Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - ALICO, INC. | exhibit322q42016.htm |

| EX-32.1 - EXHIBIT 32.1 - ALICO, INC. | exhibit321q42016.htm |

| EX-31.2 - EXHIBIT 31.2 - ALICO, INC. | exhibit312q42016.htm |

| EX-31.1 - EXHIBIT 31.1 - ALICO, INC. | exhibit311q42016.htm |

| EX-23.0 - EXHIBIT 23 - ALICO, INC. | exhibit230consent.htm |

| EX-10.35 - EXHIBIT 10.35 - ALICO, INC. | slktam2594350v1alicorabofi.htm |

| EX-10.34 - EXHIBIT 10.34 - ALICO, INC. | slktam2594347v1alicorabofi.htm |

| EX-10.33 - EXHIBIT 10.33 - ALICO, INC. | slktam2594353v1alicorabofi.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the fiscal year ended September 30, 2016 | |||

or | |||

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the transition period | |||

from____________________ | to_________________________ | ||

Commission File Number: 0-261

Alico, Inc. |

(Exact name of registrant as specified in its charter) |

Florida | 59-0906081 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

10070 Daniels Interstate Court, | ||

Suite 100, Fort Myers, FL | 33913 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: 239-226-2000

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of class: | Name of each exchange on which registered: | |

COMMON CAPITAL STOCK, $1.00 Par value, Non-cumulative | NASDAQ | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that such registrant was required to file such reports), and (2) has been subject to such filings requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 or Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer”, “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer | ¨ | Accelerated filer | þ |

Non-accelerated filer | ¨ | Smaller Reporting Company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ¨ No þ

The aggregate market value of the voting and nonvoting common equity held by non-affiliates based on the closing price, as quoted on the NASDAQ Global Market as of March 31, 2016 (the last business day of Alico’s most recently completed second fiscal quarter) was $86,944,912. Solely for the purposes of this calculation, the registrant has elected to treat all executives, officers and greater than 10% stockholders as affiliates of the registrant. There were 8,324,747 shares of common stock outstanding at December 1, 2016.

Documents Incorporated by Reference:

Portions of the Proxy Statement of Registrant for the 2017 Annual Meeting of Shareholders (to be filed with the Commission under Regulation 14A within 120 days after the end of the Registrant's fiscal year), are incorporated by reference in Part III of this report.

ALICO, INC.

FORM 10-K

For the fiscal year ended September 30, 2016

PART I | |

Item 1. Business | |

Item 1A. Risk Factors | |

Item 1B. Unresolved Staff Comments | |

Item 2. Properties | |

Item 3. Legal Proceedings | |

Item 4. Mine Safety Disclosures | |

PART II | |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

Item 6. Selected Financial Data | |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A. Quantitative and Qualitative Disclosures about Market Risk | |

Item 8. Financial Statements and Supplementary Data | |

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

Item 9A. Controls and Procedures | |

Item 9B. Other Information | |

PART III | |

Item 10. Directors, Executive Officers and Corporate Governance | |

Item 11. Executive Compensation | |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13. Certain Relationships and Related Transactions, and Director Independence | |

Item 14. Principal Accountants Fees and Services | |

PART IV | |

Item 15. Exhibits, Financial Statement Schedules | |

Signatures | |

Cautionary Statement

This Annual Report on Form 10-K contains certain “forward-looking statements,” as such term is defined in Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). They are based on management’s current expectations and assumptions regarding our business and performance, the economy and other future conditions and forecasts of future events, circumstances and results. These forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements often include words such as “may,” “will,” “could,” “should,” “would,” “believes,” “expects,” “anticipates”, “estimates”, “projects,” “intends, “plans” and other words and terms of similar substance in connection with discussions of future operating or financial performance. Such forward-looking statements include, but are not limited to, statements regarding future actions, business plans and prospects, prospective products, trends, future performance or results of current and anticipated products, sales efforts, expenses, interest rates, the outcome of contingencies, such as legal proceedings, plans relating to dividends, government regulations, the adequacy of our liquidity to meet our needs for the foreseeable future and our expectations regarding market conditions.

As with any projection or forecast, forward-looking statements are inherently susceptible to uncertainty and changes in circumstances. Our actual results may vary materially from those expressed or implied in our forward-looking statements. Should known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual results could vary materially from past results and those anticipated, estimated or projected. Investors should bear this in mind as they consider forward-looking statements.

We undertake no obligation to update forward-looking statements, whether as a result of new information, future events or otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with the Securities and Exchange Commission ("SEC"). We provide in Item 1A, “Risk Factors,” a cautionary discussion of certain risks and uncertainties related to our businesses. These are factors that we believe, individually or in the aggregate, could cause our actual results to differ materially from expected and historical results. We note these factors for investors as permitted by Section 21E of the Exchange Act. In addition, the operation and results of our business are subject to risks and uncertainties identified elsewhere in this Annual Report on Form 10-K as well as general risks and uncertainties such as those relating to general economic conditions. You should understand that it is not possible to predict or identify all such risks. Consequently, you should not consider such discussion to be a complete discussion of all potential risks or uncertainties.

PART I

Item 1. Business

Alico, Inc. (“Alico”), was incorporated under the laws of the state of Florida in 1960. Collectively with its subsidiaries (the "Company", "we", "us" or "our"), our business and operations are described below. For detailed financial information with respect to our business and our operations, see Management’s Discussion and Analysis of Financial Condition and Results of Operations which is included in Item 7 in this Annual Report on Form 10-K, and the accompanying Consolidated and Combined Financial Statements and the related Notes therein, which are included in Item 8. In addition, general information concerning our Company can be found on our website, the internet address of which is http://www.alicoinc.com. All of our filings with the SEC including, but not limited to, the Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments thereto, are available free of charge on our website as soon as reasonably practicable after such material is electronically filed or furnished with the SEC. In addition, you may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. To obtain information on the operation of the Public Reference room, you may call the SEC at 1-800-SEC-0330. Our recent press releases and information regarding corporate governance, including the charters of our audit, compensation, executive and nominating governance committees, as well as our code of business conduct and ethics are also available to be viewed or downloaded electronically at http://www.alicoinc.com. The information on our website is not part of this report or any other report we file with or furnish to the SEC.

Overview

Alico is an agribusiness and natural resources management company, with a legacy of achievement and innovation in citrus, cattle and resource conservation. The Company owns approximately 122,000 acres of land in twelve Florida counties (Alachua, Charlotte, Collier, DeSoto, Glades, Hardee, Hendry, Highlands, Lee, Martin, Osceola and Polk) including approximately 90,000 acres of mineral rights. Our principal lines of business are citrus groves, cattle ranching and conservation.

During the fiscal year ended September 30, 2015, the Company acquired three Florida citrus properties for total consideration of approximately $363,000,000. These acquisitions make Alico one of the largest citrus producers in the United States of America.

Our mission is to create value for our customers and stockholders by managing existing lands to their optimal current income and total returns, opportunistically acquiring new agricultural assets and producing high quality agricultural products while exercising responsible environmental stewardship.

We manage our land based upon its primary usage and review its performance based upon two primary classifications - Orange Co. and Conservation and Environmental Resources. In addition, Other Operations include lease income from an aggregates mine and leases of oil extraction rights to third parties among other insignificant lines of business. We present our financial results and the related discussion based upon our three business segments (Orange Co., Conservation and Environmental Resources, and Other Operations).

