Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2016

Commission file number 000-55177

LIBERATED ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

27-4715504

|

|

|

(State or other jurisdiction of incorporation or organization)

|

I.R.S. Employer Identification No.

|

|

2 Coleman Court

Southampton, New Jersey

|

08099

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

Issuer's telephone number: (845) 610-3817

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [X] No [ ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

[ ]

|

Accelerated filer

|

[ ]

|

|

Non-accelerated filer (Do not check if a smaller reporting company)

|

[ ]

|

Smaller reporting company

|

[X]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes[ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrants most recently completed second quarter. $201,265.

As of January 17, 2017 the registrant had 2,682,339 shares of common stock outstanding.

LIBERATED ENERGY, INC

|

Item #

|

Description

|

Page

Numbers

|

||

|

3

|

||||

|

3

|

||||

|

5

|

||||

|

5

|

||||

|

5

|

||||

|

6

|

||||

|

6

|

||||

|

6

|

||||

|

6

|

||||

|

7

|

||||

|

7

|

||||

|

13

|

||||

|

13

|

||||

|

28

|

||||

|

28

|

||||

|

29

|

||||

|

29

|

||||

|

29

|

||||

|

30

|

||||

|

31

|

||||

|

32

|

||||

|

32

|

||||

|

32

|

||||

|

32

|

||||

|

33

|

||||

History

Liberated Energy, Inc. is a Nevada corporation formed on September 14, 2011. We were incorporated as Mega World Food Holding Company for the purpose of selling frozen vegetable products in all areas of the world except China.

We operated in two business segments. The first is a non-emergency medical transportation service (NEMT) and the second is selling Guard Lite security lighting systems.

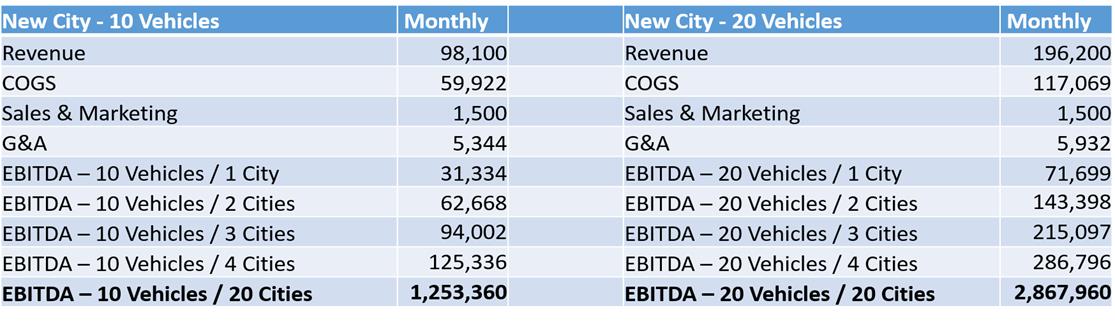

We intend to concentrate all of our efforts on operating our NEMT in the Portland, Oregon geographical area.

NON EMEREGENCY MEDFICAL TRANSPORTATION (NEMT) SERVICE

EcoCab is an employee-only green energy taxi and NEMT company using luxury Teslas in Portland, Oregon.

Company Facts:

|

•

|

EcoCab has been in business since July 22, 2015

|

|

•

|

EcoCab has grown to 46 vehicles in their fleet with a facility two miles out of downtown Portland.

|

|

•

|

EcoCab has increased revenues every month since it's start date

|

|

•

|

EcoCab now has recorded revenues of over $200,000 a month

|

|

•

|

EcoCab is a top partner with a national medical provider. Due to our member experience expertise, we have been asked to develop a model for USA expansion to be able to start operation in cities across the USA.

|

|

•

|

Revenue per hour has increased from $12.25/hr in September of 2015 to over $26.50 in October 2016

|

|

•

|

EcoCab has grown to over 129 employees on their team in their first 12 months of operations.

|

|

•

|

EcoCab has a leadership team with a proven track record in successful and sustainable start-ups

|

|

o

|

Drivers have increased revenue per day from $100-$200 in the early months; to now being able to achieve revenues of $400-$500.

|

|

o

|

Additional partners have approached us and asked to begin working with EcoCab due to our member experience results and commitment.

|

|

o

|

Using scheduling software and a skilled dispatch team we are set up for growth of 2X and 3X.

|

|

o

|

Scaling this model will require little additional fixed overhead other than a small regional office, a District Manager/Driving Coach, vehicles, and a team of drivers. Everything else can be leveraged from the base operations in Portland.

|

GUARDLITE

On January 19, 2013, pursuant to a Common Stock Purchase Agreement, dated January 7, 2013, Perpetual Wind Power Corporation, a privately held corporation formed under the laws of the State of Delaware on July 1, 2010, acquired 24,500,000 non-registered shares of the Company from its shareholders, thereby owning 24,500,000 out of a total of 25,000,000 issued and outstanding shares of the Company. Thereafter, the Company acquired from Perpetual Wind Power Corporation its patented wind and solar powered turbine technology for 2,500,000 newly issued shares of the Company which were distributed in a dividend to its shareholders and Perpetual Wind Power Corporation returned to treasury its 24,500,000 shares it acquired from the Company's shareholders. As a result of this transaction, the Company had on January 19, 2013, 3,000,000 shares issued and outstanding. On February 14, 2013, the Company changed its name from Mega World Food Holding Company to Liberated Energy, Inc. and underwent a 24 for 1 stock split, whereby the Company's outstanding shares increased from 3,000,000 to 72,000,000.

Services and Products

On January 19, 2013, the Company disposed of its wholly-owned subsidiary, Mega World Food Limited (HK). Mega World Food Limited (HK) was incorporated on June 24, 2010 and was in the business of selling frozen vegetables in all areas of the world except China. From inception, Mega World Food Limited (HK) only incurred setting up, formation or organization activities. Upon disposal, the Company ceased these operations and accordingly, the Company's financial statements have been prepared with the net assets, results of operations, and cash flows of this business displayed separately as "discontinued operations."

On January 23, 2013, we acquired from Perpetual Wind Power Corporation the rights to their wind and solar powered turbine technology for which it has a patent pending with the United States Patent and Trademark office, U.S. Patent Application Serial No. 61/257,578 as submitted on November 3, 2009.

In November 2013, we built and successfully tested an alternative energy LED lighting and security system that is now available to the market. The Guard Lite™ security lighting system is designed to deter trespassers from homes and/or properties without electricity costs. The Company has moved towards patent protection of this new device. It is anticipated that the Guard Lite™ security lighting system will only require a portion of the energy it generates so the excess energy will be able to be used for other applications.

