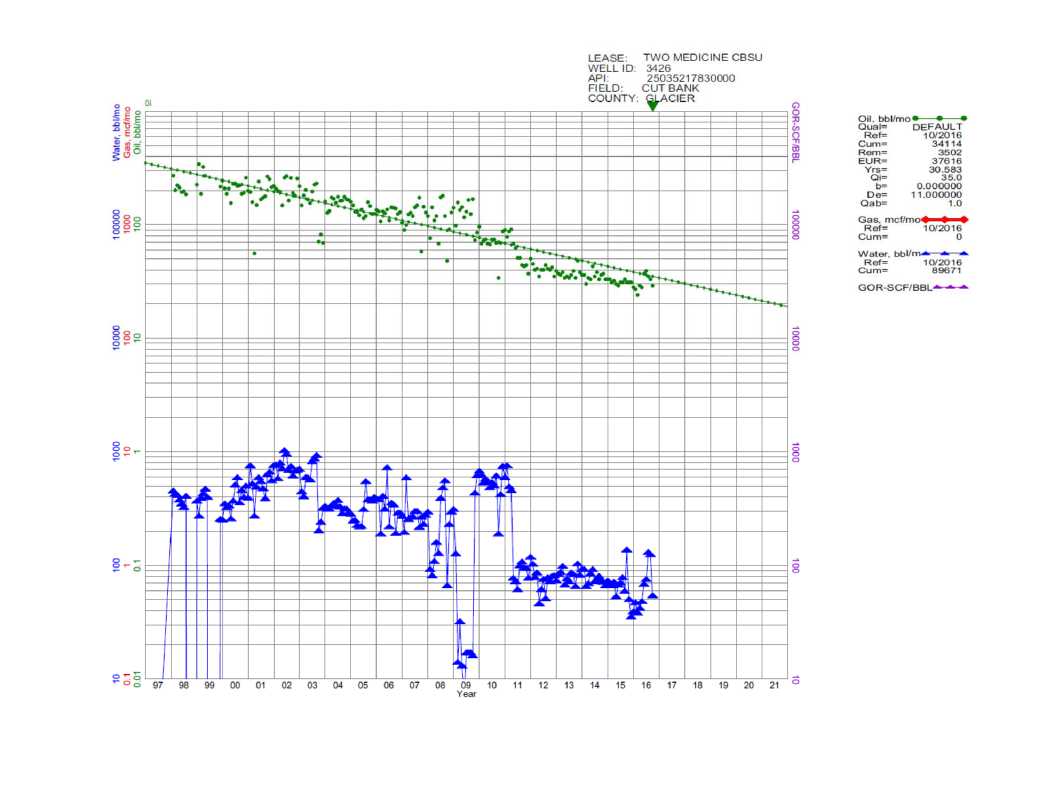

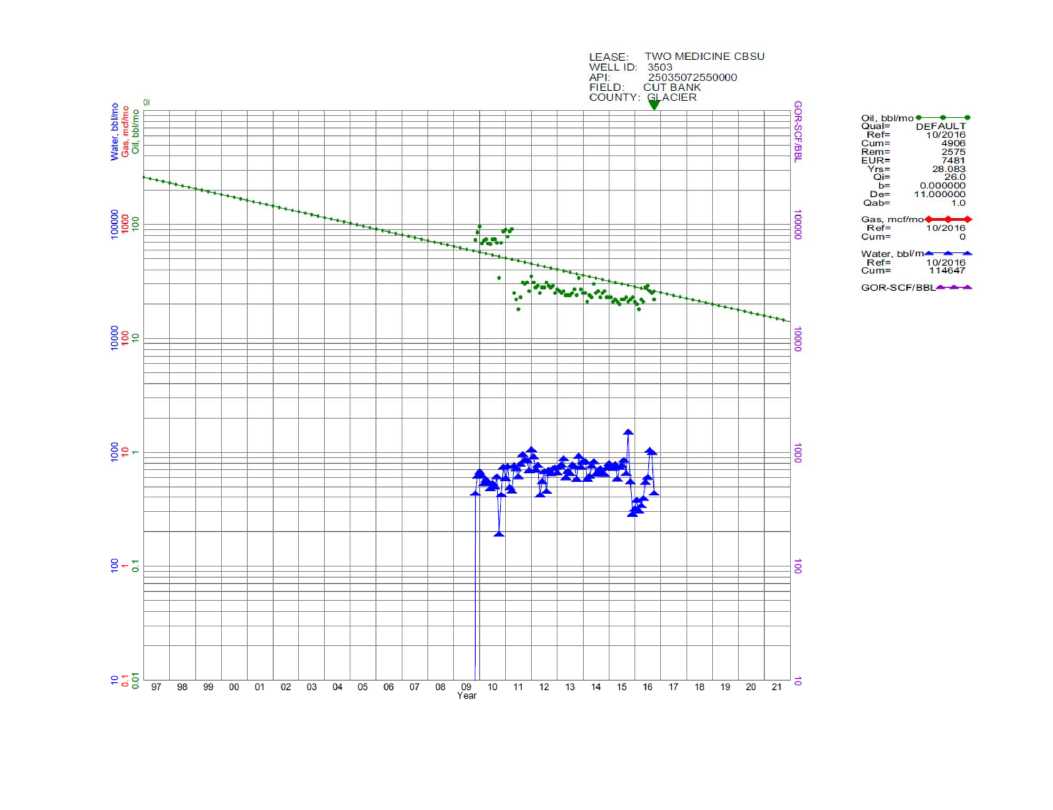