Recent Developments

Water Storage Contract Approval

In December 2012, the South Florida Water Management District (“SFWMD” or "District") issued a solicitation request for projects to be considered for the Northern Everglades Payment for Environmental Services Program. The Company submitted its response proposing a dispersed water management project on a portion of its ranch land, and on December 11, 2014 the SFWMD approved a contract with the Company, and on September 29, 2015, the SFWMD amended the contract to extend it for an additional year.

The contract term is eleven years, and allows up to one year for implementation (design, permitting, construction and construction completion certification) and ten years of operation whereby the Company will provide water retention services. Payment for these services includes an amount not to exceed $4,000,000 of reimbursement for implementation. In addition, it provides for an annual fixed payment of up to $12,000,000 for operations and maintenance costs as long as the project is in compliance with the contract.

Annual payments under the contract are subject to the SFWMD receiving funds for the project from the Florida Legislature and SFWMD Governing Board budget appropriation. Funding for the first year of the dispersed water management project was included in the budget approved in the 2016 legislative session.

1

Project permitting is in process and the Company intends to commence construction upon receipt of permits. Annual fixed payments will not commence until completion of construction.

Change in Fiscal Year of Subsidiary

As Alico, Inc. and 734 Citrus Holdings, LLC ("Silver Nip Citrus") were under common control at the time of the Merger (see Note 1. "Description of Business and Basis of Presentation" of Item 8. Financial Statements and Supplementary Data) it is required under accounting principles generally accepted in the United States of America ("U.S. GAAP") to account for this common control acquisition in a manner similar to the pooling of interest method of accounting. Under this method of accounting, the Company's Consolidated and Combined Balance Sheets as of September 30, 2016 and September 30, 2015 reflect Silver Nip Citrus’ historical carryover basis in the assets and liabilities, instead of reflecting the fair market value of the assets and liabilities. Alico has also retrospectively recast its financial statements to combine the operating results of the Company and Silver Nip Citrus from the date common control began, November 19, 2013.

Silver Nip Citrus’ fiscal year end was June 30. Their financial condition and results of operations as of and for the fiscal years ended June 30, 2015 and 2014 were included in the financial condition and results of operations of the Company as of and for the fiscal years ended September 30, 2015 and 2014, respectively. Effective October 1, 2015, the fiscal year end for Silver Nip Citrus was changed to September 30 to reflect that of the Company. Accordingly, the Company’s financial condition as of September 30, 2016 and 2015 now includes the financial condition of Silver Nip Citrus as of September 30, 2016 and 2015, respectively. The Company’s results of operations for the fiscal years ended September 30, 2016 and 2015 now includes the Silver Nip Citrus results of operations for fiscal years ended September 30, 2016 and 2015, respectively. The Company’s results of operations for the fiscal year ended September 30, 2014 include the operating results of Silver Nip Citrus from the date common control began, November 19, 2013 through September 30, 2014. The impact of this change was not material to the Consolidated and Combined Financial Statements, with an approximate $492,000 decrease in total assets and an approximate net loss of $596,000 for the transition period related to this change included in Stockholders' Equity at September 30, 2015.

Operating Segments

Operating segments are defined in Financial Accounting Standards Board ("FASB") - Accounting Standards Codification ("ASC") ASC Topic 280, "Segment Reporting" as components of public entities that engage in business activities from which they may earn revenues and incur expenses for which separate financial information is available and which is evaluated regularly by the Company’s chief operating decision maker (“CODM”) in deciding how to assess performance and allocate resources. For the fiscal year ended September 30, 2015, the Company’s CODM assessed performance and allocated resources based on five operating segments: Citrus Groves, Improved Farmland, Ranch and Conservation, Agricultural Supply Chain Management and Other Operations.

Effective October 1, 2015, which was the first day of Alico's fiscal year 2016, the Company operates three business segments related to its various land holdings, as follows:

• | Orange Co. includes activities related to planting, owning, cultivating and/or managing citrus groves in order to produce fruit for sale to fresh and processed citrus markets, including activities related to the purchase and resale of fruit and value-added services, which include contracting for the harvesting, marketing and hauling of citrus. |

• | Conservation and Environmental Resources includes activities related to cattle grazing, sod, native plant and animal sales, leasing, management and/or conservation of unimproved native pasture land. |

• | Other Operations consists of activities related to rock mining royalties, oil exploration and other insignificant lines of business. Also included are activities related to owning and/or leasing improved farmland. Improved farmland is acreage that has been converted, or is permitted to be converted, from native pasture and which may have various improvements including irrigation, drainage and roads. |

The former Citrus Groves and Agricultural Supply Chain Management segments have been combined in Orange Co. and, as a result of the disposition of its sugarcane land in fiscal year 2015, the Company is no longer involved in sugarcane and the Improved Farmland segment is no longer material to its business and has been combined in Other Operations.

The Land We Manage

We regularly review our land holdings to determine the best use of each parcel based upon our management expertise. Our total return profile is a combination of operating income potential and long-term appreciation. Land holdings not meeting our total

2

return criteria are considered surplus to our operations and will be sold or exchanged for land considered to be more compatible with our business objectives and total return profile.

Our land holdings and the operating activities in which we engage are categorized in the following table:

Gross Acreage | Operating Activities | |||

Orange Co. | ||||

Citrus Groves | 47,127 | Citrus Cultivation | ||

Citrus Nursery | 385 | Citrus Tree Development | ||

47,512 | ||||

Conservation and Environmental Resources | 70,962 | Cattle Production; Sod and Native Plant Sales; Leasing; Conservation | ||

Other Operations | ||||

Farmland | 1,825 | Leasing | ||

Other Land | 1,485 | Mining lease; Office | ||

Total | 121,784 | |||

Orange Co.

We own and manage citrus land in Alachua, DeSoto, Polk, Collier, Hendry, Charlotte, Highlands, Osceola, Martin, and Hardee Counties and engage in the cultivation of citrus trees to produce citrus for delivery to the fresh and processed citrus markets. Orange Co. citrus groves totals approximately 48,000 gross acres or 39.1% of our land holdings.

Our citrus acreage is detailed in the following table:

Net Plantable | ||||||||||||

Producing | Developing | Fallow | Total Plantable | Support & Other | Gross | |||||||

Alachua County | — | — | — | — | 385 | 385 | ||||||

DeSoto County | 15,013 | 1,090 | 482 | 16,585 | 4,623 | 21,208 | ||||||

Polk County | 4,558 | 95 | — | 4,653 | 2,152 | 6,805 | ||||||

Collier County | 4,468 | — | — | 4,468 | 2,823 | 7,291 | ||||||

Hendry County | 3,517 | 97 | 175 | 3,789 | 1,696 | 5,485 | ||||||

Charlotte County | 1,730 | — | 138 | 1,868 | 635 | 2,503 | ||||||

Highlands County | 1,093 | — | — | 1,093 | 131 | 1,224 | ||||||

Osceola County | 937 | — | — | 937 | 426 | 1,363 | ||||||

Martin County | 551 | — | — | 551 | 123 | 674 | ||||||

Hardee County | 403 | — | — | 403 | 171 | 574 | ||||||

Total | 32,270 | 1,282 | 795 | 34,347 | 13,165 | 47,512 | ||||||

Of the approximately 48,000 gross acres of citrus land we own and manage, approximately 13,200 acres are classified as support acreage. Support acreage includes acres used for roads, barns, water detention, water retention and drainage ditches integral to the cultivation of citrus trees but which are not capable of directly producing fruit. In addition, we own a citrus tree nursery and utilize the trees produced in our own operations. None of our citrus acreage is classified as available for sale. The approximately 34,300 remaining acres are classified as net plantable acres. Net plantable acres are those that are capable of directly producing fruit. These include acres that are currently producing, acres that are developing (acres that are planted in trees too young to commercially produce fruit) and acres that are fallow.