On October 11, 2016, the Company completed an agreement with Ron Knori (Kroni) Owner of EcoCab Portland, LLC by which the Company will required all outstanding ECGLLC membership interest for a 20% non-dilutive interest of the outstanding shares of the Company with the first closing of the agreement. The Company's name will be changed to EcoCab, USA, Inc as soon as practical after closing. Subsequent closing through January 31. 2017 will take place and during the period from first closing to January 31, 2017,

|

·

|

The Company will not attempt to change the current management or operations of ECPLLC without the consent of Knori, but the Company will have the right to oversee ECPLLC's revenue and payments out on a daily and monthly basis,

|

|

·

|

The Company will use commercially reasonable efforts to finance the growth of EPCLLC's revenues, but at a minimum, the Company will provide at least $400,000 in working capital funds to ECPLLC,

|

|

·

|

all LIBE convertible notes held by Carebourn Capital L.P. are retired (or Carebourn Capital L.P. consents to the issuance to Knori of the Preferred Shares they hold as collateral)

|

|

·

|

and that the Company has not closed or entered into a binding agreement to merge with, acquire, or become acquired by, another company of equal or greater fair value (private or public) to ECPLLC. If the Preferred Shares Condition is fulfilled, Knori will be issued the Preferred Shares at a Subsequent Closing. "

|

Second closing conditions" requires that ECPLLC has audited financial statements available to the Company. If the Second Tranche Condition is met, The Company will issue the additional Common Shares to SELLER at a Subsequent Closing.

Third closing conditions requires ECPLLC:

|

·

|

made audited financials available to the Company within 71 days of the First Closing Date, and

|

|

·

|

has positive earnings before interest, tax and depreciation and amortization ("EBITDA") under GAAP for the month of January 2017.

|

If the third closing Conditions are met, the Company will issue the third closing Common Shares to Knori at a Subsequent Closing. The number of third closing Common Shares will be calculated so that Knori's resulting percentage of the Company is equitable based on the fair value of ECPLLC relative to the other assets of the Company, but in no event, will Knori be required to transfer or cancel shares to reduce Knori's percentage of the outstanding common stock to below 30%. If the parties cannot agree to an equitable number of shares to issue Knori, the matter will be submitted to binding arbitration.

Additional Information

We are a public company and file annual, quarterly, and special reports and other information with the SEC. We are not required to, and do not intend to, deliver an annual report to security holders. You may read and copy any document we file at the SEC's public reference room at 100 F Street, N.E., Washington, D.C. 20549. You can request copies of these documents by writing to the SEC and paying a fee for the copying cost. Please call the SEC at 1-800-SEC-0330 for more information about the operation of the public reference room. Our filings are also available, at no charge, to the public at http://www.sec.gov.

We are a smaller reporting Company and are not required to include disclosures under this item.

We are a smaller reporting company and are not required to include disclosure under this item.

Our principal executive offices are located at 2 Colman Court, Southampton, New Jersey 08099. The office space is provided to us by our former Chief Executive Officer free of charge.

On September 15, 2016, LG Capital, LLC filed a lawsuit against the Company in the County of Kings, in the Supreme Court of the State of New York (index number 516298/2016). The filing alleges that the Company has defaulted on a number of unpaid loans from LG Capital to the Company with the total owing and due including principal and interest of $279,730.56. The Company has not counter claimed but believes that LG Capital unlawfully attempted to convert some of the loans to common stock of the Company has filed an injunction against the Company transfer agent to block LG Capital from such a conversion. In addition, the Company negotiated in good faith with LG Capital to settle the debt but to no avail.

Not Applicable

| ITEM 5. |

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

(a) Market Information.

Our common stock is quoted on the OTC Markets- Pink Sheet. We obtained our trading symbol which is LIBE.OB on February 15, 2013. For the periods indicated, the following table sets forth the high and low bid prices per share of common stock. These prices represent inter-dealer quotations without retail markup, markdown, or commission and may not necessarily represent actual transactions.

|

HIGH

|

LOW

|

|||||||

|

FISCAL YEAR ENDED SEPTEMBER 30, 2015

|

||||||||

|

First Quarter

|

$

|

216.55

|

$

|

24.14

|

||||

|

Second Quarter

|

$

|

42.76

|

$

|

4.49

|

||||

|

Third Quarter

|

$

|

41.40

|

$

|

1.72

|

||||

|

Fourth Quarter

|

$

|

24.14

|

$

|

.34

|

||||

|

HIGH

|

LOW

|

|||||||

|

FISCAL YEAR ENDED SEPTEMBER 30, 2016

|

||||||||

|

First Quarter

|

$

|

0.3448

|

$

|

0.0034

|

||||

|

Second Quarter

|

$

|

0.6897

|

$

|

0.3448

|

||||

|

Third Quarter

|

$

|

0.3448

|

$

|

0.34485

|

||||

|

Fourth Quarter

|

$

|

0.3448

|

$

|

0.06001

|

||||

(b) Holders.

As of January 13, 2017, there were approximately 46 record holders of shares of the Company's common stock.

(c) Dividend Policy.

We have not declared or paid any cash dividends on our common stock and we do not intend to declare or pay any cash dividend in the foreseeable future. The payment of dividends, if any, is within the discretion of our Board of

Directors and will depend on our earnings, if any, our capital requirements and financial condition and such other factors as our Board of Directors may consider.

(d) Securities Authorized for Issuance Under Equity Compensation Plans.

We do not have equity compensation plans.

(e) Recent Sales of Unregistered Securities.

None

Not Applicable

FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws. These forwarding-looking statements include without limitation statements regarding our expectations and beliefs about the market and industry, our goals, plans, and expectations regarding our results, our intentions and strategies regarding future operations and transactions, our beliefs regarding the future success of our business, our expectations and beliefs regarding competition, competitors, the basis of competition and our ability to compete, our beliefs and expectations regarding our ability to hire and retain personnel, our ability to expand into new geographic markets and music genres, our ability to acquire other operators and venues, our beliefs regarding period to period results of operations, our expectations regarding revenues, our expectations regarding future growth and financial performance, our beliefs and expectations regarding the adequacy of our facilities, and our beliefs and expectations regarding our financial position, ability to finance operations and growth and the amount of financing necessary to support operations. These statements are subject to risks and uncertainties that could cause actual results and events to differ materially. See "Item 1A. Risk Factors" for a discussion of certain risks. We undertake no obligation to update forward-looking statements to reflect events or circumstances occurring after the date of this annual report on Form 10-K.

As used in this annual report on Form 10-K, unless the context otherwise requires, the terms "we," "us," "the Company," and "Liberated" refer to Liberated Energy, a Nevada Corporation.