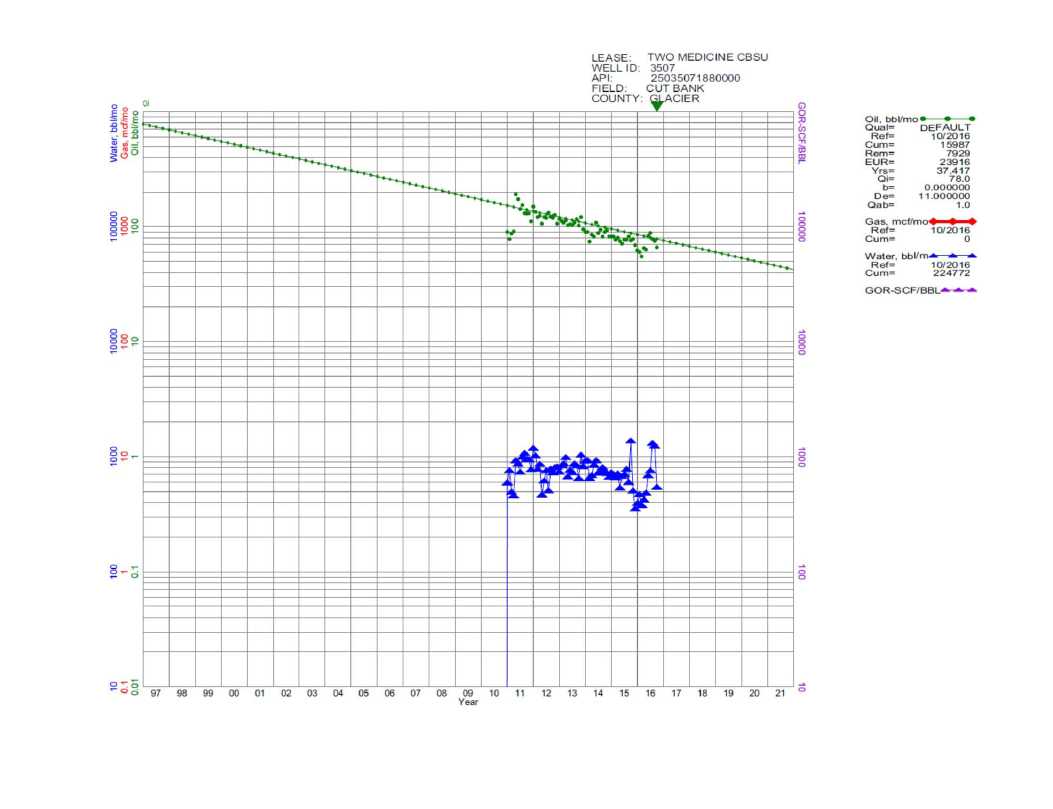

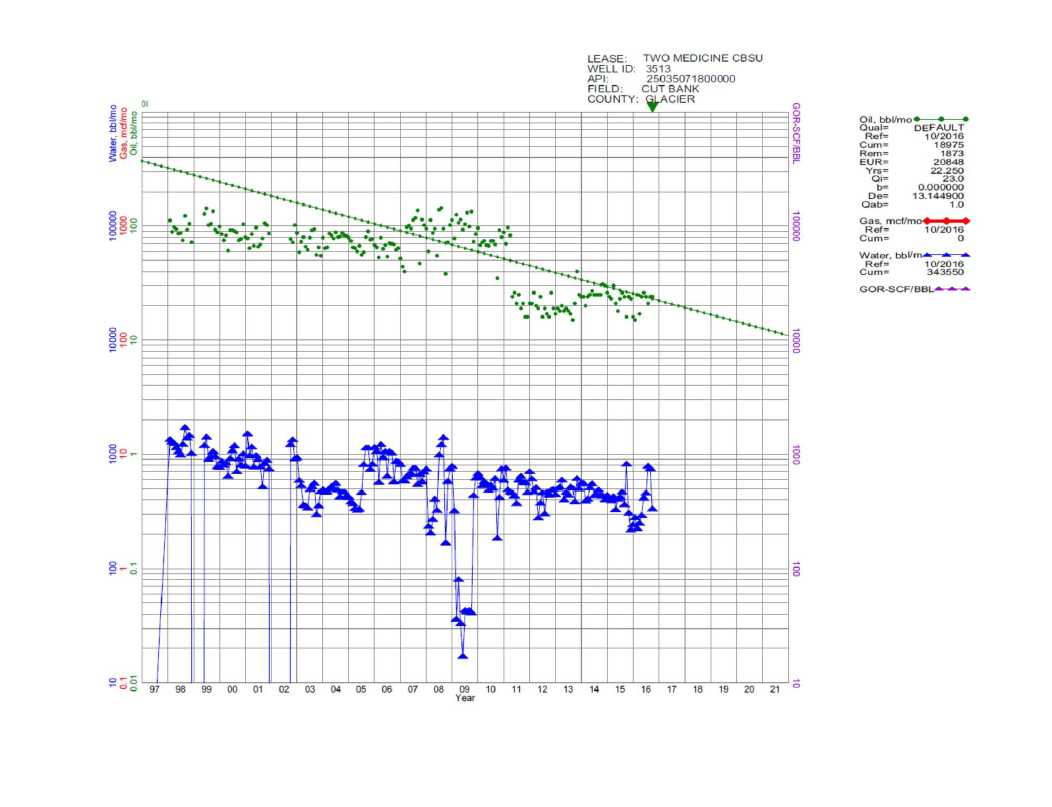

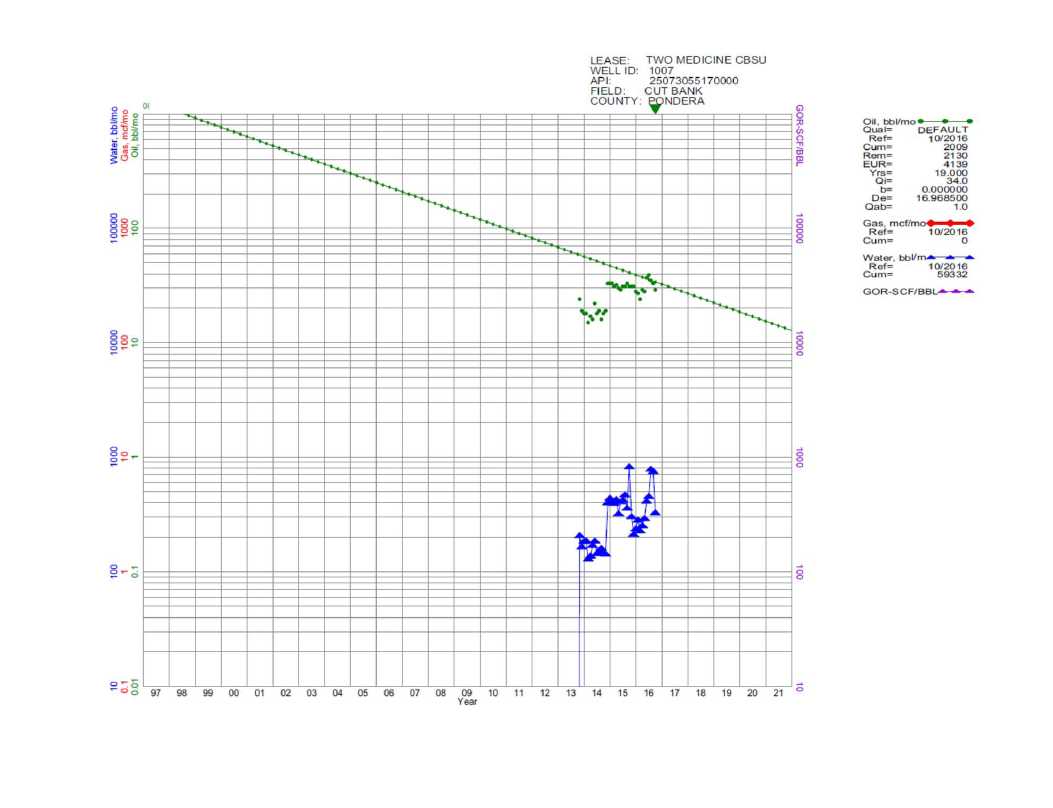