3

Our Orange Co. business segment cultivates citrus trees to produce citrus for delivery to the processed and fresh citrus markets. Our sales to the processed market are approximately 86.9% of Orange Co. revenues annually. We produce Early and Mid-Season varieties, primarily Hamlin oranges, as well as a Valencia variety for the processed market. We deliver our fruit to the processors in boxes which contain approximately 90 pounds of oranges. Because the processors convert the majority of the citrus crop into orange juice, they generally do not buy their citrus on a per box basis but rather on a pound solids basis, which is the measure of the soluble solids (sugars and acids) contained in one box of citrus fruit. We produced approximately 51,400,000, 62,200,000 and 26,600,000 pound solids for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively, on boxes delivered to processing plants of approximately 8,829,000, 10,014,000 and 4,146,000, respectively.

The average pound solids per box was 5.82, 6.21 and 6.41 for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively.

We generally use multi-year contracts with citrus processors that include pricing structures based on a minimum (“floor”) price with a price increase (“rise”) based on market conditions. Therefore, if pricing in the market is favorable relative to our floor price, we benefit from the incremental difference between the floor and the final market price.

The majority of our citrus produced for the processed citrus market in fiscal year 2016-2017 will be under minimum price contracts with a floor prices ranging from $2.05 to $2.15 per pound solids. We believe that other markets are available for our citrus products; however, new arrangements may be less favorable than our current contracts.

Our sales to the fresh market constitute approximately 3.8% of our Orange Co. revenues annually. We produce numerous varieties for the fresh fruit market including grapefruit, navel and other fresh varieties. Generally, our fresh fruit is sold to packing houses by the box and the packing houses are responsible for the harvest and haul of these boxes. We produced approximately 402,000, 466,000 and 213,000 fresh fruit boxes for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively. The majority of our citrus to be produced for the fresh citrus market in fiscal year 2016-2017 is under fixed price contracts.

Revenues from our Orange Co. operations were approximately 95.2%, 95.5% and 71.9% of our total operating revenues for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively.

Conservation and Environmental Resources

We own and manage Conservation and Environmental Resources land in Collier and Hendry Counties and engage in cattle production, sod and native plant sales, land leasing for recreational and grazing purposes and conservation activities. Of our land holdings, Conservation and Environmental Resources totals approximately 71,000 gross acres or 58.3% of our total acreage.

Our Conservation and Environmental Resources acreage is detailed in the following table as of September 30, 2016:

Acreage | ||

Hendry County | 66,940 | |

Collier County | 4,022 | |

Total | 70,962 | |

We frequently lease the same acreage for more than one purpose. The portion of our Conservation and Environmental Resources acreage that is leased for each purpose is detailed in the table below:

Grazing | Recreational | ||||

Hendry County | 1,282 | 51,686 | |||

Collier County | 4,000 | 3,493 | |||

Glades County | 145 | — | |||

Our cattle operation is engaged in the production of beef cattle and is located in Hendry and Collier Counties. The breeding herd consists of approximately 8,700 cows and bulls and we plan to increase the size of our herd in the near future to the extent practicable. We primarily sell our calves to feed yards and yearling grazing operations in the United States. We also sell cattle through local livestock auction markets and to contract cattle buyers in the United States. These buyers provide ready markets for our cattle. We believe that the loss of any one or a few of these buyers would not have a material effect on our cattle operations.

4

Revenues from our Conservation and Environmental Resources operations were approximately 4.0%, 3.6% and 7.9% of total operating revenues for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively.

Our Strategy

Our core business strategy is to maximize stockholder value through continuously improving the return on our invested capital, either by holding and managing our existing land through skilled agricultural production, leasing, or other opportunistic means of monetization, disposing of under productive land or business units and/or acquiring new land or operations with appreciation potential.

Our objectives are to produce the highest quality agricultural products, create innovative land uses, opportunistically acquire and convert undervalued assets, sell-under productive land not meeting our total return profile, generate recurring and sustainable profit with the appropriate balance of risk and reward, and exceed the expectations of stockholders, customers, clients and partners.

Our strategy is based on best management practices of our agricultural operations, environmental and conservation stewardship of our land and natural resources. We manage our land in a sustainable manner and evaluate the effect of changing land uses while considering new opportunities. Our commitment to environmental stewardship is fundamental to the Company’s core beliefs.

Competition

The orange and specialty citrus markets are intensely competitive, but no single producer has any significant market power over any market segments, as is consistent with the production of most agricultural commodities. Citrus is grown domestically in several states including Florida, California, Arizona and Texas, as well as foreign countries, most notably Brazil. Competition is impacted by several factors including quality, production, demand, brand recognition, market prices, weather, disease, export/import restrictions and foreign currency exchange rates. Beef cattle are produced throughout the United States and domestic beef sales also compete with imported beef.

Environmental Regulations

Our operations are subject to various federal, state and local laws regulating the discharge of materials into the environment. Management believes we are in compliance with all such rules including permitting and reporting requirements. Historically, compliance with environmental regulations has not had a material impact on our financial position, results of operations or cash flows.

Management monitors environmental legislation and requirements and makes every effort to remain in compliance with such regulations. In addition, we require lessees of our property to comply with environmental regulations as a condition of leasing.

Employees

As of September 30, 2016, we had 333 full-time employees. Our employees work in the following divisions:

Orange Co. | 298 |

Conservation and Environmental Resources | 6 |

Corporate, General, Administrative and Other | 29 |

Total employees | 333 |

5

Seasonal Nature of Business

Revenues from our agricultural business operations are seasonal in nature. The following table illustrates the seasonality of our agri-business revenues:

Fiscal Year | ||||||||||||

Q1 | Q2 | Q3 | Q4 | |||||||||

Ending 12/31 | Ending 3/31 | Ending 6/30 | Ending 9/30 | |||||||||

Oct | Nov | Dec | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sept | |

Harvest Fresh and Early/Mid Varieties of Oranges | ||||||||||||

Harvest Valencia Oranges | ||||||||||||

Deliver Beef Cattle | ||||||||||||

Capital resources and raw materials

Management believes that the Company will be able to meet its working capital requirements for at least the next 12 months, and over the long term, through internally generated funds, cash flows from operations, our existing lines of credit and access to capital markets. The Company has commitments that provide for lines of revolving credit that are available for our general and corporate use. Raw materials needed to cultivate the various crops grown by the Company consist primarily of fertilizers, herbicides and fuel and are readily available from local suppliers.

Available Information

We provide electronic copies of our SEC filings free of charge upon request. Any information posted on or linked from our website is not incorporated by reference in this Annual Report on Form 10-K. The SEC also maintains a website at http://www.sec.gov, which contains annual, quarterly and current reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

Item 1A. Risk Factors

Our business and results of operations are subject to numerous risks and uncertainties, many of which are beyond our control. The following is a description of the known factors that we believe may materially affect our business, financial condition, results of operations or cash flows. They should be considered carefully, in addition to the information set forth elsewhere in this Annual Report on Form 10-K, including Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8, Financial Statements and Supplementary Data, including the related Notes to the Consolidated and Combined Financial Statements in making any investment decisions with respect to our securities. Additional risks or uncertainties that are not currently known to us that we currently deem to be immaterial or that could apply to any company could also materially adversely affect our business, financial condition, results of operations or cash flows.