ORGANIZTION AND BASIS OF PRESENTATION

The following discussion and analysis is based on the audited financial statements for the years ended September 30, 2016 and 2015 of Liberated Energy, Inc., a Nevada corporation ("Liberated" the "Company," "our," or "we"). All significant inter-company amounts have been eliminated. In the opinion of management, the audited financial statements presented herein reflect all adjustments (consisting only of normal recurring adjustments) necessary for fair presentation. Interim results are not necessary indicative of results to be expected for the entire year.

We prepare our financial statements in accordance with generally accepted accounting principles (GAAP), which require that management make estimates and assumptions that affect reported amounts. Actual results could differ from these estimates.

Certain of the statements contained below are forward-looking statements (rather than historical facts) that are subject to risks and uncertainties that could cause actual results to differ materially from such forward-looking statements.

CRITICAL ACCOUNTING POLICIES & ESTIMATES

The preparation of financial statements and related disclosures in conformity with accounting principles generally accepted in the United States of America requires management to make judgments, assumptions and estimates that affect the amounts reported in our consolidated financial statements and accompanying notes. We base our estimates and judgments on historical experience and on various other assumptions that we believe are reasonable under the circumstances. However, future events are subject to change, and the best estimates and judgments routinely require adjustment. The amounts of assets and liabilities reported in our balance sheet, and the amounts of revenues and expenses reported for each of our fiscal periods, are affected by estimates and assumptions which are used for, but not limited to, the accounting for allowance for doubtful accounts, goodwill and intangible asset impairments, restructurings, inventory, and income taxes. Actual results could differ from these estimates. The following critical accounting policies are significantly affected by judgments, assumptions and estimates used in the preparation of our consolidated financial statements.

Use of Estimates

It is important to note that when preparing the financial statements in conformity with U.S. generally accepted accounting principles, management is required to make certain estimates and assumptions that affect the amounts reported and disclosed in the financial statements and related notes. Actual results could differ if those estimates and assumptions approve to be incorrect.

On an ongoing basis, we evaluate our estimates, including those related to estimated customer life, used to determine the appropriate amortization period for deferred revenue and deferred costs associated with licensing fees, the useful lives of property and equipment and our estimates of the value of common stock for the purpose of determining stock-based compensation. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable, the results of which form the basis for making judgments about the carrying values of assets and liabilities.

Revenue Recognition Policies

The Company recognizes revenues in accordance with the Securities and Exchange Commission Staff Accounting Bulletin (SAB) number 104, "Revenue Recognition." SAB 104 clarifies application of U. S. generally accepted accounting principles to revenue transactions. As of the year ended September 30, 2016, there was no deferred revenue. The Company derives its primary revenue from the sources described below, which includes sale of alternative energy devices.

Off- Balance Sheet Arrangements

We did not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures, or capital resources that is material to investors.

Cash and Cash Equivalents

For purposes of the statement of cash flows, the Company considers all highly liquid debt instruments purchased with a maturity of 90 days or less to be cash equivalents to the extent the funds are not being held for investment purposes.

Results of Operations

Year Ended September 30, 2016 Compared to Year Ended September 30, 2015

Revenue

Our revenues were zero for the year ended September 30, 2016 compared to $62,132 for September 30, 2015.

Direct Costs

Direct costs or cost of goods was zero for the year ended September 30, 2016 compared to $19,333 for September 30, 2015.

General and Administrative Expenses and Other

General and administrative costs for the year ended September 30, 2016 was $285,367 compared to $439,043 for the year ended September 30, 2015. Lower cost was attributable to lower consulting fees in 2016 compared to 2015.

Other Income (Expense)

Other expense was $33,068 for the year ended September 30, 2016 compared to $138,515 for the year ended September30, 2015.The lower amount in 2016 is directly attributed to debt settlement of $47,510 offset by impairment of assets totaling $16,234 plus interest expense of $64,345.

Net Loss

The Company incurred a net loss of $318,436 for the year ended September 30, 2016 compared to a net loss of $534,515 for the year ended September 30, 2015. Lower general and administrative expense plus decreased other expenses attributed to the higher loss in 2016 over 2015.

Financial Condition

Cash, Cash Flows, and Working Capital

The Company had a cash balance of $1,804 and a working capital deficit of $565,365 at September 30. 2016 as compared to a net cash balance of $16,921 and a working capital deficit of $366,699 at September 30, 2015. The decrease in working capital is primarily attributable loss in 2016 plus increase in current liabilities through short term debt borrowings.

Operations used $287,085 of cash during 2016 as compared to $441,895 used during 2015. The change in operating cash flows during 2015 was principally attributable to increased losses in 2015 over 2016.

There was no investing activity during the years ended September 30, 2016 or in 2015.

Financing activities provided cash flows of $271,968 during 2016 as compared to $296,462 during 2015. Cash flows provided by financing activities during the 2016 period related to debt financing of $271,968. Cash provided in financing activities in 2015 is attributed to borrowings on debt of $246,462.

Liquidity and Capital Resources

Our principal requirements for capital are to fund our day-to-day operations and to satisfy our contractual obligations, primarily for the repayment of debt.

We believe that we will be required to either improve profitability and operating cash flow or to borrow additional funds or otherwise secure additional financing, or both, to support our operations going forward. Except as described below regarding our line of credit, we do not presently have any commitments to provide financing, if needed, to support our operations.

Equity

During the year ended September 30, 2015 the Company issued 540,282 shares of common stock for debt with a value of $228,317.

During the year ended September 30, 2015 the Company issued 8,572 shares of common stock for accrued liabilities with a value of $127,968.

During the year ended September 30, 2015 the Company issued 1,428 shares of common stock to a related party for service with a value of $50,000.

During the year ended September 30, 2015 the Company issued 2,977 shares of common stock to a related party for service with a value of $98,650.

During the year ended September 30, 2016 the Company issued 1,100,000 shares of common stock to two parties for service with a value of $80,000.

During the year ended September 30, 2016 the Company issued 208,428 shares of common stock for convertible debt with a value of $39,769

Convertible Notes

On September 4, 2013, the Company issued a Convertible Note (the "Note") to JMJ Financial ("JMJ") providing JMJ with the ability to invest up to $350,000 which contains a 10% original issue discount (the "JMJ Note"). The transaction closed on September 4, 2013. JMJ provided $50,000 to the Company on the Effective Date. The net proceeds the Company received from this offering were $45,000. On December 10, 2013, JMJ provided $25,000 to the Company; the net proceeds the Company received from this offering were $22,500. On April 18, 2014, JMJ provided $40,000 to the Company; the net proceeds the Company received from this offering were $36,000. On June 23, 2014, JMJ provided $40,000 to the Company; the net proceeds the Company received from this offering were $36,000. On September 9, 2016, the Company settled the note with a payment of $15,213.33 bringing the balance of the note to zero.