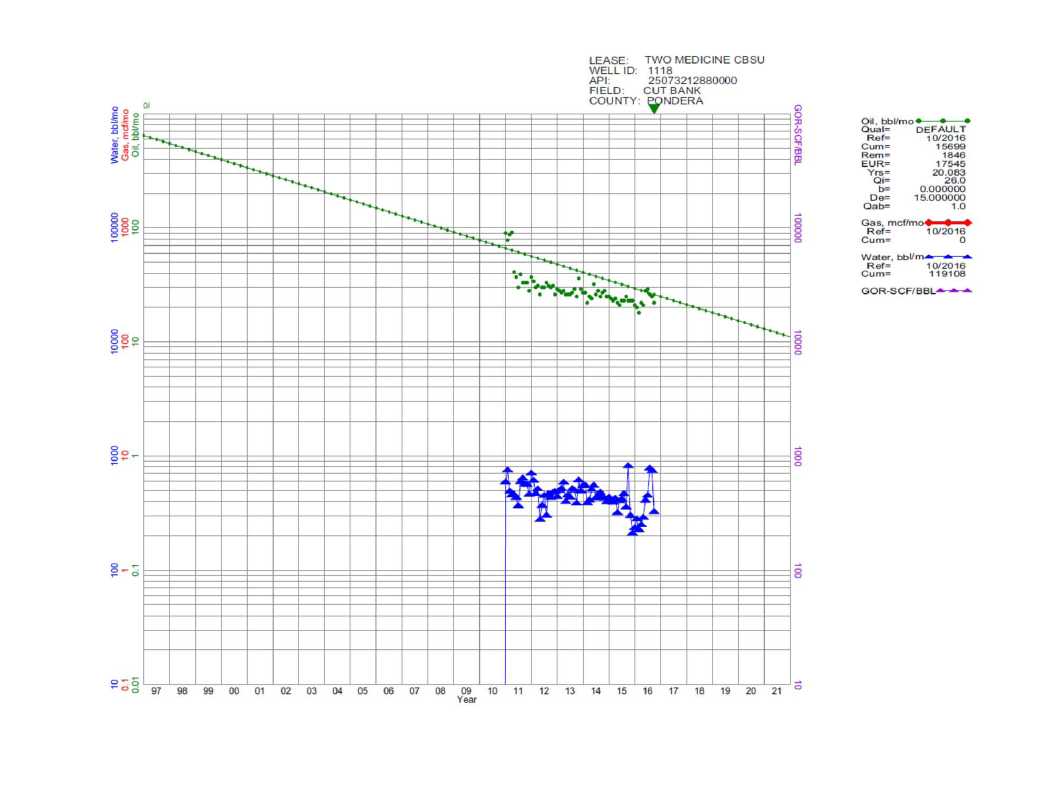

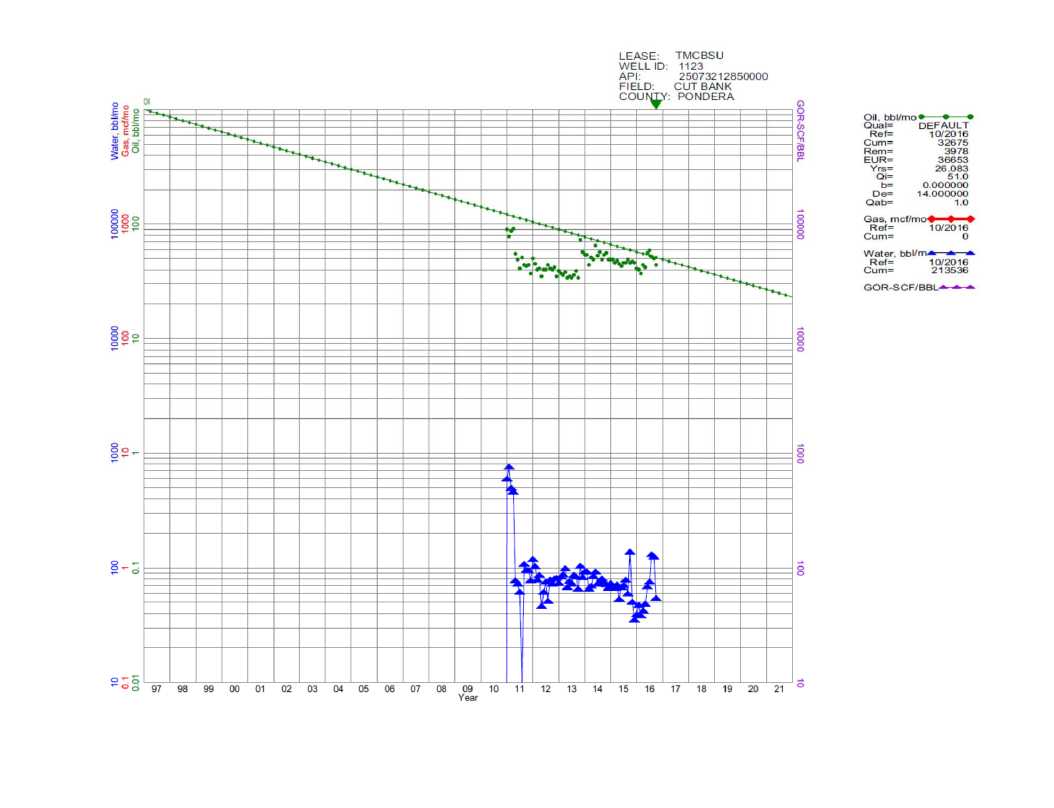