Risks related to our Business

Our citrus groves are subject to damage and loss from disease including but not limited to citrus greening and citrus canker which could negatively impact our business, financial condition, results of operations and cash flows.

Our citrus groves are subject to damage and loss from diseases such as citrus greening and citrus canker. Each of these diseases is widespread in Florida and exists in our citrus groves and in the areas where our citrus groves are located. The success of our citrus business is directly related to the viability and health of our citrus groves.

Citrus greening is one of the most serious citrus plant diseases in the world. Once a tree is infected, its productivity generally decreases. While the disease poses no threat to humans or animals, it has devastated citrus crops throughout the United States and abroad. Named for its green, misshapen fruit, citrus greening disease has now killed millions of citrus plants in the southeastern United States and has spread across the entire country. Infected trees produce fruits that are green, misshapen and bitter, unsuitable for sale as fresh fruit or for juice. Infected trees can die within a few years. At the present time, there is no known cure for citrus greening once trees are infected. Primarily as a result of citrus greening, orange production in the State of Florida has continued

6

to drop and according to the U.S. Department of Agriculture Florida had its smallest orange harvest in 52 years in the 2015-2016 harvest season. The upcoming 2016-2017 Florida harvest season is expected to decline even further. The USDA's forecast of approximately 72,000,000 boxes of oranges for the 2016-2017 season is down more than 13 percent from the approximately 81,600,000 boxes harvested last season and represents a decline of more than 52 percent since the time citrus greening was discovered at approximately 150,000,000 boxes during the 2004-05 season.

Citrus canker is a disease affecting citrus species and is caused by a bacterium and is spread by contact with infected trees or by windblown transmission. There is no known cure for citrus canker at the present time although some management practices including the use of copper-based bactericides can mitigate its spread and lessen its effect on infected trees; however, there is no assurance that available technologies to control such disease will be effective.

Both of these diseases pose a significant threat to the Florida citrus industry and to our citrus groves. While we use best management practices to attempt to control diseases and their spread, there can be no assurance that our mitigation efforts will be successful. These diseases can significantly increase our costs which could materially adversely affect our business, financial condition, results of operations and cash flows. Our citrus groves produce a significant majority of our annual operating revenues and a significant reduction in available citrus from our citrus groves could decrease our operating revenues and materially adversely affect our business, financial condition, results of operations and cash flows.

Our agricultural products are subject to supply and demand pricing which is not predictable.

Agricultural operations traditionally provide almost all of our operating revenues with citrus being the largest portion and are subject to supply and demand pricing. While according to Nielsen data consumer demand for orange juice has decreased significantly to its lowest level in almost a decade, we have been able to offset the impact of such decline with higher prices based on a lower supply of available oranges. However, there can be no assurance that we will be able to continue to do so if demand continues to decline. Although our processed citrus is subject to minimum pricing we are unable to predict with certainty the final price we will receive for our products. In some instances the harvest and growth cycle will dictate when such products must be marketed which may or may not be advantageous in obtaining the best price. Excessive supplies tend to cause severe price competition and lower prices for the commodity affected. Limited supply of certain agricultural commodities due to world and domestic market conditions can cause commodity prices to rise in certain situations. We attempt to mitigate these risks by using contracts with citrus processors that include pricing structures based on a minimum (“floor”) price and with a price increase (“rise”) if market prices exceed the floor price. As a result, our profitability may be subject to significant variability.

Our citrus groves are geographically concentrated in Florida and the effects of adverse weather conditions including hurricanes and tropical storms could adversely affect our results of operations and financial position.

Our citrus operations are concentrated in central and south Florida with our groves located in parcels in Alachua, DeSoto, Polk, Collier, Hendry, Charlotte, Highlands, Osceola, Martin and Hardee Counties. Because our groves are located in close proximity to each other, the impact of adverse weather conditions may be material to our results of operations. Florida is particularly susceptible to the occurrence of hurricanes and tropical storms. Depending on where any particular hurricane or tropical storm makes landfall, our properties could experience significant, if not catastrophic damage. Hurricanes and tropical storms have the potential to destroy crops, affect cattle breeding and impact citrus production through the loss of fruit and destruction of trees and/or plants either as a result of high winds or through the spread of windblown disease. Such damage could materially affect our citrus and cattle operations and could result in a loss of operating revenues from those products for a multi-year period. We seek to minimize hurricane risk by the purchase of insurance contracts, but the majority of our crops remain uninsured. In addition to hurricanes and tropical storms, the occurrence of other natural disasters and climate conditions in Florida, such as tornadoes, floods, freezes, unusually heavy or prolonged rain, droughts and heat waves, could have a material adverse effect on our operations and our ability to realize income from our crops or cattle.

A significant and increasing portion of our revenues are derived from our citrus business and any adverse event affecting such business could disproportionately harm our business.

Our revenues from our citrus business were approximately 95.2%, 95.5% and 71.9% of our operating revenues in fiscal years 2016, 2015 and 2014, respectively. As a result of our recently announced acquisitions of three Florida citrus properties and the disposition of our sugarcane lands, the percentage of our operating revenues derived from our citrus business has increased significantly. These acquisitions resulted in our citrus division being one of the largest citrus producers in the United States and since we will not be as diversified as we have been previously, we will be more vulnerable to adverse events or market conditions affecting our citrus business which could have a significant impact on our overall business results.

7

We maintain a significant amount of indebtedness which could adversely affect our financial condition, results of operations or cash flows and may limit our operational and financing flexibility and negatively impact our business.

As of September 30, 2016 we had approximately $197,000,000 in principal amount of indebtedness outstanding under our secured credit facilities and an additional $80,000,000 is available under our revolving lines of credit. Our loan agreements, and other debt instruments we may enter into in the future, may have negative consequences to us and could limit our business because we will use a substantial portion of our cash flows from operations to pay debt service costs which will reduce the funds available to us for corporate and general expenses and it may make us more vulnerable to economic downturns and adverse developments in our business. Our loan agreements require us to comply with various restrictive covenants and some contain financial covenants that require us to comply with specified financial ratios and tests. Our failure to meet these covenants could result in default under these loan agreements and would result in a cross-default under other loan agreements. In the event of a default and our inability to obtain a waiver of the default, all amounts outstanding under loan agreements could be declared immediately due and payable. Our loan agreements also contain various covenants that limit our ability to engage in specified types of transactions. We expect that we will depend primarily upon our citrus operations to provide funds to pay our corporate and general expenses and to pay any amounts that may become due under any credit facilities and any other indebtedness we may incur and there are factors beyond our control that could negatively affect our citrus business revenue stream. Our ability to make these payments depends on our future performance, which will be affected by various financial, business, macroeconomic and other factors, many of which we cannot control.

If we are unable to successfully develop and execute our strategic growth initiatives, or if they do not adequately address the challenges or opportunities we face, our business, financial condition and prospects may be adversely affected.

Our success is dependent in part on our ability to identify, develop and execute appropriate strategic growth initiatives that will enable us to achieve sustainable growth in the long term. The implementation of our strategic initiatives is subject to both the risks affecting our business generally and the inherent risks associated with implementing new strategies. These strategic initiatives may not be successful in generating revenues or improving operating profit and, if they are, it may take longer than anticipated. As a result and depending on evolving conditions and opportunities, we may need to adjust our strategic initiatives and such changes could be substantial, including modifying or terminating one or more of such initiatives. Termination of such initiatives may require us to write down or write off the value of our investments in them. Transition and changes in our strategic initiatives may also create uncertainty in our employees, customers and partners that could adversely affect our business and revenues. In addition, we may incur higher than expected or unanticipated costs in implementing our strategic initiatives, attempting to attract revenue opportunities or changing our strategies. There is no assurance that the implementation of any strategic growth initiative will be successful, and we may not realize anticipated benefits at levels we project or at all, which would adversely affect our business, financial condition and prospects.