On October 8, 2014, JSJ provided $60,000 to the Company; the net proceeds the Company received from this offering were $55,000. The note is convertible at 50% of the lowest trading price of the Company's stock for the 20 days prior to conversion and provides for 12% interest and matures on April 8, 2015. On July 27, 2016, the Company paid the remaining balance of the note bring note balance to zero.

On April 20, 2015, the Company issued a Convertible Note (the "Note") to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $31,500 with an interest rate of 8% per annum. The note matures on April 28, 2016. The note is convertible by the holder at a discount of 52% of the lowest trading price of the Company's stock for the 18 days prior to the conversion. AS of September 30, 2016, the outstanding balance due was $31,500 plus interest of $5,080 for a total of $37,308.

On April 28, 2015, the Company issued a Convertible Note to Service Trading Company, LLC for $22,000. The note bears an interest rate of 8% and matures on April 28, 2016. The note is convertible by the holder at a discount of 52% of the lowest trading price during the 18 days before the conversion. On September 9, 2016, the Company paid the balance of the note of $22,000 bring the balance of the note to zero.

On May 21, 2015, the Company issued a Convertible settlement note to GEL Properties for $50,000. The note was issued to settle claims by GEL pertaining to fees and interest they claimed as still due. The note Matures on May 21, 2016 bearing interest at 8% and is convertible to common stock of the company at a discount of 65% to the lowest closing bid price for the five days prior to conversion. On September 9, 2016, the Company settled the debt for $20,000 in cash and debt forgiveness of $30,000 bring the balance due to zero.

On July 13, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital"), to replace the $41,400 convertible note issued to Eastmore Capital The note matures on July 13, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. As of September 30, 2016, the outstanding balance of the note was $41,400 plus interest of $6,827 for a total of $48,227.

On July 13, 2015, LG Capital's lawsuit claims the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital"), for a principle amount of $41,400 with an interest rate of 8% per annum. The note matures on July 13, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. Per the Company the note was not funded but the Company has accrued the note and interest as of September 30, 2016, totaling $48,227.

On August 11, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,500 with an interest rate of 8% per annum. The note matures on August 11, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. AS of September 30, 2016, the outstanding balance of the principal was $27,500 and interest of $4,343 for a total of $31,843.

On August 11, 2015, LG Capital's lawsuit claims the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,500 with an interest rate of 8% per annum. The note matures on August 11, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. Per the Company the note was not funded but the Company has accrued the note and interest as of September 30, 2016, totaling $31,843.

On September 8, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,000 with an interest rate of 8% per annum. The note matures on September 8, 2016, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. As of September 30, 2016, the outstanding balance of principal was $27,000 and interest of $4,343 for a total of $31,082.

As of September 30, 2016, the outstanding aggregate balance of all notes due to LG Capital Funding, LLC is $218,480.

On November 5, 2015, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $28,000 with an interest rate of 12% per annum. The note matures on August 5, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of the principal was $28,000 plus interest of $3,037 for a total of $31,037.

On December 21, 2015, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $21,000 with an interest rate of 12% per annum. The note matures on September 16, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion.AS of September 30, 2016 the outstanding balance of the note was $21,000 in principal plus $1,967 interest for a total of $22,967.

On March 11, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $18,000 with net proceeds of $15,000 and with an interest rate of 12% per annum. The note matures on December 11, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of the note was principal of $18,000 plus interest of $1,207 for a total of $19,207.

On March 14, 2016, the Company issued a Convertible Note to LG Capital Funding, LP for a principle amount of $18,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of principal was $18,000 plus interest of $1,207 for a total of $19,207.

On May 17, 2016, the Company issued a Convertible Note Craig Savin for a principle amount of $15,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. The note

was paid in a settlement agreement whereby the Company issued 1,000,000 shares of its common stock to settle outstanding obligations including this note, a note for $5,000 and the issuance of shares for a stock subscription payable of $50,000.

On May 26, 2016, the Company issued a Convertible Note to LG Capital Funding, LP for a principle amount of $17,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. Net proceeds to the Company are $15,000 after deduction of legal fees of $2,000. As of September 30, 2016, the outstanding balance of the note was $17,000 in principal plus interest of $428 for a total of $17,428.

On June 14, 2016, the Company issued a Convertible Note Craig Savin for a principle amount of $5,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. On September 9, 2016, the Company issued 1,000,000 share of common stock for the payment of this note, a note for $15,000 plus a $50,000 stock payable due Savin. The balance of the note as of September 30, 2016, is zero.

On July 25, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $23,000 with an interest rate of 12% per annum. The note matures on July 25, 2017. The note is convertible by the holder at a discount of 45% of the lowest three trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance included principal of $23,000 plus interest of $514 for a total of $23,514.

On September 7, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $197,363,70 less legal fees of $8,000 with an interest rate of 12% per annum. The note matures on September 7, 2017. The note is convertible by the holder at a discount of 50% of the lowest three trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance included principal of $115,114 plus interest of $908 for a total of $116,022.

As the market value of the Company' stock is below it par value, Management has concluded that the benefit of the conversion feature is zero and has not allocate a value to the conversion.

Management has reviewed the terms of the convertible instruments to determine their fair value. After reviewing the characteristic and the value of the conversion, Management has determined based on note conversion history that the conversion value is equal or less than par value of the shares used for conversion thus determining that the fair value of the notes is equal to their face value.

As of June 30, 2016, the Company outstanding liability of convertible debt was $517,735 plus interest of $49,431 for a total liability of $567,166. The liability was as follows:

|

Lender

|

Principal

|

Interest

|

Total

|

|||||||||

|

LG Capital

|

258,115

|

39,044

|

297,159

|

|||||||||

|

Carebourn Capital

|

259,621

|

10,389

|

270,010

|

|||||||||

|

Total

|

$

|

517,736

|

$

|

49,433

|

$

|

567,169

|

||||||

On September 15, 2016, LG Capital, LLC filed a lawsuit against the Company. The filing alleges that the Company has defaulted on several unpaid loans from LG Capital to the Company with the total claim against the Company of $279,730.56. The Company negotiated in good faith with LG Capital to settle the debt but to no avail. After reviewing the claim filed by LG Capital, it is the opinion of Company Management that the Company's outstanding liability to LG Capital has been fully recognized and accounted for in the financial statements of the Company.

We are a smaller reporting Company and are not required to include disclosures under this item

Our financial statements are audited and appear immediately after the signature page of this report. See "Index to Financial Statements" on page F-1 of this report.

TABLE OF CONTENTS

|

F-1

|

|

|

F-2

|

|

|

F-3

|

|

|

F-4

|

|

|

F-5

|

|

|

F-6

|

Independent Registered Public Accounting Firm's Auditor's Report on the Consolidated Financial Statements

Board of Directors and Shareholders

Liberated Energy, Inc.