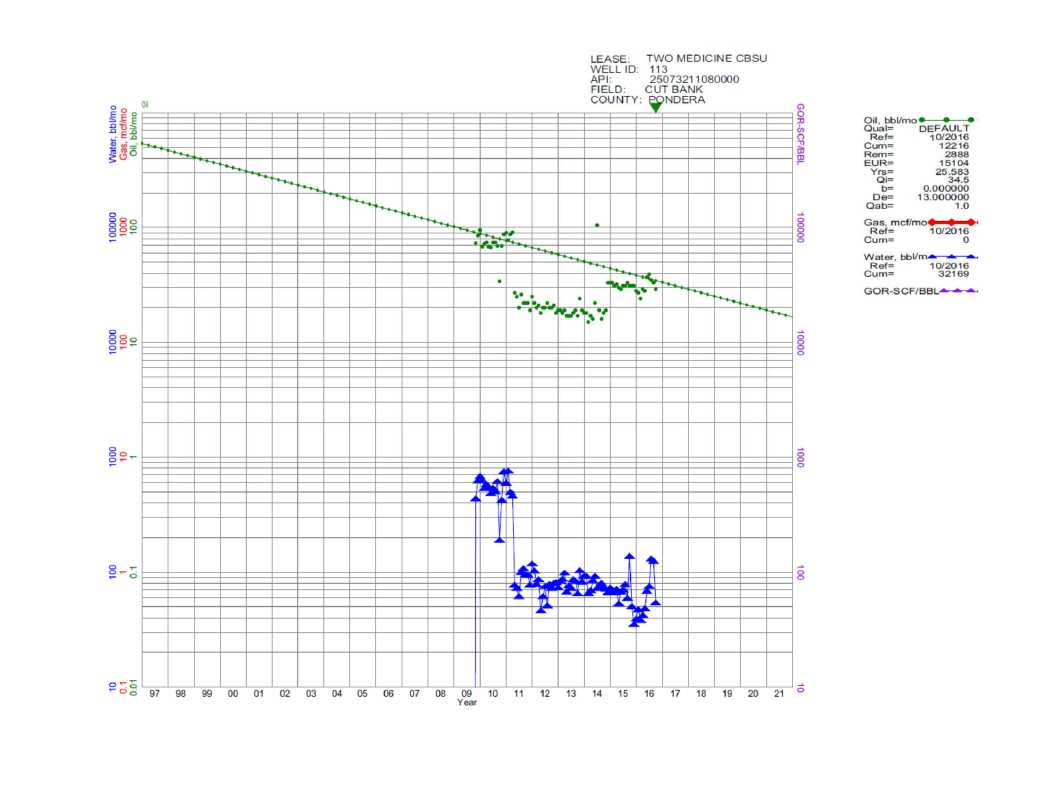

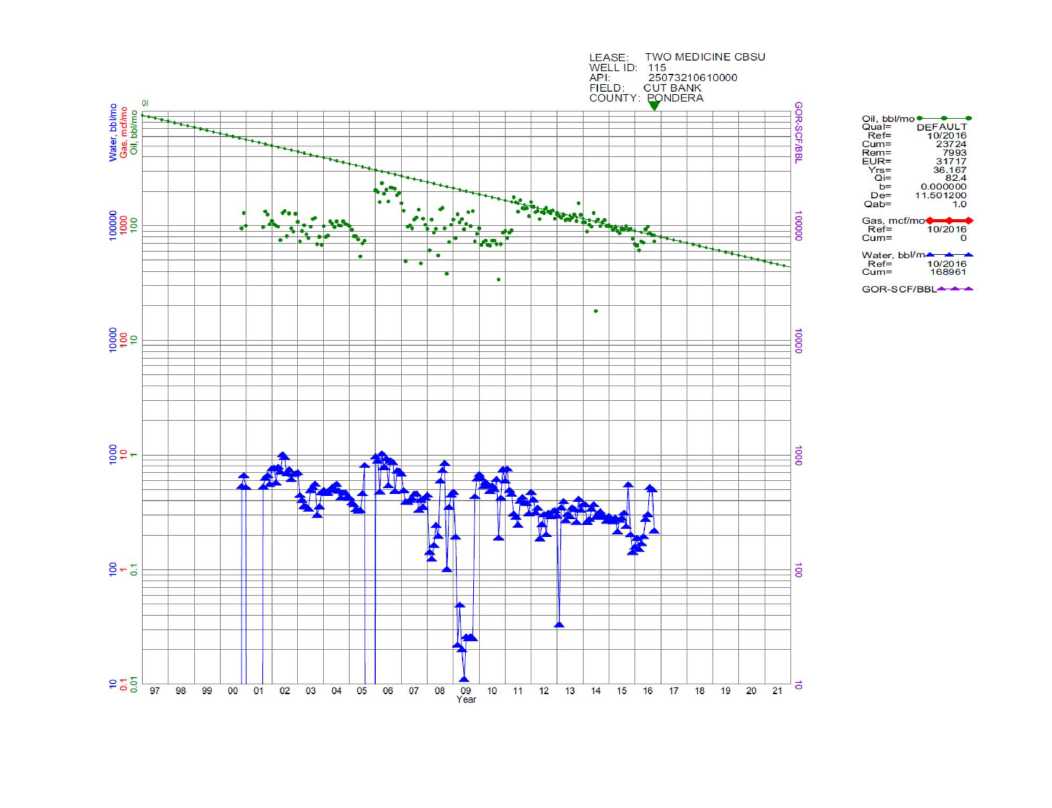