Our agricultural operations are subject to water use regulations restricting our access to water.

Our operations are dependent upon the availability of adequate surface and underground water. The availability of water is regulated by the state of Florida through water management districts which have jurisdiction over various geographic regions in which our lands are located. Currently, we have permits in place for the next 15 to 20 years for the use of underground and surface water which are adequate for our agricultural needs.

Surface water in Hendry County, where much of our agricultural land is located, comes from Lake Okeechobee via the Caloosahatchee River and a system of canals used to irrigate such land. The Army Corps of Engineers controls the level of Lake Okeechobee and ultimately determines the availability of surface water even though the use of water has been permitted by the state of Florida through the water management district. The Army Corps of Engineers decided in 2010 to lower the permissible level of Lake Okeechobee in response to concerns about the ability of the levee surrounding the lake to restrain rising waters which could result from hurricanes. Changes in availability of surface water use may result during times of drought, because of lower lake levels and could materially adversely affect our agricultural operations, financial condition, results of operations and cash flows.

Our recent acquisitions of three Florida citrus properties and the acquisition of additional agricultural assets and other businesses could pose risks.

We seek to opportunistically acquire new agricultural assets from time to time that we believe would complement our business. In fiscal year 2015, we acquired three Florida citrus properties, including Orange-Co and Silver Nip Citrus, which resulted in our citrus division being one of the largest citrus producers in the United States. While we expect that our acquisitions will successfully complement our business, we may fail to realize all of the anticipated benefits of these acquisitions, which could reduce our anticipated results. We cannot assure you that we will be able to successfully identify suitable acquisition opportunities, negotiate

8

appropriate acquisition terms, or obtain any financing that may be needed to consummate such acquisitions or complete proposed acquisitions. Acquisitions by us could result in accounting changes, potentially dilutive issuances of equity securities, increased debt and contingent liabilities, reduce the amount of cash available for dividends, debt service payments, integration issues and diversion of management’s attention, any of which could adversely affect our business, results of operations, financial condition, and cash flows. We may be unable to successfully realize the financial, operational, and other benefits we anticipate from our acquisitions and our failure to do so could adversely affect our business, results of operation and financial condition.

Dispositions of our assets may adversely affect our future results of operations.

We also routinely evaluate the benefits of disposing of certain of our assets which could include the exit from lines of business. For example, in November of 2014 we sold significant sugarcane assets and we are no longer involved in the sugarcane business. While such dispositions increase the amount of cash available to us, it could also result in a potential loss of significant operating revenues and income streams that we might not be able to replace, makes our business less diversified and could ultimately have a negative impact on our results of operations and cash flows.

If a transaction intended to qualify as a Section 1031 Exchange is later determined to be taxable, we may face adverse consequences, and if the laws applicable to such transactions are amended or repealed, we may not be able to dispose of properties on a tax deferred basis.

From time to time we dispose of properties in transactions that are intended to qualify as Section 1031 Exchanges. It is possible that the qualification of a transaction as a Section 1031 Exchange could be successfully challenged and determined to be currently taxable and we could also be required to pay interest and penalties. As a result, we may be required to borrow funds in order to pay additional property taxes, and the payment of such taxes could cause us to have less cash available. Moreover, it is possible that legislation could be enacted that could modify or repeal the laws with respect to Section 1031 Exchanges, which could make it more difficult or not possible for us to dispose of properties on a tax deferred basis.

We may undertake one or more significant corporate transactions that may not achieve their intended results, may adversely affect our financial condition and our results of operations or result in unforeseeable risks to our business.

We continuously evaluate the acquisition or disposition of operating businesses and assets and may in the future undertake one or more significant transactions. Any such acquisitive transaction could be material to our business and could take any number of forms, including mergers, joint ventures and the purchase of equity interests. The consideration for such acquisitive transactions may include, among other things, cash, common stock or equity interests in us or our subsidiaries, or a contribution of property or equipment to obtain equity interests, and in conjunction with a transaction we might incur additional indebtedness. We also routinely evaluate the benefits of disposing of certain assets. Such dispositions could take the form of asset sales, mergers or sales of equity interests.

These transactions may present significant risks such as insufficient assets to offset liabilities assumed, potential loss of significant operating revenues and income streams, increased or unexpected expenses, inadequate return of capital, regulatory or compliance issues, the triggering of certain financial covenants in our debt instruments (including accelerated repayment) and unidentified issues not discovered in due diligence. In addition, such transactions could distract management from current operations. As a result of the risks inherent in such transactions, we cannot guarantee that any such transaction will ultimately result in the realization of its anticipated benefits or that it will not have a material adverse impact on our business, financial condition, results of operations or cash flows. If we were to complete such an acquisition, disposition, investment or other strategic transaction, we may require additional debt or equity financing that could result in a significant increase in our amount of debt and our debt service obligations or the number of outstanding shares of our common stock, thereby diluting holders of our common stock outstanding prior to such acquisition.

We are subject to the risk of product contamination and product liability claims.

The sale of agricultural products for human consumption involves the risk of injury to consumers. Such injuries may result from tampering by unauthorized third parties, product contamination or spoilage, including the presence of foreign objects, substances, chemicals, other agents, or residues introduced during the growing, storage, handling or transportation phases. While we are subject to governmental inspection and regulations and believe our facilities comply in all material respects with all applicable laws and regulations, we cannot be sure that our agricultural products will not cause a health-related illness in the future or that we will not be subject to claims or lawsuits relating to such matters. Even if a product liability claim is unsuccessful or is not fully pursued, the negative publicity surrounding any assertion that our products caused illness or injury could adversely affect our reputation with existing and potential customers and our corporate and brand image. Moreover, claims or liabilities of this sort might not be covered by our insurance or by any rights of indemnity or contribution that we may have against others. We maintain product

9

liability insurance, however, we cannot be sure that we will not incur claims or liabilities for which we are not insured or that exceed the amount of our insurance coverage.

Changes in immigration laws could impact our ability to harvest our crops.

We engage third parties to provide personnel for our harvesting operations. The availability and number of such workers is subject to decrease if there are changes in the U.S. immigration laws. The scarcity of available personnel to harvest our agricultural products could cause harvesting costs to increase or could lead to the loss of product that is not timely harvested which could have a material adverse effect to our citrus grove business, financial condition, results of operations and cash flows.

Changes in demand for our agricultural products can affect demand and pricing of such products.

The general public's demand for particular food crops we grow and sell could reduce prices for some of our products. To the extent that consumer preferences evolve away from products we produce and we are unable to modify our products or develop products that satisfy new customer preferences, there could be a decrease in prices for our products. Even if market prices are unfavorable, produce items which are ready to be or have been harvested must be brought to market. Additionally, we have significant investments in our citrus groves and cannot easily shift to alternative crops for this land. A decrease in the selling price received for our products due to the factors described above could have a material adverse effect on our business.

Our citrus business is seasonal.