We have audited the accompanying balance sheets of Liberated Energy, Inc. (the "Company"), as of September 30, 2016, and 2015, and the related statements of operation, shareholders' equity, and cash flows for years ended September 30, 2016 and September 30, 2015. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to in the first paragraph above, present fairly, in all material respects, the financial position of Liberated Energy, Inc. as of September 30, 2016, 2015, and the results of its operations and their cash flows for years ended September 30, 2016 and 2015, in conformity with accounting principles generally accepted in the United States of America.

The Company's lack of operating history and financial resources raise substantial doubt about its ability to continue as a going concern. The financial statements do not include adjustments that might result from the outcome of this uncertainty and if the Company is unable to generate significant revenue or secure financing, then the Company may be required to cease or curtail its operations.

/s/ Enterprise CPAs, Ltd

Enterprise CPAs, Ltd.

Chicago, IL

January 17, 2017

F-1

LIBERATED ENERGY, INC.

|

September 30,

|

||||||||

|

2016

|

2015

|

|||||||

|

ASSETS

|

||||||||

|

CURRENT ASSETS:

|

||||||||

|

Cash and Cash Equivalents

|

$

|

1,804

|

$

|

16,921

|

||||

|

Prepaid expenses

|

--

|

--

|

||||||

|

Inventory

|

--

|

23,880

|

||||||

|

Total Current Assets

|

1,804

|

40,801

|

||||||

|

OTHER ASSESTS:

|

||||||||

|

TOTAL ASSETS

|

$

|

1,804

|

$

|

40,801

|

||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

CURRENT LIABILITIES

|

||||||||

|

Accounts payable and accrued expenses

|

$

|

49,433

|

$

|

35,754

|

||||

|

Unearned income

|

--

|

--

|

||||||

|

Convertible note payable

|

517,736

|

271,746

|

||||||

|

Note payable

|

--

|

50,000

|

||||||

|

Stock payable

|

--

|

50,000

|

||||||

|

Total Current Liabilities

|

567,169

|

407,500

|

||||||

|

TOTAL LIABILITIES

|

$

|

567,169

|

$

|

407,500

|

||||

|

STOCKHOLDERS EQUITY

|

||||||||

|

Preferred Stock:

10,000,000 shares authorized par value $0.001 per share;

10,000,000 and none issued and outstanding, respectively

|

10,000

|

10,000

|

||||||

|

Common Stock:

10,000,000,000 shares authorized par value $0.001 per share;

issued and outstanding, 1,888,832 at September 30, 2016 and

579,900 at September 30, 2015

|

1,889

|

580

|

||||||

|

Additional paid-in-capital

|

824,414

|

705,954

|

||||||

|

Accumulated deficit

|

(1,401,668

|

)

|

(1,083,232

|

)

|

||||

|

TOTAL STOCKHOLDERS' DEFICIT

|

$

|

(565,365

|

)

|

$

|

(366,698

|

)

|

||

|

TOTAL LIABILITIES AND EQUITY

|

$

|

1,804

|

$

|

40,801

|

||||

The accompanying notes are an integral part of these statements.

F-2

LIBERATED ENERGY, INC

|

2016

|

2015

|

|||||||

|

Revenues

|

$

|

--

|

$

|

62,132

|

||||

|

Cost of Goods Sold

|

--

|

19,333

|

||||||

|

Gross Profit

|

--

|

42,799

|

||||||

|

Operating Expenses

|

||||||||

|

General and Administrative Expenses

|

285,367

|

439,043

|

||||||

|

Operating loss

|

(285,367

|

)

|

(396,244

|

)

|

||||

|

Other Income (Expense):

|

||||||||

|

Interest income

|

--

|

--

|

||||||

|

Interest expenses

|

(64,345

|

)

|

(61,026

|

)

|

||||

|

Debt settlement

|

47,510

|

(35,502

|

) | |||||

|

Impairment of assets

|

(16,234

|

)

|

(41,743

|

) | ||||

|

Total other expense

|

(33,068

|

)

|

(138,515

|

)

|

||||

|

Net loss

|

$

|

(318,436

|

)

|

$

|

(534,515

|

)

|

||

|

Loss per Share, Basic & Dilutive

|

$

|

(0.43

|

)

|

$

|

(3.30

|

)

|

||

|

Weighted Average Shares Outstanding

|

798,545

|

161,909

|

||||||

The accompanying notes are an integral part of these statements.

F-3

LIBERATED ENERGY, INC.

FOR YEARS ENDED SEPTEMBER 30, 2016 AND 2015

|

Additional

|

Total

|

|||||||||||||||||||||||||||

|

Common Stock

|

Preferred Stock

|

Paid-In

|

Accumulated

|

Stockholders'

|

||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Deficit

|

||||||||||||||||||||||

|

Balance at September 31, 2014

|

93,422,721

|

93,423

|

--

|

--

|

188,176

|

(548,717

|

)

|

(267,118

|

)

|

|||||||||||||||||||

|

Common stock issued for accrued liabilities

|

30,000,000

|

30,000

|

--

|

--

|

97,968

|

--

|

127,968

|

|||||||||||||||||||||

|

Common stock issued for debt

|

1,890,988,716

|

1,890,989

|

--

|

--

|

(1,662,672

|

)

|

--

|

338,317

|

||||||||||||||||||||

|

Common stock issued for service- related party

|

5,000,000

|

5,000

|

--

|

--

|

45,000

|

--

|

50,000

|

|||||||||||||||||||||

|

Common stock issued for service

|

10,240,000

|

10,240

|

--

|

--

|

88,410

|

--

|

98,650

|

|||||||||||||||||||||

|

Preferred shares issued for service

|

--

|

--

|

10,000,000

|

10,000

|

--

|

--

|

10,000

|

|||||||||||||||||||||

|

Debt not recorded in previous year

|

(80,000

|

)

|

--

|

(80,000

|

)

|

|||||||||||||||||||||||

|

Net loss

|

--

|

--

|

--

|

--

|

--

|

(534,515

|

)

|

(5,34,515

|

)

|

|||||||||||||||||||

|

Balance at September, 2015

|

2,029,651,437

|

2,029,652

|

10,000,000

|

10,000

|

(1,323,118

|

)

|

(1,083,232

|

)

|

(366,698

|

)

|

||||||||||||||||||

|

Common stock issued for debt

|

729,504,288

|

729,504

|

--

|

--

|

(698,735

|

)

|

--

|

39,769

|

||||||||||||||||||||

|

Common stock issued for service

|

1,100,000

|

1,100

|

--

|

--

|

78,900

|

--

|

80,000

|

|||||||||||||||||||||

|

Reverse of common stock 1:3,500

|

(2,758,367,395

|

)

|

(2,758,367

|

)

|

--

|

--

|

2,758,367

|

--

|

--

|

|||||||||||||||||||

|

Rounding on reverse of common stock

|

502

|

--

|

--

|

--

|

--

|

--

|

--

|

|||||||||||||||||||||

|

Net loss

|

--

|

--

|

--

|

--

|

--

|

(318,436

|

)

|

(318,436

|

)

|

|||||||||||||||||||

|

Balance at September, 2016

|

1,888,832

|

$

|

1,889

|

10,000,000

|

$

|

10,000

|

$

|

824,414

|

$

|

(1,401,668

|

)

|

$

|

(565,365

|

)

|

||||||||||||||

The accompanying notes are an integral part of these statements.