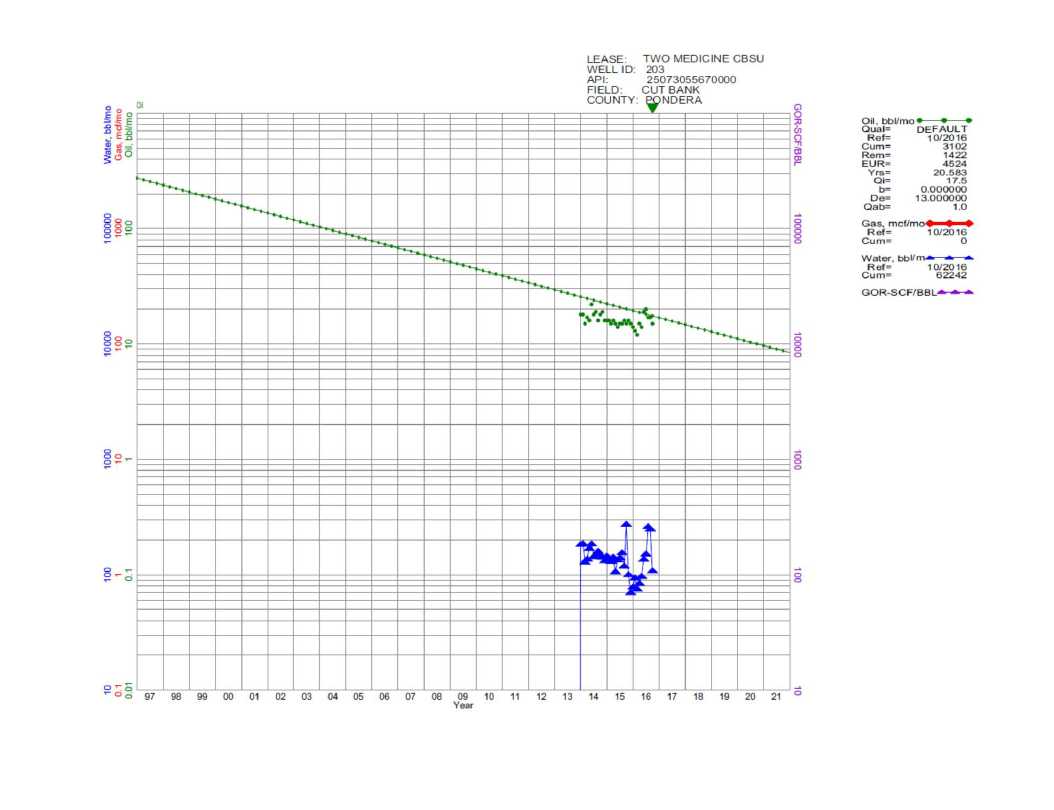

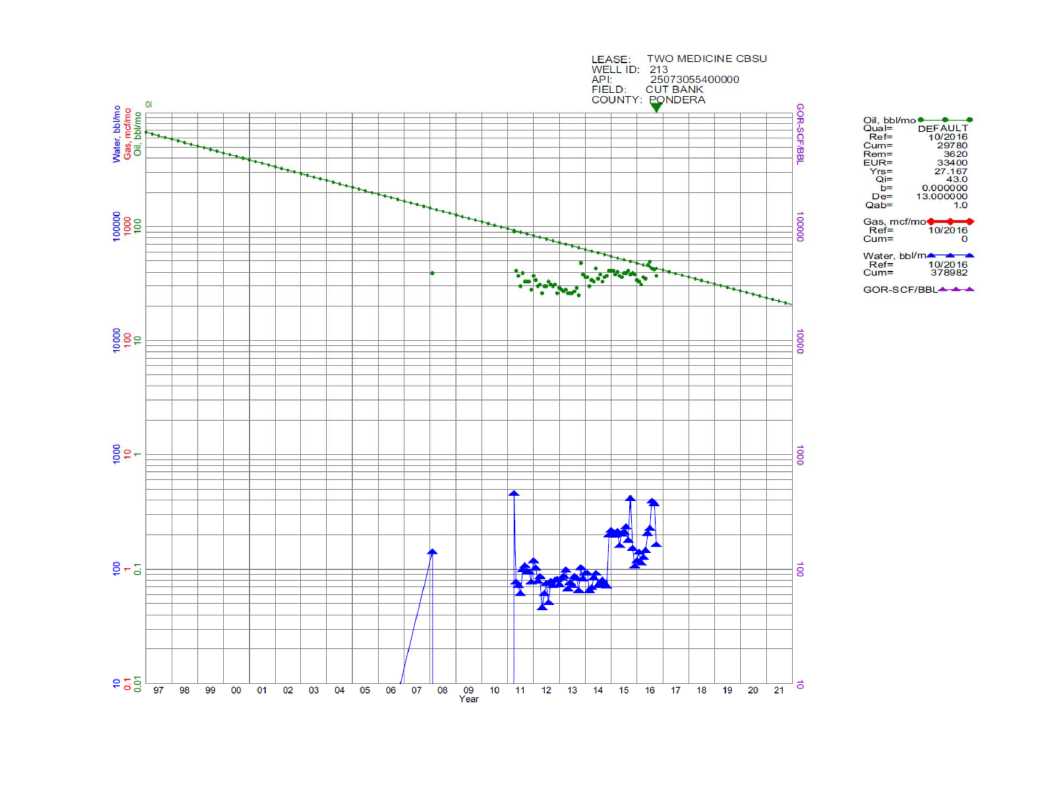

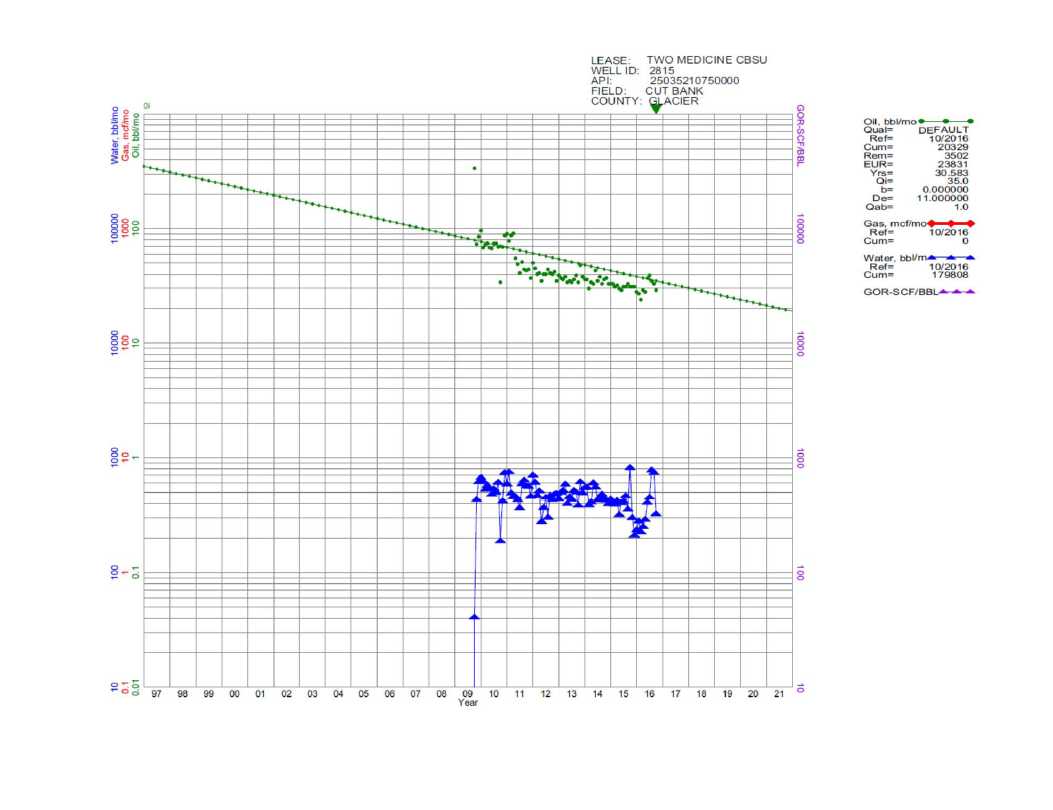