Our citrus groves produce the majority of our annual operating revenues and the citrus business is seasonal because it is tied to the growing and picking seasons. Historically, the second and third quarters of our fiscal year generally produce the majority of our annual revenues, and our working capital requirements are typically greater in the first and fourth quarters of our fiscal year coinciding with our planting cycles. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved for the full fiscal year or in future quarters. If our operating revenues in the second and third quarters are lower than expected, it would have a disproportionately large adverse impact on our annual operating results.

We face significant competition in our agricultural operations.

We face significant competition in our agricultural operations both from domestic and foreign producers and do not have any branded products. Foreign growers generally have an equal or lower cost of production, less environmental regulation and in some instances, greater resources and market flexibility than us. Because foreign growers have greater flexibility as to when they enter the U.S. market, we cannot always predict the impact these competitors will have on our business and results of operations. The competition we face from foreign suppliers of orange juice is mitigated by a governmentally imposed tariff on orange imports. A change in the government’s reduction in the orange juice tariff could adversely impact our results of operations.

Climate change, or legal, regulatory, or market measures to address climate change, may negatively affect our business and operations.

There is growing concern that carbon dioxide and other greenhouse gases in the atmosphere may have an adverse impact on global temperatures, weather patterns, and the frequency and severity of extreme weather and natural disasters. In the event that such climate change has a negative effect on the productivity of our citrus groves, it could have an adverse impact on our business and results of operations. The increasing concern over climate change also may result in more regional, federal, and/or global legal and regulatory requirements to reduce or mitigate the effects of greenhouse gases. In the event that such regulation is enacted, we may experience significant increases in our costs of operations. In particular, increasing regulation of fuel emissions could substantially increase the distribution and supply chain costs associated with our products. As a result, climate change could negatively affect our business and operations.

We benefit from reduced real estate taxes due to the agricultural classification of a majority of our land. Changes in the classification or valuation methods employed by county property appraisers could cause significant changes in our real estate tax liabilities.

In the fiscal years ended September 30, 2016, 2015 and 2014 we paid approximately $3,196,000, $4,054,000 and $2,291,000, respectively, in real estate taxes, respectively. These taxes were based upon the agricultural use (“Green Belt”) values determined by the county property appraisers in which counties we own land, of approximately $89,922,000, $123,617,000 and $74,105,000 for each of the fiscal years ended September 30, 2016, 2015 and 2014, respectively, which differs significantly from the fair values determined by the county property appraisers of approximately $533,617,000, $652,891,000 and $518,112,000, respectively.

10

Changes in state law or county policy regarding the granting of agricultural classification or calculation of Green Belt values or average millage rates could significantly impact our results of operations, cash flows and financial position.

We manage our properties in an attempt to capture their highest and best use and customarily do not sell property until it no longer meets our total return profile.

The goal for our land management program is to manage and selectively improve our lands for their most profitable use. We continually evaluate our properties focusing on location, soil capabilities, subsurface composition, topography, transportation and availability of markets for our crops, the climatic characteristics of each of the tracts, long-term capital appreciation and operating income potential. While we are primarily engaged in agricultural activities, when land does not meet our total return profile, we may determine that the property is surplus to our activities and place the property for sale or exchange.

Liability for the use of pesticides, herbicides and other potentially hazardous substances could increase our costs.

Our agricultural business involves the use of herbicides, fertilizers and pesticides, some of which may be considered hazardous or toxic substances. We may be deemed liable and have to pay for the costs or damages associated with the improper application, accidental release or the use or misuse of such substances. Our insurance may not be adequate to cover such costs or damages, or may not continue to be available at a price or under terms that are satisfactory to us. In such cases, if we are required to pay significant costs or damages, it could materially adversely affect our business, results of operations, financial condition and cash flows.

Compliance with applicable environmental laws may substantially increase our costs of doing business which could reduce our profits.

We are subject to various laws and regulations relating to the operation of our properties, which are administered by numerous federal, state and local governmental agencies. We face a potential for environmental liability by virtue of our ownership of real property. If hazardous substances (including herbicides and pesticides used by us or by any persons leasing our lands) are discovered emanating from any of our lands and the release of such substances presents a threat of harm to the public health or the environment, we may be held strictly liable for the cost of remediation of these hazardous substances. In addition, environmental laws that apply to a given site can vary greatly according to the site’s location, its present and former uses, and other factors such as the presence of wetlands or endangered species on the site. Management monitors environmental legislation and requirements and makes every effort to remain in compliance with such regulations. Furthermore, we require lessees of our properties to comply with environmental regulations as a condition of leasing. We also purchase insurance for environmental liability when it is available; however, these insurance contracts may not be adequate to cover such costs or damages or may not continue to be available at prices and terms that would be satisfactory. It is possible that in some cases the cost of compliance with these environmental laws could exceed the value of a particular tract of land, make it unsuitable for use in what would otherwise be its highest and best use, and/or be significant enough that it would materially adversely affect us.

Our business may be adversely affected if we lose key employees.

We depend to a large extent on the services of certain key management personnel. These individuals have extensive experience and expertise in our business lines and segments in which they work. The loss of any of these individuals could have a material adverse effect on our businesses. We do not maintain key-man life insurance with respect to any of our employees. Our success will be dependent on our ability to continue to employ and retain skilled personnel in our business lines and segments.

Risks Related to our Common Stock

Our largest stockholder has effective control over the election of our Board of Directors and other matters.

734 Investors, LLC ("734 Investors") and its two controlling persons, Remy Trafelet and George Brokaw, together beneficially own approximately 59% of our outstanding common stock as of December 1, 2016. Accordingly, by virtue of its ownership percentage, 734 Investors is able to elect all of our directors and officers, and has the ability to exert significant influence over our business and may make decisions with which other stockholders may disagree, including, among other things, changes in our business plan, delaying, discouraging or preventing a change of control of our Company or a potential merger, consolidation, tender offer, takeover or other business combination. Additionally, potential conflicts of interest could exist when we enter into related party transactions with 734 Investors such as the Silver Nip Citrus merger we entered into on February 28, 2015. The terms of the merger were negotiated and considered by a special committee comprised entirely of independent and disinterested members of our Board of Directors.

11

We are a “Controlled Company” under the NASDAQ Listing Rules and therefore are exempt from certain corporate governance requirements, which could reduce the influence of independent directors.

We are a “Controlled Company” under NASDAQ listing rules, because more than 50% of the voting power of our outstanding common stock is controlled by 734 Investors and its two controlling persons, Remy Trafelet and George Brokaw. As a consequence, we are exempt from certain NASDAQ requirements including the requirement that:

• | Our Board of Directors be composed of a majority of independent directors; |

• | The compensation of our officers be determined by a majority of the independent directors or a compensation committee composed solely of independent directors; and |

• | Nominations to the Board of Directors be made by a majority of the independent directors or a nominations committee composed solely of independent directors. |

However, NASDAQ does require that our independent directors have regularly scheduled meetings at which only independent directors are present. In addition, Internal Revenue Code Section 162(m) requires that a compensation committee of outside directors (within the meaning of Section 162(m)) approve stock option grants to executive officers in order for us to be able to claim deductions for the compensation expense attributable to such stock options. Notwithstanding the foregoing exemptions, we do have a majority of independent directors on our Board of Directors and we do have an Audit Committee, a Compensation Committee and a Nominating and Governance Committee composed primarily of independent directors.

Although we currently comply with certain of the NASDAQ listing rules that do not apply to controlled companies, our compliance is voluntary, and there can be no assurance that we will continue to comply with these standards in the future. If in the future our Board of Directors elects to rely on the exemptions permitted by the NASDAQ listing standards and reduce the number or proportion of independent directors on our Board and its committees, the influence of independent directors would be reduced.