F-4

LIBERATED ENERGY, INC.

FOR YEARS ENDED SEPTEMBER 30

|

2016

|

2015

|

|||||||

|

OPERATING ACTIVITIES:

|

||||||||

|

Net Loss

|

$

|

(318,436

|

)

|

$

|

(534,515

|

)

|

||

|

Adjustments to reconcile net loss to net cash used in operating activities

|

||||||||

|

Stock issued for service expense

|

10,000

|

158,650

|

||||||

|

Debt settlement

|

(30,000

|

)

|

35,502

|

|||||

|

Impairment of assets

|

--

|

41,743

|

||||||

|

Amortization of debt discount and finance charges

|

--

|

--

|

||||||

|

Changes in operating assets and liabilities

|

||||||||

|

Inventory

|

23,880

|

16,981

|

||||||

|

Prepaid expenses

|

--

|

--

|

||||||

|

Deferred revenue

|

--

|

(43,565

|

)

|

|||||

|

Accounts payable and accrued expense

|

27,471

|

(116,691

|

)

|

|||||

|

Net cash used in operating activities

|

(287,085

|

)

|

(441,895

|

)

|

||||

|

FINANCING ACTIVITIES:

|

||||||||

|

Sale of common stock

|

--

|

50,000

|

||||||

|

Proceeds from issuance of common stock warrants

|

--

|

--

|

||||||

|

Proceeds from issuance of convertible note

|

271,968

|

246,462

|

||||||

|

Net cash provided by financing activities -

|

271,968

|

296,462

|

||||||

|

Net increase (decrease) in cash and cash equivalents

|

(15,117

|

)

|

(145,433

|

)

|

||||

|

Cash and cash equivalents at Beginning of the Period

|

1,804

|

162,354

|

||||||

|

Cash and cash equivalents at End of Period

|

$

|

16,921

|

$

|

16,921

|

||||

|

SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION:

|

||||||||

|

Stock issued for convertible debt

|

$

|

29,769

|

$

|

356,284

|

||||

|

Stock issued for settlement of notes payable

|

$

|

20,000

|

$

|

--

|

||||

|

Stock issued for stock payable

|

$

|

50,000

|

$

|

--

|

||||

The accompanying notes are an integral part of these statements.

F-5

LIBERATED ENERGY, INC.

FOR THE YEARS ENDED SEPTEMBER 30, 2016 AND 2015

Note 1 - Nature of Operations

Organization

Liberated Energy, Inc. (the "Company"), formerly known as Mega World Food Holdings Company is a Nevada corporation formed on September 14, 2010.

On January 19, 2013, pursuant to a Common Stock Purchase Agreement, dated January 7, 2013, Perpetual Wind Power Corporation, a privately held corporation formed under the laws of the State of Delaware on July 1, 2010, acquired 24,500,000 non-registered shares of the Company from its shareholders, thereby owning 24,500,000 out of a total of 25,000,000 issued and outstanding shares of the Company. Thereafter, the Company acquired from Perpetual Wind Power Corporation its patented wind and solar powered turbine technology for 2,500,000 newly issued shares of the Company which were distributed in a dividend to its shareholders and Perpetual Wind Power Corporation returned to treasury its 24,500,000 shares it acquired from the Company's shareholders. As a result of this transaction, the Company had on January 19, 2013, 3,000,000 shares issued and outstanding. On February 14, 2013, the Company changed its name from Mega World Food Holding Company to Liberated Energy, Inc. and underwent a 24 for 1 stock split, whereby the Company's outstanding shares increased from 3,000,000 to 72,000,000.

On January 19, 2013, the Company disposed of its wholly-owned subsidiary, Mega World Food Limited (HK). Mega World Food Limited (HK) was incorporated on June 24, 2010 and was in the business of selling frozen vegetables in all areas of the world except China. From inception, Mega World Food Limited (HK) only incurred setting up, formation or organization activities. Upon disposal, the Company ceased these operations and accordingly, the Company's financial statements have been prepared with the net assets, results of operations, and cash flows of this business displayed separately as "discontinued operations."

On February 4, 2015, the Company increased their number of authorized preferred shares from 10,000,000 to 100,000,000 and authorized common shares from 250,000,000 to 900,000,000.

On December 31, 2015, the Company amended the preferred shares voting rights increasing the voting of each preferred share from 100 to 10,000 votes on any action voted on by the common stock holders

On July 6, 2016, the Company adopted a 1-for-3,500 reverse split of the Company's common stock that as of June 30, 2016, was not yet effective.

Note 2 - Summary of Significant Accounting Policies

Basis of Accounting

The Company maintains its books and records on the accrual basis of accounting. The accompanying financial statements have been prepared on that basis, in which revenues and gains are recognized when earned and expenses and losses are recognized when incurred.

Use of Estimates

The presentation of financial statements in conformity with generally accepted accounting principles in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets

F-6

and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

For the purpose of the statement of cash flows, cash and cash equivalents include all cash balances, which are not subject to withdrawal restrictions or penalties, and highly liquid investments and debt instruments with a maturity of three months or less from the date of purchase.

Fair Value of Financial Instruments

Our short-term financial instruments, including cash, other assets and accounts payable and accrued expenses consist primarily of instruments without extended maturities, the fair value of which, based on management's estimates, reasonably approximate their book value. The fair value of our notes and advances payable is based on management estimates and reasonably approximates their book value based on their current maturity.

Net Loss per Common Share

The Company computes per share amounts in accordance with Statement of Financial Accounting Standards (SFAS) ASC 260, Earnings per Share (EPS). ASC 260 requires presentation of basic and diluted EPS. Basic EPS is computed by dividing the income (loss) available to common shareholders by the weighted-average number of common shares outstanding for the period. Diluted EPS is based on the weighted-average number of shares of common stock and common stock equivalents outstanding during the periods.

Property, Equipment, and Intangible Assets

Property and equipment are carried at cost, less accumulated depreciation. Additions are capitalized and maintenance and repairs are charged to expense as incurred. Intangible assets consist of acquired customer and vendor databases and are carried at cost, less accumulated amortization.

Depreciation and amortization is provided principally on the straight-line basis method over the estimated useful lives of the assets.