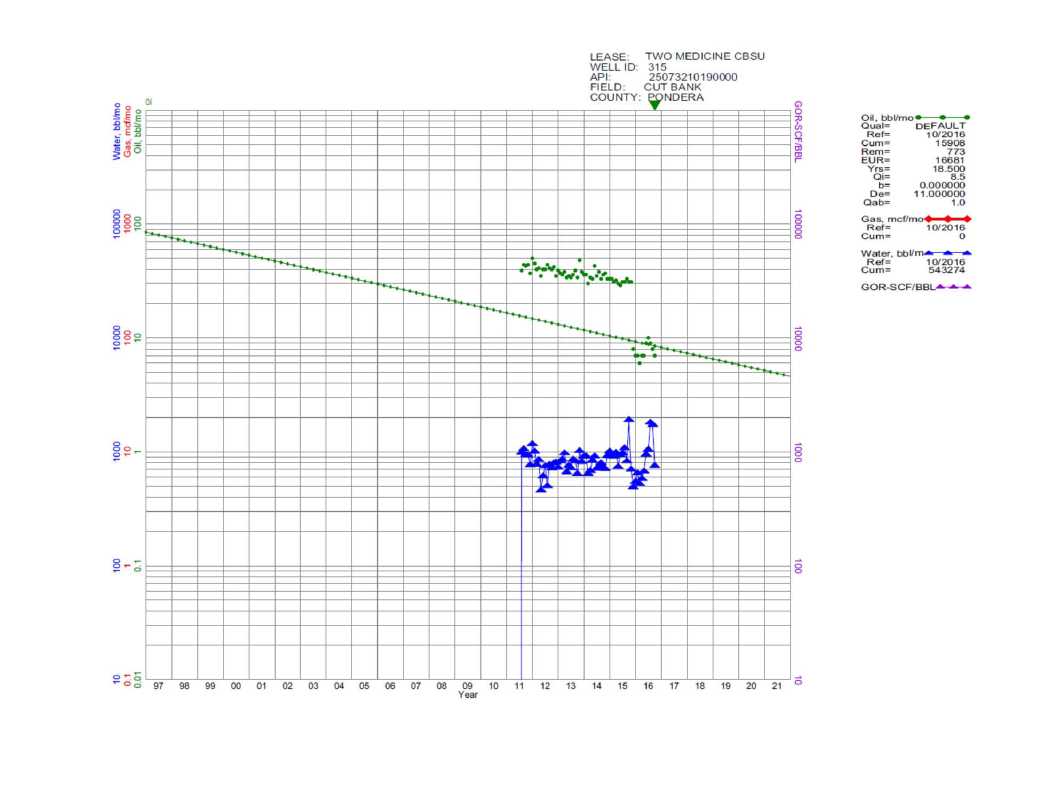

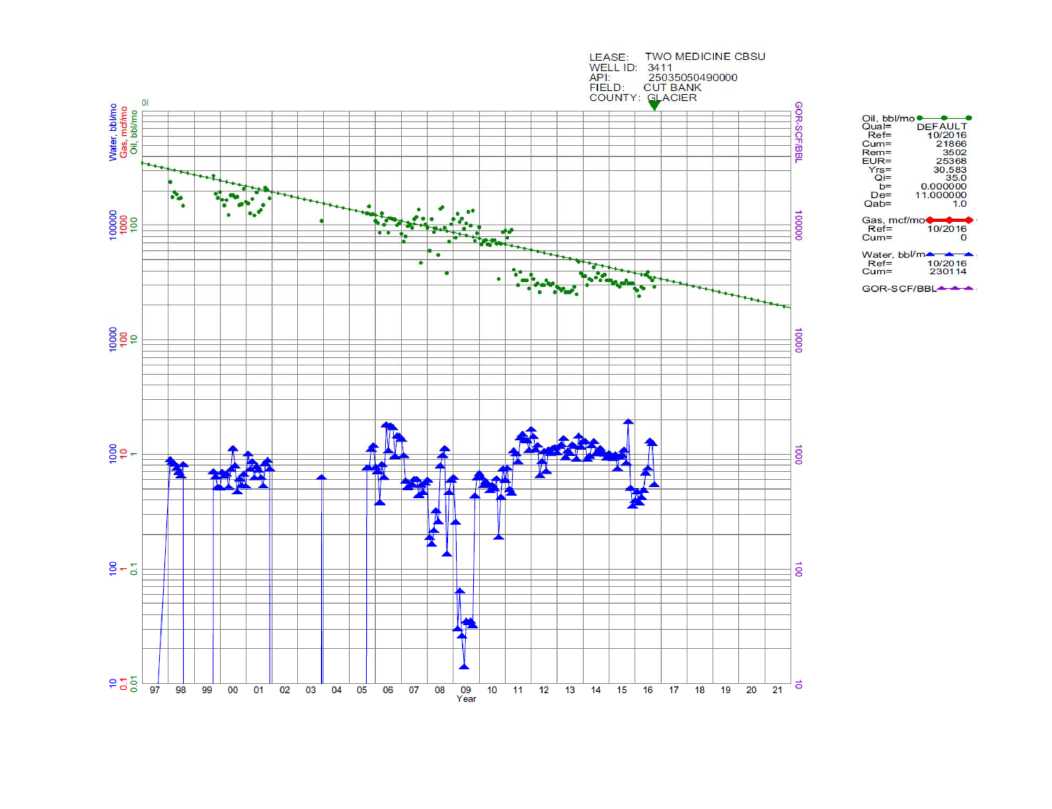