Sales of substantial amounts of our outstanding common stock by our largest stockholder could adversely affect the market price of our common stock.

Our largest stockholder, 734 Investors, beneficially owns approximately 59% of our outstanding common stock as of December 1, 2016. Our common stock is thinly traded and our common stock prices can fluctuate significantly. As such, sales of substantial amounts of our common stock into the public market by 734 Investors or perceptions that significant sales could occur, could adversely affect the market price of our common stock.

Our common stock has low trading volume.

Although our common stock trades on the NASDAQ Global Market, it is thinly traded and our average daily trading volume is low compared to the number of shares of common stock we have outstanding. The low trading volume of our common stock can cause our stock price to fluctuate significantly as well as make it difficult for you to sell your common shares quickly. As a result of our stock being thinly traded and/or our low stock price, institutional investors might not be interested in owning our common stock.

We may not be able to continue to pay or maintain our cash dividends on our common stock and the failure to do so may negatively affect our share price.

We have historically paid regular quarterly dividends to the holders of our common stock. Dividends were reduced beginning in the third fiscal quarter of 2014 in order to retain cash which increases our flexibility to reinvest in our business and pursue growth opportunities consistent with our mission. Our ability to pay cash dividends depends on, among other things, our cash flows from operations, our cash requirements, our financial condition, the degree to which we are/or become leveraged, contractual restrictions binding on us, provisions of applicable law and other factors that our Board of Directors may deem relevant. There can be no assurance that we will generate sufficient cash from continuing operations in the future, or have sufficient cash surplus or net profits to pay dividends on our common stock. Our dividend policy is based upon our directors’ current assessment of our business and the environment in which we operate and that assessment could change based on business developments (which could, for example, increase our need for capital expenditures) or new growth opportunities. Our Board of Directors may, in its discretion, decrease the level of cash dividends or entirely discontinue the payment of cash dividends. The reduction or elimination of cash dividends may negatively affect the market price of our common stock.

12

There can be no assurance that we will continue to repurchase shares of our common stock.

In fiscal year 2016, our Board of Directors authorized the repurchase of up to 50,000 shares of the Company’s common stock beginning February 18, 2016 and continuing through February 17, 2017. Our share repurchase program does not obligate us to repurchase any specific number of shares and may be suspended from time to time or terminated at any time prior to its expiration. There can be no assurance that we will repurchase shares in the future in any particular amounts or at all. A reduction in, or elimination of, share repurchases could have a negative effect on our share price.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

As of September 30, 2016, we owned approximately 122,000 acres of land located in twelve counties in Florida. Acreage in each county and the primary classification with respect to the present use of these properties is shown in the following table:

Total | Hendry | Polk | Collier | DeSoto | Glades | Lee | Alachua | Charlotte | Hardee | Highlands | Martin | Osceola | ||||||||||||||

Orange Co.: | ||||||||||||||||||||||||||

Citrus Groves | 47,127 | 5,485 | 6,805 | 7,291 | 21,208 | — | — | — | 2,503 | 574 | 1,224 | 674 | 1,363 | |||||||||||||

Citrus Nursery | 385 | — | — | — | — | — | — | 385 | — | — | — | — | — | |||||||||||||

Total Citrus Groves | 47,512 | 5,485 | 6,805 | 7,291 | 21,208 | — | — | 385 | 2,503 | 574 | 1,224 | 674 | 1,363 | |||||||||||||

Improved Farmland: | ||||||||||||||||||||||||||

Irrigated | 1,825 | 1,825 | — | — | — | — | — | — | — | — | — | — | — | |||||||||||||

Conservation and Environmental Resources | 70,962 | 66,940 | — | 4,022 | — | — | — | — | — | — | — | — | — | |||||||||||||

Commercial | 2 | — | — | — | — | — | 2 | — | — | — | — | — | — | |||||||||||||

Mining | 526 | — | — | — | — | 526 | — | — | — | — | — | — | — | |||||||||||||

Other | 957 | 957 | — | — | — | — | — | — | — | — | — | — | — | |||||||||||||

Total | 121,784 | 75,207 | 6,805 | 11,313 | 21,208 | 526 | 2 | 385 | 2,503 | 574 | 1,224 | 674 | 1,363 | |||||||||||||

Approximately 61,000 acres of the properties listed are encumbered by credit agreements totaling approximately $202,200,000 as of September 30, 2016. For a more detailed description of the credit agreements and collateral please see Note 5. “Long-Term Debt and Lines of Credit” and Note 19. "Subsequent Events" in the accompanying Notes to the Consolidated and Combined Financial Statements.

We currently collect mining royalties on approximately 526 acres of land located in Glades County, Florida. These royalties do not represent a significant portion of our operating revenues or gross profits. We have identified 850 acres on our Hendry County land that may have potential to be used as a sand mine. The Hendry County parcel is currently classified as other land.

13

Item 3. Legal Proceedings

On March 11, 2015, a putative stockholder class action lawsuit captioned Shiva Y. Stein v. Alico, Inc., et al., No. 15-CA-000645 (the “Stein lawsuit”), was filed in the Circuit Court of the Twentieth Judicial District in and for Lee County, Florida, against Alico, Inc. (“Alico”), its current and certain former directors, 734 Citrus Holdings, LLC d/b/a Silver Nip Citrus, 734 Investors, LLC (“734 Investors”), 734 Agriculture, LLC (“734 Agriculture”) and 734 Sub, LLC (“734 Sub”) in connection with the acquisition of Silver Nip Citrus by Alico (the “Merger”). The complaint alleged that Alico’s directors at the time of the Merger, 734 Investors and 734 Agriculture breached fiduciary duties to Alico stockholders in connection with the Merger and that Silver Nip and 734 Sub aided and abetted such breaches. The lawsuit sought, among other things, monetary and equitable relief, costs, fees (including attorneys’ fees) and expenses.

On May 6, 2015, a putative stockholder class action and derivative lawsuit captioned Ruth S. Dimon Trust v. George R. Brokaw, et al., No. 15-CA-001162 (the “Dimon lawsuit”), was filed in the Circuit Court of the Twentieth Judicial District in and for Lee County, Florida, against Alico, its current directors, Silver Nip Citrus, 734 Investors and 734 Agriculture in connection with the Merger of Silver Nip Citrus by Alico. The complaint alleged breach of fiduciary duty, gross mismanagement, waste of corporate assets and tortious interference with contract against Alico’s directors; unjust enrichment against three of the directors; and aiding and abetting breach of fiduciary duty against Silver Nip Citrus, 734 investors and 734 Agriculture. The lawsuit sought, among other things, rescission of the Merger, an injunction prohibiting certain payments to Silver Nip Citrus members, unspecified damages, disgorgement of profits, costs, fees (including attorneys’ fees) and expenses.

On July 17, 2015, the plaintiffs in the Stein and Dimon lawsuits filed a stipulation and proposed order consolidating their cases for all purposes under the caption, In re Alico, Inc. Shareholder Litigation, Master File No. 15-CA-000645 (the “Consolidated Action”) and seeking the appointment of a lead plaintiff and lead and liaison counsel. The court entered that proposed order on July 21, 2015.