Patent Costs

Costs incurred in filing, prosecuting and maintaining patents (principally legal fees) are expensed as incurred and recorded within general and administrative expenses on the statement of operations. Such costs aggregated approximately zero and $zero for the years ended September 30, 2016 and 2015.

Stock-Based Compensation

The Company accounts for stock-based compensation to employees and non-employees in accordance with ASC 718 requiring employee equity awards to be accounted for under the fair value method. Accordingly, share-based compensation is measured at grant date, based on the fair value of the award and is recognized as expense over the requisite employee service period. The Company accounts for stock-based compensation to other than employees in accordance with FASB ASC 505-50. Equity instruments issued to other than employees are valued at the earlier of a commitment date or upon completion of the services, based on the fair value of the equity instruments and is recognized as expense over the service period. The Company estimates the fair value of share-based payments using the Black-Scholes option-pricing model for common stock options and the closing price of the company's common stock for common share issuances.

F-7

Inventory

Inventories are stated at the cost of goods. There was zero inventory in stock in September 30, 2016 and 2015 respectively.

Revenue and Cost Recognition

It is the Company's policy that revenue from product sales or services will be recognized in accordance with ASC 605 "Revenue Recognition". Four basic criteria must be met before revenue can be recognized: (1) persuasive evidence of an arrangement exists; (2) delivery has occurred; (3) the selling price is fixed and determinable; and (4) collectability is reasonably assured. Determination of criteria (3) and (4) are based on management's judgments regarding the fixed nature of the selling prices of the products delivered and the collectability of those amounts. Provisions for discounts and rebates to customers, estimated returns and allowances, and other adjustments are provided for in the same period the related sales are recorded. The Company will defer any revenue for which the product was not delivered or is subject to refund until such time that the Company and the customer jointly determine that the product has been delivered or no refund will be required.

Income Taxes

The Company utilizes ASC 740 "Income Taxes" which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred income taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each year-end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Temporary differences between taxable income reported for financial reporting purposes and income tax purposes primarily relate to the recognition of debt costs and stock based compensation expense. The adoption of ASC 740-10 did not have a material impact on the Company's results of operations or financial condition.

Note 3 – Going Concern Matters

As shown in the accompanying financial statements, the Company has a net loss of $283,654 for the year ended September 30, 2016. As of September 30, 2016, the Company reported an accumulated deficit of $1,366,886. The Company's ability to generate continued positive cash flows is dependent on the ability to grow its operating entity as well as the ability to raise additional capital. Management is following strategic plans to accomplish these objectives, but success is not guaranteed. These factors raise substantial doubt about the Company's ability to continue as a going concern. The financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from the outcome of this uncertainty.

Note 4 – Fair Value Measurements

As defined in (Financial Accounting Standards Board ASC 820), fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (exit price). The Company utilized the market data of similar entities in its industry or assumptions that market participants would use in pricing the asset or liability, including assumptions about risk and the risks inherent in the inputs to the valuation technique. These inputs can be readily observable, market corroborated, or generally unobservable. The Company classifies fair value balances based on the observability of those inputs. FASB ASC 820 establishes a fair value hierarchy that prioritizes the inputs used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (level 1 measurement) and the lowest priority to unobservable inputs (level 3 measurement).

F-8

The three levels of the fair value hierarchy are as follows:

| Level 1 – |

Quoted prices are available in active markets for identical assets or liabilities as of the reporting date. Active markets are those in which transactions for the asset or liability occur in sufficient frequency and volume to provide pricing information on an ongoing basis. Level 1 primarily consists of financial instruments such as exchange-traded derivatives, marketable securities and listed equities.

|

| Level 2 - |

Pricing inputs are other than quoted prices in active markets included in level 1, which are either directly or indirectly observable as of the reported date and includes those financial instruments that are valued using models or other valuation methodologies. These models are primarily industry-standard models that consider various assumptions, including quoted forward prices for commodities, time value, volatility factors, and current market and contractual prices for the underlying instruments, as well as other relevant economic measures. Substantially all of these assumptions are observable in the marketplace throughout the full term of the instrument, can be derived from observable data or are supported by observable levels at which transactions are executed in the marketplace. Instruments in this category generally include non-exchange-traded derivatives such as commodity swaps, interest rate swaps, options and collars.

|

| Level 3 – |

Pricing inputs include significant inputs that are generally less observable from objective sources. These inputs may be used with internally developed methodologies that result in management's best estimate of fair value.

|

Management has determined based on note conversion history that the conversion value is equal or less than par value of the shares used for conversion thus determining that the fair value of the notes is equal to their face value.

Note 5 - Convertible Notes

On September 4, 2013, the Company issued a Convertible Note (the "Note") to JMJ Financial ("JMJ") providing JMJ with the ability to invest up to $350,000 which contains a 10% original issue discount (the "JMJ Note"). The transaction closed on September 4, 2013. JMJ provided $50,000 to the Company on the Effective Date. The net proceeds the Company received from this offering were $45,000. On December 10, 2013, JMJ provided $25,000 to the Company; the net proceeds the Company received from this offering were $22,500. On April 18, 2014, JMJ provided $40,000 to the Company; the net proceeds the Company received from this offering were $36,000. On June 23, 2014, JMJ provided $40,000 to the Company; the net proceeds the Company received from this offering were $36,000. On September 9, 2016, the Company settled the note with a payment of $15,213.33 bringing the balance of the note to zero.

On October 8, 2014, JSJ provided $60,000 to the Company; the net proceeds the Company received from this offering were $55,000. The note is convertible at 50% of the lowest trading price of the Company's stock for the 20 days prior to conversion and provides for 12% interest and matures on April 8, 2015. On July 27, 2016, the Company paid the remaining balance of the note bring note balance to zero.

On April 20, 2015, the Company issued a Convertible Note (the "Note") to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $31,500 with an interest rate of 8% per annum. The note matures on April 28, 2016. The note is convertible by the holder at a discount of 52% of the lowest trading price of the Company's stock for the 18 days prior to the conversion. AS of September 30, 2016, the outstanding balance due was $31,500 plus interest of $5,080 for a total of $37,308.

On April 28, 2015, the Company issued a Convertible Note to Service Trading Company, LLC for $22,000. The note bears an interest rate of 8% and matures on April 28, 2016. The note is convertible by the holder at a discount of 52% of the lowest trading price during the 18 days before the conversion. On September 9, 2016, the Company paid the balance of the note of $22,000 bring the balance of the note to zero.

F-9

On May 21, 2015, the Company issued a Convertible settlement note to GEL Properties for $50,000. The note was issued to settle claims by GEL pertaining to fees and interest they claimed as still due. The note Matures on May 21, 2016 bearing interest at 8% and is convertible to common stock of the company at a discount of 65% to the lowest closing bid price for the five days prior to conversion. On September 9, 2016, the Company settled the debt for $20,000 in cash and debt forgiveness of $30,000 bring the balance due to zero.