APPENDIX B

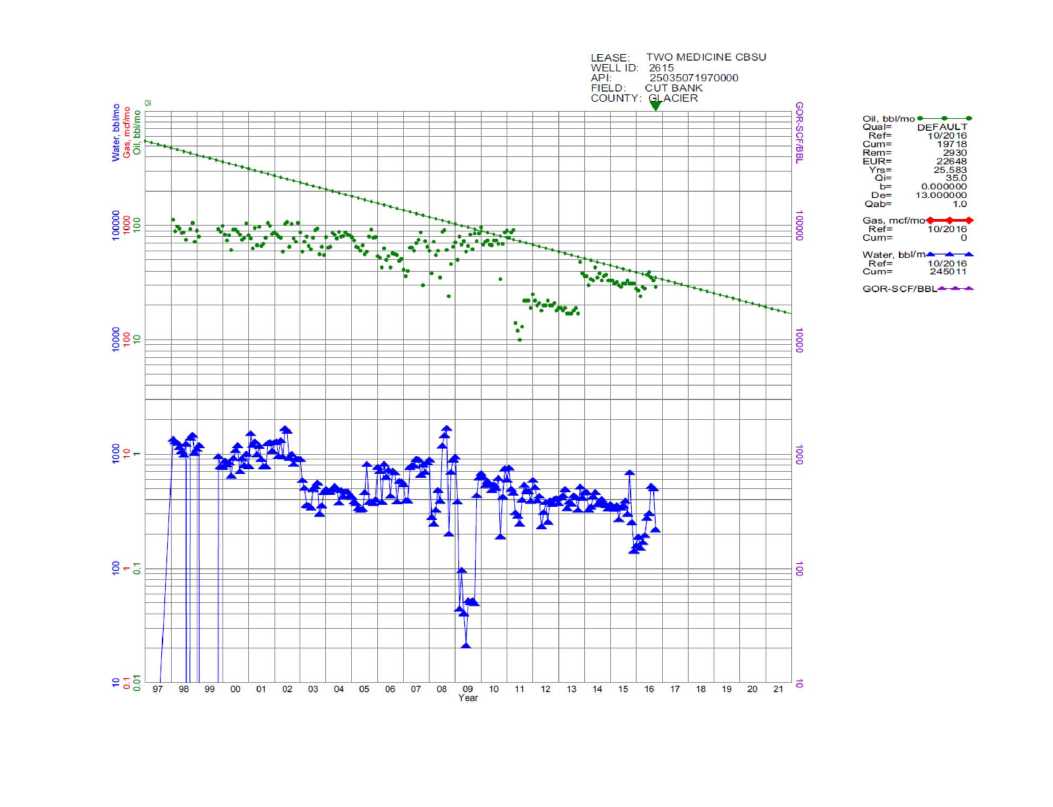

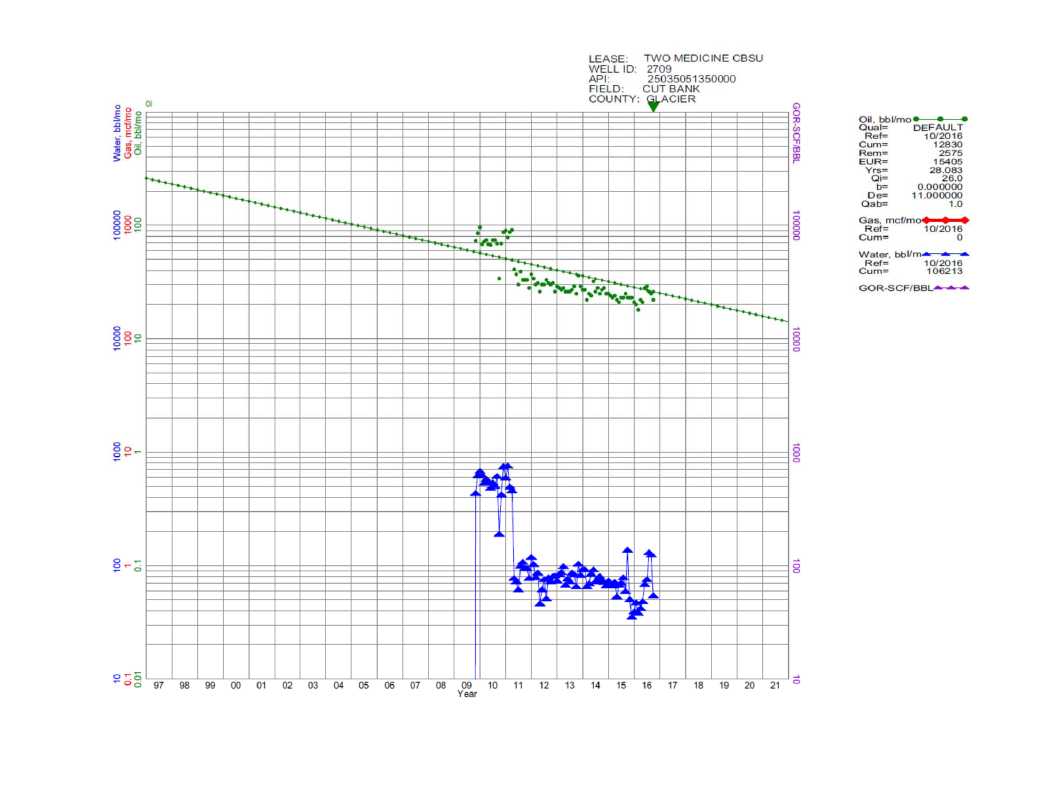