On October 16, 2015, the lead plaintiff in the Consolidated Action reported to the Court that the parties reached an agreement in principle to settle the Consolidated Action and other claims related to the Merger and that they were in the process of formally documenting their agreements. The proposed settlement contemplated that Alico would adopt certain changes to its corporate governance practices, policies and procedures concerning related party transactions; the Consolidated Action would be dismissed; and all claims that were or could have been asserted challenging any aspect of the Merger would be released. On March 31, 2016, the parties entered into a Stipulation of Settlement. The parties filed an Amended Stipulation of Settlement with the Court on April 22, 2016.

On April 28, 2016, the Court entered an order preliminarily approving the settlement and providing for notice to relevant Alico shareholders. Notice of the settlement was mailed to relevant Alico shareholders and a settlement hearing was held on September 12, 2016, during which the Court considered the fairness, reasonableness and adequacy of the settlement and plaintiffs' counsel’s request for an award of attorneys' fees and expenses.

Following the settlement hearing on September 12, 2016, the Court entered a final order and judgment that approved the settlement as fair, reasonable and adequate; directed the parties to consummate the settlement according to its terms; awarded plaintiffs’ counsel attorneys’ fees and expenses; and dismissed the Consolidated Action with prejudice.

From time to time, Alico may be involved in litigation relating to claims arising out of its operations in the normal course of business. There are no current legal proceedings to which the Company is a party to or of which any of its property is subject to that it believes will have a material adverse effect on its financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures

Not Applicable.

14

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Common Stock Prices

Our common stock is traded on the NASDAQ Global Market under the symbol ALCO. The high and low sales prices of our common stock in each quarter in the fiscal years 2016 and 2015 are presented below:

2016 Price | 2015 Price | ||||||||||||||

High | Low | High | Low | ||||||||||||

Quarter Ended: | |||||||||||||||

December 31 | $ | 45.82 | $ | 37.55 | $ | 51.83 | $ | 34.67 | |||||||

March 31 | $ | 38.56 | $ | 20.99 | $ | 58.10 | $ | 43.80 | |||||||

June 30 | $ | 32.66 | $ | 26.02 | $ | 52.74 | $ | 44.52 | |||||||

September 30 | $ | 31.95 | $ | 26.50 | $ | 48.94 | $ | 37.16 | |||||||

Holders

On December 1, 2016, our stock transfer records indicate there were 260 holders of record of our common stock. The number of registered holders includes banks and brokers who act as nominee, each of whom may represent more than one stockholder.

Dividend Policy

The declaration and amount of any actual cash dividend are in the sole discretion of our Board of Directors and are subject to numerous factors that ordinarily affect dividend policy, including the results of our operations and financial position, as well as general economic and business conditions.

The following table presents cash dividends per share of our common stock declared in fiscal years ended September 30, 2016, 2015, and 2014:

Declaration Date | Record Date | Payment Date | Per Common Share |

December 18, 2013 | March 31, 2014 | April 14, 2014 | $0.12 |

July 10, 2014 | September 30, 2014 | October 15, 2014 | $0.06 |

October 2, 2014 | December 31, 2014 | January 15, 2015 | $0.06 |

February 27, 2015 | March 31, 2015 | April 15, 2015 | $0.06 |

June 4, 2015 | June 30, 2015 | July 15, 2015 | $0.06 |

September 14, 2015 | September 30, 2015 | October 15, 2015 | $0.06 |

December 11, 2015 | December 31, 2015 | January 15, 2016 | $0.06 |

March 8, 2016 | March 31, 2016 | April 15, 2016 | $0.06 |

May 11, 2016 | June 30, 2016 | July 15, 2016 | $0.06 |

September 6, 2016 | September 30, 2016 | October 14, 2016 | $0.06 |

15

Stock Performance Graph

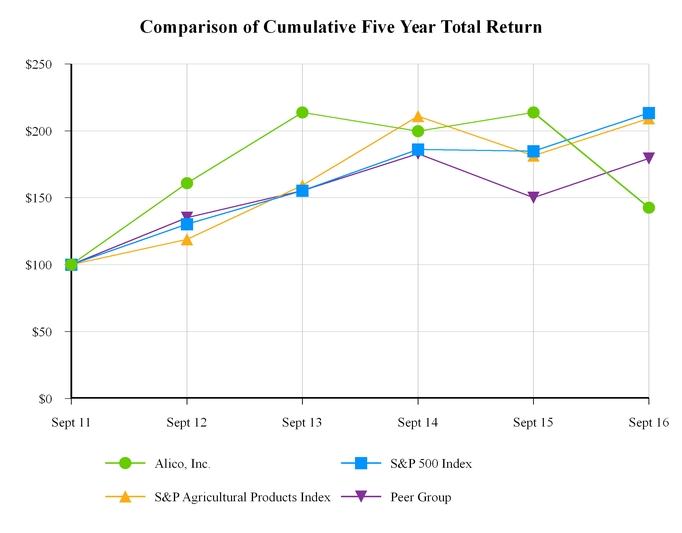

The graph below represents our common stock performance, comparing the value of $100 invested on September 30, 2011 in our common stock, the S&P 500 Index, the S&P Agricultural Products Index and a Company-constructed peer group, which includes Forestar Group, Inc., Limoneira Company, The St. Joe Company, Tejon Ranch Co. and Texas Pacific Land Trust.

INDEXED RETURNS | |||||||||||||

Base | |||||||||||||

Period | Years Ending | ||||||||||||

Company Name / Index | Sept 11 | Sept 12 | Sept 13 | Sept 14 | Sept 15 | Sept 16 | |||||||

Alico, Inc. | 100 | 160.87 | 213.75 | 199.68 | 213.84 | 142.63 | |||||||

S&P 500 Index | 100 | 130.20 | 155.39 | 186.05 | 184.91 | 213.44 | |||||||

S&P Agricultural Products Index | 100 | 118.89 | 159.25 | 211.02 | 181.47 | 209.24 | |||||||

Peer Group | 100 | 135.23 | 155.40 | 182.88 | 150.08 | 179.36 | |||||||

(Includes reinvestment of dividends)

16

Equity Compensation Arrangements

Effective January 27, 2015, the Company’s Board of Directors adopted the 2015 Stock Incentive Plan (the “2015 Plan”) which provides for up to 1,250,000 shares of the Company’s common stock to be available for issuance to provide a long-term incentive plan for officers, employees, directors and/or consultants to directly link incentives to stockholders' value. The 2015 Plan was approved by stockholders in February 2015. The adoption of the 2015 Plan supersedes the 2013 Incentive Equity Plan (the “2013 Plan”), which had been in place since April 2013. The 2013 Plan provided for the issuance of up to 350,000 shares of the Company’s common stock to Directors and Officers through March 2018. The following table illustrates the common shares remaining available for future issuance under the 2015 Plan:

Number of securities to be issued upon exercise of outstanding options, warrants and rights | Weighted-average exercise price of outstanding options, warrants and rights | Number of securities remaining available for future issuance under equity plans | |

Plan Category: | |||

Equity compensation plans approved by security holders | - | - | 1,237,500 |

Total | - | - | 1,237,500 |

Recent Sale of Unregistered Securities

None.

Issuer Repurchases of Equity Securities

In fiscal year 2015, our Board of Directors authorized the repurchase of up to 170,000 shares of the Company’s outstanding common stock beginning March 26, 2015 and continuing through December 31, 2016 (the “2015 Authorizations"). Through September 30, 2016, we had repurchased 170,000 common shares in accordance with the fiscal year 2015 Authorizations. The stock repurchases under the 2015 Authorizations were made through open market transactions at times and in such amounts as our broker determined subject to the provisions of SEC Rule 10b-18.