On July 13, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital"), to replace the $41,400 convertible note issued to Eastmore Capital The note matures on July 13, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. As of September 30, 2016, the outstanding balance of the note was $41,400 plus interest of $6,827 for a total of $48,227.

On July 13, 2015, LG Capital's lawsuit claims the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital"), for a principle amount of $41,400 with an interest rate of 8% per annum. The note matures on July 13, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. Per the Company the note was not funded but the Company has accrued the note and interest as of September 30, 2016, totaling $48,227.

On August 11, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,500 with an interest rate of 8% per annum. The note matures on August 11, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. AS of September 30, 2016, the outstanding balance of the principal was $27,500 and interest of $4,343 for a total of $31,843.

On August 11, 2015, LG Capital's lawsuit claims the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,500 with an interest rate of 8% per annum. The note matures on August 11, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. Per the Company the note was not funded but the Company has accrued the note and interest as of September 30, 2016, totaling $31,843.

On September 8, 2015, the Company issued a Convertible Note to LG CAPITAL FUNDING, LLC ("LG Capital") for a principle amount of $27,000 with an interest rate of 8% per annum. The note matures on September 8, 2016, 2016. The note is convertible by the holder at a discount of 55% of the lowest trading price of the Company's stock for the 15 days prior to the conversion. As of September 30, 2016, the outstanding balance of principal was $27,000 and interest of $4,343 for a total of $31,082.

As of September 30, 2016, the outstanding aggregate balance of all notes due to LG Capital Funding, LLC is $218,480.

On November 5, 2015, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $28,000 with an interest rate of 12% per annum. The note matures on August 5, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of the principal was $28,000 after the conversion of $6,104 to common stock of the Company plus interest of $3,037 for a total of $31,037.

On December 21, 2015, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $21,000 with an interest rate of 12% per annum. The note matures on September 16, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion.AS of September 30, 2016 the outstanding balance of the note was $21,000 in principal plus $1,967 interest for a total of $22,967.

On March 11, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $18,000 with net proceeds of $15,000 and with an interest rate of 12% per annum. The note matures on December 11, 2016. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's

F-10

stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of the note was principal of $18,000 plus interest of $1,207for a total of $19,207.

On March 14, 2016, the Company issued a Convertible Note to LG Capital Funding, LP for a principle amount of $18,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance of principal was $18,000 plus interest of $1,207 for a total of $19,207.

On May 17, 2016, the Company issued a Convertible Note Craig Savin for a principle amount of $15,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. The note was paid in a settlement agreement whereby the Company issued 1,000,000 shares of its common stock to settle outstanding obligations including this note, a note for $5,000 and the issuance of shares for a stock subscription payable of $50,000

On May 26, 2016, the Company issued a Convertible Note to LG Capital Funding, LP for a principle amount of $17,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 50% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. Net proceeds to the Company are $15,000 after deduction of legal fees of $2,000. As of September 30, 2016, the outstanding balance of the note was $17,000 in principal plus interest of $428 for a total of $17,428.

On June 14, 2016, the Company issued a Convertible Note Craig Savin for a principle amount of $5,000 with an interest rate of 12% per annum. The note matures on March 14, 2017. The note is convertible by the holder at a discount of 45% of the lowest trading price of the Company's stock for the 20 days prior to the conversion. On September 9, 2016, the Company issued 1,000,000 share of common stock for the payment of this note, a note for $15,000 plus a $50,000 stock payable due Savin. The balance of the note as of September 30, 2016, is zero.

On July 25, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $23,000 with an interest rate of 12% per annum. The note matures on July 25, 2017. The note is convertible by the holder at a discount of 45% of the lowest three trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance included principal of $23,000 plus interest of $514 for a total of $23,514.

On September 7, 2016, the Company issued a Convertible Note to Carebourn Capital, LP for a principle amount of $197,363,70 less legal fees of $8,000 with an interest rate of 12% per annum. The note matures on September 7, 2017. The note is convertible by the holder at a discount of 50% of the lowest three trading price of the Company's stock for the 20 days prior to the conversion. As of September 30, 2016, the outstanding balance included principal of $115,114 plus interest of $908 for a total of $116,022.

Management has reviewed the terms of the convertible instruments to determine their fair value. After reviewing the characteristic and the value of the conversion, Management has determined based on note conversion history that the conversion value is equal or less than par value of the shares used for conversion thus determining that the fair value of the notes is equal to their face value.

As the market value of the Company' stock is below it par value and exercise price, Management has concluded that the benefit of the conversion feature is zero and has not allocate a value to the conversion.

As of June 30, 2016, the Company outstanding liability of convertible debt was $517,735 plus interest of $49,431 for a total liability of $567,166. The liability was as follows:

F-11

|

Lender

|

Principal

|

Interest

|

Total

|

|||||||||

|

LG Capital

|

258,115

|

39,044

|

297,159

|

|||||||||

|

Carebourn Capital

|

259,621

|

10,389

|

270,010

|

|||||||||

|

Total

|

$

|

517,736

|

$

|

49,433

|

$

|

567,169

|

||||||

On September 15, 2016, LG Capital, LLC filed a lawsuit against the Company. The filing alleges that the Company has defaulted on several unpaid loans from LG Capital to the Company with the total claim against the Company of $279,730.56. The Company negotiated in good faith with LG Capital to settle the debt but to no avail. After reviewing the claim filed by LG Capital, it is the opinion of Company Management that the Company's outstanding liability to LG Capital has been fully recognized and accounted for in the financial statements of the Company. (See Note 10- Legal).

Note 6 – Related Party

On February 2, 2015, the Company issued to an officer and director of the Company 10,000,000 shares with a value of $10,000 of series A preferred stock for service. Each share has 10,000 votes on all matters of the Company in which the shareholders can vote.

Note 7 – Equity

On February 2, 2015, the Company issued 10,000,000 shares of Series A Preferred Stock to an officer and director of the Company. Each share of series A preferred has 10,000 votes for all shareholder matters compared to 1 vote for each share of common stock.

During the year ended September 30, 2015 the Company issued 540,282 shares of common stock for debt with a value of $228,317.

During the year ended September 30, 2015 the Company issued 8,572 shares of common stock for accrued liabilities with a value of $127,968.

During the year ended September 30, 2015 the Company issued 1,428 shares of common stock to a related party for service with a value of $50,000.

During the year ended September 30, 2015 the Company issued 2,977 shares of common stock to a related party for service with a value of $98,650.

During the year ended September 30, 2016 the Company issued 1,100,000 shares of common stock to two parties for service with a value of $80,000.