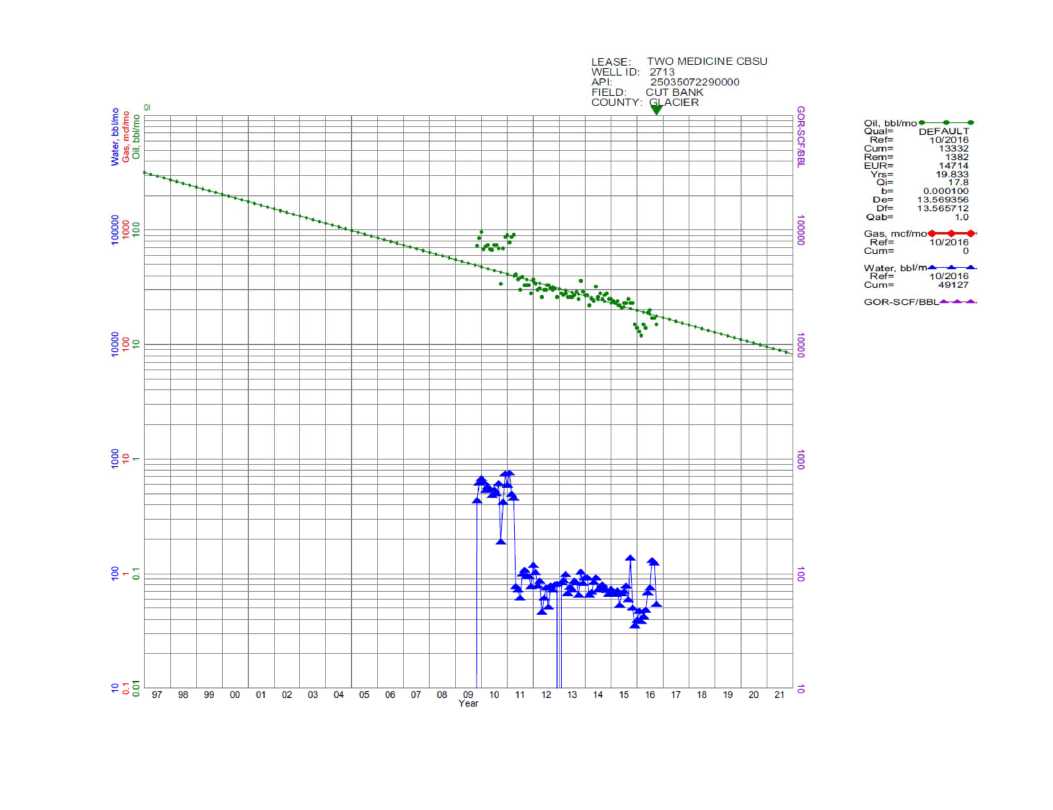

DECLINE CURVE FORECASTS

OF UNECONOMIC WELLS

![]()

![]()

![]()